Management Performance Tool jbb 6

48

Management Performance Tool Cooperative Management & Governance Seminar Nueva Segovia Consortium of Cooperative Caoayan, Ilocos Sur October 5-7, 2011

-

Upload

jo-balucanag-bitonio -

Category

Business

-

view

2.952 -

download

0

description

Cooperative management performance tools

Transcript of Management Performance Tool jbb 6

Management

Performance

Tool

Cooperative Management & Governance Seminar

Nueva Segovia Consortium of Cooperative

Caoayan, Ilocos Sur

October 5-7, 2011

Management Performance

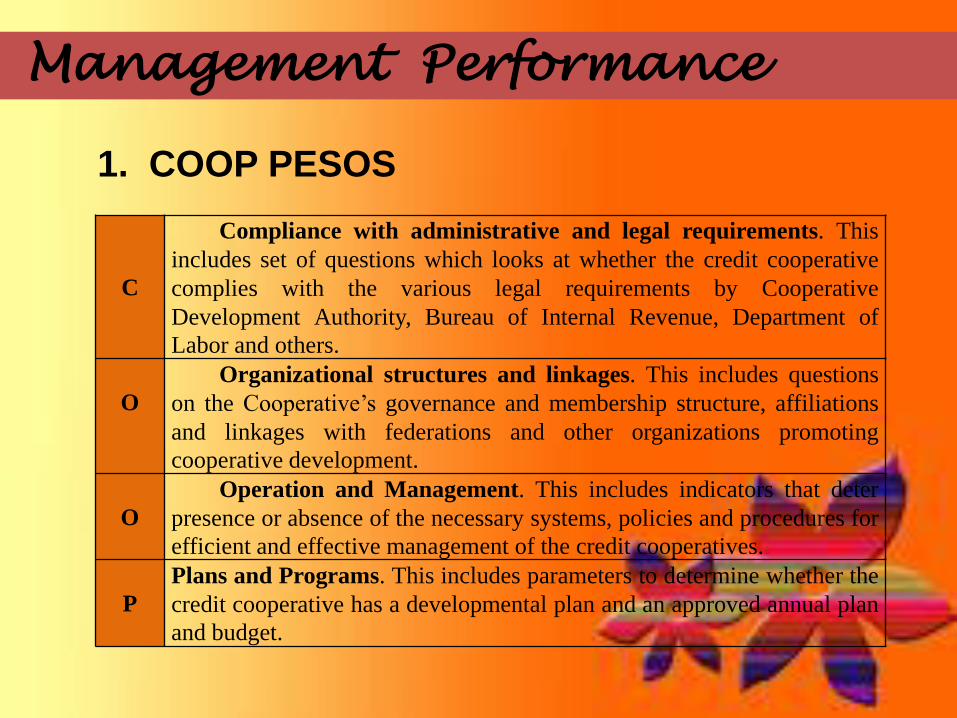

C

Compliance with administrative and legal requirements. This

includes set of questions which looks at whether the credit cooperative

complies with the various legal requirements by Cooperative

Development Authority, Bureau of Internal Revenue, Department of

Labor and others.

O

Organizational structures and linkages. This includes questions

on the Cooperative’s governance and membership structure, affiliations

and linkages with federations and other organizations promoting

cooperative development.

O

Operation and Management. This includes indicators that deter

presence or absence of the necessary systems, policies and procedures for

efficient and effective management of the credit cooperatives.

P

Plans and Programs. This includes parameters to determine whether the

credit cooperative has a developmental plan and an approved annual plan

and budget.

1. COOP PESOS

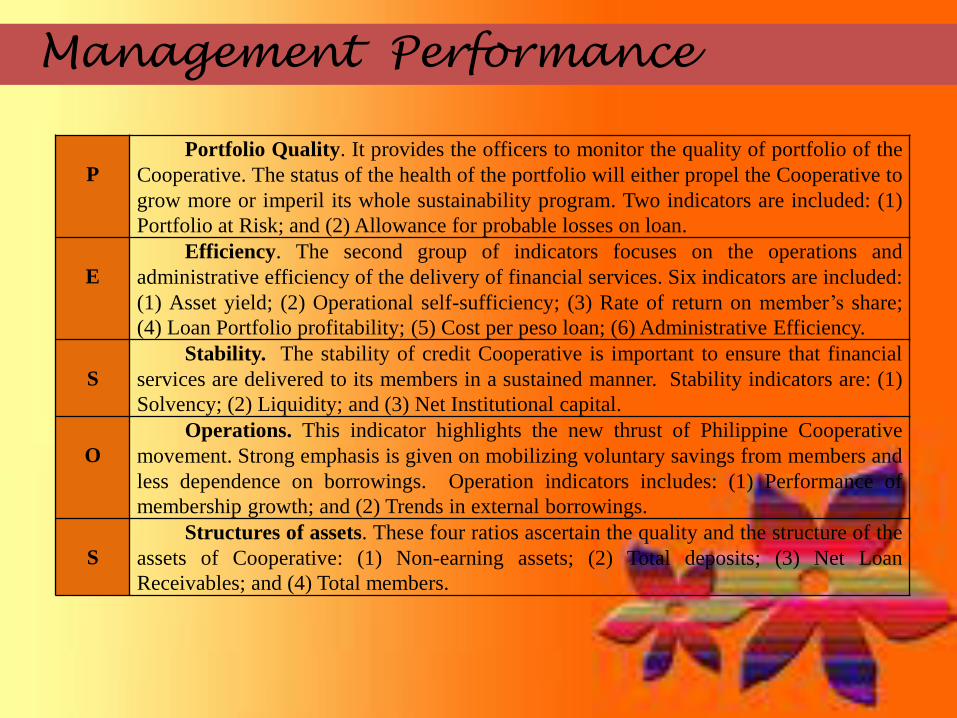

Management Performance

P

Portfolio Quality. It provides the officers to monitor the quality of portfolio of the

Cooperative. The status of the health of the portfolio will either propel the Cooperative to

grow more or imperil its whole sustainability program. Two indicators are included: (1)

Portfolio at Risk; and (2) Allowance for probable losses on loan.

E

Efficiency. The second group of indicators focuses on the operations and

administrative efficiency of the delivery of financial services. Six indicators are included:

(1) Asset yield; (2) Operational self-sufficiency; (3) Rate of return on member’s share;

(4) Loan Portfolio profitability; (5) Cost per peso loan; (6) Administrative Efficiency.

S

Stability. The stability of credit Cooperative is important to ensure that financial

services are delivered to its members in a sustained manner. Stability indicators are: (1)

Solvency; (2) Liquidity; and (3) Net Institutional capital.

O

Operations. This indicator highlights the new thrust of Philippine Cooperative

movement. Strong emphasis is given on mobilizing voluntary savings from members and

less dependence on borrowings. Operation indicators includes: (1) Performance of

membership growth; and (2) Trends in external borrowings.

