Lecture Materials RETAIL BANKING - gsb.org · Lecture Materials RETAIL BANKING Virginia Heyburn ......

40

Lecture Materials RETAIL BANKING Virginia Heyburn Vice President, Strategic Pursuits Global Sales Organization Fiserv [email protected] Miami Beach, Florida 786-239-4898 August 3, 2016

-

Upload

truongtram -

Category

Documents

-

view

224 -

download

0

Transcript of Lecture Materials RETAIL BANKING - gsb.org · Lecture Materials RETAIL BANKING Virginia Heyburn ......

Lecture Materials

RETAIL BANKING

Virginia Heyburn Vice President, Strategic Pursuits

Global Sales OrganizationFiserv

[email protected] Miami Beach, Florida

786-239-4898

August 3, 2016

Growing the Banking Franchise in a Digital World

Virginia HeyburnVice President, Fiserv

August 3rd, 2016

© 2015 Fiserv, Inc. or its affiliates.

Well informed

Highly connected

Tribal sharers and followers

Demand technology

© 2015 Fiserv, Inc. or its affiliates.

Consumers have increasing choices for all facets of financial services

3

© 2015 Fiserv, Inc. or its affiliates.

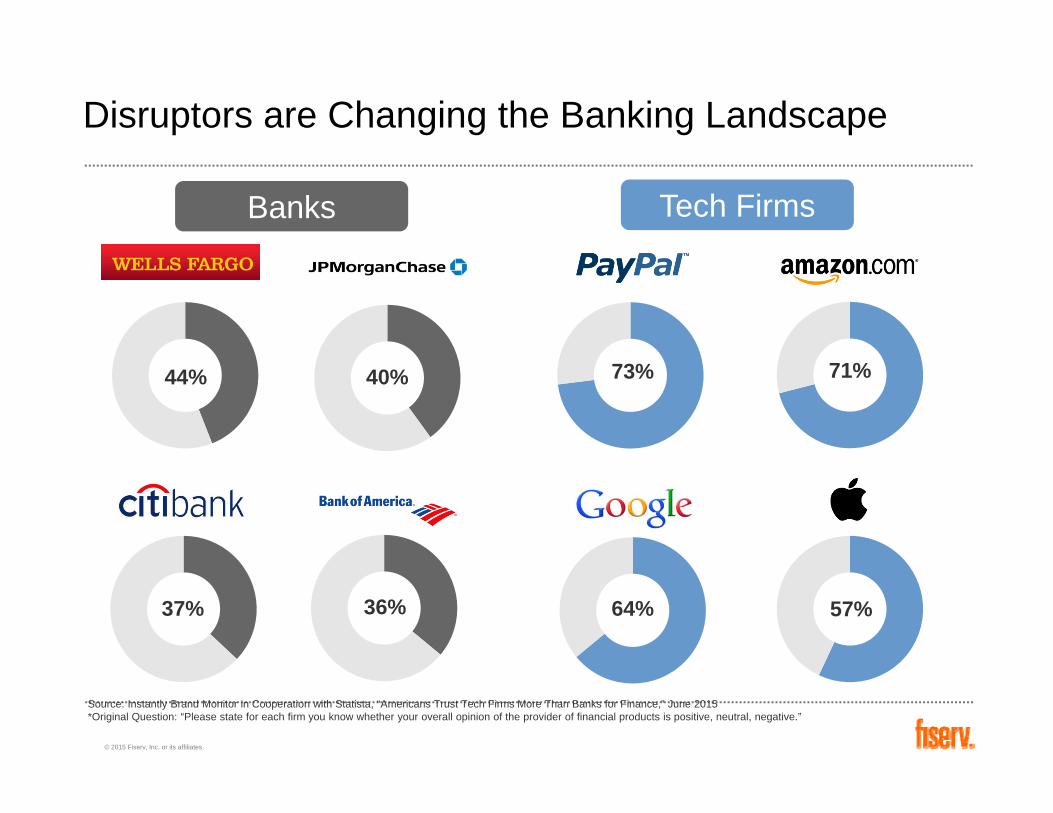

Disruptors are Changing the Banking Landscape

Source: Instantly Brand Monitor in Cooperation with Statista, “Americans Trust Tech Firms More Than Banks for Finance,” June 2015*Original Question: “Please state for each firm you know whether your overall opinion of the provider of financial products is positive, neutral, negative.”

44%

37%

40%

36%

73% 71%

64% 57%

Banks Tech Firms

© 2015 Fiserv, Inc. or its affiliates.

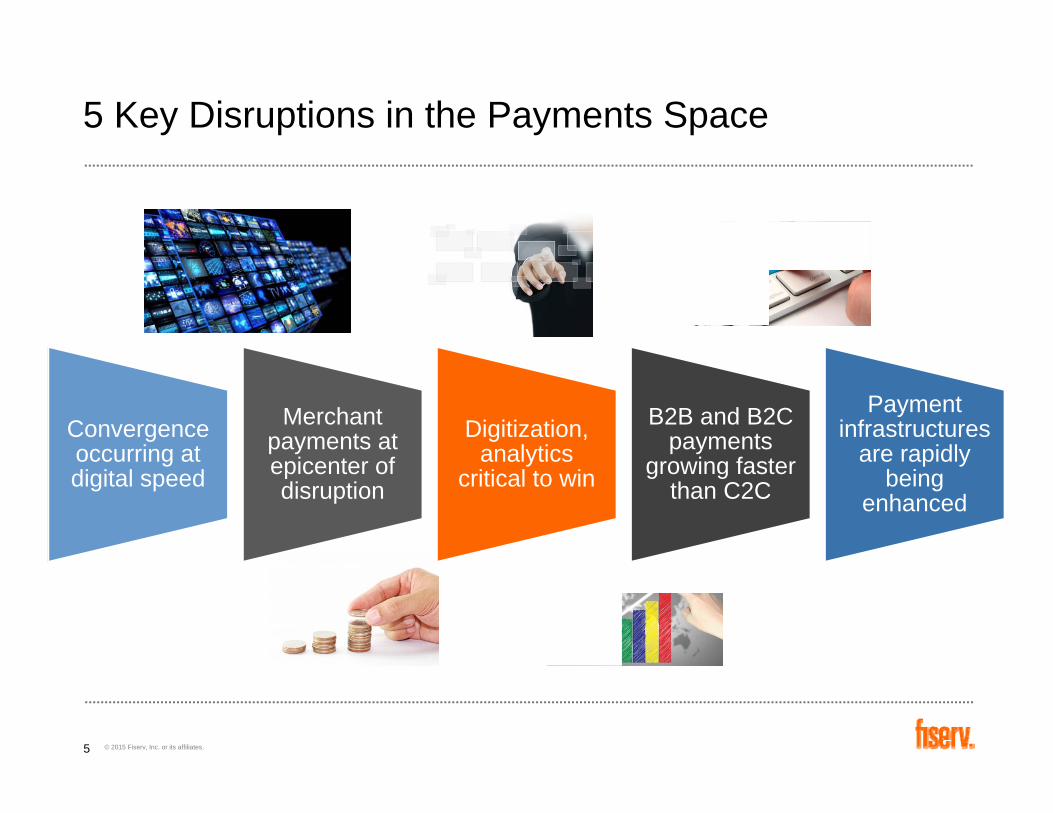

5 Key Disruptions in the Payments Space

Convergence occurring at digital speed

Merchant payments at epicenter of disruption

Digitization, analytics

critical to win

B2B and B2C payments

growing faster than C2C

Payment infrastructures

are rapidly being

enhanced

5

© 2015 Fiserv, Inc. or its affiliates.

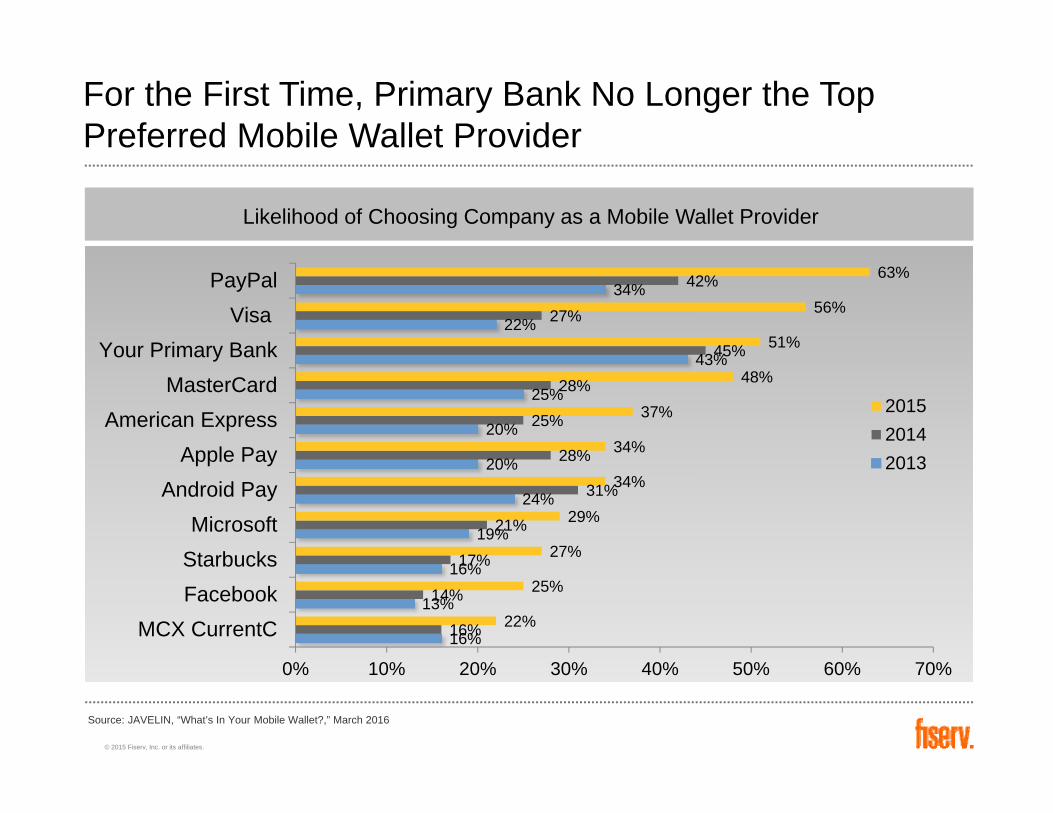

For the First Time, Primary Bank No Longer the Top Preferred Mobile Wallet Provider

