MANAGEMENT REPORT 2013 - static.lasa.com.br · Launched in the end of 2011, Sou Barato presents a...

26

MANAGEMENT REPORT 2013 In compliance with legal requirements and current Brazilian corporate legislation, Lojas Americanas S.A. is hereby presenting its Management Report containing the Parent Company and Consolidated financial and operating results for the fiscal year ending December 31 st 2013. We are also presenting in this report information regarding to the subsidiary B2W Digital, Latin America’s leading e-commerce company, which offers products and services via the Internet, television, telephone, catalogues and kiosks. Lojas Americanas owns 62.23% of its capital stock. The shares issued by Lojas Americanas and B2W are listed on the Brazilian Stock Exchange (BM&FBOVESPA) under ticker symbols LAME4 (preferred), LAME3 (common) and BTOW3, respectively. It should be noted that B2W only has common shares and is part of the Novo Mercado listing segment, the highest level of corporate governance standards in Brazil. “Multichannel Retailer” Structure Lojas Americanas operates through a multichannel service structure. Besides a chain of brick- and-mortar stores, the Company reaches its clients with a wide assortment of products and services, sold via Internet, television, telephone sales, catalogues and kiosks. *As of 12/31/2013 Bricks-and-Mortar Multichannel Retailer Ecommerce, TV, Telephone Sales, Catalogues and Kiosks Participation: 62.23% Results Consolidation: 100.00%

Transcript of MANAGEMENT REPORT 2013 - static.lasa.com.br · Launched in the end of 2011, Sou Barato presents a...

MANAGEMENT REPORT 2013

In compliance with legal requirements and current Brazilian corporate legislation, Lojas

Americanas S.A. is hereby presenting its Management Report containing the Parent Company

and Consolidated financial and operating results for the fiscal year ending December 31st 2013.

We are also presenting in this report information regarding to the subsidiary B2W Digital, Latin

America’s leading e-commerce company, which offers products and services via the Internet,

television, telephone, catalogues and kiosks. Lojas Americanas owns 62.23% of its capital stock.

The shares issued by Lojas Americanas and B2W are listed on the Brazilian Stock Exchange

(BM&FBOVESPA) under ticker symbols LAME4 (preferred), LAME3 (common) and BTOW3,

respectively. It should be noted that B2W only has common shares and is part of the Novo

Mercado listing segment, the highest level of corporate governance standards in Brazil.

“Multichannel Retailer” Structure

Lojas Americanas operates through a multichannel service structure. Besides a chain of brick-

and-mortar stores, the Company reaches its clients with a wide assortment of products and

services, sold via Internet, television, telephone sales, catalogues and kiosks.

*As of 12/31/2013

Bricks-and-Mortar

Multichannel Retailer

Ecommerce, TV, Telephone

Sales, Catalogues and Kiosks

Participation: 62.23% Results Consolidation: 100.00%

2/ 26

Lojas Americanas S.A.

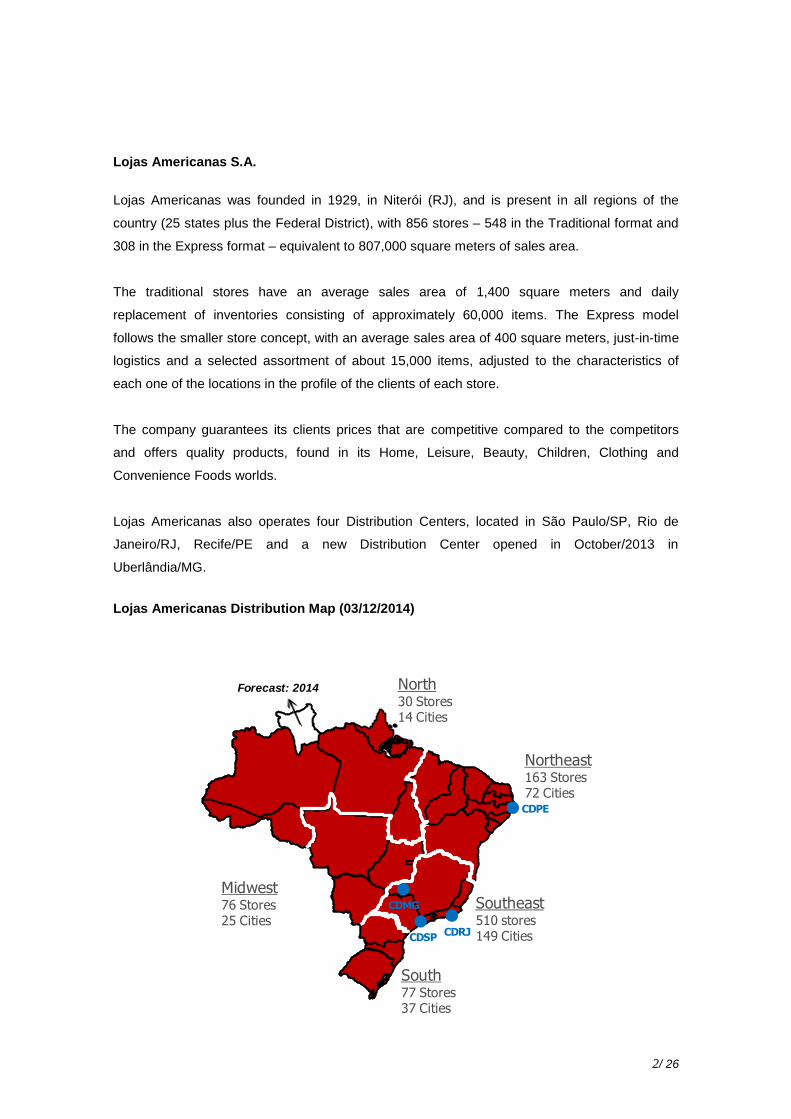

Lojas Americanas was founded in 1929, in Niterói (RJ), and is present in all regions of the

country (25 states plus the Federal District), with 856 stores – 548 in the Traditional format and

308 in the Express format – equivalent to 807,000 square meters of sales area.

The traditional stores have an average sales area of 1,400 square meters and daily

replacement of inventories consisting of approximately 60,000 items. The Express model

follows the smaller store concept, with an average sales area of 400 square meters, just-in-time

logistics and a selected assortment of about 15,000 items, adjusted to the characteristics of

each one of the locations in the profile of the clients of each store.

The company guarantees its clients prices that are competitive compared to the competitors

and offers quality products, found in its Home, Leisure, Beauty, Children, Clothing and

Convenience Foods worlds.

Lojas Americanas also operates four Distribution Centers, located in São Paulo/SP, Rio de

Janeiro/RJ, Recife/PE and a new Distribution Center opened in October/2013 in

Uberlândia/MG.

Lojas Americanas Distribution Map (03/12/2014)

105

8

North30 Stores14 Cities

Forecast: 2014

Northeast163 Stores72 Cities

Southeast510 stores149 Cities

South77 Stores 37 Cities

Midwest76 Stores25 Cities

CDMG

CDSPCDRJ

CDPE

3/ 26

B2W DIGITAL

B2W is the leading e-commerce Company in Latin America. The Company operates through a

digital platform, with businesses that present a strong synergy and a unique model,

multichannel, multibrand and multibusiness.

B2W has a portfolio with the brands Americanas.com, Submarino, Shoptime, B2W Viagens,

Ingresso.com, Submarino Finance, BLOCKBUSTER® Online and SouBarato, that offer more

than 38 categories of products and services through the internet, telesales, catalogs, TV and

kiosks distribution channels.

core business

Americanas.com

The largest Store. The lowest prices.

Since 1999, Americanas.com is Latin America's largest and most complete online store. Elected

by consumers as the number 1 in service, the brand offers more than 500,000 products that can

be purchased through the web site, telephone sales or in over 800 kiosks located inside of Lojas

Americanas brick-and-mortar stores. In addition, its delivery, travel, mobile app and B2B

services, among many others, contribute to a unique and increasingly more complete purchase

experience.

Submarino

The products you like and the Internet's best service.

Submarino - pioneer online store and benchmark in technology and innovation - offers more

than 30 categories of products through the Internet, telephone sales, mobile and catalogs, with

an emphasis on the sale of books, games, DVDs, electronics, computers, telephony, fashion

and online services. In addition, Submarino has been consolidating other services, such as

Submarino Viagens, B2B services and the Submarino Card.

4/ 26

Shoptime

Exclusive products and live demonstrations.

Shoptime is the first Brazilian homeshopping channel and operates via Internet, catalog and

telephone sales. The brand focuses on integrating its different sales channels aiming to provide

customers the best shopping experience. The Shoptime assortment emphasizes home products,

with its four private label brands: Casa & Conforto, Fun Kitchen, La Cuisine and Life Zone.

Sou Barato

Sou Barato is B2W Digital's outlet that offers a wide variety of products from the best brands,

with promotional pricing below the market average. The site sells new and repackaged products

in perfect condition, with discounts of up to 70%. Launched in the end of 2011, Sou Barato

presents a wide and varied selection of products, with more than 20 categories such as

smartphones and mobile phones, computers, TVs, electronics, among others.

B2W Viagens

B2W Viagens operates through the Americanas Viagens, Shoptime Viagens, Milevo, Submarino

Viajes and Submarino Viagens, brand with the latter having been elected by popular vote in

2013 three-time champion in terms of customer service and the Best Online Travel Agency in

the country. B2W Viagens' sites have established partnerships with more than 750 airlines,

200,000 hotels and 4,000 attractions throughout the world.