S

Structures of assets. These four ratios ascertain the quality and the structure of the

assets of Cooperative: (1) Non-earning assets; (2) Total deposits; (3) Net Loan

Receivables; and (4) Total members.

a. Profitability Ratio

Measure the capacity of the cooperative to

generate surplus

Net Operating Surplus

---------------------------------------------------------------

Gross Operating Revenue or Gross Margin

30% and above 5 points

25% to below 30% 4 points

10% to below 25% 3 points

5% to below 10% 2 points

below 5% 1 point

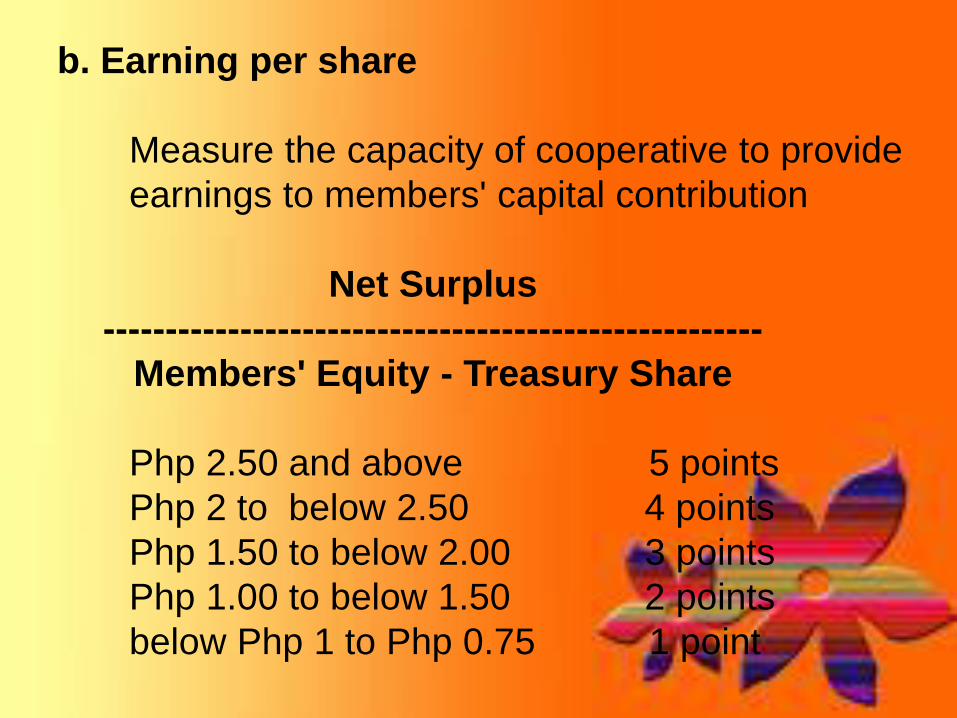

b. Earning per share

Measure the capacity of cooperative to provide

earnings to members' capital contribution

Net Surplus

-----------------------------------------------------

Members' Equity - Treasury Share

Php 2.50 and above 5 points

Php 2 to below 2.50 4 points

Php 1.50 to below 2.00 3 points

Php 1.00 to below 1.50 2 points

below Php 1 to Php 0.75 1 point

c. Profitability Growth Rate

Measure the growth rate of profitability

for the period

Earning/share end – Earning/share

beginning

------------------------------------------------------

Earning per share beginning

100% and above 5 points

75% to below 100% 4 points

50% to below 75% 3 points

30% to below 50% 2 point

10% but below 30% 1 point

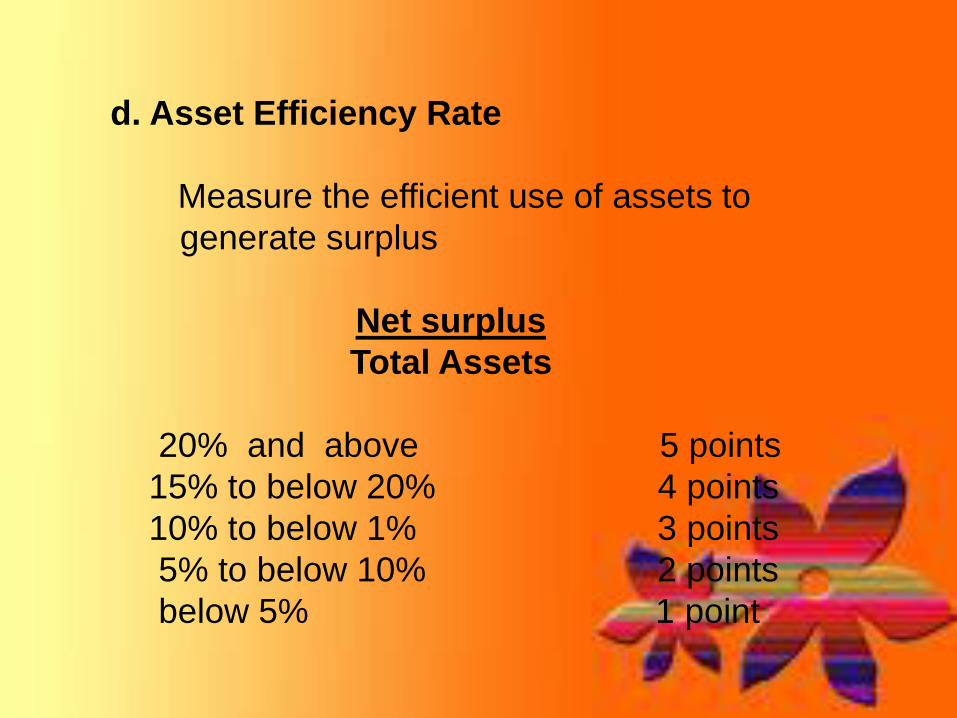

d. Asset Efficiency Rate

Measure the efficient use of assets to

generate surplus

Net surplus

Total Assets

20% and above 5 points

15% to below 20% 4 points

10% to below 1% 3 points

5% to below 10% 2 points

below 5% 1 point

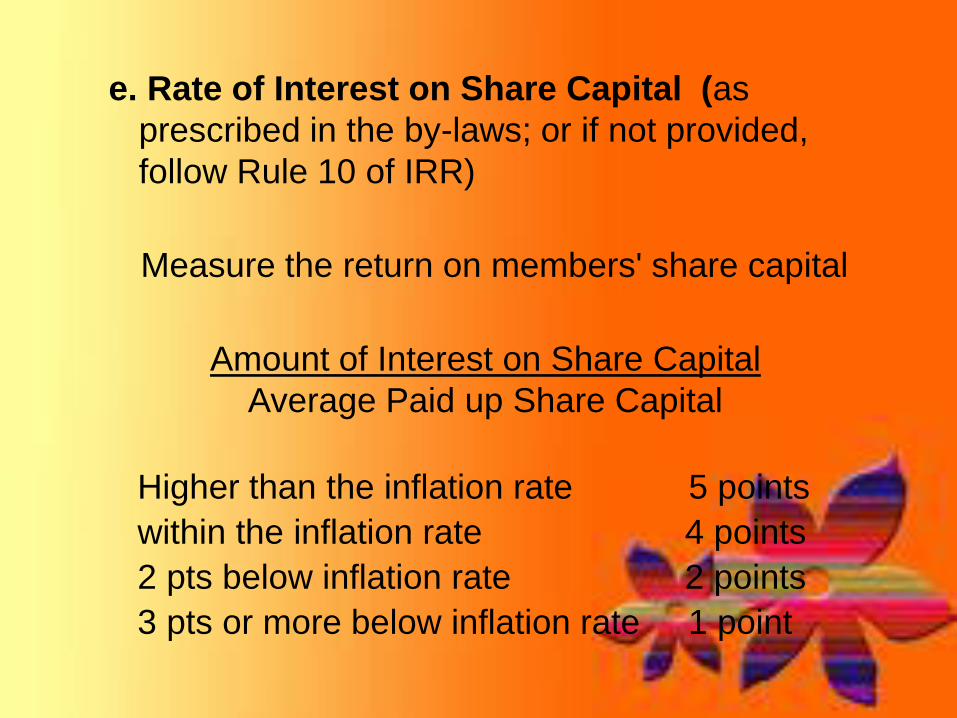

e. Rate of Interest on Share Capital (as

prescribed in the by-laws; or if not provided,

follow Rule 10 of IRR)

