Is the Chinese Currency Undervalued? - ..:: Serials...

20

Is the Chinese Currency Undervalued? Imad Moosa * and Ming Ma ** Abstract: Claims of yuan undervaluation are based on ad hoc indicators (such as China’s trade surplus, reserves and foreign exchange market intervention), on the law of one price (typically represented by the Big Mac index), and on formal models that are used to calculate the equilibrium exchange rate. It is demonstrated that the ad hoc indicators cannot be used reliably to get a feel of exchange rate misalignment, that the Big Mac index no longer shows that the yuan is undervalued, and that formal models can be used to produce the results any one wants. Some empirical results are presented to show that the yuan is currently overvalued as a result of the 2005 revaluation and the gradual appreciation since then. It is concluded that accusing China of wrong-doing and the threat of a trade war cannot be based on the politically-motivated judgment that the yuan is undervalued. JEL Classification Numbers: F31, F33 Keywords: China, Exchange Rate Misalignment, US-China Trade Dispute INTRODUCTION The US trade deficit with China is typically attributed to undervaluation of the yuan (hence overvaluation of the dollar). In February 2009, the former managing director of the IMF, Dominique Strauss-Khan, made the undervaluation of the yuan an undisputable fact of life, describing it as “common knowledge”. The Economist (2009) correctly argues that “you would assume that such strong claims were backed by solid proof, but the evidence is, in fact, mixed”. In July 2011, The Economist (2011) changed its long-held view of yuan undervaluation by announcing that its modified Big Mac index shows that the yuan was not undervalued against the dollar. Those attributing the US trade deficit with China to undervaluation of the yuan use a variety of models, concepts and indicators to demonstrate that the yuan is indeed undervalued. Undervaluation is measured by deviations from the law of one price (LOP), purchasing power parity (PPP)—in its straight or augmented versions—and from various models of the equilibrium exchange rate. These studies have produced a mixed bag of estimates, from an undervaluation of 70 percent to some overvaluation. Some economists, politicians and commentators, however, argue that there is no need for a formal model to prove that the yuan is undervalued. Instead they resort to casual empiricism, suggesting that undervaluation of the yuan is indicated by China’s massive trade surplus, huge reserves and active intervention in the foreign exchange market. * RMIT, E-mail: [email protected] ** Beijing Institute of Technology IJE : Volume 9 • Number 2 • December 2015, pp. 81-99

Transcript of Is the Chinese Currency Undervalued? - ..:: Serials...

Is the Chinese Currency Undervalued?

Imad Moosa* and Ming Ma**

Abstract: Claims of yuan undervaluation are based on ad hoc indicators (such as China’strade surplus, reserves and foreign exchange market intervention), on the law of one price(typically represented by the Big Mac index), and on formal models that are used to calculatethe equilibrium exchange rate. It is demonstrated that the ad hoc indicators cannot be usedreliably to get a feel of exchange rate misalignment, that the Big Mac index no longer showsthat the yuan is undervalued, and that formal models can be used to produce the results anyone wants. Some empirical results are presented to show that the yuan is currently overvaluedas a result of the 2005 revaluation and the gradual appreciation since then. It is concludedthat accusing China of wrong-doing and the threat of a trade war cannot be based on thepolitically-motivated judgment that the yuan is undervalued.

JEL Classification Numbers: F31, F33

Keywords: China, Exchange Rate Misalignment, US-China Trade Dispute

INTRODUCTION

The US trade deficit with China is typically attributed to undervaluation of the yuan (henceovervaluation of the dollar). In February 2009, the former managing director of the IMF,Dominique Strauss-Khan, made the undervaluation of the yuan an undisputable fact of life,describing it as “common knowledge”. The Economist (2009) correctly argues that “you wouldassume that such strong claims were backed by solid proof, but the evidence is, in fact, mixed”.In July 2011, The Economist (2011) changed its long-held view of yuan undervaluation byannouncing that its modified Big Mac index shows that the yuan was not undervalued againstthe dollar.

Those attributing the US trade deficit with China to undervaluation of the yuan use avariety of models, concepts and indicators to demonstrate that the yuan is indeed undervalued.Undervaluation is measured by deviations from the law of one price (LOP), purchasing powerparity (PPP)—in its straight or augmented versions—and from various models of the equilibriumexchange rate. These studies have produced a mixed bag of estimates, from an undervaluationof 70 percent to some overvaluation. Some economists, politicians and commentators, however,argue that there is no need for a formal model to prove that the yuan is undervalued. Insteadthey resort to casual empiricism, suggesting that undervaluation of the yuan is indicated byChina’s massive trade surplus, huge reserves and active intervention in the foreign exchangemarket.

* RMIT, E-mail: [email protected]** Beijing Institute of Technology

IJE : Volume 9 • Number 2 • December 2015, pp. 81-99

82 � Imad Moosa and Ming Ma

The objective of this paper is to is to demonstrate that there is no reliable evidence on theundervaluation of the yuan, which is in the spirit of the argument put forward by Liu (2005)who argues that “since the yuan is not a freely convertible currency, there is no market basis tojudge if the yuan is undervalued or overvalued”. Still it will be argued that the yuan is morelikely to be overvalued than undervalued, given that it has been appreciating since 2005, whilethe dollar has been kept artificially weak through quantitative easing. The significance of theissue lies in the fact that those believing that the yuan is undervalued call upon the USgovernment to impose tariffs on imports from China such that the tariff rate is equal to theestimated undervaluation.

EVIDENCE BASED ON OBSERVED INDICATORS

A view that is often expressed is that there is no need for a formal model to realize that the yuanis undervalued. Williamson (2003) argues that the Chinese currency is undervalued on thebasis of more than one indicator. He claims that “one can often get a rough idea of whether anexchange rate is overvalued, in fundamental equilibrium, or undervalued by a cursoryexamination of a country’s macroeconomic situation”. Specifically he suggests that “if acountry’s economy is overheating at the same time that it has a bigger current account surplus(or a smaller current account deficit) than is needed to maintain a sustainable balance of paymentsposition for the foreseeable future, then its currency is undervalued”. This description is aperfect fit for China—hence the yuan is undervalued.

