International Fixed Income Topic VB: Emerging Markets-Description.

26

International Fixed Income Topic VB: Emerging Markets- Description

-

date post

21-Dec-2015 -

Category

Documents

-

view

221 -

download

0

Transcript of International Fixed Income Topic VB: Emerging Markets-Description.

International Fixed Income

Topic VB: Emerging Markets-

Description

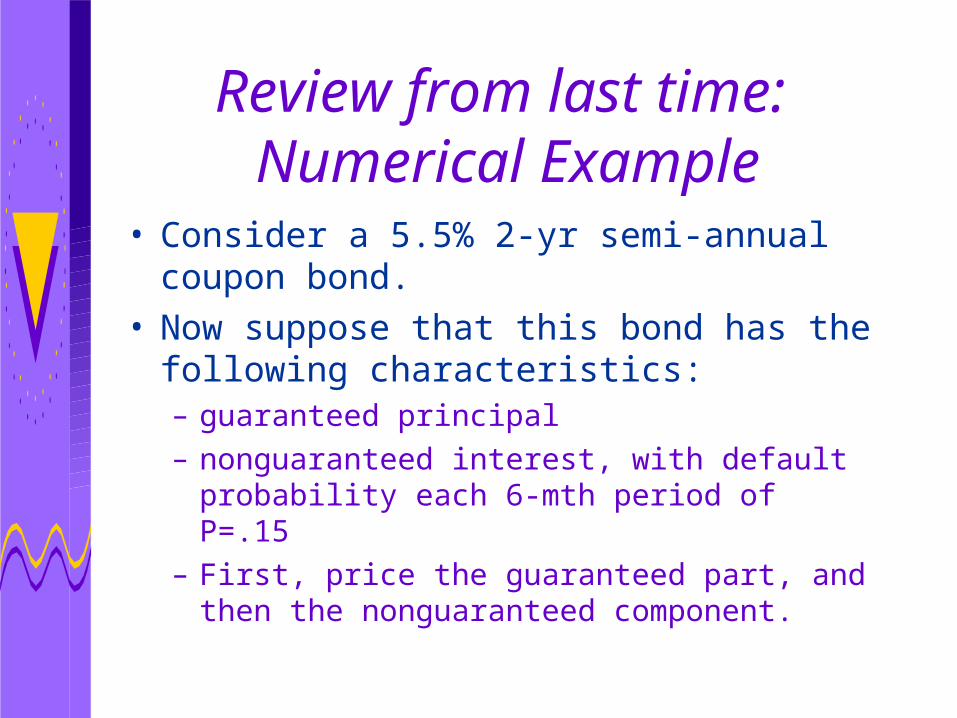

Review from last time: Numerical Example

• Consider a 5.5% 2-yr semi-annual coupon bond.

• Now suppose that this bond has the following characteristics:– guaranteed principal– nonguaranteed interest, with default

probability each 6-mth period of P=.15– First, price the guaranteed part, and

then the nonguaranteed component.

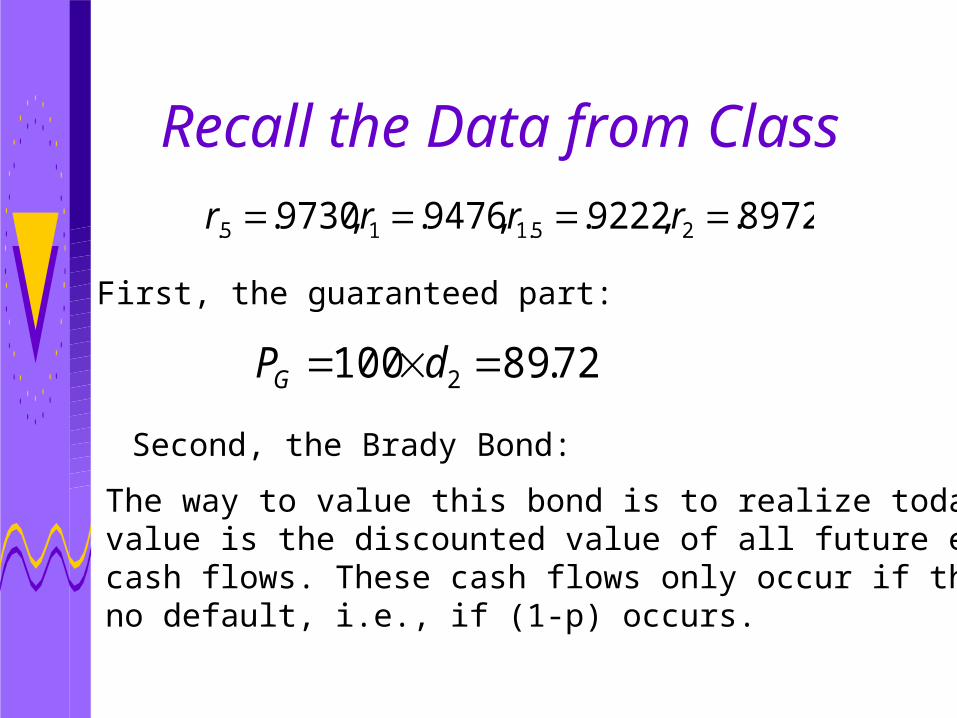

Recall the Data from Class

8972.,9222.,9476.,9730. 25.115. rrrr

72.89100 2 dPG

First, the guaranteed part:

Second, the Brady Bond:

The way to value this bond is to realize today’svalue is the discounted value of all future expectedcash flows. These cash flows only occur if there isno default, i.e., if (1-p) occurs.