Measure the return on members' share capital

Amount of Interest on Share Capital

Average Paid up Share Capital

Higher than the inflation rate 5 points

within the inflation rate 4 points

2 pts below inflation rate 2 points

3 pts or more below inflation rate 1 point

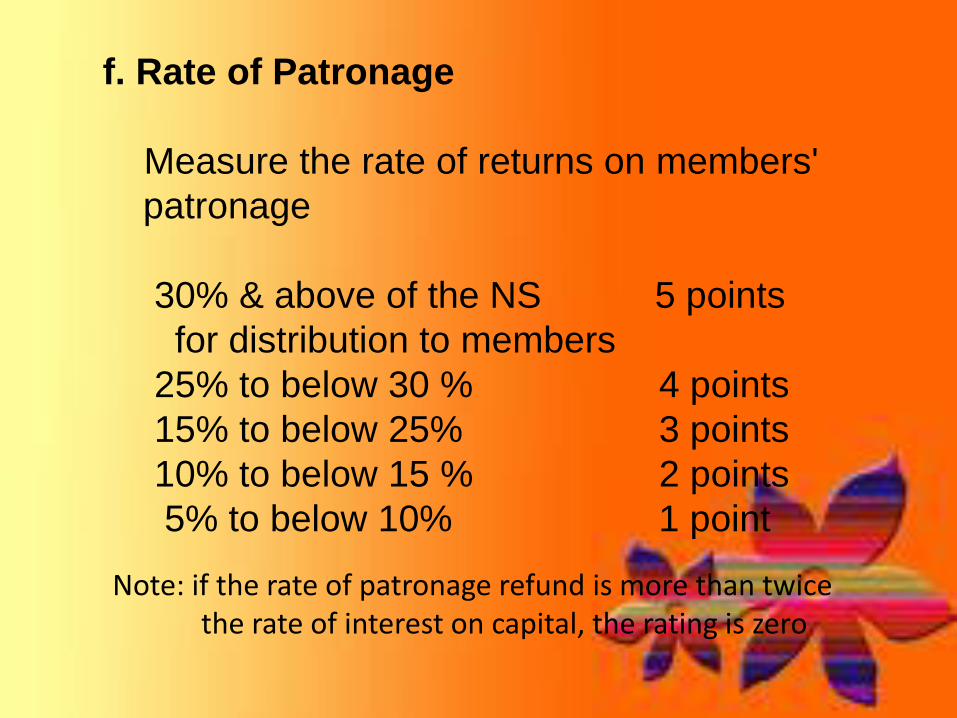

f. Rate of Patronage

Measure the rate of returns on members'

patronage

30% & above of the NS 5 points

for distribution to members

25% to below 30 % 4 points

15% to below 25% 3 points

10% to below 15 % 2 points

5% to below 10% 1 point

Note: if the rate of patronage refund is more than twice the rate of interest on capital, the rating is zero

a. Net Institutional Capital

Measure the level of institutional capital after subtracting

the allowance for probable losses

(Reserves + APLL and/or A/R) – (Problem Assets + Past Due

Receivables + Receivables Under Litigations +

Restructured Receivables)

-----------------------------------------------------------------------------------

