[email protected] Managing Director Endesa Tradingendesa.es Managing Director Endesa Trading March...

37

Investment in gas-fired generation Juan J Alba [email protected] Managing Director Endesa Trading March 25th, 2003 IEA/NEA Workshop on Power generation investment in liberalised electricity markets

Transcript of [email protected] Managing Director Endesa Tradingendesa.es Managing Director Endesa Trading March...

Investment in gas-fired generation

Juan J [email protected] DirectorEndesa Trading

March 25th, 2003IEA/NEA Workshop on Power generation investment in liberalised electricity markets

2

Contents

• The CCGT: the response for generation capacity needs

• Electricity: market, risks, regulation

• Gas: the market environment

• Are markets signals adequate for investment?

• Some final thoughts

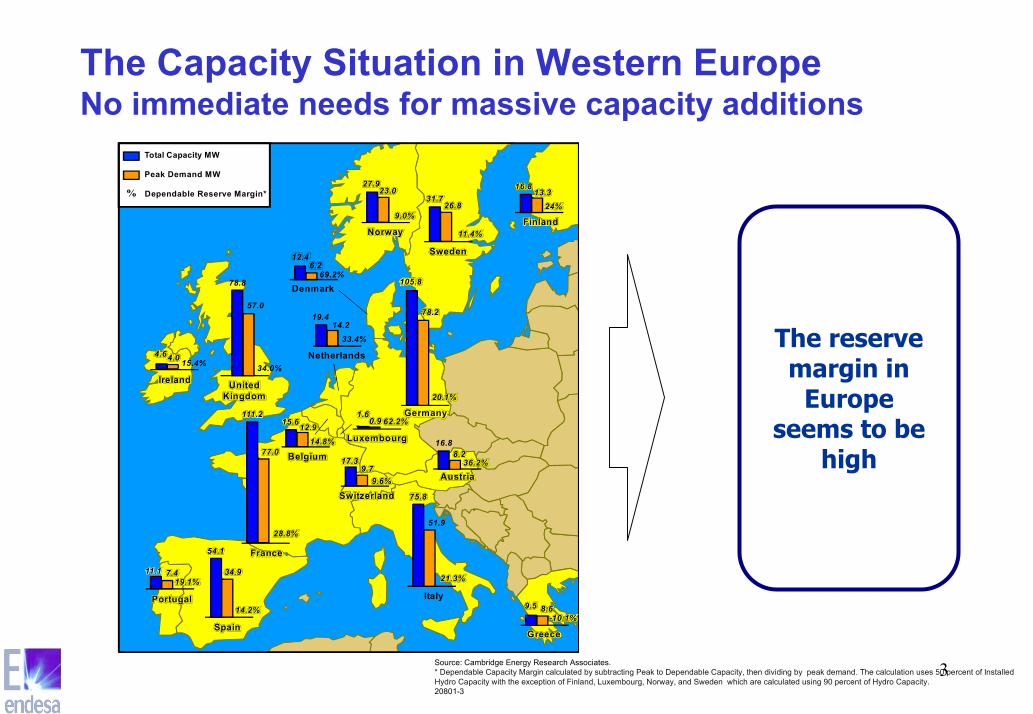

3Source: Cambridge Energy Research Associates.* Dependable Capacity Margin calculated by subtracting Peak to Dependable Capacity, then dividing by peak demand. The calculation uses 50 percent of InstalledHydro Capacity with the exception of Finland, Luxembourg, Norway, and Sweden which are calculated using 90 percent of Hydro Capacity.20801-3

Total Capacity MW

Peak Demand MW

Dependable Reserve Margin*%

France

111.2

77.0

28.8%

Belgium14.8%

12.915.6Germany

105.8

78.2

20.1%

Netherlands

33.4%14.2

19.4

Luxembourg

1.60.9 62.2%

Portugal

19.1%7.411.1

Spain

54.1

Italy

21.3%

51.9

75.8

Greece

-10.1%8.69.5

Austria

8.236.2%

Switzerland9.6%

9.717.3

14.2%

34.9

16.8

Sweden

31.726.8

11.4%Finland

24%13.3

16.8

Norway

9.0%

23.027.9

Denmark

12.46.269.2%

UnitedKingdom

34.0%

57.0

78.8

Ireland

4.64.0 15.4%

The reservemargin in

Europeseems to be

high

The Capacity Situation in Western EuropeNo immediate needs for massive capacity additions

4

Reserve Margin140%

134%

126%

120%

114%

101%

105%

106%

1996 1997 1998 1999 2000 2001 2002 2003

Peak Dem and 37.350 MW (14/01/03); 18:57 h)

