ITAN in brief - ESPON · ITAN in brief || October 2014 Mexico. The respective regions are much more...

8

ITAN in brief N ° 6 || October 2014 Integrated Territorial Analysis of the Neighbourhoods ITAN major findings – The Neighbourhoods, a new driver for European growth The (relative) importance of Neighbourhoods for Europe The ITAN report assesses the economic growth potential for EU in the next decade (2010-2020) on the basis of a simple model: we extend the average growth rate of the years 2000-2010 to the next decade, both in current US $ and PPS. As a result, we have the share of each part of the world in the global economic growth (columns 1 and 3 of Table 1). Not surprisingly, the EU, northern America and China account for most of the growth. Despite the limited growth in the last decade for the EU and the US, their growth potential remains important at global level because of their weight in the global economy. The low cost of the Yuan results in much higher figures in PPS than in current US $ in the case of China. In a second step, IGEAT team within ITAN consortium assesses what it means for the EU, considering the current geography of its trade; the basic idea is that EU will benefit more from growth in areas where Europe currently has more market shares. The result is given in columns 2 and 4: by far, EU is the major source of potential growth for itself in the next decade. Then, three major market growth potentials appear: the US, around 11% of EU growth potential, China (9% in current US $ and 19% in PPS), and the Neighbourhoods with shares similar to the US. However, more than half of this potential growth is toward the East (Russia, plus Belarus, Europe influence around the world has declined over the years. As a result, European economic influence is more and more limited to its immediate neighbourhood. However, it does not mean that the Neighbourhoods are EU most important partners. Yet European Neighbour Countries (ENCs) represent 7.5% of the European countries trade and 11% of their potential market, yet they are shifting from a rent economy to an innovative economy, they hardly are a target for European investors. Neighbours could be a significant driver for European economy, their own development relies largely on Europe, nevertheless our region remains much less economically integrated than North America (including Mexico) or East Asia. ESPON applied research 2013/1/22 Final Report, version 17/07/2014 ITAN Scientific Coordinator Prof. Pierre Beckouche Université Paris 1 / CIST +33 (0)6 8699 1466 [email protected]

Transcript of ITAN in brief - ESPON · ITAN in brief || October 2014 Mexico. The respective regions are much more...

ITAN in brief n° 6 || October 2014

Integrated Territorial Analysis of the Neighbourhoods

ITAN major findings – The Neighbourhoods, a new driver for European growth

The (relative) importance of Neighbourhoods for Europe

The ITAN report assesses the economic growth potential for EU in the next decade (2010-2020) on the basis of a simple model: we extend the average growth rate of the years 2000-2010 to the next decade, both in current US $ and PPS. As a result, we have the share of each part of the world in the global economic growth (columns 1 and 3 of Table 1). Not surprisingly, the EU, northern America and China account for most of the growth. Despite the limited growth in the last decade for the EU and the US, their growth potential remains important at global level because of their weight in the global economy. The low cost of the Yuan results in much higher figures in PPS than in current US $ in the case of China.

In a second step, IGEAT team within ITAN consortium assesses what it means for the EU, considering the current geography of its trade; the basic idea is that EU will benefit more from growth in areas where Europe currently has more market shares. The result is given in columns 2 and 4: by far, EU is the major source of potential growth for itself in the next decade. Then, three major market growth potentials appear: the US, around 11% of EU growth potential, China (9% in current US $ and 19% in PPS), and the Neighbourhoods with shares similar to the US. However, more than half of this potential growth is toward the East (Russia, plus Belarus,

Europe influence around the world has declined over the years. As a result, European economic influence is more and more limited to its immediate neighbourhood. However, it does not mean that the Neighbourhoods are EU most important partners. Yet European Neighbour Countries (ENCs) represent 7.5% of the European countries trade and 11% of their potential market, yet they are shifting from a rent economy to an innovative economy, they hardly are a target for European investors. Neighbours could be a significant driver for European economy, their own development relies largely on Europe, nevertheless our region remains much less economically integrated than North America (including Mexico) or East Asia.

ESPON applied research 2013/1/22Final Report, version 17/07/2014

ITAN Scientific CoordinatorProf. Pierre BeckoucheUniversité Paris 1 / CIST+33 (0)6 8699 [email protected]

ITAN in brief || October 2014

Ukraine, and Moldavia); Turkey also plays a significant role, while the other Neighbourhoods remain marginal for EU growth potential because of their marginal economic weight as well as their limited economic growth and the fragmenta-tion of the national markets.

