Le prospettive dell’Economia Mondiale ed Europea · Le prospettive dell’Economia Mondiale ed...

29

Le prospettive dell’Economia Mondiale ed Europea July 6, 2015 Emilio Rossi EconPartners Oxford Economics [email protected] [email protected]

Transcript of Le prospettive dell’Economia Mondiale ed Europea · Le prospettive dell’Economia Mondiale ed...

Le prospettive dell’Economia Mondiale ed Europea

July 6, 2015

Emilio Rossi EconPartners Oxford Economics

2

Real GDP Growth Compound annual growth rates, in %

Source: EconPartners calculations on Oxford Economics data

CA

GR

, in

%

-1

2

4

7

10

Japan NAFTA Emerging Asia

2003-2007 2007-2014 2014-2018

AE recovering after 2008 crisis, EM slowing

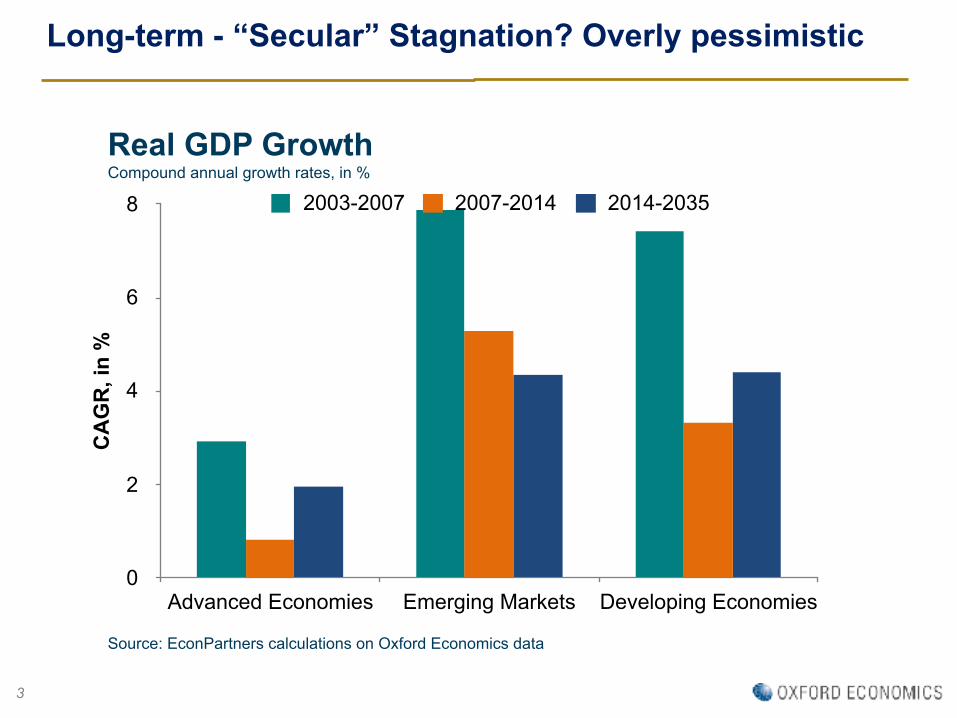

Long-term - “Secular” Stagnation? Overly pessimistic

Real GDP Growth Compound annual growth rates, in %

Source: EconPartners calculations on Oxford Economics data

3

CA

GR

, in

%

0

2

4

6

8

Advanced Economies Emerging Markets Developing Economies

2003-2007 2007-2014 2014-2035

Main factors driving low growth in the long-term

4

Share of World GDP – Technical progress vs demography

0,0

10,0

20,0

30,0

40,0

50,0

60,0

70,0

80,0

90,0

1000 1500 1820 1913 1950 2006 2012 2017 2030

Avanzati Emergenti

Source: Calculations Giovannini on A. Maddison, 2001, Groningen University data

5

Advanced Emerging

6

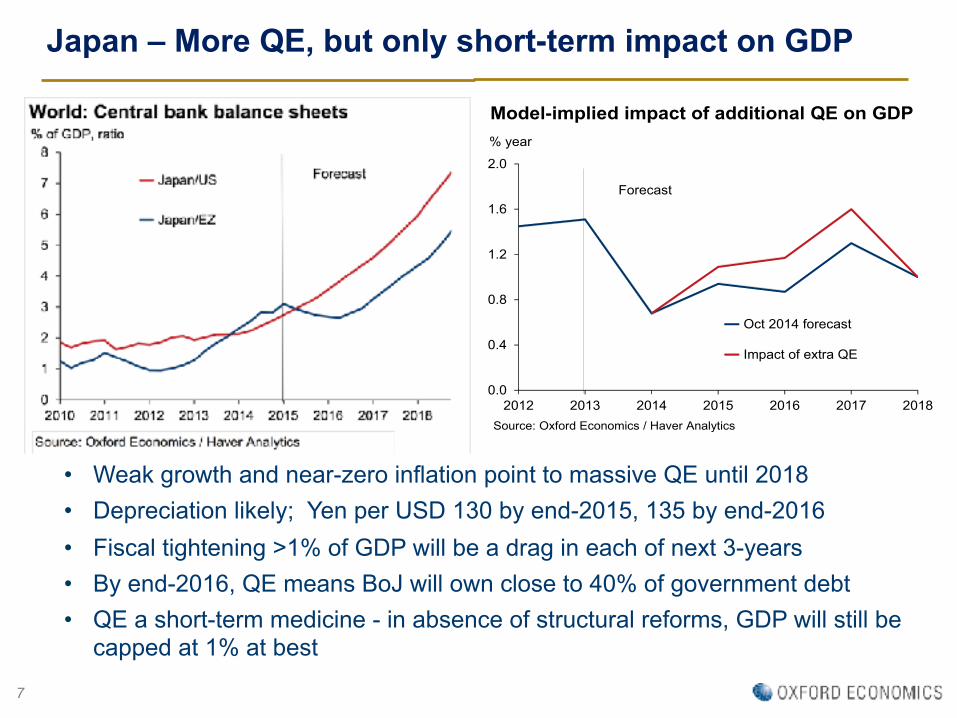

US - confidence, labour market, credit and $ on the rise

0.0

0.4

0.8

1.2

1.6

2.0

2012 2013 2014 2015 2016 2017 2018

Oct 2014 forecast

Impact of extra QE

Source: Oxford Economics / Haver Analytics

Model-implied impact of additional QE on GDP% year

Forecast

• Weak growth and near-zero inflation point to massive QE until 2018 • Depreciation likely; Yen per USD 130 by end-2015, 135 by end-2016 • Fiscal tightening >1% of GDP will be a drag in each of next 3-years • By end-2016, QE means BoJ will own close to 40% of government debt • QE a short-term medicine - in absence of structural reforms, GDP will still be

capped at 1% at best

7

Japan – More QE, but only short-term impact on GDP

Gross Fixed Investment unbalanced

• Productivity slowdown, rebalancing to more consumer oriented economy, real estate downturn - increasingly dampening domestic demand and activity

• Local government revenues will be hit hard this year, as more than 40% of overall revenues are related to property

