KCM Q32010

14

Kinnaras Capital Management LLC www.kinnaras.com 225 Flax Hill Road • Suite 1 • Norwalk, CT 06854 • Phone: 203-252-7654 • Fax: 860-529-7167 ____________________________________________________________________________________________________ Page 1 of 14 1/31/ 2010 2/ 28/2 01 0 3/ 31 /2 010 4/ 30 /201 0 5/ 31/ 20 10 6/ 30 /2 010 7/ 31/2 01 0 8/31/ 2010 9/ 30 /2 01 0 KCM Net Performance -1.27% 4.61% 6.37% 2.03% -7.42% -8.06% 4.41% -6.26% 11.45% DJIA -3.30% 2.90% 5.30% 1.50% -7.60% -3.40% 7.20% -3.90% 7.90% SP500 -3.60% 3.10% 6.00% 1.60% -8.00% -5.20% 7.00% -4.50% 8.90% NASDAQ -5.30% 4.30% 7.20% 2.70% -8.20% -6.50% 6.90% -6.24% 12.04% Q1 2010 Q2 2010 Q3 20210 YTD 2010 KCM Net Performance 9.86% -13.16% 9.08% 4.06% DJIA 4.78% -9.40% 11.16% 5.52% SP500 5.35% -11.39% 11.28% 3.88% NASDAQ 5.88% -11.85% 12.30% 4.81% November 1, 2010 Dear Investors, Kinnaras Capital Management ("KCM", "Kinnaras", or the "Firm") Separately Managed Accounts ("SMAs") returned 9.1% net in Q3 2010. Table I presents KCM SMA performance r elative to key indices. Investors should note that individual ret urns will vary based on the time one invested and that the composite return presented below is net of fees and is the time-weighted return ("TWR") of all Kinnaras SMAs. TWR is one of the most comprehensive and accurate way of gauging investment performance for managed accounts but can be skewed at times due to the timing of new portfolio openings. TABLE I: 2010 MANAGED ACCOUNT PERFORMANCE The great economist John Kenneth Galbraith said "It is a far, far better thing to have a firm anchor in nonsense than to be put out on the tr oubled seas of thought." That essentially encapsulates the current dialogue regarding economic policy. Deficit hawks have captured the debate amongst western countries and institutions and are imposing harsh austerity measures when government investment programs are the most expedient ways to generate legitimate "escape velocity" for the economy. What's particularly disheartening is that deficit hawks have been able to generate a high level of acceptance of their ideas when much of what they advocate for has been discredited by current empirical evidence. Ireland provides a g ood example of austerity i n action as it was one of the first countries to adopt aggressive deficit reduction measures. Ireland intends to reduce its deficit from 12% of GDP to <3% by 2014. Despite GDP that contracted by 7.1% in 2009, the country adopted no stimulus measures, with the government imposing three slash and burn budgets. 1 The expectation was that Ireland would take its medicine early on and recover faster by implementing heavy handed spending cuts. Deficit reduction proponents believe that during r ecessionary times, reducing government spending will send a signal to credit markets that the country is focused on paring 1 http://www.guardian.co.uk/bus iness/2010/sep/23/ire land-austerity- budgets-comment

-

Upload

amitchokshi2353 -

Category

Documents

-

view

225 -

download

0

Transcript of KCM Q32010

8/8/2019 KCM Q32010

http://slidepdf.com/reader/full/kcm-q32010 1/14

Kinnaras Capital

Management LLCwww.kinnaras.com

225 Flax Hill Road • Suite 1 • Norwalk, CT 06854 • Phone: 203-252-7654 • Fax: 860-529-7167

____________________________________________________________________________________________________Page 1 of 14

1/31/2010 2/28/2010 3/31/2010 4/30/2010 5/31/2010 6/30/2010 7/31/2010 8/31/2010 9/30/2010

KCM Net Performance -1.27% 4.61% 6.37% 2.03% -7.42% -8.06% 4.41% -6.26% 11.45%

DJIA -3.30% 2.90% 5.30% 1.50% -7.60% -3.40% 7.20% -3.90% 7.90%

SP500 -3.60% 3.10% 6.00% 1.60% -8.00% -5.20% 7.00% -4.50% 8.90%

NASDAQ -5.30% 4.30% 7.20% 2.70% -8.20% -6.50% 6.90% -6.24% 12.04%

Q1 2010 Q2 2010 Q3 20210 YTD 2010

KCM Net Performance 9.86% -13.16% 9.08% 4.06%

DJIA 4.78% -9.40% 11.16% 5.52%

SP500 5.35% -11.39% 11.28% 3.88%

NASDAQ 5.88% -11.85% 12.30% 4.81%

November 1, 2010

Dear Investors,

Kinnaras Capital Management ("KCM", "Kinnaras", or the "Firm") Separately Managed Accounts("SMAs") returned 9.1% net in Q3 2010. Table I presents KCM SMA performance relative to keyindices. Investors should note that individual returns will vary based on the time one invested and thatthe composite return presented below is net of fees and is the time-weighted return ("TWR") of allKinnaras SMAs. TWR is one of the most comprehensive and accurate way of gauging investmentperformance for managed accounts but can be skewed at times due to the timing of new portfolioopenings.

TABLE I: 2010 MANAGED ACCOUNT PERFORMANCE

The great economist John Kenneth Galbraith said "It is a far, far better thing to have a firm anchor innonsense than to be put out on the troubled seas of thought." That essentially encapsulates the currentdialogue regarding economic policy. Deficit hawks have captured the debate amongst western countriesand institutions and are imposing harsh austerity measures when government investment programs arethe most expedient ways to generate legitimate "escape velocity" for the economy.

