International Personal Finance Investor road show - Paris · PDF fileInternational Personal...

38

www.ipfin.co.uk International Personal Finance Investor road show - Paris Gerard Ryan – Chief Executive Officer David Broadbent – Finance Director 20 March 2013

Transcript of International Personal Finance Investor road show - Paris · PDF fileInternational Personal...

www.ipfin.co.uk

International Personal Finance

Investor road show - Paris

Gerard Ryan – Chief Executive Officer

David Broadbent – Finance Director

20 March 2013

www.ipfin.co.uk

• Profitable growth business

• A resilient business model

• Consistently strong trading and financial

performance

• Growth strategy building momentum

International Personal Finance

2

www.ipfin.co.uk

Profitable growth business

3

www.ipfin.co.uk

• Leading international consumer credit provider

• Small sum consumer loans

• Listed on the London Stock Exchange in 2007

• Circa £1BN market capitalisation

• 6,330 employees and 28,500 agents around the world

International Personal Finance

2.4m

customers

£95.1M

2012 PBT

28,500

agents

6

markets

4

www.ipfin.co.uk

Our markets

5

Poland

2012 PBT £54.9M

Customers 821,000

Established 1997

Czech-Slovakia

2012 PBT £27.1M

Customers 383,000

Established 1997/2001

Hungary

2012 PBT £12.5M

Customers 268,000

Established 2001

Romania

2012 PBT £4.5M

Customers 260,000

Established 2006

Mexico

2012 PBT £9.2M

Customers 683,000

Established 2003

2012 PBT adjusted to account for change in interest allocation

www.ipfin.co.uk

6

A valued and responsible business

Non-banking lender with most

ethical approach 2012 - Czech

Republic

Customer Friendly Company

2012 - Poland

Pearl of the Polish

Economy 2012 - Poland

Ranked amongst best scoring

financial services companies

for environmental and social

governance ratings

www.ipfin.co.uk

Good growth and strong returns

2,415

1,781

2006 2012

Customers (‘000s)

Profit before tax (£M)

• 78% growth since 2006

• 138% growth since 2006

• All markets profitable

• 36% growth since 2006

• 56% customer retention

– customers on third or

subsequent loan

Revenue (£M)

• 163% growth since 2006

10.5

27.6

2006 2012

EPS (p)

39.9

95.1

2006 2012

7

365.3

651.7

2006 2012

www.ipfin.co.uk

Strong record of growth

Profit before tax (£M)

39.9

50.6

76.3

61.7

100.595.1*

92.1*

0

10

20

30

40

50

60

70

80

90

100

110

2006 2007 2008 2009 2010 2011 2012

* 2010 profit stated before exceptional charge of £3.9M. 2012 profit stated before exceptional restructuring charge of £4.8M

