LEE Siak Kwee - Cloud Object Storage | Store & Retrieve...

108

DISCONTINUITIES IN THE TELECOM INDUSTRY: STRATEGIC CHOICES FOR SINGTEL by LEE Siak Kwee MBA in Singapore Programme 2008 A Management Project presented in part consideration for the degree of Master of Business Administration

Transcript of LEE Siak Kwee - Cloud Object Storage | Store & Retrieve...

DISCONTINUITIES IN THE TELECOM INDUSTRY:

STRATEGIC CHOICES FOR SINGTEL

by

LEE Siak Kwee

MBA in Singapore Programme

2008

A Management Project presented in part consideration for the degree of Master

of Business Administration

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

MBA Management Project 1 Lee Siak Kwee

EXECUTIVE SUMMARY

This report examines the corporate strategy of SingTel and show how they can be

derived from a combined analysis of its internal and external environment. An

outside-in, position-based approach using the Porter’s Five Forces (PFF) model is

used to analyse the complexities and forces shrouding the industry with the aim of

identifying the key opportunities and threats. An inside-out, resource-based approach

using the Resource Based View (RBV) is also undertaken to reveal SingTel’s key

strengths and weaknesses. Interviews were also conducted with two key management

executives within SingTel to gain a first hand understanding of the strategic issues

from an insider perspective.

Integrating the results of these two analysis and insights into a SWOT framework, a

synthesis of the key strategic factors is then performed to match those strengths that

can exploit opportunities and/or neutralize threats, and at the same time, determine

what new competence needs to be acquired by SingTel to overcome the potential of

external threats exploiting its current weaknesses. It is shown that the strategic

choices that SingTel has made as its corporate strategy are congruent and aligned with

the dynamics of its internal and external environment.

SingTel’s three-pronged corporate strategy of leading in local market; inorganic

growth through overseas investment and innovation to mitigate commoditisation, are

intricately shaped by the SWOT analysis as derived from RBV and PFF. This dual

assessment has also highlighted the need for SingTel to seriously consider an asset-

light strategy in view of mounting cost pressures and the reality that the “value” in the

value chain is progressively moving to the edges and outside of the traditional

network boundaries. On top of its innovation strategy, SingTel may need a new

corporate strategy to outsource its network and reinvent itself by focusing on building

new competences like multimedia, alliances and partnerships to tackle the emergence

of non-traditional players.

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

MBA Management Project 2 Lee Siak Kwee

TABLE OF CONTENTS Page 1. INTRODUCTION…………………………………………… 5

2. BACKGROUND……………………………………………. 7

2.1 Recent History………………………………………………. 7

2.2 SingTel’s Corporate Vision & Strategy………………….…. 8

3. METHODOLOGIES………………………………………….. 12

3.1 Hierarchy of Strategy……………………………………….. 12

3.2 External Analysis- Porter’s Five Forces……………………. 13

3.3 Internal Analysis - Resource Based View………………….. 16

3.4 Other Strategy Concepts……………………………………. 18

4. STRATEGIC ANALYSIS OF THE INDUSTRY ENVIRONMENT

……………………………………………………………….. 19

4.1 Objectives……………………………………………………. 19

4.2 Porter’s Five Forces Analysis………………………………. 19

4.2.1 Industry Competitors……………………………………….. 19

4.2.2. New Entrants ……………………………………………….. 35

4.2.3 Buyers……………………………………………………….. 40

4.2.4 Suppliers…………………………………………………….. 43

4.2.5 Substitutes…………………………………………………… 48

5. STRATEGIC ANALYSIS OF THE INTERNAL

ENVIRONMENT – A RESOURCE BASED VIEW (RBV) 51

5.1 Strengths…………………………………………………….. 51

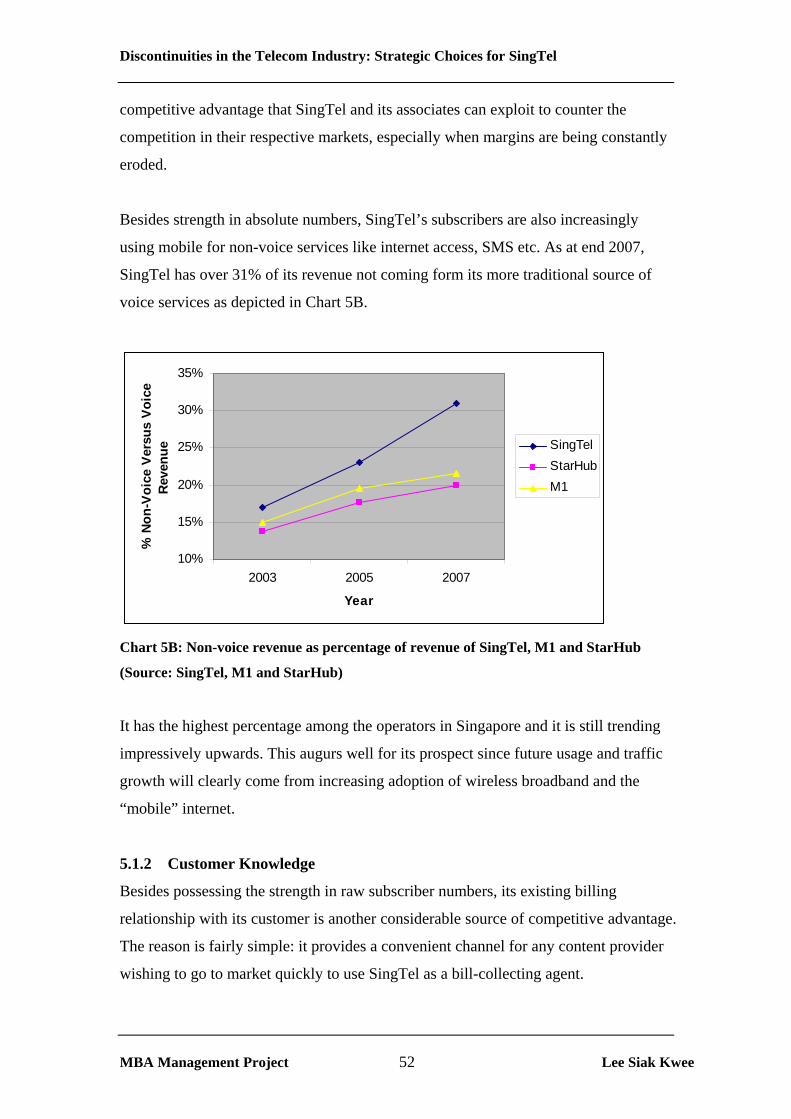

5.1.1 Strength in Numbers………………………………………… 51

5.1.2 Customer Knowledge……………………………………….. 52

5.1.3 Financial Strengths………………………………………….. 53

5.1.4 Investment Savvy…………………………………………… 54

5.1.5 Brand Equity………………………………………………… 56

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

MBA Management Project 3 Lee Siak Kwee

TABLE OF CONTENTS

Page

5.2 VRIN Criteria ……………………………………………...... 56

5.3 Potential Weaknesses?.............................................................. 57

5.3.1 Technical Capability – Core Competence or Core Rigidity?. 57

5.3.2 Government Linked – Boon or Bane?...................................... 60

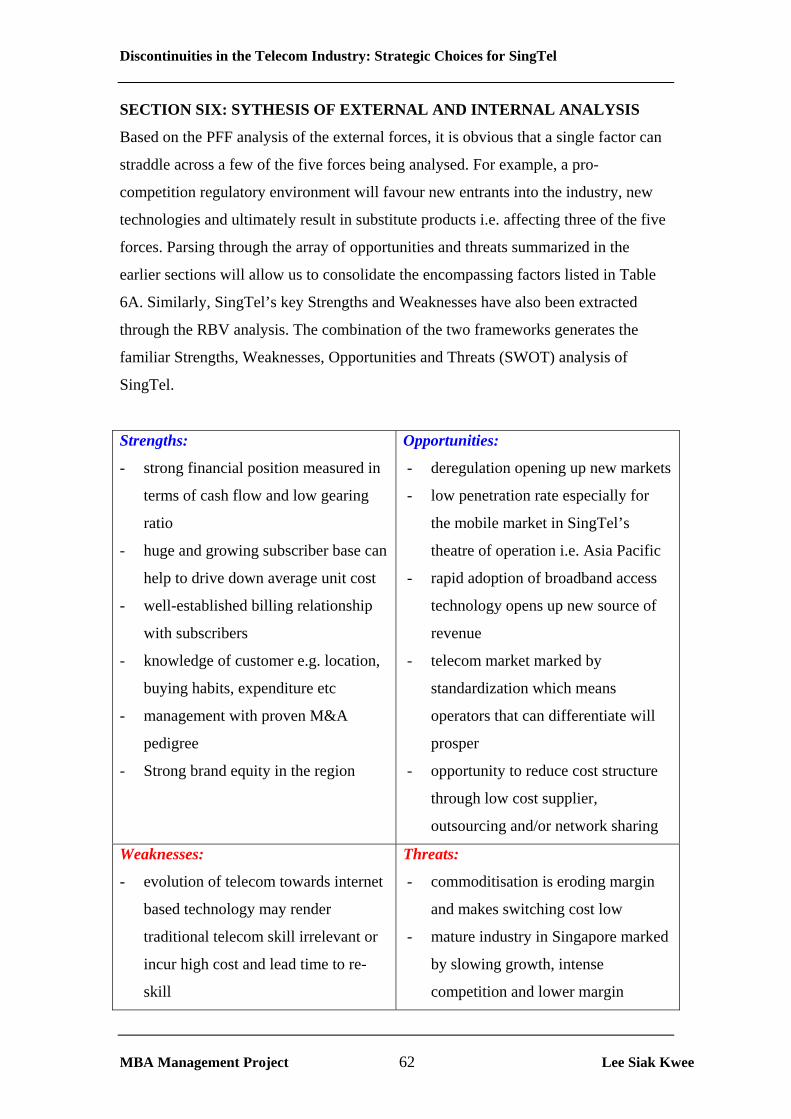

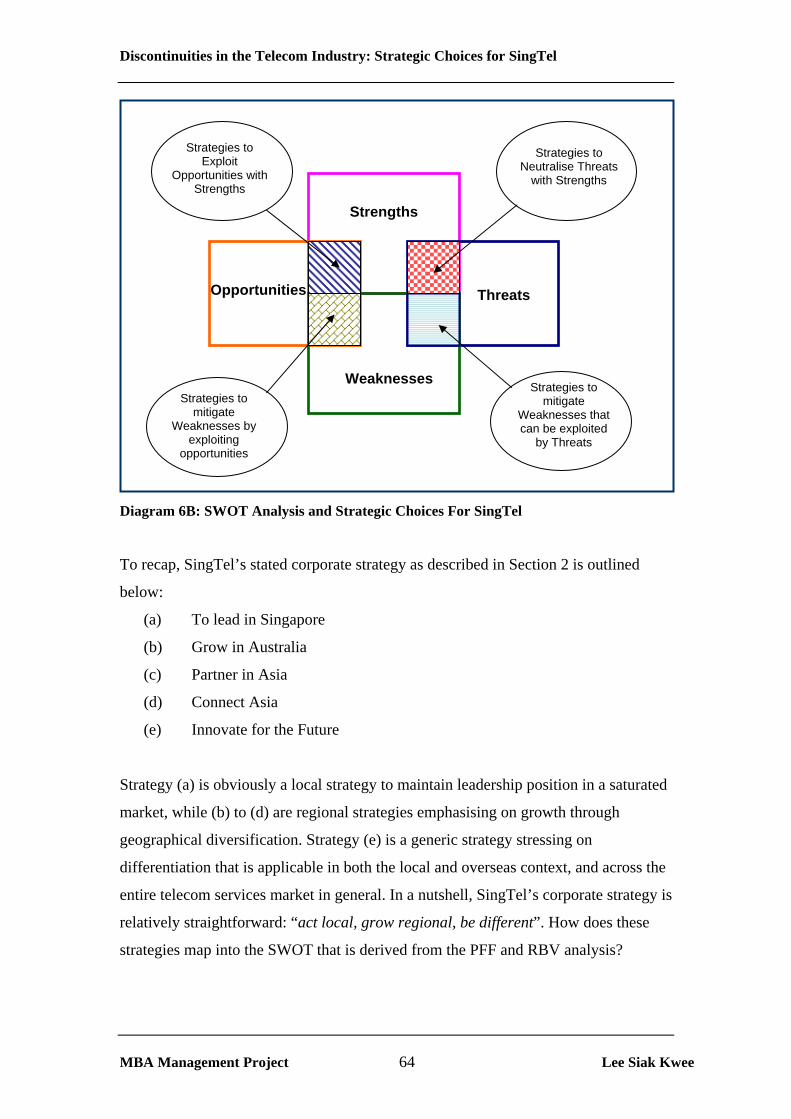

6. SYTHESIS OF EXTERNAL AND INTERNAL ANALYSIS 62

6.1 Leveraging Strengths to Exploit Opportunities

and/or Neutralize Threats……………………………………... 65

6.2 Alleviating Weaknesses and Mitigating External Threats…….. 66

6.3 Exploiting Opportunities to Alleviate Weaknesses……….…… 69

7. SUMMARY AND CONCULSIONS…………………………... 71

REFERENCES………………………………………………………….. 74

ANNEX 1 ……………………………………………………………….. 79

ANNEX 2 ……………………………………………………………….. 80

ANNEX 3 ……………………………………………………………….. 89

ANNEX 4 ……………………………………………………………….. 98

ANNEX 5 ……………………………………………………………….. 107

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

MBA Management Project 4 Lee Siak Kwee

ACKNOWLEDGEMENT

I would like to thank Dr Rajesh Kumar for his thoughtful and stimulating guidance on

this project. His invaluable advice has been instrumental in steering me onto the right

track and helping me to put the appropriate focus on the important areas.

