Malaysia Brunei - IUJ

79

COUNTRY PROFILE 2001 Malaysia Brunei This Country Profile is a reference tool, which provides analysis of historical political, infrastructural and economic trends. It is revised and updated annually. The EIU’s Country Reports analyse current trends and provide a two-year forecast The full publishing schedule for Country Profiles is now available on our website at http://www.eiu.com/schedule The Economist Intelligence Unit 15 Regent St, London SW1Y 4LR United Kingdom

Transcript of Malaysia Brunei - IUJ

COUNTRY PROFILE 2001

Malaysia

BruneiThis Country Profile is a reference tool, which providesanalysis of historical political, infrastructural and economictrends. It is revised and updated annually. The EIU’s CountryReports analyse current trends and provide a two-yearforecast

The full publishing schedule for Country Profiles is nowavailable on our website at http://www.eiu.com/schedule

The Economist Intelligence Unit15 Regent St, London SW1Y 4LRUnited Kingdom

The Economist Intelligence UnitThe Economist Intelligence Unit is a specialist publisher serving companies establishing and managingoperations across national borders. For over 50 years it has been a source of information on businessdevelopments, economic and political trends, government regulations and corporate practice worldwide.

The EIU delivers its information in four ways: through our digital portfolio, where our latest analysis isupdated daily; through printed subscription products ranging from newsletters to annual referenceworks; through research reports; and by organising seminars and presentations. The firm is a member ofThe Economist Group.

LondonThe Economist Intelligence Unit15 Regent StLondonSW1Y 4LRUnited KingdomTel: (44.20) 7830 1007Fax: (44.20) 7830 1023E-mail: [email protected]

New YorkThe Economist Intelligence UnitThe Economist Building111 West 57th StreetNew YorkNY 10019, USTel: (1.212) 554 0600Fax: (1.212) 586 0248E-mail: [email protected]

Hong KongThe Economist Intelligence Unit60/F, Central Plaza18 Harbour RoadWanchaiHong KongTel: (852) 2585 3888Fax: (852) 2802 7638E-mail: [email protected]

Website: www.eiu.com

Electronic deliveryThis publication can be viewed by subscribing online at www.store.eiu.com

Reports are also available in various other electronic formats, such as CD-ROM, Lotus Notes, on-linedatabases and as direct feeds to corporate intranets. For further information, please contact your nearestEconomist Intelligence Unit office

Copyright© 2001 The Economist Intelligence Unit Limited. All rights reserved. Neither this publication norany part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by anymeans, electronic, mechanical, photocopying, recording or otherwise, without the prior permissionof The Economist Intelligence Unit Limited.

All information in this report is verified to the best of the author’s and the publisher’s ability. However,the EIU does not accept responsibility for any loss arising from reliance on it.

ISSN 0269-5588

Symbols for tables“n/a” means not available; “–” means not applicable

Printed and distributed by Patersons Dartford, Questor Trade Park, 151 Avery Way, Dartford, Kent DA1 1JS, UK.

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

Comparative economic indicators, 2000

1

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

Contents

Malaysia

4 Basic data

5 Political background5 Historical background9 Constitution, institutions and administration

10 Political forces11 International relations and defence

14 Resources and infrastructure14 Population15 Education15 Health16 Natural resources and the environment17 Transport, communications and the Internet18 Energy provision

19 The economy19 Economic structure20 Economic policy24 Economic performance26 Regional trends

27 Economic sectors27 Agriculture, forestry and fisheries28 Mining and semi-processing29 Manufacturing30 Construction30 Financial services32 Other services

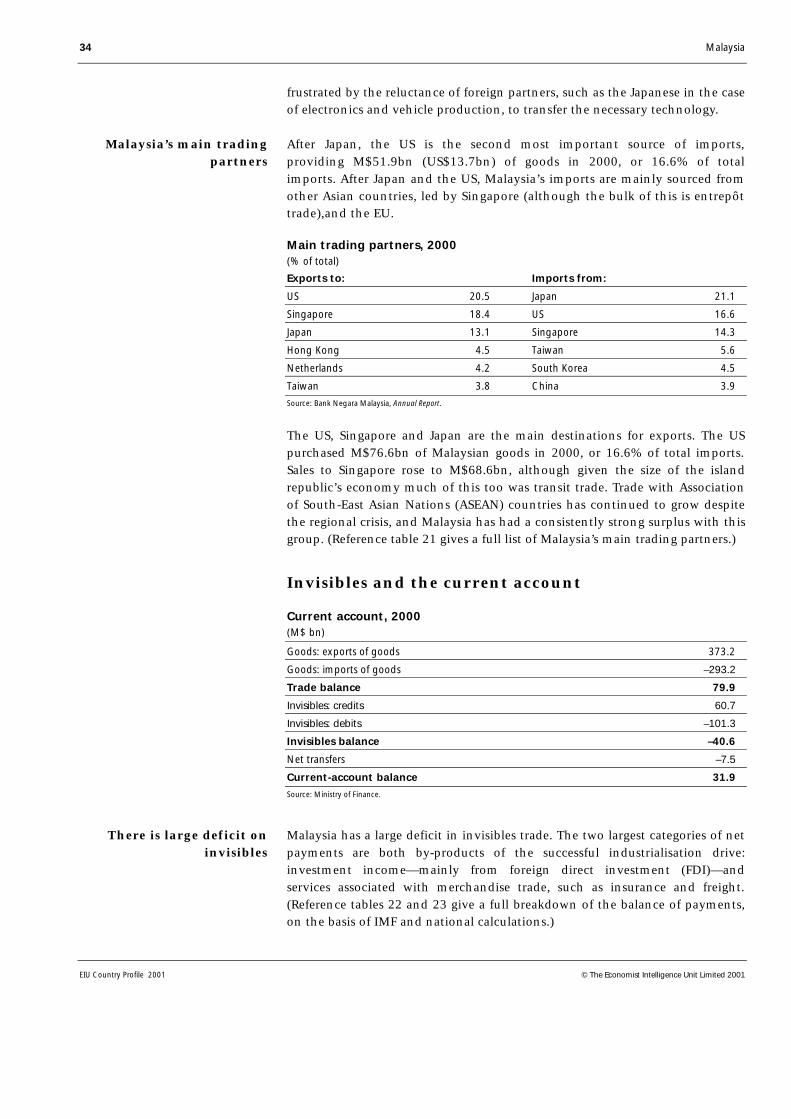

32 The external sector32 Trade in goods34 Invisibles and the current account35 Capital flows and foreign debt36 Foreign reserves and the exchange rate

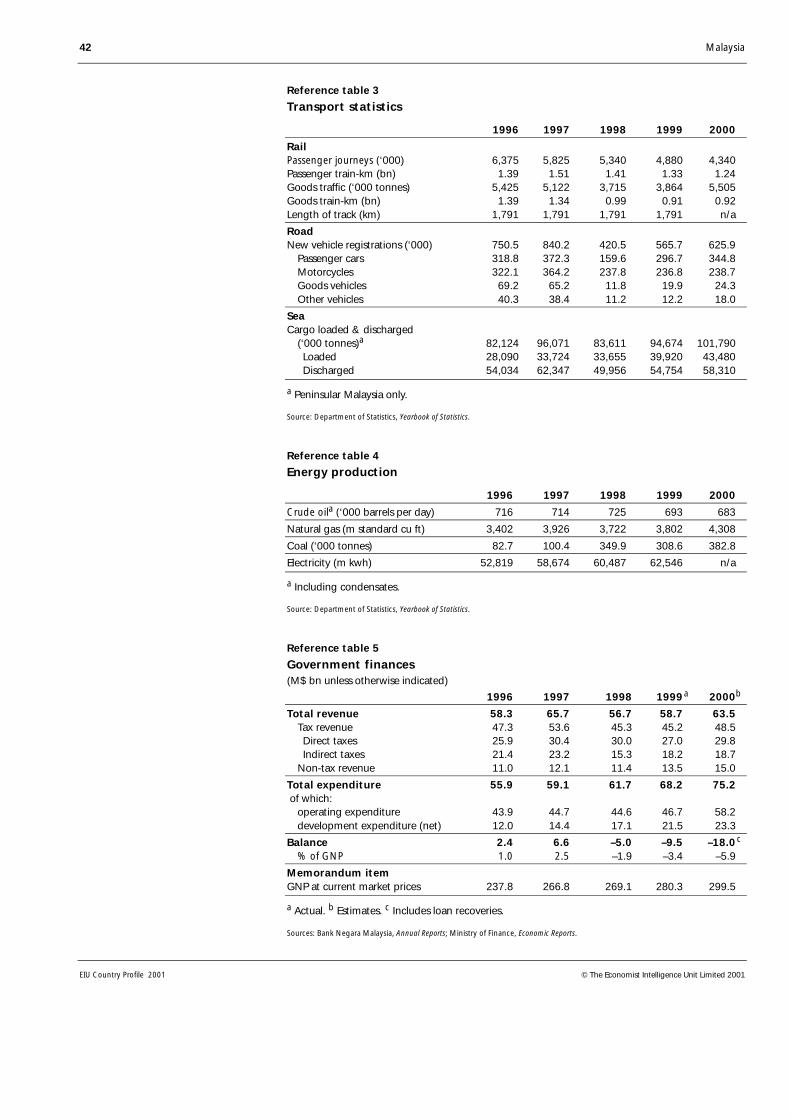

38 Appendices38 Regional organisation39 Sources of information41 Reference tables41 Population41 Labour force42 Transport statistics42 Energy production42 Government finances43 Money supply43 Interest rates43 Gross domestic product

