inventory manaement

110

CHAPTER I INTRODUCTION

-

Upload

rojamba2010 -

Category

Documents

-

view

244 -

download

4

Transcript of inventory manaement

CHAPTER I

INTRODUCTION

MEANING AND NATURE OF INVENTORY

Inventory can be referred to as sum of the value of raw materials fuels and lubricants, spare parts, maintenance consumables, semi processed materials and finished goods, stock at any given point of time.

In large companies inventory place a most significant part of the current assets. The business has about 15 to 30% of inventories in total assets.

Inventory is composed of assets that will be sold in feature in the normal course of business operations. The assets which firms stores as inventory is anticipation of need are raw materials, work in progress and finished goods.

MEANING OF INVENTORY MANAGEMENT

Inventory management consists of maintaining for a given financial investment an adequate of something in order to meet and accepted pattern of demand. Inventory considers control over costs of inventory on one hand an handle the size of inventory on other hand.

Controlling investments in inventories constitute crucial part in current assets.

An efficient inventory controlling system will decide,

What to purchaseWhen to purchaseHow to purchaseSize of purchase

2

And from where to purchase (Suppliers)

The main purpose of inventory management is to ensure

1. Required quantity of availability of raw materials 2. Minimize the investments in inventories 3. Maintain reasonable stock levels not excess or not under

stocks.

INVENTORY CONTORL

Inventory control is the system devised an adopted for controlling investments in inventory. It involves inventory planning and decision making with regard to the quantity and time of purchase, fixation of stock levels, maintenance of stock records and continuous stock – taking.

OBJECTIVES OF INVENTORY CONTROL

Inventory control includes not only of the physical stocks but also of the funds invested on it.

That twin objectives of inventory control are,

1. To maintain a balanced inventory.

2. To keep the amount invested in inventory as low as possible without hampering either flow of the production or deliveries of finished goods.

To avoid both under stocking and over stocking of inventory.

To eliminate duplication in ordering or replenishing stocks. This is possible with the help of centralized purchasing.

3

To ensure continues supply of materials, spares and finished goods so that production should not suffer and any time and customers demand should also be met.

To design proper structure for inventory management. A clear cut accountability should be fixed at various levels of the organizations.

To ensure right quality goods at reasonable prices. Suitable quality standards will ensure proper quality of stocks. The price analysis, the cost analysis will ensure paying of proper prices.

To facilitate furnishing of data for short term and long term planning and control of inventory.

NEED FOR INVENTORY MANAGEMENT

In this competitive business world each and every business organization need inventory management system for determining what to order, when to order, where and how much to order so that purchasing and storing costs are the lowest possible without affecting production and sales. Thus, inventory management control incorporates the determination of the optimum size of the inventory-how much to be order and when after taking into consideration the minimum inventory cost.

The over all inventory management includes design and inventory control organization with proper accountability establishing procedure for inventory handling disposal of scrap, simplification, standardization and codification of inventories, determining the size of inventory holdings, maintaining record points and safety stocks, economic order quantity, ABC analysis and VALUE analysis and finally framing an INVENTORY MANUAL.

4

OBJECTIVE OF THE STUDY

The main objective of the project work is to study and analyze and preparation INVENTORY MANAGEMENT in Tecumseh India products private Ltd.,

The objectives are :

1. To know the purchasing procedure of the inventories at

Tekumseh.

2. To know classification of inventories.

3. To know codification of inventories.

4. To know the analysis of the records of stock levels.

5. To know the analysis of the JIT system of Tecumseh India

products private Ltd.

6. To know the analysis of the two bin system.

7. To know the analysis of the inventory turn over ratio.

SCOPE OF THE STUDY

The study conducted with available data from the annual reports, internal reports etc… and also interacting with employees of Tecumseh and analysis was made accordingly.The study conducted for a period of 45 days it is may not be detailed in all aspects.

METHODOLOGY

5

To attain the objective of studying the inventory of Tecumseh Products India private Ltd. The information has been collected in two ways :

1. Primary data2. Secondary data

Primary Data :

In Primary data the analysis of purchasing procedure, inventory data, inventory turn over ratio, stock levels, ABC analysis, Two bin system, JIT has made possible by the discussions with various administrative executives and other concerned people of Tecumseh Products India Pvt Ltd.

Secondary Data :

The Secondary data has been collected from annual reports of organization, internet (www.Tecumseh.com) and books.

Problem identification

To design a optimum level of inventory to manufactures compressors to the organization .The optimum level of inventory avoids excess & deficits inventory. Which is dangerous for the organization.

6

Limitations:

1 The study period of 45 days as prescribed by university

2 The study is limited unto the date and information provided

by Tecumseh India products private Ltd and its annual

reports

3 The report will not provide exact Budgetary System status

and position in Tecumseh India products private Ltd; it may

vary from time to time and situation to situation.

4 This report is not helpful in investing in Tecumseh either

through disinvestments or capital market.

5 The accounting procedure and other accounting principles

are limited by the company changes in them may vary the

actual and budget performance.

7

CHAPTER IICOMPANY PROFILE

8

TECUMSEH

Mr. Ray Herrick a former employee of ford motor company

started the company in 1937 the company went into public with

an offering of 25000 shares. Mr. Ray Herrick has passed away in

1973 but vision lived through his son ken the current chairman of

the board and his grandson Mr. Todd W Herrick who has been

president and CEO since 1984 Tecumseh India is a preferred

supplier to world who of the Ac & Industry in India and in Middle

East SAARC Countries

Tecumseh products company is a US $ 2 billion cooling giant

having a global presence and a global vision with 24

manufacturing locations in 4 continents a cross 100 countries

employing over 20000 people it is the world largest independent

compressors manufacturing company with 10% market share of

the global 150 million units a year compressors Market.

Tecumseh products company products are grouped into 3

principal industry segments:

1. compressors products

2. engine and power

3. pump products

ORIGIN OF COMPANY:

9

The company was originally established and registered in 1963

under the name of USHA refrigeration industries limited(URIL)

this unit manufacturing compressors for water cooler air

conditions and water coolers lala sharat Ramji who was from

renowned industrial family of DGM and coromondal group of

companies started URIL in 1970 the URIL was changed to shri

ram refrigeration limited and the business was divers towards

Manufacturing of diesel engines and water coolers shri ram

industries played a great role line the field and capture more than

50% of market share in India shri ram industries also kept its

hands in Mr. Siddhartha c shriram ram industries also kept its

hands in Mr. Siddhartha c shriam became the chairman cum

managing director (M.D) The product saw sea change in the

industrial policy, which resulted in a great change in the industrial

sector. in the process for survival, shri Ram went into technical

collaboration with wasting house US and was named as siel

compressors.

Siel compressors were the first Indian

compressors. Later wasting House stopped manufacturing

compressors and steel went into technological collaboration with

Techmseh products company USA in 1988.TECUMSEH mean

CROUNCHING PANTHER derived from chief of the SHAWNEE tribe.

(1768-1813).it started operation to offer new state of art AW

series to Indian customers subsequently Tecumseh Products

Company took over siel group become 100% subsidiary company

of Tecumseh Products Company. As soon as Tecumseh took over

the company stopped manufacturing water coolness and

restricted its production to CFC/hermetically sealed compressor.

10

TPIPL is an ISO and 9001 certified American

based company Tecumseh India is a 100% subsidiary 10

Tecumseh products company USA, which is world only full line,

independent manufacturing locations is 4 continents across 100

countries employing over 19000 people. In India it has 20 sales

office and an extensive network of over 200 dealers and move

than 600 registered small scales industries.TPIPL has gained core

expertise in R&D AW assembly and AW machine shops such that

it acquired a lion’s shae compressors marked by gaining a 50%

share.

Hyderabad plant:

The Hyderabad plant is on a 54 acres land at the Balanagar

industrial belt 15km away from Hyderabad city on highway line

going towards HMT Limited Narsapur road at Hyderabad

TPIPL manufacture air conditioner form 100 BTU to 6lakhs BTU

(British Thermal Unit) and compressors for deep freezer, bottle

coolers and water coolers which are considered to be world’s no 1

in 150 million compressor market a year. The plant has the

manufacture capacity of 300 units per day. This plant has a

technology development center with full R&D facility. The plant is

also supported by two service centers AW service center and MC

service center and MC service center Hyderabad plant has six

regional offices among which four offices are metro cities The

remaining tow are at Ahmadabad and secunderabd., Besides

there are branch officers and depots located in prime cities

11

across the country. This plant also has network of about 177

dealers across the nation and his preferred supplies to key

original equipment manufactures like LG, VOLTAS, BLUESTAR,

GODERJ, VIDDEOCON, FEDDERS, AMTRIX, HITACHI, etc.TPIPL

Hyderabad plant was successful in getting the ISO 9001

certification for maintaining quality of compressor in 1994 and for

eco friendly environment maintenance the company has ISO

14001 certification . TPIPL Hyderabad has total of 829 permanent

employees.