Capacity Insta lled Dependable

Nuclear 7.888 7.092

Coa l 11.565 9.851

Fue l-Gas 7.594 5.024

CCGT 3.032 1.518 * *

Hydro (Conv) 13.918 8.100 *

Hydro (Pum p) 2.788 1.940

Eolic 4.830 175

Others (cogen & renew ) 6.874 4.130

T ota l 58.489 37.830

Reserve Margin 1,3%

(* ) Last 5 years average

(* * ) Capacity reduced due to natura l gas

constra ints

Reserve M arg in in stress scenario

The situation is not uniformReserve margin evolution in Spain

5

Hydro

Classic

Nuclear

0

20

40

60

80

100

120

140

Hydro

Classic

Nuclear

Hydro

Classic

Nuclear

0

20

40

60

80

100

120

140

Hydro

Classic

Nuclear

Hydro

Classic

Nuclear

0

20

40

60

80

100

120

140

Hydro

Classic

Nuclear

Hydro

Classic

Nuclear

0

20

40

60

80

100

120

140

Hydro

Classic

Nuclear

Installed capacity (GW)

Expected French demand (2010)

GW

BASE (Nuclear, 7200 G

WBASE (Nuclear, 7200

GW

BASE (Nuclear, 7200

20

40

60

80

100

GW

BASE (Nuclear, 7200 G

WBASE (Nuclear, 7200

GW

GW

20

40

60

80

100

GW

GW

GW

GW

20

40

60

80

100

GW

GW

SEMI BASE (Coal, 4000)

BASE (Nuclear, 7200

PEAK (Hydro, 2000 hours)Potential NEEDS

GW

BASE (Nuclear, 7200 G

WBASE (Nuclear, 7200

GW

BASE (Nuclear, 7200

20

40

60

80

100

GW

BASE (Nuclear, 7200 G

WBASE (Nuclear, 7200

GW

GW

20

40

60

80

100

GW

GW

GW

GW

20

40

60

80

100

GW

1000

2000

3000

4000

5000

6000

7000

8000

GW

SEMI BASE (Coal, 4000)

BASE (Nuclear, 7200

PEAK (Hydro, 2000 hours)Potential NEEDS

hours

But even France could need some capacity

6

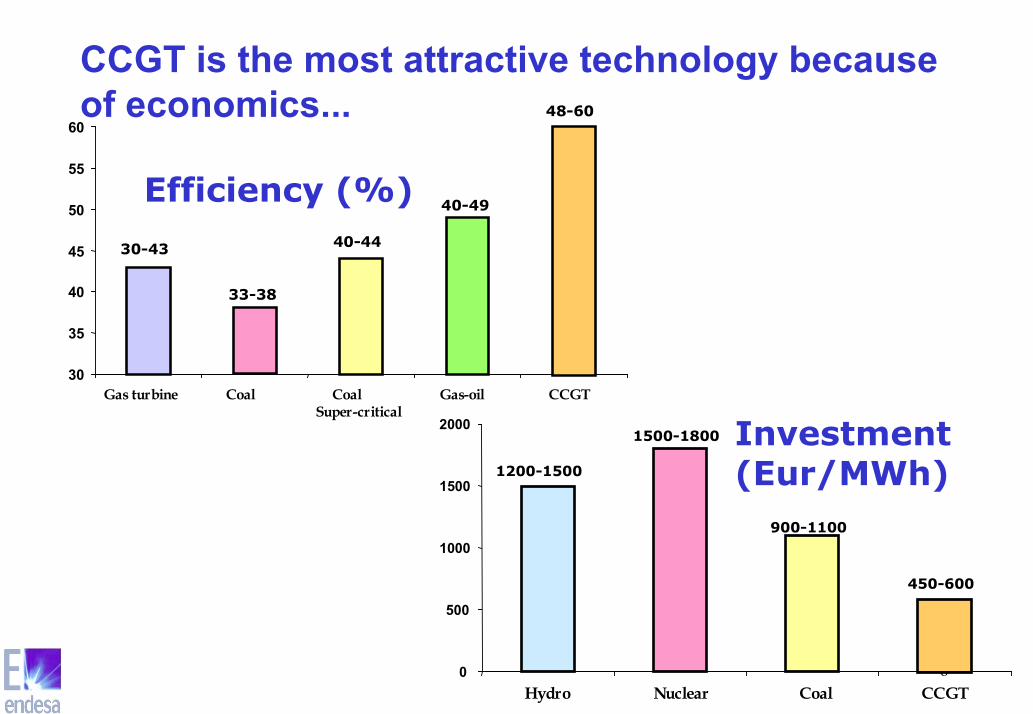

Efficiency (%)

30

35

40

45

50

55

60

Gas turbine Coal CoalSuper-critical

Gas-oil CCGT

33-38

30-43 40-44

40-49

48-60

0

500

1000

1500

2000

Hydro Nuclear Coal CCGT

1500-1800

1200-1500

900-1100

450-600

CCGT is the most attractive technology becauseof economics...