In Table 2, we focus on the importance of the Neighbourhoods in the EU relations to the world. In trade and FDI, this impor-

tance is limited. The reason is that most trade and FDI are internal in Europe. When these internal flows are excluded, Neighbourhoods appear as the main trade partner of the EU, though they remain very marginal in investment flows. Indeed, 7.5% of EU trade takes place with the Neighbourhoods, while the US only accounts for 6.2% and China for 2.2%. On the long run, in the last half-century, the importance of Neighbourhoods has been remarkably stable.

2

Table 1. Share (%) of the world main economic powers in the growth market potential for 2010-2020

Absolute growth potential 2010-2020 (current $)

Growth potential for the EU (current $)

Absolute growth potential 2010-2020 (PPS)

Growth potential for the EU (PPS)

EU27+ (1) 25.4 54.3 16.3 37.8

Eastern neighbours (2) 6.9 6.7 3.8 6.3Western Balkans 0.4 0.6 0.3 0.6Turkey 1.4 2.1 1.3 2.1Near East (3) 0.9 0.8 1.3 1.3Maghreb 0.4 0.9 0.5 1.2Neighbourhoods 9.9 11.1 7.2 11.5

North America 18.0 11.5 16.3 11.1India 2.7 1.7 7.4 5.2Japan 4.3 0.8 4.1 1.9China 15.7 8.9 23.9 19.3rest of the world 23.7 11.3 24.8 13.2TOTAL 100.0 100.0 100.0 100.0

Notes. (1) includes Switzerland, Norway, Iceland, Liechtenstein, Andorra. (2) Russia, Belarus, Ukraine, Moldavia. (3) Egype included.PPS: Purchasing Power Standard. Source: IGEAT database / ITAN

Table 2. Share (%) of Neighbourhoods and other parts of the world in EU relations and flows

Trade of goods: exports + imports

(2011)

FDI in and out (2006-2008)

Cooperation (2010) Air flows (2012) (Im)igrations

(2010) Energy supply

EU27+ (1) 70.0 71.8 0.0 80.4 37.9 42.4

Eastern neighbours (2) 3.8 2.2 1.8 1.9 5.7 21.1Western Balkans 0.5 0.2 3.5 0.7 6.1 0.3Turkey 1.3 0.7 1.7 1.7 7.9 0.1Near East (3) 0.4 0.0 3.3 0.8 1.2 0.7Israel 0.4 0.0 0.0 0.4 0.1 0.0Maghreb 1.1 0.2 4.6 1.5 8.7 10.3Neighbourhoods 7.5 3.4 14.8 7.1 29.8 32.5

Middle-East 1.7 0.5 1.5 2.0 1.7 8.6Sub-Saharan Africa 1.6 0.8 44.0 1.3 7.7 5.5North America 6.2 17.8 1.0 4.2 1.9 2.5Latin America 1.9 1.7 13.4 1.4 8.6 1.6Southern Asia 1.2 0.4 14.8 0.7 5.6 0.6Japan, Korea, Taiwab 2.2 1.1 0.0 0.5 0.6 0.8China 5.1 0.8 3.7 0.7 1.9 0.1rest of Asia & Oceania 2.8 1.9 6.8 1.1 3.8 3.4rest of the world 0.4 0.3 1.8TOTAL 100.0 100.0 100.0 100.0 100.0 100.0

Notes and source: see Table 1

October 2014 || ITAN in brief

Human flows can be tackled in two different perspectives: (i) airflows, which mainly take into account short-term mobility for medium and long distances. This mobility is mainly intra-European, since 80% of all movements are within European countries. Flows with Neighbourhoods account for more than 7% of total flows, more than any other part of the world. It indicates a distance effect, related to touristic, migratory and other types of air flows; (ii) migrations toward Europe. Neighbourhoods account for 30% of the stocks of migrants in Europe, while European themselves only account for about 38%.

Finally, Neighbourhoods also play a major role for energy supply in Europe. Europe provides 42% of its energy while Neighbourhoods provide 32.5%, two thirds from Russia and the rest from Maghreb, mostly Algeria and Libya. Middle East oil and gas producers play a limited role in comparison, with 9% of energy supply of Europe. In sum, Neighbourhoods play an important role for EU in two domains: migrations and energy supply. In contrast, Neighbourhoods are not considered as strategic economic partners, as well as in many other domains such as scien-tific cooperation.

