Lecture 12 - Divisional Performance Measures and Transfer Pricing

40

DIVISIONAL PERFORMANCE MEASURES AND TRANSFER PRICING LECTURE 12

-

Upload

judith-kukua-aboagye-danso -

Category

Documents

-

view

267 -

download

8

Transcript of Lecture 12 - Divisional Performance Measures and Transfer Pricing

DIVISIONAL PERFORMANCE MEASURES AND TRANSFER PRICING

LECTURE 12

Overview

Responsibility accounting Investment centre performance appraisal

methods Return on investment (ROI) Residual income (RI) Economic value added (EVA)

Transfer pricing Aims Approaches

Market based Cost based Opportunity cost

Introduction

Generally a company with several divisions will be a decentralised organisation. In such organisations divisional managers tend be responsible for making their own decisions concerning the operation of their division.

Advantages of decentralisation include: Decisions taken more quickly Increase motivation of management Increase quality of decisions due to local knowledge Reduce head office bureaucracy Provide better training for all levels of management

Disadvantages of decentralisation Potential for dysfunctional decision-making Duplication amongst divisions leading to greater cost Senior management loss of control

Appropriate performance evaluation methods are therefore needed.

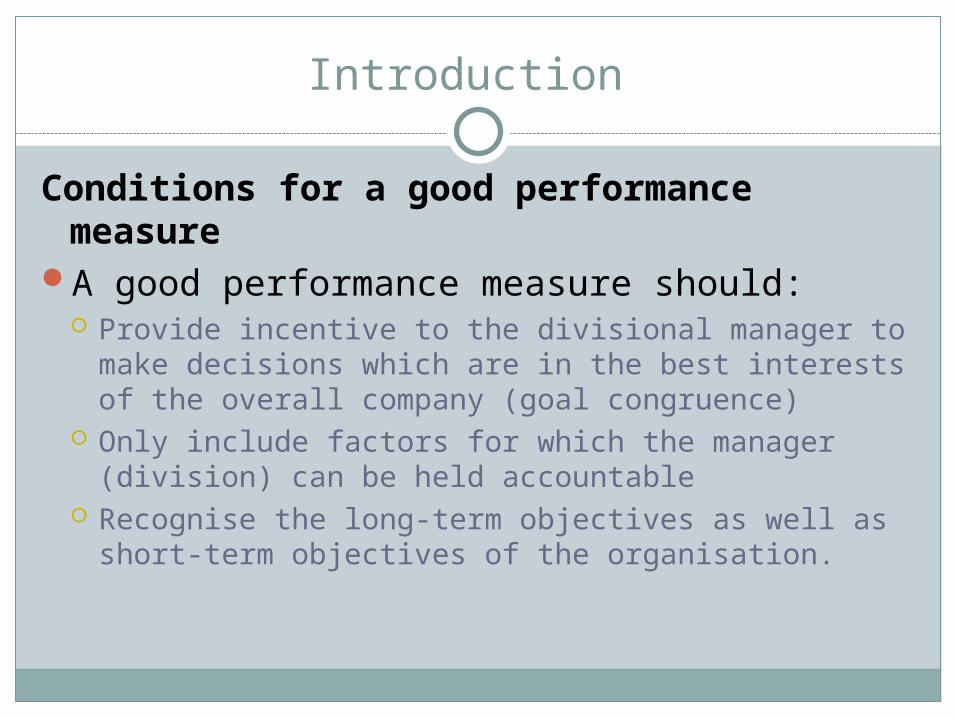

Introduction

Conditions for a good performance measure

A good performance measure should: Provide incentive to the divisional manager to make

decisions which are in the best interests of the overall company (goal congruence)

Only include factors for which the manager (division) can be held accountable

Recognise the long-term objectives as well as short-term objectives of the organisation.

