Insurer Solvency CONFERENCE PRESENTS. Welcome Presented by Concurrent Session B3 Insurer Solvency...

55

Insurer Solvency CONFERENCE PRESENTS

-

Upload

loren-barton -

Category

Documents

-

view

214 -

download

0

Transcript of Insurer Solvency CONFERENCE PRESENTS. Welcome Presented by Concurrent Session B3 Insurer Solvency...

Insurer Solvency

CONFERENCE

PRESENTS

WelcomeWelcome

Presented by

Concurrent Session B3

Insurer Solvency

Monday, September 14, 2009

CONFERENCE

3

Event_CRIMS20090914_InsurerSolvencyPanel.ppt

Presenter PanelInsurer Solvency Concurrent Session B3 September 14, 2009

Rating Agency Perspective

Richard Attanasio, Vice President, North America Property/CasualtyA.M. Best Company, Inc.

Moderator

George Simpson, Senior Manager, Insurance Risk ManagementCapital Power Corporation

Insurer Perspective

Lynn Oldfield, President Chartis

Broker Perspective

Brian McAskill, Managing Director Marsh Canada Limited

CONFERENCE

Rating Agency Perspective

Richard Attanasio - Vice President - North American P/C RIMS Canada ConferenceSeptember 14, 2009

AgendaA.M. Best’s Rating Process

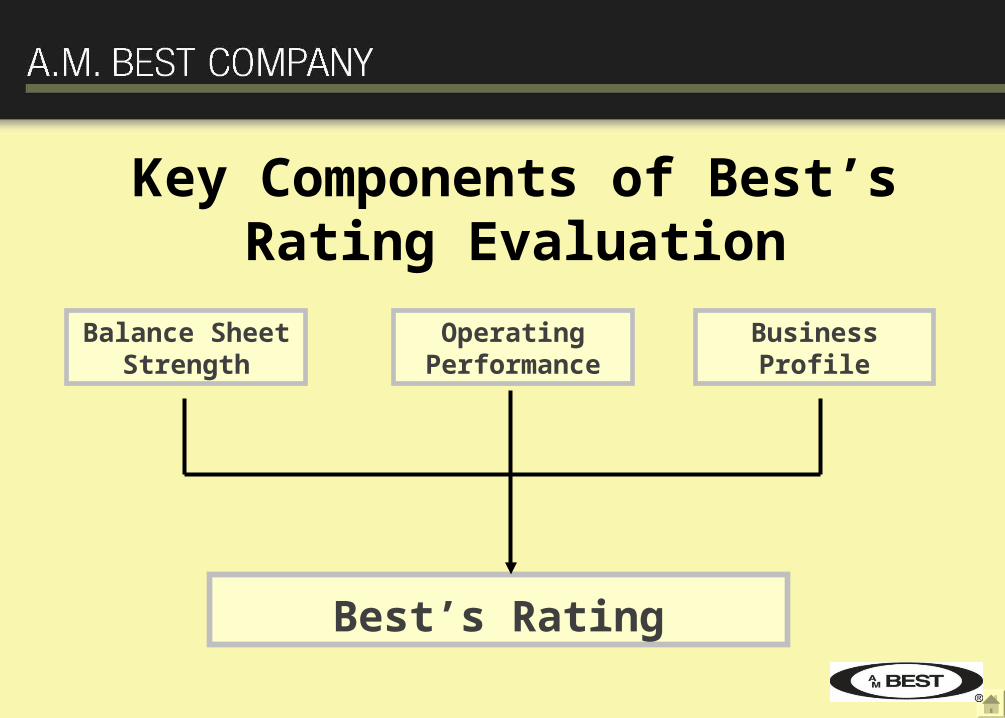

Key Components of the RatingBalance SheetOperating PerformanceBusiness Profile