Prospects: the wider region could be a response to the booming of East Asia

Figure 1 displays several conception of “European region”: EU27 + Iceland, Liechtenstein, Norway, Switzerland; + Western Balkans; + Eastern European Neighbour Countries (ENCs); + the Mediterranean ENCs; + sub-Saharan Africa, which can be regarded as an extension of the wider European region. In all cases, the contrast of its share of the world GDP is striking vis-à-vis the huge rise of the East Asian share. But indeed, the larger the European region, the higher its place in the world economy.

Figure 2 compares GDP growth since 1980 in the various neighbourhoods of Europe. It considers the ITAN Neighbourhoods, but also the Gulf plus Iraq and Iran, and EU new Member States (2004-2007), because prior to 2004 they were former Europe neighbours. The first lesson is that almost all of these neighbourhoods have an impressive economic growth, expressed in constant currency; neighbours are undeniably a major asset for Europe. Second, the economic hierarchy as dramati-cally changed during these last three decades: Eastern Neighbourhood was first and new Member States second, they are now in third and fourth position, whereas the Mediterranean and Middle-East neighbourhoods have become first and second; Western Balkans are now lagging behind.

This analysis has to be tempered by several facts: (i) the huge transition experienced by the former Socialist countries, with much better growth rates in the 2000s of course; (ii) the driving role of Israel and Turkey among the Mediterranean Neighbours, whose performance is much lower if one takes into account the sole Arab countries; (iii) the Arab countries performance is dampened by the on-going unrest and wars. Still, it has to be highlighted that European neighbouring areas are experiencing a long term shift from East to South, which is due to continue given demographic figures.

Beyond the European region case, the general trend throughout the world is that of a slowing down of economic integration within the major regions over the 2000s, due to the booming importance of a new global player: China, which has become a major trade partner for countries whatever the region they belong to. Should we conclude that the regional integration era is over? Certainly not, because the long run stays in favour of the regionalisa-tion thesis. In the 1960s, European countries would only make a third of their trade between them and trading links would still be lower between the USA, Canada and

3

Figure 1. World markets: can we cope with the rise of the East Asian region?

0

5

10

15

20

25

30

35

40

45

1973 1990 2000 2009 2030

5

10

15

20

25

30

35

40

45

1973 1990 2000 2008

Europe + Mediterranean Neighbours +Eastern Neighbours + Sub-Saharan Africa

0

2

Europe + Western Balkans

Europe + Eastern NeighboursEurope + Mediterranean Neighbours

East Asia

Nafta countriesAmericas

3

2. Morocco, Algeria, Tunisia, Libya, Egypt, Occupied Palestinian Territory, Israel,Jordan, Lebanon, Syria &Turkey

4. China, Japan, ASEAN countries, South Korea, North Korea, Australia, New-Zealand 3. Belarus, Ukraine, Moldavia, Armenia, Georgia & Azerbaijan

1. UE 27 + Iceland, Norway, Liechtenstein, Switerzland

Share of world population (%) Share of world GDP (PPP), %

Source: Angus Madison, 20124

1

1

11

Figure 2. The Neighbourhoods, a new driver of economic growth for Europe

0

200

400

600

800

1 000

1 200

1 400

1980 1990 2000 2010

Source: UNCTAD, Angus Madison & P.Beckouche, 2012

Gulf, Iraq & Iran

GDP (billion constant 2005 US $)

EU new member states (2004-2007)

Southern & Eastern Med. countries 2

Eastern neighbourhood & Russia 3

South & East Med. Arab countries

Western Balkans1

2. Including Turkey & Israel1. Excluding Slovenia

3. Belarus, Ukraine, Moldova, Georgia, Armenia, Azerbaijan & Russia

ITAN in brief || October 2014

Mexico. The respective regions are much more integrated today. Figure 3 shows that, even at a slower pace, the trade regionalisation is on-going for the US as well as for Japan. The big difference with Europe is that the latter trades very much within UE and very little with developing and emerging countries of its neighbourhood.

Another feature of the previous section has to be further analysed: the declining role of Europe in its Neighbours trade. Over the last three decades, European new Member States have drastically reoriented their trade with western Europe instead of the former Soviet bloc. But this is the reverse way for neighbourhoods, which means that EU membership is a driver to trade regional integra-tion whereas a Neighbourhood status comes down to declining integration with Europe. All neighbourhoods of Europe, in a wide meaning including Sub-Saharan Africa

and Gulf States, send to Europe a declining part of their exports and import a declining part of European products. This can be considered good news if it means a wider insertion of these countries in global economy. This can also be regarded as bad news for Europe influence which remains high upon its neighbourhoods, but is undoubtedly declining.

