INVESTOR PRESENTATION MARCH 2014 - Empyrean information made available to you in connection with the...

22

Investor Presentation August 2013 INVESTOR PRESENTATION MARCH 2014 “A profitable onshore US oil & gas development and production company focussed primarily on the development of its productive assets in Texas and California”

Transcript of INVESTOR PRESENTATION MARCH 2014 - Empyrean information made available to you in connection with the...

Investor Presentation

August 2013

INVESTOR PRESENTATION MARCH 2014

“A profitable onshore US oil & gas development and production

company focussed primarily on the development of its productive

assets in Texas and California”

EMPYREAN ENERGY PLC | Q1 2014

DISCLAIMER

These presentation materials (Presentation Materials) in respect of Empyrean Energy Plc (Company) are being issued on a strictly private and confidential basis in the United Kingdom to,and only to, Investment Professionals as defined in Section 19 of the Financial Services and Markets Act (Financial Promotion) Order 2005 (the “Financial Promotion Order”) or (b) high networth entities and other persons to whom it may lawfully be communicated falling within Article 49(1) of the Financial Promotion Order or (c) such other persons to whom it wouldotherwise be lawful to distribute it (all such persons together being referred to as “UK Relevant Persons”). In Australia, this document is only being provided to sophisticated investors (inaccordance with section 708(8) of the Corporations Act) and professional investors (in accordance with section 708(11) of the Corporations Act) or to such other persons whom it wouldotherwise be lawful to distribute it (such persons together being referred to as “Australian Relevant Persons”).

Any person who is not a Relevant Person should not rely on the presentation, this document, or its content. If you are not a Relevant Person, you should not attend the presentation, andshould immediately return any materials relating to the presentation currently in your possession. No information made available to you in connection with the presentation may be passedon, copied, reproduced or otherwise disseminated to any other person. This document is exempt from the general restrictions in relation to the communication of invitations orinducements to enter into investment activity otherwise required by section 21 of the Financial Services and Markets Act 2000 (“FSMA”) on the basis that in the UK it is only aimed at UKRelevant Persons, and has therefore not been approved by an authorised person for the purposes of section 21 of FSMA. Any investment to which this document relates (and anyinvestment activity to which it relates) is only available to Relevant Persons.

This document only contains a synopsis of information on the Company and accordingly no reliance may be placed for any purpose whatsoever on the sufficiency or completeness of suchinformation and to do so could potentially expose you to a significant risk of losing all of the property invested by you or incurred by you of additional liability. The proposals in thisdocument are preliminary. The information contained in this document is for background purposes only. No reliance should be placed on the information and no representation or warranty(express or implied) is made by Empyrean Energy Plc (the “Company”), any of their respective directors or employees or any other person, and save in respect of fraud, no liabilitywhatsoever is accepted by such person in relation thereto. Although reasonable care has been taken to ensure that the facts stated in this document are accurate and that the opinionsexpressed are fair and reasonable, no representation or warranty, express or implied, is made as to the fairness, accuracy, completeness or correctness of the information and opinionscontained in this document and no reliance should be placed on such information or opinions. None of the Company, Shore Capital or any of their respective members, directors, officers oremployees nor any other person accepts any liability whatsoever for any loss, however arising, from any use of such information or opinions (save in respect of fraud).

The distribution of this document in certain jurisdictions may be restricted by law and persons into whose possession this comes should inform themselves about, and observe, any suchrestrictions. The information contained in this document is not for publication or distribution to persons in the United States of America, its territories or possessions or to any US person(within the meaning of Regulation S under the US Securities Act 1933, as amended). Any failure to comply with this restriction may constitute a violation of United States securities law.The securities referred to in this document are not being registered under the US Securities Act of 1933, as amended, and may not be offered or sold in the United States withoutregistration or an exemption from registration. In addition, no steps have been, or will be, taken to enable the securities referred in this document to be offered in compliance with theapplicable securities law of Canada, Japan, the Republic of South Africa, or the Republic of Ireland. Accordingly, the securities referred to in this document may not be offered, sold,transferred, resold, delivered or distributed, directly or indirectly, in or into Canada, Japan, the Republic of South Africa, or the Republic of Ireland (except in transactions exempt from or notsubject to the registration requirements of the relevant securities laws of Canada, Japan, the Republic of South Africa, or the Republic of Ireland).

Certain statements contained in this document constitute “forward-looking statements”. Such forward-looking statements involve risks, uncertainties and other factors which may causethe actual results, performance or achievements of the relevant entities, or the results, to be materially different from any future results, performance or achievements expressed orimplied by such forward-looking statements. These forward-looking statements are based on numerous assumptions regarding the Company’s present and future business strategy and theenvironment in which the Company will operate in the future. There can be no assurance that the results and events contemplated by the forward-looking statements in this document, willin fact, occur.