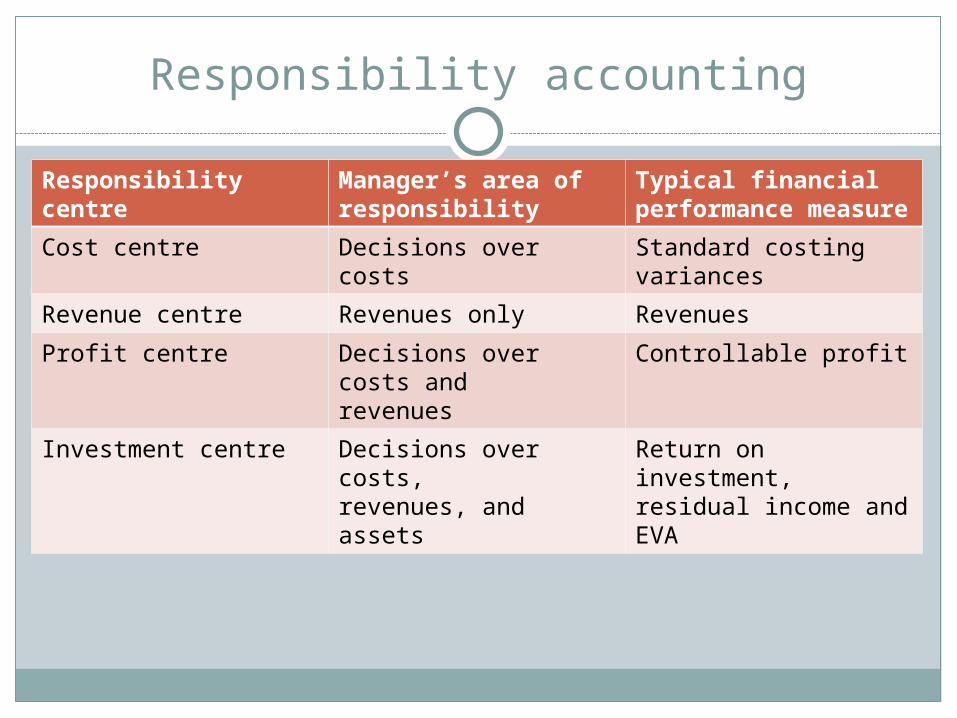

Responsibility accounting

Responsibility centre

Manager’s area of responsibility

Typical financial performance measure

Cost centre Decisions over costs Standard costing variances

Revenue centre Revenues only Revenues

Profit centre Decisions over costs andrevenues

Controllable profit

Investment centre Decisions over costs,revenues, and assets

Return on investment,residual income and EVA

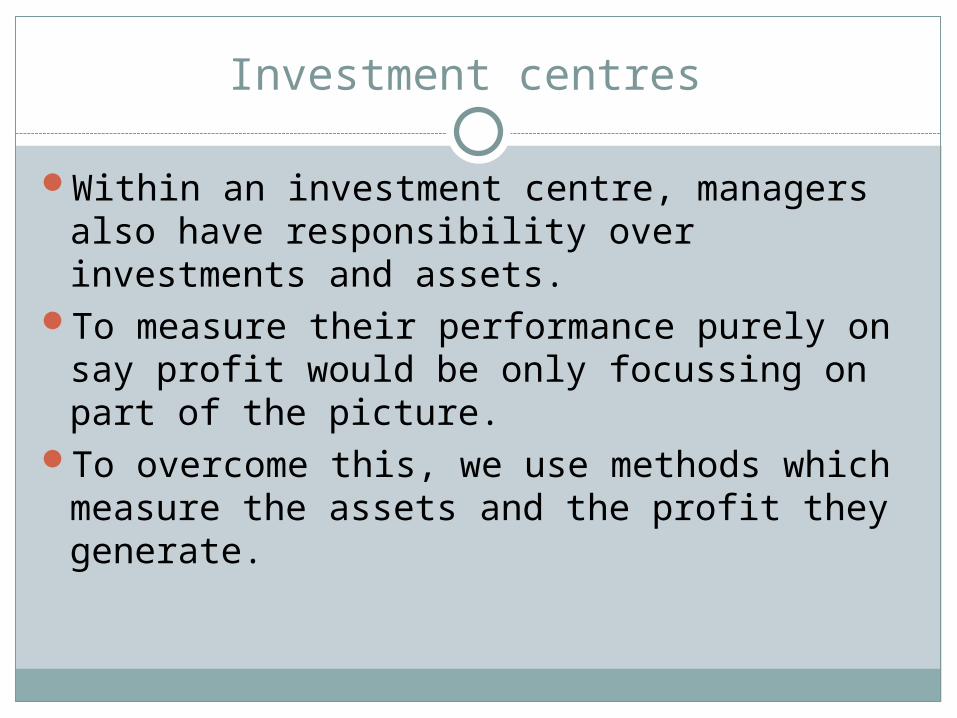

Investment centres

Within an investment centre, managers also have responsibility over investments and assets.

To measure their performance purely on say profit would be only focussing on part of the picture.

To overcome this, we use methods which measure the assets and the profit they generate.

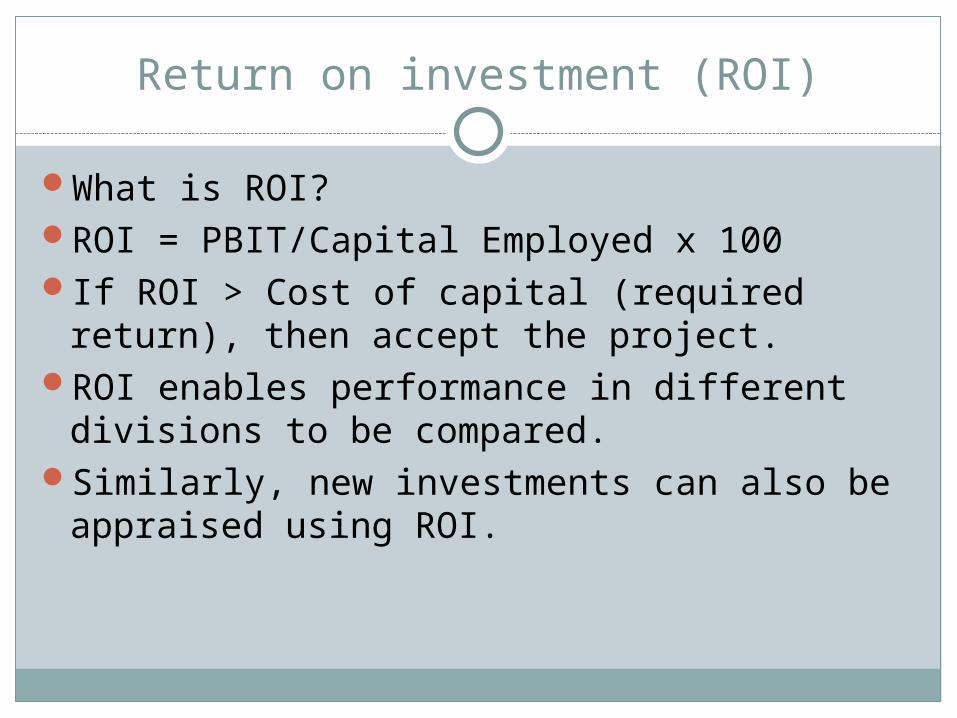

Return on investment (ROI)

What is ROI?ROI = PBIT/Capital Employed x 100If ROI > Cost of capital (required return),

then accept the project.ROI enables performance in different

divisions to be compared.Similarly, new investments can also be

appraised using ROI.

