Managing Finance and Budgets Seminar 2. Seminar 2 - Activities During this seminar we will: Review...

23

Managing Finance and Budgets Seminar 2

-

date post

20-Dec-2015 -

Category

Documents

-

view

216 -

download

2

Transcript of Managing Finance and Budgets Seminar 2. Seminar 2 - Activities During this seminar we will: Review...

Managing Finance and Budgets

Seminar 2

Seminar 2 - Activities

During this seminar we will: Review the three types of financial

statement Discuss the three statements for Day 3 of

the ‘lemonade’ stall. Review the Cash Book Activity Discuss how the February transactions for

should be recorded in the Cash Book.

Some Starting Points

Explain, and if possible elaborate on the following terms: Assets Claims Creditors Debtors

Name the three main types of financial statement, what you think they might be used for, and some of the things you might find on each of them .

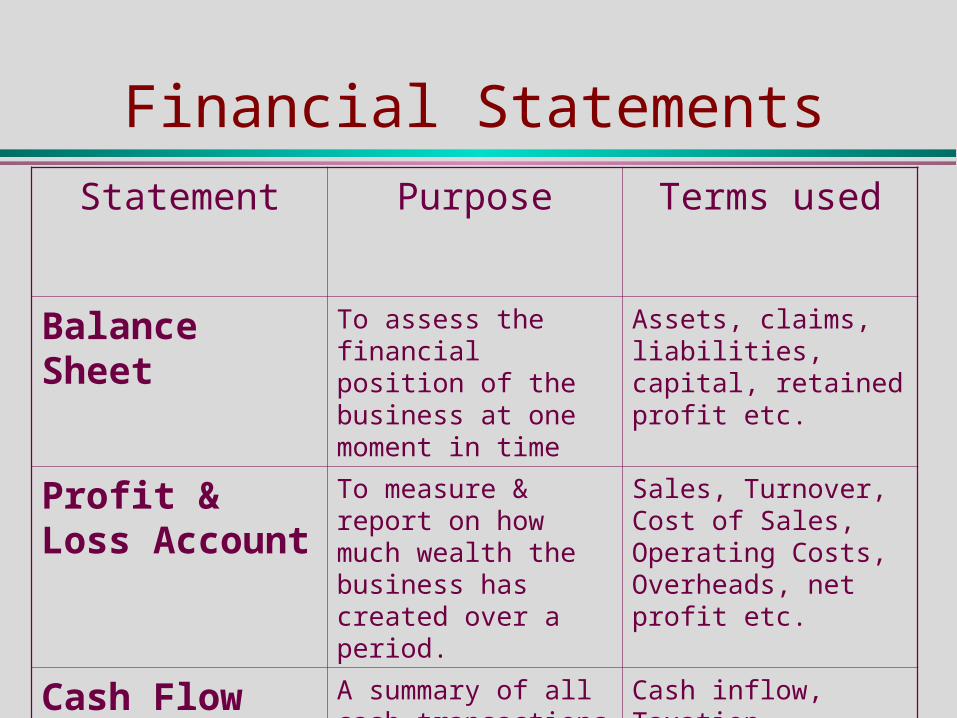

Financial StatementsStatement Purpose Terms used

Balance Sheet To assess the financial position of the business at one moment in time

Assets, claims, liabilities, capital, retained profit etc.

Profit & Loss Account

To measure & report on how much wealth the business has created over a period.

Sales, Turnover, Cost of Sales, Operating Costs, Overheads, net profit etc.

Cash Flow Statement

A summary of all cash transactions over a period

Cash inflow, Taxation, expenditure, dividends, net increase in cash

Profit and loss account

Cash flow statement

Balance sheet

Balance sheet

Balance sheet

Profit and loss account

Cash flow statement

Relationship between the balance sheet, profit and loss account and cash flow statement

Seminar Preparation Activity

On the third car boot sale that you attend, you decide to pay your friend back entirely. In addition you purchase another 250 cans of lemonade at 20p per can. This time the entry fee is £10, but it rains and you only sell 50 of your cans at 50p each.

Construct a cash flow statement, profit & loss account and a balance sheet. for the third day.