Investment(Eur/MWh)

7

00,20,4

Kgr

/tep

Carb

ón

Petr

oleo

Gas

Natu

ral

Particles

0

40

80

Kgr

/tep

Car

bón

Petr

oleo

Gas

Nat

ural

SO2

05

10

Kgr

/tep

Carb

ón

Petr

oleo

Gas

Natu

ral

NOx

025005000

Kgr

/tep

Carb

ón

Petr

oleo

Gas

Natu

ral

CO2

... and environmental impact

8

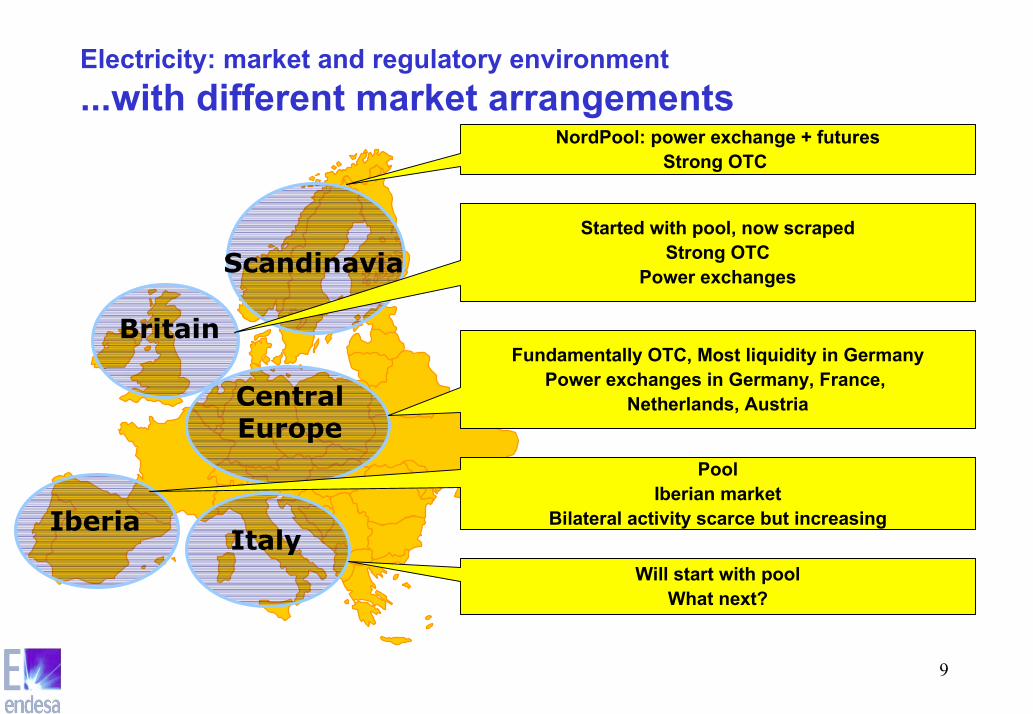

Scandinavia

CentralEurope

Britain

IberiaItaly

Electricity: market and regulatory environmentEurope has already moved from national toregional markets...

• Two very mature and integratedmarkets in Britain andScandinavia

• The largest market is in CentralEurope➔ Germany, France, Benelux,

Switzerland, Austria ...➔ Size, location

• Iberia and Italy are relativelyisolated➔ But this will change

9

Scandinavia

CentralEurope

Britain

IberiaItaly

Electricity: market and regulatory environment...with different market arrangements

NordPool: power exchange + futuresStrong OTC

Started with pool, now scrapedStrong OTC

Power exchanges

Fundamentally OTC, Most liquidity in GermanyPower exchanges in Germany, France,

Netherlands, Austria

PoolIberian market

Bilateral activity scarce but increasing

Will start with poolWhat next?

10

Electricity: market and regulatory environmentGermany and France are the core of thecontinental power markets

Baseload Cal 02

20.00

20.50

21.00

21.50

22.00

22.50

23.00

23.50

24.00

24.50

17/05/2001

24/05/2001

31/05/2001

07/06/2001

14/06/2001

21/06/2001

28/06/2001

05/07/2001

12/07/2001

19/07/2001

26/07/2001

02/08/2001

09/08/2001

16/08/2001

23/08/2001

30/08/2001

06/09/2001

13/09/2001

20/09/2001

27/09/2001

04/10/2001

11/10/2001

18/10/2001

25/10/2001

01/11/2001

08/11/2001

15/11/2001

22/11/2001

29/11/2001

06/12/2001

Eur/M

Wh

FranceGermany

• Germany was the first bilateral wholesale market in continental Europe➔ Started in 1998, currently around 1500 TWh/year➔ Volumes stabilised or reduced since Enron’s collapse➔ Much speculative trading, but greatly reduced after the fall of American traders