16%

13%

16%

19%

24%

20%

20%

25%

43%

22%

34%

16%

14%

17%

21%

31%

28%

25%

28%

45%

27%

42%

22%

25%

27%

29%

34%

34%

37%

48%

51%

56%

63%

MCX CurrentCFacebookStarbucksMicrosoft

Android PayApple Pay

American ExpressMasterCard

Your Primary BankVisa

PayPal

0% 10% 20% 30% 40% 50% 60% 70%

201520142013

Likelihood of Choosing Company as a Mobile Wallet Provider

Source: JAVELIN, “What’s In Your Mobile Wallet?,” March 2016

© 2015 Fiserv, Inc. or its affiliates.

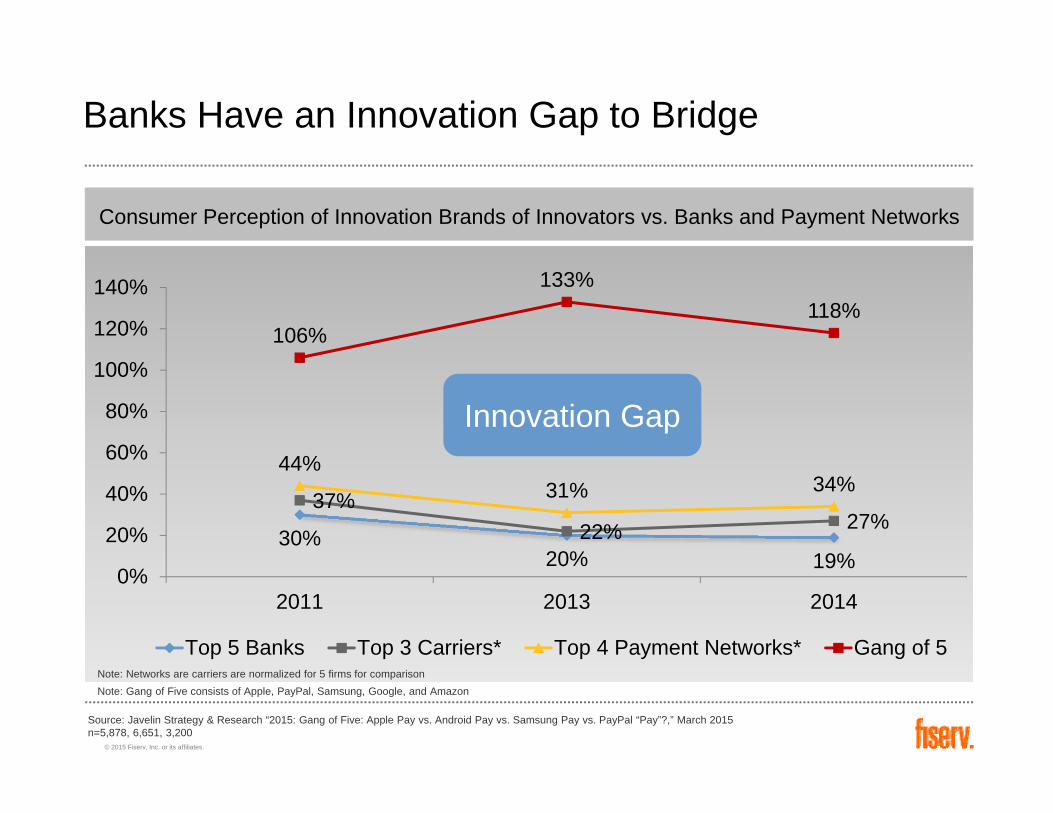

Banks Have an Innovation Gap to Bridge

30%20% 19%

37%22% 27%

44%31% 34%

106%

133%118%

2011 2013 20140%

20%

40%

60%

80%

100%

120%

140%

Top 5 Banks Top 3 Carriers* Top 4 Payment Networks* Gang of 5

Consumer Perception of Innovation Brands of Innovators vs. Banks and Payment Networks

Source: Javelin Strategy & Research “2015: Gang of Five: Apple Pay vs. Android Pay vs. Samsung Pay vs. PayPal “Pay”?,” March 2015 n=5,878, 6,651, 3,200

Note: Networks are carriers are normalized for 5 firms for comparison

Innovation Gap

Note: Gang of Five consists of Apple, PayPal, Samsung, Google, and Amazon

© 2015 Fiserv, Inc. or its affiliates.

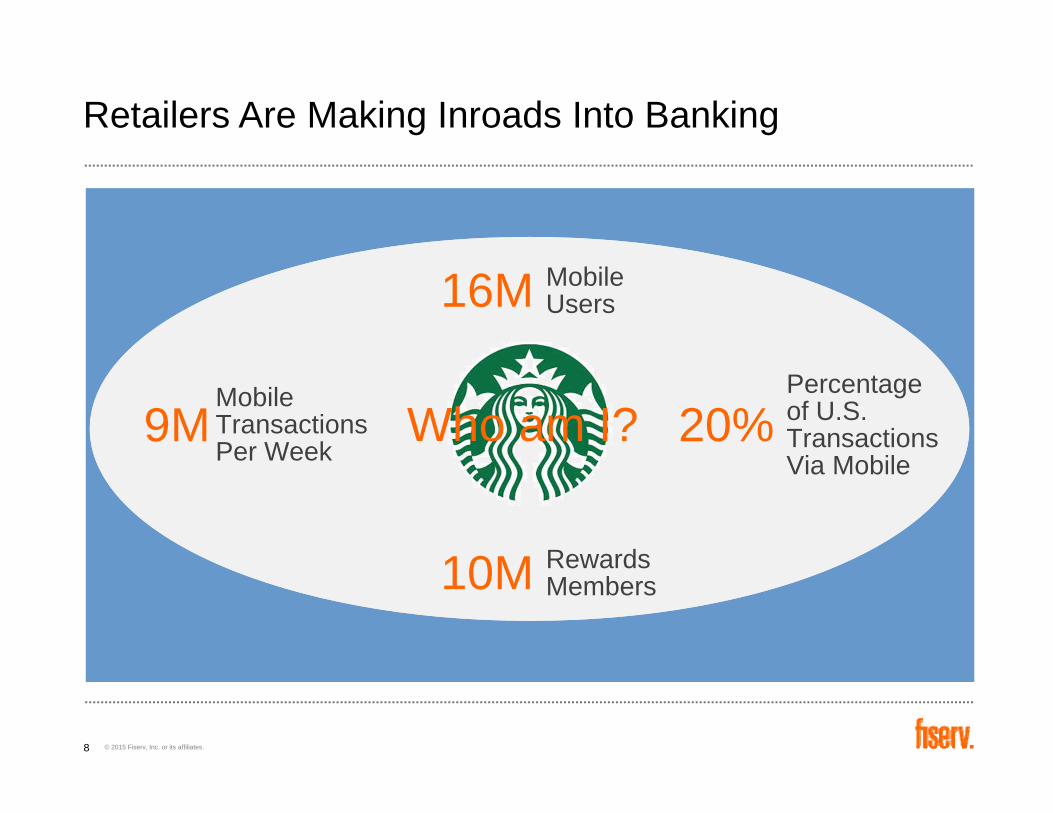

Retailers Are Making Inroads Into Banking

MobileTransactions Per Week

9M

MobileUsers16M

Percentage of U.S. Transactions Via Mobile

20%

RewardsMembers10M

Who am I?

8

© 2015 Fiserv, Inc. or its affiliates.

