SHELL COVE BOATHARBOUR OPERATION ENVIRONMENTAL MANAGEMENT PLAN

Royal Dutch Shell November 28-29, 2017

Royal Dutch Shell plcNovember 28-29, 2017

Management DayDelivering a world-class investment case

#makethefuture

Royal Dutch Shell November 28-29, 2017

Ben van BeurdenChief Executive OfficerRoyal Dutch Shell

Bangkok – Thailand

Royal Dutch Shell November 28-29, 2017 3

Definitions & cautionary note

Reserves: Our use of the term “reserves” in this presentation means SEC proved oil and gas reserves. Resources: Our use of the term “resources” in this presentation includes quantities of oil and gas not yet classified as SEC proved oil and gas reserves. Resources are consistent with the Society of Petroleum Engineers (SPE) 2P + 2C definitions.

Operating costs as defined as underlying operating expenses, which are operating expenses less identified items. Organic free cash flow is defined as free cash flow excluding inorganic capital investment and divestment proceeds. Clean CCS ROACE (Return on Average Capital Employed) is defined as defined as the sum of CCS earnings attributable to shareholders excluding identified items for the current and previous three quarters, as a percentage of the average capital employed for the same period. Capital employed consists of total equity, current debt and non-current debt. Capital investment comprises capital expenditure, exploration expense excluding well write-offs, new investments in joint ventures and associates, new finance leases and investments in Integrated Gas, Upstream and Downstream securities, all of which on an accruals basis. In 2016, the capital investment was impacted by the acquisition of BG Group plc. Divestments comprises proceeds from sale of property, plant and equipment and businesses, joint ventures and associates, and other Integrated Gas, Upstream and Downstream investments, reported in “Cash flow from investing activities”, adjusted onto an accruals basis and for any share consideration received or contingent consideration recognised upon divestment, as well as proceeds from the sale of interests in entities while retaining control (for example, proceeds from sale of interest in Shell Midstream Partners, L.P.), which are included in “Change in non-controlling interest” within “Cash flow from financing activities”. This presentation contains the following forward-looking Non-GAAP measures: Organic Free Cash Flow, Free Cash Flow, Capital Investment, CCS Earnings, CCS Earnings less identified items, Gearing, Underlying Operating Expenses, ROACE, Capital Employed and Divestments. We are unable to provide a reconciliation of the above forward-looking Non-GAAP measures to the most comparable GAAP financial measures because certain information needed to reconcile the above Non-GAAP measure to the most comparable GAAP financial measure is dependent on future events some which are outside the control of the company, such as oil and gas prices, interest rates and exchange rates. Moreover, estimating such GAAP measures consistent with the company accounting policies and the required precision necessary to provide a meaningful reconciliation is extremely difficult and could not be accomplished without unreasonable effort. Non-GAAP measures in respect of future periods which cannot be reconciled to the most comparable GAAP financial measure are calculated in a manner which is consistent with the accounting policies applied in Royal Dutch Shell plc’s financial statements. The financial measures provided by strategic themes represent a notional allocation of ROACE, capital employed, capital investment, free cash flow, organic free cash flow and underlying operating expenses of Shell’s strategic themes for the purpose of Management Day presentations. Shell’s segment reporting under IFRS 8 remains Integrated Gas, Upstream, Downstream and Corporate.

The companies in which Royal Dutch Shell plc directly and indirectly owns investments are separate legal entities. In this presentation “Shell”, “Shell group” and “Royal Dutch Shell” are sometimes used for convenience where references are made to Royal Dutch Shell plc and its subsidiaries in general. Likewise, the words “we”, “us” and “our” are also used to refer to subsidiaries in general or to those who work for them. These expressions are also used where no useful purpose is served by identifying the particular company or companies. ‘‘Subsidiaries’’, “Shell subsidiaries” and “Shell companies” as used in this presentation refer to companies over which Royal Dutch Shell plc either directly or indirectly has control. Entities and unincorporated arrangements over which Shell has joint control are generally referred to “joint ventures” and “joint operations” respectively. Entities over which Shell has significant influence but neither control nor joint control are referred to as “associates”. The term “Shell interest” is used for convenience to indicate the direct and/or indirect ownership interest held by Shell in a venture, partnership or company, after exclusion of all third-party interest.

This presentation contains forward-looking statements concerning the financial condition, results of operations and businesses of Royal Dutch Shell. All statements other than statements of historical fact are, or may be deemed to be, forward-looking statements. Forward-looking statements are statements of future expectations that are based on management’s current expectations and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in these statements. Forward-looking statements include, among other things, statements concerning the potential exposure of Royal Dutch Shell to market risks and statements expressing management’s expectations, beliefs, estimates, forecasts, projections and assumptions. These forward-looking statements are identified by their use of terms and phrases such as ‘‘anticipate’’, ‘‘believe’’, ‘‘could’’, ‘‘estimate’’, ‘‘expect’’, ‘‘goals’’, ‘‘intend’’, ‘‘may’’, ‘‘objectives’’, ‘‘outlook’’, ‘‘plan’’, ‘‘probably’’, ‘‘project’’, ‘‘risks’’, “schedule”, ‘‘seek’’, ‘‘should’’, ‘‘target’’, ‘‘will’’ and similar terms and phrases. There are a number of factors that could affect the future operations of Royal Dutch Shell and could cause those results to differ materially from those expressed in the forward-looking statements included in this presentation, including (without limitation): (a) price fluctuations in crude oil and natural gas; (b) changes in demand for Shell’s products; (c) currency fluctuations; (d) drilling and production results; (e) reserves estimates; (f) loss of market share and industry competition; (g) environmental and physical risks; (h) risks associated with the identification of suitable potential acquisition properties and targets, and successful negotiation and completion of such transactions; (i) the risk of doing business in developing countries and countries subject to international sanctions; (j) legislative, fiscal and regulatory developments including regulatory measures addressing climate change; (k) economic and financial market conditions in various countries and regions; (l) political risks, including the risks of expropriation and renegotiation of the terms of contracts with governmental entities, delays or advancements in the approval of projects and delays in the reimbursement for shared costs; and (m) changes in trading conditions. No assurance is provided that future dividend payments will match or exceed previous dividend payments. All forward-looking statements contained in this presentation are expressly qualified in their entirety by the cautionary statements contained or referred to in this section. Readers should not place undue reliance on forward-looking statements. Additional risk factors that may affect future results are contained in Royal Dutch Shell’s 20-F for the year ended December 31, 2016 (available at www.shell.com/investor and www.sec.gov ). These risk factors also expressly qualify all forward looking statements contained in this presentation and should be considered by the reader. Each forward-looking statement speaks only as of the dates of this presentation, November 28-29, 2017. Neither Royal Dutch Shell plc nor any of its subsidiaries undertake any obligation to publicly update or revise any forward-looking statement as a result of new information, future events or other information. In light of these risks, results could differ materially from those stated, implied or inferred from the forward-looking statements contained in this presentation. This presentation may contain references to Shell’s website. These references are for the readers’ convenience only. Shell is not incorporating by reference any information posted on www.shell.com. We may have used certain terms, such as resources, in this presentation that United States Securities and Exchange Commission (SEC) strictly prohibits us from including in our filings with the SEC. U.S. Investors are urged to consider closely the disclosure in our Form 20-F, File No 1-32575, available on the SEC website www.sec.gov.

Royal Dutch Shell November 28-29, 2017 4

Agenda PLENARY I Ben van Beurden – company update

Jessica Uhl – financial framework

Maarten Wetselaar – Integrated Gas

Andy Brown – Upstream

John Abbott – Downstream

Maarten Wetselaar – New Energies

Upstream

Andy Brown – Upstream Director

Shell’s carbon footprint ambition

Harry Brekelmans – Projects & Technology Director

Downstream

John Abbott – Downstream Director

Integrated Gas & New Energies

Maarten Wetselaar – Integrated Gas & New Energies Director

PLENARY II

Q&A

BREAK-OUT PANELS

Royal Dutch Shell November 28-29, 2017 5

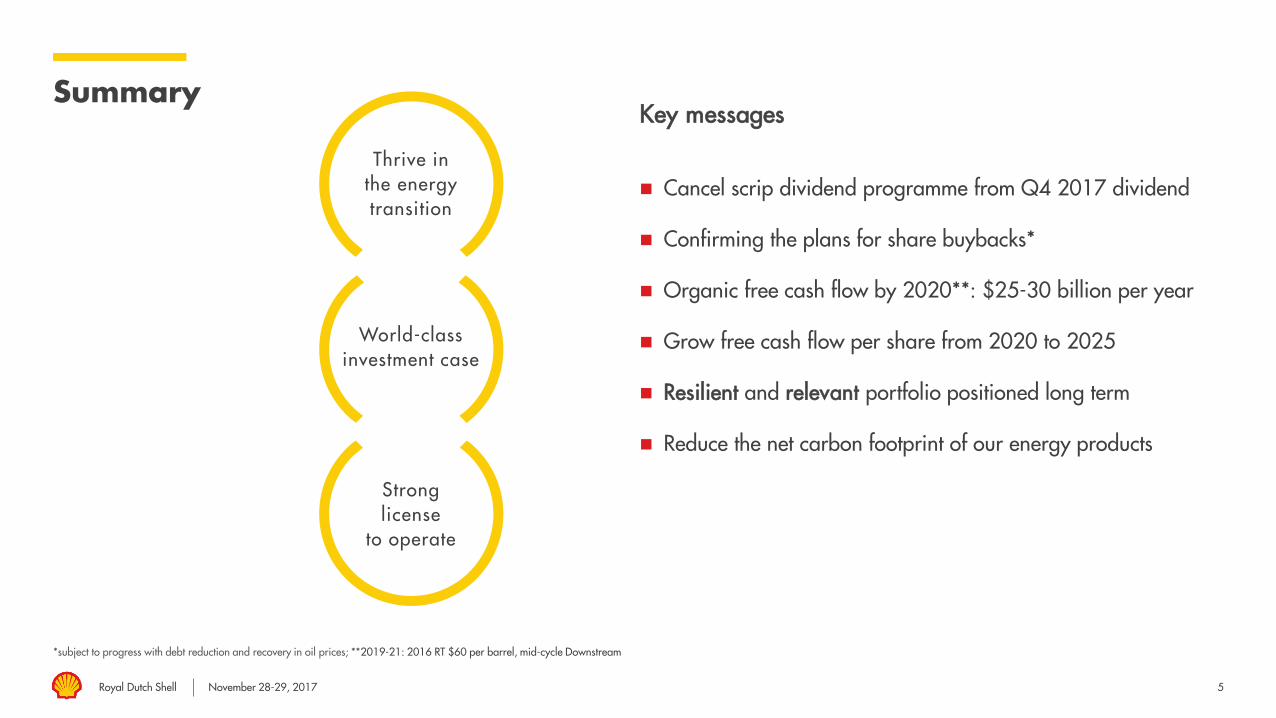

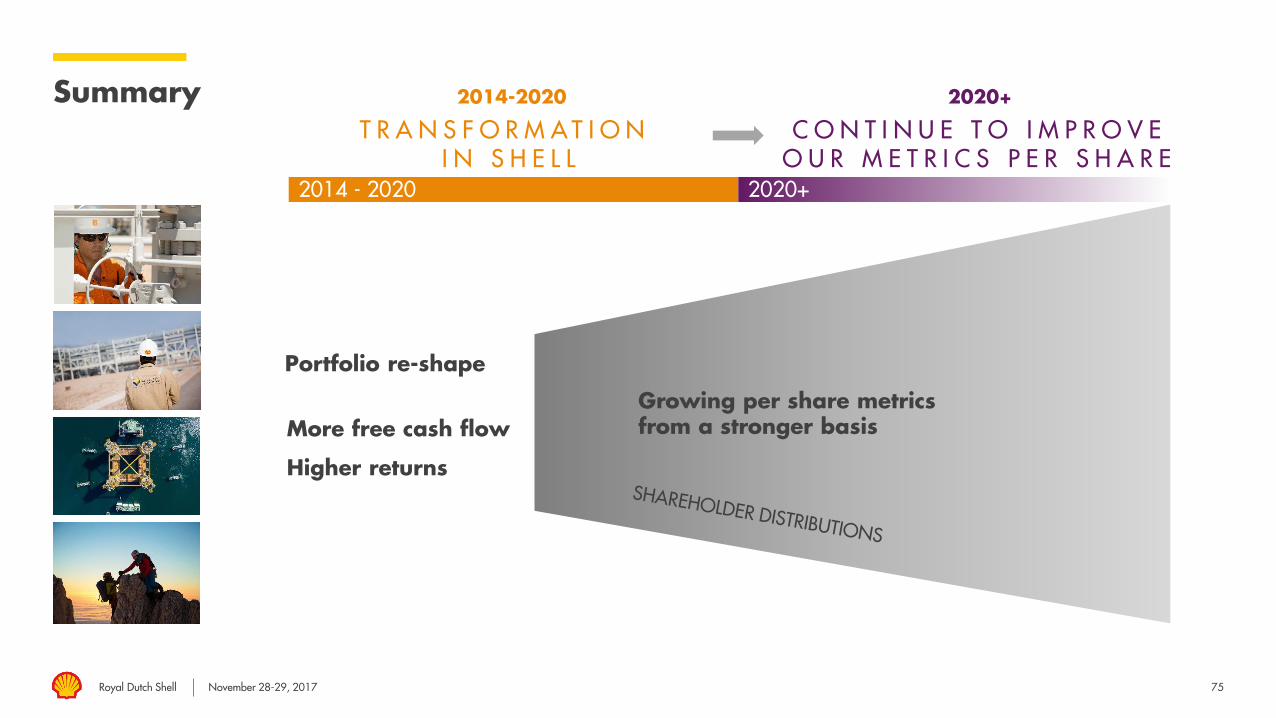

Summary

*subject to progress with debt reduction and recovery in oil prices; **2019-21: 2016 RT $60 per barrel, mid-cycle Downstream

