LIMA GLOBAL LICENSING INDUSTRY SURVEY 2015 · PDF filecompanies subject matter expertise in...

25

www.licensing.org Commissioned by LIMA GLOBAL LICENSING INDUSTRY SURVEY 2015 REPORT Prepared by Brandar Consulting LLC

Transcript of LIMA GLOBAL LICENSING INDUSTRY SURVEY 2015 · PDF filecompanies subject matter expertise in...

www.licensing.org

Commissioned by

LIMA GLOBALLICENSING INDUSTRY SURVEY

2015 REPORTPrepared by Brandar Consulting LLC

Table of ConTenTs

From the LImA PresIdent ....................................................................................3

BACKGroUnd & stUdY sCoPe.............................................................................3

eXeCUtIVe sUmmArY ................................................................................................4

LICensInG trends ....................................................................................................6

ConCLUsIons .............................................................................................................9

stUdY methodoLoGY .............................................................................................9

CAteGorY deFInItIons .........................................................................................10

LICensInG reVenUe tABLes ...............................................................................12

APPendIX Product Category trends: A Brandar Analysis ...................................17

ABoUt LImA .................................................................................................................24

LIMa GLoBaL LICensInG InDUsTRY sURVeY 2015 RePoRT 3

fRoM The LIMa PResIDenTdear Licensing Colleague:

LImA is proud to present its first-ever detailed study of the global licensing industry to you. one of LImA’s main goals is to provide reliable fact-based statistical data to help licensing professionals successfully plan for the future. Accordingly, we feel this study will provide you with an excellent and relevant tool on which to base your future marketing plans.

this finished product is the result of months of preparation, collaboration, planning, surveying, collating and interpreting, conducted on LImA’s behalf by Brandar Consulting LLC. We selected Brandar based upon its long-standing expertise in the licensing business and in conducting high quality research. Brandar is an 8-year old consulting firm committed to providing companies subject matter expertise in the areas of Brand Licensing, market research, market Analysis, Brand extension and Business strategy. the firm specializes in helping organizations start or proactively expand Brand/trademark licensing programs. the key components in its suite of services are conducting brand equity & category extension research, in-licensing brand identification research, product market analysis, modeling brand royalty potential and conducting factor analysis to set priorities for Licensing Plans.

the survey process included an extensive online questionnaire in six languages, several hundred phone calls to key licensors and agents within all the different property categories, and the examination of a wide variety of publicly-available financial data, import figures and other source material.

As the authoritative voice of the worldwide licensing industry, LImA understands that knowledge and accurate information are the keys to success in this complex, diverse and competitive business. this definitive study is one of the many services provided by LImA to the worldwide licensing community.

For more information on LImA programs and activities, please visit us at www.licensing.org. For those of you who participated, we offer you our sincere thanks.

Best regards,

Charles m. riottoPresident, LImA

BaCKGRoUnD & sTUDY sCoPeIn early 2015, LImA contracted with Brandar Consulting, LLC to complete the challenging task of accurately sizing the global Licensing market. this inaugural analysis is a bottom-up model that sizes the worldwide licensing industry by property type and product category.

the data in this report was derived from a combination of responses to our own market research survey, which was fielded in April, 2015, and recent publicly reported industry data. some 325 companies responded to our survey: 110 licensors, 125 licensees and 90 agents/consultants. the survey was fielded on-line in 6 different languages and supplemented with in-language phone interviews that resulted in reported revenues representing all major geographic regions. In all, our analysis includes specific data from 490 companies spanning the globe in the licensing industry. on top of a regional view, our report also highlights Licensed Product retail revenue and royalty data from the top 50 countries worldwide.

LIMa GLoBaL LICensInG InDUsTRY sURVeY 2015 RePoRT 4

eXeCUTIVe sUMMaRYGlobal retail sales of licensed merchandise and services in 2014 reached $241.5B, generating $13.4B in royalty revenue for the owners of the trademarks.

the top licensing property type in our worldwide study is Character & entertainment coming in with a 44.4% share of the licensed retail market with disney’s properties being a key share driver in this category. the Corporate trademarks property segment also turned out to be very sizable at 22.4% of total retail revenues. Fashion was the next largest licensed property type at 12.7% of the market, while sports Properties registered at a 9.7% share. [see Chart A below.]

on the product side of our analysis, Apparel (16.2%), toys (13.5%) and Accessories (11.6%) were the clear leading retail revenue share categories of licensed products. the size of the home décor/domestics Category which was driven by the success of some large direct to retail licensing programs was a very healthy 7.2% of the market and we expect this category to grow in future years. [see Chart B on page 5.]

on a regional basis, north America is the dominant market for licensed goods, accounting for 58% of global retail sales, followed by northern europe (13.3%) and northern Asia (7.9%). [see Chart C on page 5.]

$107,185

$54,109

$30,784

$23,398

$12,876

$4,625 $3,359

$2,360 $1,761 $1,080 Entertain/Characters

Corporate/BrandFashionSportsPublishingCollegiateCelebrityMusicArtNon- Profit

(in millions US$)

Global Retail Sales of Licensed Merchandise, By Property Type, 2014

Chart A

LIMa GLoBaL LICensInG InDUsTRY sURVeY 2015 RePoRT 5

$39,049

$32,511

$27,944

$17,489 $15,095

$14,843

$10,699

$9,667

$8,568

$8,555

$8,525

$8,404

$7,925 $6,846

$6,282

$4,039 $3,780

$11,314

Apparel

Toys

Accessories- Fashion

Home Décor

Software/ Video games/apps

Food and Beverage

CE

Health and Beauty

Sports

Publishing

Footwear

Gifts

Paper Products

Music/Video

Housewares

Infant

Promotions

Other(in millions US$)

Global Retail Sales of Licensed Merchandise, By Product Category, 2014

$140,107

$32,231

$18,968

$15,531

$10,414

$9,633 $8,330 $5,420 $903

Global Retail Sales of Licensed Merchandise, By Region, 2014

N. America (58%)Northern Europe (13.3%)N Asia (7.9%)Southern Europe (6.4%)LATAM (4.3%)SEA/PAC (4.0%)Eastern Europe (3.4%)ME/Africa (2.2%)ROW (0.4%)

(in millions US$)

$140,107

$32,231

$18,968

$15,531

$10,414

$9,633 $8,330 $5,420 $903

Global Retail Sales of Licensed Merchandise, By Region, 2014

N. America (58%)Northern Europe (13.3%)N Asia (7.9%)Southern Europe (6.4%)LATAM (4.3%)SEA/PAC (4.0%)Eastern Europe (3.4%)ME/Africa (2.2%)ROW (0.4%)

(in millions US$)

Chart B

Chart C

LIMa GLoBaL LICensInG InDUsTRY sURVeY 2015 RePoRT 6

LICensInG TRenDsone of the most encouraging signs we saw in our study was the strong year over year growth in licensed product sales reported by survey respondents. since this was the first-ever LImA Global sizing study, we asked respondents to compare their 2014 licensed product sales with those they generated in 2013. here are their aggregate responses, broken down by region:

Country % chg. ’13 to ’14

Us/Canada 14.74%LAtAm 11.20%europe 6.51%n Asia 17.75%seA/PAC 10.49%me/Africa 21.45%total 15.00%

the greatest licensing sales growth was reported in developing regions of north Asia and me/Africa, while the slowest growth occurred in europe as the region slowly recovers from its recession.

We also asked respondents to let us know what percentage of their sales of licensed products occurred via brick & mortar retail vs. e-commerce. not surprisingly, responses showed continuing rapid growth in on-line sales. on-line sales in China, as a result of developing broadband connections throughout the country and the strength of Alibaba, account for 33% of retail sales of licensed goods, the highest in the world by a wide margin. China could be a microcosm as to how the rest of the developing world could quickly adopt e-commerce platforms over traditional brick & mortar retail product distribution models because of the efficiency advantages of the e-distribution model. We have seen indications in our research that India could be following China along this path.

Country Brick & mortar on-line

Us/Canada 74.3% 25.7%LAtAm 82.5% 17.5%europe 80.3% 19.7%n Asia 83.6% 16.4%seA/PAC 92.6% 7.4%me/Africa 92.5% 7.5%total 83.6% 16.4%

one major insight emerging from our analysis is that digital technology is clearly changing the way in which consumers play and entertain themselves. Certain licensed products are now predominantly purchased and distributed through electronic means and are starting to become a much more significant share of the overall licensed product market, with the tablet and smart phone even changing the way that kids are watching entertainment programming. the combining of disney’s consumer and interactive products divisions underscores the blurring of the lines of children’s entertainment and play. the Video Games/software/Apps, Publishing and music/Video categories, distributed mostly digitally now, taken together now compromise over 12% of licensed product share.

Interestingly, as these digital segments continue to grow, they are making licensed products much more accessible to the rest of the world due to their ease of distribution in broadband connected countries. As a result of this phenomenon, north America’s share (58.0%) of licensed product sales in our study came in lower than many have previously thought, with additional share being spread to places like europe (23.1%), Latin America (4.3%) and the middle east/Africa (2.2%). Furthermore, we anticipate share in the Asia Pac region (11.9%), given its huge population, will accelerate significantly over time as these countries continue to develop economically and broadband connections become more widespread. We believe increased broadband connectivity will allow not only for more digital consumption, but also more on-line ordering of licensed products from websites like Alibaba and Amazon’s international sites.

one important question we asked respondents to the survey was to let us know about licensing industry trends, both for the industry in general as well as for their own companies.

LIMa GLoBaL LICensInG InDUsTRY sURVeY 2015 RePoRT 7

General Industry Trends

• While many cited the overwhelming success of disney’s licensing of Frozen, it was viewed as both a blessing and a curse. on the positive side it “brought the understanding back to retailers that they can sell a character license throughout the store”. on the negative side for some, Frozen was viewed as “freezing out” other attractive licenses as retailers were too overwhelming in their support of the property at the expense of placing other licensed goods on the shelf.

• once a licensing flagship category, Pre-school licensing properties appear to be making a comeback as many respondents cited the re-emergence of this sector as an exciting trend with mattel being mentioned as the major presence in the category.

