INTERNATIONAL COTTON ADVISORY COMMITTEE · INTERNATIONAL COTTON ADVISORY COMMITTEE Standing...

28

INTERNATIONAL COTTON ADVISORY COMMITTEE Standing Committee SC-M-499 Final Washington, DC June 12, 2009 MINUTES 499 th Meeting of the Standing Committee Friday, May 22, 2009 Economic and Commercial Bureau, Embassy of Egypt Washington, DC 20008 PRESENT: Delegates: Dr. Ashraf El-Rabiey, Egypt (in the Chair) Mr. José D. Molina, Argentina Mrs. Cecilia I. Marincioni, Argentina Ms. Prudence Gordon, Australia Mr. Michel Wallemacq, Belgium Mr. Emerson C. Kloss, Brazil Mr. Philip Gough, Brazil Mr. Benjamin Baguian, Burkina Faso Mr. Oumarou Chinmoun, Cameroon Mr. Chun-Fu Chang, China (Taiwan) Mr. Eric C.H. Wu, China (Taiwan) Mr. Yehia Halim, Egypt Mr. Christian Ligeard, France Ms. Antonette Debus, Germany Mrs. Banashri Bose-Harrison, India Mr. Giancarlo Gobbi, Italy Mr. Alpha Konate, Mali Ms. Christiane Bushnell, Mali Ms. Laraba E. Bhutto, Nigeria Mr. Azmat Ali Ranjha, Pakistan Ms. Magdalena Dybek, Poland Dr. Siphiwe F. Mkhize, South Africa Mr. Santiago Neches Olaso, Spain Mr. Urs Bronnimann, Switzerland Mrs. Lily Munanka, Tanzania Mrs. Ayse Gul Barkcin, Turkey Mr. Patrick A. Packnett, USA Mr. James Johnson, USA Mr. Willie Ndembela, Zambia Observers: Mr. Clemens Boonekamp, Agriculture and Commodities Division, WTO Mr. Jorge Vartparonian, Argentina Mr. Richard Haire, Australia Mr. Andrew Macdonald, Brazil Mr. Ahmed Elbosaty, Egypt Mr. Suresh Kotak, India Mr. Dhiren Sheth, India Mr. Romano Bonadei, Italy Mr. Alois Schonberger, Poland Mr. Fatih Dogan, Turkey Mr. Sebahattin Gazanfer, Turkey Mr. John Mitchell, USA Mr. Manfred Schiefer, USA Mr. Neal Gillen, ACSA, USA Mrs. Barbara Spangler, ACSA, USA

Transcript of INTERNATIONAL COTTON ADVISORY COMMITTEE · INTERNATIONAL COTTON ADVISORY COMMITTEE Standing...

INTERNATIONAL COTTON ADVISORY COMMITTEE

Standing Committee SC-M-499 Final Washington, DC June 12, 2009

MINUTES

499th

Meeting of the Standing Committee Friday, May 22, 2009

Economic and Commercial Bureau, Embassy of Egypt Washington, DC 20008

PRESENT: Delegates: Dr. Ashraf El-Rabiey, Egypt (in the Chair) Mr. José D. Molina, Argentina Mrs. Cecilia I. Marincioni, Argentina Ms. Prudence Gordon, Australia Mr. Michel Wallemacq, Belgium Mr. Emerson C. Kloss, Brazil Mr. Philip Gough, Brazil

Mr. Benjamin Baguian, Burkina Faso Mr. Oumarou Chinmoun, Cameroon Mr. Chun-Fu Chang, China (Taiwan) Mr. Eric C.H. Wu, China (Taiwan) Mr. Yehia Halim, Egypt Mr. Christian Ligeard, France Ms. Antonette Debus, Germany

Mrs. Banashri Bose-Harrison, India Mr. Giancarlo Gobbi, Italy Mr. Alpha Konate, Mali Ms. Christiane Bushnell, Mali Ms. Laraba E. Bhutto, Nigeria Mr. Azmat Ali Ranjha, Pakistan Ms. Magdalena Dybek, Poland Dr. Siphiwe F. Mkhize, South Africa Mr. Santiago Neches Olaso, Spain Mr. Urs Bronnimann, Switzerland Mrs. Lily Munanka, Tanzania Mrs. Ayse Gul Barkcin, Turkey

Mr. Patrick A. Packnett, USA Mr. James Johnson, USA Mr. Willie Ndembela, Zambia

Observers: Mr. Clemens Boonekamp, Agriculture and Commodities Division, WTO

Mr. Jorge Vartparonian, Argentina Mr. Richard Haire, Australia Mr. Andrew Macdonald, Brazil Mr. Ahmed Elbosaty, Egypt Mr. Suresh Kotak, India Mr. Dhiren Sheth, India Mr. Romano Bonadei, Italy Mr. Alois Schonberger, Poland Mr. Fatih Dogan, Turkey Mr. Sebahattin Gazanfer, Turkey Mr. John Mitchell, USA Mr. Manfred Schiefer, USA

Mr. Neal Gillen, ACSA, USA Mrs. Barbara Spangler, ACSA, USA

2

Secretariat: Dr. Terry Townsend, Executive Director Mr. Fred Arriola, Business Manager Mr. Andrei Guitchounts, Economist Mrs. Armelle Gruère, Statistician Mr. Alejandro Plastina, Economist Mrs. Carmen S. León, Administrative Assistant 1. Adoption of the Agenda The CHAIR welcomed delegates, Members of the Private Sector Advisory Panel and the Secretariat to the 499

th Meeting of the Standing Committee. The Economic and Commercial Bureau of the Embassy of

Egypt had been recently renovated, and all participants noted the beautiful décor and examples of Egyptian art on display. The CHAIR asked if there were any amendments to the proposed agenda, and seeing none found the agenda was approved. 2. Cotton and Multilateral Trade Negotiations

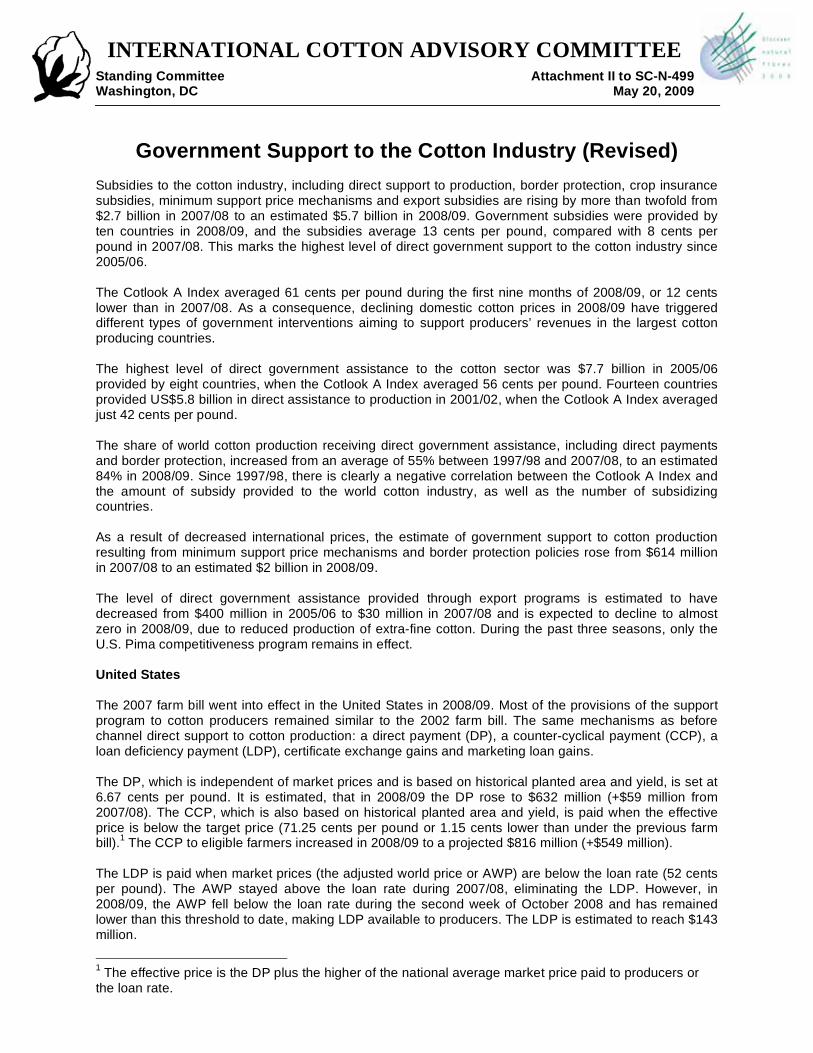

a) Report from the Secretariat: Subsidies, Quotas and Tariffs that Distort Cotton Production and Trade (Attachment II)

