Macroeconomic Factors and Growth: Theory and Case Studies Lecture 3: Case Studies Ulrich Fritsche...

38

Macroeconomic Factors and Growth: Theory and Case Studies Lecture 3: Case Studies Ulrich Fritsche Bernhard Seidel DIW Berlin

-

date post

22-Dec-2015 -

Category

Documents

-

view

215 -

download

0

Transcript of Macroeconomic Factors and Growth: Theory and Case Studies Lecture 3: Case Studies Ulrich Fritsche...

Macroeconomic Factors and Growth: Theory and Case Studies

Lecture 3: Case Studies

Ulrich FritscheBernhard Seidel

DIW Berlin

Fritsche/SeidelSeptember 2003

Structure

– Lecture 1: The „Washington Consensus“ (Fritsche)– Lecture 2: The Struggle for a “Post-Washington

Consensus” (Seidel)– Lecture 3: Case studies

– Basic aim of this lecture: Empirical evidence of Asian crises and lessons for development strategies

Fritsche/SeidelSeptember 2003

Agenda

– Asian Crisis as an example for the fight about the „Post-Washington Consensus“• Background

• Onset of the Crisis, Macroeconomic Factors

– Coping with the Crisis• Countries with IMF and Worldbank Programs

• Countries with Capital Controls

– Discussion• What did the discussion about the „Post-Washington

Consensus“ brought about?

Fritsche/SeidelSeptember 2003

Asian Crisis: Background

– „The Asian Miracle“ was the title of a 1993 World Bank publication

– In contrast to Latin America over some decades this region seemed to be „crisis prone“.

– High growth rates, low inflation, fiscal discipline, export-led growth

– Poverty rates dropped

Fritsche/SeidelSeptember 2003

The Miracle: High (Per Capita) Growth Rates

-15.00

-10.00

-5.00

0.00

5.00

10.00

15.00

1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Malaysia Indonesia Korea, Rep.Hong Kong, China China PhilippinesSingapore Thailand

Fritsche/SeidelSeptember 2003

Poverty

Source: Furman, Stiglitz et al. 1999

Fritsche/SeidelSeptember 2003

Fiscal Deficitsin % of GDP

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997

Korea, Rep. Indonesia Thailand Malaysia

Fritsche/SeidelSeptember 2003

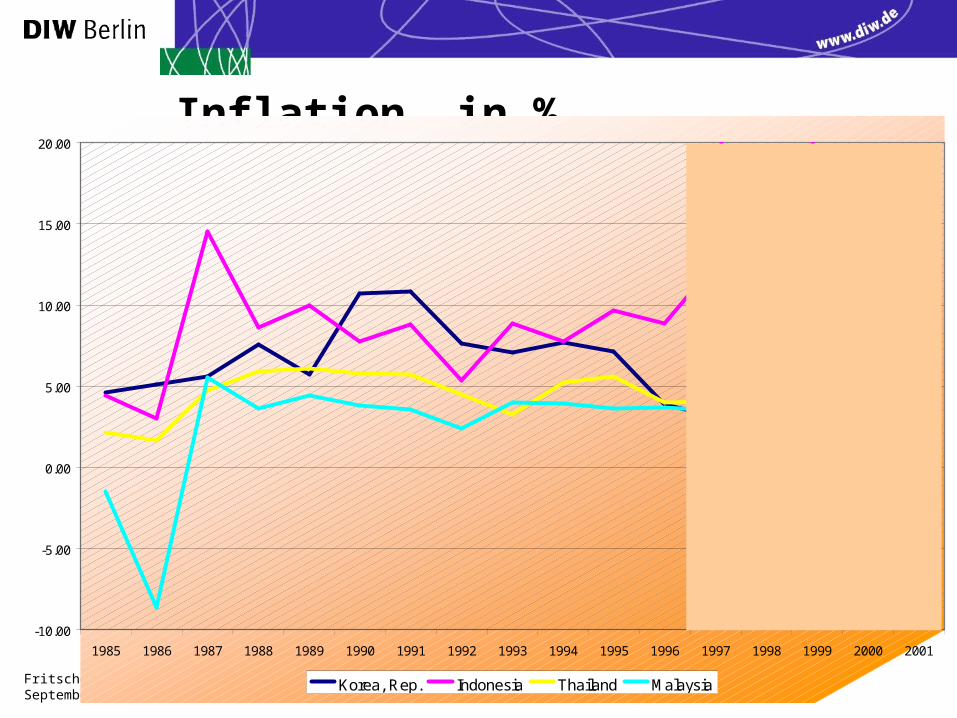

Inflation, in %

-10.00

-5.00

0.00

5.00

10.00

15.00

20.00

1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Korea, Rep. Indonesia Thailand Malaysia