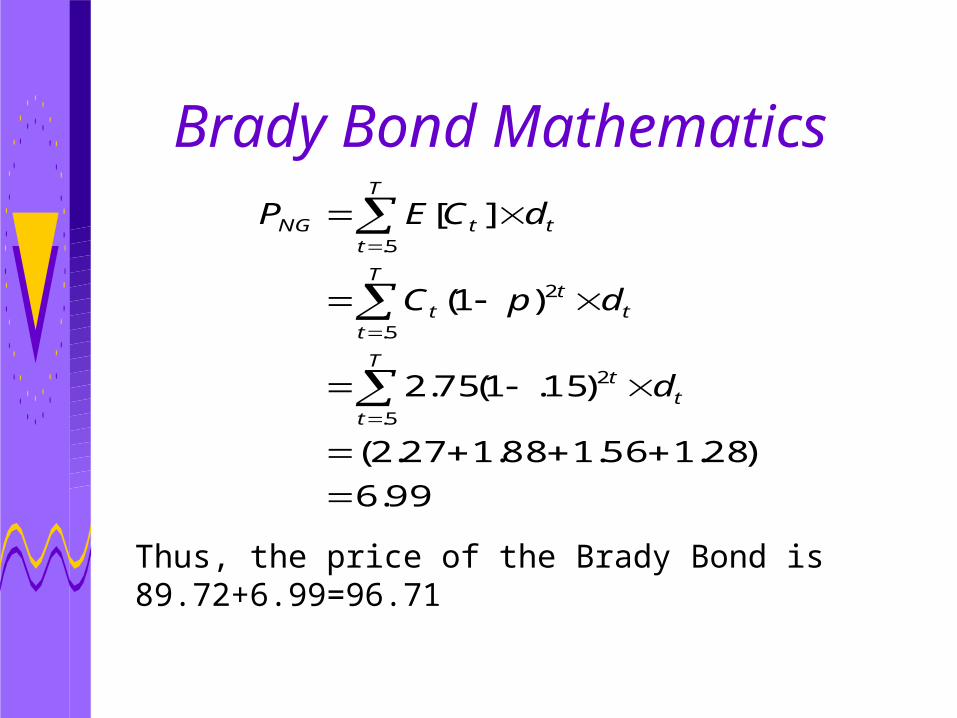

Brady Bond Mathematics

99.6

)28.156.188.127.2(

)15.1(75.2

)1(

][

5.

2

5.

2

5.

t

T

t

t

t

T

t

tt

t

T

ttNG

d

dpC

dCEP

Thus, the price of the Brady Bond is89.72+6.99=96.71

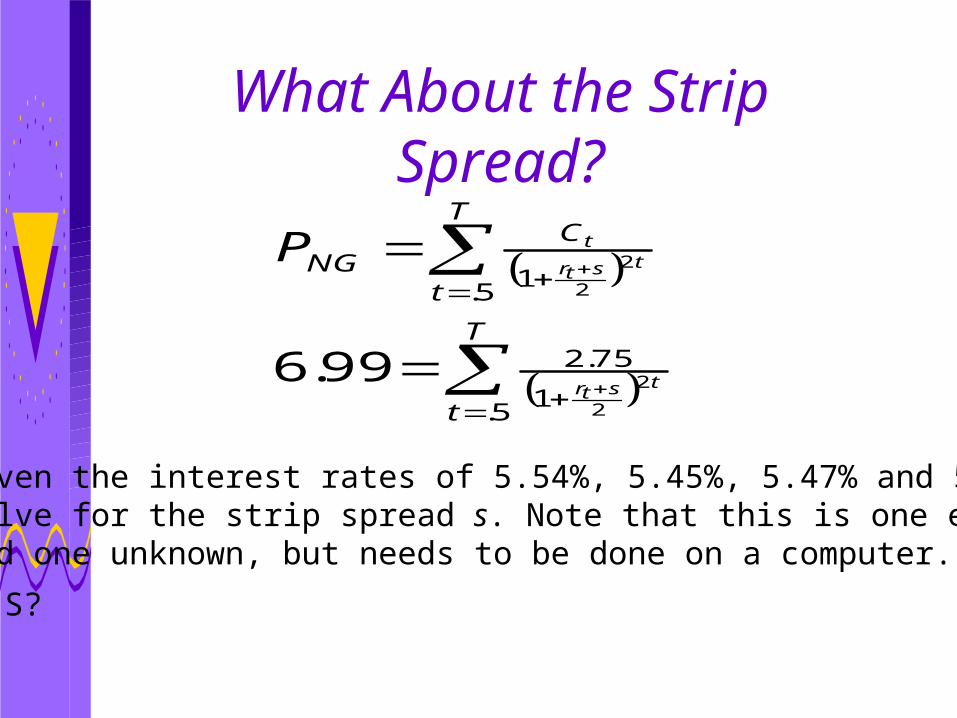

What About the Strip Spread?

T

t

T

t

CNG

tstr

tstr

tP

5.1

75.2

5.1

2

2

2

2

99.6

Given the interest rates of 5.54%, 5.45%, 5.47% and 5.5%;solve for the strip spread s. Note that this is one equationand one unknown, but needs to be done on a computer.

What is S? S=36.42%!

