Investor Presentationiclgroupv2.s3.amazonaws.com/corporate/wp-content/uploads...Investor...

69

Investor Presentation November 2015

Transcript of Investor Presentationiclgroupv2.s3.amazonaws.com/corporate/wp-content/uploads...Investor...

Investor Presentation

November 2015

Safe Harbor

All statements in this communication, other than those relating to historical facts, are “forward-looking statements” within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended These forward-looking statements and projections are not guarantees of future performance and are subject to a number of assumptions, risks, projections and uncertainties, many of which are beyond our control, which could cause actual results to differ materially from such statements or projections. Important factors that could cause actual results to differ materially from our expectations include, among others: loss or impairment of business licenses or mining permits or concessions; natural disasters; failure to raise the water level in evaporation Pond 5 in the Dead Sea; accidents or disruptions at our seaport shipping facilities or regulatory restrictions affecting our ability to export our products overseas; labor disputes, slowdowns and strikes involving our employees; currency rate fluctuations; rising interest rates; general market, political or economic conditions in the countries in which we operate; pension and health insurance liabilities; price increases or shortages with respect to our principal raw materials; volatility of supply and demand and the impact of competition; changes to laws or regulations (including environmental protection and safety and tax laws or regulations), or the application or interpretation of such laws or regulations; government examinations or investigations; the difference between actual reserves and our reserve estimates; failure to integrate or realize expected benefits from acquisitions and joint ventures; volatility or crises in the financial markets; cyclicality of our businesses; changes in demand for our fertilizer products due to a decline in agricultural product prices, lack of available credit, weather conditions, government policies or other factors beyond our control; decreases in demand for bromine-based products and other industrial products; litigation, arbitration and regulatory proceedings; and war or acts of terror. More detailed information about factors that may affect our performance may be found in “Risk Factors” in our Annual Report Form 20-F filed with the U.S. Securities and Exchange Commission on March 20, 2015. Forward-looking statements and projections represent our views and are given only as of the date of this communication and we disclaim any obligation to update or revise them, whether as a result of new information, future events or otherwise, except as required by law.

All information included in this document speaks only as of the date on which they are made, and we do not undertake any obligation to update such information afterwards. Some of the market and industry information is based on independent industry publications or other publicly available information, while other information is based on internal studies. Although we believe that these independent sources and our internal data are reliable as of their respective dates, the information contained in them has not been independently verified and we can not assure you as to the accuracy or completeness of this information.

2

Index

3

INDEX

Main Deck 1-28

Company Vision, Business Model 4-5

Business Strategy 6-17

Appendices 19-71

About ICL 19-25

Agriculture 27-47

Engineered Materials 48-59

Food 60-63

Efficiency and Operational Excellence 64-68

Our Vision: Fulfilling Humanity’s Essential Needs

4

Rise of the middle class and standard of living across the globe

Increased demand for and use of natural resources

Environmental stewardship and sustainability

We fulfill essential needs in 3 core end markets – Agriculture, Food and

Engineered Materials by utilizing an integrated value chain based on

specialty minerals

Integrated Value Chains Provide Significant Synergies

5 5

Phosphate Fertilizers

Fertilizer Grade

Phosphoric Acid

Food Grade

Phosphoric Acid

Salt (NaCl)

Phosphate Salts

Pure Magnesium

Magnesium Alloys

Compound Fertilizers

Salt (NaCl)

Potash

Specialty Fertilizers

Chlorine based Biocides

Bromine Compounds

Magnesium

Chloride

Solution

Magnesium

Chloride

Raw Materials

Potash

Sylvanite

Crude

Magnesium

Fertilizers Industrial Products Performance Products DSM Product Sold

End Brine

Elemental

Bromine

Phosphate

Rock

Chlorine

Elemental

Phosphorus

Special

Grade Acid

OPFRs & Others

Magnesia

Products (MgO)

Source Major Intermediate & Finished Products

Wildfire Extinguishers

Food Additives

Phosphorus ( Penta)

Sulfide

Polysulphate

Carnallite

PCL3 POCL3

Business Strategy

Efficiency Initiatives Contribution – Segment Breakdown

7

USD millions/year

2016 efficiency gains run-rate of $350M Segment run-rate contribution

2016E2015E2014A

ICL PP

ICL IP

Phosphatesand fertilizers

Potash

$240 million

$120 million

$350 million

Procurement

HR Commercial excellence

Production cost

efficiency

Operational Excellence Goals at Our Production Sites

8

ICL Industrial Products, ICL Performance Products

ICL Dead Sea

Potash Engineered Materials, Food

Additional production of 400kt annually beyond the 3 years compensation for the strike losses

Potash cost per tonne reduction of ~ $10 by 2016

EBITDA contribution of ~$50 million by 2016

Successful cost reduction plan implementation –labor down by 10%, P2O5 production up by 15% in 1H2015 vs. 2014

Increase Fertilizers production by ~10%

EBITDA contribution of ~ $80 million by 2016

ICL Rotem

Phosphate

Operational Excellence initiatives implementation started in 2015

Labor costs reduction at ICL Neot Hovav and the elemental bromine plant at the Dead Sea

ICL Iberia

Potash

Reduce our fixed costs per tonne by around €40/t by 2020

EBITDA contribution of ~$20 million by 2016 and ~$50 million by 2020

Operational Efficiency Achievements in Israel

9

Over 250 (over 10%) employees have already left both sites Headcount

Reduction Approx. 50 employees will leave the company by 2018.

ICL Dead Sea, ICL Neot Hovav

ICL Neot Hovav

Additional potash production - ~400kt per year ICL Dead Sea Production

Benefits – anticipated continuous operational improvements

Total benefits (NPV) ~$260 million

Anticipated labor costs savings in 2015 ~$25 million

Gross average yearly labor costs savings as of 2017 ~$80 million

Anticipated labor costs savings in 2016 ~$70 million

Major achievements

NPV of economic benefit: at least $170 million

PolysulphateTM: The Future of ICL-UK

10

Moving from high-cost potash to low-cost PolysulphateTM operations

0

200

400

600

800

1,000

1,200

2014 2020

PolysulphateTM production plan K Tonnes

“Economic” potash reserves at ICL-UK are running out

ICL plans to transition to a pure Polysulphate operation by year-end 2018

Expected production of 1 million tonnes by 2020. Further increase afterwards

Low CAPEX (~£40 million) using existing infrastructure

Additional ~£40 million for granulation facility under consideration

Transition will result in lower costs and higher operating margins for ICL-UK

Three-year accelerated depreciation of potash facilities

Improving cash contribution at ICL UK

Operating income expected to double by 2020 vs. 2015

Operating margins expected to increase to over 30% by 2020

Immediate restructuring expected to contribute $30 million annually, starting from 2H2016