Fritsche/SeidelSeptember 2003

Macroeconomic Factors

– Current account balances

– Productivity

– Exchange rates

– Bank lending and capital flows

Fritsche/SeidelSeptember 2003

International Solvency

ttt1t Y/TB)i1(B

tt1tnom

t1t b)i1(b)g1(g1Y/Y

b)gr(bbb 1tt

Legend:B...Debt, T...Trade Balance, Y...GDPr ... interest rateg ... growth rateb ... Debt/GDP ... Trade Balance/GDP

divide by GDP

growth rates

Fritsche/SeidelSeptember 2003

Resource Gap 1996

Current trade balance minus required trade surplus to stabilize the debt to GDP ratio

Source: Corsetti/Pesenti/Roubini 1998

In all countries,trade balance didnot stabilize debt to GDP in the long run

Fritsche/SeidelSeptember 2003

Current Accounts Balance in % of GDPIndonesia

-6,00

-4,00

-2,00

0,00

2,00

4,00

6,00

1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Korea

-6,00

-4,00

-2,00

0,00

2,00

4,00

6,00

8,00

10,00

12,00

14,00

1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Thailand

-10,00

-5,00

0,00

5,00

10,00

15,00

1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Malaysia

-15,00

-10,00

-5,00

0,00

5,00

10,00

15,00

20,00

1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Fritsche/SeidelSeptember 2003

Fall in Productivity

– Krugman argued some years before the crisis, that the Asian model was mainly driven by extensive production, not intensive one

– Source of the strong growth since the 80s • Increasing labor supply (demographics)

• (Physical) Capital stock accumulation

• but NOT so much productivity

– Figures from Korean „chaebols“ from 1996 would indicate a fall in the return on capital

Fritsche/SeidelSeptember 2003

The Declining ICOR

)K(fYS

gradient:

)Y(fI S

gradient: (s+)

K

y*

Fritsche/SeidelSeptember 2003

Return on Investment

Source: Corsetti/Pesenti/Roubini 1998

Fritsche/SeidelSeptember 2003

Exchange Rate Appreciation

– Exchange rate appreciation did not seem to be too problematic

– However, Japan was in crisis since the beginning of the 90s and the weak demand lead to a significant slowdown of Asian exports

– Furthermore the increasing weight of China in total exports from the region enhanced competitive pressures

Fritsche/SeidelSeptember 2003

Exchange Rates and Current AccountsIndonesia

-6,00

-4,00

-2,00

0,00

2,00

4,00

6,00

1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

0,00

50,00

100,00

150,00

200,00

250,00

Korea

-6,00

-4,00

-2,00

0,00

2,00

4,00

6,00

8,00

10,00

12,00

14,00

1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

0,00

20,00

40,00

60,00

80,00

100,00

120,00

140,00

Thailand

-10,00

-5,00

0,00

5,00

10,00

15,00

1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

0,00

20,00

40,00

60,00

80,00

100,00

120,00

140,00

Malaysia

-15,00

-10,00

-5,00

0,00

5,00

10,00

15,00

20,00

1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

0,00

20,00

40,00

60,00

80,00

100,00

120,00

140,00

160,00

Current account balancein % of GDP Official exchange rate

US-$ per LCU, 1995 = 100

Real effective exchange rate1995=100

Fritsche/SeidelSeptember 2003

Bank lending and short-term debt

– Sustained lending boom in some countries (Philippines, Singapore)

– Falling productivity growth created bad loans– Supervision, regulation was poor– Foreign debt burden increased, short-term debt

became more important– Domestic banks borrowed heavily from foreign

banks and lent mostly to domestic investors

Fritsche/SeidelSeptember 2003

Short-term debt (% of external debt)

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Malaysia Indonesia Korea, Rep. Thailand

Fritsche/SeidelSeptember 2003

Short-term debt / foreign reserves

Fritsche/SeidelSeptember 2003

IMF-Response to the CrisisAgreementsLending agreements with Thailand (Aug 97), Indonesia (Nov 97) and Korea (Dec 97)

•Financial commitments by IMF, World Bank, ADB and diverse countries

•Loans to the central bank and the government

•Macroeconomic framework (budget balance, high nominal interest rates, tight credit) targeted at exchange rate stability

•Financial sector restructuring

•‘Good governance’ and ‘structural’ measures (trade reform, demonopolization, privatization etc.)