Outline

• Emerging Markets• Stylized Facts• Case Study

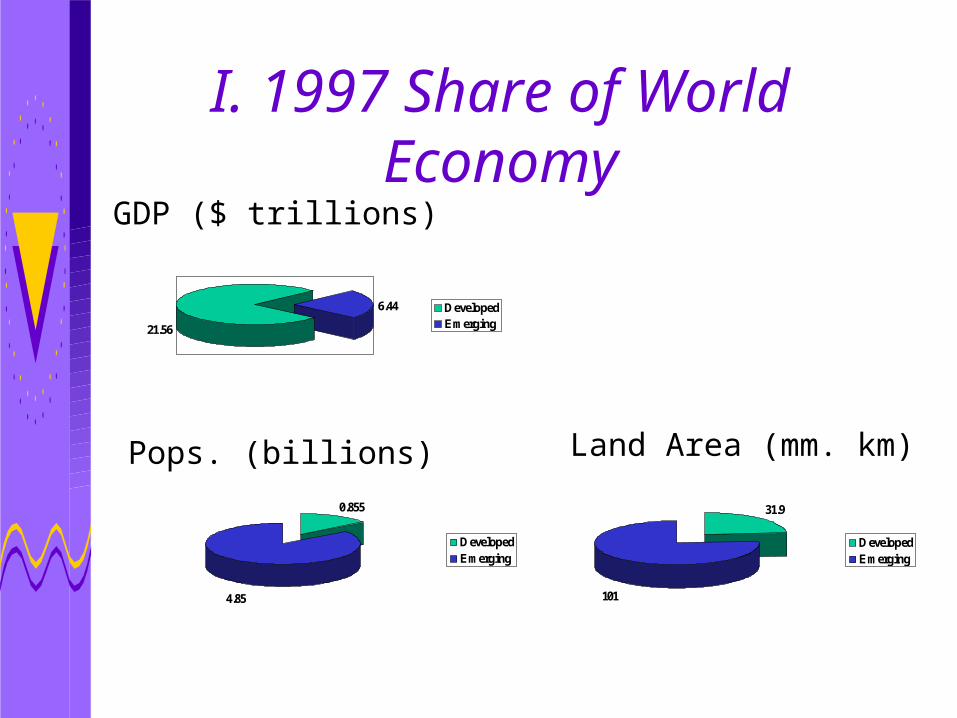

I. 1997 Share of World Economy

21.56

6.44 DevelopedEmerging

0.855

4.85

DevelopedEmerging

31.9

101

DevelopedEmerging

GDP ($ trillions)

Pops. (billions) Land Area (mm. km)

Emerging Markets

• Only a subset of these emerging market countries offer investable debt securities.

• In fixed income, emerging debt markets refer to this subset:

(see next page)

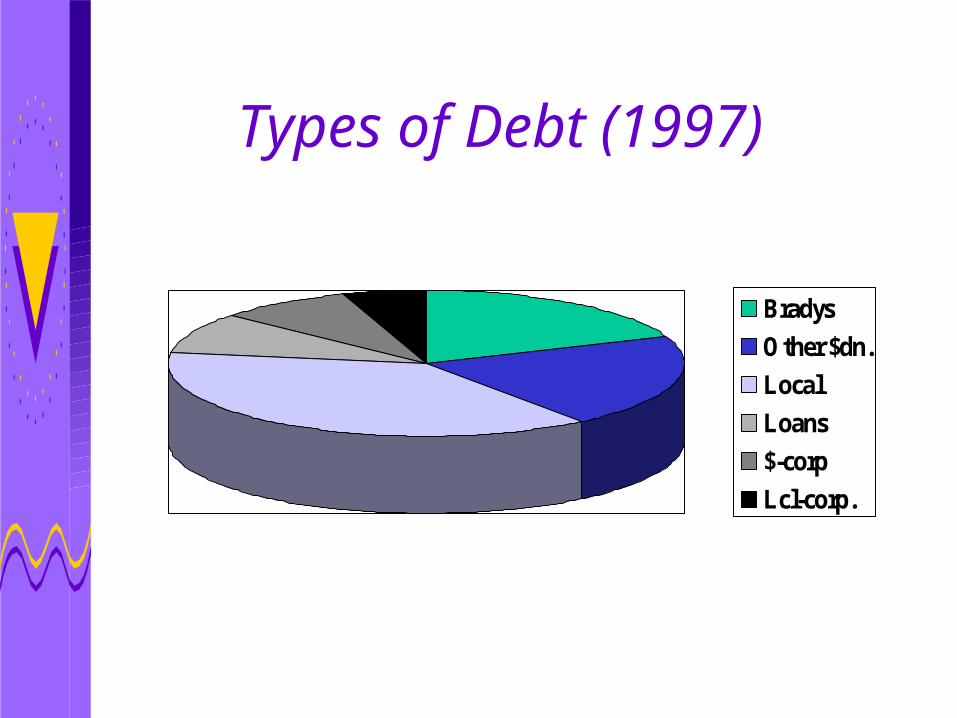

Types of Debt (1997)

BradysOther $dn.LocalLoans$-corpLcl-corp.

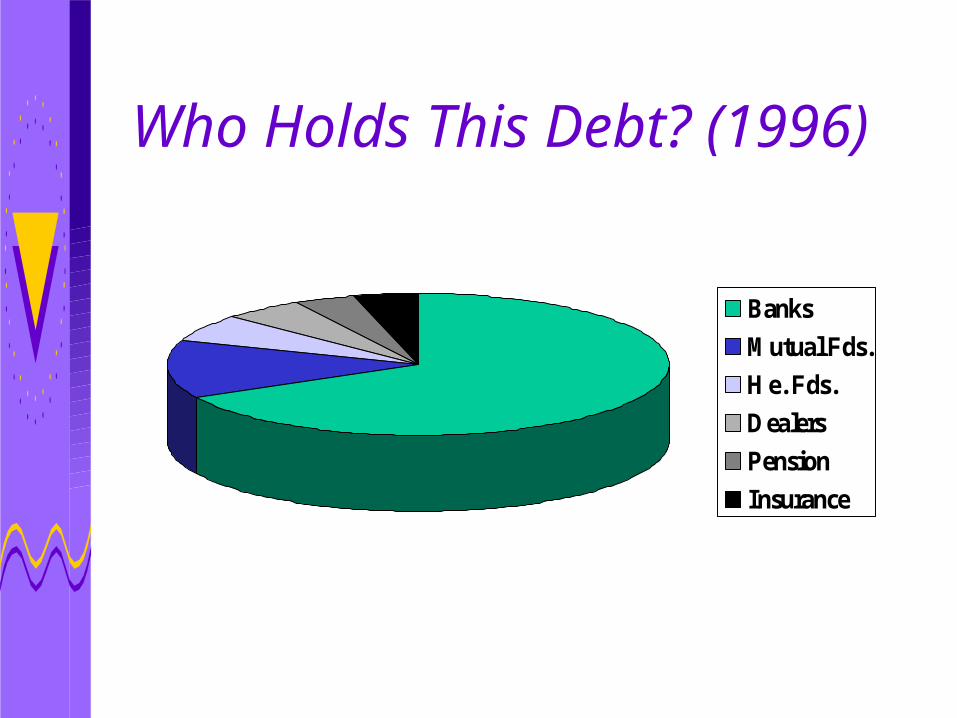

Who Holds This Debt? (1996)