8

Impairment % revenue

29.3%

21.8%23.2%

29.9%27.6%

25.8%27.0%

0%

5%

10%

15%

20%

25%

30%

35%

2006 2007 2008 2009 2010 2011 2012

www.ipfin.co.uk

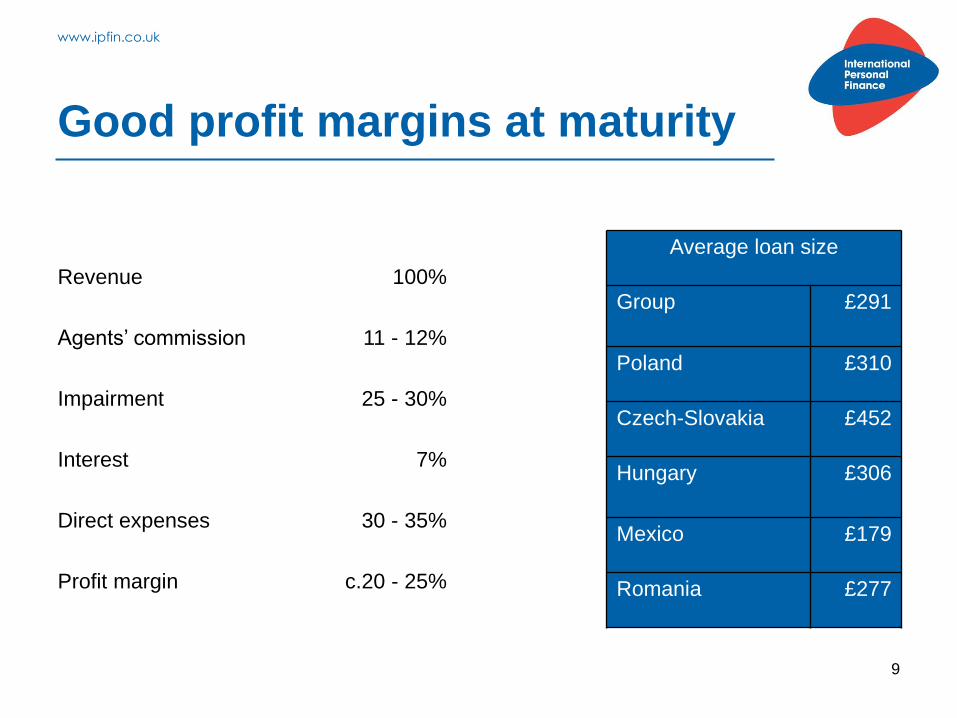

Good profit margins at maturity

Revenue 100%

Agents’ commission 11 - 12%

Impairment 25 - 30%

Interest 7%

Direct expenses 30 - 35%

Profit margin c.20 - 25%

9

Average loan size

Group £291

Poland £310

Czech-Slovakia £452

Hungary £306

Mexico £179

Romania £277

www.ipfin.co.uk

A resilient business model

10

www.ipfin.co.uk

Home credit business model

• Long-established, resilient and cash generative business model

• Simple, transparent, affordable and personal

• Small sum, short-term unsecured cash loans in local currency

• £50 - £1,000 loans repaid over a period of around 12-14 months

• Loans repaid by money transfer or optional home collection service

• Agents provide weekly face-to-face visits to customers in their homes

• Credit vetting in the home by agent, supported by application and behavioural scoring

• Low and grow lending strategy

• No default penalty charges on home collected loans

11

www.ipfin.co.uk

• Recognised financial brand: 70%+ awareness in most

markets

• 28,500 agents provide powerful engine for effective and cost

efficient customer acquisition

• National and regional advertising

• Internet growing in importance in marketing mix

• Strong retention – high proportion of eligible customers

renew loans

• Strong focus on lifetime value

Sales process

12

www.ipfin.co.uk

Powerful credit management systems

Agents

• Development of customer relationship

• Assessment of customer character, circumstances and capacity to pay

Systems

• Application scoring

• Behavioural scoring

• Centralised arrears management

• Prudent provisioning

Business Model

• Agents remunerated based on collections

• Lending based on disposable income not asset value

• No introductory offers

Credit risk based around relationship between customer and agent, supported by

application and behavioural scoring systems

13

www.ipfin.co.uk

Collections process

Field based collections Debt recovery

Wri

te o

ff –

12

we

ek

s n

on

-pa

ym

en

t

• Agent collects weekly

• Customers in arrears managed via

a combination of:

- letters

- Development Manager visits

- centralised telephone calls

• Process escalates as arrears

increase

• Central arrears management in all

markets

• Balances recovered through:

- letters

- calls

- collection agencies

- court action

• Typically collect 10 - 20% of write off

14

www.ipfin.co.uk

Prudent provisioning methodology

• Weekly Assessment

• Using third party developed actuarial models to estimate amount and timing of future cash flows

Impairment calculated

• In the event of any missed payment or portion of a payment even if agent fails to call

• No re-ageing of ‘poor’ payers

Impairment charge

• Systematic, with no management intervention

• Separate for each product in each country Models

• Formally reviewed on a regular basis to ensure reflects current performance

Provisions

Short-term loans and prudent provisioning means impairment charged to income

statement quickly

15

www.ipfin.co.uk

• Quoted UK plc on FTSE250 complying with all listing requirements

• Globally ranked in top 3 of FTSE4Good for environmental, social and corporate

governance management

• Regulated as a financial enterprise in Hungary by the PSZAF (Hungarian Financial

Supervisory Authority)

• Registered in the General Register of Non-banking Financial Institutions of the National

Bank of Romania

• In all other markets operating under local consumer credit legislation

• Proactive approach to monitoring regulatory change and involvement in policy

development

• Operate in rate cap environments (Poland 2006, Slovakia 2010, Hungary 2011)