Financial Strength Ratings/Issuer Credit Ratings

Objective of A.M. Best’s Financial Strength Ratings

To perform a constructive and

objective role in the insurance

industry toward the prevention and

detection of insurer insolvency

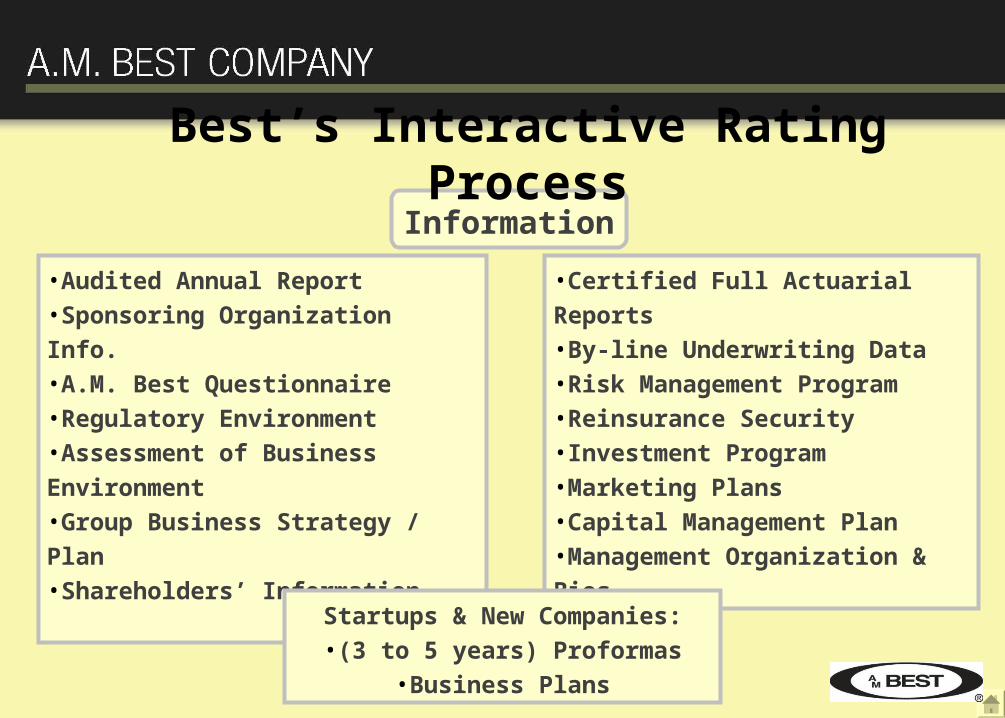

Best’s Interactive Rating Process

10-12 Week (P/C) Process (depending on the time of year)

Company Meeting

Quantitative and Qualitative Analyses(based on balance sheet strength, operating performance

& business profile)

General Structure of Agenda CEO Strategic Overview Organizational Structure Underwriting Claims & Loss Reserving Investments Enterprise Risk

Management

Corporate Governance Capital Structure Business Production Reinsurance Programs Financial Review

More Specific Information on Actual Agenda

•Certified Full Actuarial Reports•By-line Underwriting Data•Risk Management Program•Reinsurance Security•Investment Program•Marketing Plans•Capital Management Plan•Management Organization & Bios

•Audited Annual Report •Sponsoring Organization Info.•A.M. Best Questionnaire•Regulatory Environment•Assessment of Business Environment•Group Business Strategy / Plan•Shareholders’ Information