Roubini (2007) and Lardy (2005) argue that China’s surplus is indicative of exchange ratemisalignment—that is, yuan undervaluation. Lardy (2005) suggests that “by most metrics China’scurrency remains undervalued”, but he refers specifically to China’s current account surplus.Chen (2007) points out that “the hot debate” about the appropriate level of the exchange rateof the yuan and the need for having it revalued and/or for China to adopt a floating exchangerate regime are principally based on “the growing size of the Chinese current account surplusfrom the end of 90s”. Mussa (2007) is confident that the yuan is undervalued because China’scurrent account balance despite the explosive growth “establishes—beyond any reasonabledoubt—that the exchange rate of the Chinese yuan is substantially undervalued and is beingkept in this position by Chinese government policies that powerfully resist, and are intended toresist, significant appreciation of the yuan”. It is not clear at all how some circumstantialevidence, such as the occurrence of a current account surplus, establishes anything, let alonean undervalued currency, “beyond reasonable doubt”.

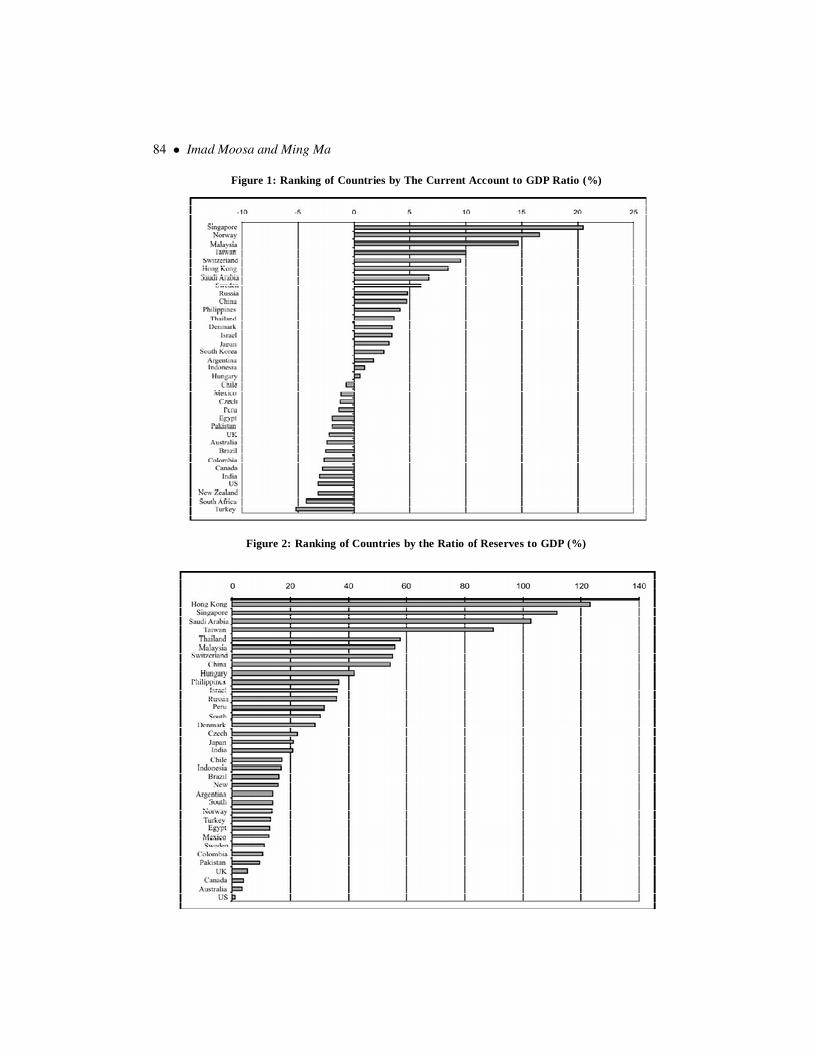

To start with, China’s current account deficit is not as big as it is portrayed to be if it ismeasured relative to GDP. Figure 1 shows the ranking of 36 countries by the currant accountas a percentage of GDP. China comes in number 10, with a current account (relative toGDP) that is less than one quarter of that of Singapore. Then there is no physical law (noteven an empirical regularity) that connects exchange rate misalignment with the externalbalance. Thin (2010) dismisses the alleged connection between the trade balance positionand exchange rate misalignment by arguing that the Indian currency is undervalued by 164percent, which means that it should command a massive surplus, but India is currently adeficit country. Apart from India, Chile, Egypt, Mexico, Pakistan, Peru, South Africa, Turkeyand the UK have deficits and undervalued (or allegedly undervalued) currencies. On the

Is the Chinese Currency Undervalued? � 83

other hand Argentina, Denmark, Israel, Norway, Sweden and Switzerland have surplusesand (allegedly) overvalued currencies.

Fatas (2010) regards as tautology the proposition that “every time we see a current accountimbalance we conclude that it is because exchange rates are not right”. The counter argumentis that a country that has a balanced budget and a surplus of domestic saving over domesticinvestment, or a country that produces more than it consumes, must have a current accountsurplus, irrespective of the exchange rate.

Consider now reserve holdings as indicator of currency undervaluation. Roubini (2007)believes that reserves are indicative of China’s exchange rate misalignment, while Chen (2007)refers to the proliferation of China’s foreign exchange reserves. Buiter and Rahbari (2011)argue that the strongest support for a long-lasting major undervaluation of the yuan is “theaccumulation of foreign exchange reserves by the Chinese authorities”. But again, China’sforeign exchange reserves are not that big relative to its GDP. Figure 2 shows that China comesin seventh place in the ranking behind Singapore, Taiwan, Thailand, Malaysia and othercountries. Yet, only China is publicly accused of accumulating reserves, which involves nowrong-doing anyway. China accumulates reserves because it has a current account surplus andbecause of the capital flows anticipating revaluation of the yuan caused by the American pressureon China to revalue its currency.

