Kentucky National Insurance Co. v. Empire Fire & Marine - Indiana

65

FOR PUBLICATION ATTORNEY FOR APPELLANT AND ATTORNEYS FOR APPELLEE AND CROSS-APPELLEE KENTUCKY CROSS-APPELLANT EMPIRE FIRE NATIONAL INSURANCE COMPANY : AND MARINE INSURANCE CO.: GALEN L. CLARK ANGELA S. CASH Travis & Herbert, PLLC R. JAY TAYLOR JR. Louisville, Kentucky Scopelitis, Garvin, Light, Hanson & Feary Indianapolis, Indiana ATTORNEY FOR APPELLEE AND CROSS-APPELLEE ALPHA LEASING CO., INC.: DAVID L. SAGE Hummel Coan Miller & Sage Louisville, Kentucky ATTORNEY FOR APPELLEES HUNTINGTON NATIONAL BANK AND HUNTINGTON LT: GARRET B. HANNEGAN Morgan & Pottinger, P.S.C. Louisville, Kentucky IN THE COURT OF APPEALS OF INDIANA KENTUCKY NATIONAL INSURANCE ) COMPANY, ) ) Appellant, ) ) vs. ) No. 22A04-0810-CV-616 ) EMPIRE FIRE AND MARINE INSURANCE ) COMPANY, ALPHA LEASING CO., INC., ) TODD ROYSE, JULIE SPEAKES, ) HUNTINGTON NATIONAL BANK, ) HUNTINGTON LT, AND UNKNOWN ) INSURANCE CO., WILLIAM “BILL” WARD, ) AND RONALD J. CARNEY, ) )

Transcript of Kentucky National Insurance Co. v. Empire Fire & Marine - Indiana

FOR PUBLICATION

ATTORNEY FOR APPELLANT AND ATTORNEYS FOR APPELLEE AND

CROSS-APPELLEE KENTUCKY CROSS-APPELLANT EMPIRE FIRE

NATIONAL INSURANCE COMPANY: AND MARINE INSURANCE CO.:

GALEN L. CLARK ANGELA S. CASH Travis & Herbert, PLLC R. JAY TAYLOR JR.

Louisville, Kentucky Scopelitis, Garvin, Light, Hanson

& Feary

Indianapolis, Indiana

ATTORNEY FOR APPELLEE AND

CROSS-APPELLEE ALPHA LEASING

CO., INC.:

DAVID L. SAGE

Hummel Coan Miller & Sage

Louisville, Kentucky

ATTORNEY FOR APPELLEES

HUNTINGTON NATIONAL BANK

AND HUNTINGTON LT:

GARRET B. HANNEGAN

Morgan & Pottinger, P.S.C.

Louisville, Kentucky

IN THE

COURT OF APPEALS OF INDIANA

KENTUCKY NATIONAL INSURANCE )

COMPANY, )

)

Appellant, )

)

vs. ) No. 22A04-0810-CV-616

)

EMPIRE FIRE AND MARINE INSURANCE )

COMPANY, ALPHA LEASING CO., INC., )

TODD ROYSE, JULIE SPEAKES, )

HUNTINGTON NATIONAL BANK, )

HUNTINGTON LT, AND UNKNOWN )

INSURANCE CO., WILLIAM “BILL” WARD, )

AND RONALD J. CARNEY, )

)

kmanter

Filed Stamp

2

Appellees. )

)

)

EMPIRE FIRE AND MARINE INSURANCE )

COMPANY, )

)

Cross-Appellant, )

)

vs. )

)

KENTUCKY NATIONAL INSURANCE )

COMPANY AND ALPHA LEASING )

CO., INC., )

)

Cross-Appellees. )

APPEAL FROM THE FLOYD CIRCUIT COURT

The Honorable J. Terrence Cody, Judge

Cause No. 22C01-0608-MF-518

January 7, 2009

OPINION - FOR PUBLICATION

BROWN, Judge

Kentucky National Insurance Company (“Kentucky National”) appeals the trial

court‟s denial of its motion for summary judgment and partial grant of summary

judgment in favor of Empire Fire and Marine Insurance Co. (“Empire Fire”), Alpha

Leasing Co., Inc. (“Alpha Leasing”), Todd Royse, Bill Ward, and Huntington National

Bank and Huntington LT (together, “Huntington”). Kentucky National raises four issues,

which we consolidate and restate as whether the trial court erred in denying its motion for

summary judgment and granting partial summary judgment to Empire Fire and Alpha

Leasing. On cross-appeal, Empire Fire raises two issues, which we consolidate and

3

restate as whether the trial court erred by denying in part its motion for summary

judgment. We affirm in part, reverse in part, and remand.1

The relevant facts follow. Alpha Leasing, a Kentucky corporation, is a company

which is engaged in the business of arranging and making leases of motor vehicles.2 In

December 1997, Alpha Leasing and Huntington entered into an Operating Agreement.

The Operating Agreement set forth the terms under which Huntington acquired motor

vehicles from Alpha Leasing for the purpose of leasing the vehicles to individuals or

business entities. According to the Operating Agreement, written motor vehicle leases

would be entered into by Huntington as lessor and the individual customers as lessees.

Alpha Leasing was authorized to enter into the vehicle leases on behalf of Huntington.

Alpha Leasing was required to procure and deliver to the lessees any vehicles to be

leased, and Alpha Leasing was required to obtain all available warranties and guarantees

applicable to the vehicles. Under Section II.C. of the Operating Agreement, Alpha

Leasing was required to cause the motor vehicles to be registered, licensed, and titled

solely in Huntington‟s name. Pursuant to Section II.D., Alpha Leasing was required,

1 We note that Kentucky National did not include a statement of issues or a statement of case in

its appellant‟s brief. We remind Kentucky National that Ind. Appellate Rule 46(A)(3) and (5) require that

the appellant‟s brief shall contain a statement of issues and a statement of case under separate headings

and that the statement of case “shall briefly describe the nature of the case, the course of the proceedings

relevant to the issues presented for review, and the disposition of these issues by the trial court . . . .” We

also note that Kentucky National did not include the applicable standard of review in its appellant‟s brief

which is required by Ind. Appellate Rule 46(A)(8)(b) (“The argument must include for each issue a

concise statement of the applicable standard of review; this statement may appear in the discussion of

each issue or under a separate heading placed before the discussion of the issues.”). We remind counsel

for Kentucky National of their professional obligation to follow the appellate rules.

2 The record reveals that Alpha Leasing arranged leases for vehicles which were titled in its name

and for vehicles which were titled to other lessors.

4

prior to delivery of a vehicle to a lessee, to verify that the lessee had insurance in effect

for the motor vehicle. Alpha Leasing was also required to notify Huntington of any loss

or damage sustained by the motor vehicle. Pursuant to Section K of the Operating

Agreement, Alpha Leasing had the sole responsibility for the condition and performance

of all leased vehicles, any actions or omissions in connection with the leases, any failure

to deliver the vehicle or to perform services, and any failure to sell or dispose of any

trade-in or any failure to pay in full the prior financing obligation on the trade-in.

Huntington also had a vehicle return policy pertaining to the vehicles leased

pursuant to the Operating Agreement and arranged by Alpha Leasing. The return policy

stated: “Alpha Leasing may only return vehicles on behalf of the lessee, as outlined in the

provisions below, provided the lease has reached maturity. This policy does not apply to

vehicles being returned by lessees prior to lease maturity.” Appellant‟s Supplemental

Appendix at 73; Appellant‟s Appendix at 181. The policy permitted Alpha Leasing to

pick up a vehicle from a lessee, obtain documentation,3 and return the vehicle by

appointment to Huntington‟s designated return location. The policy provided: “Alpha

Leasing will be responsible for ensuring the vehicle is returned within (5) business days

of pick up and that adequate insurance coverage is carried to cover the care and custody

of the vehicle while in their possession.” Appellant‟s Supplemental Appendix at 73;

Appellant‟s Appendix at 181. As part of its business operations, Alpha Leasing would

3 The documentation required by the vehicle return policy included an odometer statement and a

vehicle return waiver signed by the lessee. The documentation was to be retained in Alpha Leasing‟s

records.

5

transport vehicles leased pursuant to its Operating Agreement with Huntington from the

individual lessee to the auto auction site designated by Huntington. Huntington also

maintained inspection procedures which set forth the return center for each of

Huntington‟s operating areas.4 Huntington‟s return center for its Louisville, Kentucky

operating area was the Louisville Auto Auction.

Two commercial insurance policies were issued to Alpha Leasing covering July

2004. First, Kentucky National issued a Commercial Auto Policy (the “Kentucky

Policy”) to Alpha Leasing.5 Second, Empire Fire issued a Business Auto Policy (the

“Empire Policy”) to Alpha Leasing.

In March 1998, Alpha Leasing facilitated a lease between Huntington and Ronald

Carney.6 Pursuant to a vehicle lease agreement arranged by Alpha Leasing, Huntington

leased a Toyota Celica (the “Vehicle”) to Carney. As required by the Operating

4 It does not appear that Huntington‟s inspection procedures were included in the designated

evidence.

