Macroeconomic Stability in the Aftermath of the … Stability in the Aftermath of the Financial...

22

Macroeconomic Stability in the Aftermath of the Financial Crisis Julio Velarde Governor Central Reserve Bank of Peru CEMLA - SEACEN, Punta del Este, November 2012 1

Transcript of Macroeconomic Stability in the Aftermath of the … Stability in the Aftermath of the Financial...

Macroeconomic Stability in the Aftermath of the Financial Crisis

Julio Velarde Governor

Central Reserve Bank of Peru

CEMLA - SEACEN, Punta del Este, November 2012

1

Content

1. Benefits of macroeconomic stability 2. Monetary policy and macroeconomic

stability 3. Peru’s experience 4. Challenges for the years ahead

2

q Economic theory has associated macroeconomic stability with the following:

– (i) monetary stability, i.e., keeping inflation low and stable;

– (ii) financial stability, in particular acting as a lender of last resort to ensure adequate liquidity and a fluent functioning of the payments system;

– (iii) exchange rate stability and;

– (iv) output stability, keeping unemployment close to its natural rate.

q In the pre-crisis period, a growing number of independent central banks adopted monetary strategies aimed at preserving price stability with exchange rate flexibility while keeping an eye on output.

3

Benefits of macroeconomic stability

q The tenets of this framework based on price stability are uncontroversial :

– There is no permanent tradeoff between inflation and unemployment.

– High and volatile inflation depresses growth and distorts resource allocation.

– Inflation harms the poorest segments of society most, because they lack protection against its disruptive effects.

4

Benefits of macroeconomic stability

There is cross-country evidence in the growth literature that points to the importance of inflation for long-run economic performance…

5

Barro & Sala-i-Martin report a negative relationship between inflation and growth Easterly & Fisher (2000): “…direct measures of improvements in well-being of the poor… (are) negatively correlated with inflation.”

Benefits of macroeconomic stability

6

Several studies also point at macroeconomic stabilization as an important determinant of long-run performance: Loayza & Hnatkovska (2003): “…macroeconomic volatility and long-run economic growth are negatively related.”

Benefits of macroeconomic stability

But, the nature of macroeconomic policies used to obtain stability matters,

Aghion & Banerjee (2005): “…countercyclical budgetary policies are growth-enhacing in countries with a lower level of financial development.”

Fatás & Mihov (2011): “…it is not enough to attain low inflation and low budget deficits on average, it is also necessary to have stable inflation and stable fiscal policy.”

7

Policy volatility and growth (1970 – 2007)

Benefits of macroeconomic stability

Central Bank

Monetary Policy

Exchange Rate Policy

Macro-prudential

Policy

Macroeconomic Stability

- monetary

- financial

- exchange rate

- output

Long-run Growth

8

Monetary policy and macroeconomic stability

The Peruvian experience shows that macroeconomic volatility has been associated with lower output growth rates.

9

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

1960

19

61

1962

19

63

1964

19

65

1966

19

67

1968

19

69

1970

19

71

1972

19

73

1974

19

75

1976

19

77

1978

19

79

1980

19

81

1982

19

83

1984

19

85

1986

19

87

1988

19

89

1990

19

91

1992

19

93

1994

19

95

1996

19

97

1998

19

99

2000

20

01

2002

20

03

2004

20

05

2006

20

07

2008

20

09

2010

20

11

Crecimiento del PBI y Volatilidad del Crecimiento del PBI (Promedio móvil 10 años)

Crecimiento del PBI Volatilidad del crecimiento

Nota: La volatilidad del crecimiento se calcula mediante la desviación estándar del crecimiento de los últimos 10 años.

Monetary policy and macroeconomic stability

During the 70s and 80s, periods of high macroeconomic and policy instability, per capita GDP in Peru decreased 52 per cent.

206

100

152

80

100

120

140

160

180

200

220

1960 1963 1966 1969 1972 1975 1978 1981 1984 1987 1990 1993 1996 1999 2002 2005 2008 2011

Per Capita GDP (1960 = 100)

Period GDP growth (average)

Per Capita GDP

60’ 5,9 3,2

70’ 3,6 0,6

80’ -1,0 -2,1

90’ 4,0 1,3

01’-11’ 5,8 4,5

10

Monetary policy and macroeconomic stability

Monetary policy in emerging economies has come a long way in the control of inflation in the last two decades. This, coupled with other factors, has fostered strong economic performance in the region.

11

Monetary policy and macroeconomic stability

- 6,0

- 4,0

-2,0

0,0

2,0

4,0

6,0

8,0

10,0

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Real GDP (PPP) – Developed and Emerging Economies(% var)

Developed Economies Emerging and Developing Economies

12

Since the beginning of the 1990s, dollarization has been a significant concern to Peru’s monetary authorities in view of its potential risks to the financial system.