• Steep stock market gains look out of line with fundamentals • Chinese 2015 GDP growth at 6.6%, falling to 6.1% next year

8

China – rebalancing, ULC, real estate weigh on growth

• GDP in EM set to rise just 3.6% in 2015 – and just 2.2% ex-China (slowest since 2001)

• High debt and commodity dependence are drags on EM growth • Private sector debt ratio in emerging Asia higher than in G7, private debt in EM

(ex-China) up 20% since 2007 • Risk of a deleveraging cycle in highly indebted countries, especially in case of

external shocks9

EM growth to slow further

Worst impact from markets’ reaction to Fed rate increase

4. Eurozone - Is the pick-up in growth here to stay?

• After a recent soft patch, Eurozone economic data have once again begun to strike a slightly more positive tone – not only weak euro effect

• Solid household spending prospects and lending showing signs of life...finally! • ECB measures supporting investment • Draghi signals bond volatility for a prolonged period • Impact from eventual Grexit depending on implementation (orderly vs disorderly)

11

Investment recovery is steady rather than spectacular...

... driven by the ‘crisis’ economies

13

Eurozone – Need to rebalance ULC

ECB – QE reversing previous tightening

15

ECB Balance Sheet

Source: EconPartners calculations on ECB data Note: PSPP = Public sector purchase programme; CBPP3 = Covered bond purchase programme; ABSPP=Asset-back securities purchase programme.

Euro weakness set to last

16

• The majority of Greeks do not rightly comprehend the meaning of a foreign loan, but simply conclude that it is some European method of making a present - J.Emerson and W.H.Humphreys, London 1826

• La Grèce est le seul exemple connu d'un pays vivant en pleine banqueroute depuis le jour de sa naissance. Tous les budgets, depuis le premier jusqu'au dernier, sont en déficit. Aujourd'hui, elle renonce à l'espoir de s'acquitter [à] jamais – E. About, La Grèce contemporaine, Paris, 1858

17

Greece – NO vote should not come as a surprise

Orderly Greek exit would not be a disaster for Eurozone

18

• Mildly favorable global context - weak oil and commodities prices, overall monetary expansionary and neutral fiscal policies

• Growth in AEs compensates for growth slowdown in EMs • Change in growth parameters