My sincere appreciation also goes out to the following subject matter expert from

SingTel for agreeing to my email and face to face interview and gather valuable

insights of their thoughts on this subject. They are Mark Chong, Executive Vice

President (Networks) and Chris Lane, Group Chief Strategy Officer.

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

MBA Management Project 5 Lee Siak Kwee

SECTION ONE: INTRODUCTION

Apple’s iPhone was all the rave in the telecommunications industry in 2007. It was

named Time’s magazine “Gadget of the Year 2007” and Telecom Asia (Dec 2007)

hailed is as “easily the biggest telecom success story of 2007”. It is perhaps not major

news to hear of Apple winning another accolade for yet another iconic product, but

what is more telling is that Apple is making waves in an industry where it is

considered a non-traditional player. Such quantum shift is an unmistakable sign of the

discontinuities shaking up the hitherto stable telecommunication industry.

Technically, the iPhone falls short of what one would consider an industry “standard”;

it does not even support the latest Third Generation (3G) mobile communication

technology. What differentiates iPhone from the dizzying array of handsets in the

market is its ultra-intuitive user interface. But for operators like SingTel, what is

undoubtedly more ominous is that Apple is imposing a new business model for the

iPhone. In the markets where iPhone has been launched, not only is Apple selling it

through just one exclusive mobile operator, it is also taking a cut of the monthly

revenue generated by the iPhone user. This is unprecedented in the mobile business or

for that matter, in the more general telecom industry. It marks the first time that a

device manufacturer can have such bargaining power as to be able to demand a slice

of the operator’s recurring revenue.

The impact of iPhone is a microcosm of the discontinuities taking place in the telecom

landscape and it illustrates how existing rules are being rewritten, not by incumbents,

but by new challengers in the value chain. Besides the advent of such unconventional

new entrants, the telecom industry is also undergoing a state of constant flux through

a confluence of external factors like regulatory changes and disruptive technologies,

among other things. Such revolutionary transformation to the whole ecosystem

portends radical rather than incremental changes. It is unchartered territory and

necessitates traditional players like SingTel to seriously reassess its strategic position

in order to stay relevant in future.

The purpose of this case study is to investigate the strategic choices that SingTel has

made in its corporate strategy and how they can be derived from a combined analysis

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

MBA Management Project 6 Lee Siak Kwee

of its internal and external environment. In the first part, a detailed analysis is carried

out to understand the strategic position of SingTel vis-à-vis its external environment.

Porter’s Five Forces (Porter, 1979) model is used as it provides an elegant yet

systematic framework to analyse the underlying competitive and disruptive forces at

play within the ecosystem of the industry. The output of this assessment will provide

an incisive view of the different opportunities and threats that SingTel has to contend

with at present and in future.

The second part of the report takes the Resource Based View (RBV) approach to

determine what valuable resources are at SingTel’s disposal. This is an introspective

assessment of the organisation’s capabilities focusing on those strengths that can be

leveraged and how they can be collectively configured as bases of competitive

advantage. Similarly, the weaknesses of SingTel will also be identified so that the

potential resource gaps can be identified and filled.

Apart from the two frameworks, email and face to face interviews have also been

conducted with two top management executives within SingTel to gather their

thoughts on this topic. The strategic outputs from these analysis and discussions will

be synthesised within the familiar SWOT framework and shown how they can guide

and be used to formulate courses of action or strategic choices for SingTel. This part

of the discussion will focus on how the “fit” between the internal resources and the

external opportunities and threats is manifested in SingTel’s current corporate strategy.

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

MBA Management Project 7 Lee Siak Kwee

SECTION TWO: BACKGROUND

2.1 Recent History

With presence in countries stretching from Australia to India, Singapore

Telecommunications (SingTel) is today widely regarded as a pan-Asian

telecommunications giant. But when the former government statutory board was

listed on the Singapore Exchange in 1993, few could have imagined such a dramatic

transformation 15 years later.

The 1990s witnessed a wave of deregulation sweeping through the telecommunication

industry all over the world. Government monopolies were being dismantled as rapidly

as markets were being liberalized with the injection of more competition. ITU (2002)

reported that from 10% in 1992, more than 60% of all the countries had some form of

competition in the telecom industry by 2000. Singapore was no exception. The first

wave of deregulation hit SingTel in April 1997 with the opening up of the mobile and

paging markets. But the “big bang” came in April 2000, when the whole Singapore

telecommunications market was opened up to unlimited competition (IDA, 2000).

Accompanying the radical changes in the regulatory landscape globally, the 1990s

also saw the advent of digital technology that would revolutionarise the way people

communicate. Voice over Internet Protocol (VOIP) and the internet blurred

geographically boundaries and decimated the highly lucrative International Direct

Dial (IDD) business that was hitherto the major cash cow of traditional telecom

carriers like SingTel. From a 45.3% share of its total revenue in 1996 (Tan, 1999),

IDD revenue today has dropped to no more than 5% of total revenue (SingTel 2008).

The drop in profit margin is even more dramatic: the average IDD call rate dropped

from S$ 2.05 per minute (Foo, 2000) to less than S$0.31 per min in 2007 (SingTel,

2007). This exemplifies how disruptive technologies can cause major discontinuities

in the industry structure.

While deregulation and new technologies caused major shakeup in its domestic

markets, it also meant new opportunities were opening up for SingTel in other

markets. The erstwhile government monopoly which derived most of its profits from

its domestic market is now a major regional player with over three quarter of its

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

EBITDA (Earnings before interest, tax, depreciation and amortization) coming from

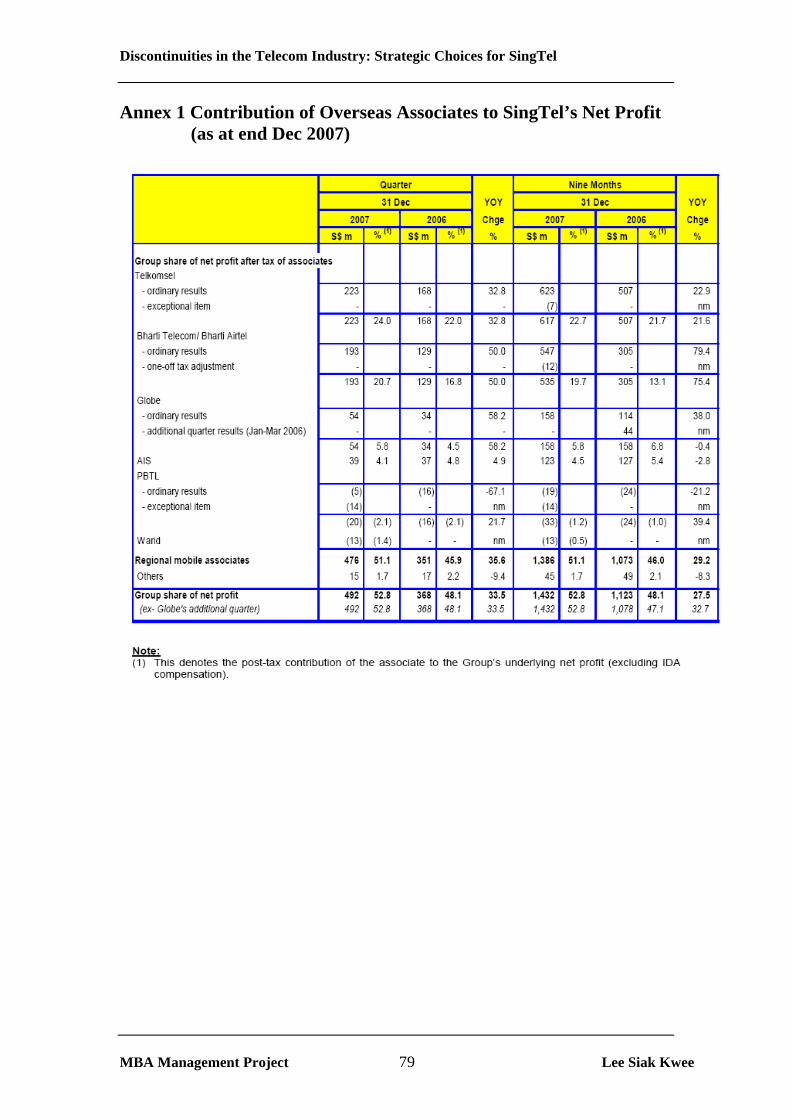

its overseas venture (SingTel, 2007) as shown in Chart 2A. Annex 1 provides a more

detail breakdown of the associates’ contribution to SingTel’s overall bottom line.

SingTel, 24%

Optus, 31%

Others, 1%

Regional Mobile, 44%

Chart 2A: SingTel’s Proportionate EBITDA Distribution as at end Dec 2007 (Source:

SingTel)

2.2 SingTel’s Corporate Vision & Strategy

SingTel’s organization structure as shown in Chart 2B is a direct reflection of its

strategic business focus. Under the Group CEO are three other line CEOs responsible

for SingTel’s three main geographical business units namely: Singapore, Optus

Australia and International.

MBA Management Project 8 Lee Siak Kwee

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

.

Chart 2B : SingTel Organisational Chart (Source: SingTel Web site: www.singtel.com)

The five elements of SingTel’s corporate strategy (SingTel, 2008) are essentially

tailored to meet its stated corporate vision which is “to be Asia Pacific’s best

communications group”:

(a) Lead in Singapore – to be the leading telecommunications operator in

Singapore with a stable and cash generative business. This is achieved

through its ability to defend its market share and margins by offering a

comprehensive package of communications services and integrated IT

services, coupled with strong brand recognition.

(b) Grow in Australia – Position the wholly-owned subsidiary Optus as

the leading challenger to the incumbent telecommunications operator.

Optus aims to maintain its track record of market share growth, expand

margins, grow profits and cashflow by delivering simple, innovative

and reliable experience for customers; ensure cost leadership in target

markets; establish leadership in attractive new markets; strengthen the

MBA Management Project 9 Lee Siak Kwee

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

MBA Management Project 10 Lee Siak Kwee

company's "challenger" culture; and leverage the scale of the SingTel

Group as a whole.

(c) Partner across Asia - SingTel key focus is on execution and

maximising the value of existing businesses and regional partnerships.

This has included reviewing opportunities to increase shareholdings in

existing associates and consider new investments. SingTel has

commendable record of making successful acquisitions and

investments. The geographic focus will remain in Asia Pacific, with a

preference for strategic investments where SingTel can add value by

taking an active role in management, and which can be funded from

internal cash flow generation.

(d) Connect Asia – To serve the needs of multinational corporations,

SingTel has a network of 38 offices in 19 countries and territories

throughout Asia Pacific, in Europe and the USA. These offices enable

SingTel to deliver reliable and quality network solutions to its

customers, either on its own or with local partners. It also has an

extensive infrastructure made up of satellite networks and submarine

cable systems throughout Asia Pacific, providing connectivity across

the region and to the rest of the world.

(e) Innovate for the Future - Providing innovative communications

solutions to meet evolving customer needs has been core to SingTel’s

success. SingTel targets to nurture its human and intellectual capital to

achieve organisational excellence in order to enhance its position as an

integrated provider of wireline and wireless services for businesses and

consumers.

Going forward, with the dynamic environment undergoing more sea-change, are these

strategies still relevant for SingTel to maintain its growth? The Singapore market,

especially in the major business areas like mobile and broadband services, is

increasingly being commoditised with market penetration at saturation point.

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

MBA Management Project 11 Lee Siak Kwee

Regionally, SingTel has also seen opportunities for acquisition becoming more

restrictive and even financially prohibitive with premium valuations demanded by

potential sellers. And the example of iPhone clearly illustrates the sort of

unconventional competitor that SingTel will have to face-off in future.

Mark Chong, EVP(Networks) of SingTel highlighted that, “The threats to any

business are often multi-faceted. Likewise, SingTel’s business is subject to challenges

from liberalisation which brings in more competition, as well as disruptive

technologies that could potentially render obsolete, investments which had yet to yield

their necessary returns.” Is SingTel’s corporate strategy a sound one vis-à-vis the

external environment that it faces and the internal resources that it can leverage on?

Does it fully uses it competitive advantage to exploit the opportunities or neutralize

threats, both present and in future? The following sections will seek to provide the

answers to these key questions.

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

MBA Management Project 12 Lee Siak Kwee

SECTION THREE: METHODOLOGIES

The two basic frameworks used in the analysis of external and internal environment

are the Porter’s Five Forces (PFF) and the Resource Based View (RBV) of the firm.

In addition, interviews have also been conducted with two key top management

executives in SingTel to gather their view on this subject. Mark Chong, the Executive

Vice President of SingTel’s Networks Group, gave general feedback through an email

interview on the strategic issues facing SingTel today and for the engineering aspect

in particular. A face to face interview was also conducted with the strategy guru in

SingTel, Chris Lane, who is the Group Chief Strategy Officer. Many of their insights

have been incorporated into the discussions throughout the paper and where

appropriate, quoted for emphasis sake. But before delving into the mechanics of the

methodologies, it is important to clearly define the scope of the “strategy” that this

report is intending to research.

There is no common definition of strategy and Mintzberg (1987), for example,

provided five different definitions although it is widely accepted that the fundamental

purpose of a business is to earn a profit over and above the cost of capital employed.

Hence strategy is basically the means to manage and direct a business in its

environment towards a competitive advantage in the market place (Porter, 1996).