11

Polysulphate™: Solid Market Potential

Readily available new natural fertilizer in the market containing four nutrients: Sulphur, Potassium, Magnesium and Calcium – a substitute for some fertilizers

~50%

~14% K

S

~36% Mg+Ca

Over 200 million tonnes resources in the ICL UK potash mine

Low production cost allows attractive economics for farmers

Environmentally friendly, no chemical processing or waste products, suitable for chloride sensitive crops and for organic agriculture

Proven market acceptance: 50 k tonnes sold in 2014. 2015 target: 120 k tonnes

Polysulphate addresses new market niches and replaces more costly existing products

2020 production and sales target – 1 million tonnes. Long term potential up to 3 million tonnes

ICL's Potash Sub-Segment Production Moderately Increasing while Adding Specialty Products

12

Potential gradual increase of production capability excluding ICL UK

5.15 5.9 7.3

0.12 1

2

0.5

0

2

4

6

8

10

12

14

2014A 2020E 2025E

Million tonnes Potash Polysulphate SOP

Incremental potash production – short term & brownfield potash

Project Production (Mt)

Comments

ICL Iberia 0.3 1st stage brownfield expansion

ICL Dead Sea 0.4

ICL UK (0.7) Beginning 2019

Polysulphate TM 1.0 By 2020

Incremental potash production – long term

Project Production (Mt)

Comments

ICL Iberia 1.0 2nd stage brownfield expansion

ICL Ethiopia - potash 1.0-1.5 Subject to detailed engineering planning and board approval ICL Ethiopia - SOP 0.5

Source: Industry publications, ICL estimates

~

Sales growth will be supported by development of new markets in India and East Africa

ICL to Become a Leading Player in China’s Phosphate Sector

13

JV includes upstream mining, bulk fertilizers and downstream specialty businesses

R&D platform: 11 projects in Food, Engineered Materials, Agro and process improvement. Additional projects by year-end

A key milestone in our strategy:

I. increasing phosphate platform by more than 50%, securing long-term reserves

II. expanding phosphate end-to-end business model with a focus on Asia

III. transforming into the world’s leading specialty phosphate player

IV. improving cost competitiveness of our phosphate network

The JV in Numbers

~$180M in the JV Investment

~RMB2,900 (~$450M) in year 1 to ~RMB3,900 (~$600M) in year 5

Revenues

Break even to low single digits in year 1 to low teens in year 5

Operating Income Margins

About $340 million spread over 5 years Additional CAPEX

Change Total ICL* JV Production capability

63% 6.5mt 2.5mt Phosphate Rock

45% 2.7mt 850kt Commodity Fertilizers

15% 895kt 115kt Specialty Fertilizers

117% 1.3mt 700kt Phosphoric Acid

26% 290kt 60kt Purified Phosphoric Acid

64% 410kt 160kt - Incl. Expansion Plans

Formation of phosphate JV with Yunnan Yuntianhua completed:

* Including 100% of the JV’s production capability

14

Danakhil Potash Project - Ethiopia

• Our gate to Africa Ethiopia

Products produced

Potential production capacity

Total CAPEX

Setup phases

Partnership – ICL’s share

Annual CAPEX – ICL’s share

SOP

0.5MT

~ $1.3 – 1.5bn

Phase I (2020) $700-800M

40-60%

~ $100 – 150 million

MOP

1.5MT

Phase II (2025) $600-700M

Project’s estimations demonstrate its attractiveness

Attractive Fast Growing Downstream Business

15

Reduce cost of production

Enlarge Product Portfolio

Establish production in attractive markets

Grow with R&D and new Strategic Partners

Specialty Fertilizers

Strategic Initiatives

Growing core business through R&D

Mid term – potential 2020 sales contribution of ~$150M

Long term – significant potential 2020 sales and profit contribution

Margin expansion, pricing, focus on customer unmet needs

Advocacy: SAFR™ (Scientific Assessment for Flame Retardants), Merquel® in China/EU

Industrial Products

Strategic Initiatives

Advanced Additives: Geographic expansion Product differentiation Lean and reliable Food Specialties: New products, functional blends,

protein modifiers Geographical expansion New ingredients, technologies

through R&D

Performance Products

Strategic Initiatives

Estimated CAGR

Estimated CAGR

Estimated CAGR (organic growth) 2015-2019: 3-5%

Estimated CAGR (organic growth) 2015-2019: 4-6%

Estimated CAGR

Estimated CAGR (organic growth) 2015-2019: 2-4%

CAPEX

Estimated CAPEX 2015-2019: $20-40 million p.a. (excluding new NOP plant)

