Divisional Performance Measurement- An Examination of the Potential Explanatory Factors

description

DIVISIONAL PERFORMANCE MANAGEMENT

Centralised Organizational Structure

• When major activities of a company are few & closely interrelated then centralised organization structure is more easily managed.

• All activities within a company are placed under the control of departmental heads.

• · These are p(roduction, marketing, finance, HR and admin, procurement and research and development.

• · Pricing, product mix and output decisions will be made by central management

• functional Organization none of the members of the 5 departments is responsible for more than a part of the processes.

• Production dept. is responsible for manufacturing of products at minimum cost & of standard quality & on time delivery.

• Marketing dept is responsible for making sales at market price • Purchasing dept is responsible for purchasing supplies & so on

but no one is responsible for the total profit of the company• . Revenue & cost including cost of investment are combined

together at CEO level, which is classified as an investment centre• Marketing function is revenue centre & rest of the dept are cost

centres.

2. PRE-REQUISITES FOR SUCESSFUL DIVISIONLIZATION

• FUNCTIONAL AND DIVISONLIZED ORGANIZATIONAL STRUCTURE

• suited to company’s engage in several dissimilar activities.• It is difficult for top management to be intimately acquainted with all the

diverse activities of various segments of the busines • It is appropriate to divide a company into separate segments or divisions and

to allow managers to operate with a great deal of independence will lead to the decision making process for instance divisional managers will normally be free to set selling prices, in which market to sale ,make product mix ,setting credit terms,advertising ,output decisions and select suppliers(this may include buying from other divisions within the company or from outsiders)

• Each divisional manager is responsible for all of the operations relating to particular product

Manager responsible for generating revenues, controlling cost and earning a satisfactory return on the capital invested in their operations• To meet the true requirements of a divisionalises profit centre a division

should be able to save majority of its output to outside customers & free to choose the sources of supply.

• The autonomous division is that managers might not pursue goals that are in the best interest of the company as a whole.

• Consider financial performance measures that will motivate pursue those goals that will best benefit the company as a whole

3. PROFIT CENTRES AND INVESTMENT CENTRES

Investment Centres:authority to make decisions on source of supply & choice of markets & make capital expenditure decisions. Division

is known as an investment centre.

• Profit Centre:•

A manger can't control investments & is responsible for the profits earned from the fixed assets assigned to him by the corporate head quarters the segment is known as profit centre.

• The divisional managers have profit loss responsibility

• Transfer prizes are assigned to the product transfer between the divisions.

• Separate profits can be reported for each division but manager have limited authority for sourcing and prizing decisions

• A divisonlized profit center should be able to sale the majority of its output to outside customers and free to choose the source of supplies.

• Cost Centre: used to describe a responsibility centre in a conventional isational structure where a manager is responsible for cost but not profit.

• 4. Disadvantages:•

Divisions take actions which will increase their divisional profits at the expense of the profits of other divisions.

•Not achieving over all Organization goals of the company may lead to a reduction in total company profits.

•Cost of activities that are common to all divisions like finance, administration, IT, HR may be greater for a divisionalised structure than for a centralised structure because for each division seperate services are required.

•Top management loses control, However, good performance evaluation together with appropriate MIS top management able to control decentralised operation.

21. ADVANTAGES OF DIVISIONALIZATION

• Decision can be made by the person who is familiar with the situation and make more informed judgments than central management,

• Decision can be made on the spot by the manager who are familiar with the product lines and production process.

• · Improve motivation and efficiency and will increase not just at the divisional management level but throughout the whole division,

• Free top management from detail involvement in day to day operations and enables them to devote more efforts to strategic plans.

• Excellent training oppurtunities for future members of top management by enabling them to acquire skills and experience.

• provide greater freedom to the manager thus, making their activities more challenging.•

managers of profit centres feel great job satisfaction than the managers of cost centres.•

Top management are not involved in day to operations which makes them devoted to more effort & strategic planning.

• DISADVANTAGE DIVISIONALIZATION• · Divisions may compete with each other, manager take action

which will increase their own profits at the cost of other divisions• · Lead to affect the overall company goals and reduction in total

company profits.• · Top management assess additional benefits will exceed the

additional cost.• · Cost of common activities to a divisionalized structure is greater

than a centralized structure. centralized accounting function may be less costly as compare to separate accounting function for each division.

