Investor Presentation - · PDF fileInvestor Presentation ... details on RM million 1Q FY2017...

58

0 www.maybank.com Investor Presentation Financial Results First Quarter FY2017 ended 31 March 2017 25 May 2017 Humanising Financial Services

-

Upload

trinhxuyen -

Category

Documents

-

view

216 -

download

0

Transcript of Investor Presentation - · PDF fileInvestor Presentation ... details on RM million 1Q FY2017...

0www.maybank.com

Investor Presentation

Financial ResultsFirst Quarter FY2017 ended 31 March 2017

25 May 2017

Humanising Financial Services

1

Table of Contents

Executive Summary 2

Results Overview 5

Prospects & Outlook 20

Appendix:

1. Financial Performance 23

2. Community Financial Services 31

3. Global Banking 36

4. Maybank Singapore 41

5. Maybank Indonesia 45

6. Other segments 50

7. Affiliates 55

Financial Results: 1Q FY2017 ended 31 March 2017

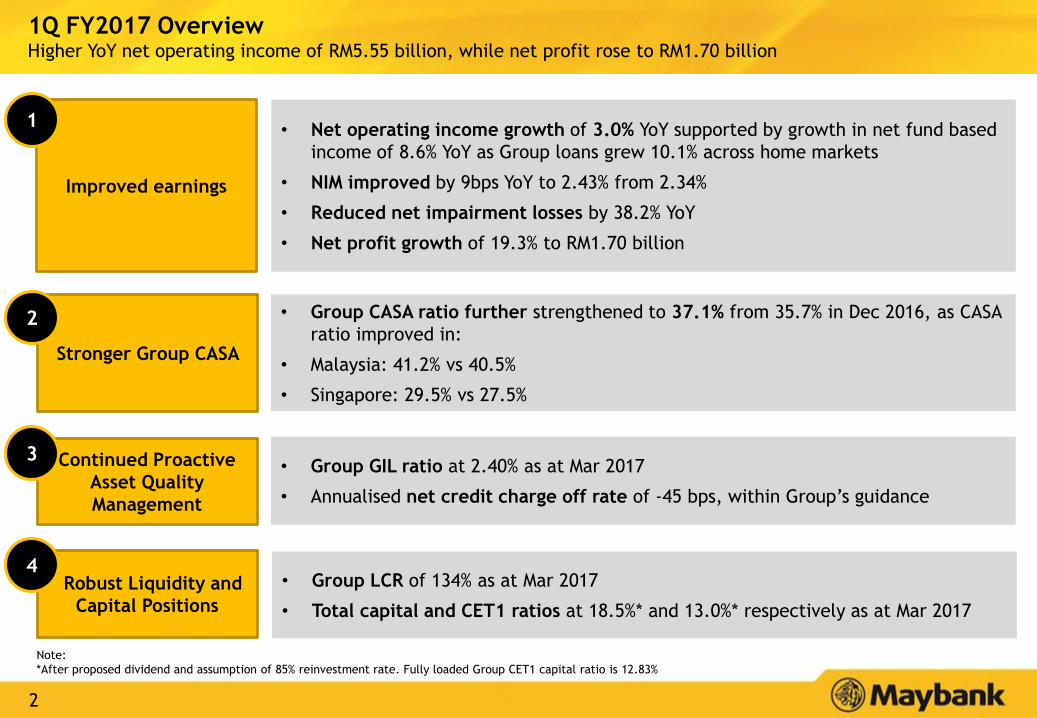

2

Improved earnings

1Q FY2017 OverviewHigher YoY net operating income of RM5.55 billion, while net profit rose to RM1.70 billion

• Net operating income growth of 3.0% YoY supported by growth in net fund based

income of 8.6% YoY as Group loans grew 10.1% across home markets

• NIM improved by 9bps YoY to 2.43% from 2.34%

• Reduced net impairment losses by 38.2% YoY

• Net profit growth of 19.3% to RM1.70 billion

1

• Group GIL ratio at 2.40% as at Mar 2017

• Annualised net credit charge off rate of -45 bps, within Group’s guidance

Continued Proactive

Asset Quality

Management

• Group LCR of 134% as at Mar 2017

• Total capital and CET1 ratios at 18.5%* and 13.0%* respectively as at Mar 2017

Robust Liquidity and

Capital Positions

4

Stronger Group CASA

2 • Group CASA ratio further strengthened to 37.1% from 35.7% in Dec 2016, as CASA

ratio improved in:

• Malaysia: 41.2% vs 40.5%

• Singapore: 29.5% vs 27.5%

3

Note:

*After proposed dividend and assumption of 85% reinvestment rate. Fully loaded Group CET1 capital ratio is 12.83%

3

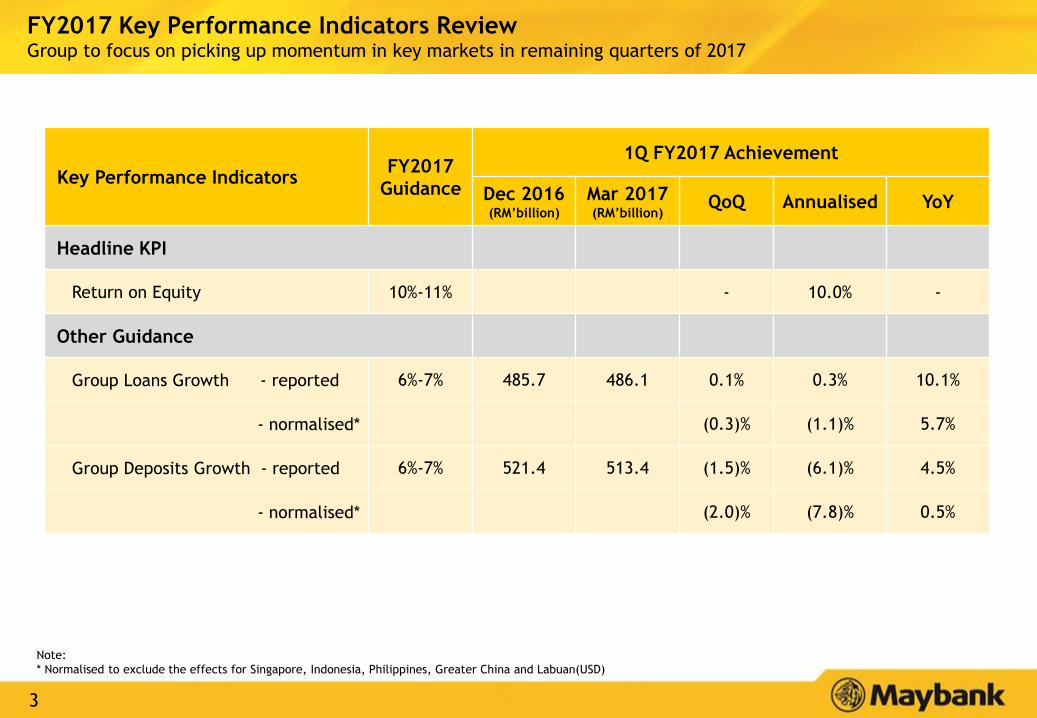

FY2017 Key Performance Indicators ReviewGroup to focus on picking up momentum in key markets in remaining quarters of 2017

Key Performance IndicatorsFY2017

Guidance

1Q FY2017 Achievement

Dec 2016(RM’billion)

Mar 2017(RM’billion)

QoQ Annualised YoY

Headline KPI

Return on Equity 10%-11% - 10.0% -

Other Guidance

Group Loans Growth - reported 6%-7% 485.7 486.1 0.1% 0.3% 10.1%

- normalised* (0.3)% (1.1)% 5.7%

Group Deposits Growth - reported 6%-7% 521.4 513.4 (1.5)% (6.1)% 4.5%

- normalised* (2.0)% (7.8)% 0.5%

Note:

* Normalised to exclude the effects for Singapore, Indonesia, Philippines, Greater China and Labuan(USD)

4

Table of Contents

Executive Summary 2

Results Overview 5

Prospects & Outlook 20

Appendix:

1. Financial Performance 23

2. Community Financial Services 31

3. Global Banking 36

4. Maybank Singapore 41

5. Maybank Indonesia 45

6. Other segments 50

7. Affiliates 55

Financial Results: 1Q FY2017 ended 31 March 2017

5

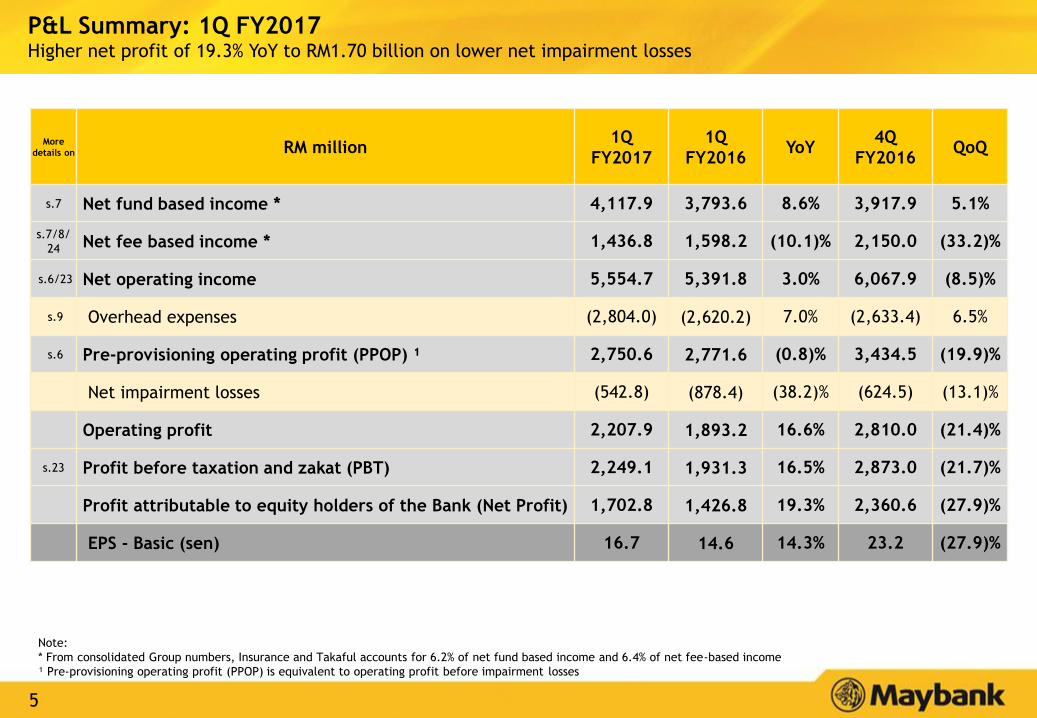

P&L Summary: 1Q FY2017Higher net profit of 19.3% YoY to RM1.70 billion on lower net impairment losses

More

details on RM million1Q

FY2017

1Q

FY2016YoY

4Q

FY2016QoQ

s.7 Net fund based income * 4,117.9 3,793.6 8.6% 3,917.9 5.1%

s.7/8/

24 Net fee based income * 1,436.8 1,598.2 (10.1)% 2,150.0 (33.2)%

s.6/23 Net operating income 5,554.7 5,391.8 3.0% 6,067.9 (8.5)%

s.9 Overhead expenses (2,804.0) (2,620.2) 7.0% (2,633.4) 6.5%

s.6 Pre-provisioning operating profit (PPOP) ¹ 2,750.6 2,771.6 (0.8)% 3,434.5 (19.9)%

Net impairment losses (542.8) (878.4) (38.2)% (624.5) (13.1)%

Operating profit 2,207.9 1,893.2 16.6% 2,810.0 (21.4)%

s.23 Profit before taxation and zakat (PBT) 2,249.1 1,931.3 16.5% 2,873.0 (21.7)%

Profit attributable to equity holders of the Bank (Net Profit) 1,702.8 1,426.8 19.3% 2,360.6 (27.9)%

EPS - Basic (sen) 16.7 14.6 14.3% 23.2 (27.9)%

Note:

* From consolidated Group numbers, Insurance and Takaful accounts for 6.2% of net fund based income and 6.4% of net fee-based income

¹ Pre-provisioning operating profit (PPOP) is equivalent to operating profit before impairment losses

6

2,772

1,3111,539

100(25)

134

2,751

1,476 1,407

64 27178

Total Group CommunityFinancial Services

Group CorporateBanking & Global

Markets

Group InvestmentBanking

Group AssetManagement

Group Insurance &Takaful

1Q FY2016

1Q FY2017

5,392

3,019

1,992

3761 292

5,555

3,292

1,900

35267

345

Total Group CommunityFinancial Services

Group CorporateBanking & Global

Markets

Group InvestmentBanking

Group AssetManagement

Group Insurance &Takaful

1Q FY2016

1Q FY2017

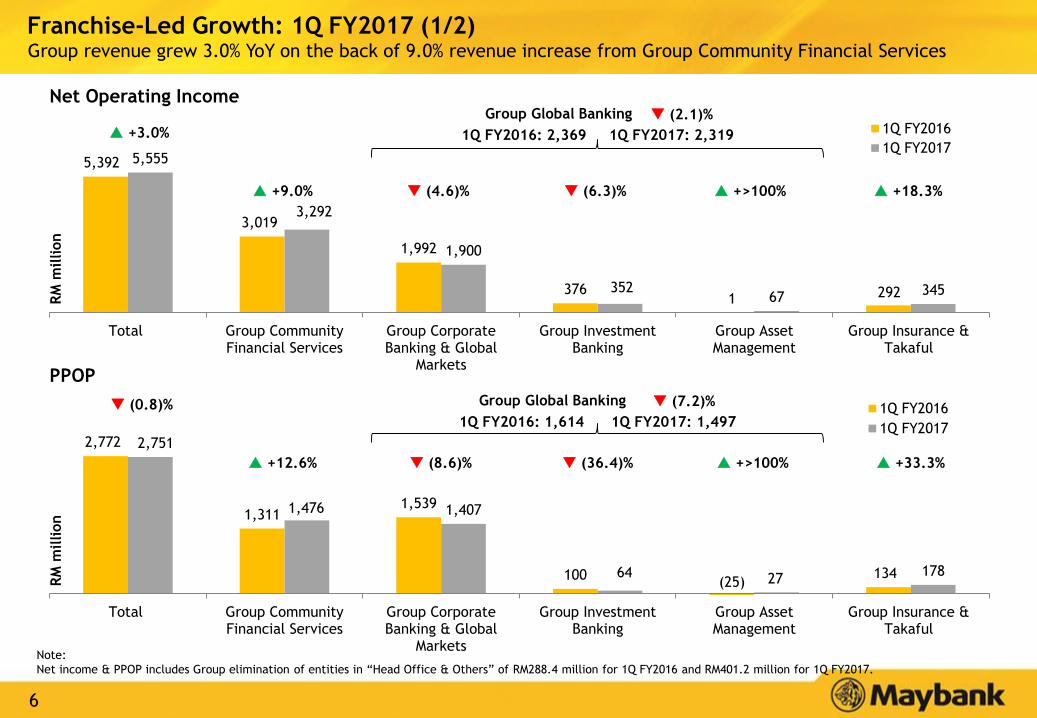

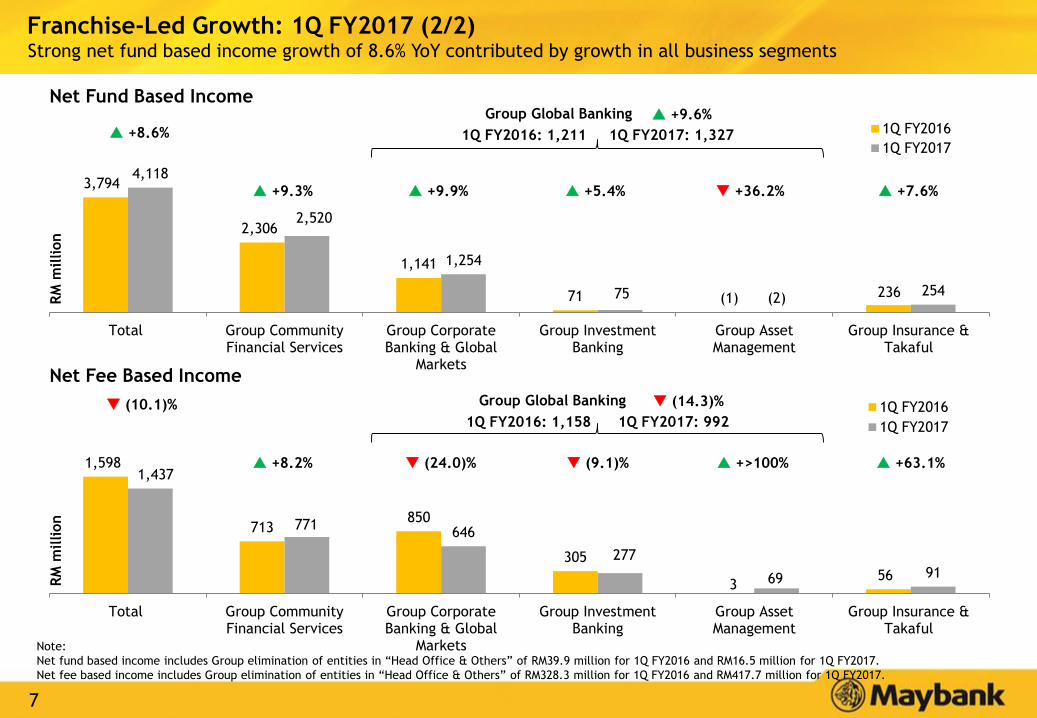

Franchise-Led Growth: 1Q FY2017 (1/2)Group revenue grew 3.0% YoY on the back of 9.0% revenue increase from Group Community Financial Services

Net Operating Income

RM

million

RM

million

PPOP

+3.0%

+9.0% (4.6)% (6.3)% +18.3% +>100%

Group Global Banking (7.2)%

1Q FY2016: 1,614 1Q FY2017: 1,497

Group Global Banking (2.1)%

1Q FY2016: 2,369 1Q FY2017: 2,319

(0.8)%

+12.6% (8.6)% (36.4)% +33.3% +>100%

Note:

Net income & PPOP includes Group elimination of entities in “Head Office & Others” of RM288.4 million for 1Q FY2016 and RM401.2 million for 1Q FY2017.

7

1,598

713850

305

356

1,437

771646

277

69 91

Total Group CommunityFinancial Services

Group CorporateBanking & Global

Markets

Group InvestmentBanking

Group AssetManagement

Group Insurance &Takaful

1Q FY2016

1Q FY2017

3,794

2,306

1,141

71 (1) 236

4,118

2,520

1,254

75 (2)254

Total Group CommunityFinancial Services

Group CorporateBanking & Global

Markets

Group InvestmentBanking

Group AssetManagement

Group Insurance &Takaful

1Q FY2016

1Q FY2017

Net Fund Based Income

RM

million

RM

million

Net Fee Based Income

+8.6%

+9.3% +9.9% +5.4% +7.6% +36.2%

Group Global Banking (14.3)%

Group Global Banking +9.6%

1Q FY2016: 1,211 1Q FY2017: 1,327

(10.1)%

+8.2% (24.0)% (9.1)% +63.1% +>100%

Franchise-Led Growth: 1Q FY2017 (2/2)Strong net fund based income growth of 8.6% YoY contributed by growth in all business segments

1Q FY2016: 1,158 1Q FY2017: 992

Note:

Net fund based income includes Group elimination of entities in “Head Office & Others” of RM39.9 million for 1Q FY2016 and RM16.5 million for 1Q FY2017.

Net fee based income includes Group elimination of entities in “Head Office & Others” of RM328.3 million for 1Q FY2016 and RM417.7 million for 1Q FY2017.