BanksMutual Fds.He. Fds.DealersPensionInsurance

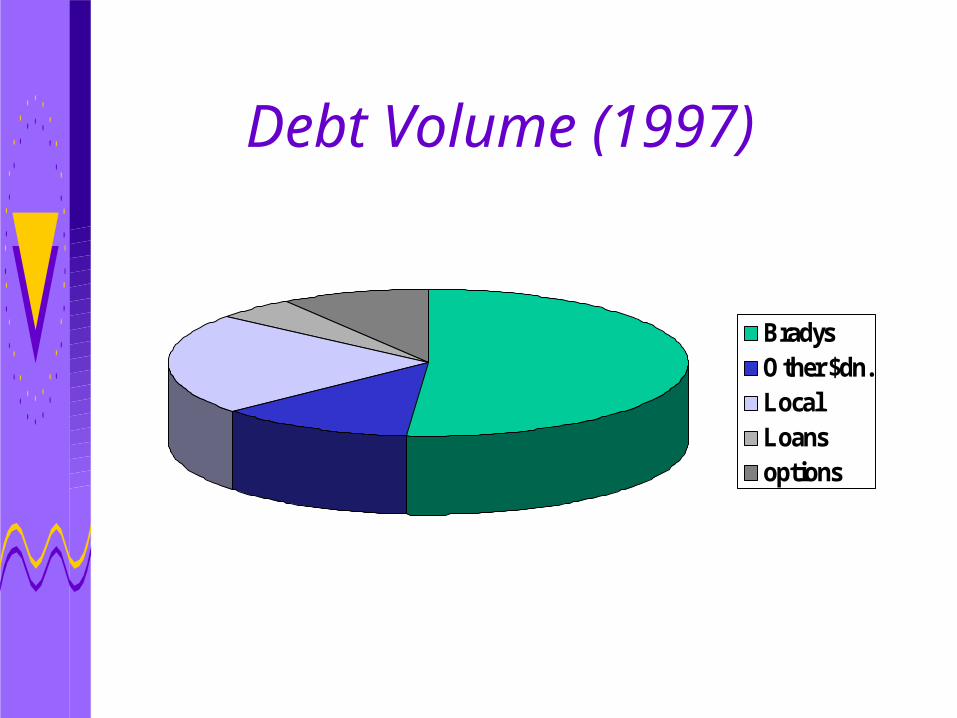

Debt Volume (1997)

BradysOther $dn.LocalLoansoptions

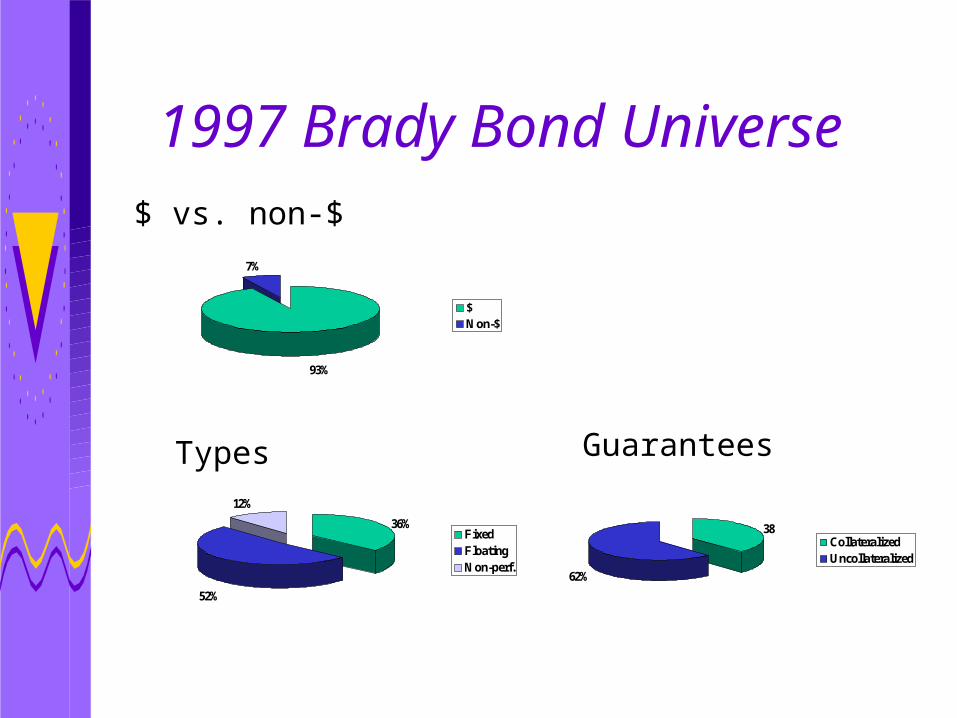

1997 Brady Bond Universe

93%

7%

$Non-$

36%

52%

12%

FixedFloatingNon-perf.