3.1 Hierarchy of Strategy

Johnson & Scholes (1999) defined strategy in 3 different levels based on a descending

hierarchy:

(a) Corporate Strategy - concerned with the overall purpose and scope of

the organisation

(b) Business Unit Strategy – focus on how to compete successfully in a

particular market

(c) Operational Strategies – deals with how the components part of the

organization in terms of resources, processes, people and their skills

effectively deliver the corporate and business level strategic direction.

Porter (1987), on the other hand, simply defines strategy in two levels: corporate and

business (or competitive) unit. It also alluded to corporate strategy as been an

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

MBA Management Project 13 Lee Siak Kwee

essential attribute of a diversified company and defines it as one concerning “what

businesses the corporation should be in and how the corporate office should manage

the array of business units”.

This case analysis primarily targets the corporate level strategy of SingTel and this is

typically embodied in the context of the company’s vision i.e. what the company does

and what it is intended to become. It is not concerned with how the different

individual line of business should compete in order to succeed in their respective

market place but more with what businesses and markets that SingTel should aspire to

compete in. In an era of convergence in the IT, telecom and the internet/media,

between the fixed and mobile industry, and where services (e.g. “triple pay” of

broadband, mobile and pay-TV) are sold in a bundle, the concept of business level

strategy cannot be easily segregated. The organisation structure of SingTel into

geographical and customer facing units also serve to further reinforce this

phenomenon. Correspondingly, it is more relevant for the PFF and RBV analysis to

focus on those factors accruing to and affecting the corporate level strategy. Wheelen

& Hunger (2000) concisely sums up the definition of corporate strategy that this

report is focusing on:

(a) The firm’s overall orientation towards growth or stability

(b) The industries or markets in which the firm competes

(c) The manner in which management coordinates activities/resources and

cultivates capabilities among product lines and business units.

3.2 External Analysis- Porter’s Five Forces

The external analysis approach is based on the idea of “strategic positioning”, and it

has in Michael E. Porter its main protagonist. Industry structure and positioning

within the industry are the two broad thrusts on which Porter’s Five Forces (PFF)

model is based on and it is used as the main concept to analyse the outside forces

surrounding SingTel.

PFF postulates that the industry that a firm competes in and its strategic position

within that industry are the two key determinants of profitability. A firm has to

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

understand the nature of its competitive environment if it is to be successful in

formulating the correct strategies. If an organization fully appreciates the competitive

forces underpinning the industry, it will be in an informed position to counteract

against any threats and will also be able influence the forces with the appropriate

strategies. Like most technology industry, the telecom industry is extremely fluid and

this means that the nature and relative power of the forces will be constantly changing

over time. Hence, the analysis will concurrently look at what the environmental

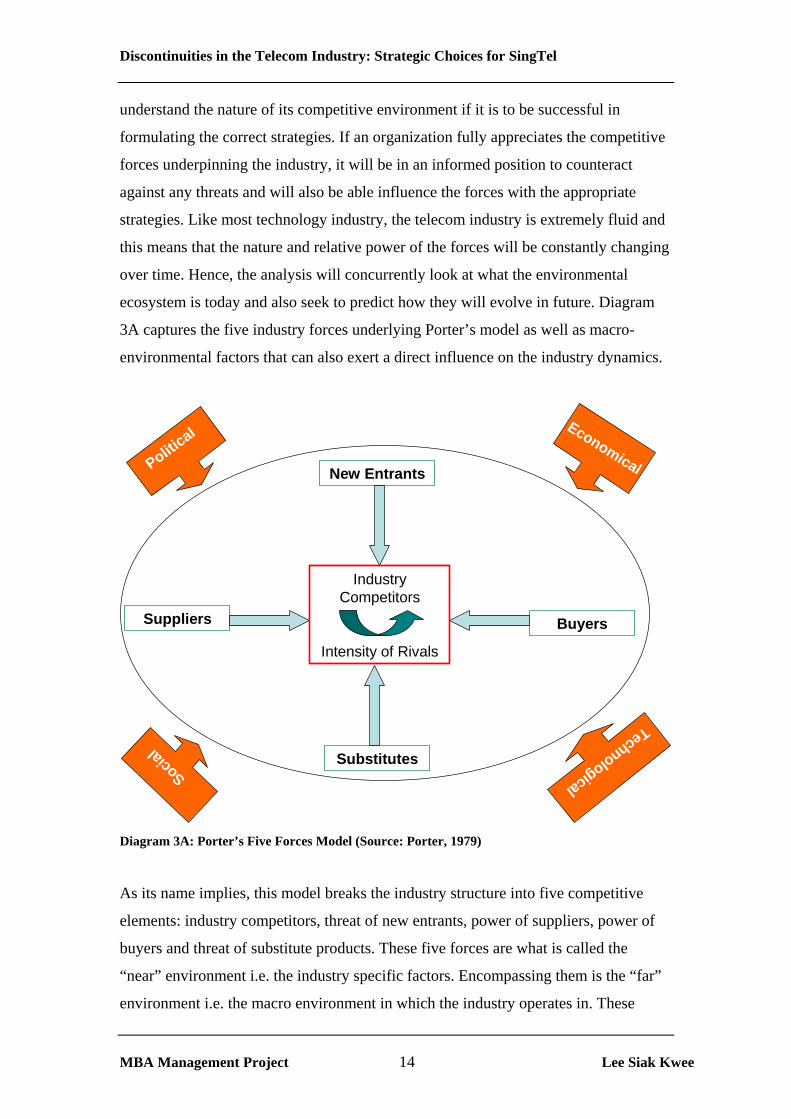

ecosystem is today and also seek to predict how they will evolve in future. Diagram

3A captures the five industry forces underlying Porter’s model as well as macro-

environmental factors that can also exert a direct influence on the industry dynamics.

New Entrants

Substitutes

BuyersSuppliers

Industry Competitors

Intensity of Rivals

Political Economical

Social

Technological

Diagram 3A: Porter’s Five Forces Model (Source: Porter, 1979)

As its name implies, this model breaks the industry structure into five competitive

elements: industry competitors, threat of new entrants, power of suppliers, power of

buyers and threat of substitute products. These five forces are what is called the

“near” environment i.e. the industry specific factors. Encompassing them is the “far”

environment i.e. the macro environment in which the industry operates in. These

MBA Management Project 14 Lee Siak Kwee

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

MBA Management Project 15 Lee Siak Kwee

macro-environmental issues comprising of political, economical, social and

technological factors will also be concurrently incorporated in the appraisal so that

their respective impact on the five forces can be properly accounted for.

The PFF is specifically chosen because the telecom industry is intricately intertwined

and profoundly impacted by forces in its external environment e.g. competition,

technology, regulatory policies etc. Having a sophisticated understanding of the

different competitive elements in the industry will allow a firm to devise the correct

strategy to counter, influence and/or change the current rules of the game. Porter

(1979) stated that “The strategist, wanting to position his company to cope best with

its industry environment or to influence that environment in the company’s favour,

must learn what makes the environment tick”. This is the core logic of adopting the

PFF model for this study i.e. it is an excellent framework as it elegantly addresses the

key competitive thrust and underlying causes encircling SingTel within the telecom

industry.

By eliciting the source of competitive forces at play in the telecom industry, the PFF

will not only identify the threats but more critically, the potential opportunities that

can be strategically exploited. However, implicit in Porter’s model is a generalisation

that firms competing within the industry have access to those resources that is

instrumental to the strategy that they pursue. Barney (1991), has argued that such

simplification “effectively eliminate firm resource heterogeneity and immobility as

possible source of competitive advantage”. Indeed, a strategy designed to capitalize

on the opportunities based on just a one-sided understanding of the industry dynamics

is unlikely to be successful if it cannot be executed due to a mismatch with the firm’s

resources and capabilities.

By introducing the value chain concept to facilitate identifying sources of firm’s

strengths and weaknesses, Porter (1985) seemed to also acknowledge that looking at

external factor alone is incomplete in formulating a strategy. Cool & Schendel (1988)

have also shown that significant performance differences exist among firms having

similar “positioning” within the same industry while others (Rumelt, 1991, Hansen &

Wernfelt, 1989) have shown that variance in firm performance between industries is

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

MBA Management Project 16 Lee Siak Kwee

substantially less than that within industries. This substantiates the contention that

corporate strategy based on industry positioning alone is inadequate and superior

performance must be the result of some other complementary factors.

An internal assessment of the firm is thus necessary to identify its valuable resources

as the ability of the firm to outperform its rivals depends on both the industry

attractiveness as well as its ability to establish competitive advantage (Grant, 1991).

By “valuable” resources, it means those resources that can generate economic rent for

SingTel within the context of the external environment i.e. a source of competitive

advantage. For this purpose, the RBV approach is examined in conjunction with the

Porterian framework so that both an outside-in (PFF) and inside-out (RBV)

perspective are captured, and the right “strategic fit” between its capabilities and the

environment can be matched.

3.3 Internal Analysis - Resource Based View

The RBV view of the firm considers that every organisation has a different collection

of physical and intangible assets, and suggests that these resources are the primary

determinants of the firm’s performance. No two companies are alike because they will

invariably be different in terms of experience, culture, management etc. Barney

(1991), Collis & Montgomery (1995) and Daft (1983) posited that these resources

enable the firm to conceive of and implement strategies that improve its efficiency

and effectiveness. These are the so-called resource portfolio and an in-depth

understanding of the possibilities presented by these resources are critical as they

form the basis on which a firm can formulate a strategy that makes the most effective

use of these resources. Such resources can be in physical form like financial resources,

intellectual rights or more intangible ones like brand name, production/technical

know-how, organisation culture etc. Technically, RBV is more of a theory than a

framework per se, although there are attempts like Grant (1991) to propose a more

formalised and structured model.

Barney (1991) and Collis & Montgomery (1995) suggested that in order to identify

the sources of sustained competitive advantage in a firm, the focus must be placed on

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

MBA Management Project 17 Lee Siak Kwee

resources that are heterogeneous and immobile. Specifically, Barney stated that

resources must pass the following market test of its value:

(a) Valuable (V)- enables a firm to employ a value-creating strategy, by

either improving efficiency or effectiveness

(b) Rare (R)– resource is limited and not easily acquired by competitors

(c) Imperfectly inimitable (I)– resource cannot be duplicated

(d) Non-substitutable (N)– no equivalent or similar resources that can

replace or act as replacement

Closer examination will reveal that conditions (a) and (b) generally produce

competitive advantage while conditions (c) and (d) can result in sustainability. In

short, these four VRIN attributes determine the degree of heterogeneity and

immobility of the resources, and consequently how useful they are in helping a firm

gain sustainable competitive advantage. The more a resource meets the VRIN

conditions, the more pivotal a role it plays in shaping the strategy of a firm. Naturally,

if all firms in the industry possess homogenous resources or is capable of gaining

access to such resources (i.e. resources are mobile), then it is hard to imagine how any

firm can possibly have a competitive advantage over the competitors in a sustained

manner since everyone is capable of eventually implementing the same strategies and

effectively nullifying each other.

In this study, RBV is used interchangeably to the concept of core competences

(Hamel & Pralahad, 1990). In general, resources are a more basic unit of analysis

while core competences is about how these resources are combined, mixed and

integrated or “the collective learning in the organization, especially how to

coordinate diverse production skills and integrate multiple streams of technologies.”

(Hamel & Pralahad, 1990).

It should be noted that the RBV of a firm is not centered around the existing resources

alone; it is equally concerned about the firm’s weaknesses especially those that can be

exploited by external threats. Consequently, the analysis will also identify the current

resource “gap” and what needs to be done to fill this gap.

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

MBA Management Project 18 Lee Siak Kwee

Combining both the PFF and RBV concepts will facilitate a more holistic approach to

the strategy formulation process and result in a hybrid resource and industry

positioning strategy. Simply put, PFF states where a firm wants to be, while RBV

provides the how of getting there.

3.4 Other Strategy Concepts

Apart from the choice of a “fit” concept as the basis of strategic management, the

other possible and popular concept is that of “stretch”. Notion of “Strategic Intent”

(Hamel & Pralahad, 1989) generally focuses on stretching the limited resources of the

organization by forcing it to be more innovative in order to compete against a much

bigger competitor. Strategic Intent identifies the firm’s ideal state and is associated

with a mind-set that the firm seeks to imbue in the organization. Although this notion

of strategy as “stretch” gives both the internal and external view of the firm, it

essentially creates “an extreme misfit between resources and ambitions” rather than

focusing on “the degree of fit between existing resources and current opportunities”

(Hamal & Pralahad, 1989).

It is felt that such an approach to strategy development is more relevant for nascent

firms with limited resources and targeting to beat a much bigger incumbent. In fact, in

Hamel & Pralahad (1989), examples of Komatsu and Canon were used as case studies

to demonstrate how fledgling companies outfox their more established competitor by

having a clear strategic intent. Hamel & Pralahad indeed also stated that “to achieve a

strategic intent, a company must usually take on a larger, better financed competitor”.

Clearly, being an incumbent and market leader, SingTel does not fit into this category

especially in the context of Singapore and even amongst its regional

telecommunication peers. It is extremely well endowed with resources, as subsequent

sections will reveal, and its main challenge is in deciding how to deploy these

resources rather than having to stretch them.

In summary, “stretch” concepts like Strategic Intent are less appropriate in this

context and Porter’s Five Forces and RBV are used as the key methodologies to

analyse the strategic choices for SingTel.

