Klicken Sie, um das Titelformat Main elements, guiding ... · Klicken Sie, um das Titelformat zu...

24

Bundesministerium der Finanzen Berlin Klicken Sie, um das Titelformat zu bearbeiten Klicken Sie, um das Format des Untertitel-Masters zu bearbeiten. 1 Crisis response in the euro area * * * Main elements, guiding principles and results Reinhard Felke* Federal Ministry of Finance How to get out of the crisis? Different approaches in Japan and the EU towards growth 2nd JEF-DGAP International Symposium Berlin, 3 June 2014 * The opinion expressed in this presentation are those of the author and do not necessarily reflect official government positions.

Transcript of Klicken Sie, um das Titelformat Main elements, guiding ... · Klicken Sie, um das Titelformat zu...

Bundesministerium der Finanzen

Berlin

Klicken Sie, um das Titelformat zu bearbeiten

Klicken Sie, um das Format des Untertitel-Masters zu bearbeiten.

1

Crisis response in the euro area * * *

Main elements, guiding principles and results

Reinhard Felke*

Federal Ministry of Finance How to get out of the crisis?

Different approaches in Japan and the EU towards growth

2nd JEF-DGAP International Symposium

Berlin, 3 June 2014 * The opinion expressed in this presentation are those of the author and

do not necessarily reflect official government positions.

Bundesministerium der Finanzen

Berlin

The euro area economy in 2014

2

The good news first…

• Confidence has returned… • Convergence of risk spreads; stabilising credit flows; gradual

normalisation in financial markets; investment is picking up

…thanks to collective action by Member States; ECB; EU/Eurogroup (programmes; differentiated fiscal strategy; accomodative monetary policy; ESM; governance reform of EMU; Banking Union etc.)

• Economic recovery is broadening • GDP forecast to expand in 2014 (1.2%) and 2015 (1.7%), including

in vulnerable countries; intra-area adjustment is progressing

• Supply side reforms show results

Bundesministerium der Finanzen

Berlin

…the challenges and risks:

• Recovery to remain weak – unfinished deleveraging, competitiveness adjustment; lingering financial

market fragmentation and uncertainty – too weak for strong employment creation and swift recovery of lost output – High unemployment could persist and affect long-term growth („hysteresis“)

• Legacy of high level of public debt

• Limited policy space

• Bank asset quality review and stress test in 2014

• New risks from external environment 3

The euro area economy in 2014

Bundesministerium der Finanzen

Berlin

„‘This time is different‘. It almost never is“. (Reinhardt & Rogoff)

but „EMU sui generis“ (Barry Eichengreen)

So, anything special about the euro area crisis ?

4

The challenge

Bundesministerium der Finanzen

Berlin

Euro area idiosyncracies: • deep economic and financial integration of 18 Member States (=>

spillovers) • single monetary policy + rules-bound decentralised fiscal and

economic policies • Common rules and institutions (Commission; fiscal surveillance)… • …but initial gaps in EMU architecture

– E.g. No national „lender of last resort“ (=> cannot issue own debt); no significant central budget; no financial stability tool; no single supervisor

• Different macro-financial starting positions across euro area Member States, including large external/macro-structural imbalances and deeply exposed banks in some (=> vulnerabilities)

5

The challenge

Bundesministerium der Finanzen

Berlin

• Vulnerable starting conditions when the crisis struck:

6

The challenge

90

100

110

120

130

140

150

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Nominal Unit Labour Cost (Index, 1999=100)

Eurozone DEU IRL GRC ESP FRA ITA PRT

• Accumulated loss of competitiveness

Bundesministerium der Finanzen

Berlin

• Vulnerable starting conditions when the crisis struck:

7

The challenge

-20

-15

-10

-5

0

5

2003 2004 2005 2006 2007 2008

% G

DP

Current Account Balance

Greece Portugal Spain Italy France Ireland Euro area

• Accumulated external imbalances

• Risk of sudden

stop

Bundesministerium der Finanzen

Berlin

8

The crisis impact

EFSF

↓

Debt Restructuring

↓

Bankruptcy Lehman Brothers

↓

0

5

10

15

20

25

30

35

40

45

02.01.2008 02.01.2009 02.01.2010 02.01.2011 02.01.2012 02.01.2013 02.01.2014

%

Interest Rates on Government Bonds

DEU GRC PRT IRL ESP ITA FRA

• Confidence evaporated

• Default risk rose • Financing costs

soared

• Bank lending reversed

Bundesministerium der Finanzen

Berlin

9

The crisis impact

• Growth slumped

• Unemployment increased

• Consumption fell and investment stopped

0

500

1.000

1.500

2.000

2.500

3.000

3.500

4.000

4.500

5.000

-8

-6

-4

-2

0

2

4

6

2007 2008 2009 2010 2011 2012 2013 2014 2015E

uros

toxx

50

Pric

e In

dex

% c

ahng

e G

DP

Real GDP Growth and Eurostoxx 50

Euro area United States Japan DJ Eurostoxx 50

Bundesministerium der Finanzen

Berlin

10

The crisis impact

• Public debt jumped

• Feeding fears of debt sustainability

40 44

72

106 113

94

124 129 133

175

0

20

40

60

80

100

120

140

160

180

200

Spain Ireland Portugal Italy Greece

Public Debt % GDP

2008

2013

Bundesministerium der Finanzen

Berlin

11

The crisis impact

FINANCIAL STABILITY

SOVEREIGN DEBT

ECONOMIC GROWTH

Negative confidence

shock

Bundesministerium der Finanzen

Berlin

• safeguarding the stability of the euro area as a whole • restoring confidence via credible measures and sustainable

solutions

• addressing fundamental weaknesses via deep structural reform • combining solidarity with conditionality, setting incentives for

structural adjustment in Member States concerned • Country-specific differentiation 12

The crisis response – guiding principles

Bundesministerium der Finanzen

Berlin

• Macro response at euro area level – Accommodative monetary policy + unconventional measures – Differentiated and time-consistent fiscal policy strategy

• Country-specific – Adjustment programmes (guided by Troika = Commission + ECB + IMF) – Wage constrains and structural reforms to restore competitiveness and

build new foundations for sustainable growth – Shoring up troubled banks within EU state-aid regime

• Institutional – EFSF/ESM – Economic governance reform (stronger fiscal rules; new macro-imbalances

tool; better economic coordination via enhanced European Semester) – Single Supervisory + Resolution Mechanism; Single Rule Book – European System of Financial Supervisors; Macro-Systemic Risk Board

13

The crisis response – main elements

Bundesministerium der Finanzen

Berlin

A broad-based recovery is taking place

Data: AMECO Spring 2014

-8

-6

-4

-2

0

2

4

2009 2010 2011 2012 2013 2014 2015

% C

hang

e

Real GDP per capita

Italy Spain Greece Portugal Euro area

Bundesministerium der Finanzen

Berlin

Supply side reforms show results

Bundesministerium der Finanzen

Berlin

Competitiveness is improving

90

100

110

120

130

140

150

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014p 2015p

Nominal Unit Labour Cost (Index, 1999=100)

Eurozone DEU IRL GRC ESP FRA ITA PRT

Data: AMECO Spring 2014

Bundesministerium der Finanzen

Berlin

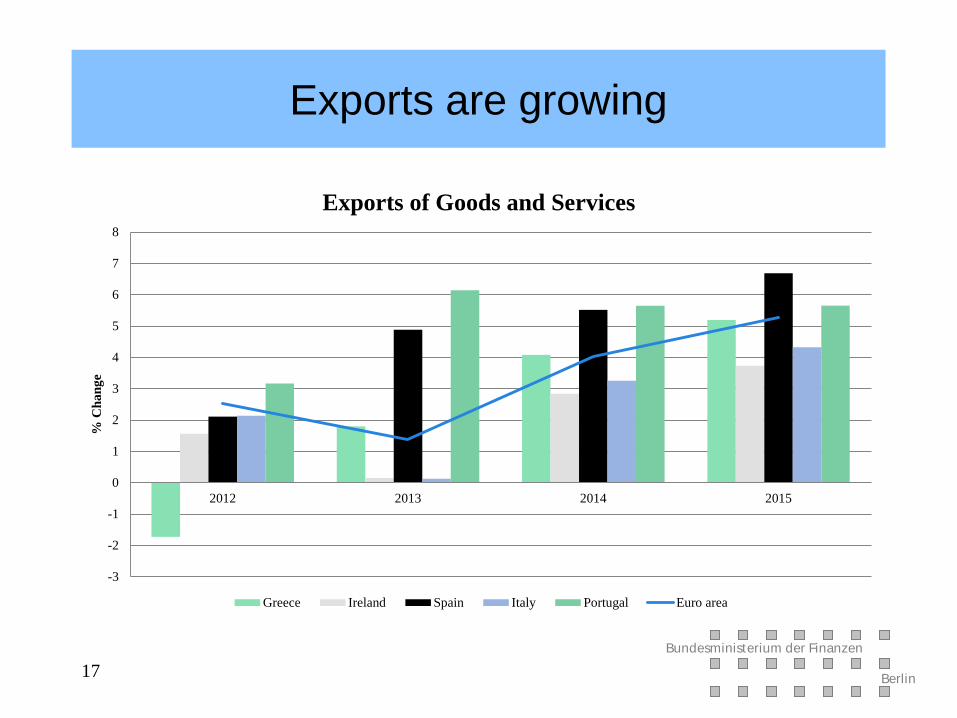

Exports are growing

17

-3

-2

-1

0

1

2

3

4

5

6

7

8

2012 2013 2014 2015

% C

hang

e

Exports of Goods and Services

Greece Ireland Spain Italy Portugal Euro area

Bundesministerium der Finanzen

Berlin

External imbalances are receding

Data: AMECO Spring 2014

-20

-15

-10

-5

0

5

2008 2009 2010 2011 2012 2013 2014 2015

% G

DP

Current Account Balance

Greece

Portugal

Spain

Italy

Euro area

Bundesministerium der Finanzen

Berlin

Reforms are progressing

19

0

0,2

0,4

0,6

0,8

1

1,2

1,4

1,6

1,8

Responsiveness to Going for Growth recommendations across OECD countries, 2011-12