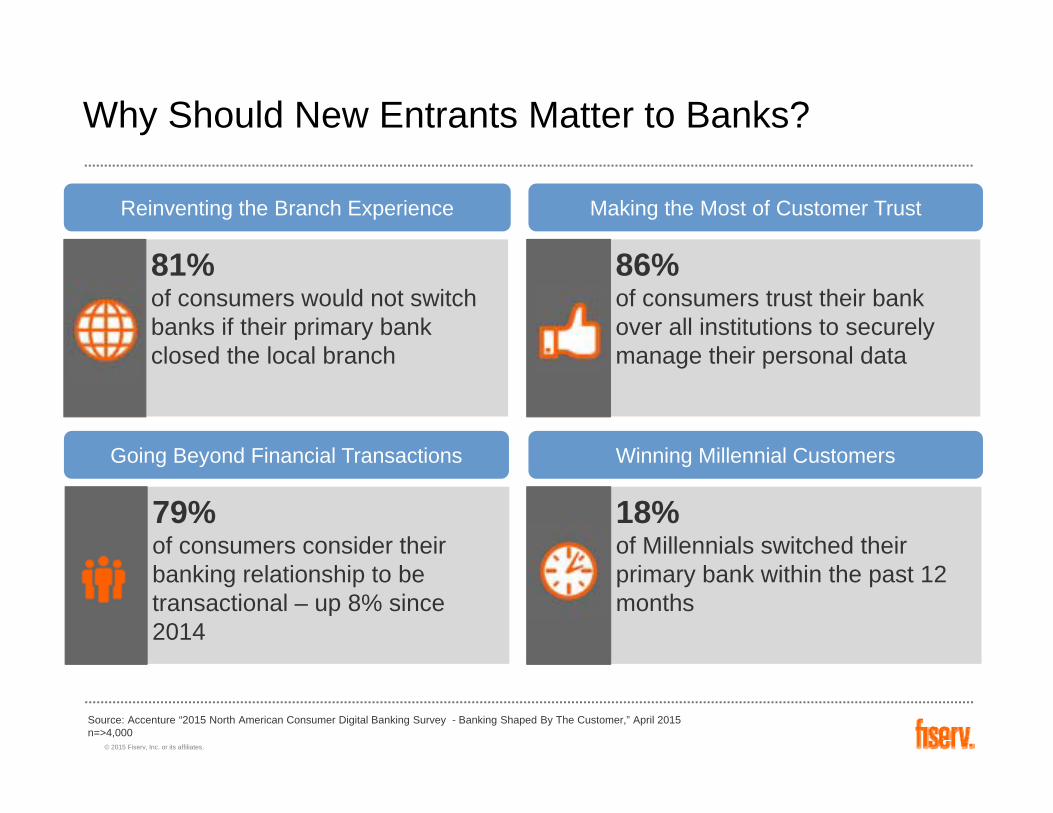

Why Should New Entrants Matter to Banks?

Source: Accenture “2015 North American Consumer Digital Banking Survey - Banking Shaped By The Customer,” April 2015n=>4,000

81%of consumers would not switch banks if their primary bank closed the local branch

79%of consumers consider their banking relationship to be transactional – up 8% since 2014

86%of consumers trust their bank over all institutions to securely manage their personal data

18%of Millennials switched their primary bank within the past 12 months

Reinventing the Branch Experience Making the Most of Customer Trust

Going Beyond Financial Transactions Winning Millennial Customers

© 2015 Fiserv, Inc. or its affiliates.

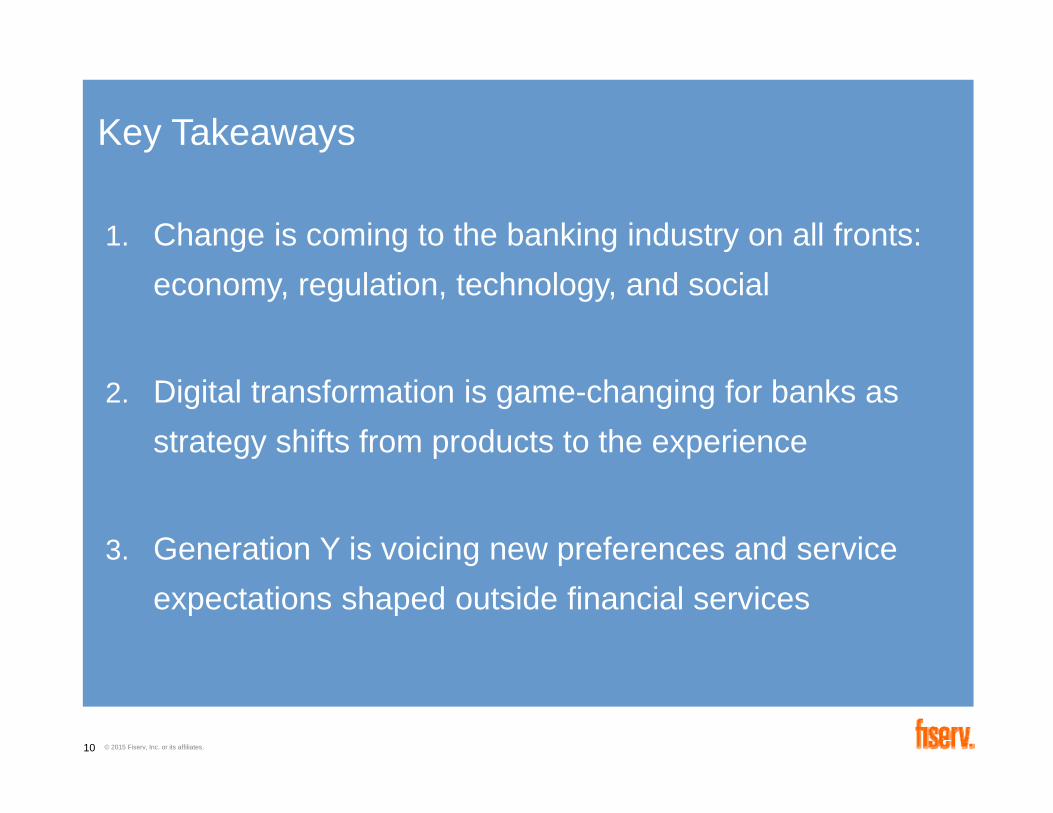

1. Change is coming to the banking industry on all fronts: economy, regulation, technology, and social

2. Digital transformation is game-changing for banks as strategy shifts from products to the experience

3. Generation Y is voicing new preferences and service expectations shaped outside financial services

10

Key Takeaways

© 2015 Fiserv, Inc. or its affiliates.

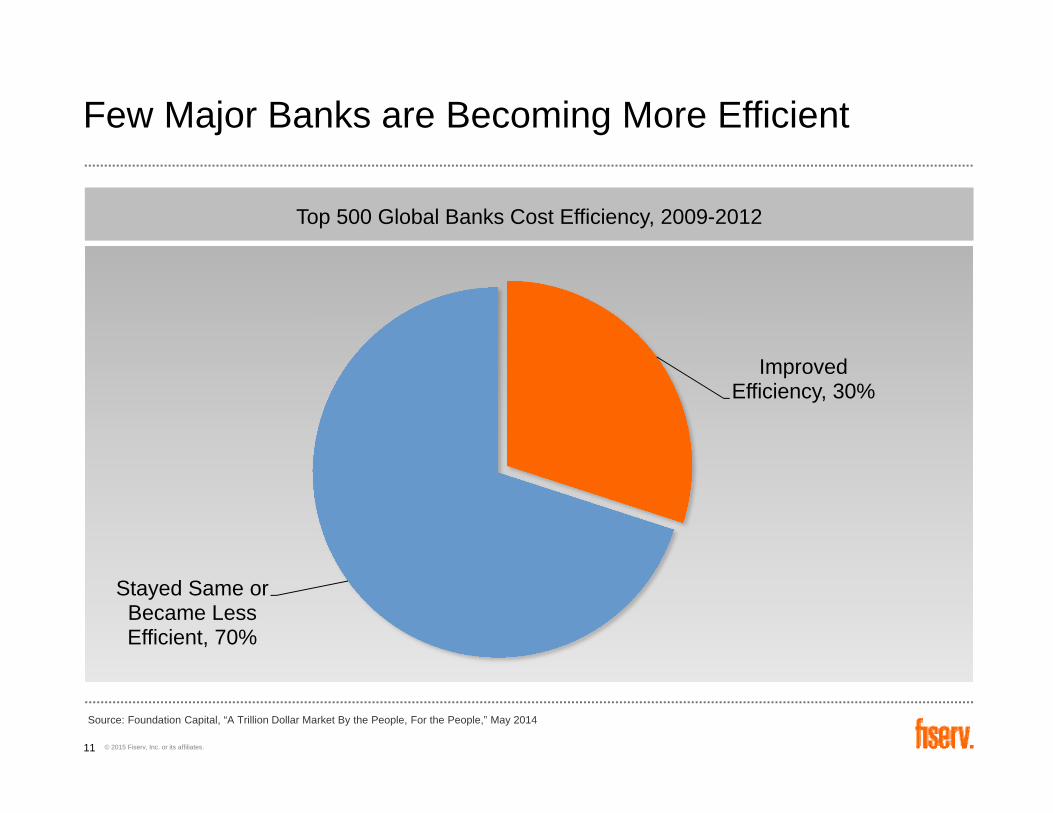

Few Major Banks are Becoming More Efficient

Improved Efficiency, 30%

Stayed Same or Became Less Efficient, 70%

Top 500 Global Banks Cost Efficiency, 2009-2012

Source: Foundation Capital, “A Trillion Dollar Market By the People, For the People,” May 2014

11

© 2015 Fiserv, Inc. or its affiliates.