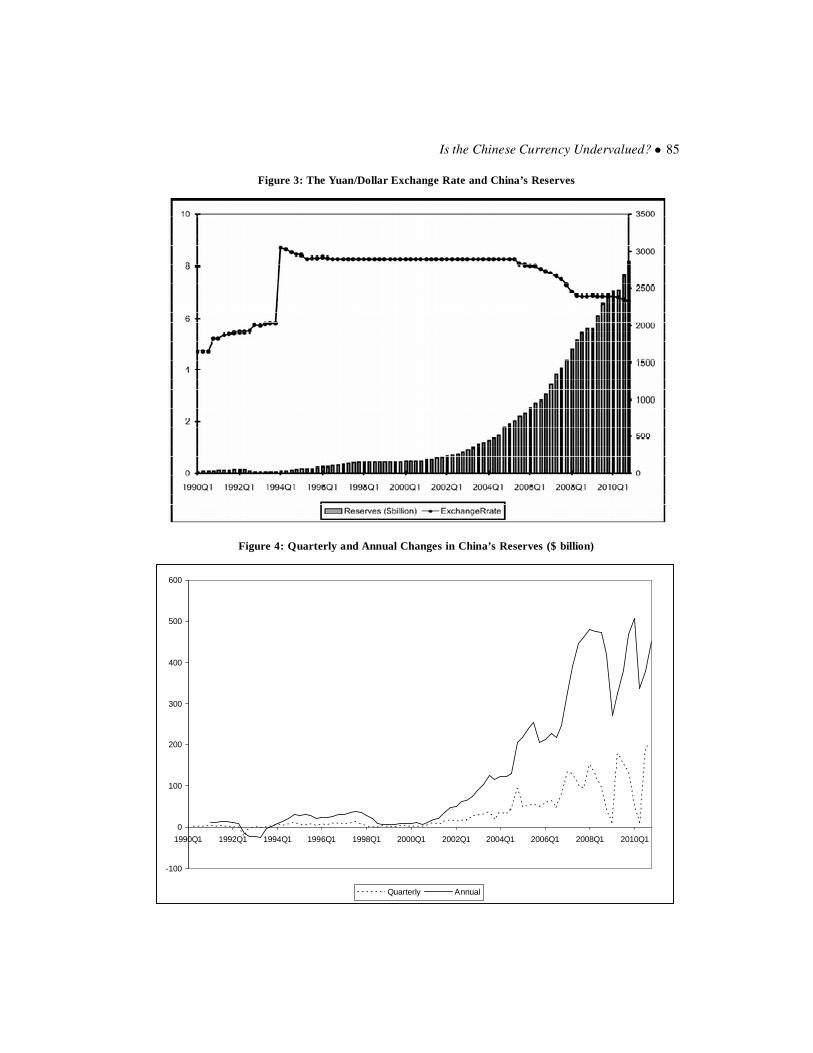

The third indicator of yuan undervaluation is intervention in the foreign exchange market.Krugman (2010) uses some flawed reasoning to indict China by arguing that “the right way tojudge is not the value of the reminbi but rather the scale of currency intervention China musteffect to keep its peg in place”. The facts and figures do not support these observations. InFigure 3 we can observe the bahaviour of the yuan/dollar exchange rate and reserves since1990.1 If international reserves arise from intervention to keep the currency undervalued, weshould see some association between reserves and the exchange rate, which is not apparent atall. China’s reserves are more related to its external surplus than to foreign exchange intervention.The dollars received by China from exports are used to buy US treasuries, which comprise thebulk of its reserves.

Bergsten (2010) points out that the Chinese authorities buy about $1 billion daily to avoidappreciation of the yuan. It is not clear where Bergsten got this exact figure, since the Chinesecentral bank does not make its intervention figures publicly available. So, the best we can do isto proxy the volume of foreign exchange intervention by period-to-period changes ininternational reserves.2 Although changes in international reserves do not constitute a goodproxy, it is compatible with the allegations that reserves reflect intervention. Figure 4 displaysquarterly and annual absolute changes in reserves (a proxy for the size of intervention). Considerwhat happened during the global financial crisis. The quarterly change in reserves declinedfrom $154 billion in the first quarter of 2008 to $7.57 billion in the first quarter of 2009, whichshould indicate declining volume of intervention. This is strange because during parts of thatperiod China abandoned temporarily the policy of gradual appreciation of the yuan, whichmeans that there should have been more rather than less intervention. Things do not add uphere.

The underlying proposition that we want to examine here is that the more a countryintervenes, the more its exchange rate is misaligned (in one direction or another). For this

84 � Imad Moosa and Ming Ma

Figure 1: Ranking of Countries by The Current Account to GDP Ratio (%)

Figure 2: Ranking of Countries by the Ratio of Reserves to GDP (%)

Is the Chinese Currency Undervalued? � 85

Figure 3: The Yuan/Dollar Exchange Rate and China’s Reserves

Figure 4: Quarterly and Annual Changes in China’s Reserves ($ billion)

-100

0

100

200

300

400

500

600

1990Q1 1992Q1 1994Q1 1996Q1 1998Q1 2000Q1 2002Q1 2004Q1 2006Q1 2008Q1 2010Q1

Quarterly Annual

86 � Imad Moosa and Ming Ma

proposition to be valid in the case of China, three conditions must be satisfied—interventionmust: (i) target the level of the exchange rate; (ii) be effective; and (iii) involve the buying ofthe dollar, targeting the bilateral exchange rate.

Starting with the first point, there are other reasons for foreign exchange market interventionapart from targeting the level of the exchange rate. These include the desire to (i) slow the rateof change of the exchange rate, (ii) dampen exchange rate volatility (in some cases to satisfyan inflation target), (iii) supply liquidity to the foreign exchange market, and (iv) influence thelevel of foreign reserves. And even if intervention targets the level of the exchange rate, thismay not be related to the desire to maintain competitiveness but rather to control inflation.Another reason for targeting the level of the exchange rate is to prevent crises. If there aresignificant currency mismatches in the economy so that foreign currency liabilities are notfully backed by foreign currency assets or earnings, domestic currency depreciation can adverselyaffect the financial position of financial institutions and firms that resort to foreign currencyfinancing.

The second point is that of the effectiveness of intervention. Anecdotal evidence showsthat intervention is ineffective unless it reinforces an already established market trend. Recallthat concerted central bank intervention failed to stem the appreciation of the dollar in thefirst half of the 1980s until the trend changed in 1985 as a result of a shift in market sentiment.As The Economist (2008) puts it, “in the correct circumstances, it [intervention] is a powerfulsignalling device for private-sector capital flows”. If the market dictates yuanappreciation, $1 billion dollar a day of intervention cannot reverse the trend. This is becausethis amount is 1/40th the daily trading of the yuan against the dollar, which according to theBank for International Settlements (2010) is ranked 17th, representing one percent of totaltrading.

The third point about targeting the dollar exchange rate is referred to in a Bank forInternational Settlements’ (2005) report. The report raises the question: how far is the bilateralexchange rate (for example, vis-à-vis the dollar) targeted rather than the effective exchangerate or the bilateral exchange rate against other currencies? The report gives reasons whyattention may have shifted to other exchange rates—one of these reasons is the creation ofthe euro, which brought forth a large single currency trading area, but it is not clear to whatextent this has been reflected in exchange rate targets or foreign reserve portfolios outsideEurope. The roles played by China and Japan in Asian trade is also important. For example,the growing production networks between China and the rest of Asia suggest that thesecountries need to pay increasing attention to their exchange rates relative to each other’scurrencies, rather than focusing exclusively on the US dollar. Also, the fact that Korea (forexample) competes directly with Japan in third markets (including the Chinese market) canreasonably motivate the assignment of a greater weight to won/yen fluctuations as opposedto won/dollar fluctuations.

