J. Russotto Brussels The forthcoming revision of the EU Directive on Taxation of Savings: Its impact...

31

J. Russotto Brussels The forthcoming revision of the EU Directive on Taxation of Savings: Its impact on Switzerland and its banks Association of Foreign Banks in Switzerland Geneva, 17 November 2008

-

Upload

rudolph-hodge -

Category

Documents

-

view

216 -

download

2

Transcript of J. Russotto Brussels The forthcoming revision of the EU Directive on Taxation of Savings: Its impact...

J. Russotto

Brussels

The forthcoming revision of the

EU Directive on Taxation of Savings:

Its impact on Switzerland and its banks

Association of Foreign Banks

in Switzerland

Geneva, 17 November 2008

2

Contents of the presentation

A. Background and history

B. Principal proposed amendments to the

Directive

C. The Swiss-EU Agreement

D. Calendar, perspectives and concluding

observations

3

• Original goal of Directive 2003/48 (“EUSD”) is …

“to enable savings income in the form of interest payments made in one Member State to beneficial owners who are individuals resident for tax purposes in another Member State to be made subject to effective taxation in accordance with the laws of the latter Member State” (Article 1).

A. Background – History

4

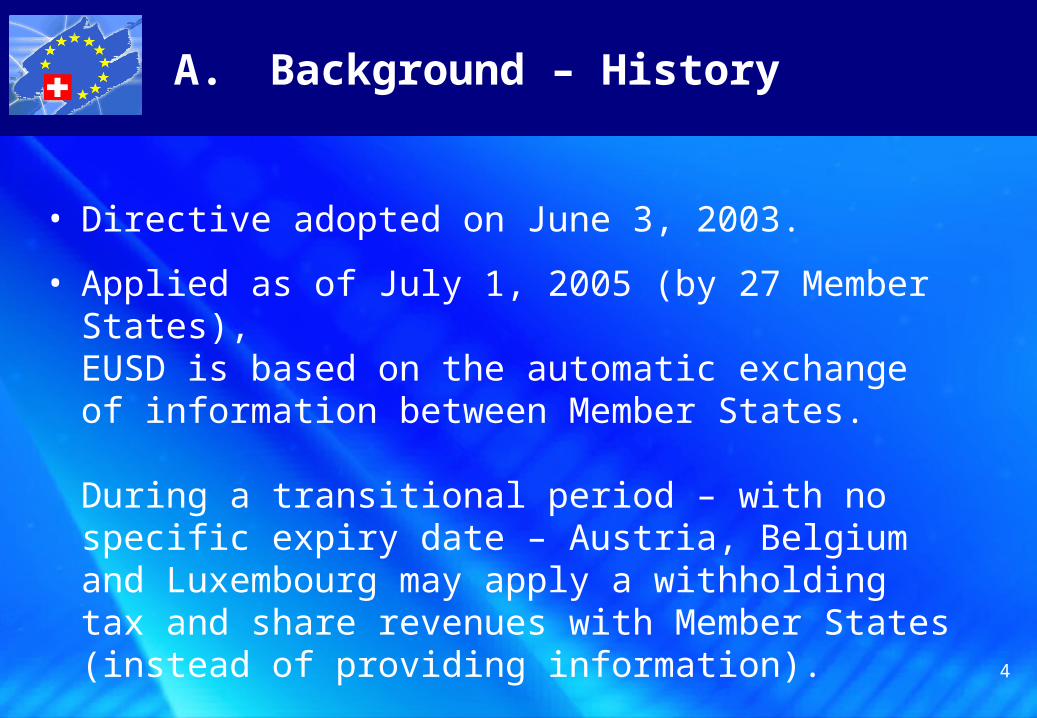

• Directive adopted on June 3, 2003.

• Applied as of July 1, 2005 (by 27 Member States),EUSD is based on the automatic exchange of information between Member States. During a transitional period – with no specific expiry date – Austria, Belgium and Luxembourg may apply a withholding tax and share revenues with Member States (instead of providing information).

