LESSON 3-1

15

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning LESSON 3-1 LESSON 3-1 Journals, Source Documents, and Recording Entries in a Journal 1. Identify the steps in which transactions are recorded in a journal. 2. Explain the importance of source- documents. 3. List the four parts of a journal entry.

-

Upload

brynne-kaufman -

Category

Documents

-

view

22 -

download

0

description

LESSON 3-1. Journals, Source Documents, and Recording Entries in a Journal. Identify the steps in which transactions are recorded in a journal. Explain the importance of source-documents. List the four parts of a journal entry. - PowerPoint PPT Presentation

Transcript of LESSON 3-1

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

LESSON 3-1LESSON 3-1

Journals, Source Documents, and Recording Entries in a Journal

1. Identify the steps in which transactions are recorded in a journal.

2. Explain the importance of source-documents.3. List the four parts of a journal entry.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

Competency: Understanding the Competency: Understanding the Accounting Cycle for a Service BusinessAccounting Cycle for a Service Business

2

LESSON 3-1

Objectives:36 Use source documents to journalize

transactions.

38 Prepare customer invoices for a service business.

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

Chapter 3 ObjectivesChapter 3 Objectives

Define accounting terms related to journalizing transactions.

Identify accounting concepts and practices related to journalizing transactions.

Record transactions to set up a business in a five-column journal.

Record transactions to buy insurance for cash and supplies on account in a five-column journal.

Record transactions that affect owner’s equity and receiving cash on account in a five-column journal.

Prove and rule a five-column journal and prove cash.

3

LESSON 3-1

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

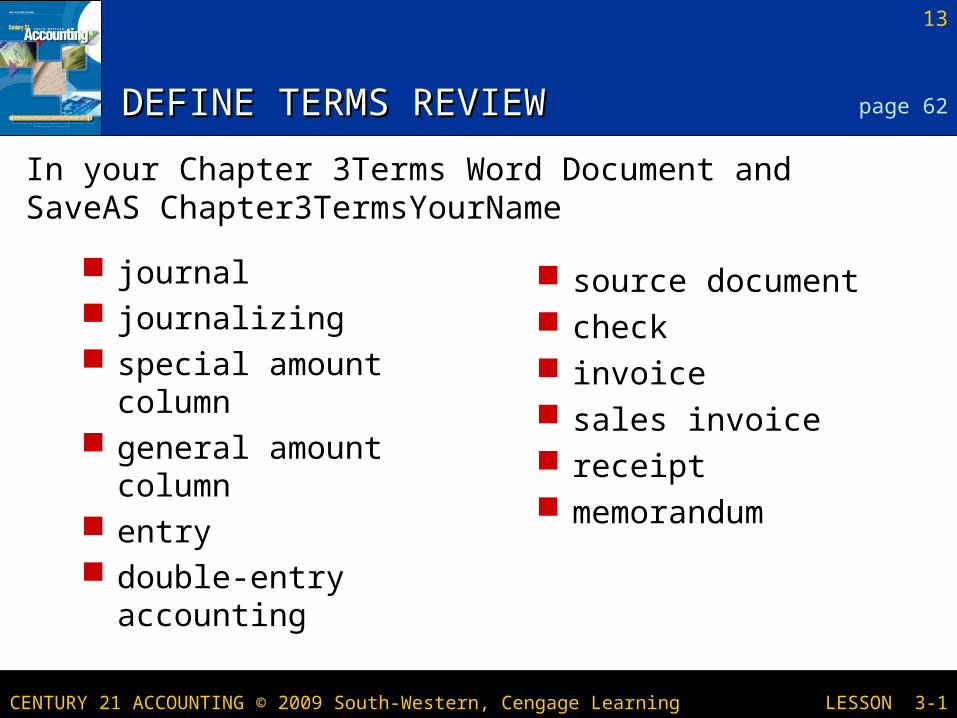

Journal – a form for recording transactions in chronological order.

Journalizing – recording transactions in a journal. Special amount column – a journal amount column

headed with an account title. General amount column – a journal amount column

that is not headed with an account title.

4

LESSON 2-1

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

Entry – Information for each transaction recorded in a journal.

Double-entry accounting – the recording of debit and credit parts of a transaction.

Source document – a business paper from which information is obtained for a journal entry.

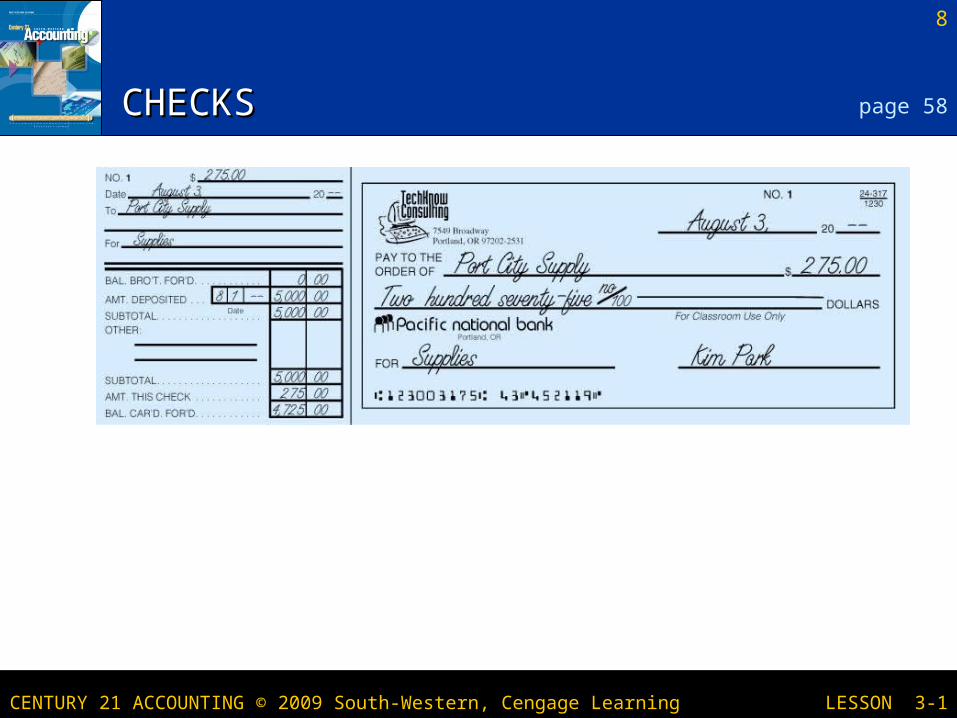

Check – a business form ordering a bank to pay cash from a bank account.