Key messages

Cancel scrip dividend programme from Q4 2017 dividend

Confirming the plans for share buybacks*

Organic free cash flow by 2020**: $25-30 billion per year

Grow free cash flow per share from 2020 to 2025

Resilient and relevant portfolio positioned long term

Reduce the net carbon footprint of our energy products

Thrive in the energy transition

World-class investment case

Strong license

to operate

Royal Dutch Shell November 28-29, 2017 6

Significant changes delivered since early ‘16

*4-quarters rolling Q3 2017; ROACE on CCS basis, excluding identified items; Shell share at peak production. Divestments: headline

BG AcquisitionCompleted and fully integrated

~$27 billion

Free cash flow* at $51 per barrel

13,000Fewer staff

11Major project start-ups

and >500kboe/d avg. production increase from start-ups

~$23 billion

Divestments completed

~$9 billionFree cash flow* and

~17% ROACE in

Downstream

Royal Dutch Shell November 28-29, 2017 7

World-class investment case

Transformation

ROACE on CCS basis, excluding identified items; *subject to progress with debt reduction and recovery in oil prices **2019-21: 2016 RT $60 per barrel, mid-cycle Downstream

Strategy is working

Implementation is on-track

2013-15average

17Q34Q rolling

2019-21average

ROACE 8% 4.6% ~10%

Organic free cash flow $5 billion p.a. ~$17 billion $25-30 billion p.a.

Gearing 14% 25.4% <20% end ’20

Buybacks $8.7 billioncumulative ‘13-’15 - at least $25 billion*

in period 2017-2020

Brent ~$90 ~$51 ~$60**

Portfolio re-shape

Clarity of purpose

Differentiated strategy

Royal Dutch Shell November 28-29, 2017 8

World-class investment case

Transformation: ways of working

Reduction in invoice value

# of FTE (thousands)

Culture change Performance unit management

Credible, competitive and affordable Accountable leadership

‘Fit for the future’

Digitalisation – benefiting cost and availability

Shell employee survey results confirm change

FTE reductions

Category spend reductions

Shell

BG

Competitive scoping - Vito

20162017E

Index base year 2014

RigsWells Installed Equipment Engineering services

Professional services

Maintenance services

Logistics

IT

-60% -50% -40% -30% -20% -10%-70%

2015

Royal Dutch Shell November 28-29, 2017

$ billion 2017E 2018-20 expectation

Operating costs <38 (underlying)

Further reductionpotential

Capital investment 25 25 – 30

Divestments 30 over 2016 – 2018

>5 p.a.2019 – 2020

Projects start-up post-2014(CFFO)

~52017

~10incremental* over

2018 – 2020

9

Four powerful levers

*2016 RT $60 per barrel, mid-cycle Downstream

Relentless portfolio high-grading

Royal Dutch Shell November 28-29, 2017 10

HSSEperformance Injuries – TRCF/million working hours

Goal zero on safety

Million tonnes CO2e

Upstream flaring

Volume in thousand tonnes

Spills – operational

Number of incidents

Process safety

HSSE priority

Performance + transparency

million working hours

Working hours (RHS)TRCF

Number of spills

Volume Spills (RHS)

Tier 1 incidents Tier 2 incidents

Royal Dutch Shell November 28-29, 2017

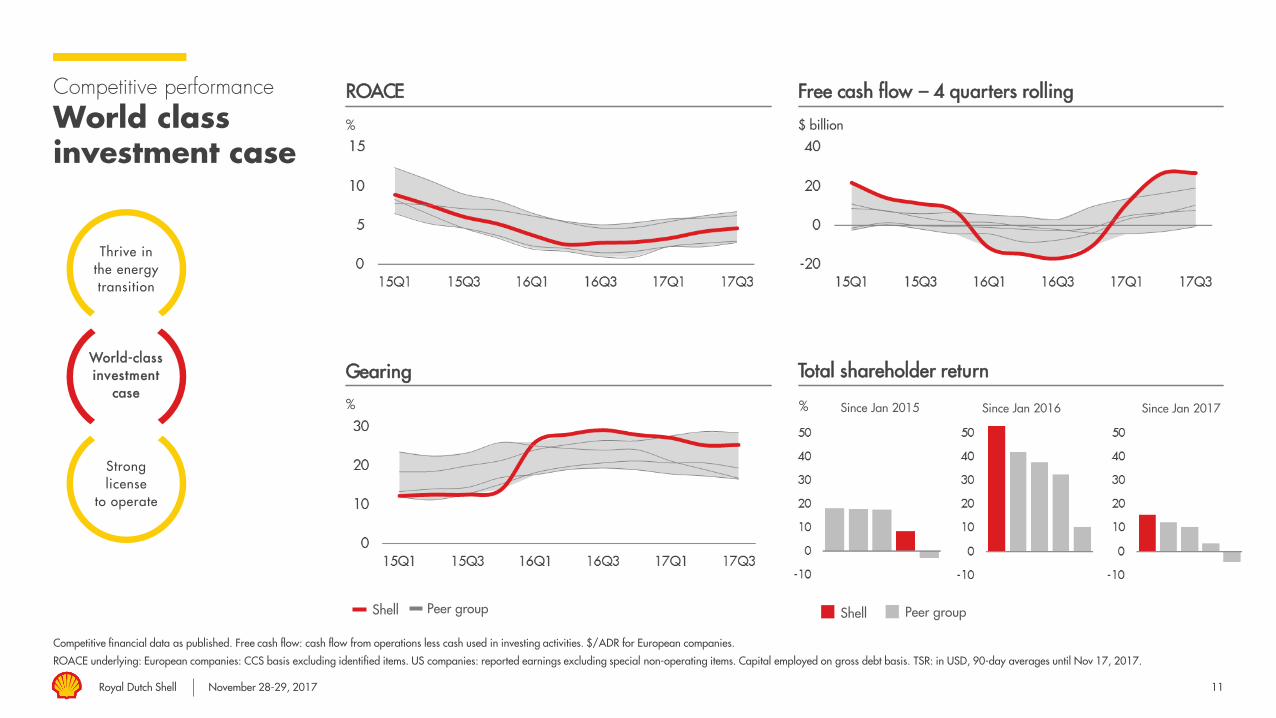

Competitive performance

World class investment case

Competitive financial data as published. Free cash flow: cash flow from operations less cash used in investing activities. $/ADR for European companies.

ROACE underlying: European companies: CCS basis excluding identified items. US companies: reported earnings excluding special non-operating items. Capital employed on gross debt basis. TSR: in USD, 90-day averages until Nov 17, 2017.

%

ROACE

%

Gearing

$ billion

Free cash flow – 4 quarters rolling

Total shareholder return

Shell Peer group

11

% Since Jan 2015 Since Jan 2016 Since Jan 2017

Shell Peer group

Thrive in the energy transition

World-class investment

case

Strong license

to operate

Royal Dutch Shell November 28-29, 2017

Emerging opportunities

12

Investment priorities & strategic intent

Cash engines

Growth priorities

Funds dividends and balance sheet Competitive and resilient Strong free cash and returns

Material future value Strategic balance Managed exposure while establishing scale

Emerging cash engines Affordable growth in advantaged positions FCF and ROACE pathway

Today by 2020

(FCF >0)

(FCF ~0)

(FCF <0)

OIL PRODUCTS

CONVENTIONAL OIL + GAS

INTEGRATEDGAS

DEEP WATERCHEMICALS

SHALESNEW ENERGIES

Royal Dutch Shell November 28-29, 2017

Capital discipline, supporting growth

ROACE on CCS basis, excluding identified items

Capital investment

$ billion

Capital investment

$ billion

Capital employed

More predictable Economic resilience of

projectsCash engines

Growth priorities

Emerging opportunities

ROACE (RHS)

%

Non- and little discretionary spend

Small scale and large value growth options

$ billion (p.a.) 2018 – 2020

Oil products 4-5

Conventional oil + gas 4-5

Integrated gas 4-5

Deep water 5-6

Chemicals 3-4

Shales 2-3

New energies 1-2

Total 25-30

Capital investment p.a. 2018-’20

13

Royal Dutch Shell November 28-29, 2017 14

2016 – 2019+

Delivering cash flow growth

Shell share at peak production

2016+ start-ups: >500kboe/d ; 9.5 mtpa LNG

Geismar AO4 (2018)

Schiehallion redevelopment (2017)Clair Ph2 (2018)

Coulomb (2018)

Fox Creek (2016-19+)

Permian (2016-19+)

Appomattox (2019+)

Kaikias Ph 1 (2019+)

Pennsylvania Chemicals (2019+)

Stones (2016)

Scotford HCU debottleneck (2016)

Brazil Deepwater(2016-19+)

Gorgon T3 (2017)

ML South start-up (2016)Baronia / Tukau Timur (2018)

Prelude FLNG (2018)

Nanhai China Chemicals (2019+)

Kashagan (2016)

Malikai (2016)

Pernis – Solvent deasphalting(2018)

Tempa Rossa(2018)

Rahab HarweelIntegrated Project (2019+)

Gbaran Ubie Ph2 (2017)Forcados Yokri Integrated Projects (FYIP) (2018)Southern Swamp AG (2019+)

Mexico retail entry (2017)

Royal Dutch Shell November 28-29, 2017

Price sensitivity:

+/- $10 Brent =

+/- ~$6 billion CFFO

Capital employed

($ bln)

Free cash flow*

($ bln p.a)

ROACE

(%)

~70% 25-30 >10

~20% 1-2 ~5

~5% (2) - (1) ~5

25-30

>5

~290 30-35 ~10

15

Financial performance:On-track

*2019-21: 2016 RT $60 per barrel, mid-cycle Downstream. **Includes Deep water in cash engines and Shales in growth priorities by 2020

2019-21 ~$6017Q3 – 4Q rolling ~$512019-21 ~$60June 2016 CMD

Cash engines

Growth priorities

Emerging opportunities

Organic FCF

Divestments & acquisitions

Total (incl. Corporate)

Capital employed

($ bln end ’17Q3)

Free cash flow($ bln p.a)

ROACE

(%)

~60% ~15 ~8

~25% ~1 ~3

~5% ~-1 ~-4

~17

~10

287 ~27 ~5

Free cash flow*

($ bln p.a)

ROACE

(%)

15-20 ~10

~5 ~10

~0 <5

20-25

~5

20-30 ~10

Previous Update**

Royal Dutch Shell November 28-29, 2017 16

Thrive in the energy transition

Societal challenge

Sources: Population – UN World Population projections; Energy consumption: 2015 – IEA World Energy Outlook (“WEO”) 2017; 2070 outlook – Shell scenarios analysis from A Better Life with a Healthy Planet

CO2 emissions: 2015 – IEA WEO 2017; 2040 – IEA WEO 2017 Current policies scenario; 2070 – Shell scenarios analysis from A better life with a healthy planet.