Figure 4. Investments in the peripheries of the Triad, slowdown in the centres

Source: World Bank, 2012

10

15

20

25

30

35

40

45

1980 1990 2000 2010

Gross fixed capital formation (% of GDP)

Pacific & East Asia (developing countries)

Japan

Latin America

USA & Canada

Morocco

Egypt

Ukraine

European Union

1980 1990 2000 2010

Map 1. FDI inflows and share in GDP in the 2000s

This map does notnecessarily reflect theopinion of the ESPONMonitoring Committee© CNRS/GIS CIST, ITAN, 2013

FDI (billion $) FDI share in GDP (%)

Regional level: National levelSource: ESPON Database, ESPON project (ITAN), CNRS GIS CIST, 2013.

Origin of data: UNCTAD - IGEAT, EuroBroadMap project (PCRD) & Europe in the world (ESPON)© UMS RIATE for administrative boundaries - For some territories no clear international statement exists

2500 32 7 3,8 2,9 1,8 0181 (USA)77 (CHN)45 (HKG)18 (IND)2 (MAR)

Figure 3. The share of developing neighbours is high in East Asian and American regions

0

10

20

30

40

50

60

70

80

90

100

1986 1996 2006 2011 1986 1996 2006 20110

10

20

30

40

50

60

70

80

90

100

0

10

20

30

40

50

60

70

80

90

100

1986 1996 2006 2011

Source: ULB - IGEAT, 2012

Share (%) of the region in the merchandise trade (export + imports values)

Western Europe Japan United states

SEMCs

EU new member states (2004-2007)Western Europe

W. Balkans & Eastern neighb.2

1

1

Rest of Latin AmericaMexicoCanada

Australia & New-ZealandRest of East Asia developingChinaAsian Dragons (Exclud.Taiwan)

2. Including Russia1. EU 15, Iceland, Liechtenstein, Norway & Switzerland

4

October 2014 || ITAN in brief

Europe invests very little in its Neighbourhoods…

East Asian region boom is based on the complementa-rity between its national economies: highly developed (Japan), developed (Dragons), and developing (China…). Developed countries have found drivers for growth in their developing neighbourhood. The complementarities are less obvious between the US and Latin America but they exist too (Figure 4). In the European wider region, this is the case when it comes to Morocco for instance, but not for Egypt, whereas Ukraine shows a chaotic path. Since the Arab spring, investment in the Mediterranean Neighbourhood as diminished.

Mediterranean Neighbours remain marginal players in the world FDI flows (Map 1). North Africa attracts less than 1% of the world FDI inflows, the Arab Near-

East (that is Near-East except Israel and Turkey) less than 0.5%. Turkey is rising but attracts less than 0.8%. Eastern Neighbourhood shows more attractive: alto-gether Western Balkans and Eastern Neighbourhood attracted 1.1% of the world FDI inflows in the 1990s and 4.3% in the 2000s. But these figures stay far away from Asian records. Under the impetus of Japanese compa-nies, emerging and developing East Asia attracted 7% of the world FDI inflows in the 1970s, 9% in the 1990s and 15.5% (Chinese boom) in the 2000s. The post-crisis period confirms this mega trend: in 2007 China has attracted US$85bn, in 2011 the figure reached 125; the other emerging and developing East Asian coun-tries respectively 150 and 210. As a whole, emerging and developing East Asian countries have attracted in 2011 22% of the world FDI inflows –much ahead of Latin America (10%), not to speak of the European Neighbour Countries.