38

62%

CollateralizedUncollateralized

$ vs. non-$

Types Guarantees

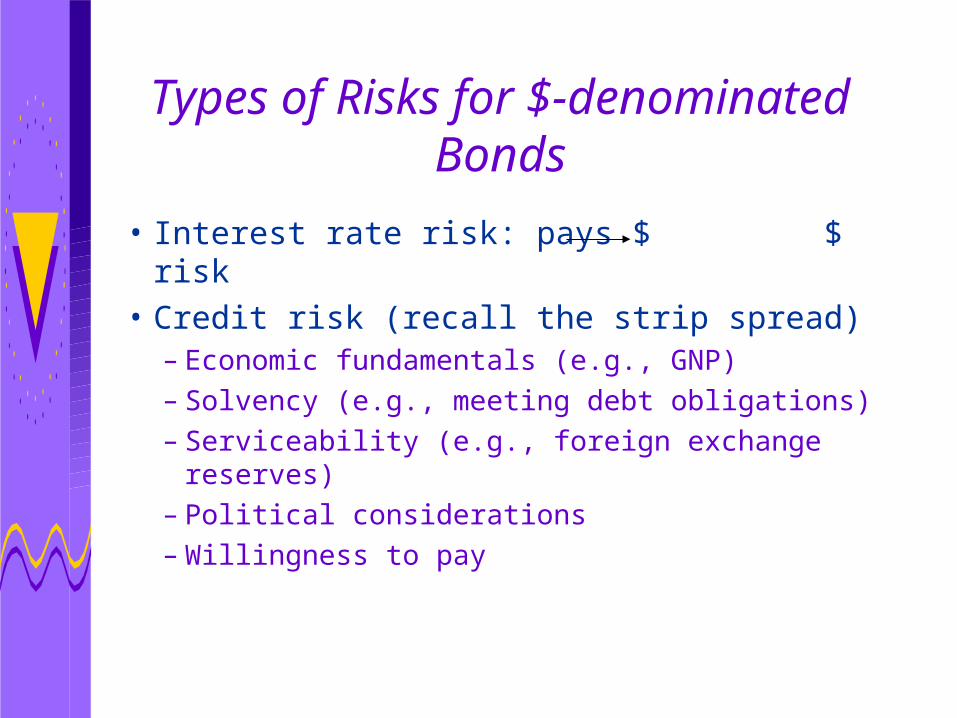

Types of Risks for $-denominated Bonds

• Interest rate risk: pays $ $ risk• Credit risk (recall the strip spread)

– Economic fundamentals (e.g., GNP)– Solvency (e.g., meeting debt

obligations)– Serviceability (e.g., foreign exchange

reserves)– Political considerations– Willingness to pay

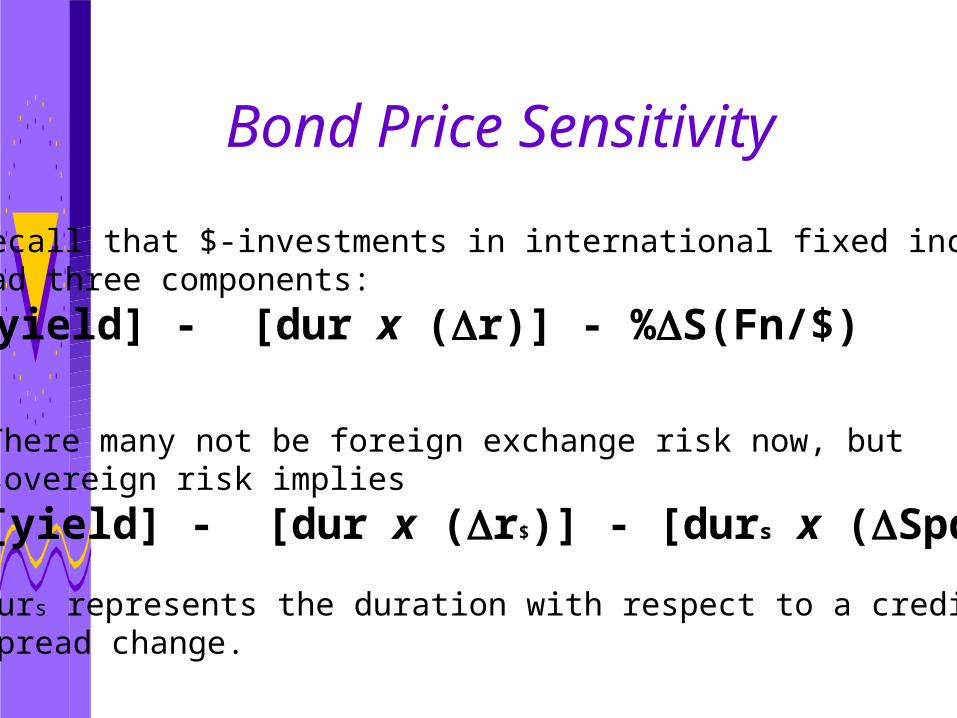

Bond Price Sensitivity

Recall that $-investments in international fixed incomehad three components:

[yield] - [dur x (r)] - %S(Fn/$)

There many not be foreign exchange risk now, butsovereign risk implies

[yield] - [dur x (r$)] - [durs x (Spd)]

Durs represents the duration with respect to a credit spread change.

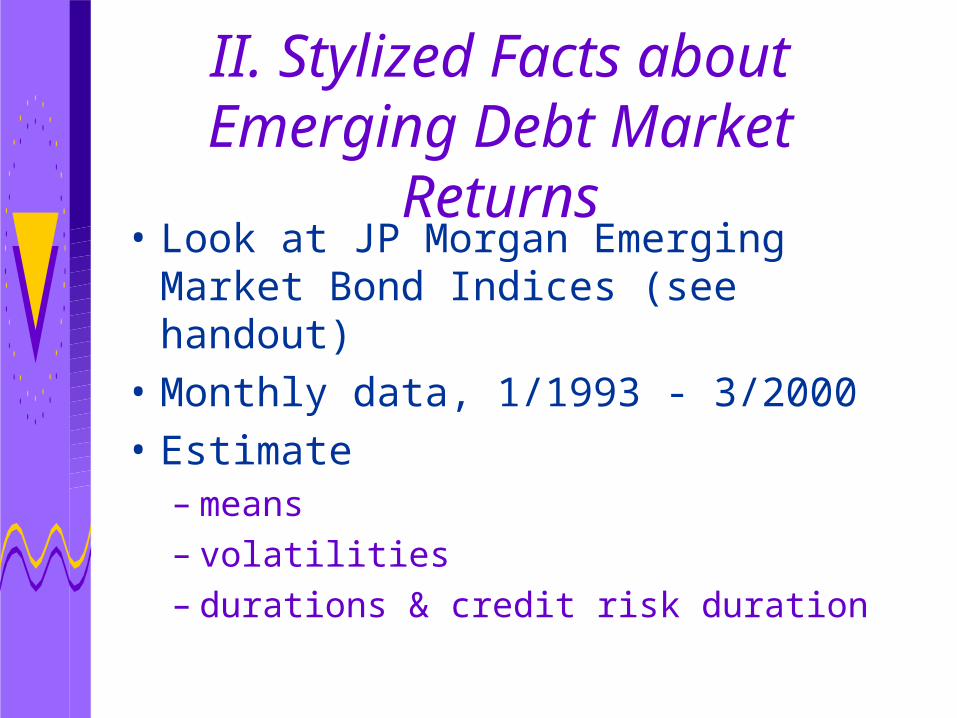

II. Stylized Facts about Emerging Debt Market

Returns• Look at JP Morgan Emerging

Market Bond Indices (see handout)