5 In support of its motion for summary judgment, it appears that Kentucky National only cited to

certain portions of the Kentucky Policy: page 9, Section 1, Symbol 9; page 15, and pages 19-37. The

response of Huntington to the summary judgment motions of Empire Fire, Kentucky National, Alpha

Leasing, and Ward included an attachment of the first two pages of the Kentucky Policy, which consisted

of the Declarations pages describing the three types of autos covered by the Kentucky Policy. In support

of its motion for summary judgment, Empire National designated the entirety of the Kentucky Policy.

Also, in support of its motion for summary judgment, which was incorporated by reference in Alpha

Leasing‟s response to Empire Fire‟s summary judgment motion, Alpha Leasing designated the entirety of

the Kentucky Policy.

6 The original 1998 vehicle lease does not appear to be included in the designated evidence in

support of Kentucky National‟s summary judgment motion or Empire Fire‟s summary judgment motion.

A copy of the 1998 vehicle lease was designated by Alpha Leasing in support of its motion for summary

judgment.

6

Agreement between Alpha Leasing and Huntington, the Vehicle was titled to and

registered in the name of Huntington.

On July 31, 2001, Carney executed a second lease agreement extending the

Vehicle‟s lease for an additional three years. Section 14 of the lease shows that Alpha

Leasing, as required by its Operating Agreement with Huntington, verified that Carney

obtained insurance coverage for the vehicle during the term of the lease. Section 18 of

the Vehicle‟s lease required Carney to maintain insurance coverage until he returned the

vehicle. Pursuant to Section 24 of the lease, Carney was permitted to terminate the lease

prior to its scheduled expiration/maturity provided he was not in default at the time of

such termination. If Carney terminated the lease prior to its scheduled

expiration/maturity, he would be required to pay an early termination fee. For purposes

of determining the early termination fee, the lease would be considered terminated during

the month during which Huntington obtained possession of the Vehicle through

repossession or return, or Huntington received the proceeds of the insurance Carney

obtained to cover the Vehicle if the Vehicle were to become a total loss due to collision,

destruction or theft.7

In December 2003, prior to the scheduled expiration/maturity of the lease term for

the Vehicle, Carney returned the Vehicle to Bill Ward, a sales agent with Alpha Leasing,

7 The vehicle lease also stated that Carney was required by law to complete a statement of the

Vehicle‟s mileage and that failure to complete an odometer disclosure statement or making a false

statement therein may result in fines and imprisonment.

7

and leased a new vehicle through Alpha Leasing.8 Alpha Leasing attempted to sell the

Vehicle and made the lease payments until the scheduled lease expiration/maturity.

On July 13, 2004, during the last month of the Vehicle‟s lease term, Alpha

Leasing hired Todd Royse9 to drive the Vehicle from Alpha Leasing‟s office located in

Louisville, Kentucky, to the Louisville Auto Auction located at 5425 Highway 32E,

Clarksville, Indiana. Later that day, the Vehicle, driven by Royse, was involved in an

automobile accident in southern Indiana with a vehicle driven by Julie Speakes.10

On

May 23, 2006, Speakes filed a lawsuit against Royse and Alpha Leasing under Cause No.

22C-01-0605-CT-316 (the “Speakes Lawsuit”).

At some point, Alpha Leasing or its insurance agent notified Empire Fire of the

accident involving the Vehicle, and Empire Fire sent a payment by check to Speakes for

property damage to her vehicle. However, Speakes did not cash the check, but returned it

8 The record and designated evidence do not appear to contain a signed vehicle return waiver.

Ward testified at his deposition that he could not recall whether Carney signed a vehicle return waiver or

if Alpha Leasing required Carney to sign a vehicle return waiver. Ward also testified that he could not

recall whether or not he discussed with Carney the termination fee under the lease of the Vehicle.

9 Royse “worked for himself” in the automobile industry. Appellee‟s Supplemental Appendix at

221. Royse could pick up and deliver vehicles, perform work on vehicle brakes and air conditioners,

complete tune-ups and oil changes, and detail, wash, vacuum, and clean vehicles.

10 In a written statement, Royse stated that he “was driving thru [sic] a trafic [sic] light that [he]

thought was green.” Appellant‟s Supplemental Appendix at 76. According to the police report regarding

the accident, Royse stated that he “thought he had a green light when entering the intersection” which

resulted in the collision, Speakes stated that “[Royse] ran the red light and hit her,” and a witness to the

accident who was in a vehicle behind Royse‟s vehicle observed Royse “run the red light and hit

[Speakes].” Id. at 22.

During his deposition, Ward testified that he had a discussion with Royse about a year after the

accident and that “Mr. Royse said he had an errand to run in Indiana to pick up some air conditioner

equipment.” Appellant‟s Supplemental Appendix at 96.

8

to Empire Fire.11

Empire Fire also sent a check to Speakes for reimbursement of her

insurance deductible and her rental car expense incurred as a result of the accident, and

Speakes cashed that check.12

On March 9, 2005, Alpha Leasing sent an automobile loss notice to Kentucky

National regarding the accident involving the Vehicle. The automobile loss notice stated

that “[Empire Fire] is claiming that they are not liable for this claim.” Appellant‟s

Appendix at 159; Appellant‟s Supplemental Appendix at 75. On March 23, 2006,

Empire Fire sent a letter to Kentucky National stating that the coverage provided by the

Empire Policy was excess/contingent and requested Kentucky National to advise as to

whether the Kentucky Policy provided coverage for Alpha Leasing. On May 30, 2006,

Alpha Leasing sent a letter by its attorney to Kentucky National together with a copy of

the complaint and related documents with respect to the Speakes Lawsuit. On June 6,

2006, Kentucky National responded to Alpha Leasing by letter and stated that Kentucky

National acknowledged no obligation to defend and indemnify Alpha Leasing because

the Vehicle was not an insured vehicle under the Kentucky Policy and because Kentucky

National did not receive timely notice of Alpha Leasing‟s claim.13

11

According to Speakes‟s response to requests for admissions, Speakes‟s insurer, State Farm

Insurance Companies, paid for the property damage to her vehicle.

12 It does not appear that the payments made by check by Empire Fire to Speakes were included

in the record or the designated evidence. Also, Speakes‟s responses to requests for admissions revealing

that Empire Fire sent payment of some amount to Speakes, while included in the appellant‟s appendix, do

not appear to have been designated by Kentucky National in support of its motion for summary judgment.

Speakes‟s responses to requests for admissions were attached to Kentucky National‟s response to Empire

Fire‟s motion for summary judgment.

13 According to Kentucky National‟s letter, in response to Alpha Leasing‟s notice of loss dated

9

In August 2006, Empire Fire filed a lawsuit under Cause No. 22C-01-0608-MR-

518, the case from which this appeal arises, against Kentucky National, Alpha Leasing,

Royse, and Speakes, requesting the court for declaratory relief related to the insurance

coverage provided by the Empire Policy in connection with the accident between Royse

and Speakes. In September 2006, Kentucky National filed an answer, counterclaim and

cross-claim asking the court for declaratory relief related to the insurance coverage

provided by the Kentucky Policy in connection with the accident. In November 2006,

Kentucky National filed a third party complaint against Huntington National Bank. In

February 2007, Huntington National Bank filed a motion to dismiss Kentucky National‟s

third party complaint, which was denied. In July 2007, Huntington National Bank filed

an answer, counterclaim against Kentucky National, cross-claims against Empire Fire,

Alpha Leasing and Royse, and third party complaints against Ward and Carney. Also in

July 2007, Kentucky National added Huntington LT and filed a third party complaint

against Huntington LT requesting declaratory relief and alleging that Huntington was

self-insured or financially responsible for the operation of the Vehicle. In September

March 9, 2005, Kentucky National sent faxes to Alpha Leasing‟s insurance agent on May 25 and 26,

2005, requesting some specific information, including information regarding the reason the accident was

not reported to Kentucky National earlier, “an explanation of who Todd Royse was,” a “copy of the

[Vehicle‟s] lease,” information regarding “what charges were filed against Mr. Royse,” and “the portion

of the policy that he felt would afford coverage for this accident.” See Appellee‟s Appendix at 32. Also

according to Kentucky National‟s letter, Alpha Leasing‟s insurance agent responded to Kentucky

National‟s request for specific information by stating that he could not obtain the information requested

and again requesting that Kentucky National assign a field investigator to the claim. It does not appear

that Empire Fire‟s letter on March 23, 2006, Alpha Leasing‟s letter on May 30, 2006, or Kentucky

National‟s letter on June 6, 2006, were included in the evidence cited by Kentucky National in support of

its summary judgment motion. However, the letters were apparently attached to Alpha Leasing‟s

response to Kentucky‟s summary judgment motion, and only the March 23, 2006, letter was referenced in

the response filing.

10

2007, Huntington LT filed an answer, counterclaim against Kentucky National, cross-

claims against Empire Fire, Alpha Leasing, and Royse, and third party complaints against

Ward and Carney. In October 2007, the court ordered mediation. The case did not settle

at mediation.

