LENDER'S SECURITY INTEREST IN CASUALTY POLICY PROCEEDS …€¦ · · 2017-12-22j:\`sbo\WSBA...

22

j:\`sbo\WSBA Insurance Seminar\Lender's Security Interest in Casualty Policy Proceeds 1 LENDER'S SECURITY INTEREST IN CASUALTY POLICY PROCEEDS Scott B. Osborne THE CONCERNS AND PRACTICES OF THE LENDER Real estate lenders face risks that are never straight-forward. Lenders must deal with not only economic cycles which affect the value of collateral pledged to repay loans, but also with natural disasters which destroy the collateral. Lenders use a variety of underwriting techniques to protect against adverse economic conditions. Casualty losses seem to be somewhat more capricious to mortgage bankers and borrowers alike, and their traditional method of dealing with this risk is to obtain insurance. If a disaster does occur, the lender is normally not the only disappointed party. Unless the borrower has the ability (and perhaps the willingness) to pay its debts from other assets, the lender is pitted against other creditors trying to collect from any insurance proceeds which may be available as a result of the casualty. Real estate lenders have fairly standard practices in perfecting their rights to insurance proceeds. For the most part, these practices have been, and continue to be, effective. There has not been a large amount of litigation among creditors asserting conflicting claims to insurance proceeds primarily because of the widespread observance of these practices by lenders. Insurable Interest of the Mortgagor and Mortgagee It is accepted law that both the mortgagor and mortgagee 1 have insurable interests in the mortgaged property. Absent some contractual undertaking to do so, the mortgagor has no obligation to obtain fire insurance 2 for the benefit of the mortgagee. The fire insurance contract is a personal undertaking between the insurance company and either the mortgagor or mortgagee who procures the policy. In both instances, the insurance company agrees to indemnify either the mortgagee or mortgagor from the diminution of the value of the mortgaged property as a result of the insured perils. The mortgagor may insure the property in an amount equal to the property's value; the mortgagee does not have an insurable interest in the property in excess of the amount of the mortgage. The mortgagor has no interest in the proceeds of the mortgagee's policy and the mortgagee has no interest in the proceeds of the mortgagor's policy. 3 Mortgagee Loss Payable Clauses Rather than have both the borrower and lender buy separate policies of fire insurance to protect their respective interests, the lender typically requires the borrower to do two things: First, the borrower covenants in the mortgage that there will be fire insurance maintained for the benefit of the mortgagee; and Second, the lender requires the borrower to obtain a fire insurance policy with a loss payable clause in favor of the lender.

-

Upload

truongnhan -

Category

Documents

-

view

217 -

download

2

Transcript of LENDER'S SECURITY INTEREST IN CASUALTY POLICY PROCEEDS …€¦ · · 2017-12-22j:\`sbo\WSBA...

j:\`sbo\WSBA Insurance Seminar\Lender's Security Interest in Casualty Policy Proceeds

1

LENDER'S SECURITY INTEREST IN

CASUALTY POLICY PROCEEDS

Scott B. Osborne

THE CONCERNS AND PRACTICES OF THE LENDER

Real estate lenders face risks that are never straight-forward. Lenders must deal with not only economic cycles which affect the value of collateral pledged to repay loans, but also with natural disasters which destroy the collateral. Lenders use a variety of underwriting techniques to protect against adverse economic conditions. Casualty losses seem to be somewhat more capricious to mortgage bankers and borrowers alike, and their traditional method of dealing with this risk is to obtain insurance.

If a disaster does occur, the lender is normally not the only disappointed party. Unless the borrower has the ability (and perhaps the willingness) to pay its debts from other assets, the lender is pitted against other creditors trying to collect from any insurance proceeds which may be available as a result of the casualty.

Real estate lenders have fairly standard practices in perfecting their rights to insurance proceeds. For the most part, these practices have been, and continue to be, effective. There has not been a large amount of litigation among creditors asserting conflicting claims to insurance proceeds primarily because of the widespread observance of these practices by lenders.

Insurable Interest of the Mortgagor and Mortgagee

It is accepted law that both the mortgagor and mortgagee1 have insurable interests in the mortgaged property. Absent some contractual undertaking to do so, the mortgagor has no obligation to obtain fire insurance2 for the benefit of the mortgagee. The fire insurance contract is a personal undertaking between the insurance company and either the mortgagor or mortgagee who procures the policy. In both instances, the insurance company agrees to indemnify either the mortgagee or mortgagor from the diminution of the value of the mortgaged property as a result of the insured perils. The mortgagor may insure the property in an amount equal to the property's value; the mortgagee does not have an insurable interest in the property in excess of the amount of the mortgage. The mortgagor has no interest in the proceeds of the mortgagee's policy and the mortgagee has no interest in the proceeds of the mortgagor's policy.3

Mortgagee Loss Payable Clauses

Rather than have both the borrower and lender buy separate policies of fire insurance to protect their respective interests, the lender typically requires the borrower to do two things:

First, the borrower covenants in the mortgage that there will be fire insurance maintained for the benefit of the mortgagee; and

Second, the lender requires the borrower to obtain a fire insurance policy with a loss payable clause in favor of the lender.

j:\`sbo\WSBA Insurance Seminar\Lender's Security Interest in Casualty Policy Proceeds

2

The effect of the first requirement is addressed below in the discussion of competing claims to insurance proceeds in those instances in which fire insurance is obtained but a loss payable clause in favor of the lender is not. The effect of a loss payable clause in favor of the lender is to grant to the lender a direct interest in the fire policy that has been obtained by the mortgagor.

There are a variety of lender loss payable clauses. The so-called "open" loss payable clause recites that any loss is payable to the lender, “as its interest may appear.” The principal disadvantage of this type of clause is that the lender is exposed to all of the defenses and limitations that the insurance company may have to its obligation to pay as a result of the acts of the mortgagor, such as the failure to pay the premium or the fact that the property has a value which is less than the then outstanding value of the mortgage4. The cases collected at 48 A.L.R. 121 (1927) and 38 A.L.R. 367 (1925) provide a summary of the various disasters that can befall a lender which relies upon an open loss payable clause for protection.

Lenders insist that the "New York," or "standard" or "union" form of loss payable clause be included in the fire policy obtained by the borrower. This clause provides that the proceeds are payable to the lender as its interest may appear, but goes on to state something equivalent to the following:

. . . this insurance, as to the interest of the mortgagee only, shall not be invalidated by any act or neglect of the mortgagor or the owner of the within described property, nor by any foreclosure or other proceedings or notice of sale relating to the property, nor by any change in the title or ownership of the property, nor by the occupation of the premises for the purposes more hazardous than are permitted by this policy, provided, that in case the mortgagor or owner shall neglect to pay any premium due under this policy, the mortgagee shall, on demand, pay the same.5

The standard form of loss payable clause eliminates the defenses and limitations that the insurance company may have against the borrower for payment of a loss otherwise covered by the policy. In return, the mortgagee guarantees to pay the policy premium. Note that this clause does not require the lender to inform the insurance company of any change in ownership of the property or of the commencement of foreclosure. Some clauses do require notice to the insurance carrier if the lender becomes aware of an increase in risk to the property.

Lenders which take these two actions - having the mortgagor covenant in the mortgage to insure the premises for the benefit of the mortgagee and insisting that the fire insurance policy has a standard mortgagee loss payable clause - have generally protected themselves against all competing creditor claims to policy proceeds.