Ingresso.com

Brazilian leader in Internet ticket sales, with more than 5 million customers, Ingresso.com offers

the convenience of secure ticket purchases through the website, telephone sales and apps for

the Iphone, Android phones and Facebook. In addition to leading the virtual world, its new

ARENA software, which was launched in 2013, is considered the most intelligent strategic

management tool in the market, allowing the Company to consolidate its presence in the

country's biggest box offices.

Submarino Finance

Submarino Finance offers the Submarino Mastercard credit card, which comes with special

advantages through Submarino, such as exclusive discounts and payment installment

conditions, differentiated credit limits and Léguas Program, a distinctive loyalty program. Over

2013, we reached the milestone of more than 830,000 cards issued, garnering a 38% share in

Submarino's website sales.

5/ 26

2. MESSAGE FROM THE MANAGEMENT

TO OUR CUSTOMERS, SHAREHOLDERS, ASSOCIATES AND SUPPLIERS:

In 2013, our multichannel strategy made major gains. The performance of our main operating

indicators continued in line with the evolution observed in recent years, combining growth and

profitability. In the consolidated view, gross revenue reached R$ 15.5 billion in 2013. In the

same period, net revenue totaled R$ 13.4 billion, representing a growth of 18.2%. The

generation of consolidated operating cash, EBITDA*, totaled R$ 1.8 billion, an increase of

17.4%, with an EBITDA margin* of 13.8%, and the net income for the year was R$ 462.9 million.

In the parent company, we can highlight the net revenue growth in the "same stores sales"

concept of 9%, which takes into account only the stores opened more than one year previously.

In the segment of bricks-and-mortar stores, we continue to demonstrate solid performance,

achieving a presence in more than 290 cities throughout the country and beginning the

operation of our fourth distribution center. The "SEMPRE MAIS BRASIL" expansion program

was successfully completed, considerably boosting the Company's number of stores, almost

doubling the number of cities served by physical stores and marking our entry into three new

states: Acre, Amapá and Tocantins. The success of the organic expansion program, initiated in

2010, is a source of pride and we are very excited about its continuity. In the next years, we will

maintain the pace of expansion with the goal of capturing the opportunities of the Brazilian retail

sector, following our vision of meeting the needs of our customers by exceeding their

expectations. Throughout 2014, we will continue strengthening our multichannel structure

aiming to bring more convenience to our consumers and to offer the best purchase experience.

For B2W Digital, 2013 represented the first stage of the three-year investment plan (2013, 2014

and 2015), allowing the Company to move forward in its strategy of being closer to the

customers. Among the investments made, we can highlight the four strategic acquisitions, of

which three were technology companies specialized in systems development - Uniconsult,

Ideais and Tarkena - and the purchase of Click-Rodo, a transportation company specialized in

operations for e-commerce. In addition, were opened three new distribution centers, increasing

B2W's storage capacity by 60%. The year also marked the launch of the fashion category and

the beginning of the marketplace operation. Other notable achievements included the choice of

B2W Digital to operate the entire Ambev online store, including its technological and logistics

platforms, and the FIFA online store, which offers licensed products exclusive to the FIFA Brazil

2014™ World Cup event.

In 2013, Lojas Americanas was elected the big winner of the "Época Reclame Aqui Award – the

Best Companies for the Consumer" in the Retail Category. The award and the RA 1000 quality

seal demonstrate that we are on the right track, seeking to realize the dreams and meeting the

consumption needs of people, sparing their time and money and exceeding their expectations.

6/ 26

Also in 2013, Lojas Americanas was chosen the best company in the retail category by Exame

magazine's Maiores e Melhores yearbook, for the seventh time. Over the year, as recompense

for the mobilization of B2W in its entirety to offer clients the best digital experience, the

Company won the market's major awards, such as: four awards in "Época Reclame Aqui Award

- the Best Companies for the Consumer" and the "Internet Top of Mind Award" for the seventh

consecutive year. These honors ratify the Company's leading position in Internet customer

service.

Within our vision of "being the best retail company in Brazil", it is important to highlight our

efforts to be regarded by society as a socially and ecologically responsible organization. To this

end, on November 1st we joined the UN Global Pact, in which we undertook to adopt the best

corporate practices with respect to human rights, labor issues, the environment and ethical

business behavior.

The realization of our objectives depends on the dedication of our associates, who are inserted

into an organizational culture characterized by meritocracy and the achievement of results. We

believe in the potential of our team and, therefore, we continue to intensify the training

programs, developing our professionals in house to grow along with the Company.

We reiterate our confidence in the development of the country and for 2014, in the same way as

in previous years, "we will continue to move forward along the path of learning and overcoming

obstacles, which naturally makes us enthusiastic because we will achieve higher levels of

results, always seeking better ways to satisfy the needs of our customers."

Finally, we wish to thank the dedication and tough attitude of our associates, as well as the

support and trust that we received from our suppliers, customers and shareholders.

THE MANAGEMENT “We always want more”

7/ 26

3. ECONOMIC LANDSCAPE

Even in the face of macroeconomic challenges in 2013 - with a Gross Domestic Product (GDP)

growth of 2.3% and inflation as measured by the IPCA (National Broad Consumer Price Index)

registering an accumulated rate of 5.9% - the level of employment remained high and retail

sales presented a growth of 4.3%.

Within the Company, we believe that the wide assortment and the low concentration of sales in

the several different categories offered by the stores and our multichannel, multibrand e

multibusiness model, bring opportunities for market share gains. During 2013, the 18.2%

consolidated net revenue growth and the 9% growth of net revenue in the "same stores sales"

concept demonstrates the resilience of our business model.

Lojas Americanas continues to be optimistic that the Brazilian retail sector offers significant

growth opportunities, reaffirms its confidence in the economic development of the country and

highlights the strength of its unique business model through its extensive nationwide presence

and multichannel service to customers.

*Source: Brazilian Institute of Geography and Statistics and Central Bank of Brazil.

8/ 26

4. STRATEGY AND INVESTMENT

In 2013, Lojas Americanas’ consolidated net revenue reached R$ 13.401 billion, a growth of

18.2% over the previous year. Of this total, R$ 7.716 billion referred to the performance of the

Parent Company (brick-and-mortar stores), which sold 12.6% more than in 2012.

In the “same stores” concept, that is, including stores inaugurated more than one year

previously, accumulated net sales in 2013 rose by 9%.

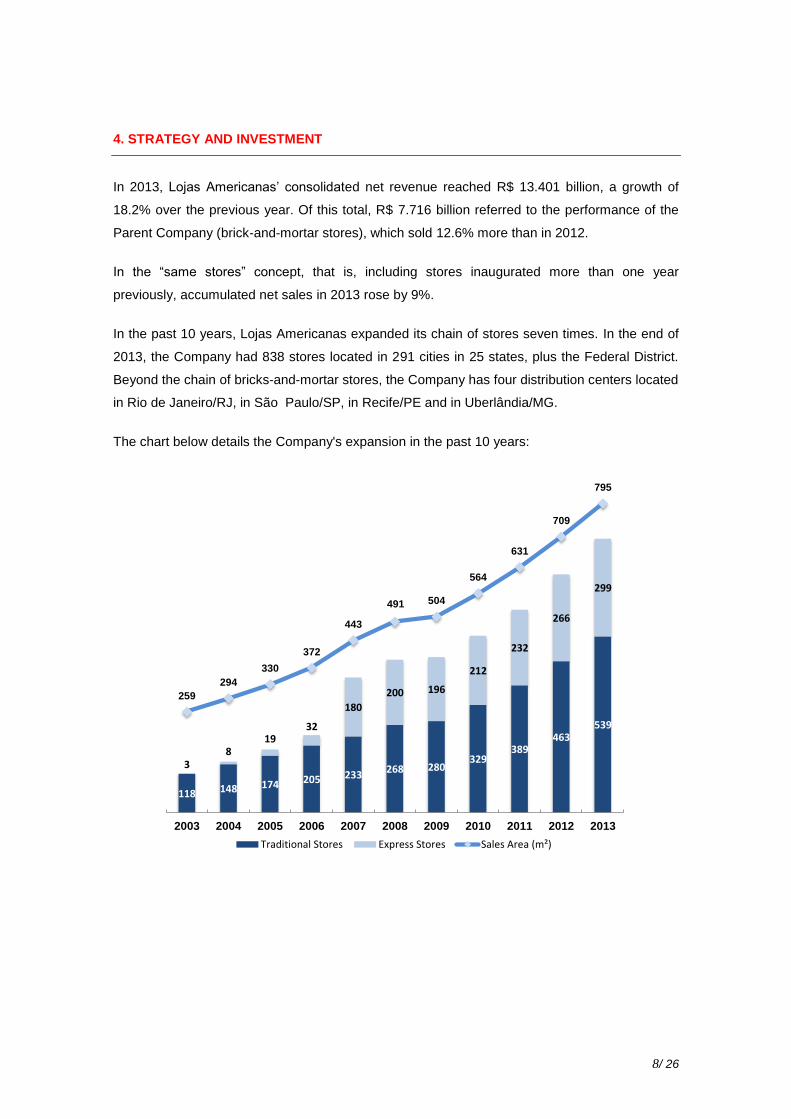

In the past 10 years, Lojas Americanas expanded its chain of stores seven times. In the end of

2013, the Company had 838 stores located in 291 cities in 25 states, plus the Federal District.

Beyond the chain of bricks-and-mortar stores, the Company has four distribution centers located

in Rio de Janeiro/RJ, in São Paulo/SP, in Recife/PE and in Uberlândia/MG.

