Local Manufacturing Potential for CSP Projects in...

24

© Fraunhofer ISI Dr. Wolfgang Eichhammer, Dr. Gabriel Morin Local Manufacturing Potential for CSP Projects in MENA Context of the study and CSP value chain: components, market structure and trends http://www.trec-uk.org.uk/resources/pictures/stills4.html http://www.flickr.com/photos/worldbank/

Transcript of Local Manufacturing Potential for CSP Projects in...

© Fraunhofer ISI

D r . W o l f g a n g E i c h h a m m e r, D r . G a b r i e l M o r i n

Local Manufactur ing Potent ia l for CSP Pro jects in MENA

Context of the study and CSP value chain: components, market structure and trends

http://www.trec-uk.org.uk/resources/pictures/stills4.html http://www.flickr.com/photos/worldbank/

© Fraunhofer ISISeite 2

• High potential for application of the technology exists in MENA itself• In difference to other renewable energy technologies, such as photovoltaic or

wind energy, the CSP potential is more limited in many of the major developed countries

• A CSP industry in MENA could serve not only the regional market but also existing markets in Southern Europe, the USA and elsewhere

• Examples of emerging wind industries in India and China demonstrate the positive effects that manufacturing of innovative renewable energy technologies can have on the respective economies

MENA could become home to a new, high potential industry in a region with large solar energy resources and benefit from the associated job- and wealth creation

Mot ivat ion: The Need for a CSP Home Bas is in MENA

© Fraunhofer ISISeite 3

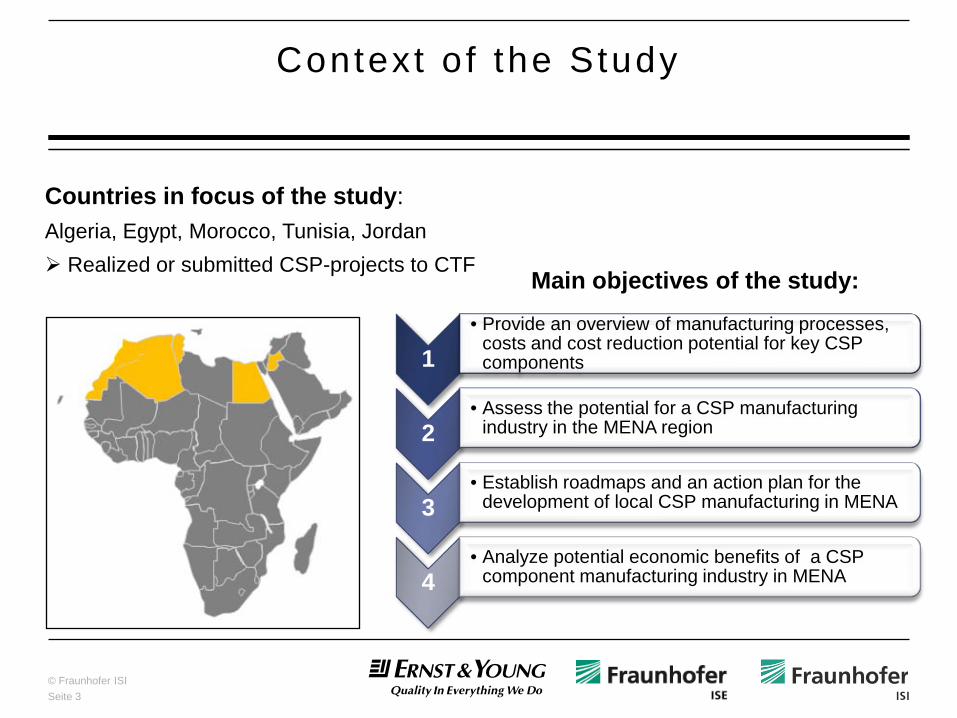

Context o f the Study

Countries in focus of the study: Algeria, Egypt, Morocco, Tunisia, Jordan Realized or submitted CSP-projects to CTF

1• Provide an overview of manufacturing processes,

costs and cost reduction potential for key CSP components

2• Assess the potential for a CSP manufacturing

industry in the MENA region

3• Establish roadmaps and an action plan for the

development of local CSP manufacturing in MENA

4• Analyze potential economic benefits of a CSP

component manufacturing industry in MENA

Main objectives of the study:

© Fraunhofer ISISeite 4

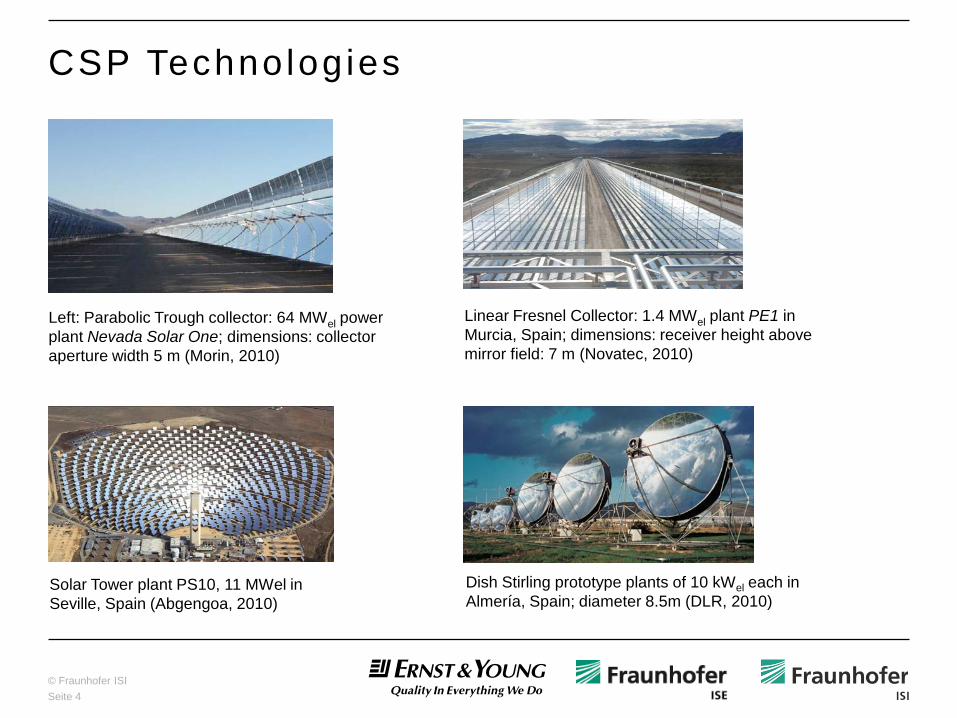

CSP Technolog ies

Left: Parabolic Trough collector: 64 MWel power plant Nevada Solar One; dimensions: collector aperture width 5 m (Morin, 2010)

Linear Fresnel Collector: 1.4 MWel plant PE1 in Murcia, Spain; dimensions: receiver height above mirror field: 7 m (Novatec, 2010)

Solar Tower plant PS10, 11 MWel in Seville, Spain (Abgengoa, 2010)

Dish Stirling prototype plants of 10 kWel each in Almería, Spain; diameter 8.5m (DLR, 2010)

© Fraunhofer ISISeite 5

CSP Market Shares and Development

Parabolic Trough today over 90% market share, today

Other CSP Technologies gaining market shares

20 GW installed CSP capacity by 2020 is feasible

BUT: Reliable financial and political framework needed !

(Συν Ωινδ Ενεργψ, 2010)

© Fraunhofer ISISeite 6

The CSP Value-chain – Oppor tun i t ies for Local Indust r ies

ProjectDevelopment Materials Components

PlantEngineering &Const ruct ion

Operat ion Dist ribut ion

Finance & Ownership

Research & Development

Polit ical Inst itut ions

Concept Engineering

Geographical Determinat ion

Determinat ion of general requirements

Concrete Steel Sand Glass Silver Copper Salt Other

chemicals

Mirrors Mount ing

Structure Receiver HTF Connect ion

piping Steam genera-

tor / heat exchanger

Pumps Storage

System Power Block Grid connect .

EPC-Contractor: Detailed

Engineering Procurement Construct ion

Operat ion & maintenance of the plant

Utility Transport &

dist ribut ion of elect ricit y

Corevaluechain

Elementsof thecorevaluechain

Essent ialpartners

ProjectDevelopment Materials Components

PlantEngineering &Const ruct ion

Operat ion Dist ribut ion

Finance & Ownership

Research & Development

Polit ical Inst itut ions

Concept Engineering

Geographical Determinat ion

Determinat ion of general requirements

Concrete Steel Sand Glass Silver Copper Salt Other

chemicals

Mirrors Mount ing

Structure Receiver HTF Connect ion

piping Steam genera-

tor / heat exchanger

Pumps Storage

System Power Block Grid connect .