The Cash Flow Statement –end of Day 2

Opening Balance: £ 80

Loan from friend: £ 30- (paid back)

Goods purchased: £ 30- (150 x 20p)

Entry Fee: £ 5-

Cash received: £ 50+ (100 x 50p)

Closing Balance: £ 65

Seminar ActivityCash Flow Statement Day 3

Opening Balance: £ 65

Loan from friend: £ 20- (now paid back)

Goods purchased: £ 50- (250 x 20p)

Entry Fee: £ 10-

Cash received: £ 25+ (50 x 50p)

Closing Balance: £ 10

NOTE:

This could not have happened in this sequence, as the business did not have enough cash after paying back the loan!

NOTE:

This could not have happened in this sequence, as the business did not have enough cash after paying back the loan!

The Profit & Loss Account –End of Day 2

Sales: £ 50 (100 x 50p)

Cost of Sales: -£ 20 (100 x 20p)

Entry Fee: -£ 5

Net Profit: £ 25

Seminar ActivityProfit & Loss Account – Day 3

Sales: £ 25 (50 x 50p)

Cost of Sales: £ 10 (50 x 20p)

Gross Profit: £ 15

Entry Fee: - £ 10

Net Profit: £ 5

The Balance Sheet –End of Day 2

Assets:

Cash: £ 65

Stock: £ 20 (100 x 20p)

Total: £ 85

Liabilities:

Loan outstanding: £ 20

Retained profits: £ 65

Total: £ 85

Seminar ActivityBalance Sheet Day 3

Assets: Cash: £ 10

Stock: £ 60 (300 x 20p)Total: £ 70

* Opening Stock: 100 cansStock Purchased + 250 cansStock Sold - 50 cansClosing Stock: 300 cans

Liabilities:

Loan outstanding: £ 0

Retained profits: £ 70

Total: £ 70

The Cash Book Spreadsheet

This side shows you what money has come into the account, and where it has come from

This side shows you what money has gone out of the account, and where it has gone to.

The Cash Book Spreadsheet

Can you explain (1) what these transactions were, and (2) where their partner entries have been recorded?

Cash Book Transactions - February

Feb 2 £1200 of Cash sales. These goods originally cost us £500 Feb 3 £800 of stock bought from warehouse on credit. Feb 4 £400 of shelving fixtures bought for cash.Feb 6 £200 of stock bought on Feb 8 returned to warehouseFeb 8 £600 of stock sold on credit for £900Feb 10 Refund of £100 on unused shelving fixturesFeb 11 £250 cash received from Trade DebtorsFeb 14 Paid £150 to Trade Creditors.Feb 18 Wages bill for the week £400 paid in cash.Feb 19 £1000 repaid to the Commercial Finance CompanyFeb 20 Paid rent of £250 in cash.Feb 21 £500 Cash sales. These goods originally cost £350Feb 22 £100 received from trade DebtorsFeb 23 £100 Cash sales. Goods originally cost £50.Feb 25 Owner withdraws £250 from the day’s takings

Entering Transactions

2nd February Sell goods for £1200 cashThese were originally bought for £500

On the SALES page, we credit CASH with the £1200

On the SALES page, we credit CASH with the £1200

Entering Transactions

2nd February Sell goods for £1200 cashThese were originally bought for £500

On the CASH page we show where this money has come from; we debit £1200 from Sales.

On the CASH page we show where this money has come from; we debit £1200 from Sales.