Subsidies to the cotton industry, including direct support to production, border protection, crop insurance subsidies, minimum support price mechanisms and export subsidies are rising by more than twofold from $2.7 billion in 2007/08 to an estimated $5.7 billion in 2008/09. The share of world cotton production receiving direct government assistance increased from an average of 55% between 1997/98 and 2007/08, to an estimated 84% in 2008/09. Provisions of the U.S. 2007 farm bill in effect in 2008/09 remained similar to the 2002 farm bill. Total direct U.S. support to cotton production, including crop insurance, increased from $888 million in 2007/08 to $3.1 billion in 2008/09, or an equivalent of 50 cents per pound of actual production. In 2008/09, in order to support producers’ prices, the Chinese government purchased 2.724 million tons of cotton. As a result, benefits received by producers are estimated at about US$1.5 billion (+$860 million from 2007/08). The government of India significantly increased minimum support prices for seedcotton for the 2008/09 season by 40% and had purchased around 2.15 million tons of cotton lint, or a little over 40% of estimated 2008/09 production. The impact of government intervention would increase cotton farm revenues in India by about US$443 million. Government support to cotton production by Pakistan is not expected to exceed US$8 million. Small changes in government support are projected for the European Union, Colombia, Turkey and Mexico. No PEPRO auctions were held in Brazil as of mid-May 2009. The General Administration of Quality Supervision Inspection & Quarantine (AQSIQ) of China (Mainland) has established a registration process for foreign cotton suppliers effective March 15, 2009. The AQSIQ registration requirement was discussed at the 497

th Meeting of the Standing Committee. The major

concern is that the system could unfairly subject suppliers to different levels of inspection and oversight. As of the beginning of May 2009, 148 companies were registered with the AQSIQ. The list of registered companies includes major and smaller cotton firms from America, Asia, Africa, Europe and Australia, from all major exporting countries, including government owned firms, private and cooperative organizations. A meeting between the AQSIQ and the Committee for International Co-operation between Cotton Associations (CICCA) was held in Beijing on April 28, 2009 to address concerns by the trade about the system. Collaboration on the issue will continue and a working group between CICCA and the AQSIQ is being established. The delegate of the UNITED STATES thanked the Secretariat for its report, and he suggested that the Secretariat should provide specific definitions of the income and price support programs included in its reports. The delegate noted that some credit support and input subsidy programs operated by some countries had not been included in the Secretariat report. The delegate noted that the Secretariat’s report included an exhaustive list of government measures in the United States, but that measures provided by other countries were not included. As one example, the delegate noted that India is offering a subsidy on exports this season, but the subsidy was not listed in the table on export subsidies provided by the

3

Secretariat. The delegate added that since crop insurance is reported as a subsidy in the United States, similar programs should be reported for other countries. The Secretariat responded to the delegate of the U.S. by agreeing that the report should be exhaustive and objective, and the Secretariat will take steps to ensure that all programs of direct relevance to the cotton sector are included in the future, including export subsidies and crop insurance programs that include a subsidy component. The executive director agreed that the export subsidy provided by India in 2008/09 should have been listed as such. The delegate of AUSTRALIA agreed that specific definitions of subsidies included in the report would be helpful. She asked why a direct payment to cotton spinners in the United States was not included. The Secretariat explained that the U.S. program that provides 4 cents per pound of cotton consumption to spinners is not of direct benefit to cotton producers and so is not included in the report. It was noted that there are a large number of programs in many countries that stimulate or protect cotton textile industries, and the Secretariat does not have the subject matter knowledge to monitor or evaluate all such programs. The delegate of ARGENTINA thanked the Secretariat for its report. However, the delegate noted that the report includes subsidies that directly distort cotton production and trade and forms of border protection that are discussed within the WTO under the category of “market access.” The delegate suggested that the Committee should not lose sight of the most important forms of distortion to cotton production and trade, such as domestic support provided by the United States and the European Union. The delegate of TURKEY asked the Secretariat to provide more information about the Pima Competitiveness program in the U.S., and she asked whether the U.S. program is similar to the 5% export tax rebate offered in India. The Secretariat pledged to provide additional information about both programs. The delegate of BRAZIL thanked the Secretariat for providing information about the exporter registration requirement implemented by AQSIQ in China (Mainland). The delegate called attention to the information contained in the Secretariat report, noting that there is a trend toward increased subsidies being provided to producers during periods of low prices.

b) Report from Mr. Clemens Boonekamp, Director - Agriculture and Commodities Division, World

Trade Organization – WTO

The CHAIR introduced Mr. Boonekamp and said that the ICAC was gratified that he was willing to travel from Geneva to participate in the Standing Committee meeting. Mr. Boonekamp thanked the Committee and the Secretariat for its cooperation with the Secretariat of the WTO. He noted that reports from the Secretariat assisted the WTO in understanding the nature and magnitude of distortions to production and trade in the cotton industry. Mr. Boonekamp reaffirmed that cotton is at the heart of the Doha Development Agenda (DDA). He said that there can be no completion of the DDA without a solution on cotton, and that WTO Members have agreed to treat cotton ambitiously, specifically and expeditiously within the negotiations on agriculture. Mr. Boonekamp noted that Benin, Burkina Faso, Chad and Mali (C4) have made a specific proposal to reduce support to the cotton sector more quickly than support to the agricultural sector in general, and that so far this is the only proposal dealing with cotton that has been tabled. However, he noted that the U.S. logically wishes to understand the impacts of the negotiations on agriculture before agreeing to cotton-specific modalities. Mr. Boonekamp said that consultations are continuing on both technical and political levels, and he expects the modalities phase of discussions in the DDA to be finished sooner, rather than later. However, after the modalities are agreed, it will still be necessary to conduct verification exercises and legal drafting. Accordingly, he cautioned the Committee that there is still much work to do in the DDA, and it seemed clear that WTO Members were not yet in a position to conclude the Round. Mr. Boonekamp did not offer a forecast as to when negotiations would begin again, noting that some countries have yet to name their agricultural negotiators after recent elections. However, he assured the ICAC that all countries understand that trade is part of the solution to the current financial crisis, and he was confident that a satisfactory conclusion to the DDA would eventually be reached.

4

The delegate of ARGENTINA thanked Mr. Boonekamp for his report. The delegate expressed the hope that the Round will conclude soon, but he expressed a reservation that even with specific limits on cotton subsidies, meaningful reductions in support may not occur if countries are allowed to expand subsidies provided under different programs that are identified as non- or minimally-trade distorting (Green Box). Mr. Boonekamp noted that definitions of Green Box payments are part of the DDA discussion. The delegate of PAKISTAN asked Mr. Boonekamp to comment on a report that some countries were suggesting that WTO members should skirt the modalities phase of the discussions in order to speed the process. Mr. Boonekamp said that there has been no firm proposal to skirt the modalities phase of the DDA. He acknowledged that an idea had been proposed to begin scheduling verification activities, but so far this remained simply an idea. The CHAIR thanked Mr. Boonekamp for his contributions and asked how the economies of the C4 countries, and other developing cotton producing countries, could withstand the losses in their cotton sectors during the prolonged negotiations over the DDA. Mr. Boonekamp noted that the WTO is not an aid agency and does not provide direct support to countries for economic development. However, the cotton dossier includes a development track, and he urged countries to mobilize resources in support of cotton-dependent developing economies. The delegate of INDIA asked if the new U.S. Trade Representative had discussed cotton specifically in meetings with the WTO Director-General. Mr. Boonekamp said he did not know what had been discussed in private between the Director-General of the WTO and the USTR, but he was confident that the USTR is aware of the cotton issue and the importance of agriculture to the DDA. Seeing no additional questions or comments, the CHAIR again thanked Mr. Boonekamp for coming to Washington to meet with the Standing Committee and for the work of the WTO Secretariat on the cotton issue. Mr. Boonekamp repeated his assurance that the work of the ICAC is of critical importance to the WTO in understanding issues related to cotton in the DDA, and he expressed his confidence in an eventual conclusion to the Round in a satisfactory manner. 3. Round Table Discussion with the Private Sector Advisory Panel (PSAP) The CHAIR invited Dr. Sebahattin Gazanfer, Chair of the PSAP, to lead a round table discussion with the Standing Committee on issues of interest to the private sector. Fourteen members of the PSAP and observers from the private sector participated in the discussion. Members of the PSAP noted that the world economic recession was having a severe impact on world cotton mill use and trade. The PSAP noted that governments are spending considerable amounts to protect or preserve financial and manufacturing industries, and they reminded delegates that the fiber-textile-and clothing/home furnishings pipelines are also deserving of support. The PSAP called attention to the employment impacts of reduced consumer demand for cotton products and suggested that governments could stimulate consumer demand by reducing taxes at the retail level. Members of the PSAP noted that despite receiving considerable support from governments, most banks were still reluctant to lend the agricultural sector, thus reducing the competitiveness of the cotton industry. Members of the PSAP noted that cotton is a highly-traded commodity, and thus the availability of trade finance and support for the principle of contract sanctity are important in supporting the industry. The PSAP urged governments to be aware of the importance of contract performance in maintaining the health of the world cotton industry and that governments should support institutions that underpin cotton trade.