• Monthly data, 1/1993 - 3/2000• Estimate

– means– volatilities– durations & credit risk duration

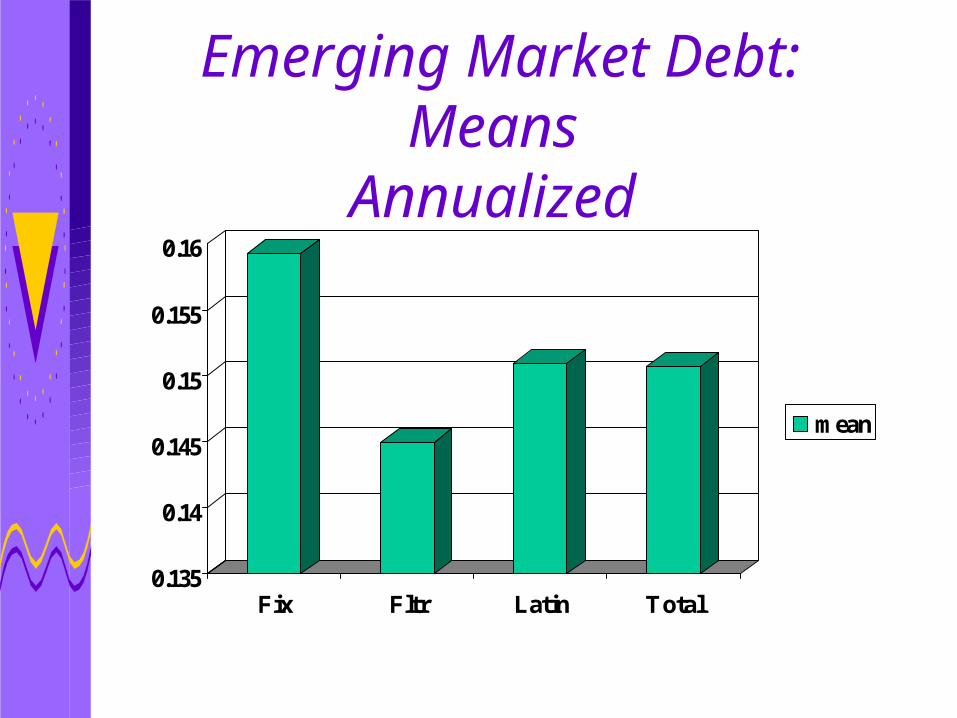

Emerging Market Debt: Means

Annualized

0.135

0.14

0.145

0.15

0.155

0.16

Fix Fltr Latin Total

mean

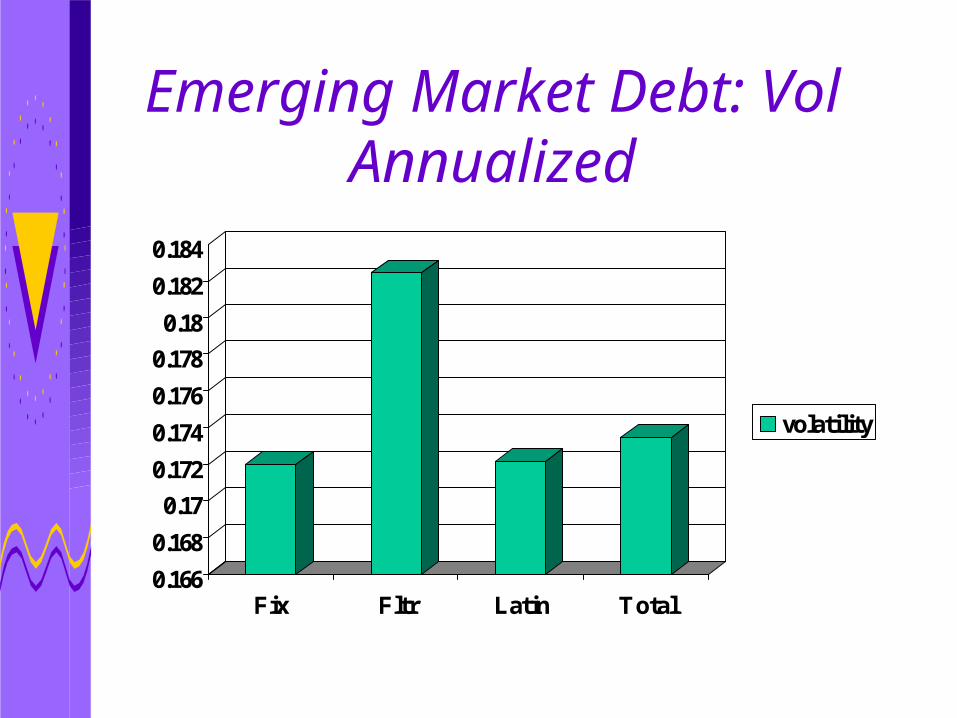

Emerging Market Debt: Vol

Annualized

0.166

0.168

0.17

0.172

0.174

0.176

0.178

0.18

0.182

0.184

Fix Fltr Latin Total

volatility

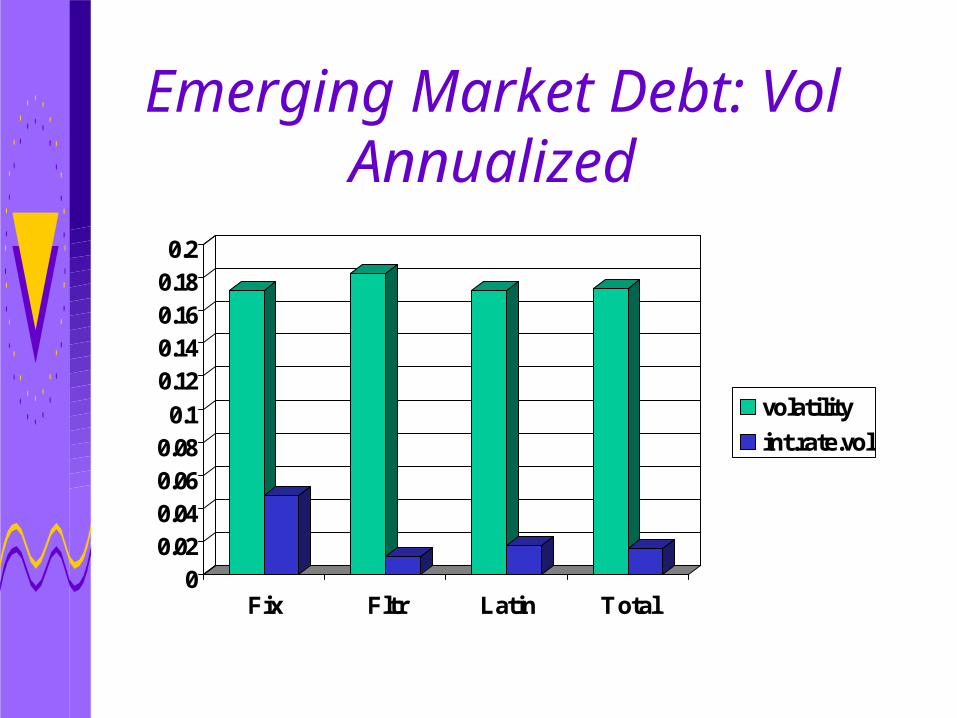

Emerging Market Debt: Vol

Annualized

00.020.040.060.080.1

0.120.140.160.180.2

Fix Fltr Latin Total

volatilityint.rate.vol

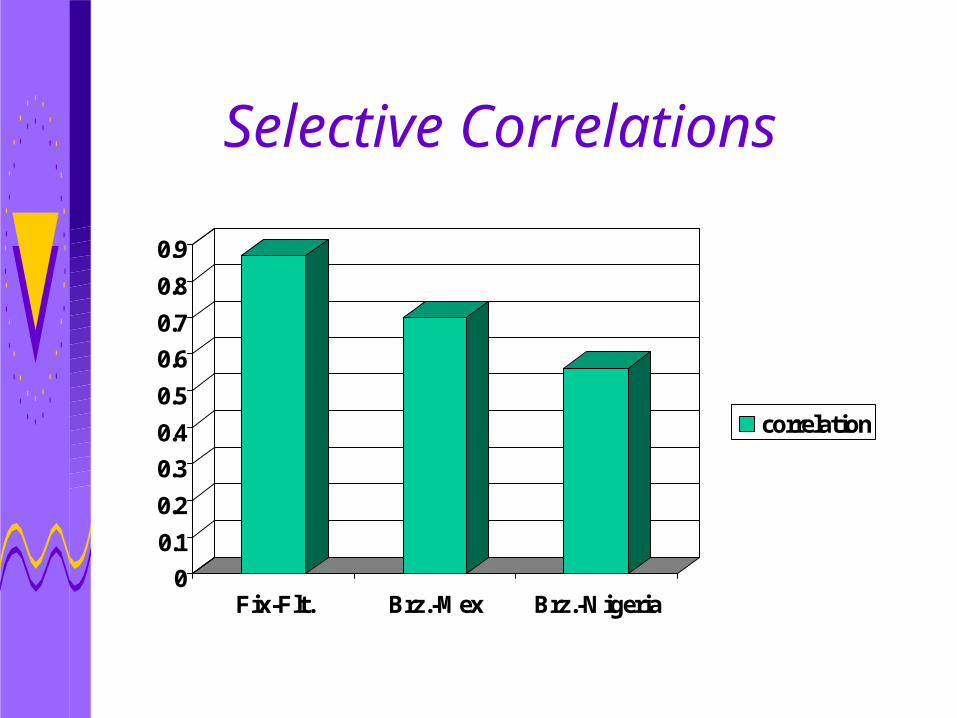

Selective Correlations

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

Fix-Flt. Brz.-Mex Brz.-Nigeria