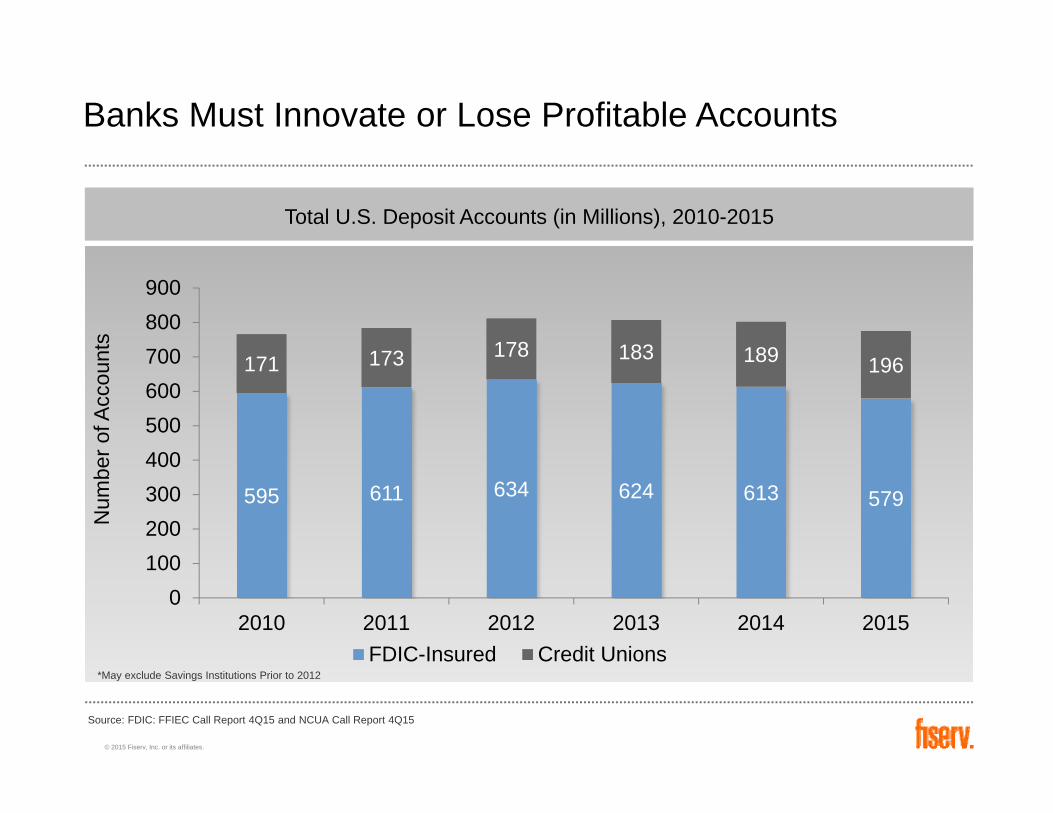

Banks Must Innovate or Lose Profitable Accounts

595 611 634 624 613 579

171 173 178 183 189 196

0100200300400500600700800900

2010 2011 2012 2013 2014 2015

Num

ber o

f Acc

ount

s

FDIC-Insured Credit Unions

Total U.S. Deposit Accounts (in Millions), 2010-2015

Source: FDIC: FFIEC Call Report 4Q15 and NCUA Call Report 4Q15

*May exclude Savings Institutions Prior to 2012

© 2015 Fiserv, Inc. or its affiliates.

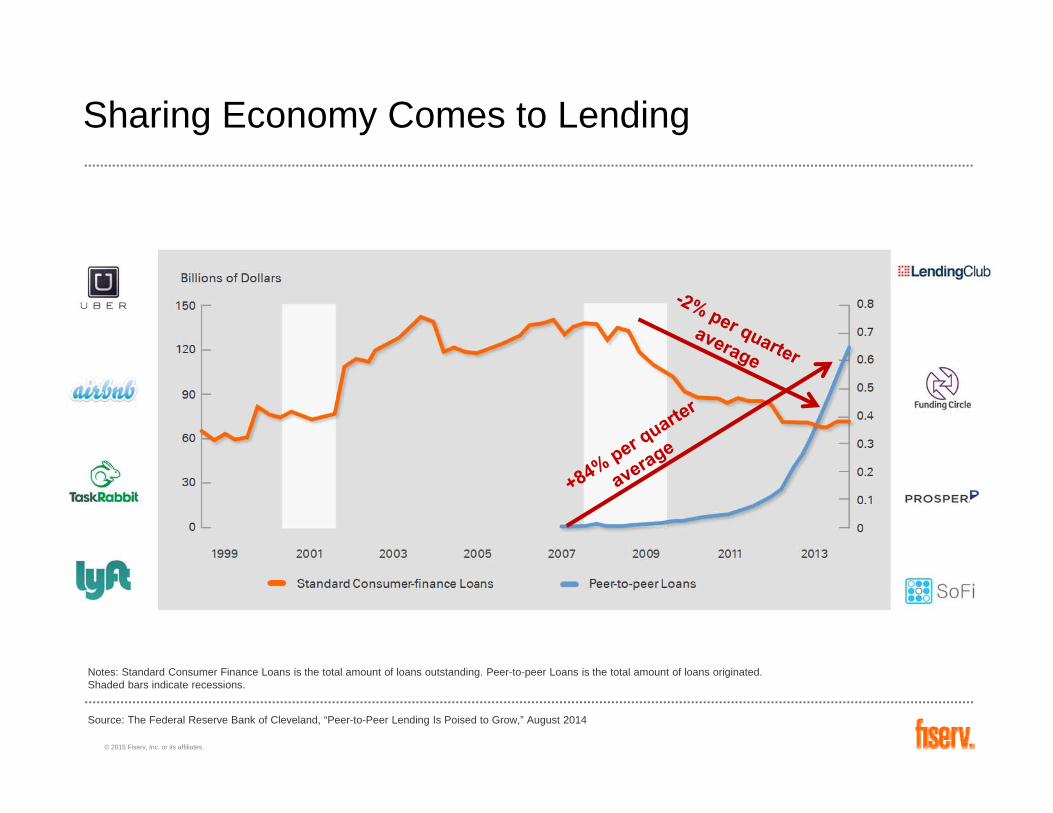

Sharing Economy Comes to Lending

Source: The Federal Reserve Bank of Cleveland, “Peer-to-Peer Lending Is Poised to Grow,” August 2014

Notes: Standard Consumer Finance Loans is the total amount of loans outstanding. Peer-to-peer Loans is the total amount of loans originated. Shaded bars indicate recessions.

© 2015 Fiserv, Inc. or its affiliates.

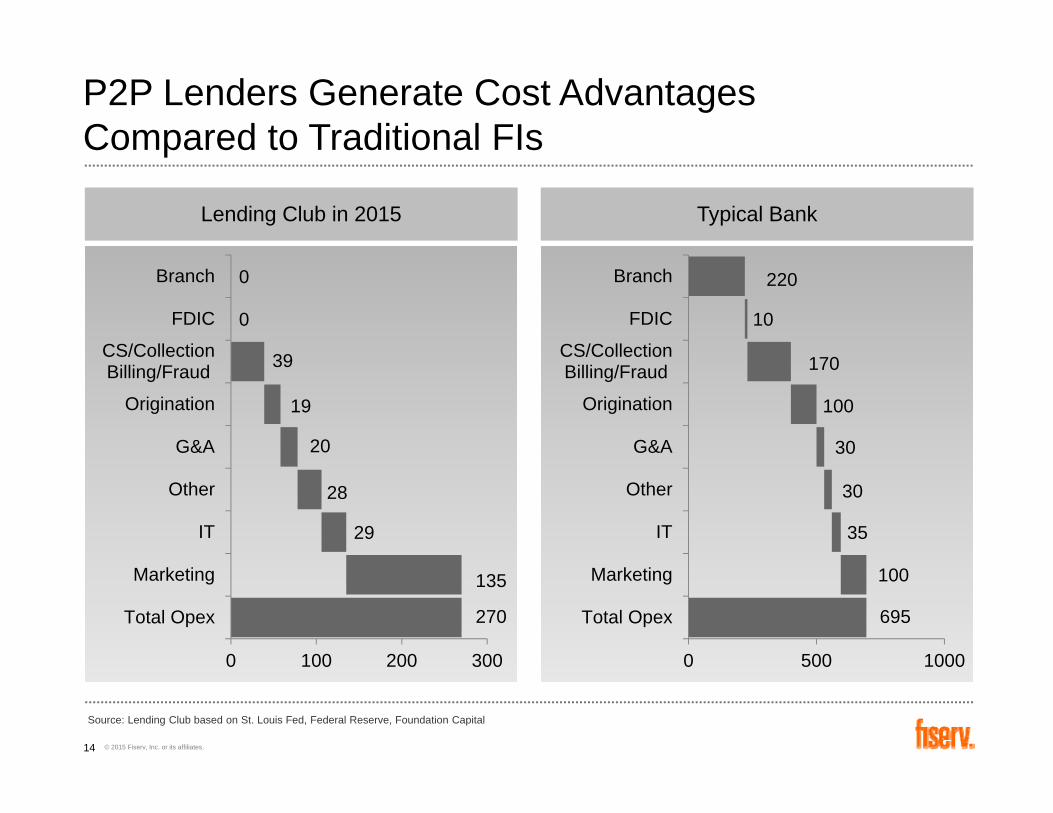

P2P Lenders Generate Cost Advantages Compared to Traditional FIs

270

135

29

28

20

19

39

0

0

0 100 200 300

Total Opex

Marketing

IT

Other

G&A

Origination

CS/CollectionBilling/Fraud

FDIC

Branch

Typical BankLending Club in 2015

695

100

35

30

30

100

170

10

220

0 500 1000

Total Opex

Marketing

IT

Other

G&A

Origination

CS/CollectionBilling/Fraud

FDIC

Branch

Source: Lending Club based on St. Louis Fed, Federal Reserve, Foundation Capital

14

© 2015 Fiserv, Inc. or its affiliates.