• The French bilateral market is growing rapidly➔ Started in 2001, now around 200 TWh/year➔ Has kept growing, a less speculative market, closer to the physical delivery

11

European Power Exchanges are growing fastNow, as spot markets, tomorrow as futures

• LPX (Germany)➔ Accounts for 5% of

German Demand➔ Averaged Hourly depth

is 2500 MWh• EEX (Germany)

➔ 0,5% of GermanDemand; Depth of 260MWh

• APX (Netherlands)➔ 12-15% of Dutch

consumption.➔ Hourly depth of 1500

MWh• PowerNext (France)

➔ Depth of 280 MWh➔ Accounts for less than

0,5% of FrenchDemand

0

50

100

150

200

250

300

350

400

450

500

week 2

5wee

k 30

week 3

5wee

k 40

week 4

5wee

k 50

week 2

week 7

week 1

2wee

k 17

week 2

2wee

k 27

week 3

2wee

k 37

week 4

2wee

k 47

week 5

2wee

k 5wee

k 10

week 1

5wee

k 20

Agg

rega

ted

Wee

kly

Vol

ume,

GW

h

LPX EEX APX PowerNext

2002

12

7 €

2 €

European Power Exchanges are growing fastThe supply and demand curve in Powernext• Currently the profile of the offer curve of the peak hours is very steep.

An small variation in the demand leads to high variations in price• The off-peak hours offer curve show a flatter profile

13

7,00

27,00

47,00

67,00

87,00

107,00

ene-

98

may

-98

sep-

98

ene-

99

may

-99

sep-

99

ene-

00

may

-00

sep-

00

ene-

01

may

-01

sep-

01

ene-

02

may

-02

sep-

02

ene-

03

euro

/ M

Wh

0

1.000

2.000

3.000

4.000

5.000

6.000

7.000

8.000

9.000

GW

h

Daily Weighted Average Price (E/MWh)

Hydro Energy (GWh)

There is also a strongcorrelation between

hydro conditions, priceand volatility

After all, hydroconditions are a short

term distorsion ofreserve margin, withan underlying long

term hydro availablecapacity

Hydro conditions are a major driver of electricityprices, and therefore a risk factorSpanish pool price Price spikes

normal in the short term(electricity cannot be stored)

14

PRODUCCION HIDRAULICA DEL SISTEMA2000-2001-2002

500

1.500

2.500

3.500

4.500

5.500

6.500

ENER

O

FEBR

ERO

MARZO

ABRI

L

MAYO

JUNIO

JULIO

AGOST

O

SEPT

IEMBR

E

OCTUB

RE

NOVIEM

BRE

DICIE

MBRE

Ener

gía(

GW

h/m

es)

Año 2001: 36.503 GWh

Año 2000: 24.883 GWh

Año 2002: 18.572 GWh

Hydro conditions are a major driver of electricityprices, and therefore a risk factorSpanish hydro production

15

Fuel- gas/hydro production & Spanish pool price

0.000

1.000

2.000

3.000

4.000

5.000

6.000

7.000

0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0%

Participación del fuel en MD

Prec

io (c

€/kW

h)

0.000

1.000

2.000

3.000

4.000

5.000

6.000

7.000

0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 30.0% 35.0% 40.0%

Participación del agua en la cobertura

Prec

ios

(c€/

kWh)

There is a non-linear relation betweenthe share of fuel-oil production and

pool price. The “discontinueties” arerelated with points at which fuel-oilstarts to be essential for demand

coverage

With high hydro productions,marginal price is set by stable coalprice. With decreasing hydro levels,

the volatility of fuel price is perceived

16

Possible environmental impact in pool prices

Investment

Fixed costs

Fuel Costs

Other variable costs

Emissions costs

(Euros/tCO2)

(Euros/MWh)

(MWh/h)

Ci

(Euros/MWh)

(MWh/h)

Ci

Cf

Depending in the type of

fuel and the efficiency of

the plant, emission costs

will have an impact as an

additional variable cost

and therefore on

wholesale prices (?)

+

17

1998 1999 2000 2001 2002

Reserve MarginPool Price (98 base)Customer Price (98 base)

But, does the wholesale price really matter?The example of Spain

Pool price has adequatelyreflected the balance of supplyand demand forces:

•Decreasing reserve margin•Changing hydro conditions•Fuel prices•Increasing LTMC

However, this evolution of poolprice has had no effectwhatsoever on prices to finalcustomers

18

61,1 58,9 60,3 62,967,5

39,838,240,241,0 39,8

1998 1999 2000 2001 2002

Régimen Ordinario Régimen Especial

10,5%

-3,0%

The effect of regulationRevenues of generation in Spain (eur/MWh)

19

7,8 7,5

5,6

4,6 4,5

1998 1999 2000 2001 2002

-42,3%

The effect of regulationThe capacity payment in Spain (eur/MWh)

20REE (83)

CHAOS

Elkraft (00)

GRTN (00)

Elia (01)

RTE (00)

REN (94)

National Grid (90)

EirGrid (99) Fingrid (96)Statnett (92)

SVK (92)

TenneT (98)

Verbund (88)

Electricity: market and regulatory environmentA variety of system operators...