Challenge for more and cleaner energy

Reduction required in the carbon intensity of every unit of energy consumed

2 0 1 5 2 0 7 0

>10 billion7 billion

1000 Exajoules570 Exajoules

Net ZeroEmissions

32 gt CO2e CO2

43 gt CO2e current policies

2 0 4 0

Increasing population

Increasing energy demand

Need to reduce CO2 emissions

Royal Dutch Shell November 28-29, 2017 17

Thrive in the energy transition

Driving to resilience

Driving to resilience:

Short-term operational targets

GHG metrics 10% of annual bonus scorecard

(Scope 1 and 2)

Emissions management focussed on areas

we can take operational action

2018: cover ~90% of the operated portfolio

(was 60% in 2017)

Transparency on resilience + flexibility of our portfolio

Supporting Task Force on Climate-related

Financial Disclosure (TCFD)

Preparing first TCFD-style disclosure by Q1 2018

Annual bonus scorecard

Short-term operational focus

Medium-term demonstration of resilience

5% Process safety

5% Personal safety

10% GHG management

Transparency

Royal Dutch Shell November 28-29, 2017 18

Thrive in the energy transition

Ambition – Net Carbon Footprint

1: Net Carbon Footprint measured on an aggregate “well to wheel” or “well to wire” basis, from production through to consumption, on grams of CO2 equivalent per megajoule of energy products consumed; chemicals + lubricants products are excluded. Carbon

Footprint of the energy system is modelled using Shell methodology aggregating lifecycle emissions of energy products on a fossil-equivalence basis. The methodology will be further reviewed and validated in collaboration with external experts.

2: Potential society trajectory includes analysis from Shell scenarios estimate of Net Zero Emissions by 2070 and IEA Energy Technology Perspectives 2017; Potential illustrative Shell trajectory

WtW gCO2e/MJ1

Ambition to reduce Net Carbon Footprint1 of our energy products by around 20% by 2035

Covers full range of emissions from energy products

Emissions in the supply chain (Scope 1 + 2; ~15%)

Emissions from consumption of our energy products (Scope 3; ~85%)

Aim to reduce overall intensity including production, supply chain, and customers

Government policy, technology, and consumer choice will drive actual energy transition pace and outcomes

Drive strategy over time in step with society

5-year reviews to ensure in line with societal progress

Flexibility and mix of options to achieve ambition

Allows for oil and gas production growth offset by evolving product mix

Ambition for Net Carbon Footprint1

WtW gCO2e/MJ1

Potential tools to achieve our 2035 ambition

Ambitions: Reduce Net Carbon

Footprint1 of our energy products by ~20% by 2035

Be in line with society Net Carbon Footprint by 2050

Society trajectory2 Shell trajectory2

2 0 3 5 A M B I T I O N

Shell “business as usual”

~20% reduction by 2035

In line with society by 2050

(Scope 1+2)

Royal Dutch Shell November 28-29, 2017 19

Summary

*subject to progress with debt reduction and recovery in oil prices; **2019-21: 2016 RT $60 per barrel, mid-cycle Downstream

Key messages

Cancel scrip dividend programme from Q4 2017 dividend

Confirming the plans for share buybacks*

Organic free cash flow by 2020**: $25-30 billion per year

Grow free cash flow per share from 2020 to 2025

Resilient and relevant portfolio positioned long term

Reduce the net carbon footprint of our energy products

Thrive in the energy transition

World-class investment case

Strong license

to operate

Royal Dutch Shell November 28-29, 2017

Jessica UhlChief Financial OfficerRoyal Dutch Shell

Royal Dutch Shell November 28-29, 2017 21

Financial framework

Foundation of the world-class investment case

Key features

Maximising value for shareholders through cycle

Multi-year timescales

Surplus free cash flow in up-cycle and dividends fully covered

in down-cycle

Gearing 0-30%; AA credit metrics

Thrive in the energy transition

World-class investment case

Strong license

to operate

Conservative financial management

FCF/share & ROACE growth Focus on shareholder

distributions

Royal Dutch Shell November 28-29, 2017 22

Financial framework

BG acquisition and shareholder distributions

BG post-offer intention statements

at the time of the acquisition

Pay at least dividends of $1.88 per

Shell share for 2016

Subject to progress with debt reduction

and recovery in oil prices:

Withdraw the scrip dividend

programme in 2017

Share buyback programme of at least

$25 billion over the period 2017-2020

Growing shareholder distributions

Delivering on the BG post-offer intention statements

Capital investment

$25-30 billion

Dividend

Interest

Debt reduction

to 20% gearing

Buybacks

Divestment

proceeds

CFFO

Surplus

CFFO

Royal Dutch Shell November 28-29, 2017 23

Free cash flow performance and payout

* 2016 RT $60 per barrel, mid-cycle Downstream

2014 cash dividend includes $3.3bln share buy backs, more than offsetting scrip issuance of $2.4bln.

$ billion

Distributions from free cash flow

Financial transformation 2014-2017

2019-2021 average:FCF $30-35 billion

Organic FCF

Divestment proceeds less acquisitions

Cash dividend

Scrip dividend Interest paid

$99/bbl $51/bbl $60/bbl*

2014 17Q34Q rolling

2019-2021average

Royal Dutch Shell November 28-29, 2017 24

Achieving divestment and debt reduction objectives

Integrated Gas split out from Upstream from 2011 onwards

* Includes Gabon, UK North Sea and Woodside divestments

$ billion

Divestment proceeds

$ billion

Net debt & gearing

Visibility on lower gearing through progress on divestments

%

Downstream/CorporateUpstreamIntegrated Gas

Announced and well-advanced deals

Net debt

Gearing (RHS)

Gearing with impact of divestments completed since Q3 2017 included (RHS)*

Royal Dutch Shell November 28-29, 2017 25

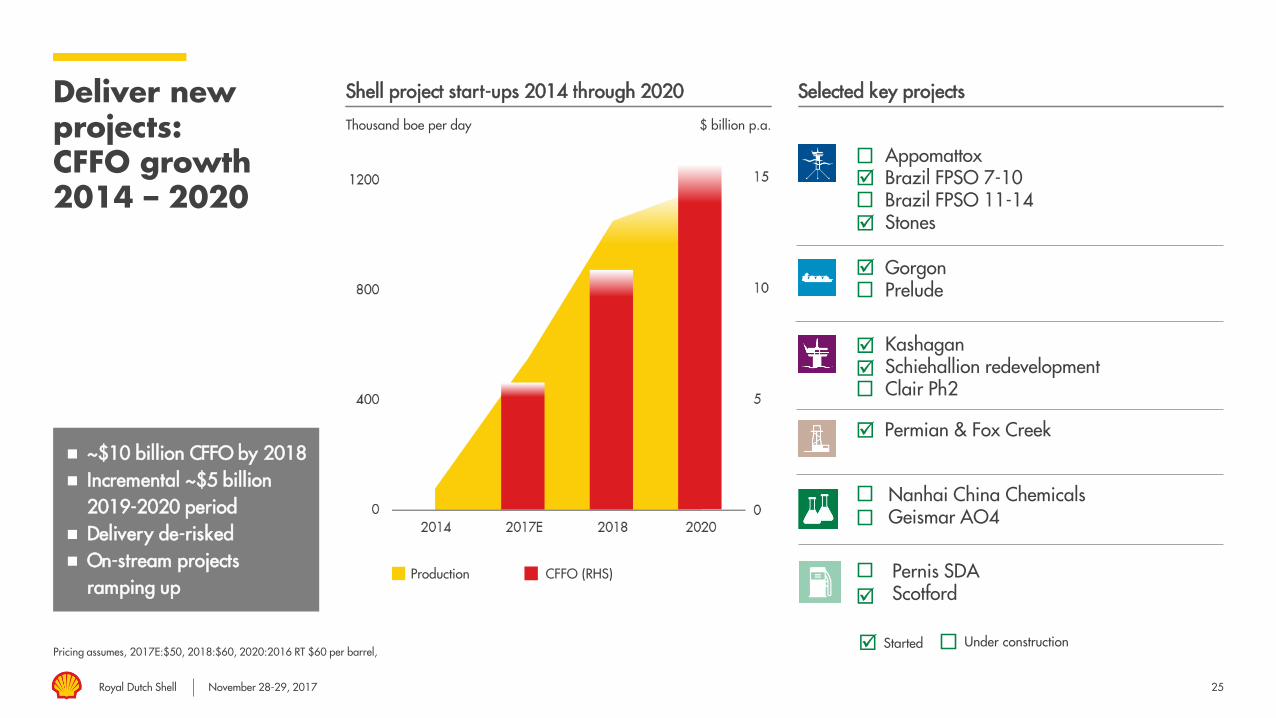

Deliver new projects:CFFO growth 2014 – 2020

Pricing assumes, 2017E:$50, 2018:$60, 2020:2016 RT $60 per barrel,

Thousand boe per day

Shell project start-ups 2014 through 2020 Selected key projects

~$10 billion CFFO by 2018 Incremental ~$5 billion

2019-2020 period Delivery de-risked On-stream projects

ramping up

$ billion p.a.

Production CFFO (RHS)

AppomattoxBrazil FPSO 7-10Brazil FPSO 11-14Stones

Permian & Fox Creek

GorgonPrelude

KashaganSchiehallion redevelopmentClair Ph2

Nanhai China ChemicalsGeismar AO4

Pernis SDAScotford

Started Under construction

Royal Dutch Shell November 28-29, 2017 26

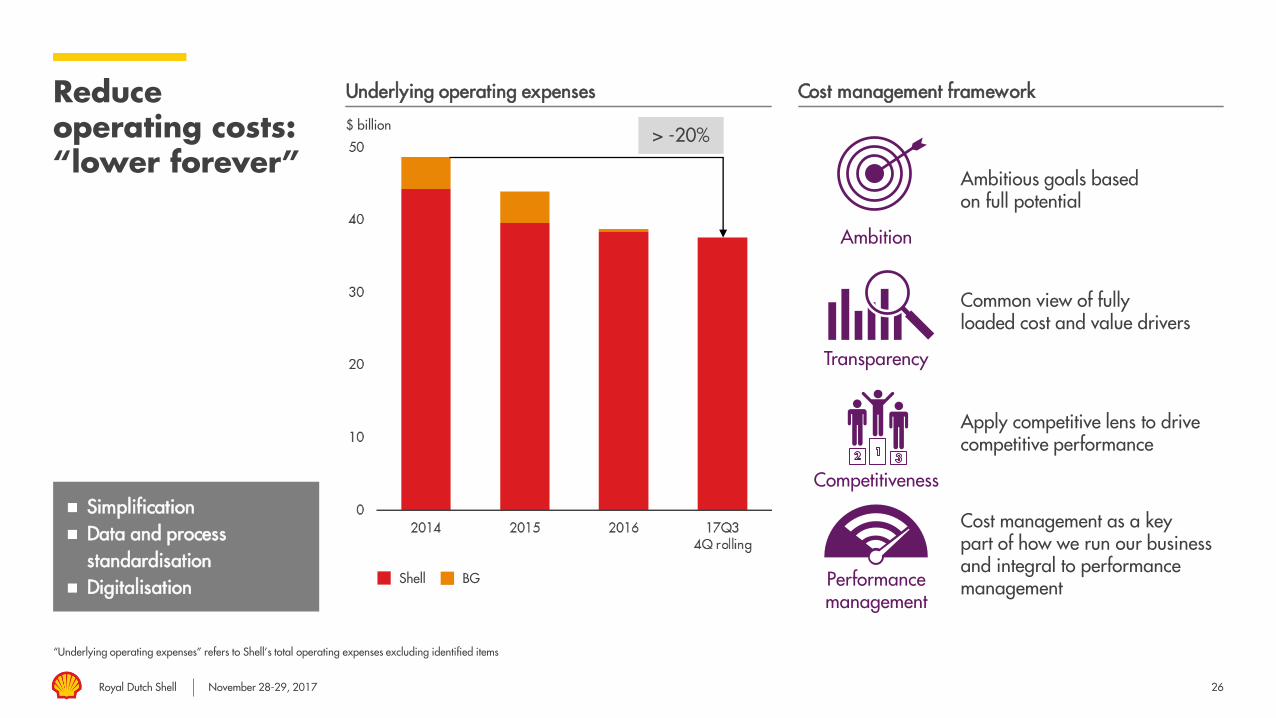

Reduce operating costs: “lower forever”

“Underlying operating expenses” refers to Shell’s total operating expenses excluding identified items

$ billion

Underlying operating expenses Cost management framework

Simplification Data and process

standardisation Digitalisation

> -20%

Shell BG

Cost management as a key part of how we run our business and integral to performance management

Apply competitive lens to drive competitive performance

Common view of fully loaded cost and value drivers

Ambitious goals based on full potential

Performance management

Competitiveness

Transparency

Ambition

Royal Dutch Shell November 28-29, 2017 27

Higher capital efficiency and more consistent capital investment

Capital investment excludes BG acquisition in 2016.