• 5. Economic Performance Of The Division:• To evaluate divisional managerial performance then only those

items directly controllable by him should be included in the profitability major.

• All allocation of indirect cost i.e. central service & administration cost which can't be controlled by the divisional manager. So, exclude such cost.

•Such cost can only be controlled by the central service managers. So, they should be held accountable.

6. Division Profit Measures:• 1.Return on investment • ROI is the most widely used financial measure of divisional performance• ROI is similar to ARR.• ROI express divisional profit as a % of the assets employed in the division• Net operating income is income before interest and taxes EBIT (earnings before interest

and tax• . Operating assets include cash, accounts receivable, inventory, plant and equipment• Non operating assets include land held for future use, an investment in another company• Average of the operating assets between the beginning and the end of the year.• Most companies use the net book value to calculate average operating assets.• An asset’s net book value decreases over time as the accumulated depreciation

increases.Consequently, ROI increases • Replacing old equipment with new equipment increases book value of assets and

decreases ROI.• An alternative is gross cost of the asset, constant over time because depreciation is

ignored;

• Corporate management will see whether the returns earned on the capital investment in a division exceeds the division's opportunity cost of capital.

• Margin and turnover are very important concepts. • Margin is ordinarily improved by increasing sales or reducing operating expenses,• ROI. can be compared to the returns of other investment centers in the

organization,• it is subject to the following:• Manager take actions that increase ROI in the short run but harm the company in

the long run such as cutting back on research and development• Manager may reject investment opportunities that are profitable for the whole

company but that would have a negative impact on the manager’s performance.• Committed costs may be relevant in assessing the performance of the business

segment but difficult to fairly assess the performance of the manager.

Residual income• To overcome disadvantages of ROI the residual income approach can be used• It is defined as a controllable contribution less a cost of capital charge on the

investment controllable by the divisional manager.• Residual income measure the managerial performance of investment centre.• Managers will be encouraged to protect their interests and also to act in the

best interest of the company.• Residual income measure risk adjusted capital cost to be incorporated where

as the ROI ignores.• Residual income suffers from the disadvantage of being absolute measures for

example , a large division is more likely to earn a larger residual income than a small division

• In the case of profit centers, managers are not authorized to make capital investment decisions .Therefore R I is not calculated

• In case of investment centre or profit centre mangers can significantly influence the investment in the working capital ,ROI appears to be an un satisfactory method and residual income is preferable

• Residual income of division x will increase and that of division Y will decrease.

• If both managers accept the project, the manager of division X would invest where as the manager of division Y would not and these decisions are in the best interest of the company as a whole

• Residual income encourage both managers to make the correct asset disposal decision

• 7. TRACEABLE FIXED COST:• Only the traceable fixed costs are charged to particular segments.

If a cost is not traceable to a segment, then it is not assigned. • A traceable fixed cost of a segment is a fixed cost that is incurred

because of the existence of the segment if the segment were eliminated, the fixed cost would disappear.

• Examples of traceable fixed costs include:• • The salary of the Fritos product manager at PepsiCo is a

traceable fixed cost of that segment• The maintenance cost for the building in which Boeing 747s are

assembled is a traceable fixed cost of that segment.

• Inappropriate Methods for Assigning Traceable Costs among Segments• In addition to omitting costs, many companies do not correctly handle

traceable fixed expenses on segmented income statements.• First, they do not trace fixed expenses to segments even when it is

feasible to do so. • Second, they use inappropriate allocation bases to allocate traceable

fixed expenses to segments. • Costs that can be traced directly to a specific segment should be charged

directly to that segment and should not be allocated to other segments. • For example, the rent for a branch office of an insurance company

should be charged directly to the branch office rather spread throughout the company

• COMMON FIXED COST:• Is a fixed cost that supports the operations of more than one

segment, but is not traceable in whole or in part to any one segment. Even if a segment were eliminated, there would be no change in a true common fixed cost.

• For example: • The salary of the CEO of General Motors is a common fixed cost of the various divisions of the company. •

• . • The cost of the receptionist’s salary at an office shared by a number of doctors is a common fixed cost of the doctors. The cost is traceable to the offi ce, but not to individual doctors.