• Food & Beverage Category brand licensing continues to be strong and many respondents spoke of – in the words of one – a “strong move toward better-for-you and organic brands.”

• It continues to get harder to get high minimum guarantees or advances as licensees want licensing to be “a shared risk busi-ness proposition” with the Licensor.

• Licensees are expecting the Licensor to provide additional resources to sell licensed products into retail and then to support the branded products once they are on-shelf. many stated that licensed brands need to be supported and promoted at retail by the licensor as much as by the licensee. “there simply needs to be more involvement from Licensors and brand owners to make licensed brands relevant for retailers.”

• there continues to be strong interest from private equity or venture backed management firms in the acquisition of trademarks with strong equity that may have gone dormant or fallen on hard times.

• oversaturation of entertainment and Celebrity properties was mentioned as a negative trend minimizing available shelf space for all. one respondent coined this sheer “brand fatigue”.

• major concerns were voiced by licensees about the lack of licensors policing unofficial products being sold on-line.

• respondents also talked about piracy of licensed goods being a “big” problem and “raging” in the Asia region, which certainly poses a significant risk to brand owners.

• As the U.s. licensing market gets increasingly saturated, there is more of an emphasis on globalization as the key to future licensing growth. A number of respondents mentioned an uplift in licensing sales in europe as the economy improves there. still others talked about concentrating on growing India and China as new licensing markets. But some spoke of unfavorable foreign exchange rates and social and political strife as being gating factors mitigating international growth right now.

• some respondents cited the difficulty of growing the licensing business in south America because a number of countries do not allow in-country licensees or distributors of licensed products to pay royalties outside their country.

• mass market price deflation is forcing the need to add more value into the licensed product feature set for the same price as generics to gain a point of difference. Brand licensing also was cited as a point of difference that can hold pricing steady.

• more large brand owners are seeking out boutique licensing agencies because they feel they can get better focus and more dedicated resources from a smaller agent.

• the classic video game market has fallen off significantly around the world with the decline in sales of game consoles with many hoping newer consoles will help turn this tide.

LIMa GLoBaL LICensInG InDUsTRY sURVeY 2015 RePoRT 8

Distribution Trends

We also asked respondents to comment on the distribution trends for the industry at large, and for their own companies:

• the rapid growth in on-line sales over brick and mortar sales was an overwhelming trend here and reinforced by the numbers we reported above. one respondent mentioned part of what is feeding the trend is that “consumers are now more confident buying on-line that which they bought in stores in the past.”

• some spoke of the difficulties that come along with e-commerce, such as the challenge of conveying the quality of their prod-uct when it is only viewed on the web. Licensors also spoke of whether they should allow their licensees to control the on-line experience through several different websites or if it is better for the brand owner to centralize and standardize the direct on-line buying experience into one website they control.

• not a lot of sales happen on brand-owner-operated sites as most prefer to shop general websites like Amazon, but the licens-ee’s website is still viewed as one of the best sources of on-line research prior to purchase.

• the importance of incorporating younger generations of marketing professionals into your on-line marketing team was dis-cussed by some as they are more attune to social networking and the on-line Pr management issues (e-Pr).

• some respondents cited that on-line retailers internationally are asking for “huge amounts of listing and registration money.”

• Concerns were voiced that smaller and independent retailers are continuing to contract their store locations – another trend making it difficult for newer licensed brands to make it to the shelf. Less shelf space to manage is making these retailers less willing to carry licensed products than their larger competitors.

• more new licensed properties are willing to do direct-to-retail (dtr) deals just to get their licensing programs off the ground.

• And “more retailers are looking for dtr licensing opportunities, but are not necessarily equipped to manage the process.” so licensors need to go into these opportunities mindful that they will need to assist their partners in process management and quality control.

• some spoke of the constant change in buyers at retailers and therefore needing buy-in from top level management to ensure licensed programs get continuing retailer support even if buyers change. others viewed this as a favorable trend, causing more senior managers at retailers to approve multiple product lines for one brand at the same time.

• Pursuing a multi-channel approach and selling to the consumer via whatever channel or combination of channels that they wish to engage in is becoming vital to competing and even gaining an advantage on your competition.

• e-commerce growth in China and India was cited as a significant opportunity/challenge – as licensees have to engage with an entirely different set of e-retailers in those regions. Both countries have really embraced on-line retail as “retailers find it easier to list and sell on-line” vs. building out a brick and mortar infrastructure in those countries.

• some respondents noted that the “right” licensed product can get better positioning on shelf and get better locations in retail stores than their traditional branded competitors.

• As it gets more and more difficult for new licensed brands to get on-shelf at the major retail chains because of the retailers’ unwillingness to take risks on a property that is not a sure thing, more non-traditional channels are embracing newer licensed brands.

° “Grocery and convenience stores are increasing their assortments. “

° “QVC and hsn saw a big rise in personality brands last year.”

° “on-line retail, both traditional and flash sale sites, continues to grow.”

° “drug stores, such as Walgreens and rite Aid, are elevating their in-store aesthetic experience to be more of a destination for health and beauty products.”

° even off-price stores such as “tJX and ross are improving their perception as a destination for a wide assortment of brands.”

° one Ce Licensee even noted that they have “grown their business recently by successfully branching out from traditional Ce retailers into the Pharmacy and supermarket channels.”

• In an effort to improve margins, many manufacturers are distributing directly to retailers now.

LIMa GLoBaL LICensInG InDUsTRY sURVeY 2015 RePoRT 9

ConCLUsIonsthe worldwide licensing industry is becoming increasingly global with much of the new opportunity outside of the more saturated north American market. economies are finally starting to rebound on a more global basis leading to strong growth trends in the licensing industry. non-traditional retail channels and on-line commerce are and will be key sources of growth going forward. direct-to-retail license agreements continue to be an important mechanism to break into retail because they offer retailers something unique in a declining brick and mortar shelf space environment and enable new brands to gain a foothold into the retail market. As physical shelf space contracts, on-line shelf space is multiplying at a very rapid pace. the impact of digital product distribution is impacting the way we live, consume and entertain ourselves and that is serving to accelerate the globalization of our industry. And finally, on-line e-commerce is turning into the key distribution channel for licensed goods in developing markets as broadband infrastructure is being put in place ahead of traditional brick and mortar retail locations. LImA’s inaugural International Licensing market size study clearly shows in all facets that the $241 Billion licensing industry is alive and well and that’s exciting news for all industry participants.

sTUDY MeThoDoLoGYIn order to meet this year’s objective of estimating global retail licensing revenues and royalties, input from licensors, licensees and agents in all the major countries were needed. therefore, we used a multi-dimensional methodology to assure sufficient input to deliver accurate estimates.

PRIMARY RESEARCH

We first started with an anonymous on-line survey similar to the survey used in the past for the Us/Canada estimates. however, we needed to modify the survey to accommodate revenues from multiple countries and multiple languages. the survey and email invitations were prepared in 6 languages – english, French, Italian, German, spanish, Japanese and Chinese – with each respon-dent having the choice of language of the survey. email and postal invitations to the survey were mailed to members and non-members from LImA’s database. Additionally, press releases were issued with survey links in major industry communications.

to insure the best response rates, sIs International was contracted to conduct telephone interviews of companies in major coun-tries in the language of the respondent’s choice for those who did not have time or desire to complete the on-line survey. the on-line survey was active during the months of march and April 2015 with telephones interviews conducted during April 2015. Between the on-line survey and telephone interviews, data was collected from approximately 325 companies responded to our survey: 110 licensors, 125 licensees and 90 Agents/consultants reporting revenues in 24 countries and all major regions.

SECONDARY RESEARCH

the next step in the research process was to fill in the gaps for major companies in the licensing industry that did not participate in the surveys. top licensing revenue companies (licensors and licensees) were identified and compared to the respondents to the surveys. major companies that did not respond were researched for publicly available licensing data. We used sources that included IBIs World, morningstar, statista, and hoover’s along with company websites, annual reports and Pr releases. In total, 490 companies’ data was collected through both the primary and secondary research methods.

MODELING/MISSING DATA

even with the most thorough research not all information can be obtained in a study of this breadth. to fill in the gaps we used industry, government census and company level data. since this study includes 100% of the Global market we needed to account for countries that did not have directly reported data. In some cases companies only reported data at a regional level so we needed to allocate their revenues to individual countries. Where country level data was not available we used an allocation model that considered several sources including ItC Imports by product category, country level GdP and Global retail revenues by country as well as the results from the 330 participants who answered the survey. A similar model using additional sources was used to allocate high level revenues to Property types and Product Categories where needed. this process allows us to estimate Licensing retail revenue and royalties by product category within each property type by country.

ROYALTY REVENUES

our models concentrated on deriving Licensed retail revenues. this report also includes royalty revenues. When actual roy-alty revenues were not provided, we used a formula to calculate royalties from retail revenues. since royalties are calculated off wholesale revenues, we first used retail gross margins by product category to derive wholesale revenues. We then applied average royalty rates for each product category to derive estimated royalty revenues.

LIMa GLoBaL LICensInG InDUsTRY sURVeY 2015 RePoRT 10

CaTeGoRY DefInITIonsPROPERTY TYPES

ART

Art licensing encompasses everything from individual artists who support their artistic endeavors via licensing to well-established businesses that create art and design specifically to decorate a wide range of products, including prints, home décor, house-wares, textiles, publishing, giftware & apparel.

CELEBRITIES (ENTERTAINMENT/ETC.)

this property includes individuals/groups and the estates of individuals who are primarily well known in the fields of entertainment and other fields such as politics and business.

ENTERTAINMENT/ CHARACTERS

this category of licensing encompasses properties springing primarily from feature films, television shows, videogames and online entertainment. (Characters and franchises that are created via books are also a popular licensing category, but are gener-ally classified as “publishing” properties.)

COLLEGIATE

this property includes College and University logos, names and slogans. Licensing programs usually target alumni with greater variety of merchandise rather than just current college students.

FASHION

the licensing of designer fashion names and brands into such categories as apparel, fashion accessories, health & beauty aids and home goods is one of the best known facets of the business.