On November 13, 2007, Empire Fire filed a motion for summary judgment

seeking a determination that the Empire Policy did not provide coverage for the Vehicle,

that Empire Fire did not waive and is not estopped from raising defenses to coverage

under the Empire Policy, and that Empire Fire‟s coverage under the Empire Policy was

secondary or excess to any coverage provided by Kentucky National. On January 18,

2008, Kentucky National filed a motion for summary judgment seeking a determination

that it did “not owe insurance coverage to [Alpha Leasing] and Royse . . . .” Appellee‟s

Appendix at 168-169.14

Also on January 18, 2008, Alpha Leasing, Ward, and Huntington

filed separate motions for summary judgment.15

In its memorandum in support of its

14

We note that Kentucky National did not submit a separate designation of evidence. In Filip v.

Block, the Indiana Supreme Court held that a party‟s designation of evidence may be placed in a motion

for summary judgment, a memorandum supporting or opposing the motion, a separate filing identifying

itself as the designation of evidence, or an appendix to the motion or memorandum. 879 N.E.2d 1076,

1081 (Ind. 2008), reh‟g denied. However, the Court also emphasized that “[t]he only requirement as to

placement is that the designation clearly identify listed materials as designated evidence in support of or

opposition to the motion for summary judgment.” Id. Also, “[i]f the designation is not in the motion

itself, it must be in a paper filed with the motion, and the motion should recite where the designation of

evidence is to be found in the accompanying papers.” Id. at 1081. Here, Kentucky National‟s motion for

summary judgment did not “recite where the designation of evidence is to be found in the accompanying

papers.” Id. Nor did Kentucky National‟s memorandum in support of its motion recite where the

designation of evidence is to be found. We remind Kentucky National‟s counsel that the Indiana

Supreme Court has held that “the courts and opposing parties should not be required to flip from one

document to another to identify the evidence a party claims is relevant to its motion.” Id. “Rather, the

entire designation must be in a single place, whether as a separate document or appendix or as a part of a

motion or other filing.” Id.

15 The record includes Alpha Leasing‟s motion for summary judgment, accompanying

11

motion, Alpha Leasing argued that the Vehicle was covered under the Empire Policy and

the Kentucky Policy.

On January 23, 2008, Huntington filed a second motion for summary judgment

against Alpha Leasing and Ward.16

The parties also filed a number of response and reply

briefs opposing the various motions for summary judgment. In response filings on

February 19, 2008, and March 3, 2008, Kentucky National argued among other things

that Alpha Leasing was entitled to summary judgment on the grounds that it was not

vicariously responsible for Royse‟s acts.

On March 3, 2008, the trial court heard argument on all of the pending motions.

In April 2008, the trial court issued an entry in the court‟s chronological case summary

granting partial summary judgment in favor of Empire Fire and Alpha Leasing. The trial

court held a hearing on July 24, 2008, to address various concerns of the parties regarding

the effect of the April 2008 ruling, and the court held a status conference on September

12, 2008.

On September 22, 2008, the trial court entered a partial order of summary

judgment regarding the issues raised by the parties in their summary judgment motions.

In its order, the trial court found the following: (1) the Empire Policy provided coverage

memorandum, and attached designation of evidence. The motions for summary judgment filed by Ward

and Huntington do not appear to be included in the record.

16 The appellant‟s appendix includes an excerpt from Huntington‟s memorandum in support of its

motion for summary judgment against Alpha Leasing and Ward. From the excerpt provided, it appears

that Huntington argued that it was entitled to recover any damages it incurred in connection with the

accident from Alpha Leasing upon the bases of conversion and negligence.

12

for the accident; (2) the Kentucky Policy provided coverage for the accident; (3) Royse

was preliminarily entitled to a defense in the Speakes Lawsuit under both the Kentucky

Policy and the Empire Policy; (4) Empire Fire did not waive its non-coverage defense by

making partial payments of claims related to the accident; (5) the coverage provided by

the Empire Policy was secondary to and in excess of the primary coverage provided by

the Kentucky Policy; and (6) Kentucky National bears the primary burden to defend

Alpha Leasing and Royse in the Speakes Lawsuit and Empire Fire shall continue to

provide a defense to Alpha Leasing and Royse. The trial court denied summary

judgment on all other issues raised by the parties in their various summary judgment

motions.

Both Kentucky National and Empire Fire appeal the trial court‟s order. Summary

judgment is appropriate only where there is no genuine issue of material fact and the

moving party is entitled to judgment as a matter of law. Ind. Trial Rule 56(c); Mangold

ex rel. Mangold v. Ind. Dep‟t of Natural Res., 756 N.E.2d 970, 973 (Ind. 2001). All facts

and reasonable inferences drawn from those facts are construed in favor of the

nonmovant. Mangold, 756 N.E.2d at 973. Our review of a summary judgment motion is

limited to those materials designated to the trial court. Id. We must carefully review a

decision on summary judgment to ensure that a party was not improperly denied its day

in court. Id. at 974. Any doubt as to the existence of an issue of material fact, or an

inference to be drawn from the facts, must be resolved in favor of the nonmoving party.

Cowe v. Forum Group, Inc., 575 N.E.2d 630, 633 (Ind. 1991).

13

A party moving for summary judgment bears the initial burden of showing no

genuine issue of material fact and the appropriateness of judgment as a matter of law.

Monroe Guar. Ins. Co. v. Magwerks Corp., 829 N.E.2d 968, 975 (Ind. 2005). If the

movant fails to make this prima facie showing, then summary judgment is precluded

regardless of whether the non-movant designates facts and evidence in response to the

movant‟s motion. Id. In reviewing a trial court‟s ruling on a motion for summary

judgment, we may affirm on any grounds supported by the Indiana Trial Rule 56

materials. Catt v. Bd. of Comm‟rs of Knox County, 779 N.E.2d 1, 3 (Ind. 2002).

The fact that the parties make cross-motions for summary judgment does not alter

our standard of review. Hartford Acc. & Indem. Co. v. Dana Corp., 690 N.E.2d 285,

291 (Ind. Ct. App. 1997), trans. denied. Instead, we must consider each motion

separately to determine whether the moving party is entitled to judgment as a matter of

law. Id. The entry of specific findings and conclusions does not alter the nature of a

summary judgment which is a judgment entered when there are no genuine issues of

material fact to be resolved. Rice v. Strunk, 670 N.E.2d 1280, 1283 (Ind. 1996). In the

summary judgment context, we are not bound by the trial court‟s specific findings of fact

and conclusions of law. Id. They merely aid our review by providing us with a statement

of reasons for the trial court‟s actions. Id.

Before we address the arguments of Kentucky National and Empire Fire, we note

that the law of Kentucky applies to this case. Choosing the appropriate state substantive

law is a decision to be made by the court of the state in which the action is pending.

14

Travelers Ins. Co. v. Rogers, 579 N.E.2d 1328, 1330 (Ind. Ct. App. 1991) (citing

Hubbard Manufacturing Co., Inc. v. Greeson, 515 N.E.2d 1071, 1073 (Ind. 1987); see

also Alli v. Eli Lilly and Co., 854 N.E.2d 372, 376 (Ind. Ct. App. 2006). Accordingly,

Indiana‟s choice of law rules apply to this case. Indiana choice-of-law provisions

generally favor contractual stipulations as to governing law. See Allen v. Great Am.

Reserve Ins. Co., 766 N.E.2d 1157, 1162 (Ind. 2002).

Indiana‟s choice of law rule for contract actions, including actions based upon

insurance contracts, is the “most intimate contacts” test. Schaffert by Schaffert v.

Jackson Nat‟l Life Ins. Co., 687 N.E.2d 230, 232 (Ind. Ct. App. 1997) (citations omitted),

trans. denied. The court will consider all acts of the parties touching the transaction in

relation to the several states involved and will apply as the law governing the transaction

the law of that state with which the facts are in most intimate contact. Hartford Acc. &

Indem. Co. v. Dana Corp., 690 N.E.2d 285, 291 (Ind. Ct. App. 1997) (citing W.H. Barber

Co. v. Hughes, 223 Ind. 570, 63 N.E.2d 417, 423 (1945)), trans. denied. The following

are representative of the factors to consider: (1) the place of contracting, (2) the place of

negotiation, (3) the place of performance, (4) the location of the subject matter of the

contract, and (5) the domicil, residence, nationality, place of incorporation and place of

business of the parties. Employers Ins. of Wausau v. Recticel Foam Corp., 716 N.E.2d

1015, 1024 (Ind. Ct. App. 1999) (citing Eby v. York-Division, Borg-Warner, 455 N.E.2d

623, 626 (Ind. Ct. App. 1983) (citing RESTATEMENT (SECOND) OF CONFLICT OF LAWS §

188 (1971))), reh‟g denied, trans. denied. The location of the subject matter of the

15

contract, also known as the principal location of the insured risk, is given greater weight

than any other single contact in determining the state of the applicable law when that risk

can be located principally in a single state. Id. at 1024-1025. It is also accorded greater

significance when the other factors do not point primarily to one forum. Id. at 1025. The

Indiana Supreme Court has also stated that “[a]n insurance policy is governed by the law

of the principal location of the insured risk during the term of the policy.” Dunn v.