THE NATURE OF THE LENDER'S POLICY INTEREST

Ownership vs. Security Interest

If the fire policy has a loss payable clause in favor of the lender, the lender has a contractual right to receive the policy proceeds up to the value of the lender's mortgage.6 This contractual right is not in the nature of a "security interest." It is in the nature of a contractual right to receive the proceeds. This distinction is important, because it explains in large part the absence of litigation

j:\`sbo\WSBA Insurance Seminar\Lender's Security Interest in Casualty Policy Proceeds

3

in the bankruptcy courts between mortgagees and various creditors claiming interests in the proceeds of fire insurance policies.

Because the mortgagee has a contractual right to money payable under the loss payable clause, the mortgagor has no right to that money. Thus the money or right to receive the money is not property or a right to property belonging to the mortgagor.7

Simply stated, fire policy proceeds belong to the lender if the policy contains a mortgagee loss payable clause. In the context of a bankruptcy proceeding involving the mortgagor-debtor, these policy proceeds are not the property of the debtor.

The Effect of the UCC

The Uniform Commercial Code ("UCC") has conditioned lenders to think in terms of security interests. Since a fire insurance policy is a contract, the natural reaction of lenders is to think of perfecting a security interest under the UCC in the contractual right (or account) to receive money following damage to property.8

The principal problem with this analysis is that insurance policies are specifically excluded from the provisions of Article 9 of the UCC.

Sec. 9-109(d). Inapplicability of Article. This Article does not apply to:

(8) A transfer of an interest in or an assignment of a claim under a policy of insurance, other than an assignment by or to a health-care provider of a health-care-insurance receivable and any subsequent assignment of the right to payment, but 9-315 and 9-322 apply with respect to proceeds and priorities in proceeds;

It is not possible under the UCC to create and perfect a security interest in a fire insurance policy. The only method of obtaining rights to payment under a fire insurance policy is to have a contractual right to receive that payment under the policy itself.

The exception to this general statement arises in the context of determining whether insurance proceeds can constitute the "proceeds" of collateral. The recent redraft of Article of the UCC continued the treatment of insurance payments as "proceeds" of personal property that were otherwise subject to a perfected security interest. This has been the result under the UCC since the 1972 amendments made it clear that it was possible to have a security interest vis a vis the borrower in “proceeds” arising from an insurance policy.

The UCC recognizes that the designation of the party to receive payment under a loss payable clause in a fire insurance policy takes precedence over any claim of a holder of a perfected security interest in the collateral that has been damaged or destroyed. The holder of a perfected security interest in collateral that is asserting a claim to insurance payments as "proceeds" from collateral has no right to pursue an action directly against the insurance company for the payment of amounts due under the policy.9

j:\`sbo\WSBA Insurance Seminar\Lender's Security Interest in Casualty Policy Proceeds

4

At first blush, it would seem that for most real estate lenders, this limited application of the UCC has little relevance. Mortgagees deal with real property. In modern mortgage transactions, however, there is a mix a real and personal property interests. Apartments contain appliances which any mortgage lender expects to acquire as part of a foreclosure. Office buildings contain a myriad of personal property - lobby art, window washing equipment and computer software used to run the building air-conditioning system - that is security for the mortgage lender's loan.

As part of the normal documentation of mortgage loans, mortgagees do include grants of security interests to the personal property that is owned by the borrower and used in connection with the real estate collateral. The perfection of that security interest provides the mortgagee with an additional claim to the insurance proceeds that may be payable with respect to that personal property· The primary claim for payment of those proceeds, however, arises because the lender has required the borrower to provide the loss payable clause as part of the fire insurance policy which covers this personal property.

Failure to Obtain Loss Payable Clause

The litigation that occurs between creditors competing over insurance proceeds arises in those instances in which the borrower has failed to obtain an insurance policy with a loss payable clause in favor of the lender. These cases are usually resolved in favor of the mortgagee, so long as the mortgage requires the mortgagor to obtain insurance for the benefit of the mortgagee.

Equitable Liens. If the mortgagor has the duty to obtain insurance for the benefit of the mortgagee, any policy payments will be subject to an equitable lien in favor of the mortgagee.10 The theories that support this equitable lien are numerous. The existence of the lien is justified under a theory of the right of the mortgagee to obtain specific enforcement of the borrowers promise to obtain the insurance. Other cases create a presumption that the mortgagor must have intended the policy to be for the benefit of the lender following the borrower's undertaking to obtain the fire insurance policy.11

This equitable lien should always prevail over other creditors.12 Since the fire insurance policy cannot be the subject of an independent security agreement pledging the proceeds of the policy, cases involving creditors with a "security interest" in the fire insurance policy competing against a mortgagee do not arise or are decided in a summary fashion.13

The same result occurs in those cases dealing with personal property. The fact pattern of these cases involves a lender that has a perfected security interest in the collateral, a lender that has required the borrower to insure the collateral, or both situations. In those cases decided prior to enactment of the 1972 amendments to Article 9 of the UCC, courts concluded that either an equitable lien existed, or the insurance payments were proceeds of the collateral.14 After the various states adopted the 1972 amendments to the UCC, there has been virtually no litigation concerning the status of insurance payments as "proceeds" of collateral.

Competing Claims. The existence of multiple mortgagees or other claimants asserting rights to insurance proceeds creates the potential for additional excitement for a real estate lender. In the case of multiple mortgagees, each mortgagee will normally require that the property be insured for their respective benefit and each mortgagee will have the benefit of a loss payable clause.

j:\`sbo\WSBA Insurance Seminar\Lender's Security Interest in Casualty Policy Proceeds

5

The proceeds of any insurance policy will be divided between these mortgagees based upon the relative priority of their respective liens.15

There are a variety of fact patterns that can arise between multiple mortgagees. For example, the first mortgagee might require the maintenance of insurance, but the policy purchased might name only a junior mortgagee in the loss payable clause. In this instance, the first mortgagee who has required the property to insured to should prevail over the junior mortgagee.16 The first mortgagee may be named in the loss payable clause, but the junior mortgagee omitted. In this case, the junior mortgagee still has a claim to the fire policy proceeds, but that claim is junior to the first mortgagee.17 The ability of the mortgagee to assert a claim directly against the insurance company in the absence of a loss payable clause will depend upon the knowledge of the insurer. If the non-named mortgagee has made the insurer aware of the mortgagee's existence and the requirement imposed upon the mortgagor to maintain insurance for the mortgagee's benefit, the insurer may well have a direct liability to the non-named mortgagee.18

The outcome from these different fact patterns depends upon whether the mortgagee requires the property to be insured for its benefit. Once that requirement is imposed upon the mortgagor, an equitable lien will arise in favor of the mortgagee. If that requirement is not present in the mortgage, the mortgagee has no claim to the policy proceeds in the absence of a loss payable clause.19

Lessees of mortgaged property generally allocate the risk of loss to the property between themselves and the landlord. The disposition of insurance proceeds in the landlord-tenant setting is often at variance with the disposition made in the lender-borrower setting. Whether or not the lease arrangement alters the rights of the lender to fire insurance policy proceeds depends upon the relationship, if any, of the lender to the lease arrangement. If the mortgage is superior to the leasehold interest and all parties are named in loss payable clauses, the mortgagee will prevail as a result of its superior interest. This is also the result in the event the lease is initially prior to the mortgage, but is subordinated to the mortgage. 20

In most of these instances, the analysis of the outcome is facilitated by viewing the mortgaged property as consisting of not only the real property, but also the fire policy proceeds. The proceeds are allocated in accordance with the relative priorities of the parties in the real property. To the extent that the junior claimants are required to have proceeds to which they have a claim paid for the benefit of the senior claims, the priority of the junior claims against the remaining property is increased. In effect, the theory of subrogation operates to continuously adjust the priorities between all of the competing claimants until all those persons claiming an interest in the real estate have been paid, assuming there is sufficient value.21

These results are reassuring to lenders. Mortgagees who require the borrower to maintain insurance can rely upon the relative priority of their mortgages to determine their respective interests in the fire insurance proceeds. This result is less comforting to the borrower who has not obtained enough insurance coverage to fully compensate all those who have an interest in the real .property which has been damaged or destroyed, or to tenants who may be depending upon the borrower’s insurance to restore the tenants’ business establishment.