21Spanish Pool (OMEL) (98)

EEX (00)

APX (99)

Italy: no yet

Belgium: no yet

Greece: no wayPortugal: no yet

England & Wales Pool (90)now! NETA (01)

Nordpool (93)

Austria: EXAAPowerNext (01)

Ireland: no yet

Electricity: market and regulatory environment...power exchanges...

22CNE (94)

Germany: ??

Dte (99)

OFGEM (86)

E-CONTROL (01)

CRE (00)

CREG (00)

ERSE (97)

AEEG (96)

CER (99)

Electricity: market and regulatory environment...and regulatory entities

23

25 - 35 €/MWh

23 - 28 €/MWh

28 - 35 €/MWh25 - 33 €/MWh

23 - 28 €/MWh

20 - 25 €/MWh

20 - 25 €/MWh

35 - 40 €/MWh

23 - 28 €/MWh

15 - 35 €/MWhNuclear

GasFuel-Oil

CoalHydro

Electricity: market and regulatory environmentForward prices in Europe are too different

24

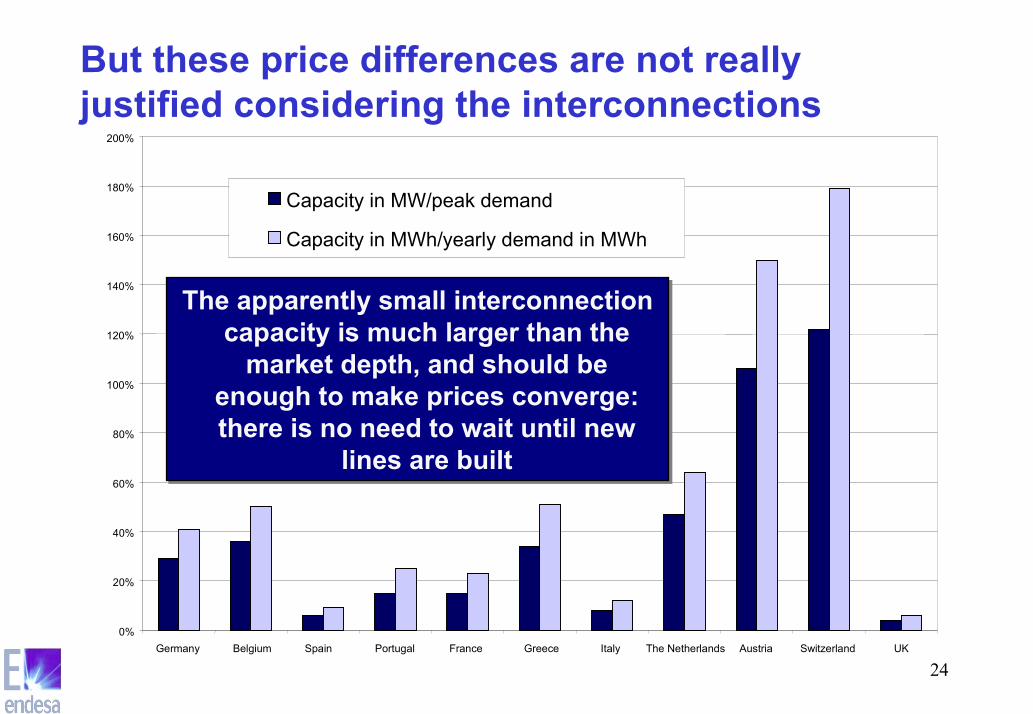

But these price differences are not reallyjustified considering the interconnections

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

200%

Germany Belgium Spain Portugal France Greece Italy The Netherlands Austria Switzerland UK