The chart below details the Company's expansion in the past 10 years:

118 148 174 205 233268 280

329389

463539

38

1932

180

200 196

212

232

266

299

259

294

330

372

443

491 504

564

631

709

795

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Traditional Stores Express Stores Sales Area (m²)

9/ 26

Expansion Plan – “SEMPRE MAIS BRASIL”

The “SEMPRE MAIS BRASIL” program announced at the end of 2009 called for the opening of

400 new stores in four years.

On December 31, 2009, the Company's 476 stores were located approximately in 150 cities in

22 states, plus the Federal District. With the conclusion of the "“SEMPRE MAIS BRASIL - 80

YEARS IN 4!" expansion program, the Company now operates 856 stores in 297 cities inside

25 states, plus the Federal District, which means it nearly doubled in size in just four years,

successfully completing the challenge laid down at the end of 2009.

During this period, we doubled the number of cities that have at least one

Lojas Americanas store, increasing our presence in cities more distant from

large urban centers and entering in Acre, Amapá and Tocantins states.

Based on economic feasibility studies and analyses conducted internally using the EVA®

(Economic Value Added) methodology, together with socio-economic data (population, income,

access to basic services, access to consumer goods, among others), we believe that at this

moment there is the possibility that our brick-and-mortar retail stores to be present in a much

broader number of cities, beyond the 297 cities were we have stores today. The study

demonstrates the opportunity that Lojas Americanas has to continue opening stores in cities

that are more distant from large urban centers.

To ensure greater efficiency in the distribution of goods, in October 2013 we started the

operation of our fourth Distribution Center, in Uberlândia-MG. The new center will ensure

greater speed in the supply of the physical stores, aiming to provide the best service to

customers in Minas Gerais and in the Midwest and North regions of the country. We believe that

the new center, of approximately 40,000 m², is essential to ensure the quality of the expansion

planned for the coming years, supporting growth and increasing the efficiency of logistics.

10/ 26

The following table presents details of the stores opened during 2013:

As of 12/31/2012 729 709.5 1.0Traditional 30 28.3 0.9Express 26 10.5 0.4

Traditional 25 23.6 0.9

Express 4 1.6 0.4

Traditional 6 5.5 0.9

Express 2 1.0 0.5

Traditional 5 5.2 1.0

Express - - -

Traditional 11 9.4 0.9

Express 2 0.8 0.4

Traditional 77 72.0 0.9

Express 34 13.9 0.4

Transfer/Remodel (2) (0.2) 0.1

As of 12/31/2013 838 795.2 0.9

Midwest

TOTAL

Northeast

South

North

Southeast

Region FormatNumber

of Stores

Sales Area

thousand m²

Average

thousand m²

Expansion Plan – Next Years

As of today, our stores are located in 25 states of the country plus the Federal District, with

distribution as follows: 59,6% in the Southeast, 17.9% in the South/Midwest and 22.5% in the

North/Northeast. We are optimistic about continuing our growth path and we will maintain the

commitment to profitability and the usual discipline in conducting the economic feasibility studies

for opening of new stores in the coming years.

Based on our confidence in the country's development, the continuation of the Company's

expansion plan will generate benefits for all regions of the country. As it has occurred historically,

the growth should be in the proportion of 70% Traditional stores (average sales area between

1,000 m² and 1,500 m²) and 30% Express stores (average sales area between 300 m² and 500

m²).

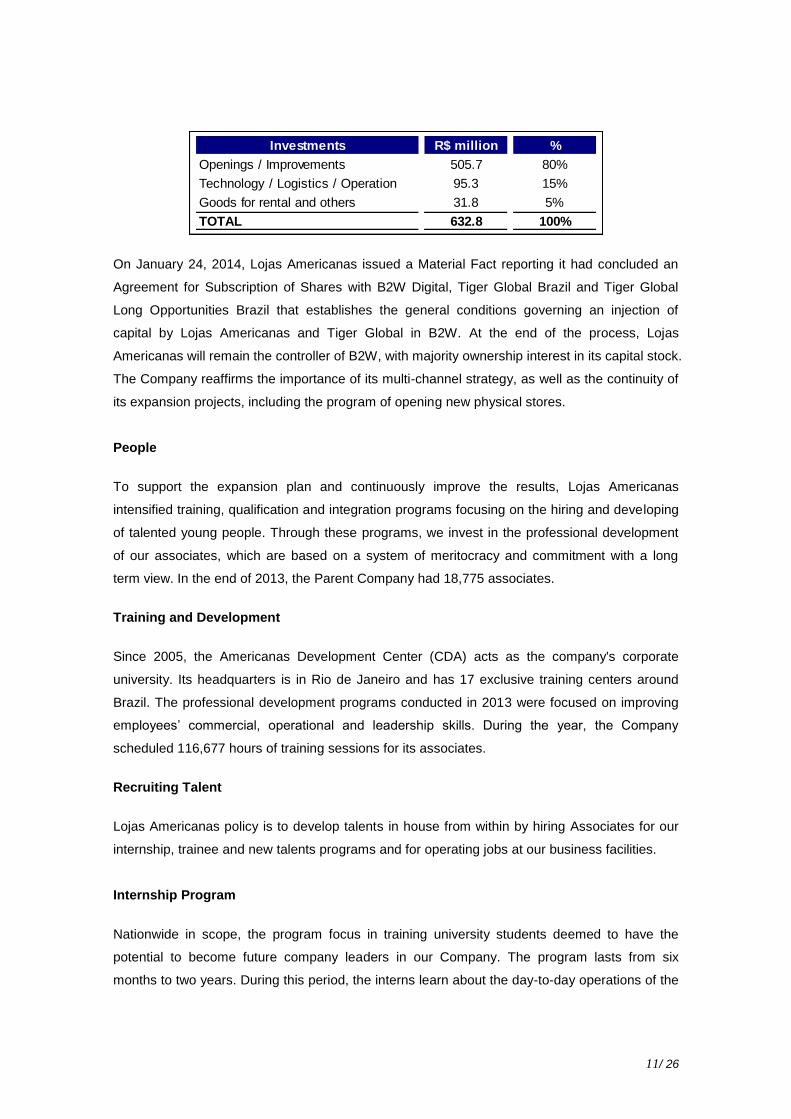

Investments

In 2013, Lojas Americanas Parent Company invested a total of R$ 632.8 million, with emphasis

on expansion, improvements in the chain of store and technological upgrade. Included in this

total are investments in goods for rental and others in the amount of R$ 31.8 million.

11/ 26

Investments R$ million %

Openings / Improvements 505.7 80%0 0%

Technology / Logistics / Operation 95.3 15%0 0%

Goods for rental and others 31.8 5%0 0%

TOTAL 632.8 100%

On January 24, 2014, Lojas Americanas issued a Material Fact reporting it had concluded an

Agreement for Subscription of Shares with B2W Digital, Tiger Global Brazil and Tiger Global

Long Opportunities Brazil that establishes the general conditions governing an injection of

capital by Lojas Americanas and Tiger Global in B2W. At the end of the process, Lojas

Americanas will remain the controller of B2W, with majority ownership interest in its capital stock.

The Company reaffirms the importance of its multi-channel strategy, as well as the continuity of

its expansion projects, including the program of opening new physical stores.

People

To support the expansion plan and continuously improve the results, Lojas Americanas

intensified training, qualification and integration programs focusing on the hiring and developing

of talented young people. Through these programs, we invest in the professional development

of our associates, which are based on a system of meritocracy and commitment with a long

term view. In the end of 2013, the Parent Company had 18,775 associates.

Training and Development

Since 2005, the Americanas Development Center (CDA) acts as the company's corporate

university. Its headquarters is in Rio de Janeiro and has 17 exclusive training centers around

Brazil. The professional development programs conducted in 2013 were focused on improving

employees’ commercial, operational and leadership skills. During the year, the Company

scheduled 116,677 hours of training sessions for its associates.

Recruiting Talent

Lojas Americanas policy is to develop talents in house from within by hiring Associates for our

internship, trainee and new talents programs and for operating jobs at our business facilities.

Internship Program

Nationwide in scope, the program focus in training university students deemed to have the

potential to become future company leaders in our Company. The program lasts from six

months to two years. During this period, the interns learn about the day-to-day operations of the

12/ 26

stores, headquarters, distribution centers and receive specific training about the challenges of

the retail segment and the insertion in the corporate culture.

Retail New Talents Program

The Program is aimed at the recruitment of young graduates and its objective is to fast-track the

development of young professionals capable of accompanying the quick-paced growth of the

group's companies. They are assigned to specific sectors right from the start of the program and

undergo training to give them an overview of all of the Company's operations.

Trainee Program

Registration for the Lojas Americanas’ Trainee Program is conducted on an annual basis. As

rapid and dynamic as the retail sector itself, this Program is conducted over 12 months,

representing an intense learning experience for young candidates whose profiles suggest they

could be future managers at Lojas Americanas. In the first six months, the trainee learns about

the company's overall operations and undergoes various corporate training modules. After this

period, each trainee is sent to one business area for on-the-job learning and they all get an

opportunity to develop a final challenging project.

Program for People with Disabilities

Lojas Americanas seeks to include and train people with disabilities in its workplaces. We offer

job positions through which the associates have the opportunity to learn retail routines and

develop themselves professionally. Recruitment of candidates occurs through partnerships with

municipal authorities and specialized consultants, who indicate them for jobs in our stores and

distribution centers around the country.