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

SECTION FOUR: STRATEGIC ANALYSIS OF THE INDUSTRY

ENVIRONMENT

4.1 Objectives

The stability and dynamism of the environment are critical considerations in the

strategy of any firm. The more volatile these parameters are, the greater the

uncertainty and the more complex the analysis becomes. The telecommunication

industry is one that is heavily influenced by its external environment, both industry-

specific as well as those pertaining to the broader macro environment. Not least of

which are for example, the regulatory regime in which it operates in, the economic

prospect, disruptive technologies etc.

The key objectives of this section are to size up the external environment for the

purpose of gaining a strategic understanding of the key threats and opportunities

facing SingTel. To this end, Porter’s Five Forces (PFF) (1979) model is used as the

broad framework on which the main analysis is developed. The output will provide a

clear perspective of the industry dynamics and collective forces that SingTel is up

against and what it can do to re-orientate itself for the future. Specifically, it looks at

the prevailing forces at play in the industry today and also attempts to extrapolate the

developments that can shape the industry in future. The diagram below outlines the

key steps in this analysis:

Assess nature & dynamics of the environment

Understand main competitive

forces & position

Identify key opportunities &

threats

4.2 Porter’s Five Forces Analysis

4.2.1 Industry Competitors

This section drills down into the rivalry that exists among the competitors in the

telecom industry. It looks at the various determinants that shape the competitive

forces and hence factors like strength/diversity of competitors, attractiveness of

market, state of market maturity, exit barriers etc will be evaluated.

MBA Management Project 19 Lee Siak Kwee

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

MBA Management Project 20 Lee Siak Kwee

4.2.1.1 Strength of Competitors

In Singapore

(a) Market Position

Although the Singapore telecommunications market has been fully liberalized since

2000 (IDA, 2000), most of the new entrants are typically niche players focusing on

targeted segments like IDD, international leased lines etc. Indeed, although a total of

29 facilities based operators (FBOs) and 535 service based operators (SBOs) were

licensed to provide telecommunications services, the International

Telecommunications Union (ITU, 2001) reported that “Although many new operators

have been licensed following the introduction of full competition, Singapore’s

telecommunications market remains dominated by SingTel, StarHub, M1 and

SCV,…...” In fact, StarHub acquired SCV (the only pay-TV operator in Singapore at

that time) in 2002 (StarHub, 2002), effectively reducing the telecom market to three

major players: SingTel, StarHub and M1.

It is only in the two key business of mobile and fixed broadband that competition can

be classified as intense. Even then, SingTel only faces two competitors in the mobile

market viz. StarHub and M1. In the fixed broadband market, the heavy capital

investment itself is a deterrent which limits the market to basically a two horse race

between SingTel and StarHub.

StarHub and M1 are both backed by experienced global telecom operators as well as

strong local partners. This has invariably contributed to their formidable presence and

success in the market. StarHub’s major local shareholders are Singapore Technologies

Telemedia (49.36% share) which is a government-owned company with interest in

wide-ranging infocomm businesses and Mediacorp (7.6%), the monopoly TV/radio

broadcaster. Its foreign partners are NTT Communications of Japan and British

Telecom (BT), although BT has since sold off its entire stake in 2004 when StarHub

was publicly listed.

M1 also has a very strong local partner in Keppel Telecom and SPH, both well

established government-related conglomerates and its foreign partner is Sunshare, a

subsidiary of Telekom Malaysia.

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

Chart 4A & B below show the market share of SingTel versus the competitors in

mobile and fixed broadband respectively:

0%5%

10%15%20%25%30%35%40%45%

2004 2005 2006 2007

End Year

Mar

ket S

hare

(Mob

ile)

SingTel StarHubM1

Chart 4A: Mobile Market Share in Singapore (Source: M1, StarHub and SingTel

Annual Reports FY2004-2007)

0%

10%

20%

30%

40%

50%

60%

2004 2005 2006 2007

End Year

Mar

ket S

hare

(Fix

ed B

raod

band

)

SingTel StarHub

Chart 4B: Broadband Market Share in Singapore (Source: Infocomm Development

Authority of Singapore (IDA) Web Site: www.ida.gov.sg)

SingTel has over the past four years managed to maintain its average market share of

40% and 55% for mobile and fixed broadband respectively. The key takeaway from

MBA Management Project 21 Lee Siak Kwee

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

these charts is that SingTel is still the clear market leader. M1 is gradually losing

ground and the main reason is that being a pure mobile-only player, it has severely

limited its ability to compete with SingTel and StarHub both of whom are able to

bundle their mobile offerings with their fixed broadband as well as their pay-TV

services.

Market share from a revenue perspective also establishes SingTel as the market leader,

as depicted in Chart 4C. Taking mobile revenue as an indicator, SingTel’s revenue

share of the mobile market is in fact higher than its subscriber market share (44%

versus 41%), implying that it has higher ARPU (average revenue per user) and hence

a more valuable customer base than StarHub and especially M1. This can be

attributed to the fact that it still retains a reputation of being a trusted and high quality

company. As such, many valuable corporate businesses are prepared to pay a

premium to stay with SingTel.

0%5%

10%15%20%25%30%35%40%45%50%

2004 2005 2006 2007

End Financial Year

Mar

ket S

hare

(Mob

ile R

even

ue)

SingTelStarhubM1

Chart 4C: Mobile Revenue Share (Source: CIMB Telecommunication Sector Analyst

Report, 26 Nov 2007)

(b) Financials

Financially, SingTel is the largest company by market capitalization on the Singapore

Exchange. The following analyses the relative strength of the three telcos over the