Country Commitment Disbursed atMarch 31, 98

Indonesia 40.0 3.0Korea 57.0 21.7Thailand 17.2 10.2

Bill. US $

Fritsche/SeidelSeptember 2003

Policy Events and the Exchange Rate, July 1997 to March 1998

Korea Thailand

Source: Radelet/Sachs 1998

Fritsche/SeidelSeptember 2003

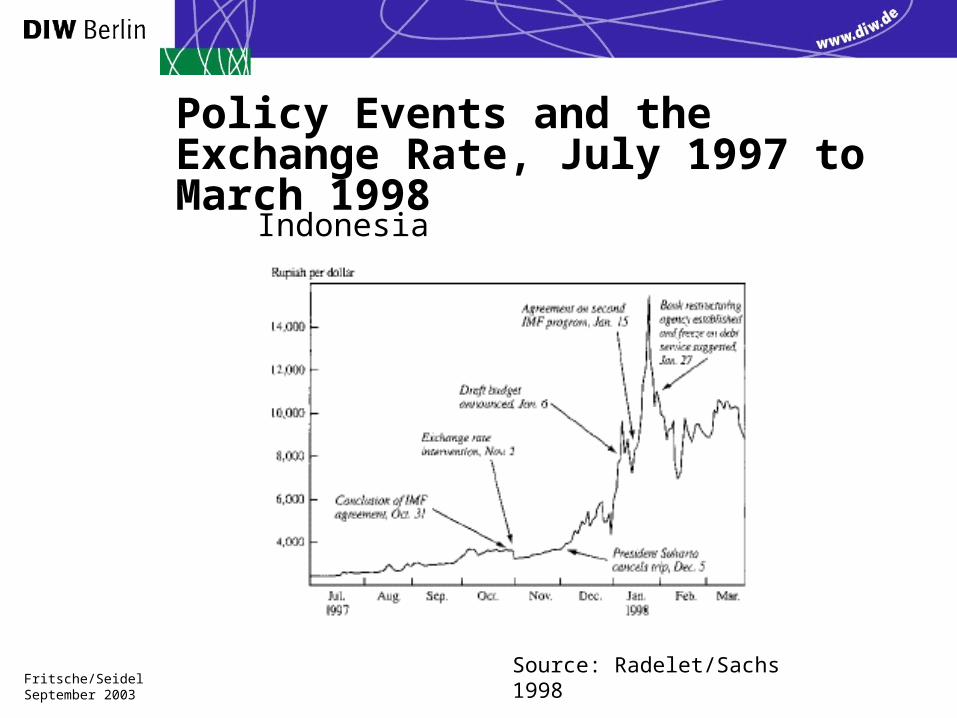

Policy Events and the Exchange Rate, July 1997 to March 1998

Indonesia

Source: Radelet/Sachs 1998

Fritsche/SeidelSeptember 2003

Forecasts of GDP Growth during the Asian Crisis

Indonesia Korea Thailand

Date Growthrate

Date Growthrate

Date Growth rate

IMF, first program 31.10.97 3.0 04.12.97 2.5 20.08.97 3.5

IMF, second program 15.01.98 0.0 25.11.97 0.0 to1.0

IMF, third program 10.04.98 -5.0 07.02.98 1.0 24.02.98 -3.0 to -1.0

IMF Econ. Outlook 04/98 -5.0 04/98 0.8 04/98 -3.1

Market forecast 02/98 -8.8 02/98 -2.5 02/98 -6.0

Fritsche/SeidelSeptember 2003

Consequences

–Socialization of private loans

•Repayments to foreign creditors

•Central bank became

- debtor of the IMF

- creditor of commercial banks

–Intervention in the exchange market to lower the Dollar-price

for domestic currency (Indonesia)

Fritsche/SeidelSeptember 2003

Failure of Re-establishing Market Confidence

– IMF’s arrival strengthens feelings about the gravity of the situation

– IMF focused on deep fundamental weakness of Asian economies, mainly of financial sector

– Announcement of restructuring financial sector (closing banks, tightening regulation etc.)