Information

Best’s Interactive Rating Process

Startups & New Companies:•(3 to 5 years) Proformas

•Business Plans

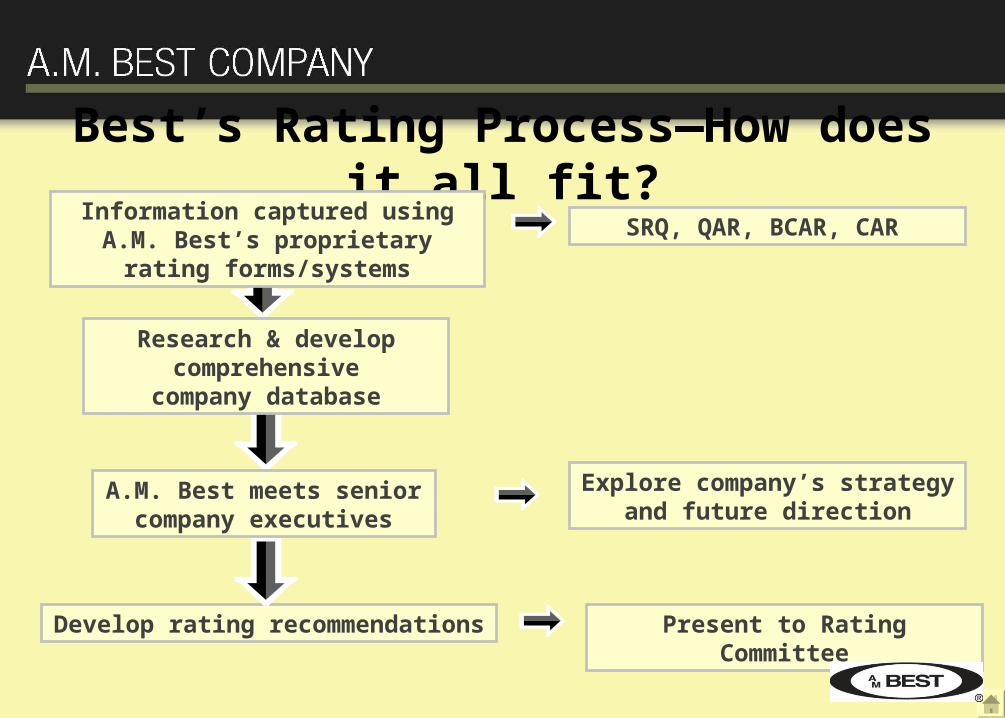

SRQ, QAR, BCAR, CAR

Develop rating recommendations

Explore company’s strategy and future direction

Best’s Rating Process—How does it all fit?

Information captured using A.M. Best’s proprietary rating

forms/systems

Research & develop comprehensive

company database

A.M. Best meets senior company executives

Present to Rating Committee

Rating Committee Process Rating committee presentation includes:

– Analyst review– Slides and other exhibits – Peer comparisons– Financial data (Consolidating financials)– Rating Tools SRQ, QAR, BCAR

Rating committee determines the rating Role of the AMB Analyst--primary relationship

manager Role of the AMB Team Leader---provides guidance

and support to Analyst

Rating Decision

Communicated to Company

Best’s Interactive Rating Process

President’s Letter

Public Reports Not Published or Released until company

has reviewed them for confidential or factual issues

Release of Best’s Ratings• Rating opinions formally evaluated every 12

months– Monitored continuously– Constant access to Analyst

• Ratings may be released throughout the year:– Upgrades– Downgrades– Affirmations– New assignments– Ratings placed under review

A.M. Best’s Rating Approach

Operating Company ICR

Insurance Affiliates

Holding Company

Non-InsuranceBusinesses

Top-Down

Bottom-Up

OperatingCompany

A.M. Best’s Rating Approach

Operating Company

ICR

Operating Company

FSR

Holding Company

ICR

Notching

Translation

Key Components of Best’s Rating Evaluation

Balance Sheet Strength

Operating Performance

BusinessProfile

Best’s Rating

Best’s Rating Evaluation Balance Sheet Strength

Capitalization/Leverage

Capital Structure/Holding Company

Quality/Soundness of Reinsurance

Adequacy of Loss Reserves

Quality/Diversification of Assets

Liquidity

ENTERPRISE RISK MANAGEMENT

Best Rating EvaluationOperating Performance

Profitability

Revenue Composition

Cycle ManagementAbility to Meet Plan

Sustainability

ENTERPRISE RISK MANAGEMENT

Best Rating EvaluationBusiness Profile

Competitive Advantages

Spread of Risk

Event Risk

Regulatory Risk

ENTERPRISE RISK MANAGEMENT

A.M. Best Rating Definitions

A.M. Best’s Issuer Credit Rating (ICR) is an opinion as to the ability of the issuer to meet its ongoing senior financial obligations.

A.M. Best’s Financial Strength Rating is an opinion as to an insurer’s ability to meet its ongoing obligations to policyholders.

A.M. Best’s Debt Rating is an opinion as to the issuer’s ability to meet its ongoing financial obligations to security holders when due.

Operating Insurance Co.

Financial Strength Rating (FSR)

ICR to Debt Notching / Holding Co.