• EU Consumer Credit Directive now implemented in all European markets

Regulation

16

www.ipfin.co.uk

Consistently strong trading

and financial performance

17

www.ipfin.co.uk

18

• Strategy for growth building momentum

• Strong underlying trading performance continued

• Further improvement in Mexico

• Good returns

• Robust balance sheet and funding position

2012 highlights

www.ipfin.co.uk

19

Strong underlying trading performance

• £95.1M profit – strong underlying profit

increase of £20.3M

• Three key drivers:

1. Accelerating revenue growth

2. Impairment in middle of target range

3. Costs managed tightly

£100.5M

£10.8M

£14.9M£20.3M

£95.1M

2011 PBT Underlying

increase

Weaker FX

rates

Additional

ESR costs

2012 PBT

www.ipfin.co.uk

20

Good returns

• Adjusted earnings per share of 27.6 pence

• Interest cover 3.3x

• Return on equity of 20.1%

• £25M share buyback completed

• Proposed full year dividend increase of 9%

to 7.7 pence per share

6.3p

7.1p

7.7p

2010 2011 2012

Increasing dividend

www.ipfin.co.uk

21

We lend short and borrow long

Receivables

£M

%

Borrowing

facilities

£M

%

Less than one year 627 96 16 5

Later than one year 23 4 295 95

650 100 311 100

At 31 December 2012

www.ipfin.co.uk

22

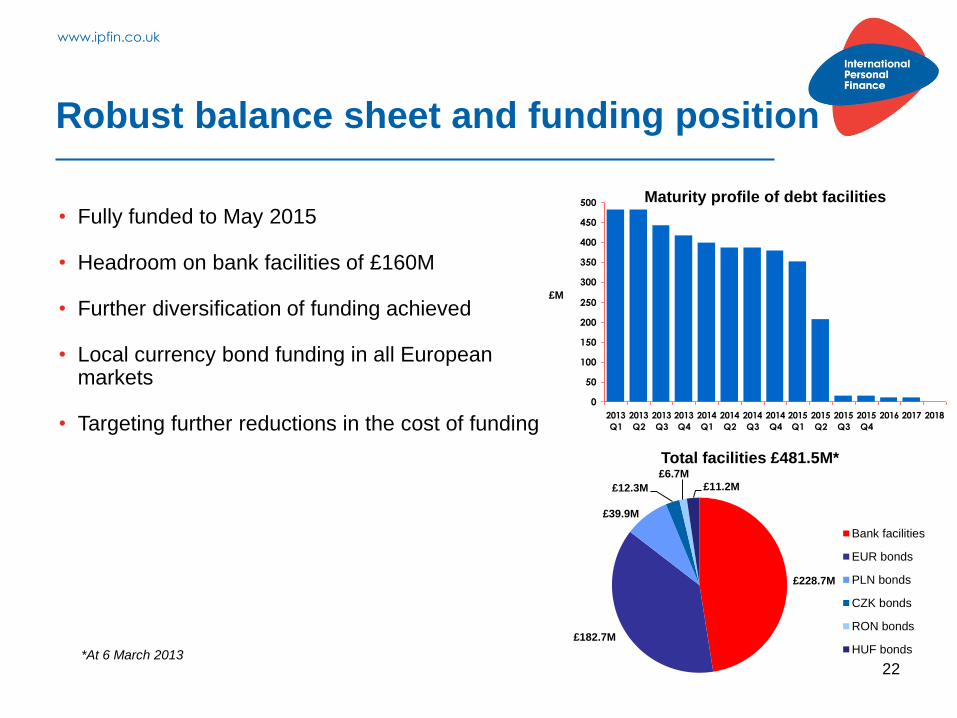

Robust balance sheet and funding position

• Fully funded to May 2015 • Headroom on bank facilities of £160M

• Further diversification of funding achieved • Local currency bond funding in all European