CAPEX

Estimated CAPEX 2015-2019: $60-75 million annually

CAPEX

Estimated CAPEX 2015-2019: $70-90 million annually

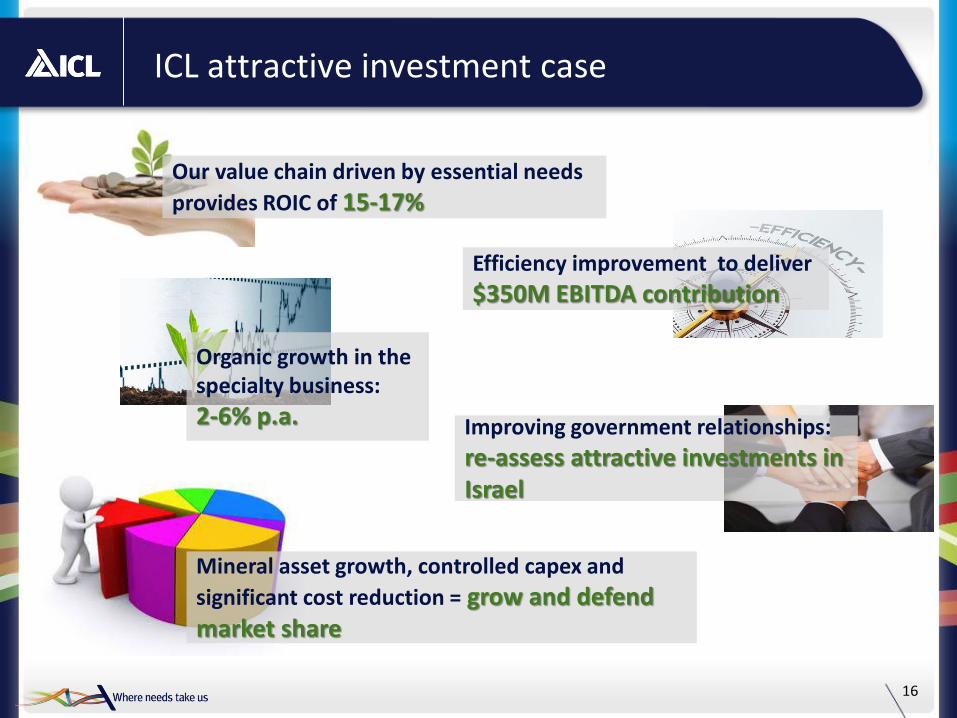

ICL attractive investment case

16

Our value chain driven by essential needs

provides ROIC of 15-17%

Efficiency improvement to deliver

$350M EBITDA contribution

Organic growth in the specialty business:

2-6% p.a. Improving government relationships:

re-assess attractive investments in Israel

Mineral asset growth, controlled capex and

significant cost reduction = grow and defend market share

Thank you

Appendices

About ICL

ICL at a Glance

20

ICL is a leading global specialty minerals company that operates a

unique integrated business model to fulfil essential needs in three

key end markets: Agriculture, Engineered Materials and Processed

Food

Utilizes sophisticated processing and product formulation

technologies to produce downstream / value-added products

Operates low-cost, geographically advantaged assets

~50% of production and ~95% of sales (2014) outside of Israel

FY2014 dividend yield: 8.3% (including special dividend) (2)(3)

Company Snapshot

Key Statistics (3) Our Business Segments

US$Bn

Market Capitalization 6.8

Net Debt 2.7

Enterprise Value 9.5

Main Shareholders Israel Corp 46.2%

PCS 13.9%

Q3 2015 Q3 2014

Revenue 1.4 1.6

Adj. EBITDA 0.34 0.35

% Margin 25% 23%

Fertilizers: One of the world's largest producers of potash, phosphate-based fertilizers and specialty fertilizers

Performance Products: Produces, markets and sells a broad range of downstream phosphate-based food additives and advanced additives

Industrial Products: Extracts bromine and magnesium from the Dead Sea and produces and markets bromine, magnesium and phosphorus compounds

19%

18%

15%

48%

Our Business Mix and End Markets (1)

Potash

Fertilizers & Phosphates

Industrial Products

Performance Products 52%

9%

8%

31%

Processed Food

Engineered Materials

Agriculture (Bulk and Specialty Fertilizers)

Fertilizers Segment

Business Mix (Based on 2014 EBITDA)

End Markets (Based on 2014 Revenue)

Other

1 Excludes adjusted EBITDA attributable to Other and eliminations; may not sum to 100% due to rounding 2 Dividend yield calculated as total dividends paid in 2014 divided by current market capitalization 3 Market data as of November 07, 2015; Net debt calculated as total debt less cash, cash equivalents and short term investments

Unique Business Model - Using Resources and Reaching Customers Globally

21

Unique Portfolio of Mineral Assets

Integrated Value Chain

Potash, Phosphates Bromine Magnesium

Potash Potash Phosphate

Mining Chemistry Formulation

Leading Positions in Concentrated Global Markets with Strong Fundamentals

Leading Positions

Israel China

Spain

UK

Ethiopia

Potash Polysulphate

US

Phosphate

From Needs to Products

22

End Markets

Flame Retardants

Industrial Solutions

Advanced Additives

Engineered Materials

~$470M ~$780M ~$650M

Food Specialties

Food

~$530M

Segments

Business lines

Contribution to sales*

Potash Fertilizers

Phosphates Fertilizers

Specialty Fertilizers

Agriculture

~$1,820M ~$910M ~$770M

* In 2014, including inter-segment sales

Unique Portfolio of Mineral Assets – Existing Assets

23

Logistical advantage - close to port of Barcelona

Vast reserves

Cost reduction initiatives

Significant expansion plans

Logistical advantage - close to Teesside port

Polysulphate – increase production to 1 million tonnes by 2020

Low CAPEX using existing infrastructure

Lower polysulphate production costs to double operating income with margins over 30% by 2020

ICL UK ICL Iberia

Dead Sea

Potash, Bromine Magnesium

Potash Potash PolysulphateTM

Low cost in potash, the world’s lowest in bromine

Near-infinite reserve life – potash and bromine

Logistical advantages – stockpiling ability, geographical position

Ongoing operational efficiency measures, including labor reduction

Integrated value chain highly biased towards value added specialty products

Successful efficiency and operational excellence plan at Rotem

Negev Desert

Phosphate

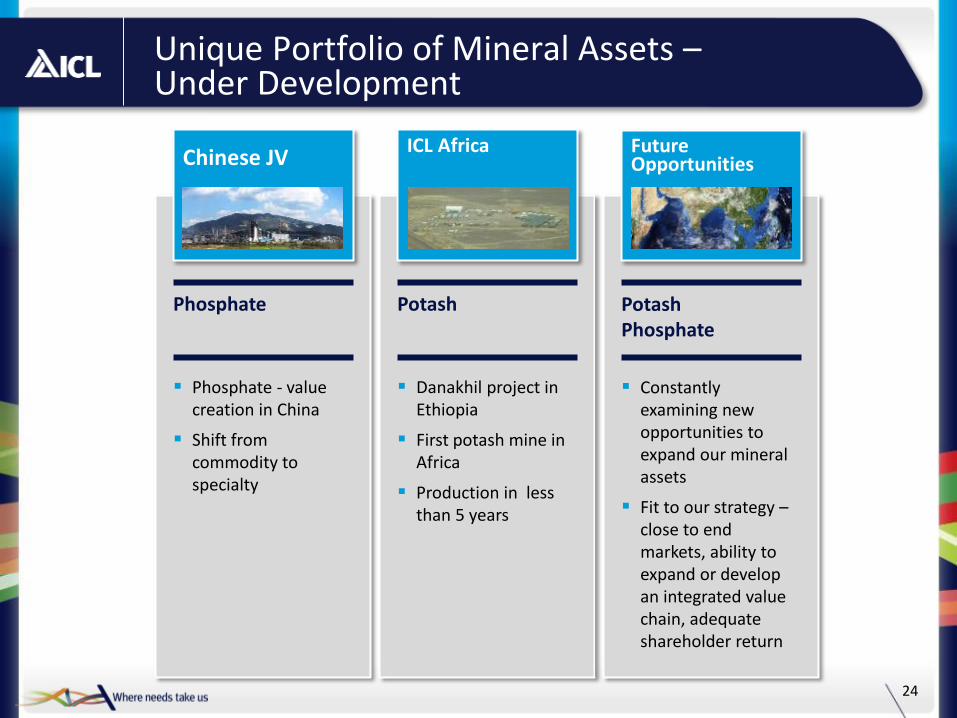

Unique Portfolio of Mineral Assets – Under Development

24

Phosphate - value creation in China

Shift from commodity to specialty

Chinese JV

Phosphate

Danakhil project in Ethiopia

First potash mine in Africa

Production in less than 5 years

ICL Africa

Potash

Constantly examining new opportunities to expand our mineral assets

Fit to our strategy – close to end markets, ability to expand or develop an integrated value chain, adequate shareholder return