In 1997 Tecumseh fully acquired SRI, Hyderabad.

In 1998 the turnover for the year was Rs.111.28 Crores with

on operational profit of Rs.14.14 Crores and PBT of Rs.

10.50 Crores.

Company not only meets its target but also increase it

market share and company think about amalgamates.

Employees for the current year are:

Permanent Worker 402

Staff 185

Officers 156

RSO 45

Total To-Dated 2006 Employees is: 788

Company have 1000 of contact Worker. It is divided as Badali

or Special Badali.

12

AC Compressors Business:

The Capacity is 3,00,000(expanding)

The plant is certified company with ISO 9001-2000

version, ISO 14001

Models Ac applications AW

Certification VDE,

Products:

Air conditioning (12,000-29, 5000 BTU per/h

Compressors

Compressors manufactured at Hyderabad:

AW series- AW.AWQ AWA etc

Rotaries (to be introduced in 2003)

The management has started development activates in

the following areas.

a) Effluent Treatment Plant

b) Tree Plantation

c) Biological Treatment Plant

d) Rain water harvesting is to increase the group

water level and TPIPL has the distinctions of

being the first organization in this regard.

13

e) Vermin culture is the process of utilizing

canteen food wastage for converting in to

natural manual.

A new project under the name of VIBHAV

ROTARY PROJECT is under construction this

completer by the month of july 2005 on

completion of this project, the production starts

form January of 2006, with a production of

10.000 units per day with this projects, the

market share of production of compressors of

Tecumseh increase to 15%

BALLABGARH PLANT

At Faridabad, in North India, they have a capacity of about a

million compressors. This plant is being relocated to an

integrated unit a Ballagarh with an investment of Rs. 200 Crores

(Approximately) This state of the art plant for manufacturing of

non-CFC compressors will be one of the best compressors

facilities in Asia. This is located on a 21 acre land on the Delhi-

Mathura National Highway.

Mr.Vipin Sondhi, Managing Director, head Tecumseh India, which

employs about 2500 people.

Tecumseh India a 100% subsidiary of Tecumseh product

company USA wills continue its mission of offering the latest

compressors to the discerning India customers.

14

Tecumseh India is the manufacturing of compressors in the

country catering to segments of segments air-conditioners,

domestic and commercial refrigeration and is a leading player

with growing Indian market for compressors in all the segments.

The company was incorporated on Jan 30.1997 &

operational commenced since 14th July 1997, after take over

of compressor division of Whirlpool of India Limited.

The company acquired the compressor business from WOIL

by taking over the plant & equipment of the compressors

division at Faridabad and the entire facilities of Ballabgarh

excluding the plastic division of WOIL.

The acquisition was funded by equity, but since taken over,

the company supplies to WOIL its requirement of

compressor.

The company recorded a turnover of Rs. Crores since taken

over till 31st Dec 1997 since purchase by WOIL did not

materialized the turnover has been less which led to net

loss Rs. 4.93 Crores.

The company is in process of implementing a major

expansion diversification programmed at Ballabgarh to

enable the manufacture of Compressor once the project

implemented by 1988 the company would be the pioneer in

manufacturing environment.

In 1998 the company recorded a turnover of 99.98 Crores

against turnover of RS 26.12 Crores for the period July 1997

to Dec 1997.

The net loss recorded was RS.6.87 Crores against RS.4.92

Crores during 1997.

15

Refrigiration+Commercial Business:

Plant is certified ISO 9001, R-134 a certified plant, and

Own limitation, Wire drawing facilities.

With capacity of 1,500,000

Models MLA ,TIE

PRODUCTS

Domestic refrigeration (330-1200 BTU per hr) and

Commercial (700 -3000 BTU per hr)

Compressors manufactured at ballabgarh ;

TIE models

MLA models

MLA CRA model

TPIPL vision:

We are not going to simply provide compressors

are going to provide customer solution”. It is our goal to be the

global leader in all of the markets which we choose to participate

we will pursue disruptive technologies to redefine our products.

TPIPL mission :

We will leverage our global expertise in mechanical,

electrical, flood handling related components and services to

provide comprehensive solution for our customers needs

16

compressors, engines, electrical motors, pumps, electronics and

controls.

We will be best in class and the most effective cost

producer by utilizing the principles of TQM,6 SIGMA and

LEAN.

Our origination will modify itself in response to change in

environment at a pace and amount of change that can be

made without eliminating or impeding our on going

effectiveness

Incisive continuous strategic thinking will be will

communicated and shared by the organization

Incisive continuous strategic thinking will be well

communicated and shared by the organization

Our commitments:

KEY BUSINESS ACTIVITIES:

Set the world industry standard of excellence for customer

satisfaction achieve total quality

To attain and surpass global quality and reliability standards

for our products.

Maintain clear technology leadership

Market share leadership with focus on customer needs.

17

Meet business and financial commitments.

IMAGE:

To build up a high degree of customers confidence by

sustaining international markets in regard to supply of spare

parts and after sale Service. The HRD policy of Tecumseh is

manifested in the code of conduct of TPIPL listed

Respect and mutual trust

Integrity and fairness in all matters

Team work

Best customer service

TPIPL QUALITY POLICY:

Committed to total customer satisfaction by meeting their needs,

expectation.

And aspiration stated, implied or latent

Striving to provide products and service of global quality

standard and to reach a position of leadership in the field of

operations, setting new values.

Continuous improvement across the organization an up

gradation of product technology and process supportive

environment, at least cost to society share be the means to

achieve the goals.

18

The approach will be through proper systems and procedures

and total involvement of employee’s vendors and other

business associates.

TPIPL ENVIRONMENT POLICY:

The vision of Tecumseh India is to be serene green and eco

friendly co-operation carrying out all its operation

contributing to preservation of environment and natural

resources for benefit at large

Among others this can be achieved through allocation of

company wide priority for sustainable development with total

involvement and commitment.

Evaluation and up gradation of current technology products

and raw materials for minimization handling and disposal of

solid liquid and gaseous waster

Realization of tangible objective and target set for continual

improvement to control and prevent pollution and conserve

resources.

Variable earning sharing of value addition

Agreement process organization needs

Non conformance reporting audits

Open house//communication meeting

Team assessment and feed back

Changing life sty les.

SAFETY POLICY:

Education and training

Creating a safe working environment

19

Providing adequate and required personal protective

equipment

Updating safety rules and procedures

Continuous improvement through safety audits Risk

assessment Audits

The Employees and all other share:

Follow safety rules and procedures.

Use all the required personal protective equipment

Adopt safe working methods

Take a proactive interest in maintaining safety standards.

TPIPL’S SEVEN DEADLYSINS:

a) Inconsistent product quality

b) Slow response to market place.

c) Lack of innovate competitive product

d) Un competitive cost structure

e) Inadequate employee involvement

f) Unresponsive customer service

g) Ineffective resource allocation

STATEGIES&PROCESS AT TPIPL:

Work place improvement.

Creativity club

KRA’S (improvement/suggestions)

20

The management has started development activities in the

following areas.

Efficient treatment plant.

Tree plantation.

Rain water harvesting is increase the ground water level and

TPIPL has distinction of being of first organization in this

regard.

Semi culture is the process of utilizing canteen food wastage

for converting into natural manure.

QUALITY IMPROVEMENT MEASURES:

Yours company’s Hyderabad &ballabgarh plant are ISO 9001

(version 2000) certification. Your company is constantly meeting

the quality requirement of Domestic& International customers.

Environmental protection & Conservation of Natural resources:

During the year, ISO 14001 first Annual Assessment after

Recertification Audit carried out by the corporate Director of

Environment control Hyderabad unit had scored 95 points and

reveal any non conformities

During Annual C0mpliance Assurance review carried out by the

corporate Director of Environment control Hyderabad unit had

scored 95 points and Ballabgarh unit had scored 89 points of

115 for 2004

21

The following conservation measures were undertaken by your

company.

Usage of De-mineralized water in place of Municipal/Bore

water in process.

I MECO BULLOWS components cleaning equipment have

been introduced in EOU for effective cleaning of

components ot minimize water & chemicals.

Export oriented unit is completely R-134 a compatible

plant.

Energy factory canteen renovation & new kitchen

equipment installation.

Construction of new septic tank for effective treatment of

sewage water.

Mezzanine floor fabrication &erection to install Dehydration

oven.

LPG yard renovation to Accommodate 5 ton LPG bullet to

cater pre treatment plant requirements.

RESEARCH AND DE VELOPMENT:

1. Specific areas in which R & D carried out by the

company

22

Designed and development high out by the energy efficient

compressors of the existing and higher cooling capacity

Improvement in product quality

Introduced AW 1000 q Compressor for small size air

conditioners

2. Benefits derived as a result of above R&D:

Development of new products

Improvement in product quality

Optimization of processing parameters

Improved customer satisfaction and developed new

customers

Lower power expense for the customer thus reducing his

recurring ex peen

3) Future plan of action:

Design improvements

High efficiency low noise compressors

Enhanced range of compressors

Product ionization of newly developed refrigerator

compressor

1) Efforts:

Technology absorption and innovation company has

focused on innovation and is working on a refrigeration

compressor, which would be equivalent or better than the best

available in the global market .