5

The delegate of GERMANY interjected that it is doubtful that governments will reduce consumer taxes to bolster the cotton textile and apparel sector, and she suggested that the industry needed to focus on remaining competitive in order to withstand the current challenges. Members of the PSAP stated that the major challenge facing the cotton industry pipeline today is not competitive production but a lack of consumer demand. It was noted that the Government of Turkey reduced the Value Added Tax (VAT) for textile items from 18% to 8% for a short time in order to stimulate demand for textile products. Members of the PSAP asked government officials to notice the discrepancy between substantial support being given to financial and industrial sectors and the much more limited levels of support being provided to agriculture and textiles. The PSAP noted that the cotton-textile-apparel & home furnishings pipeline employs far more people than banks and automobile manufacturing, and on a cost-per-job saved basis, support for the cotton sector through efforts to stimulate consumer demand could be relatively more effective. Members of the PSAP reiterated that banks should be encouraged to expand lending to the cotton value chain. The PSAP noted that agriculture is a significant contributor to world Greenhouse Gas (GHG) emissions, and that programs to cap emissions or implement cap-and-trade programs could involve agriculture. However, the PSAP urged governments to move cautiously before including agriculture in a cap & trade program, noting that current technologies for the measurement of emissions and sequestration of carbon are poorly developed and difficult to assign on a farm-by-farm basis. The PSAP noted that the opportunity to sell credits for sequestration could be beneficial to agriculture, but the risks from inaccurate measurement of emissions could be harmful to the industry. The delegate of PAKISTAN noted that the use of pesticides in cotton production is a major concern and asked the PSAP for their recommendations in the use of pesticides. Members of the PSAP acknowledged that cotton production accounts for about 2.5% of world arable land but 8% of world pesticide use (pesticides include herbicides, insecticides and other crop protection chemicals) and that reductions in pesticide use are desirable. It was noted that the adoption of biotech cotton varieties is resulting in substantial reductions in the application of insecticides. Members of the PSAP urged governments to support research and extension programs that emphasize integrated pest management (IPM) to control weeds and insects and to facilitate the utilization of biotechnology in cotton through the adoption of biosafety protocols. The PSAP urged governments to support the work of the ICAC Expert Panel on Social, Environmental and Economic Performance (SEEP) of Cotton Production. The PSAP also cautioned government officials against acceptance of inaccurate statements by opponents of the cotton industry that exaggerate the use of chemicals in cotton production and distort the negative impacts of cotton production practices without providing context as to the benefits of the cotton industry. Mr. Neal Gillen, the ICAC Secretariat representative to the United Nations Commission on International Trade Law (UNCITRAL) reported that the cotton futures contract traded in New York on the Intercontinental Exchange (ICE) had become dysfunctional in March 2008, and that better regulation of commodity futures contracts in the U.S. was needed to restore confidence in the cotton market. Mr. Gillen noted that in recent years, the Commodity Futures Trading Commission (CFTC) had granted waivers to financial funds to trade commodity futures as hedgers without having to meet speculative position limits. This had allowed an influx of money into commodity futures markets, thus reducing the role of the futures contracts as hedging tools used primarily by companies involved in cotton supply and use. Mr. Gillen reported that the American Cotton Shippers Association (ACSA) is requesting that the CFTC require all trades to be registered on regulated exchanges or cleared through a central clearing mechanism and that all parties be required to post margins covering outstanding futures and options commitments. Mr. Gillen said he expects action in the U.S. within 2009. Members of the PSAP reported to the Standing Committee that some countries require complicated and expensive adherence to phytosanitary requirements. An example was given of one country that allows only 14 days between the issuance of a phytosanitary certificate in the country of origin and the arrival of the cargo at the port of destination. This is not a realistic time frame for shipments of cotton via ocean freight. The PSAP urged countries to standardize phytosanitary requirements and to ensure that requirements are pragmatic.

6

The PSAP renewed its support for a successful conclusion to the Doha Round and urged governments to continue their efforts to negotiate a reduction and eventual elimination of measures that distort cotton production and trade. The PSAP asked governments to be aware that issues associated with resource depletion are of concern to the private sector and should be studied. The PSAP urged that the topic of water use should be discussed during the plenary meeting. Individual members of the PSAP from India, Egypt and Turkey said they were interested in establishing a new cotton classing and marketing school. The CHAIR of the Standing Committee noted that several similar schools exist in the United States, the UK, Poland and perhaps other countries, and that the Standing Committee supports all efforts to expand opportunities for training in cotton subjects. Dr. Gazanfer again thanked the Chair and members of the Standing Committee for the opportunity to engage in discussions. He thanked all members of the PSAP for traveling to Washington for the meeting, and he thanked the Secretariat for its support. The CHAIR thanked Dr. Gazanfer and members of the PSAP for their input and the quality of their work. 4. Other Matters

a) Election of Standing Committee Officers (Aide Memoire) The CHAIR called the attention of Standing Committee members to the Aide Memoire circulated on May 13, 2009 announcing that a Nominating Committee had met and agreed that Mr. Azmat Ali Ranjha of Pakistan should be nominated to serve as Chair of the Standing Committee during 2009-10, that Mr. Patrick Packnett of the U.S. should be nominated to serve as First Vice Chair and that Ms. Lily Munanka of Tanzania should be nominated to serve as Second Vice Chair. Seeing no objections, the CHAIR found that there was a consensus to forward the nominations of Mr. Ranjha, Mr. Packnett and Ms. Munanka to the Advisory Committee in Cape Town for final election. The CHAIR offered his congratulations to the three nominees.

b) Report from the Secretariat: World Cotton Situation -- distribution only (Attachment I) c) Review of the Status of Cotton Projects -- distribution only (Attachment III) d) Countries in arrears in the payment of assessments -- distribution only (Attachment IV)

The CHAIR noted that attachments I, III and IV had been included for distribution only and asked if there were comments or questions. Seeing none, the chair moved to Other Matters.

e) Other Matters The delegate of CHINA (TAIWAN) announced that his government has agreed to provide a second contribution of $10,000 to support the work of the Expert Panel on SEEP. The delegate urged other countries to do so also. The delegates of BRAZIL and SWITZERLAND announced that they will be leaving Washington in July on regular rotation of assignments. They thanked other delegates and the Secretariat for the opportunity to work cooperatively in support of the cotton industry during their assignments in Washington. The delegate of SOUTH AFRICA thanked the Chair of the Standing Committee and the Secretariat for the arrangements for the meeting and the opportunity to meet with the PSAP. The delegate said that the meeting had been helpful in better understanding the concerns of the private sector on climate change, phytosanitary regulations, the WTO and other matters. Seeing no other business, the CHAIR thanked delegates for their participation. The meeting was adjourned at 12:14 PM.

INTERNATIONAL COTTON ADVISORY COMMITTEE

Standing Committee Attachment I to SC-N-499 Washington, DC May 22, 2009

WORLD COTTON SITUATION

Outlook for World Cotton Supply and Use in 2009/10 Production Still Declining World cotton production declined in both 2007/08 (by 2%) and 2008/09 (by 10%) to 23.6 million tons, the smallest amount produced since 2003/04. These two consecutive declines resulted principally from decreases in cotton area, caused by lower cotton prices relative to competing crop prices, and higher production costs. World cotton area decreased by 5% in 2007/08 and 6% in 2008/09, to 30.8 million hectares. The world yield climbed to a record of 795 kg/ha in 2007/08, but was estimated down to 766 kg/ha in 2008/09 due mainly to unfavorable weather. In 2009/10, world cotton production is expected to continue to decline by 1% to 23.4 million tons. Decreasing cotton returns, more attractive prices for competing crops, and expected difficulties in financing inputs (due to the tightening of credit conditions as a result of the global economic crisis) are discouraging farmers from planting cotton. World cotton area is forecast down by 3% to 30 million hectares in 2009/10, the second lowest since 1950/51.

1 The average yield is projected at 782 kg/ha,

slightly higher than in 2008/09, assuming more favorable weather. China (Mainland) Despite significant government purchases from the 2008/09 crop for the national reserve at prices above international levels, average seedcotton prices paid to farmers were lower in 2008/09 than in the previous season. As production costs increased significantly in 2008/09, but the average yield was smaller and prices received were also lower, net returns to cotton producers declined. As a result, cotton area is estimated down by 9% in China (Mainland) to 5.7 million hectares. Assuming a slightly higher yield in 2009/10, production is expected to decline by 7% to 7.5 million tons. This would be the smallest crop since 2005/06. India The considerable increase in seedcotton Minimum Support Prices (MSPs for the main varieties of cotton were raised by around 40% from 2007/08) supported producers’ prices above international levels in 2008/09. This seems to have offset the decline in yields caused by an unfavorable monsoon season. Cotton area in India is expected to increase by 1% to 9.5 million hectares in 2009/10, accounting for 32% of world cotton area. Assuming a small rise in the average yield, production is forecast 9% higher at 5.4 million tons. United States Cotton prices remain less attractive than prices of competing crops in the United States. In addition, the increase in agricultural production costs in recent years has affected cotton more than its main competing crops (corn, soybeans and wheat). As a result, US planted cotton area is projected down in 2009/10 for the third consecutive season, to 3.6 million hectares, the lowest since 1983/84. However, assuming an abandonment rate lower than in 2008/09 (when it was unusually high), harvested cotton area could increase slightly to 3.1 million hectares (but would be the second lowest in 20 years). The average yield is projected a little higher than in 2008/09. As a result, production is expected to increase by 4% to 2.9 million tons in 2009/10. Pakistan Under the influence of international cotton prices and the decline in domestic mill use, local cotton prices declined significantly between August and November 2008. These prices stabilized in December and recovered partially in January and February 2009. Cotton area is expected to increase slightly in 2009/10, to 2.9 million hectares. Assuming an average yield similar to the one estimated in 2008/09, production is expected to increase by 2% to 2 million tons.