It is a condition of your receipt of this document or attending this presentation that you fall within, and you warrant and undertake to the Company and the Blue Oar Group that (i) you fallwithin one of the categories of Relevant Persons described above, (ii) you have read, agree to and will comply with the terms of this disclaimer and (iii) you will conduct your own analysis orother verification of the data set out in the presentation materials and will bear the responsibility for all costs incurred in doing so.

The information presented in this document is subject to change without notice. Financial amounts in this document are expressed in Pounds Sterling or £ unless otherwise stated. USD or$ shall mean the lawful currency of the United States of America

2

EMPYREAN ENERGY PLC | Q1 2014

PORTFOLIO

Sugarloaf AMISouth Texas

3% WI

Operator: Marathon Oil

Riverbend ProjectEast Texas

10% WI

Operator: Krescent

Energy Partners II, LP

EAGLE FORD SHALE: PRODUCTION & DEVELOPMENT AUSTIN CHALK: APPRAISAL

PRODUCTION ADVANCED EXPLORATION

Sugarloaf Block ASouth Texas

7.5% WI

Operator: ConocoPhillips

PRODUCTION

3

Eagle Oil Pool

ProjectOnshore California

57.2% WI

Operator: Strata-X

EMPYREAN ENERGY PLC | Q1 2014

OVERVIEW

Profitable AIM listed oil and gas production company with multiple onshore US projectstargeting proven formations at varying stage of development

Current 1P Reserves of 2.3 million barrels of oil equivalent (‘MMboe’) and 2P Reserves of4.39MMboe at flagship Sugarloaf AMI project – updated CPR currently being modelled

Excellent financial growth evidenced by interim results for six months to 30 September 2013including over 3,500% increase in net profit to £2.4million following success and step up indrilling in the Eagle Ford Shale, Texas

Strong US operators - US majors including Marathon Oil and ConocoPhillips

Up to US$50 million loan from Macquarie Bank to develop the flagship Sugarloaf AMI

Blue sky to come from the potential to add Austin Chalk production to Eagle Ford Shaleproduction