Meridian Mut. Ins. Co., 836 N.E.2d 249, 251 (Ind. 2005).

However, a court need only undergo the analysis above if there is a difference

between the relevant laws of the different states. Hartford Acc. & Indem. Co., 690

N.E.2d at 291 (“[B]efore entangling itself in messy issues of conflict of laws a court

ought to satisfy itself that there actually is a difference between the relevant laws of the

different states.”) (citing Barron v. Ford Motor Co. of Canada Ltd., 965 F.2d 195, 197

(7th Cir. 1992), cert. denied, 506 U.S. 1001, 113 S. Ct. 605 (1992)). “If the purposes and

policies of two potential rules are the same, the forum should apply the forum law.” Id.;

see also Simon v. U.S., 805 N.E.2d 798, 805 (Ind. 2004) (noting that because there was a

conflict between the laws of Indiana and Pennsylvania that was “important enough to

affect the outcome of the litigation,” the Court needed to determine which State‟s law to

apply). In addition, the Indiana Supreme Court has held that Indiana does not engage in

dépeçage, which is “the process of analyzing different issues within the same case

separately under the laws of different states.” Simon, 805 N.E.2d at 801. “Although

Indiana allows different claims to be analyzed separately, it does not allow issues within

16

those counts to be analyzed separately.” Id. (“For example, an Indiana court might

analyze a contract claim and a tort claim independently but would not separately analyze

and apply the law of different jurisdictions to issues within each claim.”).

Here, we conclude that there are differences between the relevant laws of Indiana

and Kentucky that may affect the outcome of the litigation in this case. Specifically, as

discussed in detail in Section I.B.2. of this opinion, Kentucky law differs from Indiana

law with respect to whether late notice, given to an insurer by an insured, of a claim

under an insurance policy that requires prompt notice is presumptively prejudicial to the

insurer. Compare Tri-Etch, Inc. v. Cincinnati Ins. Co., 909 N.E.2d 997, 1005 (Ind. 2009)

(observing that, under Indiana law, late notice is presumptively prejudicial to an insurer),

reh‟g denied; with Jones v. Bituminous Cas. Co., 821 S.W.2d 798, 803 (Ky. 1991)

(observing that, under Kentucky law, “the burden is on the insurance carrier to prove

there was in fact some substantial prejudice caused by the delay in reporting the

occurrence”). Also, as discussed in Section II.D. of this opinion, Kentucky law differs

from Indiana law in the context of this case with respect to the priority of the coverage

provided by two insurance policies where both policies contain excess coverage

provisions.

Because there is a difference between the relevant laws of Indiana and Kentucky

that may affect the outcome of the litigation in this case, we apply the “most intimate

contacts” test as set forth above. See Schaffert by Schaffert, 687 N.E.2d at 232. The

designated evidence reveals that the insured Alpha Leasing was a Kentucky corporation,

17

Alpha Leasing‟s offices were located in Kentucky, Alpha Leasing issued checks from its

Kentucky location, and Alpha Leasing had operations in Kentucky. Also, endorsements

entitled “Kentucky Changes” were added to both the Kentucky Policy and the Empire

Policy. Further, Alpha Leasing‟s application for insurance included a “GEOGRAPHIC

BREAKDOWN” showing sixty vehicles in Kentucky, two vehicles in Indiana, one

vehicle in Florida, and one vehicle in Pennsylvania. It appears that the only contacts

occurring outside the State of Kentucky were the place of the accident, the small number

of vehicles located in other states at the time of contracting, including two vehicles in

Indiana, and the location of the Huntington‟s vehicle return location. Although the

automobile accident which provided the motivation for the declaratory action in this case

occurred in the State of Indiana, we conclude that the principal location of the insured

risk with respect to the declaratory action based upon the insurance contracts at issue was

in the State of Kentucky. While the record is not clear on the place of negotiation, we

conclude based upon the designated evidence contained in the record, and especially in

light of the fact that this court has explained that the most important factor is the principal

location of the insured risk (in this case, Alpha Leasing‟s various vehicles), that

Kentucky is the “state with which the facts are in most intimate contact.” See Hartford

Acc. & Indem. Co., 690 N.E.2d at 291. See also State Farm Mut. Auto. Ins. Co. v.

Conway, 779 F. Supp. 963, 967 (S.D. 1991) (noting that the only contact occurring

outside of the State of Indiana was the place of the accident); Employers Ins., 716 N.E.2d

at 1024 (explaining that the place of performance bears little weight on the choice of law

18

determination where the place of performance is uncertain or unknown at the time of

contracting). Accordingly, Kentucky law applies in this case. See Bedle v. Kowars, 796

N.E.2d 300, 303 (Ind. Ct. App. 2003) (applying the substantive law of Ohio after finding

that Ohio had the most intimate contacts to the litigation); Schaffert, 687 N.E.2d at

234 (applying the “most intimate contacts” test and concluding that Illinois substantive

law was applicable); OVRS Acquisition Corp. v. Cmty. Health Services, Inc., 657 N.E.2d

117, 124 (Ind. Ct. App. 1995) (applying Indiana‟s most intimate contacts choice of law

rule and finding that Kentucky substantive law was applicable because it had the most

intimate contacts to the litigation where the defendant was a Kentucky corporation, the

plaintiff had its principal place of business in Kentucky, and the contract was signed in

Kentucky), reh‟g denied, trans. denied; see also Simon, 805 N.E.2d at 805 (determining

which state‟s law applied where there was a conflict between the states‟ laws important

enough to affect the outcome of the litigation). Further, we apply Kentucky law to every

issue raised with respect to the insurance coverage claims in this case. See Simon, 805

N.E.2d at 801 (holding that Indiana does not engage in “the process of analyzing different

issues within the same case separately under the laws of different states”).

Initially, we review Kentucky law regarding the interpretation of insurance

policies. We observe that under Kentucky law an “insurance policy is a contract.”

Kentucky Ass‟n of Counties All Lines Fund Trust v. McClendon, 157 S.W.3d 626,

631 n.11 (Ky. 2005) (citation omitted); Aetna Cas. & Sur. Co. v. Com., 179 S.W.3d 830,

857 (Ky. 2005). The interpretation and construction of a contract is a matter of law for

19

the courts to decide and is subject to de novo review. 3D Enterprises Contracting Corp.

v. Louisville and Jefferson County Metropolitan Sewer Dist, 174 S.W.3d 440, 448 (Ky.

2005), reh‟g denied. Terms used within insurance contracts should be given their

ordinary meaning as persons with the ordinary and usual understanding would construe

them. Sutton v. Shelter Mutual Insurance Co., 971 S.W.2d 807, 808 (Ky. Ct. App. 1997),

reh‟g denied. In construing an insurance policy, the policy shall be read as a whole.

Fidelity & Cas. Co. of New York v. Cooper, 126 S.W. 111, 113 (Ky. 1910); Sun Life Ins.

Co. v. Taylor, 108 Ky. 408, 56 S.W. 668 (1900).17

Exclusions shall be strictly construed

to make insurance effective. Transport Ins. Co. v. Ford, 886 S.W.2d 901, 904 (Ky. Ct.

App. 1994). Furthermore, it is a fundamental rule in the construction of insurance policy

contracts that the contract shall be liberally construed and any doubts resolved in favor of

the insured. State Farm Mut. Auto. Ins. Co. v. Shelton, 413 S.W.2d 344, 347 (Ky. 1967).

An ambiguous contract is one capable of more than one different, reasonable

interpretation. Cent. Bank & Trust Co. v. Kincaid, 617 S.W.2d 32, 33 (Ky. 1981).

Furthermore, “[i]n the field of insurance law recognition frequently has been given

to the principle that an insurance company may not rely upon a noncompliance by the

insured with a condition of the policy if the company has sustained no prejudice by

17

We note that prior to 1976, the Kentucky Court of Appeals was the highest court in Kentucky.

As a result of constitutional amendments which became effective in 1976, the Kentucky Supreme Court

became the highest court in Kentucky and the Kentucky Court of Appeals became an intermediate

appellate court. See K.Y. Const. of 1891, §§ 109-124, as amended by 1974 Ky. Acts. Ch. 84, §§ 1-3

(effective Jan. 1, 1976).

20

reason of the noncompliance.” Newark Ins. Co. v. Ezell, 520 S.W.2d 318, 321 (Ky.

1975).

We turn now to the issues raised by Kentucky National and Empire Fire.

I.

The first issue raised on appeal is whether the trial court erred in ruling on the

summary judgment motions of Kentucky National and Alpha Leasing. Kentucky

National appears to argue that the trial court erred in denying its motion for summary

judgment because: (A) the Kentucky Policy did not cover the Vehicle; (B) Alpha Leasing

failed to comply with terms of the Kentucky Policy; and (C) Alpha Leasing concealed or

misrepresented material facts. We address each argument separately.