A. Background – History

5

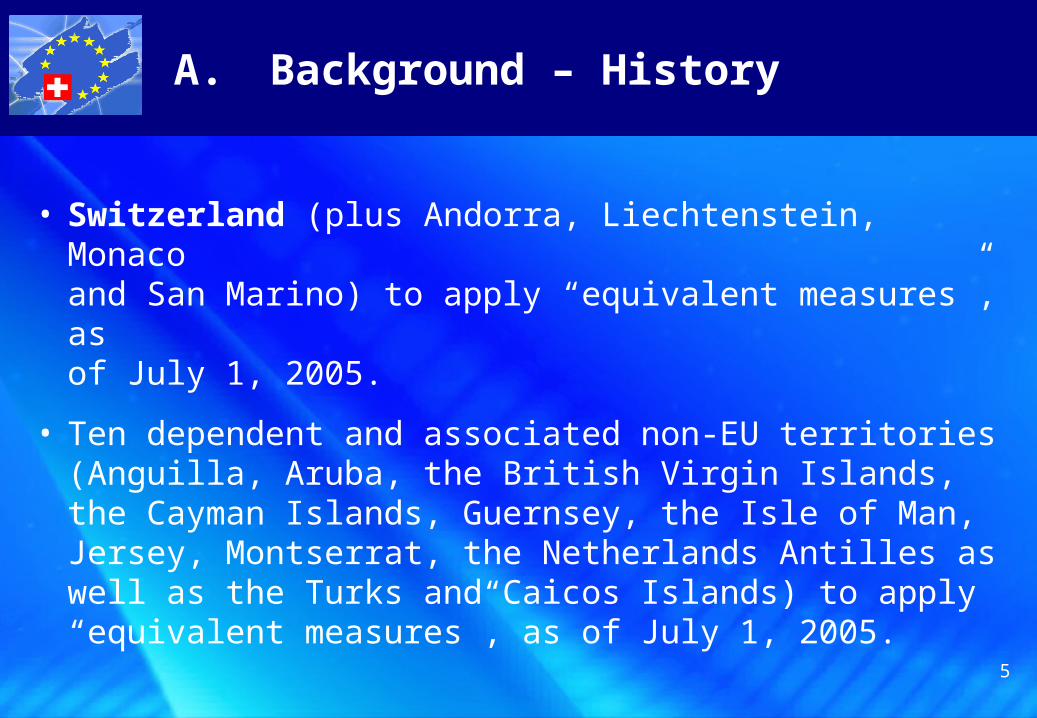

• Switzerland (plus Andorra, Liechtenstein, Monaco and San Marino) to apply “equivalent measures”, as of July 1, 2005.

• Ten dependent and associated non-EU territories (Anguilla, Aruba, the British Virgin Islands, the Cayman Islands, Guernsey, the Isle of Man, Jersey, Montserrat, the Netherlands Antilles as well as the Turks and Caicos Islands) to apply “equivalent measures”, as of July 1, 2005.

A. Background – History

6

A. Background – History

• Article 18 EUSD provides for periodic review of its

operation.

• Limited data availability (2005/2006) makes a detailed

quantitative analysis of EUSD difficult.

7

A. Background – History

• Acceleration of the review, in March 2008, following the Liechtenstein / Germany events: succession of Commission working groups and consultation with industry expert groups lead to Commission report of September 15, 2008.

• November 13, 2008: adoption by the Commission of the proposal amending EUSD, after its first three years of operation.

8

Review process indicated that:

• Coverage of EUSD is not as wide as intended

• There are many loopholes (in both automatic

exchange of information and withholding tax)

• Results of information exchange system are

debatable.

A. Background – History

9

Specific problems identified by the Commission:

1. Use of intermediary structures

2. Different treatment of investment funds (non-authorized UCITS)

3. Use of comparable products to debt claims (e.g., life insurance contracts)

4. Identification of beneficial owners

5. Use of conduit vehicles in third countries

6. Lack of statistics from Member States.

A. Background – History

10

The international dimension of EUSD review was also

carefully assessed: how best to prevent relocation of

savings to non-EU countries as a result of a

reinforced EUSD.