MUSIC

Product licensing and merchandising based on musical groups, musicians and their works. (does not include the licensing of music itself for advertising and other commercial purposes.)

NON-PROFIT

Licensing of non-profit organizations such as museums, churches, charity and special interest organizations such as the AsPCA.

SPORTS (LEAGUES/INDIVIDUALS)

this includes:

major sports leagues — i.e. national Football League, major League Baseball, national Basketball Association and the national hockey League – along with nAsCAr. each of those leagues runs the licensing business on behalf of its teams out of a central-ized league office.

smaller professional sports leagues – organizations such as the International olympic Committee and major sports events such as the olympics and FIFA World Cup, as well as athletes.

CORPORATE/BRAND NAME

the licensing of company names, logos, trademarks or brands (i.e. harley-davidson, Coca-Cola).

PUBLISHING

this type of property includes any brand or character that exists in print media (magazines, books, newspaper, etc.). once a pub-lishing property migrates to other media such as movies, tV, apps, video games the property is re-classified under entertainment/Characters Properties.

LIMa GLoBaL LICensInG InDUsTRY sURVeY 2015 RePoRT 11

PRODUCT CATEGORIES

Accessories, Fashion (e.g. small leather goods, jewelry, luggage, bag, purses, belts, hats, etc.)

Apparel (e.g. tops, bottoms, dresses, menswear, outerwear, etc.)

Consumer Electronics (e.g. audio and video equipment, computers and computer accessories, cellphone cases, headphones, etc.)

Food/Beverage (e.g. coffee, yogurt, breakfast cereal, cake mixes, soft drinks, wine & spirits etc.)

Footwear (e.g. slippers, sneakers, children’s shoes, etc.)

Gifts/Collectibles

Health/Beauty Products (e.g. fragrances, skin care, shaving goods, hair care, etc.)

Home Décor (e.g. Furniture/Furnishings, wall hangings, kitchen/bath/bed domestics, wall art, floor coverings, etc.)

Housewares (e.g. small electrics, kitchen accessories, cooking utensils, pots, pans, flatware, glassware etc.)

Infant Products (e.g. layette, diapers, infant apparel, baby care products, strollers etc.)

Music/Video (e.g. dVds, Cds, streams, etc.) *does not refer to the licensing of music itself i.e. for muzak, commercials, etc.

Paper Products/School Supplies (e.g. notebooks, party goods, greeting cards, posters, prints etc.)

Promotions (refers to licensing of a property for the purpose of promoting/advertising a product )

Publishing (e.g. books, comics, magazines, etc.)

Software and Video Games (e.g. apps, console-based games, mobile games, computer games, etc.)

Sporting Goods (e.g. athletic equipment, balls, etc.)

Toys/Games (not software/Video) (e.g. action figures, board games, toy vehicles, dolls etc.)

COUNTRY/REGIONS

REGION COUNTRIES FROM TOP 50 COUNTRIES FROM REST OF WORLD (ROW) (In order of Retail Sales volume)

north America Us and Canada

northern europe Germany, UK, the netherlands, Belgium, switzerland, sweden, norway, Ireland, denmark, Finland

southern europe France, Italy, spain, Austria, turkey, Portugal, Greece

eastern europe russia, Poland, Czech republic, slovakia, Ukraine, hungary, romania, Kazakhstan

Lithuania, Bulgaria, Belarus, Latvia, slovenia, Croatia, estonia, serbia, Bosnia and herzegovina, Georgia, Albania, moldova, macedonia, Armenia, montenegro

LAtAm mexico, Brazil, Chile, Columbia, Peru, Venezuela

Argentina, ecuador, Paraguay, Panama, dominica republic, Costa rica, Guatemala, el salvador, Uruguay, honduras, Jamaica, netherland Antilles, Bolivia, nicaragua, Aruba, Bahamas, trinidad and tobago, Cuba, Barbados, haiti, Bermuda, BVI, Cayman, Antigua and Barbuda, Belize, st Lucia, turk and Caicos, st Kitts, dominica, Grenada, st Vincent and Grenadines, Anguilla

n Asia China, hong Kong, Japan, taiwan north Korea, mongolia

southeast Asia/PAC Australia, new Zealand, south Korea, singapore, Viet nam, India, malaysia, thailand

Indonesia, Philippines, myanmar, Bangladesh, macao, Pakistan, tajikistan, sri Lanka, Kyrgyzstan, nepal, Brunei, new Caledonia, Cambodia, new Guinea, Lao, French Polynesia, Fiji, maldives, Cook Is, marshall Is. samoa, micronesia