1 World cotton area was estimated at 29.5 million hectares in 1986/87.

2

Uzbekistan Cotton plantings in Uzbekistan were little affected by variations in international prices in the past. Cotton area has remained stable since 2000/01, ranging from 1.39 to 1.45 million hectares. However, the Uzbek government announced in October 2008 that the target cotton area would be reduced in 2009/10 by around 5 percent, to 1.3 million hectares in order to increase the production of food crops. Assuming a yield similar to last season’s yield, production is expected to decrease by 4% to 1.0 million tons in 2009/10. CFA Zone The combination of low seed cotton prices and other problems, including inclement weather, higher fertilizer prices, delayed and/or diminished input applications, contributed to decrease the incentive to grow cotton in the region in the last few years. Cotton area declined from a record 2.5 million hectares in 2004/05 to 1.4 million hectares in 2008/09, the lowest since 1993/94. Cotton production in the region dropped by half from a record of 1.1 million tons in 2004/05 to 550,000 tons in 2008/09. The average regional yield has remained below 400 kg/ha since 2005/06 but has recovered slightly in the last two seasons. The minimum seed cotton prices to be paid to producers in 2009/10 are starting to be announced in some countries, and they are lower than in 2008/09. The tight credit conditions might impact the cotton companies’ and local farmers’ ability to purchase adequate quantities of fertilizers and pesticides in 2009/10. Cotton area is expected to continue to decline to 1.3 million hectares, and production is forecast at 500,000 tons, 9% lower than the level reached in 2008/09 and the lowest since 1989/90. Turkey Cotton area in Turkey declined significantly during the last two seasons, reaching 365,000 hectares in 2008/09, or 42% less than in 2006/07 and the smallest since the 1940s. In the last few years, farmers’ returns from cotton production were lower than returns from alternative crops, such as maize, wheat and soybeans. This has encouraged farmers to cultivate less cotton in favor of these other crops. Production was estimated at 450,000 tons in 2008/09, 28% less than in the previous season. Prices of cotton remain less attractive than prices of competing commodities, and its production cost are higher. Lower seed cotton premiums than last season were announced for 2008/09. As a result, it is expected that cotton area in Turkey is continuing to decline in 2009/10 to 330,000 hectares. Production is forecast a little over 400,000 tons, the smallest since the end of the 1960s. Brazil Area devoted to cotton in Brazil declined in the last two seasons because of higher production costs and difficulties in obtaining credit, which are amplified by the decline in forward purchases by merchants. Brazilian 2009/10 cotton plantings will start in November 2009 and are expected to continue to decrease by 6% to 800,000 hectares. Production is forecast at 1.16 million tons, down by 7% from 2008/09. Possible Small Recovery in Mill Use World cotton mill use was estimated stable in 2007/08, at 26.3 million tons, but fell in 2008/09 for the first time in a decade, by an estimated 13% (the largest decline since World War Two) to 22.9 million tons. World cotton mill use is expected to increase slightly to 23.1 million tons (+1%) in 2009/10. This projection is based on a modest recovery in world economic growth in 2010. According to the April 2009 projections of the International Monetary Fund (IMF), global economic growth decelerated from 5.2% in 2007 to 3.2% in 2008, and a contraction of 1.3% in global economic growth is expected in 2009. A gradual recovery to 1.9% growth is forecast in 2010. However, the global economic outlook for 2010 remains very uncertain. Cotton mill use is expected to partially recover in China (Mainland), India, Pakistan, Bangladesh, Indonesia and Vietnam in 2009/10. Chinese cotton mill use is forecast at 9.2 million tons, up by 2% from 2008/09 and accounting for 40% of the world total. Indian cotton mill use is projected to rise by 3% to 3.9 million tons. Pakistan cotton mill use is expected 2% higher at 2.5 million tons. Since 2007/08, these three countries have accounted for about two-thirds of global cotton mill use. However, cotton mill use is expected to continue to decline in Turkey, the United States, and many smaller consuming countries in Asia, North America and Europe.

3

Upturn in Trade World cotton trade was estimated at 8.3 million tons in 2007/08. However, as a result of the decline in demand from importing countries, world cotton trade is projected down sharply to 6.0 million tons in 2008/09; this is the smallest volume traded since 2000/01. World cotton trade is expected to partially recover in 2009/10. World imports are projected 9% higher at 6.6 million tons. An expected increase in imports by China (Mainland) to 1.7 million tons, as cotton mill use is expected to increase, would significantly contribute to this rebound. Imports by Bangladesh and Turkey are also forecast to increase in 2009/10, to around 600,000 tons each. Imports by Pakistan are expected to increase to 535,000 tons. The rise in shipments to Pakistan and Bangladesh would result from rebounding mill use, while the rise in shipments to Turkey would make up for the expected decline in production. India is expected to account for most of the expected rise in exports, with Indian shipments forecast to almost triple to 1.2 million tons. India’s share of world exports is expected to rebound to 18% in 2009/10, similar to the share reached in 2007/08. Uzbek exports are also forecast to increase to 700,000 tons and Australian exports to 340,000 tons. However, exports from the United States are expected to decline by 11% to 2.3 million tons in 2009/10, and exports from Brazil are forecast down to less than 300,000 tons. Stocks Rising Again World ending stocks declined slightly in 2007/08, to 12.4 million tons, but they are projected to increase by 6% to 13.1 million tons by the end of 2008/09. Their share of world mill use is expected to increase from 47% in 2007/08 to 57% in 2009/10, the highest share since 1998/99. World production is forecast to exceed mill use in 2009/10 for the fifth time in six seasons. As a result, world cotton stocks are expected to increase by 3% to a record of 13.4 million tons, accounting for 58% of world mill use. Stocks outside of China (Mainland) are forecast 4% higher than in 2008/09 at 9.6 million tons. Stocks in China (Mainland) are expected to remain stable at 3.8 million tons. Cotton Prices Expected Slightly Lower Taking into account the expected significant increase in the stocks-to-mill use ratio in the World-less-China (Mainland) in 2008/09, and the average Cotlook A Index between August 2008 and the first three weeks of April 2009, the ICAC Price Model 2007 projects the season-average Cotlook A Index at 60 cents per pound in 2008/09, down by 18% from last season. The 95% confidence interval ranges from 58 to 62 cents per pound. Based on this price forecast for 2008/09, the ICAC Price Model 2007 forecasts a season-average Cotlook A Index of 58 cents per pound in 2009/10 (the 95% confidence interval is between 47 and 66 cents per pound). This would represent a 3% decline from the 2008/09 average. However, major uncertainties regarding projected cotton trade in 2009/10 pose substantial downward risks to the forecast.

1

Outlook on World Cotton

Supply and Use

Armelle Gruere, ICAC

SCM 499

May 22, 200918

20

22

24

26

28

99/00 01/02 03/04 05/06 07/08 09/10

Million tons

World Production and Mill Use

Production

Consumption

300

500

700

900

1,100

99/00 01/02 03/04 05/06 07/08 09/10

10

20

30

40

World Cotton Area and Yield

Million hectaresKg/ha

Area

Yield

Production

0

2

4

6

8

China

(M)

India US Pak. Brazil Uzbek. CFA Turkey

08/09 09/10

Million tons

World Cotton Mill Use

Million Tons

0

5

10

15

20

25

30

99/00 01/02 03/04 05/06 07/08 09/10

China (M) Rest of the World

World Imports

0

2.5

5

7.5

10

99/00 01/02 03/04 05/06 07/08 09/10

China (M) Rest of the W

Million tons

2

Exports

0

1

2

3

USA India Uzbek. Brazil CFA Australia

08/09 09/10

Million tons

35%

45%

55%

65%

99/00 01/02 03/04 05/06 07/08 09/10

SMU in World-less-China (M)

40

50

60

70

80

90

100

84/85 89/90 94/95 99/00 04/05 09/10

Cotlook A IndexSeason-average (US cents/lb)

58

66

47

International Cotton Advisory

Committee

ICAC SUPPLY AND DISTRIBUTION OF COTTON

Years Beginning August 1

2005 2006 2007 2008 2009 2010

Est. Proj. Proj. Proj.

Million Metric Tons

BEGINNING STOCKS

WORLD TOTAL 11.628 12.318 12.710 12.381 13.07 13.40

CHINA (MAINLAND) 2.622 3.991 3.653 3.321 3.78 3.77 USA 1.196 1.321 2.064 2.187 1.59 1.42

PRODUCTION

WORLD TOTAL 25.639 26.718 26.213 23.620 23.45 22.61

CHINA (MAINLAND) 6.616 7.975 8.071 8.025 7.47 7.10

INDIA 4.097 4.760 5.355 4.930 5.36 5.19

USA 5.201 4.700 4.182 2.790 2.90 2.88

PAKISTAN 2.194 2.147 1.894 1.960 2.00 1.92

BRAZIL 1.038 1.524 1.603 1.253 1.16 1.11

UZBEKISTAN 1.210 1.171 1.206 1.070 1.03 0.98

OTHERS 5.283 4.441 3.903 3.592 3.53 3.43

CONSUMPTION

WORLD TOTAL 24.947 26.357 26.319 22.874 23.11 23.17

CHINA (MAINLAND) 9.439 10.600 10.900 9.000 9.18 9.30

INDIA 3.655 3.908 3.986 3.767 3.88 3.95

PAKISTAN 2.532 2.633 2.637 2.426 2.47 2.52

EU, C. EUR. & TURKEY 2.110 2.079 1.744 1.344 1.29 1.22

EAST ASIA & AUSTRALIA 1.885 1.872 1.823 1.648 1.63 1.62

USA 1.278 1.074 0.999 0.773 0.75 0.72

BRAZIL 0.973 1.000 1.033 0.961 0.96 0.93

CIS 0.633 0.682 0.664 0.601 0.59 0.58

OTHERS 2.441 2.509 2.533 2.353 2.35 2.33

EXPORTS

WORLD TOTAL 9.731 8.101 8.368 6.057 6.56 7.04

USA 3.821 2.833 2.973 2.613 2.33 2.27

INDIA 0.751 0.960 1.530 0.400 1.15 1.49

UZBEKISTAN 1.020 0.980 0.887 0.550 0.70 0.84

CFA ZONE 1.010 0.924 0.589 0.475 0.48 0.50 BRAZIL 0.429 0.283 0.486 0.540 0.28 0.24 AUSTRALIA 0.628 0.465 0.265 0.230 0.34 0.44

IMPORTS

WORLD TOTAL 9.605 8.127 8.275 6.000 6.56 7.04

CHINA (MAINLAND) 4.200 2.306 2.511 1.452 1.72 2.21

EAST ASIA & AUSTRALIA 1.776 1.902 1.839 1.602 1.63 1.59

EU, C. EUR. & TURKEY 1.274 1.342 1.081 0.747 0.85 0.79

PAKISTAN 0.352 0.502 0.851 0.375 0.54 0.65

CIS 0.333 0.322 0.271 0.238 0.23 0.00

TRADE IMBALANCE 1/ -0.126 0.026 -0.093 -0.057 0.00 0.00

STOCKS ADJUSTMENT 2/ 0.123 0.005 -0.129 0.000 0.00 0.00

ENDING STOCKS

WORLD TOTAL 12.318 12.710 12.381 13.070 13.40 12.85

CHINA (MAINLAND) 3.991 3.653 3.321 3.775 3.77 3.77 USA 1.321 2.064 2.187 1.592 1.42 1.31

ENDING STOCKS/MILL USE (%)

WORLD-LESS-CHINA (M) 3/ 54 57 59 67 69 66

CHINA (MAINLAND) 4/ 42 34 30 42 41 40

COTLOOK A INDEX 5/ 56.15 59.15 72.90 60* 58**

1/ The inclusion of linters and waste, changes in weight during transit, differences in reporting periods and measurement error account for differences between world imports and exports.2/ Difference between calculated stocks and actual; amounts for forward seasons are anticipated.3/ World-less-China (Mainland) ending stocks divided by World-less-China (Mainland)'s mill use, multiplied by 100.4/ China (Mainland)'s ending stocks divided by China (Mainland)'s mill use, multiplied by 100.