ROI

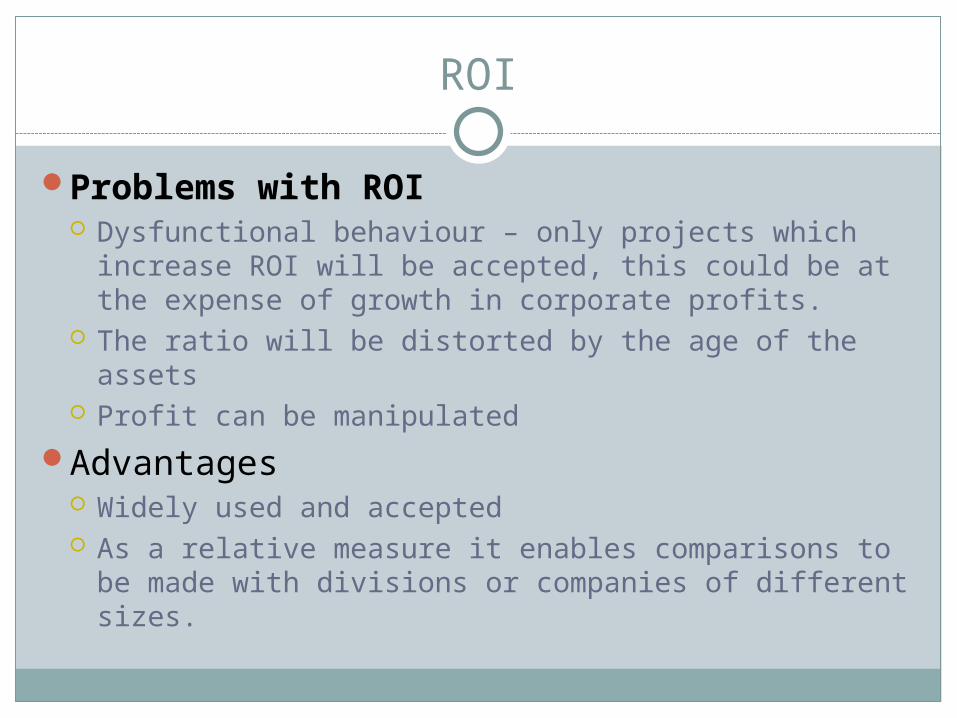

Problems with ROI Dysfunctional behaviour – only projects which

increase ROI will be accepted, this could be at the expense of growth in corporate profits.

The ratio will be distorted by the age of the assets Profit can be manipulated

Advantages Widely used and accepted As a relative measure it enables comparisons to be

made with divisions or companies of different sizes.

Example 1

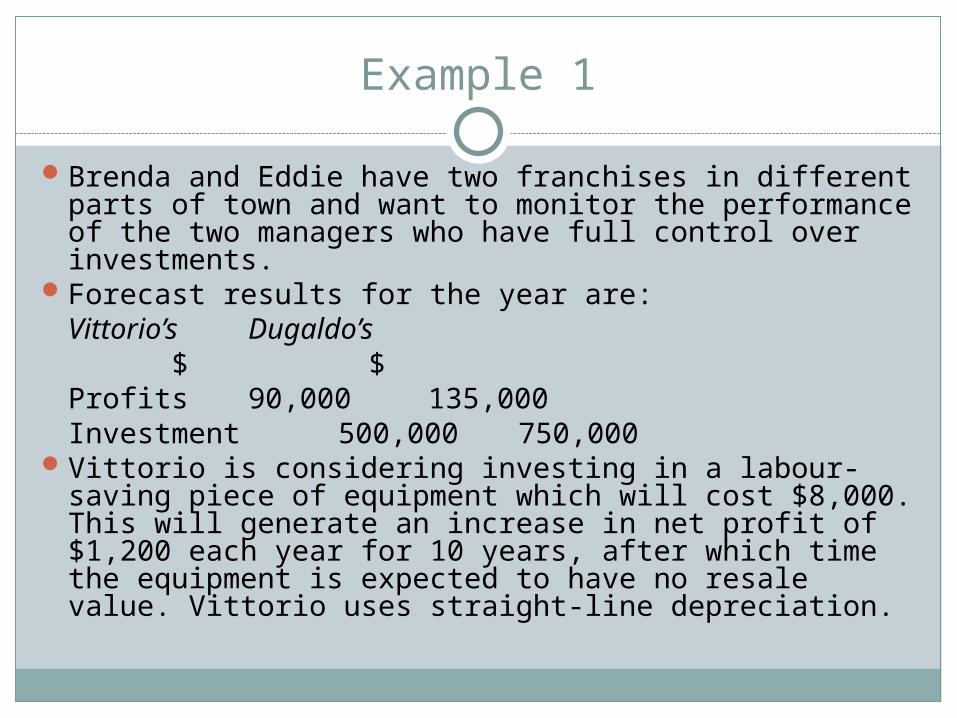

Brenda and Eddie have two franchises in different parts of town and want to monitor the performance of the two managers who have full control over investments.

Forecast results for the year are:Vittorio’s Dugaldo’s $ $

Profits 90,000 135,000Investment 500,000 750,000

Vittorio is considering investing in a labour-saving piece of equipment which will cost $8,000. This will generate an increase in net profit of $1,200 each year for 10 years, after which time the equipment is expected to have no resale value. Vittorio uses straight-line depreciation.

Example 1 (cont’d)

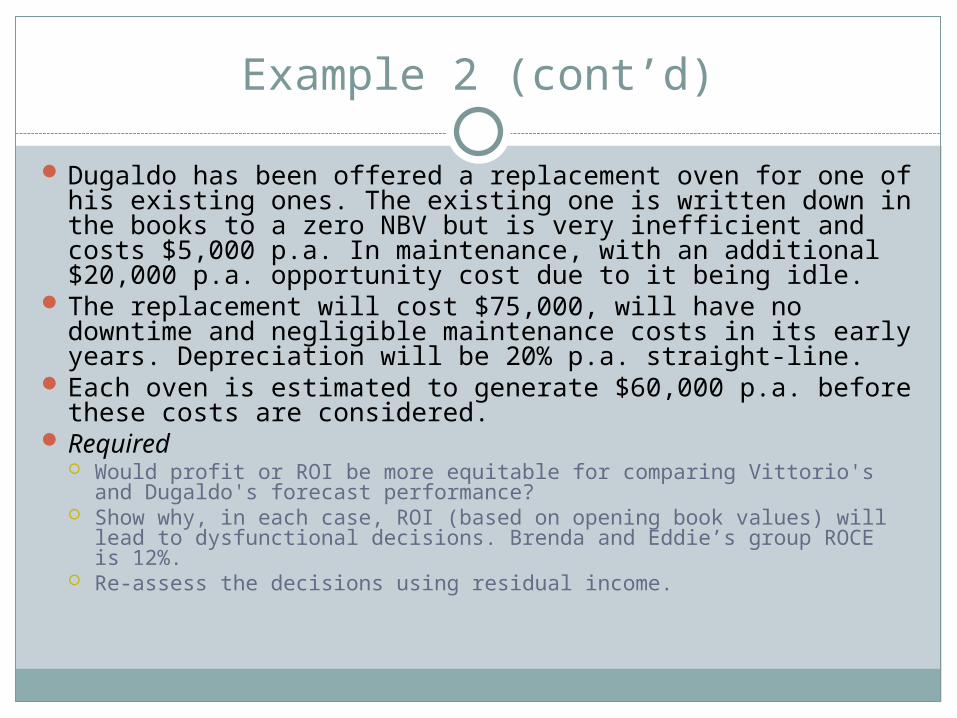

Dugaldo has been offered a replacement oven for one of his existing ones. The existing one is written down in the books to a zero NBV but is very inefficient and costs $5,000 p.a. In maintenance, with an additional $20,000 p.a. opportunity cost due to it being idle.