markets • Targeting further reductions in the cost of funding

Maturity profile of debt facilities

£M

0

50

100

150

200

250

300

350

400

450

500

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

2014

Q3

2014

Q4

2015

Q1

2015

Q2

2015

Q3

2015

Q4

2016 2017 2018

*At 6 March 2013

£228.7M

£182.7M

£39.9M

£12.3M

£6.7M

£11.2M

Total facilities £481.5M*

Bank facilities

EUR bonds

PLN bonds

CZK bonds

RON bonds

HUF bonds

www.ipfin.co.uk

23

58.5%59.2%

57.8%

Target

55%

• Gearing low and stable at 0.8x

• £25M buyback completed in November

• Equity represents 57.8% of receivables

• Capacity to invest in growth opportunities

Equity to receivables

Robust balance sheet and funding position

Dec 2011 Jun 2012 Dec 2012

www.ipfin.co.uk

Growth strategy

building momentum

www.ipfin.co.uk

25

Our strategy for growth

Expand footprint

Improve customer engagement

Develop sales culture

Execution

www.ipfin.co.uk

26

• Adjacent market strategy

• Shorten J-curve

• Leverage existing infrastructure

• Reduce costs

• Favourable business environments

• Demand for shorter-term, lower value loans

• Positive economic prospects

• Controlled pilots to assess potential

• Expected £4M - £5M investment in 2013

Bulgaria

• 7.2 million population