2

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

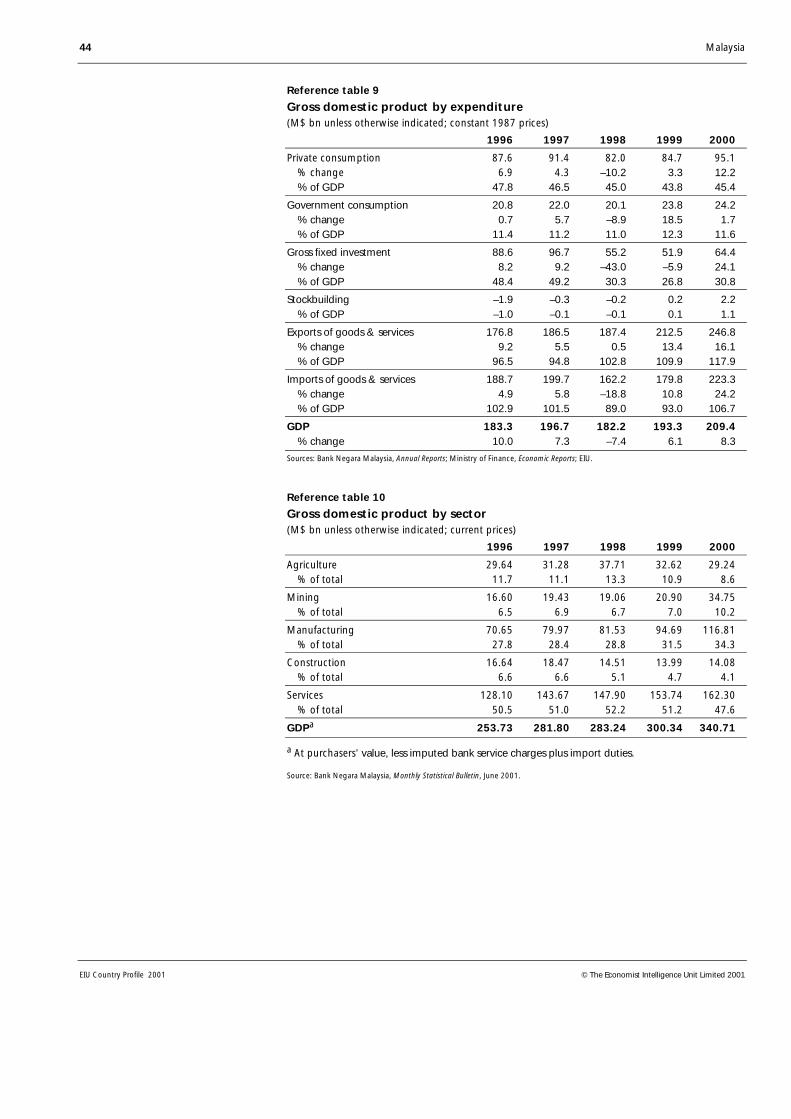

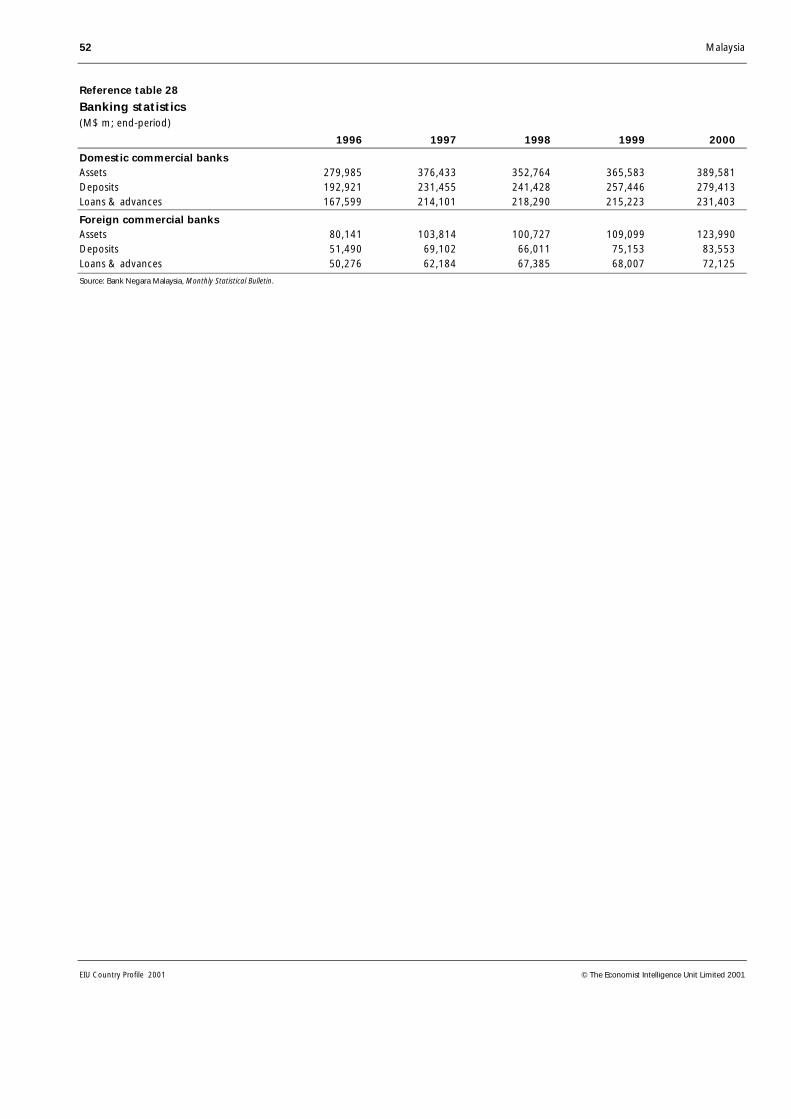

44 Gross domestic product by expenditure44 Gross domestic product by sector45 Consumer price index45 Agricultural and forestry production45 Minerals production46 Manufacturing production46 Construction statistics46 Stockmarket indicators47 Exports47 Imports48 Main traditional exports48 Imports by category48 Main trading partners49 Balance of payments, IMF series50 Balance of payments, national series50 External debt, World Bank series51 Official development assistance51 Foreign reserves51 Exchange rates52 Banking statistics

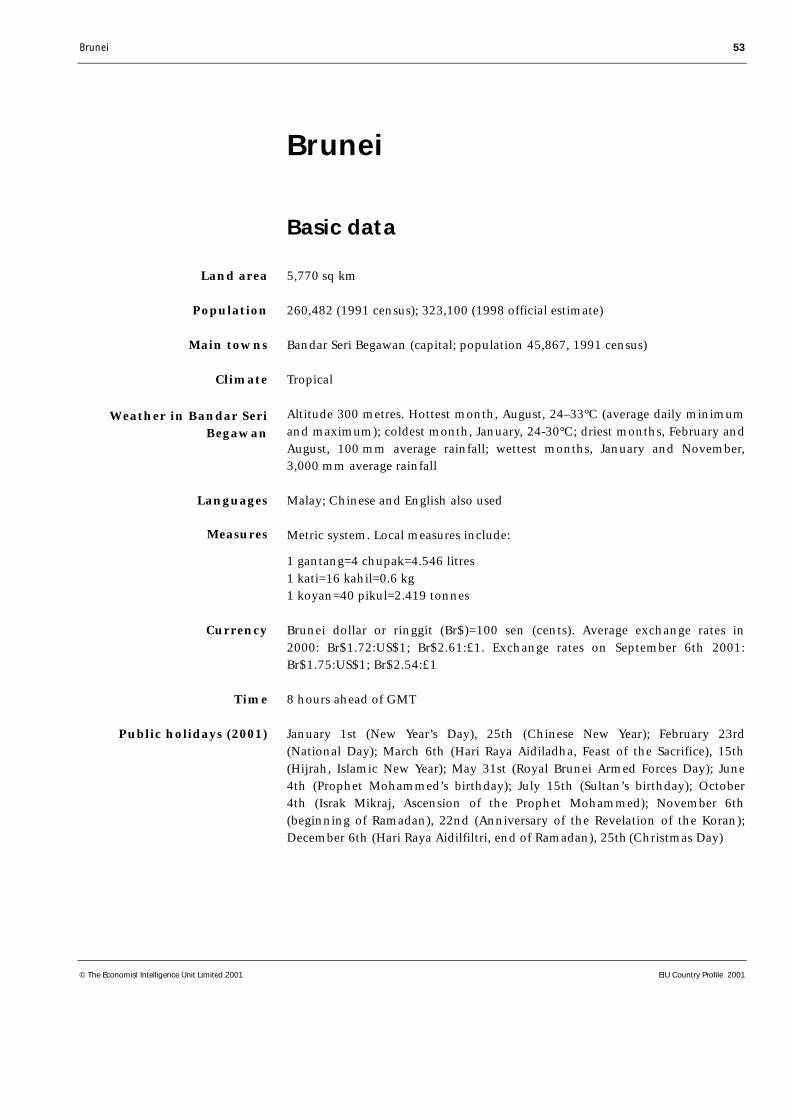

Brunei

53 Basic data

54 Political background54 Historical background54 Constitution, institutions and administration55 Political forces57 International relations and defence

58 Resources and infrastructure58 Population59 Education and health59 Natural resources and the environment60 Transport, communications and the Internet61 Energy provision

61 The economy61 Economic structure62 Economic policy63 Economic performance

64 Economic sectors64 Agriculture, forestry and fishing64 Mining and semi-processing65 Manufacturing65 Construction65 Financial services66 Other services

66 The external sector66 Trade in goods67 Invisibles and the current account

3

© The Economist Intelligence Unit Limited 2001 EIU Country Profile 2001

67 Capital flows and foreign debt67 Foreign reserves and the exchange rate

69 Appendices69 Sources of information70 Reference tables70 Population70 Labour force, 199170 Transport and telecommunications71 National energy statistics71 Government finances71 Money supply72 Gross domestic product72 Gross domestic product by sector73 Consumer prices73 Agricultural production73 Forestry production73 Oil and natural gas production and prices73 Balance of trade74 Main exports74 Main imports74 Main trading partners75 Balance of payments, national series75 Exchange rates75 International reserves

4 Malaysia

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

Malaysia

Basic data

330,113 sq km

23.8m (mid-2001 estimate)

Population in ‘000 (2000)

Kuala Lumpur (capital) 1,298Kelang 649Ipoh 566Petaling Jaya 438Johor Baharu 385

Tropical

Hottest months, April and May, 23-33°C (average daily minimum andmaximum); coldest month, December, 22-32°C; driest month, July, 99 mmaverage rainfall; wettest month, April, 292 mm average rainfall

Malay, Chinese, English, Tamil, Itan Dusan, Bajau and others

Metric system with gradual conversion from UK (imperial) system. Localmeasures include:

1 pikul=25 gantang=60.48 kg1 koyan=40 pikul=2.419 tonnes

Malaysian dollar or ringgit (M$, or RM)=100 sen (cents). Average exchangerates in 2000: M$3.8:US$1 (pegged at that rate on September 2nd 1998);M$5.76:£1. Exchange rates on September 6th 2001: M$3.8:US$1; M$5.52:£1

Peninsula: 7 hours ahead of GMT; Sabah and Sarawak: 8 hours ahead of GMT

January 24th-26th (Chinese New Year); March 6th (Hari Raya Haji); March26th (Islamic New Year); May 1st (Labour Day), 7th (Vesak Day); June 2nd(King’s birthday), 4th (Prophet Mohammed’s birthday); August 31st (NationalDay); November 14th (Deepavali); December 16th-18th (Hari Raya Puasa, endof Ramadan), 25th (Christmas Day)

Total area

Population

Main towns

Climate

Weather in Kuala Lumpur(altitude 39 metres)

Languages

Measures

Currency

Time

Public holidays (2001)

Malaysia 5

© The Economist Intelligence Unit Limited 2001 EIU Country Profile 2001

Political background

Fundamental to the understanding of Malaysia’s political development is anappreciation of its geographic, ethnic and cultural diversity. Political parties arelargely based on ethnicity, locality or religion. Basic themes of post-warpolitical history are the maintenance of racial harmony, positivediscrimination in favour of the bumiputera (“sons of the soil”, the ethnicMalays and other indigenous peoples), and friction between Islamic parties andthe government. Since independence in 1957, Malaysia has been ruled bycoalition governments, dominated by the principal Malay party, the UnitedMalays National Organisation (UMNO). Since 1981 the prime minister hasbeen Dr Mahathir Mohamad.

Historical development

The Malay peninsula came under British influence after the East IndiaCompany obtained the island of Penang as a trading settlement in 1786 andbecame the dominant force in the following century. Malacca and Singapore—founded in 1819 by Stamford Raffles—were ruled directly with Penang as theStraits Settlements. Treaties of protection were extended to Selangor, Perak,Negeri Sembilan and Pahang, which became the Federated Malay States in1895. The remaining five peninsular states—Kedah, Perlis, Kelantan,Terengganu and Johor—came under British control in the first two decades ofthe twentieth century as the Unfederated Malay States. Internal governmentremained largely under the control of the traditional rulers, particularly in thefour so-called Unfederated Malay States. The colonial administrationencouraged (and sponsored) immigrants from southern China and southernIndia, whose employment in the tin mines and on the plantations speeded thetransition from a trading outpost to a commodity producer.