It has upgradedits test lab facilities and reduced its

dependence on foreign test labs. This gives indigenous capability

to develop, test and launch new products.

23

2) Benefits: Derived as a result of the above efforts is product

improvement, cost reduction, product development import

substitution etc.

Departments of TPIPL:

Rotary project(new)

Human resource development

It

Welfare department

FCD

CTS&S---

TDC

Attendance and pay office(A&PO)

Electronic data processing (EDP)

Provident fund and credit cooperative society(PF&CCS)

Maintenance and engineering department(MED)

EOU

Logistics

Quality control department

AW PRESS shop

Aw machine shop

Dispensary

Canteen

Chemical and technological laboratories

Legal compliance and going beyond setting new standards

Stores

Material and purchase

Accounts and audit

24

Products of Tecumseh:

Tecumseh products are grouped into 3 principal industry

segments

Compressor products

Engine and power train products

Pump products

New products from Tecumseh:

AW 1000QC COMPRESSRS

Compact 1-ton compressors

Ideal for Compact RAC units

Products from the well known AW series of compressors

Silent and efficient

Very well accepted by the market

AE 2415 AK Compressors:

A huge energy saving compressors that cuts power bills compact

and light weight

Wide voltage range

Manufactures with state of technology

Dependable friend for all deep freezers

Finance management:

1), cadres

25

2). Functions of Finance Department

Milestones:

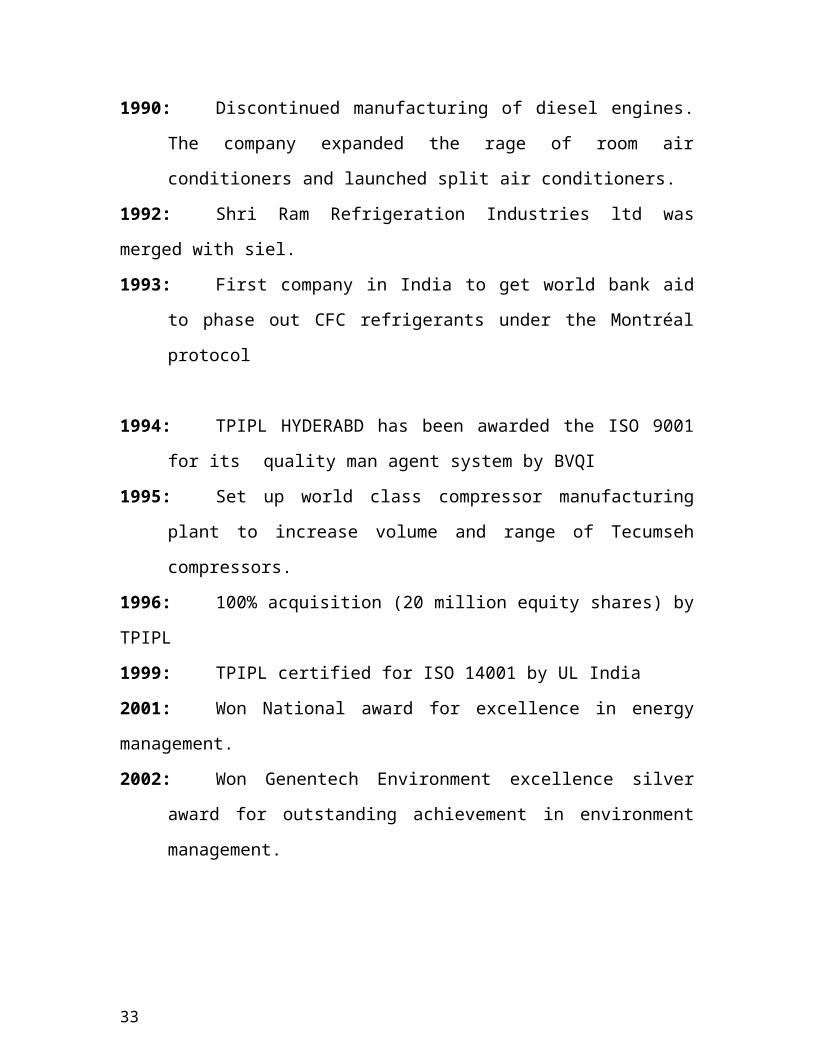

1961: Technical collaboration with wasting house electrical

international company USA.

1962: The name IRI was changed to USHA Refrigeration

Industrial Limited

1964: Started production of Wasting house compressors, this

is known as SRX

1966: The name of USHA refrigeration industries limited was

again changed to shri ram refrigeration industries limited

1967: Manufacturing of water coolers was added.

1969: Added manufacturing of diesel engines pumps sets

1986: started marketing electronics voltage connectors

1987: Added manufacturing of room air conditioners entered

into technical collaboration agreement with Tecumseh

products company USA worlds largest manufacturer of air

conditioning compressors.

1990: Discontinued manufacturing of diesel engines. The

company expanded the rage of room air conditioners and

launched split air conditioners.

1992: Shri Ram Refrigeration Industries ltd was merged with

siel.

1993: First company in India to get world bank aid to phase

out CFC refrigerants under the Montréal protocol

26

1994: TPIPL HYDERABD has been awarded the ISO 9001 for

its quality man agent system by BVQI

1995: Set up world class compressor manufacturing plant to

increase volume and range of Tecumseh compressors.

1996: 100% acquisition (20 million equity shares) by TPIPL

1999: TPIPL certified for ISO 14001 by UL India

2001: Won National award for excellence in energy

management.

2002: Won Genentech Environment excellence silver award

for outstanding achievement in environment management.

2003: Won Genentech Environment excellence silver award

award for outstanding achievement in environment

management.

2004: TPIPL has achieved the prestigious National award for

excellence energy efficient unit conducted by CII at

Chennai.

2005: Won Genentech safety award.

27

CERTIFICATIONS:-

ISO 9001-2000 VERSION:

As Tecumseh is ISO 9001-2000 certified company it makes all the

employees aware of the OSO norms. The topics covered under

this training program are

1. Back ground to revision of ISO 9001 standards

2. Concepts used in the new standard.

3. Process based quality management system model.

4. Alignment with other standard for example ISO –EMS 14000,

health and safety

5. Overview of 9001:2000

a) Scope

b) Application normative reference

c) Terms and definitions

6. Key definitions in new standards

7. Concept of continual improvement

Under overview of 9001-2000 the program also include

information on five clauses

28

1. Quality management system: It includes

a) General requirement

b) Quality management

c) Documents requirement

d) Control of document

e) Control of records

2. Management responsibility: It includes

Management commitment

Customer focus

Quality policy

Quality objectives

Responsibility and authority

Communication

Management review

3. Resource management: It includes:

a) Provision of resources

b) Human resource competence and awareness and training

c) Infrastructure

d) Work environment

4. Product realization: It includes

a) Planning of public relations

b) Customer related process

c) Customer communication design

29

d) Purchasing

e) Control of production

f) Service provision

g) Control of monitoring

h) Measuring devices

5. Measurements analysis and improvement Monitoring

and measurement of

a) Customers

b) Internal audit

c) Procedures

d) Product

I. Control of non conforming product

II. Data analysis

III. Corrective actions and improvements

IV. Preventive action

Due to exposure to ISO 9001-2000 norms and requirement the

employees know how to carry out their work. They know about

record maintenance and its importance. Thus making all the

employees aware of these standards it will be easy for the

organizations to produce quality products.

30

CHAPTER IIICONCEPTUAL FRAMEWORK

INVENTORY MANAGEMENT

Tecumseh Products India Private Limited.

31

INTRODUCTION:

Every enterprise needs inventory for smooth running of its

activities. It server as a link between the production and

distribution process. The greater a time lag, the higher the

requirement of inventory the unforeseen fluctuation of inventory

demand and supply of goods, fluctuating inventory prices,

necessitate the need for inventory management.

The investment inventory constitutes the most significant

part of the current assets inventory of the under taking. Thus it is

very essential to have a proper control and management of

inventory.

Meaning and nature of inventory

The general meaning of inventory is stock of goods or list of

goods inventory. In accounting language it means stock of

finished goods. For inventory manufacturing concern it includes

raw materials, work in progress, consumables finished goods and

spares etc.

32

1) Raw materials:

If forms a major input inventory in organization. The

quantity of raw materials required will be determined by

the rate of consumption.

2) Work in Progress :

The work in progress is that stage of stocks, which are in

between raw materials and finished goods.

3) Consumables :

These are the material, which are needed to smoothen, the

process of production. These do not directly go into

production, but act as catalyst.