What's particularly disheartening is that deficit hawks have been able to generate a high level of acceptance of their ideas when much of what they advocate for has been discredited by current empiricalevidence. Ireland provides a good example of austerity in action as it was one of the first countries to

adopt aggressive deficit reduction measures. Ireland intends to reduce its deficit from 12% of GDP to<3% by 2014. Despite GDP that contracted by 7.1% in 2009, the country adopted no stimulusmeasures, with the government imposing three slash and burn budgets.1

The expectation was that Ireland would take its medicine early on and recover faster by implementingheavy handed spending cuts. Deficit reduction proponents believe that during recessionary times,reducing government spending will send a signal to credit markets that the country is focused on paring

1 http://www.guardian.co.uk/business/2010/sep/23/ireland-austerity-budgets-comment

8/8/2019 KCM Q32010

http://slidepdf.com/reader/full/kcm-q32010 2/14

____________________________________________________________________________________________________Page 2 of 14

down its deficit and debt and once those programs are enacted, credit markets will reward the countrywith reduced borrowing costs as debt levels decline. They also believe that reduced public spendingwill allow the private sector to take a larger role in the economic recovery.

So how has the Celtic Tiger fared? In its latest reported quarter - Q2 2010 - Ireland reported a 1.8%drop in GDP, with the country falling into a double-dip recession. Unemployment has risen to nearly14% and long-term unemployment is at 5.3%. Ireland's borrowing costs have also continued to rise with10 year Ireland bonds running at nearly 6.5%. These results are not consistent with the expectations of deficit reduction advocates, especially since Ireland began its austerity measures in spring 2009.

Ireland was able to demonstrate GDP growth of roughly 2.7% in Q1 2010 but this growth was largelydue to foreign transfers. As MIT professor Simon Johnson and Effective Intervention Chairman PeterBoone pointed out earlier this year, Ireland's GDP statistic can be a bit misleading because of its statusas a corporate tax haven. Johnson and Boone stated that "roughly 20 percent of Irish gross domesticproduct is actually 'profit transfers' that raise little tax for Ireland and are owned by foreign companies.Since most of these profits are subject to the tax code, they are accounted for in Ireland where they arelightly taxed; they should not be counted as part of Ireland’s potential tax base."

2

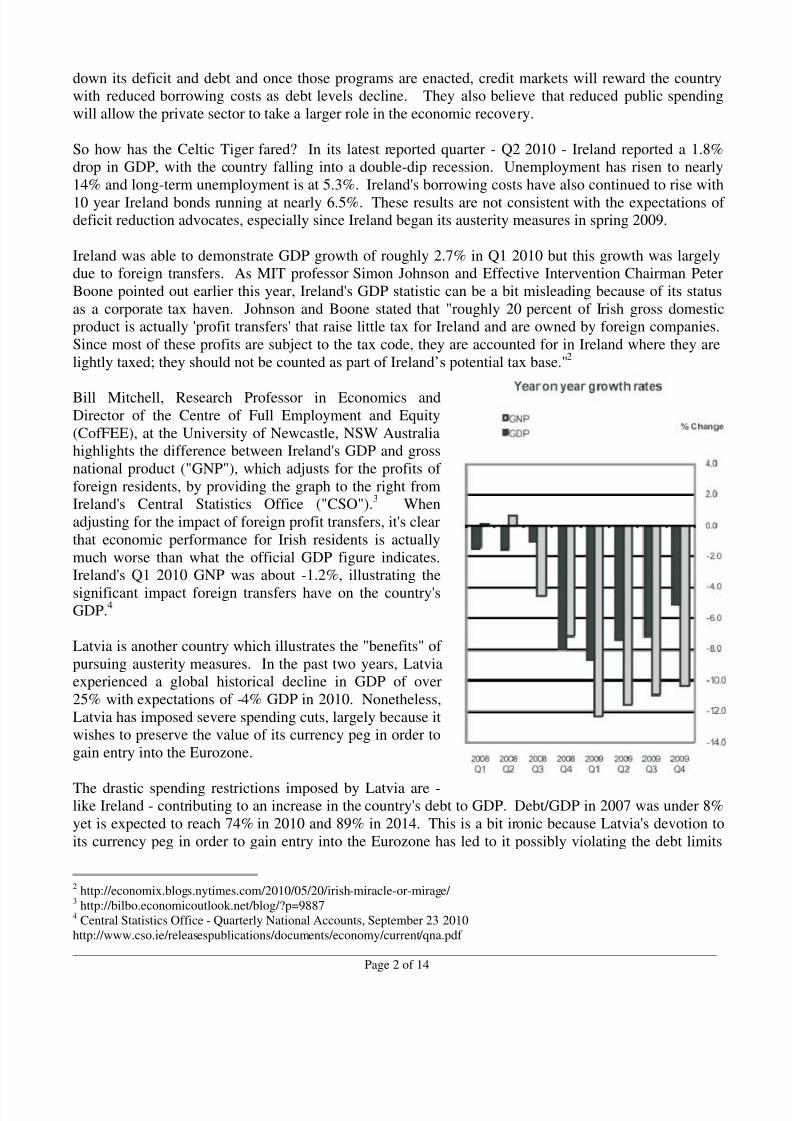

Bill Mitchell, Research Professor in Economics andDirector of the Centre of Full Employment and Equity(CofFEE), at the University of Newcastle, NSW Australiahighlights the difference between Ireland's GDP and grossnational product ("GNP"), which adjusts for the profits of foreign residents, by providing the graph to the right fromIreland's Central Statistics Office ("CSO").3 Whenadjusting for the impact of foreign profit transfers, it's clearthat economic performance for Irish residents is actuallymuch worse than what the official GDP figure indicates.Ireland's Q1 2010 GNP was about -1.2%, illustrating the

significant impact foreign transfers have on the country'sGDP.