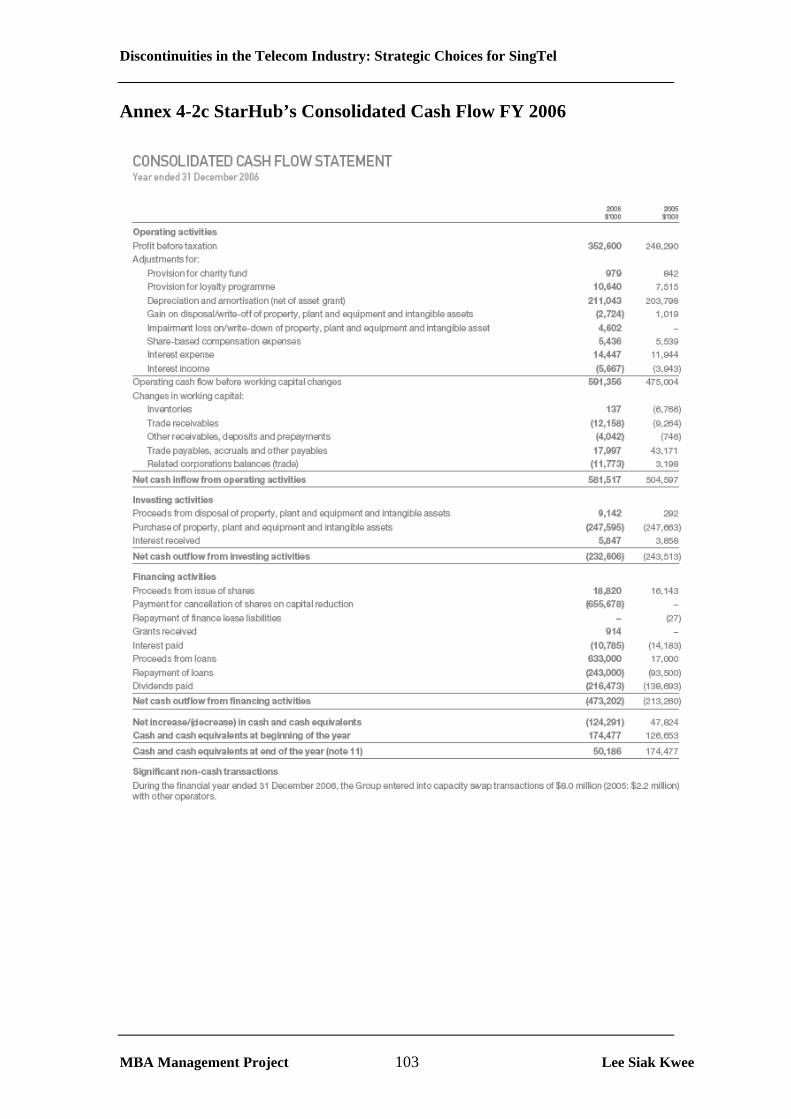

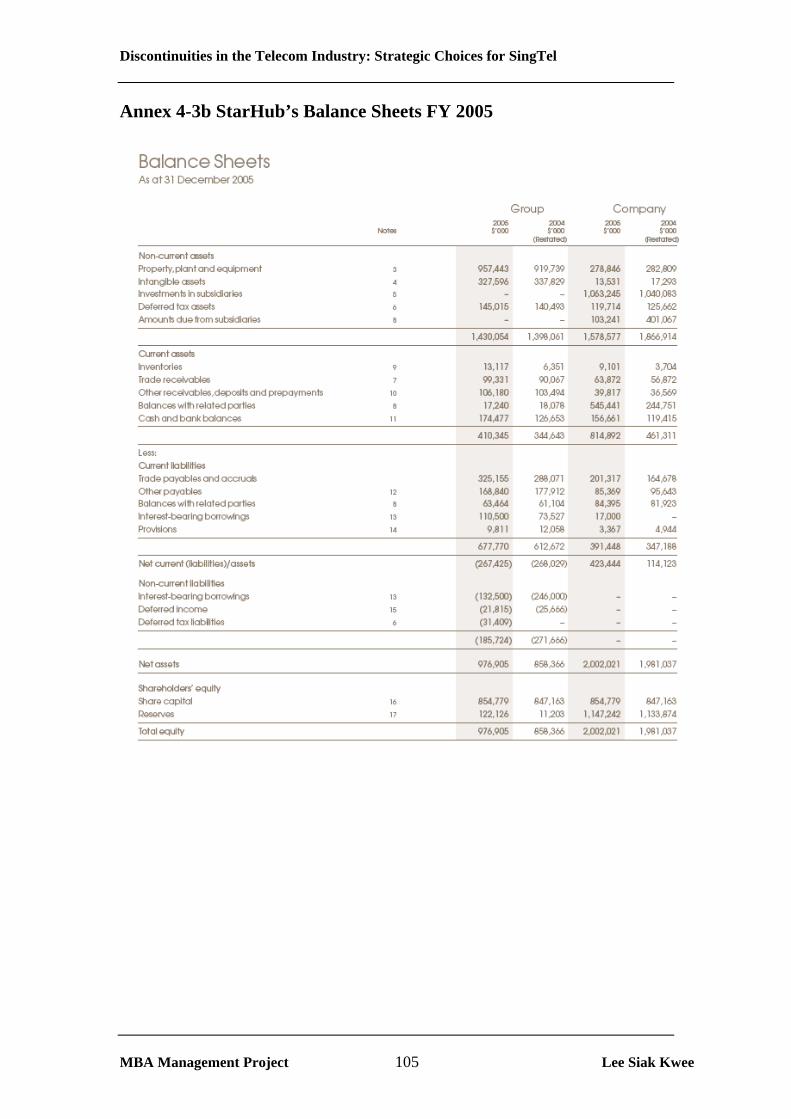

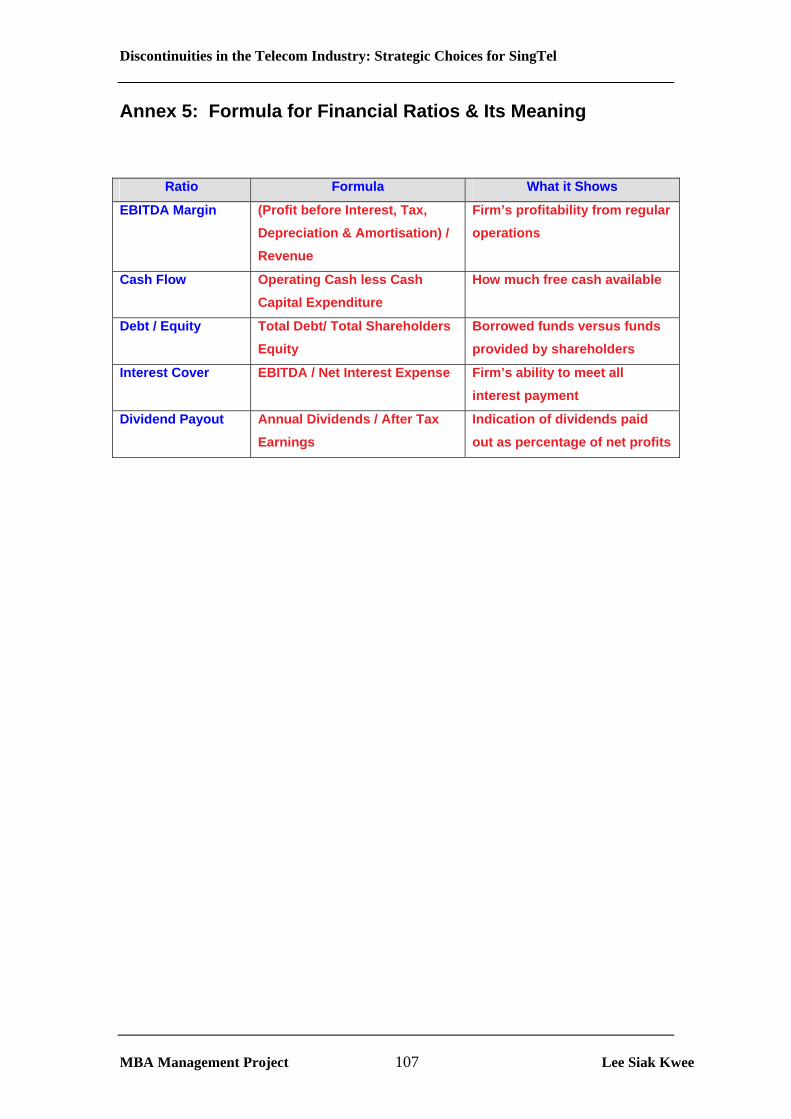

past 3 years with respect to some key financial ratios. The detailed financial

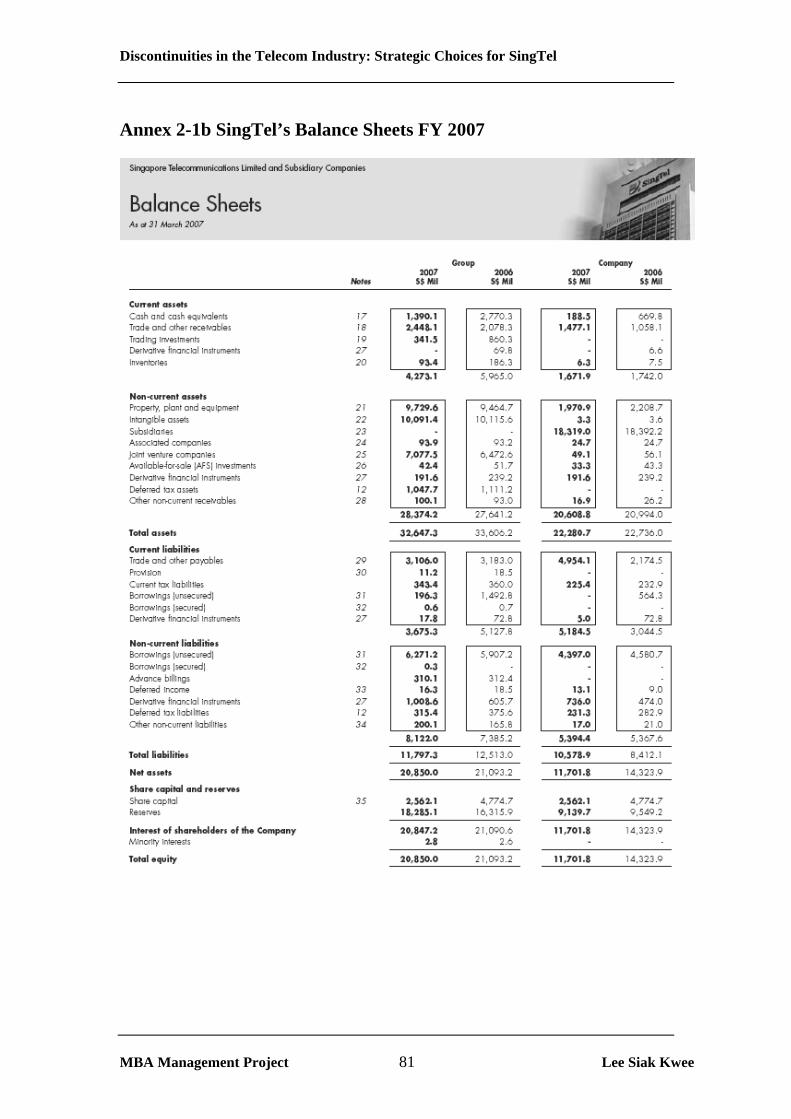

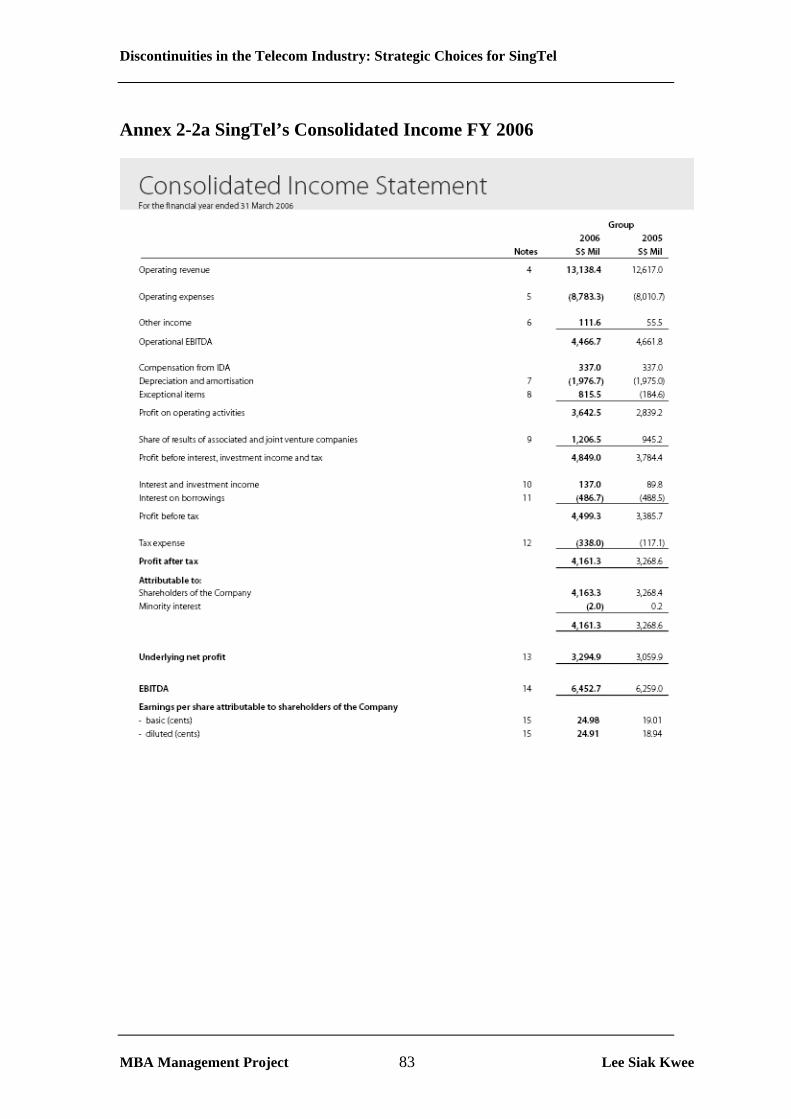

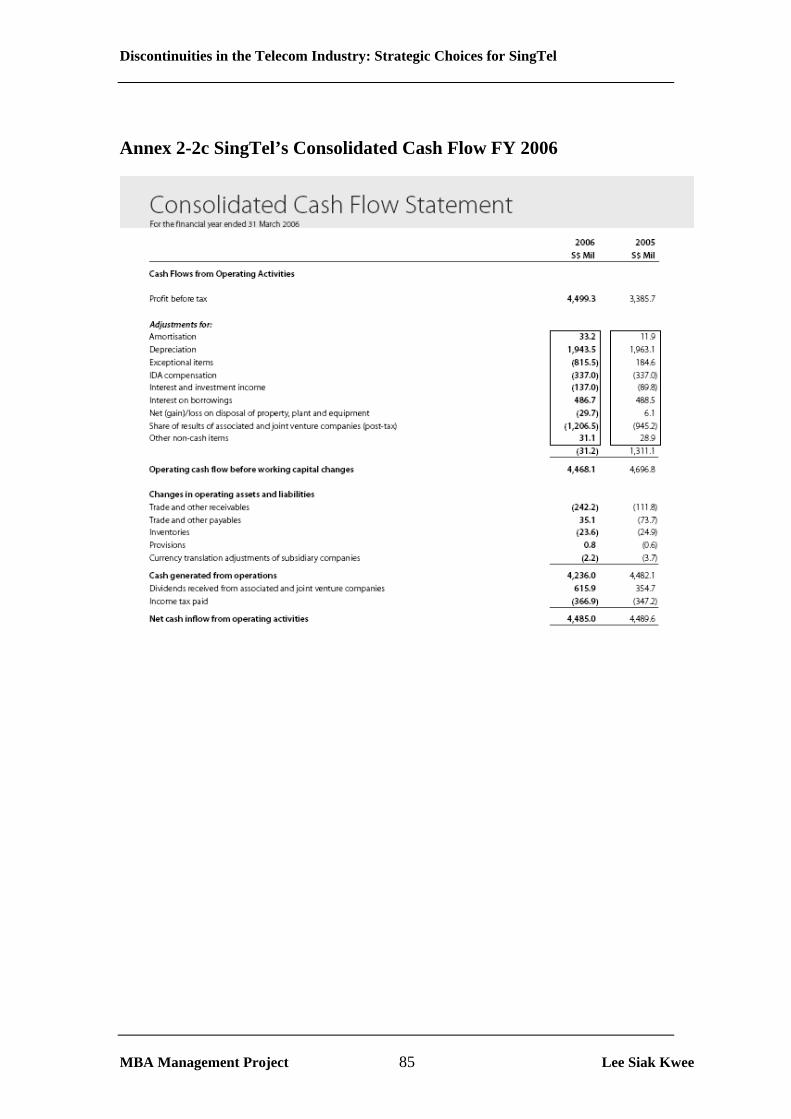

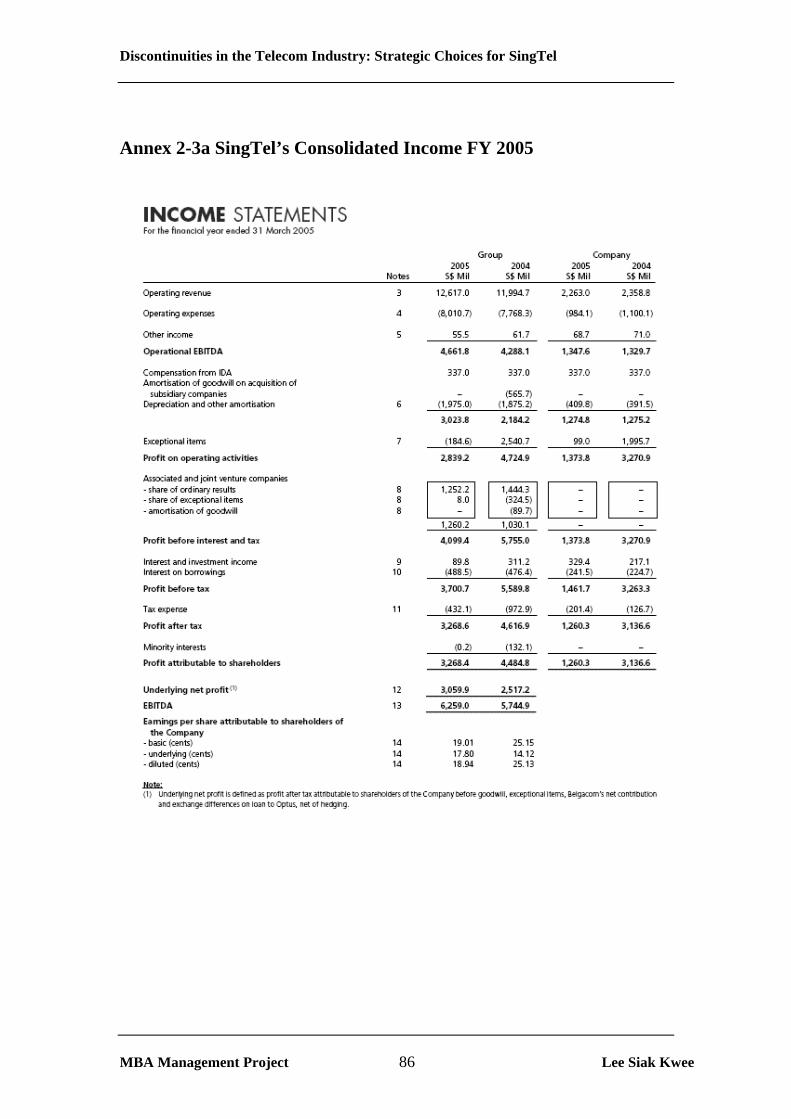

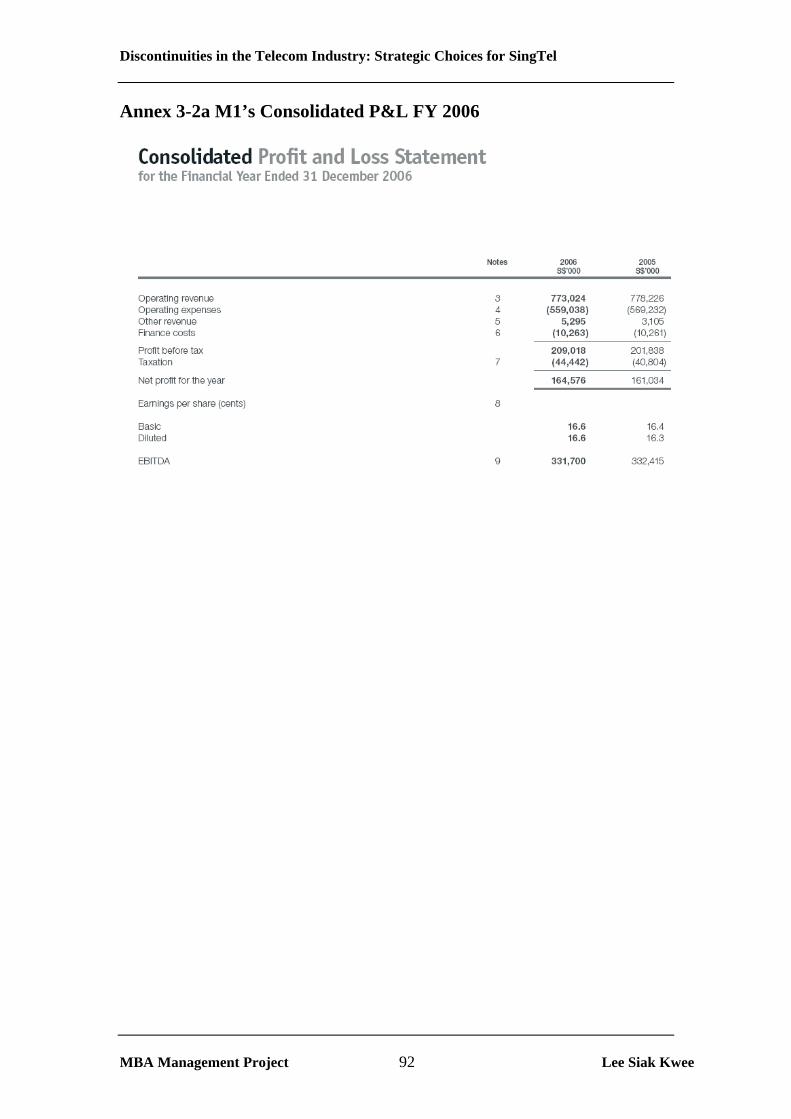

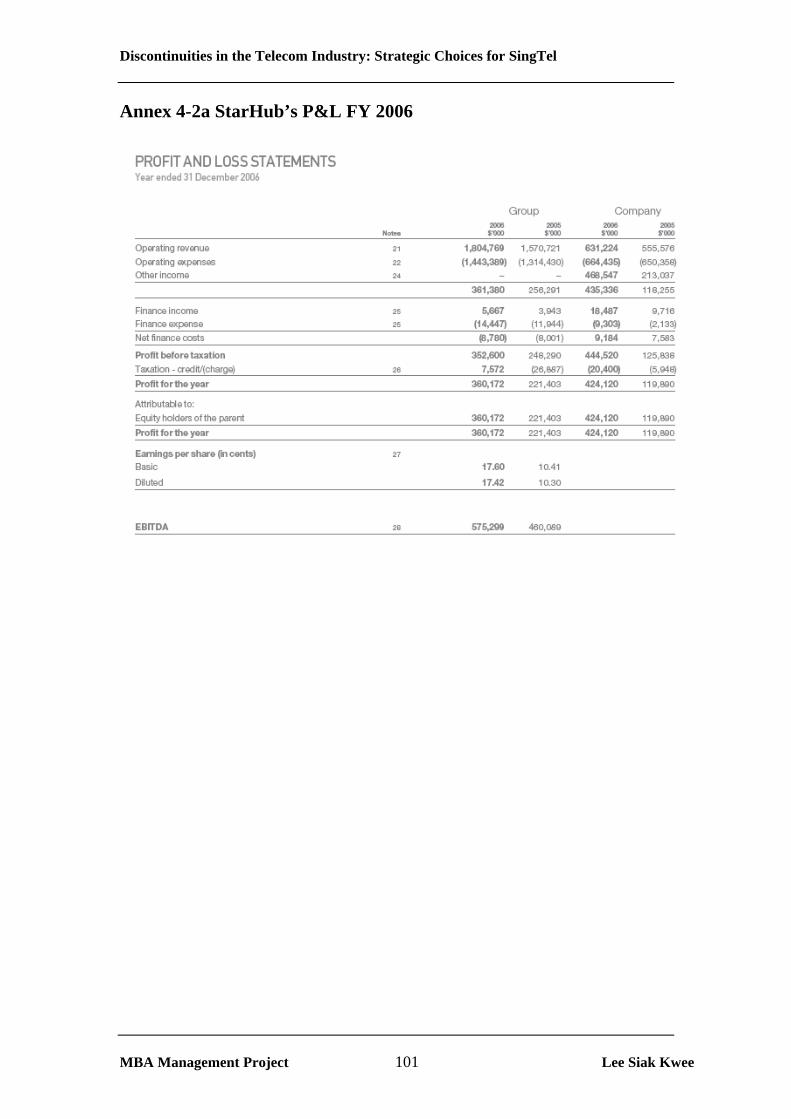

statements of each company are provided in Annex 2 to 4 while the definition of each

of the ratios is provided in Annex 5. It should be noted that the financial year of

MBA Management Project 22 Lee Siak Kwee

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

SingTel is from 01 Apr to end March while M1 and StarHub follows the calendar

year.

-2.0%0.0%2.0%4.0%6.0%8.0%

10.0%12.0%14.0%16.0%18.0%

2005 2006 2007

Year

Rev

enue

Gro

wth

SingTelStarHubM1

Chart 4D: Revenue growth for past 3 years for SingTel, M1 and StarHub. (Source:

SingTel, M1 and StarHub)

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

2005 2006 2007

Year

EBI

TDA

Gro

wth

SingTelStarHubM1

Chart 4E: EBITDA growth for past 3 years for SingTel, M1 and StarHub

(Source: SingTel, M1 and StarHub)

EBITDA & REVENUE Growth: Chart 4D & E compares the Revenue and EBIDTA

growth of the three telcos for the past three financial years. StarHub is by far the best

performer with an enviable double digit growth in both revenue and EBITDA. This is

in sharp contrast to the flat top line growth and slight erosion of EBITDA for both M1

and SingTel. This shows that not only is StarHub growing and snatching revenue

MBA Management Project 23 Lee Siak Kwee

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

market share at the expense of both operators, it is also doing this at a much lower

cost as shown in its relatively higher EBITDA.

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

2005 2006 2007

Year End

EBIT

DA

Mar

gin

SingTelStarHubM1

Chart 4F: EBITDA Margin for past 3 years for SingTel, M1 and StarHub

(Source: SingTel, M1 and StarHub)

EBITDA Margin: Although SingTel still shows the highest absolute EBITDA or

operating margin as illustrated in Chart 4F, a worrying sign is that it is trending

downwards, implying that its expenses is growing at a faster rate than its revenue.

Comparatively, StarHub has been impressively improving on its margin and still

growing its top and bottom line at the same time. Its margin is lower than M1

because it is dragged down by its pay-TV business which is generally a high capital

investment and low margin business.

MBA Management Project 24 Lee Siak Kwee

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

0200400600800

1,0001,2001,4001,6001,8002,000

SingTel StarHub M1

Operator

Free

Cas

h Fl

ow in

S$

mils

200520062007

Chart 4G: Free Cash Flow for the past 3 years for SingTel, M1 and StarHub (Source:

SingTel, M1 and StarHub)

Free Cash Flow/Dividend : Looking at Chart 4G, SingTel’s free cash flow stands

heads and shoulders above the rest and this cash holding gives it tremendous

flexibility to take advantage of any investment opportunity both in Singapore and

overseas. On the other hand, M1 and StarHub have no regional ambition and have

consistently chosen to return surplus cash to its shareholders instead. Table 4H below

shows the declared dividend policy of the three telcos:

SingTel Pay 50% of underlying net profit after tax as ordinary dividends. (SingTel

15th AGM, 2007)

StarHub 18cts per share or about 90% of net profit after tax (StarHub, 2008)

M1 For FY2007, aim to make a total cash distribution to shareholders

equivalent to at least 80% of full-year net profit after tax. (M1, 2008)

Table 4H: Dividend Policies of SingTel, StarHub & M1 (Source: SingTel, StarHub &

M1)

This high dividend payout ratio of M1 and StarHub is also reflected in their respective

dividend yield and in absolute terms, both operators actually pay out more dividends