• .

• ARBITRARY ALLOCATION OF FIXED COST: • For example, some companies allocate selling and administrative expenses on the

basis of sales revenues. • Thus, if a segment generates 20% of total company sales, it would be allocated 20%

of the company’s selling and administrative expenses as its “fair share.”. • For example, sales should be used to allocate selling and administrative expenses

only if a 10% increase in sales will result in a 10% increase in selling and administrative expenses.

• Costs should be allocated to segments if it is highly correlated with the real cost driver).

• Nestle, Switzerland , has been working to overcome inefficiencies resulting from its decentralized management structure.

• For example, “each candy and ice cream factory was ordering its own sugar Nestle hopes to significantly reduce costs and simplify recordkeeping by centralizing its raw materials purchases

• SEGMENT MARGIN:• Segment margin is obtained by deducting traceable fi xed cost from the contribution margin.• It represents the margin available after a segment has covered all of its own costs. • Best judge of the long-run profitability of a segment it considers those costs that are caused by

the segment. • If a segment can’t cover its own costs, then it should be dropped •

COST ASSIGNED TO A SEGMENT:• From research and development, to product design, manufacturing, marketing, distribution, and

customer service, are required to bring a product or service to the customer.• The distinction between traceable and common fi xed costs is crucial because traceable fixed

costs are charged to segments and common fixed costs are not• Many organizations now integrate financial measures such as ROI and residual income in a

coordinated system of performance measures known as a balanced scorecard. 529 Balanced•

Segmented income statements provide information for evaluating the profitability and performance of divisions, product lines, sales territories, and other segments of a company.

• 25. ALTERNATIVE DIVISIONAL PROFIT MEASURES• Where a division is a profit centre, depreciation is not a

controllable cost since the manager does not have authority to make capital investment decisions.

• Depreciation is a controllable expense for an investment centre in respect of those assets that are controllable by the divisional manager.

• Controllable contribution is the most appropriate measure of a divisional manager performance because it measures the ability of managers to use the resources under their control effectively

• It should be evaluated relative to a budget performance so that market conditions can be taken into account.

• 26.CONTROLLABLE AND UNCONTROLLABLE COST• Depreciation of divisional assets and head office finance and legal staff assigned to

providing services for specific divisions would fall into this category, these expenses can be avoided if a decision were taken to close the division.

• EXAMPLE:• Suppose manager of division X has an asset that generates a return of 19% and the

manager of division Y has asset that yield a return of 12%• The manager of division X can increase ROI by disposing off the assets where as the

ROI of division Y will decline if the asset is sold.• Asset disposal appropriate where assets earn a return less than the cost of capital• Assets in division X should be kept and divisions Y asset sold• Both managers can increase their ROI by making decisions that are not n the best

interest of the company.

• 29. ADDRESSING THE DIVERSE FUNCTIONAL CONSEQUENCES OF SHORT TERM FINANCIAL PERFORMANCE MEASURES

• The prime objective of a company is to maximize the share holder value• In the stock exchanges ,the share prize are derived considering the companys

performance as a whole and not at the segmental level .• Using ARR as performance measures can encourage managers to become short term

oriented decisions i.e. is by rejecting profitable long term investment• By not making investment in profitable products they can reduce current period cost.• Manager can boost their performance measure in a particular period by destroying

customer and employee good will• For instance, force employees to work excessive towards the end of measurement period

so that maximum goods can be sold .to maximize short term profitability.This effect quality of goods, customer satisfaction, future sales and de-motivation and increased labour turn over

• Where two divisional managers have same amount of investment and produce same ROI it does not mean that their performance is the same

• One manager may have build up customer good will by offering excellent service and also paid great attention to training education research and development

• While another may not have given these items any consideration

• DISTINGUISHING BETWEEN THE MANAGERAL AND ECONOMIC PERFORMANCE OF THE DIVISION

• · A manager may be assigned to an aligned division to improve performance and succeed in improving the performance of the division but the division still is unprofitable due to industry factors such as over capacity and a decline market. The future of division might be uncertain but manager promoted due to good performance

• · Conversely a division report significant profits but due to management deficiencies, the performance may still be un satisfactory provided favorable economic environment is taken into account

• · To evaluate the divisional manager than only those items directly controllable by the manager should be included in the performance measure.