correlation

Conclusions

• Emerging markets trade much more like equity returns in terms of returns/risk. Why?

• Most of the volatility is due to credit risk, i.e., $ interest rate risk plays only a small role. Why?

• Given this, correlations seem to be particularly high. Why?

III. Case Study

• Did investors foresee the collapse of the Mexican peso in 1994?

• Look at short-term debt instruments over 1993-94 time period:– cetes (23% of mkt): peso-denominated– tesobonos (55% of mkt): $-denominated

albeit w/ capital controls

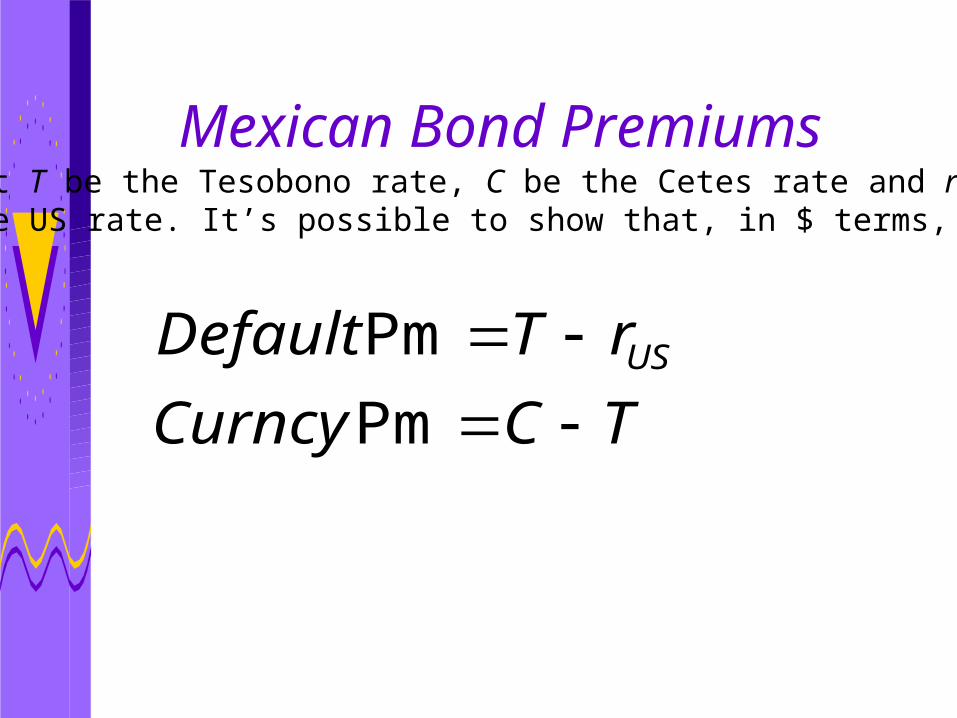

Mexican Bond Premiums

TCCurncy

rTDefault US

Pm

Pm

Let T be the Tesobono rate, C be the Cetes rate and r bethe US rate. It’s possible to show that, in $ terms,