It seems, therefore, that intervention may not target the level of the exchange rate, that it istypically ineffective and that it does not necessarily target the bilateral exchange rate againstthe dollar. Hence there is no support for the proposition that the yuan is undervalued becauseof China’s intervention in the foreign exchange market. Judging exchange rate misalignmentby ad hoc indicators is therefore flawed and hazardous.

Is the Chinese Currency Undervalued? � 87

EVIDENCE BASED ON THE LOP

The law of one price (LOP) is the basis of the colourful Big Mac index (BMI) used by TheEconomist magazine to estimate the extent of undervaluation or overvaluation of currencies—that is, exchange rate misalignment. The idea is very simple: the price of a commodity in twocountries must be equal when converted to the same currency. Thus, the dollar price of a BigMac in China must be equal to the dollar price of a Big Mac in the US. If this equality does nothold, the exchange rate is misaligned. This means that to restore the common currency priceequality, the exchange rate or/and prices must change via the process of commodity arbitrage.However, the law of one price is a law only when it is applied to internationally-tradedhomogenous commodities such as gold, as it explains why gold has the same dollar priceanywhere in the world. But to generalize this “law” and use it to measure exchange ratemisalignment is rather heroic, to say the least, although it is rather entertaining in the case ofthe Big Mac index.

On the basis of comparing the prices of Big Macs in China and the US, The Economist(2010) reached the conclusion that “China’s yuan [is] one of the most undervalued currenciesin the Big Mac index”. The exchange rate that is compatible with the LOP is calculated as theratio of yuan price in China to the dollar price in the US. If the actual exchange rate is higherthan the LOP-consistent rate, the yuan is considered to be undervalued. Figure 5 shows theextent of undervaluation of the yuan according to the Big Mac index during the period 1998-2010—it has varied between a maximum of 59 percent and a minimum of 48 percent.3 Whileit is logical to expect the extent of undervaluation to become smaller as the yuan appreciates,this is not to be observed since the yuan started to appreciate in July 2005.

Estimates of yuan undervaluation as judged by the Big Mac index cannot be taken seriously.A Big Mac costs less in China than in the US, which some would take to indicate an undervaluedyuan, not because of the exchange rate but because the lower price in China can be sustained,given a lower level of wages compared to the US. MacDonalds operates in China because it isprofitable to sell Big Macs at a lower price than in the US. Raising the price when demand iselastic reduces total revenue and hence profit. Thus, the difference in the dollar price of BigMac has to do more with wages (the prices of factors of production in general) than withexchange rates. Funke and Rahn (2004) point out that with seemingly infinite pools ofunderemployed workers in the countryside and in inefficient state-owned enterprises, as wellas pitifully low standard of living, China looks like it should be able to out-compete othereconomies in almost any category of manufacturing with significant labour inputs.

Notwithstanding the fact that the Big Mac index has become the best-known regular featurein The Economist, the logic behind it is twisted. It is based on the assumption that differences inthe prices of Big Macs is due only to exchange rates. Even The Economist (2009) argues againstits own Big Mac index because the index would tell us that “the currencies of virtually all low-income countries are undervalued, since prices are generally lower in these countries than in richones”. Figure 6 shows clearly positive correlation between the dollar price of Big Mac and GDPper capita.4 This empirical observation confirms the Balassa-Samuelson hypothesis, stipulatingthat average prices are higher in rich than in poor countries (Balassa, 1964).

In its issue of 30 July 2011, The Economist (2011) came up with the so-called “gormet”version of the Big Mac index, which suggests that “the yuan is not that undervalued”. The

88 � Imad Moosa and Ming Ma

Figure 5: The Extent of Undervaluation of the Yuan Measured by the Big Mac Index

Figure 6: The Dollar Price of Big Mac versus the Dollar GDP per Capita

Is the Chinese Currency Undervalued? � 89

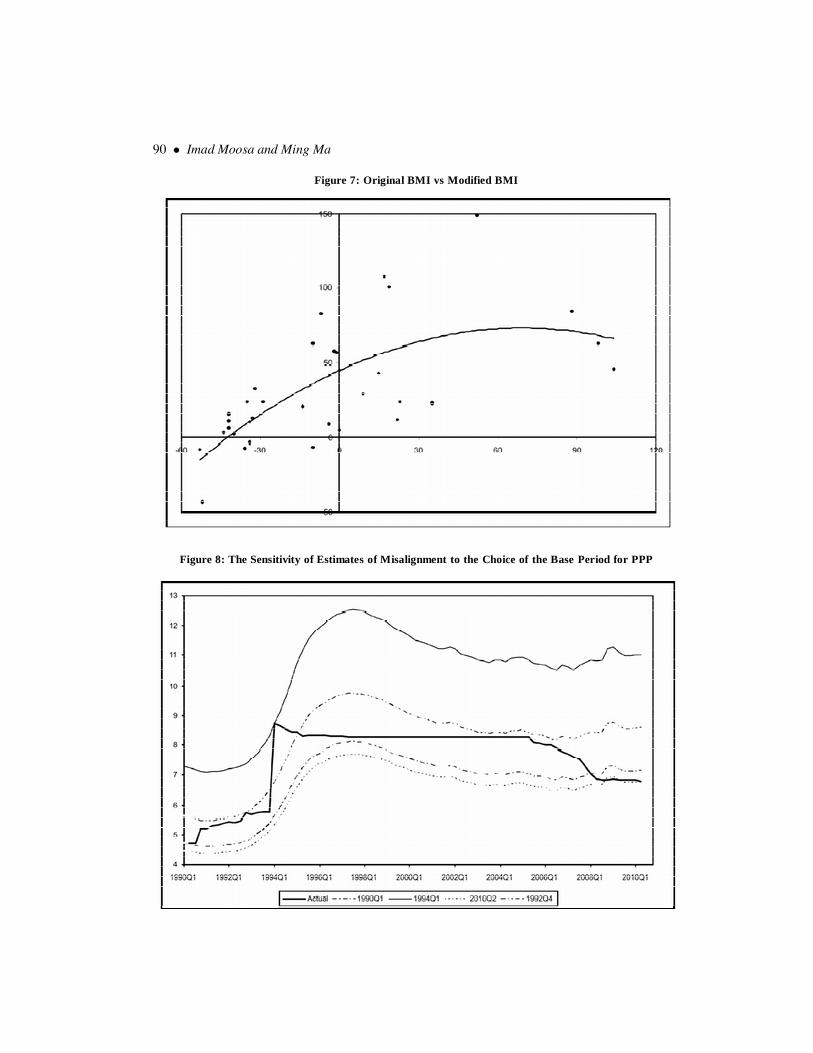

“gormet” Big Mac index is prepared by modifying the original index to take into accountdifferences in GDP per capita. Although Figure 7 shows fairly strong positive correlation betweenthe original and modified BMIs, the two indices exhibit significantly different results for theChinese currency (4 percent undervaluation versus 3 percent overvaluation). Which one arewe supposed to believe?5