Marathon is accelerating its Eagle Ford Shale activity in 2014

Experienced Board with strong understanding of the oil and gas arena

4

EMPYREAN ENERGY PLC | Q1 2014

CORPORATE STRUCTURE

Market EPIC Share Price

Shares in Issue

Market Cap

12 month price range

Cash Debt Facility

Drawn Debt

Repaid Debt

AIM EME13

pence221

million£29.52 million

5.1 – 13.5 pence

US$1.93 million

US$50 million

US$12.75million

US$2 million

Board of Directors

Non-exec Chairman: Patrick Cross

Chief Executive Officer: Tom Kelly

Technical Director: Frank Brophy

Finance Director: John Laycock

Significant Shareholders

TD Direct Investing Nominees (Europe) Ltd 16.62%

Tom Kelly 9.47%

Barclay Share Nominees Ltd 8.57%

HSDL Nominees Limited 5.34%

W B Nominees Limited 5.26%

LR Nominees Limited 5.07%

Other 49.67%-£6,000,000

-£4,000,000

-£2,000,000

£-

£2,000,000

£4,000,000

2010 2011 2012 2013

Ne

t P

rofi

t/Lo

ss G

BP

Full Year Net Profit After Tax

Growth

Net Profit After Tax

5

EMPYREAN ENERGY PLC | Q1 2014

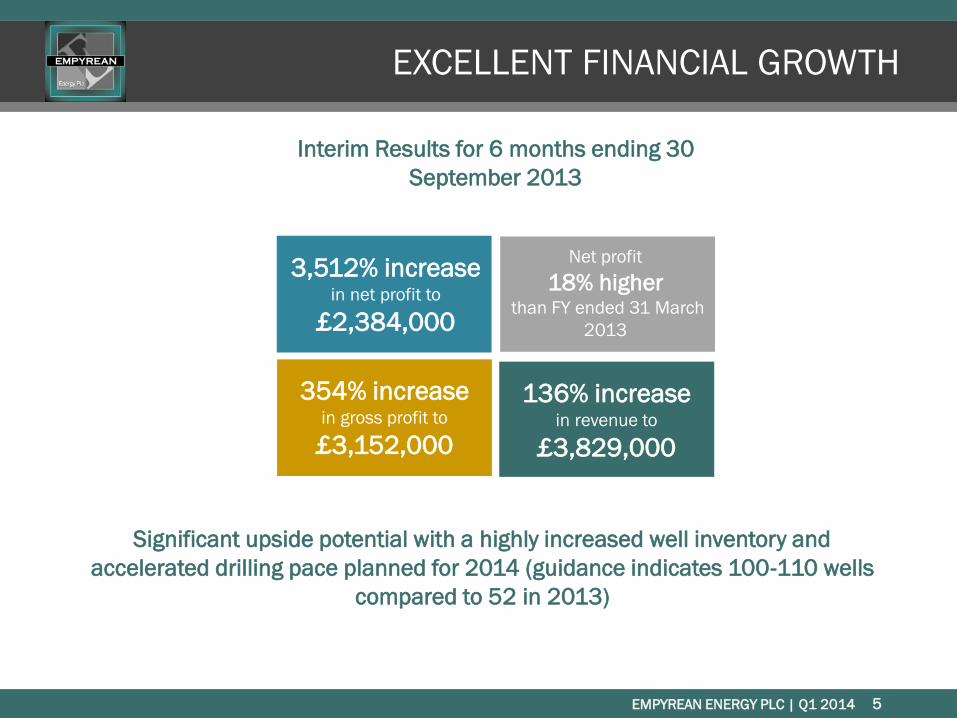

EXCELLENT FINANCIAL GROWTH

Net profit

18% higherthan FY ended 31 March

2013

136% increase in revenue to

£3,829,000

354% increase in gross profit to

£3,152,000

3,512% increase in net profit to

£2,384,000

Interim Results for 6 months ending 30

September 2013

Significant upside potential with a highly increased well inventory and

accelerated drilling pace planned for 2014 (guidance indicates 100-110 wells

compared to 52 in 2013)

5

EMPYREAN ENERGY PLC | Q1 2014

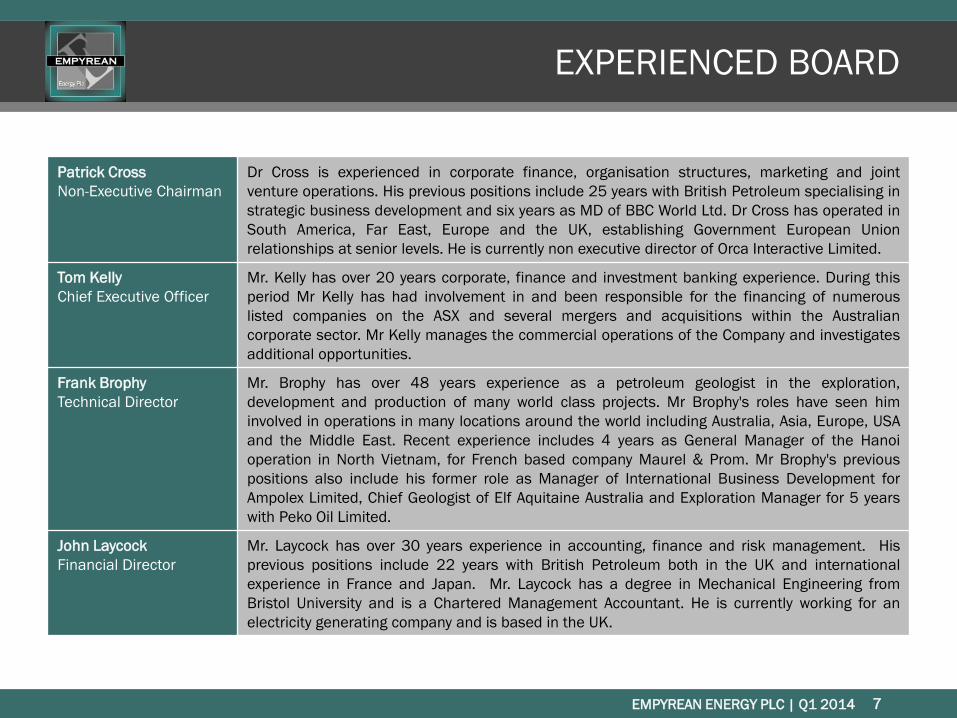

EXPERIENCED BOARD

Patrick Cross

Non-Executive Chairman

Dr Cross is experienced in corporate finance, organisation structures, marketing and joint

venture operations. His previous positions include 25 years with British Petroleum specialising in

strategic business development and six years as MD of BBC World Ltd. Dr Cross has operated in

South America, Far East, Europe and the UK, establishing Government European Union

relationships at senior levels. He is currently non executive director of Orca Interactive Limited.

Tom Kelly

Chief Executive Officer

Mr. Kelly has over 20 years corporate, finance and investment banking experience. During this

period Mr Kelly has had involvement in and been responsible for the financing of numerous

listed companies on the ASX and several mergers and acquisitions within the Australian

corporate sector. Mr Kelly manages the commercial operations of the Company and investigates

additional opportunities.

Frank Brophy

Technical Director

Mr. Brophy has over 48 years experience as a petroleum geologist in the exploration,

development and production of many world class projects. Mr Brophy's roles have seen him

involved in operations in many locations around the world including Australia, Asia, Europe, USA

and the Middle East. Recent experience includes 4 years as General Manager of the Hanoi

operation in North Vietnam, for French based company Maurel & Prom. Mr Brophy's previous

positions also include his former role as Manager of International Business Development for

Ampolex Limited, Chief Geologist of Elf Aquitaine Australia and Exploration Manager for 5 years

with Peko Oil Limited.

John Laycock

Financial Director

Mr. Laycock has over 30 years experience in accounting, finance and risk management. His

previous positions include 22 years with British Petroleum both in the UK and international

experience in France and Japan. Mr. Laycock has a degree in Mechanical Engineering from

Bristol University and is a Chartered Management Accountant. He is currently working for an

electricity generating company and is based in the UK.