A. Background – History

11

Definition of savings income (Article 6)

The objective is that EUSD covers substantially equivalent income (to interest payments) from certain innovative financial products and from certain life insurance contracts. Savings income would thus include securities which are equivalent to debt claims (capital is protected up to 95% of total capital invested).

B. Principal proposed amendments to the Directive

12

Expanded definition of savings income (Article 6)

• Establish symmetry in treatment of UCITS and non-UCITS investment funds

• Inclusion of certain life insurance contracts.

B. Principal proposed amendments to the Directive

13

B. Principal proposed amendments to the Directive

Extension to legal entities(Articles 1 & 2)

Broadening the scope of EUSD to cover all payments to legal entities and arrangements held by individuals in

– other Member States, or

– non-EU jurisdictions.

14

B. Principal proposed amendments to the Directive

Extension to legal entities(Articles 1 & 2)

Paying agents in the EU – who are subject to EU anti-money laundering rules – to apply a “look-through” approach when making payment to intermediary structures established outside the EU (new Annex I – Cf. Point 2 as regards Switzerland).

15

B. Principal proposed amendments to the Directive

Extension to legal entities(Articles 1 & 2)

New Annex I also contains a list of several types of legal entities.

16

Definition of “beneficial owner”(Article 2)

As a consequence of the expanded scope of EUSD to legal entities, there is a redefinition of the concept of “beneficial owner” (Article 2.1(b)).

B. Principal proposed amendments to the Directive

17

B. Principal proposed amendments to the Directive

Definition of “paying agent upon receipt”(Article 4)

• New provisions intended to ensure consistent application

• To replace existing approach (upstream economic assessment) by a treatment based on a “positive” definition of the intermediary structures

• New approach would apply to certain types of entities (a “positive” list is included in a new Annex III), such as certain trusts and partnerships.

18

• Switzerland does not participate in the automatic exchange of information system

• Switzerland agrees to introduce a withholding tax system on interest income paid or credited by a paying agent (bank) established in Switzerland to a beneficial owner (an individual) with a tax domicile in one of the EU Member States.