A. Coverage of the Vehicle under the Kentucky Policy

Kentucky National argues that the trial court erred in denying its motion for

summary judgment and Alpha Leasing‟s motion for summary judgment regarding

coverage of the Vehicle under the Kentucky Policy.

The Kentucky Policy provided that Kentucky National “will pay all sums an

„insured‟ legally must pay as damages because of „bodily injury‟ or „property damage‟ to

which this insurance applies, caused by an „accident‟ and resulting from the ownership,

maintenance or use of a covered „auto.‟” Appellant‟s Supplemental Appendix at 10. The

Declarations page of the Kentucky Policy indicated that Alpha Leasing purchased

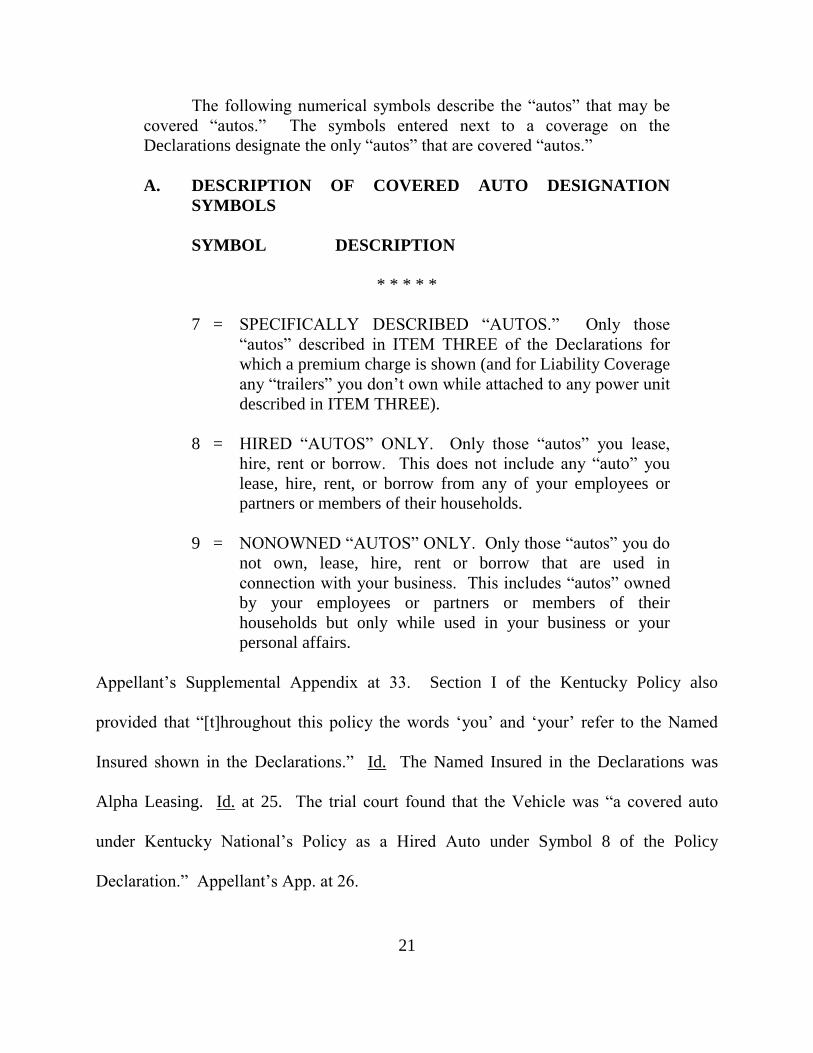

liability insurance for covered autos described in Symbols 7, 8, and 9. Section I of the

Kentucky Policy, entitled “COVERED AUTOS,” provided in relevant part:

21

The following numerical symbols describe the “autos” that may be

covered “autos.” The symbols entered next to a coverage on the

Declarations designate the only “autos” that are covered “autos.”

A. DESCRIPTION OF COVERED AUTO DESIGNATION

SYMBOLS

SYMBOL DESCRIPTION

* * * * *

7 = SPECIFICALLY DESCRIBED “AUTOS.” Only those

“autos” described in ITEM THREE of the Declarations for

which a premium charge is shown (and for Liability Coverage

any “trailers” you don‟t own while attached to any power unit

described in ITEM THREE).

8 = HIRED “AUTOS” ONLY. Only those “autos” you lease,

hire, rent or borrow. This does not include any “auto” you

lease, hire, rent, or borrow from any of your employees or

partners or members of their households.

9 = NONOWNED “AUTOS” ONLY. Only those “autos” you do

not own, lease, hire, rent or borrow that are used in

connection with your business. This includes “autos” owned

by your employees or partners or members of their

households but only while used in your business or your

personal affairs.

Appellant‟s Supplemental Appendix at 33. Section I of the Kentucky Policy also

provided that “[t]hroughout this policy the words „you‟ and „your‟ refer to the Named

Insured shown in the Declarations.” Id. The Named Insured in the Declarations was

Alpha Leasing. Id. at 25. The trial court found that the Vehicle was “a covered auto

under Kentucky National‟s Policy as a Hired Auto under Symbol 8 of the Policy

Declaration.” Appellant‟s App. at 26.

22

Kentucky National argues that the Vehicle was not covered under Symbol 8

because the evidence does not show that the Vehicle was leased, borrowed, or rented by

Alpha Leasing. With respect to its argument that Alpha Leasing did not “lease” the

Vehicle under Symbol 8, Kentucky National argues that “Alpha was neither the „Lessee‟

nor the „Lessor‟ under the existing lease agreement . . . .” Appellant‟s Brief at 17.

Kentucky National further argues that if Alpha Leasing had borrowed the Vehicle from

Carney for the purpose of returning it to Huntington, Alpha Leasing was no longer

borrowing the Vehicle at the time of the accident because it “kept the Vehicle longer than

the five (5) days authorized under Carney‟s lease.” Id. Kentucky National also appears

to argue that Symbol 9 does not cover the Vehicle because “there is a fact question as to

whether, at the time of the Accident, Royse was using the Vehicle in connection with

Alpha‟s business.” See id. at 18.

Empire Fire argues that “Alpha Leasing had temporary possession of the Vehicle,

and the right to exercise control over the Vehicle, following Carney‟s return of the

Vehicle, and pursuant to the Operating Agreement with [Huntington], which expressly

delegated responsibility for the Vehicle to Alpha Leasing.” Appellee/Cross-Appellant

Empire Fire‟s Brief at 27. Huntington argues that the Vehicle “was a covered auto under

either Symbol 8 or Symbol 9.” Appellee Huntington‟s Brief at 11. Alpha Leasing argues

that the Vehicle was a covered auto under either Symbol 8 or Symbol 9 and that

Kentucky National failed to show that “Alpha Leasing‟s connection with this vehicle [is

23

anything] other than as part of its business as a leasing broker.” Appellee Alpha

Leasing‟s Brief at 18.

Alpha Leasing purchased liability coverage for vehicles that would be covered

under the terms of either Symbol 8 or Symbol 9 of Section I.A. of the Kentucky Policy.

Symbol 8, the “hired autos” provision, provided coverage for vehicles which Alpha

Leasing “lease[d], hire[d], rent[ed] or borrow[ed].” Appellant‟s Supplemental Appendix

at 33. Terms used within insurance contracts should be given their ordinary meaning as

persons with the ordinary and usual understanding would construe them. See Sutton, 971

S.W.2d at 808. The term “borrow” has been defined as: “To obtain or receive

(something) on loan with the promise or understanding of returning it or its equivalent.”

THE AMERICAN HERITAGE DICTIONARY OF THE ENGLISH LANGUAGE 214 (4th ed. 2006).

See Vinson v. Gobrecht, 560 S.W.2d 242, 243 (Ky. Ct. App. 1977) (noting that the

appellant/bailee borrowed an automobile from the appellee/bailor); see also Payne v.

Terry, 367 S.W.2d 277, 279 (Ky. 1963) (referring to a dictionary for the definition of the

term “borrow” as used in another context).

Here, Alpha Leasing did “borrow” the Vehicle given the ordinary meaning of that

term. In December 2003, prior to the scheduled expiration/maturity of the lease term for

the Vehicle, Carney returned the Vehicle to Ward at Alpha Leasing, and Carney leased a

new vehicle through Ward at Alpha Leasing. Carney, who had leased vehicles through

Ward and Alpha Leasing on previous occasions, testified that he and Ward “would just

swap cars there, sign the papers on the new car, and that would be it.” Appellant‟s

24

Appendix at 101. Carney also testified that Ward “delivers cars, takes cars away,

paperwork is simple, it‟s in order, ready to go; we move on.” Id. at 102. Under the

Operating Agreement, Alpha Leasing was “engaged in the business of arranging and

making leases of motor vehicles available to the public.” Appellant‟s Supplemental

Appendix at 68; Appellant‟s Appendix at 176. Alpha Leasing was required, prior to

delivery of a vehicle to a lessee, to verify that the lessee had in effect insurance for the

motor vehicle. Alpha Leasing was solely responsible for the condition and performance

of all vehicles and for the sale, disposal, or trade-in of any vehicle. Thus, the Operating

Agreement contemplated that Alpha Leasing would have temporary possession of

vehicles leased pursuant to its terms both prior to the delivery of the vehicles to lessees

and perhaps after lessees returned the vehicles to Alpha Leasing for ultimate delivery to

one of Huntington‟s auction locations.