7

EMPYREAN ENERGY PLC | Q1 2014

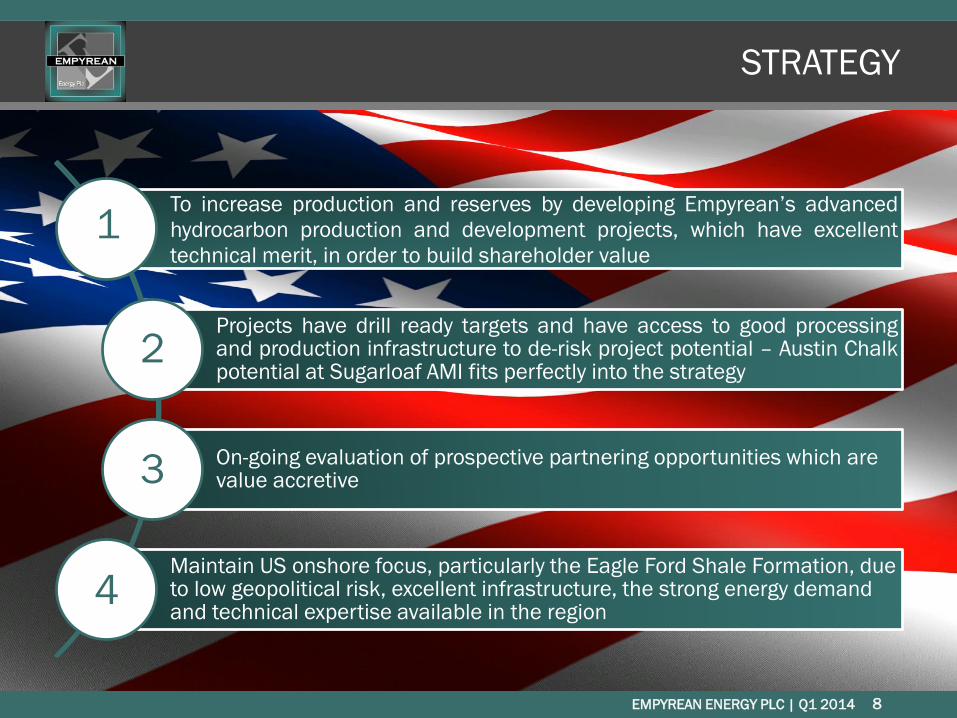

STRATEGY

To increase production and reserves by developing Empyrean’s advanced

hydrocarbon production and development projects, which have excellent

technical merit, in order to build shareholder value

Projects have drill ready targets and have access to good processingand production infrastructure to de-risk project potential – Austin Chalkpotential at Sugarloaf AMI fits perfectly into the strategy

On-going evaluation of prospective partnering opportunities which are value accretive

Maintain US onshore focus, particularly the Eagle Ford Shale Formation, due to low geopolitical risk, excellent infrastructure, the strong energy demand and technical expertise available in the region

1

2

3

4

8

EMPYREAN ENERGY PLC | Q1 2014

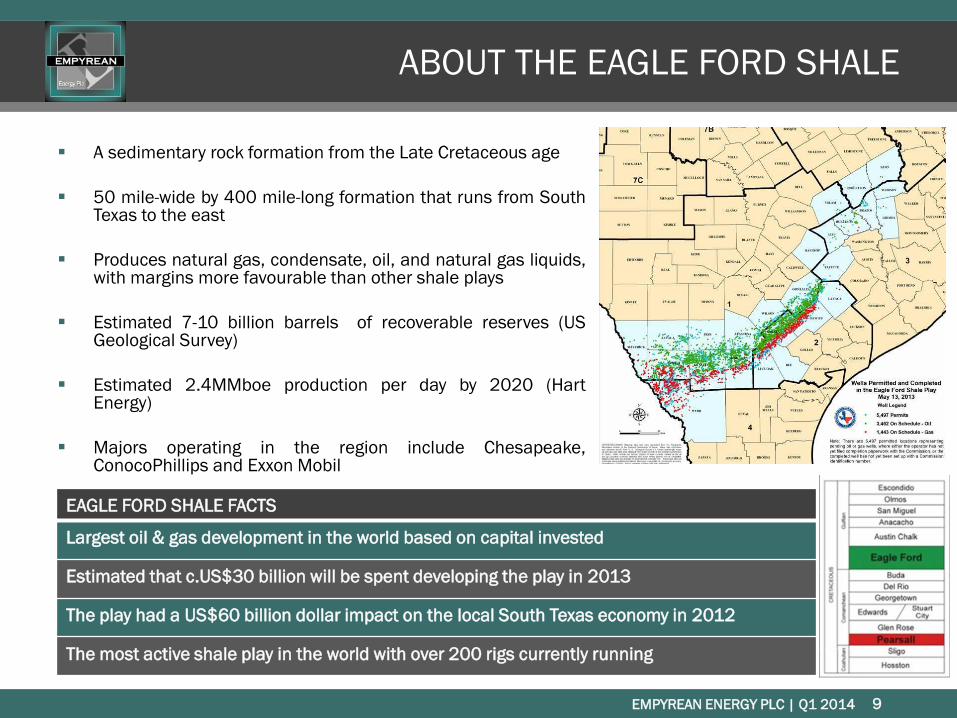

ABOUT THE EAGLE FORD SHALE

A sedimentary rock formation from the Late Cretaceous age

50 mile-wide by 400 mile-long formation that runs from SouthTexas to the east

Produces natural gas, condensate, oil, and natural gas liquids,with margins more favourable than other shale plays