• No Secular stagnation but lower growth rates for a prolonged period

• World trade loosing steam as a world growth engine • EU needs to revise governance and Treaties to adapt them to a changed

and further changing world • In a low growth environment, fiscal policies become more difficult to

balance • no space for inefficient public expenditure • need to reduce taxes and push on investment, growth

• Policies aimed at increasing potential output become even more crucial than in the past

19

Summary and final considerations

World GDP Growth% Change on Previous Year

2013 2014 2015 2016 2017 2018US 2.2 2.4 2.3 2.8 2.7 2.8Japan 1.6 -0.1 0.8 1.8 0.8 0.6Eurozone, of which: -0.4 0.9 1.6 1.9 1.7 1.6 Germany 0.2 1.6 2.0 2.2 1.7 1.3 France 0.7 0.2 1.3 1.7 1.6 1.5 Italy -1.7 -0.4 0.6 1.0 1.1 1.0UK 1.7 2.8 2.6 2.8 2.7 2.5China 7.7 7.4 6.6 6.1 5.7 5.5India 6.4 7.2 7.5 7.5 7.0 6.8Brazil 2.7 0.1 -1.3 0.7 2.6 3.2Mexico 1.7 2.1 2.7 3.1 3.4 3.5Eastern Europe 1.9 1.5 -0.7 2.5 3.5 3.7MENA 1.5 2.3 3.0 3.9 4.2 4.3World 2.5 2.6 2.6 3.1 3.2 3.2World, at PPP 3.2 3.3 3.2 3.8 3.9 3.9

20

Oxford Economics World Forecast

Long-term - “Secular” Stagnation? Overly pessimistic

R. Gordon: • Ageing (and expensive health technology) leads to higher savings • Slowing technical progress - leading to lower TFP for a sustained period -

and scarce investment demand despite low rates • Impact of technical changes in previous industrial revolutions (steam power,

electricity, combustion engine, running water…) much greater than current changes (questionable)

L. Summers: • excess savings ! no attainable interest rate that brings the economy to full

employment ! CBs pushed to zero interest rates, can’t activate adequate demand

• Capital flight from EM - lowering interest rates of AE assets • Shortage of safe assets (QE related) • Income inequality • Trade lesser growth engine K. Rogoff: • High debt levels and need for deleveraging (weighing on demand)

21

• Unione Europea (UE) – Processo iniziato anni 50 e culminato nel Trattato Maastricht 1992-93

• Scudo contro ripetersi dei conflitti sanguinosi dei secoli passati • Volontà di ruolo politico ed economico in mondo globalizzato • Processo di condivisione di sovranità tra Stati • Euro – passo (prematuro?) nel processo di unificazione

• Euro oggi • moneta comune di 19 Stati dell’UE e di oltre 330 milioni di cittadini • 24,4% delle riserve valutarie mondiali (18% nel 1999) contro il

61,2% del $/USA • 59 paesi e territori con moneta vincolata, direttamente o

indirettamente, all’euro

Fonte: Consiglio Europeo, 12 febbraio 2015

22

Europa - temi di fondo

• Contesto globale timidamente favorevole

• prezzi petrolio e commodities deboli

• politiche monetarie complessivamente accomodanti

• politiche fiscali mediamente neutrali

• …ma in contesto di bassa crescita

• Economie avanzate in progressivo, lento miglioramento

• Emergenti in rallentamento, in alcuni casi preoccupante, e con rischi crescenti

• Rischi globali orientati sul lato negativo - mercati finanziari, Cina, USA, Europa (Grexit)

23

Economia globale - temi di fondo

Diverging monetary policies

Central bank policies diverge in 2015, but overall supportive: •Fed raises rates to 0.6-0.65% by year-end •ECB to keep rates on hold for a long period

•BoJ purchases equivalent to 15% of GDP 2015; 20% in 2016 •PBoC to cut interest rates and reduce reserve requirements further in 2015

• On a six-month annualised basis, US and Eurozone broad money is growing at the same speed as in China …

• …highlighting healthier prospects for US and Eurozone…

• …but also pointing to continued slowing growth in China

2.3% 2.8%

2.3% 2.4%

25

US - low growth for a world engine

• «Il fatto che l'area dell'euro non si sia ripresa dalla crisi allo stesso modo degli Stati Uniti potrebbe indicare che un’unione monetaria incompleta si adegua molto più lentamente di un’unione dotata di un assetto istituzionale più completo» (sito Commissione Europea)

• Report di 4 Presidenti (2012) – visione EMU… senza Presidente del Parlamento Europeo – discrasia democratica tra PE e istituzioni di governo UE

• Piano Juncker (Nov. 2014) – Ottimistico sulla leva di investimenti privati - capitale 21 miliardi (di cui 13 effettivi) «crea» 315 miliardi investimenti