Young Apprentice Project

Always concerned with preparing students for the job market, we have developed the Young

Apprentice Project together with the National Commercial Apprenticeship Service (Senac) or

equivalent organizations in cities where we have business units. The contract is for a fixed

period of time and each youth participating is committed to enrolling in and regularly attending

elementary school.

13/ 26

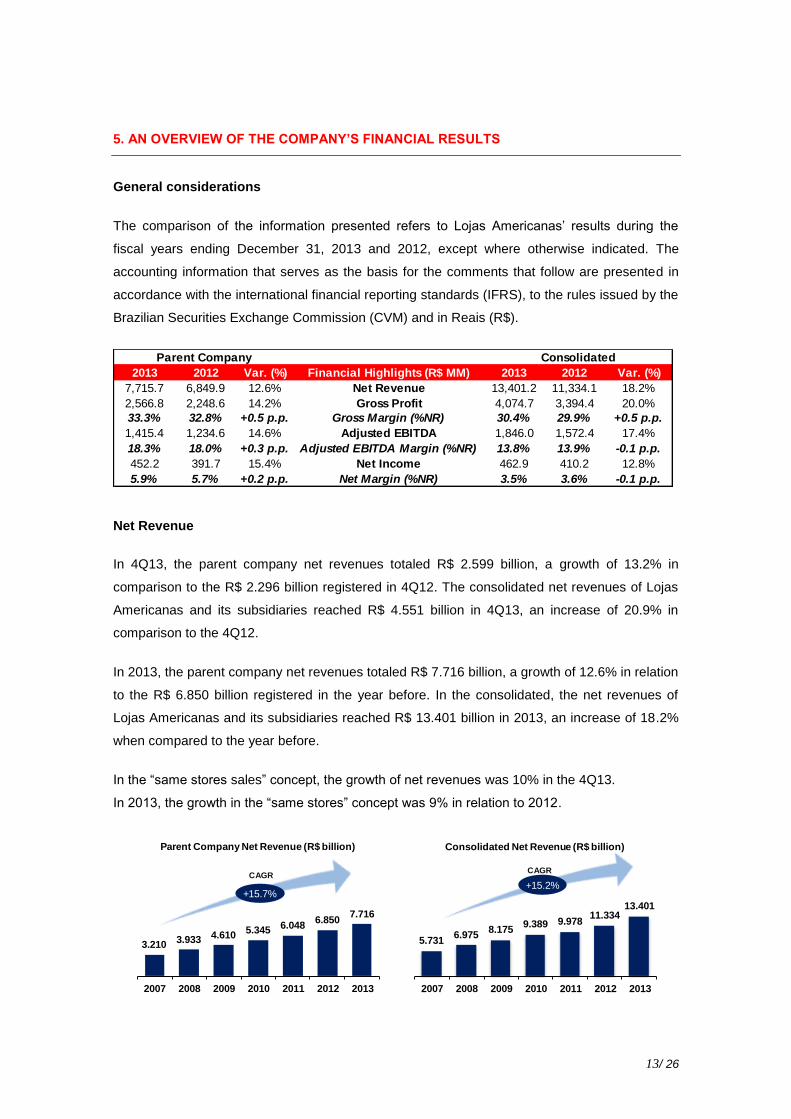

5. AN OVERVIEW OF THE COMPANY’S FINANCIAL RESULTS

General considerations

The comparison of the information presented refers to Lojas Americanas’ results during the

fiscal years ending December 31, 2013 and 2012, except where otherwise indicated. The

accounting information that serves as the basis for the comments that follow are presented in

accordance with the international financial reporting standards (IFRS), to the rules issued by the

Brazilian Securities Exchange Commission (CVM) and in Reais (R$).

2013 2012 Var. (%) Financial Highlights (R$ MM) 2013 2012 Var. (%)

7,715.7 6,849.9 12.6% Net Revenue 13,401.2 11,334.1 18.2%

2,566.8 2,248.6 14.2% Gross Profit 4,074.7 3,394.4 20.0%

33.3% 32.8% +0.5 p.p. Gross Margin (%NR) 30.4% 29.9% +0.5 p.p.

1,415.4 1,234.6 14.6% Adjusted EBITDA 1,846.0 1,572.4 17.4%

18.3% 18.0% +0.3 p.p. Adjusted EBITDA Margin (%NR) 13.8% 13.9% -0.1 p.p.

452.2 391.7 15.4% Net Income 462.9 410.2 12.8%

5.9% 5.7% +0.2 p.p. Net Margin (%NR) 3.5% 3.6% -0.1 p.p.

Parent Company Consolidated

Net Revenue

In 4Q13, the parent company net revenues totaled R$ 2.599 billion, a growth of 13.2% in

comparison to the R$ 2.296 billion registered in 4Q12. The consolidated net revenues of Lojas

Americanas and its subsidiaries reached R$ 4.551 billion in 4Q13, an increase of 20.9% in

comparison to the 4Q12.

In 2013, the parent company net revenues totaled R$ 7.716 billion, a growth of 12.6% in relation

to the R$ 6.850 billion registered in the year before. In the consolidated, the net revenues of

Lojas Americanas and its subsidiaries reached R$ 13.401 billion in 2013, an increase of 18.2%

when compared to the year before.

In the “same stores sales” concept, the growth of net revenues was 10% in the 4Q13.

In 2013, the growth in the “same stores” concept was 9% in relation to 2012.

3.2103.933 4.610

5.3456.048

6.8507.716

2007 2008 2009 2010 2011 2012 2013

+15.7%

CAGR

Parent Company Net Revenue (R$ billion)

5.7316.975

8.1759.389 9.978

11.33413.401

2007 2008 2009 2010 2011 2012 2013

+15.2%

CAGR

Consolidated Net Revenue (R$ billion)

14/ 26

Gross Profit and Gross Margin In the parent company, the gross margin was 37.0% of net revenues (NR) in 4Q13, an evolution

of 0.4 p.p. when compared to the gross margin of 36.6% of NR reported in 4Q12. The

consolidated gross margin in 4Q13 was 32.2% of NR, which represents an improvement of 0.1

p.p. in relation to the same period of the preceding year.

In the parent company, the gross margin was 33.3% of NR in 2013, an evolution of 0.5 p.p.

when compared to the gross margin of 32.8% of NR reported in 2012. The consolidated gross

margin in 2013 was 30.4% of NR, an improvement of 0.5 p.p. in relation to the same period of

the preceding year.

9661,226 1,391

1,6251,927

2,2492,567

30.131.2

30.2 30.4

31.932.8

33.3

28. 5

29. 5

30. 5

31. 5

32. 5

33. 5

34. 5

35. 5

0

500

1000

1500

2000

2500

3000

2007 2008 2009 2010 2011 2012 2013

+17.7%

CAGR

Parent Company Gross Profit (R$ million)

1,8322,234

2,5762,930 2,978

3,394

4,075

32.0 32.0 31.5 31.229.8 29.9 30.4

30. 0

31. 0

32. 0

33. 0

34. 0

35. 0

36. 0

0

500

1000

1500

2000

2500

3000

3500

4000

4500

2007 2008 2009 2010 2011 2012 2013

+14.3%

CAGR

Consolidated Gross Profit (R$ million)

Selling, General and Administrative Expenses In 4Q13, the parent company selling, general and administrative expenses totaled R$ 339.7

million, or 13.1% of NR, a reduction of 0.3 p.p. in relation to 4Q12. From a consolidated point of

view, selling, general and administrative expenses totaled R$ 680.7 million in 4Q13, or 15.0% of

NR, a variation of +0.1 p.p. in comparison to the same period of 2012.

In 2013, the parent company selling, general and administrative expenses totaled R$ 1,151.4

million, or 15.0% of NR. The consolidated selling, general and administrative expenses totaled

R$ 2,228.7 million in 2013, or 16.6% of NR.

17.8 17.416.2

15.2 14.9 14.8 15.0

2007 2008 2009 2010 2011 2012 2013

Parent Company Sales, General and Administrative Expenses (%NR)

19.4 19.218.1

16.815.4 16.0 16.6

2007 2008 2009 2010 2011 2012 2013

Consolidated Sales, General and Administrative Expenses (%NR)

15/ 26

Adjusted EBITDA In 4Q13, the parent company EBITDA reached R$ 622.0 million, an increase of 16.9% when

compared to 4Q12. The parent company EBITDA margin for the period was 23.9%, 0.7 p.p.

above the margin reported in 4Q12.

In the consolidated, EBITDA totaled R$ 783.1 million in 4Q13, representing a 21.1% increase in

relation to 4Q12. The consolidated EBITDA margin was 17.2% of net revenues in 4Q13, same

level reported in 4Q12.

In 2013, the parent company EBITDA reached R$ 1,415.4 million, a growth of 14.6% when

compared to 2012. In the same period, parent company EBITDA margin was 18.3%, an

increase of 0.3 p.p. in relation to 2012.

In 2013, the consolidated EBITDA totaled R$ 1,846.0 million, an improvement of 17.4% in

comparison to 2012. The consolidated EBITDA margin was 13.8% of net revenues in 2013, a

variation of -0.1 p.p. in relation to the preceding year.