Estimated 7-10 billion barrels of recoverable reserves (USGeological Survey)

Estimated 2.4MMboe production per day by 2020 (HartEnergy)

Majors operating in the region include Chesapeake,ConocoPhillips and Exxon Mobil

EAGLE FORD SHALE FACTS

Largest oil & gas development in the world based on capital invested

Estimated that c.US$30 billion will be spent developing the play in 2013

The play had a US$60 billion dollar impact on the local South Texas economy in 2012

The most active shale play in the world with over 200 rigs currently running

9

EMPYREAN ENERGY PLC | Q1 2014

EAGLE FORD SHALE: A HIGHLY ACTIVE PLAY

+1,100 wells were spud in the Eagle Ford

Shale in Q3 2013

The play accounted for 1,133 or more than

10% of the 9,175 wells spud in the U.S. during

the quarter

Marathon has allocated US$2.3bn to the Eagle

Ford Shale in 2014 to drill net 250-260 wells

with US$225m for central batteries & pipeline

construction

10

EMPYREAN ENERGY PLC | Q1 2014

SUGARLOAF AMI – AVERAGE 3% WI

A significant new condensate/ gas discovery with

exciting upside

Marathon committed to optimising drilling,

completion and production processes:

Drilling times improved dramatically <20 days

Micro seismic

Tracer Monitoring

Wellbore orientation

Fracture stimulation

Pad drilling

Minimise capex, opex and surface footprint

At least 80% of expected revenues will come from

liquids

Updated CPR currently being modelled – near

term upside potential

An Eagle Ford Shale play with strong upside potential from the Austin Chalk, Pearsall

Shale and Wilcox formations, operated by oil and gas major Marathon Oil11

11

Net acreage position

729 acresof 24,300 gross acres

Gross wells on production

121currently in the field

2P Reserves

4.3 millionbarrels of oil equivalent

in Eagle Ford Shale only

Current net production

of

904BOEPD

Estimated

>400 wells to develop Eagle Ford

Shale alone

Operated by

Marathon Oil

EMPYREAN ENERGY PLC | Q1 2014

AGGRESSIVE DEVELOPMENT

Marathon has announced its intention to co-develop the Austin Chalk alongside the EagleFord Shale with the possibility of a further 300 wells to develop this formation

Provides low risk development upside potential with additional short term potential reserve gainsas the Austin Chalk is further appraised – huge value driver for the Company

Optimisation of the field through down-spacing initiatives:

Over 90% of 2013 wells being drilled at less than 60 acre spacing

Wells drilled at 40-60 acre spacing achieved higher initial production than wells previously drilledat 80-160 acre spacing

Selected areas to be developed at 40 acre spacing and also to be trialled for 30 acre infill densityspacing

Marathon has forecast a reduction in gross drilling costs with a well cost target of US$6.5-7.5 million per well during 2014

Drilling time reduced by 50% and stimulation cycle time reduced by 40% since 2012

Additional processing facilities and pipeline capacity planned for 2014

12

EMPYREAN ENERGY PLC | Q1 2014

SUGARLOAF WELL SPACING INITIATIVES

13

Marathon has announced successful down-spacing results and an intention to co-

develop the Austin Chalk with the Eagle Ford Shale. Selected areas are to be

developed at 40 acre spacing and also to be trialled for 30 acre infill density spacing.

The Austin Chalk provides an exceptional low risk appraisal opportunity that can

leverage off of existing infrastructure, Additional potential from the Pearsall Shale and