8

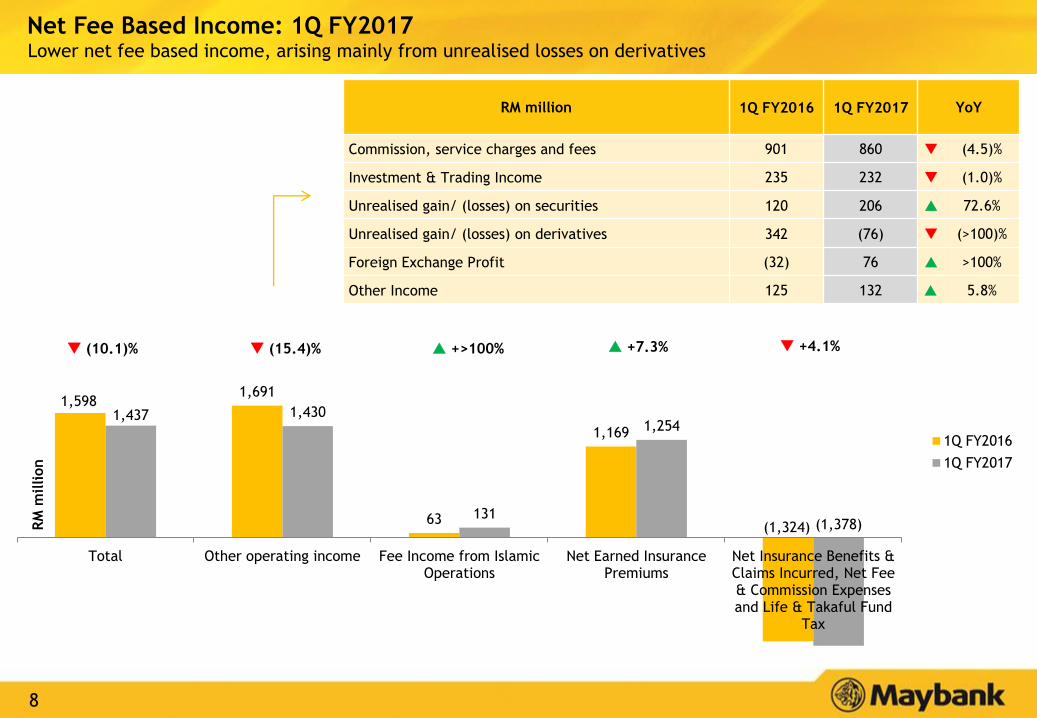

1,598 1,691

63

1,169

(1,324)

1,437 1,430

131

1,254

(1,378)

Total Other operating income Fee Income from IslamicOperations

Net Earned InsurancePremiums

Net Insurance Benefits &Claims Incurred, Net Fee& Commission Expensesand Life & Takaful Fund

Tax

1Q FY2016

1Q FY2017

RM

million

RM million 1Q FY2016 1Q FY2017 YoY

Commission, service charges and fees 901 860 (4.5)%

Investment & Trading Income 235 232 (1.0)%

Unrealised gain/ (losses) on securities 120 206 72.6%

Unrealised gain/ (losses) on derivatives 342 (76) (>100)%

Foreign Exchange Profit (32) 76 >100%

Other Income 125 132 5.8%

Net Fee Based Income: 1Q FY2017Lower net fee based income, arising mainly from unrealised losses on derivatives

(10.1)% (15.4)% +>100% +7.3% +4.1%

9

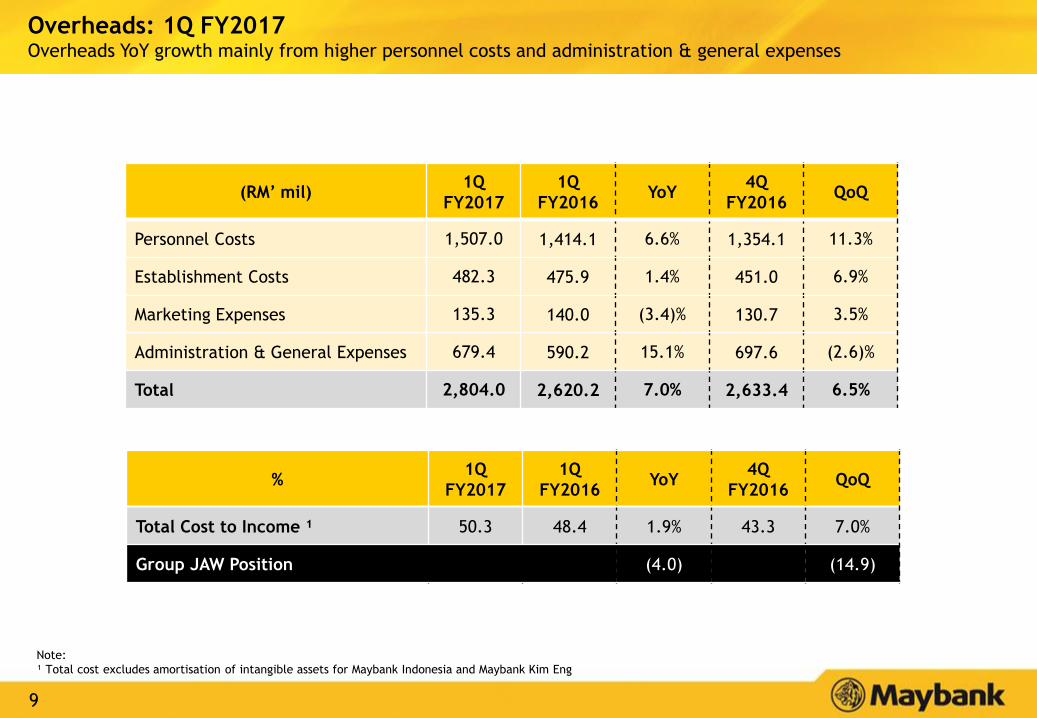

(RM’ mil)1Q

FY2017

1Q

FY2016YoY

4Q

FY2016QoQ

Personnel Costs 1,507.0 1,414.1 6.6% 1,354.1 11.3%

Establishment Costs 482.3 475.9 1.4% 451.0 6.9%

Marketing Expenses 135.3 140.0 (3.4)% 130.7 3.5%

Administration & General Expenses 679.4 590.2 15.1% 697.6 (2.6)%

Total 2,804.0 2,620.2 7.0% 2,633.4 6.5%

%1Q

FY2017

1Q

FY2016YoY

4Q

FY2016QoQ

Total Cost to Income ¹ 50.3 48.4 1.9% 43.3 7.0%

Group JAW Position (4.0) (14.9)

Overheads: 1Q FY2017Overheads YoY growth mainly from higher personnel costs and administration & general expenses

Note:

¹ Total cost excludes amortisation of intangible assets for Maybank Indonesia and Maybank Kim Eng

10

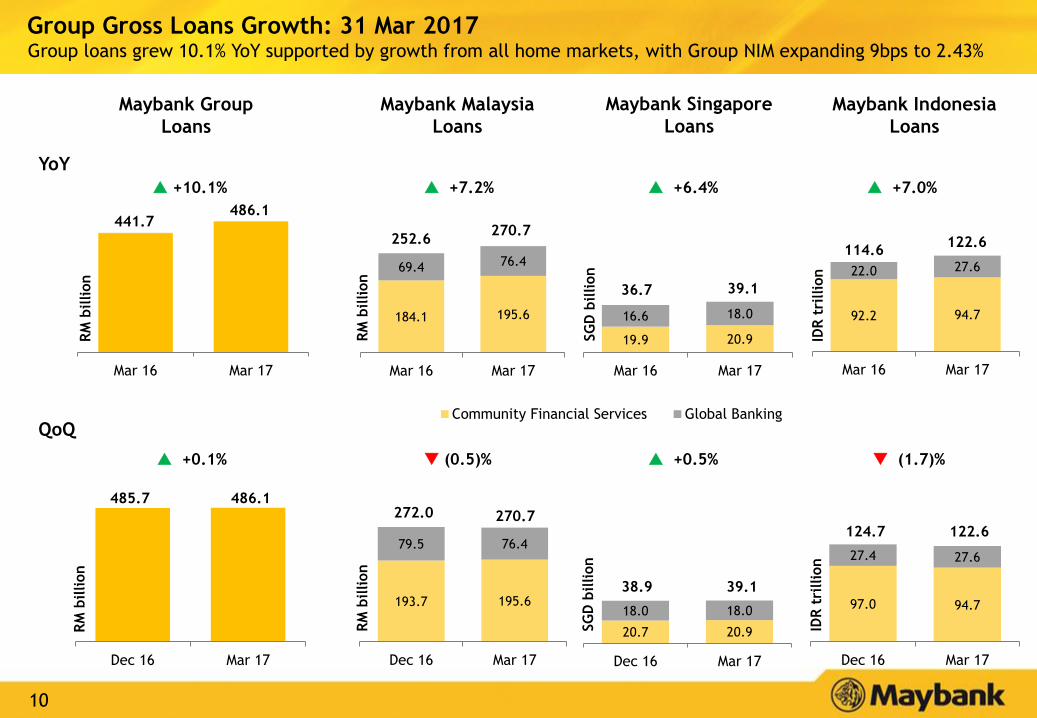

193.7 195.6

79.5 76.4

Dec 16 Mar 17

Community Financial Services Global Banking

485.7 486.1

Dec 16 Mar 17

441.7486.1

Mar 16 Mar 17

Group Gross Loans Growth: 31 Mar 2017Group loans grew 10.1% YoY supported by growth from all home markets, with Group NIM expanding 9bps to 2.43%

184.1 195.6

69.4 76.4

Mar 16 Mar 17

19.9 20.9

16.6 18.0

Mar 16 Mar 17

92.2 94.7

22.0 27.6

Mar 16 Mar 17

Maybank Group

Loans

270.7252.6

39.136.7

122.6114.6

20.7 20.9

18.0 18.0

Dec 16 Mar 17

97.0 94.7

27.4 27.6

Dec 16 Mar 17

270.7272.0

39.138.9

122.6124.7

QoQ

RM

billion

SG

D b

illion

IDR

tri

llio

n

RM

billion

RM

billion

SG

D b

illion

IDR

tri

llio

n

YoY

Maybank Malaysia

Loans

Maybank Singapore

Loans

Maybank Indonesia

Loans

(0.5)% +0.5% (1.7)% +0.1%

+7.2% +6.4% +7.0% +10.1%

RM

billion

11

521.4 513.4

Dec 16 Mar 17

121.9 124.4

163.5 159.5

15.9 18.5

Dec 16 Mar 17

CASA Fixed Deposits Others

12.5 12.9

32.0 29.4

1.1 1.3

Dec 16 Mar 17

46.0 43.7

73.3 74.3

Dec 16 Mar 17

115.7 124.4

163.5 159.5

14.9 18.5

Mar 16 Mar 17

9.3 12.9

35.4 29.4

1.0 1.3

Mar 16 Mar 17

42.9 43.7

72.3 74.3

Mar 16 Mar 17

491.5 513.4

Mar 16 Mar 17

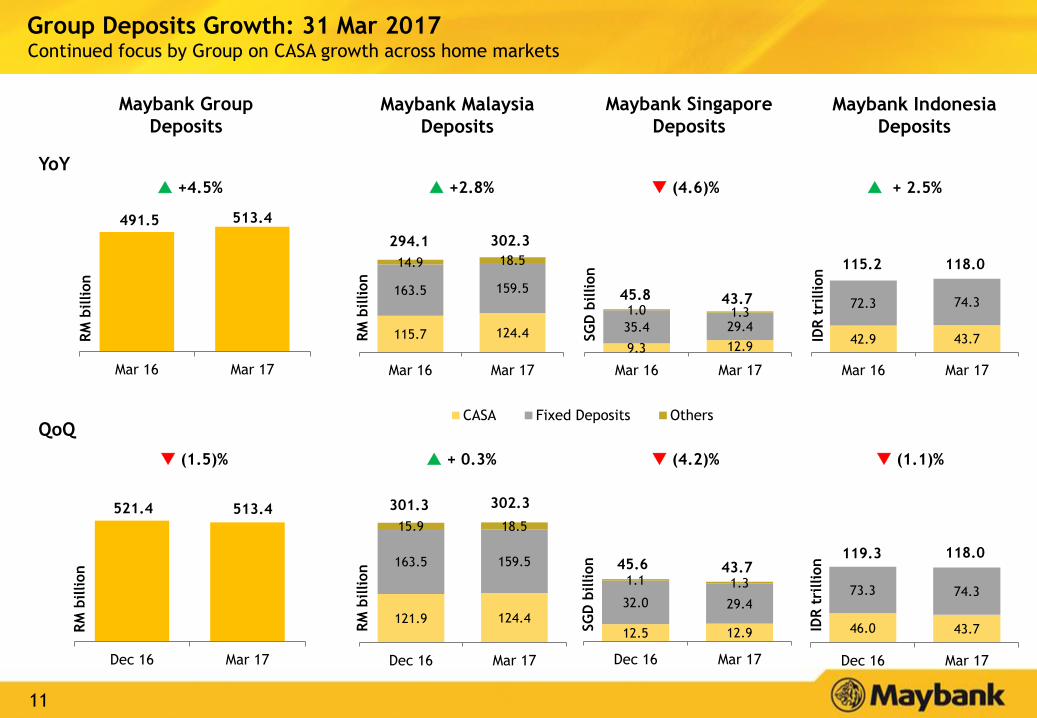

Group Deposits Growth: 31 Mar 2017Continued focus by Group on CASA growth across home markets

+ 0.3% (4.2)% (1.1)% (1.5)%

RM

billion

RM

billion

SG

D b

illion

IDR

tri

llio

n

302.3301.3

43.745.6118.0119.3

Maybank Group

Deposits

Maybank Malaysia

Deposits

Maybank Singapore

Deposits

Maybank Indonesia

Deposits

+2.8% (4.6)% + 2.5% +4.5%

RM

billion

RM

billion

SG

D b

illion

IDR

tri

llio

n

302.3294.1

43.745.8

118.0115.2

YoY

QoQ

12

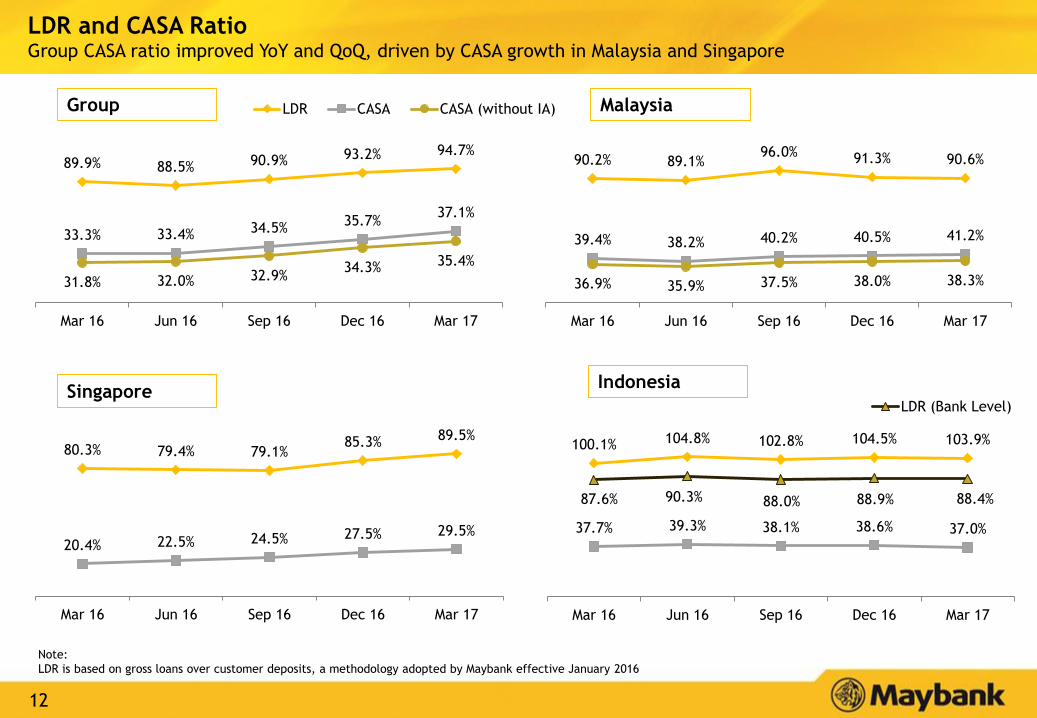

89.9% 88.5% 90.9% 93.2% 94.7%

33.3% 33.4% 34.5%35.7%

37.1%

31.8% 32.0% 32.9%34.3% 35.4%

25.0%

30.0%

35.0%

40.0%

45.0%

50.0%

Mar 16 Jun 16 Sep 16 Dec 16 Mar 17

LDR CASA CASA (without IA)

90.2% 89.1%96.0% 91.3% 90.6%

39.4% 38.2% 40.2% 40.5% 41.2%

36.9% 35.9% 37.5% 38.0% 38.3%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

Mar 16 Jun 16 Sep 16 Dec 16 Mar 17

LDR and CASA RatioGroup CASA ratio improved YoY and QoQ, driven by CASA growth in Malaysia and Singapore

SingaporeIndonesia

Group Malaysia

100.1% 104.8% 102.8% 104.5% 103.9%

37.7% 39.3% 38.1% 38.6% 37.0%

87.6% 90.3% 88.0% 88.9% 88.4%

Mar 16 Jun 16 Sep 16 Dec 16 Mar 17

LDR (Bank Level)

80.3% 79.4% 79.1%85.3% 89.5%

20.4% 22.5% 24.5% 27.5% 29.5%

Mar 16 Jun 16 Sep 16 Dec 16 Mar 17

Note:

LDR is based on gross loans over customer deposits, a methodology adopted by Maybank effective January 2016

13

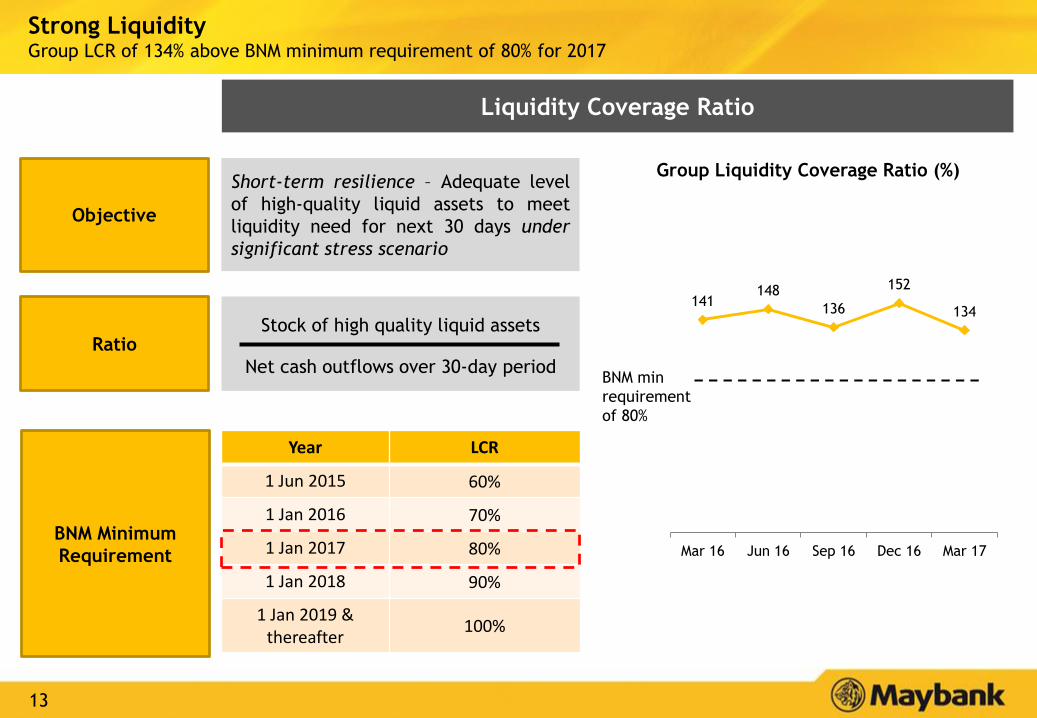

Strong LiquidityGroup LCR of 134% above BNM minimum requirement of 80% for 2017

Objective

Short-term resilience – Adequate level

of high-quality liquid assets to meet

liquidity need for next 30 days under

significant stress scenario

Stock of high quality liquid assets

Net cash outflows over 30-day period

Ratio

BNM Minimum

Requirement

Year LCR

1 Jun 2015 60%

1 Jan 2016 70%

1 Jan 2017 80%

1 Jan 2018 90%

1 Jan 2019 & thereafter

100%

141148

136

152

134

Mar 16 Jun 16 Sep 16 Dec 16 Mar 17

Group Liquidity Coverage Ratio (%)