393 541

644 811

1,029 1,235

1,415

12.3%

13.8% 14.0%15.2%

17.0%18.0% 18.3%

2007 2008 2009 2010 2011 2012 2013

EBITDA (R$ million) EBITDA (% NR)

+23.8%

CAGR

Parent Company Adjusted EBITDA

720896

1,093

1,355 1,4451,572

1,846

12.6% 12.8%13.4%

14.4% 14.5%13.9% 13.8%

2007 2008 2009 2010 2011 2012 2013EBITDA (R$ million) EBITDA (% NR)

+17.0%

CAGR

Consolidated Adjusted EBITDA

Adjusted EBITDA (Operating profit before interest, taxes, depreciation and amortization, other operating income/expenses, equity accounting, minority participation, statutory participation and discontinued operations) is presented as additional information because we believe it represents an important indicator of our operating performance, besides being useful for keeping the comparability with previous reported results.

EBITDA (CVM 527/12)

On October 4th, 2012, Brazilian Securities Exchange Commission (CVM) enacted the

Instruction 527/12, which disposes about the voluntary disclosure of not accounting information,

as EBITDA. The Instruction aims to standardize the disclosure, in order to improve the

understanding of this information and making it comparable among the publicly listed

companies.

16/ 26

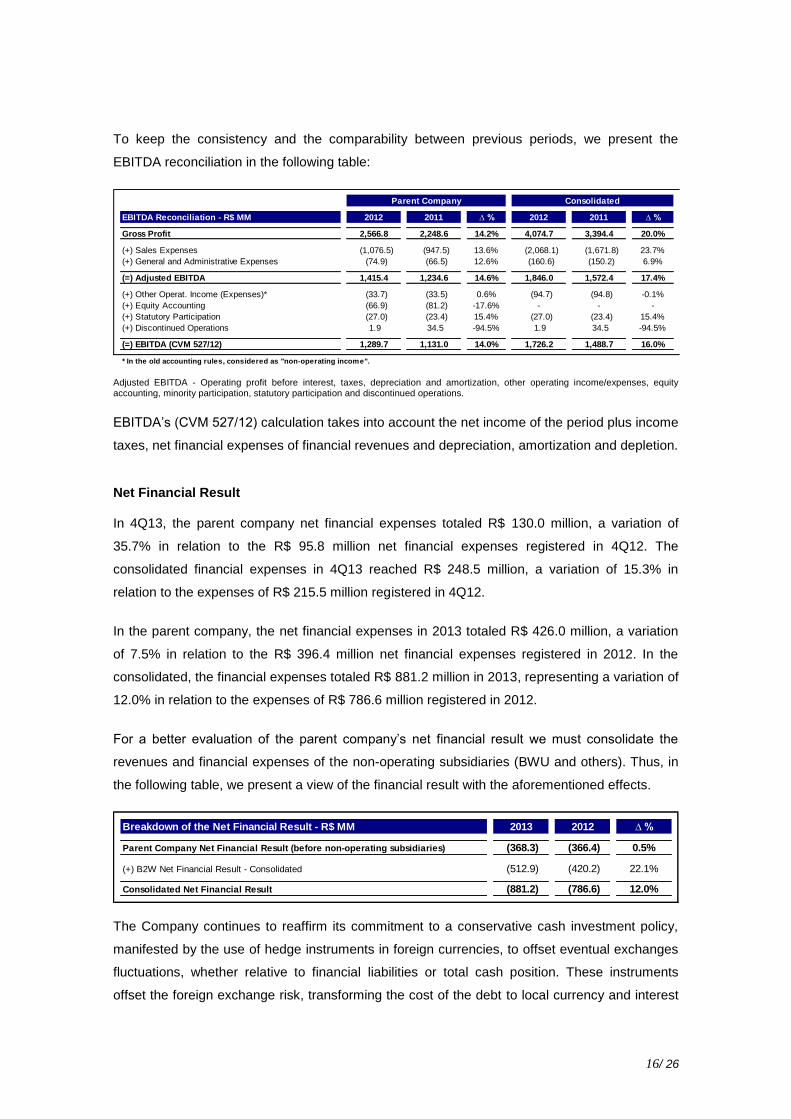

To keep the consistency and the comparability between previous periods, we present the

EBITDA reconciliation in the following table:

EBITDA Reconciliation - R$ MM 2012 2011 ∆ % 2012 2011 ∆ %

Gross Profit 2,566.8 2,248.6 14.2% 4,074.7 3,394.4 20.0%

(+) Sales Expenses (1,076.5) (947.5) 13.6% (2,068.1) (1,671.8) 23.7%

(+) General and Administrative Expenses (74.9) (66.5) 12.6% (160.6) (150.2) 6.9%

(=) Adjusted EBITDA 1,415.4 1,234.6 14.6% 1,846.0 1,572.4 17.4%

(+) Other Operat. Income (Expenses)* (33.7) (33.5) 0.6% (94.7) (94.8) -0.1%

(+) Equity Accounting (66.9) (81.2) -17.6% - - -

(+) Statutory Participation (27.0) (23.4) 15.4% (27.0) (23.4) 15.4%

(+) Discontinued Operations 1.9 34.5 -94.5% 1.9 34.5 -94.5%

(=) EBITDA (CVM 527/12) 1,289.7 1,131.0 14.0% 1,726.2 1,488.7 16.0%

* In the old accounting rules, considered as "non-operating income".

Parent Company Consolidated

Adjusted EBITDA - Operating profit before interest, taxes, depreciation and amortization, other operating income/expenses, equity accounting, minority participation, statutory participation and discontinued operations.

EBITDA’s (CVM 527/12) calculation takes into account the net income of the period plus income

taxes, net financial expenses of financial revenues and depreciation, amortization and depletion.

Net Financial Result In 4Q13, the parent company net financial expenses totaled R$ 130.0 million, a variation of

35.7% in relation to the R$ 95.8 million net financial expenses registered in 4Q12. The

consolidated financial expenses in 4Q13 reached R$ 248.5 million, a variation of 15.3% in

relation to the expenses of R$ 215.5 million registered in 4Q12.

In the parent company, the net financial expenses in 2013 totaled R$ 426.0 million, a variation

of 7.5% in relation to the R$ 396.4 million net financial expenses registered in 2012. In the

consolidated, the financial expenses totaled R$ 881.2 million in 2013, representing a variation of

12.0% in relation to the expenses of R$ 786.6 million registered in 2012.

For a better evaluation of the parent company’s net financial result we must consolidate the

revenues and financial expenses of the non-operating subsidiaries (BWU and others). Thus, in

the following table, we present a view of the financial result with the aforementioned effects.

Breakdown of the Net Financial Result - R$ MM 2013 2012 ∆ %

Parent Company Net Financial Result (before non-operating subsidiaries) (368.3) (366.4) 0.5%

(+) B2W Net Financial Result - Consolidated (512.9) (420.2) 22.1%

Consolidated Net Financial Result (881.2) (786.6) 12.0%

The Company continues to reaffirm its commitment to a conservative cash investment policy,

manifested by the use of hedge instruments in foreign currencies, to offset eventual exchanges

fluctuations, whether relative to financial liabilities or total cash position. These instruments

offset the foreign exchange risk, transforming the cost of the debt to local currency and interest

17/ 26

rates (as a percentage of CDI*). Similarly, it is worth mentioning that the Company’s cash is

invested with Brazil’s largest financial institutions.

*CDI - Interbank Deposit Certificate: average rate of funding through the interbank market.

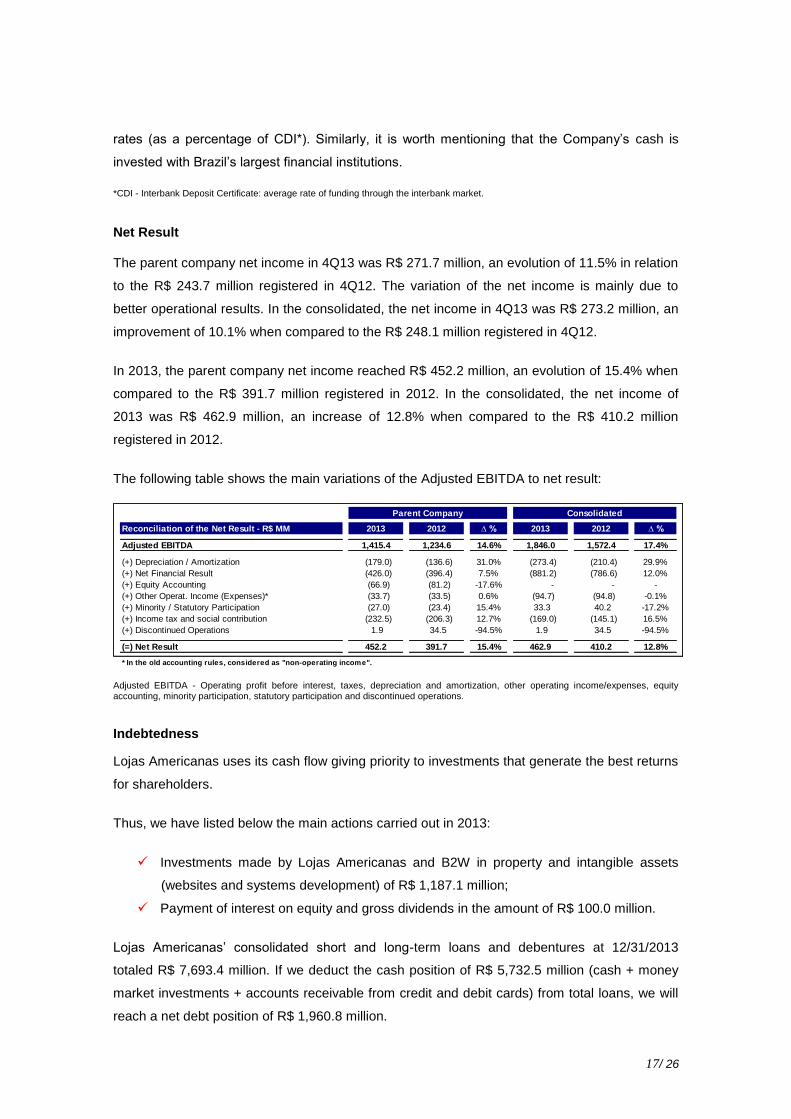

Net Result The parent company net income in 4Q13 was R$ 271.7 million, an evolution of 11.5% in relation

to the R$ 243.7 million registered in 4Q12. The variation of the net income is mainly due to

better operational results. In the consolidated, the net income in 4Q13 was R$ 273.2 million, an

improvement of 10.1% when compared to the R$ 248.1 million registered in 4Q12.