The Second World War was a watershed, shattering the myth of whitesuperiority. The Japanese occupation of Malaya was followed by chaos,lawlessness and the emergence of Malay nationalism. The newly restoredBritish colonial system favoured Malayan social and economic advancement,and sought to create a more integrated territory and a stronger centralgovernment. The new Malayan Union soon collapsed and a guerrilla war wasstarted by the (largely ethnic Chinese) Malayan Communist Party (MCP),leading to the declaration of the Emergency in 1948. Rapid progress to fullindependence and the establishment of democracy in a pluralist society werepart of the anti-insurgency strategy. Independence was proclaimed in 1957.British policy helped to shape Malaysia, by expanding the peninsula-basedfederation in 1963 to include the two former British-ruled areas in northernBorneo, Sarawak and Sabah, along with Singapore, which withdrew from thefederation in 1965. The 1969 general election led to serious racial riots, inwhich many Chinese were killed. In the political crisis that followed, theAlliance, which had ruled since independence and consisted of UMNO, theMalaysian Chinese Association (MCA) and the Malaysian Indian Congress(MIC), was replaced by a broader-based coalition, the Barisan Nasional (BN,

Malaya comes under Britishinfluence

Malaysia is created

6 Malaysia

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

National Front). With minor changes in its composition, the BN has ruledMalaysia ever since.

The bumiputera account for 63% of the population, and have dominated thepolitical system since independence. The electoral system makes support in theMalay-dominated rural areas crucial for political success at the national level.In Sabah and Sarawak indigenous minorities retain similar traditional politicallinks. At the 1999 general election, UMNO lost a substantial part of the Malayvote, resulting in an even split between UMNO on the one hand and theopposition parties Parti Islam sa-Malaysia (PAS) and Parti Keadilan Nasional(PKN) on the other.

The ethnic Chinese, who constitute 24% of the population, enjoy greatereconomic power than the Malays, are largely urbanised, and form a higherproportion of the population in Malaysia than in other South-east Asiancountries (apart from the special case of Singapore). Chinese voters havetended to divide along class lines familiar in industrialised countries, somesupporting Chinese right-of-centre parties in the government coalition, such asthe MCA, and others left-of-centre opposition parties, such as the DemocraticAction Party (DAP). At the 1999 general election, the continued allegiance of amajority of the Chinese electorate helped to keep the BN in power with a two-thirds majority.

Indians, who make up 7% of the population, mostly vote along ethnic lines,expressed through the MIC, a member of the BN.

After the 1969 riots, the BN government instituted the 20-year New EconomicPolicy (NEP), a programme of positive discrimination aimed at reducinginterracial tensions by improving the incomes and economic power of thebumiputera. The National Development Policy (NDP), which followed the NEPafter 1990, relaxed some of the positive discrimination measures that favourthe bumiputera. An extended period of strong economic growth—at least until1998—made it possible to raise the status of the bumiputera withouttransferring wealth from the ethnic Chinese, thereby avoiding seriousintercommunal conflict.

The BN has capitalised on the considerable advantages of incumbency tomaintain its dominance of the political landscape. Ostensibly in the interestsof public order, it has tended to keep formal election campaigns short,discouraged rallies and threatened to use sweeping powers of detention againstopponents. It won two-thirds of the votes cast and 162 of the 192 seats in thelower chamber, the Dewan Rakyat, in the 1995 general election. Federal andstate parliamentary elections held on November 29th 1999 saw the BN’s shareof the overall vote fall to 56.4%, from 65.9% in 1995, although it retained atwo-thirds majority in the national assembly.

Ethnicity and politicalparties

The New Economic Policy

Incumbency benefitsthe BN

Malaysia 7

© The Economist Intelligence Unit Limited 2001 EIU Country Profile 2001

Recent election results(no. of seats)

1990 1995 1999

Barisan Nasional (BN) 127 162 148 United Malays National Organisation (UMNO) 71 88 72 Malaysian Chinese Association (MCA) 18 30 28 Parti Pesaka Bumiputera Bersatu (PPBB) 10 13 10 Malaysian Indian Congress (MIC) 6 6 7 Gerakan Rakyat Malaysia 5 7 7 Sarawak United People’s Party (SUPP) 4 6 7 Parti Bangsa Dayak Sarawak (PBDS) 4 4 6 Sarawak National Party (SNAP) 3 4 4 United Sabah National Org (USNO) 6 4 3 Sabah Progressive Party (SPP) 0 0 2 Liberal Democrat Party (LDP) 0 0 1 BN Direct 0 0 1

Barisan Alternatif (BA, Alternative Front)a – – 42 Parti Islam sa-Malaysia (PAS) 7 7 27 Democratic Action Party (DAP) 20 9 10 Parti Keadilan Nasional (PKN) – – 5

Parti Bersatu Sabah (PBS) 14 8 3

Parti Melayu Semangat ‘46 (S46)b 8 6 –

Others 4 0 0

Total 180 192 193

a The 1999 election was the first that the BA contested as a coalition. b Part of UMNO in 1986,broke away in 1987, returned in 1996.

Source: Election Commission.

The major reason for the BN losses in the 1999 elections was a split in theethnic Malay vote. The 1997-98 Asian economic crisis had exposed corruptionwithin UMNO and raised a desire for reform and a change of leadership,especially among younger UMNO politicians. The deputy prime minister,Anwar Ibrahim, who became the focal point of the reformasi movement, wasdismissed from the government in September 1998, expelled from UMNO, andcharged with obstruction of justice and sodomy; on the first count, Mr Anwarwas sentenced to six years in jail. The dubious treatment of Dr Mahathir’s long-standing heir apparent, his severe beating in police custody and his contro-versial trial unleashed a vigorous campaign for political reform that revitalisedthe opposition. UMNO’s share of the vote declined in the 1999 election from39.4% to 31.8%, while its representation in the lower house dropped to 72from what had in effect been 94 seats (including the six seats held by PartyMelayu Semangat ’46, which rejoined UMNO in 1996). The main beneficiarywas the Malay-based opposition party, PAS. It took 27 seats in the lower house,up from seven, wrested control of the Terengganu state parliament whileretaining neighbouring Kelantan, and made strong inroads in other northernMalay-belt states, including Dr Mahathir’s native Kedah.

Divisions within the Malay community are potentially seriously destabilising,with negative implications for race relations and the economic outlook. Thedivisions frequently focus on Dr Mahathir’s personality, his intransigence

The campaign forpolitical reform

Doubtful political stability

8 Malaysia

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

and reluctance to give up the position of prime minister; in theory, at least,the transition is secure—the deputy prime minister, Abdullah Badawi, isDr Mahathir’s anointed successor. A smooth succession could possibly befollowed by a continuation of the status quo, with only minor reforms.However, the real divisions go deeper and relate to conflicts, left unresolvedsince the formation of Malaysia, about the nature and inclusiveness ofMalaysian society. Dr Mahathir has tightly controlled political life, especiallyin recent years; his departure could destabilise UMNO’s system of politicalcontrol and open up fundamental social and political conflicts. Furtherdestabilising influences could come from a deteriorating economy, reducingUMNO’s ability to offer patronage, and from a more assertive judiciary,preventing the government from asserting control. The opposition alliance,the Barisan Alternatif (BA, Alternative Front), is divided, being dominated byPAS, with its two main partners, the DAP and the PKN objecting to thesocially divisive intention of PAS to found an Islamic state, should the BAwin the next general election.

Important recent events

May 1997: Dr Mahathir appoints Mr Anwar as acting prime minister andacting president of the United Malays National Organisation (UMNO) duringhis absence. Mr Anwar’s brief stewardship is distinguished by a campaignagainst official corruption, which is unprecedented in its severity.

September 1997: Dr Mahathir dismisses as “ridiculous” allegations of sexualmisconduct made against Mr Anwar. The deputy prime minister characterisesthe accusations as a “declaration of war” by unnamed UMNO membersworried by his anti-corruption drive.

June 1998: Dr Mahathir uses UMNO’s annual general assembly to quashmounting criticism of his leadership by Anwar loyalists, revealing that some ofthem have benefited from official largesse. Mr Anwar is made all but redundantas finance minister by the recall of Daim Zainuddin as special functionsminister in charge of “economic development”.

September 1998: Mr Anwar is sacked from the government and expelledfrom UMNO. After leading a series of anti-Mahathir rallies he is arrested,beaten in custody and indicted on charges of obstructing justice andof sodomy.

April 1999: Following a five-month trial, Mr Anwar is controversiallyconvicted of obstruction of justice and sentenced to six years in jail, triggeringdemonstrations by his supporters and criticism by foreign governments.

November 1999: The ruling BN coalition wins the general election,controlling more than two-thirds of the seats in the national parliament, butnonetheless has a reduced mandate. The BN loses a second state assembly—Terengganu—to the opposition Parti Islam sa-Malaysia.

November 2000: The ruling coalition suffers a humiliating defeat in a by-election in the Lunas constituency in Dr Mahathir’s native Kedah state, a seatthat the BN had held since independence.

Malaysia 9

© The Economist Intelligence Unit Limited 2001 EIU Country Profile 2001

January 2001: A new chief justice, Dzaiddin Abdullah, is appointed with areputation for independence and incorruptibility. Mr Dzaiddin’s agenda is toclean up the image of the judiciary, tarnished by compliance with thegovernment. After Mr Dzaiddin’s appointment, the judiciary increasinglyrefuses to bow to the authorities.

June 2001: Daim Zainuddin, finance minister and confidant of Dr Mahathir,resigns, as the prime minister embarks on a campaign against corruption inUMNO and cronyism, in order to revive the party’s fortunes. Mr Daim was themastermind behind Malaysia’s recovery after the 1997 Asian financial crisisand was responsible for the bailing out of politically well connected businesses.

July 2001: Mr Anwar launches an appeal against his sentence for sodomy. Theappointment of Mr Dzaiddin as the new chief justice has increased his chancesof a successful appeal.

Constitution, institutions and administration

Malaysia is a federal, constitutional monarchy within the Commonwealth. Theposition of king (yang di-pertuan agong, meaning “supreme ruler”) is rotatedevery five years. The nine-strong Conference of Rulers of the states of thepeninsula, excluding Malacca and Penang (the sultans of Kedah, Perak, Johor,Selangor, Pahang, Terengganu and Kelantan; the yang di-pertuan besar, orsupreme minister, of Negeri Sembilan; and the raja of Perlis) elects one of itsnumber to serve as king.

The powers granted to the traditional rulers on independence have beenmodified. Rulers and their families have in the past been accused by UMNOparty members of abusing their power for private gain and exceeding theirconstitutional authority. In 1992 UMNO drew up a code of conduct forrulers. After some alterations, a compromise was eventually reached inFebruary 1993, and constitutional amendments were passed that limitedrulers’ personal legal immunity.

The federal parliament consists of an upper chamber, the Senate or DewanNegara (Council of the Nation), of 68 members, of whom 42 members areappointed by the king and 13 pairs are elected by the state legislatures, and alower chamber, the House of Representatives or Dewan Rakyat (Council of thePeople), directly elected by universal suffrage. The number of seats in theDewan Rakyat was increased from 180 to 192 before the 1995 general election,and to 193 in 1999. The lower house has long been a rubber stamp for the BN,with little real debate on draft legislation or issues taking place there.