• Retail banks dominate larger

loan supply

• Non-bank operators serving

target customers

Lithuania

• 3.2 million population

• Reduced lending by banks

• Some fast cash providers

Planned market entries in 2013

www.ipfin.co.uk

27

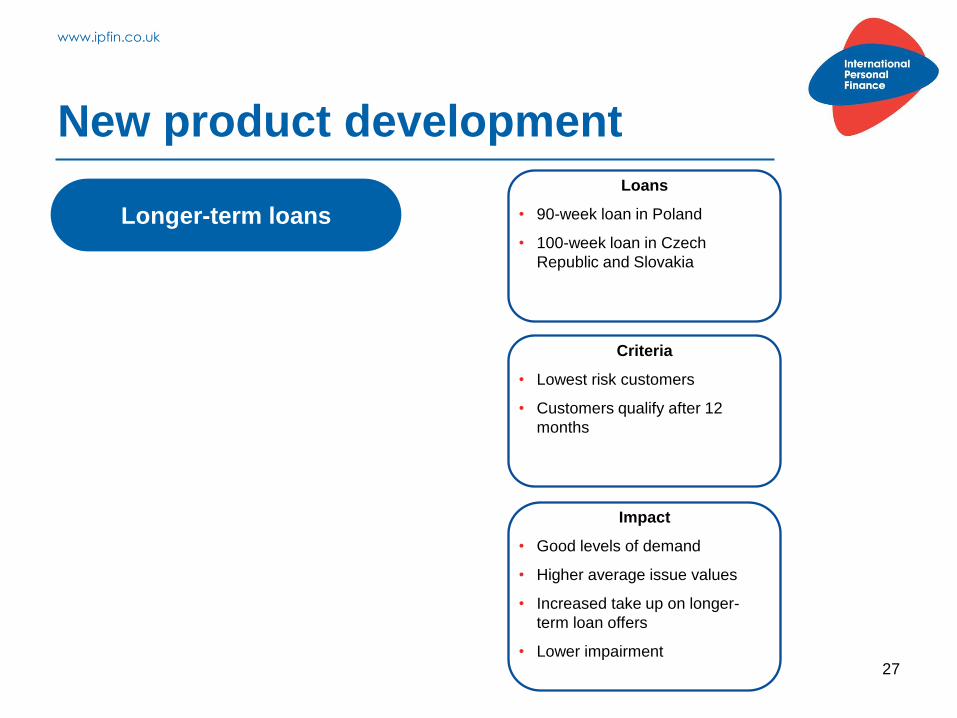

New product development

Criteria

• Lowest risk customers

• Customers qualify after 12

months

Impact

• Good levels of demand

• Higher average issue values

• Increased take up on longer-

term loan offers

• Lower impairment

Loans

• 90-week loan in Poland

• 100-week loan in Czech

Republic and Slovakia

Longer-term loans

www.ipfin.co.uk

28

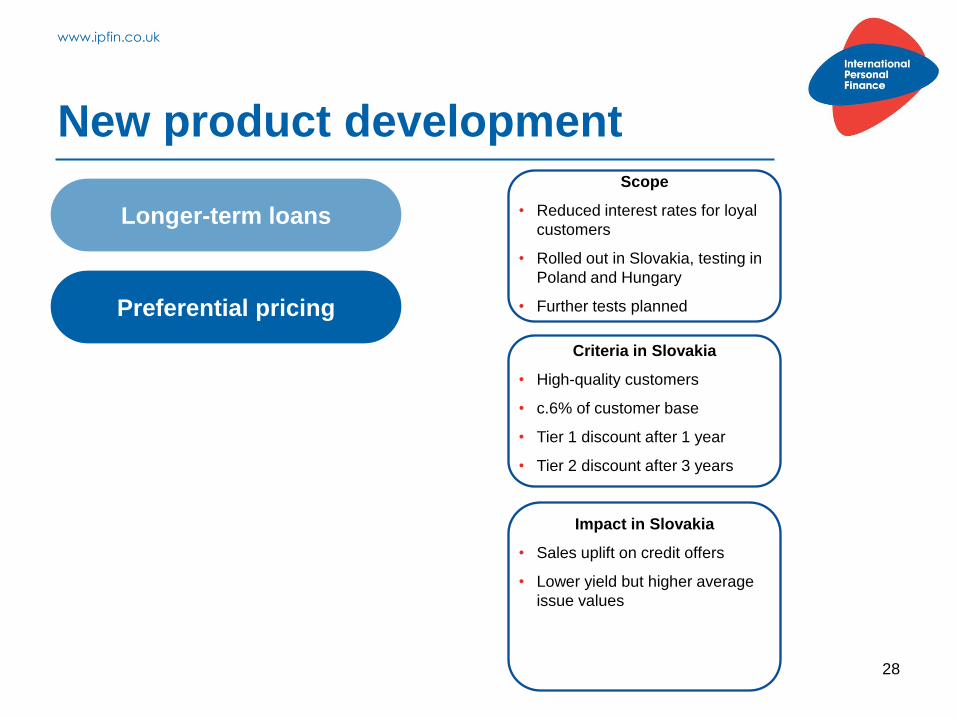

New product development

Criteria in Slovakia

• High-quality customers

• c.6% of customer base

• Tier 1 discount after 1 year

• Tier 2 discount after 3 years

Impact in Slovakia

• Sales uplift on credit offers

• Lower yield but higher average

issue values

Scope

• Reduced interest rates for loyal

customers

• Rolled out in Slovakia, testing in

Poland and Hungary

• Further tests planned

Longer-term loans

Preferential pricing

www.ipfin.co.uk

29

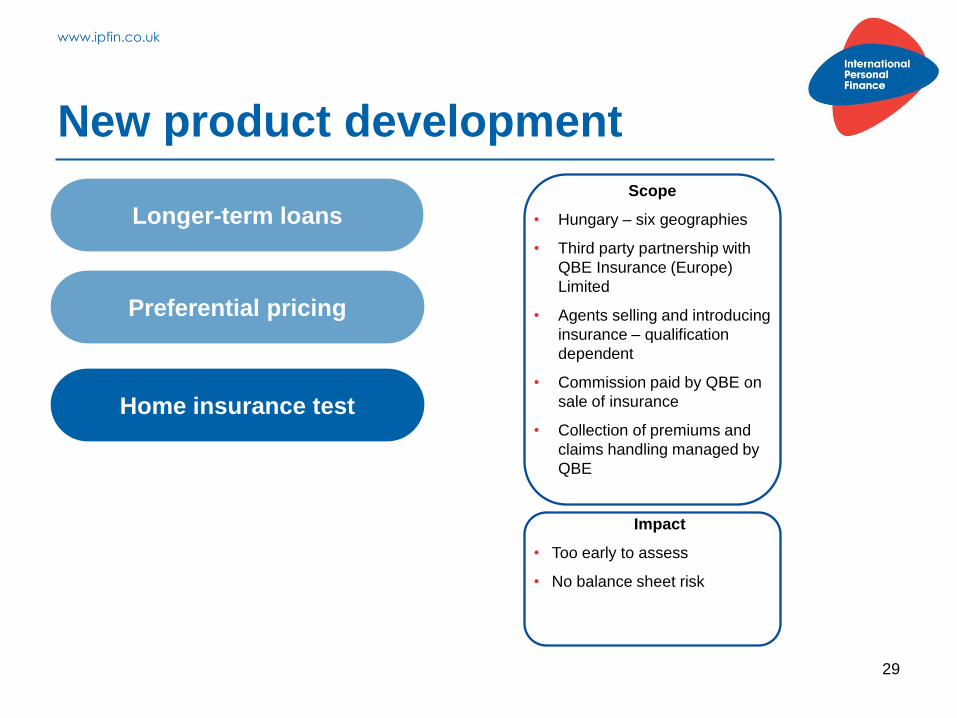

New product development

Scope

• Hungary – six geographies

• Third party partnership with

QBE Insurance (Europe)