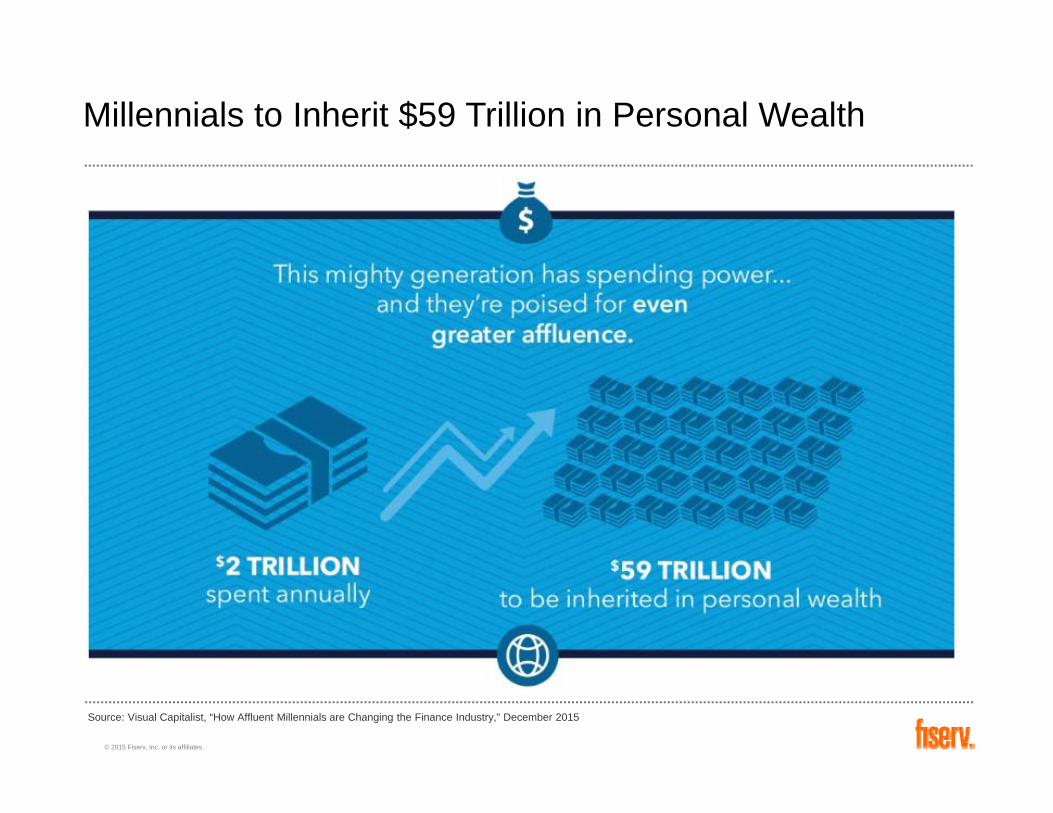

Millennials to Inherit $59 Trillion in Personal Wealth

Source: Visual Capitalist, “How Affluent Millennials are Changing the Finance Industry,” December 2015

2030

© 2015 Fiserv, Inc. or its affiliates.

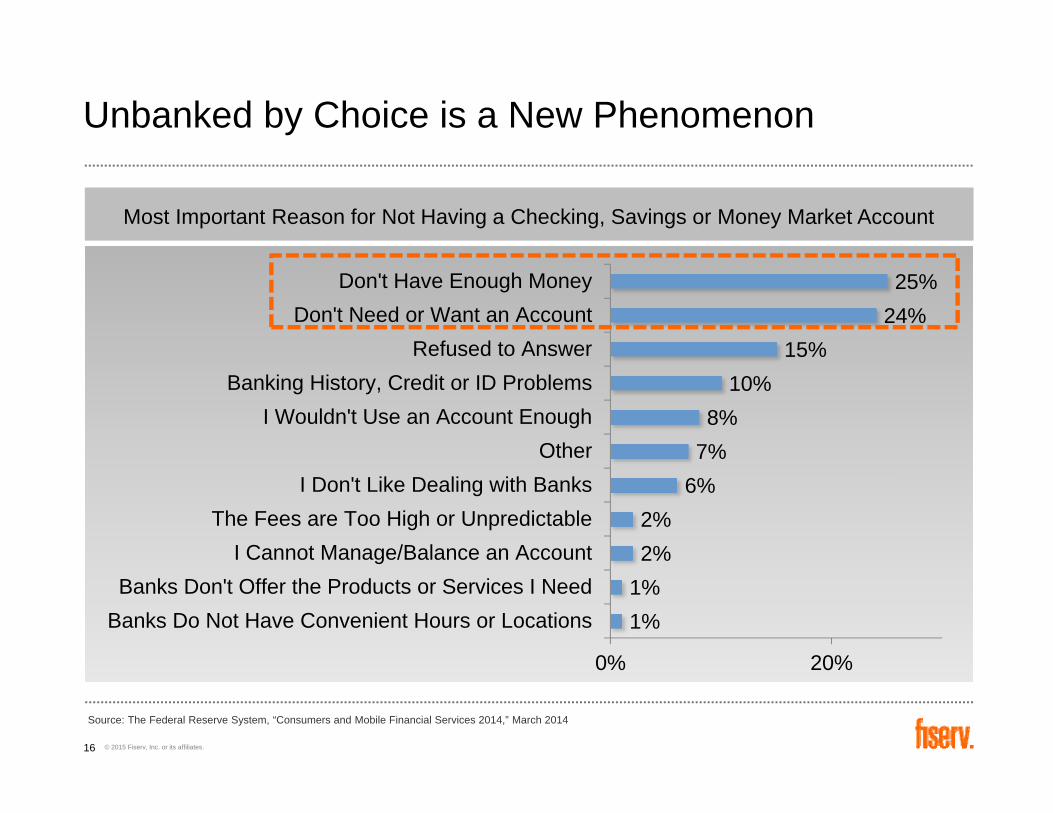

Unbanked by Choice is a New Phenomenon

1%1%2%2%

6%7%8%

10%15%

24%25%

0% 20%

Banks Do Not Have Convenient Hours or LocationsBanks Don't Offer the Products or Services I Need

I Cannot Manage/Balance an AccountThe Fees are Too High or Unpredictable

I Don't Like Dealing with BanksOther

I Wouldn't Use an Account EnoughBanking History, Credit or ID Problems

Refused to AnswerDon't Need or Want an Account

Don't Have Enough Money

Most Important Reason for Not Having a Checking, Savings or Money Market Account

Source: The Federal Reserve System, “Consumers and Mobile Financial Services 2014,” March 2014

16

© 2015 Fiserv, Inc. or its affiliates.

Disruptive Innovation

© 2015 Fiserv, Inc. or its affiliates.

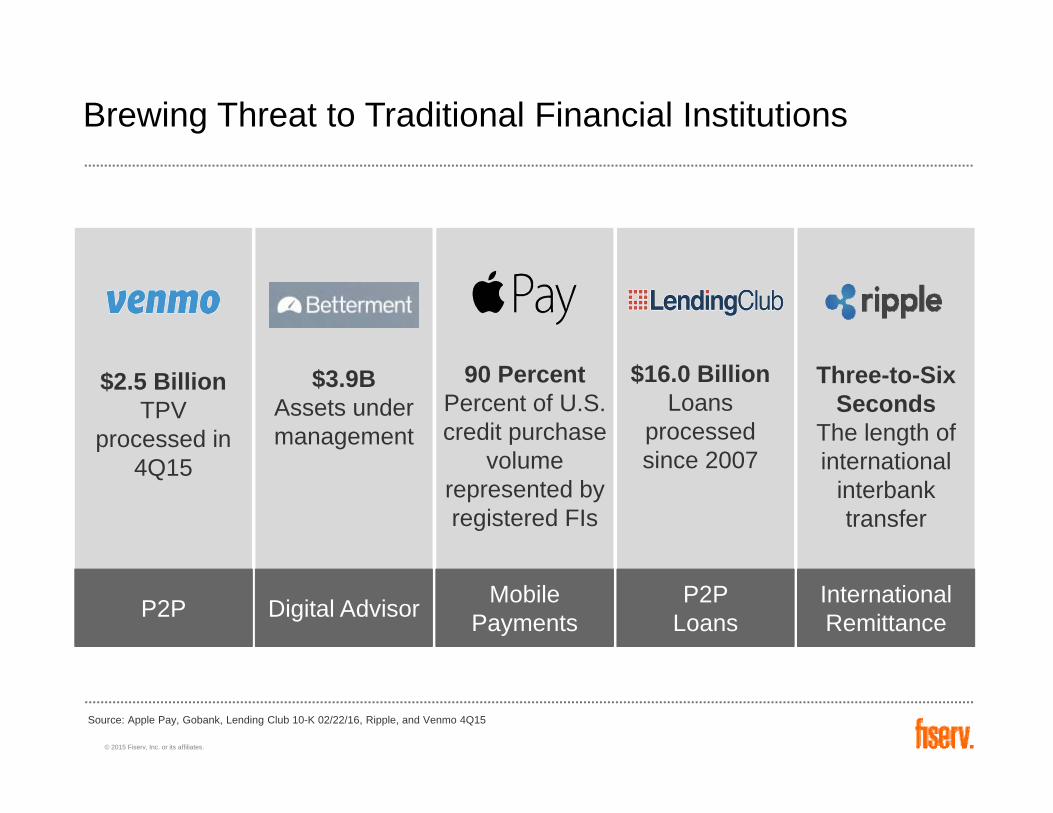

Brewing Threat to Traditional Financial Institutions

$2.5 BillionTPV

processed in 4Q15

P2P

90 PercentPercent of U.S. credit purchase

volume represented by registered FIs

MobilePayments

P2P Loans

$16.0 BillionLoans

processed since 2007

Digital Advisor

$3.9BAssets under management

International Remittance

Three-to-Six Seconds

The length of international

interbank transfer

Source: Apple Pay, Gobank, Lending Club 10-K 02/22/16, Ripple, and Venmo 4Q15

© 2015 Fiserv, Inc. or its affiliates.

Who Will Drive the Primary Banking Relationship?

19

© 2015 Fiserv, Inc. or its affiliates.