4

Latvia is another country which illustrates the "benefits" of pursuing austerity measures. In the past two years, Latviaexperienced a global historical decline in GDP of over25% with expectations of -4% GDP in 2010. Nonetheless,Latvia has imposed severe spending cuts, largely because itwishes to preserve the value of its currency peg in order togain entry into the Eurozone.

The drastic spending restrictions imposed by Latvia are -like Ireland - contributing to an increase in the country's debt to GDP. Debt/GDP in 2007 was under 8%yet is expected to reach 74% in 2010 and 89% in 2014. This is a bit ironic because Latvia's devotion toits currency peg in order to gain entry into the Eurozone has led to it possibly violating the debt limits

2 http://economix.blogs.nytimes.com/2010/05/20/irish-miracle-or-mirage/ 3 http://bilbo.economicoutlook.net/blog/?p=98874 Central Statistics Office - Quarterly National Accounts, September 23 2010http://www.cso.ie/releasespublications/documents/economy/current/qna.pdf

8/8/2019 KCM Q32010

http://slidepdf.com/reader/full/kcm-q32010 3/14

____________________________________________________________________________________________________Page 3 of 14

stipulated by the Maastricht Treaty which sets out financial conditions for countries wishing to adopt theeuro.

Latvia's unemployment situationhas shown no material signs of improvement as illustrated in thechart to the right and thecountry's Q2 2010 GDP notcheda decline of roughly 3%.5 Aswith Ireland, it's very difficult tosee any tangible benefits thathave accrued to Latvia as a resultof pursuing these callouspolicies.

Excessive spending cuts during amassive economic contractionstrains a country's tax revenues

which is why Debt/GDP riseseven more. Borrowing costs have risen, not declined, contrary to the expectations of deficit hawks.

In addition, the economies of both countries continue to decline with unemployment showing nomaterial signs of improvement. In the case of Ireland, increased unemployment has further pressuredthe country's fragile banking system. In September, the country announced it would bailout Allied IrishBank ("AIB") with the country's total bill for bank bailouts reaching $68B.6 Robert Peston, businesseditor of the BBC, indicated that total capital provided to Ireland's banks amounted to 30% of GDP andwould cost Ireland's taxpayers €22,500 each.

7

So the point is if a big tab needs to be paid, why not spend it on something that can at the very least

directly benefit ordinary citizens? Ireland could spend 30% of its GDP to back-stop banks yet thecountry has been reluctant to deploy any capital on high multiplier fiscal projects? If some forms of direct stimulus were utilized, there's a good possibility unemployment would be sharply declining,resulting in people having cash in their hands and the ability to service their debts, alleviating some of the pressure on the banking system and possibly reducing the total bailout bill for Ireland. Instead,draconian cuts were implemented and the Irish are still spending a fortune to keep its banking systemalive. Further, large swaths of the working population of these countries see their skills erode andbecome potentially unemployable as these problems persist while the most talented and skilled workerseventually seek to migrate to better opportunities. It's hard to see how these policies make sense yetthey continue to receive substantial airtime.

In the case of Ireland and Latvia, default was perhaps the only other choice. However, given theweakness of their economy, these two countries may just be postponing the inevitable. Unlike Irelandand Latvia, the US has no constraints in financing projects that can assist in an economic recovery.Nonetheless, the US is pursuing policies enacted by deficit hawks, driven by misinformation regarding

5 Chart from Eurostat/Google Public Data6 http://www.nytimes.com/2010/10/01/business/global/01euro.html7 http://www.bbc.co.uk/news/business-11441473

8/8/2019 KCM Q32010

http://slidepdf.com/reader/full/kcm-q32010 4/14

____________________________________________________________________________________________________Page 4 of 14

"out of control" government spending and how the country has to get back to its "principles" implyingthat the country was far leaner and spartan in decades past.

That may be the perception but it's not reality. The following chart uses data from the Office of Management & Budget ("OMB").

8As one can see, total government spending as a percent of GDP and

federal government spending as a percent of GDP have both remained fairly consistent since 1970. Thespike in spending as a percent of GDP since 2008 has been due to the severity of the economiccontraction in 2008, which was far more severe than anything in the past 80 years. Various stabilizerssuch as unemployment benefits and food stamps kick in as the economy contracts but the main culpritfor higher spending as a percent of GDP is due to contracting GDP.

Total Government Spending and Federal Spending as a Percent of GDP

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

1 9 7 0

1 9 7 2

1 9 7 4

1 9 7 6

1 9 7 8

1 9 8 0

1 9 8 2

1 9 8 4

1 9 8 6

1 9 8 8

1 9 9 0

1 9 9 2

1 9 9 4

1 9 9 6

1 9 9 8

2 0 0 0

2 0 0 2

2 0 0 4

2 0 0 6

2 0 0 8

Total Gov't Exp as % of GDP Total Federal as % of GDP

This is further supported by data fromthe Federal Reserve ("Fed").9 Government expenditures havemaintained their historical trend, evenslightly declining during the middle of

the recession. Once again, the mainproblem is government receipts, whichhave suffered a sharp drop due to therecession and commensurate high levelof unemployment.