The replacement will cost $75,000, will have no downtime and negligible maintenance costs in its early years. Depreciation will be 20% p.a. straight-line.

Each oven is estimated to generate $60,000 p.a. before these costs are considered.

Required Would profit or ROI be more equitable for comparing Vittorio's

and Dugaldo's forecast performance? Show why, in each case, ROI (based on opening book values) will

lead to dysfunctional decisions. Brenda and Eddie’s group ROCE is 12%.

Answer

Residual income

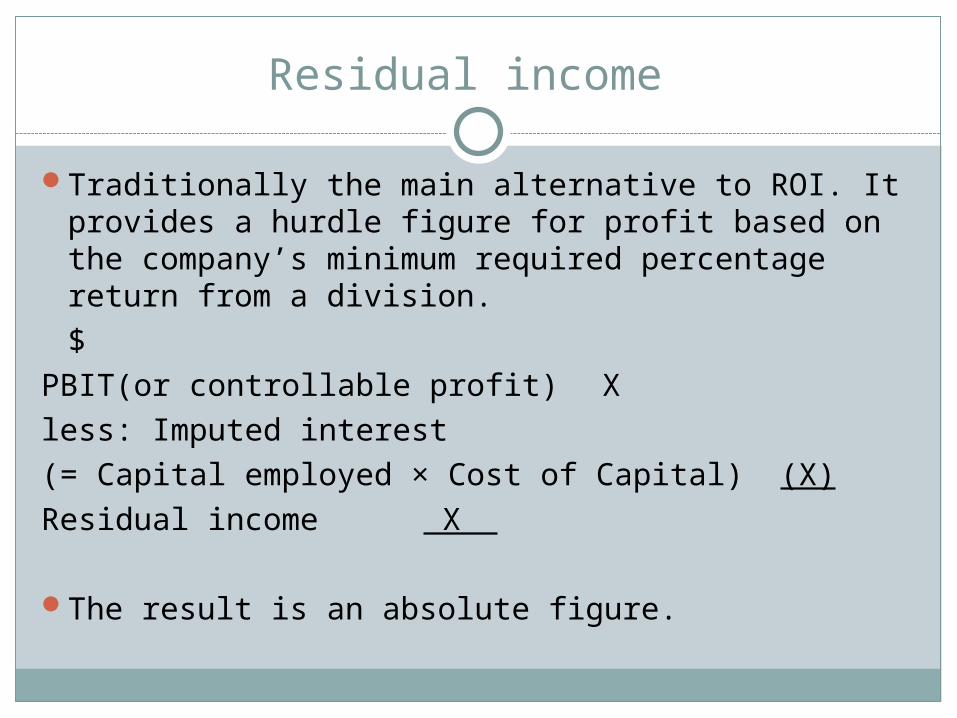

Traditionally the main alternative to ROI. It provides a hurdle figure for profit based on the company’s minimum required percentage return from a division.

$PBIT(or controllable profit) Xless: Imputed interest(= Capital employed × Cost of Capital) (X)Residual income X

The result is an absolute figure.

Example 2

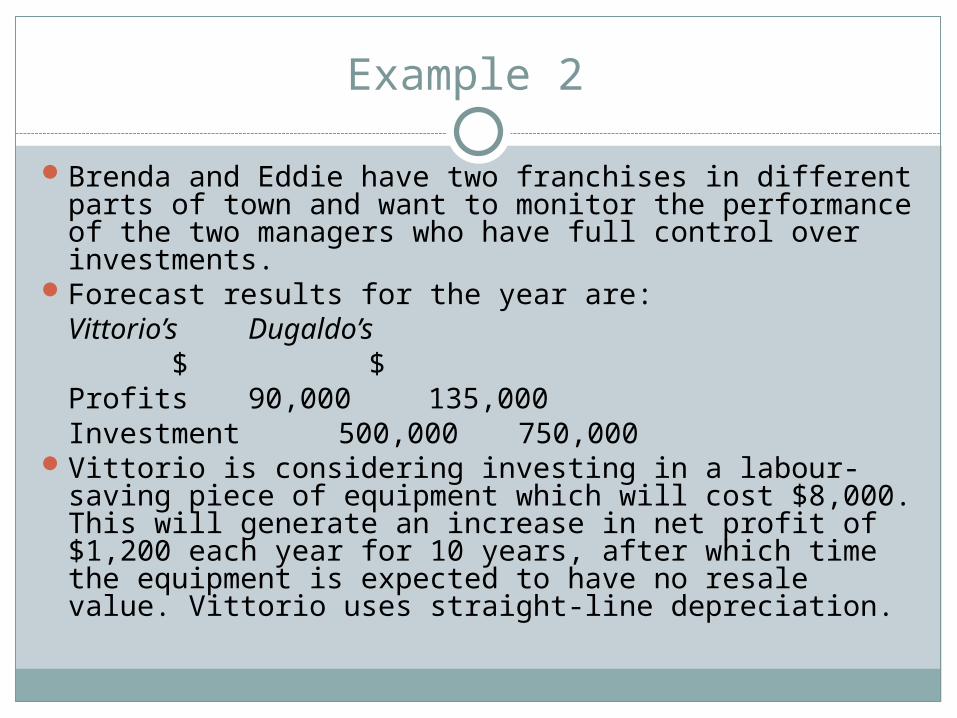

Brenda and Eddie have two franchises in different parts of town and want to monitor the performance of the two managers who have full control over investments.

Forecast results for the year are:Vittorio’s Dugaldo’s $ $

Profits 90,000 135,000Investment 500,000 750,000

Vittorio is considering investing in a labour-saving piece of equipment which will cost $8,000. This will generate an increase in net profit of $1,200 each year for 10 years, after which time the equipment is expected to have no resale value. Vittorio uses straight-line depreciation.

Example 2 (cont’d)

Dugaldo has been offered a replacement oven for one of his existing ones. The existing one is written down in the books to a zero NBV but is very inefficient and costs $5,000 p.a. In maintenance, with an additional $20,000 p.a. opportunity cost due to it being idle.