Each of the 13 states has an Executive Council dealing with non-federalmatters under a menteri besar (chief minister) who is answerable to elected stateassemblies. The constitutional head of each state government is either one ofthe traditional rulers or (in Penang, Malacca, Sabah and Sarawak) a stategovernor appointed by the king, on the advice of the federal government.

A federal constitutionalmonarchy

The federal parliament

The states’ ExecutiveCouncils

10 Malaysia

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

The Malaysian judicial system still resembles the UK system inherited from thecolonial period. As with the traditional rulers, the government has establisheda code of conduct for judges, the breaching of which may result in dismissal.Important changes have taken place in recent years, including the abolition ofthe jury system in 1995, tending to increase the power of the executive andreduce the scope for independent action by the judiciary. The appointment inJanuary 2001 of a new chief justice, Dzaiddin Abdullah, has lifted expectationsthat the judiciary will reassert its independence.

Political forces

UMNO, the party of Malay nationalists in the colonial period, remains themost important of the Malay parties, although it has lost support, attractingonly just over half of the total Malay vote in the 1999 election. The presidentof UMNO invariably serves as the prime minister. Elections to leading partyposts and to the UMNO supreme council determine the leadership successionand can also affect the posts occupied by ministers in the cabinet. Anincumbent leader is rarely challenged, but Dr Mahathir was almost defeated inthe internal UMNO elections of April 1987.

PAS thrives as a haven for Malay protest votes. But the party has yet to clarifythe role of Islam in its manifesto if it intends to present itself—and the BA—asa viable alternative for those voters dissatisfied with UMNO but suspicious ofplans to transform Malaysia into a theocracy. It is unlikely that PAS could wrestpower from UMNO with an austere Islamist agenda.

At the time of independence, the MCA was the acknowledged politicalrepresentative of the ethnic Chinese. It quickly became an apologist for thegovernment coalition in which it served, and was identified with the richerChinese and business interests. It is the second largest party in the BN afterUMNO but its leadership succession is proving a divisive issue. The party’s nextleader will be decided in the next triennial party elections, due in mid-2002.Gerakan Rakyat, founded as a left-of-centre multiracial party, and the DAP, alsoa multiracial party but further to the left, both mainly attract ethnic Chinesevoters (although the DAP also has prominent Indian and Malay members).

One of the features of political activity in the past was the open and directparticipation by coalition parties in entrepreneurial activities and companyownership as a means of obtaining party funds. UMNO, the biggest party(open since 1992 to other bumiputera besides Malays, and with a totalmembership of more than 2m), had the biggest portfolio of businesses. Theseactivities were criticised for putting temptation in the way of bothbusinessmen and politicians. They were officially wound down, but the shareswere transferred to “safe hands”—in practice, groups or individuals with closelinks to influential party members. UMNO’s major business interest is theconglomerate, Renong, which was taken back into government ownership inJuly 2001 after it failed to solve its debt problems. The MCA was also engagedin business activities grouped under a holding company, Multi-Purpose

Changes to the judicialsystem

UMNO is the dominantMalay party

UMNO’s corporate links

Chinese and multiracialparties

PAS tackles its Islamistagenda

Malaysia 11

© The Economist Intelligence Unit Limited 2001 EIU Country Profile 2001

Holdings (MPH). It has been less successful than UMNO in retaining influenceover management after disposing of its shares in these companies.

Key political figures

Mahathir Mohamad: Prime minister and president of the United MalaysNational Organisation (UMNO). In July 2001 he became Asia’s longest-servingelected ruler when he celebrated 20 years in office. He is the architect of boththe economic advance of the Malay community and the rapid industrialgrowth of Malaysia. His popularity has been in decline since the 1997 Asianeconomic crisis, a trend that accelerated with the ouster in September 1998 ofAnwar Ibrahim, his deputy in the party and government, and the campaign forchange that it triggered. He was returned unopposed in May 2000 for anotherthree-year term as UMNO president. Dr Mahathir has said that he will notstand for parliament in the next general election, due by 2004, but shows nosign of yielding power before then.

Abdullah Ahmad Badawi: Deputy president of UMNO and deputy primeminister. He is one of Dr Mahathir’s most trusted aides and first in line tosucceed him. He is an affable but unassuming personality, and many stillquestion his ability to unite the BN if he does assume power.

Anwar Ibrahim: Dr Mahathir’s former deputy in UMNO and former deputyprime minister. He is appealing against his controversial 15-year sentence forabuse of power and sodomy. His detention has inspired the reformistmovements prepared openly to question Dr Mahathir’s dominance of theestablished order. It is possible that the Federal Court will overturn hisconviction, thereby paving the way for a comeback to the political arena.

Najib Tun Razak: UMNO’s senior vice-president, defence minister and sonof a former prime minister, Tun Razak. He is popular, has a reputation forputting the party’s interests before his own interests and holds a strong thirdplace in the UMNO hierarchy. He also has ambitions to succeed Dr Mahathir.

Abdul Hadi Awang: The chief minister of the hydrocarbon-rich north-eastern peninsular state of Terengganu which fell to the opposition PartiIslam sa-Malaysia in the November 1999 poll. Mr Awang leads the effortsof PAS to broaden its appeal to non-Muslims and will remain atloggerheads with UMNO.

Dzaiddin Abdullah: Malaysia’s new chief justice. He is at the forefront ofefforts to clean up the image of the judiciary, tarnished by frequentallegations of corruption and political interference. Since Mr Dzaiddin’sappointment in December 2000, the judiciary has increasingly refused tobow to the authorities.

International relations and defence

Malaysia has always been active in a number of international bodies, andunder Dr Mahathir the country has adopted highly vocal positions on anumber of international questions. Dr Mahathir has also been noted for hisrefusal to heed criticism of his government’s human-rights record and for his

Dr Mahathir’s world view

12 Malaysia

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

readiness to disparage press freedom and the more open democratic practicesof the US and Europe. On the economic front, Dr Mahathir has characterisedmany international initiatives on trade union rights and on environmentalprotection as measures devised by the rich, developed countries to obstruct thedevelopment of newly industrialising countries.

Dr Mahathir continues to attack foreigners for allegedly trying to topple hisgovernment and wages war against foreign multinationals for preying on weakMalaysian firms. He blamed the Asian financial crisis, triggered in mid-1997 bythe large-scale sell-off of regional currencies and stocks, on Western“speculators”, and launched an outspoken campaign for the establishment ofsome degree of international supervision of short-term capital flows. Hecriticised the austerity-based remedies advocated by the InternationalMonetary Fund (IMF), an organisation that he dismissed as little more than anexecutor of policies framed by the US government, of which he is alsoincreasingly critical. Malaysia has called for the creation of a regional monetaryfund for Asia. In April 2001 “ASEAN+3”, the ten countries of the Association ofSouth-East Asian Nations (ASEAN) and Japan, China and South Korea, agreedto set up a network of currency swap arrangements that link the disbursementof short-term liquidity to IMF conditions. Malaysia is proposing to develop thiscurrency swap scheme further and strengthen financial co-operation amongAsian countries.

Relations with neighbouring Singapore remain sensitive, and Malaysia isconcerned about the situation in Indonesia, a major source of illegalimmigration and air pollution from forest fires. It has border disagreementswith Indonesia and the Philippines, and it is resisting China’s claims in theSouth China Sea. Malaysia was a founder-member of ASEAN and also amember of the broader but more loose-knit Asia-Pacific EconomicCo-operation (APEC) forum. In 1991 Dr Mahathir proposed setting up anotherregional body, the East Asian Economic Group, later renamed the East AsianEconomic Caucus (EAEC), to strengthen the negotiating power of Asianeconomies vis-à-vis such blocs as the EU and the North American Free-TradeAgreement (NAFTA). The government remains wary of the potentially negativeimpact on local businesses of global and regional trade pacts. In May 2000 thegovernment controversially succeeded in persuading its ASEAN counterparts toallow Malaysia to defer until 2005 the scheduled reduction in duties on motorvehicles produced elsewhere in the ASEAN area. This move could harm theplanned creation of an ASEAN Free-Trade Area (AFTA) by 2003.

The government has allocated M$10.7bn (US$2.8bn) to the Ministry ofDefence under the Eighth Malaysia Plan, which runs to end-2005. Under a15-year strategic plan, Malaysia’s armed forces, which at present mainly servein an anti-insurgency capacity, will develop a full capability to deter externalthreats. Malaysia has bilateral defence and military training agreements withthe UK, Australia and New Zealand, but remains a member of the Non-aligned Movement.

ASEAN, APEC and theproposed EAEC

Defence spending remainshigh

Malaysia 13

© The Economist Intelligence Unit Limited 2001 EIU Country Profile 2001

Security risk in Malaysia

The security risk to foreign companies operating in Malaysia is low but hasincreased over the past twelve months. It finds its origin in the widespreadfrustration with the government, which has blocked most traditional means ofprotest through censorship, libel suits, tight controls on demonstrations and—until recently—an unquestioned control of the judiciary. The governmentcontinues to wield the draconian Internal Security Act (ISA), which allows forindefinite detention without trial. The opposition’s frustration is made worseby the seemingly endless duration of the reign of the 76-year-old Dr Mahathir,who in July 2001 celebrated his twentieth year in office, and shows no sign ofwanting to retire.

Social unrest: The major risk to business comes from the return of economicand political conditions which are conducive to the outbreak of racial violence.Tensions persist below the surface between the majority Malays on the onehand and the minority ethnic Chinese and Indian populations on the other. Inthe most serious post-war racial conflict in 1969, divisions within the Malaymajority led to the scapegoating of the ethnic Chinese, hundreds of whomwere killed in riots. The Malay majority is once again split, but this time theeconomy is also turning down, which could cause many Malays to lose theirjobs. Racial tensions are not just below the surface. In a never explainedincident early in 2001 a number of ethnic Indians were killed during a riot inKuala Lumpur. However, given the tight controls by the government, the near-term risk of large-scale racial violence appears quite low.

There is no immediate risk of a return of the large-scale demonstrationsagainst the government and the ruling United Malays National Organisationthat last took place in 1998, when the deposed deputy prime minister, AnwarIbrahim, led reformasi (“reform”) demonstrations. However, unrest is likely torise should Mr Anwar be successful in one or more of his several appealsagainst his convictions.

There is widespread awareness within Malaysia that it is heavily dependent onforeign direct investment. The opposition is unlikely specifically to targetforeign businesses.

Armed conflict: The risk of armed conflict affecting business is low. Reportsof—apparently large, Islamic-based—violence have increased over the pasttwelve months but it is unclear to what extent the incidents have been stagedby the government, in an attempt to compromise the main opposition party,PAS, by associating it with Islamic extremism. However, there are no “no-go”areas in Malaysia and the government remains clearly very much in control ofthe country.

Organised crime: Malaysia is, in general, a safe country. Violent crime,kidnapping and extortion are rare and organised crime is seldom a threat toforeign business. Foreigners are, however, often the target of pickpocketing,burglaries, car break-ins and purse-snatching.