Future Opportunities

Potash Phosphate

Strategy Highlights

25

Unique business model Build global

integrated value chains

Execute on $350M efficiency improvements Improve positioning

on production cost curve

Cross-organization process improvement

Grow core business Organic growth Acquisitions

Mineral assets Capability

Enhancing Acquisitions

Asset allocation focused on total shareholder return Divestiture of non-core

assets Attractive dividend

policy

ICL Segments, Business Environment, Additional Strategic Milestones

Agriculture

Growth Factors - Fertilizers and Food Products

28

Meat Consumption

Population

Fertilizer consumption

1.0

2.0

3.0

4.0

5.0

6.0 Index, relative to 1962

Yield Growth Required to Meet World’s Food Needs Population, Meat and Fertilizers [Base 1962]

Source: IFA, USDA, USA Census

Diminishing arable land per capita

World Grains Production & Consumption

29 Grains and Pulses: Barley, Corn, Millet, Mixed Grain, Oats, Rice, Rye, Sorghum, Wheat

16.72%

19.80%

21.77%

16%

18%

20%

22%

24%

26%

28%

30%

32%

34%

36%

38%

1.4

1.5

1.6

1.7

1.8

1.9

2.0

2.1

2.2

2.3

2.4

2.5

Bill

ion

To

nn

e

Consumption Production Stock to Use

Sources: USDA, (Updated October 2015)

$1

$3

$5

$7

$9

$11

$13

$15

$17

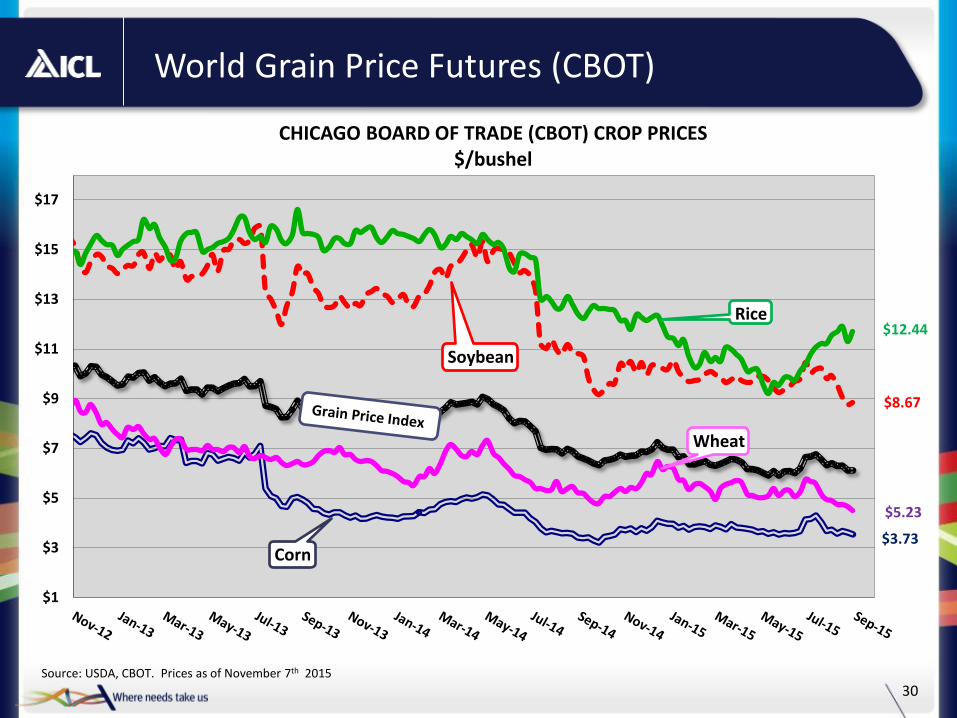

CHICAGO BOARD OF TRADE (CBOT) CROP PRICES $/bushel

Corn

Rice

Soybean

Wheat

World Grain Price Futures (CBOT)

30 Source: USDA, CBOT. Prices as of November 7th 2015

$12.44

$5.23

$3.73

$8.67

31

Fertilizer Prices

Potash Prices

FOB Vancouver standard KCl

US$/t spot US$/t spot

Average DAP fob Tampa

Average GTSP, fob North Africa

Phosphate Prices

* Source: Fertilizer Week, prices as of October 15, 2015

FOB NOLA granular KCl

200

250

300

350

400

450

500

550

600

650

0

100

200

300

400

500

600

700

32

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Ind

ex o

f Fe

rtili

zer

Pri

ce R

atio

to

GP

I Bas

e 20

02

MOP/GPI

DAP/GPI

Fertilizers are Affordable

*GPI = Grain Price Index formula: [(wheat price*7) + (maize price*8) + (rice price*4.5) + (soybean price*2.5)] /22]

Source: CBOT, Fertilizer Week & ICL

33

China China China

China China India

India India

India India

Brazil

Brazil Brazil

Brazil

Brazil

USA

USA

USA

USA

USA

SE Asia

SE Asia

SE Asia

SE Asia

SE Asia

RoW

RoW

RoW

RoW

RoW China India

Brazil RoW

1999 2006 2013 2014 China India Brazil RoW 2020 2025

80*

72*

53

62

Potash Demand Growth Estimates Source: CRU

Region 1999-2014

CAGR

2014-2020

Growth (tonnes)