Liquidity Coverage Ratio

BNM min

requirement

of 80%

14

865.1

981.7

370.3

615.7

542.5

1Q FY2016 2Q FY2016 3Q FY2016 4Q FY2016 1Q FY2017

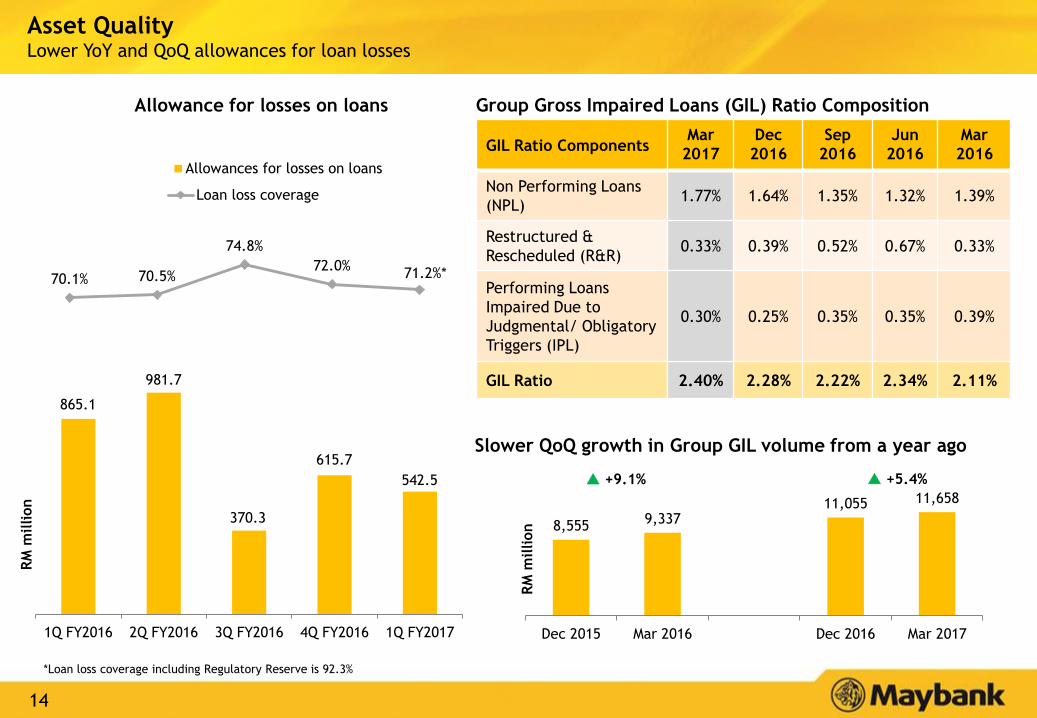

Allowances for losses on loans

70.1% 70.5%

74.8%

72.0%71.2%*

Loan loss coverage

Allowance for losses on loans

Asset QualityLower YoY and QoQ allowances for loan losses

RM

million

*Loan loss coverage including Regulatory Reserve is 92.3%

GIL Ratio ComponentsMar

2017

Dec

2016

Sep

2016

Jun

2016

Mar

2016

Non Performing Loans

(NPL)1.77% 1.64% 1.35% 1.32% 1.39%

Restructured &

Rescheduled (R&R)0.33% 0.39% 0.52% 0.67% 0.33%

Performing Loans

Impaired Due to

Judgmental/ Obligatory

Triggers (IPL)

0.30% 0.25% 0.35% 0.35% 0.39%

GIL Ratio 2.40% 2.28% 2.22% 2.34% 2.11%

Group Gross Impaired Loans (GIL) Ratio Composition

8,5559,337

11,055 11,658

Dec 2015 Mar 2016 Dec 2016 Mar 2017

Slower QoQ growth in Group GIL volume from a year ago

RM

million

+9.1% +5.4%

15

Mar 16 Jun 16 Sep 16 Dec 16 Mar 17

Gross Impaired Loans

Net Impaired Loans

1.28% 1.38%0.98%

1.30%1.68%

1.08% 1.16%0.76%

1.07%1.37%

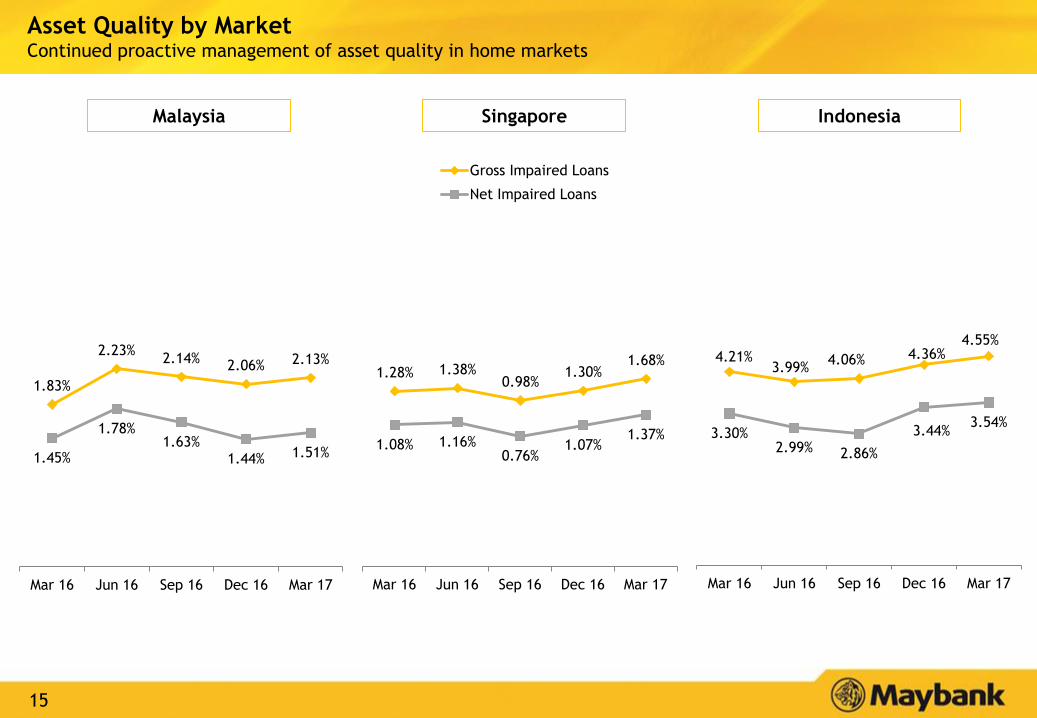

Asset Quality by MarketContinued proactive management of asset quality in home markets

4.21%3.99%

4.06% 4.36%4.55%

3.30%2.99% 2.86%

3.44%3.54%

Mar 16 Jun 16 Sep 16 Dec 16 Mar 17

1.83%

2.23%2.14%

2.06% 2.13%

1.45%

1.78%1.63%

1.44% 1.51%

Mar 16 Jun 16 Sep 16 Dec 16 Mar 17

Malaysia Singapore Indonesia

16

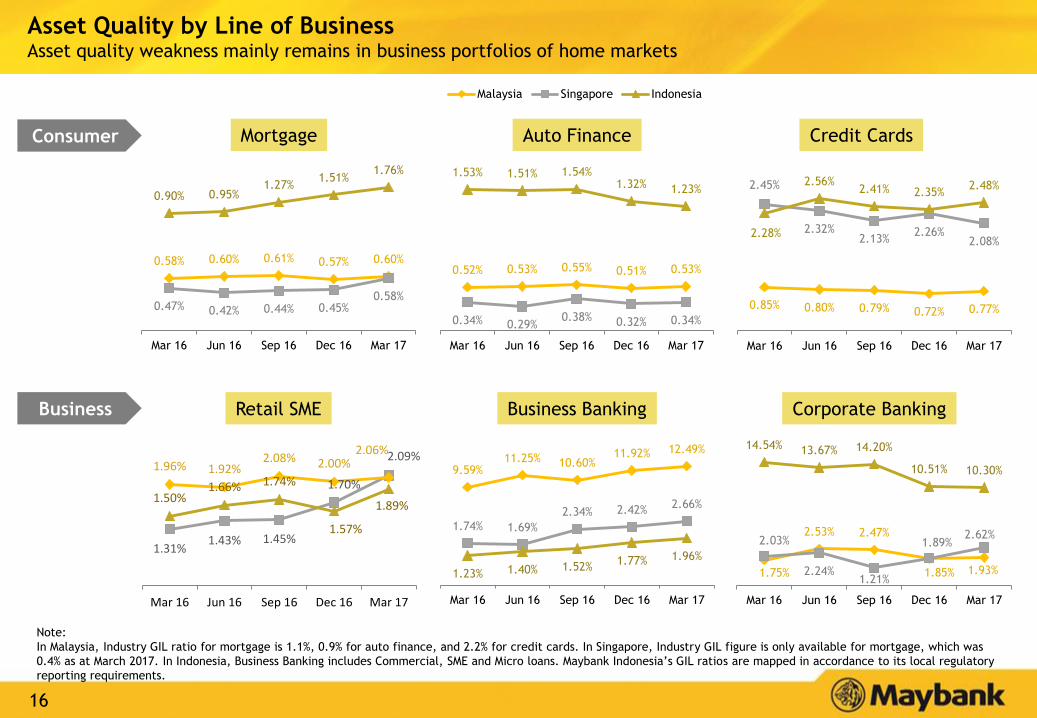

Asset Quality by Line of BusinessAsset quality weakness mainly remains in business portfolios of home markets

Mortgage Auto Finance Credit Cards

Retail SME Business Banking Corporate Banking

Consumer

Business

Note:

In Malaysia, Industry GIL ratio for mortgage is 1.1%, 0.9% for auto finance, and 2.2% for credit cards. In Singapore, Industry GIL figure is only available for mortgage, which was

0.4% as at March 2017. In Indonesia, Business Banking includes Commercial, SME and Micro loans. Maybank Indonesia’s GIL ratios are mapped in accordance to its local regulatory

reporting requirements.

0.58% 0.60% 0.61% 0.57% 0.60%

0.47% 0.42% 0.44% 0.45%0.58%

0.90% 0.95%1.27%

1.51%1.76%

-3.00%

-2.00%

-1.00%

0.00%

1.00%

2.00%

3.00%

0.00%

0.50%

1.00%

1.50%

2.00%

Mar 16 Jun 16 Sep 16 Dec 16 Mar 17

0.52% 0.53% 0.55% 0.51% 0.53%

0.34% 0.29%0.38% 0.32% 0.34%

1.53% 1.51% 1.54%1.32% 1.23%

-1.00%

-0.50%

0.00%

0.50%

1.00%

1.50%

2.00%

0.00%

0.50%

1.00%

1.50%

2.00%

Mar 16 Jun 16 Sep 16 Dec 16 Mar 17

Malaysia Singapore Indonesia

0.85% 0.80% 0.79% 0.72% 0.77%

2.45%

2.32%2.13%

2.26%2.08%

2.28%

2.56%2.41% 2.35%

2.48%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

Mar 16 Jun 16 Sep 16 Dec 16 Mar 17

1.74% 1.69%

2.34% 2.42%2.66%

1.23% 1.40% 1.52%1.77% 1.96%

9.59%11.25% 10.60%

11.92% 12.49%

-4.00%

1.00%

6.00%

11.00%

16.00%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

Mar 16 Jun 16 Sep 16 Dec 16 Mar 17

1.75%

2.53% 2.47%

1.85% 1.93%

2.03%

2.24%1.21%

1.89%2.62%

14.54% 13.67% 14.20%

10.51% 10.30%

-6.00%

-1.00%

4.00%

9.00%

14.00%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

10.00%

Mar 16 Jun 16 Sep 16 Dec 16 Mar 17

1.31%1.43% 1.45%

1.70%

2.09%

1.50%1.66% 1.74%

1.57%

1.89%

1.96% 1.92%2.08% 2.00%

2.06%

Mar 16 Jun 16 Sep 16 Dec 16 Mar 17

17

40%

3%

46%

11%

Normal

Special Mention Account

Watchlist

GIL

82% comes

from

supporting

upstream

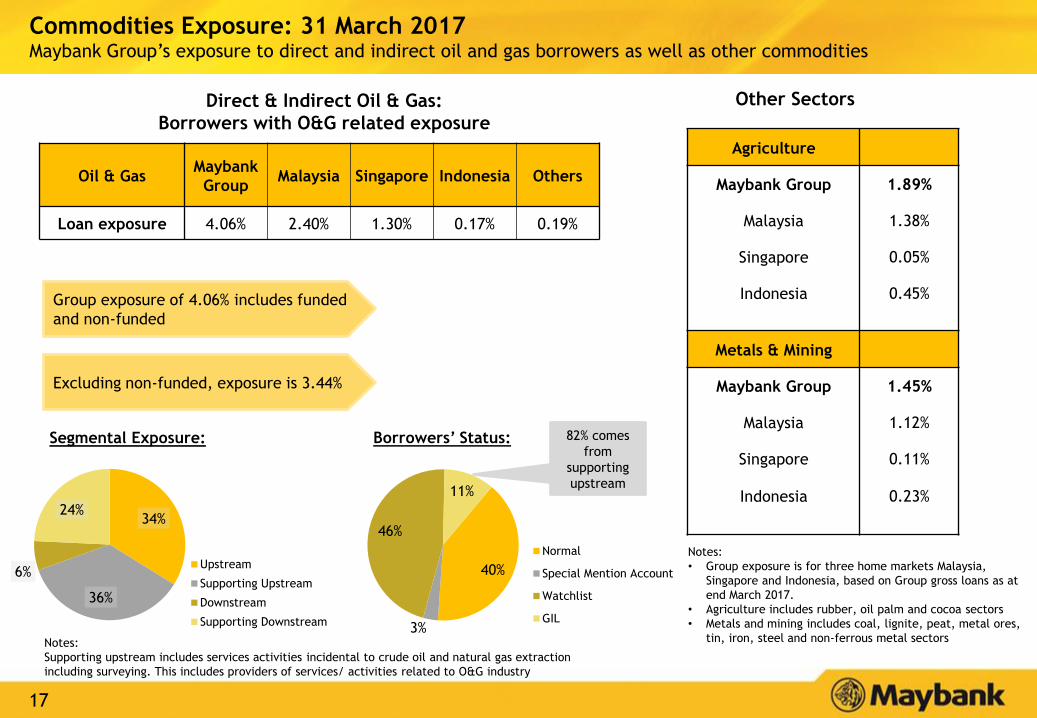

Commodities Exposure: 31 March 2017Maybank Group’s exposure to direct and indirect oil and gas borrowers as well as other commodities

Notes:

• Group exposure is for three home markets Malaysia,

Singapore and Indonesia, based on Group gross loans as at

end March 2017.

• Agriculture includes rubber, oil palm and cocoa sectors

• Metals and mining includes coal, lignite, peat, metal ores,

tin, iron, steel and non-ferrous metal sectors

Agriculture

Maybank Group 1.89%

Malaysia 1.38%

Singapore 0.05%

Indonesia 0.45%

Metals & Mining

Maybank Group 1.45%

Malaysia 1.12%

Singapore 0.11%

Indonesia 0.23%

Oil & GasMaybank

GroupMalaysia Singapore Indonesia Others

Loan exposure 4.06% 2.40% 1.30% 0.17% 0.19%

Borrowers’ Status:Segmental Exposure:

Direct & Indirect Oil & Gas:

Borrowers with O&G related exposure

Other Sectors

Group exposure of 4.06% includes funded

and non-funded

34%

36%

6%

24%

Upstream

Supporting Upstream

Downstream

Supporting Downstream

Notes:

Supporting upstream includes services activities incidental to crude oil and natural gas extraction

including surveying. This includes providers of services/ activities related to O&G industry

Excluding non-funded, exposure is 3.44%

18

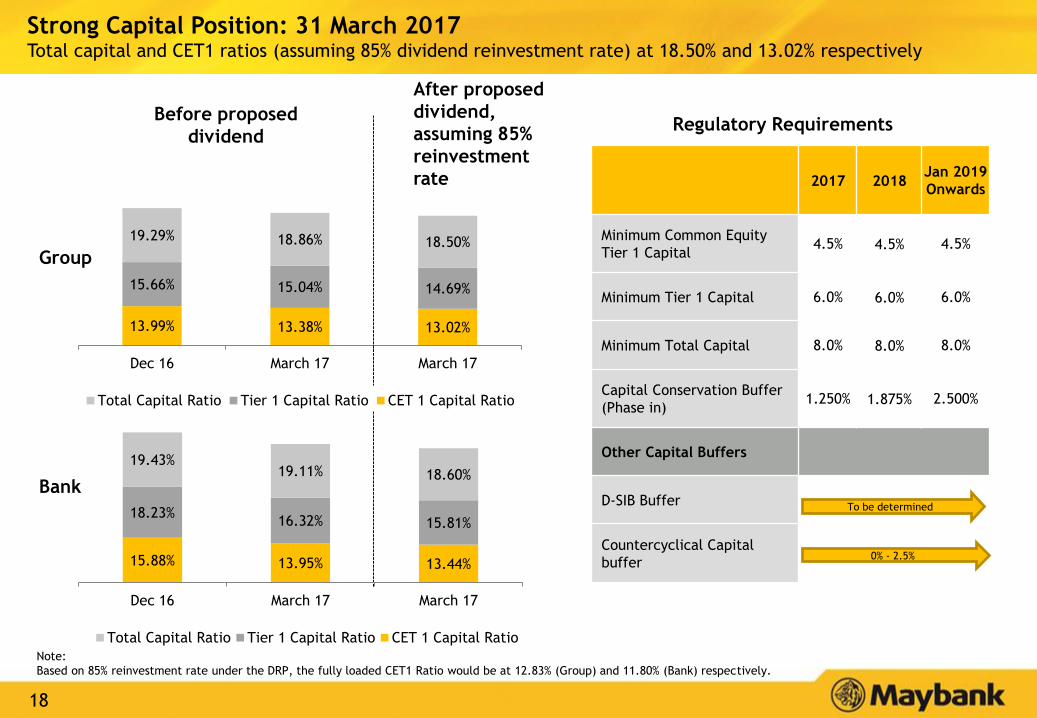

13.99% 13.38% 13.02%

15.66% 15.04% 14.69%

19.29% 18.86% 18.50%

Dec 16 March 17 March 17

Total Capital Ratio Tier 1 Capital Ratio CET 1 Capital Ratio

Group

Bank

Strong Capital Position: 31 March 2017Total capital and CET1 ratios (assuming 85% dividend reinvestment rate) at 18.50% and 13.02% respectively

Before proposed

dividend

After proposed

dividend,

assuming 85%

reinvestment

rate 2017 2018Jan 2019

Onwards

Minimum Common Equity

Tier 1 Capital4.5% 4.5% 4.5%

Minimum Tier 1 Capital 6.0% 6.0% 6.0%

Minimum Total Capital 8.0% 8.0% 8.0%

Capital Conservation Buffer

(Phase in)1.250% 1.875% 2.500%

Other Capital Buffers

D-SIB Buffer

Countercyclical Capital

buffer

Regulatory Requirements

To be determined

0% - 2.5%

Note:

Based on 85% reinvestment rate under the DRP, the fully loaded CET1 Ratio would be at 12.83% (Group) and 11.80% (Bank) respectively.