EPC-Contractor: Detailed

Engineering Procurement Construct ion

Operat ion & maintenance of the plant

Utility Transport &

dist ribut ion of elect ricit y

Corevaluechain

Elementsof thecorevaluechain

Essent ialpartners

Analysis of the CSP value-chain:

•Identification of current market players•Review of production processes•Cost analysis / cost reduction potential•Complexity assessment for components

© Fraunhofer ISISeite 7

Components of Parabol ic Trough Power Plants

© Fraunhofer ISISeite 8

Co l lec tor : Meta l Suppor t (Examples)Sample Collectors Flagsol Skal-ET 150

(e.g. Andasol I-III)Solargenix SGX-2(e.g. Nevada Solar One)

Structure Torque box design-galvanized steel

Recycled aluminum orsteel struts and geo hubs

kg/m² per aperture area

~ 18.5 kg/m² steel ~ 11-12 kg/m² aluminum

Material quality 85% S235JRG214% S355JRG21% X5CrNi 19-10

6061 T6 aluminum(70-80% recycled content)

Materials used Equal angles (60%),Plates (10%),Square Tubes (15%),Rods, mills, profiles and fasteners (15%)

Similar parts

© Fraunhofer ISISeite 9

Va lue Chain in CSP – Par t 1

Components

Valu

e ch

ain

Mirrors Receiver

Flabeg Gmbh Guardian Ind. Rioglass Solar Saint -Gobain Pilkington Glaston 3M Alanod Glasstech Inc. Ref lec Tech HEROGlas Cristaleria

Espagnola SA

Schot t Solar AG Siemens

(Solel Solar Sys)

Mount ing Structure

Abengoa Flagsol Acciona Grupo Sener Siemens Sky Fuel Inc Albiasa Alcoa Areva (Ausra)

Com

pani

es

EPC

EPC

AbengoaSolar

Flagsol Duro

Felguera Samca Sky Fuel Albiasa Solar Abener Orascom MAN

Ferrostaal ACS Cobra

ProjectDevelop. Materials

Concept Engineering

Raw & Semi-f inished

Solar Millennium

Abengoa Solar Aries Ibereolica Torresol/

Masdar Novatec Abengoa Epuron Fichtner Brightsource eSolar St irling Energy

Systems (SES) M+W Zander

Pilkington ThyssenKrupp Heidelberg

Cement Hydro Bert ram

Heatec Haifa

Chemicals SQM BASF Linde

Components

Valu

e ch

ain

Mirrors Receiver

Flabeg Gmbh Guardian Ind. Rioglass Solar Saint -Gobain Pilkington Glaston 3M Alanod Glasstech Inc. Ref lec Tech HEROGlas Cristaleria

Espagnola SA

Schot t Solar AG Siemens

(Solel Solar Sys)

Mount ing Structure

Abengoa Flagsol Acciona Grupo Sener Siemens Sky Fuel Inc Albiasa Alcoa Areva (Ausra)