2014-2020

CAGR

China 7% 1.3 1.5%

India 3% 2.2 7%

Brazil 6% 2.7 4%

USA 1% (0.4) 1%-

SE Asia 6% 2.1 4.4%

RoW 0% 2 2%

Total 3% 10 2.5%

After 2020 annual growth rate returns to 2%, and reaches 18M tonnes

growth from 2014 to 2025

Million tonnes KCl

Source: CRU, ICL estimates

*FertEcon estimations for 2020 & 2025: 75M tonnes & 81.5M tonnes, respectively

34

Agriculture

ICL Dead Sea

ICL Rotem

ICL Turkey

5,855 Employees Worldwide

ICL Haifa

ICL UK

ICL Iberia

ICL Germany

ICL The Netherlands

Fuentes

Nutrisi Everris

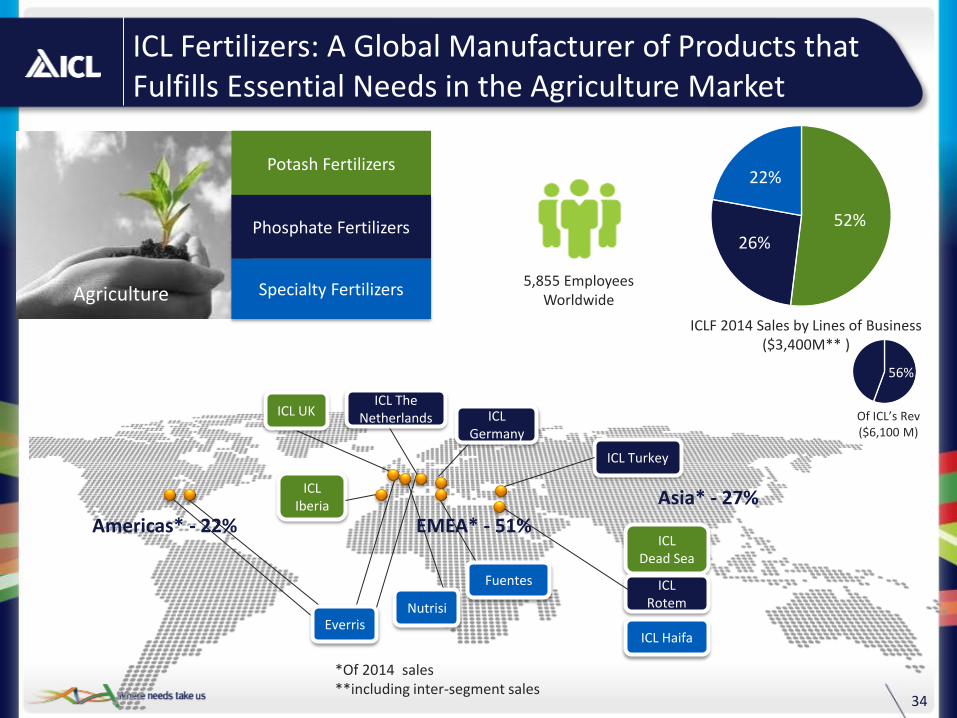

ICL Fertilizers: A Global Manufacturer of Products that Fulfills Essential Needs in the Agriculture Market

Potash Fertilizers

Phosphate Fertilizers

Specialty Fertilizers

52% 26%

22%

ICLF 2014 Sales by Lines of Business ($3,400M** )

Of ICL’s Rev ($6,100 M)

56%

Americas* - 22%

Asia* - 27%

EMEA* - 51%

*Of 2014 sales **including inter-segment sales

Strategic Geographic Advantage Clear Service Advantage to Developed and Emerging Markets

Destination (Days) Destination ($/tonne)

Country of Departure Mine-to-Port (km)

(1) China India Brazil China India Brazil

Israel ~200 23 11 22 21 15 17

UK ~30 34 22 20 32 27 17

Spain ~85 27 15 17 34 26 17

Germany ~350 34 23 20 30 26 16

Russia / Belarus ~600 39 27 25 24 26 18

Canada West Coast ~1,700 35 47 43 15 26 29

Source: ICL estimates, Netpas

China

India

IL

Europe

Brazil

US

Low plant gate-to-port costs and ocean freight costs with faster time to markets

• ICL has Shorter and Lower Cost Shipping Routes to Emerging Markets

35 1 Israel based on average from Dead Sea to Port of Eilat and Ashdod; Germany based on Werra to Port of Hamburg and Bremerhaven; Canada based on Saskatchewan to Port of

Vancouver; Russia based on Starobin to Port of Klaipeda; Spain based on Cabanasas Mine to Port of Barcelona; UK based on Cleveland Potash, Saltburn-by-the-Sea to Teesport Commerce Park

36

1

3

4

5

2

ICL Dead Sea – Raw Material Extraction

Pumping and

evaporation process

1

2

3

4

5

37

The Phosphate Market and ICL’s Position

43.0

46.4

- 0.2 0.2 0.4

1.7

1.2

2014consumption

USA China Brazil India RoW 2019consumption

Million tonnes P2O5

Source: CRU

We are active in the TSP, SSP and Phosphoric Acid

• TSP marketing focuses on Brazil, USA and Europe

SSP marketing focuses mainly on Brazil

• We are the largest supplier of PK fertilizers in Europe

• We plan to become a supplier of DAP in future

CAGR 2014-2019: 1.5%

Specialties

Light

Specialties

Commodities

• Added value

• Higher prices

• Smaller volumes

• Selective distribution

Specialty Fertilizers vs. Commodities

CRF (Controlled Release Fertilizers)

WSNPK (Water Soluble Fertilizers)

NOP (Potassium Nitrate)

CN (Calcium Nitrate)

Soluble (MAP/MKP)

“Special NPK”

38

Our Advantages

Supply chain

Production process-technology adding

value

Market position R&D Innovate the next generation

• Controlled release fertilizers • Fertigation and foliar solubles • Enhanced nutrients and water efficiency

• Back integrated • Access to high quality raw material • Efficient supply chain (high synergies)

• Highly professional Agronomic Sales team • Integrated and tailored service • Full product portfolio • Distributor loyalty • Strong Branding