per share than SingTel despite their relatively smaller size. But the implication is that

they are considered as dividend yield stocks in the market and their share price may

take a direct hit, at least in the short term, if they decide to divert some of these cash

MBA Management Project 25 Lee Siak Kwee

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

MBA Management Project 26 Lee Siak Kwee

to a new venture. SingTel, on the other hand, has much more scope to deploy its cash

on hand.

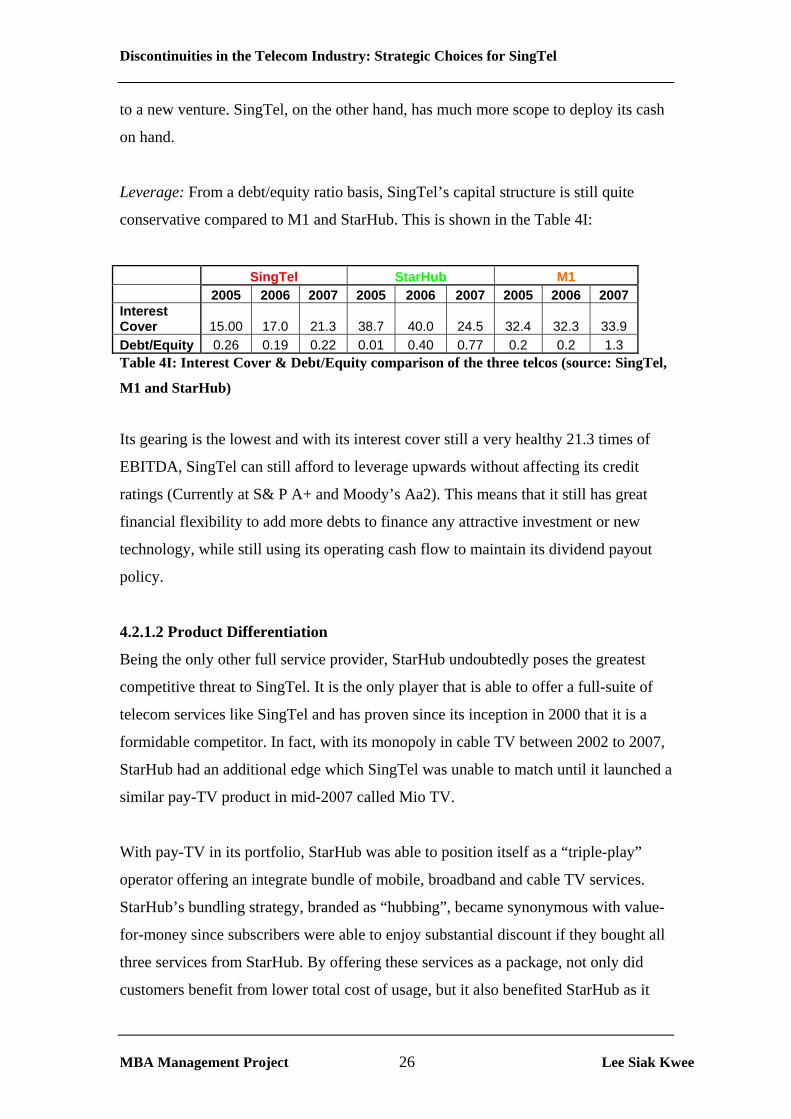

Leverage: From a debt/equity ratio basis, SingTel’s capital structure is still quite

conservative compared to M1 and StarHub. This is shown in the Table 4I:

SingTel StarHub M1 2005 2006 2007 2005 2006 2007 2005 2006 2007 Interest Cover 15.00 17.0 21.3 38.7 40.0 24.5 32.4 32.3 33.9 Debt/Equity 0.26 0.19 0.22 0.01 0.40 0.77 0.2 0.2 1.3 Table 4I: Interest Cover & Debt/Equity comparison of the three telcos (source: SingTel,

M1 and StarHub)

Its gearing is the lowest and with its interest cover still a very healthy 21.3 times of

EBITDA, SingTel can still afford to leverage upwards without affecting its credit

ratings (Currently at S& P A+ and Moody’s Aa2). This means that it still has great

financial flexibility to add more debts to finance any attractive investment or new

technology, while still using its operating cash flow to maintain its dividend payout

policy.

4.2.1.2 Product Differentiation

Being the only other full service provider, StarHub undoubtedly poses the greatest

competitive threat to SingTel. It is the only player that is able to offer a full-suite of

telecom services like SingTel and has proven since its inception in 2000 that it is a

formidable competitor. In fact, with its monopoly in cable TV between 2002 to 2007,

StarHub had an additional edge which SingTel was unable to match until it launched a

similar pay-TV product in mid-2007 called Mio TV.

With pay-TV in its portfolio, StarHub was able to position itself as a “triple-play”

operator offering an integrate bundle of mobile, broadband and cable TV services.

StarHub’s bundling strategy, branded as “hubbing”, became synonymous with value-

for-money since subscribers were able to enjoy substantial discount if they bought all

three services from StarHub. By offering these services as a package, not only did

customers benefit from lower total cost of usage, but it also benefited StarHub as it

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

MBA Management Project 27 Lee Siak Kwee

saved on marketing/distributing the products individually. Technically, StarHub’s

newer cable infrastructure is also more superior to SingTel’s legacy copper lines; it is

already able to offer 100Mbps download speed compared to SingTel’s 10Mbps.

This wildly successful strategy propelled StarHub from zero market share at its

inception in 2000 to almost 33% today (versus SingTel’s 40%). In the process, it also

overtook M1, even though M1 had entered the market 3 years earlier in 1997. Without

an equivalent pay-TV offering, SingTel was not able to counter this key

differentiation until its Mio TV premiered in 2007. Even then, being first in the pay

TV market has allowed StarHub to lock-in key TV programs on long term contracts.

Staple like the English Premier League (EPL) soccer telecast is a “must-have” for the

majority of viewers in Singapore and it was reported that StarHub paid S$250 mil in

2007 to acquire the rights to broadcast EPL for the next 3 years (Siew, 2007). This

was 4 times higher than what it paid for the existing rights and it highlights both the

intensity of the rivalry as well as how critical such popular content is to the pay-TV

business.

Traditionally, SingTel has been heavily dependent on voice services, especially IDD

as its main revenue stream. But technology like Voice over IP has all but destroyed

that lucrative business model and IDD has been relegated to commodity status today.

