Jin Hyung Kim - United Nationsunpan1.un.org/intradoc/groups/public/documents/un/unpan031732.pdf ·...

24

Byong Seob Kim Jin Hyung Kim

Transcript of Jin Hyung Kim - United Nationsunpan1.un.org/intradoc/groups/public/documents/un/unpan031732.pdf ·...

Byong Seob KimJin Hyung Kim

Public Prosecution ReformPublic Prosecution ReformIVIV

Gov. Innovation & TrustGov. Innovation & TrustIIIIII

Why Trust in Government? Why Trust in Government? IIII

II IntroductionIntroduction

National Tax Service ReformNational Tax Service ReformVV

Policy Implications & Conclusion Policy Implications & Conclusion VIVI

IntroductionIntroductionIII

1. Describe why emphasizes ‘principle & trust’ as a vision for government innovation.

2. Explain what we have reformed to increase public trust in government.

3. Analyze effect of government innovation on trust in government

4. Suggest policy implications for improving trust in government.

Why Trust in Government?Why Trust in Government?IIIIII

Even in low trust, economic growth achieved in the pastBut for a leading nation, high level of trust neededEffective policy implementation & realizing policy objectives, high level of trust needed

Even in low trust, economic growth achieved in the pastBut for a leading nation, high level of trust neededEffective policy implementation & realizing policy objectives, high level of trust needed

Success in economic recoveryPeace in Korean PeninsulaBut, repeated corruption & scandals

Success in economic recoveryPeace in Korean PeninsulaBut, repeated corruption & scandals

From Gov.-ledState to

Governance State

From legacy &liabilities of Former Gov.

Traditionally ‘in-group’ focused on personal ties‘Out-group’ & ‘between-group’ belittled: low social trustTraditionally ‘in-group’ focused on personal ties‘Out-group’ & ‘between-group’ belittled: low social trust

TrustCharacteristic

of Korea

$$

Why Trust in Government?Why Trust in Government?IIIIII

Ruling entity

(politicians and top officials) ‘In-group’

big businessmen

favorfavorCorruptive Union between Power & Wealth

Two sons of the then-President (Kim Dae-jung) convictedPublic detest and distrust high: civic movement

Principle and TrustPrinciple and Trust

Scandals leading to Public Distrust

Gov. Innovation & TrustGov. Innovation & TrustIIIIIIIII

Local Referendum SystemResident Recall SystemResident Suit SystemPromotion of online Participation, and more….

Local Referendum SystemResident Recall SystemResident Suit SystemPromotion of online Participation, and more….

Expanding AdministrativeInformation DisclosureConstructing Digital BudgetAccounting SystemIntroducing Record Management SystemConstructing E-GovernmentInfrastructure, and more….

Expanding AdministrativeInformation DisclosureConstructing Digital BudgetAccounting SystemIntroducing Record Management SystemConstructing E-GovernmentInfrastructure, and more….

Innovative Tasks for More Participation Gov.

Innovative Tasks for More Participation Gov.

Innovative Tasks for More Transparent Gov.

Innovative Tasks for More Transparent Gov.

** For more information, please refer to the book “A New Wave of Government Innovation in Korea

’94 ’95 ’96 ’97 ’98 ’99 ’00 ’01 ’02 ’03 ’04 ‘05

[ MOGAHA (2005) )

The Number of Annual Application of Administrative Information Disclosure The Number of Annual Application of Administrative Information DThe Number of Annual Application of Administrative Information Disclosure isclosure

12,14621,559

17,14618,694

26,33842,930

61,586

86,006

108,147

192,295

104,024

130,841

• Non-disclosure: 11,412(9%)

• Partial dislcosure: 12,568(11%)

• Entire disclosure: 96.899(80%)

• Non-disclosure11,412(9%)

• Partial dislcosure12,568(11%)

• Entire disclosure 96.899(80%)

• Total number of applications

cases

• Total number of applications

cases

The Number of Disclosure of Administrative Information in 2006The Number of Disclosure of Administrative Information in 2006

[ MOGAHA (2006) ]

Gov. Innovation & TrustGov. Innovation & TrustIIIIIIIII

Participation, Transparency;

from the experiences.

Major FactorsMajor

Factors

Complex Factorsand Causal

Relationship

Complex Factorsand Causal

Relationship

Participation, Transparency; Intervening VAR

but their correlation to trust is hard to find.

Reform Measures

Participation

Transparency

Trust in Government

Trust in Government

Citizen’s Expectation

Organizational Level

A test model of trust in government

1. Public distrust in Prosecutor1. Public distrust in Prosecutor

3. Effect of reform on trust in government• Content Analysis

Integrity Perception Index

3. Effect of reform on trust in government• Content Analysis

Integrity Perception Index

2. Reform measures• Independence from politics, especially from the President.• ‘democratic controls’ of the prosecution

- Reinforce the function and role of the Minister of Justice to check prosecutors

- Hearing system for the nomination of the Prosecutor General- Civil monitoring and civil Ombudsman have been introduced.