Effect of Foreclosure

j:\`sbo\WSBA Insurance Seminar\Lender's Security Interest in Casualty Policy Proceeds

6

The effect of foreclosure on the right of a lender to share in insurance proceeds depends upon three variables: (1) Did the loss occur prior to or after the foreclosure was completed; (2) If the property was sold at foreclosure, was there a deficiency; and (3) Did the policy contain an open or standard form of loss payee clause.

Losses Prior to Foreclosure Sale. If the loss occurs prior to the foreclosure sale, the normal rules concerning disbursement of the policy proceeds apply. The determination of the amount of policy proceeds to be paid to the lender is fixed as of the date of the loss and is calculated by the amount owed to the lender.22 The lender is entitled to apply the proceeds in full or partial satisfaction of the indebtedness, depending upon the amount of proceeds available and the balance owed on the debt. Proceeds in excess of the debt are paid to the borrower.

If the lender has received a judgment on the debt, the amount of the judgment may limit the amount that can be recovered under the policy. 23 The insurance company may attempt to limit the amount recovered by excluding certain items advanced under the mortgage, such as real estate taxes, late fees and other costs that have inflated the amount of the mortgage above the unamortized balance as of the date of the loss as well as any post-loss interest and foreclosure costs.

The disposition of policy proceeds if the mortgage has been foreclosed and a sale has occurred may depend upon whether the policy contains an open or standard mortgage loss payable provision. Under either clause, the foreclosure sale will terminate the right of the mortgagee to collect any portion of the policy proceeds if the full amount of the debt is bid at the sale. If the lender has received complete payment from the foreclosure sale as a result of bidding the entire amount of the judgment, the mortgagee has suffered no loss that is covered by the policy. 24

If the insurance policy contains a standard mortgage loss payable clause, then, depending upon the amount of the bid at the sale, the right to recover may continue following foreclosure on the theory that the standard mortgage clause creates a separate insurance contract with the mortgagee. It is possible that in order to recover a deficiency, the lender must actually enter a deficiency judgment against the borrower in order to avoid the argument that the debt has been fully repaid. 25

The message in these rules is that if a loss occurs prior to the foreclosure sale, the lender should collect the insurance prior to proceeding with the sale. This will eliminate any argument on the part of the insurance company that the mortgagee’s interest has been reduced or eliminated as a result of the sale, particularly in those states in which deficiency judgments are not allowed following non-judicial foreclosures.

Losses After the Foreclosure Sale. If the loss occurs after the sale, the type of payable clause will determine whether there is any recovery for the lender. If the insurance policy has an open clause, post-sale losses are not covered. The coverage afforded under the open clause is only for the lender, as a lender, and not as the owner of the property. 26

There is authority that the lender is covered for a post-foreclosure sale loss under a standard mortgage clause. Again, the theory is that the standard clause creates an independent insurance contract between the lender and the insurance company, so coverage is provided so

j:\`sbo\WSBA Insurance Seminar\Lender's Security Interest in Casualty Policy Proceeds

7

long as the premiums are paid. There is authority to contrary, however, under the theory that the standard mortgage clause is supposed to provide protection for the lender in its status as a mortgagee and was not intended to provide coverage when the lender becomes the actual owner of the property. 27

The prudent lender will obtain separate insurance following the foreclosure sale, or confirm with the existing carrier that the coverage continues following the sale. As noted above, under the standard mortgage clause, the lender may or may not be required to inform the insurance company of a change in ownership of the property or an increase in hazard, but the prudent lender should contact the insurance company upon the commencement of foreclosure, and certain upon completion of the sale to determine whether coverage will continue or whether it is necessary to obtain a new policy.

j:\`sbo\WSBA Insurance Seminar\Lender's Security Interest in Casualty Policy Proceeds

8

ENDNOTES

*Scott B. Osborne is of counsel to the firm of K & L Gates LLP in its Seattle, Washington office.

1. References to "mortgages" in general refer to all variants of real property security devices, including traditional mortgages, deeds of trust and real estate contracts·

2. The term "fire insurance" refers to a policy of insurance that covers damage to property as a result of fire, lightning and other natural hazards. Keeton & Widiss, Insurance Law, §1.5(b) (1988).

3. See generally, Appleman, Insurance Law and Practice, § 3381 (1970); Nelson &Whitman, Real Estate Finance Law, § 4.13 (3rd ed. 1993).

4. Inland Finance Co. v. Home Insurance Co., 134 Wash. 485, 236 P. 73 (1925).

5. Appleman, supra note 3, § 3401.

6. This statement does not address the right of the borrower, under certain circumstances, to insist upon the application of those proceeds by the lender toward the reconstruction of improvements which have been damaged or destroyed.

7. Paskow v. Calvert Fire Ins. Co., 579 F.2d 949, 951 (5th Cir. 1978)

8. The UCC, prior to 1972 revisions defined "contract right" as

. . . a right to payment under a contract not yet earned by performance and not evidenced by an instrument or chattel paper.

The definition was removed in the 1972 amendments to the UCC because the commentators believed it was redundant with the definitions of "Accounts."

[Code Index] U.C.C. Rep. Serv. (Callaghan) ¶ 9106.

9. Judah AMC & Jeep, Inc. v. Old Republic Ins. Co., 293 N.W.2d 212, 29 UCCRS 687 (Iowa 1980); United Companies Life Ins. Co. v. State Farm & Fire Cas. Co., 477 So. 2d 645 (Fla. App. 1 Dist. 1985); 9 Anderson, Uniform Commercial Code, § 9-306:15 (3rd Ed. 1985).

10. Schleimer v. Empire Mut. Ins. Co., 65 Misc.2d 520, 318 N.Y.S.2d 182, rev'd 337 N.Y.S.2d 872, 71 Misc.2d 1014, aff'd 352 N.Y.S.2d 429, 43 A.D.2d 825 (1971); Knapp v. Victory Corp., 279 S.C. 80, 302 S.E.2d 330 (1983); Appleman, supra note 3, § 3381.