Similarly, mobile services risk following down this slippery path if it still continues to

be driven by voice traffic. Even data traffic generated by the strong take up of

broadband internet service is also being commoditised with operators offering fixed

subscription for unlimited access. This state of affairs has all but reduced operators

like SingTel into “bit-pipe” carriers.

4.2.1.3 Industry Attractiveness

The Table 4J and 4K below show the latest IDA statistics on the mobile and

broadband services market in Singapore respectively:

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

2004200520062007

End Year

Num

ber o

f Mob

ile

Sub

scri

bers

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

140.0%

Pene

tratio

n R

ate

MobileMobile Penetration

Table 4J: Number of Mobile Subscribers and Market Penetration in Singapore (Source:

IDA Statistics on Telecom Services 2004-2007 (www.ida.gov.sg))

-100,000200,000300,000400,000500,000600,000700,000800,000900,000

1,000,000

2004 2005 2006 2007

End Year

Num

ber

of R

esid

entia

l Br

oadb

and

Con

nect

ions

0.0%10.0%20.0%30.0%40.0%50.0%60.0%70.0%80.0%90.0%

Hous

ehol

d P

enet

raio

n R

ate

Broadband

BroadbandHouseholdPenetration

Table 4K: Number of Residential Broadband Connections and Household Penetration

Rate in Singapore (Source: IDA Statistics of Telecom Services 2004 -2007

(ww.ida.gov.sg))

With mobile penetration already exceeding more than 100% of population and

broadband connecting over 77% of the households, the telecom market in Singapore

can be considered a highly mature one. Although the market still grew from 2006 to

2007 with the mobile and broadband penetration rate by about 20 and 10 percentage

points respectively, the revenue growth rate tells a slightly different story.

MBA Management Project 28 Lee Siak Kwee

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

MBA Management Project 29 Lee Siak Kwee

In financial year 2007, the best performer StarHub achieved only 11.6% growth while

the other two were mostly flat. Even though the absolute number of subscribers has

grown, revenue growth has not followed proportionately, signifying that the new

subscribers are of much lower value. This is a tell-tale sign that the market is reaching

the lower tiers where the customers are usually extremely price sensitive. Such

developments entail that going forward, the emphasis for SingTel will be in

maintaining efficiency and a low cost structure in order to protect the margins.

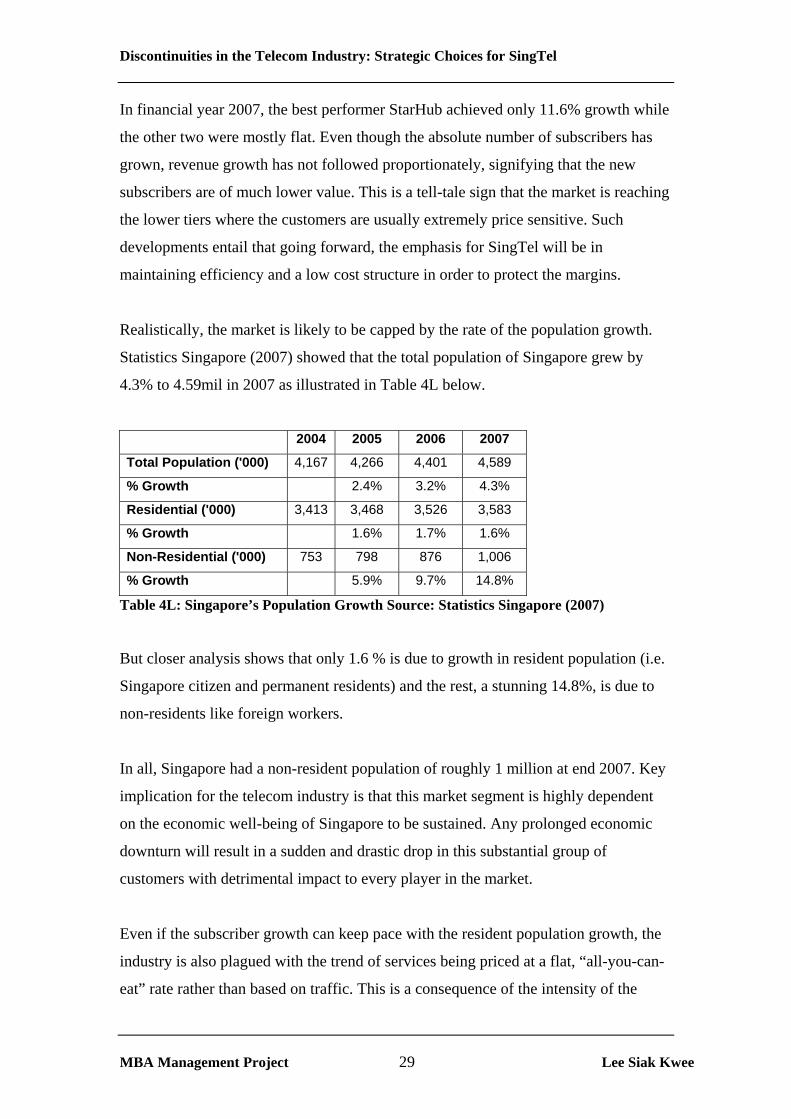

Realistically, the market is likely to be capped by the rate of the population growth.

Statistics Singapore (2007) showed that the total population of Singapore grew by

4.3% to 4.59mil in 2007 as illustrated in Table 4L below.

2004 2005 2006 2007

Total Population ('000) 4,167 4,266 4,401 4,589

% Growth 2.4% 3.2% 4.3%

Residential ('000) 3,413 3,468 3,526 3,583

% Growth 1.6% 1.7% 1.6%

Non-Residential ('000) 753 798 876 1,006

% Growth 5.9% 9.7% 14.8%

Table 4L: Singapore’s Population Growth Source: Statistics Singapore (2007)

But closer analysis shows that only 1.6 % is due to growth in resident population (i.e.

Singapore citizen and permanent residents) and the rest, a stunning 14.8%, is due to

non-residents like foreign workers.

In all, Singapore had a non-resident population of roughly 1 million at end 2007. Key

implication for the telecom industry is that this market segment is highly dependent

on the economic well-being of Singapore to be sustained. Any prolonged economic

downturn will result in a sudden and drastic drop in this substantial group of

customers with detrimental impact to every player in the market.

Even if the subscriber growth can keep pace with the resident population growth, the

industry is also plagued with the trend of services being priced at a flat, “all-you-can-

eat” rate rather than based on traffic. This is a consequence of the intensity of the

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

MBA Management Project 30 Lee Siak Kwee

competition in a mature market and a further testament that traditional telco services

like broadband and mobile are already behaving like commodities.

With flat rate pricing, there is very little upside for the telcos but instead, more

resources must be put in place to bear the additional cost of carrying the traffic e.g.

through network expansion. Video-type services which are bandwidth guzzler (like

the popular YouTube), has generated tremendous amount of internet traffic, but

unfortunately for the telcos, it has not translated into a new revenue stream.

Despite the apparent gloomy picture that has been painted for the telecom industry,

there is yet some silver lining. The ubiquitous accessibility to broadband mobile

coupled with user-friendly multimedia handheld devices is a potential catalyst to

make the internet go “mobile”. iPhone for example, has been claimed by Renee

Obermann (CEO of Deutsche Telekom) to drive mobile internet data usage by 30

times more than other phones (Unstrung, 2008). This “anywhere, anytime”

connectivity paradigm will be the next driver of traffic for the mobile operators. Of

course, traffic alone will not make the industry any more attractive than it is today but

such pervasive mobile usage will facilitate operators to offer more on-line (and

chargeable) services and more dramatically, opens up the possibility for operators to

emulate the advertisement-funded business model of the internet. This is a distinct

possibility as operators can leverage on their knowledge of e.g. the location of the

subscribers to sell such information to advertisers. With user generated content, social

networking, blogging and other similar Web 2.0 type services becoming the rage,

such “contextual” information will become extremely relevant.

In a nutshell, the Singapore telecom industry has reached a maturity stage in the life

cycle of the market and market share can either be gained by stealing current higher

value customers from other competitors or cutting prices to entice a new segment of

price sensitive subscribers. Even though growth rate has tapered off and competition

is rife, it is unlikely to decline as the telecom services are used on a recurring basis

and subscribers are usually charged monthly subscription or usage fee. In addition, the

trend towards mobile internet presents an attractive proposition that can be exploited.

The telecom industry is without doubt still an attractive industry that provides strong

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

MBA Management Project 31 Lee Siak Kwee

recurring cash flow, relatively healthy profit margins, and potential for an internet-

based business model in future.

4.2.1.4 Capacity/Fixed Cost

High fixed cost is a natural trait of the telecom industry. Infrastructure cost typically

run into 10s and even 100s of millions of dollars even for a small country like

Singapore. Although the Singapore market is fairly mature, investment is still

constantly needed to upgrade the network e.g. to support the latest mobile technology

like 3G, upgrade from ADSL to ADSL+ to support higher broadband access, etc.

Each of the three mobile operators paid S$100mil for their respective 3G license, and

this was just for the rights to use the frequency. It excludes the cost of the

infrastructure as well any operating cost necessary to get the network up and running.

Such is the magnitude of investment required in the telecom industry. Obviously, with

such high upfront capital expenditure, having the minimum economy of scale is

critical to at least cover the running cost and hopefully, get a decent return on the

initial investment in the long run. This is a reason why it is common to see operators

subsidizing handsets, modems etc, and locking in customers with long term contract

in order to ramp up to the desired subscriber scale. Although the incumbent operators

are all saddled with high operating and network upgrade cost, they do not face any

more such pressure to gain customers quickly since they have all attained a sufficient

size to be highly profitable while controlling their cost/margins. However, the danger

is that this does not preclude a new operator coming into the market e.g. with a new

disruptive and cheaper technology, and shake the market with a low cost strategy to

obtain the turnover required.

4.2.1.5 Acquisition

A shakeout in the telecom industry in Singapore is an unlikely scenario with all the

three incumbents having sufficiently large market share to remain sufficiently

profitable. Mergers and acquisition activities between the big three is also not a

probable event as first, the regulator will not be keen to see a duopoly develop.

Moreover, the current telecommunications code has very stringent guidelines

regarding any consolidation that eliminates direct competitors resulting in what IDA

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

MBA Management Project 32 Lee Siak Kwee

would call “significant market power”. Secondly, there is also very little incentive for

the incumbents to merge or acquire each other since the market is already flattening

out and there is little to gain strategically from such a move.

Foreign acquisition, however, is a more probable scenario. Foreign players taking a

strategic stake have already happened with M1, with the investment by Telekom

Malaysia’s subsidiary Sunshare in 2005. Such an acquisition could result in new

players with “very different personalities” (Porter, 1979) entering and attempting to

re-write the rules of the market. Although so far, Sunshare has proven to be a

relatively quiet partner, the fact that there is now no regulatory restriction on foreign

ownership means that in future, SingTel may be faced with fighting a truly global

operator in its own backyards. Likewise, new technologies may create the window of

opportunity for foreign players to acquire a stake in one of the operators so as to gain

immediate access to the existing subscriber base, distribution channels and brand

name.

4.2.1.6 Regionally

SingTel early forays into the regional market were helped by two key developments:

the Asian financial crisis in 1997 and the dot.com bust of 2001. In the fallout of the

1997 crisis, cash-rich SingTel took advantage of the opportunity to buy out distressed

assets and AIS in Thailand was one of these companies that SingTel invested to help

pay off its massive US$ denominated debts.

During the short lived euphoria of the dot.com era, many European operators bought

into the madness and bid an estimated US$100 bil for new 3rd generation (3G) mobile

licenses throughout Western Europe. When the bubble burst in 2001, all these

operators were left holding on to massive debts and on business models that can no

longer justify the astronomical price tag. Consequently, many operators had to off-

load their stake in their ventures around the world in order to pay off their debts.

SingTel was on hand to capitalize. In 2001, it paid US$602 mil for a 22.3% stake in

Telkomsel in Indonesia from KPN (the Dutch mobile operator) (Clark, 2001) and in

the same year, it bought wholesale from Cable & Wireless a 53% stake in Optus in

Australia.

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

MBA Management Project 33 Lee Siak Kwee

7 years later however, many of these global telcos have got rid of these excesses and

are making their forays into the Asia Pacific region again. These competitors that

SingTel face in the regional arena are telcos with similar profile: cash-rich former

government monopoly faced with a saturated home market. These are the likes of

Vodafone, NTT Docomo of Japan, etc. However, in terms of size, these competitors

dwarf SingTel considerably. Vodafone for example, has a market capitalization of

£99 bil (as at end Dec 07) and a subscriber base in excess of 252 mil spread over a

global footprint covering USA, Europe, Middle East, Africa and Asia Pacific

(Vodafone, 2008).

Naturally, SingTel faces an up hill task competing against these global giants

especially if they are prepared to pay over the top premium to buy stakes in other

companies. Group CEO of SingTel, Ms Chua Sock Koong, admitted as much in reply

to question in a recent press interview: “More overseas companies are targeting Asia

for acquisitions…….for SingTel, ``the challenge is not lack of capital…” (Bloomberg,

2008).