LIMa GLoBaL LICensInG InDUsTRY sURVeY 2015 RePoRT 12

LICensInG ReVenUe TaBLes – GLoBaL LICensInG ReTaIL ReVenUesPr

oper

tyTo

tal

Acce

ssor

ies-

Fash

ion

Appa

rel

CEFo

od an

d Be

vera

geFo

otwe

arHe

alth

and

Beau

tyHo

me

Déco

rHo

usew

ares

Infa

ntMu

sic/V

ideo

Softw

are/

Vide

o ga

mes

/apps

Pape

r Pr

oduc

tsPu

blish

ing

Spor

tsTo

ysGi

ftsPr

omot

ions

Othe

r

Art

$ 1,7

61

$ 13

3

$ 19

2

$

21

$ 74

$ 8

$ 15

$ 16

7

$

129

$

21

$ 26

$ 33

$ 28

2

$

101

$ 18

$

195

$ 25

7

$

5

$

85

Celeb

rity $

3,359

$

444

$

696

$ 53

$

299

$ 12

6

$ 30

6

$ 18

3

$

227

$

51

$ 40

$ 80

$ 38

$ 18

1

$

158

$ 17

1

$

125

$ 44

$ 13

8

Enter

tain/C

hara

cters

$ 10

7,185

$ 8,5

07

$ 12,7

57

$ 3,5

15

$

5,541

$ 2,5

42

$

3,029

$

3,206

$ 1,3

15

$ 2,8

47

$

6,034

$

8,987

$

5,221

$ 6,6

32

$ 2,4

72

$

26,91

0

$ 3,8

04

$

2,592

$

1,273

Colle

giate

$ 4,6

25

$ 75

0

$ 85

0

$

2

$

7

$ 16

7

$ 2

$ 25

2

$

665

$

1

$

2

$

417

$ 85

$ 1

$

581

$ 50

6

$

332

$ 1

$ 4

Fash

ion $

30,78

4

$ 9,5

77

$ 8,4

28

$

624

$

177

$ 3,2

90

$

3,715

$

1,564

$ 56

9

$ 48

9

$ 30

$ 19

8

$

461

$ 41

9

$

72

$ 57

3

$

365

$ 10

2

$ 13

3

Music

$ 2,3

60

$ 38

5

$ 1,3

17

$

27

$ 68

$ 10

$

18

$

22

$ 28

$ 8

$ 30

$ 43

$ 29

$ 18

8

$

20

$ 98

$

22

$ 5

$ 43

Non-

Pro

fit $

1,080

$

134

$

167

$ 27

$

58

$

18

$ 77

$ 30

$

37

$

6

$

40

$

47

$

21

$

23

$

35

$ 12

1

$

60

$ 56

$ 12

3

Spor

ts $

23,39

8

$ 2,8

85

$ 6,8

03

$

373

$

212

$ 48

7

$ 54

$ 64

$

367

$

129

$

305

$

3,834

$

959

$ 23

4

$

3,254

$ 1,5

46

$

1,384

$ 18

0

$ 32

5

Corp

orate

/Bra

nd $

54,10

9

$ 4,9

95

$ 7,6

26

$

6,033

$ 8,3

70

$

1,799

$ 2,4

20

$ 1,3

70

$

2,824

$

471

$

335

$

1,427

$

810

$ 75

1

$

1,922

$ 2,3

43

$

2,028

$ 78

2

$ 7,8

04

Publi

shing

$ 12

,876

$

135

$

214

$ 25

$

37

$

77

$ 30

$ 10

,632

$

121

$

17

$ 4

$ 28

$ 20

$ 24

$ 37

$

48

$ 28

$

14

$

1,387

TOTA

L W

W $

241,5

38

$

27,94

4

$ 3

9,049

$ 1

0,699

$

14,84

3

$ 8,5

25

$

9,667

$

17,48

9

$ 6,2

82

$ 4,0

39

$

6,846

$

15,09

5

$ 7,9

25

$

8,555

$

8,568

$ 32

,511

$

8,404

$ 3,7

80

$ 11,3

14

Prop

erty

Tota

l %

Acce

ssor

ies-

Fash

ion

Appa

rel

CEFo

od an

d Be

vera

geFo

otwe

arHe

alth

and

Beau

tyHo

me

Déco

rHo

usew

ares

Infa

ntMu

sic/V

ideo

Softw

are/

Vide

o ga

mes

/apps

Pape

r Pr

oduc

tsPu

blish

ing

Spor

tsTo

ysGi

ftsPr

omot

ions

Othe

r

Art

100.0

%7.5

%10

.9%1.2

%4.2

%0.5

%0.9

%9.5

%7.3

%1.2

%1.5

%1.9

%16

.0%5.7

%1.0

%11

.1%14

.6%0.3

%4.8

%

Celeb

rity10

0.0%

13.2%

20.7%

1.6%

8.9%

3.8%

9.1%

5.4%

6.8%

1.5%

1.2%

2.4%

1.1%

5.4%

4.7%

5.1%

3.7%

1.3%

4.1%

Enter

tain/C

hara

cters

100.0

%7.9

%11

.9%3.3

%5.2

%2.4

%2.8

%3.0

%1.2

%2.7

%5.6

%8.4

%4.9

%6.2

%2.3

%25

.1%3.5

%2.4

%1.2

%

Colle

giate

100.0

%16

.2%18

.4%0.1

%0.2

%3.6

%0.0

%5.4

%14

.4%0.0

%0.0

%9.0

%1.8

%0.0

%12

.6%10

.9%7.2

%0.0

%0.1

%

Fash

ion10

0.0%

31.1%

27.4%

2.0%

0.6%

10.7%

12.1%

5.1%

1.8%

1.6%

0.1%

0.6%

1.5%

1.4%

0.2%

1.9%

1.2%

0.3%

0.4%

Music

100.0

%16

.3%55

.8%1.1

%2.9

%0.4

%0.8

%0.9

%1.2

%0.3

%1.3

%1.8

%1.2

%8.0

%0.8

%4.2

%0.9

%0.2

%1.8

%

Non-

Pro

fit10

0.0%

12.4%

15.4%

2.5%

5.4%

1.7%

7.1%

2.8%

3.4%

0.6%

3.7%

4.3%

1.9%

2.2%

3.3%

11.2%

5.5%

5.2%

11.4%

Spor

ts10

0.0%

12.3%

29.1%

1.6%

0.9%

2.1%

0.2%

0.3%

1.6%

0.5%

1.3%

16.4%

4.1%

1.0%

13.9%

6.6%

5.9%

0.8%

1.4%

Corp

orate

/Bra

nd10

0.0%

9.2%

14.1%

11.1%

15.5%

3.3%

4.5%

2.5%

5.2%

0.9%

0.6%

2.6%

1.5%

1.4%

3.6%

4.3%

3.7%

1.4%

14.4%

Publi

shing

100.0

%1.0

%1.7

%0.2

%0.3

%0.6

%0.2

%82

.6%0.9

%0.1

%0.0

%0.2

%0.2

%0.2

%0.3

%0.4

%0.2

%0.1

%10

.8%

TOTA

L W

W10

0.0%

11.6%

16.2%

4.4%

6.1%

3.5%

4.0%

7.2%

2.6%

1.7%

2.8%

6.2%

3.3%

3.5%

3.5%

13.5%

3.5%

1.6%

4.7%

Prop

erty

Tota

l WW

%Ac

cess

ories

- Fa

shio

n Ap

pare

lCE

Food

and

Beve

rage

Foot

wear

Healt

h an

d Be

auty

Hom

e Dé

cor

Hous

ewar

esIn

fant

Music

/Vid

eoSo

ftwar

e/ Vi

deo

gam

es/ap

psPa

per

Prod

ucts

Publ

ishin

gSp

orts

Toys

Gifts

Prom

otio

nsOt

her

Art

0.7%

0.5%

0.5%

0.2%

0.5%

0.1%

0.2%

1.0%

2.1%

0.5%

0.4%

0.2%

3.6%

1.2%

0.2%

0.6%

3.1%

0.1%

0.8%

Celeb

rity1.4

%1.6

%1.8

%0.5

%2.0

%1.5

%3.2

%1.0

%3.6

%1.3

%0.6

%0.5

%0.5

%2.1

%1.8

%0.5

%1.5

%1.2

%1.2

%

Enter

tain/C

hara

cters

44.4%

30.4%

32.7%

32.8%

37.3%

29.8%

31.3%

18.3%

20.9%

70.5%

88.1%

59.5%

65.9%

77.5%

28.8%

82.8%

45.3%

68.6%

11.2%

Colle

giate

1.9%

2.7%

2.2%

0.0%

0.0%

2.0%

0.0%

1.4%

10.6%

0.0%

0.0%

2.8%

1.1%

0.0%

6.8%

1.6%

4.0%

0.0%

0.0%

Fash

ion12

.7%34

.3%21

.6%5.8

%1.2

%38

.6%38

.4%8.9

%9.1

%12

.1%0.4

%1.3

%5.8

%4.9

%0.8

%1.8

%4.3

%2.7

%1.2

%

Music

1.0%

1.4%

3.4%

0.3%

0.5%

0.1%

0.2%

0.1%

0.4%

0.2%

0.4%

0.3%

0.4%

2.2%

0.2%

0.3%

0.3%

0.1%

0.4%

Non-

Pro

fit0.4

%0.5

%0.4

%0.2

%0.4

%0.2

%0.8

%0.2

%0.6

%0.2

%0.6

%0.3

%0.3

%0.3

%0.4

%0.4

%0.7

%1.5

%1.1

%

Spor

ts9.7

%10

.3%17

.4%3.5

%1.4

%5.7

%0.6

%0.4

%5.8

%3.2

%4.5

%25

.4%12

.1%2.7

%38

.0%4.8

%16

.5%4.8

%2.9

%

Corp

orate

/Bra

nd22

.4%17

.9%19

.5%56

.4%56

.4%21

.1%25

.0%7.8

%45

.0%11

.7%4.9

%9.5

%10

.2%8.8

%22

.4%7.2

%24

.1%20

.7%69

.0%

Publi

shing

5.3%

0.5%

0.5%

0.2%

0.2%

0.9%

0.3%

60.8%

1.9%

0.4%

0.1%

0.2%

0.2%

0.3%

0.4%

0.1%

0.3%

0.4%

12.3%

TOTA

L W

W10

0.0%

100.0

%10

0.0%

100.0

%10

0.0%

100.0

%10

0.0%

100.0

%10

0.0%

100.0

%10

0.0%

100.0

%10

0.0%

100.0

%10

0.0%

100.0

%10

0.0%

100.0

%10

0.0%

Glo

bal R

etai

l Sal

es o

f Lic

ense

d M

erch

andi

se, B

y Pr

oper

ty T

ype

and

Prod

uct C

ateg

ory,

2014

(in

mill

ions

of U

S$)

Glo

bal R

etai

l Sal

es o

f Lic

ense

d M

erch

andi

se, B

y Pr

oduc

t Cat

egor

y, 20

14 (a

s a

perc

enta

ge o

f Pro

pert

y)

Glo

bal R

etai

l Sal

es o

f Lic

ense

d M

erch

andi

se, B

y Pr

oper

ty T

ype,

201

4 (a

s a

perc

enta

ge o

f Pro

duct

Cat

egor

y)