The replacement will cost $75,000, will have no downtime and negligible maintenance costs in its early years. Depreciation will be 20% p.a. straight-line.

Each oven is estimated to generate $60,000 p.a. before these costs are considered.

Required Would profit or ROI be more equitable for comparing Vittorio's and

Dugaldo's forecast performance? Show why, in each case, ROI (based on opening book values) will lead

to dysfunctional decisions. Brenda and Eddie’s group ROCE is 12%. Re-assess the decisions using residual income.

Answer

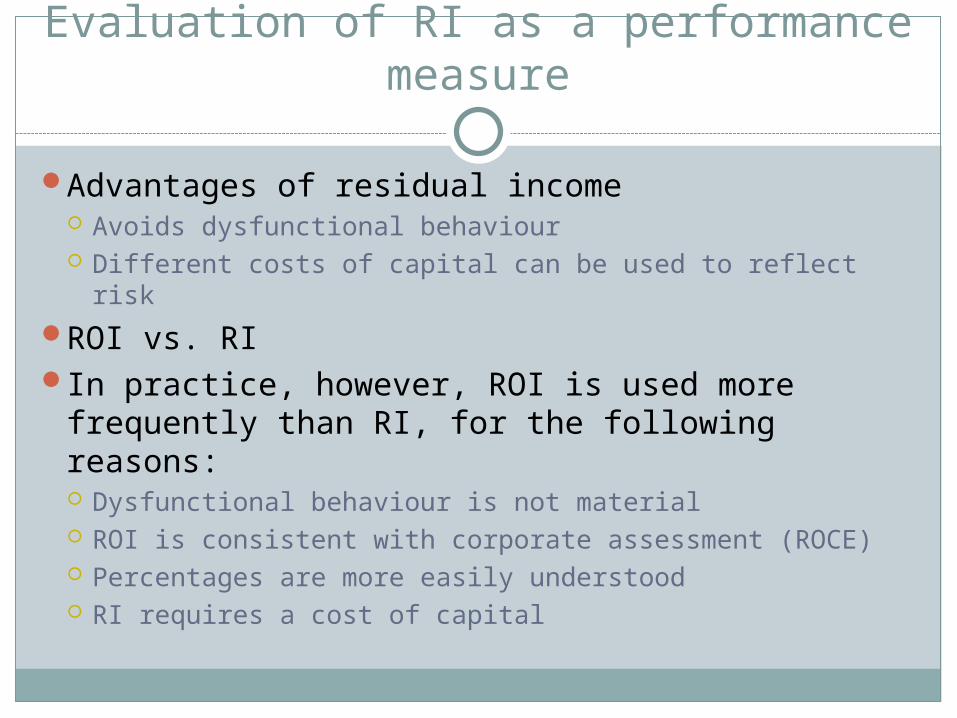

Evaluation of RI as a performance measure

Advantages of residual income Avoids dysfunctional behaviour Different costs of capital can be used to reflect risk

ROI vs. RIIn practice, however, ROI is used more

frequently than RI, for the following reasons: Dysfunctional behaviour is not material ROI is consistent with corporate assessment (ROCE) Percentages are more easily understood RI requires a cost of capital

Example 3

Discuss the strengths and weaknesses of ROI and RI as methods of assessing the performance of divisions.

Answer

Economic value added (EVA)

EVA is similar, but superior, measure to RI.It is directly linked to the creation of

shareholder wealth and is calculated as follows:NOPAT Xless: Economic value of capital employed x WACC (X)EVA X

Note: WACC = weighted average cost of capital

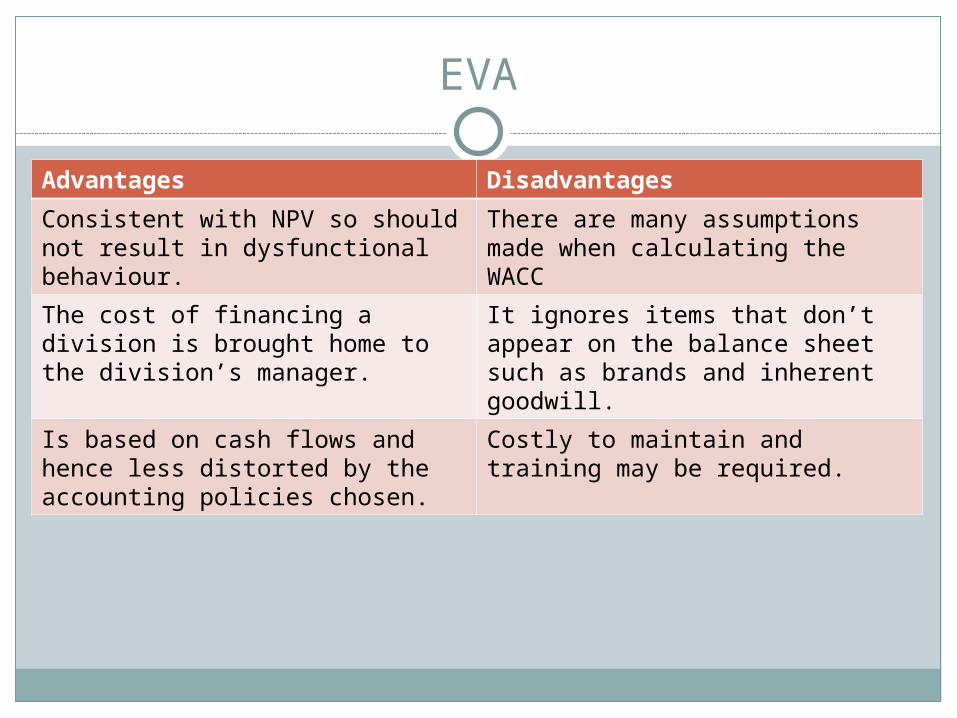

EVA

Advantages Disadvantages

Consistent with NPV so should not result in dysfunctional behaviour.

There are many assumptions made when calculating the WACC

The cost of financing a division is brought home to the division’s manager.

It ignores items that don’t appear on the balance sheet such as brands and inherent goodwill.

Is based on cash flows and hence less distorted by the accounting policies chosen.

Costly to maintain and training may be required.