15.88% 13.95% 13.44%

18.23%16.32% 15.81%

19.43%19.11% 18.60%

Dec 16 March 17 March 17

Total Capital Ratio Tier 1 Capital Ratio CET 1 Capital Ratio

19

Table of Contents

Executive Summary 2

Results Overview 5

Prospects & Outlook 20

Appendix:

1. Financial Performance 23

2. Community Financial Services 31

3. Global Banking 36

4. Maybank Singapore 41

5. Maybank Indonesia 45

6. Other segments 50

7. Affiliates 55

Financial Results: 1Q FY2017 ended 31 March 2017

20

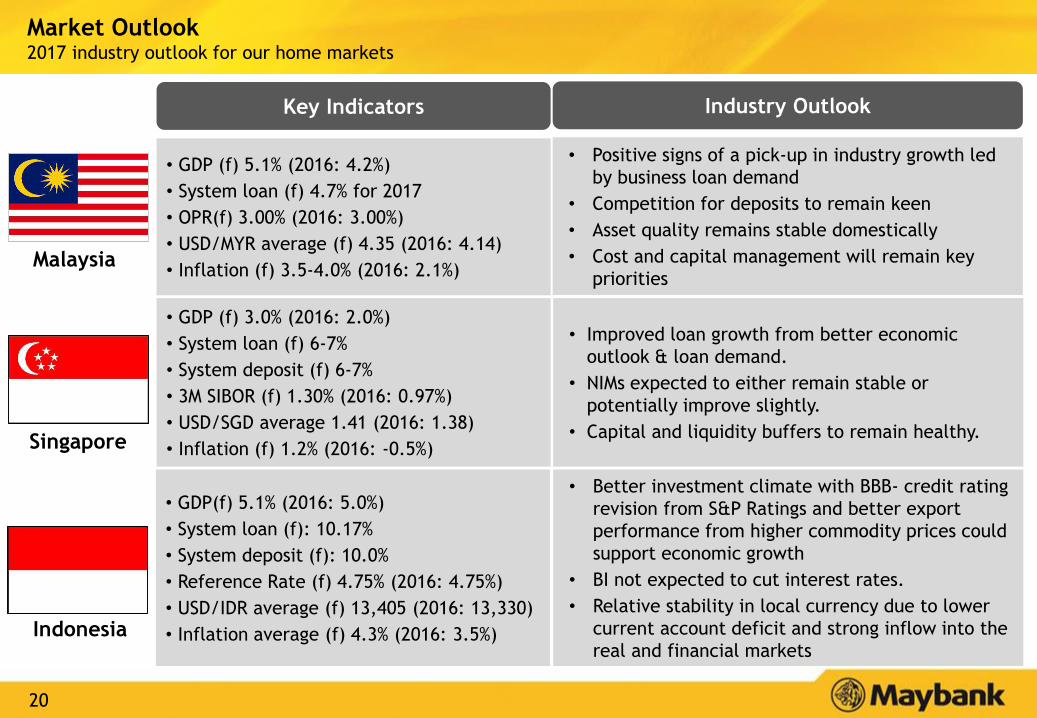

Market Outlook2017 industry outlook for our home markets

Key Indicators Industry Outlook

Singapore

Malaysia

Indonesia

• GDP (f) 5.1% (2016: 4.2%)

• System loan (f) 4.7% for 2017

• OPR(f) 3.00% (2016: 3.00%)

• USD/MYR average (f) 4.35 (2016: 4.14)

• Inflation (f) 3.5-4.0% (2016: 2.1%)

• GDP (f) 3.0% (2016: 2.0%)

• System loan (f) 6-7%

• System deposit (f) 6-7%

• 3M SIBOR (f) 1.30% (2016: 0.97%)

• USD/SGD average 1.41 (2016: 1.38)

• Inflation (f) 1.2% (2016: -0.5%)

• GDP(f) 5.1% (2016: 5.0%)

• System loan (f): 10.17%

• System deposit (f): 10.0%

• Reference Rate (f) 4.75% (2016: 4.75%)

• USD/IDR average (f) 13,405 (2016: 13,330)

• Inflation average (f) 4.3% (2016: 3.5%)

• Better investment climate with BBB- credit rating

revision from S&P Ratings and better export

performance from higher commodity prices could

support economic growth

• BI not expected to cut interest rates.

• Relative stability in local currency due to lower

current account deficit and strong inflow into the

real and financial markets

• Improved loan growth from better economic

outlook & loan demand.

• NIMs expected to either remain stable or

potentially improve slightly.

• Capital and liquidity buffers to remain healthy.

• Positive signs of a pick-up in industry growth led

by business loan demand

• Competition for deposits to remain keen

• Asset quality remains stable domestically

• Cost and capital management will remain key

priorities

21

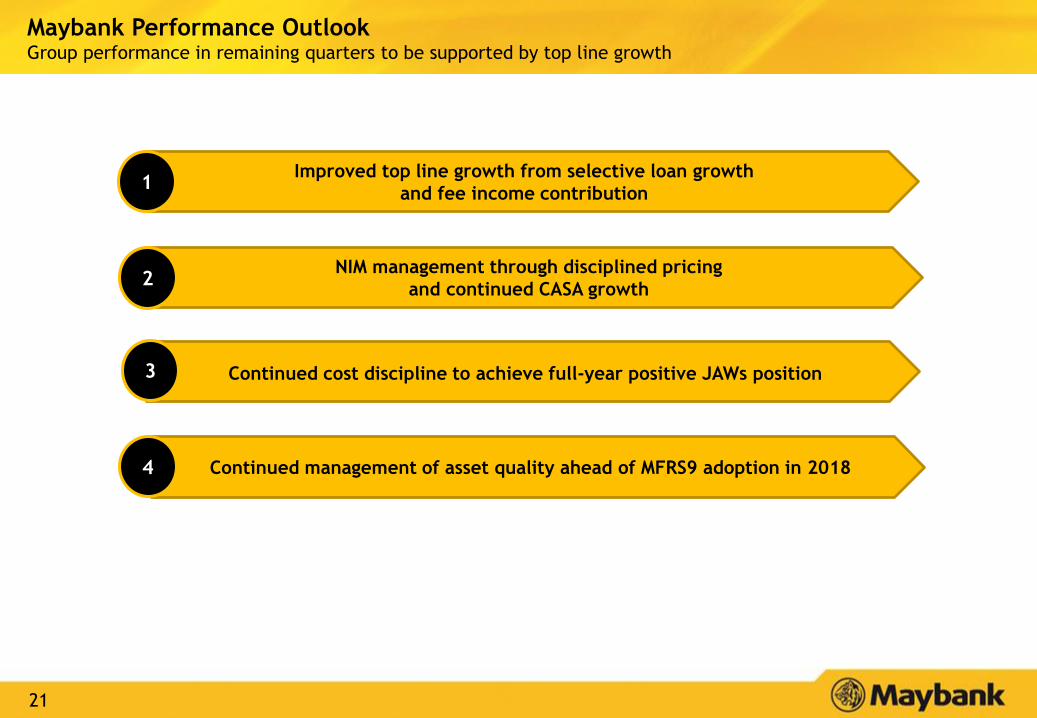

Continued cost discipline to achieve full-year positive JAWs position

NIM management through disciplined pricing

and continued CASA growth

Continued management of asset quality ahead of MFRS9 adoption in 2018

Maybank Performance OutlookGroup performance in remaining quarters to be supported by top line growth

2

4

Improved top line growth from selective loan growth

and fee income contribution1

3

22

Table of Contents

Executive Summary 2

Results Overview 5

Prospects & Outlook 20

Appendix:

1. Financial Performance 23

2. Community Financial Services 31

3. Global Banking 36

4. Maybank Singapore 41

5. Maybank Indonesia 45

6. Other segments 50

7. Affiliates 55

Financial Results: 1Q FY2017 ended 31 March 2017

23

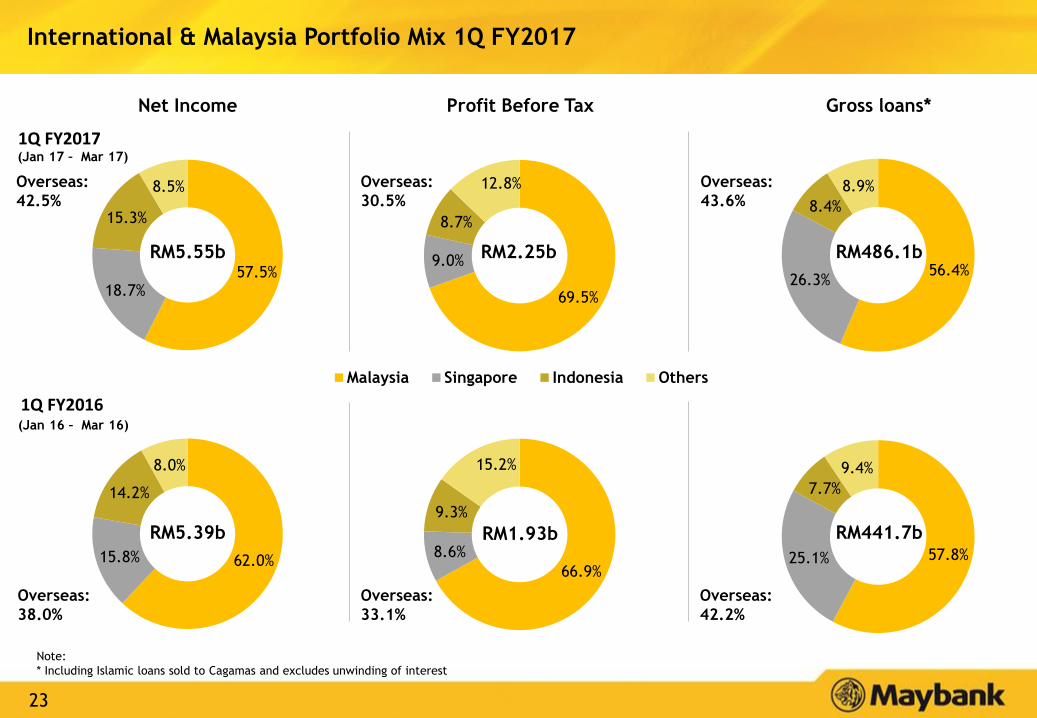

57.8%25.1%

7.7%

9.4%

66.9%

8.6%

9.3%

15.2%

57.5%18.7%

15.3%

8.5%

69.5%

9.0%

8.7%

12.8%

Malaysia Singapore Indonesia Others

International & Malaysia Portfolio Mix 1Q FY2017

Overseas:

42.2%

1Q FY2016

Net Income Profit Before Tax

1Q FY2017

Overseas:

38.0%

Overseas:

33.1%

Gross loans*

(Jan 16 – Mar 16)

56.4%26.3%

8.4%

8.9%Overseas:

43.6%

Overseas:

42.5%

Overseas:

30.5%

(Jan 17 – Mar 17)

62.0%15.8%

14.2%

8.0%

RM2.25b RM486.1b

RM1.93b RM441.7bRM5.39b

RM5.55b

Note:

* Including Islamic loans sold to Cagamas and excludes unwinding of interest

24

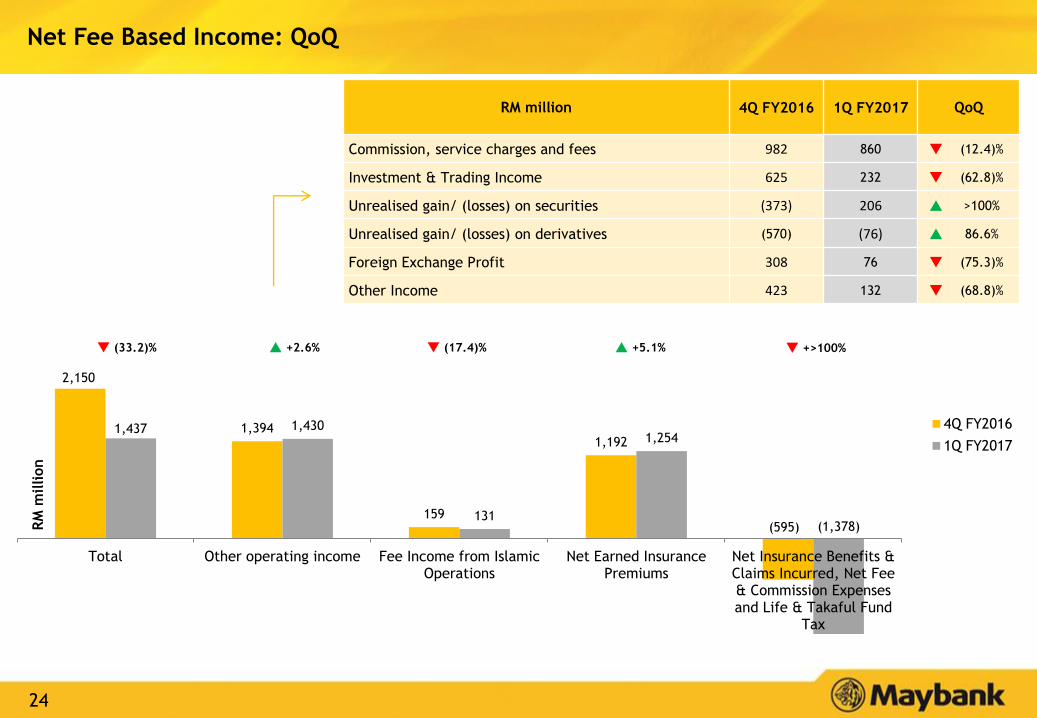

2,150

1,394

159

1,192

(595)

1,437 1,430

131

1,254

(1,378)

Total Other operating income Fee Income from IslamicOperations

Net Earned InsurancePremiums

Net Insurance Benefits &Claims Incurred, Net Fee& Commission Expensesand Life & Takaful Fund

Tax

4Q FY2016

1Q FY2017

RM

million

RM million 4Q FY2016 1Q FY2017 QoQ

Commission, service charges and fees 982 860 (12.4)%

Investment & Trading Income 625 232 (62.8)%

Unrealised gain/ (losses) on securities (373) 206 >100%

Unrealised gain/ (losses) on derivatives (570) (76) 86.6%

Foreign Exchange Profit 308 76 (75.3)%

Other Income 423 132 (68.8)%

Net Fee Based Income: QoQ

(33.2)% +2.6% (17.4)% +5.1% +>100%

25

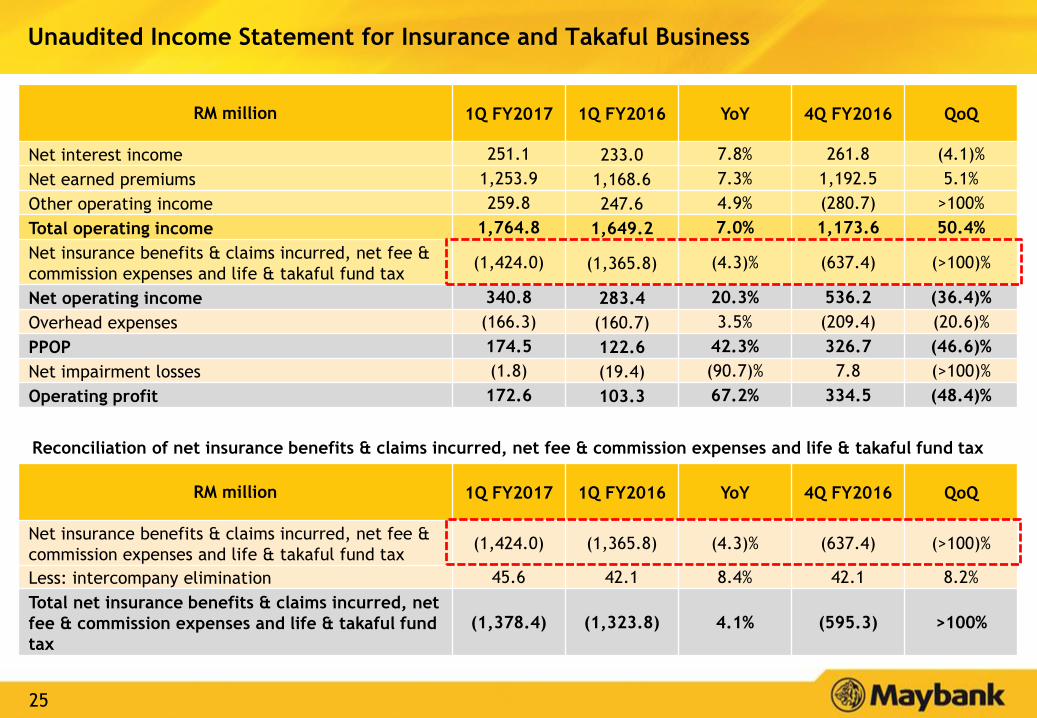

Unaudited Income Statement for Insurance and Takaful Business

RM million 1Q FY2017 1Q FY2016 YoY 4Q FY2016 QoQ

Net interest income 251.1 233.0 7.8% 261.8 (4.1)%

Net earned premiums 1,253.9 1,168.6 7.3% 1,192.5 5.1%

Other operating income 259.8 247.6 4.9% (280.7) >100%

Total operating income 1,764.8 1,649.2 7.0% 1,173.6 50.4%

Net insurance benefits & claims incurred, net fee &

commission expenses and life & takaful fund tax(1,424.0) (1,365.8) (4.3)% (637.4) (>100)%

Net operating income 340.8 283.4 20.3% 536.2 (36.4)%

Overhead expenses (166.3) (160.7) 3.5% (209.4) (20.6)%

PPOP 174.5 122.6 42.3% 326.7 (46.6)%

Net impairment losses (1.8) (19.4) (90.7)% 7.8 (>100)%

Operating profit 172.6 103.3 67.2% 334.5 (48.4)%

RM million 1Q FY2017 1Q FY2016 YoY 4Q FY2016 QoQ

Net insurance benefits & claims incurred, net fee &

commission expenses and life & takaful fund tax(1,424.0) (1,365.8) (4.3)% (637.4) (>100)%

Less: intercompany elimination 45.6 42.1 8.4% 42.1 8.2%

Total net insurance benefits & claims incurred, net

fee & commission expenses and life & takaful fund

tax

(1,378.4) (1,323.8) 4.1% (595.3) >100%

Reconciliation of net insurance benefits & claims incurred, net fee & commission expenses and life & takaful fund tax

26

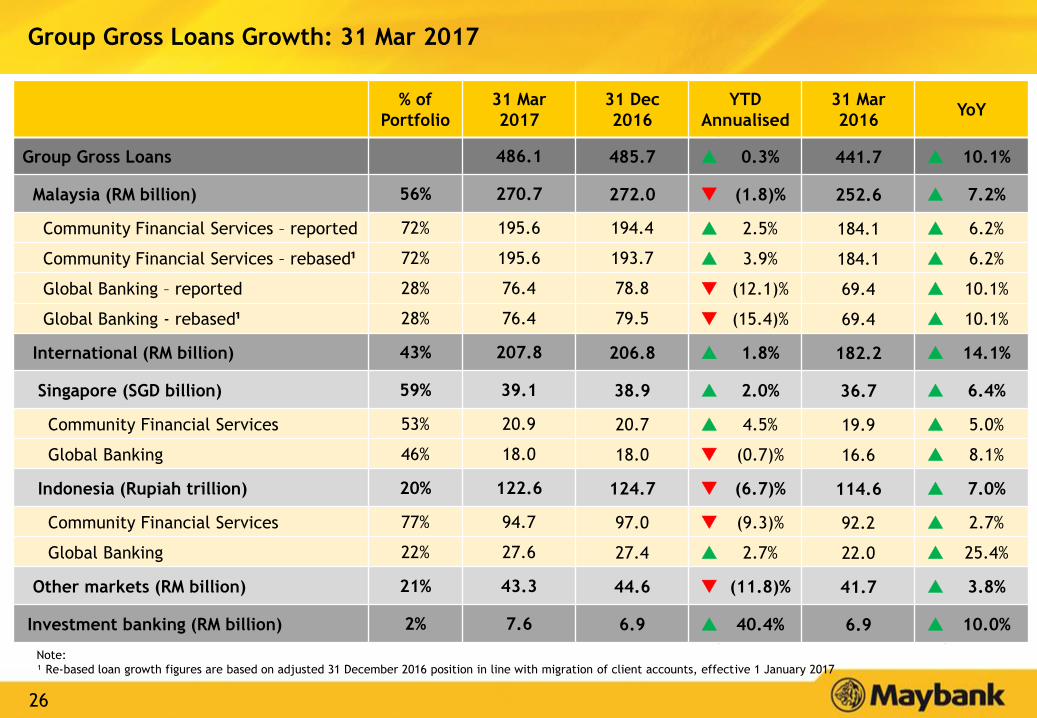

Group Gross Loans Growth: 31 Mar 2017

% of

Portfolio

31 Mar

2017

31 Dec

2016

YTD

Annualised

31 Mar

2016YoY

Group Gross Loans 486.1 485.7 0.3% 441.7 10.1%

Malaysia (RM billion) 56% 270.7 272.0 (1.8)% 252.6 7.2%

Community Financial Services – reported 72% 195.6 194.4 2.5% 184.1 6.2%

Community Financial Services – rebased¹ 72% 195.6 193.7 3.9% 184.1 6.2%

Global Banking – reported 28% 76.4 78.8 (12.1)% 69.4 10.1%

Global Banking - rebased¹ 28% 76.4 79.5 (15.4)% 69.4 10.1%

International (RM billion) 43% 207.8 206.8 1.8% 182.2 14.1%

Singapore (SGD billion) 59% 39.1 38.9 2.0% 36.7 6.4%

Community Financial Services 53% 20.9 20.7 4.5% 19.9 5.0%

Global Banking 46% 18.0 18.0 (0.7)% 16.6 8.1%

Indonesia (Rupiah trillion) 20% 122.6 124.7 (6.7)% 114.6 7.0%

Community Financial Services 77% 94.7 97.0 (9.3)% 92.2 2.7%

Global Banking 22% 27.6 27.4 2.7% 22.0 25.4%

Other markets (RM billion) 21% 43.3 44.6 (11.8)% 41.7 3.8%

Investment banking (RM billion) 2% 7.6 6.9 40.4% 6.9 10.0%

Note:

¹ Re-based loan growth figures are based on adjusted 31 December 2016 position in line with migration of client accounts, effective 1 January 2017