Wilcox formations

13

EMPYREAN ENERGY PLC | Q1 2014

BUILDING RESERVES, PRODUCTION & VALUE

BUILDING

RESERVESBUILDING

PRODUCTIONBUILDING

VALUE

Closer well

spacing of 40 and

60 acres

Testing of

Additional

Formations

On-going

drilling of

prospects

Well down-spacing

initiatives successful with

over 90% of 2013 wells

being drilled at less than

60 acre spacing

The Austin Chalk - two

Austin Chalk wells

commenced production in

June 2013 and have

performed similarly to the

Eagle Ford Shale

Opportunity to drill

+400 wells to develop

the Eagle Ford Shale

depending on spacing

density

Selected areas to be

developed at 40 acre

spacing and also to be

trialled for 30 acre infill

density spacing

Pearsall Shale and Wilcox

have been earmarked by

Marathon as holding

substantial potential within

the field

A further +300 wells

to develop the Austin

Chalk should appraisal

continue to be

successful

14

EMPYREAN ENERGY PLC | Q1 2014

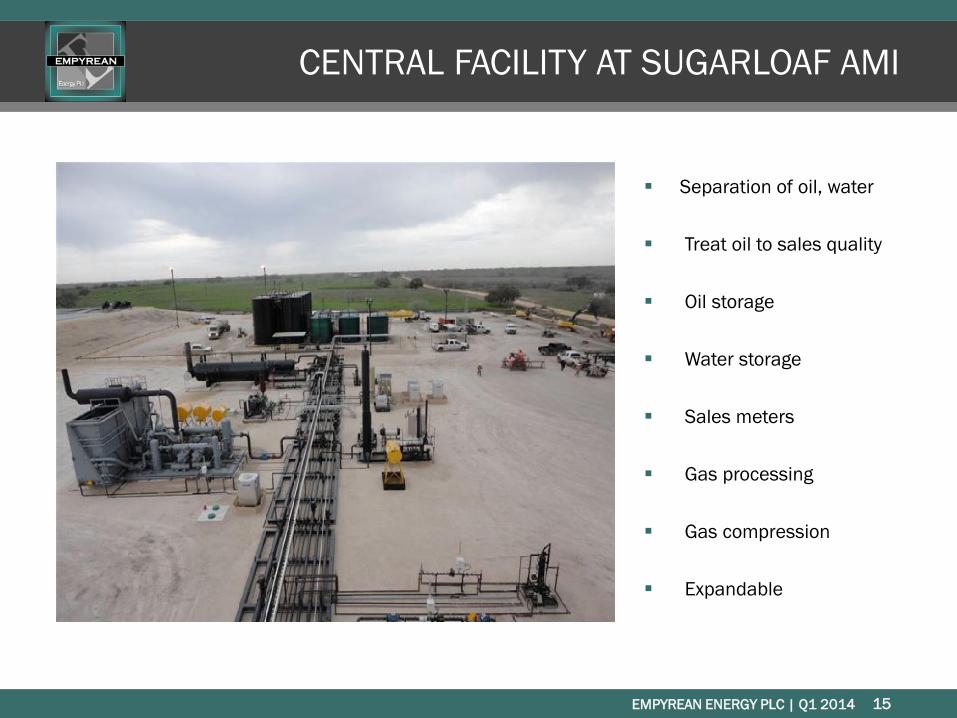

CENTRAL FACILITY AT SUGARLOAF AMI

Separation of oil, water

Treat oil to sales quality

Oil storage

Water storage

Sales meters

Gas processing

Gas compression

Expandable

15

EMPYREAN ENERGY PLC | Q1 2014

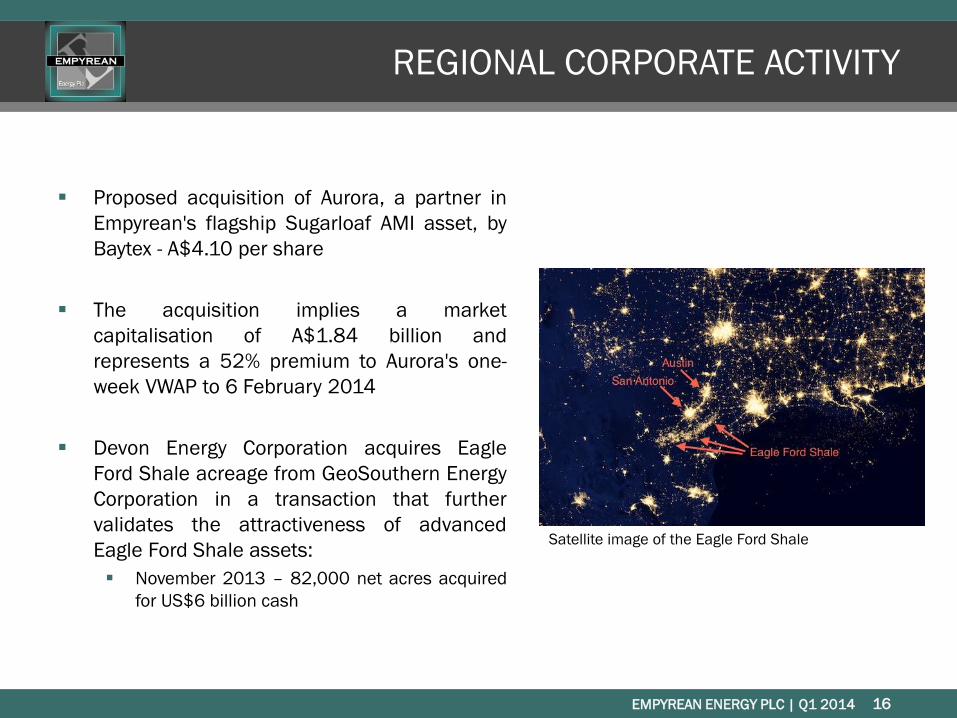

REGIONAL CORPORATE ACTIVITY

Proposed acquisition of Aurora, a partner in

Empyrean's flagship Sugarloaf AMI asset, by

Baytex - A$4.10 per share

The acquisition implies a market

capitalisation of A$1.84 billion and

represents a 52% premium to Aurora's one-

week VWAP to 6 February 2014

Devon Energy Corporation acquires Eagle

Ford Shale acreage from GeoSouthern Energy

Corporation in a transaction that further

validates the attractiveness of advanced

Eagle Ford Shale assets:

November 2013 – 82,000 net acres acquired

for US$6 billion cash

1616

Satellite image of the Eagle Ford Shale

EMPYREAN ENERGY PLC | Q1 2014

SUGARLOAF BLOCK A – AVERAGE 7.5% WI

Lies contiguous to the Sugarloaf AMIacreage in South Texas

Production held by wells targeting theEagle Ford Shale formation

Two new wells, Baker Trust-4 andMarlene Olson-3, are also targetingthis formation

Baker Trust-4 well (2.45% WI) reachedan approximate measured depth of17,948 feet with a lateral length ofapproximately 5,000 feet

Currently awaiting completion results

Marlene Olson-3 well (0.85% WI)reached an approximate measureddepth of 20,601 feet with a laterallength approximately 7,600 feet

Currently awaiting completion results

Net acreage position

43.5 acresof 580 gross acres

Operated by

ConocoPhillips

Recent activity includes participation in

2New wells

US major Conoco has been active in

acreage surrounding Block A and

Empyrean’s participation in two new wells

in a highly productive highway of the Eagle

Ford Shale marks an exciting step-up in

activity on the Company’s acreage

17

EMPYREAN ENERGY PLC | Q1 2014

DEVELOPMENT IN SAN JOAQUIN BASIN, CALIFORNIA

18

EAGLE OIL POOL PROJECT

EMPYREAN ENERGY PLC | Q1 2014

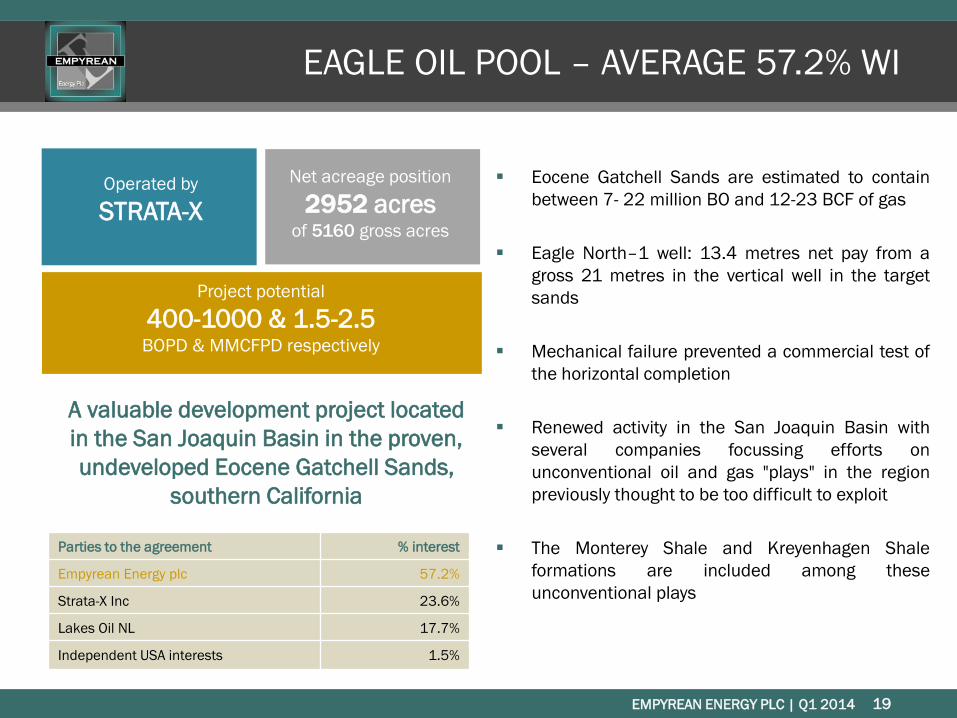

EAGLE OIL POOL – AVERAGE 57.2% WI

Eocene Gatchell Sands are estimated to contain

between 7- 22 million BO and 12-23 BCF of gas

Eagle North–1 well: 13.4 metres net pay from a

gross 21 metres in the vertical well in the target

sands

Mechanical failure prevented a commercial test of

the horizontal completion

Renewed activity in the San Joaquin Basin with

several companies focussing efforts on

unconventional oil and gas "plays" in the region

previously thought to be too difficult to exploit

The Monterey Shale and Kreyenhagen Shale

formations are included among these

unconventional plays

Parties to the agreement % interest

Empyrean Energy plc 57.2%

Strata-X Inc 23.6%

Lakes Oil NL 17.7%

Independent USA interests 1.5%

1919

Net acreage position

2952 acresof 5160 gross acres

Operated by

STRATA-X

Project potential

400-1000 & 1.5-2.5BOPD & MMCFPD respectively

A valuable development project located

in the San Joaquin Basin in the proven,

