IT Financial Management: un cambio di prospettiva … · IT Financial Management: un cambio di...

22

AIEA Sessione di studio Milano, 5 novembre 2009 IT Financial Management: un cambio di prospettiva per il miglior governo dell‟IT Christian Cantù Partner iCONS – Innovative Consulting

Transcript of IT Financial Management: un cambio di prospettiva … · IT Financial Management: un cambio di...

AIEA Sessione di studio

Milano, 5 novembre 2009

IT Financial Management: un cambio di prospettiva per il miglior governo dell‟IT

Christian CantùPartner iCONS – Innovative Consulting

Introduzione

Laureato in Ingegneria Gestionale al Politecnico di Milano

Co-fondatore e partner di iCONS – Innovative Consulting e iSYS –

Innovative Systems

Socio itSMF Italia, responsabile del gruppo di lavoro ITIL e Sourcing

Rappresentante itSMF Italia per iDaSC (itSMF International Chapter

Development and Support Committee)

IT Service Manager, ITIL Expert, itSMF ISO20000 Consultant,

PRINCE2 Practitioner, M_o_R/BiSL/CobiT Foundation

Co-autore dell‟articolo “The unclear relationship between change,

release and project management”, pubblicato in “Global Best

Practices”, VHP

Indirizzo mail [email protected]

In tempi di crisi … ma non solo

I costi costituiscono un parametro chiave per guidare la strategia IT

L‟IT Financial Management aiuta a controllare la relazione tra costi e

qualità dei servizi IT

From IT Financial Management, VHP

and ITIL V3

Che cosa è l‟IT Financial

Management 1 di 2

Financial Management, un insieme di responsabilità e attività che includeAdministration – Recording, clarifying and interpreting financial transactions and events (this involves maintaining records, book-keeping, preparing balance sheets and profit and loss accounts, preparing value added statements, managing cash, handling depreciation and accounting for inflation).

Management control - Predicting the financial performance of the business and providing a basis for decision-making and for raising finance; accounting for and analyzing costs, thus providing the basis for allocation of costs to products, services or activities, preparing and controlling financial budgets, analyzing performance in terms of variance analysis (cost-volume-profit analysis), financial aspects of risk analysis, cost-benefit analysis and cost-effectiveness analysis.

Finance - Controlling and optimizing the use of financial resources (raising funds, planning for loan requirements/funds surplus, relationships with credit institutes, management of payments to suppliers and collection of revenue from customers, support for investment decisions, obligations for tax payments to government).

L‟IT è parte di un‟organizzazione e l‟IT Financial Management, al di fuori del contesto dell‟IT Service Management, può essere interpretato come un sottoinsieme di responsabilità e attività del financial management assegnate all’IT

Che cosa è l‟IT Financial

Management 2 di 2

Nel contesto dell‟IT Service Management, l‟IT Financial

Management è un sottoinsieme specifico di responsabilità e attività

In ISO/IEC 20000 we find Budgeting and Accounting for IT Service, with

objective: “to budget and account for the cost of service provision”

IT financial management: ‟a common abbreviation of financial management

for IT services‟

Financial Management for IT Services: „the process responsible for

managing an IT service provider's budgeting, accounting and charging

requirements‟From ITIL v2 and v3

Diversi scenari di evoluzione

Ciascuno scenario

è caratterizzato da

peculiarità, dal

punto di vista di:

Prospettiva

Benefici

Ruoli

Processi

Strumenti

Goals and objectives related toorganization’s ones (such as knowing the cost

of functions and the value of assets to achievebusiness objectives)

IT Financial Management

maturity and complexity

Internal IT

Departments

Budgeting, accounting and (potentially)

charging for IT Services

Evaluating IT Services (total cost of provisionand value for the users/customers)

Internal IT

Service Providers

Market focused

IT Service Providers

Incremental goals of IT

Financial Management

Dependency from corporate FM, usually no charging

ITSM culture, sometimes charging, strong link to

corporate FM but specific needs (e.g. forecasting)

“Independent” (IT) Financial Management

Figure from IT Financial Management, VHP

Il modello di processi di IT Financial

Management

Figure from IT Financial Management, VHP

The objective of the annual closure activity is to provide agreed reports (e.g. profit and loss statements) for

the closed budget year.

The objective of delta management is to take a decision on deltas between forecasted (balance at a date plus

estimations to the end of budget period), or actual costs, versus budgeted costs

and revenues at the time they are determined.

The objective of budget review is to check and review a previously defined and agreed budget and to set a new

budget, which will replace the previous and will become ’current’, used to verify

and track progress of costs and revenues.

The objective of the periodic closure activity is to provide accurate and

reliable information and reports (e.g. profit and loss statement) about actual

costs and revenues of a closed period of the financial year or budget year (for

example a specific month).

Budgeting, in our context, is the activity ensuring that the correct financial

budget is defined for the provision of IT services. It is also the means of

delegating control and monitoring performance against predefined targets.