LIMa GLoBaL LICensInG InDUsTRY sURVeY 2015 RePoRT 13

LICensInG ReVenUe TaBLes – GLoBaL LICensInG RoYaLTY ReVenUesPr

oper

tyTo

tal

Acce

ssor

ies-

Fash

ion

Appa

rel

CEFo

od an

d Be

vera

geFo

otwe

arHe

alth

and

Beau

tyHo

me

Déco

rHo

usew

ares

Infa

ntMu

sic/V

ideo

Softw

are/

Vide

o ga

mes

/apps

Pape

r Pr

oduc

tsPu

blish

ing

Spor

tsTo

ysGi

ftsPr

omot

ions

Othe

r

Art

$ 94

$

8

$

12

$

1

$

3

$ 0

$

1

$ 7

$ 7

$ 1

$

1

$

2

$ 16

$ 5

$

1

$ 12

$

13

$ 0

$

4

Celeb

rity $

184

$

26

$ 43

$ 2

$ 11

$ 7

$

17

$

8

$

12

$ 3

$

2

$

5

$ 2

$

10

$

8

$ 10

$

7

$ 3

$

7

Enter

tain/C

hara

cters

$ 6,2

43

$ 51

6

$ 81

6

$ 16

5

$ 21

0

$

139

$ 17

8

$

150

$

69

$ 16

0

$

324

$

589

$ 30

3

$

359

$ 13

4

$

1,701

$ 20

6

$

152

$ 73

Colle

giate

$ 26

4

$ 44

$

52

$

0

$

0

$ 9

$

0

$ 12

$

35

$ 0

$

0

$

27

$

5

$ 0

$

31

$ 31

$

18

$ 0

$

0

Fash

ion $

1,765

$

562

$

517

$

28

$ 6

$

176

$ 21

2

$

72

$ 30

$

27

$ 1

$ 13

$ 26

$ 22

$ 4

$

35

$ 20

$

6

$ 7

Music

$ 13

8

$ 23

$

81

$

1

$

2

$ 1

$

1

$ 1

$ 1

$ 0

$

1

$

3

$ 2

$

10

$

1

$ 6

$

1

$ 0

$

2

Non-

Pro

fit $

55

$ 6

$ 10

$ 1

$ 2

$

1

$ 2

$

1

$

2

$

0

$ 2

$ 3

$

1

$ 1

$

2

$ 7

$

3

$ 3

$

6

Spor

ts $

1,354

$

169

$

410

$

18

$ 8

$

26

$ 3

$

3

$

19

$ 7

$

15

$

236

$ 55

$ 12

$ 17

5

$

95

$ 74

$

10

$

18

Corp

orate

/Bra

nd $

2,710

$

290

$

466

$

264

$

283

$ 91

$

138

$ 62

$

129

$

24

$ 16

$ 89

$ 46

$ 40

$ 10

3

$

140

$ 10

6

$

45

$

379

Publi

shing

$ 61

5

$ 8

$ 13

$ 1

$ 1

$

4

$ 2

$

492

$

6

$

1

$ 0

$ 2

$

1

$ 1

$

2

$ 3

$

1

$ 1

$

75

TOTA

L W

W $

13,42

2

$

1,653

$ 2,42

0 $

482

$

526

$ 45

4

$

553

$ 80

8

$ 31

0

$ 22

3

$

364

$

969

$ 45

6

$

460

$ 46

1

$

2,041

$ 44

9

$

220

$ 57

2

Prop

erty

Tota

l %

Acce

ssor

ies-

Fash

ion

Appa

rel

CEFo

od an

d Be

vera

geFo

otwe

arHe

alth

and

Beau

tyHo

me

Déco

rHo

usew

ares

Infa

ntMu

sic/V

ideo

Softw

are/

Vide

o ga

mes

/apps

Pape

r Pr

oduc

tsPu

blish

ing

Spor

tsTo

ysGi

ftsPr

omot

ions

Othe

r

Art

100%

8.0%

12.5%

1.0%

2.9%

0.5%

0.9%

7.6%

7.0%

1.2%

1.4%

2.3%

16.7%

5.7%

1.0%

12.7%

14.1%

0.3%

4.3%

Celeb

rity10

0%14

.2%23

.2%1.3

%5.9

%3.7

%9.5

%4.6

%6.4

%1.5

%1.0

%2.8

%1.2

%5.2

%4.6

%5.7

%3.6

%1.4

%4.1

%

Enter

tain/C

hara

cters

100%

8.3%

13.1%

2.6%

3.4%

2.2%

2.8%

2.4%

1.1%

2.6%

5.2%

9.4%

4.8%

5.7%

2.2%

27.2%

3.3%

2.4%

1.2%

Colle

giate

100%

16.7%

19.7%

0.0%

0.1%

3.4%

0.0%

4.4%

13.1%

0.0%

0.0%

10.2%

1.8%

0.0%

11.8%

11.8%

6.7%

0.0%

0.1%

Fash

ion10

0%31

.9%29

.3%1.6

%0.4

%10

.0%12

.0%4.1

%1.7

%1.5

%0.1

%0.7

%1.5

%1.3

%0.2

%2.0

%1.1

%0.3

%0.4

%

Music

100%

16.3%

58.4%

0.9%

1.8%

0.4%

0.8%

0.7%

1.0%

0.3%

1.0%

2.0%

1.2%

7.2%

0.8%

4.4%

0.8%

0.2%

1.7%

Non-

Pro

fit10

0%11

.0%18

.5%2.2

%3.8

%1.7

%4.0

%2.5

%3.5

%0.6

%3.5

%5.5

%2.2

%2.2

%3.4

%13

.4%5.8

%5.8

%10

.4%

Spor

ts10

0%12

.5%30

.3%1.4

%0.6

%1.9

%0.2

%0.2

%1.4

%0.5

%1.1

%17

.4%4.0

%0.9

%12

.9%7.0

%5.5

%0.8

%1.3

%

Corp

orate

/Bra

nd10

0%10

.7%17

.2%9.7

%10

.4%3.3

%5.1

%2.3

%4.8

%0.9

%0.6

%3.3

%1.7

%1.5

%3.8

%5.2

%3.9

%1.7

%14

.0%

Publi

shing

100%

1.3%

2.1%

0.2%

0.2%

0.7%

0.3%

80.0%

1.0%

0.1%

0.0%

0.3%

0.2%

0.2%

0.3%

0.5%

0.2%

0.1%

12.2%

TOTA

L W

W10

0%12

.3%18

.0%3.6

%3.9

%3.4

%4.1

%6.0

%2.3

%1.7

%2.7

%7.2

%3.4

%3.4

%3.4

%15

.2%3.3

%1.6

%4.3

%

Prop

erty

Tota

l WW

%Ac

cess

ories

- Fa

shio

n Ap

pare

lCE

Food

and

Beve

rage

Foot

wear

Healt

h an

d Be

auty

Hom

e Dé

cor

Hous

ewar

esIn

fant

Music

/Vid

eoSo

ftwar

e/ Vi

deo

gam

es/ap

psPa

per

Prod

ucts

Publ

ishin

gSp

orts

Toys

Gifts

Prom

otio

nsOt

her

Art

0.7%

0.5%

0.5%

0.2%

0.5%

0.1%

0.1%

0.9%

2.1%

0.5%

0.3%

0.2%

3.4%

1.2%

0.2%

0.6%

3.0%

0.1%

0.7%

Celeb

rity1.4

%1.6

%1.8

%0.5

%2.1

%1.5

%3.2

%1.0

%3.8

%1.3

%0.5

%0.5

%0.5

%2.1

%1.8

%0.5

%1.5

%1.1

%1.3

%

Enter

tain/C

hara

cters

46.5%

31.2%

33.7%

34.2%

39.8%

30.6%

32.1%

18.5%

22.2%

71.7%

89.2%

60.8%

66.3%

77.9%

29.1%

83.3%

45.9%

69.0%

12.8%

Colle

giate

2.0%

2.7%

2.2%

0.0%

0.0%

2.0%

0.0%

1.4%

11.2%

0.0%

0.0%

2.8%

1.1%

0.0%

6.7%

1.5%

4.0%

0.0%

0.0%

Fash

ion13

.1%34

.0%21

.4%5.8

%1.2

%38

.9%38

.2%9.0

%9.6

%12

.0%0.4

%1.3

%5.8

%4.8

%0.8

%1.7

%4.3

%2.7

%1.3

%

Music

1.0%

1.4%

3.3%

0.3%

0.5%

0.1%

0.2%

0.1%

0.5%

0.2%

0.4%

0.3%

0.4%

2.2%

0.2%

0.3%

0.3%

0.1%

0.4%

Non-

Pro

fit0.4

%0.4

%0.4

%0.2

%0.4

%0.2

%0.4

%0.2

%0.6

%0.2

%0.5

%0.3

%0.3

%0.3

%0.4

%0.4

%0.7

%1.5

%1.0

%

Spor

ts10

.1%10

.3%17

.0%3.8

%1.5

%5.8

%0.6

%0.4

%6.2

%3.2

%4.1

%24

.4%12

.0%2.7

%37

.9%4.6

%16

.5%4.7

%3.1

%

Corp

orate

/Bra

nd20

.2%17

.6%19

.3%54

.7%53

.7%20

.0%24

.9%7.6

%41

.8%10

.5%4.5

%9.2

%10

.1%8.6

%22

.3%6.9

%23

.5%20

.4%66

.3%

Publi

shing

4.6%

0.5%

0.5%

0.2%

0.3%

0.9%

0.3%

60.9%

2.0%

0.4%

0.0%

0.2%

0.2%

0.3%

0.4%

0.1%

0.3%

0.4%

13.1%

TOTA

L W

W10

0.0%

100.0

%10

0.0%

100.0

%10

0.0%

100.0

%10

0.0%

100.0

%10

0.0%

100.0

%10

0.0%

100.0

%10

0.0%

100.0

%10

0.0%

100.0

%10

0.0%

100.0

%10

0.0%

Glo

bal R

oyal

ties

from

Lic

ense

d M

erch

andi

se, B

y Pr

oper

ty T

ype

and

Prod

uct C

ateg

ory,

2014

(in

mill

ions

of U

S$)

Glo

bal R

oyal

ties

from

Lic

ense

d M

erch

andi

se, B

y Pr

oduc

t Cat

egor

y, 20

14 (a

s a

perc

enta

ge o

f Pro

pert

y Ty

pe)

Glo

bal R

oyal

ties

Lice

nsed

Mer

chan

dise

, By

Prop

erty

Typ

e, 2

014

(as

a pe

rcen

tage

of P

rodu

ct C

ateg

ory)

LIMa GLoBaL LICensInG InDUsTRY sURVeY 2015 RePoRT 14

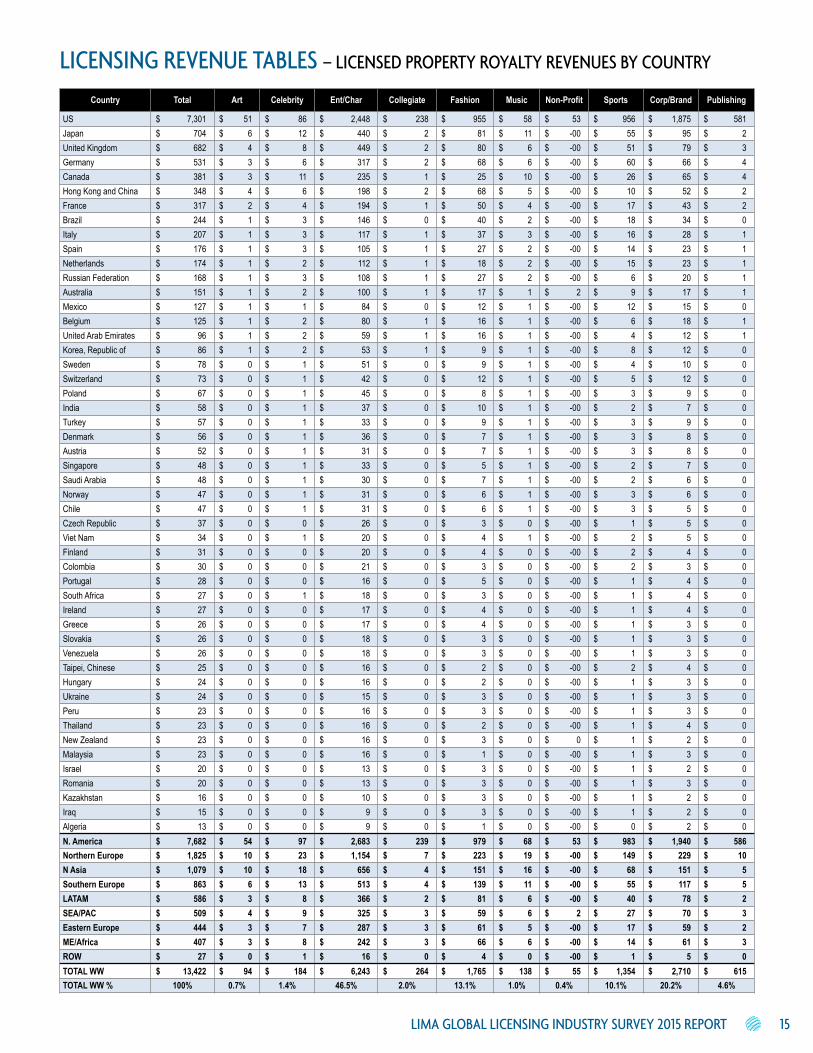

LICensInG ReVenUe TaBLes – LICenseD PRoPeRTY ReTaIL ReVenUes BY CoUnTRY

Country Total Art Celebrity Ent/Char Collegiate Fashion Music Non-Profit Sports Corp/Brand Publishing