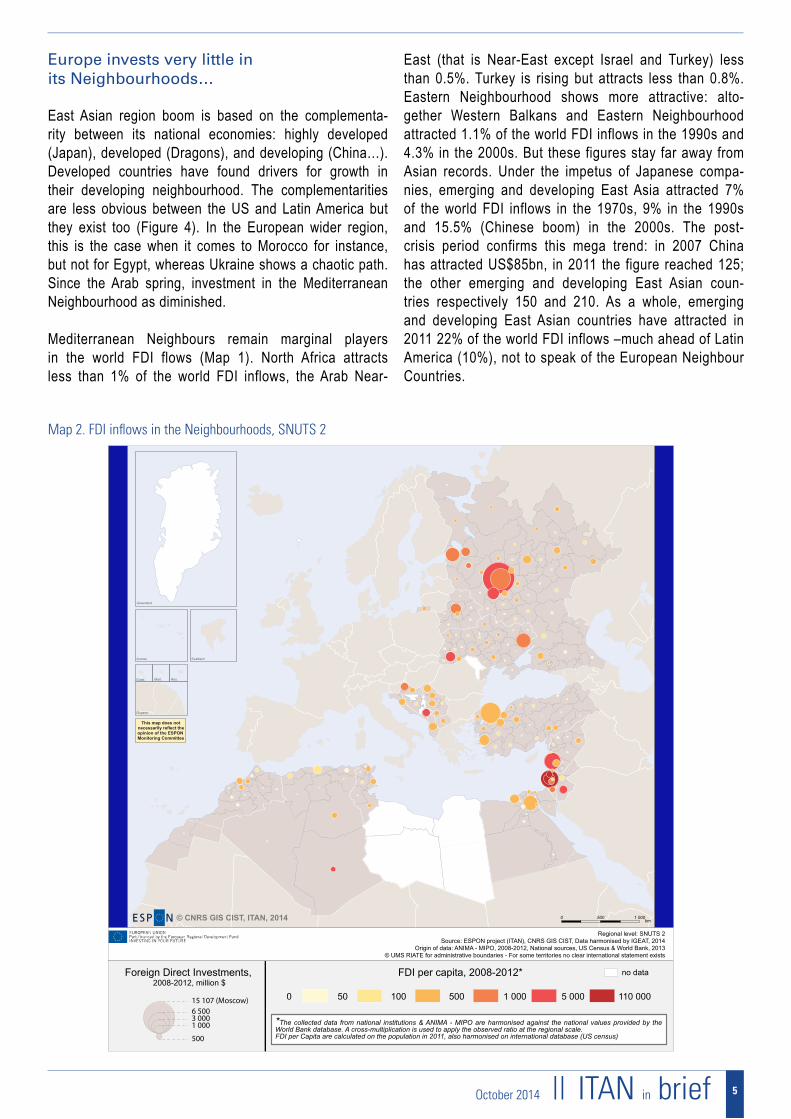

Map 2. FDI inflows in the Neighbourhoods, SNUTS 2

This map does notnecessarily reflect theopinion of the ESPONMonitoring Committee

0 1 000500km© CNRS GIS CIST, ITAN, 2014

Acores

Guyane

Guad. Mart. Reu.

Greenland

Svalbard

Regional level: SNUTS 2Source: ESPON project (ITAN), CNRS GIS CIST, Data harmonised by IGEAT, 2014

Origin of data: ANIMA - MIPO, 2008-2012, National sources, US Census & World Bank, 2013© UMS RIATE for administrative boundaries - For some territories no clear international statement exists

Foreign Direct Investments, 2008-2012, million $

FDI per capita, 2008-2012*

500100500 5 0001 000 110 000

no data

15 107 (Moscow) 6 500 3 000 1 000

500

*The collected data from national institutions & ANIMA - MIPO are harmonised against the national values provided by the World Bank database. A cross-multiplication is used to apply the observed ratio at the regional scale. FDI per Capita are calculated on the population in 2011, also harmonised on international database (US census)