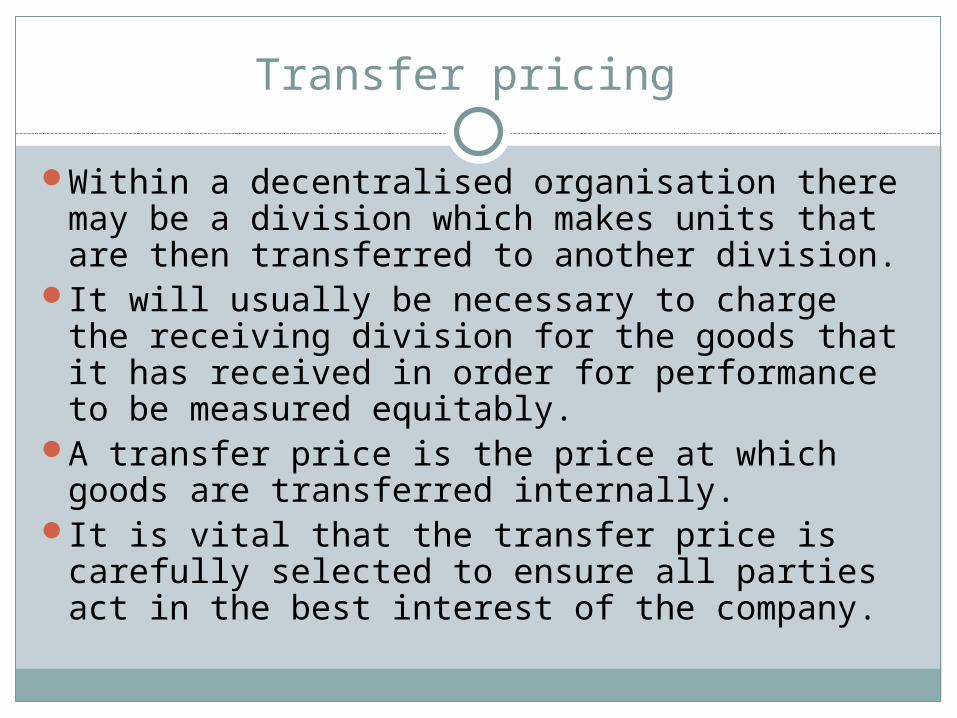

Transfer pricing

Within a decentralised organisation there may be a division which makes units that are then transferred to another division.

It will usually be necessary to charge the receiving division for the goods that it has received in order for performance to be measured equitably.

A transfer price is the price at which goods are transferred internally.

It is vital that the transfer price is carefully selected to ensure all parties act in the best interest of the company.

Transfer price

The goals of a transfer pricing system are: Goal congruence Equitable performance measurement Retain divisional autonomy Motivate divisional managers Optimum resource allocation

Transfer pricing in practice

Market based approaches If an external market exists for transferred goods (and

there is unsatisfied demand externally), the transfer price can be set as the external market price.

The selling division will earn at least the same profit on internal sales as external sales, the receiving division will pay a commercial price and both divisions will have their profit measured in an equitable way. The managers of both divisions will behave in a goal congruent way.

If savings are made by selling internally then this may be reflected in the transfer price, e.g. by offering a discount equivalent to saved transport costs.

Example 4

What are the advantages and disadvantages of a market-based approach?

Answer

Transfer pricing in practice

Cost based approaches The idea behind these approaches are similar to those involved

in manufacturing accounts, that is to say the supplying division has its costs of manufacturing refunded and is also given a profit margin to encourage the transfer.

Actual cost vs. standard cost Use of actual costs would result in: all inefficiencies passed on to buying division no encouragement for cost control in selling division buying division does not know in advance what price it will be

paying performance measurement is therefore difficult

Using standard costs overcomes all these problems.

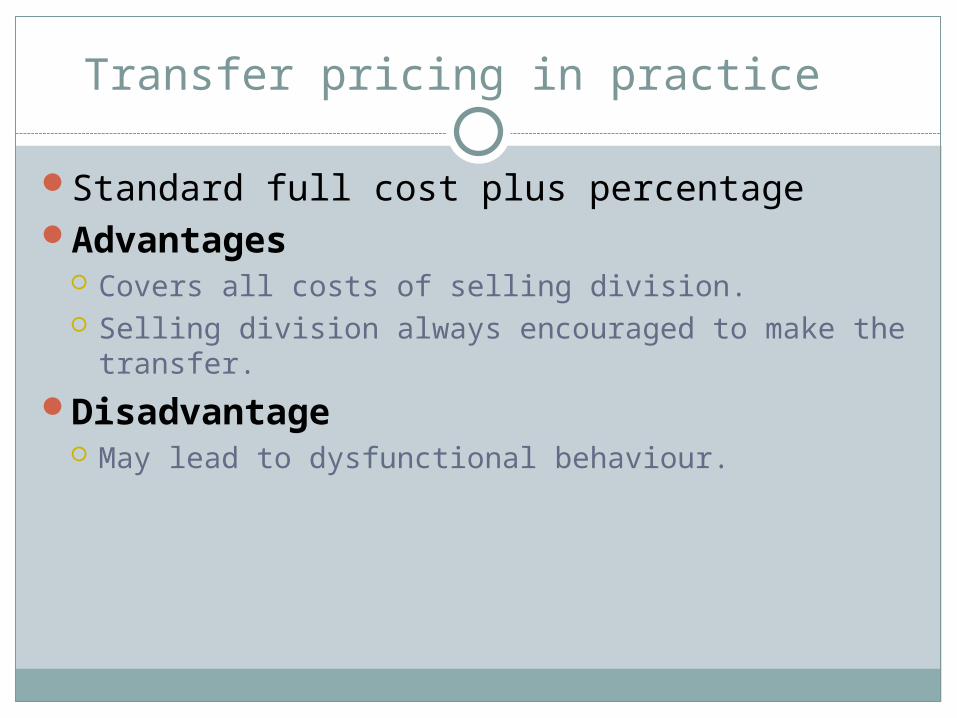

Transfer pricing in practice

Standard full cost plus percentageAdvantages

Covers all costs of selling division. Selling division always encouraged to make the

transfer.

Disadvantage May lead to dysfunctional behaviour.