37,8

45,5

0

10

20

30

40

50

60

70

80

90

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

Dollarization Ratio(%)

Broad money dollarization

Credit dollarization

Peru´s experience

Peru’s IT framework departs somewhat from international standards in that the BCRP uses other instruments in addition to policy interest rates, with an aim to reduce balance sheet effects associated with financial dollarization.

13

Peru´s experience

Additionally, high reserve requirements on foreign currency deposits contribute to: a) ensuring adequate liquidity; b) reducing pressure on bank credit; and c) internalizing dollarization risks. High reserve requirements on banks’ short-term foreign liabilities also reduce their exposure to “sudden stops”.

14

38,8

55,0

20

25

30

35

40

45

50

55

60

Ene-‐06

Abr-‐06

Jul-‐0

6

Oct-‐06

Ene-‐07

Abr-‐07

Jul-‐0

7

Oct-‐07

Ene-‐08

Abr-‐08

Jul-‐0

8

Oct-‐08

Ene-‐09

Abr-‐09

Jul-‐0

9

Oct-‐09

Ene-‐10

Abr-‐10

Jul-‐1

0

Oct-‐10

Ene-‐11

Abr-‐11

Jul-‐1

1

Oct-‐11

Ene-‐12

Abr-‐12

Jul-‐1

2

Foreign Currency Reserve Ratios(as percentage of total obligations subject to legal requirements)

Average rate

Marginal rate

%

Before 2008 crisis During

2008 crisis

After2008 crisis

31

17

82

45

70

84

81

0

10

20

30

40

50

60

70

80

90

100

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

Jan-‐07

Mar-‐07

May-‐07

Jul-‐0

7Sep-‐07

Nov-‐07

Jan-‐08

Mar-‐08

May-‐08

Jul-‐0

8Sep-‐08

Nov-‐08

Jan-‐09

Mar-‐09

May-‐09

Jul-‐0

9Sep-‐09

Nov-‐09

Jan-‐10

Mar-‐10

May-‐10

Jul-‐1

0Sep-‐10

Nov-‐10

Jan-‐11

Mar-‐11

May-‐11

Jul-‐1

1Sep-‐11

Nov-‐11

Jan-‐12

Mar-‐12

May-‐12

Jul-‐1

2

External Liabilitioes of banks entities (Balance in US$ million and ratio in percentage)

Long term external liabilities Short term external liabilities Long term external liabilities /Total external liabilities

The long term financing increased after the exoneration of reserve

requirement on long term external liabilities.

Peru´s experience

15

FOREX intervention aims at reducing exchange rate volatility to prevent balance sheet effects, without any commitment on the exchange rate level.

-600

-400

-200

0

200

400

600

2,650

2,750

2,850

2,950

3,050

3,150

3,250

3,350D

ec-0

7Ja

n-0

8F

eb-0

8M

ar-0

8A

pr-0

8M

ay-0

8Ju

n-0

8Ju

l-08

Au

g-08

Oct

-08

Nov

-08

Dec

-08

Jan

-09

Feb

-09

Mar

-09

Apr

-09

May

-09

Jun

-09

Jul-0

9A

ug-

09S

ep-0

9O

ct-0

9N

ov-0

9D

ec-0

9Ja

n-1

0F

eb-1

0M

ar-1

0A

pr-1

0M

ay-1

0Ju

n-1

0Ju

l-10

Aug

-10

Sep

-10

Oct

-10

Nov

-10

Dec

-10

Jan

-11

Feb

-11

Mar

-11

Apr

-11

May

-11

Jun

-11

Jul-1

1A

ug-

11S

ep-1

1

Net

FX

Pur

chas

es (m

illon

s of

US

dol

lars

)

Exc

hang

e ra

te (P

EN

per

US

dol

lar)

Nominal Exchange Rate and Net Forex Intervention

Net FX purchases CDR BCRP Exchange rate

US$ Millions Net Purchases

Net maturity of CDR-BCRP

Net placements of CDLD

Acummulated 2007 10 306 0 0Acummulated 2008 2 754 -1 421 0Acummulated 2009 108 1 421 0Acummulated 2010 8 963 0 160Acummulated Octuber 3, 2011 1 493 -590 -160Acummulated 2007 - 2011 23 624 -590 0

During the 2008 crisis

After the 2008 crisis

Peru´s experience

The growing size of the BCRP’s balance-sheet has been supported by a solid fiscal position, the use of reserve requirements and, to a lesser degree, the placement of BCRP securities.

Central Reserve Bank of Peru

Assets LiabilitiesInternational reserves 27,6 Public sector deposits 10,5

In domestic currency 6,7In foreign currency 3,8

Reserve requirements 7,6In domestic currency 2,6In foreign currency 5,0

Central Bank instruments 3,6Cash holdings 5,7Other liabilities 0,2

Peru: Central Reserve Bank Balance Sheet(As percentages of GDP. Figures of December 31, 2011)

16

Peru´s experience

The BCRP’s Forex intervention has neither created real exchange rate misalignments nor prevented a sustained dedollarization process.