Similarly, under Huntington‟s vehicle return waiver, Alpha Leasing was

authorized to pick up a vehicle from a lessee and return the vehicle by appointment to one

of Huntington‟s auction locations. The return policy also stated that “Alpha Leasing may

only return vehicles on behalf of the lessee . . . provided the lease has reached maturity.

This policy does not apply to vehicles being returned by lessees prior to lease maturity.”

Appellant‟s Appendix at 181.18

Thus, under the provisions of Huntington‟s vehicle

18

Kentucky National argues that Alpha Leasing was no longer borrowing the Vehicle at the time

of the accident because it “kept the Vehicle longer than the five (5) days authorized under Carney‟s

lease.” Appellant‟s Brief at 17. However, the record does not show that Carney authorized Alpha

Leasing to possess the Vehicle for only five days under the terms of the Vehicle‟s lease or otherwise

limited Alpha Leasing‟s possession of the Vehicle when he returned the Vehicle. The five-day rule

referred to by Kentucky National was found in Huntington‟s vehicle return policy, which stated that

25

return policy, it appears that Alpha Leasing was not required to return a vehicle to

Huntington if the lease for that vehicle had not yet reached maturity. The return policy

required Alpha Leasing to carry adequate insurance coverage for the care and custody of

any vehicle while in its possession. Thus, Huntington‟s vehicle return policy

contemplated that Alpha Leasing may have temporary possession of vehicles leased

pursuant to the terms of the Operating Agreement, including after lessees returned the

vehicles to Alpha Leasing either at or before the maturity of the vehicle leases. Under the

circumstances, we conclude that the language in Symbol 8 of the Kentucky Policy

covering “those „autos‟ you . . . borrow” included the Vehicle at the time of the accident.

In addition, the phrase “you lease” in Symbol 8 was capable of more than one

reasonable interpretation. The phrase “you lease” could reasonably be interpreted, as

Kentucky National argues, to include only those vehicles which were leased pursuant to a

lease agreement under which Alpha Leasing was the named lessor. However, on the

other hand, under the circumstances the phrase may also be reasonably interpreted to

include those vehicles for which Alpha Leasing arranged leases pursuant to its Operating

Agreement with Huntington. See Appellant‟s Appendix at 176-177 (Operating

Agreement provided that Alpha Leasing was “engaged in the business of arranging and

“Alpha Leasing will be responsible for ensuring the vehicle is returned within (5) business days of pick

up and that adequate insurance coverage is carried to cover the care and custody of the vehicle while in

their possession.” Appellant‟s Supplemental Appendix at 73; Appellant‟s Appendix at 181. However,

the return policy also stated: “Alpha Leasing may only return vehicles on behalf of the lessee, as outlined

in the provisions below, provided the lease has reached maturity. This policy does not apply to vehicles

being returned by lessees prior to lease maturity.” Id. Kentucky National does not point to evidence that

Alpha Leasing was in possession of the Vehicle without the permission of either Carney or Huntington

after Carney returned the Vehicle to Alpha Leasing and at the time of the accident.

26

making leases of motor vehicles available to the public” and that Alpha Leasing “entered

into [lease agreements] on behalf of Huntington . . . in accordance with the provisions of

this Agreement.”); Appellant‟s Appendix at 43, 48 (the vehicle‟s lease was signed by

Robert Leidgen, the owner of Alpha Leasing, on behalf of Alpha Leasing and

Huntington). Because the language in Symbol 8 of the Kentucky Policy covering “those

„autos‟ you lease” was “capable of more than one different, reasonable interpretation,”

Central Bank & Trust Co., 617 S.W.2d at 33, the language was ambiguous, and we must

liberally construe the policy and resolve any doubts in favor of Alpha Leasing as the

insured. State Farm Mut. Auto. Ins. Co., 413 S.W.2d at 347. Thus, Symbol 8 of the

Kentucky Policy also covered the Vehicle as one of “those „autos‟ [Alpha Leasing]

lease[d].”

We conclude that the Vehicle driven by Royse at the time of the accident was a

covered auto under Symbol 8 of the Kentucky Policy.19

The trial court did not err in

granting summary judgment to Alpha Leasing on the issue that the Kentucky Policy

provided coverage for the Vehicle as a covered auto.

B. Failure to Comply with Terms of the Kentucky Policy

19

With respect to Symbol 9 of the Kentucky Policy, Empire Fire argues that Kentucky National

failed to designate admissible evidence supporting its argument that the Vehicle was not used “in

connection with” Alpha Leasing‟s business at the time of the accident because Ward‟s testimony that he

had a discussion with Royse about a year after the accident and that Royse said that he had an errand to

run in Indiana to pick up some air conditioner equipment was inadmissible hearsay. Huntington argues

that Ward‟s testimony was inadmissible hearsay testimony and that the phrase “in connection with” is

broad enough to include the Vehicle even if Royse did run an errand on his way to the auto auction.

Because we find that the Vehicle was a covered auto under Symbol 8 of the Kentucky Policy, we need not

address the parties‟ arguments regarding whether the Vehicle was covered under Symbol 9 of the

Kentucky Policy.

27

Kentucky National next argues that the trial court erred in denying its motion for

summary judgment upon the basis that Alpha Leasing failed to comply with terms of the

Kentucky Policy. Specifically, Kentucky National argues that Alpha Leasing and Royse:

(1) did not provide Kentucky National with prompt notice of the accident; (2) failed to

cooperate with Kentucky National; and (3) failed to permit inspection of the Vehicle and

records showing loss.

1. Failure to Provide Notice

Kentucky National argues that Section IV.A.2.a. of the Kentucky Policy “clearly

and unambiguously required Alpha to promptly notify Kentucky National of the accident

and Speakes‟ and Alpha‟s claims. Alpha‟s untimely notice fails to comply with a

condition precedent for coverage.” Appellant‟s Brief at 11. Kentucky National argues

that Alpha Leasing‟s “failure to give Kentucky National reasonably prompt notice of the

accident prejudiced Kentucky National‟s ability to investigate Alpha‟s claim and to

defend this current action (as well as the parallel tort action).” Id. at 12. Specifically,

Kentucky National appears to argue that it was prejudiced because, had Alpha Leasing

given it notice prior to the date that it did, Kentucky National “could have asked [Royse]

questions that might have shed light on the coverage issues pertinent to Kentucky

National‟s investigation and evaluation” and could have obtained information from

papers and documents that were misplaced and from witnesses whose memories have

faded. Id.

28

Alpha Leasing argues Kentucky National “fails to cite to this Court what papers or

documents it believes are missing or to explain to this Court how those papers or

documents are „important‟ to this case.” Appellee Alpha Leasing‟s Brief at 12. In

addition, Alpha Leasing argues that “[a]ny alleged notice issues were not initially raised

by Kentucky National as causing any prejudice to the company.” Id. at 11-12. Alpha

Leasing also argues that Kentucky National “may not sit on its hands” by not

participating in the defense of Alpha Leasing or Royse from March 2005 until September

2008 and “then complain about how the case was defended by others.” Id. at 14. Empire

Fire argues that “Kentucky National failed to designate any evidence to the trial court

suggesting that it was prejudiced by the timing of Alpha Leasing‟s notice of the

Accident.” Appellee/Cross-Appellant Empire Fire‟s Brief at 30. Huntington adopts the

arguments of Alpha Leasing and Empire Fire with respect to the issue of notice.

Section IV.A.2.a. of the Kentucky Policy stated:

In the event of “accident”, claim, “suit” or “loss”, you must give us or our

authorized representative prompt notice of the “accident” or “loss”.

Include:

(1) How, when and where the “accident” or “loss” occurred;

(2) The “insured‟s” name and address; and

(3) To the extent possible, the names and addresses of any

injured persons and witnesses.

Appellant‟s Supplemental Appendix at 39.

Initially, we compare the relevant laws of Indiana and Kentucky pertaining to late

notice given by an insured to an insurer of a claim under an insurance policy that requires

prompt notice. Under Indiana law, a finding of prejudice to the insurer from the

29

insured‟s violation of a policy provision relieves the insurer from providing coverage

under the insurance contract. Tri-Etch, Inc., 909 N.E.2d at 1005. The Indiana Supreme

Court recently observed that American jurisdictions fall into three groups on the need to

establish prejudice from late notice. Id. at 1004. “Some hold that prejudice is irrelevant

to enforcement of a late notice defense. Others require an insurer asserting this defense

to demonstrate actual prejudice, and a third group creates a rebuttable presumption of

prejudice in favor of the insurer.” Id. at 1004-1005. “Indiana is generally placed in the

third category . . . .” Id. at 1005; see also Dreaded, Inc. v. St. Paul Guardian Ins. Co., 904

N.E.2d 1267, 1272 (Ind. 2009) (noting that Indiana is among the few jurisdictions that

employ a presumption of prejudice analysis); Charles C. Marvel, Annotation, MODERN

STATUS OF RULES REQUIRING LIABILITY INSURER TO SHOW PREJUDICE TO ESCAPE

LIABILITY BECAUSE OF INSURED‟S FAILURE OR DELAY IN GIVING NOTICE OF ACCIDENT

OR CLAIM, OR IN FORWARDING SUIT PAPERS, 32 A.L.R.4th 141 § 2 (1984, Supp. 2008)

(summarizing variations among decisions in different jurisdictions regarding the

requirement of prejudice).