– Budgetary discipline meant heavy contractionary impact (Thailand 2.6 %, Indonesia 1-2 %, Korea 1.5 % of GDP); Raising interest rates fuels fear of crashes

– Uncertainties about the prompt availability of commitments and about IMF as lender of last resort

Fritsche/SeidelSeptember 2003

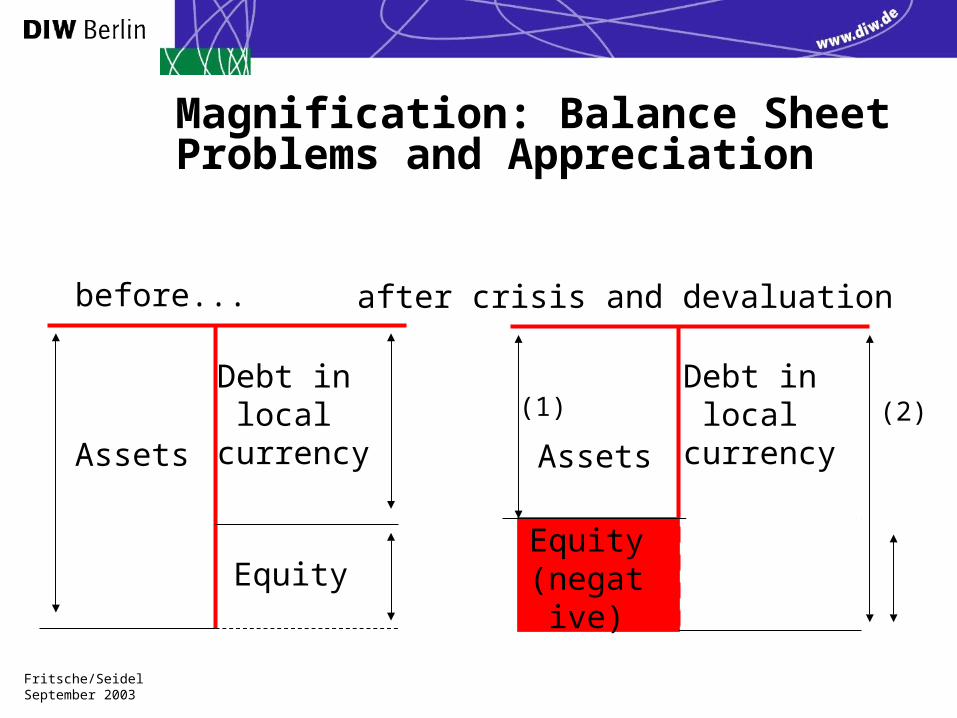

Magnification: Balance Sheet Problems and Appreciation

Debt in local

currency

Equity

Assets

before...

Assets

after crisis and devaluation

Debt in local

currency

(1) (2)

Equity(negative)