Total Assets

10% and above 6 points

8% to below 10% 5 points

6% to below 8% 4 points

4% to below 6% 3 points

2% to below 4% 2 points

below 2% 1 point

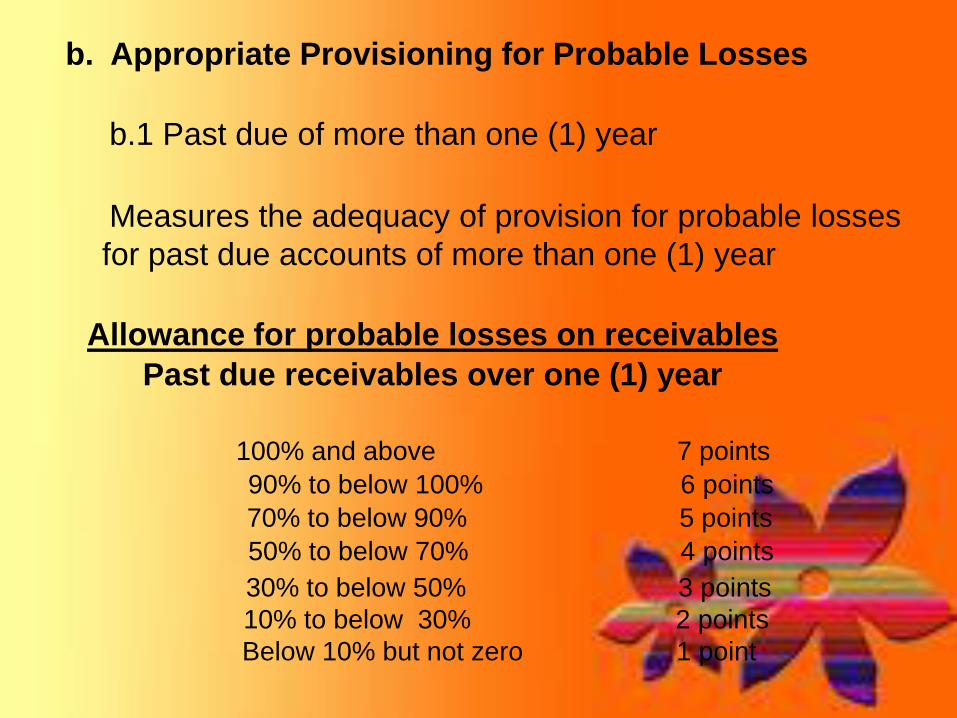

b. Appropriate Provisioning for Probable Losses

b.1 Past due of more than one (1) year

Measures the adequacy of provision for probable losses

for past due accounts of more than one (1) year

Allowance for probable losses on receivables

Past due receivables over one (1) year

100% and above 7 points

90% to below 100% 6 points

70% to below 90% 5 points

50% to below 70% 4 points

30% to below 50% 3 points

10% to below 30% 2 points

Below 10% but not zero 1 point

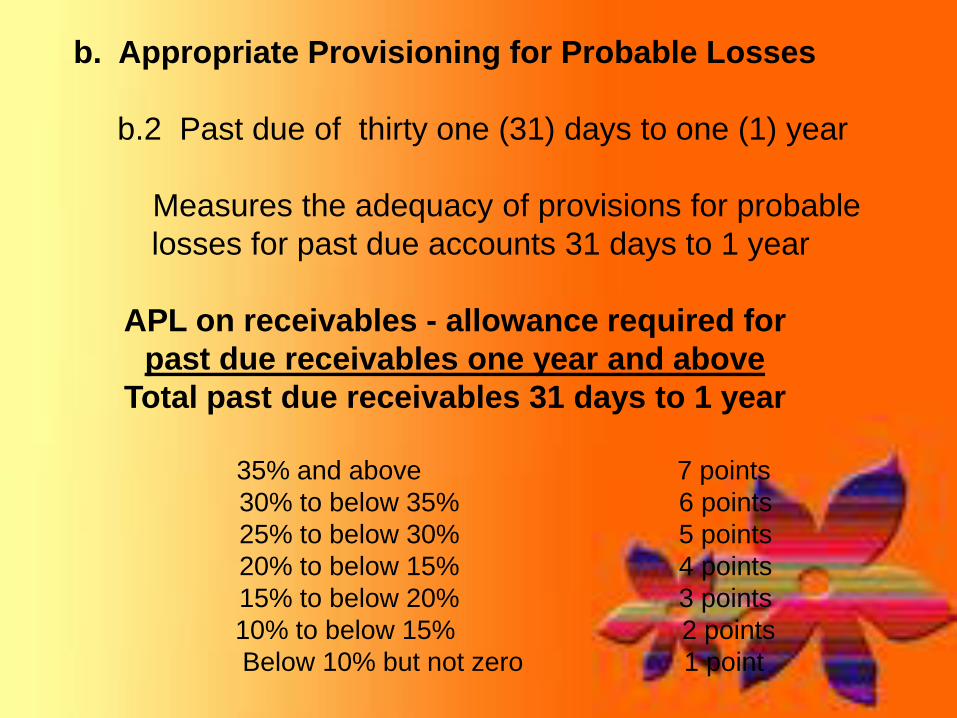

b. Appropriate Provisioning for Probable Losses

b.2 Past due of thirty one (31) days to one (1) year

Measures the adequacy of provisions for probable

losses for past due accounts 31 days to 1 year

APL on receivables - allowance required for

past due receivables one year and above

Total past due receivables 31 days to 1 year

35% and above 7 points

30% to below 35% 6 points

25% to below 30% 5 points

20% to below 15% 4 points

15% to below 20% 3 points

10% to below 15% 2 points

Below 10% but not zero 1 point

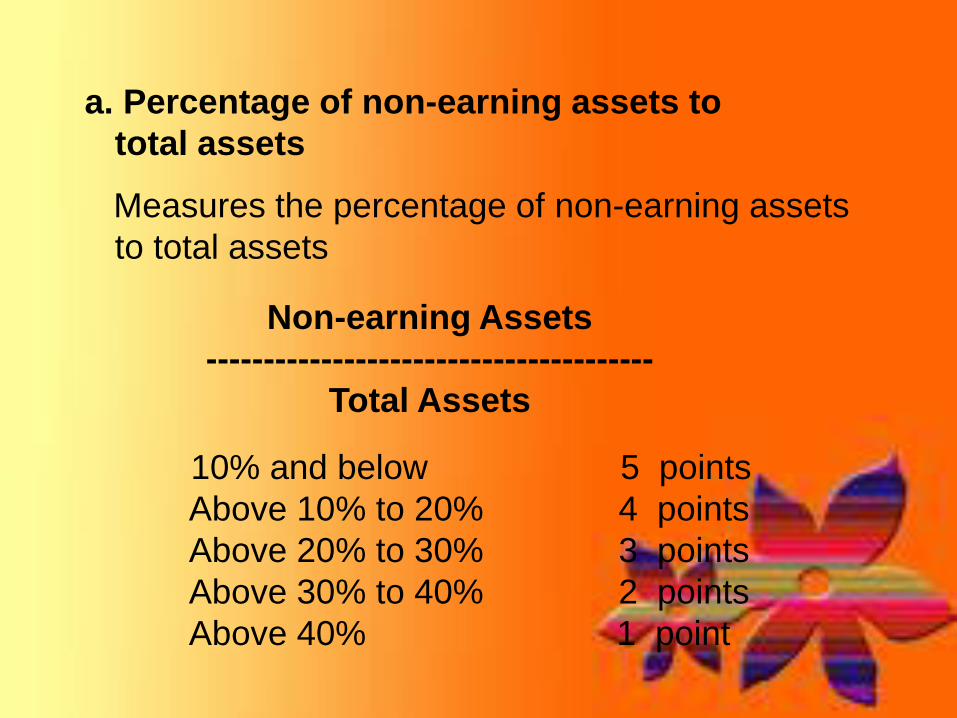

a. Percentage of non-earning assets to

total assets

Measures the percentage of non-earning assets

to total assets

Non-earning Assets

---------------------------------------

Total Assets

10% and below 5 points

Above 10% to 20% 4 points

Above 20% to 30% 3 points

Above 30% to 40% 2 points

Above 40% 1 point

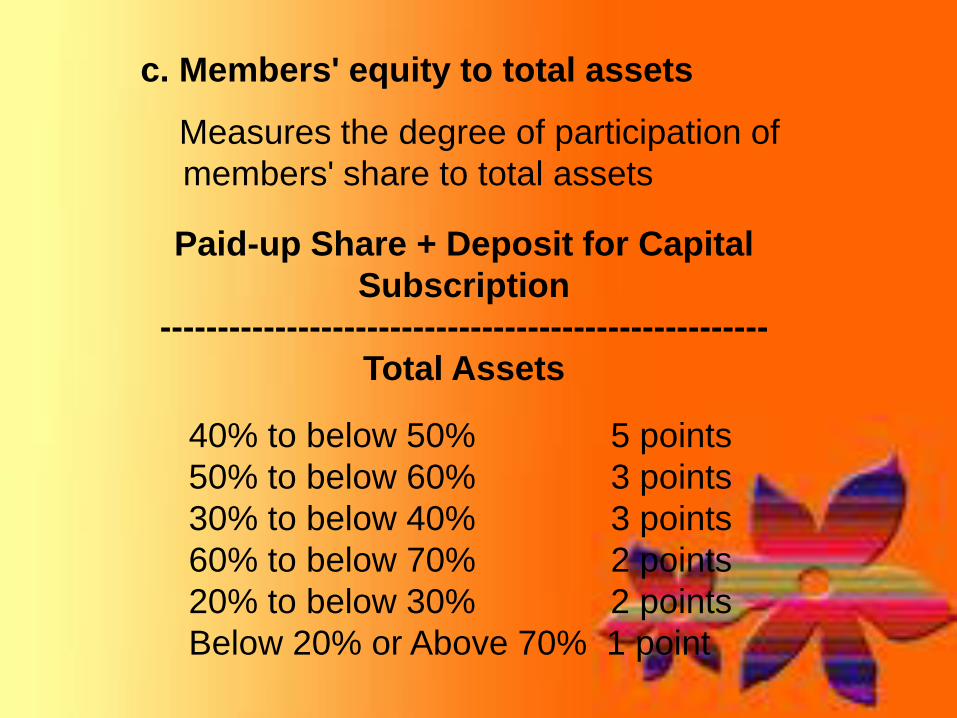

c. Members' equity to total assets

Measures the degree of participation of

members' share to total assets