8 http://www.whitehouse.gov/omb/budget/Historicals/ (Table 15.3 - Total Government Expenditures as Percentage of GDP)9 http://research.stlouisfed.org/fred2/graph/?#

8/8/2019 KCM Q32010

http://slidepdf.com/reader/full/kcm-q32010 5/14

____________________________________________________________________________________________________Page 5 of 14

These problems ultimately relate to the massive output gap the US is facing. The output gap is basicallythe difference between what the US economy can produce and what it is currently producing. The UScurrently has an output gap that is nearly $1T and current economic growth is far too slow to close thatgap. The Washington Post recently released an interactive graph that does an excellent job of illustrating this problem.

10The chart below is from one frame of the interactive graph but readers may

benefit by visiting the site highlighted in the footnotes.

The big risk with the current output gap is that there are no aggressive policies being considered to closethis gap. The longer this gap persists, the longer it takes for unemployment to decline. According to theWashington Post's Neil Irwin, the current rate of 1.7% GDP growth is not sufficient enough to everclose this gap and unemployment would likely increase to near 12% by 2020. A growth rate of 3%would close this gap by 2020 and reduce unemployment to 5% while growth of 6% could close theoutput gap by 2012 and reduce unemployment to 5%.

The challenge is that policy makers are ignoring the only element of GDP that can stimulate the demandnecessary to close this gap. GDP can be broken down into a few components: C (private consumption)+ G (public/government consumption) + I (investment) + (X-I) (trade surplus or deficit). With the

exception of public consumption, every other component is severely constrained.

The travails of the private sector are well known at this point and all center around an over leveragedconsumer. People are saving a lot more, over 6% of their income, compared to recent historical rates of under 1% and at times even under 0%. This is necessary as consumers repair their balance sheets but inaggregate will reduce total economic output.

10 http://www.washingtonpost.com/wp-srv/business/the-output-gap/index.html

8/8/2019 KCM Q32010

http://slidepdf.com/reader/full/kcm-q32010 6/14

____________________________________________________________________________________________________Page 6 of 14

Investment is constrained because of lack of demand, resulting in 5% of the country's industrial capacitybeing idled. There are some policies that have been offered such as a 100% bonus depreciationallowance for small businesses but this is unlikely to work. The following chart is from the latest surveyof small businesses, courtesy of the National Federation of Independent Business.

11The number one

concern by a significant margin is lack of sales/demand. Taxes have generally remained the biggestconcern of small business by a wide margin since 1986 so it's quite telling that weak business prospectconcerns have jumped so significantly since 2008. The lack of sales is likely to keep businesses on thesidelines with respect to capital expenditure decisions, regardless of the sizeable tax incentive. In fact,the Institute for Supply Management ("ISM") conducted a survey in 2005 following the bonusdepreciation provision offered in 2004 whereby 66% of respondents indicated that the provision had noeffect on the timing of capital spending.

12

So with respect to GDP, both "C" and "I" are not in a position to make meaningful contributions toGDP. As for "(X-I)", there's nothing in our bag of tricks to quickly change the US into a net exporter.As is widely known, countries are engaged in a race to devalue their currencies in order to driveeconomic growth through exports. The US is probably the most poorly equipped to devalue its currencybecause most countries want a stronger USD relative to their own currency. In addition, the USD is a

reserve currency so during times of stress, the USD is likely to strengthen.

This leaves "G" as really the only available component to drive growth and it's startling that policymakers are not seizing on this opportunity. The US has near limitless capacity to finance any projectrelative to most peers with 10 Year and 30 Year Treasuries at just 2.63% and 3.88%. Given high levelsof unemployment, labor costs are very low so with low borrowing and labor costs, it’s hard to believe

11 http://www.nfib.com/Portals/0/PDF/sbet/sbet201010.pdf 12 http://www.federalreserve.gov/pubs/feds/2006/200619/index.html

8/8/2019 KCM Q32010

http://slidepdf.com/reader/full/kcm-q32010 7/14

____________________________________________________________________________________________________Page 7 of 14

that the government is not seizing on this opportunity to enact aggressive stimulus projects that canimprove the country.

For example, the US still has very old water pipes, some dating to the late 1800’s, that are in significantneed of upgrades. The 2009 American Recovery and Reinvestment Act set aside just $2B for drinkingwater systems but the Environmental Protections Agency ("EPA") estimates the country's drinking watersystems require over $300B in new investment and upgrades.

13This is a project that could immediately

employ people in a very critical investment at cheap funding rates and labor costs yet we're content to siton the sidelines while millions remain jobless.

Another area of focus should be on aggressively expanding broadband quality in the US. Cisco Systems("CSCO") recently released results of its third survey from Said Business School at Oxford Universitywhere it examined broadband quality. South Korea, Hong Kong, Japan, and Iceland rounded out the topfour while Switzerland, Luxembourg, and Singapore were tied for fifth. The US came in at 15th.Information and speed/quality of delivery of that information are critical to compete in a globaleconomy and the US should not be an also-ran in cutting edge technology. Scientific American put itbest

14:

The average U.S. household has to pay an exorbitant amount of money for an Internet connection that the rest of the industrial world would find mediocre. According to a recent

report by the Berkman Center for Internet and Society at Harvard University, broadband

Internet service in the U.S. is not just slower and more expensive than it is in tech-savvy nations

such as South Korea and Japan; the U.S. has fallen behind infrastructure-challenged countries

such as Portugal and Italy as well.