• · Allocation of indirect cost including central administration cost which cannot be controlled by the divisional manager, such cost not to be included in performance measure. These costs can only be controlled where they are incurred.

• A balanced scorecard is an integrated system of performance measures designed to support an organization’s strategy.

• The various measures in a balanced scorecard should be linked on a plausible cause-and-effect basis from the very lowest level up through the organization’s ultimate objectives.

• A theory about how specific actions taken by various people in the organization will further the organization’s objectives.

• The theory should be viewed as tentative and subject to change if the actions do not in fact result in improvements in the organization’s financial and other goals.

• If the theory changes, then the performance measures on the balanced scorecard should also change.

• The balanced scorecard is a dynamic measurement system that evolves as an organization learns more about what

• In profit centre depreciation is not a controllable cost since manager has no authority to make capital investment.• Depreciation should be controllable expense for an investment centre in respect of assets, controlled by the manager•

Controllable contribution is appropriate major since it major the ability of a manager to use the resources under their control.

•Where a manager is not bound to receive services from within the company the expense is clearly controllable

•Where division has no choice but to accept head office cost. This can be regarded as non controllable over heads.

•Those overheads that are attributable to a division and which would be avoided if the division was closed are deducted from the controllable contribution to drive the true divisional contribution

• If the division is independent it would have to incur the cost of these services performed by the head office as well because division would have to incur if treated as a separate company

•Companies may prefer to use divisional net profit when comparing the economic performance of a division with the similar companies

• Factors influencing companies to allocate the cost of shared resources to divisions are attributed to the following:

-To show total cost for operating a division.- Such cost incurred and must be charged to division.- would incur such cost if they were independent unit bear full business risk as being the part of the company

• 27.RETURN ON INVESTMENT (ROI)• A situation where division A earn a profit $1 million and division B a profit of $2million. Can we conclude that

division B is more profitable than division A.?• The answer is no• Since we should consider whether are returning a sufficiently high return on the capital invested in he division.• Suppose that 4 million capitals are invested in division A and 20 million in division B.• DIVISION A’S ROI is 25% and for B is 10%.• The corporate management will see the return earned on a particular division exceed the division opportunity

cost of capital (i.e. returns available from the alternative use of the capital.)• Suppose the return available on similar investment to that in division B is 15% than the performance B is

questionable. If profitability cannot be improved ROI suggest that division A is very profitable.• Another feature of the ROI is that it can be used a common denominator for comparing the returns of dissimilar

businesses such as other divisions with in the group or outside competitors.• It is widely used for many years in all types of organizations so that most managers understand and consider it

to be of considerable importance• Despite widely used there are a number of problems exists when this measure is used for example divisional

ROI can be increased by actions that will make the as a whole verse of and conversely actions that decrease the divisional ROI but make the company as whole better off.

• In other evaluating divisional managers on the basis of ROI may not encourage goal objective