C. The Swiss-EU Agreement

19

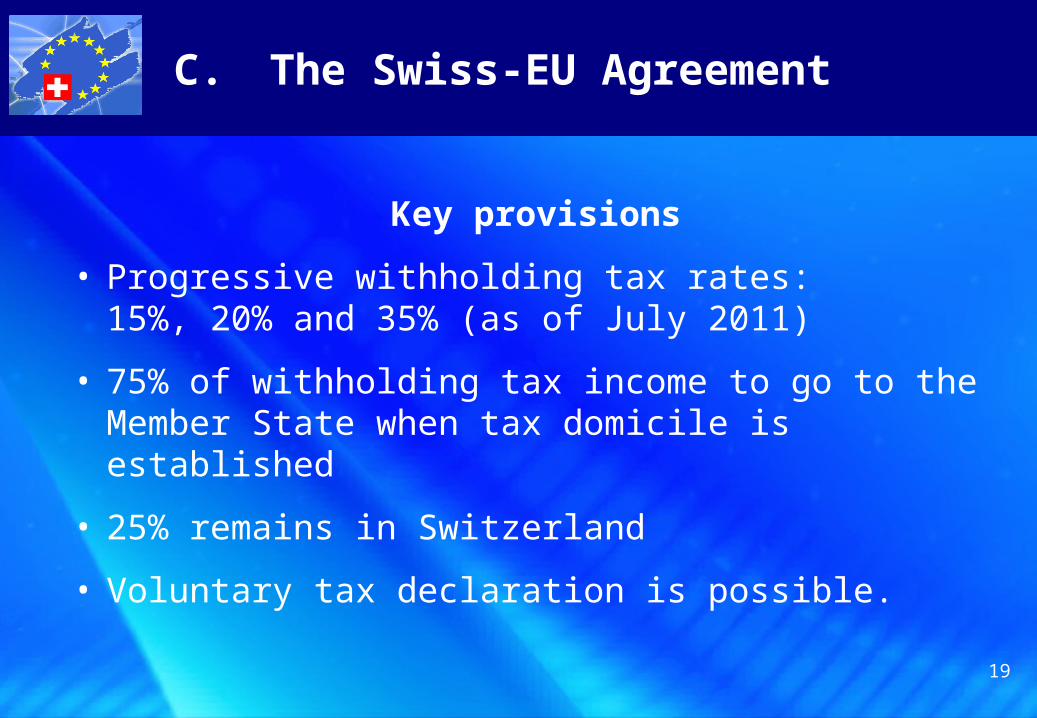

Key provisions

• Progressive withholding tax rates: 15%, 20% and 35% (as of July 2011)

• 75% of withholding tax income to go to the Member State when tax domicile is established

• 25% remains in Switzerland

• Voluntary tax declaration is possible.

C. The Swiss-EU Agreement

20

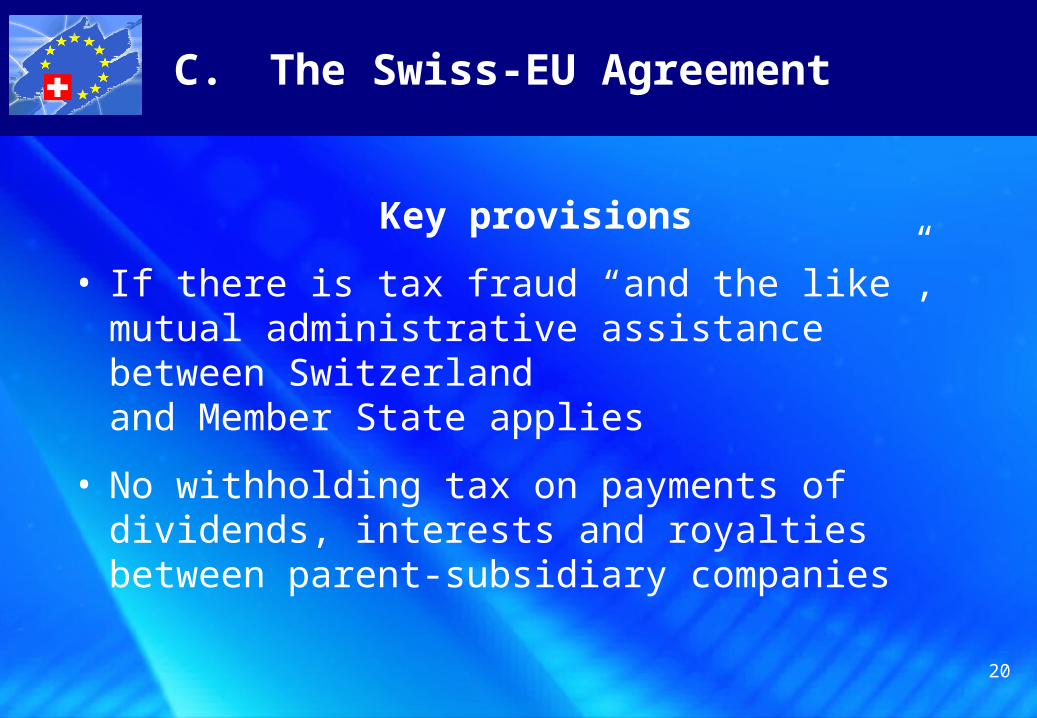

Key provisions

• If there is tax fraud “and the like”, mutual administrative assistance between Switzerland and Member State applies

• No withholding tax on payments of dividends, interests and royalties between parent-subsidiary companies

C. The Swiss-EU Agreement

21

C. The Swiss-EU Agreement

Key provisions

• At least every three years, consultation between Switzerland and the EU when Parties have acquired sufficient experience with the functioning of the Agreement – with a view to improving its operation (Article 13)

• Agreement is accompanied by a Memorandum of Understanding (“MOU”), including a provision regarding future negotiations between the EU and other important financial centres