US $ 133,267 $ 955 $ 1,602 $ 41,623 $ 4,163 $ 16,666 $ 988 $ 958 $ 16,478 $ 37,580 $ 12,255 Japan $ 12,198 $ 125 $ 205 $ 7,492 $ 34 $ 1,405 $ 186 $ -00 $ 956 $ 1,750 $ 44 United Kingdom $ 11,944 $ 73 $ 144 $ 7,665 $ 30 $ 1,394 $ 110 $ -00 $ 891 $ 1,580 $ 57 Germany $ 9,345 $ 50 $ 115 $ 5,439 $ 37 $ 1,179 $ 97 $ -00 $ 1,041 $ 1,318 $ 69 Canada $ 6,840 $ 64 $ 219 $ 4,044 $ 20 $ 440 $ 170 $ -00 $ 455 $ 1,346 $ 82 Hong Kong and China $ 6,139 $ 72 $ 108 $ 3,416 $ 27 $ 1,180 $ 81 $ -00 $ 184 $ 1,031 $ 40 France $ 5,563 $ 35 $ 78 $ 3,320 $ 26 $ 863 $ 65 $ -00 $ 291 $ 851 $ 34 Brazil $ 4,255 $ 21 $ 49 $ 2,473 $ 5 $ 685 $ 37 $ -00 $ 311 $ 670 $ 4 Italy $ 3,649 $ 24 $ 56 $ 2,022 $ 15 $ 644 $ 46 $ -00 $ 279 $ 542 $ 21 Netherlands $ 3,085 $ 16 $ 39 $ 1,929 $ 13 $ 311 $ 30 $ -00 $ 255 $ 475 $ 17 Spain $ 3,069 $ 23 $ 46 $ 1,789 $ 12 $ 461 $ 41 $ -00 $ 238 $ 441 $ 17 Russian Federation $ 2,986 $ 20 $ 47 $ 1,875 $ 15 $ 471 $ 33 $ -00 $ 101 $ 403 $ 20 Australia $ 2,688 $ 21 $ 33 $ 1,697 $ 12 $ 292 $ 22 $ 106 $ 158 $ 332 $ 15 Belgium $ 2,268 $ 15 $ 38 $ 1,409 $ 11 $ 280 $ 25 $ -00 $ 108 $ 368 $ 14 Mexico $ 2,198 $ 12 $ 25 $ 1,407 $ 8 $ 212 $ 16 $ -00 $ 203 $ 309 $ 6 United Arab Emirates $ 1,718 $ 12 $ 29 $ 1,051 $ 9 $ 281 $ 25 $ -00 $ 64 $ 232 $ 14 Korea, Republic of $ 1,492 $ 12 $ 30 $ 894 $ 9 $ 150 $ 23 $ -00 $ 136 $ 231 $ 7 Sweden $ 1,389 $ 8 $ 19 $ 891 $ 6 $ 154 $ 14 $ -00 $ 77 $ 215 $ 5 Switzerland $ 1,332 $ 8 $ 20 $ 750 $ 7 $ 202 $ 17 $ -00 $ 81 $ 238 $ 9 Poland $ 1,192 $ 8 $ 17 $ 773 $ 6 $ 139 $ 13 $ -00 $ 50 $ 180 $ 5 India $ 1,023 $ 8 $ 16 $ 638 $ 4 $ 166 $ 10 $ -00 $ 35 $ 142 $ 4 Turkey $ 1,003 $ 7 $ 19 $ 568 $ 6 $ 163 $ 12 $ -00 $ 51 $ 172 $ 5 Denmark $ 993 $ 6 $ 15 $ 627 $ 5 $ 124 $ 12 $ -00 $ 48 $ 151 $ 4 Austria $ 919 $ 6 $ 15 $ 536 $ 7 $ 128 $ 12 $ -00 $ 59 $ 151 $ 5 Singapore $ 885 $ 8 $ 19 $ 582 $ 4 $ 80 $ 9 $ -00 $ 31 $ 150 $ 3 Saudi Arabia $ 865 $ 6 $ 14 $ 544 $ 5 $ 125 $ 11 $ -00 $ 28 $ 128 $ 5 Norway $ 828 $ 5 $ 12 $ 529 $ 4 $ 103 $ 9 $ -00 $ 46 $ 117 $ 3 Chile $ 817 $ 5 $ 11 $ 522 $ 4 $ 110 $ 9 $ -00 $ 54 $ 100 $ 3 Czech Republic $ 660 $ 4 $ 9 $ 457 $ 4 $ 59 $ 6 $ -00 $ 26 $ 91 $ 3 Viet Nam $ 592 $ 6 $ 15 $ 344 $ 3 $ 67 $ 15 $ -00 $ 33 $ 105 $ 3 Finland $ 555 $ 3 $ 8 $ 350 $ 3 $ 71 $ 6 $ -00 $ 31 $ 81 $ 2 Colombia $ 538 $ 3 $ 7 $ 370 $ 2 $ 48 $ 5 $ -00 $ 36 $ 66 $ 2 Portugal $ 505 $ 3 $ 8 $ 288 $ 2 $ 82 $ 7 $ -00 $ 26 $ 86 $ 2 Ireland $ 493 $ 3 $ 8 $ 296 $ 2 $ 70 $ 6 $ -00 $ 23 $ 82 $ 2 South Africa $ 487 $ 4 $ 9 $ 313 $ 3 $ 53 $ 6 $ -00 $ 18 $ 77 $ 3 Slovakia $ 477 $ 3 $ 7 $ 320 $ 2 $ 51 $ 5 $ -00 $ 26 $ 62 $ 2 Greece $ 471 $ 3 $ 7 $ 304 $ 2 $ 67 $ 5 $ -00 $ 20 $ 62 $ 2 Venezuela $ 464 $ 3 $ 7 $ 306 $ 2 $ 54 $ 5 $ -00 $ 25 $ 60 $ 2 Taipei, Chinese $ 448 $ 4 $ 8 $ 286 $ 2 $ 31 $ 5 $ -00 $ 34 $ 76 $ 2 Ukraine $ 435 $ 3 $ 7 $ 277 $ 2 $ 58 $ 4 $ -00 $ 16 $ 65 $ 2 Hungary $ 431 $ 3 $ 6 $ 289 $ 2 $ 44 $ 4 $ -00 $ 22 $ 61 $ 2 Malaysia $ 422 $ 4 $ 8 $ 288 $ 2 $ 26 $ 4 $ -00 $ 16 $ 71 $ 2 Peru $ 414 $ 3 $ 5 $ 283 $ 2 $ 49 $ 3 $ -00 $ 14 $ 54 $ 2 New Zealand $ 413 $ 3 $ 6 $ 273 $ 2 $ 46 $ 4 $ 17 $ 13 $ 48 $ 2 Thailand $ 413 $ 6 $ 8 $ 268 $ 2 $ 32 $ 4 $ -00 $ 19 $ 72 $ 2 Israel $ 361 $ 3 $ 6 $ 230 $ 2 $ 54 $ 5 $ -00 $ 14 $ 46 $ 2 Romania $ 353 $ 2 $ 6 $ 224 $ 2 $ 48 $ 4 $ -00 $ 12 $ 54 $ 2 Kazakhstan $ 288 $ 2 $ 5 $ 173 $ 2 $ 49 $ 4 $ -00 $ 11 $ 43 $ 2 Iraq $ 265 $ 2 $ 5 $ 159 $ 2 $ 47 $ 4 $ -00 $ 9 $ 36 $ 2 Algeria $ 234 $ 2 $ 4 $ 158 $ 2 $ 21 $ 2 $ -00 $ 8 $ 35 $ 2 N. America $ 140,107 $ 1,018 $ 1,821 $ 45,667 $ 4,183 $ 17,106 $ 1,158 $ 958 $ 16,933 $ 38,926 $ 12,337 Northern Europe $ 32,231 $ 188 $ 419 $ 19,884 $ 117 $ 3,888 $ 326 $ -00 $ 2,601 $ 4,626 $ 182 N Asia $ 18,968 $ 202 $ 322 $ 11,331 $ 64 $ 2,647 $ 272 $ -00 $ 1,176 $ 2,868 $ 86 Southern Europe $ 15,531 $ 101 $ 228 $ 9,058 $ 70 $ 2,471 $ 187 $ -00 $ 964 $ 2,366 $ 87 LATAM $ 10,414 $ 59 $ 137 $ 6,343 $ 39 $ 1,436 $ 100 $ -00 $ 693 $ 1,575 $ 31 SEA/PAC $ 9,633 $ 77 $ 157 $ 6,066 $ 50 $ 1,075 $ 110 $ 123 $ 475 $ 1,452 $ 48 Eastern Europe $ 8,330 $ 54 $ 125 $ 5,308 $ 44 $ 1,122 $ 87 $ -00 $ 301 $ 1,244 $ 45 ME/Africa $ 5,420 $ 57 $ 140 $ 3,097 $ 54 $ 824 $ 111 $ -00 $ 241 $ 838 $ 57 ROW $ 903 $ 4 $ 10 $ 431 $ 4 $ 215 $ 9 $ -00 $ 13 $ 214 $ 4 TOTAL WW $ 241,538 $ 1,761 $ 3,359 $ 107,185 $ 4,625 $ 30,784 $ 2,360 $ 1,080 $ 23,398 $ 54,109 $ 12,876 TOTAL WW % 100.0% 0.7% 1.4% 44.4% 1.9% 12.7% 1.0% 0.4% 9.7% 22.4% 5.3%

LIMa GLoBaL LICensInG InDUsTRY sURVeY 2015 RePoRT 15

LICensInG ReVenUe TaBLes – LICenseD PRoPeRTY RoYaLTY ReVenUes BY CoUnTRY

Country Total Art Celebrity Ent/Char Collegiate Fashion Music Non-Profit Sports Corp/Brand Publishing