$ billion

Capital investment

Capital discipline Resilient projects Flexibility

Shell BG

$25-30 billion

> -40%

Increased capital efficiency

Resilient projects

$30 billion per year ceiling

Options to reduce capital investment below $25 billion if warranted

Sustain current cash flow at a capital investment level of $17- 20 billion

Royal Dutch Shell November 28-29, 2017 28

World-class investment case

Cash flow priorities

Priorities for cash Debt reduction Dividends

Buybacks & capital

investment

1 2 3

Continue to reduce gearing to 20%

Cancel scrip dividend Buy back shares

Progress towards a world-class investment case Increase shareholder distributions

Royal Dutch Shell November 28-29, 2017

Maarten WetselaarIntegrated Gas & New Energies DirectorRoyal Dutch Shell

Royal Dutch Shell November 28-29, 2017

Cash engine

As of Q3 2017; capital employed includes new energies; average capital investment per annum in period 2018-20

Creating & securing demand Optimisation Managing supply

Capital employed: $90 billion

Production: 1.0 mboe/d

Liquefaction volume:34 mtpa

LNG sales volumes: 64 mtpa

Capital investment: $4-5 billion

30

LNG

Gas and power

Gas-to-liquids premium products

Marketing and trading

Shipping and transport

Regasification

Gas and liquids production

Liquefaction

Gas-to-liquids

Integrated Gas

World leader Growing markets Differentiated portfolio Cash delivery

Royal Dutch Shell November 28-29, 2017

Capital employed

$ per barrel

31

Integrated Gas

Financial performance

Earnings and ROACE on CCS basis, excluding identified items. Capital employed under construction: assets under construction plus exploration and evaluation assets.

$ billion

Cash flow from operations

Earnings and ROACE

$90 billion as of Q3 2017

$ billion

LNG liquefaction and sales volumes

Resilience Cash delivery and growth $8 – 10 billion organic FCF

by 2020 ~10% ROACE by 2020

CFFO excl. working capital Brent (RHS)

Earnings ROACE (RHS)

%

Liquefaction volumes Sales volumes

In service Under construction

$62 billion as of Q3 2015

Million tonnes

Royal Dutch Shell November 28-29, 2017 32

Integrated Gas

Gas-to-liquidsvalue chain

Pearl - the world’s largest gas-to-liquids plant

Marketing integration

Integrated value chain Differentiated products Premium vs Brent

Continuous innovation

Record-breaking offshore performance

Jane.Adam: replace with

piucture of Helix Ultra only

North Field Pearl GTL Plant

Royal Dutch Shell November 28-29, 2017 33

Integrated Gas

Policy and economics driving gas growth

OECD - Electricity output by source

bcm

Beijing gas demand

Structural shift to gas Cleaner and affordable

energy solution

Source: Embassy of the USA – Beijing, China; National Bureau of Statistics of China, Beijing Gas Group Co. Ltd.

Action plan for air

pollution prevention

Enhanced plan for tackling air

pollution

Fine particulate matterPM 2.5

Beijing Area Gas Demand (BCM)

Source: IEA World Energy Statistics

UK carbon floor price

US shale growth

Rapid increase in renewables generation

PM 2.5

Natural Gas Coal

Nuclear Hydro

Renewables (excl. Hydro) Biofuels/Waste, etc.Oil

Decree on coal-to-gas switch in

non-power sector

%

Royal Dutch Shell November 28-29, 2017 34

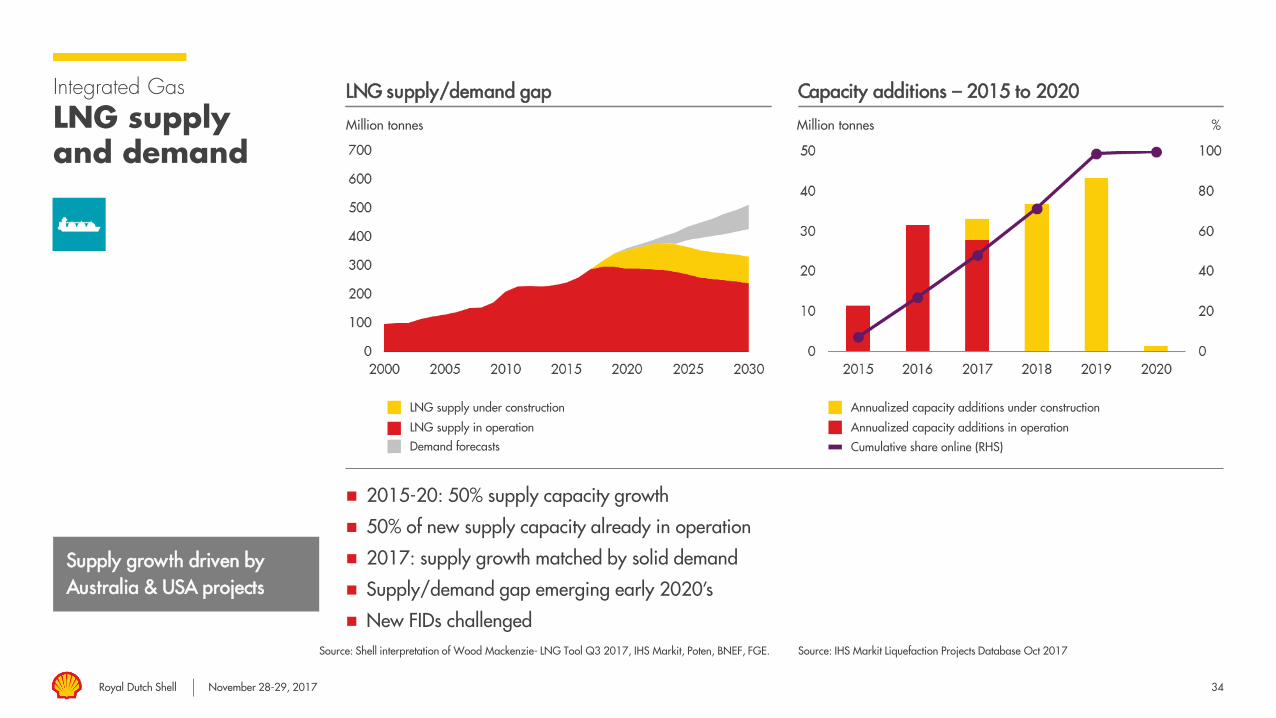

Integrated Gas

LNG supplyand demand

Source: Shell interpretation of Wood Mackenzie- LNG Tool Q3 2017, IHS Markit, Poten, BNEF, FGE.

Million tonnes

2015-20: 50% supply capacity growth

50% of new supply capacity already in operation

2017: supply growth matched by solid demand

Supply/demand gap emerging early 2020’s

New FIDs challenged

LNG supply/demand gap Capacity additions – 2015 to 2020

Supply growth driven by Australia & USA projects

LNG supply in operation

Demand forecasts

LNG supply under construction Annualized capacity additions under construction

Annualized capacity additions in operation

Cumulative share online (RHS)

Source: IHS Markit Liquefaction Projects Database Oct 2017

Million tonnes %

Royal Dutch Shell November 28-29, 2017

Integrated Gas

LNG – Global integrated value chain

Largest LNG marketer

Largest supplier to China & JKT

Leader in LNG for transport

Gas advocacy

Deliveries to 25+ countries

2 LNG cargoes loaded every day

Regas capacity in 10 terminals

90 LNG carriers

Production: 1 million boe/d

13 LNG plants – all supply basins

LNG supply from 17 countries

C R E AT I N G A N D S E C U R I N G D E M A N D O P T I M I S AT I O N M A N A G I N G

S U P P L Y

Leverage portfolio flexibility and

arbitrage opportunities

Market-driven value chain

35

JKT: Japan, Korea, Taiwan

Royal Dutch Shell November 28-29, 2017 36

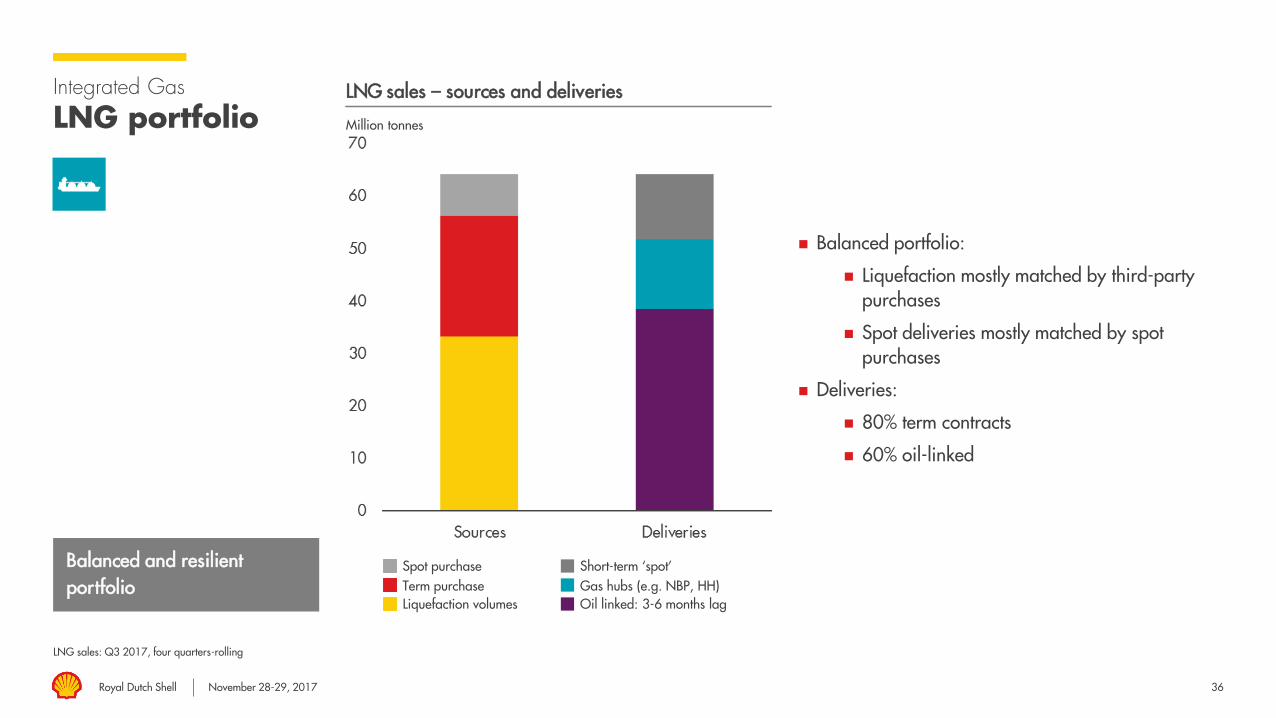

Integrated Gas

LNG portfolio

LNG sales: Q3 2017, four quarters-rolling

Million tonnes

Balanced portfolio:

Liquefaction mostly matched by third-party purchases

Spot deliveries mostly matched by spot purchases

Deliveries:

80% term contracts

60% oil-linked

LNG sales – sources and deliveries

Short-term ‘spot’Gas hubs (e.g. NBP, HH)Oil linked: 3-6 months lag

Term purchaseLiquefaction volumes

Spot purchaseBalanced and resilient portfolio

Royal Dutch Shell November 28-29, 2017 37

Integrated Gas

Create and secure demand

2017 - Shell and JV marketed volumes

% total sales – geographic split

LNG customers Market-specific strategies

Globally balanced and diversified customers portfolio

Gasnor

Dragon RotterdamEurope

BarcelonaAttiki

Qatar

Brazil

Altamira`

Costa Azul

Cove Point

Lake Charles

Canada

USAChina

Hangzhou

Singapore

Australia

Indonesia

India

HaziraMahanagar Gas`

LNG Import terminals (incl. capacity rights)

Natural Gas Distribution

D-LNG Fuel Markets

D-LNG Fuel Target Markets

Gas and power marketing and trading

LNG Markets

Evolving business model in mature markets

Securing positions in priority growth markets

Trading portfolio optimization

Grow Downstream-LNG fuel markets

Gas advocacy

Elba

Royal Dutch Shell November 28-29, 2017 38

Integrated Gas

World-class LNG supply portfolio

Source: Shell Financial Statement, IHS Markit for 3rd parties’ capacity – October 2017 - Total excl. recently announced Engie acquisition

Million tonnes per annum

Liquefaction capacity by independent company Leading portfolio

13 liquefaction plants

41 million tonnes per annum capacity

95% reliability

Utilisation upside – feedgas availability

Focus on unit cost reduction All supply basins Operational excellence

In operation Under construction

Brunei LNGMalaysia LNG

Sakhalin

QCLNG

PreludeNorth West Shelf

Gorgon

Gasnor

Existing

Under construction

Oman LNG

Qatar Gas 4

Nigeria LNG Atlantic LNG

Peru LNG

Egypt LNG

Royal Dutch Shell November 28-29, 2017

North American projects set new market benchmark

‘’Build’’ as well as ‘’Buy’’ opportunities

Advantaged positions

Capital efficiency – technical & commercial innovation

Differentiated portfolio and financial strength

39

Integrated Gas

Selective growth: pre-FID portfolio

Cost of supply includes shipping costs, excludes finding costs and fiscal take

$/mmBtu

LNG pre-FID unit cost of supply Cost of supply is key

Competitive pre-FID opportunities in all supply basins

LNG Canada

Lake Charles

Abadi

Browse

Tanzania

Sakhalin expansion

Nigeria LNGexpansion

Baltic LNG

Mozambique GTL

In-/Post-FEED

Pre-FEED

Royal Dutch Shell November 28-29, 2017

Cash engine

As of Q3 2017; capital employed includes new energies; average capital investment per annum in period 2018-20