14 Malaysia

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

Resources and infrastructure

Population

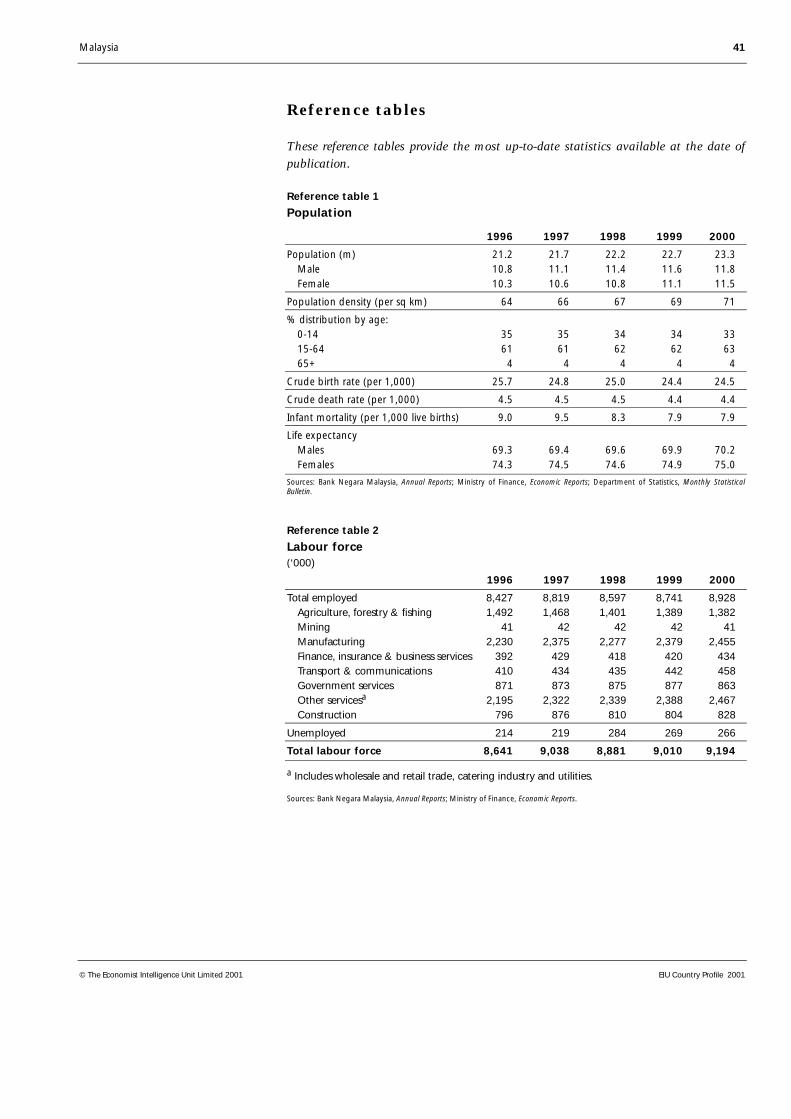

The Malaysian population is estimated to have reached 23.8m by mid-2001.The Eighth Malaysia Plan projects an annual average increase of 2.3% in2001-05; in 1996-2000 the annual average rate of growth was 2.4%. Around80% of the population lives in peninsular Malaysia. The rate of growth hasbeen the fastest in Malaysia’s more developed states, at 2.8% during1996-2000. The dependency ratio (those under the age of 15 and over the ageof 64 divided by the rest of the population) is expected to continue to decline,from 59.1% in 2000 to 55.3% in 2005, as the median age rises from 23.9 yearsto 25.3 years.

The average population density, at 70.6 persons per sq km in 2000, is relativelylow. However, there are wide disparities between the peninsula and the sparselypopulated Borneo states. The proportion of the population living in urbanareas stood at 61.8% in 2000, up from 55.1% in 1995. (Reference table 1provides historical data on population.)

Population, 2001(mid-year estimates)

‘000 %

Total 23,795 100.0Malaysian 22,529 94.7 Bumiputera 14,886 62.6 Malay 12,341 51.9 Other bumiputera 2,545 10.7 Chinese 5,720 24.0 Indian 1,671 7.0 Others 252 1.1Non-Malaysian 1,266 5.3

Age structure0-14 7,881 33.115-64 14,956 62.965+ 958 4.0Median age (years) 23.9 –

Source: Department of Statistics, Monthly Bulletin of Statistics.

Rates of population growth vary considerably between the main ethnic groups,probably owing to differences in geographical location, income levels andtraditions. In 1996-2000 the annual average rates of growth of the bumiputera(“sons of the soil”, ethnic Malays and other indigenous peoples), Chinese andIndian communities were 3.2%, 1.4% and 1.8%, respectively. The Chinese,long urbanised and enjoying higher average incomes, now have smallerfamilies; the Malay urban population is growing, but most families remain inrural areas.

Mean monthly gross household income increased from M$2,020 (US$532 atthe current pegged exchange rate of M$3.8:US$1) in 1995 to M$2,472 in 1999,

Growth rates vary betweenthe main ethnic groups

Fairly rapid populationgrowth

Malaysia 15

© The Economist Intelligence Unit Limited 2001 EIU Country Profile 2001

an average growth rate of 5.2% annually, according to official data. Theproportion of lower-income households, defined as those earnings betweenM$1,500 and M$3,000, increased from 32.3% in 1995 to 37% in 1999. Growthrates varied by ethnic group. The mean monthly income of Malay householdsexpanded by 5.5% annually to M$1,984, that of Chinese households by 4.6% ayear to M$3,456, and that of Indian households by 6.3% a year to M$2,702.The mean monthly income of urban households rose by 4.6% annually toM$3,103 in 1999, and that of rural households by 6.7% to M$1,718.

Slowing death and birth rates presage an increase in the proportion of thepopulation aged over 65 and a decline in the under-14 age group, as well as arise in the median age, accompanied by further urbanisation.

Education

The government places great emphasis on raising the general level ofeducational achievement. It provides universal education up to secondarylevel, and there is, in addition, a large number of private-sector schools andcolleges. The provision of state tertiary educational institutions has steadilyexpanded. Sending pupils abroad for study, a long tradition on the part of bothfamilies and the government, intensified during the boom years. The switch tothe use of Malay as the medium of instruction in all state secondary schoolsencouraged the trend. State assistance mostly takes the form of soft loans,repayable when students graduate and take paid employment. Under the termsof the New Economic Policy (NEP), almost all government assistance wasdirected towards the children of bumiputera. Owing to the recent economiccrisis, many of those studying overseas were brought home, increasing thepressure on local educational institutions. Tamil and Mandarin Chinesecontinue to be the languages of instruction in some primary schools. Thegovernment, disappointed with the failure of bumiputera students to qualify foruniversity places, announced in August 2001 that university entrance would bebased on merit henceforth.

Health

The public health system, with its emphasis on community-based care, haslong been internationally recognised as a model provider of quality services atlittle or no cost to consumers. As a result, Malaysia’s basic indicators comparefavourably with most other Asian countries. But there are geographicalvariations: health indicators for Sabah, Sarawak and some predominantly ruralstates on the Malayan peninsula are well below average.

Already low by regional standards, government spending on the health sectorfell from 3% of GDP in 1990 to 2.4% in 1998, reflecting the authorities’ desiregradually to reduce their role as a provider. But the Eighth Malaysia Plan,which covers 2001-05, has targeted government spending on heath atM$5.5bn (US$1.4bn), or 5% of the social sector development budget,representing a 47.3% increase over the M$3.7bn allocated in the SeventhMalaysia Plan.

A model system, albeit withregional disparities

Education given highpriority

16 Malaysia

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

While the Seventh Malaysia Plan (1996-2000) focused on an expansionarydevelopment programme that saw a strong increase in the numbers of newprivate hospitals and clinics, the Eighth Malaysia Plan aims for an overallimprovement in the quality of public health services with greater emphasis onthe use of information technology, improvements in the quality of healthpersonnel and upgrading rural facilities. A total of M$715m (US$188m) hasbeen allocated for rural and environmental health.

Natural resources and the environment

In the colonial period economic development was dominated by tin miningand the cultivation of natural rubber. Depletion of the richest, lowest-cost tindeposits, rising labour costs and a period of low tin prices combined to reducelocal production and end Malaysia’s dominant position as the world’s largestproducer of tin concentrates. However, it is still one of the world’s maincentres of tin refining, although it must supplement declining domestic mineoutput with imported concentrates.

Petroleum and natural gas are now more important mineral products. Both oiland natural gas are extracted from two main areas in the South China Sea, offTerengganu and off Sabah.

Malaysia is no longer the world’s biggest producer of natural rubber, itsdeclining output having been overtaken in 1993 by rising production inThailand and Indonesia. Plantation companies have for many years beenswitching to the more profitable cultivation of oil palm. Malaysia is the world’slargest producer of palm oil.

Malaysia remains the world’s leading producer of tropical sawlogs. For someyears its pre-eminence resulted partly from the flouting of controls on tree-felling by loggers. These controls are now being imposed more strictly andoutput has fallen. Bans on log exports were originally imposed as much toencourage more downstream processing as to preserve the Malaysianrainforest. Controls are now linked to replanting.

It has been the aim of successive Malaysian governments to raise earnings fromall primary products by increasing the degree of domestic processing. Thecountry now has large commodity-based industries: demand from rubbergoods manufacturers has reached the point where rubber must be imported,because falling domestic output is fully committed to trading contracts.

Minerals

Rubber and palm oil

Timber

Domestic processing

Malaysia 17

© The Economist Intelligence Unit Limited 2001 EIU Country Profile 2001

Transport, communications and the Internet

Malaysia’s physical infrastructure compares favourably with that of most othercountries in the region, having benefited from substantial investment—bothprivate and public—during the boom years. Between 1995 and 2000, the totalroad network increased from 61,380km to 65,880km. A slowdown in privateinvestment owing to the financial crisis was offset to some extent by increasedgovernment spending on roads in 1999 and 2000.

Malaysia has made considerable progress in the creation of a more integrated,efficient and reliable urban transport system, although the 1997-98 economicdownturn caused several rail projects to run into financial difficulties.

Rapid economic growth stimulated air traffic and led to the construction ofKuala Lumpur International Airport (KLIA), which opened in June 1998. TheM$9bn new airport, largely completed before the economic crisis struck, canhandle 25m passengers a year. But its distance from Kuala Lumpur as well as afall off in business and a reduction in the number of international carrierslanding at KLIA, have left it heavily underused.

More than 90% of Malaysia’s international trade is conducted throughseaports, which handled 220.8m tonnes in 2000, up from 152.3m tonnes in1995, largely because of a rise in containerised and liquid bulk cargo. A hugeexpansion is planned on the central west coast at Klang, as well as at TanjungPelepas in Johor, in order to compete with Singapore, which in 2000 stillhandled 24% of Malaysia’s international trade. (Reference table 3 provides avariety of transport indicators.)

The monopoly of Telekom Malaysia, which is largely state-owned, over theprovision of fixed-line and cellular services ended in 1994 with the licensing ofseveral competitors. However, Telekom remains the dominant provider offixed-line services; in 2000 there were 21 fixed-line telephones for every 100people. The newcomers have tended to concentrate on mobile telephony,raising the number of subscribers from 872,000 in 1995 to 5.1m in 2000. Theensuing competition has brought lower tariffs and improved service quality.

The development of information and communications technology (ICT) playsa crucial role in the government’s plans for the economy. ICT usage, measuredin terms of installed personal computers, rose from 29.5 per 1,000 head ofpopulation in 1995 to 95.7 in 2000. The number of Internet subscribersincreased from 13,000 in 1995 to about 1.7m in December 2000. There werefive Internet service providers in Malaysia in 2001. The government activelypromotes electronic services but keeps a wary eye on the Internet, fearinguncensored criticism.