* The price projection for 2008/09 is based on the ending stocks/consumption ratio in the world-less-China (Mainland) in 2006/07, in 2007/08 (estimate), and in 2008/09 (projection), on the ratio of Chinese net imports to world imports in 2007/08 (estimate) and 2008/09 (projection), and on the average price for the first ten months of 2008/09.95% confidence interval: 58 to 62 cents per pound.** The price projection for 2009/10 is based on the ending stocks/consumption ratio in the world-less-China (Mainland) in 2007/08 (estimate), in 2008/09 (projection), and in 2009/10 (projection), and on the ratio of Chinese net imports to world imports in 2008/09 (projection) and 2009/10 (projection).95% confidence interval: 47 to 66 cents per pound.

May 20, 2009

5/ U.S. cents per pound.

INTERNATIONAL COTTON ADVISORY COMMITTEE

Standing Committee Attachment II to SC-N-499 Washington, DC May 20, 2009

Government Support to the Cotton Industry (Revised)

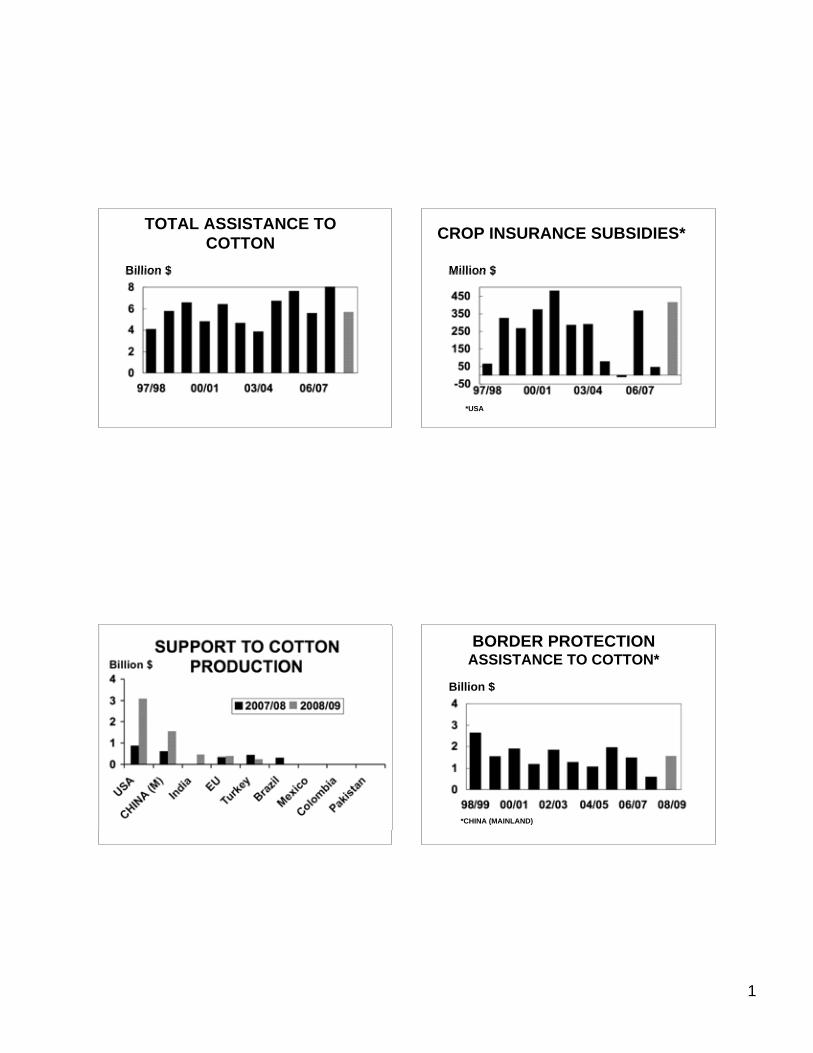

Subsidies to the cotton industry, including direct support to production, border protection, crop insurance subsidies, minimum support price mechanisms and export subsidies are rising by more than twofold from $2.7 billion in 2007/08 to an estimated $5.7 billion in 2008/09. Government subsidies were provided by ten countries in 2008/09, and the subsidies average 13 cents per pound, compared with 8 cents per pound in 2007/08. This marks the highest level of direct government support to the cotton industry since 2005/06. The Cotlook A Index averaged 61 cents per pound during the first nine months of 2008/09, or 12 cents lower than in 2007/08. As a consequence, declining domestic cotton prices in 2008/09 have triggered different types of government interventions aiming to support producers’ revenues in the largest cotton producing countries. The highest level of direct government assistance to the cotton sector was $7.7 billion in 2005/06 provided by eight countries, when the Cotlook A Index averaged 56 cents per pound. Fourteen countries provided US$5.8 billion in direct assistance to production in 2001/02, when the Cotlook A Index averaged just 42 cents per pound. The share of world cotton production receiving direct government assistance, including direct payments and border protection, increased from an average of 55% between 1997/98 and 2007/08, to an estimated 84% in 2008/09. Since 1997/98, there is clearly a negative correlation between the Cotlook A Index and the amount of subsidy provided to the world cotton industry, as well as the number of subsidizing countries. As a result of decreased international prices, the estimate of government support to cotton production resulting from minimum support price mechanisms and border protection policies rose from $614 million in 2007/08 to an estimated $2 billion in 2008/09. The level of direct government assistance provided through export programs is estimated to have decreased from $400 million in 2005/06 to $30 million in 2007/08 and is expected to decline to almost zero in 2008/09, due to reduced production of extra-fine cotton. During the past three seasons, only the U.S. Pima competitiveness program remains in effect. United States The 2007 farm bill went into effect in the United States in 2008/09. Most of the provisions of the support program to cotton producers remained similar to the 2002 farm bill. The same mechanisms as before channel direct support to cotton production: a direct payment (DP), a counter-cyclical payment (CCP), a loan deficiency payment (LDP), certificate exchange gains and marketing loan gains. The DP, which is independent of market prices and is based on historical planted area and yield, is set at 6.67 cents per pound. It is estimated, that in 2008/09 the DP rose to $632 million (+$59 million from 2007/08). The CCP, which is also based on historical planted area and yield, is paid when the effective price is below the target price (71.25 cents per pound or 1.15 cents lower than under the previous farm bill).

1 The CCP to eligible farmers increased in 2008/09 to a projected $816 million (+$549 million).

The LDP is paid when market prices (the adjusted world price or AWP) are below the loan rate (52 cents per pound). The AWP stayed above the loan rate during 2007/08, eliminating the LDP. However, in 2008/09, the AWP fell below the loan rate during the second week of October 2008 and has remained lower than this threshold to date, making LDP available to producers. The LDP is estimated to reach $143 million.

1 The effective price is the DP plus the higher of the national average market price paid to producers or

the loan rate.

2

In addition, producers are able to buy commodity certificates at the rate of the adjusted world price (AWP) and exchange them on the same day for cotton pledged as collateral to the Commodity Credit Corporation (CCC) for a commodity loan. Realized gains from the certificate exchange, called certificate exchange gains, equal the amount by which the loan rate exceeds the AWP. Certificate exchange gains are similar to the LDP. It is estimated that certificate exchange gains rose from zero in 2007/08 to $884 million. Producers also may receive gains called marketing loan gains if the loan repayment rate is less than the loan principal, also called loan write-offs. Marketing loan gains rose from zero in 2007/08, to a projected $97 million in 2008/09. Another form of government support to cotton production in the USA is provided through subsidized crop insurance to protect producers against losses to crop yields caused by natural disasters. Nearly every cause of decline in crop yields is covered by this multi-peril crop insurance, such as weather, pests, and fire, but not producer negligence. While the insurance is sold to farmers, largely through private insurance providers, the USDA’s Risk Management Agency (RMA) pays in excess of 50% of the premiums. Additionally, the RMA pays the private insurance providers toward their administrative and operating costs, plus the RMA’s own administrative costs under the program. On average, more than 90% of planted cotton acreage is enrolled in the program. By design, the crop insurance program is supposed to be actuarially sound, meaning that over time total premiums are supposed to cover total indemnities. In practice, however, during the past 11 years, the premiums exceeded indemnities only in 1997, 2004, 2005 and 2007. The net losses (indemnities over premiums) fall upon the government, because it reinsures the privately marketed policies. The net losses are added to the premium subsidies to calculate a total cost of crop insurance to the government. Total premium and indemnity subsidies averaged $249 million per year between 1997 and 2008, with the highest cost of $482 million paid in 2001. The government received $9 million in 2005 when the unsubsidized part of premiums exceeded premium subsidies and indemnities. Total crop subsidies fluctuated from 0.5 cent per pound of total production to 7 cents per pound during the past 11 years. In 2008/09 total crop insurance subsidies are estimated at $413 million (+366 million from 2007/08), or 6.7 cents per pound (+6.2 cents per pound) of total production. Total direct U.S. support to cotton production increased from $888 million in 2007/08 to $3.1 billion in 2008/09, or an equivalent of 50 cents per pound of actual production. During the past 11 years the highest U.S. direct support to cotton production of $3.9 billion was provided in 2004/05, an equivalent of 35 cents per pound of production. China (Mainland) During the past several seasons, government policies in China (Mainland) were aimed at supporting cotton production by exercising border protection measures based on sliding scale duties. As a result of import quotas, domestic cotton prices in China (Mainland) were above international prices in recent seasons. The Secretariat uses the difference between domestic and imported cotton prices as an estimate of the support to Chinese domestic cotton prices, which results from border protection. In 2008/09, in order to support producers’ prices, the Chinese government started directly buying considerable amounts of cotton. The China National Cotton Reserves Corporation (CNCRC) purchased a total of 2.724 million tons of cotton, or a third of the estimated 2008/09 production. The cotton purchased for the government reserve was paid at a base procurement price of 12,600 yuan/ton for Type 328 (equivalent to 84 US cents/lb as of the beginning of May, 2009). Government purchases of cotton in 2008/09 have maintained domestic cotton prices in China (Mainland) above international prices. The Secretariat uses the difference between domestic and imported cotton prices as an estimate of the support to Chinese cotton prices that results from government interventions. The price differential between the CC index (an index of mill delivered cotton in China) and the FC Index L (an index of imported cotton arriving in Chinese main ports), adjusted to include value added tax, port