22

C. The Swiss-EU Agreement

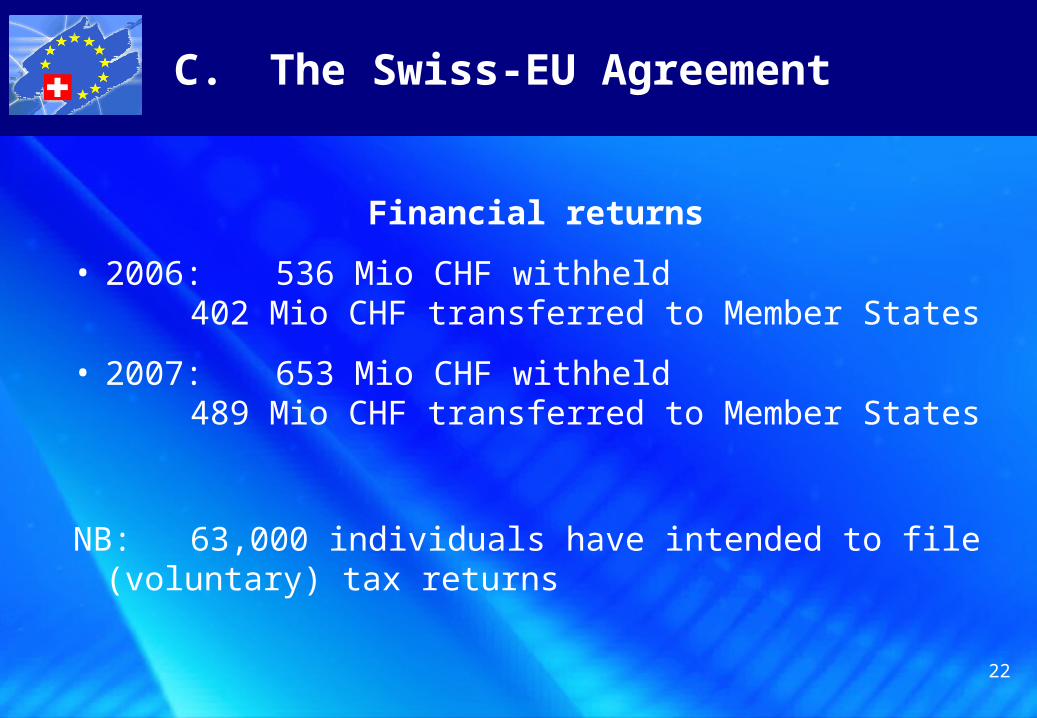

Financial returns

• 2006:536 Mio CHF withheld 402 Mio CHF transferred to Member States

• 2007:653 Mio CHF withheld 489 Mio CHF transferred to Member States

NB: 63,000 individuals have intended to file (voluntary) tax returns

23

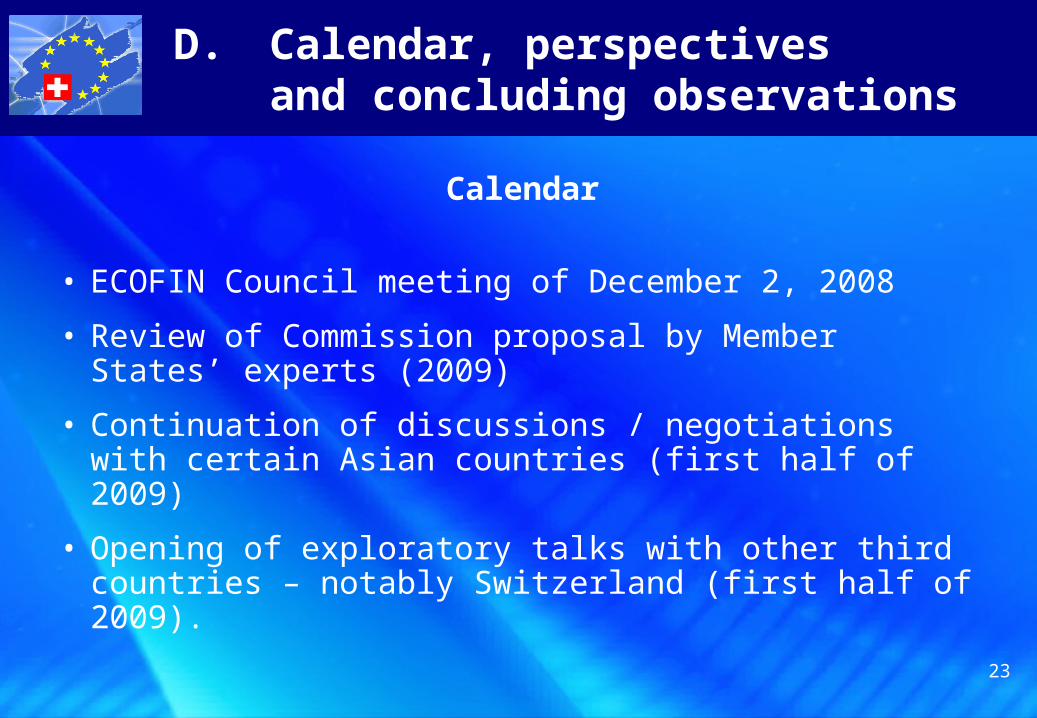

Calendar

• ECOFIN Council meeting of December 2, 2008

• Review of Commission proposal by Member States’ experts (2009)

• Continuation of discussions / negotiations with certain Asian countries (first half of 2009)

• Opening of exploratory talks with other third countries – notably Switzerland (first half of 2009).

D. Calendar, perspectives and concluding observations

24

Perspectives

• A significant task ahead

• Relevance and impact of current tax climate

• Germany and France announced intention to achieve greater fiscal transparency (October 21, at OECD gathering)

• Could there be an accelerated drive towards an information exchange system as sole system under the amended EUSD ?

D. Calendar, perspectives and concluding observations

25

Expected reactions from Member States

• France, Germany

• Austria, Belgium and Luxembourg

• UK

• Other Member State groupings

D. Calendar, perspectives and concluding observations

26

Third-country positions

• Asian countries

• Dependent and associated non-EU territories

• Non-EU countries: Liechtenstein, Monaco, Andorra and San Marino

• Switzerland

D. Calendar, perspectives and concluding observations

27

Concluding observations

In general:

1. Will there ever be an amended EUSD?