5

ITAN in brief || October 2014

… even in their dynamic territories

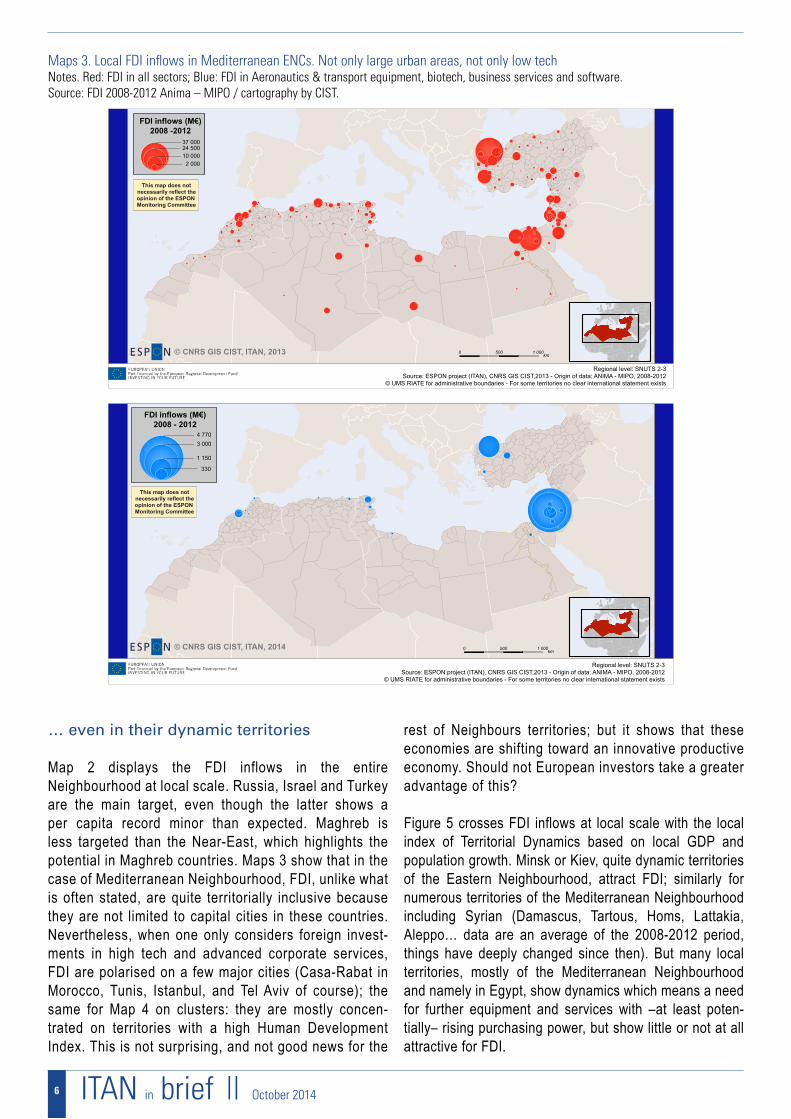

Map 2 displays the FDI inflows in the entire Neighbourhood at local scale. Russia, Israel and Turkey are the main target, even though the latter shows a per capita record minor than expected. Maghreb is less targeted than the Near-East, which highlights the potential in Maghreb countries. Maps 3 show that in the case of Mediterranean Neighbourhood, FDI, unlike what is often stated, are quite territorially inclusive because they are not limited to capital cities in these countries. Nevertheless, when one only considers foreign invest-ments in high tech and advanced corporate services, FDI are polarised on a few major cities (Casa-Rabat in Morocco, Tunis, Istanbul, and Tel Aviv of course); the same for Map 4 on clusters: they are mostly concen-trated on territories with a high Human Development Index. This is not surprising, and not good news for the

rest of Neighbours territories; but it shows that these economies are shifting toward an innovative productive economy. Should not European investors take a greater advantage of this?

Figure 5 crosses FDI inflows at local scale with the local index of Territorial Dynamics based on local GDP and population growth. Minsk or Kiev, quite dynamic territories of the Eastern Neighbourhood, attract FDI; similarly for numerous territories of the Mediterranean Neighbourhood including Syrian (Damascus, Tartous, Homs, Lattakia, Aleppo… data are an average of the 2008-2012 period, things have deeply changed since then). But many local territories, mostly of the Mediterranean Neighbourhood and namely in Egypt, show dynamics which means a need for further equipment and services with –at least poten-tially– rising purchasing power, but show little or not at all attractive for FDI.

Maps 3. Local FDI inflows in Mediterranean ENCs. Not only large urban areas, not only low techNotes. Red: FDI in all sectors; Blue: FDI in Aeronautics & transport equipment, biotech, business services and software.Source: FDI 2008-2012 Anima – MIPO / cartography by CIST.

Regional level: SNUTS 2-3Source: ESPON project (ITAN), CNRS GIS CIST,2013 - Origin of data: ANIMA - MIPO, 2008-2012

© UMS RIATE for administrative boundaries - For some territories no clear international statement exists

This map does notnecessarily reflect theopinion of the ESPONMonitoring Committee

© CNRS GIS CIST, ITAN, 2013 0 1 000500km

2 00010 00024 50037 000

FDI inflows (M€)2008 -2012

Regional level: SNUTS 2-3Source: ESPON project (ITAN), CNRS GIS CIST,2013 - Origin of data: ANIMA - MIPO, 2008-2012

© UMS RIATE for administrative boundaries - For some territories no clear international statement exists

© CNRS GIS CIST, ITAN, 2014

This map does notnecessarily reflect theopinion of the ESPONMonitoring Committee

0 1 000500km

FDI inflows (M€)2008 - 2012

4 7703 000

1 150

330

6

October 2014 || ITAN in brief

Developing countries rely very much on investment from their developed neighbours

Seen from developing countries standpoint, the geog-raphy of FDI flows is different, because they highly rely on investments originated from their developed neigh-bours. For example Morocco, Tunisia or even Turkey FDI inflows highly come from Europe: 85% for Morocco, 57% for Tunisia and 77% for Turkey at the end of the 2000s. What is the evolution? Again, the role of Europe as FDI provider for the whole Mediterranean ENCs is declining: more than 50% at the beginning of the 2000s, 30% in 2010 (the figure is 20% for the Gulf as origin of FDI invested in Mediterranean ENCs). In other regions, figures are alike: half FDI flows in Mexico come from the US; the bulk of FDI flows in China or Thailand comes from Japan and the Dragons (along with Caribbean tax havens, Maps 5).