US $ 7,301 $ 51 $ 86 $ 2,448 $ 238 $ 955 $ 58 $ 53 $ 956 $ 1,875 $ 581 Japan $ 704 $ 6 $ 12 $ 440 $ 2 $ 81 $ 11 $ -00 $ 55 $ 95 $ 2 United Kingdom $ 682 $ 4 $ 8 $ 449 $ 2 $ 80 $ 6 $ -00 $ 51 $ 79 $ 3 Germany $ 531 $ 3 $ 6 $ 317 $ 2 $ 68 $ 6 $ -00 $ 60 $ 66 $ 4 Canada $ 381 $ 3 $ 11 $ 235 $ 1 $ 25 $ 10 $ -00 $ 26 $ 65 $ 4 Hong Kong and China $ 348 $ 4 $ 6 $ 198 $ 2 $ 68 $ 5 $ -00 $ 10 $ 52 $ 2 France $ 317 $ 2 $ 4 $ 194 $ 1 $ 50 $ 4 $ -00 $ 17 $ 43 $ 2 Brazil $ 244 $ 1 $ 3 $ 146 $ 0 $ 40 $ 2 $ -00 $ 18 $ 34 $ 0 Italy $ 207 $ 1 $ 3 $ 117 $ 1 $ 37 $ 3 $ -00 $ 16 $ 28 $ 1 Spain $ 176 $ 1 $ 3 $ 105 $ 1 $ 27 $ 2 $ -00 $ 14 $ 23 $ 1 Netherlands $ 174 $ 1 $ 2 $ 112 $ 1 $ 18 $ 2 $ -00 $ 15 $ 23 $ 1 Russian Federation $ 168 $ 1 $ 3 $ 108 $ 1 $ 27 $ 2 $ -00 $ 6 $ 20 $ 1 Australia $ 151 $ 1 $ 2 $ 100 $ 1 $ 17 $ 1 $ 2 $ 9 $ 17 $ 1 Mexico $ 127 $ 1 $ 1 $ 84 $ 0 $ 12 $ 1 $ -00 $ 12 $ 15 $ 0 Belgium $ 125 $ 1 $ 2 $ 80 $ 1 $ 16 $ 1 $ -00 $ 6 $ 18 $ 1 United Arab Emirates $ 96 $ 1 $ 2 $ 59 $ 1 $ 16 $ 1 $ -00 $ 4 $ 12 $ 1 Korea, Republic of $ 86 $ 1 $ 2 $ 53 $ 1 $ 9 $ 1 $ -00 $ 8 $ 12 $ 0 Sweden $ 78 $ 0 $ 1 $ 51 $ 0 $ 9 $ 1 $ -00 $ 4 $ 10 $ 0 Switzerland $ 73 $ 0 $ 1 $ 42 $ 0 $ 12 $ 1 $ -00 $ 5 $ 12 $ 0 Poland $ 67 $ 0 $ 1 $ 45 $ 0 $ 8 $ 1 $ -00 $ 3 $ 9 $ 0 India $ 58 $ 0 $ 1 $ 37 $ 0 $ 10 $ 1 $ -00 $ 2 $ 7 $ 0 Turkey $ 57 $ 0 $ 1 $ 33 $ 0 $ 9 $ 1 $ -00 $ 3 $ 9 $ 0 Denmark $ 56 $ 0 $ 1 $ 36 $ 0 $ 7 $ 1 $ -00 $ 3 $ 8 $ 0 Austria $ 52 $ 0 $ 1 $ 31 $ 0 $ 7 $ 1 $ -00 $ 3 $ 8 $ 0 Singapore $ 48 $ 0 $ 1 $ 33 $ 0 $ 5 $ 1 $ -00 $ 2 $ 7 $ 0 Saudi Arabia $ 48 $ 0 $ 1 $ 30 $ 0 $ 7 $ 1 $ -00 $ 2 $ 6 $ 0 Norway $ 47 $ 0 $ 1 $ 31 $ 0 $ 6 $ 1 $ -00 $ 3 $ 6 $ 0 Chile $ 47 $ 0 $ 1 $ 31 $ 0 $ 6 $ 1 $ -00 $ 3 $ 5 $ 0 Czech Republic $ 37 $ 0 $ 0 $ 26 $ 0 $ 3 $ 0 $ -00 $ 1 $ 5 $ 0 Viet Nam $ 34 $ 0 $ 1 $ 20 $ 0 $ 4 $ 1 $ -00 $ 2 $ 5 $ 0 Finland $ 31 $ 0 $ 0 $ 20 $ 0 $ 4 $ 0 $ -00 $ 2 $ 4 $ 0 Colombia $ 30 $ 0 $ 0 $ 21 $ 0 $ 3 $ 0 $ -00 $ 2 $ 3 $ 0 Portugal $ 28 $ 0 $ 0 $ 16 $ 0 $ 5 $ 0 $ -00 $ 1 $ 4 $ 0 South Africa $ 27 $ 0 $ 1 $ 18 $ 0 $ 3 $ 0 $ -00 $ 1 $ 4 $ 0 Ireland $ 27 $ 0 $ 0 $ 17 $ 0 $ 4 $ 0 $ -00 $ 1 $ 4 $ 0 Greece $ 26 $ 0 $ 0 $ 17 $ 0 $ 4 $ 0 $ -00 $ 1 $ 3 $ 0 Slovakia $ 26 $ 0 $ 0 $ 18 $ 0 $ 3 $ 0 $ -00 $ 1 $ 3 $ 0 Venezuela $ 26 $ 0 $ 0 $ 18 $ 0 $ 3 $ 0 $ -00 $ 1 $ 3 $ 0 Taipei, Chinese $ 25 $ 0 $ 0 $ 16 $ 0 $ 2 $ 0 $ -00 $ 2 $ 4 $ 0 Hungary $ 24 $ 0 $ 0 $ 16 $ 0 $ 2 $ 0 $ -00 $ 1 $ 3 $ 0 Ukraine $ 24 $ 0 $ 0 $ 15 $ 0 $ 3 $ 0 $ -00 $ 1 $ 3 $ 0 Peru $ 23 $ 0 $ 0 $ 16 $ 0 $ 3 $ 0 $ -00 $ 1 $ 3 $ 0 Thailand $ 23 $ 0 $ 0 $ 16 $ 0 $ 2 $ 0 $ -00 $ 1 $ 4 $ 0 New Zealand $ 23 $ 0 $ 0 $ 16 $ 0 $ 3 $ 0 $ 0 $ 1 $ 2 $ 0 Malaysia $ 23 $ 0 $ 0 $ 16 $ 0 $ 1 $ 0 $ -00 $ 1 $ 3 $ 0 Israel $ 20 $ 0 $ 0 $ 13 $ 0 $ 3 $ 0 $ -00 $ 1 $ 2 $ 0 Romania $ 20 $ 0 $ 0 $ 13 $ 0 $ 3 $ 0 $ -00 $ 1 $ 3 $ 0 Kazakhstan $ 16 $ 0 $ 0 $ 10 $ 0 $ 3 $ 0 $ -00 $ 1 $ 2 $ 0 Iraq $ 15 $ 0 $ 0 $ 9 $ 0 $ 3 $ 0 $ -00 $ 1 $ 2 $ 0 Algeria $ 13 $ 0 $ 0 $ 9 $ 0 $ 1 $ 0 $ -00 $ 0 $ 2 $ 0 N. America $ 7,682 $ 54 $ 97 $ 2,683 $ 239 $ 979 $ 68 $ 53 $ 983 $ 1,940 $ 586 Northern Europe $ 1,825 $ 10 $ 23 $ 1,154 $ 7 $ 223 $ 19 $ -00 $ 149 $ 229 $ 10 N Asia $ 1,079 $ 10 $ 18 $ 656 $ 4 $ 151 $ 16 $ -00 $ 68 $ 151 $ 5 Southern Europe $ 863 $ 6 $ 13 $ 513 $ 4 $ 139 $ 11 $ -00 $ 55 $ 117 $ 5 LATAM $ 586 $ 3 $ 8 $ 366 $ 2 $ 81 $ 6 $ -00 $ 40 $ 78 $ 2 SEA/PAC $ 509 $ 4 $ 9 $ 325 $ 3 $ 59 $ 6 $ 2 $ 27 $ 70 $ 3 Eastern Europe $ 444 $ 3 $ 7 $ 287 $ 3 $ 61 $ 5 $ -00 $ 17 $ 59 $ 2 ME/Africa $ 407 $ 3 $ 8 $ 242 $ 3 $ 66 $ 6 $ -00 $ 14 $ 61 $ 3 ROW $ 27 $ 0 $ 1 $ 16 $ 0 $ 4 $ 0 $ -00 $ 1 $ 5 $ 0 TOTAL WW $ 13,422 $ 94 $ 184 $ 6,243 $ 264 $ 1,765 $ 138 $ 55 $ 1,354 $ 2,710 $ 615 TOTAL WW % 100% 0.7% 1.4% 46.5% 2.0% 13.1% 1.0% 0.4% 10.1% 20.2% 4.6%