3

charges and transportation to mills averaged 8.7 US cents per pound from August 2008 to May 2009 (3.4 cents per pound in 2007/08). As a result, the estimate of benefits resulting from government intervention in China (Mainland) received by producers as of mid-season 2008/09 is about US$1.5 billion (+$860 million from 2007/08). The Chinese government also announced in the last quarter of 2008 that it might delay the opening of sliding-scale cotton import quotas in 2009. The annual 894,000 ton-quota associated with a 1% duty and agreed upon China (Mainland)’s accession to the World Trade Organization was opened as expected on January 1, 2009. No additional quota for 2009 has been announced since. India The government of India significantly increased seed cotton minimum support prices (MSPs) for the 2008/09 season. MSPs were increased by around 40% from last season for the main varieties produced in India. When farmers’ seedcotton prices fall below these minimum prices, government agencies start buying seedcotton at the MSPs, and do so until market prices reach these levels again. Indian seedcotton prices have been affected by the trend in international prices since the beginning of the season and fell below the MSPs. As a result, by the end of April 2009 government agencies had purchased around 2.15 million tons of cotton lint, or a little over 40% of estimated 2008/09 production. The Secretariat uses prices for the H-4 cotton variety as the reference for which the MSP was increased from 2,030 to 2,850 rupees per quintal between 2007/08 and 2008/09. The Secretariat used the average difference between spot prices of H-4 seedcotton and the Cotlook A Index calculated between October 2008 and April 2009, adjusted for transportation cost, as an estimate of the support to India cotton prices that results from government’s intervention. The average differential between the adjusted spot prices for H-4 and the Cotlook A Index between October 2008 and April 2009 was 4 US cents per pound. The difference, if applied to total production, would indicate that the impact of government intervention as a result of MSP increase would increase cotton farm revenues in India by about US$443 million. The Indian government also announced a 5% tax credit on cotton exports with effect from April 1, 2008, and discounts for volume purchases of cotton from government agencies’ stocks. By the end of April, over one million tons of government agencies’ stocks had been sold to domestic mills and traders, leaving a little less than one million tons under government control. Pakistan The Trading Corporation of Pakistan (TCP) purchases cotton when domestic prices fall below the minimum price announced by the government. The TCP purchased in December 2008 and January 2009 around 100,000 tons of cotton from ginners, or about 5% of the estimated 2008/09 crop, at around 3,200 Pakistan rupees per maund (49 US cents per pound in December 2008). However, as of mid-May 2009 only a third of the cotton contracted by the TCP had been delivered, while the remaining contracts could be canceled by the growers due to increased prices in the domestic market. The Secretariat estimates that total expenses by the TCP on cotton support up to now have totaled around 650 million Pakistan rupees or US$8 million. European Union Changes in EU Common Agricultural Policy (CAP) were made effective January 1, 2006 applicable to the 2006/07, 2007/08 and 2008/09 seasons. Under this new program, EU cotton producers receive 65% of EU support as a single decoupled payment (income aid) and the remaining 35% as an area payment (coupled or production aid). The total budget allocated for these payments is around 770 million, the same as under the previous regime. In 2008/09 the 35% coupled payment is given for a maximum area of 270,000 hectares in Greece and 48,000 hectares in Spain and is proportionately reduced if claims exceed the maximum area allocated to each country. To receive coupled area payments, producers must plant cotton and grow the crop until the stage of boll opening in normal agricultural conditions, but they are not forced to harvest the cotton. The amount of coupled support to cotton production in 2008/09 in the EU is estimated at $383 million (+$25 million from 2007/08). The amount of direct subsidy per pound of cotton in 2007/08 increased from 42 to 55 US cents per pound for Greek cotton and from 93 to 228 US cents per

4

pound for Spanish cotton. The higher direct subsidy per pound of cotton in Spain is due to significantly lower-than-average yields. Turkey The government of Turkey pays a premium per kilogram of seedcotton to cotton producers (the premium is higher for seedcotton produced from certified seeds). The premiums announced for 2008/09 are 0.27TRL/kg for seedcotton produced from regular seeds (or 20 US cents per pound of lint as of May 15, 2009) and 0.32TRL/kg for seedcotton produced from certified seeds (or 24 US cents per pound of lint as of May 15, 2009). These premiums are slightly lower than in 2007/08. Assuming that 90% of Turkish cotton production is produced from certified seeds, and that all cotton producers will apply for the premium, the Secretariat estimates that total payments to cotton producers in Turkey could amount to 354 million new Turkish liras, equivalent to US$233 million (as of May 15, 2009). This is much lower than the total payments provided in 2007/08 (US$429 million), due mainly to the decline in production. Brazil There were several types of income support programs for producers utilized by the government of Brazil in the past, including a program based on government purchases with guaranteed prices. A program based on marketing through direct subsidies paid to producers based on guaranteed prices, but without direct acquisition of cotton by the government, was implemented in 2006 and continued in 2007 and in 2008. The program actively implemented during 2006/07 and 2007/08 is called the Equalizer Price Paid to the Producer (PEPRO – Prêmio Equalizador Pago ao Produtor). In essence, the premium paid under the program represents the difference between the minimum-guaranteed price and the price the buyer is willing to pay. The minimum-guaranteed price is set at R$ (Brazilian reais) 44.60 per arroba (15 kg) of lint, or an equivalent of 63.50 cents per pound at the exchange rate as of May 2009. The PEPRO is used to compensate farmers for the weakening US dollar in relation to the reais. The actual size of the premium is determined at auctions organized by the government, where a large number of participants in practice bid for the premium. The government’s view is that a very competitive auction tends to result in a lower level of subsidies paid to producers. A total of R$209 million, or US$95 million, was paid to producers under the program during 2005/06, or the equivalent of 4 U.S. cents per pound. In 2006/07, payments under the program reached R$587 million, or $290 million, the equivalent of 9 US cents per pound. PEPRO auctions held in May-June 2008 resulted in total subsidies paid in 2007/08 amounting to R$549 million, equivalent of $337 million, or 10 cents per pound. As of May 20, 2009 there were no PEPRO auctions in 2008/09. Mexico In Mexico, a support price mechanism exists for major agricultural commodities, including cotton. The 2008/09 target price for cotton is 12,600 pesos/ton, or 43 US cents per pound as of May 15, 2009. The target price was reduced drastically from 67.75 US cents per pound set in 2007/08. The actual amount of support provided by the government to cotton producers is equal to the difference between the target price and the market price. The Secretariat estimates that during 2008/09 the amount of support provided by Mexico will be close to zero, because market prices remain above the target price. Colombia In Colombia, direct government payments to producers in 2008/09 are estimated at $10 million, averaging 10 cents per pound, about the same as in 2007/08. Registration of Cotton Exporters by the Government of China (Mainland) The General Administration of Quality Supervision Inspection & Quarantine (AQSIQ) of China (Mainland) has established a requirement for a registration process for foreign cotton suppliers effective March 15, 2009. The issue of the AQSIQ registration requirement was discussed at the 497

th Meeting of the

Standing Committee, where some delegates expressed their concerns about the new system. The major concerns are that the system would unfairly subject suppliers to different levels of inspection and oversight potentially based on a single infraction and may also damage the reputation of foreign suppliers through the publication of the downgraded ratings. The potential disruption in trade from this system could

5

be compounded by quality assessment methods for imported cotton diverging from those used internationally or used by China (Mainland) for domestic cotton. The Secretariat was instructed to monitor and report on developments with the AQSIQ registration system incorporating this information into the reports to the Committee. A total of four lists of registered companies was published by AQSIQ this year. As of the beginning of May 2009, 148 companies were registered with the AQSIQ. The list of registered companies includes major and smaller cotton firms from America, Asia, Africa, Europe and Australia, from all major exporting countries, including government owned firms, private and cooperative organizations. A meeting between the AQSIQ and Committee for International Co-operation between Cotton Associations (CICCA) officials was held in Beijing on April 28, 2009 to address concerns by CICCA members about the system. It was decided to continue collaboration on the issue by creating a working group between the International Cotton Association (ICA) and the AQSIQ.

Average AverageProduction Assistance Assistance

per Pound Assistance to per Pound Assistance to

Country Produced Production Production Produced Production1,000 tons US cents US$ Millions 1,000 tons US cents US$ Millions

USA 4,182 10 888 2,790 50 3,069Greece 285 42 265 240 55 293Turkey 625 31 429 450 23 233

Brazil 1,603 10 337 1,253 0 0Spain 41 103 93 18 228 90Mexico 137 3 8 125 0Colombia 38 12 10 36 13 10India 4,930 4 443China (Mainland) 8,071 4 684 8,025 9 1,544

Pakistan 1,923 0.2 8

All Countries 14,982 8 2,714 19,790 13 5,691

* Income and price support programs only. Credit and other assistance not included. ** Preliminary.