Periodic forecasting is aimed at defining the costs and revenues from a certain

instant, e.g. when forecast is required, to the end of a period, for example the budget year. Forecast, together with

balance, is typically used to be compared with budget.

The objective of investment evaluation is to determine the suitability of investing money to implement an initiative (e.g. an IT project). This is performed by comparing costs with the

benefits expected from implementing the initiative.

The objective of policy management is to define

and maintain a set of policies to manage IT

financial management.

The objective of planning is to predict and control the spending of

money to achieve the business objective in the medium/long term. The business objectives are defined

in the strategic business plan.The objective of pricing is to determine the selling price of the IT services supplied. The objective of charging is to

charge customers according to agreed terms and

conditions.

Relazioni con ITILv3

Figure from IT Financial Management, VHP

Service

Strategy

Service

Design

Service

Transition

Service

Operation

Continual Service

Improvement

Policy Management

IT Financial Planning

Pricing

InvestmentsEvaluation

Delta Management

Annual Budget

Budget Review

PeriodicClosure

AnnualClosure

Charging

PeriodicForecasting

Come può l’IT Financial Management essere collocato

unicamente nella fase Service Strategy del ciclo di vita del

servizio?

L‟obiettivo dell‟IT Financial Management

per un IT Service Provider interno

Quale il principale obiettivo dell’IT

Financial Management per un IT Service

Provider interno?

La conoscenza affidabile del full cost dei servizi IT erogati!

Questa è la direzione delle best

practice …

There shall be clear policies and processes for:

a)…..

b) apportioning indirect costs and allocating direct costs to services;

c)…..

ISO/IEC 20000 oggi

There shall be clear policies and processes for:

a) …..

b) apportioning indirect costs and allocating direct costs to services to provide an overall cost for each service;

c) …..

ISO/IEC 20000 nuovo draft

Perché …

… è così importante da raggiungere?

Facilita e supporta il processo decisionale e le buone decisioni

circa i Servizi IT (ad esempio, riduzione/ottimizzazione della

qualità dei servizi, outsourcing, …)

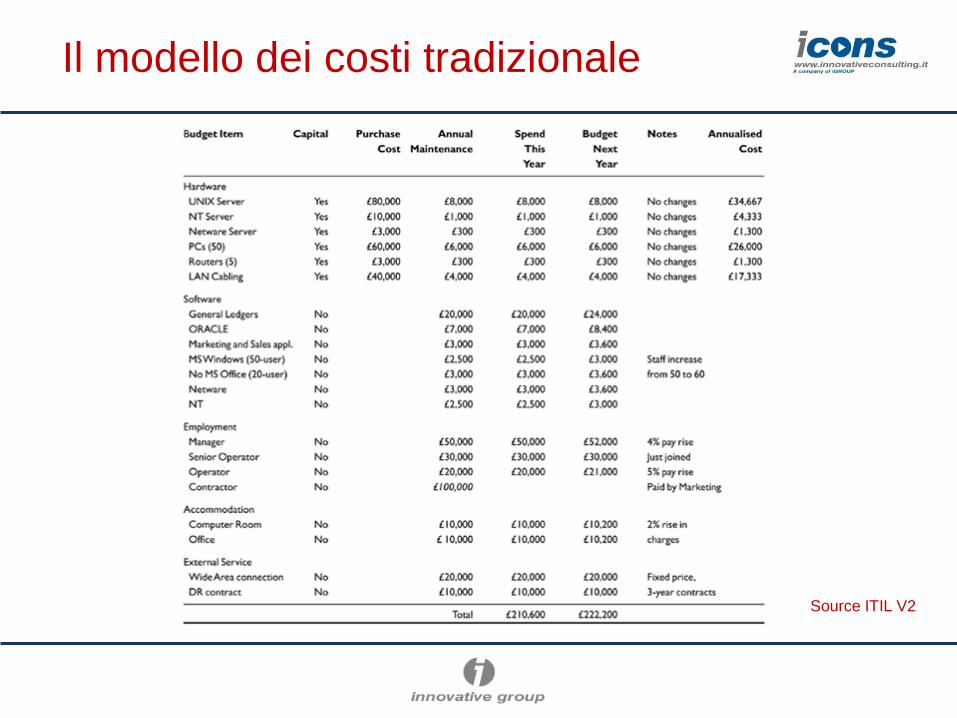

Il modello dei costi tradizionale

Source ITIL V2

La determinazione del costo per il

cliente – metodo tradizionale

Source ITIL V2

La determinazione del costo per IT

(Business) Service – metodo tradizionale

Source ITIL V2

Il Catalogo Servizi

Figure from ITIL v3, Service Design

La determinazione del costo dei servizi IT

– metodo basato sui Servizi IT

Mail Service

Server

Management

Branch Office

Connectivity

Workstation

Service

Backbone

Connectivity

HW ManagementHousing

Fleet

Management

Business Services

Technical Services

PC Applications

Management

Service Architecture

Apportioned

Costs

Direct

costs

Operating System

upgrade project

Technical Service Business ServiceProject

hardware

software

people

accommodatio

n

external

services

transfer

Figure from IT Financial Management, VHP

Principali differenze di metodo

Tradizionale Basato sui Servizi IT

Generalmente, viene calcolato il solocosto dei servizi di tipo “business”