In 2013, the parent company net income reached R$ 452.2 million, an evolution of 15.4% when

compared to the R$ 391.7 million registered in 2012. In the consolidated, the net income of

2013 was R$ 462.9 million, an increase of 12.8% when compared to the R$ 410.2 million

registered in 2012.

The following table shows the main variations of the Adjusted EBITDA to net result:

Reconciliation of the Net Result - R$ MM 2013 2012 ∆ % 2013 2012 ∆ %

Adjusted EBITDA 1,415.4 1,234.6 14.6% 1,846.0 1,572.4 17.4%

(+) Depreciation / Amortization (179.0) (136.6) 31.0% (273.4) (210.4) 29.9%

(+) Net Financial Result (426.0) (396.4) 7.5% (881.2) (786.6) 12.0%

(+) Equity Accounting (66.9) (81.2) -17.6% - - -

(+) Other Operat. Income (Expenses)* (33.7) (33.5) 0.6% (94.7) (94.8) -0.1%

(+) Minority / Statutory Participation (27.0) (23.4) 15.4% 33.3 40.2 -17.2%

(+) Income tax and social contribution (232.5) (206.3) 12.7% (169.0) (145.1) 16.5%

(+) Discontinued Operations 1.9 34.5 -94.5% 1.9 34.5 -94.5%

(=) Net Result 452.2 391.7 15.4% 462.9 410.2 12.8%

* In the old accounting rules, considered as "non-operating income".

Parent Company Consolidated

Adjusted EBITDA - Operating profit before interest, taxes, depreciation and amortization, other operating income/expenses, equity accounting, minority participation, statutory participation and discontinued operations.

Indebtedness

Lojas Americanas uses its cash flow giving priority to investments that generate the best returns

for shareholders.

Thus, we have listed below the main actions carried out in 2013:

Investments made by Lojas Americanas and B2W in property and intangible assets

(websites and systems development) of R$ 1,187.1 million;

Payment of interest on equity and gross dividends in the amount of R$ 100.0 million.

Lojas Americanas’ consolidated short and long-term loans and debentures at 12/31/2013

totaled R$ 7,693.4 million. If we deduct the cash position of R$ 5,732.5 million (cash + money

market investments + accounts receivable from credit and debit cards) from total loans, we will

reach a net debt position of R$ 1,960.8 million.

18/ 26

R$ million

Indebtedness - R$ MM 12/31/2013 12/31/2012 12/31/2013 12/31/2012

Short Term Debt 152.8 598.9 527.7 1,193.6

Short Term Debentures 88.4 144.1 220.0 166.5

Shot Term Indebtedness 241.2 743.0 747.7 1,360.1

Long Term Debt 1,382.2 941.5 4,314.7 2,556.8

Long Term Debentures 2,333.5 1,934.2 2,631.0 2,335.4

Long Term Indebtedness 3,715.7 2,875.7 6,945.7 4,892.2

Total Debt (1) 3,956.9 3,618.7 7,693.4 6,252.3

Cash and banks 325.0 141.2 424.0 183.5

Money market investments 1,471.0 1,330.0 3,664.4 2,924.8

635.1 711.9 1,644.2 1,521.1

Total Cash (2) 2,431.1 2,183.1 5,732.6 4,629.4

Net Cash (Debt) (2) - (1) (1,525.8) (1,435.6) (1,960.8) (1,622.9)

Net Debt / Adjusted EBITDA LTM 1.1 1.2 1.1 1.0

Average Maturity of Debt (in days) 1,178 1,188 1,139 1,075

Accounts receivable

Parent Company Consolidated

Adjusted EBITDA - Operating profit before interest, taxes, depreciation and amortization, other operating income/expenses, equity accounting, minority participation, statutory participation and discontinued operations.

At 12/31/2013, the Company’s net debt was 1.1x the 12-month accumulated EBITDA. The

average maturity of the debt was 1,139 days in 12/31/2013 (37 months). In the parent company

point of view, the Company net debt was 1.1x the 12-month accumulated EBITDA. The average

maturity of the debt was 1,178 days in 12/31/2013 (39 months).

In order to face the uncertainties and the volatility of the financial market, Lojas Americanas is

guided by the principle of preserving cash and extending its debt profile. During the past years,

a number of initiatives were taken with this objective in mind, which permits us to consolidate

the Company’s long-term growth plan. Throughout June, the Company’s Board of Directors

approved the widening of the Shareholder’s Equity of the Fundo de Investimento em Direitos

Creditórios (FIDC) in R$ 707.6 million, reaching approximately R$ 1.3 billion. The FIDC model

of credit card structured by the Company is a unique tool in the market and represents an

important source of fundraising.

Accounts receivable are composed of receivables from credit cards, net of the discounted value

which have immediate liquidity and can be considered as cash. The breakdown of accounts

receivable from the consolidated point of view of Lojas Americanas is shown in the following

table:

R$ million

Accounts Receivable Conciliation - R$ MM 12/31/2013 12/31/2012 12/31/2013 12/31/2012

Gross credit-cards receivable 1,069.9 971.9 3,535.0 2,869.0

Electronic debits and checks receivables 17.8 32.0 17.8 32.0

Receivable discounts (452.6) (292.0) (1,908.6) (1,379.9)

635.1 711.9 1,644.2 1,521.1

Present-value adjustment (13.7) (10.4) (20.7) (17.2)

Allowance for doubtful accounts (2.6) (3.5) (39.1) (53.2)

Other accounts receivable 6.1 4.3 191.3 171.5

Contas a Receber Líquido Consolidado 624.9 702.3 1,775.7 1,622.2

Accounts Receivable from credit / debit cards

Parent Company Consolidated

19/ 26

Because of the adoption of the new CPCs/IFRS, in particular the CPC 38 and its corresponding

IAS 39, the Company began to write off (derecognize) receivables from credit card

administrators in the moment they were effectively discounted (as of the explanatory notes of

the financial statements). However, to better demonstrate the volume of receivables discounted

on the base-dates analyzed, in the chart above the Company presents the accounts receivable

adjusted by the discounts made until the base-dates under analysis.

No Exposure to Foreign Exchange Variations In the end of 2013, Lojas Americanas S.A. balance sheet recorded foreign currency

denominated debt. Such debt, however, is FULLY PROTECTED against any foreign exchange

fluctuations through derivative (swap) operations that replace the foreign exchange risk for the

variation in the basic Brazilian interest rate (CDI).

Sales by Means of Payment The breakdown of the sales, by means of payment in 2013 and 2012 can be seen in the

following table:

Means of Payment 2013 2012 Var. 2013 2012 Var.

Cash 60% 60% - 51% 50% +1 p.p.

Credit Cards 40% 40% - 49% 50% -1 p.p.

Parent Company Consolidated

Parent Company Net Working Capital

Lojas Americanas’ net working capital in 4Q13 was negative 6 day, a variation of 14 days when

compared with the -20 days presented in 4Q12. During the fourth quarter of 2013, we began the

operations of our fourth distribution center, in Uberlândia/MG. This important step for the future

of the Company, in a first moment, increased the inventory level. We believe this is a non-

recurring effect and that, with the operational leverage of the new center, the Company's net

working capital will be benefited.

-20

-6

12/31/2012 12/31/2013

14 Days

-20

-6

12/31/2012 12/31/2013

14 Days

(Net Working Capital = Days of Inventory + Days of Accounts Receivable – Days of Suppliers)

20/ 26

The no need of working capital for Lojas Americanas during the period, demonstrates the

constant striving to improve our operating processes and the development of partnerships with

our suppliers.

Customer Service’s Level

Lojas Americanas is very proud to be the winner of the 2013 Época

Reclame Aqui - As Melhores Empresas para o Consumidor Award, in the

Retail Category. This victory reinforces the commitment that Lojas

Americanas has with customers, whose mission is to "realize the dreams

and meet the consumption needs of the people, sparing their time and

money and exceeding their expectations". We thank our customers and

associates who were part of this achievement.

Lojas Americanas S.A. has RA 1000 Seal since October 2012. It was created

by the claims registrations website, Reclame Aqui, in order to reward

companies that have excellent levels of customer service. Companies that

receive the Seal demonstrate their commitment to the consumer after sales,

increasing consumer confidence in your brand, services and products.

Lojas Americanas received RA 1000 for its excellent levels of customer’s

Response, Solution and Evaluation. With regard to the complaints registered by the website,

100% of the cases were promptly answered and 96% were conveniently solved.

The Company stands out in Reclame Aqui Top 20 Enterprises Rankings*. Among thousands of

subscribed companies, Lojas Americanas S.A. is in 12th PLACE IN THE BEST SOLUTION

INDEXES RANKING, in 8th PLACE IN THE BEST RETURN TO DO BUSINESS INDEXES

RANKING and in 10th PLACE IN THE BEST AVERAGE EVALUATIONS RANKING.