Com

pani

es

EPC

EPC

AbengoaSolar

Flagsol Duro

Felguera Samca Sky Fuel Albiasa Solar Abener Orascom MAN

Ferrostaal ACS Cobra

ProjectDevelop. Materials

Concept Engineering

Raw & Semi-f inished

Solar Millennium

Abengoa Solar Aries Ibereolica Torresol/

Masdar Novatec Abengoa Epuron Fichtner Brightsource eSolar St irling Energy

Systems (SES) M+W Zander

Pilkington ThyssenKrupp Heidelberg

Cement Hydro Bert ram

Heatec Haifa

Chemicals SQM BASF Linde

© Fraunhofer ISISeite 10

Va lue Chain in CSP – Par t 2

Storage System

Power Block& pumps

Grid Connect ionHTF

Dow Chemicals Solut ia Linde BASF

Steam Generator/

Heat Exchanger

Connect ing Piping

Abengoa Bharat Heavy

Elect rical Ltd. Acciona ACS Cobra Bilf ingerBerger Käfer

Siemens MAN Turbo GE Power

Components

Sener MAN Turbo Kraf tanlagen

München Siemens GE Power Alstom ABB

MAN Ferrostaal Siemens Abengoa Solar ABB

Valu

e ch

ain

Com

pani

es

Storage System

Power Block& pumps

Grid Connect ionHTF

Dow Chemicals Solut ia Linde BASF

Steam Generator/

Heat Exchanger

Connect ing Piping

Abengoa Bharat Heavy

Elect rical Ltd. Acciona ACS Cobra Bilf ingerBerger Käfer

Siemens MAN Turbo GE Power

Components

Sener MAN Turbo Kraf tanlagen

München Siemens GE Power Alstom ABB

MAN Ferrostaal Siemens Abengoa Solar ABB

Valu

e ch

ain

Com

pani

es

© Fraunhofer ISISeite 11

Va lue Chain in CSP – Par t 3

Operat ion Dist ribut ion

Operat ion&Maintenance

Ut ility / TransportDist ribut ion

Va

lue

chai

nCo

mpa

nies

Nevada Solar Iberdrola Acciona ACS Cobra Abengoa Flagsol MAN

Ferrostaal FPL Energy

APS Endesa

Finance &Ownership

Research &Development

Polit icalInst itut ions

Local banks Internat ional

banks World Bank African

Development Bank

Investors Public

inst itut ions

Plataforma Solar de Almeria

DLR Fraunhofer Ciemat NREL Sandia Nat ional

Laboratory

Local governments

Esse

ntia

l par

tner

s

Operat ion Dist ribut ion

Operat ion&Maintenance

Ut ility / TransportDist ribut ion

Va

lue

chai

nCo

mpa

nies

Nevada Solar Iberdrola Acciona ACS Cobra Abengoa Flagsol MAN

Ferrostaal FPL Energy

APS Endesa

Finance &Ownership

Research &Development

Polit icalInst itut ions

Local banks Internat ional

banks World Bank African

Development Bank

Investors Public

inst itut ions

Plataforma Solar de Almeria

DLR Fraunhofer Ciemat NREL Sandia Nat ional

Laboratory

Local governments

Esse

ntia

l par

tner

s

© Fraunhofer ISISeite 12

Cost Structure of 50 MW PTC plant with 7.5 h storage

© Fraunhofer ISISeite 13

Complex i ty versus Investment - In tens i ty

© Fraunhofer ISISeite 14

Conc lus ion : CSP Componen ts P roduc t i on in MENA

Near-term: Low-Investment and Low-Complexity Activities in MENA:

Collector Assembly

Collector Installations

Civil: Groundworks, Collector Foundations, Buildings, Infrastructure

⇒ MENA manufacturing of approximately 17% of plant invest (+ optional EPC, Proj. Management)

If sustainable MENA-CSP-Markets are given:

More investment-intensive and more complex CSP-Activities in MENA:

Mirror Production

Receiver Production

Other specialized components and processes

⇒ Local Value Creation: up to 80% of plant invest

© Fraunhofer ISISeite 15

Contact:

Wolfgang EichhammerDeputy Head Competence Centre Energy Policy and Energy Systems Fraunhofer Institute for Systems and Innovation Research ISI Breslauer Strasse 48 | 76139 Karlsruhe | Germany

Phone +49 721 6809-158 | Fax +49 721 6809-272 [email protected] http://www.isi.fraunhofer.de

Thank you for your At tent ion!

© Fraunhofer ISISeite 16

Backup

© Fraunhofer ISISeite 17

Potent ia l o f the CSP Technology

Schott AG: Memorandum zur solarthermischen Kraftwerkstechnologie , 2006

Potential for solar thermal power generation worldwide

© Fraunhofer ISISeite 18

Current CSP Pro ject Development

ATKearney: Solar Thermal Electricity 2025, Report June 2010

Existing and planned solar thermal electricity capacity through 2015

© Fraunhofer ISISeite 19

Current CSP projects classified by applied technology [in MW capacity]

CSP Pro ject Development

Operational Construction Planningphase

Tower 44 17 1603

Parabolic 778 1400 8144

Fresnel 9 30 134

Dish & Stirling 2 1 2247

Sun & Wind Energy 6/2010CSP projects by country (operating, under construction and in planning phase)

Sun & Wind Energy 6/2010

© Fraunhofer ISISeite 20

Work ing Pr inc ip le o f Parabol ic Trough Power Plant(Andasol Example)

(Σολαρµιλλεννιυµ, 2009)