Large investments ininfrastructure

A new internationalairport

Port capacity continuesto expand

Telecommunications

The Internet

18 Malaysia

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

Energy provision

Malaysia is well endowed with energy resources. It is a net exporter of oil andgas, which are extracted from beneath the South China Sea. Receptioninstallations in Terengganu handle the oil and gas extracted from fields east ofthe peninsula; other fields are located north of Sarawak and around the coastof Sabah. Coal is mined in Sarawak, and the high rainfall and ruggedtopography of both peninsular Malaysia and Sabah and Sarawak provideextensive scope for hydroelectric power, still largely to be exploited.

Energy balance, 2000(m tonnes oil equivalent)

Oil Gas Coal Electricitya Other Total

Primary supplyProduction 37.5 40.0 0.1 1.2b 2.4 81.2Imports 16.0 0.0 1.2 0.0 0.0 17.2Exports –28.5 –20.5 0.0 0.0 0.0 –49.0Stock change 0.0 0.0 0.0 0.0 0.0 0.0Total 25.0 19.5 1.3 1.2b 2.4 49.4

0.4c 48.6

Processing & transformationInput to refining –20.0 0.0 0.0 0.0 0.0 –20.0Input to transformation –4.0 –12.0 –0.4 –1.2b 0.0 –17.6Refining/transformation output 20.0 0.0 0.0 6.0c 0.0 26.0Energy industry fuel/loss –2.5 –5.0 0.0 –0.5c –1.0 –9.0Final consumptionTransport fuels 10.7 – 0.0 0.0 0.0 10.7Industrial fuels 5.5 1.5 0.9 2.7c 0.1 10.7Residential fuels 1.5 – – 2.8c 1.3 5.6Non-energy uses 0.8 1.0 0.0 0.0 0.0 1.8Total 18.5 2.5 0.9 5.5c 1.4 28.8

a Primary electricity output and imports and exports of electricity are expressed as input equivalents on an assumed generating efficiency of 33%.b Input basis. c Output basis.

Source: Energy Data Associates.

Rapid industrial development boosted demand for electricity significantly, andthe resulting supply shortfall led the government in the early 1990s to awardcontracts to private consortia, known as independent power providers (IPPs),to build and operate thermal generating plants to supply the national grid.The IPPs produced 37% of Malaysia’s electricity in 2000. Malaysia’s reservemargin—the difference between installed capacity and peak demand—remains large: by end-2000 the reserve margin stood at 32%. However, by 2005Tenaga Nasional, peninsular Malaysia’s main, predominantly state-ownedutility, and the IPPs are expected to raise installed capacity by 61% to meet ananticipated surge in demand. The government has revived the giant 2,400-mwBakun Hydroelectric Project on Borneo. (Reference table 4 provides nationalenergy statistics.)

The power industry readiesfor surge in demand

There are substantialenergy resources

Malaysia 19

© The Economist Intelligence Unit Limited 2001 EIU Country Profile 2001

The economy

Economic structure

Main economic indicators, 2000

GDP growth (%) 8.3

Consumer price inflation (av; %) 1.5

Gross national savings (% of GDP) 39.5

Current-account balance (US$ bn) 7.9

Total external debt (year-end estimate; US$ bn) 44.1

Exchange rate (av; M$:US$) 3.8

Population (m; mid-year estimate)a 23.8

a 2001.

Sources: Bank Negara Malaysia; official and EIU estimates.

In line with its vision of becoming a fully developed nation by 2020 Malaysiahas industrialised rapidly, transforming itself from an economy whoselivelihood relied primarily on the production of mineral and agriculturalexport commodities—palm oil, natural rubber, tropical timber and other minormineral and agricultural products—into an economy dominated bymanufacturing. The manufacturing sector continues to strengthen its positionas the leading contributor to GDP, increasing its share to 34.3% in 2000, from31.5% in 1999.

Malaysia plays a leading role in the world markets for some of its commodities.It is still an important source of rubber and is the dominant world producer ofpalm oil. Palm oil output reached a record 10.8m tonnes in 2000.

Manufactures account for 85% of gross export earnings. Electronic goods arethe single most important category, growing at a double-digit rate for most ofthe past 25 years, declining only in 1985 and probably also in 2001.Production is heavily dependent on imported parts. Government policy isaiming to raise the domestic content of exports. The strong export orientationof the electronics industry has made it highly vulnerable to fluctuations inglobal demand.

Malaysia’s rapid growth over the last 20 years has been financed and sustainedby high domestic savings and by large inflows of foreign direct investment(FDI). These inflows reached a peak of 8.7% of GDP in 1992-93, but have sincestabilised, standing at 4.9% of GDP in 2000. A large but declining part of theFDI inflow is channelled into manufacturing, which in 1998-2000 accountedfor 43% of FDI inflows, with 35% taken by the services sector. Malaysia ishoping to attract investment in higher knowledge content industries in linewith its ambitions to become a knowledge-based economy.

High rate of capitalinvestment

Electronics productiondominates

Manufacturing is thelargest sector

20 Malaysia

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

Comparative economic indicators, 2000

Malaysia Thailand Singapore Indonesia US

GDP (US$ bn) 89.3 121.9 91.4 153 9,873

GDP per head (US$) 3,841 1,954 22,753 721 35,032

Consumer price inflation (av; %) 1.5 1.6 1.4 3.7 3.4

Current-account balance (US$ bn) 7.9 9.2 21.8 7.7 –435.4 % of GDP 8.8 7.5 23.9 5.0 –4.4

Exports of goods fob (US$ bn) 98.1 67.9 138.9 62.5 775.7

Imports of goods fob (US$ bn) 77.6 56.2 127.5 37.4 1,222.8

External debt (US$ bn) 44.1 80.5 9.7 142.6 n/a

Debt-service ratio, paid (%) 5.2 18.4 1.9 28.9 n/a

Source: EIU, CountryData.

Economic policy

Fiscal policy tends to be prudent, with revenue during the boom yearsoutstripping current outlays and, for much of the 1990s, developmentspending as well. (See Reference table 5 for historical data on governmentfinances.) For the past four years, however, the government has followed astimulative fiscal policy, initially to aid economic recovery from the regionalfinancial crisis and, later on, to limit the impact of the global slowdown on thedomestic economy. The budget went into deficit in 1998. The 2001 budgetforecasts a deficit of M$16.1bn (US$4.2bn). Slower revenue growth is likely towiden that deficit. In March 2001 the government unveiled a fiscal package,which included M$3bn of additional public works expenditure; the economywill probably feel the impact in 2002. Further fiscal stimulative measures toboost private investment and attract foreign direct investment are to beexpected in the 2002 budget, to be announced in October.

Government finances, 2000a

% changeM$ bn year on year

Revenue 63.5 8.2 Tax revenue 48.5 7.3 Direct taxes 29.8 10.4 Indirect taxes 18.7 2.7 Non-tax revenue 15.0 11.1

Expenditure 75.2 10.3 Operating 58.2 24.6 Development (net) 23.3 8.4

Balance –18.0b 89.5

a Estimated. b Includes loan recoveries.

Source: Ministry of Finance, Economic Report 2000/2001.

Monetary policy is accommodative, reinforcing the impact of the expansionaryfiscal measures. Further interest-rate cuts can be expected if economic activitydoes not pick up. (See Reference table 6 for data on money supply growth andReference table 7 for interest rates.) The Malaysian ringgit has been pegged to

Fiscal policy isgenerally prudent

Malaysia 21

© The Economist Intelligence Unit Limited 2001 EIU Country Profile 2001

the US dollar at M$3.80:US$1 since 1998; persistent dollar strength in thatperiod has meant that Malaysia has lost competitiveness, especially in relationto neighbouring economies. There is no indication that the government willwant to change the fixed currency regime but its determination might bechallenged if the regional economic slowdown were to drag on.

Official development strategies have been based on a series of five-year plans.In line with the objective of becoming a fully developed nation by 2020, thegovernment in April 2001 unveiled its Eighth Malaysia Plan (EMP), which aimsfor 7.5% growth in 2001-05. The structural shift towards high-end manu-facturing is expected to continue; manufacturing, agriculture and services areexpected to contribute 35.8%, 7% and 55.1%, respectively, to GDP by 2005.The EMP replaces the Seventh Malaysia Plan which ran from 1996-2000, whenannual average growth reached only 4.7%, well below the plan’s original targetof 8%. The new growth target will be difficult to achieve, given the plunge inelectronics exports in 2001, which raises longer-term concerns about the globaldemand for electronics products and Malaysia’s sustainable rate of economicgrowth. The government may find it impossible to make up for slow economicgrowth in the early years of the plan with faster growth later in 2004-05. Aswas the case in the earlier plan, the economic expansion is expected to bedriven by an upturn in private investment. The EMP aims for an average 19%annual rise in private investment, after contracting by 11.6% under theSeventh Malaysia Plan. Public investment is intended to grow by only 1.1%annually, while the public sector declines as a share of GDP and resumes itsrole as the facilitator of private-sector participation in the economy. Whileforeign investment will remain important, its share of total investment isexpected to decline, in part because of the expected global competition forforeign funds.

Malaysia’s five-year plans

Seventh Plan Eighth PlanTarget Outturn Target

Real GDP growth (%) 8.0 4.7 7.5

Inflation (av; %) 2.7 3.4 2.7

GNP per head (M$; end-period) 14,788 13,359 17,779

Unemployment (%) 2.8 3.1 2.7

General government balance (% of GNP) 1.5 1.5 1.5

Current-account balance (% of GNP) 0.5 6.5 3.9

Source: Economic Planning Unit, Eighth Malaysia Five-Year Plan (2001-2005).‘

The EMP, together with the Second Industrial Masterplan (1996-2005),emphasise the importance of strengthening the links between industries andproviding them with appropriate support, in particular through thedevelopment of human resources, physical infrastructure and other services.The EMP aims to achieve its growth targets by boosting productivity: accordingto the plan, 2.8 percentage points of the targeted average 7.5% annual GDPgrowth will come from an increase in total factor productivity. The moreefficient use of labour and capital will hinge on improving the quality and

Five-year plans

22 Malaysia

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

skills of the workforce, which the government may find difficult to achievewithin the plan period.

Federal government development allocation and expenditure by sector(M$ m)

Seventh Plan Eighth PlanAllocation Outturn Allocation

Economic 49,351.6 47,171.9 50,514.6 Agricultural development 8,286.9 8,139.3 7,860.0 Mineral resources development 46.1 40.8 50.0 Commerce & industry 12,208.8 11,257.8 10,295.4 Transport 21,677.7 20,826.2 21,818.9 Communications 51.3 47.0 146.5 Energy 2,544.0 2,543.6 2,601.6 Water resources 3,131.5 2,999.5 5,988.4 Feasibility study 299.3 264.9 131.0 Research & development 1,106.0 1,052.8 1,622.8

Social 32,156.0 31,284.0 37,518.1 Education & training 20,185.8 19,724.1 22,660.0 Health 3,737.1 3,725.5 5,500.0 Information & broadcasting 246.2 192.3 254.1 Housing 3,372.4 3,330.8 4,223.3 Culture, youth & sports 1,571.3 1,365.4 964.8 Local authorities & welfare services 1,624.9 1,565.1 2,972.6 Village & community development 1,350.4 1,318.5 943.3 Purchase of land 67.9 62.3 0.0

Security 12,747.6 11,644.0 10,750.0 Defence 10,293.9 9,539.3 8,750.0 Internal security 2,453.7 2,104.7 2,000.0

General administration 9,309.7 8,937.1 11,217.3

Total 103,564.9 99,037.0 110,000.0

Source: Economic Planning Unit, Eighth Malaysia Five-Year Plan (2001-2005).