Map 4. Clusters in Maghreb: shifting from a rent to an innovative economy

")!(

!(

!(

!(

!(

!(

!(

!(!(!(

")

")

!(

!(!(!(

!(

")")

")

")

")

")!(

!(

!(

!(

")

!(

")

")

")

")

!(

!(

RabatCasablanca

Tunis

Monastir

average

strong

weak

Local Humandevelopment index

(*) Information and communication technology

")Others!(

")Environment!(

")ICT*!(

")Metal & electronics!(

")Textiles & clothing!(

")Agro-food sector!(

Establishedor emerging Expected

Sector & Condition

Regional level: SNUTS3 V1Source: ESPON Database, ITAN, CNRS GIS-CIST, 2014

Origin of data: National statistics institutes, IPEMED© UMS RIATE for administrative boundaries

For some territories no clear international statement exists

km4002000© CNRS GIS-CIST, ITAN, 2014

This map does notnecessarily reflect theopinion of the ESPONMonitoring Committee

Figure 5. Highly dynamic territories and FDI inflows: a crosscut methodology

0,1

1

10

100

1000

10000

Sou

th R

egio

nM

oskv

aLe

bano

nM

insk

City

Kha

nty-

Man

siys

kiy

avvt

onom

nyy

okru

gD

amas

cus

Dei

r ez-

Zor

As

Suw

ays

Koc

aeli,

Sak

arya

, Düz

ce, B

olu,

Yal

ova

Dis

trict

of T

unis

Cha

ouia

Oua

rdig

haH

atay

, Kah

ram

anm

araş

, Osm

aniy

eM

iddl

e R

egio

nTa

rtous

(Tar

tus)

Edl

eb (i

dlib

)N

ord-

est

Mar

rake

ch T

ensi

ft A

l Hao

uzR

espu

blik

a D

ages

tan

Asw

anH

oms

Dou

kkal

a A

bda

Al-R

akka

(Ar-R

aqqa

h)A

l Min

yaC

ity o

f Kyi

vA

lepp

oL&

apos

;Orie

ntal

Al-S

wed

aa (A

s Su

way

da)

Fes

Boul

eman

eTa

dla

Azila

lBa

ni S

uway

fLa

ayou

ne B

oujd

our S

akia

El H

amra

Al-L

atta

kia

(Lat

akia

)A

l Buh

ayra

hA

syut

Dam

ascu

s co

untry

side

Al W

adi a

l Jad

idN

orth

Reg

ion

Taza

Al H

ocei

ma

Taou

nat

Al M

inuf

iyah

Ad

Daq

ahliy

ahR

espu

blik

a In

gush

etiy

aA

sh S

harq

iyah

Al Q

alyu

biya

hA

l Fay

yum

Mat

ruh

Oue

d E

d da

hab

Lago

uira

Ham

aD

araa

Al-Q

unei

tra (Q

unei

tra)

Al-H

assa

ke (A

r-H

asak

ah)

Kaf

r ash

Sha

ykh

Al G

harb

iyah

Yam

alo-

Nen

etsk

iy a

vton

omny

y ok

rug

Source: ANIMA, National sources, World Bank, 2013

FDI (2008-2012) $ per capita cf. See map «territorial dynamic, 2000-2010»

The collected data from national institutions & ANIMA - MIPO are harmonised against the national values provided by the World Bank database. A cross-multiplication is used to apply the observed ratio at the regional scale. FDI per Capita are calculated on the population in 2011, also harmonised on international database (US census)

Total population annual growth rate

2000 - 2010

Average* +1 σ- 1 σ**

- 1 σ

Average

GDP annual growth rate2000 - 2010

+1 σ Dynamic territories

No FDI0 - 11 - 100 ($ per capita)100 - 1 790

7

This dossier can be consulted online, with extendable images, onwww.gis-cist.fr/portfolio/itan_dossier6

Maps 5. Where do FDI inflows come from? Geographical proximity matters (average 2006-2008)

This map does notnecessarily reflect theopinion of the ESPONMonitoring Committee

Acores

Guyane

Guad. Mart. Reu.