Paid-up Share + Deposit for Capital

Subscription

-----------------------------------------------------

Total Assets

40% to below 50% 5 points

50% to below 60% 3 points

30% to below 40% 3 points

60% to below 70% 2 points

20% to below 30% 2 points

Below 20% or Above 70% 1 point

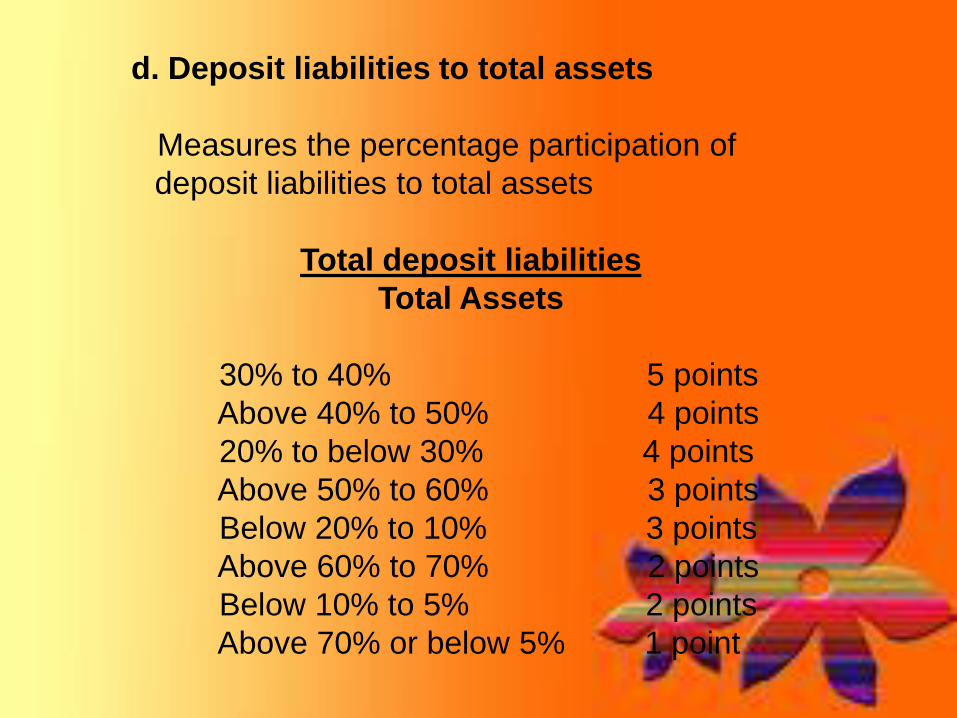

d. Deposit liabilities to total assets

Measures the percentage participation of

deposit liabilities to total assets

Total deposit liabilities

Total Assets

30% to 40% 5 points

Above 40% to 50% 4 points

20% to below 30% 4 points

Above 50% to 60% 3 points

Below 20% to 10% 3 points

Above 60% to 70% 2 points

Below 10% to 5% 2 points

Above 70% or below 5% 1 point

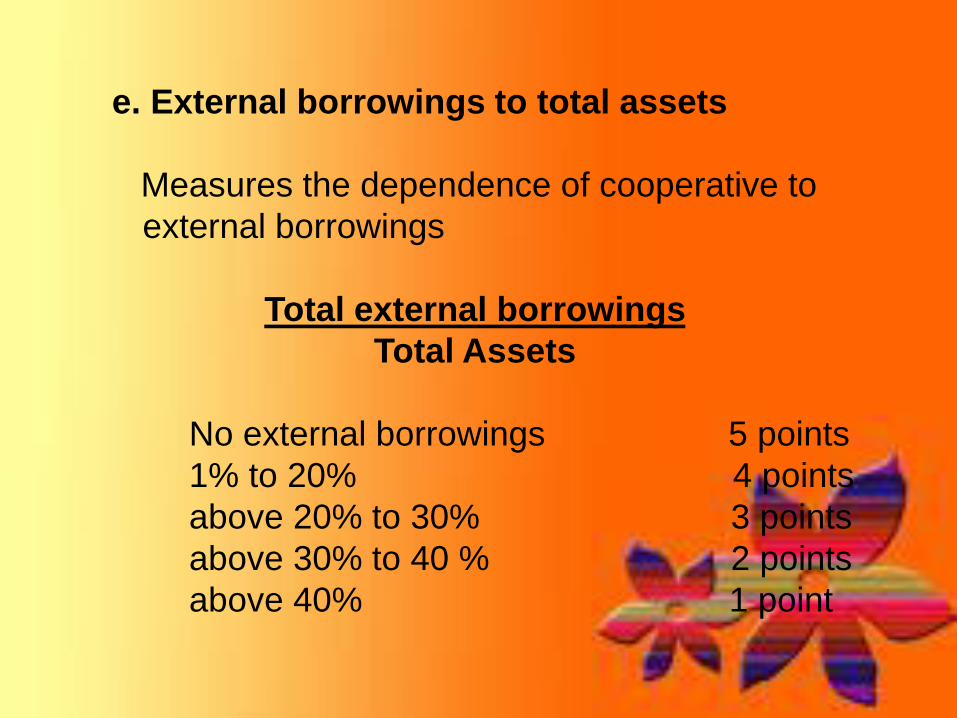

e. External borrowings to total assets

Measures the dependence of cooperative to

external borrowings

Total external borrowings

Total Assets

No external borrowings 5 points

1% to 20% 4 points

above 20% to 30% 3 points

above 30% to 40 % 2 points

above 40% 1 point

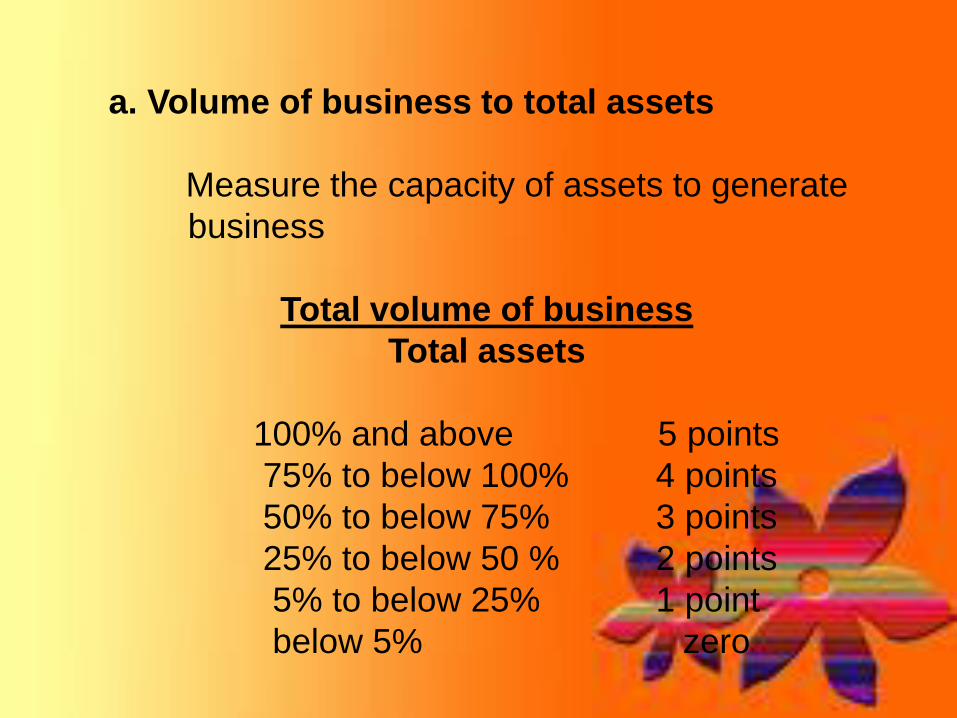

a. Volume of business to total assets

Measure the capacity of assets to generate

business

Total volume of business

Total assets

100% and above 5 points

75% to below 100% 4 points

50% to below 75% 3 points

25% to below 50 % 2 points

5% to below 25% 1 point

below 5% zero

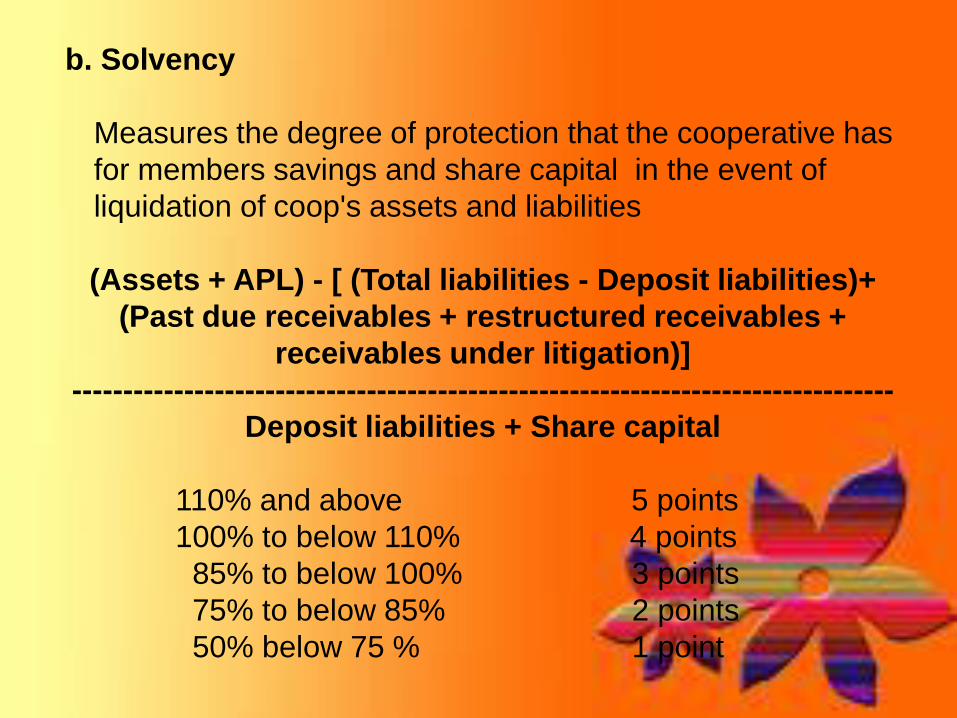

b. Solvency

Measures the degree of protection that the cooperative has

for members savings and share capital in the event of

liquidation of coop's assets and liabilities

(Assets + APL) - [ (Total liabilities - Deposit liabilities)+

(Past due receivables + restructured receivables +

receivables under litigation)]

---------------------------------------------------------------------------------