27

RM billion% of

Portfolio

31 Mar

2017

31 Dec

2016

YTD

Annualised

31 Mar

2016YoY

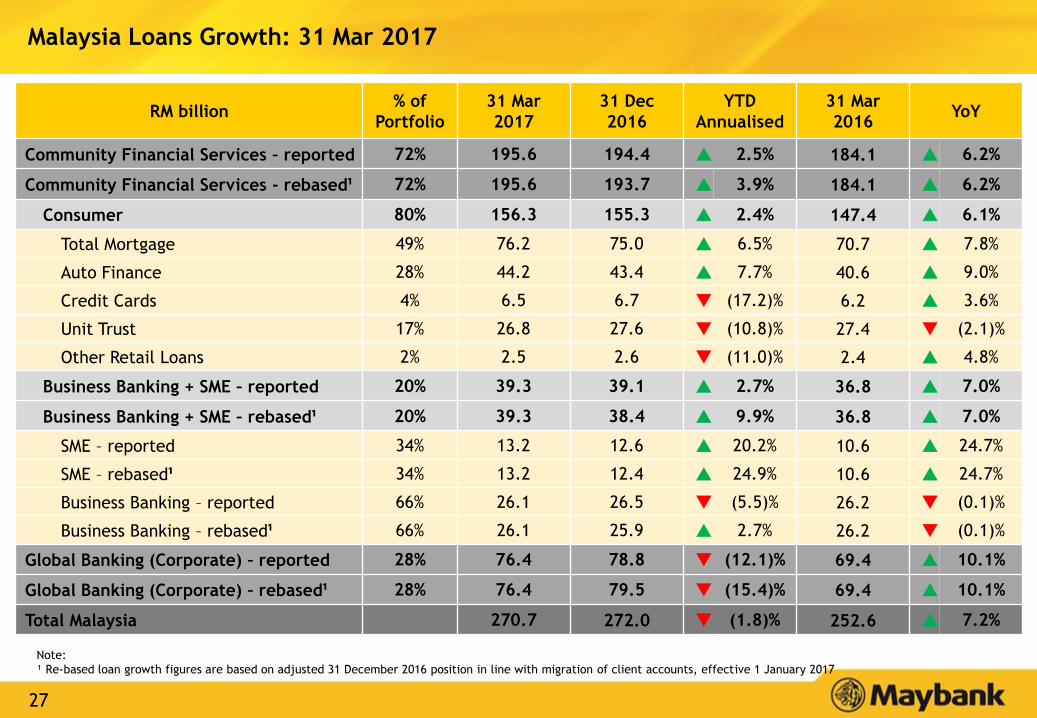

Community Financial Services – reported 72% 195.6 194.4 2.5% 184.1 6.2%

Community Financial Services - rebased¹ 72% 195.6 193.7 3.9% 184.1 6.2%

Consumer 80% 156.3 155.3 2.4% 147.4 6.1%

Total Mortgage 49% 76.2 75.0 6.5% 70.7 7.8%

Auto Finance 28% 44.2 43.4 7.7% 40.6 9.0%

Credit Cards 4% 6.5 6.7 (17.2)% 6.2 3.6%

Unit Trust 17% 26.8 27.6 (10.8)% 27.4 (2.1)%

Other Retail Loans 2% 2.5 2.6 (11.0)% 2.4 4.8%

Business Banking + SME – reported 20% 39.3 39.1 2.7% 36.8 7.0%

Business Banking + SME – rebased¹ 20% 39.3 38.4 9.9% 36.8 7.0%

SME – reported 34% 13.2 12.6 20.2% 10.6 24.7%

SME – rebased¹ 34% 13.2 12.4 24.9% 10.6 24.7%

Business Banking – reported 66% 26.1 26.5 (5.5)% 26.2 (0.1)%

Business Banking – rebased¹ 66% 26.1 25.9 2.7% 26.2 (0.1)%

Global Banking (Corporate) – reported 28% 76.4 78.8 (12.1)% 69.4 10.1%

Global Banking (Corporate) – rebased¹ 28% 76.4 79.5 (15.4)% 69.4 10.1%

Total Malaysia 270.7 272.0 (1.8)% 252.6 7.2%

Malaysia Loans Growth: 31 Mar 2017

Note:

¹ Re-based loan growth figures are based on adjusted 31 December 2016 position in line with migration of client accounts, effective 1 January 2017

28

Group Deposits Growth: 31 Mar 2017

% of

Portfolio

31 Mar

2017

31 Dec

2016

YTD

Annualised

31 Mar

2016YoY

Group Gross Deposits 513.4 521.4 (6.1)% 491.5 4.5%

Malaysia (RM billion) 59% 302.3 301.3 1.4% 294.1 2.8%

Savings Deposits 14% 41.2 38.8 25.5% 41.4 (0.4)%

Current Accounts 28% 83.2 83.2 0.1% 74.3 11.9%

Fixed Deposits 53% 159.5 163.5 (9.9)% 163.5 (2.4)%

Others 6% 18.5 15.9 64.9% 14.9 23.6%

International 41% 213.0 221.6 (15.4)% 198.9 7.1%

Singapore (SGD billion) 65% 43.7 45.6 (16.9)% 45.8 (4.6)%

Savings Deposits 13% 5.8 5.7 3.0% 4.3 35.3%

Current Accounts 16% 7.1 6.8 18.9% 5.1 40.1%

Fixed Deposits 67% 29.4 32.0 (31.8)% 35.4 (16.9)%

Others 3% 1.3 1.1 94.1% 1.0 35.4%

Indonesia (Rupiah trillion) 18% 118.0 119.3 (4.5)% 115.2 2.5%

Savings Deposits 21% 24.8 25.6 (12.5)% 25.6 (2.9)%

Current Accounts 16% 18.9 20.4 (30.0)% 17.3 9.2%

Fixed Deposits 63% 74.3 73.3 5.5% 72.3 2.7%

29

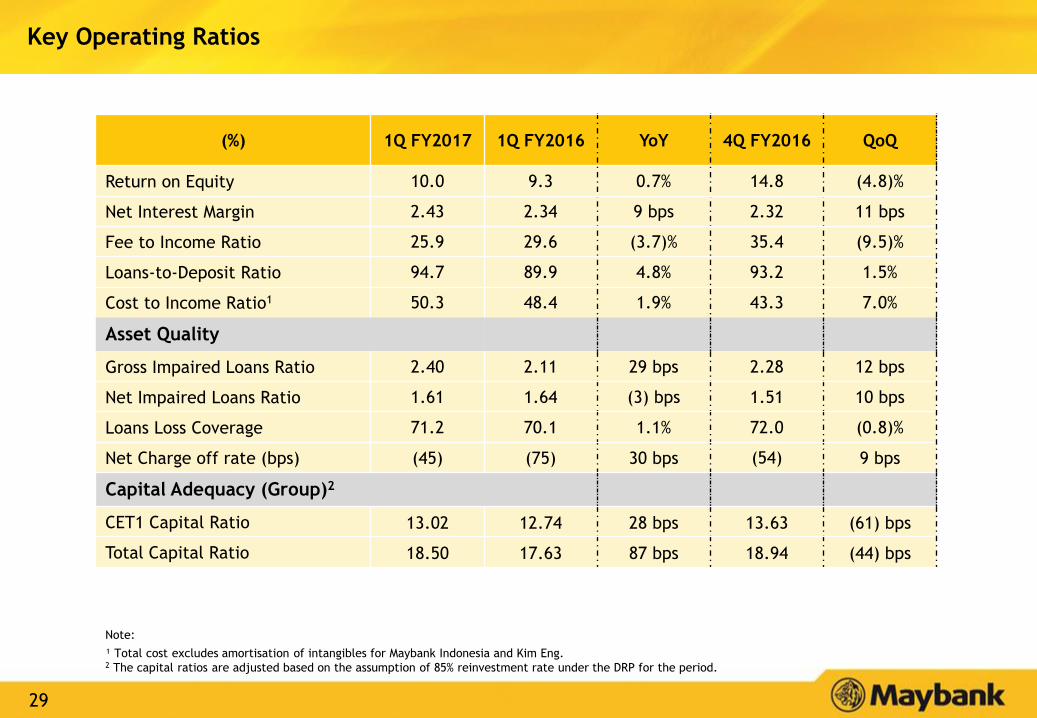

Key Operating Ratios

(%) 1Q FY2017 1Q FY2016 YoY 4Q FY2016 QoQ

Return on Equity 10.0 9.3 0.7% 14.8 (4.8)%

Net Interest Margin 2.43 2.34 9 bps 2.32 11 bps

Fee to Income Ratio 25.9 29.6 (3.7)% 35.4 (9.5)%

Loans-to-Deposit Ratio 94.7 89.9 4.8% 93.2 1.5%

Cost to Income Ratio1 50.3 48.4 1.9% 43.3 7.0%

Asset Quality

Gross Impaired Loans Ratio 2.40 2.11 29 bps 2.28 12 bps

Net Impaired Loans Ratio 1.61 1.64 (3) bps 1.51 10 bps

Loans Loss Coverage 71.2 70.1 1.1% 72.0 (0.8)%

Net Charge off rate (bps) (45) (75) 30 bps (54) 9 bps

Capital Adequacy (Group)2

CET1 Capital Ratio 13.02 12.74 28 bps 13.63 (61) bps

Total Capital Ratio 18.50 17.63 87 bps 18.94 (44) bps

Note:

¹ Total cost excludes amortisation of intangibles for Maybank Indonesia and Kim Eng.2 The capital ratios are adjusted based on the assumption of 85% reinvestment rate under the DRP for the period.

30

Table of Contents

Executive Summary 2

Results Overview 5

Prospects & Outlook 20

Appendix:

1. Financial Performance 23

2. Community Financial Services 31

3. Global Banking 36

4. Maybank Singapore 41

5. Maybank Indonesia 45

6. Other segments 50

7. Affiliates 55

Financial Results: 1Q FY2017 ended 31 March 2017

31

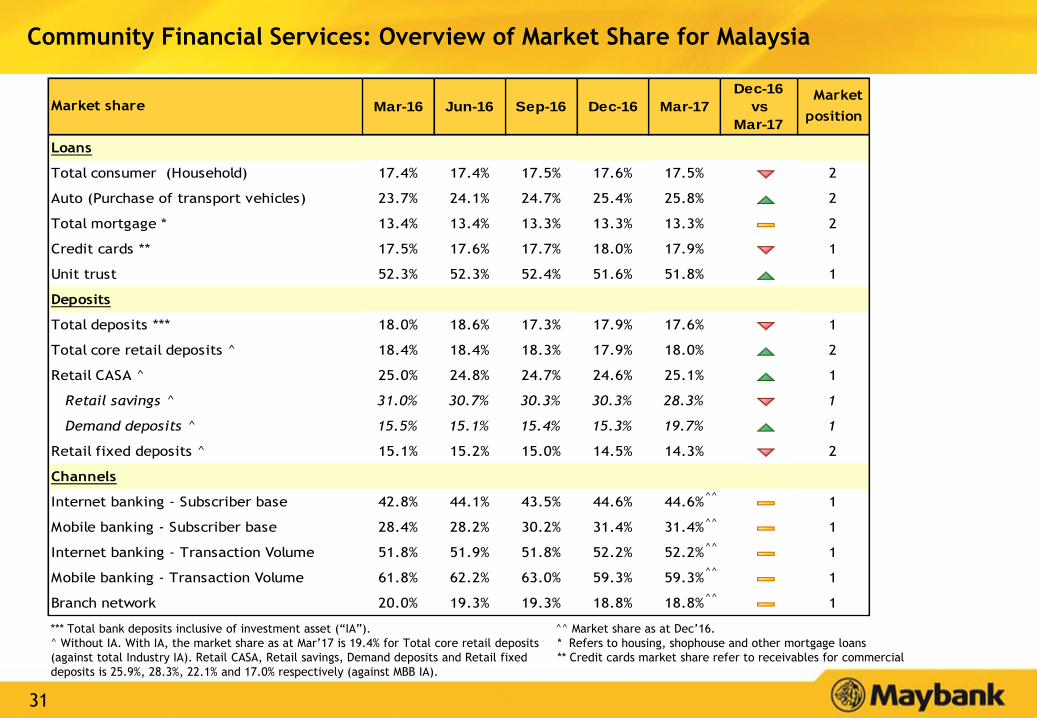

Community Financial Services: Overview of Market Share for Malaysia

Loans

Total consumer (Household) 17.4% 17.4% 17.5% 17.6% 17.5% # 2

Auto (Purchase of transport vehicles) 23.7% 24.1% 24.7% 25.4% 25.8% # 2

Total mortgage * 13.4% 13.4% 13.3% 13.3% 13.3% # 2

Credit cards ** 17.5% 17.6% 17.7% 18.0% 17.9% # 1

Unit trust 52.3% 52.3% 52.4% 51.6% 51.8% # 1

Deposits

Total deposits *** 18.0% 18.6% 17.3% 17.9% 17.6% # 1

Total core retail deposits ^ 18.4% 18.4% 18.3% 17.9% 18.0% # 2

Retail CASA ^ 25.0% 24.8% 24.7% 24.6% 25.1% # 1

Retail savings ^ 31.0% 30.7% 30.3% 30.3% 28.3% # 1

Demand deposits ^ 15.5% 15.1% 15.4% 15.3% 19.7% # 1

Retail fixed deposits ^ 15.1% 15.2% 15.0% 14.5% 14.3% # 2

Channels

Internet banking - Subscriber base 42.8% 44.1% 43.5% 44.6% 44.6% # 1

Mobile banking - Subscriber base 28.4% 28.2% 30.2% 31.4% 31.4% # 1

Internet banking - Transaction Volume 51.8% 51.9% 51.8% 52.2% 52.2% # 1

Mobile banking - Transaction Volume 61.8% 62.2% 63.0% 59.3% 59.3% # 1

Branch network 20.0% 19.3% 19.3% 18.8% 18.8% # 1

Dec-16

vs

Mar-17

Market

positionMar-16 Dec-16 Mar-17Sep-16Market share Jun-16

*** Total bank deposits inclusive of investment asset (“IA”).

^ Without IA. With IA, the market share as at Mar’17 is 19.4% for Total core retail deposits

(against total Industry IA). Retail CASA, Retail savings, Demand deposits and Retail fixed

deposits is 25.9%, 28.3%, 22.1% and 17.0% respectively (against MBB IA).

^^ Market share as at Dec’16.

* Refers to housing, shophouse and other mortgage loans

** Credit cards market share refer to receivables for commercial

^^

^^

^^

^^

^^

32

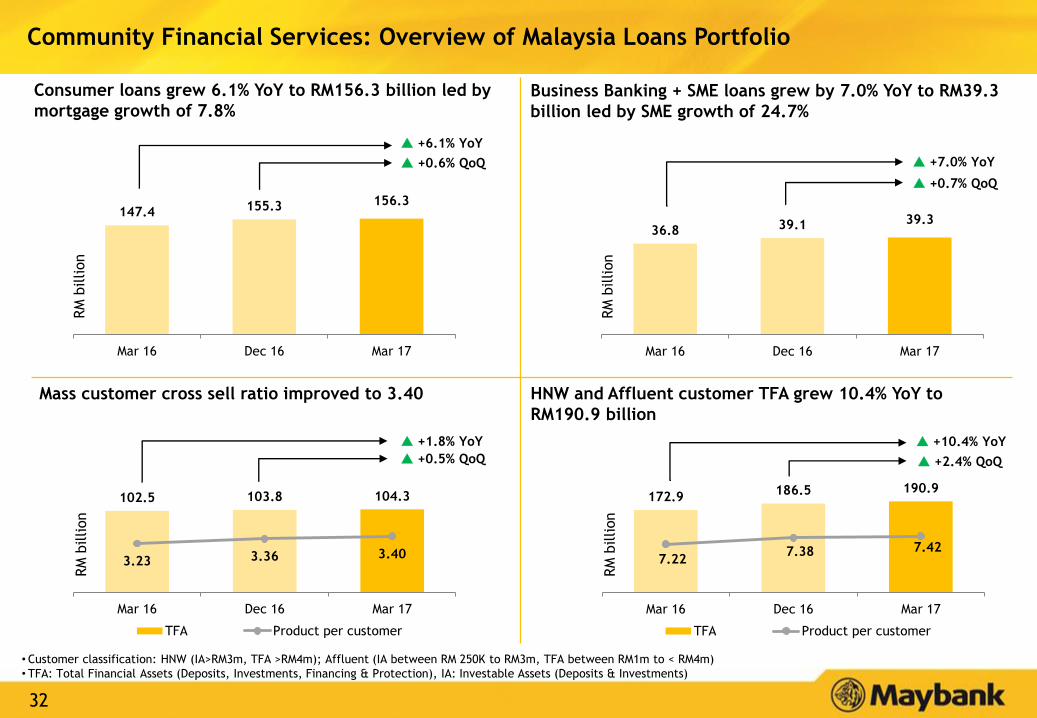

Community Financial Services: Overview of Malaysia Loans Portfolio

172.9186.5 190.9

7.227.38 7.42

Mar 16 Dec 16 Mar 17

TFA Product per customer

102.5 103.8 104.3

3.23 3.36 3.40

Mar 16 Dec 16 Mar 17

TFA Product per customer

36.8 39.1 39.3

0

10

20

30

40

50

60

Mar 16 Dec 16 Mar 17

147.4 155.3 156.3

020406080

100120140160180200

Mar 16 Dec 16 Mar 17

+6.1% YoY

Consumer loans grew 6.1% YoY to RM156.3 billion led by

mortgage growth of 7.8%

• Customer classification: HNW (IA>RM3m, TFA >RM4m); Affluent (IA between RM 250K to RM3m, TFA between RM1m to < RM4m)

• TFA: Total Financial Assets (Deposits, Investments, Financing & Protection), IA: Investable Assets (Deposits & Investments)

+0.6% QoQ

HNW and Affluent customer TFA grew 10.4% YoY to

RM190.9 billion

Mass customer cross sell ratio improved to 3.40

RM

billion

RM

billion

+7.0% YoY

+0.7% QoQ

RM

billion

+1.8% YoY

RM

billion

+10.4% YoY

+0.5% QoQ +2.4% QoQ

Business Banking + SME loans grew by 7.0% YoY to RM39.3

billion led by SME growth of 24.7%

33

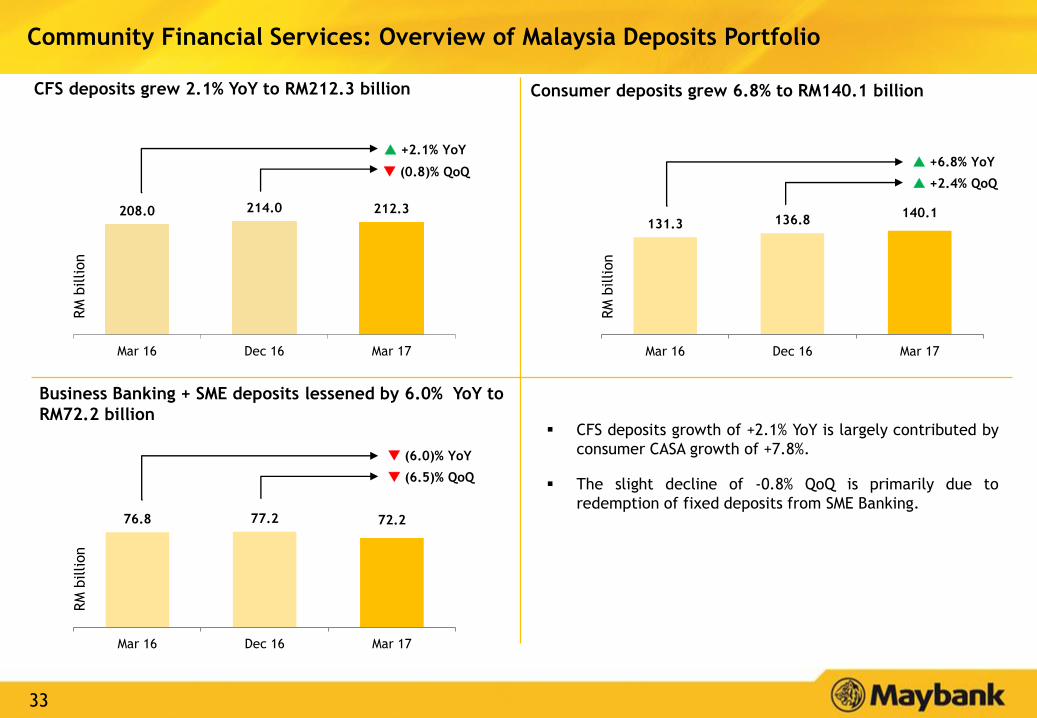

Community Financial Services: Overview of Malaysia Deposits Portfolio

208.0 214.0 212.3

0

50

100

150

200

250

Mar 16 Dec 16 Mar 17

(0.8)% QoQ

131.3 136.8140.1

020406080

100120140160180200

Mar 16 Dec 16 Mar 17

+2.1% YoY

RM

billion

RM

billion

+6.8% YoY

+2.4% QoQ

CFS deposits growth of +2.1% YoY is largely contributed by

consumer CASA growth of +7.8%.