FSR to Credit Market Scale / ICR

Guide To Best's Financial Strength Ratings

B, B- FairC++, C+ MarginalC, C- WeakD PoorE Under Regulatory SupervisionF In Liquidation

Vulnerable Ratings

Secure Ratings

A++, A+ SuperiorA, A- ExcellentB++, B+ Good

FSR and ICR Rating Translation

FSR ICR

Se

cure

Inve

stm

en

t G

rad

e

A++ aaaaa+

A+ aaaa-

A a+a

A- a-

B++ bbb+bbb

B+ bbb-

FSR ICR

Vu

lne

rab

le

No

n-I

nv

es

tme

nt

Gra

deB bb+

bb

B- bb-

C++ b+b

C+ b-

C ccc+ccc

C-ccc-cc

Key Rating ComponentsSecure

A++ B+Vulnerable

B D

Balance SheetStrength

OperatingPerformance

BusinessProfile

Outstanding

Very Stable/Strong

Strong market positionSustainable advantages

Well-diversified

Weak

Volatile/Poor

Questionable viabilityCompetitive disadvantages

Concentrated risk

A.M. Best has regularly produced impairment studies of its ratings

Impairment rates consistently increase with time & rating degradation:– A superior rated (A++ or A+) insurer has a

one-year impairment rate of about 0.06%– At the next lower rating level (A and A-),

this rate increases by nearly 3.5 times– Vulnerable category has a default rate of

more than 15 times that of a secured rating

Best’s Ratings Are Predictive

A.M. Best FSR Default StudyCumulative Average Default Rate By Year

Based on 1977-2005 Data

A rating of C/C- has a 21% probability of default within six years and

approximately 40% within 15 years.

INSURERSOLVENCYINSURER PERSPECTIVE PRESENTED BY

LYNN OLDFIELD

ROLE

MEMBERS

COVERAGES

LIMITS & DEDUCTIBLES

WHY INSURERS FAIL…

RAPID GROWTH

INSUFFIENT LOSS RESERVES

PRICE INADEQUACY

Source: Canadian Underwriter, “Why Insurers Fail”; D. Leadbetter et al., pg 38-41, June 2009

Data Deficiency and Poor

Information-Management

Practices

PRICING CHALLENGES

Pricing Challenges

in New Markets

Pricing Under Duress

Disruption of Link Between Pricing and Expected

Claims Costs

INSURANCE PRICING

Source: Canadian Underwriter, “Why Insurers Fail”; D. Leadbetter et al., pg 38-41, June 2009

CLIENT EXPOSURE

INSOLVENCY…

Short Rate RP

CancellationMid Term

New Policy Insurance

Cost

Runoff or Insolvent

Insurer Cover

PACICC Recovery Limited

Claims and IBNR

Source: Canadian Underwriter, “Why Insurers Fail”; D. Leadbetter et al., pg 38-41, June 2009

CO

VE

RA

GE

(in

mill

ion

s)

YEAR

$1

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

$110

$120

$130

1940 1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

CASE STUDY: COVERAGE TIMELINE 1940-2005

EACH COLOUR REPRESENTS AN INSURER49 INSURANCE COMPANIES IN 65 YEARS

Source: Excess Liability Exposure: A View from Above, Seminar Presentation, R. Goldstein et al., April 18, 2009

CO

VE

RA

GE

(in

mill

ion

s)

$1

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

$110

$120

$130

YEAR

1940 1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

CASE STUDY: COVERAGE TIMELINE 1940-2005

HOLES IN COVERAGE FROM INSOLVENCIES

Source: Excess Liability Exposure: A View from Above, Seminar Presentation, R. Goldstein et al., April 18, 2009

RISK MANAGER GUIDE TO INSURER REVIEW RATING

BROKERGUIDANCE

FACE

TIME

POLICY

SURPLUS

HOLDER

FINANCIAL

REVIEW

PEER

DISCUSSION

AGENCIES

CLAIMSHANDLING &RESERVING

INSURER CORE COMPETENCIES

RISK

APPETITEUNDERWRITI

NGCAPACITY

EMPLOYEES

COMMUNICATIONS

ACCESS TO

LEADERSHIP

Chartis is a world leading property-casualty and general insurance organization serving more than 40 million clients in over 160 countries and jurisdictions. With a 90-year history, one of the industry most extensive ranges of products and services, deep claims expertise and excellent financial strength, Chartis enables its commercial and personal insurance clients alike to manage virtually any risk with confidence.