The Malaysian way of dealing with the speculative capital flows and the sharpeconomic downturn in 1997-98, without the assistance of the InternationalMonetary Fund (IMF), has attracted a great deal of attention. Criticism of thecapital controls died down after Malaysia’s economic performance proved atleast as good as that of the regional economies that had sought the IMF’s help,and after the IMF grudgingly admitted that capital controls might, after all,have a role to play during a balance-of-payments crisis. Malaysia’s financialcrisis was triggered in mid-1997 by heavy selling of the ringgit and shares byforeign fund managers. It degenerated into a full-blown recession and led tothe imposition of capital and currency controls in September 1998 (see Theexternal sector: Foreign reserves and the exchange rate). Dr Mahathir justifiedthe controls because of what he called the “disastrous” failure of the freemarket. They were essentially designed to halt the speculative flight of capitalthat had battered the ringgit and share prices for more than a year.Accompanied by the fixing of the exchange rate at M$3.8:US$1, they alsoallowed for a further easing of interest rates without undermining the value ofthe ringgit. Official agencies used the breathing space afforded by the controlsto try to restore the overextended financial system to health—inter alia, vianon-performing loan carve-outs, the recapitalisation of banks and debt

Capital controls largelyabolished

Malaysia 23

© The Economist Intelligence Unit Limited 2001 EIU Country Profile 2001

reschedulings—but the government also bailed out many badly run but wellconnected corporations.

Public-sector development allocation(M$ m)

Seventh Plan Eighth PlanAllocation Outturn Allocation

Transport 20,913.1 20,484.2 21,222.1 Roadsa 12,429.9 12,269.5 14,002.6 Urban transport 404.2 404.0 705.6 Rail 5,450.3 5,450.3 4,081.0 Ports 1,157.4 1,089.2 1,500.0 Airports 1,471.3 1,271.2 932.9

Utilities 3,445.3 3,048.0 5,549.9 Water supply 2,776.8 2,382.7 3,966.3 Sewerage 668.5 665.3 1,583.6

Communications 51.0 39.6 228.0 Telecommunications & post 10.2 4.1 146.7 Meteorological services 40.8 35.5 81.3

Total 24,409.4 23,571.8 27,000.0

a Excludes localised roads in regional development areas, some local authorities and agriculturalroads.

Source: Economic Planning Unit, Eighth Malaysia Five-Year Plan (2001-2005).

Although the prime minister stated repeatedly that the capital and currencycontrols would remain in place until the international community tookconcrete steps to regulate such short-term flows—which has not takenplace—the controls have been largely dismantled. In May 2001 the 10% levyon the repatriation of profits from portfolio investments held for less thanone year—the last residual restriction on foreign investors—was abolished.Capital controls now exist for Malaysians only, but could easily and quicklybe restored during a crisis. The currency peg remains and offshore ringgittrade is still banned. Malaysia remains committed to the fixed exchange rate,despite criticism of its inflexibility and a loss of competitiveness owing to USdollar strength.

There are few indications that the government intends to revise its approachto failing, politically favoured businesses in the near future, despiteassurances that it will consult more closely with the public and will probemore closely the abilities of the companies involved in the controversialprivatisation initiative. The high-profile campaign of privatising governmentassets was launched in the 1980s with the explicit intention of promotingMalay interests by increasing the share of the nation’s corporate assets in thehands of bumiputera (ethnic Malays and other indigenous peoples). Criticshave said that many lucrative projects went to political favourites with littleindustry knowledge or expertise. The 1997-98 economic downturn showedup the weaknesses and the lack of managerial skills in many wellconnected companies.

Although many companies have been bailed out, the resolution of the baddebt problem has been difficult and slow, requiring additional government

Approach to privatisationunchanged

24 Malaysia

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

help at a later stage. The failure of the programme was highlighted by the buy-back, in December 2000, of a controlling 29% stake in the debt-ridden nationalcarrier, Malaysian Airline System (MAS), held by a former business associate ofthe finance minister, Daim Zainuddin, for M$1.79bn; at M$8 a share, this wasthree and a half times the MAS share price on the open market. Thegovernment’s decision, in August 2001, to take over the heavily indebtedRenong UEM may be a prelude to a takeover of the whole Renong group, oneof Malaysia’s largest companies, which has close relations with UMNO.

In January the government introduced a controversial self-assessment schemefor Malaysia-based corporate taxpayers. By removing the task from the InternalRevenue Board (IRB), the government aims to lift efficiency and accountingpractices. But business heads say that the legislation was put together tooquickly with little regard for the views of the 280,000 companies whichaccount for nearly half of the M$29bn collected annually by the IRB. Theyhave complained about the difficulty for the taxpayer in interpreting complextax legislation in the first place and the stiff penalties for those failing to do so,which mean that anyone responsible for submitting an incorrect return canface a jail term of up to three years. Dr Mahathir has hinted that thegovernment is likely to reduce the corporate tax rate, currently standing at28%, in the 2002 budget to be presented in October 2001. This rate is higherthan the levels prevailing in many other Asian countries, includingneighbouring Singapore. A reduction would enhance Malaysia’s com-petitiveness, but it is doubtful whether it would raise the rate of domesticinvestment to compensate for the expected drop in FDI flows.

Taxation policy in the coming years is expected to continue to favour low-income earners. The 2001 budget highlighted this with a number ofconcessions, including an increase in the annual rebate payable to individualtaxpayers from M$110 (US$29) to M$350 and raising the eligibility thresholdfrom M$10,000 (US$2,630) to M$35,000.

Economic performance

Malaysia suffered a brief recession in the mid-1980s and then enjoyed a periodof consistently fast growth until 1998, with the economic expansion driven bymanufacturing investment and exports. (Reference tables 8-10 provide data onMalaysia’s gross domestic product.) Malaysia’s dependence on exports,particularly electronics and electrical goods, which make up 62% of exports, hasmade economic growth vulnerable to global fluctuations in the demand forthese products. Malaysia has benefited from the surge in global demand forinformation and communication technology goods, which pulled its economyout of recession in 1999. However, during 2001 there was a savage downturn inthe global demand for investment goods, which resulted in a plunge in Malaysiaexports and a sharp fall in GDP growth for the second time this decade. Withother regional economies also weakening, no quick or strong recovery seemslikely in 2001 or 2002. Domestic demand will provide some support, but will beunable to compensate fully for the fall off in demand for exports.

Outlook depressed byelectronics sector

Changes to taxation policy

Malaysia 25

© The Economist Intelligence Unit Limited 2001 EIU Country Profile 2001

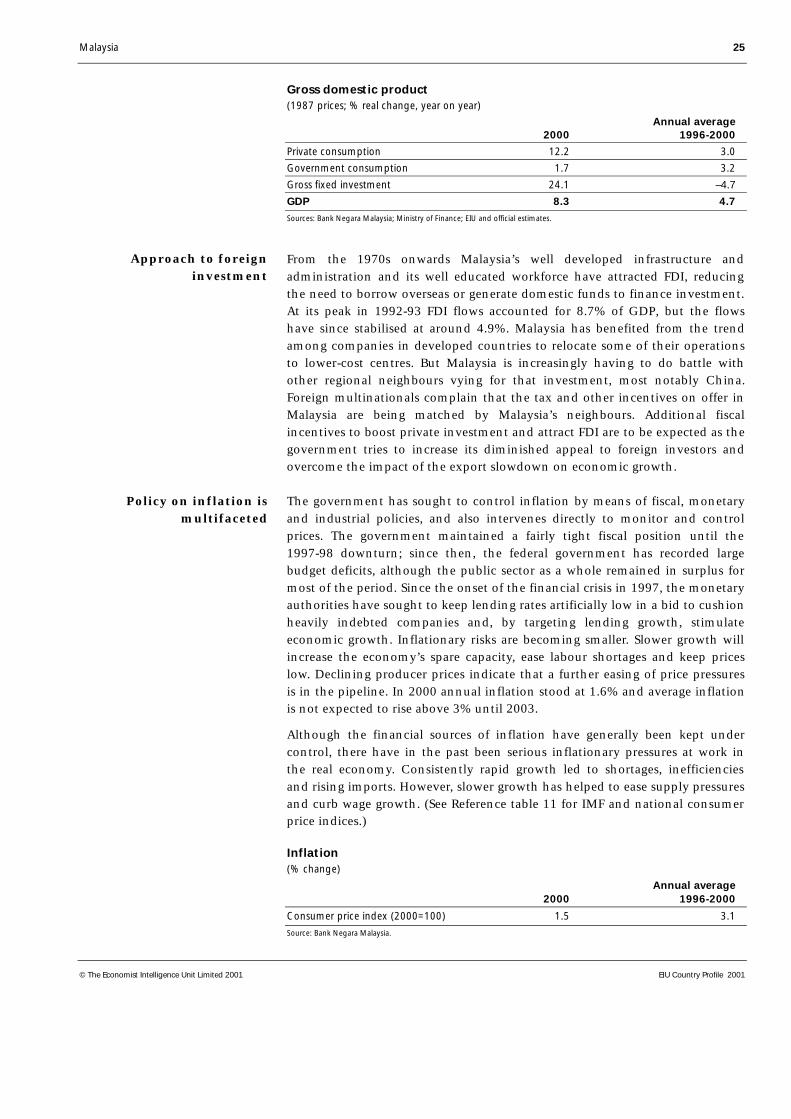

Gross domestic product(1987 prices; % real change, year on year)

Annual average2000 1996-2000

Private consumption 12.2 3.0

Government consumption 1.7 3.2

Gross fixed investment 24.1 –4.7

GDP 8.3 4.7

Sources: Bank Negara Malaysia; Ministry of Finance; EIU and official estimates.

From the 1970s onwards Malaysia’s well developed infrastructure andadministration and its well educated workforce have attracted FDI, reducingthe need to borrow overseas or generate domestic funds to finance investment.At its peak in 1992-93 FDI flows accounted for 8.7% of GDP, but the flowshave since stabilised at around 4.9%. Malaysia has benefited from the trendamong companies in developed countries to relocate some of their operationsto lower-cost centres. But Malaysia is increasingly having to do battle withother regional neighbours vying for that investment, most notably China.Foreign multinationals complain that the tax and other incentives on offer inMalaysia are being matched by Malaysia’s neighbours. Additional fiscalincentives to boost private investment and attract FDI are to be expected as thegovernment tries to increase its diminished appeal to foreign investors andovercome the impact of the export slowdown on economic growth.

The government has sought to control inflation by means of fiscal, monetaryand industrial policies, and also intervenes directly to monitor and controlprices. The government maintained a fairly tight fiscal position until the1997-98 downturn; since then, the federal government has recorded largebudget deficits, although the public sector as a whole remained in surplus formost of the period. Since the onset of the financial crisis in 1997, the monetaryauthorities have sought to keep lending rates artificially low in a bid to cushionheavily indebted companies and, by targeting lending growth, stimulateeconomic growth. Inflationary risks are becoming smaller. Slower growth willincrease the economy’s spare capacity, ease labour shortages and keep priceslow. Declining producer prices indicate that a further easing of price pressuresis in the pipeline. In 2000 annual inflation stood at 1.6% and average inflationis not expected to rise above 3% until 2003.

Although the financial sources of inflation have generally been kept undercontrol, there have in the past been serious inflationary pressures at work inthe real economy. Consistently rapid growth led to shortages, inefficienciesand rising imports. However, slower growth has helped to ease supply pressuresand curb wage growth. (See Reference table 11 for IMF and national consumerprice indices.)