11. Gulf National Bank v. Hartford Fire Insurance Co., 264 S.2d 401 (Miss. 1972).

12. See Rural Acceptance Corporation v. Pierce, 157 Ind. App. 90, 298 N.E.2d 499, 502 (1973):

It has long been the law that a prior equitable interest is superior to a judgment lien.

j:\`sbo\WSBA Insurance Seminar\Lender's Security Interest in Casualty Policy Proceeds

9

13. A general creditor asserted a right to proceeds of a fire insurance policy in In Re Oak Winds, 4 Bankr. 528 (M.D. Fla. 1980). The creditor asserted that these proceeds should be made available to debtor to facilitate a reorganization:

This proposition [that the fire insurance proceeds should be made available to the debtor]

. . . is without any factual or legal support, either on the theory that Rodgets [the general creditor] is entitled to the insurance proceeds because the Bank failed to perfect a security interest in the funds in conformity with the applicable provisions of the U.C.C. by filing a Financing Statement or on the ground that these funds belong, in any event to the general estate. These propositions have been resolved conclusively in Paskow v. Calvert Fire Insurance Company, 579 F.2d 949 (5th Cir. 1978), where it - was held that the holder of a valid mortgage who holds a validly perfected security interest in personalty has a continued cognizable interest in the insurance proceeds and when the collateral which is insured is destroyed or damaged, the secured party is entitled to be paid out of the proceeds to the extent of its interest in the collateral especially when it was named as a loss payee or was named as a co-insured in the policy. The courts of this State reached the same conclusion. Insurance Management Corp. v. Cable Services of Florida, Inc., et al., 359 So.2d 572 (Fla. App. 1978).

Id., at 531.

14. Paskow v. Calvert Fire Ins. Co., supra note 7; In Re Sexton, 16 Bankr. 240 (Tenn. 1981).

15. Appleman, supra, § 3382.

16. See Gulf National Bank v. Hartford Fire Insurance Co., supra, note 13.

17. See Greenberg v. 1625 Putnam Ave. Corporation, 241 A.D. 623, 268 N.Y.S. 553 (1934).

18. Employers Mutual Casualty Co. v. Standard Drug Co., 234 So.2d 330 (Miss. 1970).

19. Cases discussing these fact patterns are collected at 9 A.L.R.2d 299.

20. Loving v. Ponderosa Systems, Inc., 479 N.E.2d 531 (Ind. 1985).

21. As pointed out in Loving v. Ponderosa Systems, Inc., supra, note 20, the theory of subrogation can also apply to allow a tenant to recover its share of insurance proceeds paid to a senior mortgagee. Following the application of insurance proceeds to the mortgage debt, the tenant, who has an obligation to rebuild the premises and who maintained the fire insurance policy, has the right to recover from the landlord the cost of reconstruction to the extent of the fire policy proceeds paid to the mortgagee. This outcome has the effect of shifting the risk of lack of availability of insurance proceeds to

j:\`sbo\WSBA Insurance Seminar\Lender's Security Interest in Casualty Policy Proceeds

10

the borrower-owner, notwithstanding the tenant's covenant to pay the cost of all repairs irrespective of the availability of insurance proceeds.

22. See Sportsmen’s Park v. N.Y. Prop. Underwriting Ass’n, 97 A.D.2nd 893, 894, 470 N.Y.S.2d 456, 459 (1983):

“The extent of a mortgagee's interest is determined, in the first instance, by the total amount of its lien, including the outstanding principal amount of the debt plus interest, plus any amounts expended to protect its security (i.e., taxes, insurance premiums, etc.), all as of the date of the fire [citations omitted].

23. Laurel National Bank v. Mutual Benefit Ins. Co., 444 A.2d 130 (Pa.Super. 1982); Grady v. Utica Mutual Ins. Co., 419 N.Y.S.2d 565 (N.Y. 2d Dept’t 1979); and Ben-Morris Co. v. Hanover Insurance Co., 333 N.E. 2d 455 (Mass.App. 1975).

24. Helmer v. Texas Farmers Insurance Co., 632 S.W.2d 194 (Tex.App. 1982); Nationwide Mutual Fire Ins. Co. v. Wilborn, 279 So.2d 460 (Ala.1973).

25. Sportsmen’s Park, supra.

26. Benton Banking Co. v. Tennessee Farmers Mutual Ins., 906 S.W.2d 426 (Tenn. 1995).

27. Cases providing coverage include Secured Realty Investment Fund v. Highlands Ins. Co., 678 So.2d 852 (Fla. 1996); Federal National Mortgage Association v. Ohio Casualty Ins. Co., 208 N.W.2d 573 (Mich. Ct. App. 1973). For a contrary view, see Economy Preferred Ins. V. Schomaker, 900 S.W.2d 252 (Mo.Ct.App. 1995).

j:\`sbo\WSBA Insurance Seminar\Lender's Security Interest in Casualty Policy Proceeds

11

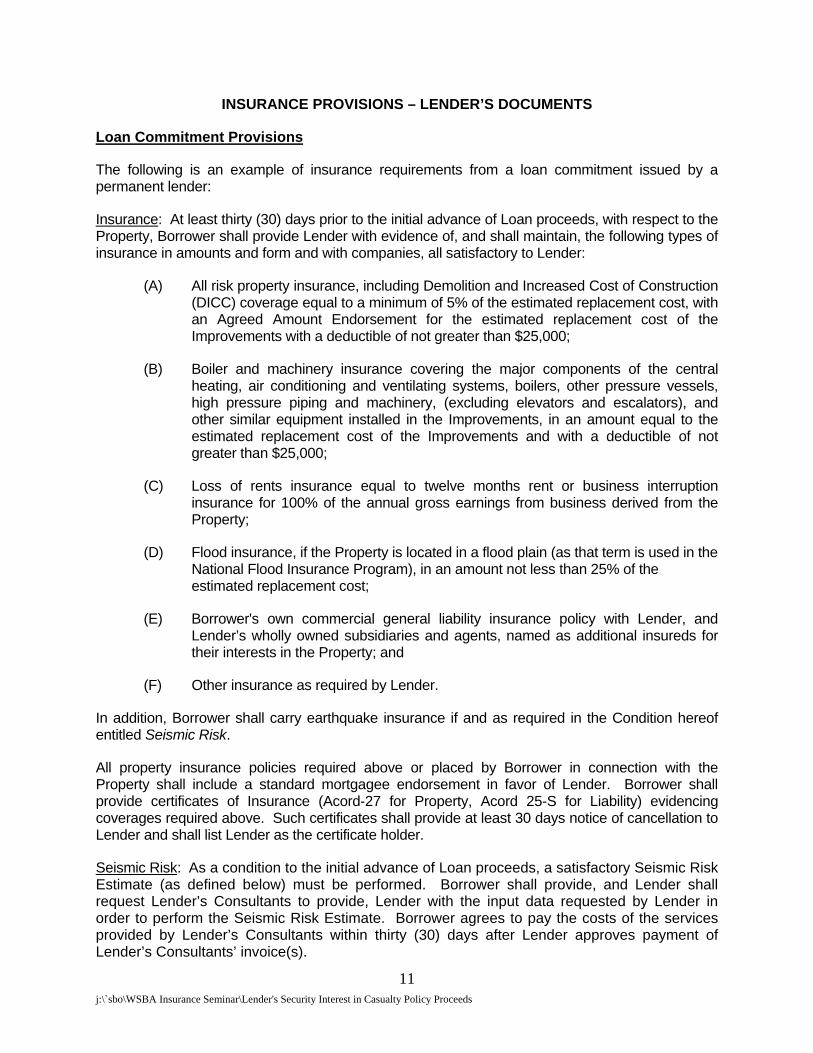

INSURANCE PROVISIONS – LENDER’S DOCUMENTS

Loan Commitment Provisions

The following is an example of insurance requirements from a loan commitment issued by a permanent lender:

Insurance: At least thirty (30) days prior to the initial advance of Loan proceeds, with respect to the Property, Borrower shall provide Lender with evidence of, and shall maintain, the following types of insurance in amounts and form and with companies, all satisfactory to Lender:

(A) All risk property insurance, including Demolition and Increased Cost of Construction (DICC) coverage equal to a minimum of 5% of the estimated replacement cost, with an Agreed Amount Endorsement for the estimated replacement cost of the Improvements with a deductible of not greater than $25,000;

(B) Boiler and machinery insurance covering the major components of the central heating, air conditioning and ventilating systems, boilers, other pressure vessels, high pressure piping and machinery, (excluding elevators and escalators), and other similar equipment installed in the Improvements, in an amount equal to the estimated replacement cost of the Improvements and with a deductible of not greater than $25,000;

(C) Loss of rents insurance equal to twelve months rent or business interruption insurance for 100% of the annual gross earnings from business derived from the Property;

(D) Flood insurance, if the Property is located in a flood plain (as that term is used in the National Flood Insurance Program), in an amount not less than 25% of the estimated replacement cost;

(E) Borrower's own commercial general liability insurance policy with Lender, and Lender’s wholly owned subsidiaries and agents, named as additional insureds for their interests in the Property; and

(F) Other insurance as required by Lender.

In addition, Borrower shall carry earthquake insurance if and as required in the Condition hereof entitled Seismic Risk.

All property insurance policies required above or placed by Borrower in connection with the Property shall include a standard mortgagee endorsement in favor of Lender. Borrower shall provide certificates of Insurance (Acord-27 for Property, Acord 25-S for Liability) evidencing coverages required above. Such certificates shall provide at least 30 days notice of cancellation to Lender and shall list Lender as the certificate holder.

Seismic Risk: As a condition to the initial advance of Loan proceeds, a satisfactory Seismic Risk Estimate (as defined below) must be performed. Borrower shall provide, and Lender shall request Lender’s Consultants to provide, Lender with the input data requested by Lender in order to perform the Seismic Risk Estimate. Borrower agrees to pay the costs of the services provided by Lender’s Consultants within thirty (30) days after Lender approves payment of Lender’s Consultants’ invoice(s).

j:\`sbo\WSBA Insurance Seminar\Lender's Security Interest in Casualty Policy Proceeds

12

Lender shall not require Earthquake Insurance (as defined below) or earthquake retrofit work in connection with the Loan if the Seismic Risk Estimate meets Minimum Seismic Criteria (as defined below). Lender may terminate the Commitment if the Specified Loss Percentage (as defined below) is greater than 30% OR if the Loan Plus Specified Loss (as defined below) is greater than 100% of the Market Value (as defined below).

If the Property does not meet the Minimum Seismic Criteria and Lender does not elect to terminate the Commitment, Borrower may be required, at Lender’s sole option, to:

(A) Enter into a Seismic Retrofit Agreement pursuant to which Borrower agrees to perform seismic retrofit to be completed within one year after the initial advance of Loan proceeds/redesign work to be completed prior to the commencement of construction satisfactory to Lender, and/or

(B) Provide Lender with evidence of, and maintain during the term of the Loan, Earthquake Insurance. Notwithstanding the foregoing, if Borrower shall complete seismic retrofit work, satisfactory to Lender, which results in the Property meeting Lender’s then current criteria for eliminating Earthquake Insurance, as verified by a subsequent Seismic Risk Estimate, Borrower shall no longer be required to maintain Earthquake Insurance.

If the Property is damaged by an earthquake at any time between the date hereof and payment of the Loan in full:

(X) Lender may require a new Seismic Risk Estimate to be performed at Borrower’s expense, and

(Y) Borrower shall perform repair and retrofit work, satisfactory to Lender, which results in (i) the complete repair of the Property and (ii) the performance of a subsequent Seismic Risk Estimate verifying that the Property meets Minimum Seismic Criteria. Such work shall be commenced and completed as soon as possible and in any event within one year of the earthquake, except that completion of all such repair and retrofit work on or before the Commitment Expiration Date shall be a condition to the advance of Loan proceeds.

Without limiting the Borrower’s obligation to cause the Property to satisfy Minimum Seismic Criteria, during any period of time in which the Property does not satisfy Minimum Seismic Criteria, Borrower shall provide Lender with evidence of, and maintain, Earthquake Insurance.

“Earthquake Insurance” means a policy satisfactory to Lender with a deductible of no greater than 5% of the Replacement Cost and in an amount calculated as follows: (i) the Loan Amount plus (ii) the Specified Loss Dollar Amount plus (iii) 5% of the Replacement Cost minus (iv) 90% of the Market Value.

“Loan Plus Specified Loss” means the sum of the Loan Amount and the Specified Loss Dollar Amount.

“Market Value” means the estimated fair market value of the Property, determined by Lender is its sole discretion, at the time a Seismic Risk Estimate is performed.

j:\`sbo\WSBA Insurance Seminar\Lender's Security Interest in Casualty Policy Proceeds

13

“Minimum Seismic Criteria” means that both the Specified Loss Percentage for the Property is less than or equal to 30% and the Loan Plus Specified Loss is less than or equal to 90% of the Market Value.

“Model” means a computer based seismic model selected by Lender, currently the Insurance and Investment Risk Assessment System (“IRAS”) program by Risk Management Solutions (“RMS”).

“Replacement Cost” means the estimated total cost, determined by Lender in its sole discretion, to construct all of the Improvements as if the Property were completely unimproved (not including the cost of site work, utilities and foundation).

“Seismic Risk Estimate” refers to the results of a seismic risk estimate for the Property produced by the Model. Borrower agrees that it will not rely for its own evaluation purposes on the Seismic Risk Estimate produced by or for Lender.

“Specified Loss Dollar Amount” means the Specified Loss Percentage multiplied by the Replacement Cost.

"Specified Loss Percentage" means an estimate produced by the Model of the earthquake damage to the Property, expressed as a percentage of Replacement Cost. Lender’s parameters for the Model are based on a 90% probability that the level of damage predicted will not be exceeded in an earthquake with an expected 475 year return period.

. . .

Application of Insurance Loss Proceeds: Insurance loss proceeds from all property insurance policies, whether or not required by Lender, shall, at Lender's option, be applied on the Loan, whether or not due, or to the restoration of the Property. If Lender elects to apply the insurance loss proceeds to the prepayment of the Loan, no prepayment fee shall be due on such prepayment.

Notwithstanding the foregoing, Lender agrees that, if the insurance loss proceeds are less than the unpaid principal balance of the Loan and if the casualty occurs prior to the last three (3) years of the Loan term, the insurance loss proceeds (less expenses of collection) shall be applied to restoration of the Property to its condition prior to the casualty, subject to satisfaction of the following conditions:

(A) There shall be no existing Event of Default at the time of the casualty, and if there shall occur any Event of Default after the date of the casualty, Lender shall have no further obligation to release insurance loss proceeds hereunder.

(B) The casualty insurer shall not have denied liability for payment of insurance loss proceeds as a result of any act, neglect, use or occupancy of the Property by Borrower or any tenant of the Property.