4) Finished Goods :

These are the goods, which are ready to sale for the

consumers. The stock of finished goods provides as buffer

between production and market.

5) Spares:

Spares also from a part of inventory. The stocking policies

differ from industry to industry.

Inventories cost account for nearly 55 percent of the cost of

production, as it is clear from an analysis of financial statements

of large number of private and public sector organizations. So, It

33

essential to establish suitable procedures for proper control of

materials from the time of purchase order placed with supplier

until they have been consumed properly and accounted for.

Definition:

The term inventory refers to assets, which will be sold in

future in the normal course of business operations. The

assets, which the firm stores as inventory in anticipation of

need, are raw materials, work-in-progress/process, and

finished goods.

Inventory often constitute a major element of a total working

capital and hence ft has been correctly observed, 'Good

inventory management is good financial management’.

Inventory control is a system, which ensures the provision of

the required quantity at the required time with the minimum

amount of capital.

Inventories are the second largest asset category for the

manufacturing firms next to plant and equipment.

Inventory control includes scheduling, the requirements,

purchasing, receiving and inspecting, maintaining stock

records and stock control. Inventory control is a matter of

34

coordination. A proper material control helps in improving

the input-output ratio.

Objective of inventory management

The main objective of inventory management are operational and

financial. The operational object means availability of materials

and spares in sufficient quantities for undisturbed flow of

production. The financial objective means investments in

inventories should not remain idle and minimum working capital

should be locked in it.

THE OTHER OBJECTIVES ARE:

1) To ensure continues supply of inventories to the production.

2) To avoid over stocking and under stocking.

3) To maintain optimum level of investment in inventories.

4) To keep material cost under control, to keep low cost of

production.

5) To eliminate duplication in ordering or replacing stocks.

6) To minimize losses through, deterioration, pilferage, wastage

and damages.

7) Designing structures for good inventory management.

35

8) Perpetual inventory control of materials.

9) To ensure right quality of goods at reasonable prices. Analysis

of prices cost and value.

10) To facilitate data for short and long term planning and

control of

inventory.

NEED FOR INVENTORY CONTROL:

If a cost accounting system is to be effective there must be a

proper control of inventory and supplies form the time orders

are placed with suppliers until they have been effectively

utilized in production.

Materials are equivalent to cash and they make up an

important part of the total cost. It is essential that materials

should be properly safeguarded and correctly accounted.

Proper control of material can make a substantial

contribution to the efficiency of a business. The success of a

business concern largely depends upon efficient purchasing,

storage, consumption and accounting.

In a large firm the planning and routing department is

responsible for arranging how and where the work is to be

done and issue instructions. It sets definite time schedules

so that necessary materials are delivered to the proper

36

department in proper time not too long before hand neither

lest it should interfere with other work nor after they are

required as this result in idle time.

Business firm keep inventories for different purposes. Every

firm big or small trading or manufacturing has to maintain

some minimum level of inventories. Based on some motives

the inventories are maintained.

a. Transaction motives:

Every firm has to maintain some level of inventory to meet

the day-to-day requirements of sales, production process,

customer demand etc. In this finished goods as well as raw

material are kept as inventories for smooth production

process of the firm.

b. Precautionary motive:

A firm should keep some inventory for unforeseen

circumstances also like loss due to natural calamities in a

particular area, strikes, lay outs etc so the firm must have

some finished goods as well as raw-materials tc meet

circumstances.

c. Speculative motive:

The firm may be made to keep some inventory in order to

capitalize an opportunity to make profit due to price

fluctuations.

37

REASONS AND BENEFITS OF INVENTORY:

The optimal level of maintaining inventory is a subjective

matter and depends upon the features of a particular firm,

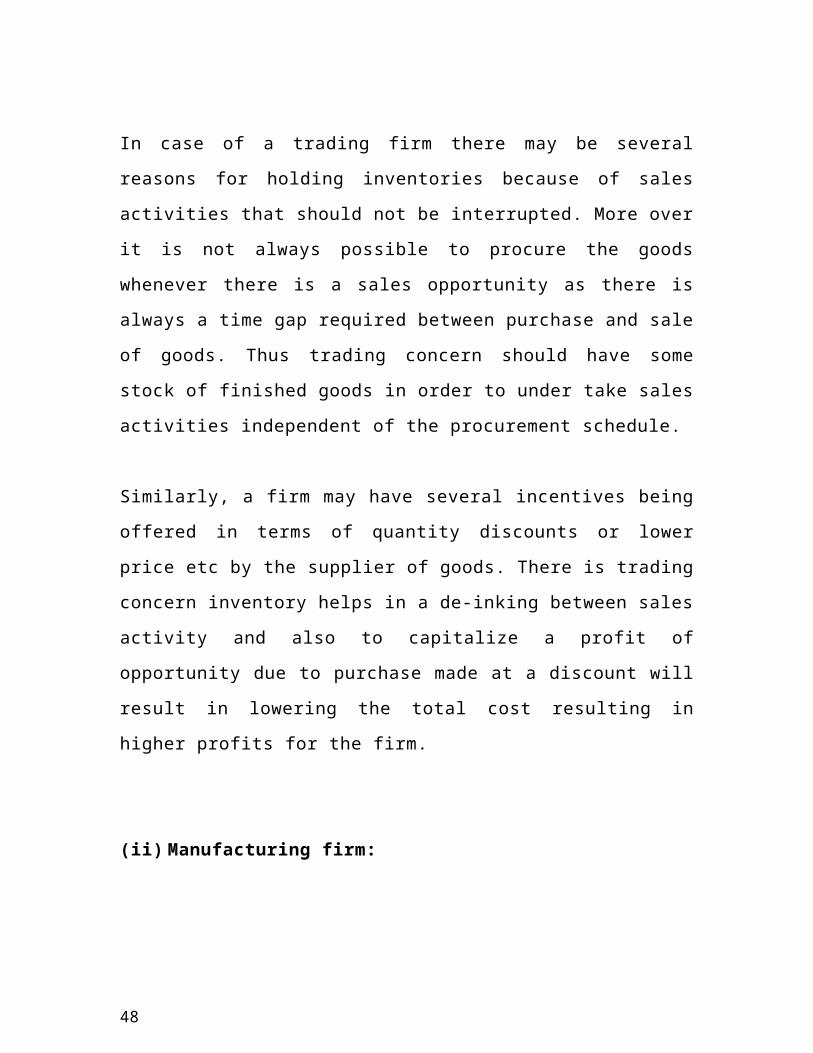

(i) Trading firm:

In case of a trading firm there may be several reasons for

holding inventories because of sales activities that should

not be interrupted. More over it is not always possible to

procure the goods whenever there is a sales opportunity as

there is always a time gap required between purchase and

sale of goods. Thus trading concern should have some stock

of finished goods in order to under take sales activities

independent of the procurement schedule.

Similarly, a firm may have several incentives being offered in

terms of quantity discounts or lower price etc by the supplier

of goods. There is trading concern inventory helps in a de-

inking between sales activity and also to capitalize a profit of

opportunity due to purchase made at a discount will result in

lowering the total cost resulting in higher profits for the firm.

38

(ii) Manufacturing firm:

A manufacturing firm should have inventory of not only the

finished goods, but also of raw materials and work-in-

progress for following reasons.

(a) Uninterrupted production schedule:

Every manufacturing firm must have sufficient stock of raw

materials in order to have the regular and uninterrupted

production schedule. If there is stock out of raw materials in

order to have the regular and uninterrupted production

schedule. If there is stock out of raw material at any stage of

production process then the whole production may come to a

half. This may result in custom dissatisfaction as the goods

cannot be delivered in time more over the fixed cost will

continue to be incurred even ff there is no production.

Further work-in-progress would let the production process

run smooth. In most of manufacturing concerns the work in

progress is a natural outcome of the production schedule and

it also helps in fulfilling when some sales orders, even if the

supply of raw-materials have stopped.

(b) Independent sales activity:

Inventory of finished goods is required not only in trading

concern but manufacturing firms should also have sufficient

stock of finished goods. The production schedule is a time

39

consuming process and in most of the cases goods cannot be

produced just after receiving orders. Therefore, every firm

has to maintain minimum level of finished goods in order to

deliver the goods as soon as the order is received.

ESSENTIALS OF INVENTORY CONTROL:

The important requirements of Inventory control are:

a) The proper co-ordination among the departments

involved in buying, receiving, inspecting, ciorage,

consuming and accounting.

b) Centralization of purchasing under the control of

competent buyer whenever possible.

c) Proper scheduling of material requirements.

d) Proper classification of materials with codes, material

standardization and simplification.

e) The operation of a system of internal check to ensure

that all transactions involving materials and

equipment are checked by properly authorized and

independent persons.

f) The storage of materials is well planned and kept in

properly. Planned and kept in properly designated

location, subject to adequate safeguard and

supervision.

g) The operation of a system of perpetual inventory so

that it is possible to determine at any time, the

amount and value of each kind of material in stock.