Creating & securing demand Optimisation Managing supply

Capital employed: $90 billion

Production: 1.0 mboe/d

Liquefaction volume:34 mtpa

LNG sales volumes: 64 mtpa

Capital investment: $4-5 billion

40

LNG

Gas and power

Gas-to-liquids premium products

Marketing and trading

Shipping and transport

Regasification

Gas and liquids production

Liquefaction

Gas-to-liquids

Integrated Gas

World leader Growing markets Differentiated portfolio Cash delivery

Royal Dutch Shell November 28-29, 2017

Appomattox hull arrival in Ingleside Texas – USA

Andrew BrownUpstream DirectorRoyal Dutch Shell

Royal Dutch Shell November 28-29, 2017 42

Upstream

High-grading position

Operational excellence focus

Driving continuous improvement

Advantaged portfolio

Delivery track record

Continuing to lower costs

Enhance position

Improved competitiveness

Accelerating selective growth

Cash engines Growth priorities Emerging opportunities

Delivering profitable growth

Conventional oil & gas Deep water Shales

$39 billion

1.6 mboe/d

$4-5 billion

Capital employed:

Production:

Capital Investment:

$63 billion

0.7 mboe/d

$5-6 billion

$18 billion

0.3 mboe/d

$2-3 billion

Capital employed:

Production:

Capital Investment:

Capital employed:

Production:

Capital Investment:

Capital employed and production based on Q3 2017; capital investment in period 2018-20; data excludes oil sands

Perdido – USA Gulf of Mexico Permian - USAGbaran Ubie - Nigeria

Royal Dutch Shell November 28-29, 2017

CFFO Quarterly

43

Upstream financial performance

$ billion

Cash flow from operations

$ CFFO per boe

Unit cash flow

$ billion

Organic free cash flow

$ billion

Earnings by strategic theme & ROACE

Drive stability & sustain cash delivery

Portfolio delivering higher cash margins

$ per barrel

%

Brent (RHS)

16Q1 16Q3 16Q4 17Q116Q2 17Q317Q2

+$10 per barrel margin

$52 $52$44$99Brent

Conventional oil & gas ShalesDeep water Other ROACE (RHS)

4 quarter rolling (RHS)

$ billion

Cash flow from operations includes working capital; earnings excludes identified items; data includes oil sands

Royal Dutch Shell November 28-29, 2017 44

“Fit for the future”

Improving results

Gap to potential

Granular improvement plans

Rigorous cadence

50% fewer tier 1 & 2 incidents

Production Availability Total costProcess safety

Competitive unit operating costs

>90%Unlock 150 kboe/d from optimization

Million boe per day

Production & availability

$ billion

Upstream operating costs

%

Availability (RHS)BG portion in integration year

ProductionBG portion in integration year

Total Upstream operating costs

2018 aspirations

Royal Dutch Shell November 28-29, 2017 45

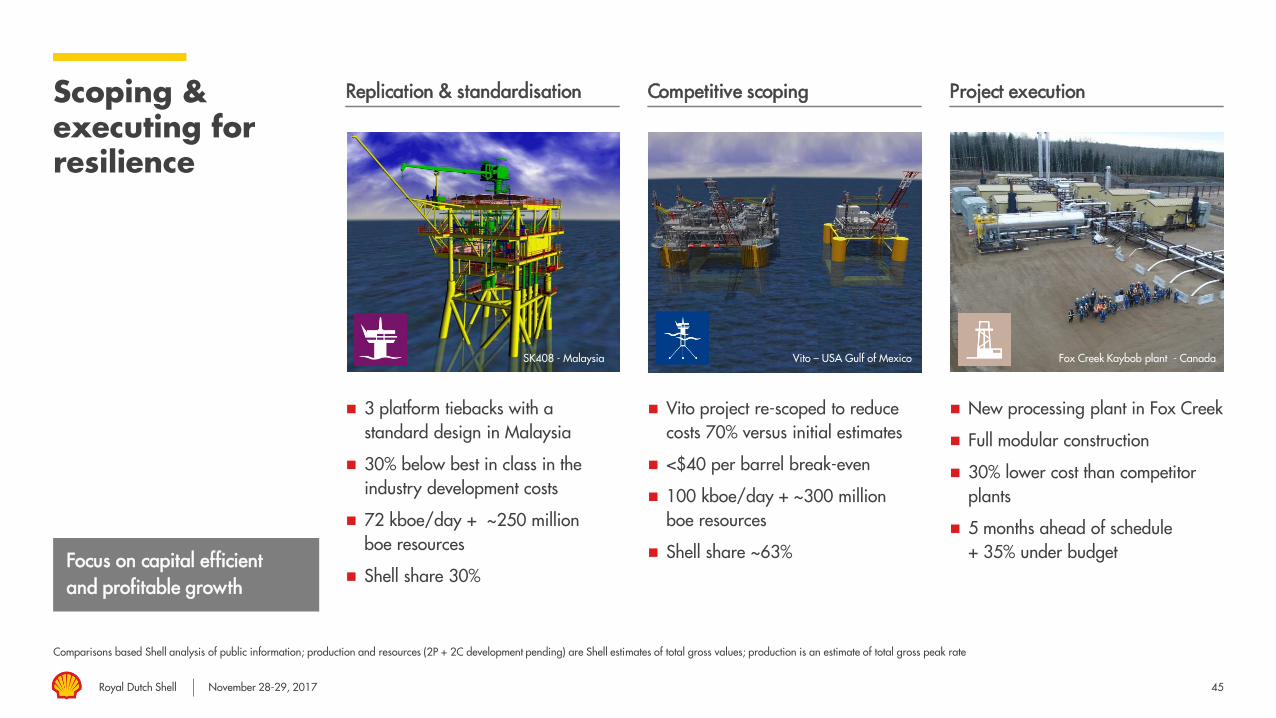

Scoping & executing for resilience

Replication & standardisation Competitive scoping Project execution

3 platform tiebacks with a standard design in Malaysia

30% below best in class in the industry development costs

72 kboe/day + ~250 million boe resources

Shell share 30%

Vito project re-scoped to reduce costs 70% versus initial estimates

<$40 per barrel break-even

100 kboe/day + ~300 million boe resources

Shell share ~63%

New processing plant in Fox Creek

Full modular construction

30% lower cost than competitor plants

5 months ahead of schedule + 35% under budgetFocus on capital efficient

and profitable growth

Fox Creek Kaybob plant - CanadaVito – USA Gulf of MexicoSK408 - Malaysia

Comparisons based Shell analysis of public information; production and resources (2P + 2C development pending) are Shell estimates of total gross values; production is an estimate of total gross peak rate

Royal Dutch Shell November 28-29, 2017 46

Project delivery 2016+

Key Upstream start-ups & under construction

Started >400 kboe/d since 2016

>600 kboe/d still to start through into the early 2020’s

FPSO 9▪ 100 kboe/d▪ Shell 30%

Kashagan▪ 370 kboe/d▪ Shell 17%

Stones▪ 50 kboe/d▪ Shell 100%

FPSO 7+8+10▪ 450 kboe/d▪ Shell 25%

ML South▪ 40 kboe/d▪ Shell 35%

✓

✓

✓On-stream

✓

✓

Forcados Yokri▪ 50 kboe/d▪ Shell 30%

Gbaran Ubie Ph2▪ 150 kboe/d▪ Shell 30%

Malikai▪ 60 kboe/d▪ Shell 35%

Schiehallion redevelopment▪ 125 kboe/d▪ Shell 45%

Baronia/Tukau Timur▪ 65 kboe/d▪ Shell 40%

✓

Clair Ph2▪ 100 kboe/d▪ Shell 28%

✓

Coulomb Ph2▪ 10 kboe/d▪ Shell 100%

Kaikias Ph1▪ 40 kboe/d▪ Shell 80%

Tempa Rossa▪ 50 kboe/d▪ Shell 25%

✓

Southern Swamp AG▪ 30 kboe/d▪ Shell 30%

Rabab HarweelIntegrated Project▪ 40 kboe/d▪ Shell 34%

Permian & Fox Creek▪ 200 kboe/dincremental Shell shareby 2020

✓

FPSO 11+12+13+14+15▪ 750 kboe/d▪ Shell 25%1

Appomattox▪ 175 kboe/d▪ Shell 79%

Libra EWT FPSO▪ 50 kboe/d▪ Shell 20%

1 Berbigão, Sururu and Atapú West (3 FPSOs) are subject to unitisation agreements

Individual project volumes are total gross peak production with the exception of the Brazil FPSOs which is oil capacity as per operator; sum is estimate of Shell share production at peak

✓

Royal Dutch Shell November 28-29, 2017 47

Conventional oil & gas

Portfolio & priorities

Million boe per day

Production & availability

$ billion

Operating costs

$ CFFO per boe

Unit cash flow

Nigeria

KazakhstanUK

Norway

Divesting the non-core assets

Improving existing operations – fit for the future

Negotiating to more resilient positions

Selective growth to offset decline

%

4Q rolling

Production Availability (RHS)

Royal Dutch Shell November 28-29, 2017 48

Conventional oil & gas

Sustaining the engine

2019-21: 2016 RT $60 per barrel

Million boe per day

Production

Project break-even prices

$ billion

Organic free cash flow1

On-stream Under constructionPre-FID &Exploration (risked)

0

2016 2019-21Eaverage

2017E

$5-6 billion

Pre-FID funnel break-even price $ per barrel

Robust project funnel

Sustaining the engine with disciplined investment

Large portfolio of low break-even price projects

Percentage of capital investment

0% 100%50%

1 Corrected November 7, 2018.

Royal Dutch Shell November 28-29, 2017 49

Deep water

A leading IOC position

Thousand boe per day

Advantaged portfolio

Pre-FID funnel break-even price $ per barrel

Competitive growth

$ per boe

Production excellence

Deep water pioneer

Top tier acreage & basins

Global scale provides competitive advantage

Pre-FID deep water project average forward looking BEP is <$30 per barrel

Efficient execution, competitive scoping and affordable technology

Structural operating cost reductions with further opportunity

Disciplined approach to maximize availability

Up to 70kboe/d production unlocked in 2017

Strong deep water capabilities combined with advantaged portfolio

%

2014 2017Shell Peer group range Availability (RHS)Unit costs

Percentage of capital investment

Peer group range based on Wood Mackenzie data; break-even price is the Brent estimate of the FID forward NPV break-even; direct unit costs exclude feasibility, research & development, decommissioning & restoration and idle rig expense

Royal Dutch Shell November 28-29, 2017 50

Deep water

World class delivery

Progressing to >900 kboe/d by 2020

Maintain production through mid-2020s with discovered volumes & defined projects

Upside growth with exploration

Capital discipline – doing more with less

Accelerating and increasing organic free cash flow by lowering costs & improving production

2019-21: 2016 RT $60 per barrel

Transition from growth priority to cash engine

Thousand boe per day

Production

$ billion

Organic free cash flow1

BrazilGulf of Mexico Other

$6-7 billion

0

2016 2019-21Eaverage2017E

1 Corrected November 7, 2018.

Royal Dutch Shell November 28-29, 2017 51

Shales

Enhancing competitiveness

$ per boe 2017 YTD

Direct field costs - Permian

$ million 2017 YTD (normalized to 7500’ lateral)

Drill & complete - Permian Capabilities & technology

Reduced direct field operating costs by 33% in past year and 60% in last 2 years

Reduced drill and complete per well by 35% in last 2 years

Canada remote drilling center used for Argentina wells

iShales end-to-end future field development solutionNimble as an independent

& leverage capabilities of a major

Drill Complete

Basinco-ventures ShellBasin

co-ventures ShellRemote drilling center - Canada

Royal Dutch Shell November 28-29, 2017 52

Shales

Building a growth business

2019-21: 2016 RT $60 per barrel

Near-term selective acceleration of Permian & Fox Creek Duvernay

Growth of ~200 kboe/d by 2020

Average break-even price ~$40 per barrel

Accelerating free cash flow break-even versus 2016 Capital Markets Day by 1 year within previous capital guidance