Greenland

Svalbard

Inflows of FDI to Turkey (M€)

© CNRS GIS CIST, ITAN, 2013

Regional level: National levelSource: ESPON Database, ESPON project (ITAN), CNRS GIS CIST, 2013 - Origin of data: ANIMA - MIPO, 2013

© UMS RIATE for administrative boundaries - For some territories no clear international statement exists

0 1 500750km

Central Asia

Sub Saharan Africa

FDI inflows fromthe rest of the world:

North America

Latin America

Eastern Asia

Southern Asia

10 000

3 000900100

This map does notnecessarily reflect theopinion of the ESPONMonitoring Committee

Acores

Guyane

Guad. Mart. Reu.

Greenland

Svalbard

FDI inflows fromthe rest of the world:

North America

Latin America

Eastern Asia

Southern Asia

Inflows of FDI to Egypt (M€)

15 3009 200

2 5001 000

100

© CNRS GIS CIST, ITAN, 2013

Regional level: National levelSource: ESPON Database, ESPON project (ITAN), CNRS GIS CIST, 2013 - Origin of data: ANIMA - MIPO, 2013

© UMS RIATE for administrative boundaries - For some territories no clear international statement exists

0 1 500750km

This map does notnecessarily reflect theopinion of the ESPONMonitoring Committee© CNRS GIS CIST, ITAN, 2013

Origin of FDI in % (annual average)

Regional level: National levelSource: ESPON Database, ESPON project (ITAN), CNRS GIS CIST, H.Pecout, 2013

Origin of data: UNCTAD - IGEAT, EuroBroadMap project (PCRD) & Europe in the world (ESPON)© UMS RIATE for administrative boundaries - For some territories no clear international statement exists

Origin of Foreign Direct Investments in Mexico (%)

57% (USA)

16% (NLD) 5% (BEL) 5% (ESP) 4% (GBR) 4% (FRA)

FDI in Mexico FDI in Thailand

FDI in Turkey FDI in Egypt

This map does notnecessarily reflect theopinion of the ESPONMonitoring Committee© CNRS GIS CIST, ITAN, 2013

Regional level: National levelSource: ESPON Database, ESPON project (ITAN), CNRS GIS CIST, 2013

Origin of data: UNCTAD - IGEAT, EuroBroadMap project (PCRD) & Europe in the world (ESPON)© UMS RIATE for administrative boundaries - For some territories no clear international statement exists

Origin of Foreign DirectInvestments in Thailand (%)

32% (SGP)

29% (JPN)

7% (USA) 6% (BMU) 5% (PAN) 4% (NLD)

SGP

BMU

ITAN project fundingITAN project is financed by the ESPON 2013 Programme (European Observation Network for Territorial Development and Cohesion).www.espon.eu

ITAN objectives– Providing territorial evidence for a better knowledge of the Neighbourhood territories (from Morocco to Russia and the Arctic territories), their dynamics, flows between these regions and the ESPON territory

– Building a sustainable database: diverse data types (statistical, network, spatial, grid data) at local level in each country of the European Neighbourhoods, and mapping analyses

– Giving recommendations on territorial cooperation to be picked-up in the territorial agenda of the EU Member States, Iceland, Liechtenstein, Norway and Switzerland and the Neighbour countries, and to be included within the European Neighbourhood Policy

ITAN projectwww.espon.eu/main/Menu_Projects/Menu_AppliedResearch/itan.html

ITAN consortium– CNRS / CIST (International College of Territorial Sciences), France

www.gis-cist.fr– IGEAT, Université Libre de Bruxelles, Belgium – igeat.ulb.ac.be– MCRIT, Barcelona, Spain – www.mcrit.com– NORDREGIO, Stockholm, Sweden – www.nordregio.se+ close cooperation with a network of scientists of all the Neighbour countries

![Nordic regionalisation of a greenhouse-gas …/RMK110[1].pdf · Nordic regionalisation of a greenhouse-gas ... Report number/Publikation RMK No. 110 ... Nordic regionalisation of](https://static.fdocuments.in/doc/165x107/5b81a2b97f8b9a7b6f8ccf17/nordic-regionalisation-of-a-greenhouse-gas-rmk1101pdf-nordic-regionalisation.jpg)