Average AverageExports Assistance Assistance

per Pound Assistance to per Pound Assistance to

Country Exported Exports Exports Exported Exports1,000 tons US cents US$ Millions 1,000 tons US cents US$ Millions

USA 2,973 0 30 2,613 0 0 Upland cotton 2,791 0 2,563 0 0

Pima 181 8 30 50 0 0

Total 2,973 0 30 2,613 0 0

** Preliminary.

2007/08 2008/09 **

Level of Direct Assistance Provided by Governments to

the Cotton Sector Through Production Programs *

2007/08 2008/09 **

Level of Direct Assistance Provided by Governments to

the Cotton Sector Through Export Programs

Level of Assistance Provided by USA to the Cotton

Sector Through Crop Insurance Programs

Average CropWorld Assistance Insurance

Production per Pound AssistanceProduced

1,000 tons US cents US$ Millions

1997/98 4,092 0.7 671998/99 3,030 4.9 3261999/00 3,694 3.3 267

2000/01 3,742 4.5 3742001/02 4,420 4.9 4822002/03 3,747 3.5 2872003/04 3,975 3.3 2902004/05 5,062 0.7 812005/06 5,201 -0.1 -92006/07 4,700 3.5 3672007/08 4,182 0.5 472008/09 ** 2,790 6.7 413

** Preliminary.

Total Level of Assistance Provided by Governments to

the Cotton Sector Through All Programs *

AverageAssistanceper Pound Assistance to

Production Produced Production1,000 tons US cents US$ Millions

1997/98 20,187 9.2 4,1081998/99 18,817 13.9 5,7721999/00 19,195 15.6 6,5882000/01 19,537 11 4,8332001/02 21,679 13 6,4462002/03 19,586 12 4,6692003/04 21,117 8 3,8922004/05 27,001 11 6,7372005/06 25,639 14 7,6732006/07 26,718 9 5,5932007/08 26,213 5 2,7442008/09 ** 23,579 11 5,691

* Income and price support programs only. Credit and other assistance not included. ** Preliminary.

1

TOTAL ASSISTANCE TO

COTTON

Billion $

CROP INSURANCE SUBSIDIES*

Million $

*USA

BORDER PROTECTIONASSISTANCE TO COTTON*

Billion $

*CHINA (MAINLAND)

INTERNATIONAL COTTON ADVISORY COMMITTEE

1629 K Street NW, Suite 702, Washington, DC 20006 USA

Telephone (202) 463-6660 • Fax (202) 463-6950 • e-mail [email protected]

Aide Memoire

To: Delegates to the Standing Committee, Coordinating Agencies and Members of the Private Sector Advisory Panel

From: Executive Director

Subject: Nominations of Standing Committee Officers for 2009-10

Date: May 13, 2009

A nominating committee met in the Economic & Commercial Bureau, Embassy of Egypt, to propose a slate of officers for the Standing Committee for the coming year. Delegates from Brazil, China (Taiwan), Egypt and Pakistan and the executive director attended the meeting. Dr. Ashraf El-Rabiey of Egypt, Chair of the Standing Committee, served as Chair of the Nominating Committee. The Rules and Regulations specify that when practicable, the First Vice Chair will be nominated to succeed the outgoing Chair and the Second Vice Chair nominated to succeed the First Vice Chair. The current First Vice Chair of the Standing Committee, Mr. Azmat Ali Ranjha, Minister (Trade), Embassy of Pakistan, will be able to serve as Chair next year. Accordingly, there was a consensus to nominate Mr. Ranjha as Chair. However, the current Second Vice Chair, Ms. Ayse Gül Barkçin, Chief Commercial Counselor, Embassy of the Republic of Turkey, expects to be reassigned to capital and will not be available to serve on the Standing Committee next year. The Rules and Regulations say that the election of officers should take into account: 1. Rotation on as broad a geographical basis as possible, 2. Adequate representation to importing and exporting countries, 3. Ability, interest and participation in the work of the Committee, and 4. Timely payment of assessments. After consideration of these factors, the Nominating Committee agreed that Mr. Patrick Packnett, Assistant Deputy Administrator, Foreign Agriculture Service, USDA, should be nominated to the post of First Vice Chair. The Nominating Committee agreed that Mrs. Lily Munanka, Head of Chancery, Embassy of Tanzania should be nominated to the post of Second Vice Chair. The nominations will be forwarded to the Standing Committee for provisional approval at its next meeting scheduled for May 22, 2009 at the Economic & Commercial Bureau, Embassy of Egypt. The recommendations of the Standing Committee will be forwarded to the Advisory Committee in Cape Town for final approval.

INTERNATIONAL COTTON ADVISORY COMMITTEE

Standing Committee Attachment III to SC-N-499 Washington, DC May 21, 2008

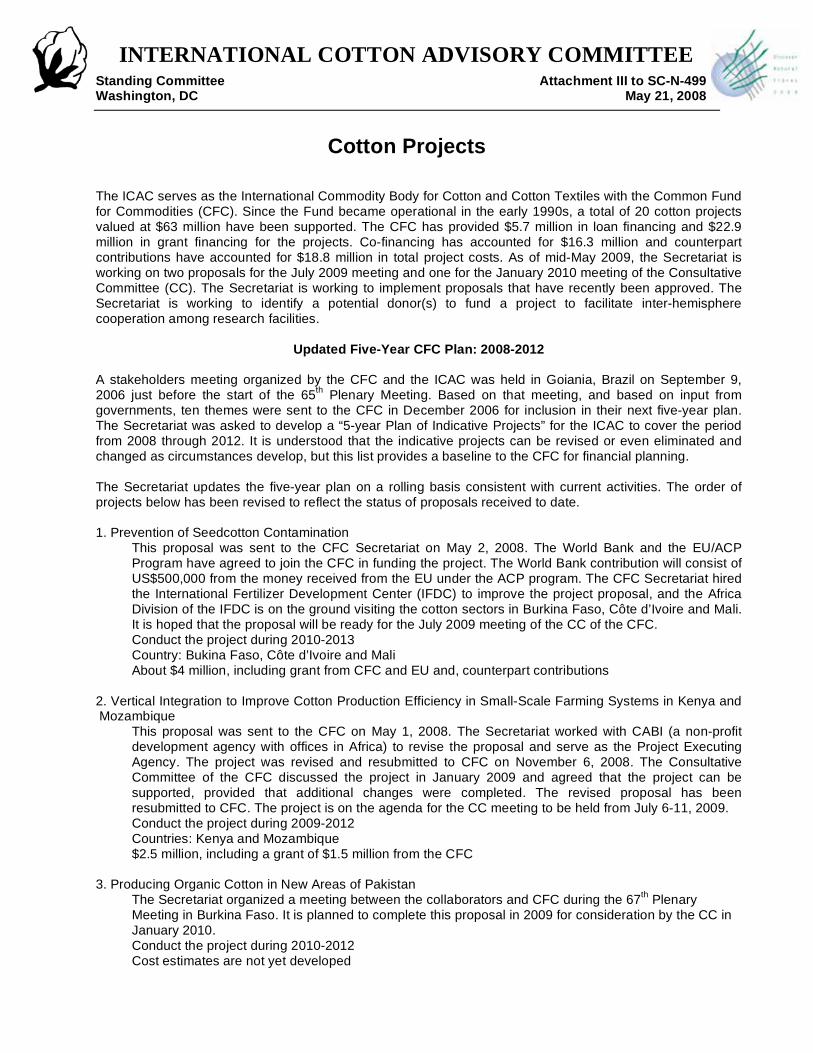

Cotton Projects The ICAC serves as the International Commodity Body for Cotton and Cotton Textiles with the Common Fund for Commodities (CFC). Since the Fund became operational in the early 1990s, a total of 20 cotton projects valued at $63 million have been supported. The CFC has provided $5.7 million in loan financing and $22.9 million in grant financing for the projects. Co-financing has accounted for $16.3 million and counterpart contributions have accounted for $18.8 million in total project costs. As of mid-May 2009, the Secretariat is working on two proposals for the July 2009 meeting and one for the January 2010 meeting of the Consultative Committee (CC). The Secretariat is working to implement proposals that have recently been approved. The Secretariat is working to identify a potential donor(s) to fund a project to facilitate inter-hemisphere cooperation among research facilities.

Updated Five-Year CFC Plan: 2008-2012 A stakeholders meeting organized by the CFC and the ICAC was held in Goiania, Brazil on September 9, 2006 just before the start of the 65

th Plenary Meeting. Based on that meeting, and based on input from

governments, ten themes were sent to the CFC in December 2006 for inclusion in their next five-year plan. The Secretariat was asked to develop a “5-year Plan of Indicative Projects” for the ICAC to cover the period from 2008 through 2012. It is understood that the indicative projects can be revised or even eliminated and changed as circumstances develop, but this list provides a baseline to the CFC for financial planning. The Secretariat updates the five-year plan on a rolling basis consistent with current activities. The order of projects below has been revised to reflect the status of proposals received to date. 1. Prevention of Seedcotton Contamination This proposal was sent to the CFC Secretariat on May 2, 2008. The World Bank and the EU/ACP

Program have agreed to join the CFC in funding the project. The World Bank contribution will consist of US$500,000 from the money received from the EU under the ACP program. The CFC Secretariat hired the International Fertilizer Development Center (IFDC) to improve the project proposal, and the Africa Division of the IFDC is on the ground visiting the cotton sectors in Burkina Faso, Côte d’Ivoire and Mali. It is hoped that the proposal will be ready for the July 2009 meeting of the CC of the CFC.