Build a material & sustainable growth business post 2020

Thousand boe per day

Permian 2017 growth

Thousand boe per day

Production 2020 growth

$ billion

Organic free cash flow1

Western Canada Gas

Western Canada LTO

Appalachia

Permian

Argentina

Haynesville

Liquids rich

Dry gasFox Creek Duvernay

+75%

Actual Estimate

>200%

Dry gas Permian Fox Creek &Argentina

0

$1-2 billion

2016 2019-21Eaverage2017EJan Dec

1 Corrected November 7, 2018.

Royal Dutch Shell November 28-29, 2017 53

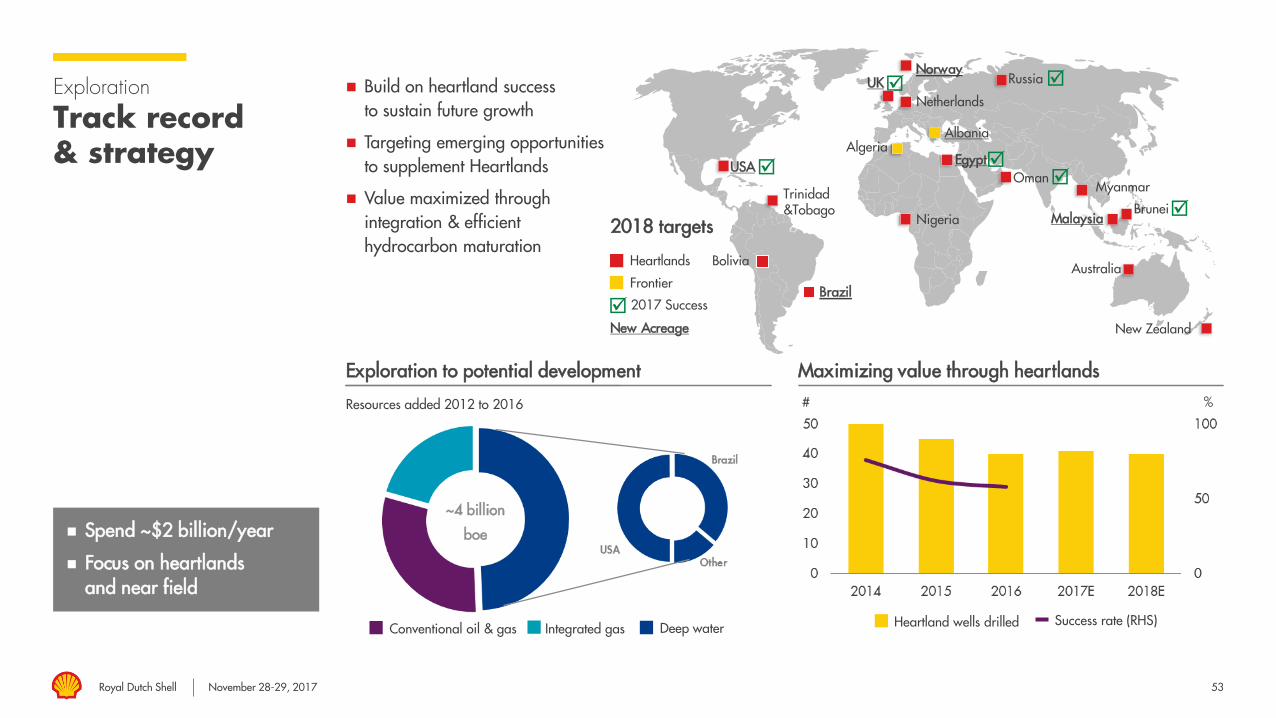

Exploration

Track record & strategy

Resources added 2012 to 2016

Exploration to potential development#

Maximizing value through heartlands

Spend ~$2 billion/year

Focus on heartlands and near field

Build on heartland success to sustain future growth

Targeting emerging opportunities to supplement Heartlands

Value maximized through integration & efficient hydrocarbon maturation

2018 targets

Heartlands

Frontier

Trinidad &Tobago

USA

Tanzania

Nigeria

UKNetherlands

Albania

Oman Egypt

Russia

BruneiMalaysia

2017 Success

Norway

Bolivia Australia

Algeria

Brazil

Myanmar

New ZealandNew Acreage

~4 billion

boe

Conventional oil & gas Integrated gas Deep water Heartland wells drilled Success rate (RHS)

%

Royal Dutch Shell November 28-29, 2017

Reserves (SEC proved)Discovered resources (2P+2C development pending)

Conventionaloil & gas

Deep water Shales

54

Robust development potential

Billion boe

Significant discovered resources pending development

Project costs down dramatically with room for further reduction

Competitive project funnel to develop

Reserves & resources

$ per boe

Deep water unit development costs

-45%

$ per boe

COG operated unit development costs

-45%

Shales break-even price (Permian example)$ per barrel

0

40

20

Net risked well count260013000

<$40 $40-50

Royal Dutch Shell November 28-29, 2017 55

2018-2022

Pre-FID Options

Individual project volumes are Shell’s current estimates of total gross peak production; sum is estimate of Shell share production at peak excluding shales

Potential >750 kboe/d peak

Penguins redevelopment▪ 45 kboe/d▪ Shell 50%

WDDM 9B▪ 60 kboe/d▪ Shell 50%

PDO enhanced recovery & waterflood projects▪ 50 kboe/d▪ Shell 34%

Gumusut-Kakap Ph2▪ 50 kboe/d▪ Shell 30.4%

Tyra future▪ 75 kboe/d▪ Shell 37%

Pegaga▪ 95 kboe/d▪ Shell 20%

Vito▪ 100 kboe/d▪ Shell 63.11%

Libra 1▪ 160 kboe/d▪ Shell 20%

Libra 2+3+4▪ ~450 kboe/d▪ Shell 20%

Argentinashales options

North America shales options

Bonga South West▪ 175 kboe/d▪ Shell 42.95%

Val D’Agri Ph2▪ 65 kboe/d▪ Shell 39%

Pierce Depressurisation▪ 25 kboe/d▪ Shell 92.52%

HI development▪ 75 kboe/d▪ Shell 40%

Gbaran Ph3▪ 70 kboe/d▪ Shell 30%

Marjoram/Rosmari▪ 60 kboe/d▪ Shell 75%

Bonga main life extension▪ 90 kboe/d▪ Shell 55%

Clair South▪ 60 kboe/d▪ Shell 28%

Ormen Lange recovery▪ 50 kboe/d▪ Shell 18%

Assa North▪ 60 kboe/d▪ Shell 30%

Uzu development▪ 45 kboe/d▪ Shell 30%

Kashagan CC01▪ 100 kboe/d▪ Shell 17%

KGK expansion Ph1▪ 40 kboe/d▪ Shell 29%

Pearls Khazar▪ 40 kboe/d▪ Shell 55%

Kalamkas▪ 55 kboe/d▪ Shell 17%

Jackdaw▪ 40 kboe/d▪ Shell 70%

Troll Ph3▪ 255 kboe/d▪ Shell 8.1%

SK408▪ 72 kboe/d▪ Shell 30%

Royal Dutch Shell November 28-29, 2017 56

Upstream

High-grading position

Operational excellence focus

Driving continuous improvement

Advantaged portfolio

Delivery track record

Continuing to lower costs

Enhance position

Improved competitiveness

Accelerating selective growth

Cash engines Growth priorities Emerging opportunities

Delivering profitable growth

Conventional oil & gas Deep water Shales

$39 billion

1.6 mboe/d

$4-5 billion

Capital employed:

Production:

Capital Investment:

$63 billion

0.7 mboe/d

$5-6 billion

$18 billion

0.3 mboe/d

$2-3 billion

Capital employed:

Production:

Capital Investment:

Capital employed:

Production:

Capital Investment:

Capital employed and production based on Q3 2017; capital investment in period 2018-20; data excludes oil sands

Perdido – USA Gulf of Mexico Permian - USAGbaran Ubie - Nigeria

Royal Dutch Shell November 28-29, 2017

John AbbottDownstream DirectorRoyal Dutch Shell

Bangkok – Thailand

Royal Dutch Shell November 28-29, 2017 58

Downstream Cash engine

Capital employed and volumes based on Q3 2017

Capital investment is in period 2018-2020; Source brand preference: Ipsos – Global Customer Tracker (covering 30+ markets)

Further strengthen our financial performance

Upgrading our portfolio

Returns + free cash flow improvement

Chemicals growth priority

Marketing Refining & Trading Chemicals

Growth priority

Customer offer + brand leverage

Differentiated products

Global #1 Brand

Full integration with trading

Improve retained assets

Reducing refining capacity

Advantaged feedstock

Strong product portfolio

Proprietary technology

$18 billion

6.5 mboe/d

$23 billion

2.6 mboe/d

$15 billion

~17 mtpa

$3-4 billion

Capital employed: Capital employed:

Sales volumes:

Capital Investment:

Refinery processing:

Capital employed:

Sales volumes:

$4-5 billionCapital investment:

Royal Dutch Shell November 28-29, 2017

Marketing

59

Downstream financial performance

Earnings and ROACE on CCS basis, excluding identified items; Source brand preference: Ipsos – Global Customer Tracker (covering 30+ markets)

$ billion

Cash flow

%

Global brand preference

$56 billion at end Q3’17

Capital employed

$ billion

Earnings by sub-segments + ROACE

Strong cash generation

Oil Products: $6 - 7 billion organic FCF by 2020

Competitive returns

%

ROACE (RHS)Refining & Trading

ChemicalsMarketingShell Other majors

$ billion

Working capital movement

CFFO excluding working capital

Free cash flow (RHS) Refining & Trading Chemicals

Royal Dutch Shell November 28-29, 2017

1,050,000 bpd 875,000 bpd 460,000 bpd

Deer Park ( 50%)

Buenos Aires (100%)

Miro (32%)Rheinland (100%)

Schwedt (38%)

Pernis (100%)

Pulau Bukom(100%)

Tabangao (55%)

Fredericia (100%)

Puget Sound(100%)

Martinez (100%)

Scotford (100%)

Sarnia (100%)

Durban (38%)

Karachi (30%)

Al Jubail (50%)

60

Investing in selective growth

Refining and Trading

Shell capacity as at end Q3 2017

Refinery capacity in thousand barrels per day (100%)

Retain competitive sites

Exits 2005–16Announced exitsRetained site 2017

Refineries (barrels per day)

Announced exits

London Rotterdam

Singapore

Dubai

Houston

Convent (100%)Norco (100%)

Trading offices

0 – 100,000101,000 – 200,000201,000+

Calgary

Beijing

Royal Dutch Shell November 28-29, 2017 61

Downstream asset integration:Rhine envelope & Eastern US portfolio

Rhine envelope Integration of Motiva assets to the DS portfolio

P o r t A r t hu rC o n v en t

N o r co

Global trading options Rostock

PCK SchwedtHarburg

SeefeldArnhem

Pernis

Rheinland

Flörsheim

Würzburg

LobauLinz

Salzburg

Zurich

Geneva

BertrangeLudwigshafen

MiRO Karlsruhe

Altmannshofen

Moerdijk

RMR

RRP

Chemical plant

Refinery

Storage depot

Pipeline

100% Shell assets

Joint venture

Shell terminalsShell refineriesShell markets

Motiva

Royal Dutch Shell November 28-29, 2017 62

Investing in selective growth

Shell Oil Products – marketing

%

Marketing – ROACE

$ billion

Marketing – free cash flow

Mexico – Retail country entry

Retail country entry - Mexico Shell Recharge - UK

Royal Dutch Shell November 28-29, 2017

Oil ProductsRetail’s 5 ambitions for 2025

63

50%

Increase margin share from non-

fuels retail to 50%

20%

Fuels margin from low-emission

energy solutions

LOWER CARBON

Reduce carbon intensity of our

retail outlets by at least 50%

EVERY CUSTOMER

Treated like a guest on site & in the digital world

100%

Sites committed to local communities

unified by a global social

cause

1 2 3 4 5

Royal Dutch Shell November 28-29, 2017

Digitalisation

Jiffy lube is a 100% Shell venture

Connected customer Innovation New business models

Shell App

>3 million downloads

715,000 active users in >35 markets

Quick, easy and personalised

experience

Enhanced payment and loyalty

proposition

Connected car

World’s first in car cashless payment

system

Launched with Jaguar Land Rover

Creates opportunities for new B2B

business models

FitCar powered by Jiffy lube

Provides customers with maintenance

alerts, trip info and more

More new B2C and B2B business

models underway

64

Royal Dutch Shell November 28-29, 2017

Under construction

65

Growth projects

Chemicals Million metric tonnes

Ethylene capacity

Nanhai II

Pennsylvaniachemicals

USGCrestructuring

Nanhai I

Bukom start-up

65

Geismar, USA

Nanhai, China

Pennsylvania, USA

425,000 metric tonnes per annum additional Alpha Olefins capacity

New liquids cracker and derivatives units

Capacity: ~1.2 million metric tonnes ethylene per annum

50/50 JV with CNOOC

Greenfield FID 2016

Capacity: ~1.5 million metrictonnes ethylene per annum and polyethylene derivatives