The Seal and the important position reinforce Lojas Americanas’ goal of bringing more

convenience to their clients and exceeding their expectations when meeting their needs.

* As of December 31, 2013

21/ 26

B2W Indicators

We are presenting below the results for 2013 of our subsidiary B2W (BOVESPA: BTOW3).

The accounting information that serves as the basis for the following comments are presented

according to international financial reporting standards (IFRS) as well as the regulations issued

by the Brazilian Securities Exchange Commission (CVM) and the Novo Mercado listing

regulations, and are in reais (R$). The comparisons refer to 2012.

B2W DIGITAL announces Gross Revenue of R$ 6,964.8 million in 2013

In 2013, the consolidated gross revenue reached R$ 6,964.8 million comparing to R$ 5,421.0

million in 2012, representing a growth of 28.5%. In 4Q13, the consolidated gross revenue

reached R$ 2,366.2, a growth of 29.4% versus 4Q12;

B2W DIGITAL announces Adjusted EBITDA of R$ 431.1 million in 2013

In 2013, consolidated adjusted EBITDA reached R$ 431.1 million comparing to R$ 331.2

million in 2012, representing a growth of 30.2%. In 4Q13, consolidated adjusted EBITDA

reached R$ 162.5 million, a growth of 42.4% versus 4Q12;

B2W DIGITAL announces capital increase in the amount of R$ 2.38 billion

The Capital Increase aims to improve the Company’s capital structure and the resources

obtained with this will be destined to the amortization of part of the Company’s debt;

B2W DIGITAL launches the web services platform [B] Seller

The [B] Seller is an online store creation and backoffice/ERP system integrated platform, that

offers to the merchants the possibility to create and operate their online stores with high

performance;

B2W DIGITAL will operate the Ipiranga’s “KM de Vantagens” online store

B2W DIGITAL was chosen to operate the “KM de Vantagens” e-commerce platform through

Shoptime brand. In addition, the operation will allow the Ipiranga loyalty program clients to

change the rewards for products of the brand;

B2W DIGITAL announces the launch of 4 private label brands

B2W launched in December/13 the private label brands Newme, Meemo, Topdesk and Orb,

that are available in Americanas.com, Submarino and Shoptime websites. The brands are

related respectively to Healthy and Beauty, Petshop, Stationery and Furniture categories.

Adjusted EBITDA (Operational earnings before interest, taxes, depreciation and amortization and excluding other operational revenues/expenses and equity accounting).

22/ 26

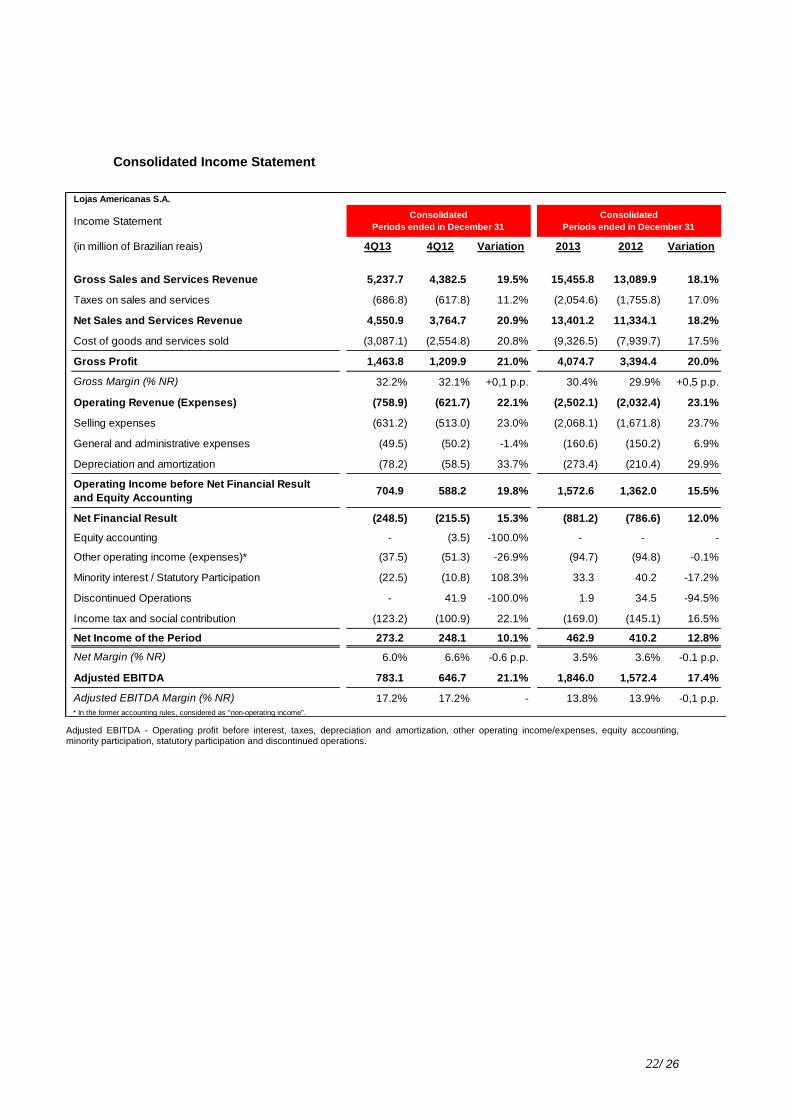

Consolidated Income Statement

Lojas Americanas S.A.

Income Statement

(in million of Brazilian reais) 4Q13 4Q12 Variation 2013 2012 Variation

Gross Sales and Services Revenue 5,237.7 4,382.5 19.5% 15,455.8 13,089.9 18.1%

Taxes on sales and services (686.8) (617.8) 11.2% (2,054.6) (1,755.8) 17.0%

Net Sales and Services Revenue 4,550.9 3,764.7 20.9% 13,401.2 11,334.1 18.2%

Cost of goods and services sold (3,087.1) (2,554.8) 20.8% (9,326.5) (7,939.7) 17.5%

Gross Profit 1,463.8 1,209.9 21.0% 4,074.7 3,394.4 20.0%

Gross Margin (% NR) 32.2% 32.1% +0,1 p.p. 30.4% 29.9% +0,5 p.p.

Operating Revenue (Expenses) (758.9) (621.7) 22.1% (2,502.1) (2,032.4) 23.1%

Selling expenses (631.2) (513.0) 23.0% (2,068.1) (1,671.8) 23.7%

General and administrative expenses (49.5) (50.2) -1.4% (160.6) (150.2) 6.9%

Depreciation and amortization (78.2) (58.5) 33.7% (273.4) (210.4) 29.9%

Operating Income before Net Financial Result

and Equity Accounting704.9 588.2 19.8% 1,572.6 1,362.0 15.5%

Net Financial Result (248.5) (215.5) 15.3% (881.2) (786.6) 12.0%

Equity accounting - (3.5) -100.0% - - -

Other operating income (expenses)* (37.5) (51.3) -26.9% (94.7) (94.8) -0.1%

Minority interest / Statutory Participation (22.5) (10.8) 108.3% 33.3 40.2 -17.2%

Discontinued Operations - 41.9 -100.0% 1.9 34.5 -94.5%

Income tax and social contribution (123.2) (100.9) 22.1% (169.0) (145.1) 16.5%

Net Income of the Period 273.2 248.1 10.1% 462.9 410.2 12.8%

Net Margin (% NR) 6.0% 6.6% -0.6 p.p. 3.5% 3.6% -0.1 p.p.

Adjusted EBITDA 783.1 646.7 21.1% 1,846.0 1,572.4 17.4%

Adjusted EBITDA Margin (% NR) 17.2% 17.2% - 13.8% 13.9% -0,1 p.p.

* In the former accounting rules, considered as "non-operating income".

Consolidated

Periods ended in December 31

Consolidated

Periods ended in December 31

Adjusted EBITDA - Operating profit before interest, taxes, depreciation and amortization, other operating income/expenses, equity accounting, minority participation, statutory participation and discontinued operations.