Notwithstanding the tough competition that SingTel faces for new acquisition, its

focus on the Asia Pacific region and on mobile business in particular positions it in a

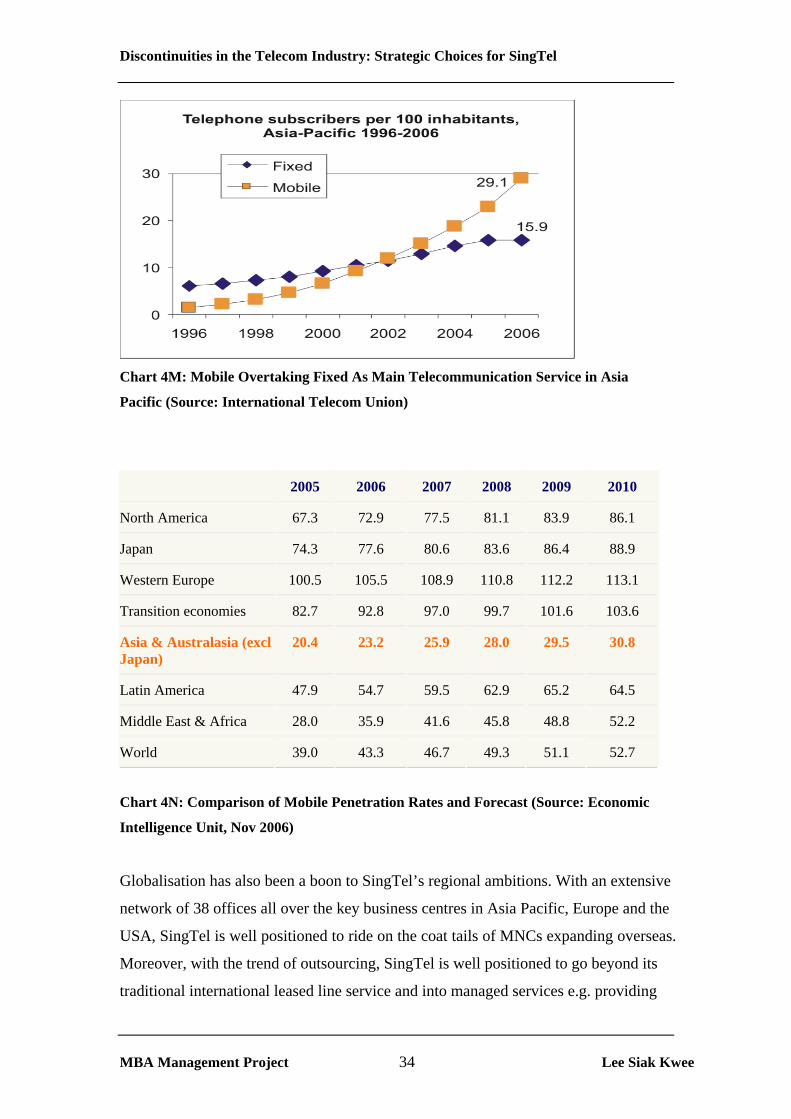

market that still has enormous potential for growth. Chart 4M illustrates how mobile

has overtaken fixed line as a main form of telecommunication in the Asia Pacific

region and this is not surprising considering that in big countries like China and India,

going wireless is a much faster and cheaper route. The attractiveness of the Asia

Pacific market is underscored by the relatively low mobile penetration rates compared

to developed regions like America and Europe in Chart 4N. This augurs well for

every player in this highly attractive industry in Asia Pacific which is also SingTel’s

main battle ground.

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

Chart 4M: Mobile Overtaking Fixed As Main Telecommunication Service in Asia

Pacific (Source: International Telecom Union)

2005 2006 2007 2008 2009 2010

North America 67.3 72.9 77.5 81.1 83.9 86.1

Japan 74.3 77.6 80.6 83.6 86.4 88.9

Western Europe 100.5 105.5 108.9 110.8 112.2 113.1

Transition economies 82.7 92.8 97.0 99.7 101.6 103.6

Asia & Australasia (excl Japan)

20.4 23.2 25.9 28.0 29.5 30.8

Latin America 47.9 54.7 59.5 62.9 65.2 64.5

Middle East & Africa 28.0 35.9 41.6 45.8 48.8 52.2

World 39.0 43.3 46.7 49.3 51.1 52.7

Chart 4N: Comparison of Mobile Penetration Rates and Forecast (Source: Economic

Intelligence Unit, Nov 2006)

Globalisation has also been a boon to SingTel’s regional ambitions. With an extensive

network of 38 offices all over the key business centres in Asia Pacific, Europe and the

USA, SingTel is well positioned to ride on the coat tails of MNCs expanding overseas.

Moreover, with the trend of outsourcing, SingTel is well positioned to go beyond its

traditional international leased line service and into managed services e.g. providing

MBA Management Project 34 Lee Siak Kwee

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

end to end service from hosting of servers, to network security and round the clock

maintenance. But of course, the global market place is also the playground of the likes

of big boys like AT&T, Deutsche Telekom and Verizon, and hence competition will

be extremely intense.

Summary of Industry Rivalry

Key Opportunities:

• Ubiquitous access facilitated by fixed and mobile broadband, together with

demand for internet based services creates new revenue opportunity for

SingTel to reduce its dependence on carriage services and move vertically into

new space in the value chain.

• Regional telecom markets are lowly penetrated and offers SingTel many

investment opportunities especially in the mobile market

Key Threats:

• StarHub , as the only other full service provider with strong partner, healthy

financial position and superior broadband network, poses the greatest threat to

SingTel’s number one position in the market

• The local market is reaching a mature stage in the industry life cycle. This is

exacerbated by intense competition, little product differentiation and eroding

margins due to prevalence of flat pricing.

• Big global operators are competing with SingTel for investment opportunities

in the region

4.2.2 New Entrants

The threat of new players in the industry is very much a factor of whether there are

barriers of entry and five major sources are discussed:

4.2.2.1 Capital Requirements & Economies of Scale

With the market penetration in excess of 120% for mobile and over 77% for

broadband, SingTel and the other two incumbent operators are enjoying high level of

economies of scale. This also implies that they will have significant cost advantage

MBA Management Project 35 Lee Siak Kwee

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

MBA Management Project 36 Lee Siak Kwee

over any new players coming into the market. SingTel’s well established

infrastructure has taken it years to build and this creates an extremely high entry

barrier. Its fixed line local loop reaches into virtually every household and

commercial buildings in Singapore and its mobile network has also the whole of

Singapore well blanketed. Any new entrants intending to match the breadth and depth

of SingTel’s network would naturally be discouraged by both the high capital

investment and long gestation period, not to mention that the need to undercut the

incumbents in terms of pricing to gain any significant foothold in the market place.

It is primarily due to this entry barrier that most of the newcomers do not focus on

being facility-based operator (FBO) that requires high capital investment but rather

service-based operators owning minimal asset, and unrestricted by regulatory license

quota. These are usually boutique outfit that buys wholesale capacity from the FBOs

(e.g. SingTel) and target specific market segments (e.g. lucrative corporate customers)

and value added service like IDD services, ringtone download etc.

4.2.2.2 Brand Equity

The success of StarHub and M1 has proven that brand equity is not a high barrier to

entry. Within 3 months of its launch in April 2000, StarHub had gained 79,000 mobile

subscribers and 60% of the incremental market share, 260,000 dial-up subscribers (or

a whopping 24% of the TOTAL market share) and a more modest 5% of the IDD

market share (StarHub, 2000). These numbers bear testimony that brand equity can be

overcome if a new competitor can create highly differentiated value propositions

which StarHub has done with its innovative “per-second” billing and “free incoming

call” offerings.

Call tariff in Singapore had long been charged on a 6-seconds charging block basis

and users were also charged for incoming calls. Both these charging schemes were

“legacy” used by SingTel for all its time-based services like fixed line, IDD and

mobile. When M1 entered the market in 1997, it also saw no reason to upset this

cushy arrangement and instead depended on its status as the first challenger to

SingTel to capture market share. So when StarHub stormed the industry with such

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

MBA Management Project 37 Lee Siak Kwee

revolutionary ideas, it quickly established itself as a value-for-money player and

gained market share quickly.

With such intense competition and commoditisation, brand equity has only limited

effect, perhaps only to more quality conscious corporate customers. But to the mass

market consumers, even a household name like SingTel count for little if an

alternative service provider is perceived to offer a more attractive value proposition.

4.2.2.3 Access to Distribution Channels

With Singapore being such a small and densely built-up country, access to

distribution channels is not a major source of barriers to entry. Again, the success of

StarHub demonstrates that even a new operator with sufficient resources can penetrate

into the market relatively quickly.

Access to physical distribution channels may not even be a factor as a barrier to entry

in the internet era. MobTV, an internet based pay-TV services offered by the local

broadcaster, MediaCorp, behaves like any internet based service provider or so called

“e-tailer”; it does not need any brick and mortar distribution channel to sell its

services. Users can just use any existing internet connection to access the services,

effectively diminishing the role played by broadband provider like SingTel to that of a

bit pipe. With cost per bandwidth of internet access trending ever lower, these

internet-based content providers are effectively getting a cheap ride.

4.2.2.4 Cost Disadvantages Independent of Size

Although new players may potentially face cost disadvantages pertaining to

experience, lack of market/operating knowledge, access to favourable location (e.g. to

build base station for mobile coverage) etc, this barrier to entry is not a potential

show-stopper as shown by M1 and StarHub.

Both used the same strategy to overcome this source of barrier to entry when they

entered the competitive fray. While they have the local knowledge of the Singapore

market, they lack the technology competence to operate a telecom network. This was

easily overcome by roping in experienced foreign telcos as their technology partner

and this enabled them to shorten their learning curve as well as time to market.

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

MBA Management Project 38 Lee Siak Kwee

4.2.2.5 Government Policy

The telecom market is fully liberalised since 2000 but for markets like mobile

services, the threat of new entrant is low as the three incumbent operators including

SingTel have exclusive rights for the next 15 years for 3G (and 8 years for 2G). But

for other services like IDD, call back, international leased circuit, content services etc,

it is a completely open field and SingTel faces a myriad of both small and global

operators competing for the same market.

Hamel & Pralahad (1989) stated that “assessing the current tactical advantages of

known competitors will not help you understand the resolution, stamina and

inventiveness of potential competitors”. Indeed, SingTel’s greatest challenge going

forward is not against these known competitors but against non-traditional

competitors bent on shaking up the existing value chain and with a strategic intent of

redrawing the industry rules. With an open market and borderless internet world, such

competitors can literally come from anywhere.

The astounding success of Apple’s iPhone is a preview of things to come for the

telecom industry. Although on face value it is a partnership, iPhone’s business model

of taking a share of subscriber’s monthly revenue and working with only one operator

in each market makes it as real a competitor as anyone else in the market. In fact, it is

even more surreptitious as it feeds on the operator’s subscriber without needing to

expense any direct acquisition cost.

Similarly, the example of StarHub paying premium price for exclusive rights to the

English Premier League shows the type of leverage content owner has over the

success of pay TV business. It exemplifies why ownership of content is becoming a

vital competitive differentiator and more worryingly, the dependency of telcos on

such content owners for their fortunes. Hence, the threat of media players and content

owners developing into mainstream competitors and dominating the value chain is a

very strong possibility.

The award by IDA in Oct 2006 of three licenses to implement nationwide Wifi

services (IDA, Oct 2006) shows that a regulatory regime that is welcoming of new

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

MBA Management Project 39 Lee Siak Kwee

technology can also open doors to new entrants to the market. Although SingTel is

one of the three winners, the more noteworthy points are:

• the other 2 winners, Qmax and iCell are “greenfield” new comers into

the wireless broadband market. Incumbents StarHub and M1 both bid

but were not selected.

• The rollout is heavily funded by the government. In fact, not only is

the network subsidised, licensees are also required to provide basic

public Wifi free of charge for at least 2 years.

At the moment, IDA has also embarked on a highly ambitious plan called “The Next

Generation National Broadband Network” to be put in place by 2012 (IDA, Sept

2006). This new network is capable of delivering broadband speeds up to 1 Gbps

(compared to the highest 100Mbps offered today), and aims to offer pervasive

connectivity and fibre-to-the-home for every household in Singapore.

Besides funding this costly initiative, IDA is revolutionarising how the services are to

be provided. The new framework distinctly separates the operation of the network

from the service provider function. Traditionally, these functions are all owned by the

telcos and new service-based operator wanting to offer service has no choice but to

buy capacity from a facility-based operator e.g. SingTel. Needless to say, such a

model puts the service based operator at a serious disadvantage since SingTel is also a

competitor. With this new open-access model, the playing field is totally leveled and

ANY service provider can compete equally and on non-discriminatory terms with the

rest.

Potentially, such government policy can have dire effect on SingTel’s position in the

market as it will eradicate any competitive advantage that SingTel has build up over

the years on its legacy network.

By June 2008, Singapore will finally have a true number portability facility available

for all the mobile and fixed line subscribers. IDA has mandated this requirement so

that users switching service provider can still retain their current phone number. This

Discontinuities in the Telecom Industry: Strategic Choices for SingTel

lowers the barrier to switching as previously, having to give up a number known to

business associates and social contacts was a high deterrent for users to switch service

provider. This regulation is expected to increase the churn rate, and SingTel, with the

largest group of customers, will naturally have the most to lose.

With the telecom market constantly evolving with new technologies, and a

progressive regulator in IDA that is determined to push for open access and more

consumer choice, it is but a foregone conclusion that liberal government policies will

continue to favour and encourage the entry of new players into the industry. Chris

Lane goes as far as saying that regulatory “poses the biggest risk, it is the most

immediate and threatens to destroy value for SingTel”.

Summary of New Entrant Coming into the Industry.

Key Opportunities:

• Nil

Key Threats:

• Brand equity and access to distribution channels are not significant barriers to

entry. In addition, the evolution towards internet-based transaction may even

negate the value of having physical retail outlets.