Capacity in MW/peak demand

Capacity in MWh/yearly demand in MWh

The apparently small interconnectioncapacity is much larger than the

market depth, and should beenough to make prices converge:there is no need to wait until new

lines are built

The apparently small interconnectioncapacity is much larger than the

market depth, and should beenough to make prices converge:there is no need to wait until new

lines are built

25

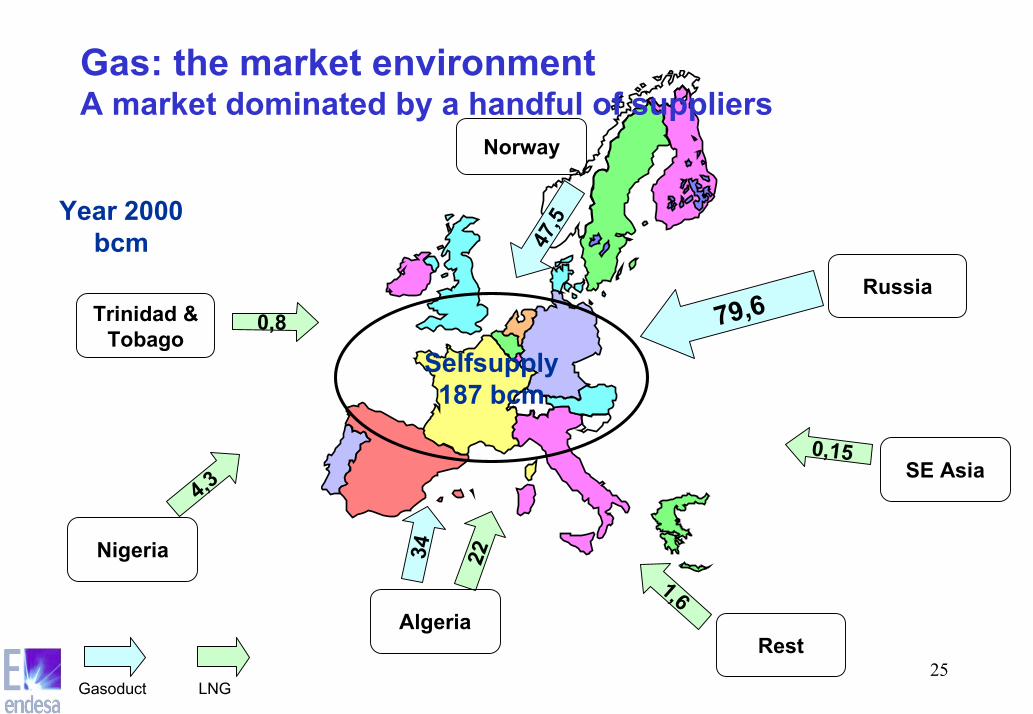

79,6Russia

47,5

Norway

Gasoduct LNG

34 22

Algeria1,6

Rest

4,3

Nigeria

0,8Trinidad &Tobago

Year 2000bcm

0,15SE Asia

Selfsupply187 bcm

Gas: the market environmentA market dominated by a handful of suppliers

26

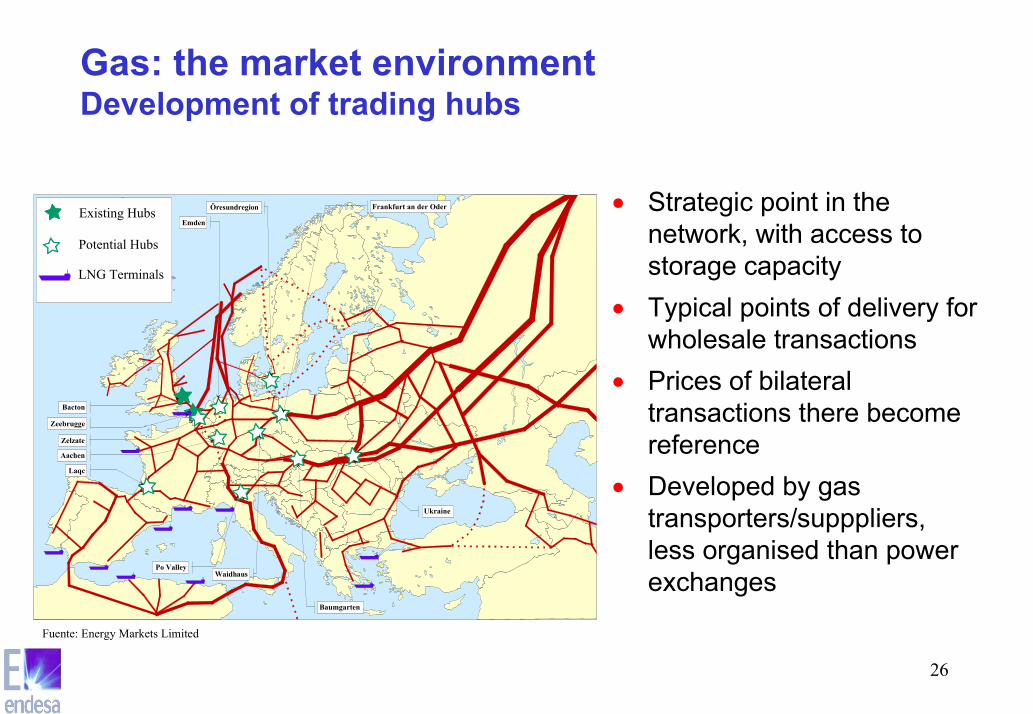

• Strategic point in thenetwork, with access tostorage capacity

• Typical points of delivery forwholesale transactions

• Prices of bilateraltransactions there becomereference

• Developed by gastransporters/supppliers,less organised than powerexchanges

Zelzate

Potential Hubs

Existing Hubs

LNG Terminals

Zeebrugge

Bacton

Aachen

Laqc

Emden

Frankfurt an der OderÖresundregion

WaidhausPo Valley

Ukraine

Baumgarten

Fuente: Energy Markets Limited

Gas: the market environmentDevelopment of trading hubs

27

Gas... and comparison with electricity• Oligopoly

➔ A handful of external suppliers➔ Typically one large distributor/supplier

per country

• Rigid➔ Long term contracts➔ Take or Pay➔ Small spot market➔ UK only significant traded market

• Regional markets➔ Transport bottlenecks➔ Regulatory problems: network tariffs

• More competition, suppliers in eachcountry

➔ More progress regarding independenceof transmission system operator

• More wholesale/trading activity➔ Bilateral and exchanges➔ Germany, France, Netherlands