2. Reform measures• Independence from politics, especially from the President.• ‘democratic controls’ of the prosecution

- Reinforce the function and role of the Minister of Justice to check prosecutors

- Hearing system for the nomination of the Prosecutor General- Civil monitoring and civil Ombudsman have been introduced.

Public Prosecution Reform CasePublic Prosecution Reform CaseIVIVIV

200

100

300

(case)

162162

2626

110110 124124

100100

140140

212166

22 22 22

57571111 1111 44 1212

2525

516516

Annual frequency of the number of “prosecution reform” citation in Korea’s 5 major newspapers

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

9

8

7

6

5

4

3

4.26

7.288.15

8.377.80

( Point )

KICAC Integrity Perceptions IndexKICAC Integrity Perceptions Index

Integrity Score(out of 10 points)

Source: Korea Independent Commission Against Corruption (KICAC)

2002 2003 2004 2005 2006 (Year)

5.82

6.80

8.188.42 8.77

6.43

7.71

8.38 8.688.77

Public Organization Average

National Tax Service

Prosecutor’s Office

1. Negative Perception on NTS

Negative perception began to be imprinted during the Japanese colonial period Such public perception on taxes and behavior of revenue officials remained after independence.As taxes were assessed more or less at the discretion of the taxinspector, exposure to corruption for revenue officials and unfair taxation to some extent was inevitable.Reform measures demanded to root out negative perception and behavior

National Tax Service ReformNational Tax Service ReformVVV

2. Reform measures

Major strategy to overcome the problem-to identify all the sources of tax revenue,-without direct contact between tax payerand revenue official

Many reform measures were implemented toward this directionsince the National Tax Service (NTS) was

established in 1966

National Tax Service ReformNational Tax Service ReformVVV

1999 reform measure

-Reorganizationof NTS

-Credit card,

For participation; income deductions, credit card lottery system.More transparency; the rate of

credit card payment

For participation; income deductions, credit card lottery system.More transparency; the rate of

credit card payment

National Tax Service ReformNational Tax Service ReformVVV

2003 reform measure

-Hometax-Cash Receipt

System

Toward participation, various tax support programs for business; income deductions as well as lottery system for consumer. -More transparency; Cash receipt

and credit card usage as a percentage of private consumption spending; Estimate of automatic exposure from credit cards and cash receipts

Toward participation, various tax support programs for business; income deductions as well as lottery system for consumer. -More transparency; Cash receipt

and credit card usage as a percentage of private consumption spending; Estimate of automatic exposure from credit cards and cash receipts

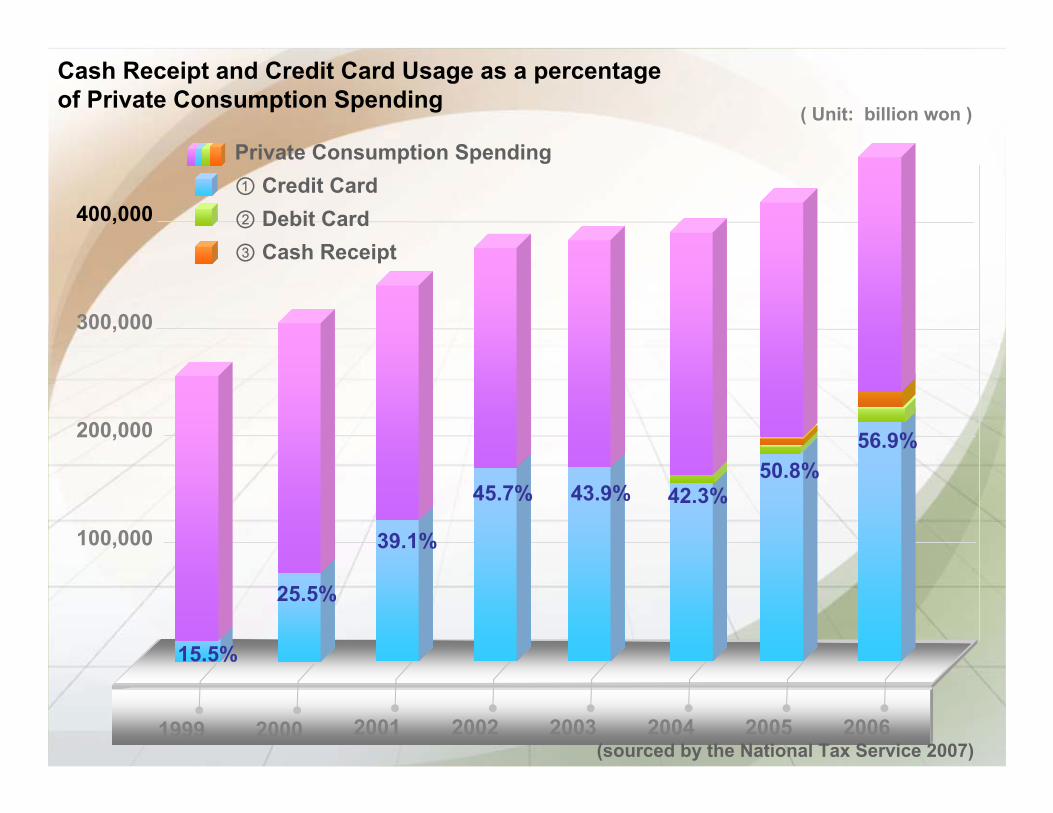

National Tax Service ReformNational Tax Service ReformVVV

200,000

300,000

400,000

2004 2005 20062001 2002 20031999 2000

100,000

Cash Receipt and Credit Card Usage as a percentage of Private Consumption Spending