Deviation from LOP can also be attributed to pricing to market. The basic idea is that theprice of an imported good in a particular country does not only depend on the exchange ratebut also on the price in the country of origin and profit margins. Export firms tend to stabilizedestination market prices in the face of nominal exchange rate changes in order to protectmarket share. Prices are typically lower in poor countries because exporters aim at maintainingtheir market shares, which can be accomplished by reducing the profit margin in terms of theexporter’s currency. Profit margins may also be reduced in response to an adverse change inthe exchange rate, in which case the exchange rate will remain looking as if it were misaligned.The inevitable conclusion is that the LOP (represented by the Big Mac index or otherwise)cannot be taken seriously, let alone declaring a trade war on the basis of its predictions.

EVIDENCE BASED ON PPP

PPP is an extension of the LOP to more than one commodity. According to PPP the equilibriumexchange rate should be at a level that equates the prices of an identical basket of commoditieswhen converted to the same currency. The “ultimate” basket of commodities comprises thegoods and services that we consume every day, a basket that has price represented by theconsumer price index.

A major problem with PPP is how to determine the starting point for calculating the PPP-consistent exchange rate. This is because the results are crucially affected by the choice of thebase period, which gives leeway to subjective judgement. Consider Figure 8, which showsquarterly observations on the yuan/dollar exchange rate over the period 1990-2010. Fourdifferent base periods are used for the purpose of calculating the PPP rate: 1990Q1 (base rate4.72), 1994Q1 (base rate 8.71), 2010Q2 (base rate 6.79) and 1992Q4 (base rate 5.75). In thefirst case, the yuan is undervalued except for the later part of the period, with an averagemisalignment of 11.23 percent. In the second case, the yuan is consistently overvalued with anaverage misalignment of 27.17 percent. In the third case, the yuan is mostly undervalued withan average misalignment of 17.17 percent. And in the fourth case, it is mixed with an averagemisalignment of 7.23 percent.

Again, what are we supposed to believe? Presumably the base period should be associatedwith some sort of equilibrium in the trade balance or current account. If this is the case then theappropriate base period should be 1990Q1, because it was around that time that the Chinesetrade balance and current account changed from negative to positive. If this is the case, thenthe yuan (according to PPP) must be overvalued.

There are other problems with PPP that cast doubt on the reliability of the estimates of theequilibrium exchange rate. Since the PPP rate is calculated by adjusting the base period exchangerate for price changes proxied by price indices, it follows that cross-country differences in theconstruction of price indices render the results unreliable. There are certainly differences betweenhow the consumer price index is calculated in the US and China because of significantly

90 � Imad Moosa and Ming Ma

Figure 7: Original BMI vs Modified BMI

Figure 8: The Sensitivity of Estimates of Misalignment to the Choice of the Base Period for PPP

Is the Chinese Currency Undervalued? � 91

Figure 9: Measures of Misalignment as Judged by Four Models

92 � Imad Moosa and Ming Ma

different spending and consumption patterns. For this reason the weights of the goods in theconsumption basket differ across countries. There are also differences in the quality of goodsincluded in the basket used to calculate the consumer price index, thus we will not be comparingapples with apples. Furthermore, PPP tells us that the exchange rate is determined by onefactor only (the inflation differential), which cannot be true. The problem is that even if weaugment the PPP model by other variables, the augmented model remains unreliable.

PPP in its various forms is supported by the available empirical evidence only over a verylong period of time (tens of years) or under hyperinflation, as was evident during the Germanhyperinflation of the 1920s. Neither of these conditions is relevant for the current debate.Some claims have been made about the failure of PPP in the recent floating period being a “USdollar phenomenon” and that the validity of PPP is affected by government intervention andannouncements concerning exchange rate policies. There is also the claim that PPP seems toperform better when wholesale prices rather than consumer prices are used. In general, however,the evidence is not robust—PPP is supported only when dodgy econometric techniques areused to test the theory. Estimates of exchange rate misalignment based on the simple andaugmented PPP will be presented later.

CONCEPTUAL PROBLEMS

Estimates of exchange rate misalignment require the estimation of an equilibrium exchangerate—similar to the LOP- and PPP-consistent exchange rates. The problem is that this is not anexact science, and there is no agreement on what the equilibrium exchange rate is. The conceptsused by economists working on exchange rate misalignment are too abstract to be useful forany practical purpose, including the declaration of a trade war.

To start with, no-one seems to know precisely what “equilibrium” means with reference tothe exchange rate (if at all). Driver and Westaway (2004) make this point clear by arguing that“when thinking about the meaning of equilibrium it quickly becomes apparent that it is adifficult concept to pin down”. The debate over what constitutes equilibrium involves issues asdiverse as its existence, uniqueness, optimality, determination, evolution over time, and indeedif it is even valid to talk about equilibrium. Hence Driver and Westaway express the view thatequilibrium “means different things to different people and this is no less true in the context ofexchange rates than it is for any other field in economics”. One idea is that since the exchangerate is determined continuously in the foreign exchange market by the supply of and demandfor currencies, the exchange rate will always be at its equilibrium value. Thus we have theconcept of the market equilibrium exchange rate, which is the one that balances the demandfor and supply of the underlying currency in the absence of official intervention. This is a nicetheoretical notion that has no place in the real world.

With respect to the equilibrium exchange rate, distinction is made among short-runequilibrium, medium-run equilibrium and long-run equilibrium (Driver and Westaway, 2004).Various equilibrium exchange rate concepts are typically specified in very general terms—noattempt has been made to specify the relevant fundamentals. Since there is more than onedefinition of equilibrium, the choice between the available approaches must be judged relativeto the question of interest. However, there are different ways to measure the equilibriumexchange rate for any given time horizon or underlying question.