39

40

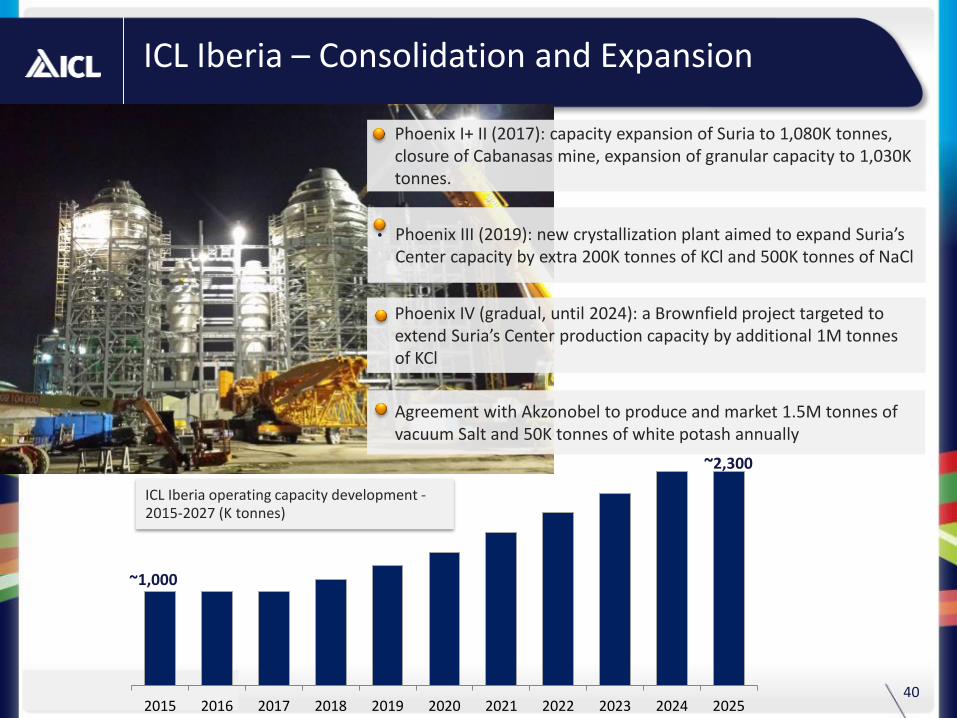

ICL Iberia – Consolidation and Expansion

ICL Iberia operating capacity development - 2015-2027 (K tonnes)

• Phoenix I+ II (2017): capacity expansion of Suria to 1,080K tonnes, closure of Cabanasas mine, expansion of granular capacity to 1,030K tonnes.

• Phoenix III (2019): new crystallization plant aimed to expand Suria’s Center capacity by extra 200K tonnes of KCl and 500K tonnes of NaCl

• Phoenix IV (gradual, until 2024): a Brownfield project targeted to extend Suria’s Center production capacity by additional 1M tonnes of KCl

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

~1,000

~2,300

• Agreement with Akzonobel to produce and market 1.5M tonnes of vacuum Salt and 50K tonnes of white potash annually

ICL to Establish Bulk Blending Facilities Across Ethiopia to Support Demand Growth

Bulk Blending - fertilizer plant designed to blend several nutrients. The final formula is determined according to the crop needs and availability of nutrient in the soil

Several locations has been investigated

First Bulk Blend was already established in Tulu Bolo by the Ethiopian Government

Djibouti Port

Allana Potash

Oromia

Amhara

SNNP

Tigray Mekele

Nekemte

Tulu Bolo

Worabe

Bahar Dar

• Alternatives examined by ICL • Sites where the Ethiopian Government established or intend to

establish BB facilities without any private business partner

Fertilizers are considered as a strategic commodity in Ethiopia

The plants are design to serve an area of about 200Km radius, use 150 k tonnes of potash annually through various number of formulas

The Ethiopian Gov. is defining the preferred cooperation model between the public and private sectors

41

42

Fulfilling Potash Demand Growth Potential in India

An ICL & IPL JV, Bringing India to the state of the art potash fertilization

- K +K

The program enters its 3rd year, covers 52 districts in 9 states around India

21 experienced agronomists help providing evidence of the profitable use of potash

~400 farmer activities (Oct ’13 – Apr ’15) including field days, jeep campaigns, crop seminars and farmers meetings.

~2,000 Demonstration plots (Oct ’13 – Apr ’15) with more than 20 crops

Results: 15-35% average increase in yields;

Success stories demonstrate benefit-to-cost ratios between 13:1 and 43:1

43

Africa – Driving Demand in an Unexploited Potash Market

Potential potash consumption of more than 400k tonnes between Ethiopia, Tanzania & Kenya. Current consumption – 40-50k tonnes

Africa has 12% of the world’s arable land but only 20% is cultivated

Only 7% is irrigated (40% in Asia)

Share in global population to grow from 15% in 2010 to 23% in 2050

Only 1.7% of global potash consumption

Program led by ICL in collaboration with

Ethiopian partners

Range of activities to increase awareness among farmers of the benefits of potash:

Demonstration plots, outreach to farmers

Soil fertility mapping

Research and validation

Expansion into Tanzania

44

ICL Specialty Fertilizers Strategy to Deliver High Growth Rates

4-6 % CAGR

1-2 % Market Growth

Ornamental Horticulture

(21% of sales)

6-8 % CAGR

0 % Market Growth Professional Turf

(8.5% of sales)

>10% CAGR

5-6 % Market Growth Specialty

Agriculture (60% of sales)

1-3 % CAGR

1 % Market Growth

Chemicals (10.5% of sales)

45

ICL Specialty Fertilizers: The Path for Faster than the Market Growth

0.7 1.4

0.8

1.4 1.4

2.6

2023

5.4

2014

2.9

Market USD bn

1 Other straights includes MAP/MKP, Calcium Nitrate, SOP

ws NPK

NOP

Other Straights1

9%

SOLUBLES

2023

5.4

2014

3.5

5%

FOLIAR LIQUIDS

2023

3.5

2014

0.9

16%

Controlled Release Fert.

ICL Specialty Fertilizers Growth Pillars

Establish production in

attractive markets

Enlarge Product Portfolio-

New Potassium Nitrate

production plant

Reduce cost of production

New production

plants with focus on

emerging markets

Grow with R&D

and new Strategic

Partners

New cost efficient

coating generation

46

Produt Development Trials US$/acre Current practice CRF

Fertilizer volume (lbs N/acre) 60 40

Fertilizer costs 103 103

Application costs 43 20

Yield value 1,188 1,284

Net value1 1,042 1,160

(2 less)

(1/3 less)

(+11%)

Sugar production in Florida

+ 11 % income

2 fewer applications

33% less N

Adoption time 2-5 years

Has to taste fertilizer to check quality!