(sourced by the National Tax Service 2007)

Private Consumption Spending ① Credit Card② Debit Card ③ Cash Receipt

15.5%

25.5%

39.1%

45.7% 43.9% 42.3%50.8%

56.9%

( Unit: billion won )

2004 2005 20062001 2002 20031999 2000

Cash Receipt and Credit Card Usage as a percentage of Private Consumption Spending

(sourced by the National Tax Service 2007)

① Credit Card② Debit Card ③ Cash Receipt

15.5%

25.5%

39.1%

45.7% 43.9% 42.3%50.8%

56.9%

50%

25%

3. Effect of reform on Trust in Government

- Integrity Perception Index - Integrity Perception Index

- Taxpayer Satisfaction index- Taxpayer Satisfaction index

National Tax Service ReformNational Tax Service ReformVVV

9

8

7

6

5

4

3

4.26

7.288.15

8.377.80

( Point )

KICAC Integrity Perceptions IndexKICAC Integrity Perceptions Index

Integrity Score(out of 10 points)

Source: Korea Independent Commission Against Corruption (KICAC)

2002 2003 2004 2005 2006 (Year)

5.82

6.80

8.188.42 8.77

6.43

7.71

8.38 8.688.77

Public Organization Average

National Tax Service

Prosecutor’s Office

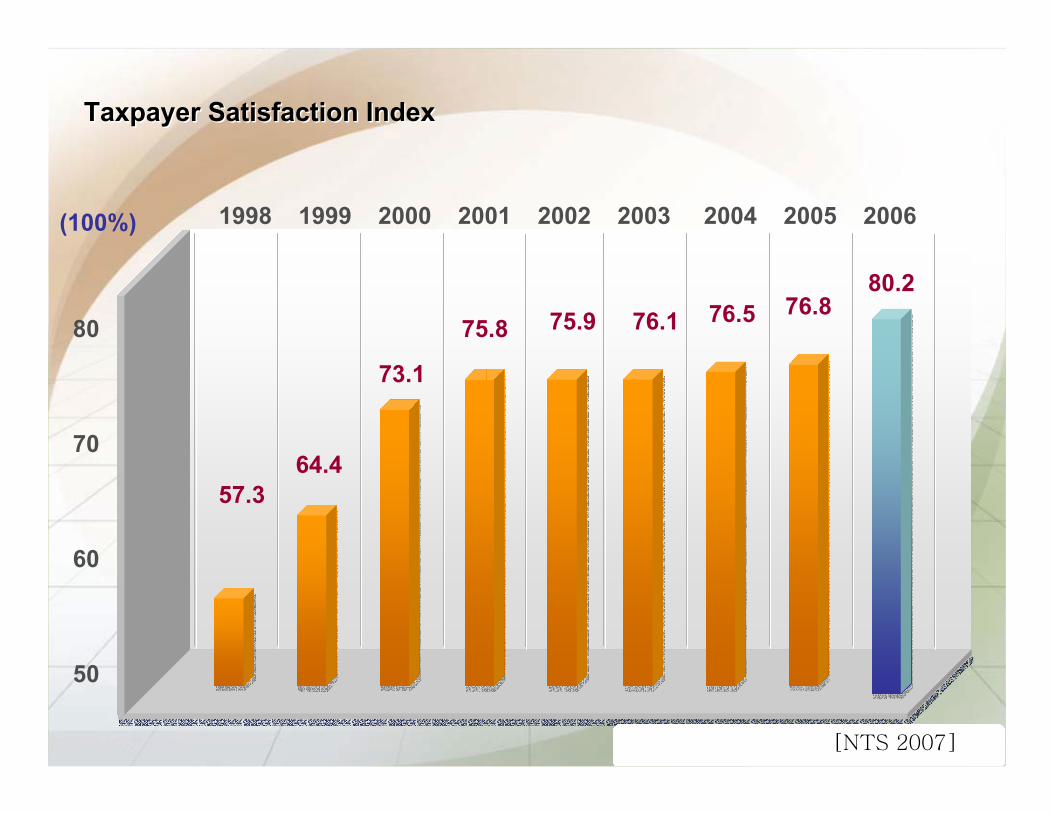

80

70

60

50

(100%)

[NTS 2007]

1998 1999 2000 2001 2002 2003 2004 2005 2006

75.9 76.1 76.5 76.880.2

57.364.4

73.1

75.8

Taxpayer Satisfaction Index Taxpayer Satisfaction Index

Policy Implications & Conclusion Policy Implications & Conclusion VIVI