© Fraunhofer ISISeite 21

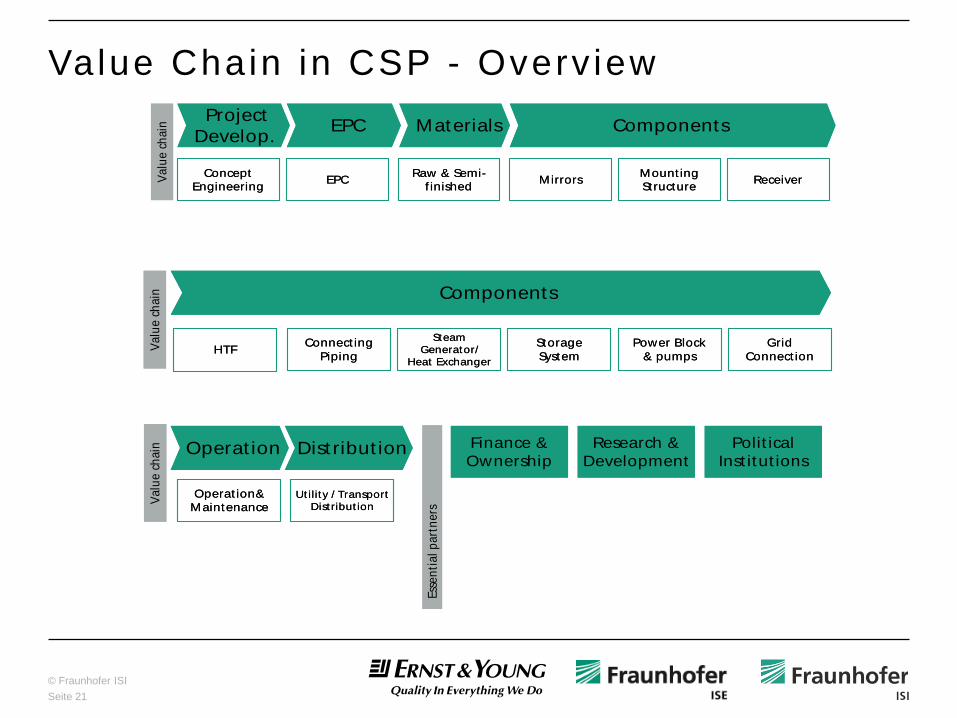

Va lue Chain in CSP - Overv iewComponents

Valu

e ch

ain

Mirrors Receiver

Mount ing Structure

EPC

EPC

ProjectDevelop. Materials

Concept Engineering

Raw & Semi-f inished

Components

Valu

e ch

ain

Mirrors Receiver

Mount ing Structure

EPC

EPC

ProjectDevelop. Materials

Concept Engineering

Raw & Semi-f inished

Storage System

Power Block& pumps

Grid Connect ionHTF

Steam Generator/

Heat Exchanger

Connect ing Piping

Components

Valu

e ch

ain

Storage System

Power Block& pumps

Grid Connect ionHTF

Steam Generator/

Heat Exchanger

Connect ing Piping

Components

Valu

e ch

ain

Operat ion Dist ribut ion

Operat ion&Maintenance

Ut ility / TransportDist ribut ion

Va

lue

chai

npa

nies

Nevada Solar Iberdrola Acciona ACS Cobra Abengoa

APS Endesa

Finance &Ownership

Research &Development

Polit icalInst itut ions

Local banks Internat ional

banks World Bank African

Development Bank

Investors

Plataforma Solar de Almeria

DLR Fraunhofer Ciemat NREL Sandia Nat ional

L b t

Local governments

Esse

ntia

l par

tner

s

Operat ion Dist ribut ion

Operat ion&Maintenance

Ut ility / TransportDist ribut ion

Va

lue

chai

npa

nies

Nevada Solar Iberdrola Acciona ACS Cobra Abengoa

APS Endesa

Finance &Ownership

Research &Development

Polit icalInst itut ions

Local banks Internat ional

banks World Bank African

Development Bank

Investors

Plataforma Solar de Almeria

DLR Fraunhofer Ciemat NREL Sandia Nat ional

L b t

Local governments

Esse

ntia

l par

tner

s

© Fraunhofer ISISeite 22

Assessment of potential for MENA industries to provide CSP components

Identification of potential players

Identification of technical & economic barriers for a CSP industry in MENA

2. Assessment o f Indust ry Capabi l i t ies for CSP Components and Serv ices

• Industry surveys in CSP relevant sectors (MENA and globally)- Steel production/transformation- Float glass/mirror production- Electronic industry- Service providers (EPC)