40

h) A suitable method of valuation of materials is essential

because it affects the cost of jobs and the value of

closing stock of materials.

Objectives of Inventory Control:

The main objectives of inventory control are:

i. To maintain a large size of inventory for efficient and

smooth production and sales operation.

ii. To maintain a minimum investment in inventories to

maximize profitability.

iii. To ensure a continuous supply of raw materials to

facilitate uninterrupted production.

iv. To maintain sufficient stocks of raw materials in

periods of short supply and anticipate price change.

v. Maintain sufficient finished goods inventory for

smooth sales operation and efficient customer

service.

vi. Minimize the carrying cost and time.

vii. Control investment in inventories and keep it at an

optimum level.

41

Advantages of Inventory Control:

The following are suggested advantages:

I. Eliminates wastage in use of material,

II. It reduces the risk of loss from fraud and theft.

III. It helps in keeping perpetual inventory and other

records to facilitate the preparation of accurate

material reports to management,

IV. To reduces the capital tied up in inventories,

V. It reduces cost of storage,

VI. It furnishes quickly and accurately the value of

materials used in various department.

VII. It prevents delays in production due to lack of

materials by supplying, proper quantities at the right

time.

Disadvantages of Inventory Control:

Every firm has to maintain optimal level of inventories. It not

the following will be the result in form of losses.

I. Opportunity cost: Every firm has to maintain inventory for

that some investment is needed it is know as Opportunity

cost and handle the investment in inventory are more the

42

funds are blocks up with inventory.

II. Excessive inventories: It will lead to firm losses due to

excessive carrying costs and the risk of liquidity. It is also

referred as Danger level

III. Inadequate Inventory: it is another danger which results is

production hold-up and failure to meet delivery

commitments .In adequate raw materials and work -in -

process inventors will results in frequent production

interruptions .It finished goods are not sufficient customers

may shifts to competitors.

IV. Danger due to physical decoration: It is one of the reason

with the inventories due to maintaining stocks at high

levels they will be deteriorated due to passage of time,

some times due to mishandling or improper storage

facilities.

Costs involved in inventory:

Every firms maintains inventory depending upon requirement

and other features of firm for holding such inventory some

cost will be incurred there are as follows:

(a) Carrying Cost;

This is the cost incurred in Keeping or maintaining an

inventory of one unit of raw materials, work-in -process or

finished goods. Here there are two basic cost involved.

43

(i) Cost of storage:

It includes cost of storing one unit of raw materials by the

firm. This cost may be for the storage of materials. Like rent

of spaces occupied by stock, stock for security, cost of

infrastructure, cost of insurance, and cost of pilferage,

warehousing costs, handling cost etc.

(ii) Cost of financing:

This cost includes the cost of funds invested in the

inventories .It includes the required rate of return on the

investments in inventory in addition to storage cost etc. The

Carrying cost include there fore both real cost and

opportunity cost associated with the funds invested in the

inventories.

The total carrying cost is entirely variable and rise in directly

proportion to the level of inventories carried.

Total carrying cost = (carrying Cost per unit) x (Average

inventory)

(b) Cost of ordering:

The cost of ordering includes the cost of acquisitions of

inventories. It is the cost of preparation and execution of an

44

order including cost of paper work and Communicating with

the supplier.

The total ordering cost is inversely proportion to annual

inventory of firm. The ordering cost may have a fixed

component, which is not affected by the order size: and a

variable component, which changes with the order size.

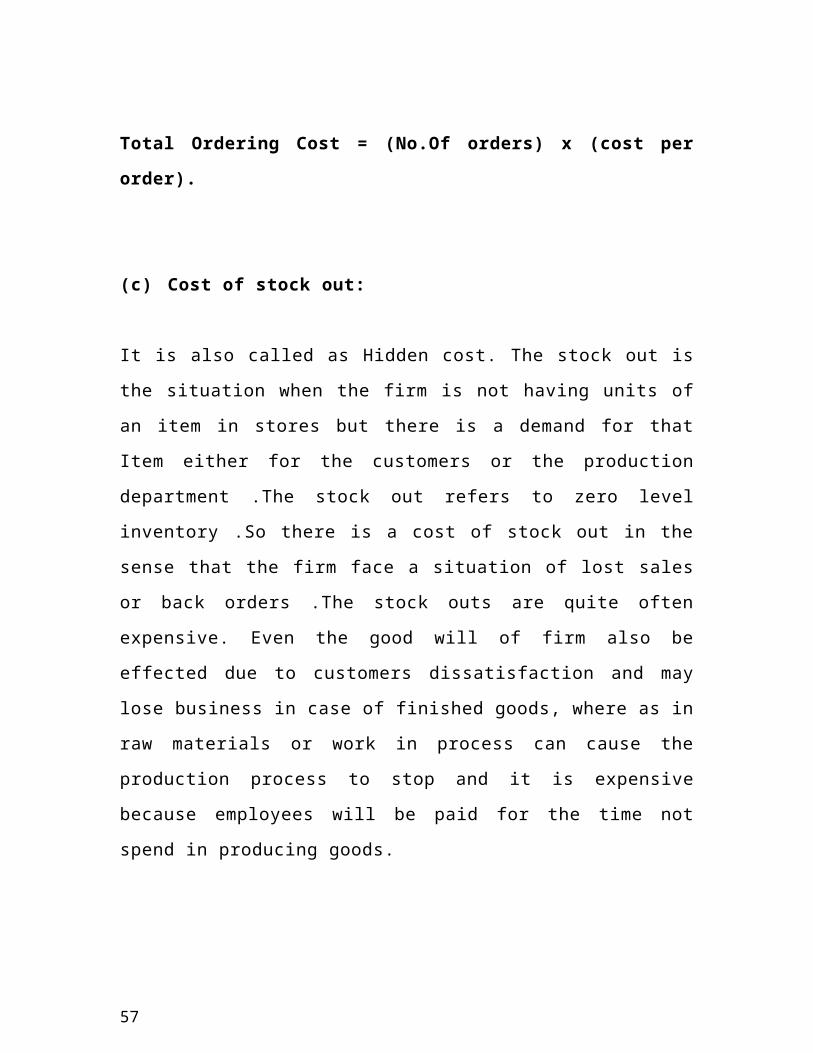

Total Ordering Cost = (No.Of orders) x (cost per

order).

(c) Cost of stock out:

It is also called as Hidden cost. The stock out is the situation

when the firm is not having units of an item in stores but

there is a demand for that Item either for the customers or

the production department .The stock out refers to zero level

inventory .So there is a cost of stock out in the sense that

the firm face a situation of lost sales or back orders .The

stock outs are quite often expensive. Even the good will of

firm also be effected due to customers dissatisfaction and

may lose business in case of finished goods, where as in raw

materials or work in process can cause the production

process to stop and it is expensive because employees will

be paid for the time not spend in producing goods.

45

The carrying cost and the ordering cost are opposite forces

and collectively. They determine the level of inventors in a

firm.

Total cost =(cost of items purchased) +(Total Carrying

and ordering cost)

Valuation of Inventory:

The methods of valuing inventory are combination of the

actual cost and replacement cost plans. The chief advantage

of the cost or net realizable value rule is that it is

conservative. Hence the methods of Valuation of inventory

are quite independent of system of mincing.

In balance sheet closing stock is shown under current assets

and is also credited to manufacturing or trading accounts.

The inventories are valued on the basis as follows.

Cost of raw materials in stock may include freight

charges and carrying cost. But such cost should not

exceed market price,

46

Work -in -process is generally valued at cost, which

includes cost of materials, labor. And the proportionate

factory overhead, as it is reasonable according to degree

of completion,

Cost of finished goods wound normally to be total or full

cost it includes prime cost plus appropriate amount of

the overhead. Selling and distribution cost is deducted

on the other hand work in progress may be valued at

work in progress may be Valued at work cost, marginal

cost, prime cost or, even at direct materials.