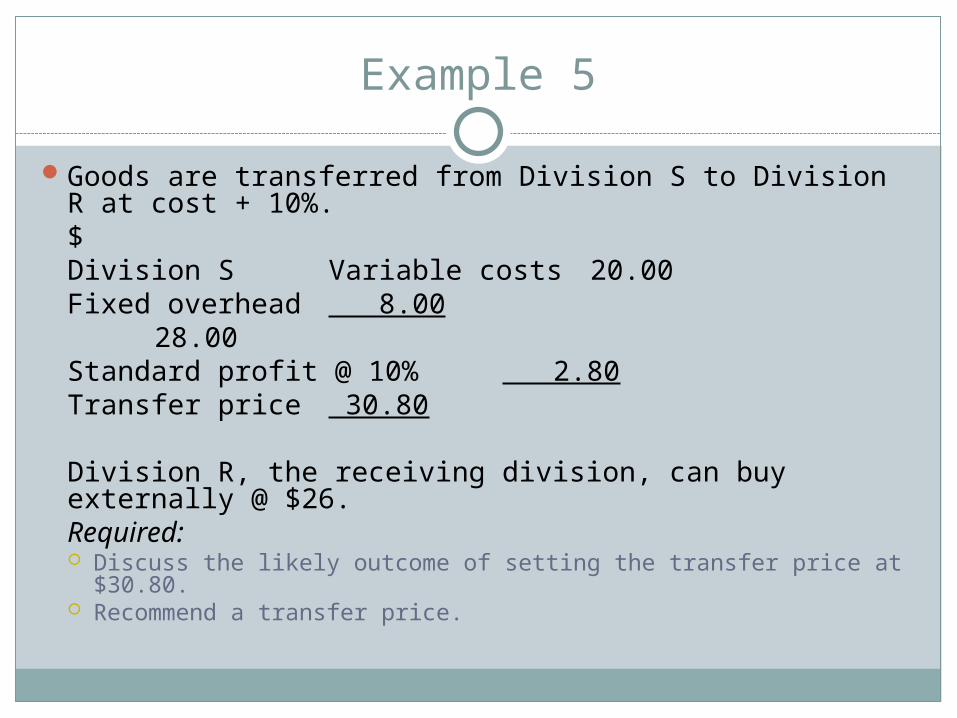

Example 5

Goods are transferred from Division S to Division R at cost + 10%.

$Division S Variable costs 20.00

Fixed overhead 8.00 28.00

Standard profit @ 10% 2.80Transfer price 30.80

Division R, the receiving division, can buy externally @ $26.Required: Discuss the likely outcome of setting the transfer price at $30.80. Recommend a transfer price.

Answer

Transfer pricing in practice

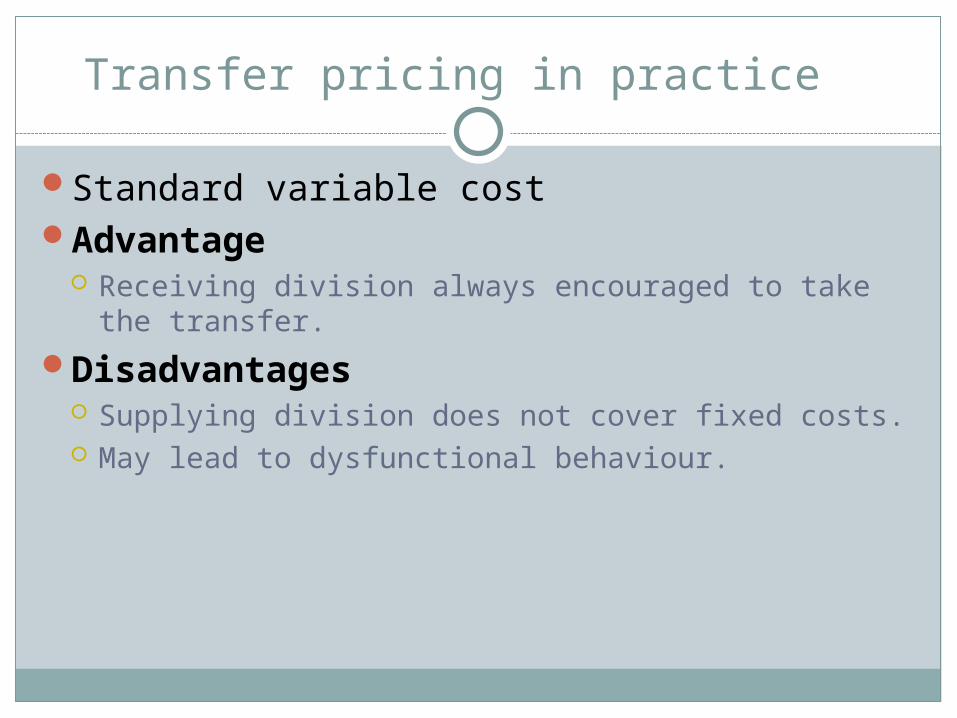

Standard variable costAdvantage

Receiving division always encouraged to take the transfer.

Disadvantages Supplying division does not cover fixed costs. May lead to dysfunctional behaviour.

Opportunity cost based approach to transfer pricing

Minimum transfer price = marginal cost to selling division + opportunity cost to selling division

Maximum transfer price = external purchase price If external market for intermediate product, opportunity

cost = contribution foregone If no external market, the opportunity cost is likely to be

nil. (Beware of situations when the company is at full capacity on

another task.)Opportunity cost-based approaches should

always result in goal congruent behaviour.