Chartis is the marketing name for the worldwide property-casualty and general insurance operations of Chartis Inc. For additional information, please visit our website at www.chartisinsurance.com.

www.marsh.ca www.marsh.com

Insurer SolvencyBroker Perspective

September 14, 2009

Brian McAskillManaging DirectorMarsh Canada Limited

CONFERENCE

37

Event_CRIMS20090914_InsurerSolvencyPanel.ppt

Marsh

AgendaInsurer Solvency – Broker Perspective

Risk Management Concerns

Regulatory Environment

Broker Role

Insurer Transparency

38

Event_CRIMS20090914_InsurerSolvencyPanel.ppt

Marsh

Risk Manager ConcernsInsurer Solvency – Broker Perspective

How concerned are you currently about the level of risk associated with insurers?

Financial Institutions Communications, Media, Technology

Retail, Consumer Brands

Very Concerned 7% 15% 6%

Fairly Concerned 26% 17% 28%

What steps are you taking to manage the risks associated with your insurers?

ActionFinancial Institutions Communications,

Media, TechnologyRetail, Consumer Brands

Look at their rating 21% 7% 14%

Comparing Insurance Companies/Benchmarking

13% 17% 7%

39

Event_CRIMS20090914_InsurerSolvencyPanel.ppt

Marsh

Risk Manager Concerns (continued) Insurer Solvency – Broker Perspective

Key steps risk managers are taking to manage the level of risk with their insurers– Understand the insurer’s corporate legal organization structure

Branch or subsidiary – Meet with their insurers – Review insurer ratings and utilize broker expertise in interpreting

confusing and conflicting data– Spread their risk across more insurers– Buy Side A - Difference in Conditions (DIC) – drops down in event

of insurer insolvency– Benchmark insurers– Determine your minimum acceptable rating and have a

contingency plan in place if an insurer is downgraded below that level

– Negotiate prorated return premium - for credit rating changes

40

Event_CRIMS20090914_InsurerSolvencyPanel.ppt

Marsh

Risk Manager Concerns (continued) Insurer Solvency – Broker Perspective

What is affecting client perceptions and what drives actual change in relationships?

1. Concerns about solvency

2. Price and coverage enhancements or restrictions

3. Poor claims payment practice historically

4. Debt covenants that require a certain minimum rating (e.g. real estate industry)

5. Concentration of risk (client side) and position in coverage towers

6. “CNN Factor”

7. Fanning of the flames by competitors

8. Lack of direct personal connectivity

9. Increased claims frequency/severity caused change (insurer decision)

41

Event_CRIMS20090914_InsurerSolvencyPanel.ppt

Marsh

Risk Manager Concerns (continued) Insurer Solvency – Broker Perspective

Questions being asked include– “Will there be an insurer to pay my claims?”– “Have they changed their reserving practices?”– “Have they changed their claims philosophy?”– Incurred But Not Reported (IBNR) – “In case of insurer failure,

how is IBNR treated?” Those claims on file and reported prior to the declared insolvency are

admitted if proof of loss has been provided Pure IBNR – Normally courts provide a date for clients to replace

coverage and allow the ability to report losses to that date IBNR would be picked up in the new policy through the

claims-made provisions Otherwise, IBNR issues simply off the table and there is no recourse

after the court declared policy replacement date

42

Event_CRIMS20090914_InsurerSolvencyPanel.ppt

Marsh

Risk Manager Concerns (continued) Insurer Solvency – Broker Perspective

Also clients are– Assessing where insurers sit on certain layers– Challenging structures by line of coverage

As are some insurers – excess (XS) players following primaries

– Directors and officers (D&O) and long-tail business Increased interest and concern at board level Need for pro-active communication of accurate information by

risk managers

– Concerned about employee turnover at insurer, movement of underwriters, and succession planning, for example D&O underwriting teams have moved in the United States Canada has done a better job keeping personnel