Responsiveness rate Responsiveness rate adjusted for the difficulty to undertake reform

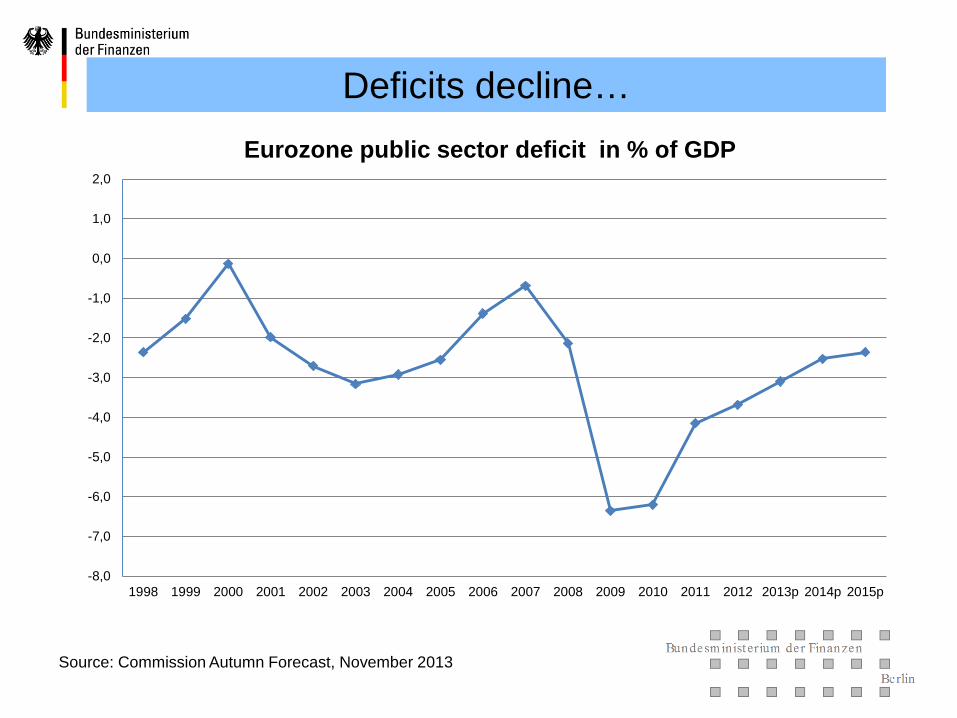

Deficits decline…

Source: Commission Autumn Forecast, November 2013

-8,0

-7,0

-6,0

-5,0

-4,0

-3,0

-2,0

-1,0

0,0

1,0

2,0

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013p 2014p 2015p

Eurozone public sector deficit in % of GDP

Source: Commission Autumn Forecast, November 2013

60

65

70

75

80

85

90

95

100

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013p 2014p 2015p

Eurozone public debt – high but stabilising - in % GDP-

Source: Commission Autumn Forecast, November 2013

0,0

60,0

120,0

180,0

240,0

300,0

DEU FRA UK ESP Eurozone USA IRL PRT ITA GRC Japan

Public debt in international comparison - 2013 in % of GDP -

Bundesministerium der Finanzen

Berlin

• Move from recovery to sustained growth

• Maintain twin-strategy of differentiated fiscal consolidation combined with structural reforms to enhance growth and competitiveness and to bring debt levels to safe territory

• Improve the quality of public finances – Improve quality of consolidation – Raise efficiency of social security systems; public administrations etc.

• Implement Banking Union (SSM/SRM); consolidate banks

• Foster the functioning of the EU internal market

23

The challenge ahead

Bundesministerium der Finanzen

Berlin

Thank you… … for your attention!

Reinhard Felke Director - European Economic and Monetary Union; Bilateral Relations, EU Enlargement Federal Ministry of Finance Wilhelmstraße 97, D-10117 Berlin Telefon: +49 30 18 682-1731 Fax: +49 30 18 682-1156 Mail: [email protected] Internet: http://www.bundesfinanzministerium.de

![OpenScape Business V2 How to: Konfiguration A1 Telekom ... · Open Scape Business V2 – How To: Konfiguration A1 Telekom Austria 7 Klicken Sie [OK & Weiter] Im nächsten Schritt](https://static.fdocuments.in/doc/165x107/60619377621f8b5c55391a37/openscape-business-v2-how-to-konfiguration-a1-telekom-open-scape-business-v2.jpg)