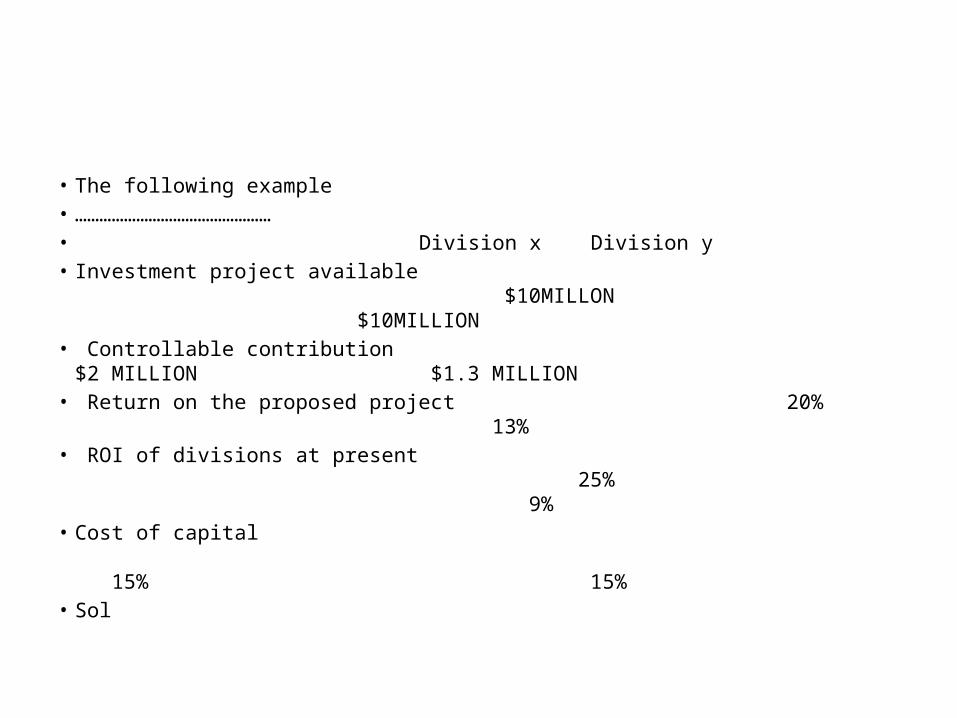

• The following example• …………………………………………• Division x Division y• Investment project available $10MILLON

$10MILLION• Controllable contribution $2 MILLION $1.3

MILLION• Return on the proposed project 20% 13%• ROI of divisions at present 25%

9%• Cost of capital 15%

15%• Sol

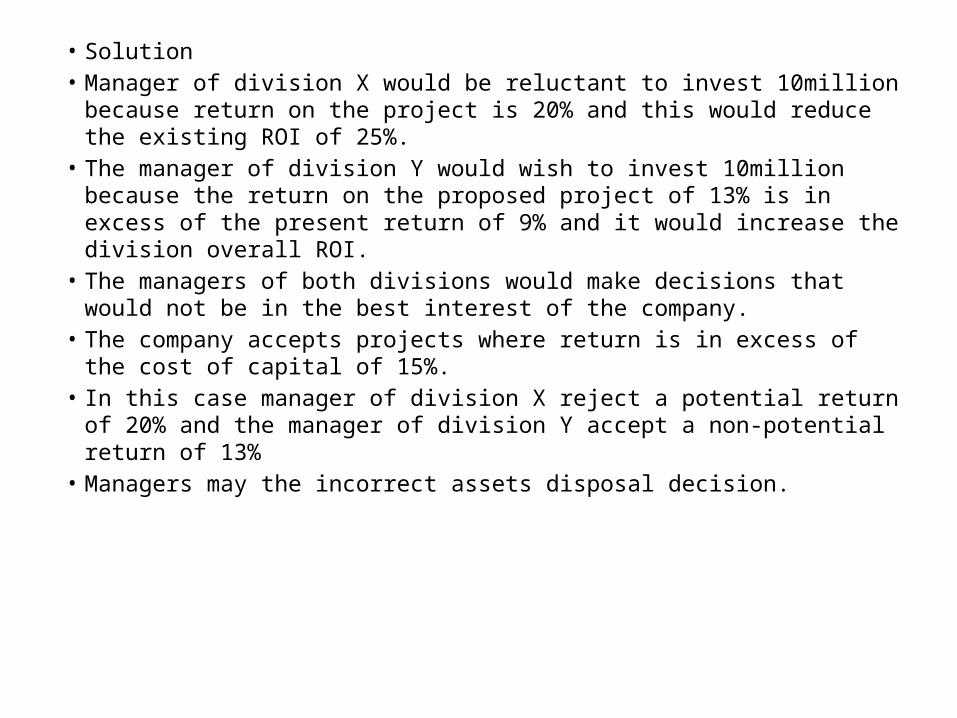

• Solution• Manager of division X would be reluctant to invest 10million because return

on the project is 20% and this would reduce the existing ROI of 25%.• The manager of division Y would wish to invest 10million because the

return on the proposed project of 13% is in excess of the present return of 9% and it would increase the division overall ROI.

• The managers of both divisions would make decisions that would not be in the best interest of the company.

• The company accepts projects where return is in excess of the cost of capital of 15%.

• In this case manager of division X reject a potential return of 20% and the manager of division Y accept a non-potential return of 13%

• Managers may the incorrect assets disposal decision.