Deposit liabilities + Share capital

110% and above 5 points

100% to below 110% 4 points

85% to below 100% 3 points

75% to below 85% 2 points

50% below 75 % 1 point

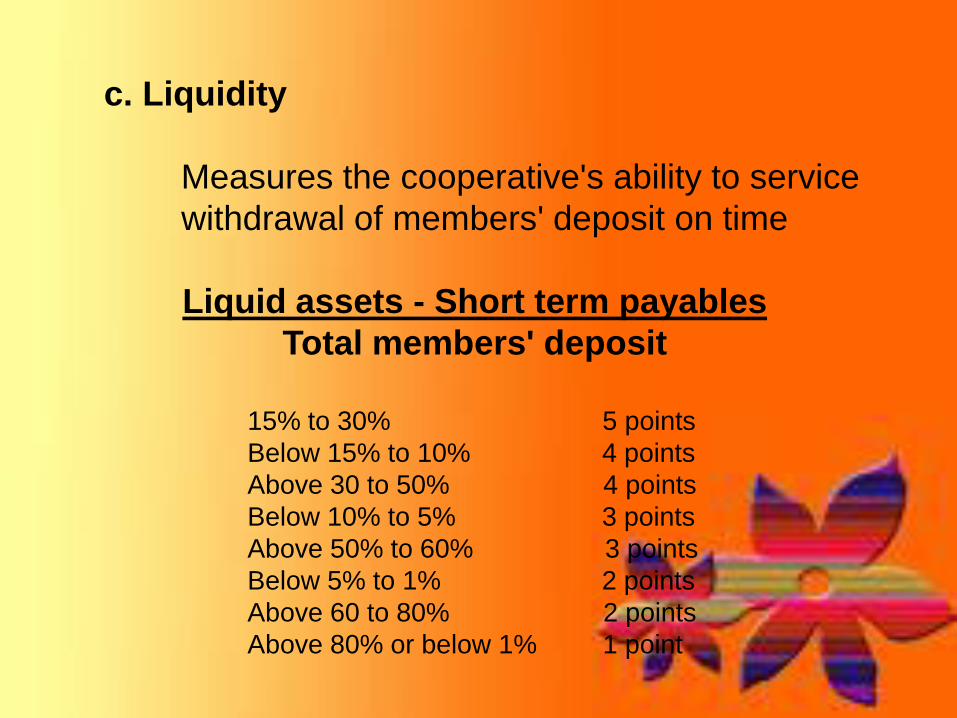

c. Liquidity

Measures the cooperative's ability to service

withdrawal of members' deposit on time

Liquid assets - Short term payables

Total members' deposit

15% to 30% 5 points

Below 15% to 10% 4 points

Above 30 to 50% 4 points

Below 10% to 5% 3 points

Above 50% to 60% 3 points

Below 5% to 1% 2 points

Above 60 to 80% 2 points

Above 80% or below 1% 1 point

d. Efficiency

d.1 Cost per volume of business

Measures the efficiency in managing the cooperative's

business

Operating cost – (Members‘ Benefit Expense

+ Social Service Expense)

----------------------------------------------------------------------------

total volume of business

25 cents and below 5 points

26 to 22 cents 3 points

33 to 39 cents 2 points

40 to 46 cents 1 point

47 cents and above zero

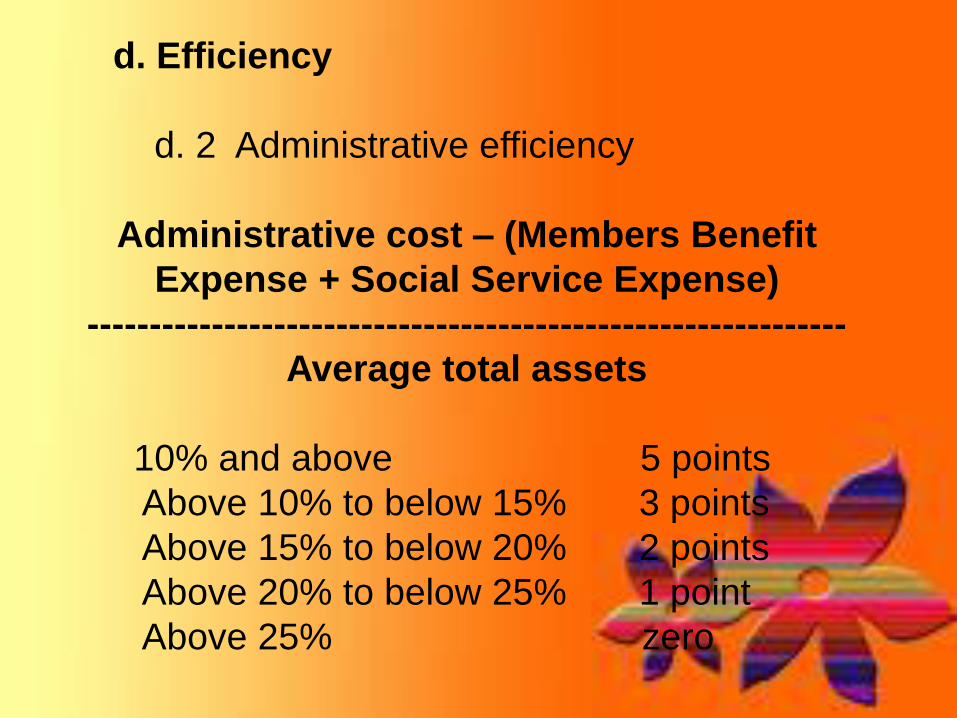

d. Efficiency

d. 2 Administrative efficiency

Administrative cost – (Members Benefit

Expense + Social Service Expense)

-------------------------------------------------------------

Average total assets

10% and above 5 points

Above 10% to below 15% 3 points

Above 15% to below 20% 2 points

Above 20% to below 25% 1 point

Above 25% zero

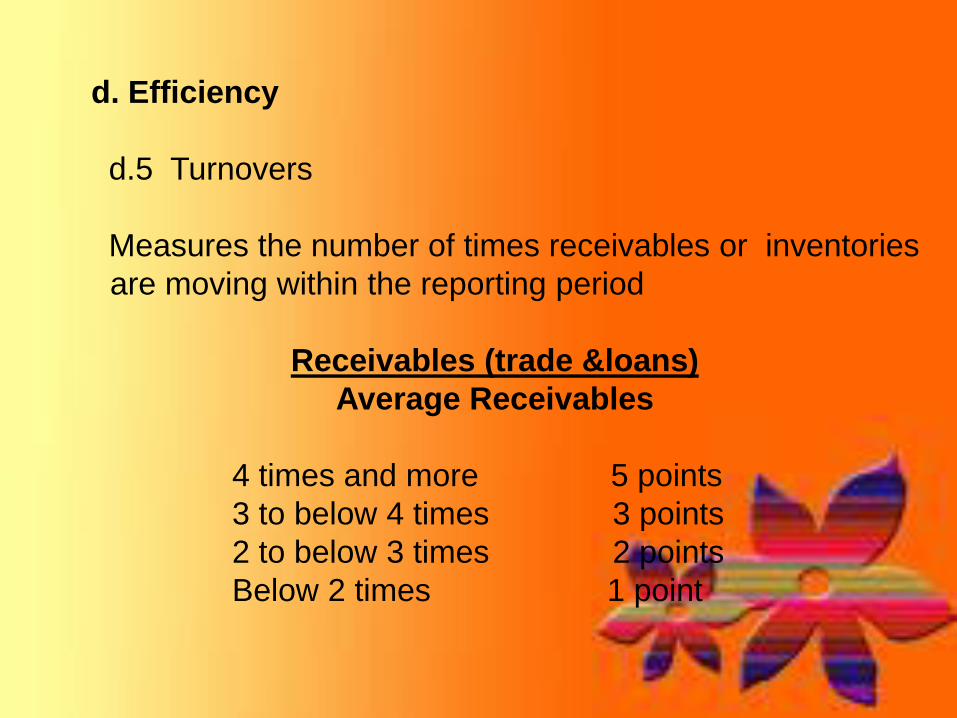

d. Efficiency

d.5 Turnovers

Measures the number of times receivables or inventories

are moving within the reporting period

Receivables (trade &loans)

Average Receivables

4 times and more 5 points

3 to below 4 times 3 points

2 to below 3 times 2 points

Below 2 times 1 point

Protection, Effective Financial

Structure, Asset Quality, Rates of

Return, Liquidity, and Signs of

Growth, the PEARLS system was

originally designed and implemented

with Guatemalan credit unions in the

late 1980s.