Is the Chinese Currency Undervalued? � 93

Driver and Westaway (2004) make it clear that the literature on exchange rate misalignmentis vague about how the exchange rate is measured—whether it is nominal or real and whetherit is bilateral or effective. If it is the real exchange rate, a question arises as to the choice of theprice indices needed to convert the nominal exchange rate into the corresponding real rate. Forsome, the core concept is that of the nominal bilateral exchange rate, which is the rate involvedin the current debate. However, most theories of equilibrium exchange rates emphasize thereal effective exchange rate by using different definitions of the relevant price indices to convertthe nominal into a real rate.

PITFALLS IN EXCHANGE RATE ECONOMICS

Explaining the behaviour of the real effective exchange rate and measuring its “appropriate”level must be a horrendous job, given that neoclassical exchange rate economicsdoes not provide a satisfactory model to explain and predict the nominal exchange ratebetween two currencies. It has long been established that any of the neoclassicalmacroeconomic models that relate the exchange rate to economic fundamentals cannotoutperform, in terms of predictive power, the random walk model (for example, Meese andRogoff, 1983).

The reality is that exchange rates are too volatile to be explained in terms ofmacroeconomic variables (such as growth rates, inflation and the balance of payments) as inthe standard neoclassical models. Exchange rates typically exhibit movements that can bedescribed as bubbles followed by crashes. This simply means that exchange rates exhibitsustained upward movements for a long period of time in a bubble-like movement, then theycrash by losing all of the previous gains over a short (or shorter) period of time. For example,in 2008 it took the Australian dollar four months to lose what it had gained against the USdollar in the previous five years and two months. Exchange rate models also fail to explainvolatility clustering—the observation that periods of tranquility and turbulence alternate inan unpredictable manner.

The problem with neoclassical exchange rate determination models is not only that theyare not supported by the available empirical evidence, but also the very theoretical foundationsof these models. To be more specific, the problem of these models lies in the rationalrepresentative agent postulate, which has dominated neoclassical economics since the startof the so-called “rational expectations revolution”. This “revolution” has fallen out of favourbecause it could not survive its encounter with reality in financial markets. The unrealisticassumptions underlying exchange rate models include the following: (i) the representativeagent is assumed to maximize utility continuously in an intertemporal framework; (ii) theforecasts made by this agent are rational, in the sense that they are based on the collectionand processing of all available information, including information embedded in the structureof the model—hence, no systematic forecasting errors are made; and (iii) the market isefficient, in the sense that exchange rates reflect all available information about thedetermining fundamental variables. The global financial crisis has demonstrated at a greatcost that these assumptions are not valid. If a satisfactory model is unavailable to explain thenominal bilateral exchange rate, what hope have we got to explain the real effective exchangerate?

94 � Imad Moosa and Ming Ma

ESTIMATES OF EXCHANGE RATE MISALIGNMENT

The conceptual, theoretical and econometric problems associated with the “science” of exchangerate misalignment have led to a wide range of estimates for the extent of undervaluation of theyuan. The results are highly sensitive to a number of factors including the underlyingassumptions, sample period, definitions, the methods used to calculate the effective exchangerate, and so on. It is invariably the case that economists who are ideologically motivated choosethe methods, definitions and sample periods that give them results supporting their beliefs.

Cline and Williamson (2009) provide estimates of fundamental exchange rates (and henceestimates of misalignment) for a number of countries. They reach the conclusion that “the onlylarge countries that display large imbalances and therefore systemic threats are the UnitedStates and China”. Their most recent estimates still show the yuan to be undervalued (Clineand Williamson, 2011).

In a speech delivered in Beijing, John Williamson referred to estimates prepared by hiscolleagues at the Peterson Institute for International Economics (Williamson, 2003). He referredto the work of Goldstein and Lardy (2003), suggesting that that a revaluation of 15 to 25percent was needed. Goldstein (2004) found the yuan to be undervalued by about 15 to 25percent by using two methods to measure the equilibrium exchange rate of yuan: the “underlyingbalance approach” and an approach based on “adjustment of global payments imbalances”. Itis strange then that the yuan is still seen as undervalued by economists affiliated with thePeterson Institute for International Economics despite the appreciation of the currency since2005. In contrast, Wang (2004) found it difficult to arrive at any firm and robust conclusionabout the equilibrium exchange rate of the yuan, using a variety of existing techniques. Andwhile the PPP-based model of the OECD puts the undervaluation of the yuan at 70 percent,some studies find the yuan to be slightly undervalued or even overvalued (Thin, 2010). Byusing the methodology of the current account gap, Wang (2004) found either a smallundervaluation or even overvaluation.

In a study of the effect of de-pegging of the yuan on China’s international competitiveness,Sinnakkannu and Nassir (2006) argue that the yuan was slightly undervalued prior to the July2005 revaluation, which made it overvalued afterwards. Fu (2009) concludes that as a result ofthe reform of 2005, “the RMB exchange rate has almost come to its equilibrium value”. Anotherstudy found that yuan’s undervaluation to be less than 3 percent over the period 1994-2006(Zhang, 2008). Funke and Rahn (2004) conclude that “while the renminbi is somewhatundervalued against the dollar, the misalignment is not nearly as exaggerated as many popularclaims”.

Cheung et al. (2008) found that the estimated misalignment of the yuan detected in theirprevious study (Chinn et al., 2006) disappeared completely when they examined a new dataset. They argue that “this finding highlights the fact that statistical uncertainty is somethingthat needs to be taken seriously in policy debates”. After conducting various robustness checks,they conclude that “although the point estimates indicate the RMB is undervalued in almost allsamples, in almost no case is the deviation statistically significant”. These findings highlightthe significant degree of uncertainty surrounding empirical estimates of “equilibrium realexchange rates”, thereby underscoring the difficulty of accurately assessing the degree of yuanundervaluation.

Is the Chinese Currency Undervalued? � 95

Dunaway et al. (2006) demonstrate that “equilibrium real exchange rate estimates obtainedfrom the various approaches and models commonly used in the literature exhibit substantialvariations in response to small perturbations in model specifications, explanatory variabledefinitions, and time periods”. They make it clear that “because of the methodological andempirical difficulties involved in establishing the equilibrium exchange rate for a currencyand/or estimating the deviation of the actual real exchange rate from its equilibrium level, it isnot surprising that researchers have come up with a wide range of estimates”. Furthermore,they point out that “this has been particularly so in the case of attempts to estimate the equilibriumexchange rate for China’s currency”. By using a simple model explaining the real effectiveexchange rate of the yuan in terms of productivity and net foreign assets, they found that thatthe estimate of undervaluation could be reduced by up to 37.9 percentage points just byintroducing simple changes, such as replacing the ratio of net foreign assets to GDP with theratio of net foreign assets to exports. When another model was estimated for a sample of 11countries they found that “randomly dropping one country from the 11-country panel changesthe estimates of the deviation of the actual real exchange rate from its predicted equilibriumlevel by 6-43 percentage points relative to the baseline estimates”.