The consequences are far worse than having to wait a few extra seconds for a movie to load.

Because broadband connections are the railroads of the 21st century—essential infrastructure

required to transmit products (these days, in the form of information) from seller to buyer—our

creaky Internet makes it harder for U.S. entrepreneurs to compete in global markets. As

evidence, consider that the U.S. came in dead last in another recent study that compared howquickly 40 countries and regions have been progressing toward a knowledge-based economy

over the past 10 years. “We are at risk in the global race for leadership in innovation,” FCC

chairman Julius Genachowski said recently. “Consumers in Japan and France are paying less

for broadband and getting faster connections. We’ve got work to do.”

Rather than capitalize on these opportunities that are necessities to remain competitive with the rest of the world, government projects are viewed as unwarranted expenses. There are many viableinvestments to be made but we're content with sitting on our hands or pursuing costlier, less effectiveways of stimulating the economy. There are always critics of government funded programs, many arevalid, but investing in key initiatives such as those mentioned above can produce a tremendous return on

investment.

The Erie Canal opened around this time in 1825, connecting Lake Erie and the Hudson River, and wasconsidered an engineering marvel. It yielded significant productivity gains reducing transportation costsby over 90%. While recent generations can look back in admiration, it is important to note that the ErieCanal experienced its own share of derision as critics at the time dubbed it "Clinton's Ditch." Skeptics

13 http://www.nytimes.com/2009/04/18/us/18water.html14 http://www.scientificamerican.com/article.cfm?id=competition-and-the-internet

8/8/2019 KCM Q32010

http://slidepdf.com/reader/full/kcm-q32010 8/14

____________________________________________________________________________________________________Page 8 of 14

viewed New York Governor Dewitt Clinton's project as a hole in the ground and waste of money. Thesame criticisms would arise with a number of proposed infrastructure projects today but nothing wouldget as much bang for the buck as these types of programs. So while developing countries like China areunveiling high speed (262mph) trains, US policy makers continue to punt on any productive projects,hoping that monetary policy implemented by the Fed can make a significant impact.

That brings us to current markets where the Fed's plan for quantitative easing 2.0 ("QE2") has beenstoking equity markets over the past two months. QE2 expectations have focused on roughly $500B inpurchases by the Fed. This is far too small an amount to make any difference but is consistent with theFed's history of under delivering. At any rate, while mortgage rates are near historical lows, thepercentage of consumers that meet credit criteria for refinancing and home purchases is low. Inaddition, reducing borrowing rates by a few basis points is not likely to spur significant demand givencurrent low borrowing rates.

This strategy of providing supply in the form of cheaper capital through monetary policy or tax subsidiesin the case of bonus depreciation won't work in an environment with a massive dearth of demand.Nonetheless, there will still be winners from the Fed's policies. QE2 will maintain an accommodativeborrowing environment for large companies who will choose to issue debt for either massive share

repurchases or strategic acquisitions. Leveraged buyout funds will also be able to take advantage of cheap funding to acquire companies.

One of our holdings - Brocade Communications ("BRCD") - could be a potential target for either astrategic or financial buyer. BRCD provides networking equipment and solutions with a main focus onEthernet networking and storage area networking ("SAN"). BRCD sells its products to large tech firmssuch as EMC, Hewlett Packard ("HPQ"), and IBM that go on to incorporate its products into broadernetworking and technology infrastructure solutions.

BRCD is cheap relative to its peers and is a play on data center and network upgrades in the corporateworld. Cloud computing and virtualization are key focus areas for corporate IT and BRCD's products,

such as its Brocade One line, are used to construct networks and IT infrastructure capable of handlingthese growing needs. With a market capitalization of roughly $2.8B, BRCD could be an attractive targetfor either a strategic or financial buyer.

For example, HPQ purchased BRCD competitor 3Com for roughly $2.7B in late 2009. This gave HPQa strong foothold in Ethernet Switching, one of BRCD's key segments. HPQ could opt to acquire BRCDto establish an even stronger presence in this segment and also bolster its data storage solutions segment.HPQ has a market capitalization of nearly $100B, a strong balance sheet, and more than enough cashflow whereby BRCD would be an easy acquisition.

Aside from HPQ, competitors such as EMC, NetApp ("NTAP"), or Juniper Networks ("JNPR") could

also acquire BRCD. JNPR competes with both HPQ and BRCD in Ethernet Switching. Both aresmaller competitors than HPQ (via 3Com) but BRCD is nearly 30% larger than JNPR in this segment.By acquiring BRCD, JNPR would be a very solid #2 in this segment and pricing in this segment couldfirm up.