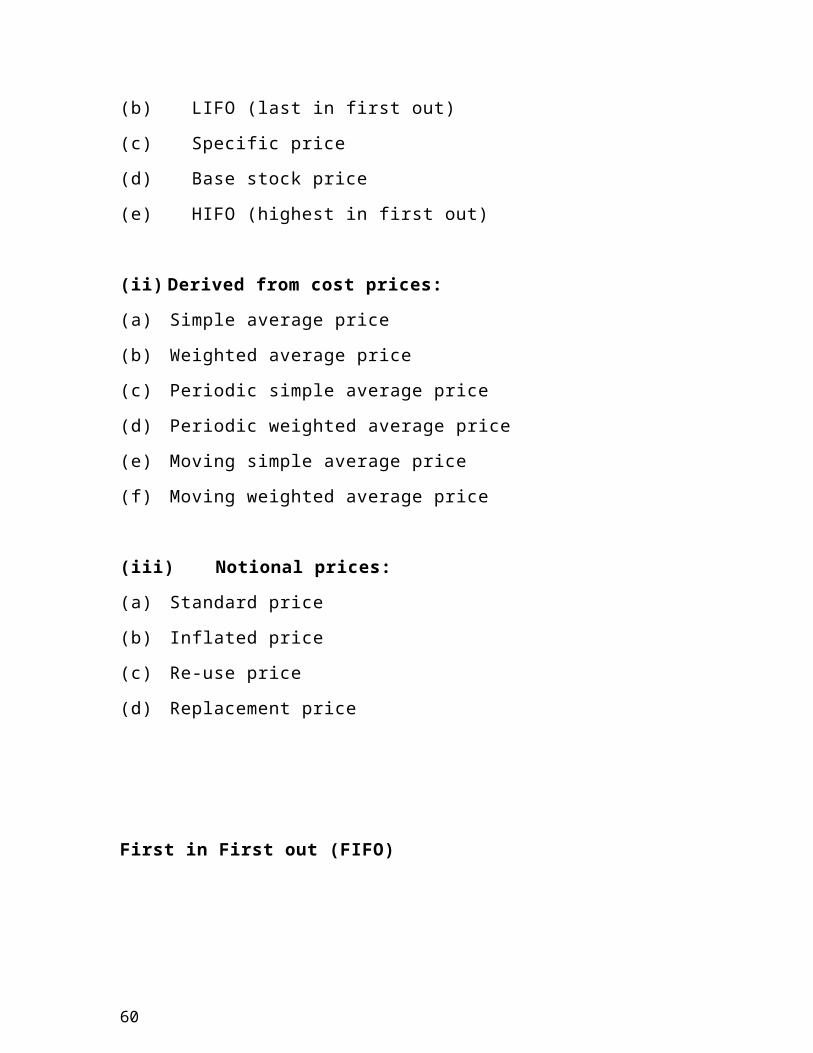

ISSUE PRICING METHODS:

There are two categories:

(i) Cost prices:

(a) FIFO (First in First out)

(b) LIFO (last in first out)

(c) Specific price

(d) Base stock price

(e) HIFO (highest in first out)

(ii) Derived from cost prices:

(a) Simple average price

(b) Weighted average price

(c) Periodic simple average price

47

(d) Periodic weighted average price

(e) Moving simple average price

(f) Moving weighted average price

(iii) Notional prices:

(a) Standard price

(b) Inflated price

(c) Re-use price

(d) Replacement price

First in First out (FIFO)

This is the price paid for the material first taken into stock

from which the material to be priced could have been drawn.

Under this method stocks of materials may not be used up in

chronological order but for pricing purpose it is assumed that

items longest in stock are used up first. The method is most

suitable for use where in material is slow-moving and

comparatively high unit cost.

Advantages:

i. Price is based on actual cost and not on basis of

approximations such as no profits or losses arises by

reasons of adopting this method.

48

ii. The resulting stock balance generally represents fair

commercial valuation of stock.

iii. It is based on traditional principles.

Disadvantages:

i. The number of calculations in the stores ledger

involved tends to be complicated with increase in

clerical error.

ii. The cost of consecutive similar jobs will differ if the

price changes suddenly,

iii. In times of rising prices, the charge to production is

unduly low as the cost of replacing the material will

be higher.

Last in first out (LIFO)

This is the price paid for the material last taken into stock

from which the materials to be priced could have been

drawn. This method also ensure material being issued at the

actual cost. Its use is based on the principle that costs

should be as closely as possible related to current price

level. Under this method production cost is calculated on

basis on replacement cost.

Advantages:

49

i. Production is charged at the most recent prices so that it

is based on the principle that cost should be related to

current price levels.

ii. It obviates the necessity for continuously ascertaining the

replacement price.

iii. Neither profit nor loss is usually made by using this

method.

iv. In the times of rising prices there is no wind fall profit as

would have been obtained under FIFO method.

Disadvantages:

i. Needs more clerical work.

ii. Compassion among similar jobs is very difficult.

iii. Stock valves relating to prices of the oldest cost on hand

may be entirely out of the current replacement prices.

Weighted average price:

This is the price which is calculated by dividing the total cost

of material in the stock from which the material to be priced

have been drawn, by the total quantity of material in the

stock. This method differs from all other methods because

here issue prices are calculated on receipts of materials and

50

not on issue of materials. Thus as soon as new lot is received

a new price is calculated and issues are then taken.

Advantages:

i. This method is advantageous where the price varies

widely as its use even out the effect of these wide

variations.

ii. The basis of price calculations is a simple one

involving only the division of total amount of material

in stock by quantity in stock.

iii. Calculation of new prices arises only when receipt of

stocks are received.

iv. Stock records under this method give a fair indication

of the stock values, which can be used in financial

analysis.

Disadvantages:

This method is completed than simple average because it

takes into consideration the total quantities and total costs

in stock.

i. Profit or loss may be incurred as in simple average

price,

ii. As LIFO or FIFO this method calls for many

calculations,

iii. In order to calculate the accurate value of issues the

average price must normally be calculated to four to

five decimal places.

51

Standard price:

It is the predetermination of fixed price on basis of a

specification of all factors affecting price like the quantity of

materials in hand and to be normally purchased and rate of

discount compared with existing price including or excluding

freight and ware housing expense.

A standard price for each material is set and the actual price

paid is compared with standard. It is paid exceeds the

standard a loss will be realized if not profit will be obtained.

Advantages:

i. This method is easy to operate.

ii. Comparing the actual prices with the standard price

will determine the efficiency of purchase department.

iii. The effect of price variations is eliminated from job

costs.

iv. It reduces classical costs by eliminating detailed cost

records.

v. In times of inflation or price fluctuations is very

difficult to fix a standard price.

vi. This method also incurs a profit or loss on issues and

closing stock.

Inflated price:

This is the price, which includes a charge designed to

cover the cost

52

of contingencies or related costs

This price includes not only the cost involved in bringing

the material

to the purchases premises but also the loss due to

evaporation and

Breakage etc. as well as carrying costs.

MATERIAL PURCHASING AND PURCHASING PROCEDURE

Purchase of material is one of the important function of material

management. At times more than 50% of the total product cost

is material.

Functions of Purchase Department

1. Deciding the items to be purchased based on demand.

2. Selection of sources of supply.

53

3. Collection the price information.

4. Placing the ordered.

5. Follow-up the ordered.

6. Checking the invoices.

7. Maintenance of purchase records.

8. Maintenance of vendors relations.

PURCHASE PROCEDURE

Purchasing procedure start with the initiation of purchase

requisitions and ends with the receipt of materials in the stores.

CENTERIZED PURCHASING

It is most important and relevant to large organizations operating

deferent plants may or may not be located at different places.

For a single place organization decentralization might be feasible

on a very limited place. But where as M & M Ltd., is a multiple

plants operating organization.

In Mahindra and Mahindra Centralized purchasing procedure is

following to purchase of materials.

Centralized purchasing avoids duplications of efforts and

working at cross purpose from one plant to another.

Centralized purchasing permits consolidation of order of

materials commonly used for two or more plants. The

54

ultimately results in greater buying power, favorable

contracts and trade agreements.

Easier to maintain the quality of purchased parts / items

through centralized testing and inspection. It is also

possible to conduct testing and inspection facilities.

Centralized purchasing permits to avail facilities like

quantity discounts and cash discounts thus its helps to

reduce cost.

It is beneficial to vendor also in case the size of order

constituted major proportion of his total production

capacity

TECHNIQUES OF INVENTORY MANAGEMENT:

Main problems in inventory management are to answer.

(i) Are all items of inventory important if not what are

items to be given more importance?

(ii) What should be the size of the order for

55

replenishment be placed?

(iii) What should be the over level?

To answer these following techniques are used,

Economic Order Quantity

ABC Analysis

VED Analysis

RE-ORDER Level

Safety Stock

Just-in-time Inventory

ABC Analysis:

It is based on proposition that

(ii) Managerial items and efforts are scare and limited

(iii) Some items of inventory are more important than

others.

56

ABC ANALYSIS:

ABC analysis classifies various inventory into three sets or

groups of priority and allocates managerial efforts in

proportion of the priority the most important item are

classified into class-A, those of intermediate importance are

classified as "class-B" and remaining items are classified into

class-C'.

The financial manager has to monitor the items belonging to

monitor the items belonging to different groups in that order

of priority and depending upon the consumptions.

The items with the highest value is given top priority and

soon and are more controlled then low value item. The re-

rational limits are as follows.

Category % of Items % of total materials

A 5-10 70-85

B 10-20 10-20

C 70-85 5-10

Procedure:

57

(i) Items with the highest value is given top priority and

soon.

(ii) There after cumulative totals of annual value of

consumption are expressed as percentage of total

value of consumptions,

(iii) Then these percentage values are divided into three

categories.