Chen (2007) estimated the equilibrium real effective exchange rate of the yuan against thecurrencies of China’s 13 biggest trading partners over the period 1994-2006. His findingsshow that equilibrium exchange rate exhibited a steady rise during the period 1994-1999,followed by a steady fall afterwards. While the results show that the yuan was undervaluedduring most of the sample period, this misalignment has a trend to become smaller and smaller.He concluded that in the after-reform period, a small degree of overvaluation replaced thisundervaluation.

Cheung et al. (2008) argue that “while the empirical results thus far point to the difficultyin establishing the claim that RMB is significantly undervalued, it is imperative to recognizethat these results do not constitute evidence of no undervaluation”. They further argue that“the statistical evidence is so weak that we cannot reject a wide range of hypotheses”, whichmeans that “the empirical relationship is very imprecisely estimated” and that “the empiricalmodels and data are not sharp enough to allow a definite statistical conclusion”. They alsoargue that “the drastic changes in the estimated degrees of misalignment highlight the uncertaintythat is attendant the data we use in these sorts of analyses”.

Even those who accuse China of wrong-doing admit that no-one knows the extent ofmisalignment of the yuan. Williamson (2003) admits that “none of us has a satisfactorymacroeconometric model at our disposal to back up our estimates or guesses”. Krugman (2010)agrees with the proposition that no one knows the fair value of the yuan. Evidence on themisalignment of the yuan/dollar exchange rate is a mixed bag and highly unreliable. The problemis that the diversity of the results is highly conducive to “cherry picking” by those who want toconfirm a preconceived belief.

SOME EMPIRICAL RESULTS

In this section we present some estimates of exchange rate misalignment using quarterly datacovering the period up to the end of 2010. Four models are used for the purpose of calculatingthe equilibrium exchange rate—these models are encompassed in the general specification

96 � Imad Moosa and Ming Ma

* * * *0 1 2 3 4( ) ( ) ( ) ( )� � � � � � � � � � � � � � � �t t t t t t t t t ts m m y y i i p p (1)

where s is the log of the exchange rate, m is the log of the money supply, y is the log of output(proxied by industrial production), i is the interest rate, and p is the general price level (proxiedby consumer prices). Since the exchange rate is expressed as yuan per dollar, an asterisk indicatesthe corresponding Chinese variable. The specifications of four models are derived by imposingcertain coefficient restrictions on equation (1): PPP (�

1 = �

2 = �

3 = 0), augmented PPP (�

1 = �

2

= 0), the flexible-price monetary model (�4 = 0) and the flow model (�

1 = 0).

The log of the equilibrium exchange rate is calculated as* * * *

0 1 2 3 4ˆ ˆ ˆ ˆ ˆ( ) ( ) ( ) ( )� � � � � � � � � � � � � � � �t t t t t t t t t ts m m y y i i p p (2)

where �̂i is the estimated value of �

i. Hence the equilibrium exchange rate is calculated as

)exp( tt sS � (3)

The four models are estimated using quarterly data covering the period 1998:4-2010:4.Once the models have been estimated, the equilibrium exchange rate is derived from the modelsby using equations (2) and (3).

Figure 9 shows the actual and equilibrium exchange rates derived from the four models.Since the exchange rate is expressed as yuan/dollar, the yuan is undervalued if the actualexchange rate is higher than the equilibrium rate, and vice versa. The simplest of these models,PPP, shows that the yuan was undervalued up to the first quarter of 2007 at an average rate of5.2 percent, but at the end of 2010 it was overvalued by 16 percent. When the PPP model isadjusted by taking into account the interest rate differential, the results show that the yuan wasovervalued for a short period before July 2005 but at the end of 2010, the yuan was overvaluedby 8.2 percent. The monetary model and flow model produce more or less similar results,showing that the yuan was generally undervalued before July 2005 then it became overvaluedfollowing the policy change introduced by the Chinese at that time. At the end of 2010, the twomodels show that the yuan was overvalued by about 9 percent.

There is no way to say which of these estimates is more reasonable than the other. However,the results show that the yuan is not undervalued by a significant amount, even before July2005. What we can say, is that it has become implausible to claim that the yuan is stillundervalued despite the more than 20 percent nominal appreciation since July 2005 and despitethe fact that the dollar has been kept weak by quantitative easing.

CONCLUSION

The conclusion that can be derived from a review of the studies of exchange rate misalignmentas applied to the Chinese yuan is the following. While there are those peddling the idea that theyuan is significantly undervalued, there are those who disagree. The latter believe that theyuan may be (have been) undervalued but not by as much as it is typically portrayed to be, and/or the revaluation of the yuan in July 2005 and subsequent appreciation would have eliminatedany undervaluation. The empirical results presented in this paper support the view of thosewho disagree with the proposition that the yuan is grossly undervalued. The fact remains,

Is the Chinese Currency Undervalued? � 97

however, that exchange rate determination models cannot be relied on with a great degree ofconfidence to measure exchange rate misalignment.

The yuan cannot be judged to be undervalued by using ad hoc indicators such as the tradebalance, reserves or the size of foreign exchange market. The Big Mac index, which has beenused consistently to blame China for the US trade deficit no longer shows that the yuan isundervalued. Indeed common sense would tell us that there are more reasons to believe thatthe yuan is overvalued than undervalued. What is more important, however, is that accusingChina of wrong-doing and the threat of a trade war cannot be based on a politically-motivatedjudgment that the yuan is undervalued.

Notes

1. Reserves are defined as in the IMF’s International Financial Statistics—international reserves minusgold.

2. Neely (2000) identifies a problem with the effectiveness of intervention, which is the use of changesin international reserves as a proxy for the size of intervention. He concludes that “it is difficult tosay whether changes in reserves are an adequate proxy for intervention”. Goldstein and Lardy (2008)share this position in such a way as to condemn China by arguing that “increases in holdings offoreign exchange reserves are downward-biased estimates of official intervention in the foreignexchange market”, meaning that the scale of Chinese intervention is bigger than what it appears tobe. In the absence of exact figures this is a reasonable approximation.