JNPR has a market capitalization of roughly $17B and is valued at 21.0x 2011 EPS, 3.8x EnterpriseValue ("EV")/LTM Sales, and 16.6x EV/LTM EBITDA. JNPR has a balance sheet with over $2B in netcash. JNPR's clean balance sheet, strong cash flow, and highly valued stock provide it with a number of financing strategies to consider if it wished to acquire BRCD. JNPR is roughly twice as large as BRCD

8/8/2019 KCM Q32010

http://slidepdf.com/reader/full/kcm-q32010 9/14

____________________________________________________________________________________________________Page 9 of 14

Transaction MetricsOffer Price $8.50

Current Price (10/27/10) $6.19Premium 37.3%Shares (MM) 487

Equity Value ($MM) 4,140Enterprise Value ($MM) 4,813EV/LTM EBITDA (incl Stock Comp) 9.3x

Transaction Structure ($MM)

Capital /EBITDASponsor Equity 1,685 3.3x

Financing

Term Loan B 2,066 4.0xSenior Notes 590 1.1x

Senior Sub Notes 295 0.6x

Total Debt 2,951 5.7x

PROJECTIONS ($MM) (Kinnaras Estimates)

2011 2012 2013 2014

Sales 2,184 2,304 2,396 2,492

Gross Profit 1,215 1,278 1,327 1,377

Gross Profit Margin 55.6% 55.5% 55.4% 55.3%

EBIT 403 435 452 470

+D&A 159 166 174 182

EBITDA 562 602 626 651

EBITDA Margin 25.7% 26.1% 26.1% 26.1%

Less:

Interest Expense 256 254 253 251

Principal Repayment 21 20 20 20

Taxes (30%) 44 54 60 66

CapEx 125 131 138 144

Free Cash Flow 116 141 156 170

FCF Margin 5.3% 6.1% 6.5% 6.8%

EBITDA 562 602 626 651

Exit Multiple 10.0x 10.0x 10.0x 10.0x

Enterprise Value 5,617 6,015 6,260 6,514

Less: Net Debt 2,814 2,652 2,476 2,286

Equity Value 2,803 3,363 3,784 4,228

in terms of scale but the market values it much more richly, in part because JNPR has boasted strongergrowth rates recently. JNPR could acquire BRCD on the cheap as BRCD is valued far less than itsbroader peer group, and increase JNPR's size by roughly 50%.

BRCD is even cheap enough to attract capital from financial sponsors. Part of the reason BRCD ischeap is because its growth has been lower than its peers. Its margins have also been under pressure inpart because it is still working through a reorganization process since acquiring Foundry Networks("Foundry") in 2008. Nonetheless, BRCD does have attractive long-term growth rates, high operatingmargins, and an improved cash flow outlook in 2011 and beyond. For example, BRCD has spentsignificant capital on its new corporate campus but those associated costs will be completed by 2010.As Exhibit I illustrates, BRCD could be an attractive investment for an LBO firm.

EXHIBIT I: BRCD LEVERAGED BUYOUT MODEL15

15 Projections for LBO model exclude equity issuance/stock compensation expense as BRCD would be private. Projectedgross profit, EBIT, and EBITDA based on BRCD's Non-GAAP adjustments which exclude stock compensation.

8/8/2019 KCM Q32010

http://slidepdf.com/reader/full/kcm-q32010 10/14

8/8/2019 KCM Q32010

http://slidepdf.com/reader/full/kcm-q32010 11/14

____________________________________________________________________________________________________Page 11 of 14

opportunities. Most of these are in small and micro capitalization opportunities. TSO was sold forsimilar reasons to KFT but also because we had additional refinery exposure through our investment inWestern Refining ("WNR"). RJET was one of our largest holdings and was sold because it wasapproaching our valuation estimate of $10-11.

Our other key positions are Citigroup ("C") and Sprint-Nextel ("S"). C's credit outlook continues toimprove but investors still have to deal with the overhang related to the US Treasury disposing of itsstake in C as well as the earnings drag stemming from Citi Holdings. Investors will note that C wasessentially split into a "good" and "bad" bank. Citi Holdings is the "bad" bank and its assets are beingwound down. The drag on C from those Citi Holdings is becoming smaller as the assets are disposed of.In addition, C does not pay a dividend but could be in a position in the coming 12-18 months to returncapital to shareholders. Reinstating a dividend and reduced earnings drag from a shrinking CitiHoldings will eventually boost C shares as a normalized operating scenario becomes more apparent. Inaddition, C will benefit from a very low effective tax rate stemming from the accumulation of considerable net operating losses during the financial crisis. These various factors in combinationshould warrant a share price well above $5 in the coming year.

S has been our most confounding investment this year...confounding because in my estimation it's

attractively valued and also has a number of positive catalysts that are coming to fruition, but alsofrustrating because the stock continues to be range bound between the high $3's and low $5's almostirrespective of its earning reports. S continues to improve operationally but its highest share price in2010 was in late May stemming from a Goldman Sachs upgrade. In late July, S released impressive Q2results whereby its share price surged over 10% only to top out over the next few days before losingabout 25% over the course of August. The stock rebounded through September and most of Octoberuntil it released Q3 earnings on October 27, 2010 when S missed analyst EPS estimates (-$0.30 vs -$0.28 est).

While the market has punished S since this earnings release, the company's fundamentals are moving inthe right direction. S beat Street estimates for both revenue and postpaid subscriber losses. Many

analysts had expected S to grow revenues in Q4 or 2011 yet revenues were up in Q3 driven in part bythe addition of 644,000 wireless subscribers, which was the company's highest quarterly net additionsince 2006. To put that in context, in Q3 2009, S lost nearly 550,000 wireless subscribers. The hugepositive swing demonstrates management has taken the right steps to stop the hemorrhaging and bringgrowth back to the company. This 1MM+ swing in subscribers contributed to the first year over yearimprovement in quarterly growth in over three years.