Thus, under Indiana law, late notice is presumptively prejudicial to an insurer. See

Tri-Etch, Inc., 909 N.E.2d at 1005 (citing Miller v. Dilts, 463 N.E.2d 257 (Ind. 1984)).

However, an “injured party can establish some evidence that prejudice did not occur in

the particular situation.” Miller, 463 N.E.2d at 265. “Once such evidence is introduced,

the question becomes one for the trier of fact to determine whether any prejudice actually

30

existed. The insurance carrier in turn can present evidence in support of its claim of

prejudice.” Id. at 265-266.

Kentucky courts have also considered whether, and under what circumstances,

failure to provide prompt notice of loss to an insurance company would defeat the

insurer‟s obligation to provide coverage. See Jones, 821 S.W.2d at 801. In Jones, the

Kentucky Supreme Court held that an insurer may not deny coverage because an insured

failed to provide prompt notice of loss unless the insurer can prove that it is reasonably

probable that it suffered substantial prejudice from the delay in notice. 821 S.W.2d at

802-803. The court also held that “the burden is on the insurance carrier to prove there

was in fact some substantial prejudice caused by the delay in reporting the occurrence.”

Id. at 803. Summary judgment is appropriate on the issue of prejudice only where proof

of prejudice is conclusive or there is failure of proof on the subject. Id.; see also Best v.

West American Ins. Co., 270 S.W.3d 398, 405 (Ky. Ct. App. 2008) (“Pursuant to Jones v.

Bituminous Cas. Corp., 821 S.W.2d 798, 802 (Ky. 1991), an insurer may not deny

coverage because the insured failed to provide prompt notice of loss unless the insurer

can prove that it is reasonably probable that it suffered substantial prejudice from the

delay in notice.”), reh‟g denied.

In this case, if we were to apply Indiana law, there would be a presumption that

any late notice given by Alpha Leasing was prejudicial to Kentucky National. See Tri-

Etch, Inc., 909 N.E.2d at 1005. However, if Alpha Leasing designated any evidence to

the trial court showing that Kentucky National did not suffer prejudice in this particular

31

situation, then the question would become one for the trier of fact. See Miller, 463

N.E.2d at 265-266. On the other hand, under Kentucky law, Kentucky National as the

insurer bears the burden of proving that it is reasonably probable that it suffered

substantial prejudice from the delay in notice. See Jones, 821 S.W.2d at 802-803. If

Kentucky National failed to designate facts establishing that it suffered such prejudice,

then summary judgment is inappropriate. See id. at 803. Because there is a difference

between the law of Indiana and Kentucky which may affect the outcome of the litigation

in this case, we apply the law of the State of Kentucky, as previously discussed, because

it is the “state with which the facts are in most intimate contact.” See Hartford Acc. &

Indem. Co., 690 N.E.2d at 291.

Here, the designated evidence reveals that on July 13, 2004, Todd Royse, who had

been hired to drive the Vehicle from Alpha Leasing‟s office in Louisville, Kentucky, to

Huntington‟s vehicle return location in Clarksville, Indiana, was involved in an

automobile accident in southern Indiana with a vehicle driven by Julie Speakes. The

designated evidence also shows that on March 9, 2005, Alpha Leasing sent an automobile

loss notice to Kentucky National regarding the accident involving the Vehicle. The

automobile loss notice stated that “[Empire Fire] is claiming that they are not liable for

this claim.” Appellant‟s Appendix at 159; Appellant‟s Supplemental Appendix at 75.

Thus, Alpha Leasing notified Kentucky National of the accident involving the Vehicle

almost eight months after the accident occurred.

32

Our review of the record reveals that Kentucky National did not designate

evidence establishing that it suffered prejudice as a result of Alpha Leasing‟s allegedly

late notice of the accident involving the Vehicle.20

With respect to Kentucky National‟s

argument that Alpha Leasing did not provide it with prompt notice and that such late

notice prejudiced its ability to interview witnesses, including Royse, or that witnesses‟

memories have faded, Kentucky National did not designate evidence establishing that any

of the witnesses to the accident were unavailable. According to the police report, which

was designated, Speakes was driving the vehicle that was in the collision with the

Vehicle driven by Royse. Also, the police report provided the name and contact

information for a witness who was behind the Vehicle and observed the collision.

Kentucky National does not designate evidence showing that Speakes or the witness who

observed the collision were unavailable or that their memories have faded. In addition,

with respect to Royse, Kentucky National includes in its appellant‟s appendix a copy of

requests for admissions which were to be submitted to Royse. However, we observe that

Kentucky National did not designate any evidence showing that it submitted its requests

20

We observe that cases in Indiana and Kentucky have indicated that notice given by an insured

to an insurer over seven months after an accident occurs may constitute late notice. See Miller v. Dilts,

463 N.E.2d 257, 265 (Ind. 1984) (observing that notice given almost seven months after an accident

occurred did not constitute timely notice); Jones v. Bituminous Cas. Corp., 821 S.W.2d 798, 800 (Ky.

1991) (noting that the trial court determined that notice given to an insurer six and one-half months after

the claim arose did not constitute prompt notice).

33

for admissions to Royse, that Royse received its requests, or that Royse failed to timely

respond to its requests.21

With respect to Kentucky National‟s argument that Alpha Leasing did not provide

it with prompt notice and that such late notice prejudiced its ability to obtain documents

that may have been misplaced, it does not appear that Kentucky National designated

evidence establishing which and how particular documents would have assisted its

defense of Alpha Leasing and Royse. In support of its argument that “papers and

documents” were misplaced, Kentucky National cites to a portion of Ward‟s deposition

in which Ward is questioned about various documents relating to the Vehicle. However,

Ward‟s testimony set forth in the designated portion of his deposition pertains to

particular documents, specifically a vehicle return waiver and an odometer statement, that

were to be completed by Alpha Leasing in connection with the return or delivery of the

Vehicle to Alpha Leasing by Carney. Completion of those two documents was required

by the Operating Agreement and appear to relate to Carney‟s early termination of the

lease of the Vehicle and perhaps to the calculation of possible costs/fees under the

Vehicle‟s lease. The documents do not appear to relate to the accident involving the

Vehicle. Kentucky National does not explain, nor can we determine, how a more timely

notice of the accident by Alpha Leasing would have preserved those two documents or

how those documents would have assisted Kentucky National in its defense of Alpha

21

Apparently Huntington also submitted requests for admissions to Royse. However, no

evidence was designated showing that Royse received or failed to respond to those requests for

admissions either.

34

Leasing or Royse in the Speakes Lawsuit. Based upon our review of the documents we

cannot say that it was reasonably probable that Kentucky National suffered “substantial

prejudice” by any such delay.22

See Rosi v. Business Furniture Corp., 615 N.E.2d 431,

434 (Ind. 1993) (observing that appellate courts are prohibited “from reversing summary

judgment orders on the ground that there is a genuine issue of material fact unless the

material facts and relevant evidence were specifically designated to the trial court.”);

Rood v. Mobile Lithotripter of Indiana, Ltd., 844 N.E.2d 502, 506 (Ind. Ct. App. 2006)

22

We note that the parties discuss correspondence between Empire Fire and Kentucky National

dated March 23, 2006, and between an attorney representing Alpha Leasing and Kentucky National dated

May 30, 2006, and June 6, 2006, regarding coverage under the Kentucky Policy. However, that

correspondence was not designated by Kentucky National. (The letters were attached to Alpha Leasing‟s

response to Kentucky‟s summary judgment motion, and only the March 23, 2006, letter was referenced in

the response filing.)

In its correspondence dated June 6, 2006, Kentucky National stated that it had sent faxes to Alpha

Leasing‟s insurance agent on May 25, 2005, and May 26, 2005, requesting information regarding the

reason the accident was not reported to Kentucky National earlier, “an explanation of who Todd Royse

was,” a “copy of the lease,” information regarding “what charges were filed against Mr. Royse,” and “the

portion of the policy that he felt would afford coverage for this accident.” See Appellee‟s Appendix at

32. Even if the June 6, 2006, letter had been designated, the information contained in the letter does not

appear to establish that Alpha Leasing provided notice to Kentucky National prior to March 9, 2005. Nor

does the information in the letter appear to establish any facts indicating that Kentucky National did or

did not suffer prejudice as a result of receiving notice of the accident involving the Vehicle approximately

seven and one-half months after the accident.