5

LESSON 2-1

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

Invoice – a form describing the goods or services sold, the quantity, and the price.

Sales invoice – An invoice used as a source document for recording a sale on account.

Receipt – A business form giving written acknowledgement for cash received.

Memorandum – a form on which a brief message is written describing a transaction.

6

LESSON 2-1

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

7

LESSON 3-1

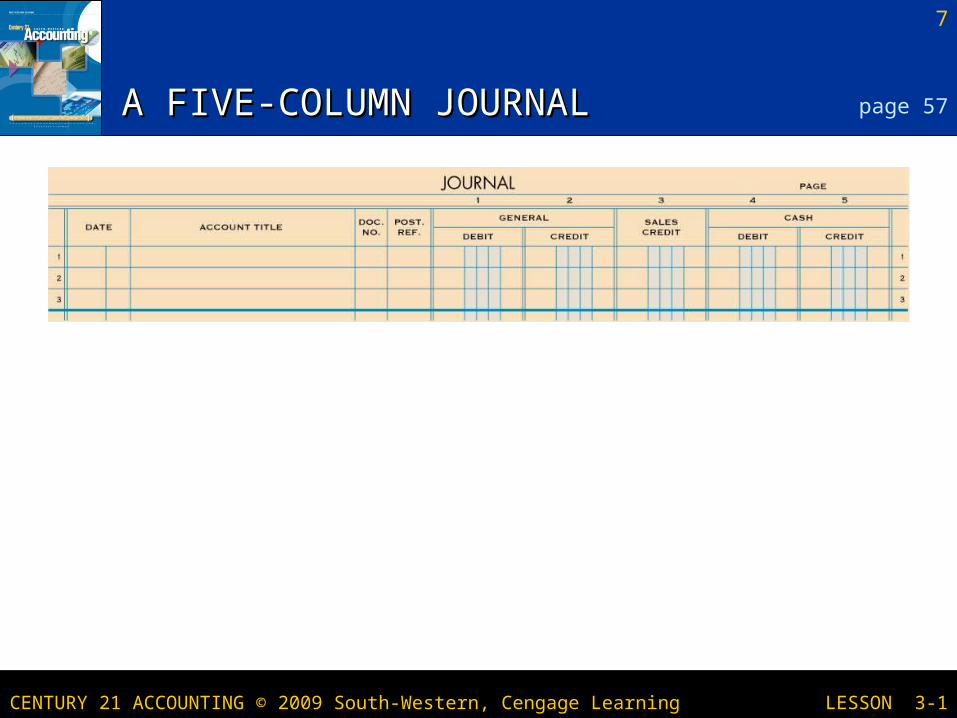

A FIVE-COLUMN JOURNALA FIVE-COLUMN JOURNAL page 57

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

8

LESSON 3-1

CHECKSCHECKS page 58

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

9

LESSON 3-1

SALES INVOICESSALES INVOICES page 58

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

10

LESSON 3-1

OTHER SOURCE DOCUMENTSOTHER SOURCE DOCUMENTS page 59

memorandummemorandum

calculator tapecalculator tape

receiptreceipt

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

11

LESSON 3-1

RECEIVED CASH FROM OWNER AS AN RECEIVED CASH FROM OWNER AS AN INVESTMENTINVESTMENT page 60

August 1. Received cash from owner as an investment, $5,000.00. Receipt No. 1.

1. Write the date in the Date column.

2. Write the debit amount in the Cash Debit column.

3. Record the credit amount in the General Credit column. Write the title of the account in the Account Title column.

4. Write the source document number in the Doc. No. column.

1122

4433 33

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

12

LESSON 3-1

PAID CASH FOR SUPPLIESPAID CASH FOR SUPPLIES page 61

August 3. Paid cash for supplies, $275.00. Check No. 1.

1. Write the date in the Date column.

2. Record the debit amount in the General Debit column. Write the title of the account in the Account Title column.

3. Write the credit amount in the Cash Credit column.

4. Write the source document number in the Doc. No. column.

1144

3322 22

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

13

LESSON 3-1

DEFINE TERMS REVIEWDEFINE TERMS REVIEW

journal journalizing special amount column general amount column entry double-entry accounting

source document check invoice sales invoice receipt memorandum

page 62

In your Chapter 3Terms Word Document and SaveAS Chapter3TermsYourName

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

Exit Ticket for Chapter 3-1Exit Ticket for Chapter 3-1

1. In what order are transactions recorded in a journal?

2. Why are source-documents important?

3. List the four parts of a journal entry.

14

LESSON 3-1

In a Word Document, SaveAS: Chapter3-1AYUYourNameDrop a copy in my InBox today before you leave!

CENTURY 21 ACCOUNTING © 2009 South-Western, Cengage Learning

Chapter 3-1 Assignments Chapter 3-1 Assignments Complete on ApliaComplete on Aplia

Work Together 3-1 On Your Own 3-1 Application Problem 3-1

15

LESSON 3-1