S has also fully turned around its customer service quality, which in years past was a huge deterrent tothe brand. S came in #1 or #2 in five of six regions in a recent JD Power & Associates Wireless CallQuality Performance Study and moved from last place in recent years to a tie for first in a JD PowerRetail Sales Satisfaction Study. In addition, S was the fastest growing postpaid brand in terms of net

new customers in Q3, indicating that S is taking share from its competition.

S churn rates, which represent customer attrition and erode profitability, continue to remain low. Before2010, S churn rates were well over 2% and hampered the company's operating margins. For its twomost recent quarters, S churn rates have been under 2%. If the company can maintain churn rates atthese levels, improved profitability will begin to materialize.

While S appears to be on the right track, investor expectations leading into Q3 were clearly for an evenfaster turnaround. I believe S is perhaps 1-2 quarters away from returning itself to positive growth on a

8/8/2019 KCM Q32010

http://slidepdf.com/reader/full/kcm-q32010 12/14

____________________________________________________________________________________________________Page 12 of 14

net postpaid addition basis. The market values S relatively poorly compared to its peer group but asinvestor sentiment begins to appreciate a potential growth and earnings leverage story, S shares could dovery well.

Right now there are a few issues inhibiting margins. The first is that Q3 was the first quarter where thecompany's two hottest phones, the HTC EVO and Samsung Epic 4G, were released. The EVO came outin the final two weeks of Q2 so Q3 was really when it had a full quarter of availability while the Epic 4Gwas released in the latter part of Q3. The costs of smartphones, especially two of the very best such asthe EVO and Epic, raise the company's cost of products as S, like other telecoms, heavily subsidizes thecost of handsets. 16 As a result, S is paying for these phones upfront in the form of heavy subsidies butwon't reap the benefits of these phones until its customers cycle beyond the first few weeks of usage.

As these subscribers with more expensive plans and devices are cycled through the company's loweraverage revenue per user (“ARPU”) base of subscribers, ARPU should increase and more than offset thehigh cost subsidies associated with these smartphones. Investors should also note that just 45% of thecompany's current customers have a smartphone and that 60% of the company's new sales aresmartphones. As that base of smartphone subscribers increases, the overall cost drag of these newerphones should be more than offset by higher ARPU.

Another catalyst for S is the rationalization of its network. S has two networks: code division multipleaccess ("CDMA") and Integrated Digital Enhanced Network ("iDEN") stemming from its horrificacquisition of Nextel. The company has 49MM subscribers of which 33MM are postpaid, 12MMprepaid, and 4MM wholesale/affiliates. The postpaid segment offers the highest profit subscribers whileprepaid offers major growth.

There are 6MM postpaid and 5MM prepaid subscribers on the iDEN network. No other large carriersupports this format and there is far less phone support for the iDEN format. More importantly, iDENhas been a major source of customer losses for S. In Q2 2010, S added 136,000 CDMA postpaidcustomers but saw 364,000 iDEN subscribers leave while its prepaid segment experienced a gain of

638,000 CDMA customers but a loss of 465,000 iDEN customers. In Q3 2010, S added 276,000postpaid subscribers to its CDMA network but lost 383,000 iDEN customers while its prepaid segmentnotched 1.2MM new CDMA customers offset by losses of 700,000 iDEN customers.

iDEN is a dying format in the US for the retail customer and business professional yet the company'smaintenance of this network format, combined with servicing a diminishing subscriber base is a hugecost drag. During the Q2 2010 earnings call, S management indicated that S will be modernizing itsnetwork and a recent interview with CEO Dan Hesse suggested iDEN would soon be phased out as partof this modernization plan. During the Q3 2010 conference call, Hesse indicated operating resultswould reflect these efforts in 2012.

This matters because cost of service ("COS") is a huge cost component for S and is currently acompetitive disadvantage as its main competitors can leverage costs around just one network format(VZ- CDMA, AT&T - GSM, T-Mobile - GSM). The company's COS account for roughly 61% of itstotal cost of goods/services sold. Between equipment costs and service costs, the company is able to

16 PC World ranked Epic and EVO #1 and #2, ZDNet ranked EVO as the "Best Smartphone", Popular Mechanics awardedthe EVO with the 2010 Breakthrough Product Award, Laptop Magazine suggest that "Sprint has the best 1-2 punch of anycarrier" regarding the EVO and Epic

8/8/2019 KCM Q32010

http://slidepdf.com/reader/full/kcm-q32010 13/14

____________________________________________________________________________________________________Page 13 of 14

generate gross margins of roughly 47%. S has also done an excellent job of controlling its operatingcosts so any improvement in gross margins should largely flow through to its operating earnings.

Exhibit II illustrates the potential benefits S could reap from its modernization plan with the highlightedsegments emphasizing the areas that would directly impacted from these efforts. The projections inExhibit II assume the costs associated with the modernization plan would run roughly $3B over twoyears and would yield a cost reduction in COS of roughly $2B by 2012 and beyond. If themodernization plan is effective, S could be well above $7 per share.