(C) Lender shall be satisfied that all insurance loss proceeds, together with supplemental funds to be made available by Borrower, shall be sufficient to complete restoration of the Property. Any remaining insurance loss proceeds may, at the option of Lender, be applied on the Loan, whether or not due, or be released to Borrower.

(D) If required by Lender, Lender shall be furnished a satisfactory report addressed to Lender from an environmental engineer or other qualified professional satisfactory to

j:\`sbo\WSBA Insurance Seminar\Lender's Security Interest in Casualty Policy Proceeds

14

Lender to the effect that no adverse environmental impact to the Property resulted from the casualty.

(E) Lender shall release casualty insurance proceeds as restoration of the Property progresses if Lender is furnished satisfactory evidence of the costs of restoration and if, at the time of such release, there shall exist no Monetary Default (as hereinafter defined) and no default under the Loan with respect to which Lender shall have given Borrower notice pursuant to the Condition hereof entitled Notice of Default. If the estimated cost of restoration exceeds $250,000, (i) the drawings and specifications for the restoration shall be approved by Lender in writing prior to commencement of the restoration and (ii) Lender shall receive an administration fee equal to (a) 1% of the cost of restoration if the cost of restoration is $5,000,000 or less or (b) the sum of $50,000 and 1/2% of the cost of restoration in excess of $5,000,000 if the cost of restoration is greater than $5,000,000.

(F) Prior to each release of funds, Borrower shall obtain for the benefit of Lender an endorsement to Lender's title insurance policy insuring Lender’s lien as a first and valid lien on the Property subject only to liens and encumbrances theretofore approved by Lender.

(G) Borrower shall pay all costs and expenses incurred by Lender, including, but not limited to, outside legal fees, title insurance costs, third-party disbursement fees, third-party engineering reports and inspections deemed necessary by Lender.

(H) All reciprocal easement and operating agreements, if any, benefiting the Property shall remain in full force and effect between the parties thereto on and after restoration of the Property.

(I) Lender shall be satisfied that Projected Debt Service Coverage of at least 1.10 will be produced from the leasing of not more than __________ square feet of space to former tenants or approved new tenants with leases satisfactory to Lender for terms of at least five (5) years to commence not later than thirty (30) days following completion of such restoration (the "Approved Leases").

(J) All leases in effect at the time of the casualty with tenants who have entered into Lender's form of Non-Disturbance and Attornment Agreement or similar agreement shall remain in full force and each tenant thereunder shall be obligated, or shall elect, to continue the lease at full rental (subject only to abatement, if any, during any period in which the Property or portion thereof shall not be used and occupied by such tenant as a result of the casualty).

(K) Without limiting the Seismic Risk provisions hereof, if the casualty has resulted in whole or part from an earthquake: (a) Borrower shall have supplied Lender with a “Seismic Risk Estimate” (in accordance with the Seismic Risk provisions herein) which show that the Property will meet “Minimum Seismic Criteria” (as defined in the Seismic Risk provisions herein) upon completion of repair and retrofit work which can be completed within one year of the earthquake, (b) prior to commencement of the restoration, Borrower shall have committed in writing to Lender that Borrower will do such repair and retrofit work as shall be necessary to cause the Property to in fact meet Minimum Seismic Criteria following completion of restoration, and (c) Lender must at all times during the restoration be reasonably satisfied that the Property will

j:\`sbo\WSBA Insurance Seminar\Lender's Security Interest in Casualty Policy Proceeds

15

meet Minimum Seismic Criteria following completion of the restoration, Borrower hereby agreeing to supply Lender with such evidence thereof as Lender shall request from time to time.

As used herein, "Projected Debt Service Coverage" means a number calculated by dividing Projected Operating Income Available for Debt Service for the first fiscal year following restoration of the Property by the debt service during the same fiscal year under all loans secured by any portion of the Property. For purposes of the preceding sentence, "debt service" means the greater of (x) debt service due under all such loans during the first fiscal year following completion of the restoration of the Property and (y) debt service that would be due and payable during such fiscal year if all such loans were amortized over 20 years (whether or not amortization is actually required) and if interest on such loans were due as it accrues at the face rate shown on the notes therefor (whether or not such loans require interest payments based on such face rates).

"Projected Operating Income Available for Debt Service" means projected gross annual rent from the Approved Leases for the first full fiscal year following completion of the restoration of the Property less:

(A) The operating expenses of the Property for the last fiscal year preceding the casualty and

(B) the following:

(i) a replacement reserve for future tenant improvements, leasing commissions and structural items based on not less than $_____ per square foot per annum;

(ii) the amount, if any, by which actual gross income during such fiscal period exceeds the sum of that which would be earned from the rental of 94% of the gross leaseable area of the Property;

(iii) the amount, if any, by which the actual management fee is less than 4% of effective gross income during such fiscal period;

(iv) the amount, if any, by which the actual real estate taxes are less than $_____ per square foot per annum; and

(v) the amount, if any, by which total operating expenses, excluding management fees, real estate taxes and replacement reserves, are less than $_____ per square foot per annum.

All projections referenced above shall be calculated in a manner satisfactory to Lender.

Sample Provisions for Deed of Trust – Long Term Lender

Granting Clause:

REAL PROPERTY GRANT. Grantor irrevocably sells, transfers, grants, conveys, assigns and warrants to Trustee, its successors and assigns, in trust, with power of sale and right of entry and possession, all of Grantor's present and

j:\`sbo\WSBA Insurance Seminar\Lender's Security Interest in Casualty Policy Proceeds

16

future estate, right, title and interest in and to the following which are collectively referred to as the "Real Property":

. . .

(c) all present and future income, rents, revenue, profits, proceeds, accounts receivables and other benefits from the Land and/or Improvements and all deposits made with respect to the Land and/or Improvements, including, but not limited to, any security given to utility companies by Grantor, any advance payment of real estate taxes or assessments, or insurance premiums made by Grantor and all claims or demands relating to such deposits and other security, including claims for refunds of tax payments or assessments, and all insurance proceeds payable to Grantor in connection with the Land and/or Improvements whether or not such insurance coverage is specifically required under the terms of this Deed of Trust ("Insurance Proceeds") (all of the items set forth in this paragraph are referred to collectively as "Rents and Profits"); . . .

Insurance Requirements:

3.01 REQUIRED INSURANCE AND TERMS OF INSURANCE POLICIES.

(a) During the term of this Deed of Trust, Grantor at its sole cost and expense must provide insurance policies and certificates of insurance satisfactory to Beneficiary as to amounts, types of coverage and the companies underwriting these coverages. In no event will such policies be terminated or otherwise allowed to lapse. Grantor shall be responsible for its own deductibles. Grantor shall also pay for any insurance, or any increase of policy limits, not described in the Deed of Trust which Grantor requires for its own protection or for compliance with government statutes. Grantor's insurance shall be primary and without contribution from any insurance procured by Beneficiary.