Fritsche/SeidelSeptember 2003

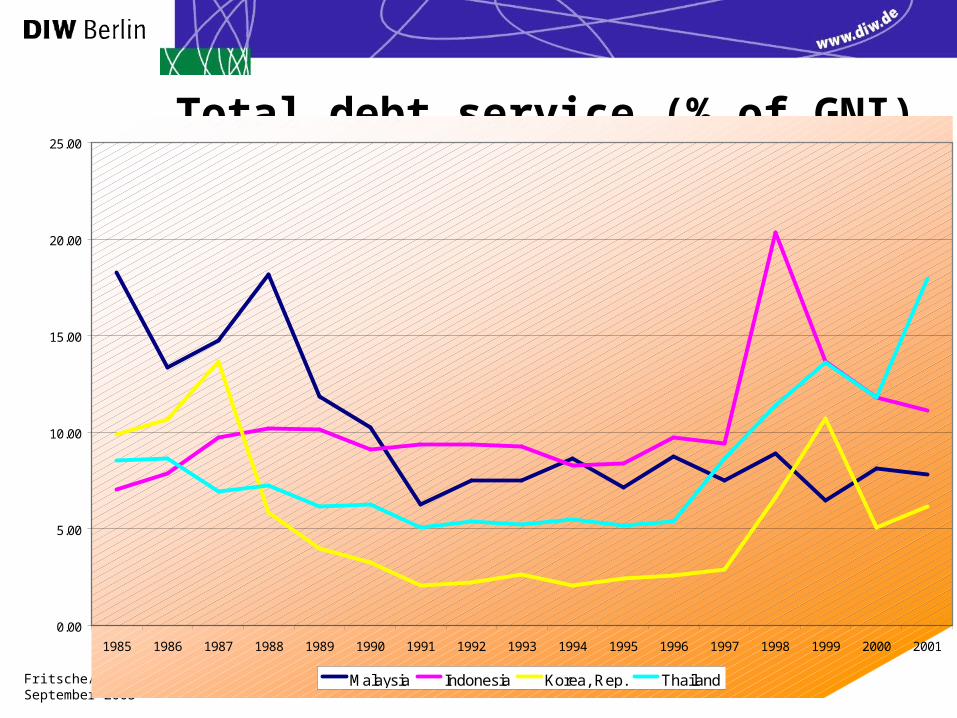

Total debt service (% of GNI)

0.00

5.00

10.00

15.00

20.00

25.00

1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Malaysia Indonesia Korea, Rep. Thailand

Fritsche/SeidelSeptember 2003

Savings-Investment-Balance, in % of GDP

Indonesia

-10,00

-5,00

0,00

5,00

10,00

15,00

20,00

25,00

30,00

35,00

40,00

1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Korea

-10,00

-5,00

0,00

5,00

10,00

15,00

20,00

25,00

30,00

35,00

40,00

45,00

1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Thailand

-20,00

-10,00

0,00

10,00

20,00

30,00

40,00

50,00

1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Malaysia

-20,00

-10,00

0,00

10,00

20,00

30,00

40,00

50,00

60,00

1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Gross domestic savings

Gross fixed capital formation

Current account balance

Fritsche/SeidelSeptember 2003

Indonesia

0,00

5,00

10,00

15,00

20,00

25,00

30,00

35,00

1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

-30,00

-25,00

-20,00

-15,00

-10,00

-5,00

0,00

5,00

10,00

15,00

20,00

25,00

Investment to GDP and Real Interest Rate

Gross fixed capital formation

Real interest rate

Korea

0,00

5,00

10,00

15,00

20,00

25,00

30,00

35,00

40,00

45,00

1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

-2,00

0,00

2,00

4,00

6,00

8,00

10,00

12,00

14,00

Thailand

0,00

5,00

10,00

15,00

20,00

25,00

30,00

35,00

40,00

45,00

1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

0,00

2,00

4,00

6,00

8,00

10,00

12,00

14,00

16,00

Malaysia

0,00

5,00

10,00

15,00

20,00

25,00

30,00

35,00

40,00

45,00

50,00

1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

0,00

5,00

10,00

15,00

20,00

25,00

Fritsche/SeidelSeptember 2003

Malaysian Capital Controls (CC)in Consequence of Financial Crisis

Aims of Capital Controls

– Provision of stability– Independence of monetary policy from exchange

rate fluctuation– Insulating national economy from external shocks– Avoiding contagion effects of the crisis in

neighbouring countries

Fritsche/SeidelSeptember 2003

Measures by Bank Negara Malaysia (BNM) I

– September 1, 1998 • One-year waiting period on repatriation of portfolio investment

• Mandatory repatriation of Ringgit held abroad

• Restriction on transfers of funds between external accounts

• Limits of transport of Ringgit by travelers

• Prohibition of resident/non-resident Ringgit credit arrangements

• Prohibition of trade settlement in Ringgit

• Prohibition of resident/non-resident offer side swaps and similar hedge transactions