ABC analysis helps in allocating managerial efforts in

proportion to importance of various items of inventory.

ECONOMIC ORDER QUANTITY:

After various inventory items are classified on the basis of

the ABC analysis the management becomes aware of the

type of control that would be appropriate for each of the

three categories of the inventory items.

The determination of the appropriate quantity to be

purchased in each lot to replenish stock as a solution to the

order quantity problems necessitates resolution of conflicting

goals. Buying in a higher average inventory level will assure.

(i) Smooth production / sale operation and

(ii) Lower ordering or setup costs. But it will involve

higher carrying costs. On the other hand small orders would

reduce the carrying cost of inventory by reducing the

average inventory level but the ordering costs would

58

increase, as there is a likelihood of interruption in operations

due to stock-outs. A firm should not place either too high or

small orders on the basis of a trade off between benefits

derived from the availability of inventory and the cost of

carrying that level of inventory, appropriate or optimum level

of order to be placed should be determined. The optimum

level of inventory is popularly referred to as the economic

order quantity or economic lot size. It may be defined as that

level of inventory order that minimizes the total lost

associated with inventory management. It is based on some

assumptions, which are restrictive.

a. The firm knows with certainty the annual usage of a

particular item of inventory.

b. Rate at which the firm uses inventory is steady over

time.

c. The orders placed to replenish inventory stocks are

received at exactly that point in time when inventories

reach zero.

d.

EOQ can be illustrated by

(i) Trial and error approach,

(ii) Mathematical approach.

Trial and Error approach:

59

In this approach the procedure of procuring the inventory is

assumed the smaller the lot the lower is average inventory

and vice versa and high average inventory would involve

high carrying costs. This approach is used for determination

of EOQ uses different permutations and combinations of lots

of inventory purchases so as to find out the least ordering

and carrying cost combinations. The carrying cost and

acquisition cost for different sizes of order to purchase

inventories are computed and the order size with lowest total

cost of inventory is EOQ.

Mathematical Approach:

The EOQ quantity can use a short-cut method calculated by

following

EOQ=

Where,

A = Annual usage of inventory

B = Buying cost per order

C = carrying cost per unit

Limitations:

60

While using EOQ it should be noted that it suffers from

shortcomings, which are mainly due to the restrictive nature

of the assumptions on which it is based.

The important limitation is assumption of a constant

consumption usage and, the instant replenishment of

inventory is of doubtful validity

There may be unusual and unexpected demand for stocks to

meet such [contingencies the firm has to keen additional

inventories like safety stocks. Another weakness is to

assume known annual inventories is open to question and

there is likelihood of a discrepancy between the actual and

expected demand leading to wrong estimate of EOQ.

VED ANALYSIS:

Vital Essential and Desirable analysis is done mainly for

control of spare parts keeping in view of the criticality to

production.

Vital spares are spare the stock-out of which even for a short

time will stop production for quite sometime. Essential

spares are spares the absence of which cannot be tolerated

for more than a few hours a day. Desirable spares are those,

which are needed, but their absence for even a week or so

will lead to stoppage of production.

61

THE RE-ORDER LEVEL:

The re-order level is the level of inventory at which the fresh

order for that item must be placed to procure fresh supply.

The re-order level depends upon

a) Length of time between the placement of an

order and receiving the supply.

b) The usage rate of the item. The inventory is

constantly being used up. The rate at which the

inventory is being used up. The rate at which

the inventory is being used up is called the

usage rate.

The reorder level can be determined as follows:

R = M+tu

R = Reorder level

M = Minimum level of inventory

T = Time gap / delivery time

62

U = Usage rate

The reorder level and inventory patterns have be shown as

follows:

The figure shows that if the usage rate is constant, the

orders are made at even intervals for the same amounts

each time and the inventory goes to zero just before an

order is received.

Safety Stock:

The safety stock protects firm from Trade offs due to

unanticipated demand for the items level of inventory

investment is however increased by the amount of safety

63

stock. Safety level is ascertained in inventory as a part

because there is always an uncertainty involved in time lag

usage rate or other factor.

Usually smaller the safety level greater the risk of stock-

outs. If stock-levels are predictable then there is a chance of

stock out occurring. However stock inflows and outflows are

unpredictable or lesser predictable it becomes to carry

additional safety stock to prevent unexpected stock outs so

usage rate is estimated if cost is low then no safety stock is

needed.

JUST-IN-TIME INVENTORY:

The basic concept is that every firm should keep a minimum

level of inventory on hand, relying suppliers to furnish stock

64

just in time as and when required. JIT helps in emphasizing

sufficient levels of stocks to ensure that production will not

be interrupted. Although the large inventories may be bad

idea due to heavy carrying JIT is a modern approach to

inventory management and the goal is essentially to

minimize such inventories and there by maximizing the

turnover.

JIT system significantly reduces inventory-carrying cost by

requiring that the raw materials be procured just in time to

be placed into production. Additionally the work in process

inventory is minimized by eliminating inventory is minimized

by eliminating inventory buffers between different

production departments.

If JIT is to be implemented successfully there must be a high

degree of coordination and co-operation between the

supplier and manufacturer and among different production

centers. JIT does not appear to have any relation with EOQ

however it is in fact alters some of the assumptions of EOQ

model. The average inventory level under the EOQ model is

defined as

Average inventory= 1/2 EOQ + safety level JIT attacks this

equation in two ways.

(i) By reducing the ordering cost

(ii) By reducing the safety stock.

65

The basic philosophy in JIT is that the benefits, associated

with reducing inventory and delivery time to a bare minimum

through adjustment in the EOQ model; will more than offset

the costs associated with the increased possibility of stock-

outs.

66

CHAPTER IV

DATA ANALYSIS

DETERMINATION OF STOCK LEVELS

Carrying of to much and too little of inventories is determinate to the firm. If the inventory level is too little, the

67

firm will face frequent stock – outs involving heavy ordering cost and if the inventory level of inventory where costs are the minimum and at the same time their ID.No.Stock-out, which may result in loss of sale or stoppage of production. Various stock levels are discussed below.

MINIMUM STOCK LEVEL

This is the lower limit below which the stock of any item should not normally be allowed to fall. This is also technically known as safety or buffer stock. The prime considerations in fixing the minimum stock level or safety stocks are :

a. Average rate of consumption.b. Lead time.

Minimum Stock Level = Reordering level - (Normal consumption X Normal Reorder Period)

Lead-Time :

A purchasing firm requires some time to process the order and time is also required by the supplying firm to execute the order. The time taken processing the order and the executing it is known as lead-time. It is essential to maintain some inventory during this period.

Reorder Level :

Reorder level is fixed between the minimum and maximum levels. When stock of a material reaches at this point, the store keeper should initiate action for the purchase of material. The reorder level is slightly more than minimum stock level to guard against

a. Abnormal usageb. Abnormal delay in supply

68

Reorder level = Maximum consumption X Maximum period required

during the period for delivery

MAXIMUM STOCK LEVEL :

Maximum stock level represents the upper limit beyond which the quantity of any item is not normally allowed to rise. The main object of establishing this limit is to ensure that unnecessary working capital is not blocked in stores. Theoretically, maximum stock level is the sum – total of minimum stock level and economic order quantity.

Maximum level = Reorder Level + Reordering quantity – Minimum consumption.

AVERAGE STOCK LEVEL :

The average stock level is calculated as such :

Average stock = minimum stock level + ½ of re-order quantity.

DANGER LEVEL :

This is generally fixed below the minimum stock level. Normal stock should not be below the minimum level. If it reaches the danger level at any point of time, urgent action for replenishment of stock must be taken to prevent stock out.

ESTIMATION OF STOCK LEVELS :

There are different techniques used in the calculation of the stock levels.

Reordering Quantity - 2500 units

Reordering Period - 4 – 5 weeks

69

Weekly usage :-

Maximum usage - 900 units

Normal usage - 700 units

Minimum usage - 500 units

Reordering Level = Maximum consumption X Maximum Reordering Period

= 900 X 5 = 4500 units.

Ex :- Consider “Load King” for calculation purpose.Calculated of the load king compressor as 500 units.

Normal Daily consumption = 700 units

Normal Reorder period = 4.5 weeks

Reorder level = 4500 units

Minimum usage = 500 units

Minimum Reorder period = 4 weeks

Maximum Reorder period = 5 weeks

MINIMUM STOCK LEVEL

= Reorder Level – (Normal consumption X Normal

Reorder Period)

= 4500 – (700 X 4.5)

= 4500 – 3150

= 1350 Units

MAXIMUM STOCK LEVEL

70

= Reorder Level + Reorder Quantity – (Minimum

consumption X

Minimum Reorder

Period)

= 4500 + 2500 – (500 X 4)

= 7000 – 2000

= 5000 Units

AVERAGE STOCK LEVEL

= Minimum stock + ½ of Reordering Quantity.