– Canadian Underwriter, August 2009 article - Phoenix Rising

43

Event_CRIMS20090914_InsurerSolvencyPanel.ppt

Marsh

Regulatory EnvironmentInsurer Solvency – Broker Perspective

Office of the Superintendent of Financial Institutions (OSFI) and provincial regulators are responsible for regulation to

– Provide confidence in regulating the insurance companies– Supervise and regulate financial institutions– Determine the institution is in sound financial condition– Regular meetings with insurers to discuss results– Promptly advise the board of a financial institution of any concerns

they have– Work with financial institutions to correct

44

Event_CRIMS20090914_InsurerSolvencyPanel.ppt

Marsh

Regulatory Environment (continued) Insurer Solvency – Broker Perspective

During the recent economic and insurer crisis – OSFI was silent during insurer crisis period– OSFI Web site – standard summary financial data – but extremely limited

amount of information– Clients/brokers rely on public information – good in the U.S., but not much

financial information is available in Canada that is public or readily accessible

– Brokers/clients had to seek financial information and clarification from insurers

– Events took place in an untimely fashion and required financial analysts to interpret

Why this matters– To provide risk assessment and timely intervention help to safeguard the

policyholders– Allows brokers to act as a liaison and be proactive to ensure findings are

appropriately communicated to our clients– Presents objective information about insurer

45

Event_CRIMS20090914_InsurerSolvencyPanel.ppt

Marsh

Regulatory Environment (continued) Insurer Solvency – Broker Perspective

INSURANCE COMPANIES ACT

PART XV - REGULATION OF COMPANIES, SOCIETIES, FOREIGN COMPANIES AND PROVINCIAL COMPANIES — SUPERINTENDENT

Confidential information672. (1) Subject to section 673, all information regarding the business or affairs of a company,

society, foreign company or provincial company, or regarding a person dealing with any of them, that is obtained by the Superintendent, or by any person acting under the direction of the Superintendent, as a result of the administration or enforcement of any Act of Parliament, and all information prepared from that information, is confidential and shall be treated accordingly.

Disclosure by Superintendent673. (1) The Superintendent shall disclose, at such times and in such manner as the Minister may

determine, such information obtained by the Superintendent under this Act as the Minister considers ought to be disclosed for the purposes of the analysis of the financial condition of a company, society, foreign company or provincial company …

Disclosure by a company, etc.673.1 (1) A company, society, foreign company or provincial company shall make available to the public

such information concerning (a) the compensation of its executives, as that expression is defined by the regulations, and(b) its business and affairs for the purposes of the analysis of its financial condition,

in such form and manner and at such times as may be required by or pursuant to such regulations as the Governor in Council may make for the purpose.

[Source: Insurance Companies Act (1991, c. 47), Department of Justice Canada, Act current to August 12th, 2009]

46

Event_CRIMS20090914_InsurerSolvencyPanel.ppt

Marsh

Regulatory Environment (continued) Insurer Solvency – Broker Perspective

Opportunities

1. Provide more information in communications by identifying the actions they are taking, for example– Report more frequently as "Topic is under review" or "We have

reviewed the information as at such and such date or time“

2. Consider creating practices – externally, for example– If there is an "amber alert" policy internally, state that and create

appropriate communication plans to respond to these alert levels

3. Allow for increased transparency in the information that is publicly available

47

Event_CRIMS20090914_InsurerSolvencyPanel.ppt

Marsh

Broker RoleInsurer Solvency – Broker Perspective

Articulate what the risk management community is expressing and doing

Provide clients information about insurers

Monitor developments in the industry globally

Set minimum financial guidelines for insurers by country and monitor key financial indicators

Meet with insurers to understand local market issues

Facilitate collaborative client and underwriter meetings

48

Event_CRIMS20090914_InsurerSolvencyPanel.ppt

Marsh

Broker Role (continued)Insurer Solvency – Broker Perspective

Education and Advisory– To present facts, not state opinion other than client advice– Provide security presentations and produce reports on major insurers– Determine if insurer meets guidelines and discuss with clients– Discuss insurer financial strength… not their credit rating