The slight decline of -0.8% QoQ is primarily due to

redemption of fixed deposits from SME Banking.76.8 77.2 72.2

0

20

40

60

80

100

120

Mar 16 Dec 16 Mar 17

(6.0)% YoY

(6.5)% QoQ

RM

billion

CFS deposits grew 2.1% YoY to RM212.3 billion

Business Banking + SME deposits lessened by 6.0% YoY to

RM72.2 billion

Consumer deposits grew 6.8% to RM140.1 billion

34

Community Financial Services: Overview of CFS Malaysia Asset Quality

Total GIL ratio for consumer financing portfolio

remained stable at 0.5%.

Combined GIL ratio for Business Banking + SME showed

an increase to 9.0%, due to impairment from Business

Banking.

708.1 739.0 783.7

0.5 0.5 0.5

Mar 16 Dec 16 Mar 17

GIL (RM'm) GIL (%)

3,415.2

4,134.3

1.9 2.1 2.2

Mar 16 Dec 16 Mar 17

GIL (RM'm) GIL (%)

2,707.1

3,395.2 3,517.9

2.0 2.0 2.1

7.48.7 9.0

Mar 16 Dec 16 Mar 17

GIL (RM'm) GIL for SME (%) GIL for SME + BB (%)

4,301.6

CFS GIL increased marginally to 2.2% due to a slight uptick

in Business Banking GIL

Business Banking + SME GIL increased to 9.0%

Consumer GIL remained stable at 0.5%, lower than the

industry average of 1.0%

35

Table of Contents

Executive Summary 2

Results Overview 5

Prospects & Outlook 20

Appendix:

1. Financial Performance 23

2. Community Financial Services 31

3. Global Banking 36

4. Maybank Singapore 41

5. Maybank Indonesia 45

6. Other segments 50

7. Affiliates 55

Financial Results: 1Q FY2017 ended 31 March 2017

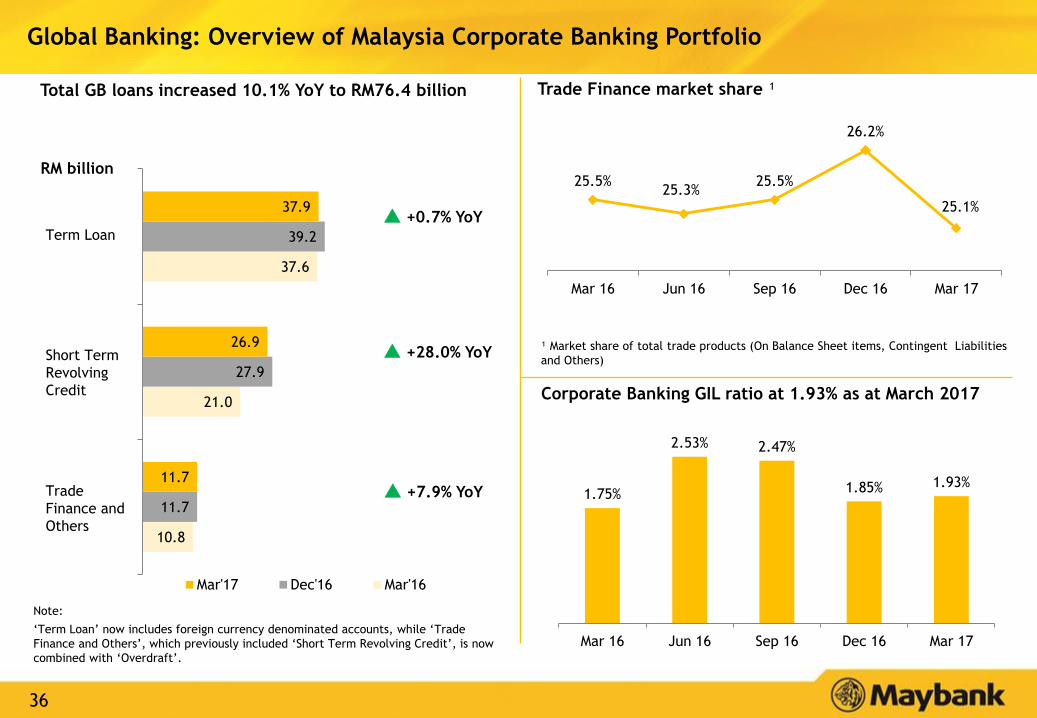

36

10.8

21.0

37.6

11.7

27.9

39.2

11.7

26.9

37.9

Mar'17 Dec'16 Mar'16

RM billion

Note:

‘Term Loan’ now includes foreign currency denominated accounts, while ‘Trade

Finance and Others’, which previously included ‘Short Term Revolving Credit’, is now

combined with ‘Overdraft’.

Term Loan

Global Banking: Overview of Malaysia Corporate Banking Portfolio

Trade Finance market share ¹Total GB loans increased 10.1% YoY to RM76.4 billion

Corporate Banking GIL ratio at 1.93% as at March 2017

Short Term

Revolving

Credit

Trade

Finance and

Others

¹ Market share of total trade products (On Balance Sheet items, Contingent Liabilities

and Others) +28.0% YoY

+7.9% YoY

+0.7% YoY

25.5%25.3%

25.5%

26.2%

25.1%

Mar 16 Jun 16 Sep 16 Dec 16 Mar 17

1.75%

2.53% 2.47%

1.85% 1.93%

Mar 16 Jun 16 Sep 16 Dec 16 Mar 17

37

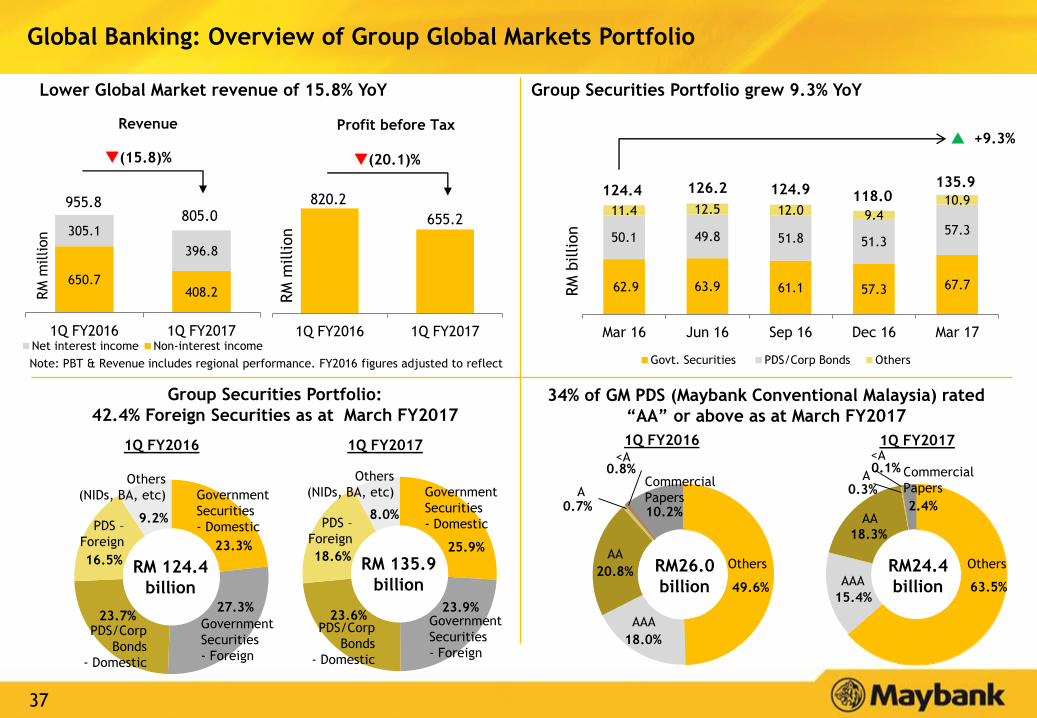

650.7408.2

305.1

396.8

1Q FY2016 1Q FY2017Net interest income Non-interest income

Group Securities Portfolio:

42.4% Foreign Securities as at March FY2017

Group Securities Portfolio grew 9.3% YoY Lower Global Market revenue of 15.8% YoY

34% of GM PDS (Maybank Conventional Malaysia) rated

“AA” or above as at March FY2017

Global Banking: Overview of Group Global Markets Portfolio

820.2

655.2

1Q FY2016 1Q FY2017

(20.1)%

RM

million

Note: PBT & Revenue includes regional performance. FY2016 figures adjusted to reflect

Revenue Profit before Tax

(15.8)%

955.8

RM

million

805.0

1Q FY20171Q FY2016

23.3%

27.3%23.7%

16.5%

9.2%

RM 124.4

billion

Government

Securities

- Domestic

Government

Securities

- Foreign

PDS/Corp

Bonds

- Domestic

PDS –

Foreign

Others

(NIDs, BA, etc)

25.9%

23.9%23.6%

18.6%

8.0%

RM 135.9

billion

Government

Securities

- Domestic

Government

Securities

- Foreign

PDS/Corp

Bonds

- Domestic

PDS –

Foreign

Others

(NIDs, BA, etc)

1Q FY2016

49.6%

18.0%

20.8%

0.7%

0.8%

10.2%

RM26.0

billion

Commercial

Papers

Others

AAA

AA

A

<A

1Q FY2017

63.5%15.4%

18.3%

0.3%

0.1%

2.4%

RM24.4

billion

Commercial

Papers

Others

AAA

AA

A

<A

62.9 63.9 61.1 57.3 67.7

50.1 49.8 51.8 51.357.3

11.4 12.5 12.0 9.410.9

Mar 16 Jun 16 Sep 16 Dec 16 Mar 17

Govt. Securities PDS/Corp Bonds Others

+9.3%

RM

billion

124.4 126.2 124.9 118.0135.9

38

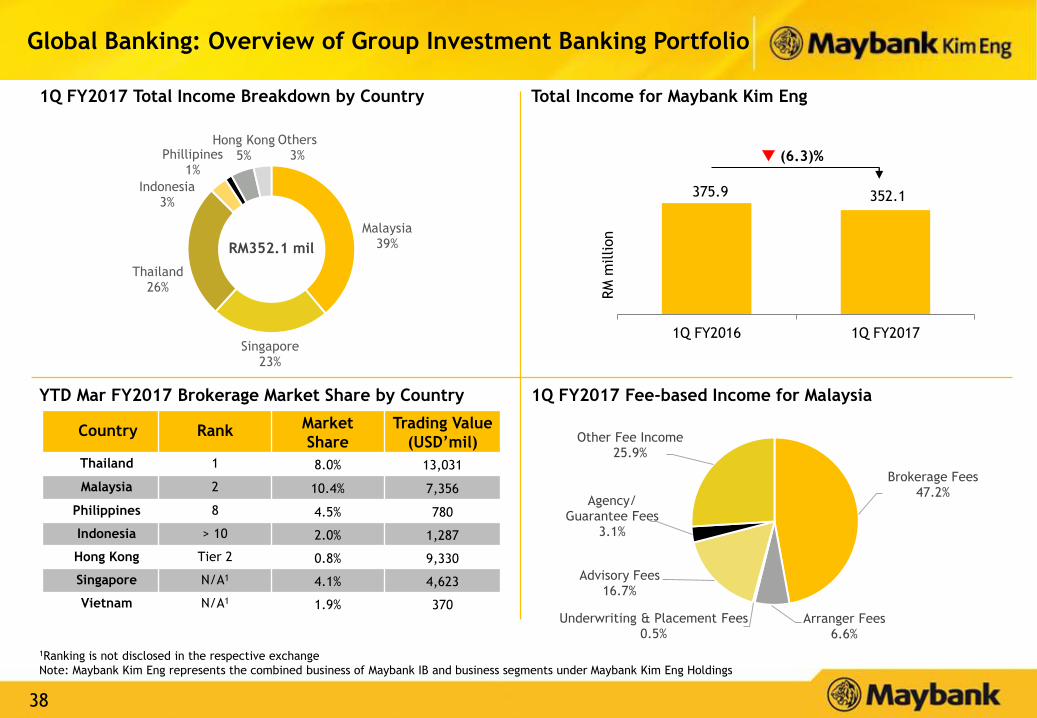

YTD Mar FY2017 Brokerage Market Share by Country

Country RankMarket

Share

Trading Value

(USD’mil)

Thailand 1 8.0% 13,031

Malaysia 2 10.4% 7,356

Philippines 8 4.5% 780

Indonesia > 10 2.0% 1,287

Hong Kong Tier 2 0.8% 9,330

Singapore N/A1 4.1% 4,623

Vietnam N/A1 1.9% 370

1Q FY2017 Fee-based Income for Malaysia

Total Income for Maybank Kim Eng

1Ranking is not disclosed in the respective exchange

Note: Maybank Kim Eng represents the combined business of Maybank IB and business segments under Maybank Kim Eng Holdings

Global Banking: Overview of Group Investment Banking Portfolio

Malaysia39%

Singapore23%

Thailand26%

Indonesia3%

Phillipines1%

Hong Kong5%

Others3%

1Q FY2017 Total Income Breakdown by Country

375.9 352.1

-

100.0

200.0

300.0

400.0

500.0

1Q FY2016 1Q FY2017

(6.3)%

RM

million

Brokerage Fees47.2%

Arranger Fees6.6%

Underwriting & Placement Fees0.5%

Advisory Fees16.7%

Agency/ Guarantee Fees

3.1%

Other Fee Income25.9%

RM352.1 mil

39 39

Global Banking: Notable Deals for 1Q FY2017

FENGHUANG DEVELOPMENT

SDN BHD

RM1.0 Billion

Medium Term Notes Programme

Sole Principal Adviser, Sole Lead

Arranger & Sole Lead Manager

Malaysia

Jan 2017

SGD430.0 Million &

RMB400.0 Million

DASIN RETAIL TRUST

Syndicated Dual-Currency Term

Loan Facilities

Coordinator, Mandated Lead

Arranger & Bookrunner

Singapore

Jan 2017

PT TRANS RETAIL INDONESIA

USD575.0 Million

Syndicated Term Loan

Mandated Lead Arranger

Indonesia

Jan 2017

GOVCO HOLDINGS BERHAD

RM3.0 Billion

Government Guaranteed Islamic

Medium Term Notes Issuance

Joint Lead Manager

Malaysia

Feb 2017

GOVCO HOLDINGS

Jan 2017

SABANA SHARI’AH

COMPLIANT REIT

SGD80.2 Million

(USD56.1 Million)

Rights Issues

Joint Lead Manager & Joint

Underwriter

Singapore

OXLEY GEM PTE LTD

SGD585.0 Million

Syndicated Term Loan & Revolving

Credit Facilities

Sole Mandated Lead Manager &

Bookrunner

Singapore

Feb 2017

AFFIN BANK BHD

RM1.0 Billion

Subordinated MTN

Joint Principal Adviser, Joint Lead

Arranger & Joint Lead Manager

Malaysia

Feb 2017

NEW PARK PROPERTY

PTE LTD

SGD760.0 Million

Syndicated Term Loan & Revolving

Credit Facilities

Sole Mandated Lead Arranger &

Bookrunner

Singapore

Mar 2017

HD SAISON FINANCE

COMPANY LTD

USD30.0 Million

Syndicated Term Loan Facility

Mandated Lead Arranger &

Bookrunner

Vietnam

Feb 2017

SAPURAKENCANA TMC

SDN BHD

USD658.0 Million

Term Loan Facility

Coordinating Bank, Inter-creditor

Agent, Facility Agent & Security

Agent

Malaysia

Mar 2017

TANJUNG BIN ENERGY

SDN BHD

RM800.0 Million

Unrated Perpetual Sukuk

Joint Principal Adviser, Joint Lead

Arranger & Joint Lead Manager

Malaysia

Mar 2017

WCT HOLDINGS BERHAD

RM177.8 Million

(USD40.2 Million)

Primary Placement

Sole Principal Adviser, Sole Global

Coordinator, Joint Bookrunner &

Joint Placement Agent

Malaysia

Mar 2017

40

Table of Contents

Executive Summary 2

Results Overview 5

Prospects & Outlook 20

Appendix:

1. Financial Performance 23

2. Community Financial Services 31

3. Global Banking 36

4. Maybank Singapore 41

5. Maybank Indonesia 45

6. Other segments 50

7. Affiliates 55

Financial Results: 1Q FY2017 ended 31 March 2017

41

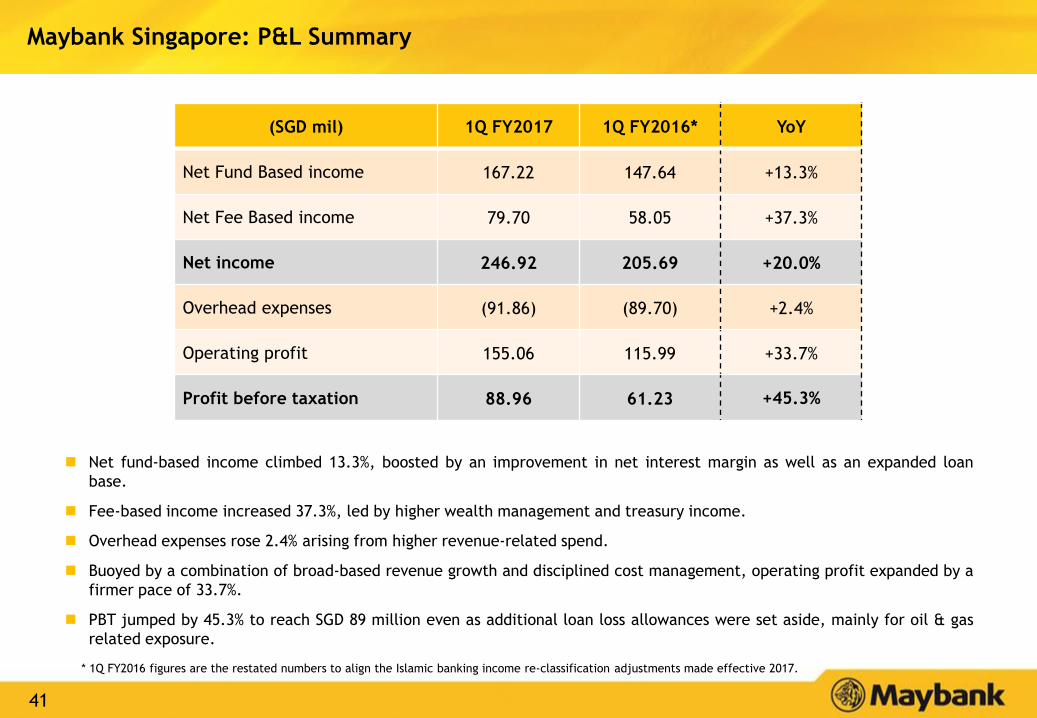

Maybank Singapore: P&L Summary

(SGD mil) 1Q FY2017 1Q FY2016* YoY

Net Fund Based income 167.22 147.64 +13.3%

Net Fee Based income 79.70 58.05 +37.3%

Net income 246.92 205.69 +20.0%

Overhead expenses (91.86) (89.70) +2.4%

Operating profit 155.06 115.99 +33.7%

Profit before taxation 88.96 61.23 +45.3%

Net fund-based income climbed 13.3%, boosted by an improvement in net interest margin as well as an expanded loan

base.

Fee-based income increased 37.3%, led by higher wealth management and treasury income.

Overhead expenses rose 2.4% arising from higher revenue-related spend.

Buoyed by a combination of broad-based revenue growth and disciplined cost management, operating profit expanded by a

firmer pace of 33.7%.

PBT jumped by 45.3% to reach SGD 89 million even as additional loan loss allowances were set aside, mainly for oil & gas

related exposure.

* 1Q FY2016 figures are the restated numbers to align the Islamic banking income re-classification adjustments made effective 2017.