Limited

• Agents selling and introducing

insurance – qualification

dependent

• Commission paid by QBE on

sale of insurance

• Collection of premiums and

claims handling managed by

QBE

Impact

• Too early to assess

• No balance sheet risk

Longer-term loans

Preferential pricing

Home insurance test

www.ipfin.co.uk

Appendices

30

www.ipfin.co.uk

31

Group

2012

£M

2011

£M

Change at CER %

Customer numbers (000s) 2,415 2,323 4.0

Credit issued 882.1 844.5 13.2

Average net receivables 588.3 575.5 11.2

Revenue (net of ESRs) 651.7 649.5 8.8

Impairment (176.2) (167.7) (14.3)

Finance costs (41.6) (42.9) (4.8)

Agents’ commission (74.9) (72.9) (11.3)

Other costs (263.9) (265.5) (4.6)

Profit before taxation* 95.1 100.5

Year ended 31 December 2012

* Excluding an exceptional restructuring charge of £4.8M

www.ipfin.co.uk

32

Balance sheet

Dec 2012

£M

Dec 2011

£M

Change at CER

%

Fixed assets 31.5 34.2 (9.5)

Receivables 650.3 560.4 12.7

Cash 24.2 17.9 32.2

Borrowings (310.8) (276.5) (9.9)

Other net liabilities (19.4) (8.3) (145.6)

Equity 375.8 327.7

www.ipfin.co.uk

33

Change in interest allocation

2012 Reported profit

Adjustment 2012 Adjusted

profit

£M £M £M

Poland 62.2 (7.3) 54.9

Czech-Slovakia 28.8 (1.7) 27.1

Hungary 10.1 2.4 12.5

Romania 2.2 2.3 4.5

Mexico 4.9 4.3 9.2

UK costs (13.1) - (13.1)

Profit before taxation* 95.1 - 95.1

* Excluding an exceptional restructuring charge of £4.8M

www.ipfin.co.uk

Strong financial fundamentals

49.4%

1.3x

3.2x

2009

54.5%

1.0x

3.8x

2010

58.5%

0.8x

3.4x

2011 2012

17.6% 22.2% 22.7%

Equity to receivables

Gearing

Interest cover

Return on equity

Strong cash flow and capital generation

34

57.8%

1.3x 0.8x

3.3x

20.1%

www.ipfin.co.uk

35

Our markets

Year entered

EU member?

Fitch rating

Population (M)

Customers (000s)

Dec 2012

Poland 1997 A- 38.2 821

Czech Republic 1997 A+ 10.5 383

Slovakia 2001 A+ 5.4

Hungary 2001 BB+ 10.0 268

Mexico 2003 BBB 114.8 683

Romania 2006 BBB- 21.4 260

www.ipfin.co.uk

36

Forecast GDP growth

Source: Citibank

2.0

1.3

2.8

0.9

2.0

0.7

1.7

0.3

1.3

3.93.6

3.8

0.2

1.0

2.9

0.0

0.40.7

(1.2)

(0.2)

(1.7)(2)

(1)

0

1

2

3

4

5

Poland Czech Slovakia Hungary Mexico Romania UK

2014 2012 2013

%

www.ipfin.co.uk

37

Consumer confidence

(40)

(35)

(30)

(25)

(20)

(15)

(10)

(5)

0Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

IPF European markets (weighted)

Mexico

UK Sources: Europe - EU Consumer confidence Indicator; Mexico - Reuters

2012 2010 2011

www.ipfin.co.uk

Contact

Rachel Moran

Investor Relations Manager

International Personal Finance No 3 Leeds City Office Park Leeds LS11 5BD United Kingdom

T: +44 (0)113 285 6700