Industrial capability

• Collection of complementary data: patent/foreign trade analyses in CSP relevant industrial sectors

Sectoralcompetitive-

ness

• Surveys at public and private institutions & organizations relevant for CSP development

Status of institutional framework

© Fraunhofer ISISeite 23

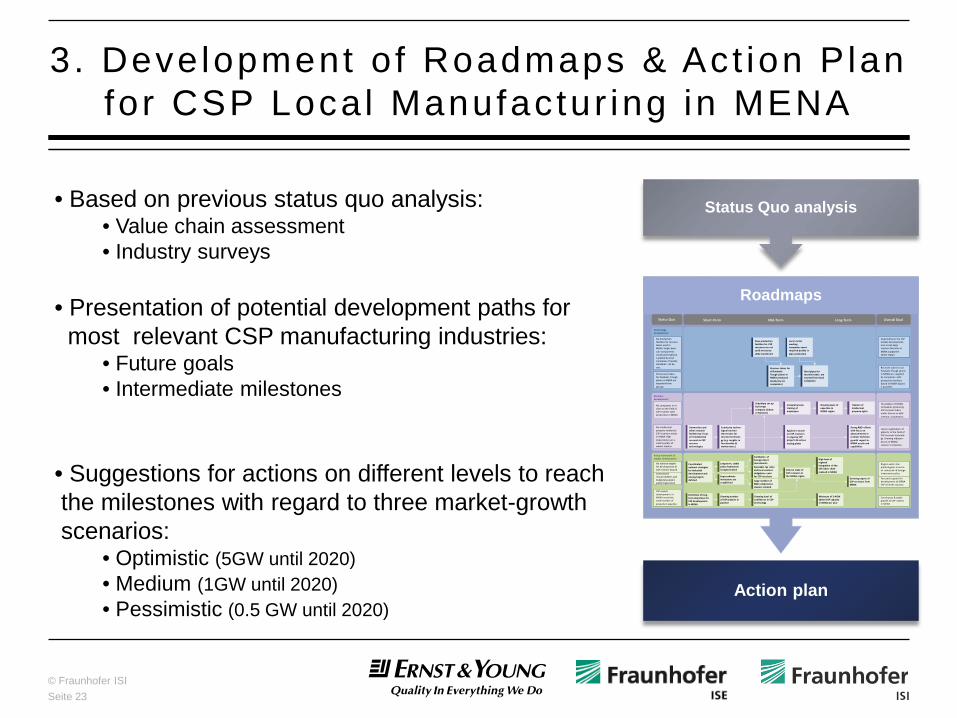

3 . Development o f Roadmaps & Act ion Plan for CSP Local Manufactur ing in MENA

• Based on previous status quo analysis:• Value chain assessment• Industry surveys

• Presentation of potential development paths for most relevant CSP manufacturing industries:

• Future goals • Intermediate milestones

• Suggestions for actions on different levels to reach the milestones with regard to three market-growth scenarios:

• Optimistic (5GW until 2020)• Medium (1GW until 2020)• Pessimistic (0.5 GW until 2020)

Status Quo analysis

Action plan

RoadmapsShort-Term Mid-Term Long-Term

Policy framework & market development

No production facilities for receiver tubes exist in MENA. Single basic sub-components could potentially be supplied by local companies if quality standards can be met.

Business development

Technology development

All receiver tubes for Parabolic Trough plants in MENA are imported from abroad

No companies in or close to the field of CSP receiver tube production in MENA

CSP market development in MENA uncertain, small number of projects in pipeline

Depending on the CSP market development, one or two large receiver factories in MENA supply the whole region.

Region-wide clear political goals in terms of industrial- & foreign investment policy

Continuous & stable growth of CSP market in MENA

Focused support for development of MENA CSP receiver industry

Status Quo Overall Goal

No national targets for development of CSP receiver branch

No intellectual property related to CSP receivers exists in MENA. High dependency on a small number of market leaders

Future registration of patents in the field of CSP receiver technolo-gy. Growing indepen-dence of MENA receiver companies.