LIMA GLOBAL LICENSING INDUSTRY SURVEY 2015 REPORT 16

LICENSING REVENUE TABLES – US AND CANADA LICENSING RETAIL & ROYALTY REVENUESPr

oper

tyTo

tal

Acce

ssor

ies-

Fash

ion

Appa

rel

CEFo

od an

d Be

vera

geFo

otwe

arHe

alth

and

Beau

tyHo

me

Déco

rHo

usew

ares

Infa

ntMu

sic/V

ideo

Softw

are/

Vide

o ga

mes

/apps

Pape

r Pr

oduc

tsPu

blish

ing

Spor

tsTo

ysGi

ftsPr

omot

ions

Othe

r

Art

$ 1,0

18

$ 83

$

72

$ 6

$ 25

$ 2

$ 3

$ 12

5

$

83

$

9

$

13

$

10

$

197

$ 70

$ 5

$

93

$ 20

9

$

1

$

14

Celeb

rity $

1,821

$

196

$

259

$ 24

$

194

$ 40

$

241

$

152

$ 18

8

$ 39

$

12

$

34

$

6

$ 15

5

$

46

$ 53

$

112

$ 9

$ 61

Enter

tain/C

hara

cters

$ 45

,667

$

3,724

$

5,149

$ 1,5

67

$

2,228

$ 1,0

19

$

1,382

$

1,500

$ 70

1

$ 1,1

99

$

2,541

$

4,175

$

2,074

$ 3,0

06

$ 1,0

93

$

11,10

1

$ 1,6

30

$

973

$

605

Colle

giate

$ 4,1

83

$ 67

7

$ 76

7

$

2

$

6

$ 15

0

$ 1

$ 22

8

$

602

$

1

$

2

$

378

$ 77

$ 1

$

527

$ 45

8

$

301

$ 0

$ 4

Fash

ion $

17,10

6

$ 5,5

66

$ 4,3

36

$

469

$

74

$

1,604

$ 2,2

45

$ 92

8

$

323

$

211

$

12

$

132

$ 24

9

$

270

$ 31

$

390

$ 15

7

$

43

$

65

Music

$ 1,1

58

$ 18

9

$ 64

6

$

13

$ 34

$ 5

$ 9

$ 11

$

14

$

4

$

15

$

21

$

14

$

92

$

10

$ 48

$

11

$ 3

$ 21

Non-

Pro

fit $

958

$

91

$ 16

7

$

27

$ 58

$ 18

$

22

$

30

$ 37

$ 6

$ 40

$ 47

$ 21

$ 23

$ 35

$

121

$ 60

$

56

$

98

Spor

ts $

16,93

3

$ 2,2

58

$ 4,7

45

$

235

$

158

$ 33

6

$ 40

$ 47

$

307

$

95

$ 15

9

$ 2,7

16

$ 80

6

$

126

$ 2,3

05

$

1,201

$ 1,0

04

$

106

$

288

Corp

orate

/Bra

nd $

38,92

6

$ 3,4

34

$ 4,9

95

$

4,698

$ 6,0

82

$

1,212

$ 1,7

76

$ 99

6

$

2,045

$

341

$

220

$

967

$ 63

3

$

547

$ 1,2

70

$

1,597

$ 1,3

87

$

559

$

6,169

Publi

shing

$ 12

,337

$

57

$ 10

1

$

8

$

22

$

44

$ 23

$ 10

,560

$

59

$

6

$

1

$

12

$

7

$ 7

$

25

$ 19

$

27

$ 4

$ 1,3

54

TOTA

L W

W $

140,1

07

$

16,27

3

$ 2

1,239

$

7,049

$ 8,8

81

$

4,430

$ 5,7

42

$ 14

,577

$

4,359

$

1,911

$ 3,0

15

$ 8,4

92

$ 4,0

84

$

4,299

$

5,346

$ 15

,083

$

4,896

$ 1,7

53

$ 8,6

79

Prop

erty

Tota

lAc

cess

ories

- Fa

shio

n Ap

pare

lCE

Food

and

Beve

rage

Foot

wear

Healt

h an

d Be

auty

Hom

e Dé

cor

Hous

ewar

esIn

fant

Music

/Vid

eoSo

ftwar

e/ Vi

deo

gam

es/ap

psPa

per

Prod

ucts

Publ

ishin

gSp

orts

Toys

Gifts

Prom

otio

nsOt

her

Art

$ 54

$ 5

$ 4

$

0

$

1

$ 0

$ 0

$ 5

$

4

$

0

$

1

$

1

$ 11

$ 4

$

0

$ 6

$

11

$ 0

$ 1

Celeb

rity $

97

$

12

$ 16

$

1

$

7

$ 2

$ 14

$ 7

$

10

$

2

$

1

$

2

$ 0

$

8

$ 2

$

3

$ 6

$

1

$

3

Enter

tain/C

hara

cters

$ 2,6

83

$ 23

1

$ 33

3

$

74

$ 85

$ 56

$

82

$

70

$ 37

$ 68

$

139

$

274

$ 12

0

$

164

$ 59

$

710

$ 90

$

57

$

35

Colle

giate

$ 23

9

$ 40

$

47

$ 0

$ 0

$

8

$

0

$

11

$ 31

$ 0

$ 0

$ 24

$ 4

$

0

$ 28

$

28

$ 16

$

0

$

0

Fash

ion $

979

$

327

$

266

$ 21

$

3

$ 86

$

128

$

43

$ 17

$ 12

$

1

$

9

$ 14

$ 14

$ 2

$

24

$ 9

$

2

$

4

Music

$ 68

$ 11

$

40

$ 1

$ 1

$

0

$

1

$

0

$ 1

$ 0

$ 1

$ 1

$

1

$ 5

$

1

$ 3

$

1

$ 0

$ 1

Non-

Pro

fit $

53

$

5

$

10

$ 1

$ 2

$

1

$

1

$

1

$ 2

$ 0

$ 2

$ 3

$

1

$ 1

$

2

$ 7

$

3

$ 3

$ 5

Spor

ts $

983

$

133

$

287

$ 11

$

6

$ 18

$

2

$

2

$ 16

$ 5

$ 8

$ 16

9

$

46

$

7

$ 12

4

$

74

$ 54

$

6

$

16

Corp

orate

/Bra

nd $

1,940

$

199

$

306

$ 20

6

$ 20

5

$

61

$ 10

1

$ 45

$

93

$

17

$ 11

$ 60

$ 36

$ 29

$ 68

$

96

$ 72

$

32

$

303

Publi

shing

$ 58

6

$ 3

$ 6

$

0

$

1

$ 2

$ 1

$ 48

9

$

3

$

0

$

0

$

1

$ 0

$

0

$ 1

$

1

$ 1

$

0

$

73

TOTA

L W

W $

7,682

$

966

$

1,315

$ 31

6

$ 31

1

$

235

$

330

$

674

$ 21

4

$ 10

6

$ 16

2

$ 54

4

$

234

$ 23

2

$

287

$ 95

2

$

263

$ 10

2

$ 44

1

US

and

Can

ada

Reta

il S

ales

of L

icen

sed

Mer

chan

dise

, By

Prop

erty

Typ

e an

d Pr

oduc

t Cat

egor

y, 20

14 (i

n m

illio

ns o

f US

$)

US

and

Can

ada

Roya

lties

from

Lic

ense

d M

erch

andi

se, B

y Pr

oper

ty T

ype

and

Prod

uct C

ateg

ory,

2014

(in

mill

ions

of U

S$)

For d

etai

led

tabl

es fo

r the

Top

10

coun

trie

s an

d al

l Wor

ld R

egio

ns p

leas

e re

fer t

o th

e ac

com

pany

ing

docu

men

t.

LIMa GLoBaL LICensInG InDUsTRY sURVeY 2015 RePoRT 17

aPPenDIXPRODUCT CATEGORY TRENDS: A BRANDAR ANALYSIS

As we formulated this Licensing market sizing Analysis, we examined trends occurring in the underlying Product Categories that brands/properties are licensing into. We gleaned this information from the various Industry reports we reviewed and wanted to share some of our learnings here as well as they may help with targeting future opportunities.

Accessories:

demand for the global Accessory manufacturing industry has resurged over the past five years, as global economic conditions have improved and consumers have resumed the spending they delayed during the recession. demand for higher priced luxury products increased in countries such as China, India and Brazil, while many europe-based companies are placing greater focus on the Asian market as incomes in the region rise.

As a result, industry revenue is anticipated to grow an annualized 2.2% over the five years preceding 2015 this is driven in large part by increasing wealth and consequentially spending on luxury items; especially by Chinese and Indian consumers who account for 36.4% of the world’s population.

Items produced in europe (Italy and France, in particular) are regarded as high-quality luxury Accessory products that command premium prices. however, companies that operate in developed economies are increasingly sourcing accessories and handbags from manufacturers in China, where production costs are lower. As wages in China rise though, production is shifting to other lower-cost producers in Asia, such as Vietnam. As a result of these trends, the size of the industry is expected to grow; however, the number of Accessory companies in europe and the United states will decline.

over the next five years, demand for handbags and accessories will grow as conditions in the global economy, especially in Western europe and north America, strengthen. manufacturers of less expensive Accessory products are mainly located in the emerging market regions of Asia and south America. In contrast, designers, large wholesalers and retailers are mostly located in europe, the United states and the developed Asian countries such as hong Kong and Japan. Companies that operate in developed economies like the United states and the United Kingdom have outsourced many of their accessory and handbag manufacturing activities to emerging economies to reduce costs. the continued existence of these luxury brands’ home base manufacturing operations is largely attributable to the prestige associated in this category with “made in Italy or France” products as opposed to “made in Asia” products. Products that are manufactured in europe are generally regarded as high-quality, luxury products that carry high prices.

overall, profit margins have grown from an estimated 6.2% of revenue in 2010 to 6.7% in 2015; although they still remain below their historical levels of 7.0% - 8.0%. With the advent of fast fashion, which brings designs from the runway to stores in a matter of weeks, individual manufacturers’ response times are quite crucial in this product segment. manufacturers that cannot quickly meet demand for new trends will be at a disadvantage. IBIsWorld forecasts that Accessory industry revenue will increase at an annualized rate of 4.5% over the five years leading to 2020.

Apparel:

rebounding global economies will bring good news to the global Apparel manufacturing industry over the next five years. rising per capita disposable incomes, coupled with the steady upward trend in the global population, will give way to greater demand for Apparel. demand is most heavily influenced by per capita disposable income though. It determines the quantity, quality and frequency of apparel purchases. demand for high-value luxury apparel is growing across the board. Chinese luxury consumers are expected to increasingly become a target market for many high-end apparel companies.

the United states is the industry’s largest market. the country generates an estimated 16.7% of industry revenue due to its large population, high standards of living and high consumption expenditures. Women’s and girls’ Apparel is expected to account for almost two-thirds of revenue generated by this industry worldwide, while men’s and boys’ Apparel is expected to account for 36.5% of revenue. Consumer preference for premium denim items has grown over the past five years; coinciding with the steady shift away from strict professional work attire to a more relaxed and casual dress code.

As China’s middle class continues to grow, industry operators are shifting their focus. For almost two to three decades, many producers off-shored production to China in order to take advantage of more affordable labor costs and less-stringent regula-tions and exported their apparel to developed countries where they could charge relatively higher prices. however, with growth in China’s middle-class, industry operators are expected to shift their focus to the growing Chinese consumer segment.

In addition, a relatively recent trend, reshoring is also gaining traction. As manufacturers shift their strategy from producing in China for the Western markets to now producing in China for their Asian and european markets more exclusively, many apparel

LIMa GLoBaL LICensInG InDUsTRY sURVeY 2015 RePoRT 18

manufacturers are looking to re-shore production back to western economies. this trend is being aided by rising labor costs in China and greater manufacturing competitiveness in the United states.