Policies of insurance shall be delivered to Beneficiary in accordance with the following requirements:

(1) All Risk Property insurance on the Improvements and the Personal Property, including contingent liability from Operation of Building Laws, Demolition Costs and Increased Cost of Construction endorsements, in each case (i) in an amount equal to 100% of the "Full Replacement Cost" of the Improvements and Personal Property, which for purposes of this Article III shall mean actual replacement value (exclusive of costs of excavations, foundations, underground utilities and footings) with a waiver of depreciation and with a Replacement Cost Endorsement; (ii) containing an agreed amount endorsement with respect to the Improvements and Personal Property waiving all co-insurance provisions; (iii) providing for no deductible in excess of $10,000; and (iv) containing an "Ordinance or Law Coverage" or "Enforcement" endorsement if any of the Improvements or the use of the Property shall constitute non-conforming structures or uses. The Full Replacement Cost shall be determined from time to time by an appraiser or contractor designated and paid by Grantor and approved by Beneficiary or by an engineer or appraiser in the regular employ of the insurer.

j:\`sbo\WSBA Insurance Seminar\Lender's Security Interest in Casualty Policy Proceeds

17

(2) Commercial General Liability insurance against claims for personal injury, bodily injury, death or property damage occurring upon, in or about the Property, such insurance (i) to be on the so-called "occurrence" form with a combined single limit of not less than the amount set forth in the Defined Terms; (ii) to continue at not less than this limit until required to be changed by Beneficiary in writing by reason of changed economic conditions making such protection inadequate; and (iii) to cover at least the following hazards: (a) premises and operations; (b) products and completed operations on an "if any" basis; (c) independent contractors; (d) blanket contractual liability for all written and oral contracts; and (e) contractual liability covering the indemnities contained in this Deed of Trust to the extent available.

(3) Business Income insurance in an amount sufficient to prevent Grantor from becoming a co-insurer within the terms of the applicable policies, and sufficient to recover one (1) year's "Business Income" (as hereinafter defined). The amount shown in the Defined Terms is the current estimate of one year's "Business Income". "Business Income" shall mean the sum of (i) the total anticipated gross income from occupancy of the Property, (ii) the amount of all charges (such as, but not limited to, operating expenses, insurance premiums and taxes) which are the obligation of tenants or occupants to Grantor, (iii) the fair market rental value of any portion of the Property which is occupied by Grantor, and (iv) any other amounts payable to Grantor or to any affiliate of Grantor pursuant to leases.

(4) If Beneficiary determines at any time that any part of the Property is located in an area identified on a Flood Hazard Boundary Map or Flood Insurance Rate Map issued by the Federal Emergency Management Agency as having special flood hazards and flood insurance has been made available, Grantor will maintain a flood insurance policy meeting the requirements of the current guidelines of the Federal Insurance Administration with a generally acceptable insurance carrier, in an amount not less than the lesser of (i) the outstanding principal balance of the Loan or (ii) the maximum amount of insurance which is available under the National Flood Insurance Act of 1968, the Flood Disaster Protection Act of 1973 or the National Flood Insurance Reform Act of 1994, as amended.

(5) During the period of any construction or renovation or alteration of the Improvements, a so-called "Builder's All Risk" insurance policy in non-reporting form for any Improvements under construction, renovation or alteration including, without limitation, for demolition and increased cost of construction or renovation, in an amount approved by Beneficiary including an Occupancy endorsement and Worker's Compensation Insurance covering all persons engaged in the construction, renovation or alteration in an amount at least equal to the minimum required by statutory limits of the State.

(6) Workers' Compensation insurance, subject to the statutory limits of the State, and employer's liability insurance with a limit of at least $1,000,000 per accident and per disease per employee, and $1,000,000

j:\`sbo\WSBA Insurance Seminar\Lender's Security Interest in Casualty Policy Proceeds

18

for disease in the aggregate in respect of any work or operations on or about the Property, or in connection with the Property or its operations (if applicable).

(7) Boiler & Machinery insurance covering the major components of the central heating, air conditioning and ventilating systems, boilers, other pressure vessels, high pressure piping and machinery, elevators and escalators, if any, and other similar equipment installed in the Improvements, in an amount equal to one hundred percent (100%) of the full replacement cost of all equipment installed in, on or at the Improvements. These policies shall insure against physical damage to and loss of occupancy and use of the Improvements arising out of an accident or breakdown.

(8) Such other insurance as may from time to time be reasonably required by Beneficiary against other insurable hazards, including, but not limited to, vandalism, earthquake, sinkhole and mine subsidence.

(b) Beneficiary's interest must be clearly stated by endorsement in the insurance policies described in this Section 3.01 as follows:

(1) The policies of insurance referenced in Subsections (a)(1), (a)(3), (a)(4), (a)(5) and (a)(7) of this Section 3.01 shall identify Beneficiary under the New York Standard Mortgagee Clause (non-contributory) endorsement.

(2) The insurance policy referenced in Section 3.01 (a)(2) shall name Beneficiary as an additional insured.

(3) All of the policies referred to in Section 3.01 shall provide for at least thirty (30) days' written notice to Beneficiary in the event of policy cancellation and/or material change.

(c) All the insurance companies must be authorized to do business in New York State and the State and be approved by Beneficiary. The insurance companies must have a general policy rating of A or better and a financial class of X or better by A.M. Best Company, Inc. and a claims paying ability of BBB or better according to Standard & Poors. If there are any Securities (as defined in Section 12.01) issued with respect to this Loan which have been assigned a rating by a credit rating agency approved by Beneficiary (a "Rating Agency"), the insurance company shall have a claims paying ability rating by such Rating Agency equal to or greater than the rating of the highest class of the Securities. Grantor shall deliver evidence satisfactory to Beneficiary of payment of premiums due under the insurance policies.

(d) Certified copies of the policies, and any endorsements, shall be made available for inspection by Beneficiary upon request. If any policy is canceled before the Loan is satisfied, and Grantor fails to immediately procure replacement insurance, Beneficiary reserves the right but shall not have the obligation immediately to procure replacement insurance at Grantor's cost.

j:\`sbo\WSBA Insurance Seminar\Lender's Security Interest in Casualty Policy Proceeds

19

(e) Grantor shall be required during the term of the Loan to continue to provide Beneficiary with original renewal policies or replacements of the insurance policies referenced in Section 3.01 (a). Beneficiary may accept Certificates of Insurance evidencing insurance policies referenced in Subsections (a)(2), (a)(4), and (a)(6) of this Section 3.01 instead of requiring the actual policies. Beneficiary shall be provided with renewal Certificates of Insurance, or Binders, not less than fifteen (15) days prior to each expiration. The failure of Grantor to maintain the insurance required under this Article III shall not constitute a waiver of Grantor's obligation to fulfill these requirements.

(f) All binders, policies, endorsements, certificates, and cancellation notices are to be sent to the Beneficiary's Address for Insurance Notification as set forth in the Defined Terms until changed by notice from Beneficiary.

3.02 ADJUSTMENT OF CLAIMS. Grantor hereby authorizes and empowers Beneficiary to settle, adjust or compromise any claims for damage to, or loss or destruction of, all or a portion of the Property, regardless of whether there are Insurance Proceeds available or whether any such Insurance Proceeds are sufficient in amount to fully compensate for such damage, loss or destruction.

3.03 ASSIGNMENT TO BENEFICIARY. In the event of the foreclosure of this Deed of Trust or other transfer of the title to the Property in extinguishment of the Secured Indebtedness, all right, title and interest of Grantor in and to any insurance policy, or premiums or payments in satisfaction of claims or any other rights under these insurance policies and any other insurance policies covering the Property shall pass to the transferee of the Property.