Inflation(% change)

Annual average2000 1996-2000

Consumer price index (2000=100) 1.5 3.1

Source: Bank Negara Malaysia.

Policy on inflation ismultifaceted

Approach to foreigninvestment

26 Malaysia

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

The consumer price index (CPI) is the most widely cited measure of pricemovements. It is derived from a weighted average of the householdexpenditure patterns of five income groups and includes 430 items, of which20 are subject to price control. The 20 controlled items have a high weightingin the index.

By concentrating its attention on these items, the government has managedthe index and given the impression of controlling inflation. This policy ofcontrolling prices reduces the hardships caused to poorer households byinflation (and may, as a result, have a knock-on effect on wage rates among thelowest-paid workers), but both the policy and the CPI conceal rather thancombat underlying inflationary pressures.

Malaysia’s traditionally tight labour market has loosened as a result of theeconomic slowdown. Unemployment was only 2.7% in 1997 according to theDepartment of Statistics. It has since edged up, standing at 3.1% in 2000, after3.4% in 1999. In past downturns the government has responded byrepatriating large numbers of foreign workers.

Manufacturing sector wages(% change)

Annual average2000 1996-2000

Wages 4.6 4.7

Source: Bank Negara Malaysia.

As Malaysia moves to become a knowledge-based economy, one of the greatestchallenges is the need to equip workers with new skills. In 2000 productivityimprovements generally outpaced growth in real wages. (See Reference table 2for historical data on the labour force.)

Regional trends

Economic development is concentrated in the western states of the peninsula.After trading operations had been established in the Straits Settlements, tinmining and plantation developments began in Selangor, Perak and Johor—areas that, together with Penang, still have the largest concentrations ofmanufacturing industry. Penang and the Kelang Valley (in central Selangor,between Kuala Lumpur and the coast) are the main locations of export-oriented manufacturing. Penang’s customs-free industrial zones have been thefocus of investment by international electronics companies, while the KlangValley has the largest and longest-established concentration of generalmanufacturing operations.

Successive five-year plans have fostered the location of industrial projects innew areas, still mainly in states on the west of the peninsula (Kedah, NegeriSembilan and Malacca). In the predominantly rural states on the east coast ofthe peninsula (Kelantan, Terengganu and Pahang) and the two Borneo states(Sabah and Sarawak) industrial activity is mainly related to the processing oflocal raw materials. Timber processing has developed in all of these states.

A tight labour market

Imbalances in development

Malaysia 27

© The Economist Intelligence Unit Limited 2001 EIU Country Profile 2001

Primary oil and gas installations are necessarily located close to offshoresources. Terengganu on the east coast of the peninsula and Sabah on the islandof Borneo have reception units. Manufacturing operations using oil and gashave grown up around these primary industries, including petrochemicalfacilities in Terengganu and Pahang. Other primary industries have generatedsimilarly related manufacturing units: a tinplate production line in thesouthern state of Johor serves Malaysia’s main fruit-canning industry, forinstance. Production of plantation crops is widely dispersed among all states ofthe federation.

Kelantan is still dominated by agriculture. Rice and natural rubber account fortwo-thirds of the cultivated area. The state also produces 90% of domesticallygrown tobacco. There is substantial logging activity, but little local sawing andprocessing capacity. Income per head in Kelantan is the lowest and slowestgrowing in Malaysia.

Economic sectors

Agriculture, forestry and fisheries

In recent years the output of the agricultural, forestry and fisheries sectorstaken together has stagnated, and the relative importance of these rural-basedsectors within the economy as a whole has declined because of the rapidgrowth of the industrial and services sectors. (Reference table 12 gives historicaldata on agricultural and forestry production.)

The most important activities are subsistence or domestic food production(fisheries and the cultivation of rice being the most important subsectors),plantation crops for international markets, led by rubber, palm oil, cocoa, fruit,pepper and coconut oil, and timber.

Agriculture and forestry production, 2000(‘000 tonnes unless otherwise indicated)

Palm oil 10,839

Rubber 616

Sawlogs (‘000 cu metres) 23,898

Cocoa 70

Source: Bank Negara Malaysia, Annual Report.

Production of rice, once the dominant subsistence crop of Malay farmers, hasbeen threatened by the general drift to the towns, competing uses for land andcompetition for labour from the manufacturing industry. As a potent symbolof traditional Malay life, rice growing continues to attract special governmenthelp, such as schemes for raising yields and productivity. Malaysia is now a netimporter of rice. This is not a problem, however, because there are importantsurplus countries in the region—Thailand and Vietnam.

Rice

Agriculture is of decliningimportance

28 Malaysia

EIU Country Profile 2001 © The Economist Intelligence Unit Limited 2001

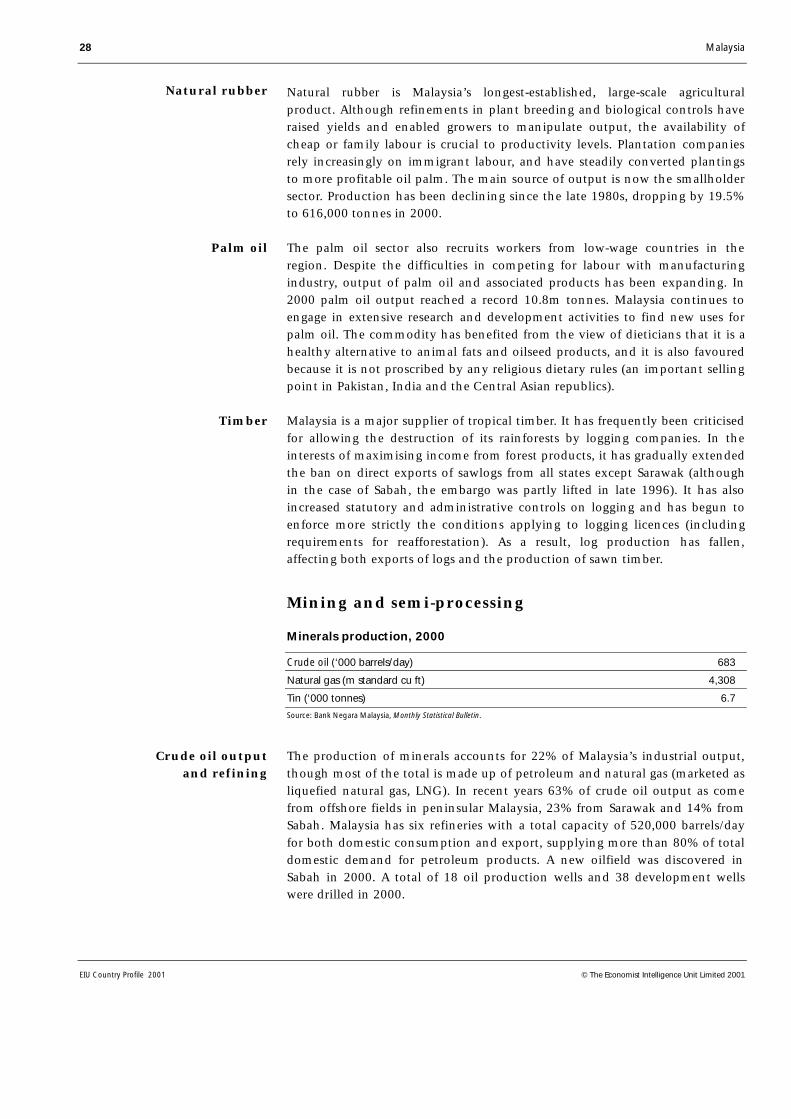

Natural rubber is Malaysia’s longest-established, large-scale agriculturalproduct. Although refinements in plant breeding and biological controls haveraised yields and enabled growers to manipulate output, the availability ofcheap or family labour is crucial to productivity levels. Plantation companiesrely increasingly on immigrant labour, and have steadily converted plantingsto more profitable oil palm. The main source of output is now the smallholdersector. Production has been declining since the late 1980s, dropping by 19.5%to 616,000 tonnes in 2000.

The palm oil sector also recruits workers from low-wage countries in theregion. Despite the difficulties in competing for labour with manufacturingindustry, output of palm oil and associated products has been expanding. In2000 palm oil output reached a record 10.8m tonnes. Malaysia continues toengage in extensive research and development activities to find new uses forpalm oil. The commodity has benefited from the view of dieticians that it is ahealthy alternative to animal fats and oilseed products, and it is also favouredbecause it is not proscribed by any religious dietary rules (an important sellingpoint in Pakistan, India and the Central Asian republics).

Malaysia is a major supplier of tropical timber. It has frequently been criticisedfor allowing the destruction of its rainforests by logging companies. In theinterests of maximising income from forest products, it has gradually extendedthe ban on direct exports of sawlogs from all states except Sarawak (althoughin the case of Sabah, the embargo was partly lifted in late 1996). It has alsoincreased statutory and administrative controls on logging and has begun toenforce more strictly the conditions applying to logging licences (includingrequirements for reafforestation). As a result, log production has fallen,affecting both exports of logs and the production of sawn timber.

Mining and semi-processing

Minerals production, 2000

Crude oil (‘000 barrels/day) 683

Natural gas (m standard cu ft) 4,308

Tin (‘000 tonnes) 6.7

Source: Bank Negara Malaysia, Monthly Statistical Bulletin.

The production of minerals accounts for 22% of Malaysia’s industrial output,though most of the total is made up of petroleum and natural gas (marketed asliquefied natural gas, LNG). In recent years 63% of crude oil output as comefrom offshore fields in peninsular Malaysia, 23% from Sarawak and 14% fromSabah. Malaysia has six refineries with a total capacity of 520,000 barrels/dayfor both domestic consumption and export, supplying more than 80% of totaldomestic demand for petroleum products. A new oilfield was discovered inSabah in 2000. A total of 18 oil production wells and 38 development wellswere drilled in 2000.

Natural rubber

Palm oil

Crude oil outputand refining

Timber

Malaysia 29

© The Economist Intelligence Unit Limited 2001 EIU Country Profile 2001

In contrast to the relative stability of crude oil output, production of naturalgas continues to grow. Between 1995 and 2000 production increased by 42%.In 2000 natural gas output rose by 13.3% in response to increased utilisationby the power generation sector and stronger demand from the manufacturingsector at home and higher demand for LNG in Japan and Taiwan. The increasein demand was partly met by the opening of a new gas field in Terengganu inFebruary 2000. Three new gas fields are expected to begin production in 2002,and a further five in 2003.

Malaysian output of tin concentrates reflects the precipitous decline inmining activity since the mid-1980s. The 6,686 tonnes of tin concentrateproduced in 2000 represent a year-on-year fall in output of 8.9% owing tothe closure of some tin mines during the year. There are now around 38 unitsof all types, compared with the 141 units in operation in 1990. Malaysia’sother main mineral operation is the Mamut copper mine in Sabah. Iron oreand bauxite ore are also mined. (Reference table 13 includes historical dataon minerals production.)

Manufacturing

When, over 20 years ago, the government set out to build up export-orientedmanufacturing capacity based on inward direct investment, there was already along history of investment in import-substitution industries and an establishedpolicy of developing industries based on increased internal processing ofoutput from domestic primary industries.

Manufacturing, 2000(%)

Output growth 25.0 Export-oriented 31.6 Domestic-oriented 17.2

Share of labour force 27.5

Share of total outstanding loans 16.4

Capacity utilisation 80.0

Source: Bank Negara Malaysia, Annual Report.