42

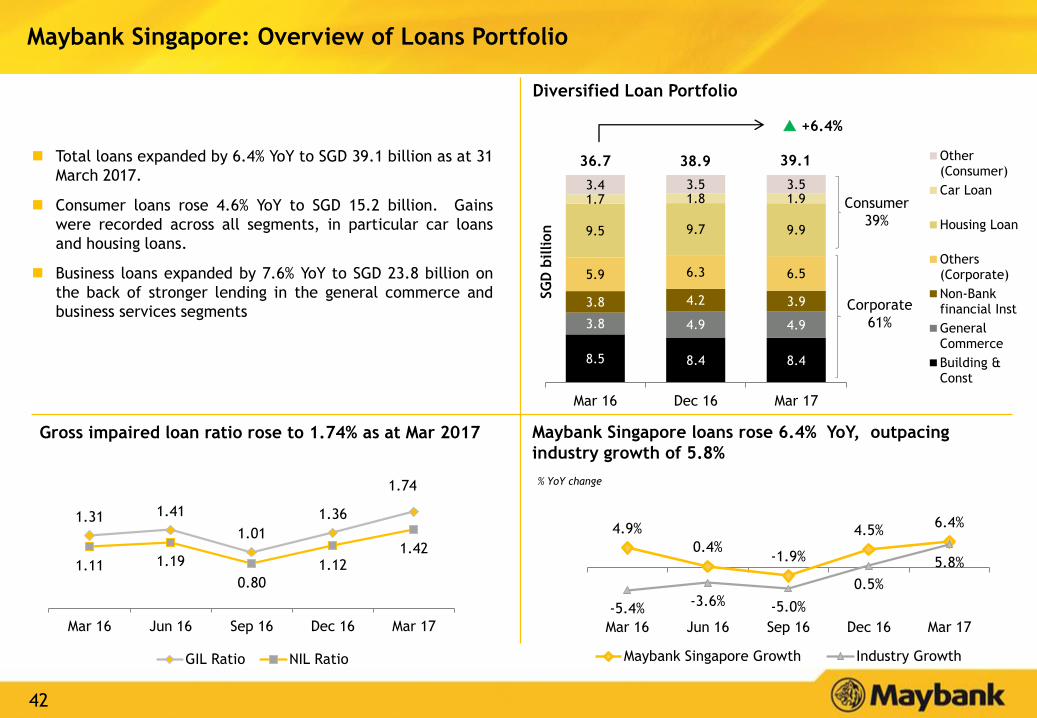

8.5 8.4 8.4

3.8 4.9 4.9

3.8 4.2 3.9

5.9 6.3 6.5

9.5 9.7 9.9

1.7 1.8 1.93.4 3.5 3.5

Mar 16 Dec 16 Mar 17

Other(Consumer)

Car Loan

Housing Loan

Others(Corporate)

Non-Bankfinancial Inst

GeneralCommerce

Building &Const

Gross impaired loan ratio rose to 1.74% as at Mar 2017 Maybank Singapore loans rose 6.4% YoY, outpacing

industry growth of 5.8%

Diversified Loan Portfolio

38.9

Consumer

39%

Corporate

61%

SG

D b

illion

Total loans expanded by 6.4% YoY to SGD 39.1 billion as at 31

March 2017.

Consumer loans rose 4.6% YoY to SGD 15.2 billion. Gains

were recorded across all segments, in particular car loans

and housing loans.

Business loans expanded by 7.6% YoY to SGD 23.8 billion on

the back of stronger lending in the general commerce and

business services segments

4.9%

0.4%-1.9%

4.5%6.4%

-5.4%-3.6% -5.0%

0.5%

5.8%

-10.0%

10.0%

Mar 16 Jun 16 Sep 16 Dec 16 Mar 17

Maybank Singapore Growth Industry Growth

+6.4%

Maybank Singapore: Overview of Loans Portfolio

1.31 1.41

1.01

1.36

1.74

1.11 1.19

0.80

1.121.42

Mar 16 Jun 16 Sep 16 Dec 16 Mar 17

GIL Ratio NIL Ratio

% YoY change

39.136.7

43

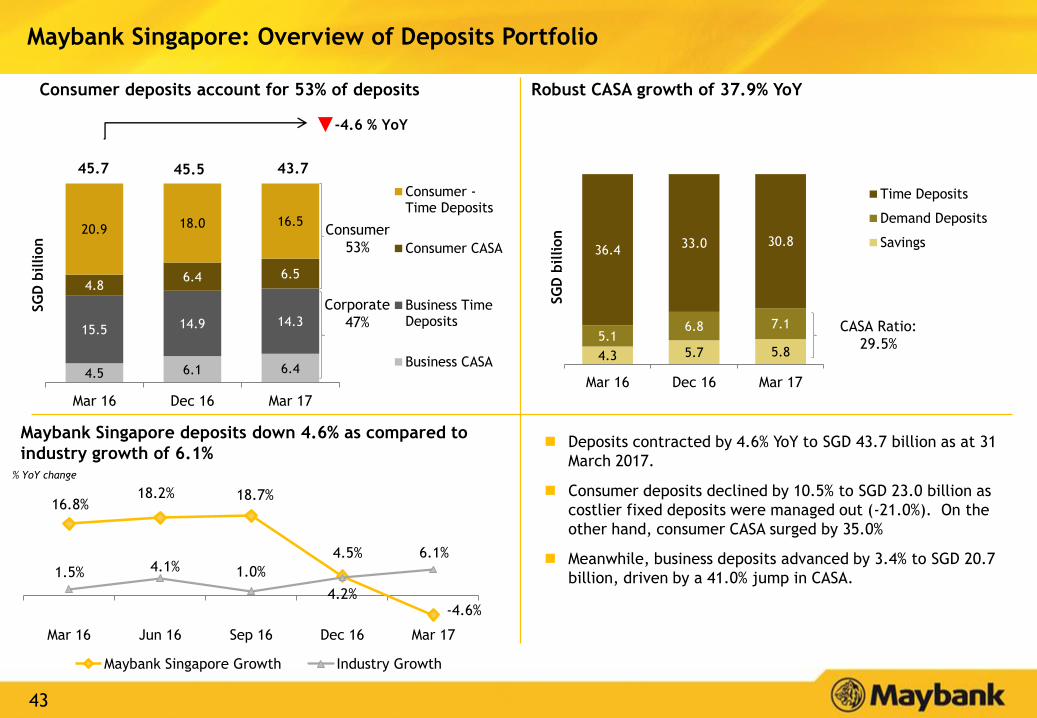

-4.6 % YoY

4.5 6.1 6.4

15.5 14.9 14.3

4.86.4 6.5

20.9 18.0 16.5

Mar 16 Dec 16 Mar 17

Consumer -Time Deposits

Consumer CASA

Business TimeDeposits

Business CASA

Maybank Singapore: Overview of Deposits Portfolio

45.5

Consumer

53%

Corporate

47%

SG

D b

illion

4.3 5.7 5.8

5.16.8 7.1

36.433.0 30.8

Mar 16 Dec 16 Mar 17

Time Deposits

Demand Deposits

Savings

CASA Ratio:

29.5%

16.8%18.2% 18.7%

4.5%

-4.6%

1.5% 4.1% 1.0%

4.2%

6.1%

Mar 16 Jun 16 Sep 16 Dec 16 Mar 17

Maybank Singapore Growth Industry Growth

Deposits contracted by 4.6% YoY to SGD 43.7 billion as at 31

March 2017.

Consumer deposits declined by 10.5% to SGD 23.0 billion as

costlier fixed deposits were managed out (-21.0%). On the

other hand, consumer CASA surged by 35.0%

Meanwhile, business deposits advanced by 3.4% to SGD 20.7

billion, driven by a 41.0% jump in CASA.

SG

D b

illion

% YoY change

Maybank Singapore deposits down 4.6% as compared to

industry growth of 6.1%

Consumer deposits account for 53% of deposits Robust CASA growth of 37.9% YoY

43.745.7

44

Table of Contents

Executive Summary 2

Results Overview 5

Prospects & Outlook 20

Appendix:

1. Financial Performance 23

2. Community Financial Services 31

3. Global Banking 36

4. Maybank Singapore 41

5. Maybank Indonesia 45

6. Other segments 50

7. Affiliates 55

Financial Results: 1Q FY2017 ended 31 March 2017

45

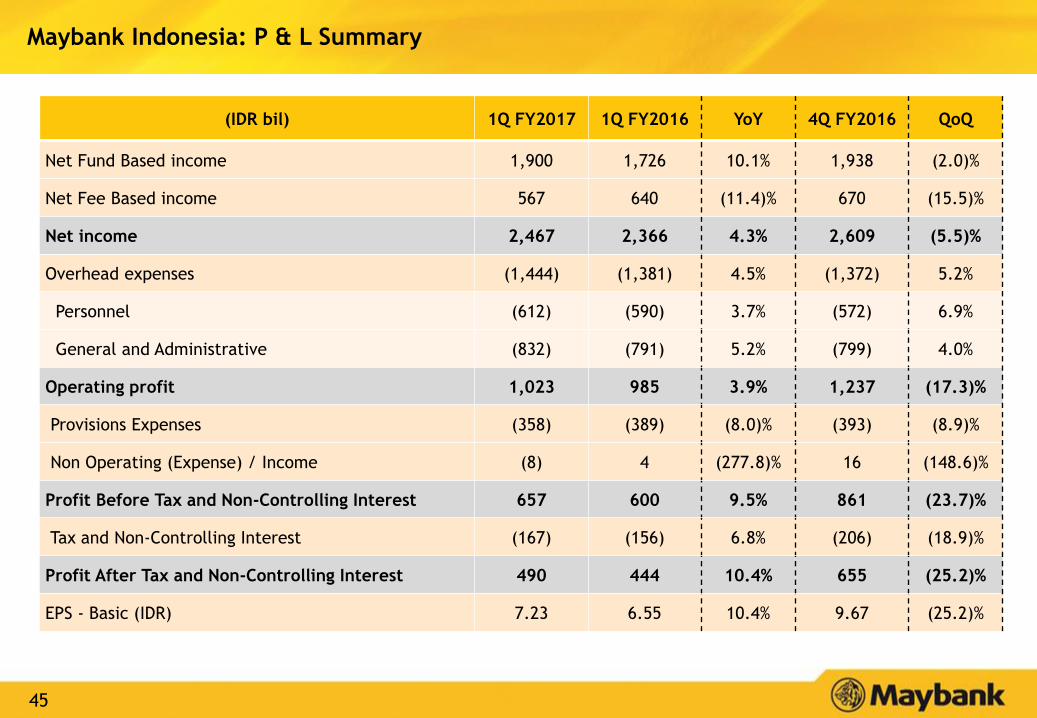

Maybank Indonesia: P & L Summary

(IDR bil) 1Q FY2017 1Q FY2016 YoY 4Q FY2016 QoQ

Net Fund Based income 1,900 1,726 10.1% 1,938 (2.0)%

Net Fee Based income 567 640 (11.4)% 670 (15.5)%

Net income 2,467 2,366 4.3% 2,609 (5.5)%

Overhead expenses (1,444) (1,381) 4.5% (1,372) 5.2%

Personnel (612) (590) 3.7% (572) 6.9%

General and Administrative (832) (791) 5.2% (799) 4.0%

Operating profit 1,023 985 3.9% 1,237 (17.3)%

Provisions Expenses (358) (389) (8.0)% (393) (8.9)%

Non Operating (Expense) / Income (8) 4 (277.8)% 16 (148.6)%

Profit Before Tax and Non-Controlling Interest 657 600 9.5% 861 (23.7)%

Tax and Non-Controlling Interest (167) (156) 6.8% (206) (18.9)%

Profit After Tax and Non-Controlling Interest 490 444 10.4% 655 (25.2)%

EPS - Basic (IDR) 7.23 6.55 10.4% 9.67 (25.2)%

46

16.2 17.3 20.4 18.9

25.6 25.6 25.6 24.8

73.7 71.9 72.9 74.0

Dec-15 Mar-16 Dec-16 Mar-17

Current Account Saving Account Time Deposit

21.5 21.5 25.7 26.0

91.1 91.3 96.0 93.8

Dec-15 Mar-16 Dec-16 Mar-17

Global Banking Community Financial Services (CFS)

6.2% YoY

Asset Quality (Consolidated)

Loans composition (Consolidated) IDR Trillion

Maybank Indonesia: Portfolio Overview

112.9112.5119.9121.8

Net Interest Margin (Consolidated)

Deposits (Consolidated) IDR Trillion

2.5% YoY

114.8115.5 117.7118.9

3.82% 3.79% 3.90%3.51% 3.63%

2.56% 2.42% 2.32% 2.25% 2.26%

Mar-16 Jun-16 Sep-16 Dec-16 Mar-17

Impaired Loans - Gross Impaired Loans - Net

4.84% 4.83%5.12% 5.17%

Dec-15 Mar-16 Dec-16 Mar-17

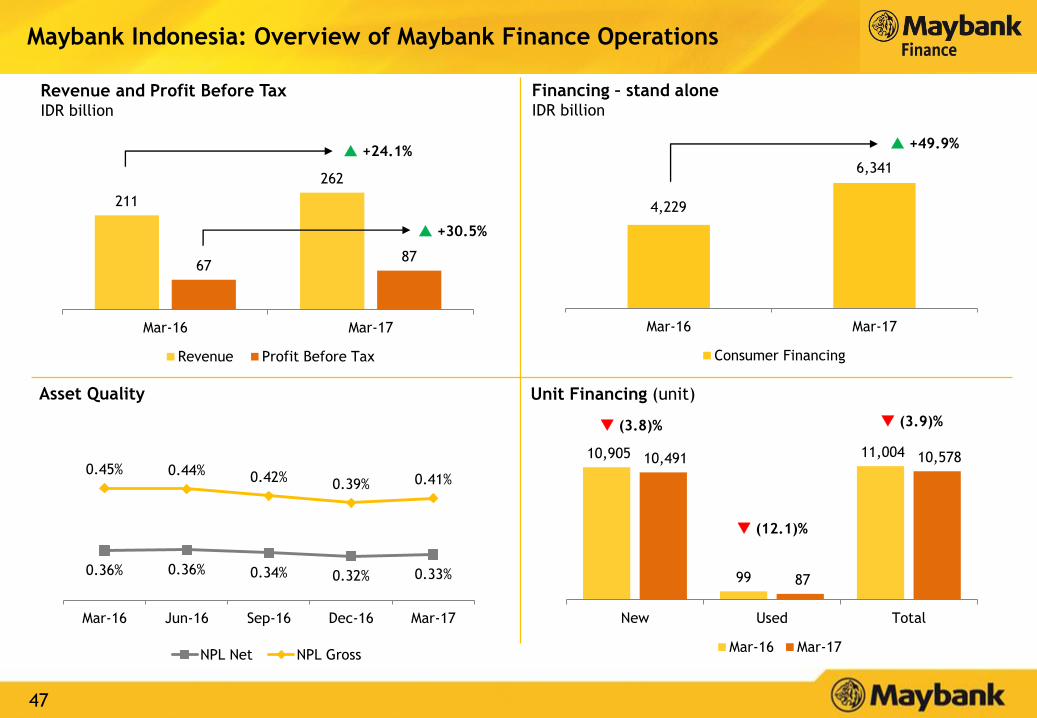

47

4,229

6,341

Mar-16 Mar-17

Consumer Financing

10,905

99

11,004 10,491

87

10,578

New Used Total

Mar-16 Mar-17

211

262

6787

Mar-16 Mar-17

Revenue Profit Before Tax

(3.8)%

(12.1)%

(3.9)%

+24.1% +49.9%

Asset Quality

Financing – stand aloneIDR billion

Unit Financing (unit)

Revenue and Profit Before Tax IDR billion

Maybank Indonesia: Overview of Maybank Finance Operations

+30.5%

0.36% 0.36% 0.34% 0.32% 0.33%

0.45% 0.44% 0.42%0.39% 0.41%

Mar-16 Jun-16 Sep-16 Dec-16 Mar-17

NPL Net NPL Gross

48

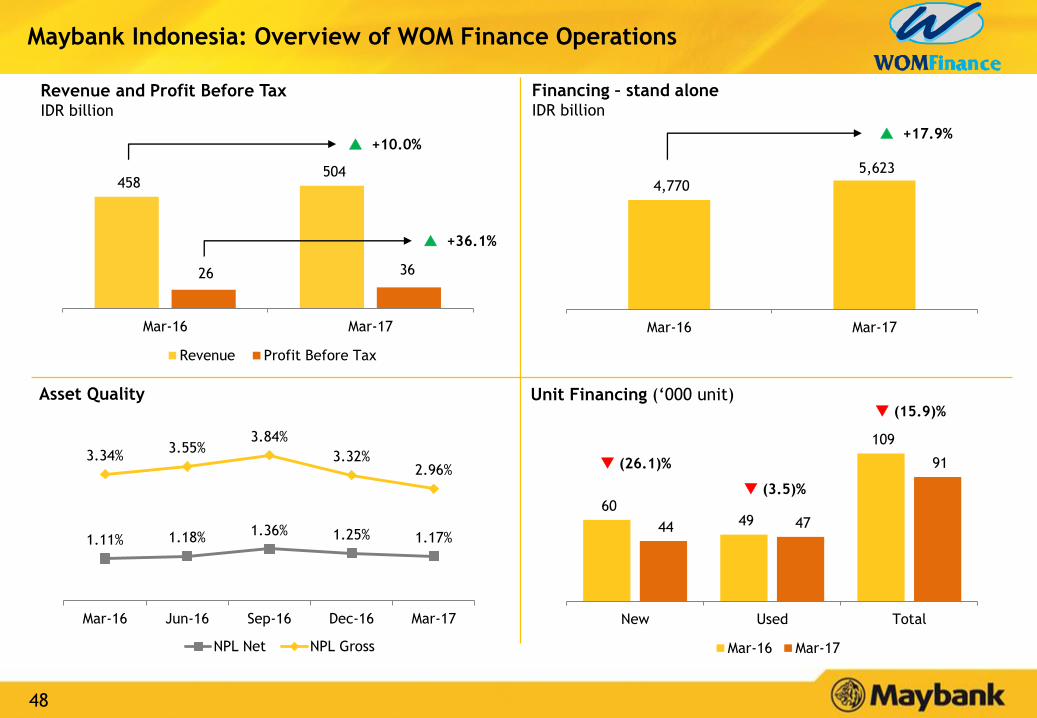

458 504

26 36

Mar-16 Mar-17

Revenue Profit Before Tax

Unit Financing (‘000 unit)

1.11% 1.18%1.36% 1.25% 1.17%

3.34%3.55%

3.84%

3.32%2.96%

Mar-16 Jun-16 Sep-16 Dec-16 Mar-17

NPL Net NPL Gross

60 49

109

44 47

91

New Used Total

Mar-16 Mar-17

(26.1)%

(3.5)%

(15.9)%Asset Quality

+10.0% +17.9%

Maybank Indonesia: Overview of WOM Finance Operations

+36.1%

4,770

5,623

Mar-16 Mar-17

Financing – stand aloneIDR billion

Revenue and Profit Before Tax IDR billion

49

Table of Contents

Executive Summary 2

Results Overview 5

Prospects & Outlook 20

Appendix:

1. Financial Performance 23

2. Community Financial Services 31

3. Global Banking 36

4. Maybank Singapore 41

5. Maybank Indonesia 45

6. Other segments 50

7. Affiliates 55

Financial Results: 1Q FY2017 ended 31 March 2017

50

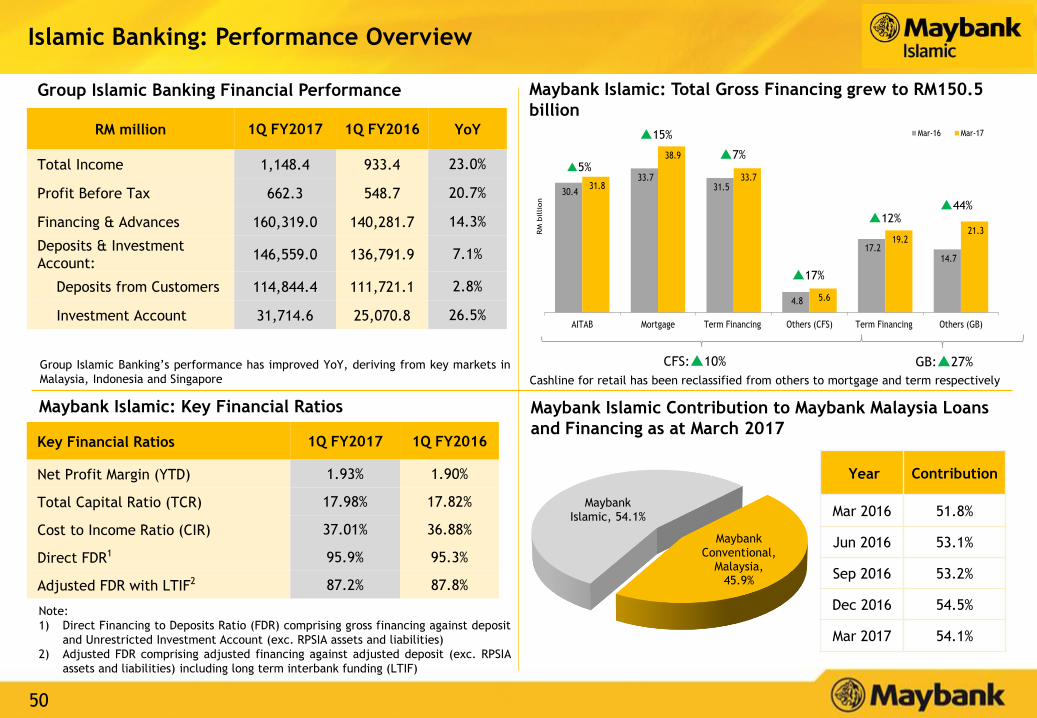

Maybank Islamic, 54.1%

Maybank Conventional,

Malaysia, 45.9%

30.4

33.7 31.5

4.8

17.2 14.7

31.8

38.9

33.7

5.6

19.2 21.3

AITAB Mortgage Term Financing Others (CFS) Term Financing Others (GB)