= 500 + (½ X 2500)

= 500 + 1250

= 1750 Units

Minimum Stock Level = 1350 Units

Average Stock Level = 1750 Units

Maximum Stock Level= 5000 Units

INVENTORY TURN OVER RATIO

“A Ratio which measures the number of times a firms average inventory is sold during a year” – Kohler.

Computation of inventory turn over ratios for different items of materials and comparison of the turnover ratios provide a useful guidance for measuring inventory performance. A high turnover rate indicates that the material in question is a fast moving one. A low turnover rate on the other hand indicates over investments and looking up of working capital on undesirable items.

71

“Inventory or Stock turnover is measured in terms of the ratio of the value of materials consumed to the average inventory during the period”. The ratio indicates the number of time the average inventory is consumed and replenished by dividing number of days for which the average inventory is held can be ascertained.

Comparing the number of days in the case of two different materials, it is possible to known which is fast moving and which slow on that basis attempt may be made to reduce the amount of capital locked up and prevent over stocking of slow moving items.

Average Inventory = Opening Stock + Closing Stock 2

Inventory turnover ratio = Material consumed Average Inventory

Inventory turnover in number of days = Number of days in a year

Inventory turnover ratio

INVENTORY TURNOVER RATIO

Cost of goods soldINVENTORY TURNOVER RATIO =------------------------------

Average inventory

(Rs in 000’s)Year Cost of goods

soldAverage inventory

Ratio

2002-03 2563442 358048 7.162003-04 2210210 439610 5.032004-05 2163508 528333 4.092005-06 2484589 596074 4.17

72

2006-07 3044561 697949 4.362007-08 4120957 1008066 4.09

INVENTORY HOLDING RATIO

365INVENTORY HOLDING RATIO=---------------

Inventory turnover ratio(Rs in 000’s)

Year Days Inventory turn over ratio

Inventory holding ratio

2002-03 365 7.16 512003-04 365 5.03 732004-05 365 4.09 892005-06 365 4.17 882006-07 365 4.36 842007-08 365 4.09 89

Ratio

7.76

5.034.09 4.17 4.36 4.09

0

1

2

3

4

5

6

7

8

9

2002-03 2003-04 2004-05 2005-06 2006-07 2007-08

Ratio

73

INVENTORY ANALYSIS AT TECUMSEH INDIA PRODUCTS PVT.LTD

(Rs in 000’s)Year Inventory Current assets % in inventory

&CA2002-03 495036 909946 54.402003-04 561630 1078274 52.092004-05 630518 1500977 42.012005-06 765380 1688733 45.322006-07 1250752 2307604 54.202007-08 1312456 2504689 55.23

Inventory holding ratio

51

7389 88 84 89

0102030405060708090

100

2002-03

2003-04

2004-05

2005-06

2006-07

2007-08

Inventory holding ratio

74

% in inventory &CA

54.4 52.0942.01 45.32

54.2 55.23

0

10

20

30

40

50

60

1 2 3 4 5 6 7 8

% in inventory &CA

YEARS 2008 2007 2006 2005 2004 2003

Opening Inventory (Rs. In Lakhs)

49970

45675

46904

55253

51554

43697

Closing Inventory(Rs. In Lakhs)

75983

49970

45675

46904

55253

51554

INVENTORY TURNOVER RATIO

YEARS

INVENTORY

CONSUMED (Rupees in Lakhs)

AVERAGE INVENTOR

Y(Rupees in

Lakhs)

INVENTORY

TURNOVER RATIO

INVENTORY

TURNOVER IN

NUMBER OF DAYS

75

March – 2008

459537.10

49970 + 75983

2= 62976.5

459537.1062976.5= 7.296

365..7.296

= 50.027

March – 2007

335286.52

45675 + 49970

2= 47822.5

335286.5247822.5= 7.01

366..7.01

= 52.21

March – 2006

250021.84

46904 + 45675

2= 46389.5

250021.8446389.5= 5.389

365..5.389

= 67.73

March – 2005

211723.1

55253 + 46904

2= 51078.5

211723.151078.5= 4.145

365..4.24

= 88.05

March – 2004

235858.13

51554 + 55253

2= 53403.5

235858.1353403.5= 4.416

365..4.41

= 82.65

March – 2003

221023.23

53697 + 51554

2= 47625.5

221023.2347625.5= 4.64

366..4.64

= 78.87

76

INVENTORY TURNOVER RATIO

4.64 4.416 4.1455.389

7.01 7.296

012345678

2003 2004 2005 2006 2007 2008

YEARS

% O

F

INV

EN

TO

RY

INVENTORY TURNOVER RATIO

INVENTORY TURNOVER RATIO

4.64 4.416 4.1455.389

7.01 7.296

012345678

2003 2004 2005 2006 2007 2008

YEARS

% O

F I

NV

EN

TO

RY

INVENTORY TURNOVER RATIO

77

INVENTORY IN NUMBER OF DAY

78.87 82.65 88.05

67.7352.21 50.027

0

20

40

60

80

100

2003 2004 2005 2006 2007 2008

YEARS

INVENTORY IN NUMBER OF DAY

78

I NV

EN

TO

RY

IN

NU

MB

E R O

F D

AY

S

INERPRETATION:

A high turnover ratio indicates that the material in question is a

fast moving one and also a low amount of stocks are replacing

stocks in large number of installment. In the year 2006, 2007,

2008, the stock turnover ratio is gradually decreasing and the

inventory faced a bad position in these three years. And from

2003, 2004, 2005, the stock turnover ratio continuously

increased from 5.38 to 7.296 and the inventory in number of

days is low. This position indicates that the stocks are fast

moving and get converted in to sales quickly.

INVENTORY IN NUMBER OF DAY

78.87 82.65 88.05

67.7352.21 50.027

0

20

40

60

80

100

2003 2004 2005 2006 2007 2008

YEARS

INV

EN

TO

RY

IN

NU

MB

ER

OF

DA

YS

INVENTORY IN NUMBER OF DAY

79

COMPRESSOR PRODUCTION AND DISPATCH

YEAR

COMPRESSOR PRODUCTION (QUANTITY IN

MIL.UNITS)

COMPRESSOR DISPATCH

(QUANTITY IN MIL.UNITS )

MARCH 31ST 2006 25,797 25,416

MARCH 31ST 2007 34,186 33,766

MARCH 31ST 2008 33,630 33,885

COMPRESSOR PRODUCTION & DISPATCH

0

5000

10000

15000

20000

25000

30000

35000

40000

2006 2007 2008

YEARS

P R O D U C TI

O N

&

DIS

PAT

CH

Production

Dispatch

80

INERPRETATION:

The inflow of raw materials and dispatch of finished goods from

the organization is in good position. In march 31st 2006 the

difference between the compressor production and dispatched is

381 and in march 31st 2005 the close stock in the go down is also

dispatched from the organization and as well as in the year 2007

31st march the stored compressors are dispatched from the

company. This indicates that the consuming storage cost is very

low and risk related to preservation of the stock is very less.

81

CHAPTER VFINDINGS

82

FINDINGS

On the personnel interaction with the financial department as

well as with the primary and secondary arrived they are :

1. The analysis is carried out for a period of five years i.e

2003-2004 to 2007-2008 is not sufficient to conclude the

inventory positions of the company as well taken up to

study for a period of 6 weeks Is too less still we strived

out best in exploiting the present inventory positions of

the company

2. Inventory valuations is followed in weighted average

method based on cost concept of the project costing is

undertaken.

3. The inventory is different items of production hence ABC

analysis and two bin system are followed

4. Some items are found to be slow and non moving the

slow moving items are spare and consumable goods

hence whenever necessary arises these items are being

used non moving items are also found in the inventory.

5. The reasons for non moving of inventory from stores are

studied. Due to MOQ(Minimum order quantity) clause

these items procured extra than the requirement.

6. The high inventory turnover ratio at indicates efficiency

of the firms inventory management

7. The material consumption was also increasing

simultaneously with sales.

83

8. The company s efficiency in turning its inventory is

increasing. The companies utilization of inventory in

generating sales is good they yearly holing of all types of

inventory is decreasing this is positive trend

9. The company efficiency in turning the inventory is

increasing the company’s utilization of inventory in

generating sales is good the yearly holing of all types of

inventory is decreasing this is positive trend.

10. The over all inventory position of the company is

satisfactory.

84

CONCLUSIONS

CONCLUSIONS

85

To days business scenario inventory management is

becoming very crucial part of the organization. The system of

inventory management in Tecumseh India products private

limited very effective. The organization is basically and

assembling unit and thus inventory place a most significant role

in the decision making process. From the various calculations

and figures relating to inventory management it is clear that the

inventory classification of A items are maintain for 1 – 3 days, as

a result it reduce investment in raw material, reducing the lead

time and also the large quantity discount because the stock are

kept for 1 – 3 days.

In the classification of ABC items XYZ procedure is following

in Tecumseh Plant has launched the different type of KANBAN

card system for class C items.