• Regional markets➔ Transport bottlenecks➔ Regulatory problems: network tariffs

28

Gas: the market environmentDrivers of gas prices in Europe

• Liquidity of wholesale markets➔ NBP➔ Zeebrugge (UK-Bel)➔ Emden/Bunde (Ger-Neth)➔ Zelzate (Neth-Bel)

• LNG➔ Atlantic arbitrage➔ Ships➔ USD/EUR

• Supply flexibility➔ Storage➔ North sea➔ Netherlands

• Oil market➔ Indexations➔ Traders psichology➔ USD/EUR

€/MWh

29

0

25

50

75

100

125

Euro

/MW

h

1998 1999 2000 2001 2002

25,7 26,731,9 31,5

38,9

Are markets signals adequate for investment?Even in a market with high wholesale prices, like Spain, prices donot provide adequate signals (until the last moment)

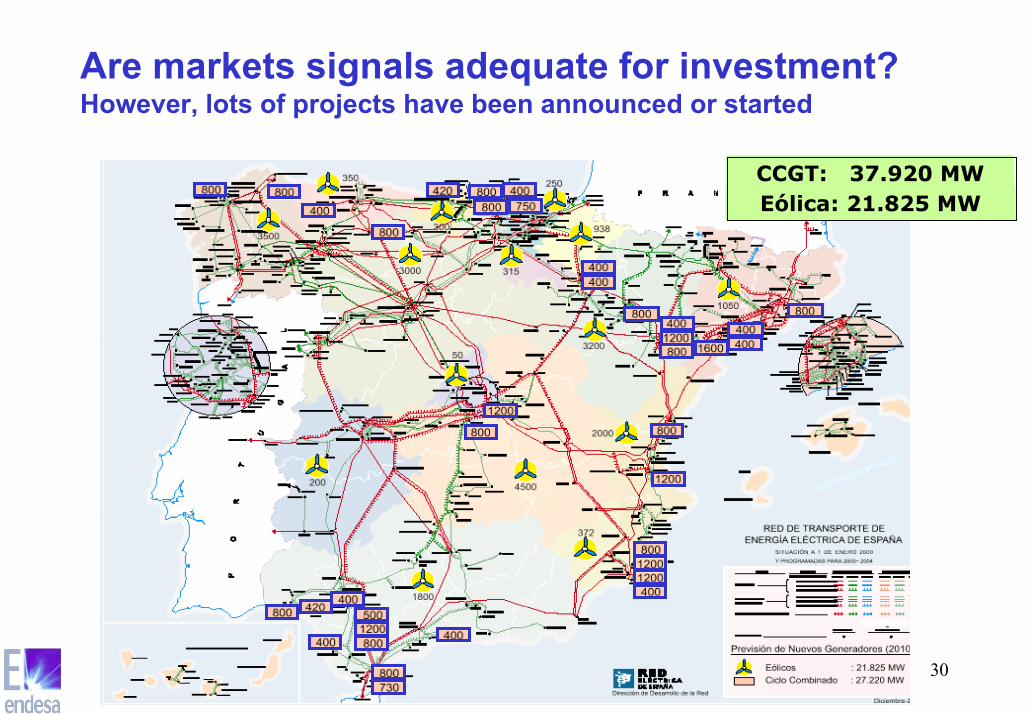

30

CCGT: 37.920 MWEólica: 21.825 MW

Are markets signals adequate for investment?However, lots of projects have been announced or started

31

Expected electricity prices

0

10

20

30

40

50

60

2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Base price (long term model results) Forward Base price (16/8/02)Peak price (long term model results) Forward Peak price (16/8/02)

Precios de electricidad esperados

0

10

20

30

40

50

60

2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Precio base modelo de largo plazo Precio forward base FranciaPrecio pico modelo de largo plazo Precio forward pico FranciaEscenario precio base considerado Escenario precio pico considerado

Wholesale prices in France-GermanySignificant gap between forward curve & economic reality

• Using a business dynamic long term model wecan conclude that:

➔ No clear trend in the expected Central Europeanelectricity prices

➔ Significant volatility can be expected due to theuncertainties of new capacity installed and thesensitivity of prices to small changes in capacity

• Big gap between forward curve and resultsobtained from the model.