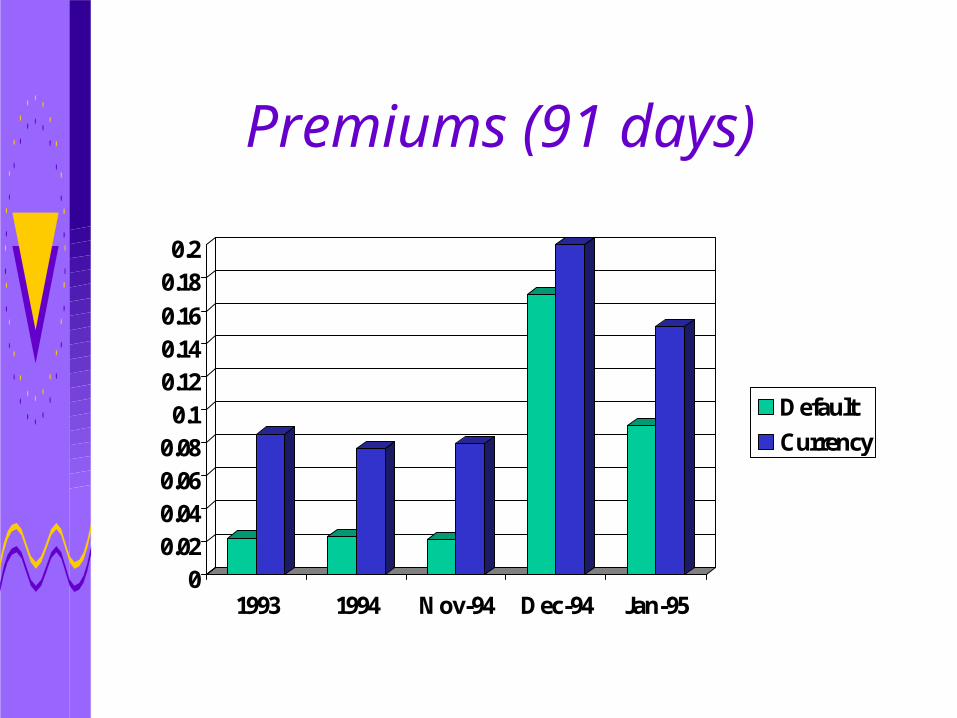

Premiums (91 days)

00.020.040.060.080.1

0.120.140.160.180.2

1993 1994 Nov-94 Dec-94 Jan-95

DefaultCurrency

What about the 182-day Cetes and Tesebonos?

• Assuming the expectations hypothesis, could we have looked prior to September-November of 1994, and inferred devaluation risk from the longer maturity bonds?

• The answer is no - there was no sign of a currency premium on longer versus shorter bonds.

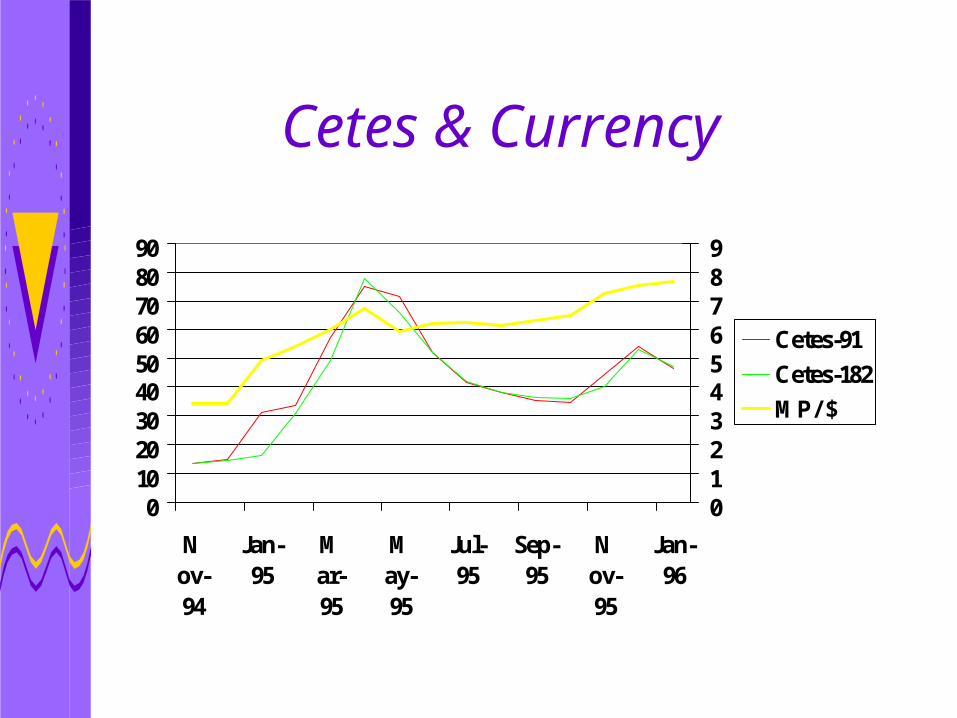

Cetes & Currency

0102030405060708090

Nov-94

Jan-95

Mar-95

May-95

Jul-95

Sep-95

Nov-95

Jan-96

0123456789

Cetes-91Cetes-182MP/$