undeveloped Eocene Gatchell Sands,

southern California

EMPYREAN ENERGY PLC | Q1 2014

RIVERBEND – AVERAGE 10% WI

Located onshore Texas in Jasper County

The Cartwright-1 well was drilled initially

targeting the Austin Chalk

A down hole obstruction meant it was

recompleted in the Wilcox formation in

May 2013

The well is currently producing nominal

amounts of gas and oil

20

Net acreage position

205 acresof 2053 gross acres

Operated by

Krescent Energy

Currently producing from the

Wilcoxformation

20

Potential to produce from the Austin Chalk

formation remains at Riverbend

EMPYREAN ENERGY PLC | Q1 2014

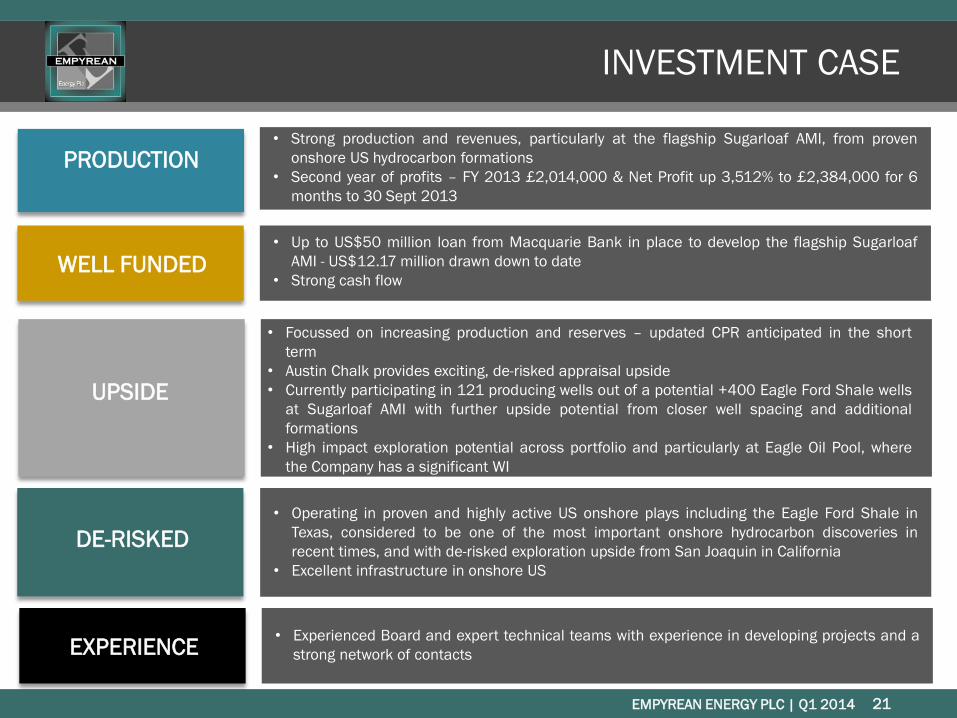

• Strong production and revenues, particularly at the flagship Sugarloaf AMI, from proven

onshore US hydrocarbon formations

• Second year of profits – FY 2013 £2,014,000 & Net Profit up 3,512% to £2,384,000 for 6

months to 30 Sept 2013

• Focussed on increasing production and reserves – updated CPR anticipated in the short

term

• Austin Chalk provides exciting, de-risked appraisal upside

• Currently participating in 121 producing wells out of a potential +400 Eagle Ford Shale wells

at Sugarloaf AMI with further upside potential from closer well spacing and additional

formations

• High impact exploration potential across portfolio and particularly at Eagle Oil Pool, where

the Company has a significant WI

INVESTMENT CASE

DE-RISKED

• Operating in proven and highly active US onshore plays including the Eagle Ford Shale in

Texas, considered to be one of the most important onshore hydrocarbon discoveries in

recent times, and with de-risked exploration upside from San Joaquin in California

• Excellent infrastructure in onshore US

UPSIDE

PRODUCTION

EXPERIENCE• Experienced Board and expert technical teams with experience in developing projects and a

strong network of contacts

WELL FUNDED• Up to US$50 million loan from Macquarie Bank in place to develop the flagship Sugarloaf

AMI - US$12.17 million drawn down to date

• Strong cash flow

21

EMPYREAN ENERGY PLC | Q1 2014

CONTACT

Tom Kelly

Empyrean Energy plc

T: +61 (419) 045 044

Lottie Brocklehurst/ Elisabeth Cowell

St Brides Media & Finance Ltd

T: +44 (0) 20 7236 1177

E: [email protected]/ [email protected]

22