Viene determinato il costo di tutti i servizi IT, di tipo “technical” e “business”

Inputs:• Costi diretti• Costi indiretti riallocati• Costi non assorbiti riallocati

Inputs:• Costi diretti• Costi dei servizi technical riallocati

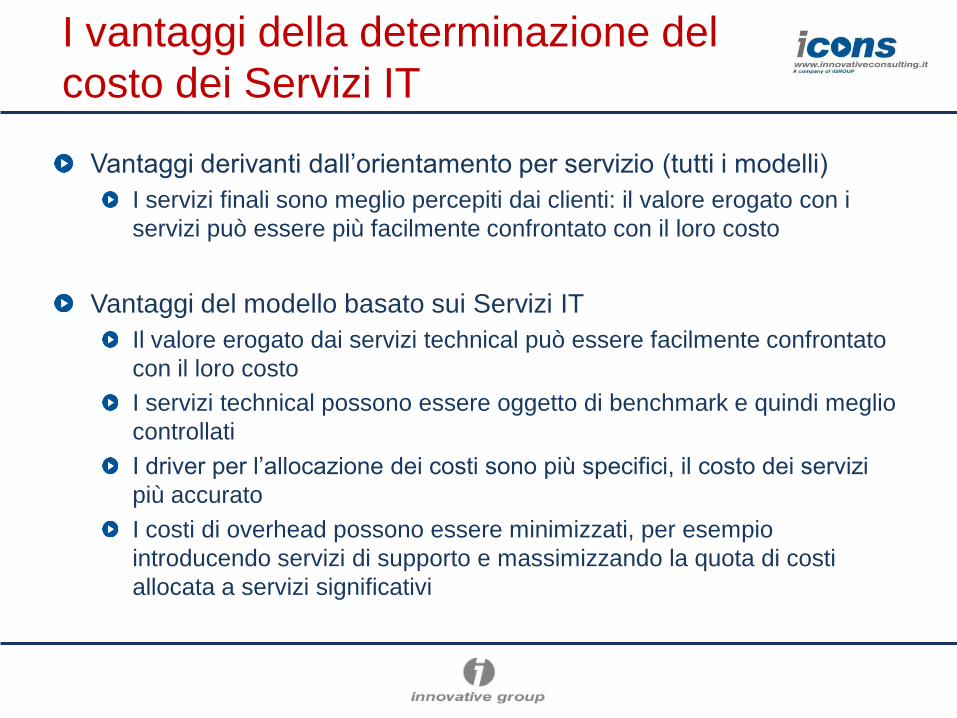

I vantaggi della determinazione del

costo dei Servizi IT

Vantaggi derivanti dall‟orientamento per servizio (tutti i modelli)

I servizi finali sono meglio percepiti dai clienti: il valore erogato con i

servizi può essere più facilmente confrontato con il loro costo

Vantaggi del modello basato sui Servizi IT

Il valore erogato dai servizi technical può essere facilmente confrontato

con il loro costo

I servizi technical possono essere oggetto di benchmark e quindi meglio

controllati

I driver per l‟allocazione dei costi sono più specifici, il costo dei servizi

più accurato

I costi di overhead possono essere minimizzati, per esempio

introducendo servizi di supporto e massimizzando la quota di costi

allocata a servizi significativi

Per avere successo …

L‟applicazione di un modello basato completamente sui Servizi IT è tanto più accurata ed affidabile se

Il catalogo dei servizi è ben disegnato

È operativo un Configuration Management Database (CMDB), in cui sono chiaramente identificati i Configuration Items (CI) appartenenti a ciascun servizio IT

I costi sono allocati ad un servizio sulla base dei CIs appartenenti al servizio

I driver per l‟allocazione dei costi ai servizi sono significativi e precisi

L‟applicazione del modello ha un impatto significativo su:

Responsabilità

Modo di operare (le persone devono sempre conoscere il servizio per cui stanno operando)

Strumenti di Service Management, incluso quello a supporto dell‟IT Financial Management (ad es. timesheet per servizio)

Partners (ad es. fatture per servizio IT)

Conclusioni

L‟IT Financial Management deve divenire una disciplina diriferimento, per la sua rilevanza ed elementi specifici che lacaratterizzano

Secondo la norma ISO/IEC20000, i Service Provider IT devonopuntare alla gestione dei costi IT per ciascun servizio erogato

A tal fine, diversi modelli possono essere utilizzati (tradizionale einnovativo, basato completamento sul concetto di Servizio IT)

Il metodo basato completamento sui servizi IT è più accurato, marichiede effort e di attuare cambiamenti

Non c‟è ampia letteratura sull‟argomento, incluso ITIL; questo gap ècolmato dalla recente pubblicazione IT Financial Management diVHP

Q&A