1. Mobile access means customers are engaging their banks more than ever

2. Technology is emerging as an important loyalty builder for banks seeking deeper customer relationships

3. Technology is leveling the playing field among large and small banks

4. Alternative lending is gaining favor with consumers

20

Key Takeaways

© 2015 Fiserv, Inc. or its affiliates.

Payments Have Not Kept Pace

• Days, not minutes

• Cut-off times

• Weekends and holidays

• Instant delivery options are very limited

$$

21

© 2015 Fiserv, Inc. or its affiliates.

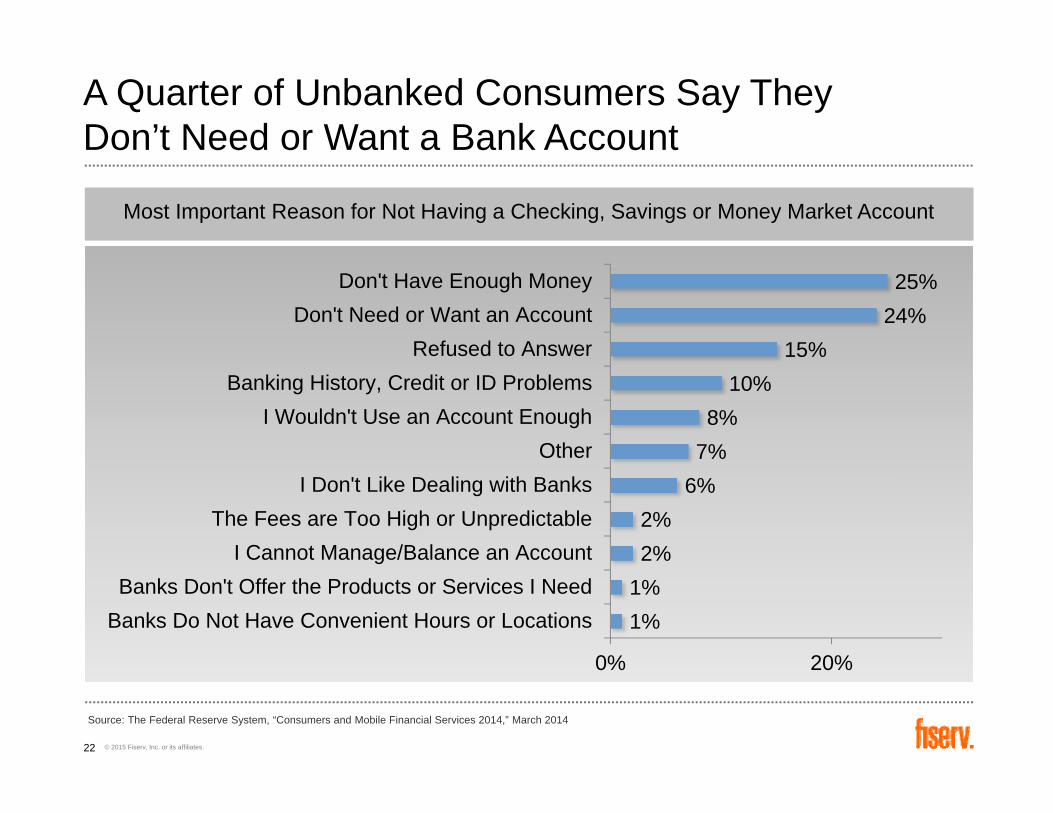

A Quarter of Unbanked Consumers Say They Don’t Need or Want a Bank Account

1%1%2%2%

6%7%8%

10%15%

24%25%

0% 20%

Banks Do Not Have Convenient Hours or LocationsBanks Don't Offer the Products or Services I Need

I Cannot Manage/Balance an AccountThe Fees are Too High or Unpredictable

I Don't Like Dealing with BanksOther

I Wouldn't Use an Account EnoughBanking History, Credit or ID Problems

Refused to AnswerDon't Need or Want an Account

Don't Have Enough Money

Most Important Reason for Not Having a Checking, Savings or Money Market Account

Source: The Federal Reserve System, “Consumers and Mobile Financial Services 2014,” March 2014

22

© 2015 Fiserv, Inc. or its affiliates.

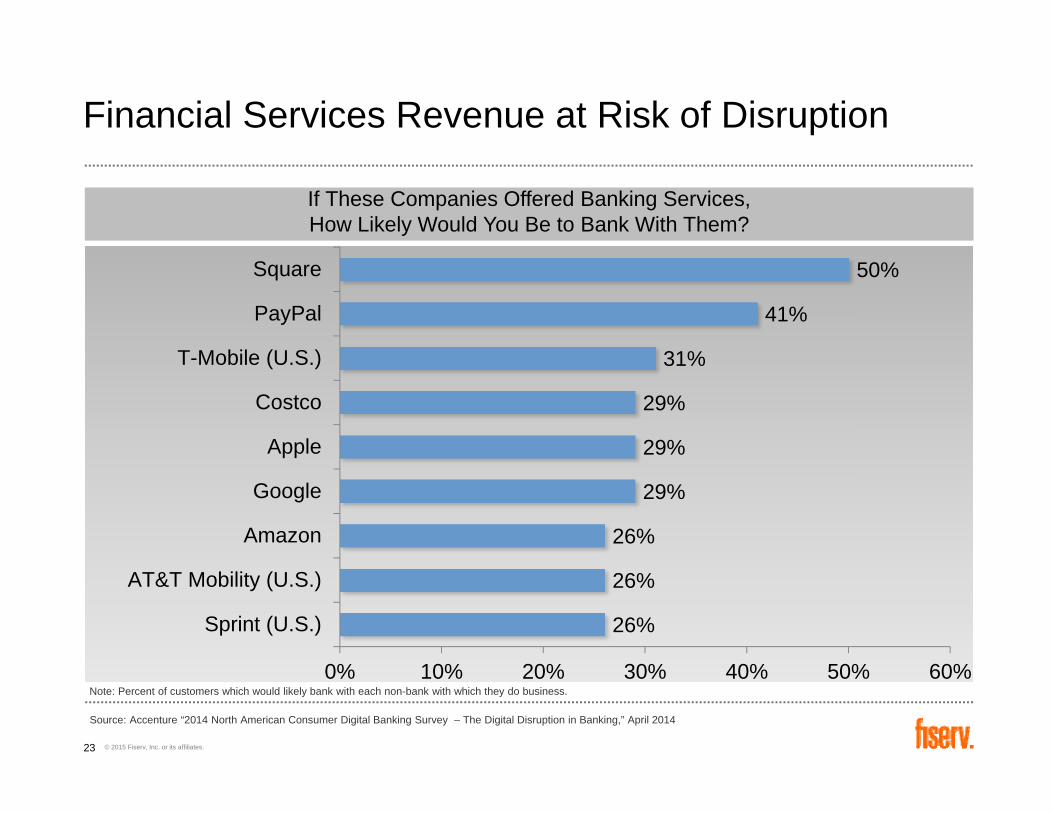

Financial Services Revenue at Risk of Disruption

26%

26%

26%

29%

29%

29%

31%

41%

50%

Sprint (U.S.)

AT&T Mobility (U.S.)

Amazon

Apple

Costco

T-Mobile (U.S.)

PayPal

Square

0% 10% 20% 30% 40% 50% 60%

If These Companies Offered Banking Services, How Likely Would You Be to Bank With Them?

Source: Accenture “2014 North American Consumer Digital Banking Survey – The Digital Disruption in Banking,” April 2014

Note: Percent of customers which would likely bank with each non-bank with which they do business.

23

© 2015 Fiserv, Inc. or its affiliates.

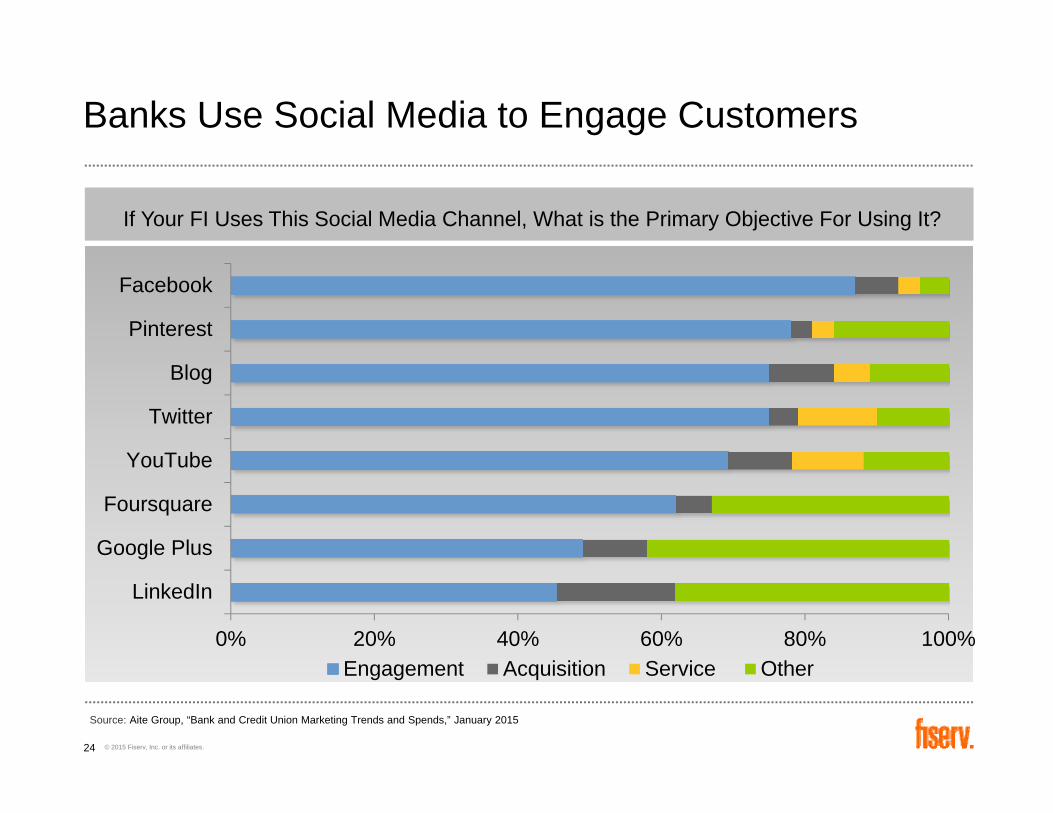

Banks Use Social Media to Engage Customers

0% 20% 40% 60% 80% 100%

Google Plus

Foursquare

YouTube

Blog

Engagement Acquisition Service Other

If Your FI Uses This Social Media Channel, What is the Primary Objective For Using It?