Proof of Performance and Market Education

Proof of performance

Market education: new technologies adoption

• Field Biology

• Product Evaluation

• Product development

• Trials

• Grower/Food industry

• Projects

Geographical Expansion

47

Production moves closer to Emerging Markets

High logistic synergies

Improve Yield & Quality

Innovative technology

Market education

Worldwide Agronomist team

Focus on Plants needs

Knowledge and experience in the market

Strategic alliance with YTH

Engineered Materials

ICL Industrial Products: Vast Global Footprint

49

2500 Employees worldwide

Of ICL sales in 2014

22% EMEA

Americas

Asia

Plant

Sales

R&D

Sales by region $1.3B sales in 2014

ICL Industrial Products - from Assets to Markets

50

Bromine

Phosphorus

Mineral Salts

Magnesium

Chlorine

Flame Retardants

Energy and Intermediates

Microbial Solutions

Mineral Applications

Chemistries Key Markets

Back Integration to Customer Solutions

Global Trends Supporting Our Business

51

Population Regulation & Environmental Standard of living

FURNITURE & TEXTILE TRANSPORTATION

WATER TREATMENT

CONSTRUCTION

INTERMEDIATES FOR FOOD,

PHARMA, AGRO OIL & GAS

POWER PLANTS

ELECTRONICS

Global Cost Leader in Bromine

52

0.02 – 0.03 0.03 – 0.05 0.5 – 0.9

3.5 – 4.5 2.5 – 5.5

11.0 – 12.0 g/liter

UndergroundWells

(China)

Sea Water(China, Japan)

Shallow Sea(Ukraine)

Salt Lake(India)

UndergroundWells (U.S.)

Dead SeaOperations

(Israel, Jordan)

• The Dead Sea provides the highest concentration of Bromine

• Cost is related to concentration

• Abundant supply

Source: ICL estimates, MarketsandMarkets

A Global Leader in a Concentrated Market

53

ICL holds the largest capacity Global Bromine Capacity, by producer

280 280

120 120

95 91

92 88

93 83

64 69

2014 2019

Albemarle (Dead Sea)

ICL (Dead Sea)

Other

Albemarle (US)

Chemtura (US)

China

Bromine demand by industry - 2014

Market utilization rates: 70-80%

Flame retardants

41%

Brominated organic

intermediates 21%

Clear brine fluids 18%

Industrial 8%

Biocides 6%

Fumigants 3%

Mercury control

3%

744 731

Source: ICL estimates, MarketsandMarkets

Strategy and Investment Highlights

54

Grow our core business: Organic growth Margin expansion Pricing Portfolio management

Cost reduction: Operational excellence Reduction of labor costs Divest non-core businesses

Advocacy: SAFR™ (Scientific

Assessment for Flame Retardants)

Flame retardants standards

Merquel® in China/EU

Grow the Bromine pie: In-house R&D Outside technical

collaborations Focus on customer unmet

needs to bring new products and solutions

55

Industrial Products’ Growth Projects - a Significant Contribution To Future Sales

FURNITURE & TEXTILE

TRANSPORTATION WATER

TREATMENT CONSTRUCTION

INTERMEDIATES FOR FOOD, PHARMA,

AGRO

OIL & GAS POWER PLANTS ELECTRONICS

Growth areas – short to mid term

Next generation Polymeric and Reactive flame retardants

Brominated biocides

Merquel and Clear Brine Fluids

Purified potassium chloride

Energy Storage

2020 estimated contribution

Potential sales of ~$150M with above average operating income

Growth areas – long term

Energy storage

Gold extraction

Soil fumigation

3-D printing

Significant contribution beyond 2020

Growing core business through in-house R&D

Margin expansion, pricing, focus on customer unmet needs

Advocacy: SAFR™ (Scientific Assessment for Flame Retardants), Merquel® in China/EU

Implementing

growth strategy

ICL Performance Products: Overview

56

Of ICL Sales in 2014*

25% 40%

32%

28%

Non Core

3,300 Employees Worldwide

Advanced Additives

Food Specialties

Sales by Business unit $1.5B sales in 2014

Americas 40%

Asia/Pacific 15%

EMEA 45%

'06 '07 '08 '09 '10 '11 '12 '13 '14 '15E '16E '17E '18E '19E

Op

era

tin

g In

com

e %

Rev

en

ue

(m

$)

Core (Rev $) Non Core (Rev $) Core (OI %) Non Core (OI %)

ICL Performance Products: Focus on Core

57

Thermphos –

P2S5

business

$1,711M

1,533

Estimated CAGR 2015-2019: 3-5% Estimated operating margin expansion: about 150-250 basis points

Advanced Additives – A Stable Portfolio With Broad Applications

58

Advanced Additives – Expand Through Differentiation

59

Class A Fire

ICL provides products and services that help prevent, control, and suppress fires

World-wide reputation A strong market position

2014 acquisition of Auxquimia: specialists in the Class B Foam for oil, refinery and chemical industry

Complete and broad portfolio Own testing facilities Fluorine free product innovations