➔ Prices obtained from the model are consistentwith expected costs

➔ What does this say about the forward curve?• It seems reasonable to assume a increase in

wholesale prices to adapt to the actual cost ofnew capacity

32

Wholesale prices in France-GermanySignificant gap between forward curve & economic reality

20

25

30

35

40

45

50

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

eur/M

Wh

base peak forward curve

Long termequilibrium pricethat allowscompleterecovery ofCCGT costsThis price level iscompatible withcurrent retailprices (similar tothe embeddedprices in pricesto smallcustomers)

Forward curve(market prices,not estimates)

Current disparity between marketprices and prices “embedded” intariffs cannot continue muchbeyond the total liberalisation ofretail market

33

Are markets signals adequate for investment?Spikes are natural in the short term prices, but are they reasonablein the forward curve?

1919,5

2020,5

2121,5

2222,5

2323,5

2424,5

2525,5

2626,5

2727,5

2828,5

2929,5

30

17-a

br-0

0

17-m

ay-0

0

17-ju

n-00

17-ju

l-00

17-a

go-0

0

17-s

ep-0

0

17-o

ct-0

0

17-n

ov-0

0

17-d

ic-0

0

17-e

ne-0

1

17-fe

b-01

17-m

ar-0

1

17-a

br-0

1

17-m

ay-0

1

17-ju

n-01

17-ju

l-01

17-a

go-0

1

17-s

ep-0

1

17-o

ct-0

1

17-n

ov-0

1

17-d

ic-0

1

17-e

ne-0

2

17-fe

b-02

17-m

ar-0

2

17-a

br-0

2

17-m

ay-0

2

17-ju

n-02

17-ju

l-02

17-a

go-0

2

17-s

ep-0

2

17-o

ct-0

2

17-n

ov-0

2

17-d

ic-0

2

17-e

ne-0

3

17-fe

b-03

17-m

ar-0

3

CAL 2002 CAL 2003 CAL 2004

34

Final thoughtsAre markets signals adequate for investment?

• An illiquid/non competitive market is not credible➔ Cannot be the basis for supply and generation activities in competition...

• How can we increase liquidity/credibility of the market?➔ Divestitures (the English solution) would be a way of bringing competition

and increasing liquidity✔ Bot no continental government seems to be seriously considering this...

national champions are the preferred objective➔ New entrants will take years to make an impact

✔ And “real” new entrants are in very short supply these days...➔ Only the development of an integrated European electricity market would

offer the possibility of a liquid market, with a sufficient number ofsignificant players

✔ Only the neighbours are bringing some real competition to the currentconcentrated markets

35

Final thoughtsThe key: fair access to electricity networks

• The objective: an European market in electricity➔ Only this can bring sufficient competition and liquidity in a reasonable time

frame➔ The place where that market is supposed to exist is the network

• Fair access to the network is the key to the development of theEuropean market

• The current level of network infrastructure allows for asignificant degree of integration of the markets➔ The barrier is not infrastructure, but long term contracts and regulation

• Access to the network is not cross-border trading➔ No more multiple networks, but one single European network!

36

WHEN

will prices raiseagain?

• WHEN capacity reserve margins tightens up.➔ This tends to happen before everybody expects

(though it can also reverse rapidly)

• WHEN interconnections allow to “transmit” scarcityin certain areas to the rest of Europe➔ Spain, Norway, Italy, Portugal

• WHEN neighbouring countries (Eastern Europe)stop exporting.➔ This could happen much more rapidly than expected

• BUT MAINLY, WHEN prices to final customers andwholesale prices are representative of real marketforces and not only political/economic interests

Final thoughtsWholesale prices will increase

37

Final thoughtsDealing with risks• A critical need to manage risk: flexibility

➔ In electricity & gas: balancing and flexible access to the network• Investment needs long term economic signals

➔ Even the most liquid markets provide forward curves for a limited time horizon• Regulatory measures have been tried

➔ Capacity payments (England, Spain, South America)➔ Capacity contracts (US)➔ But no clear solution➔ ...and beware regulatory interference with price spikes

• The most important need is the development of a real market➔ liquid➔ competitive➔ ... a single European market

• This is a regulatory/political issue: infrastructure is not the main barrier