Sample Deed of Trust Insurance Provisions – Construction Lender

Granting Clause:

. . .

COLLATERAL. The following described estate, property and rights of Grantor are also included as security for the performance of each covenant and agreement of Grantor contained herein and the payment of all sums of money secured hereby:

. . .

(a) All compensation, awards, damages, rights of action and proceeds (including insurance proceeds and any interest on any of the foregoing) arising out of or relating to a taking or damaging of the Property by reason of any public or private improvement, condemnation proceeding (including change of grade), fire, earthquake or other casualty, injury or decrease in the value of the Property.

. . .

INSURANCE.

j:\`sbo\WSBA Insurance Seminar\Lender's Security Interest in Casualty Policy Proceeds

20

(a) Grantor shall maintain such insurance on the Collateral as may be required from time to time by Beneficiary, with premiums prepaid, providing replacement cost coverage and insuring against loss by fire and such other risks covered by extended coverage insurance, and such other perils and risks as Beneficiary may require from time to time, including earthquake, loss of rents and business interruption. Grantor also shall maintain comprehensive general public liability insurance and if the Property is located in a designated flood hazard area, flood insurance. All insurance shall be with companies satisfactory to Beneficiary and in such amounts and with such coverages as Beneficiary may require from time to time, with lender's loss payable clauses in favor of and in form satisfactory to Beneficiary. At least thirty (30) days prior to the expiration of the term of any insurance policy, Grantor shall furnish Beneficiary with written evidence of renewal or issuance of a satisfactory replacement policy. If requested Grantor shall deliver copies of all polices to Beneficiary. Each policy of insurance shall provide Beneficiary with no less than forty-five (45) days prior written notice of any cancellation, expiration, non-renewal or modification.

(b) In the event of foreclosure of this Deed of Trust all interest of Grantor in any insurance policies pertaining to the Collateral and in any claims against the policies and in any proceeds due under the policies shall pass to Beneficiary.

(c) If under the terms of any Lease the lessee is required to maintain insurance of the type required by the Loan Documents and if the insurance is maintained for the benefit of both the lessor and Beneficiary, Beneficiary will accept such policies provided all of the requirements of Beneficiary and the Loan Documents are met. In the event the lessee fails to maintain such insurance, Grantor shall promptly obtain such policies as are required by the Loan Documents.

(d) If Grantor fails to maintain any insurance required of it by Beneficiary, or fails to pay any premiums with respect to such insurance, Beneficiary may obtain such replacement insurance as it deems necessary or desirable, or pay the necessary premium on behalf of Grantor, and any sums expended by Beneficiary in so doing shall be added to the principal balance of the Note and bear interest at the default interest rate set forth in the Note.

DAMAGES AND CONDEMNATION AND INSURANCE PROCEEDS.

(a) Grantor hereby absolutely and irrevocably assigns to Beneficiary, and authorizes the payor to pay to Beneficiary, the following claims, causes of action, awards, payments and rights to payment: (i) all awards of damages and all other compensation payable directly or indirectly because of a condemnation, proposed condemnation or taking for public or private use which affects all or part of the Collateral or any interest in it; (ii) all other awards, claims and causes of action, arising out of any warranty affecting all or any part of the Collateral, or for damage or injury to or decrease in value of all or part of the Collateral or any interest in it; (iii) all proceeds of any insurance policies payable because of loss sustained to all or part of the Collateral; and (iv) all interest which may accrue on any of the foregoing.

j:\`sbo\WSBA Insurance Seminar\Lender's Security Interest in Casualty Policy Proceeds

21

(b) Grantor shall immediately notify Beneficiary in writing if: (i) any damage occurs or any injury or loss is sustained in the amount of $25,000 or more to all or part of the Collateral, or any action or proceeding relating to any such damage, injury or loss is commenced; or (ii) any offer is made, or any action or proceeding is commenced, which relates to any actual or proposed condemnation or taking of all or part of the Collateral. If Beneficiary chooses to do so, it may in its own name appear in or prosecute any action or proceeding to enforce any cause of action based on warranty, or for damage, injury or loss to all or part of the Collateral, and it may make any compromise or settlement of the action or proceeding. Beneficiary, if it so chooses, may participate in any action or proceeding relating to condemnation or taking of all or part of the Collateral, and may join Grantor in adjusting any loss covered by insurance.

(c) All proceeds of these assigned claims, other property and rights which Grantor may receive or be entitled to shall be paid to Beneficiary. In each instance, Beneficiary shall apply those proceeds first toward reimbursement of all of Beneficiary's costs and expenses of recovering the proceeds, including attorneys' fees.

(d) If, in any instance, each and all of the following conditions are satisfied in Beneficiary's reasonable judgment, Beneficiary shall permit Grantor to use the balance of the proceeds ("Net Claims Proceeds") to pay costs of repairing or reconstructing the Collateral in the manner described below: (i) the plans and specifications, cost breakdown, construction contract, construction schedule, contractor and payment and performance bond for the work of repair or reconstruction must all be acceptable to Beneficiary; (ii) Beneficiary must receive evidence satisfactory to it that after repair or reconstruction, the Collateral will be at least as valuable as it was immediately before the damage or condemnation occurred; (iii) the Net Claims Proceeds must be sufficient in Beneficiary's determination to pay for the total cost of repair or reconstruction, including all associated development costs and interest projected to be payable on the Note until the repair or reconstruction is complete; or Grantor must provide its own funds in an amount equal to the difference between the Net Claims Proceeds and a reasonable estimate, made by Grantor and found acceptable by Beneficiary, of the total cost of repair or reconstruction; (iv) Beneficiary must receive evidence satisfactory to it that all Leases which it may find acceptable will continue after the repair or reconstruction is complete; (v) Beneficiary has received evidence satisfactory to it, that reconstruction and/or repair can be completed at least three (3) months prior to the date the Note secured by this Deed of Trust is due and payable; and (vi) no default under any of the Loan Documents shall have occurred and be continuing. If the foregoing conditions are met to Beneficiary's satisfaction, Beneficiary shall hold the Net Claims Proceeds and any funds which Grantor is required to provide and shall disburse them to Grantor to pay costs of repair or reconstruction upon presentation of evidence reasonably satisfactory to Beneficiary that repair or reconstruction has been completed satisfactorily and lien-free. However, if Beneficiary finds that one or more of the conditions are not satisfied, it may apply the Net Claims Proceeds to pay or prepay some or all of the Note.

j:\`sbo\WSBA Insurance Seminar\Lender's Security Interest in Casualty Policy Proceeds

22

Assignment of Lease Provision

2. Present and Absolute Assignment of Leases. Assignor absolutely, pres-ently and unconditionally grants, assigns and transfers to Assignee all of Assignor's right, title and interest in and to the Leases. This grant includes without limitation: (a) all rent payable under the Leases; (b) all tenant security deposits held by Assignor pursuant to the Leases; (c) all additional rent payable under the Leases; (d) all proceeds of insurance payable to Assignor under the Leases and all awards and payments on account of any taking or condemnation; and (e) all claims, damages and other amounts payable to Assignor in the event of a default under or termination of any of the Leases, including without limitation all of Assignor's claims to the payment of damages arising from any rejection by a tenant of any Lease under the Bankruptcy Code as amended from time to time. All of the items referred to in this Section 2 are collectively referred to in this Agreement as the "Income".