Class B Fire

Fire Safety Products

Food

61

Food Specialties – What We Do

Linking Markets with Consumer Trends

Sugar Fat

Sodium

Proteins Fibers

Minerals Antioxidants

Healthy Reduction versus Healthy Enhancements

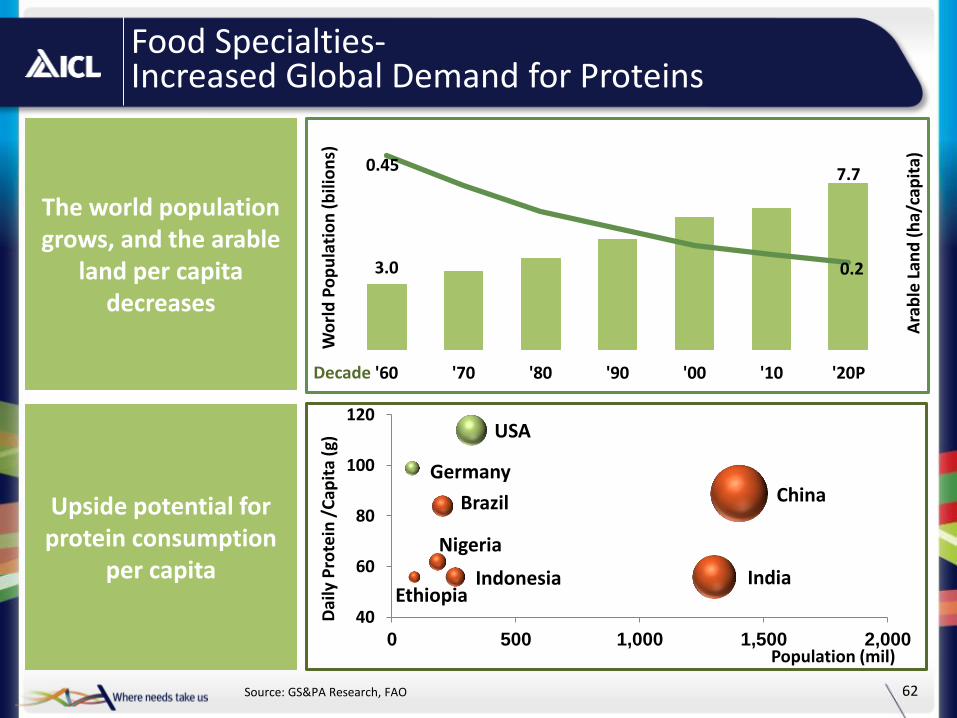

Food Specialties- Increased Global Demand for Proteins

62

Upside potential for protein consumption

per capita

Brazil China

Ethiopia

Germany

India Indonesia

Nigeria

USA

40

60

80

100

120

0 500 1,000 1,500 2,000

Dai

ly P

rote

in /

Cap

ita

(g)

Population (mil)

3.0

7.7 0.45

0.2

'60 '70 '80 '90 '00 '10 '20P

Ara

ble

Lan

d (

ha/

cap

ita)

Wo

rld

Po

pu

lati

on

(b

ilio

ns)

The world population grows, and the arable

land per capita decreases

Decade

Source: GS&PA Research, FAO

Food Specialties – Add Technology Platforms: Whey Proteins in Europe

63

Acquisition of Prolactal/Rovita in Q1/2015 is a big step in implementing the strategy

2014 annual revenue of $110 M; market growth of approximately 10% annually

Proprietary technology can be expanded into other regions

Dair

y

Meat/

Po

ult

ry

/ S

eafo

od

Bakery

Bevera

ge

Phosphate Salts

Whey Proteins

Vegetable Proteins

Spices

Efficiency and Operational Excellence

ACE Drives Functional Excellence in 5 Key Processes

Commercial excellence

ACE streams

Energy efficiency

Procurement

CAPEX (investment)

R&D

Current Status

Establishment of the commercial excellence

program.

Establishment of a new global function: CIO

Establishment of a new global function: CTO

Establishment of a new global function: CPO

Ongoing efforts

Volume Activity

~ $6000 million of Revenues

Annual spending: ~ $400 million

Annual spending: ~ $4000 million

Annual CAPEX spending: ~ $800 million

~ $6000 million of Revenues

Asset productivity

Revenue increase

Cost reduction

ICL’s core value creation drivers

65

Procurement Savings: Three Potential Levers

What did we do? • One global ICL

approach – regions & management level

• Coordination alignment between global and regional

• Excellent global team work

• Exploration of supply options over the entire value chain

• One global contract or no contract

Result: • Annual saving: $2.1 M

(25%) • Global contract for the

US, Israel & Europe

AC

E

Supplier management

Process management

Demand management

Volume consolidation

Supplier partnerships

Negotiation

Transportation agreements

Make-or-buy opportunities

Simplify specifications to fulfill (not exceed) requirements

Find "replacements" and alternative technologies

Manage service levels/demand

Reduce waste

Success story- Phenol contract

66

As project progresses, budget is committed, ability to change project decisions/add value decreases:

100%

Low

High

Project life cycle

0%

CAPEX Value Engineering

A systematic and structured approach for improving projects, products, and processes

Used to analyze and improve manufacturing products and processes, design and construction projects

Helps achieve an optimum balance between function, performance, quality, safety and cost

The proper balance results in the maximum value for the project

AC

E

Ability to improve value

Commitment of funds

CAPEX value engineering:

Potential cash flow contribution: ~$100M

67

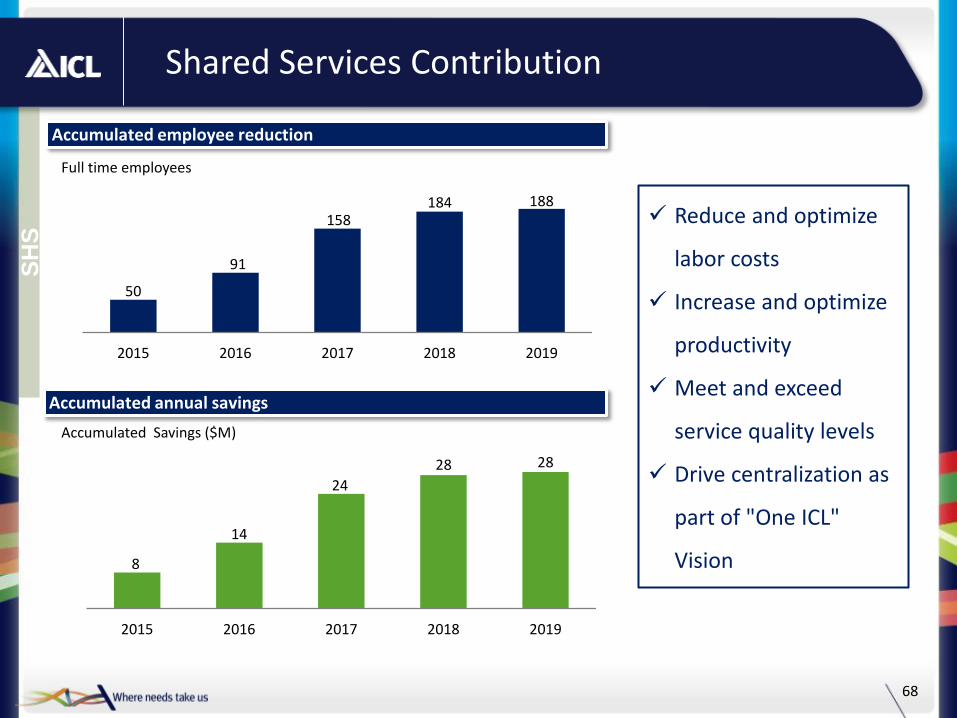

Shared Services Contribution

Reduce and optimize

labor costs

Increase and optimize

productivity

Meet and exceed

service quality levels

Drive centralization as

part of "One ICL"

Vision

Full time employees

50

91

158 184 188

2015 2016 2017 2018 2019

Accumulated employee reduction

Accumulated annual savings

Accumulated Savings ($M)

8

14

24

28 28

2015 2016 2017 2018 2019

SH

S

68

Thank you