Example 6

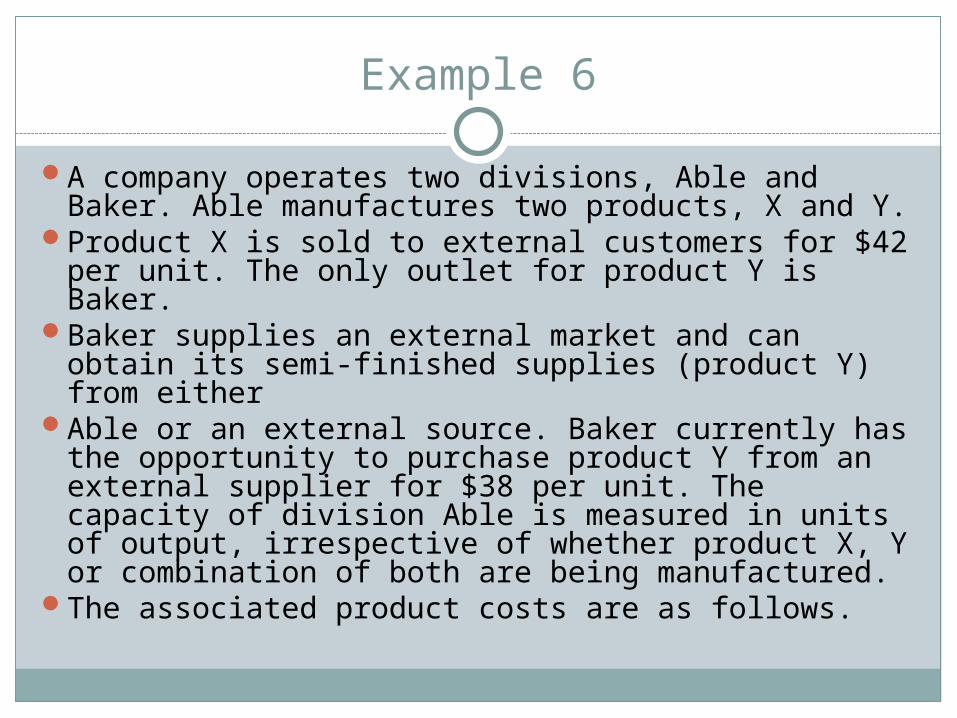

A company operates two divisions, Able and Baker. Able manufactures two products, X and Y.

Product X is sold to external customers for $42 per unit. The only outlet for product Y is Baker.

Baker supplies an external market and can obtain its semi-finished supplies (product Y) from either

Able or an external source. Baker currently has the opportunity to purchase product Y from an external supplier for $38 per unit. The capacity of division Able is measured in units of output, irrespective of whether product X, Y or combination of both are being manufactured.

The associated product costs are as follows.

Example 6 (cont’d)

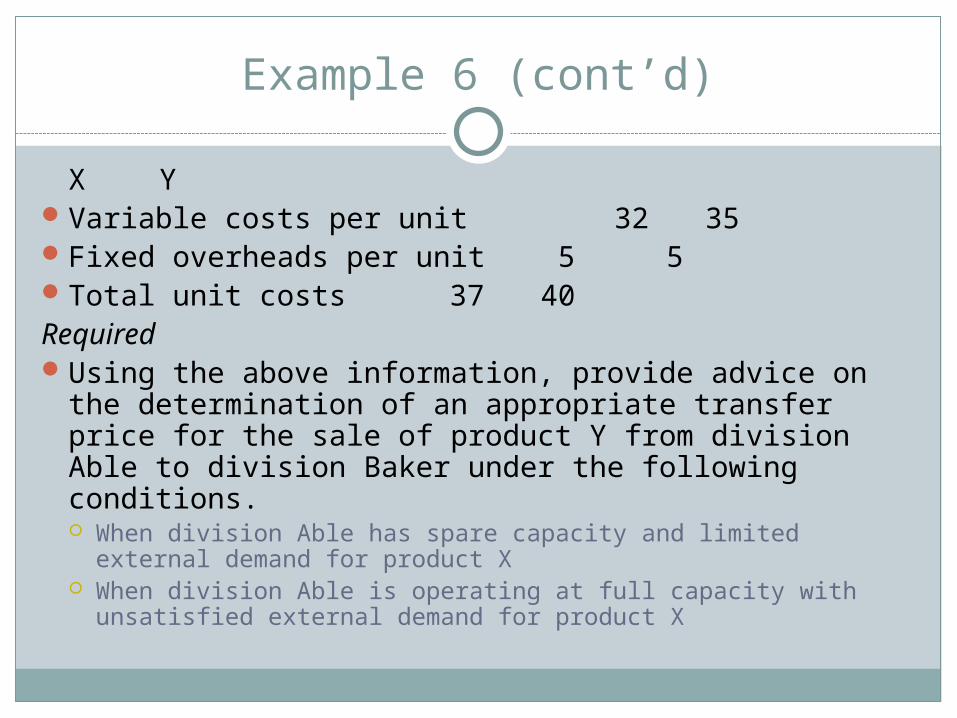

X YVariable costs per unit 32 35Fixed overheads per unit 5

5Total unit costs 37 40RequiredUsing the above information, provide advice on the

determination of an appropriate transfer price for the sale of product Y from division Able to division Baker under the following conditions. When division Able has spare capacity and limited external

demand for product X When division Able is operating at full capacity with unsatisfied

external demand for product X

Answer

Transfer pricing

Head office intervention In practice, companies tend to employ a system

whereby, broadly, the production plan is imposed by head office and transfers are made using cost information from within the company i.e. transfers are made at cost plus a profit element.

Advantage of head office imposed plan: No problems need arise (goal congruence).

Disadvantages of head office imposed plan: Loss of autonomous divisional decision-making power De-motivating

Imperfect market When units costs and revenues are not constant but vary with

output careful analysis will need to be undertaken to establish the output that will maximise profit for the group and then the transfer price that will maximise profit in both divisions.

Example 7

Furniture Co is a large company that manufactures and sells furniture. It has three divisions:

Division A purchases logs and produces finished planks. Approximately 2/3 of its output is sold to

Division B, with the remainder sold externally. Division B manufactures furniture. The policy of Furniture Co is that the

Division B must buy all its timber from Division A and sell all its output to Division C.

Division C sells furniture to outlets. It only sells items purchased from Div B.

Currently return on investment (ROI) is used to assess divisional performance. Each division adopts a cost-plus pricing policy for all external and internal sales. The senior management of Furniture Co has stated that the divisions should consider themselves to be independent businesses as far as possible.

Required: For each division suggest, with reasons, the behavioural consequences that

might arise as a result of the current performance evaluation methods. Suggest with reasons, an appropriate transfer pricing policy that could be

used for transfers from Division B to Division C, indicating any problems that may arise as a consequence of the policy you suggest.

Answer

Example 8

AJH Ltd has two divisions. Division 1 manufactures a component called the Woody which it

sells on the external market as well as transferring to Division 2. Division 2 then sells the Woody after further processing as the Woody Deluxe.

The following information is available:Division 1 Division 2

Market price Woody 150Market price Woody Deluxe 300Production costs 60 80Non-production overheads 150,000 150,000External demand 5,000 3,000

75% of the production cost per component is variable.Division 1 sets a transfer price of marginal cost plus 40%.

Required: Calculate the profit generated by each division.

Answer

End of Lecture

Questions?