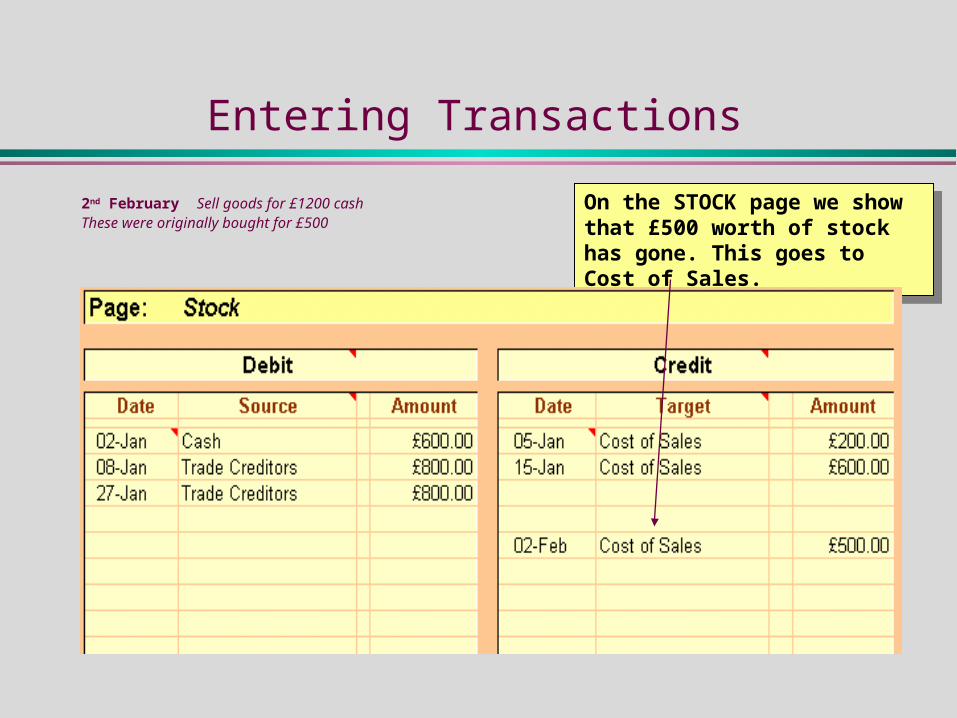

Entering Transactions

2nd February Sell goods for £1200 cashThese were originally bought for £500

On the STOCK page we show that £500 worth of stock has gone. This goes to Cost of Sales.

On the STOCK page we show that £500 worth of stock has gone. This goes to Cost of Sales.

Entering Transactions

2nd February Sell goods for £1200 cashThese were originally bought for £500

On the COST OF SALES page we show that Stock has now been reduced by £500.

On the COST OF SALES page we show that Stock has now been reduced by £500.

Final Cash page for February

Trial Balance for February

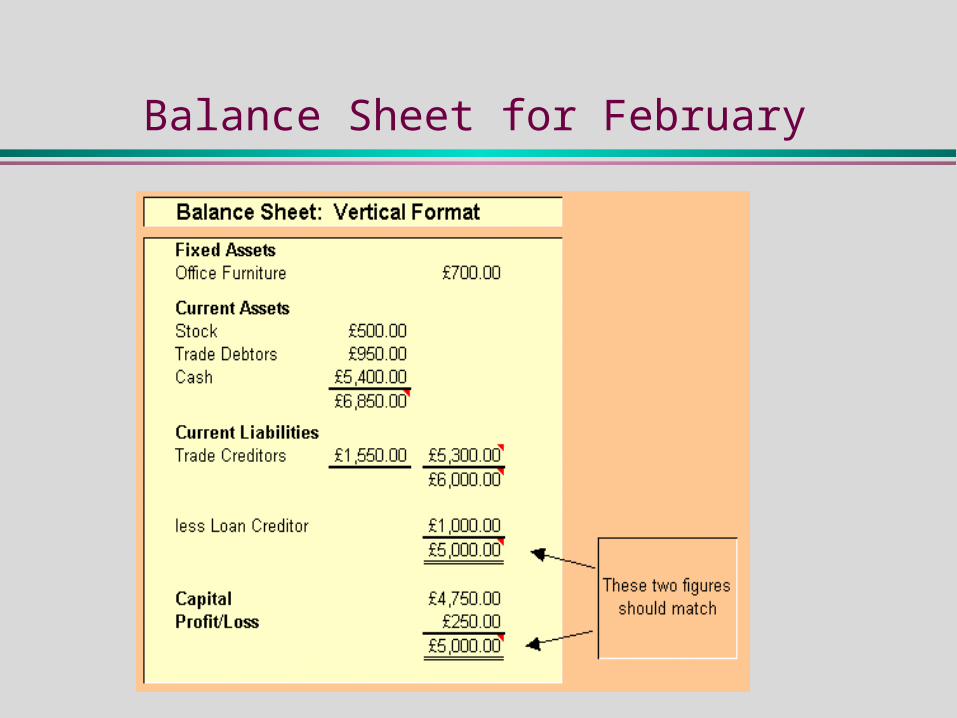

Balance Sheet for February

Balance Sheet for February

![Candide Socratic Seminar. Chapter 1 Discuss Pangloss’ philosophy. [p. 12, #2]](https://static.fdocuments.in/doc/165x107/56649e425503460f94b34fc8/candide-socratic-seminar-chapter-1-discuss-pangloss-philosophy-p-12.jpg)