2006Nanhai

2010 USGC go-light strategy

2010 Singapore

2016+ China + USA

LiquidGas

2022

Feedstock mix

SADAF exit

Royal Dutch Shell November 28-29, 2017 66

Organic growth

Chemicals

Earnings and ROACE on CCS basis, excluding identified items; Shell ROACE calculations for 2012 has been restated for the impact of IAS 19

$ billion

Earnings + ROACE

Targets aspiration per year mid-’20s:

Earnings: ~$3.5 - 4 billion

Cash flow: ~$5 - 6 billion

Base capex: ~$1 - 1.5 billion

Improve base business

Expand current base

portfolio

Adding to portfolio –

growth

%

Earnings ROACE (RHS)

Royal Dutch Shell November 28-29, 2017 67

Downstream Cash engine

Capital employed and volumes based on Q3 2017

Capital investment is in period 2018-2020; Source brand preference: Ipsos – Global Customer Tracker (covering 30+ markets)

Further strengthen our financial performance

Upgrading our portfolio

Returns + free cash flow improvement

Chemicals growth priority

Marketing Refining & Trading Chemicals

Growth priority

Customer offer + brand leverage

Differentiated products

Global #1 Brand

Full integration with trading

Improve retained assets

Reducing refining capacity

Advantaged feedstock

Strong product portfolio

Proprietary technology

$18 billion

6.5 mboe/d

$23 billion

2.6 mboe/d

$15 billion

~17 mtpa

$3-4 billion

Capital employed: Capital employed:

Sales volumes:

Capital Investment:

Refinery processing:

Capital employed:

Sales volumes:

$4-5 billionCapital investment:

Royal Dutch Shell November 28-29, 2017

Maarten WetselaarIntegrated Gas & New Energies DirectorRoyal Dutch Shell

Royal Dutch Shell November 28-29, 2017 69

New Energies

Focus areas:

Biofuels

Hydrogen

Emerging Opportunities

Focus areas:

Trading, marketing and customer access

Low-carbon generation and storage (solar, wind, gas)

Build integrated value chains

Exploit adjacencies to existing businesses

Discipline and commerciality

Not equipment manufacturing

New Fuels Power

Groundbirch, Canada

Royal Dutch Shell November 28-29, 2017 70

New Energies

Market drivers and differentiators

Market development Shell differentiators Energy transition

World needs more and cleaner

energy

Commercial technologies and

policy drive towards

de-carbonization

Growing role of electricity and

renewables

Power markets expected to

grow faster than the overall

energy system

Global transition expected to be

gradual, local transitions may

be significantly faster

Experience, global footprint,

adjacencies

Trading, optimisation, risk

management

Brand and customers

Energy value chain integration

Royal Dutch Shell November 28-29, 2017 71

New Fuels Biofuels Hydrogen

First generation experience through Raízen joint

venture

One of the largest blenders and traders of biofuels

Developing a second generation advanced biofuels

business

Existing sites in Germany, UK, and USA

Working with partners to develop around

400 sites by 2023 in Germany

Demand driven expansion, including the

Netherlands and California, USA Adjacencies to existing downstream businesses

Raízen - Brazil Hamburg -Germany

Royal Dutch Shell November 28-29, 2017

Portfolio resilience through a Power value chain

C U S T O M E R S O P T I M I S AT I O N S U P P LY & G E N E R AT I O N

72

Adjacencies to existing gas businesses

Value chain integrator Demand-driven

development

Secure demand in key markets

Commercial, industrial, and

residential

Optimise intermittent demand

and supply

Trading opportunities

Wind, solar, and selected gas and

storage assets

Selective capacity ownership to

create portfolio flexibility

Leverage portfolio flexibility and arbitrage opportunities

Multiple parties are active on the demand side

Not all products are supplied by Shell; some are purchased from third parties

Royal Dutch Shell November 28-29, 2017 73

New Energies

Capital and returns

New Fuels Power

New Fuels looks for capital light opportunities

Work in partnerships and consortia

Target downstream returns

Investment in customer access

Selective asset ownership

Target returns of 8 – 12%

Selective an opportunity

driven investment

Capital investment: $1 – 2

billion

Organic + inorganic

NoordzeeWind, The NetherlandsWuppertal, Germany

Royal Dutch Shell November 28-29, 2017

Ben van BeurdenChief Executive OfficerRoyal Dutch Shell

Royal Dutch Shell November 28-29, 2017 75

SummaryT R A N S F O R M A T I O N

I N S H E L LC O N T I N U E T O I M P R O V E

O U R M E T R I C S P E R S H A R E

2014-2020 2020+

2014 - 2020 2020+

Growing per share metrics from a stronger basis

Portfolio re-shape

More free cash flow

Higher returns

Royal Dutch Shell November 28-29, 2017 76

Questions & Answers

Ben van BeurdenChief Executive Officer

Jessica UhlChief Financial Officer

Royal Dutch Shell November 28-29, 2017

Royal Dutch Shell November 28-29, 2017

Royal Dutch Shell plcNovember 28-29, 2017

Management Day – Break-out panelsDelivering a world-class investment case

#makethefuture

Royal Dutch Shell November 28-29, 2017 78

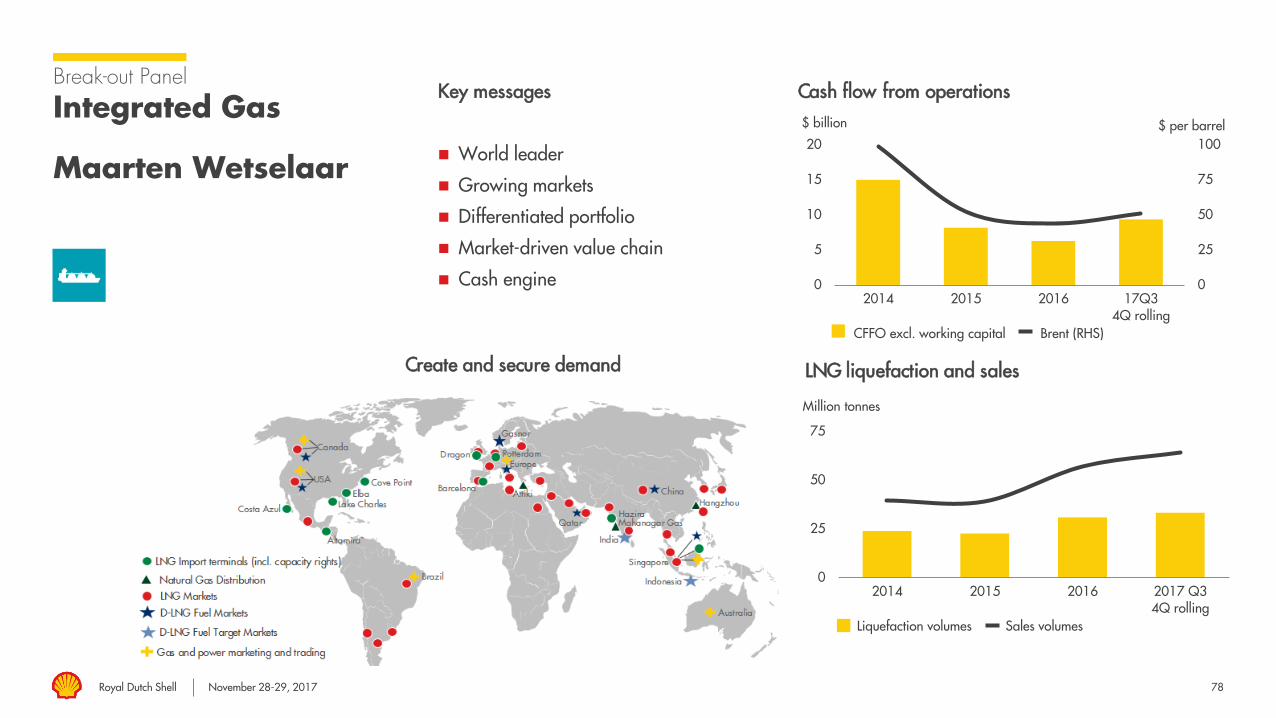

Cash flow from operations

LNG liquefaction and sales

Break-out Panel

Integrated Gas

Maarten Wetselaar

Key messages

World leader

Growing markets

Differentiated portfolio

Market-driven value chain

Cash engine

$ per barrel$ billion

0

25

50

75

100

0

5

10

15

20

2014 2015 2016 17Q34Q rolling

CFFO excl. working capital Brent (RHS)

0

25

50

75

2014 2015 2016 2017 Q34Q rolling

Liquefaction volumes Sales volumes

Million tonnes

Create and secure demand

Royal Dutch Shell November 28-29, 2017 79

Break-out Panel

New Energies

Maarten Wetselaar

Key messages

Emerging opportunity with focus on

New Fuels and Power

Selective, disciplined and commercial

investments

Leverage adjacencies and competitive

advantages

Build a new value chain that will

thrive in the energy transition

Volume Spills

NoordzeeWind , The Netherlands

Royal Dutch Shell November 28-29, 2017 80

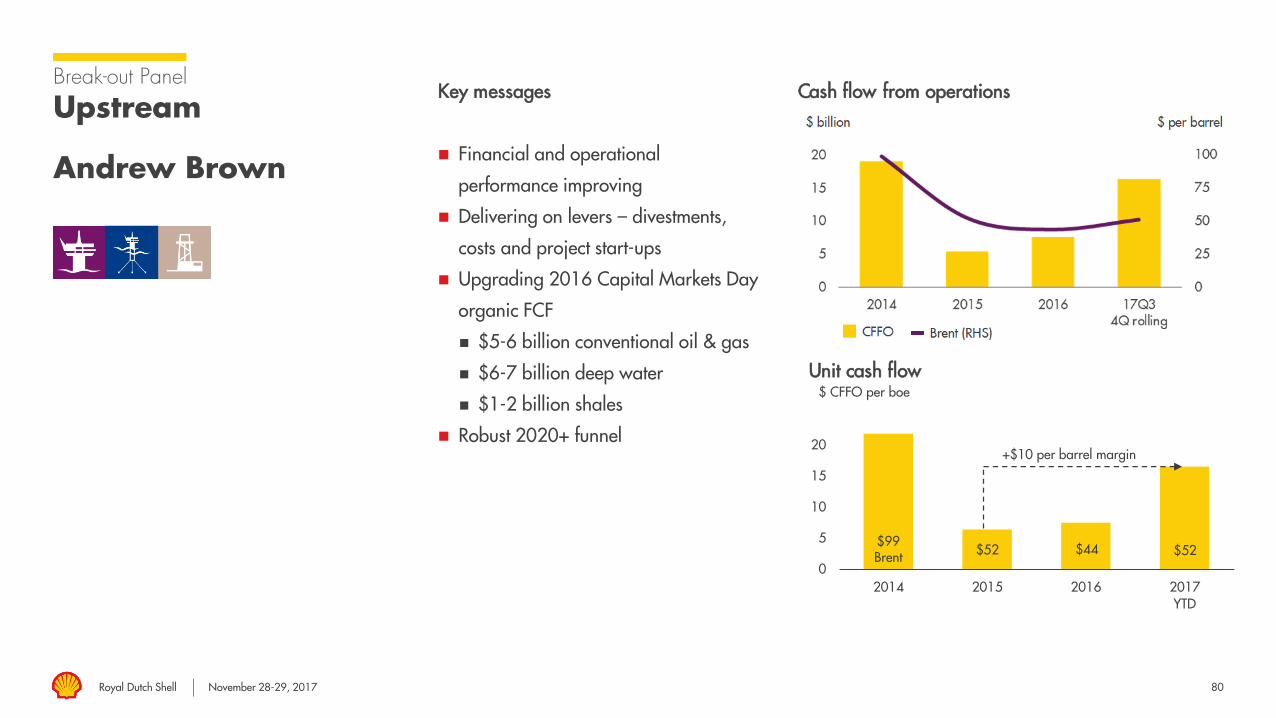

Cash flow from operations

Unit cash flow

0

5

10

15

20

2014 2015 2016 2017YTD

+$10 per barrel margin

$52 $52$44$99Brent

$ CFFO per boe

Break-out Panel

Upstream

Andrew Brown

Key messages

Financial and operational

performance improving

Delivering on levers – divestments,

costs and project start-ups

Upgrading 2016 Capital Markets Day

organic FCF

$5-6 billion conventional oil & gas

$6-7 billion deep water

$1-2 billion shales

Robust 2020+ funnel

Royal Dutch Shell November 28-29, 2017 81

Downstream Cash engine

Capital employed and volumes based on Q3 2017

Capital investment is in period 2018-2020; Source brand preference: Ipsos – Global Customer Tracker (covering 30+ markets)