• Report dei 5 Presidenti (22 Giugno 2015) – 3 fasi • «Approfondire facendo»: strumenti e trattati esistenti per rilanciare

competitività e convergenza, politiche bilancio responsabili – fino a giugno 2017

• «Completare l’UEM» - Libro Bianco primavera 2017 • Fase finale – • Energia, digitale, mercato dei capitali, beni e servizi indicati come

mercati di cui completare l’unificazione 26

Europa – Governance farraginosa rallenta decisioni

• Report dei 5 Presidenti (22 Giugno 2015) – 3 fasi • «Approfondire facendo»: strumenti e trattati esistenti per rilanciare

competitività e convergenza, politiche bilancio responsabili – fino a giugno 2017

• «Completare l’UEM» - Libro Bianco primavera 2017 • Fase finale – • Energia, digitale, mercato dei capitali, beni e servizi indicati come

mercati di cui completare l’unificazione

27

Europa – Governance farraginosa rallenta decisioni

• Non ci sono vincitori o vittoria di Pirro • Grecia dovrà adottare misure austerità in ogni caso – oppure

diventare un paese da default seriale – manifatturiero 9% del PIL • Le classi deboli della Grecia le più penalizzate dal prolungamento

della crisi • Europa ha confermato debolezze di governance politica,

amplificandole nella gestione del caso Greco • Disillusione in larghi strati della popolazione, sentimento Europeista

in declino • Nessuna revisione dei trattati in senso solidaristico – Report dei 5

Presidenti buona base ma prudente nella tempistica • Dietro alla crisi europea, rifiuto di prendere atto del trasferimento

epocale di risorse verso emergenti – I tassi di crescita post-WW2 o degli anni ‘90 e fino alla crisi saranno irripetibili per alcuni decenni

• Ritracciamento del livello di benessere nelle economie avanzate storicamente pericoloso dal punto di vista sociale (esempio di Alvin Hansen, 1938) 28

Crisi Grecia

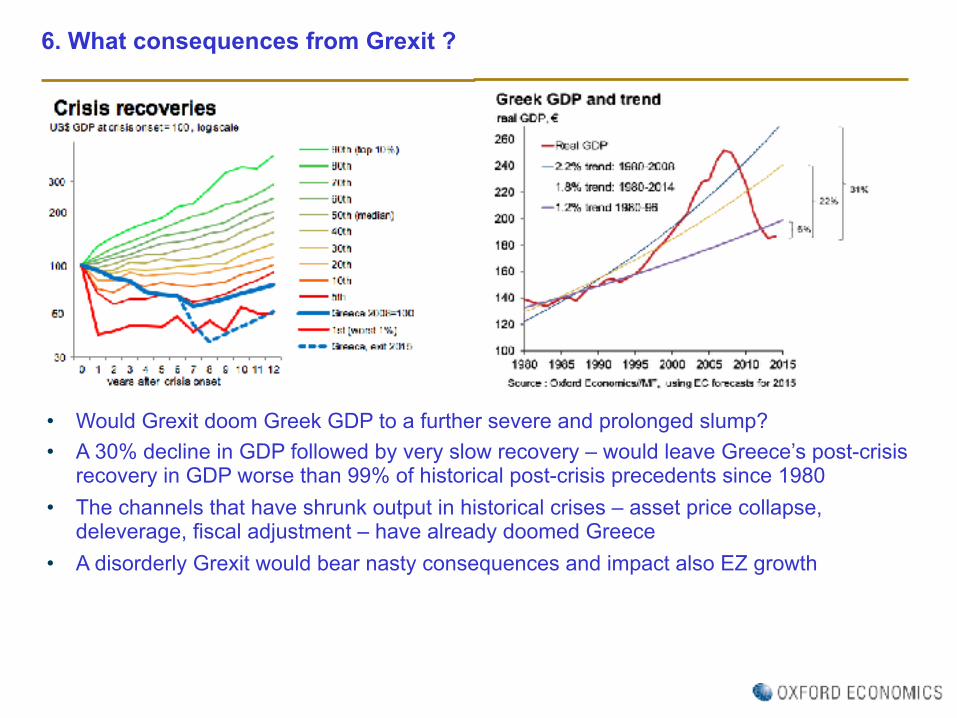

6. What consequences from Grexit ?

• Would Grexit doom Greek GDP to a further severe and prolonged slump? • A 30% decline in GDP followed by very slow recovery – would leave Greece’s post-crisis

recovery in GDP worse than 99% of historical post-crisis precedents since 1980 • The channels that have shrunk output in historical crises – asset price collapse,

deleverage, fiscal adjustment – have already doomed Greece • A disorderly Grexit would bear nasty consequences and impact also EZ growth