Insurers under stress - Conduct market security group, one-to-one client meetings/calls as well as open client calls

Provide insurer security tools to allow clients to monitor their insurance program and changes in ratings including explanations for those changes

49

Event_CRIMS20090914_InsurerSolvencyPanel.ppt

Marsh

Insurer TransparencyInsurer Solvency – Broker Perspective

1. Provide enhanced transparency/disclosure of your financial performance– Make full P&C1 and P&C2’s available on request– How are you raising capital?– Why the change in capital?– What is the quality and detail of the investments?

2. Focus on the claims process – To provide consistency– Expedite settlements– Help brokers and our clients understand the development of your

claims reserving– Be prepared to discuss various reinsurance arrangements by placement

3. “Inadequate pricing of insurance is by far the most persuasive solvency risk factor” (Canadian Underwriter, June 2009)

50

Event_CRIMS20090914_InsurerSolvencyPanel.ppt

Marsh

Insurer Transparency (continued)Insurer Solvency – Broker Perspective

4. Do not write products simply to improve the bottom line without strong expertise—particularly for non-traditional risks Be in it for the long term as ultimately it affects the client when you

discontinue sources of coverage

5. Get the right message out – soon– Address the “street issues” and understand that it exists– Verify your position through other means– Consider an anonymous survey asking “How do we stack up?”– Let us know that you are active this way– Be conscious of each other and control how your teams comment on

other insurers as they generally do not know the facts and can impact your reputation and that of others

– Remember that industry solvency is an overall visual Intra-insurer competitive strategies around solvency are damaging

51

Event_CRIMS20090914_InsurerSolvencyPanel.ppt

Marsh

In Conclusion Insurer Solvency – Broker Perspective

Four things that we feel will support an insured's buying decision are– Information– Expertise– Transparency– Communication

52

Event_CRIMS20090914_InsurerSolvencyPanel.ppt

Marsh

DISCLAIMER

The information contained herein is based on sources we believe reliable, but we did not verify nor do we guarantee its accuracy. It should be understood to be general risk management and insurance information only. Marsh makes no representations or warranties, expressed or implied, concerning the financial condition, solvency, or application of policy wordings of insurers or reinsurers nor does Marsh make any representations or warranty that coverages may be placed on terms acceptable to you. The information contained in this presentation provides only a general overview of subjects covered, is not intended to be taken as advice regarding any individual situation, and should not be relied upon as such. Statements concerning tax and/or legal matters should be understood to be general observations based solely on our experience as risk consultants and insurance brokers and should not be relied upon as tax and/or legal advice, which we are not authorized to provide. Insureds should consult their own qualified insurance, tax and/or legal advisors regarding specific risk management and insurance coverage issues. Marsh assumes no responsibility for any loss or damage sustained in reliance of this presentation.

Marsh is part of the family of MMC companies, including Guy Carpenter, Mercer, the Oliver Wyman Group (including Lippincott and NERA Economic Consulting), and Kroll.

The materials, data and/or methodologies used in this presentation are proprietary to Marsh. This document or any portion of the information it contains may not be copied or reproduced in any form without the permission of Marsh Canada Limited, except that clients of any of the companies of MMC need not obtain such permission when using this report for their internal purposes, so long as this page is included with all such copies or reproductions.

Copyright 2009 Marsh Canada Limited. All rights reserved.

www.marsh.ca www.marsh.com

WelcomeWelcome

Presented by

Concurrent Session B3

Insurer Solvency

Monday, September 14, 2009

CONFERENCE

THANK YOU FOR ATTENDING THE

CONFERENCE

ENJOY THE REST OF YOUR CONFERENCE!

![Conduct of Business Supervisory Update · “But, my insurer is [UMA ABC]!!” THE EVIDENCE Solvency and liquidity challenges No TCF embedment plan No data from third parties No monitoring](https://static.fdocuments.in/doc/165x107/5f5b7094d9a1ee0118466180/conduct-of-business-supervisory-update-aoebut-my-insurer-is-uma-abca-the.jpg)