3. It is measured by the gap between the actual rate and the equilibrium rate (as a percentage of theactual rate).

4. Figure 6 is based on data for the same countries appearing in Figure 1 and Figure 2. These are thecountries for which The Economist reported the price of Big Mac in July 2011.

5. Moosa (2011) suggests another index based on the cover price of The Economist. This index producesmarkedly different results from those obtained from the original Big Mac index.

References

Balassa B. (1964), The Purchasing Power Parity Doctrine: A Reappraisal, Journal of Political Economy,72, 584-96.

Bank for International Settlements (2005), Foreign Exchange Market Intervention in Emerging Markets:Motives, Techniques and Implications, BIS Papers, No 24, May.

Bank for International Settlements (2010), Triennial Central Bank Survey of Foreign Exchange andDerivatives Market Activity in 2010 - Final Results. http://www.bis.org/publ/rpfxf10t.htm.

Bergsten, C.F. (2010), Correcting the Chinese Exchange Rate: An Action Plan, Testimony before theCommittee on Ways and Means, US House of Representatives, 24 March. Available at http://www.piie.com/ publications/testimony/testimony.cfm? ResearchID =1523.

Buiter, W. and Rahbari, E. (2011), The ‘Strong Dollar’ Policy of the US: Alice-in-Wonderland Semanticsvs. Economic Reality, Global Economic Views, Citibank, 26 May.

Chen, J. (2007), Behavioral Equilibrium Exchange Rate and Misalignment of Renminbi: A RecentEmpirical Study. Paper presented at the 6th International Conference on the Chinese Economy, 18-19 October, Paris.

98 � Imad Moosa and Ming Ma

Chinn, M.D., Cheung, Y.W., and Fujii, E. (2006), Why the Renminbi Might be Overvalued (But ProbablyIsn’t), University of Wisconsin, Madison, September. Available from http://www.ssc.wisc.edu/~mchinn/RMB_paper. pdf.

Cheung, Y-W., Chinn, M.D. and Fujii, E. (2008), Pitfalls in Measuring Exchange Rate Misalignment:The Yuan and Other Currencies, NBER Working Papers, No 14168.

Cline, W.R. and Williamson, J. (2009), Estimates of Fundamental Equilibrium Exchange Rates, PetersenInstitute for International Economics.

Cline, W.R. and Williamson, J. (2011), Estimates of Fundamental Equilibrium Exchange Rates, Policybrief PB11-5, Petersen Institute for International Economics.

Driver R.L. and Westaway, P.F. (2004), Concepts of Equilibrium Exchange Rates, Bank of EnglandWorking Papers, No 248.

Dunaway, S., Leigh, L. and Li, X. (2006), How Robust are Estimates of Equilibrium Real ExchangeRates? The Case of China, IMF Working Papers, No 06/220, 2006.

Fatas, A. (2010), Current Account Imbalances and Exchange Rates, 7 April. http://fatasmihov.blogspot.com/2010/04/current-account-imbalances-and-exchange.html

Fu, Z-Y. (2009), Achievement, Problems and Countermeasures of RMB Exchange Rate System Reformsince 2005. http://en.cnki.com.cn/Article_en/CJFDTotal-GXSY200903018.htm.

Funke. M. and Rahn. J. (2004), Just How Undervalued is the Chinese Renminbi?’Working Paper, Bankof Finland. Available at http://www.bof.fi/NR/rdonlyres/F3372088-5FE8-4995-A1C7-4D8BCBF18A88/0/dp1404.pdf.

Goldstein, M. (2004), Adjusting China’s Exchange Rate Policies, Working Paper 04-1, Petersen Institutefor International Economics, Washington DC.

Goldstein, M. and Lardy, N. (2003), Two-Stage Currency Reform for China, Asian Wall Street Journal,12 September.

Goldstein, M. and Lardy, N. (2008), China’s Exchange Rate Policy: An Overview of Some Key Issues,in Goldstein, M. and Lardy, N. (eds) Debating China’s Exchange Rate Policy, Washington: PetersonInstitute for International Economics.

Krugman, P. (2010), China is “Really the Bad Guy” in Currency War, 14 October. Available at http://www.creditwritedowns.com/2010/10/krugman-china-is-really-the-bad-guy-in-currency-war.html.

Liu, H.C.K. (2005), The Coming Trade War and Global Depression, Asia Times on Line, 18 June.

Lardy, N. (2005), Exchange Rate and Monetary Policy in China, Cato Journal, 25, 41-47.

Meese, R.A. and Rogoff, K. (1983), Empirical Exchange Rate Models of the Seventies: Do They Fit Outof Sample?, Journal of International Economics, 14, 3-24.

Moosa, I.A. (2011), The US-China Trade Dispute: Facts, Figures and Myths, Cheltenham (UK): EdwardElgar (forthcoming).

Mussa, M. (2007), IMF Surveillance over China’s Exchange Rate Policy, The Peterson Institute forInternational Economics, 2007. Available at http://www.iie.com/ publications/papers/mussa1007.pdf.

Neely, C.J. (2000), Are Changes in Foreign Exchange Reserves Well Correlated with Official Intervention?Federal Reserve Bank of St Louis Economic Review, September/October, 17-31.

Roubini, N. (2007), Why China Should Abandon its Dollar Peg?, International Finance, 10, 71-89.

Is the Chinese Currency Undervalued? � 99

Sinnakkannu, J. and Nassir, A. (2006), A Study on the Effect of De-Pegging of the Renminbi Against theUS Dollar on the China’s International Trade Competitiveness, International Research Journal ofFinance and Economics, 5, 64-77.

The Economist (2008), Divine Intervention, 27 March.

The Economist (2009), Burger-thy-Neighbour Policies, 5 February.

The Economist (2010), An Indigestible Problem: Why China Needs More Expensive Burgers, 14 October.

The Economist (2011), Beefed-up Burgernomics, 30 July.

Thin, W. (2010), More on Geithner’s Currency Classifications, 21 October. Available at http://www.creditwritedowns.com/2010/10/more-on-geithners-currency- classifications.html.

Wang, T. (2004), ‘Exchange Rate Dynamics’, China’s Growth and Integration into the World Economy:Prospects and Challenges, IMF Occasional Papers, No. 232.

Williamson, J. (2003), The Renminbi Exchange Rate and the Global Monetary System, Lecture deliveredat the Central University of Finance and Economics, Beijing, 29 October.

Zhang, Z-B. (2008), The Empirical Analysis of the Appropriate Level of Renminbi (RMB) ExchangeRate. Available at http://en.cnki.com.cn/Article_en/ CJFDTOTAL-BUSI200801046.htm.