Foundation of MENA companies producing CSP receiver tubes under license or with internat. cooperation

New production facilities for CSP receivers are set up & necessary skills transferred

Universities and other research facilities lay focus on fundamental research in CSP receiver technologies

Minimum of 2-4GW added CSP capacity in MENA per year

Growing number of CSP projects in pipeline

Coordinated national strategies for industrial development and energy targets defined

Superordinateinstitutions are established

Facilitation of foreign direct investments

Definition of long-term objectives for CSP development in MENA

Large number of R&D competence clusters created

Institutional responsibilities and budgetary powers partly fragmented

Intense trade of CSP receivers in the MENA region

Favorable tax rates and local content obligations exist for CSP receivers

Growing level of confidence in CSP technology

Long-term, stable policy framework is implemented

High level of regional integration of the CSP value chain realized in MENA

Strong R&D efforts with focus on advancements in receiver technolo-gy with regard to MENA needs and capabilities

Steel pipes for receiver tubes are sourced from local companies

Receiver tubes for all Parabolic Trough plants in MENA produced locally (by int. companies)

Growing export of CSP receivers from MENA

Receiver tubes for all Parabolic Trough plants in MENA are supplied by companies with production facilities based in MENA. Export is possible.

Growing level of expertise in MENA region

Comprehensive training of employees

Subsidiary set up by foreign company (Schott or Siemens)

Applied research on CSP receivers in ongoing CSP projects & various testing plants

Transfer of intellectual property rights

Local metal-working companies meet required quality in pipe production

Conducive techno-logical environ-ment exists for receiver technolo-gy (e.g. insights in functionality & maintenance)

© Fraunhofer ISISeite 24

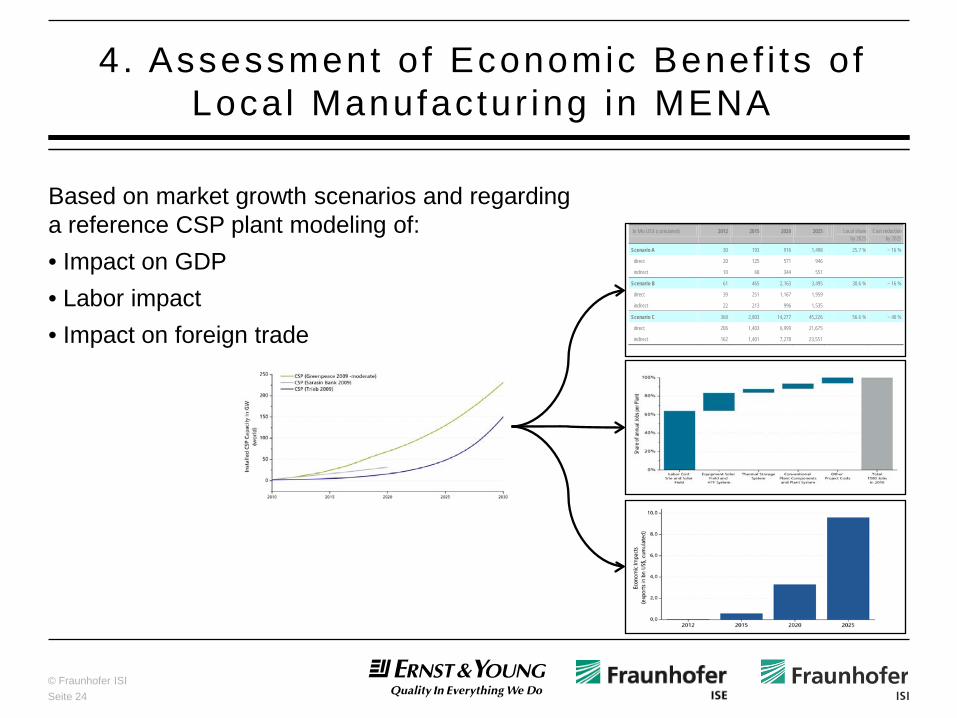

Based on market growth scenarios and regarding a reference CSP plant modeling of: • Impact on GDP• Labor impact• Impact on foreign trade

4 . Assessment o f Economic Benef i ts o f Local Manufactur ing in MENA

In Mio US$ (cumulated) 2012 2015 2020 2025 Local share by 2025

Cost reduction by 2025

Scenario A 30 193 916 1,498 25.7 % ~ 16 %

direct 20 125 571 946

indirect 10 68 344 551

Scenario B 61 465 2,163 3,495 30.6 % ~ 16 %

direct 39 251 1,167 1,959

indirect 22 213 996 1,535

Scenario C 368 2,803 14,277 45,226 56.6 % ~ 40 %

direct 206 1,403 6,999 21,675

indirect 162 1,401 7,278 23,551