23/ 26

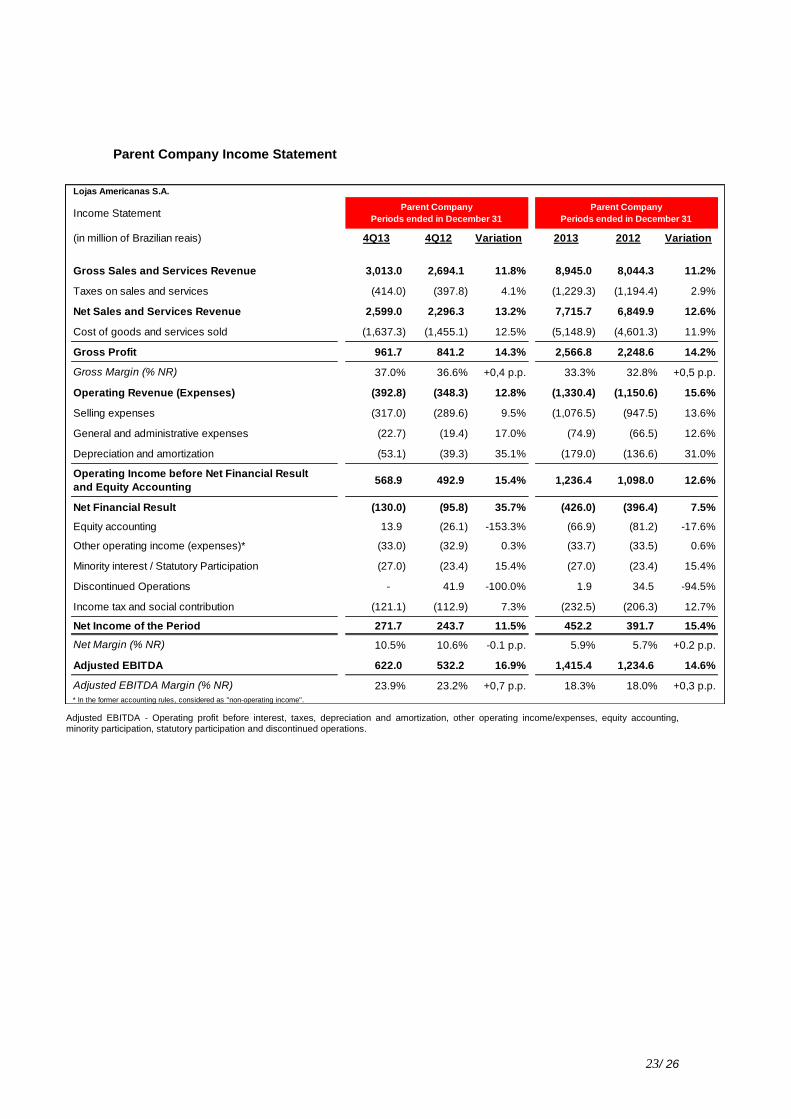

Parent Company Income Statement

Lojas Americanas S.A.

Income Statement

(in million of Brazilian reais) 4Q13 4Q12 Variation 2013 2012 Variation

Gross Sales and Services Revenue 3,013.0 2,694.1 11.8% 8,945.0 8,044.3 11.2%

Taxes on sales and services (414.0) (397.8) 4.1% (1,229.3) (1,194.4) 2.9%

Net Sales and Services Revenue 2,599.0 2,296.3 13.2% 7,715.7 6,849.9 12.6%

Cost of goods and services sold (1,637.3) (1,455.1) 12.5% (5,148.9) (4,601.3) 11.9%

Gross Profit 961.7 841.2 14.3% 2,566.8 2,248.6 14.2%

Gross Margin (% NR) 37.0% 36.6% +0,4 p.p. 33.3% 32.8% +0,5 p.p.

Operating Revenue (Expenses) (392.8) (348.3) 12.8% (1,330.4) (1,150.6) 15.6%

Selling expenses (317.0) (289.6) 9.5% (1,076.5) (947.5) 13.6%

General and administrative expenses (22.7) (19.4) 17.0% (74.9) (66.5) 12.6%

Depreciation and amortization (53.1) (39.3) 35.1% (179.0) (136.6) 31.0%

Operating Income before Net Financial Result

and Equity Accounting568.9 492.9 15.4% 1,236.4 1,098.0 12.6%

Net Financial Result (130.0) (95.8) 35.7% (426.0) (396.4) 7.5%

Equity accounting 13.9 (26.1) -153.3% (66.9) (81.2) -17.6%

Other operating income (expenses)* (33.0) (32.9) 0.3% (33.7) (33.5) 0.6%

Minority interest / Statutory Participation (27.0) (23.4) 15.4% (27.0) (23.4) 15.4%

Discontinued Operations - 41.9 -100.0% 1.9 34.5 -94.5%

Income tax and social contribution (121.1) (112.9) 7.3% (232.5) (206.3) 12.7%

Net Income of the Period 271.7 243.7 11.5% 452.2 391.7 15.4%

Net Margin (% NR) 10.5% 10.6% -0.1 p.p. 5.9% 5.7% +0.2 p.p.

Adjusted EBITDA 622.0 532.2 16.9% 1,415.4 1,234.6 14.6%

Adjusted EBITDA Margin (% NR) 23.9% 23.2% +0,7 p.p. 18.3% 18.0% +0,3 p.p.

* In the former accounting rules, considered as "non-operating income".

Parent Company

Periods ended in December 31

Parent Company

Periods ended in December 31

Adjusted EBITDA - Operating profit before interest, taxes, depreciation and amortization, other operating income/expenses, equity accounting, minority participation, statutory participation and discontinued operations.

24/ 26

6. CORPORATE GOVERNANCE AND CAPITAL MARKETS

Since 1940, Lojas Americanas S.A. has been listed on Brazilian Stock Exchange

(BM&FBOVESPA). The Company has a shareholder base composed of common shares

(LAME3) and preferred shares (LAME4).

Lojas Americanas has a Board of Directors consisting of eight members, five appointed by the

controllers, one appointed by minority shareholders, and two appointed by the Board of

Directors. Lojas Americanas also has a Fiscal Council formed by three members, two being

indicated by the controllers and one indicated by the minority shareholders.

The Board of Directors and the Executive Board determine the Company's guidelines,

supported by internal committees, including the Finance Committee, the People and

Remuneration Committee, the Digital Committee and the Sustainability Committee.

100% Tag Along Rights for all Shareholders

Lojas Americanas has maintained a commitment, as part of its Bylaws, to concede 100% tag-

along rights for all of the Company’s common and preferred shares since 2006. This guarantees

that all Lojas Americanas’ shareholders will receive equal treatment in the event of a change of

ownership, with the right to sell their shares under the same conditions as the controlling

shareholders being guaranteed.

Dividends Policy

In 2013, R$ 100.00 million was distributed to the shareholders, of which R$ 62.5 million was in

the form of dividends and R$ 37.5 million was as payment of interest on own equity (before

income tax withheld at the source), based on the net profit realized during the year of 2012. The

Company’s Bylaws, in line with the principles of existing legislation, establish the minimum value

for dividends at 25% of net profit for the fiscal period, after the setting up of a 5% legal reserve.

Share Buy-Back Program

Lojas Americanas has had a buy-back program in effect since 2003 for the purchase of

Company shares, with the objective of holding them in treasury or future cancellation. The

program calls for the buy-back of up to 4,114,520 common nominative subscribed shares and

4,803,596 nominative subscribed preferred shares.

25/ 26

Stock

Lojas Americanas preferred shares (LAME4) are traded on the Ibovespa, the most important

indicator of the average performance of prices of shares traded on Brazilian stock markets.

Moreover, the Company’s common and preferred shares are part of the differentiated Share

Tag-Along Index (ITAG). This indicator is composed of the shares of companies that offer the

same conditions to minority shareholders in the event of a change in ownership control.

Furthermore, Lojas Americanas S.A. also is on other important indexes, such as the IBRX-50,

ICO2, ICON, IVBX-2, MLCX and MSCI-Barra.

Independent Auditors

Pursuant to CVM Instruction 381, the Company reports that its independent auditors rendered

services for evaluation of companies acquisitions to the Company and its subsidiary B2W

having been hired on February 20, April 19, July 05, and September 05, 2013, receiving fees of

R$ 260,000, representing about 20% of the total fees related to the external auditing services.

The aforementioned services already have been carried out and are not in conflict with the rules

regarding independence of independent auditors.

The Company’s policy regarding the hiring of independent auditors for services not related to

the outside audit assures that there is no conflict of interest or loss of independence or

objectivity with regard to the independent auditors’ work.

26/ 26

7. SOCIO-ENVIRONMENTAL ASPECTS

Sustainability Committee

Aligned with the vision of the Company as a socially and environmentally

responsible company, the Sustainability Committee - Green Company concept

was created in 2007 and formalized by the Board of Directors in 2010. Its

objectives are: to strengthen environmental awareness, reduce water and energy

consumption and the generation of waste, and develop environmental projects

applicable to the reality of the business and of the communities.

As of the establishment of this committee, the subject has gained great resonance within the

Company. To satisfy the requirements that have emerged, a specific Sustainability department

was set up in 2012, dedicated to developing suitable socio-environmental and economic

actions.

Social and Environmental Aspects

The following are the main highlights of the Sustainability Area in 2013:

We published our first Sustainability Report, already according to the GRI guidelines -

the highest worldwide standard for sustainability reports

We inaugurated B2W Digital's new sustainable building, the BIT (B2W Technology and

Innovation), following LEED certification guidelines - the highest standard for

environmentally sustainable buildings in the world.

We joined the Global Compact of the United Nations on November 1. With this, we have

joined forces with other companies that are also committed to these issues.

Partnership with INCA (National Cancer Institute), supporting the Pink October

campaign whose objective is to alert about the importance of early diagnosis of breast

cancer, we donated 1,000 cans of powdered milk, 1,200 books and 40 pouffes for

patients in treatment.

Donation of toys in needy districts of Angra dos Reis and Valença (cities in Rio de

Janeiro state).

Donation of more than 2,000 food hampers and 500 Christmas trees for the residents of

the Alemão Complex in the city of Rio de Janeiro.

For more information about the Company's environmental and economic actions in 2013, visit

the Sustainability Report 2013 through the following link http://ri.lasa.com.br/.

![DSAT · 2015. 7. 22. · cheng han weng long so, u sam sol, chi mencj sonci chin cheng sono tan i sot', sou, sot], sou, sou, sot], sou, sot], sou, sou, sou, sou, in 10 hong kam choi](https://static.fdocuments.in/doc/165x107/60c2f5f91082346bf41443bb/2015-7-22-cheng-han-weng-long-so-u-sam-sol-chi-mencj-sonci-chin-cheng-sono.jpg)