Conduct the project during 2010-2013 Country: Bukina Faso, Côte d’Ivoire and Mali About $4 million, including grant from CFC and EU and, counterpart contributions 2. Vertical Integration to Improve Cotton Production Efficiency in Small-Scale Farming Systems in Kenya and Mozambique This proposal was sent to the CFC on May 1, 2008. The Secretariat worked with CABI (a non-profit

development agency with offices in Africa) to revise the proposal and serve as the Project Executing Agency. The project was revised and resubmitted to CFC on November 6, 2008. The Consultative Committee of the CFC discussed the project in January 2009 and agreed that the project can be supported, provided that additional changes were completed. The revised proposal has been resubmitted to CFC. The project is on the agenda for the CC meeting to be held from July 6-11, 2009.

Conduct the project during 2009-2012 Countries: Kenya and Mozambique $2.5 million, including a grant of $1.5 million from the CFC 3. Producing Organic Cotton in New Areas of Pakistan The Secretariat organized a meeting between the collaborators and CFC during the 67

th Plenary

Meeting in Burkina Faso. It is planned to complete this proposal in 2009 for consideration by the CC in January 2010.

Conduct the project during 2010-2012 Cost estimates are not yet developed

2

4. By-Product Uses of Cotton in Zambia ICAC Secretariat has received a first draft of the proposal and started early consultations with the CFC

on the document. Conduct the project during 2010-2013 Exact Cost estimates are not available yet 5. Cotton Processing in West Africa This project is no longer being developed 6. Elimination of Insecticides from Intensive Farming Practices Complete this proposal in 2008/09 for consideration by the CC in July 2009 Conduct the project during 2009-2012 $5.0 million [The Secretariat does not have a proposal in the pipeline to fulfill this concept. Countries are invited to

consider this idea and develop a project proposal in cooperation with the Secretariat.] 7. Supply of Certified Planting Seed to Small Growers Complete this proposal in 2009 for consideration by the CC in January 2010 Conduct the project during 2010-2012 $2.0 mil (grant), 5.00 million (loan) [The Secretariat does not have a proposal in the pipeline to fulfill this concept. Countries are invited to

consider this idea and develop a project proposal in cooperation with the Secretariat.] 8. National Cotton Classification Systems in Syria & Nigeria Complete this proposal during 2010 based on results of the CSITC, for consideration by the CC in

January 2011 Conduct the project during 2011-2014 $4.0 million

I. New Proposals or Proposals Under Development Prevention of Seed cotton Contamination This is a continuation of the CFC/ICAC 32FT ‘Production and Marketing of Uncontaminated Cotton in Mali’ undertaken by the Cotton Program, Institute of Rural Economy, Bamako, Mali from July 1, 2006 to February 29, 2008. The CFC/ICAC 32FT project established the level and type of contamination in seedcotton and lint, and found out how and why these contaminants are added to cotton. The new project will implement recommendations of the Fast Track project CFC/ICAC 32FT. The Secretariat has worked with the head of cotton research for CMDT, the cotton company in Mali, to develop the full project proposal. The Standing Committee approved this project in principle at the 492nd Meeting, subject to the condition that the Secretariat will work with the CFC to ensure that the project does not duplicate other efforts underway in the region. The proposal was sent to the CFC for consideration by the Consultative Committee (CC) at its meeting in July 2008. The CFC Secretariat indicated that they are concerned that the impending privatization of CMDT will disrupt project implementation. They are also concerned about projections for co-financing. The ICAC Secretariat and the CFC are optimistic that IFDC will develop a good proposal. It is hoped that the proposal will be ready for the July meeting of the CFC. EU and CFC will jointly support this project with some additional funding from the World Bank under ACP program. Vertical Integration to Improve Cotton Production Efficiency in Small-scale Farming Systems The profitability of cotton production for small producers in Sub-Saharan Africa is often marginal, due to average yields that are well below the potential of current varieties under rain-grown conditions [average seed cotton yields among smallholders in southern and eastern Africa range from 400 – 750 kg/ha, while yields in research plots can reach over 3000 kg/ha]. There is wide scope for improvements in production efficiency in the smallholder sector, placing the initial emphasis on profitability for the grower, rather than on increased yields. This can be addressed by ensuring that systems are in place to maximize the benefits of input use through promoting integrated crop management, backed by greater investment in the provision of technology

3

and associated support services. One way to do this is to encourage input and service delivery by the private sector through a vertically integrated commodity chain. Improved access to technology and the support to improving farmer’s knowledge of cotton ICM will improve the efficiency of input use, which, in turn, will encourage more farmers to grow cotton and lead to increases in national production as well as raising the average seed cotton yield. The Secretariat worked with a researcher from the Natural Resources Institute in the UK to develop the full project proposal. The Standing Committee approved this project in principle at the 492nd Meeting, subject to the condition that the Secretariat will work with the CFC to ensure that the project does not duplicate other efforts underway in the region. The proposal was revised by CABI Africa who will serve as the Project Executing Agency. CFC discussed the revised proposal in a meeting from January 19-24, 2009. CFC considered the project supportable but advised to make some changes in budget and enhance the role of ginneries in the project. The re-revised project is with the CFC and will be discussed by CC in the July meeting of the CFC. Promotion of Cotton Processing in West Africa The Secretariat received a proposal in early 2007 from the United Nations Industrial Development Organization (UNIDO) on the Promotion of Cotton Processing in West and Central Africa. The project aimed to help French speaking cotton-producing countries in West and Central Africa to process more cotton locally through expansion and improvement of handicraft weaving, dying and sewing activities. The UNIDO Secretariat, the ICAC Secretariat and the Ministère du Commerce, de la Promotion de l'Enterprise et de l'Artisanat, of Burkina Faso collaborated on the proposal for more than one year. However, it became apparent to the ICAC Secretariat that this project would not fulfill a valid need in the region. Since early 2007 when the UNIDO proposal was received, the Secretariat has become aware of a multitude of similar, and in some cases identical, projects to the one being proposed. Artisanal weaving projects are ubiquitous throughout Africa and have been supported by national and international programs since the 1970s. At the 67

th Plenary Meeting in Ouagadougou in November 2008, the Organizing Committee arranged

a fashion show featuring handmade cotton garments from Burkina Faso. It is self evident that additional support for artisanal weaving would not meet the objectives of the CFC to finance projects that would demonstrate new technologies of benefit to the cotton sector. Therefore, the Secretariat is no longer pursuing this particular proposal. However, the Secretariat remains open to suggestions for additional projects aimed at enhancing demand for cotton. Boll Weevil Control in Argentina Argentina prepared a proposal for a Fast Track Project to test the feasibility of minimizing the boll weevil population by attracting and killing the weevils during the off-season rather than spraying and killing the weevils during the growing season. The proposal was discussed and approved at the January 2007 meeting of the Consultative Committee of the CFC. Technical work has been concluded and accounts have been closed on this project. Argentina has already submitted the financial report to CFC. The Secretariat has received the revised report and is currently reviewing it for its completeness before recommending to CFC that report be accepted and project may be closed. Price Risk Management The Secretariat worked with the Secretariat of the CFC for nearly a decade to develop a project to improve the capacities of cotton producers in East and Southern African countries to make use of futures and options contracts traded in New York and elsewhere. The CFC Secretariat initiated this project, and money was quickly appropriated. However, a plethora of logistical impediments prevented implementation of the project. The latest word from the CFC Secretariat is that the project is “frozen” for the time being. Inter-Hemisphere Collaboration to Expedite Research Results for Small Scale Cotton Farmers Cotton is grown year round. While cotton growers in the Northern Hemisphere are harvesting, growers in the Southern Hemisphere are preparing to plant. Likewise, research involving field experiments is started and terminated at different times of the year in each hemisphere. Consequently, researchers in each hemisphere have to wait for the next season to confirm results or verify recommendations.

4

Based on a recommendation from the 66

th Plenary Meeting in 2007 in Turkey, the Secretariat has developed

a proposal to facilitate cooperation among research institutes in the northern and southern hemispheres so as to shorten the time required to complete seed breeding and other research projects. The ICAC Secretariat is seeking to establish sister-institute relationships between research institutes in the northern and southern hemispheres. It is envisioned that three sister-institute relationships involving six institutes (3 each in the northern and southern hemispheres) will be established. The ICAC contacted 12 potential collaborators (institutes/countries) with a potential interest in the Inter-Hemisphere linkage project to seek their opinions on the proposed linkages. The responses have been extremely encouraging. There is no doubt that national institutes need a coordinating organization and resources to facilitate international communication and visits. The ICAC Secretariat is willing to provide the coordination facility and implement the project directly. However, the help from an outside consultant is needed. The project proposal was sent to the EC, and the initial response was not negative. However, additional discussions indicated that the project proposal was not sufficiently time bound, outcome oriented or focused on Africa to warrant EC interest. Accordingly, the Secretariat is seeking new supporter for this proposal.

II. Summary of Ongoing Projects Funded by the CFC: 1) Commercial Standardization of Instrument Testing of Cotton

Project Executing Agency: Faserinstitut Bremen e.V., Germany Project Cost: $7.788 million CFC Grant: $2.030 million Counterpart Contributions: $2.753 million EC co-financing: $3.0 million

The project on Commercial Standardization of Instrument Testing of Cotton (CSITC) is now operational.

The CFC is contributing $2 million to the project, and $3 million is being provided through co-financing from the European Commission under its All-ACP Support Programme on Agricultural Commodities. The Secretariat is satisfied with the progress made so far.

2) Utilization of Cotton Plant By-Produce for Value Added Products

Project Executing Agency: Central Institute for Research on Cotton Technology (CIRCOT), India Project Cost: $2.190 million CFC Grant: $918,886

Counterpart Contribution: $1.377 million This project will develop processes for the commercially feasible production of fiberboard using cotton

stalk residue. A mid-term evaluation of the project was undertaken in November 2007. The project was scheduled for completion by September 30, 2008. The project has been extended to December 31, 2009 subject to the condition that project funds from the CFC are not affected. The final workshop for disseminating results to other countries is planned from November 8-10, 2009 in Nagpur, India. The Secretariat will attend the workshop. A researcher from the project has been invited to the 68

th Plenary