Source: Aite Group, “Bank and Credit Union Marketing Trends and Spends,” January 2015

24

© 2015 Fiserv, Inc. or its affiliates.

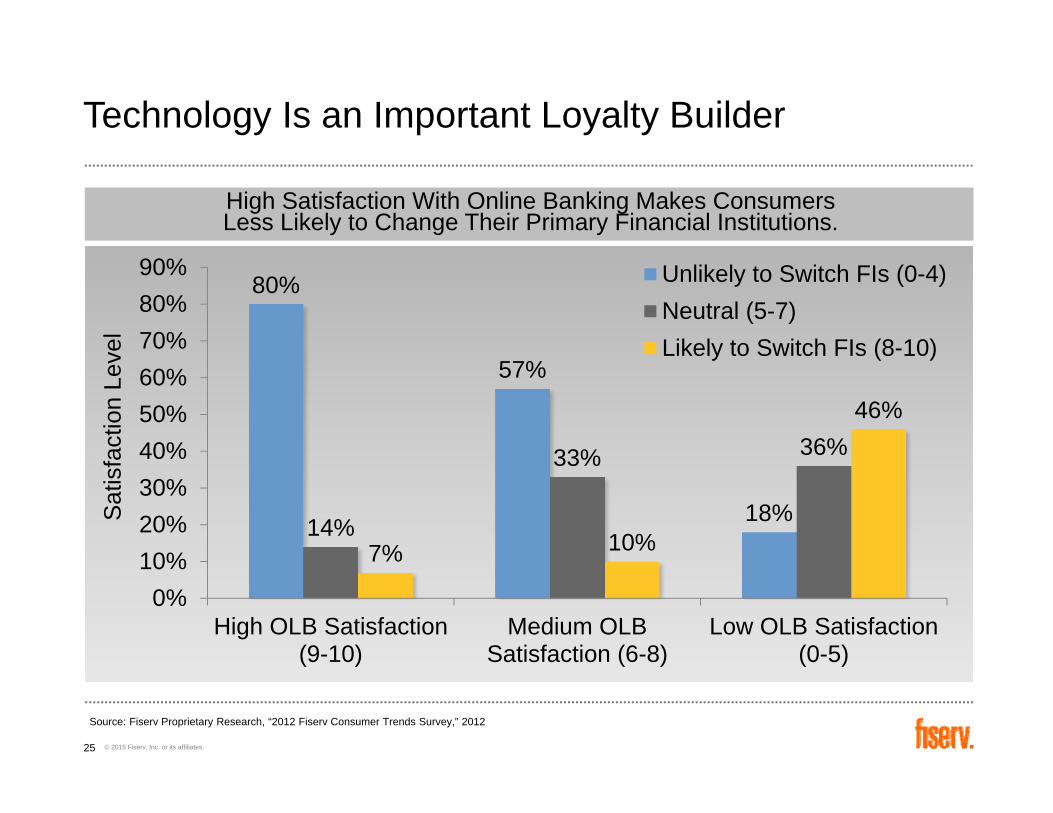

Technology Is an Important Loyalty Builder

80%

57%

18%14%

33% 36%

7% 10%

46%

0%10%20%30%40%50%60%70%80%90%

High OLB Satisfaction(9-10)

Medium OLBSatisfaction (6-8)

Low OLB Satisfaction(0-5)

Sat

isfa

ctio

n Le

vel

Unlikely to Switch FIs (0-4)Neutral (5-7)Likely to Switch FIs (8-10)

High Satisfaction With Online Banking Makes Consumers Less Likely to Change Their Primary Financial Institutions.

Source: Fiserv Proprietary Research, “2012 Fiserv Consumer Trends Survey,” 2012

25

© 2015 Fiserv, Inc. or its affiliates.

1. The payments landscape is transforming with new technology capabilities

2. Paper-based payments are in decline as cards-based payments are favored by consumers

3. Banks are competing with a host of new players

26

Key Takeaways

© 2015 Fiserv, Inc. or its affiliates.

It’s a Different World

© 2015 Fiserv, Inc. or its affiliates.

Invisible Payments

Instant Money Movement

Internet of Things

Data-Driven Relationships

Mobile Everywhere

© 2015 Fiserv, Inc. or its affiliates.

Looking to the Future

© 2015 Fiserv, Inc. or its affiliates.

“The Internet of Things (IoT) describes the phenomenon of everyday devices connecting to the Internet through tiny embedded sensors and computing power.”

Accenture

The Internet of Things

© 2015 Fiserv, Inc. or its affiliates.

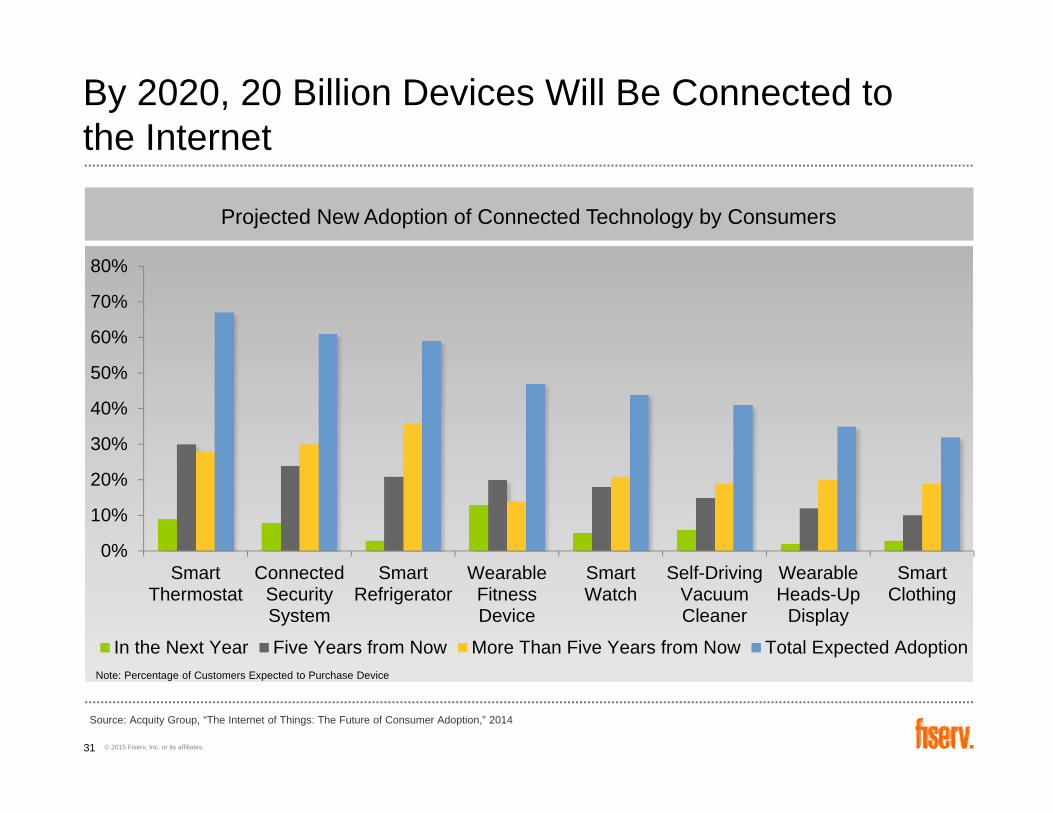

By 2020, 20 Billion Devices Will Be Connected to the Internet

0%

10%

20%

30%

40%

50%

60%

70%

80%

SmartThermostat

ConnectedSecuritySystem

SmartRefrigerator

WearableFitnessDevice

SmartWatch

Self-DrivingVacuumCleaner

WearableHeads-Up

Display

SmartClothing

In the Next Year Five Years from Now More Than Five Years from Now Total Expected Adoption

Projected New Adoption of Connected Technology by Consumers

Source: Acquity Group, “The Internet of Things: The Future of Consumer Adoption,” 2014

Note: Percentage of Customers Expected to Purchase Device

31

© 2015 Fiserv, Inc. or its affiliates.