4. PEARLS

5. CAMEl

(C) CapitaL(A) Asset quality(M) Management(E) Earnings and(L) Asset Liability management

6. Gawad Pitak

Given by Land Bank of the Philippines

LANDBANK also has its own Cooperative Accreditation

Criteria or CAC, based on the seven pillars of

cooperativism - membership, capital build-up and

savings, leadership and management, business

operations, books of accounts and financial statements,

and affiliations. Using these criteria, LANDBANK annually

rates co-ops and classifies them A, B, C, D, and F

according to their maturity levels

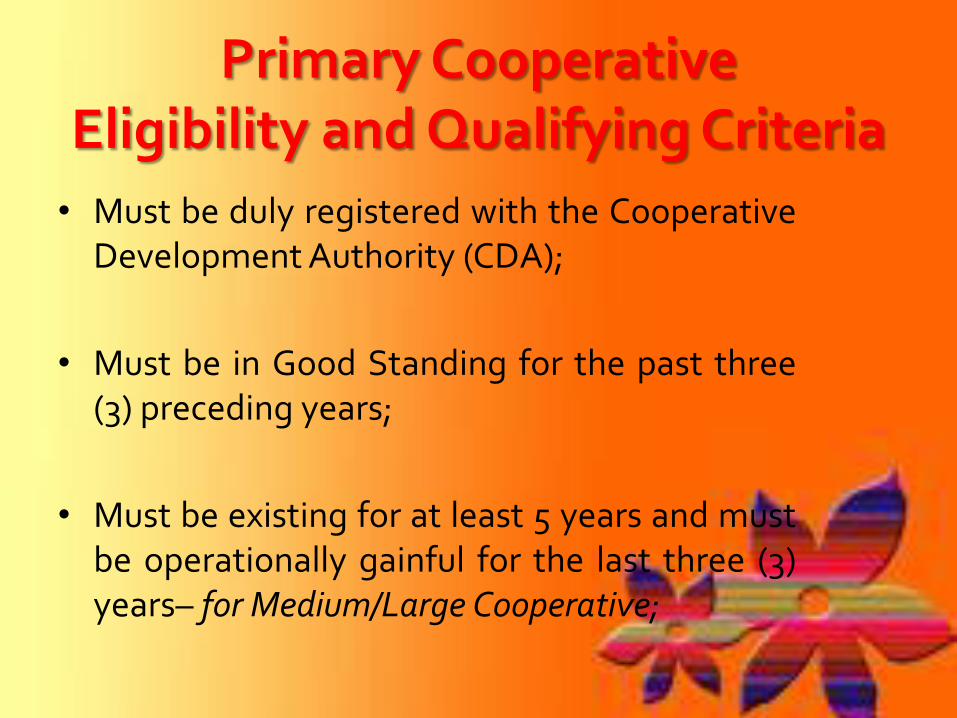

Primary CooperativeEligibility and Qualifying Criteria

• Must be duly registered with the CooperativeDevelopment Authority (CDA);

• Must be in Good Standing for the past three(3) preceding years;

• Must be existing for at least 5 years and mustbe operationally gainful for the last three (3)years– for Medium/Large Cooperative;

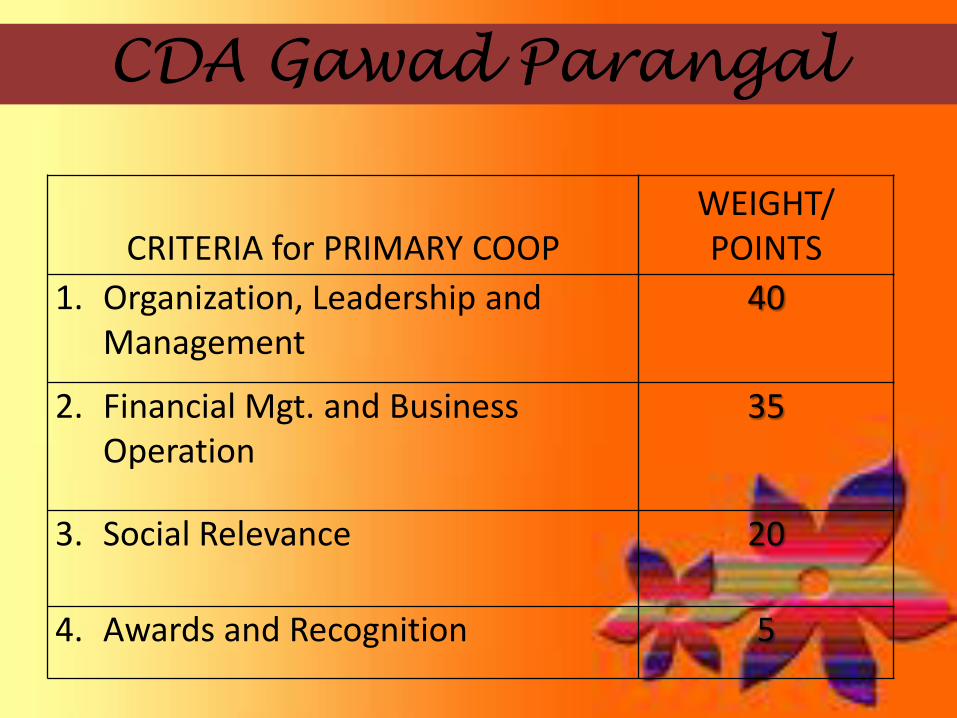

CDA Gawad Parangal

CRITERIA for PRIMARY COOPWEIGHT/ POINTS

1. Organization, Leadership and Management

40

2. Financial Mgt. and Business Operation

35

3. Social Relevance 20

4. Awards and Recognition 5

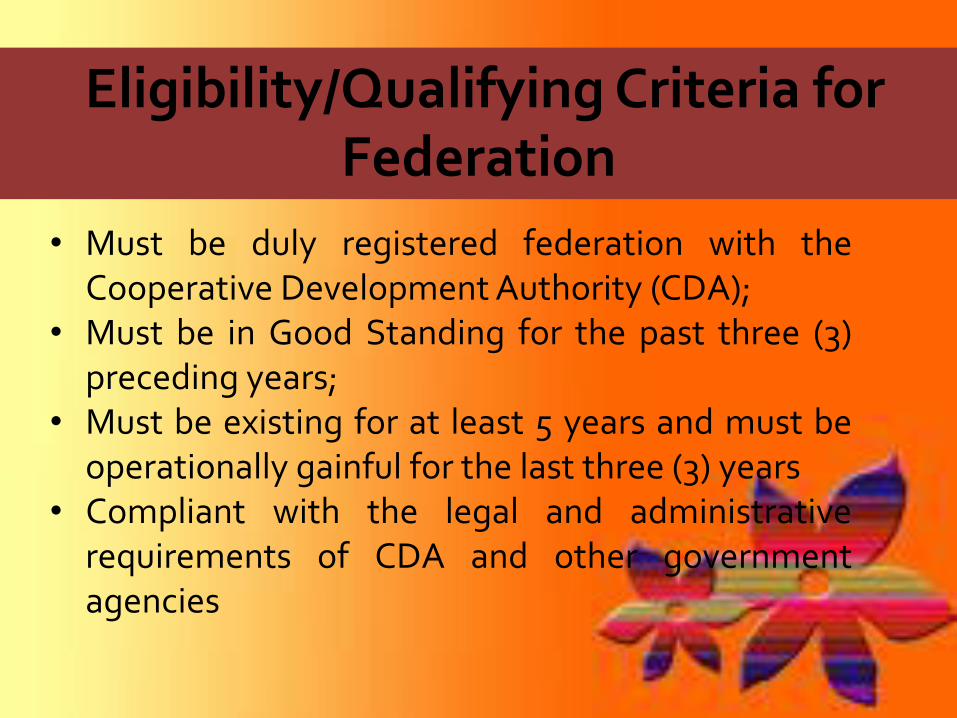

Eligibility/Qualifying Criteria for Federation

• Must be duly registered federation with theCooperative Development Authority (CDA);