• Freezing CLOB (Central Limit Order Book) share transactions

– September 2, 1998 • Fixing the exchange rate of Ringgit at 3.8 to the Dollar

Fritsche/SeidelSeptember 2003

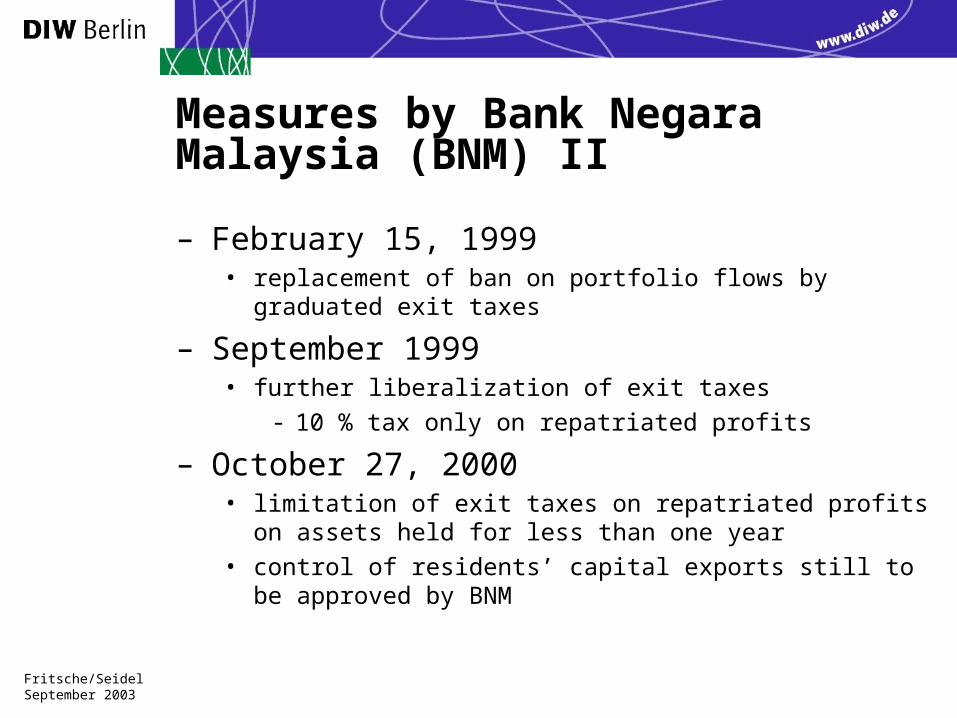

Measures by Bank Negara Malaysia (BNM) II

– February 15, 1999 • replacement of ban on portfolio flows by graduated exit taxes

– September 1999• further liberalization of exit taxes

- 10 % tax only on repatriated profits

– October 27, 2000• limitation of exit taxes on repatriated profits on assets held for

less than one year

• control of residents’ capital exports still to be approved by BNM

Fritsche/SeidelSeptember 2003

Effects on Capital Flows

Source: World Bank (2001)

Fritsche/SeidelSeptember 2003

Consequences

– Sovereign spread 300 basis points higher than in other crisis countries, going down to 150 basis points in May 150

– Low FDI flows into Malaysia as well as into the other countries (no significant influence of CC)

– Exodus of portfolio capital, reversed in 2000 to inflows

– Efficient and effective controls– Exchange rate fixed at an under-evaluated level– Regulatory and supervisory reform of financial

sector and capital market– Safeguard of political stability

Fritsche/SeidelSeptember 2003

Exports, Inflation and GDP-GrowthPost-Crisis Development

-15

-10

-5

0

5

10

15

1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

Malaysia Indonesia Korea, Rep. Thailand

-10

-5

0

5

10

15

20

1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

GrowthInflation

-15

-10

-5

0

5

10

15

20

25

30

1996 1997 1998 1999 2000 2001

Exports

Fritsche/SeidelSeptember 2003

Conclusions I

– Asian financial crisis was a result of latent macroeconomic weakness, receding confidence, high vulnerability of banking systems, overshooting reactions and herding

– The crisis hit the real economies hard by decreasing GDP, raising poverty

– Neither large support programs with bail-outs for the creditors nor reversing capital market liberalization and re-introducing capital control could help to avoid economic and financial distortions

Fritsche/SeidelSeptember 2003

Conclusions IIReducing vulnerability as political Agenda

– Priority for market forces• Liberalization

• Regulation and supervision

– Proper organization of banking system and financial markets

– Flexible exchange rate regime– Provision of infrastructure– Sound fiscal and monetary policy– Proper institution building