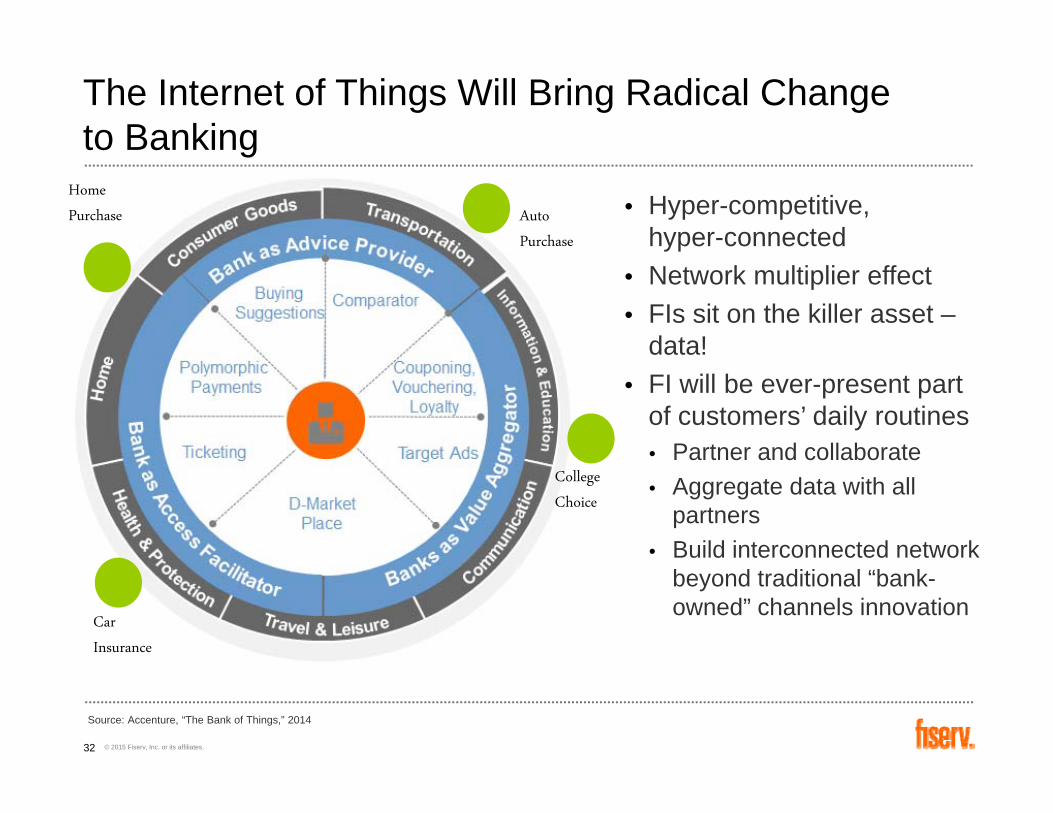

The Internet of Things Will Bring Radical Change to Banking

• Hyper-competitive, hyper-connected

• Network multiplier effect• FIs sit on the killer asset –

data!• FI will be ever-present part

of customers’ daily routines• Partner and collaborate• Aggregate data with all

partners• Build interconnected network

beyond traditional “bank-owned” channels innovation

Source: Accenture, “The Bank of Things,” 2014

Auto

Purchase

College

Choice

Car

Insurance

Home

Purchase

32

© 2015 Fiserv, Inc. or its affiliates.

Reverse Mentoring: Everyone is Connected

© 2015 Fiserv, Inc. or its affiliates.

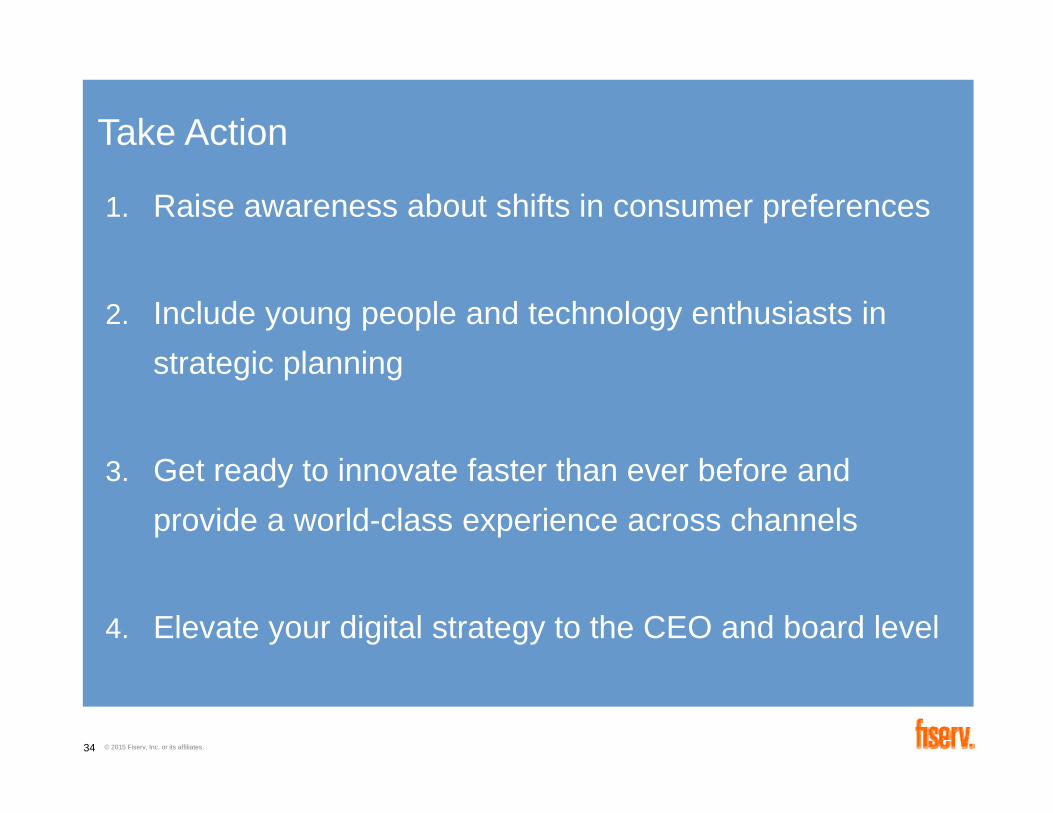

1. Raise awareness about shifts in consumer preferences

2. Include young people and technology enthusiasts in strategic planning

3. Get ready to innovate faster than ever before and provide a world-class experience across channels

4. Elevate your digital strategy to the CEO and board level

34

Take Action

© 2015 Fiserv, Inc. or its affiliates.

Thought for the Day:

Expect “revolutionary change” in payments speed

in the next 3-5 years

35

Virginia [email protected]

Growing the Banking Franchise in a Digital World

Virginia HeyburnVice President, Fiserv

August 3rd, 2015

© 2015 Fiserv, Inc. or its affiliates.

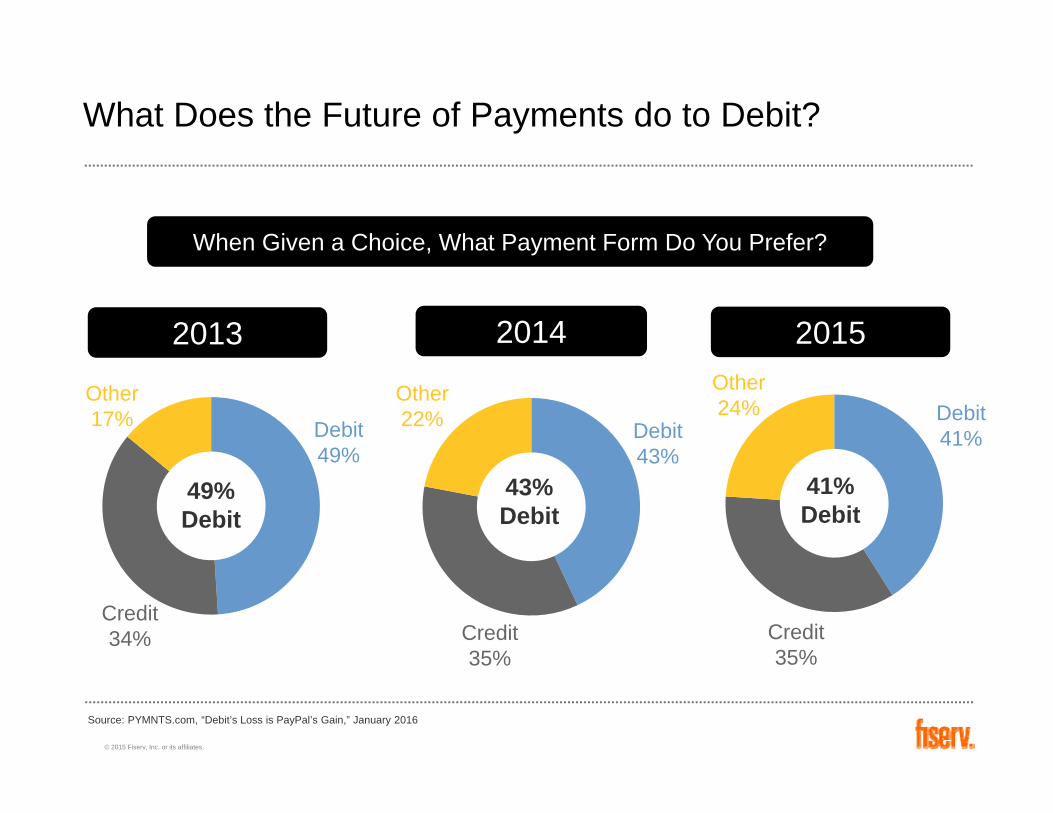

What Does the Future of Payments do to Debit?

49%Debit

When Given a Choice, What Payment Form Do You Prefer?

2013 2014 2015

Source: PYMNTS.com, “Debit’s Loss is PayPal’s Gain,” January 2016

Debit49%

Debit43%

Debit41%

Credit35%

Credit35%

Credit34%

43%Debit

41%Debit

Other17%

Other22%

Other24%