2. Looking at the review process, is time of the essence?

3. Will the proposed amendments be able to properly close the current loopholes?

4. Will the review of the EUSD proposal cause disruption to the “coexistence system” (exchange of information and withholding tax)?

D. Calendar, perspectives and concluding observations

28

As for Switzerland

1. Why Switzerland should care about the forthcoming EUSD proposal.

2. The system established by the Swiss-EU Agreement may be called into question in the medium term.

D. Calendar, perspectives and concluding observations

29

D. Calendar, perspectives and concluding observations

3. What could be the Swiss response, in the event the EU decides to review the operation of the Swiss-EU Agreement and, subsequently, propose a renegotiation of the Agreement?

4. Beyond compliance costs, the impact of an amended EUSD on Swiss banks will be considerable.

30

D. Calendar, perspectives and concluding observations

Final remark

An amended EUSD, followed by a possible renegotiation of the existing Swiss-EU Agreement may well represent the most important development in Swiss-EU bilateral relations in the coming five years.

31

![“Despite its outward strength, the [pharma] industry is ......“Despite its outward strength, the [pharma] industry is ailing. The ‘pipelines’ of forthcoming drugs on which](https://static.fdocuments.in/doc/165x107/5e92c27cd3268366384f0a7b/aoedespite-its-outward-strength-the-pharma-industry-is-aoedespite-its.jpg)

![Forthcoming Budget 2011-12[1]](https://static.fdocuments.in/doc/165x107/577d1d971a28ab4e1e8c9795/forthcoming-budget-2011-121.jpg)