17

Multilateral Real Exchange Rate and Equilibrium Real Exchange rate (2009 = 100)

The estimation folows the BEER methodology with data until september 2012.

Peru´s experience

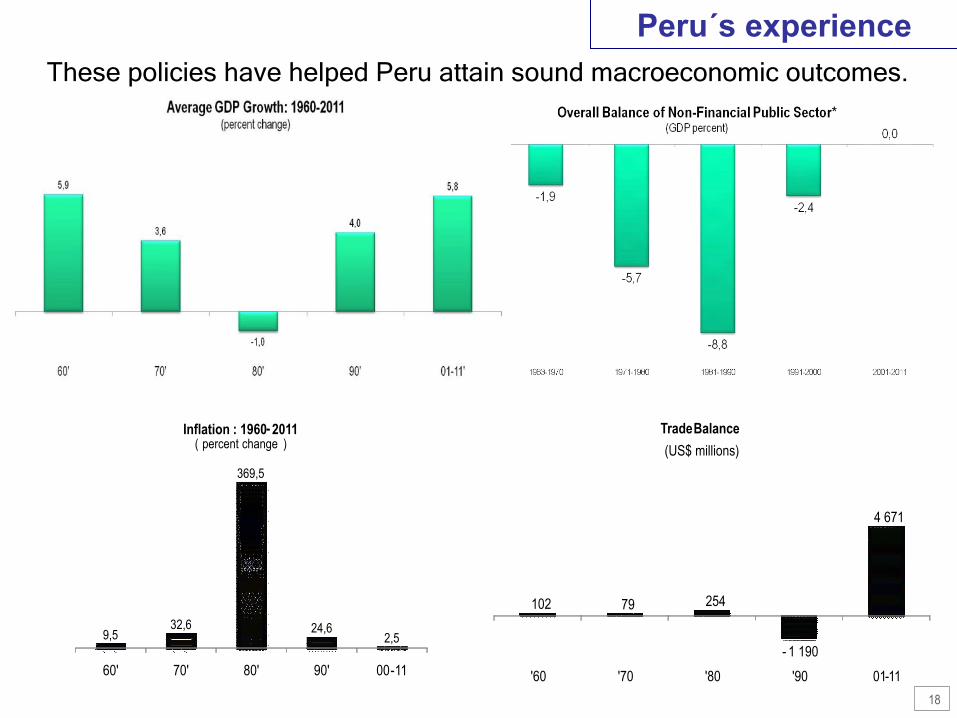

These policies have helped Peru attain sound macroeconomic outcomes.

102 79 254

- 1 190

4 671

'60 '70 '80 '90 01 - 11

Trade Balance (US$ millions)

9,5 32,6

369,5

24,6 2,5

60' 70' 80' 90' 00 - 11

Inflation : 1960 - 2011 ( percent change )

18

Peru´s experience

q We have learned from the crisis that macroeconomic stability demands an array of policies in order to anticipate and cope with shocks originating from multiple sources.

q This requires both an institutional framework to establish the principles and instruments governing macro-regulation and a clear distinction between the roles of monetary and macro-regulatory policy.

q In the face of various potential sources of destabilizing shocks for the economy, central banks require a set of instruments wider than the standard monetary policy toolkit.

q Such instruments have the common objective of deterring economic agents from excessive risk taking and enhancing the resilience of the economy against low-probability but high-impact events.

19

Challenges ahead

q Several central banks, especially in emerging market economies, have used instruments such as capital requirements, counter-cyclical provisioning, additional liquidity requirements, and debt limits to meet these objectives.

q However, the use of these instruments represents an important challenge to the authorities, as they typically impose efficiency costs on financial intermediation, which nevertheless are lower than the benefits from preserving financial stability.

q Shortcomings may be limited by using the right mix of instruments —especially distributing the burden of macro-prudential regulation among a wider set of tools.

20

Challenges ahead

q It is fundamental to ensure adequate communication between the regulatory, supervisory, monetary and fiscal authorities to guarantee the effectiveness of macro-prudential policies.

q For central banks in particular, it is important to keep in mind that macro-prudential policies can and must be implemented while preserving the two pillars of monetary policy; i.e., independence and the single mandate to preserve monetary stability.

q Many challenges remain going forward. In particular, the limits between monetary and macro-prudential policy need to be further clarified; and additional work is required to identify areas where the complementarity between monetary and macro-prudential policies can be maximized.

21

Challenges ahead

Macroeconomic Stability in the Aftermath of the Financial Crisis

Julio Velarde Governor

Central Reserve Bank of Peru

CEMLA - SEACEN, Punta del Este, November 2012

22