Further strengthen our financial performance

Upgrading our portfolio

Returns + free cash flow improvement

Chemicals growth priority

Marketing Refining & Trading Chemicals

Growth priority

Customer offer + brand leverage

Differentiated products

Global #1 Brand

Full integration with trading

Improve retained assets

Reducing refining capacity

Advantaged feedstock

Strong product portfolio

Proprietary technology

$18 billion

6.5 mboe/d

$23 billion

2.6 mboe/d

$15 billion

~17 mtpa

$3-4 billion

Capital employed: Capital employed:

Sales volumes:

Capital Investment:

Refinery processing:

Capital employed:

Sales volumes:

$4-5 billionCapital investment:

Royal Dutch Shell November 28-29, 2017

Harry BrekelmansProjects and Technology DirectorRoyal Dutch Shell

Royal Dutch Shell November 28-29, 2017 83

Thrive in the energy transition

Driving to resilience and ambition

1: TCFD - Task Force for Climate-related Financial Disclosures

Demonstrating Shell’s approach across multiple time horizons

TIME HORIZON

SHORT TERM

GHG management

Focussed on areas

we can take

operational action

Included in annual

bonus scorecard

MEDIUM TERM

Strategic positioning and portfolio resilience

Demonstrated by disclosures aligned to

TCFD1 recommendations

Demonstrate financial resilience

of portfolio to energy transition and

climate change actions

LONG TERM

Net Carbon Footprint methodology

Covers full range of emissions from our energy

products through to consumption

1-3 YEARS 5-10 YEARS >10 YEARS

5% Process safety

5% Personal safety

10% GHG management

Sustainable

development

Royal Dutch Shell November 28-29, 2017 84

Thrive in the energy transition

Net Carbon Footprint

Net Carbon Footprint also includes the use of natural sinks and carbon capture usage and storage, not shown in diagram

Shell oil productionUpstream assets

Oil transportShipping or pipeline

Shell refineryDownstream assets Distribution

3rd party crude supplyCountry average

3rd party oil productsRegional average

Shell gas productionUpstream assets

Oil products

Pipeline gas Gas pipelinePipeline

Shell gas productionUpstream assets

Gas pipelinePipeline

Shell LNGShell assets

ShippingLNG transport

Regasification & pipeline

LNG

GTL Shell gas productionUpstream assets

Gas pipelinePipeline

Shell GTLGTL assets DistributionShipping

LNG transport

Biofuels Shell biofuel production(1st / 2nd generation)

TransportRoad/shipping Distribution

E N D - U S E

Transportation

Industrial

Electric power

Residential & commercial

3rd party LNG

3rd party gas

Solar/wind/gridRenewable &grid electricity

3rd party electricityElectricity

Royal Dutch Shell November 28-29, 2017 85

Thrive in the energy transition

Ambition – Net Carbon Footprint

1: Net Carbon Footprint measured on an aggregate “well to wheel” or “well to wire” basis, from production through to consumption, on grams of CO2 equivalent per megajoule of energy products consumed; chemicals + lubricants products are excluded. Carbon

Footprint of the energy system is modelled using Shell methodology aggregating lifecycle emissions of energy products on a fossil-equivalence basis. The methodology will be further reviewed and validated in collaboration with external experts.

2: Potential society trajectory includes analysis from Shell scenarios estimate of Net Zero Emissions by 2070 and IEA Energy Technology Perspectives 2017; Potential illustrative Shell trajectory

WtW gCO2e/MJ1

Ambition to reduce Net Carbon Footprint1 of our energy products by around 20% by 2035

Covers full range of emissions from energy products

Aim to reduce overall intensity including production, supply chain, and customers

Government policy, technology, and consumer choice will drive actual energy transition pace and outcomes

Drive strategy over time in step with society

5-year reviews to ensure in line with societal progress

Ambition for Net Carbon Footprint1

Ambitions: Reduce Net Carbon

Footprint1 of our energy products by ~20% by 2035

Be in line with society Net Carbon Footprint by 2050 Society trajectory2 Shell trajectory2

Shell “business as usual”

In line with society by 2050

~20% reduction by 2035

Royal Dutch Shell November 28-29, 2017 86

Thrive in the energy transition

Ambition – Net Carbon Footprint

1: Net Carbon Footprint measured on an aggregate “well to wheel” or “well to wire” basis, from production through to consumption, on grams of CO2 equivalent per megajoule of energy products consumed; chemicals + lubricants products are excluded. Carbon

Footprint of the energy system is modelled using Shell methodology aggregating lifecycle emissions of energy products on a fossil-equivalence basis. The methodology will be further reviewed and validated in collaboration with external experts.

WtW gCO2e/MJ1

Flexibility and mix of options to achieve ambition

Allows for oil and gas production growth offset by evolving product mix

Changing product mix gives greatest opportunity

Top-quartile scope 1 + 2 emissions has limited overall impact

Potential tools to achieve our 2035 Net Carbon Footprint1 ambition

Shell is active in each of these areas

2 0 3 5 A M B I T I O N

Existing examples:

Wind power Quest CCSRaìzenbiofuels

Shell Recharge +New Motion

Flare reduction

Increased LNG

Nature based offsets

2 0 3 5 A M B I T I O N

(Scope 1+2)

Royal Dutch Shell November 28-29, 2017 87

Thrive in the energy transition

Examples of CO2abatement

Shell reduced heavy paraffin synthesis off-gas (HOG) operational flaring at the plant to zero

HOG gas now used as a fuel to power the plant

Also generates electricity exported to Kahramaa, Qatar’s national Electricity and Water Company

Removed 700,000 tonnes of CO2 a year

Pearl GTL

Bukom refinery Singapore

~68 MW cogeneration unit installed in 2015

Recovering waste heat to generate steam

Expected to reduce total energy consumption at Bukomby between 4% - 5%

Saving more than 200,000 tonnes of CO2 a year

Bukom refinery

Flare in utilities area, Pearl GTL, Qatar Bukom refinery, Singapore

Short-term operational focus

Royal Dutch Shell November 28-29, 2017

Royal Dutch Shell plcNovember 28-29, 2017

Management Day – AppendicesDelivering a world-class investment case

#makethefuture

Royal Dutch Shell November 28-29, 2017 89

Integrated Gas

LNG supplyand demand

Source: IHS Markit LNG Waterborne Trade, November 2017. January to October (inclusive) 2017 – JKT: Japan Korea Taiwan - Exports & imports are based on loading & unloading month, respectively, they may not equal as a result

Million tonnes (DES)

Supply development

Million tonnes (DES)

Demand development

Supply growth matched by solid demand

Royal Dutch Shell November 28-29, 2017 90

Investing in selective growth

Shell premium products

%

Global retail – premium product penetration

%

Global lubes - premium products penetration

Shell V-Power is the world’s most widely sold

premium fuel (68 markets)

#1 or #2 in high quality fuels across 90% of markets

Leveraging GTL base oil with Pureplus®

Global #1 for 11 years (including in China)

Royal Dutch Shell November 28-29, 2017 91

Downstream competitive landscape

Downstream: Earnings on local GAAP basis adjusted for inventory valuation differences and excluding identified items, cap. emp based on 2015 reported data; Peer group: CVX, TOT, BP, XOM, RDSChemicals: Earnings excluding identified items; peer group: XOM, LBI, DOW, BP, RDS Source brand preference: Ipsos – Global Customer Tracker (covering 30+ markets)

%

Downstream ROACE

%

Chemicals ROACE

%

Oil Products ROACE

Global brand preference

Brand

Shell Other majorsShell Chemicals peer group

Shell Peers

17Q3

4Q rolling

14Q1 15Q1 16Q1 17Q1

Royal Dutch Shell November 28-29, 2017 92

Shell Midstream Partners

Building scale with high quality midstream assets

Strategic portfolio linking Shell’s integrated footprint

Resilient framework

Diversified portfolio

Sustainable growth

Distribution growth since IPO$ct/LP unitholder

14Q4 17Q3

16.25

31.8+96%

Royal Dutch Shell November 28-29, 2017 93

Thrive in the energy transition

Emissions example: passenger vehicles

Electrification moves end-use emissions to power generation

Power generation isin turn decarbonised

Gasoline / Diesel chain

Electric chain

Illustrative size of emission

Well to Wheels CO2 emissions

Well to Wheels CO2 emissions

Well to tank Tank to wheel15% 85%

Well to tank Tank to wheel100% 0%

Illustrative size of emission from an asset No emission asset

Royal Dutch Shell November 28-29, 2017 94

Shell scenarios and modelling

Societal scenarios explore “how

the world might work” in the

future, and is an essential front-

end input in energy modelling

Different parts of the world

will develop in their own

ways and at different paces

Technology innovation enables

new options

Resource availability can be

an enabler as well as a

constraint

The scenarios and models deal

with disruptions and

non-linear relationships

Modelling helps to demonstrate

the plausibility of the scenarios

▪ Shell scenarios underpinned by detailed models and databases

Mountains/Oceans

Demand

Supply

Resources

Translating the societal-political-economic

scenarios into “So what for energy?”

Royal Dutch Shell November 28-29, 2017 95

Shell scenarios analysis

Net-zero emissions by 2070

Shell is working on a scenario that achieves net-zero emissions by 2070, required for a 2°C pathway. This is plausible

in the medium term, and becomes normative1 in the long term

What one has to believe2:

▪ China CO2 peaks before 2030, India in 2038, Africa in 2055

▪ 100% of new car sales are electric vehicles (EV) by 2030 in EU, Japan, China and by 2035 in the USA

▪ Government-led CO2 pricing of $80/tonne by 2030 then stimulates ~1 large-scale CCS plant3 daily until 2070

▪ Consumers use 40% less energy in their homes by 2070 to do the same things as today

▪ Electricity rises from ~ 20% today to 50% of final consumption globally by 2070

▪ Solar PV installation grows from 90 GW a year today to1,500 GW a year in 2050

▪ The use of biomass and biofuels increases fivefold by 2060 to ~32 mln boe a day (about 1/3 of today’s oil)

1: Normative means exploring the pathway that needs to be taken in order to reach a specific future situation. 2: Source: Shell World Energy Model

3: A large-scale CCS plant is assumed to capture 1 million tonnes CO2 per year

▪ All available measures are required across the world championed by leading countries and followed by others to reach net-zero emissions by 2070

Royal Dutch Shell November 28-29, 2017 96

IEA World Energy Outlook 2017 scenarios

The IEA Current Policies (CPS) and New Policies (NPS) scenarios start with assumptions about policies and see

where they lead. The Sustainable Development Scenario (SDS) sets the end-goal (Paris goal) and works back to

the present

Source: IEA World Energy Outlook 2017

▪ IEA scenarios are not forecasts, but depict alternative futures, along pathways the world could travel if certain conditions are met

IEA assumptions:

▪ Energy demand growth of 0.1% a year in the IEA

Sustainable Development Scenarios compared

to1.4% in the IEA Current Policies scenario

▪ If net-zero emissions is achieved by 2100 then

there is an even chance that temperature rise

could be limited to below 2 degrees Celsius

▪ If net-zero emissions is achieved earlier, or is

followed by a period of net negative emissions,

the likely rise in temperature is lower

Royal Dutch Shell November 28-29, 2017 97

Energy transition

Engagement with TCFD

1: We are engaging with the task force to suggest forms of disclosure which, where commercially possible, will be most relevant and useful to investors

2: We also include other relevant information in other disclosures such as CDP

Governance Strategy Risk Management Metrics & Targets

Primary source2 Annual Report Energy Transition Report

Annual Report Sustainability Report

Comment Climate change part of risk factors

We consider different time horizons

Demonstrate portfolio flexibility over next 10 years

We use scenarios to assess longer-term options

Tools and processes in place to manage risks and opportunities

Detailed list of risks and opportunities via CDP

Metrics reported via Sustainability Report and website for many years

Ambitions for 2035 and 2050 articulated, with application of Net Carbon Footprint methodology going forward

Shell’s response to TCFD recommendations1

▪ Shell supports the TCFD▪ Member of Oil & Gas

Preparer Forum▪ Working to prepare

disclosures for 2018

Royal Dutch Shell November 28-29, 2017

Royal Dutch Shell plcNovember 28-29, 2017

Management Day Delivering a world-class investment case

#makethefuture