EXHIBIT II: SPRINT NEXTEL PROJECTIONS17 2010 2011 2012 2010 2011 2012

Revenues 32.2 33.2 33.5 Cash Flow Analysis:

Cost of Service 10.6 11.0 8.8 EBITDA 5.6 5.7 8.2

Cost of Products 6.6 7.0 7.0 - Cash Taxes 0.0 0.0 0.0Total COGS 17.2 17.9 15.7 - Maintenance CapEx (2.0) (1.5) (1.5)

Gross Profit 15.1 15.3 17.8 - FCC License Expenditures (0.6) (0.6) (0.6)

SG&A 9.5 9.6 9.7 - Network Modernization Plan 0.0 (1.5) (1.5)

EBITDA 5.6 5.7 8.2 Cash Flow before Financing Needs 3.0 2.1 4.6D&A 6.5 5.9 5.5 - Interest Expense (1.4) (1.4) (1.1)

EBIT (0.9) (0.2) 2.7 - Debt Maturities 0.0 (1.7) (2.8)Interest Exp (1.4) (1.4) (1.1) Cash Flow 1.5 (0.9) 0.7

EBT (2.3) (1.6) 1.6Taxes (40%) (0.9) (0.6) 0.6 Cash Balance 5.2 4.3 5.0Net Income (1.4) (0.9) 1.0 Total Debt 20.3 18.6 15.9

Shares (MM) 3.0 3.0 3.0

EPS ($0.47) ($0.32) $0.32

Operating Metrics:

Revenue Growth 0.1% 3.0% 1.0%

COS/Rev 32.9% 33.0% 26.1%COP/Rev 20.4% 21.0% 20.8%

COGS/Rev 53.3% 54.0% 46.9%

Gross Profit Margin 46.7% 46.0% 53.1%EBITDA Margin 17.3% 17.2% 24.3%

The Cash Flow Analysis table in Exhibit II demonstrates that S can also afford these future upgrades andmore importantly has enough cash on hand to address principal maturities. Clearly there are a numberof positive fundamental catalysts both current and in the future that the company is realizing. However,the market action of S is currently dictated by its relationship with Clearwire Corporation ("CLWR").

S owns 54% of CLWR, which is basically the company's 4G strategy. CLWR provides 4G service inthe US, currently covering 63MM people with the expectation of covering roughly 120MM by the endof 2010. In fact, on November 1, 2010 CLWR will launch 4G service in New York City followed byplans to launch 4G in San Francisco and Los Angeles in the coming weeks.

CLWR is continuing to roll out its service nationwide but this requires considerable capital, perhaps up

to $4B in total capital over the next 12-18 months whereby CLWR will likely need an equity infusion inH1 2011. In late September, reports suggested that Deutsche Telekom ("DT"), through its subsidiary T-Mobile ("TM"), was considering an investment in CLWR. This did not materialize and it appears thatthis was due to S, which as majority owner of CLWR opposed an outside investment.

This was a bad move and delayed, if not eliminated one potential catalyst for S shareholders. If TM wasallowed to invest in CLWR, it could have set the stage for a potential consolidation of S into DK.

17 Projections (Non-GAAP) based on Kinnaras estimates

8/8/2019 KCM Q32010

http://slidepdf.com/reader/full/kcm-q32010 14/14

____________________________________________________________________________________________________Page 14 of 14

Perhaps TM/DK would have directly bought S and then consolidated CLWR into the combined entity.Unfortunately, TM can now either roll out its own 4G network or partner with independent 4G providerssuch as a LightSquared, which is owned by hedge fund Harbinger Capital Partners.

The one good thing is that this is an issue that needs to get resolved relatively soon given the near termfunding needs of CLWR. Given the company's cash balance and ability to handle near-term debtmaturities, S could fund immediate CLWR needs of up to $1B-$1.5B. However, S management shouldseriously consider engaging TM, primarily because this combination would yield an entity that is muchless hampered by capital constraints and also can leverage a broader subscriber base over a growing 4Gnetwork.

Currently, CLWR's existing 4G network can handle a lot of subscribers but because the technology isrelatively nascent and tied mainly to S's existing subscribers that upgrade to 4G service, the costs of thatnetwork are spread over a relatively small subscriber base. Adding TM's 34MM subscribers wouldallow a combined TM/S/CLWR to introduce 4G over a much broader customer base, yieldingsignificant scale benefits. While S can succeed on its own and drive share price appreciation, aconsolidation would yield the fastest benefit to existing S investors.

Aside from S and other holdings mentioned in this update, the portfolio is currently being deployed intonew opportunities as well as keeping a sizeable portion in cash. We turned over a fair portion of theportfolio in the early part of Q4 because of larger valuation gaps appearing in the small cap segmentrelative to large capitalization companies and some holdings like RJET nearing our valuation estimates.

As always, feel free to contact me with any questions.

Best regards,

Amit Chokshi

DISCLAIMER: Any views expressed herein are provided for information purposes only and should not be construed in any way as an offer, anendorsement, or inducement to invest with any fund, manager, or program mentioned here or elsewhere. Neither Kinnaras Capital Management LLC norany persons or entities associated with the firm make any warranty, express or implied, as to the suitability of any investment, or assume any responsibilityor liability for any losses, damages, costs, or expenses, of any kind or description, arising out of your use of this document or your investment in anyinvestment fund. You understand that you are solely responsible for reviewing any investment fund, its offering, and any statements made by a fund or itsmanager and for performing such due diligence as you may deem appropriate, including consulting your own legal and tax advisers, and that anyinformation provided by Kinnaras Capital Management LLC and this document shall not form the primary basis of your investment decision. This materialis based upon information Kinnaras Capital Management LLC believes to be reliable. However, Kinnaras Capital Management LLC does not represent thatit is accurate, complete, and/or up-to-date and, if applicable, time indicated. Kinnaras Capital Management LLC does not accept any responsibility to updateany opinion, analyses, or other information contained in the material.