Kentucky National also appears to argue that it was prejudiced by the defense initially provided

by Empire Fire to Alpha Leasing and Royse. Specifically, Kentucky National states that “[i]nitially,

Empire hired two lawyers from the same law firm to represent both [Alpha Leasing] and Royse” and that

“[d]espite the obvious conflict of interest . . . [,] counsel employed by Empire filed a single Answer for

both Alpha and Royse alleging (to Alpha‟s disadvantage) that Royse was an agent of Alpha in one part of

the Answer and denying (to Royse‟s disadvantage) that Royse was not an agent of Alpha.” Appellant‟s

Brief at 13. Kentucky National acknowledges that Empire has since provided separate counsel for Alpha

Leasing and Royse. Kentucky National fails to develop its argument, cite to authority, or point to any

designated evidence in support of its argument that the conflict of interest, which may have existed when

two attorneys who practiced at the same law firm represented Alpha Leasing and Royse, prejudiced

Kentucky National. Therefore, this argument is waived. See Loomis v. Ameritech Corp., 764 N.E.2d

658, 668 (Ind. Ct. App. 2002) (holding argument waived for failure to cite authority or provide cogent

argument), reh‟g denied, trans. denied.

35

(“On appeal, we may not reverse a ruling on summary judgment on the ground that there

is a genuine issue of material fact unless the material fact and the relevant evidence have

been specifically designated to the trial court”).

We do acknowledge that Alpha Leasing did not designate evidence establishing

that Speakes, Royse, and the witness of the collision who was identified in the police

report were available, that their memories have not faded, or that other information

contained in documents to be retained by Alpha Leasing was not misplaced. However,

under Kentucky law, Kentucky National as the insurer bore the burden of proving that it

was reasonably probable that it suffered substantial prejudice from the delay in notice.

See Jones, 821 S.W.2d at 802-803.

In summary, our review of the record does not reveal designated evidence

establishing that Kentucky National suffered substantial prejudice as a result of receiving

notice of the accident involving the Vehicle approximately eight months after the

accident. As a result, we cannot say that the trial court erred in denying Kentucky

National‟s motion for summary judgment on this basis. See, e.g., Jones, 821 S.W.2d at

803 (reversing the trial court‟s grant of summary judgment and observing that

“[s]ummary judgment is appropriate on the issue of prejudice only where proof of

prejudice is conclusive or there is failure of proof on the subject”); Best, 270 S.W.3d at

405 (noting that an insurance company failed to cite any evidence showing that it

suffered substantial prejudice from a delay in notice from its insured and finding

therefore that summary judgment was not warranted).

36

2. Failure to Cooperate

Kentucky National argues that Alpha Leasing and Royse failed to cooperate with

Kentucky National as required by the Kentucky Policy. Specifically, Kentucky National

argues that because “[a]llegations have been filed . . . claiming that Royse is an „insured‟

under Kentucky National‟s policy . . . [,] the „cooperation‟ requirement of Kentucky

National‟s policy is in force as to Royse . . . .” Appellant‟s Brief at 14. Alpha Leasing

argues that “Kentucky National has argued throughout this case . . . that Alpha Leasing is

not responsible for the actions of Mr. Royse . . . . Kentucky National cannot now lump

together Royse and Alpha Leasing as relates to its cooperation clause.” Appellee Alpha

Leasing‟s Brief at 14. Alpha Leasing also argues that “Kentucky National is in no

position to complain about a lack of cooperation when it has failed to provide a defense

in this matter.” Id. Empire Fire appears to argue that Kentucky National failed to

designate any evidence to the trial court in support of its contention that Alpha Leasing

failed to comply with any cooperation requirement in the Kentucky Policy. Huntington

adopts the arguments of Alpha Leasing and Empire Fire with respect to the issue of

cooperation.

Section IV.A.2.b. of the Kentucky Policy, part of sub-section A entitled Loss

Conditions, stated:

Additionally, you and any other involved “insured” must:

* * * * *

37

(2) immediately send us copies of any request, demand, order,

notice, summons or legal paper received concerning the claim

or “suit”;

(3) Cooperate with us in the investigation, settlement or defense

of the claim or “suit”; . . . .

Appellant‟s Supplemental Appendix at 39.

Initially, we note that Kentucky National does not develop a cogent argument or

cite to any authority in support of its argument that Alpha Leasing is not entitled to

coverage as an insured under the Kentucky Policy even if Royse did or were to fail to

cooperate in Kentucky National‟s defense of him. Therefore, Kentucky National‟s

argument that Alpha Leasing failed to comply with the general cooperation provision of

the Kentucky Policy is waived. See Loomis v. Ameritech Corp., 764 N.E.2d 658, 668

(Ind. Ct. App. 2002) (holding argument waived for failure to cite authority or provide

cogent argument), reh‟g denied, trans. denied. Even if Kentucky National did not waive

its argument with respect to Alpha Leasing, we observe that Kentucky National does not

point us to any designated evidence showing that Alpha Leasing failed to cooperate with

any investigation by or defense provided by Kentucky National.23

Therefore, the trial

court properly denied Kentucky National‟s motion for summary judgment upon the basis

that Alpha Leasing failed to cooperate with Kentucky National.

With respect to Royse, it does not appear that Kentucky National designated

evidence establishing that Royse failed to cooperate with any investigation by or defense

23

We note that the record shows that the Speakes Lawsuit was filed on May 23, 2006, and that

Alpha Leasing sent a letter by its attorney to Kentucky National together with a copy of the complaint and

related documents with respect to the Speakes Lawsuit on May 30, 2006.

38

provided by Kentucky National. As previously mentioned, Kentucky National includes

in its appellant‟s appendix a copy of requests for admissions which were to be submitted

to Royse. However, Kentucky National did not designate any evidence showing that it

submitted its requests for admissions to Royse, that Royse received its requests, or that

Royse failed to timely respond to its requests. Also, no evidence was designated showing

that Royse received or failed to respond to requests for admissions submitted by

Huntington. Moreover, also as previously mentioned, Kentucky National did not

designate evidence establishing that the other witnesses to the accident were unavailable.

We also note that the designated police report shows that a witness observed the collision

involving Speakes‟s vehicle and the vehicle driven by Royse. Even if Royse did fail to

respond to requests for admissions or failed to participate in this case, Kentucky National

did not designate evidence to the trial court showing that such a failure or absence by

Royse did or would constitute a substantial violation of the cooperation clause found in

the Kentucky Policy sufficient to void coverage as a matter of law.

Based upon the designated evidence, we cannot say that Kentucky National

established that Royse failed to cooperate with any investigation or defense that

Kentucky National may have undertaken on his behalf. Nor did Kentucky National

designate evidence showing that it suffered any prejudice as a result of Royse‟s alleged

failure to cooperate. As a result, and construing all facts and reasonable inferences drawn

from those facts in favor of the nonmovants, we conclude that the trial court properly

denied Kentucky National‟s motion for summary judgment upon the basis that Royse

39

failed to cooperate with Kentucky National. See Newark Ins. Co., 520 S.W.2d at

321 (noting that there was no claim by the insurer that any of the legitimate protective

purposes of the policy condition at issue was impaired or that the insurer suffered any

prejudice from the alleged noncompliance of the insured); Western Farm Bureau Mut.

Ins. Co. v. Danville Const. Co., 463 S.W.2d 125, 128-130 (Ky. 1971) (concluding that

factual material submitted to the trial court of the insured‟s failure or refusal to attend a

trial or appear as a witness was not sufficient to support a conclusion that there was a

substantial violation of the cooperation clause by the insured, and observing that various

factors of materiality, diligence on the insurer‟s part, or the excusability of the absence

from the insured‟s point of view, have rarely been regarded as individually controlling

and typically present a question of fact for the jury); see also Rosi, 615 N.E.2d at 434

(observing that we may not reverse summary judgment unless the relevant evidence was

“specifically designated to the trial court.”); Rood, 844 N.E.2d at 506 (noting that “we

may not reverse a ruling on summary judgment on the ground that there is a genuine

issue of material fact unless the material fact and the relevant evidence have been

specifically designated to the trial court.”).

3. Failure to Permit Inspections

Kentucky National argues that Alpha Leasing failed to permit inspection of the

Vehicle and records proving loss as required by the Kentucky Policy. Specifically,

Kentucky National argues that it was not notified of the accident before the Vehicle was

repaired and “is unable to gather important details regarding the Vehicle and the Accident

40

– such as significant odometer readings, and the „vehicle return waiver.‟” Appellant‟s

Brief at 16. Alpha Leasing argues that the provision in the Kentucky Policy requiring

inspection “relates to claims to property damage not personal injury” and that Kentucky

National “does not cite this Court to any particular documents which it claims are missing

and relevant to the coverage issues in this case.” Appellee Alpha Leasing‟s Brief at 15.

Alpha Leasing also argues: “What possible value or difference could the „post accident‟

actions of these parties play in the coverage issues with regard to the accident of July 13,

2004? . . . What Alpha and Huntington did afterwards with regard to liquidating this

vehicle at the auto auction is immaterial.” Id.

Section IV.A.2.c. of the Kentucky Policy, also part of sub-section A entitled Loss

Conditions, stated:

If there is “loss” to a covered “auto” or its equipment you must also do the