RM

billion

Mar-16 Mar-17

Islamic Banking: Performance Overview

Group Islamic Banking Financial Performance

Maybank Islamic: Key Financial Ratios

Maybank Islamic: Total Gross Financing grew to RM150.5

billion

CFS:10%

RM million 1Q FY2017 1Q FY2016 YoY

Total Income 1,148.4 933.4 23.0%

Profit Before Tax 662.3 548.7 20.7%

Financing & Advances 160,319.0 140,281.7 14.3%

Deposits & Investment

Account:146,559.0 136,791.9 7.1%

Deposits from Customers 114,844.4 111,721.1 2.8%

Investment Account 31,714.6 25,070.8 26.5%

Key Financial Ratios 1Q FY2017 1Q FY2016

Net Profit Margin (YTD) 1.93% 1.90%

Total Capital Ratio (TCR) 17.98% 17.82%

Cost to Income Ratio (CIR) 37.01% 36.88%

Direct FDR1 95.9% 95.3%

Adjusted FDR with LTIF2 87.2% 87.8%

Maybank Islamic Contribution to Maybank Malaysia Loans

and Financing as at March 2017

Year Contribution

Mar 2016 51.8%

Jun 2016 53.1%

Sep 2016 53.2%

Dec 2016 54.5%

Mar 2017 54.1%

Note:

1) Direct Financing to Deposits Ratio (FDR) comprising gross financing against deposit

and Unrestricted Investment Account (exc. RPSIA assets and liabilities)

2) Adjusted FDR comprising adjusted financing against adjusted deposit (exc. RPSIA

assets and liabilities) including long term interbank funding (LTIF)

GB:27%

15%

7%

17%

44%

5%

12%

Cashline for retail has been reclassified from others to mortgage and term respectively

Group Islamic Banking’s performance has improved YoY, deriving from key markets in

Malaysia, Indonesia and Singapore

51

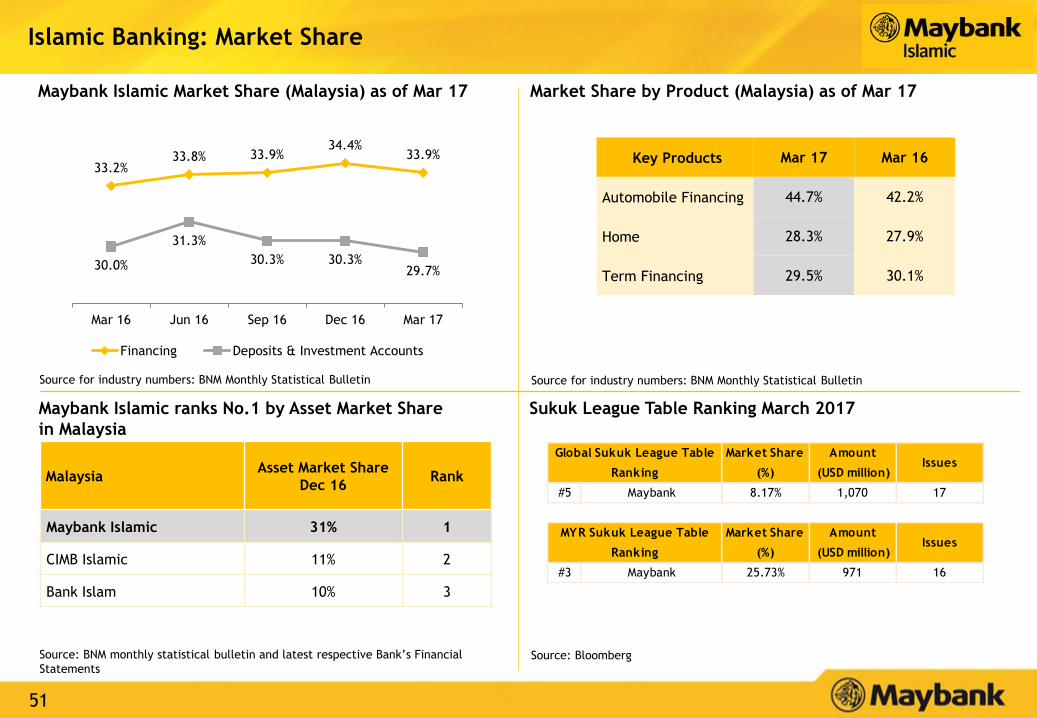

Maybank Islamic Market Share (Malaysia) as of Mar 17

Maybank Islamic ranks No.1 by Asset Market Share

in Malaysia

Source: BNM monthly statistical bulletin and latest respective Bank’s Financial

Statements

MalaysiaAsset Market Share

Dec 16Rank

Maybank Islamic 31% 1

CIMB Islamic 11% 2

Bank Islam 10% 3

Source: Bloomberg

Sukuk League Table Ranking March 2017

Key Products Mar 17 Mar 16

Automobile Financing 44.7% 42.2%

Home 28.3% 27.9%

Term Financing 29.5% 30.1%

Source for industry numbers: BNM Monthly Statistical Bulletin

Islamic Banking: Market Share

Market Share by Product (Malaysia) as of Mar 17

Source for industry numbers: BNM Monthly Statistical Bulletin

Market Share

(%)

Amount

(USD million)Issues

#5 Maybank 8.17% 1,070 17

Market Share

(%)

Amount

(USD million)Issues

#3 Maybank 25.73% 971 16

Global Sukuk League Table

Ranking

MYR Sukuk League Table

Ranking

33.2%33.8% 33.9%

34.4%33.9%

30.0%

31.3%

30.3% 30.3%29.7%

Mar 16 Jun 16 Sep 16 Dec 16 Mar 17

Financing Deposits & Investment Accounts

52

32.0 32.7

Mar 16 Mar 17

109.6

192.6

1Q FY2016 1Q FY2017

Insurance and Takaful: Performance Overview

Total Assets (RM billion)

Gross Premium

Profit Before Tax (RM million)

• PBT includes estimated transfer of RM24.5 million from Family Fund in 1Q FY2017.

Life / Family (New Business) Market Share

No. 4 in Life/Family

(New Business)

No. 1 in General

Insurance and

Takaful

* Market Share is for period Jan’16 – Dec’16 (Source: LIAM / ISM Statistics)

General Insurance and Takaful Market Share

75.6% YoY 2.2% YoY

0 500 1,000 1,500 2,000

Total Life/Family…

Total General

Misc

Personal Accident

MAT

Motor

Fire

Total Life/Family

Group Premium

Credit Premium

Regular Premium

Single Premium

1Q FY2017

1Q FY2016

Total Family/Life

& General

RM’million

132.6%

15.5%

4.1%

2.0%

14.2%

14.3%

16.6%

(0.9)%

(36.5)%

(7.0)%

(14.5)%

(1.9)%

7.6%

14.1%

15.2%

21.6%

0.0% 10.0% 20.0%

Etiqa Ins. & Tak.

GE Ins. & Tak.

Prudential Ins. & Tak.

AIA Ins. & Tak.

8.0%

10.4%

12.6%

0.0% 5.0% 10.0% 15.0%

AmGeneral Insurance

Allianz Insurance

Etiqa Ins. & Tak.

53

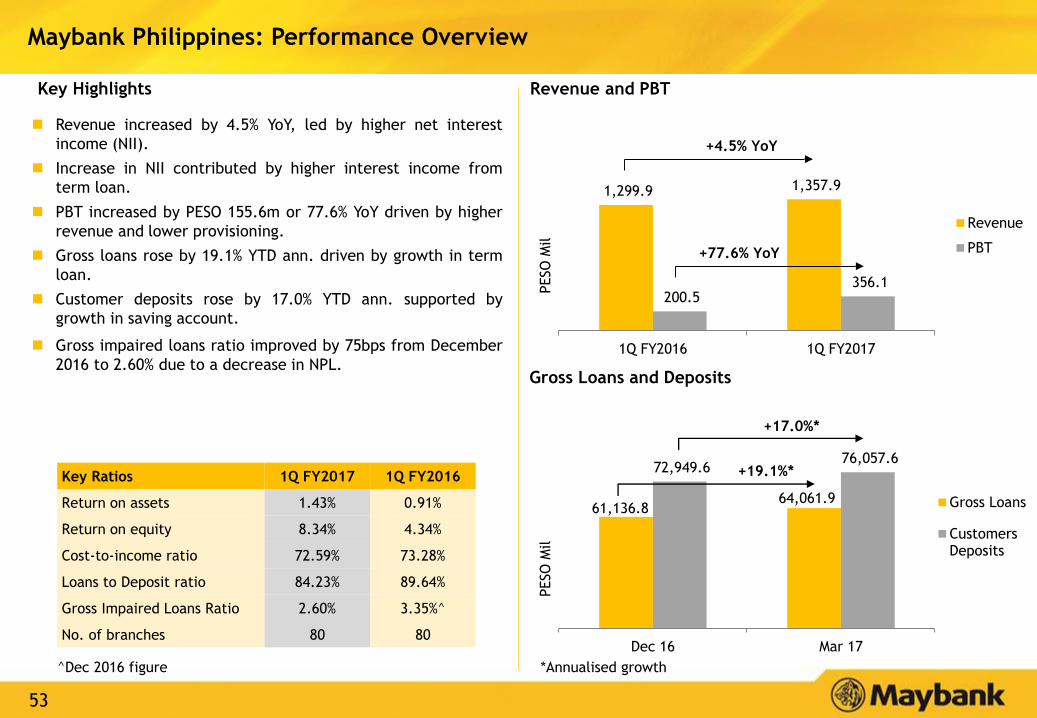

61,136.8 64,061.9

72,949.6 76,057.6

Dec 16 Mar 17

Gross Loans

CustomersDeposits

1,299.9 1,357.9

200.5 356.1

1Q FY2016 1Q FY2017

Revenue

PBT

Maybank Philippines: Performance Overview

Revenue increased by 4.5% YoY, led by higher net interest

income (NII).

Increase in NII contributed by higher interest income from

term loan.

PBT increased by PESO 155.6m or 77.6% YoY driven by higher

revenue and lower provisioning.

Gross loans rose by 19.1% YTD ann. driven by growth in term

loan.

Customer deposits rose by 17.0% YTD ann. supported by

growth in saving account.

Gross impaired loans ratio improved by 75bps from December

2016 to 2.60% due to a decrease in NPL.

+4.5% YoY

+77.6% YoY

Revenue and PBT

Gross Loans and Deposits

Key Highlights

PESO

Mil

PESO

Mil

+19.1%*

+17.0%*

Key Ratios 1Q FY2017 1Q FY2016

Return on assets 1.43% 0.91%

Return on equity 8.34% 4.34%

Cost-to-income ratio 72.59% 73.28%

Loans to Deposit ratio 84.23% 89.64%

Gross Impaired Loans Ratio 2.60% 3.35%^

No. of branches 80 80

*Annualised growth^Dec 2016 figure

54

Table of Contents

Executive Summary 2

Results Overview 5

Prospects & Outlook 20

Appendix:

1. Financial Performance 23

2. Community Financial Services 31

3. Global Banking 36

4. Maybank Singapore 41

5. Maybank Indonesia 45

6. Other segments 50

7. Affiliates 55

Financial Results: 1Q FY2017 ended 31 March 2017

55

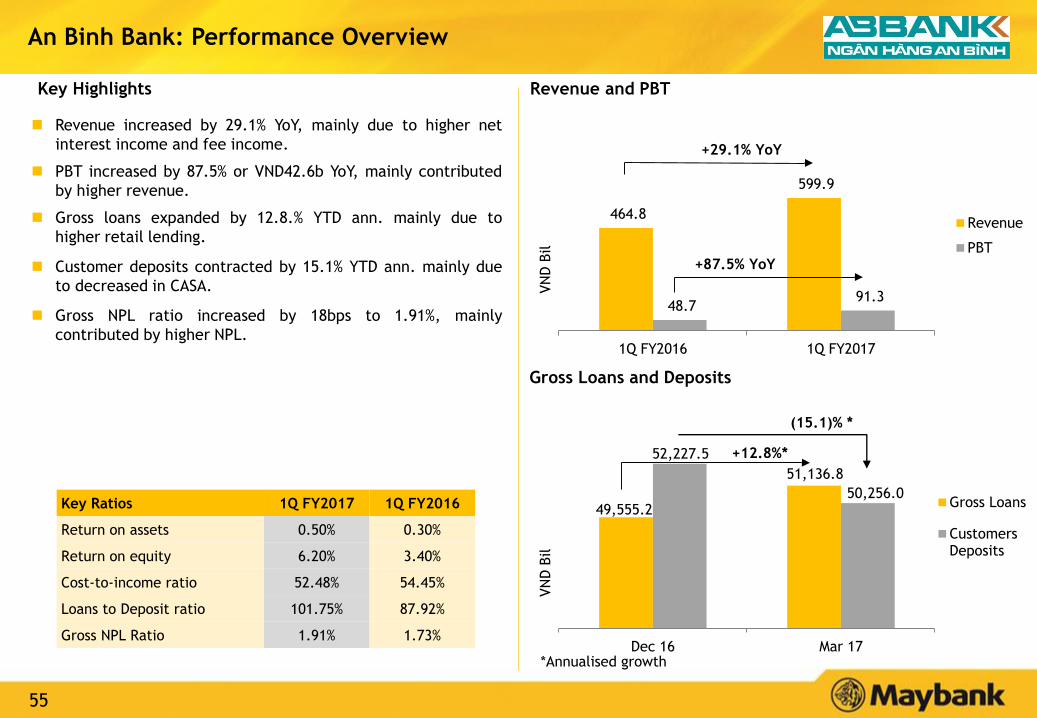

464.8

599.9

48.7 91.3

1Q FY2016 1Q FY2017

Revenue

PBT

An Binh Bank: Performance Overview

Revenue increased by 29.1% YoY, mainly due to higher net

interest income and fee income.

PBT increased by 87.5% or VND42.6b YoY, mainly contributed

by higher revenue.

Gross loans expanded by 12.8.% YTD ann. mainly due to

higher retail lending.

Customer deposits contracted by 15.1% YTD ann. mainly due

to decreased in CASA.

Gross NPL ratio increased by 18bps to 1.91%, mainly

contributed by higher NPL.

Key Ratios 1Q FY2017 1Q FY2016

Return on assets 0.50% 0.30%

Return on equity 6.20% 3.40%

Cost-to-income ratio 52.48% 54.45%

Loans to Deposit ratio 101.75% 87.92%

Gross NPL Ratio 1.91% 1.73%

VN

D B

ilVN

D B

il

+29.1% YoY

+87.5% YoY

49,555.2

51,136.8

52,227.5

50,256.0

Dec 16 Mar 17

Gross Loans

CustomersDeposits

+12.8%*

(15.1)% *

Gross Loans and Deposits

Revenue and PBTKey Highlights

*Annualised growth

56

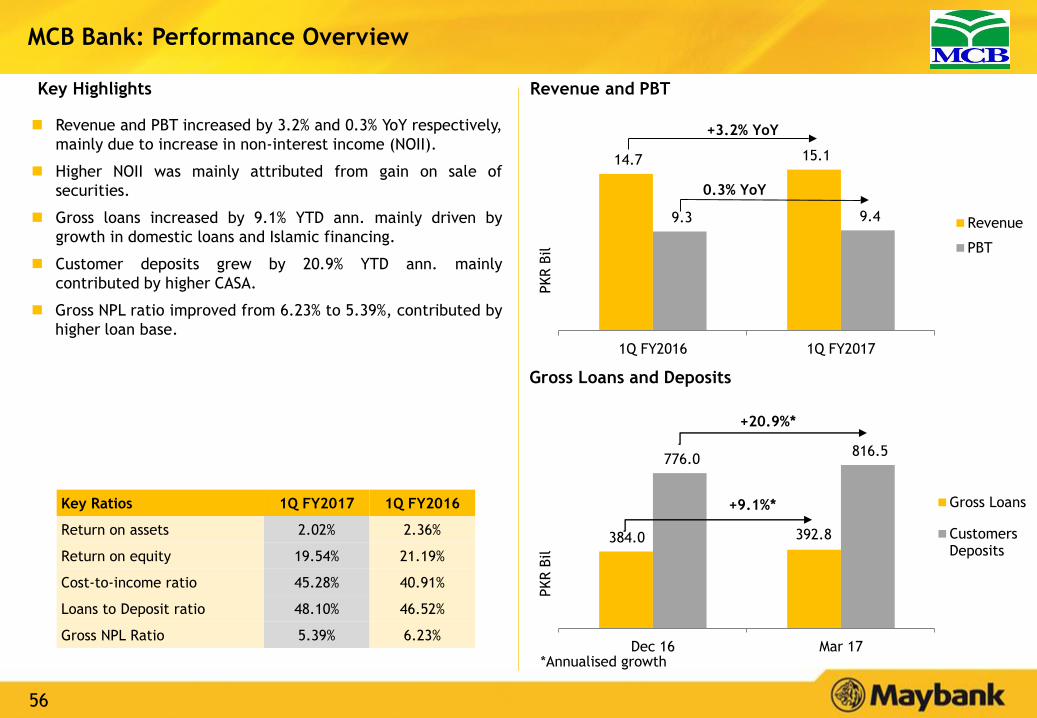

MCB Bank: Performance Overview

14.7 15.1

9.3 9.4

1Q FY2016 1Q FY2017

Revenue

PBT

+3.2% YoY

0.3% YoY

384.0 392.8

776.0 816.5

Dec 16 Mar 17

Gross Loans

CustomersDeposits

+20.9%*

+9.1%*

PKR B

ilPKR B

il

Key Ratios 1Q FY2017 1Q FY2016

Return on assets 2.02% 2.36%

Return on equity 19.54% 21.19%

Cost-to-income ratio 45.28% 40.91%

Loans to Deposit ratio 48.10% 46.52%

Gross NPL Ratio 5.39% 6.23%

Gross Loans and Deposits

Revenue and PBT increased by 3.2% and 0.3% YoY respectively,

mainly due to increase in non-interest income (NOII).

Higher NOII was mainly attributed from gain on sale of

securities.

Gross loans increased by 9.1% YTD ann. mainly driven by

growth in domestic loans and Islamic financing.

Customer deposits grew by 20.9% YTD ann. mainly

contributed by higher CASA.

Gross NPL ratio improved from 6.23% to 5.39%, contributed by

higher loan base.

Revenue and PBTKey Highlights

*Annualised growth

57

Dato’ Amirul Feisal Wan Zahir

Group Chief Financial Officer

Contact: (6)03-2074 7703

Email: [email protected]

MALAYAN BANKING BERHAD

14th Floor, Menara Maybank

100, Jalan Tun Perak

50050 Kuala Lumpur, Malaysia

Tel : (6)03-2070 8833

www.maybank.com

Jeeva Arulampalam

Head, Group Investor Relations

Contact: (6)03-2074 8346

Email: [email protected]

Disclaimer. This presentation has been prepared by Malayan Banking Berhad (the “Company”) for information purposes only and does not purport to contain all the

information that may be required to evaluate the Company or its financial position. No representation or warranty, express or implied, is given by or on behalf of the

Company as to the accuracy or completeness of the information or opinions contained in this presentation.

The presentation does not constitute or form part of an offer, solicitation or invitation of any offer, to buy or subscribe for any securities, nor should it or any part of

it form the basis of, or be relied in any connection with, any contract, investment decision or commitment whatsoever.

The Company does not accept any liability whatsoever for any loss howsoever arising from any use of this presentation or their contents or otherwise arising in

connection therewith.

Investor Relations Contact

Humanising Financial Services