• Must be in Good Standing for the past three (3)preceding years;

• Must be existing for at least 5 years and must beoperationally gainful for the last three (3) years

• Compliant with the legal and administrativerequirements of CDA and other governmentagencies

CRITERIA WEIGHT/ POINTS

1.Organization, Leadership and Management

40

2.Financial Mgt. and Business Operation

35

3.Social Relevance 20

4.Awards and Recognition 5

Eligibility/Qualifying Criteria for Union

• Must be duly registered union with the CooperativeDevelopment Authority (CDA);

• Must be in Good Standing for the past three (3)preceding years;

• Must be existing for at least 5 years and must becontinuously operating for the last three (3) years

• Compliant with the legal and administrativerequirements of CDA and other government agencies

CRITERIA WEIGHT

1.Organization, Leadership and Management

40

2.Services Rendered 35

3.Social Relevance 20

4.Awards and Recognition 5

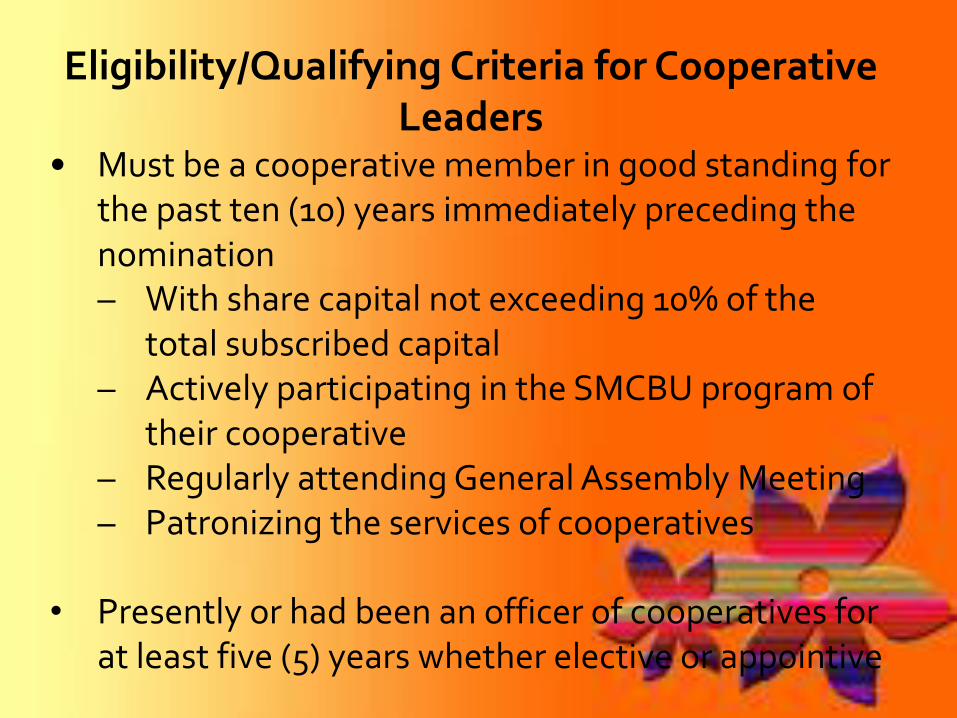

Eligibility/Qualifying Criteria for Cooperative Leaders

• Must be a cooperative member in good standing for the past ten (10) years immediately preceding the nomination – With share capital not exceeding 10% of the

total subscribed capital – Actively participating in the SMCBU program of

their cooperative – Regularly attending General Assembly Meeting – Patronizing the services of cooperatives

• Presently or had been an officer of cooperatives for at least five (5) years whether elective or appointive

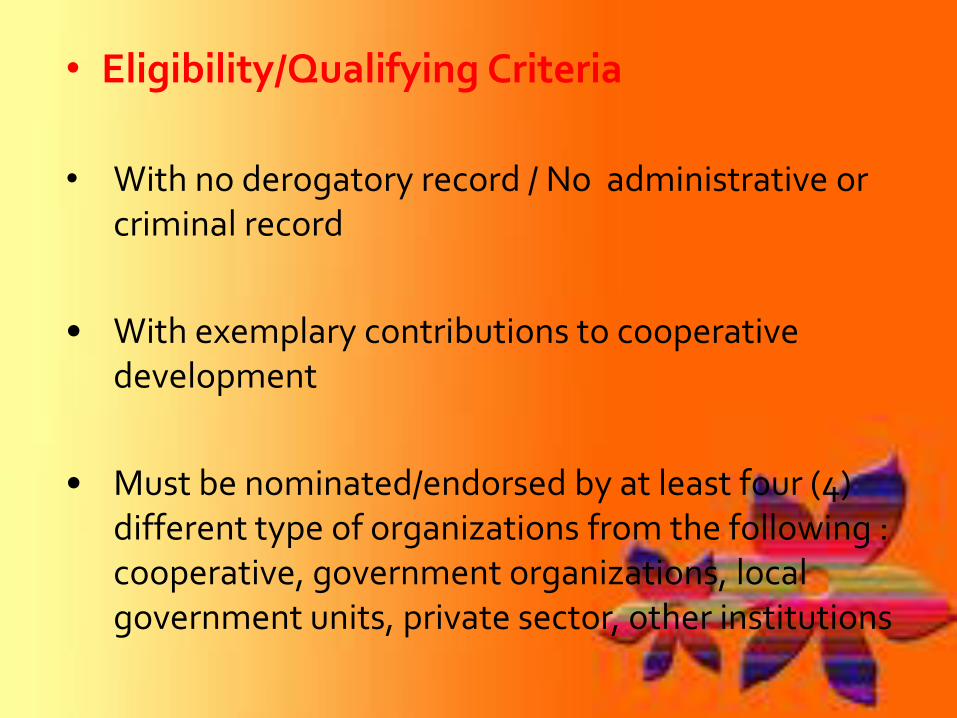

• Eligibility/Qualifying Criteria

• With no derogatory record / No administrative or criminal record

• With exemplary contributions to cooperative development

• Must be nominated/endorsed by at least four (4) different type of organizations from the following : cooperative, government organizations, local government units, private sector, other institutions

Eligibility/Qualifying Criteria CDO-LGU

• Must come from a province/chartered or independentcity or components cities and municipalities

• Formally organized/established/created office

• With Cooperative Development Officer duly appointed

• With staff and budget

• Must have relevant cooperative developmentprogram/s.

• Must be endorsed by CDS and at least one (1)cooperative in the area

CRITERIA WEIGHT/ POINTS

1.Organization, Management & Leadership

40

2. Program Implementation 60

TOTAL 100

The balanced scorecard (BSC) is astrategic performance management tool – a

semi-standard structured report, supported

by proven design methods and automation

tools, that can be used by managers to keep

track of the execution of activities by the

staff within their control and to monitor the

consequences arising from these actions.

8. Balanced Scorecard

It is the most widely adopted performance

management framework reported in the annual

survey of management tools undertaken by Bain

& Company, and has been widely adopted in

English-speaking western countries and

Scandinavia in the early 1990s). Since 2000, use

of the Balanced Scorecard, its derivatives (e.g.,

performance prism), and other similar tools

(e.g., Results Based Management) has alsobecome common in the Middle East, Asia andSpanish-speaking countries.

8. Balanced Scorecard