Insurance - Corporativo MAPFRE · Insurance 27 July 2017 Spain MAPFRE, S.A. ... Harish Gohil +44...

17

Insurance www.fitchratings.com 27 July 2017 Spain MAPFRE, S.A. And Its Main Operating Subsidiaries Full Rating Report Key Rating Drivers Resilient Underwriting Performance: In 2016, MAPFRE, S.A. demonstrated resilient underwriting performance despite difficulties in its core markets, including an economic slowdown in Brazil. The group reported a combined ratio of 97.4% in 2016 (2015: 98.6%). The improvement in the combined ratio reflects stronger underwriting discipline and cost-saving initiatives in MAPFRE’s core markets. Fitch Ratings expects MAPFRE’s technical profitability to remain strong and stable over the next 12-24 months. Robust Capital Adequacy: Fitch considers MAPFRE to be strongly capitalised, based on a ‘Strong’ score from the agency’s Prism factor-based model (FBM). The group’s regulatory Solvency II (SII) ratio also was strong at 210% at end-2016 (end-2015: 198%). Own funds backing the SII ratio largely consist of Unrestricted Tier 1 capital. However, the quality of capital is somewhat reduced by the goodwill of EUR2.0 billion in 2016 on MAPFRE’s balance sheet, which is equivalent to 22% of shareholders’ equity. Low Financial Debt Leverage: MAPFRE’s Fitch-calculated financial leverage was 15% in 2016 (2015: 13%). Fitch considers MAPFRE’s financial leverage ratio as low (the median guideline for the ‘A’ rating category is 28%) and a positive rating factor. Strong International Franchise: MAPFRE has a strong market position in Spain, where it is the leader in the non-life segment, and in Latin America, particularly Brazil. MAPFRE’s share of Spanish non-life insurance was 14.6%, life 6.3% and Latin American non-life 7.6% in 2016. This makes it the 11th-largest European and the third-largest Latin American insurance group. Sovereign Constraint: MAPFRE’s exposure to sovereign debt (Spanish sovereign debt to equity was 148% at end-2016), used to match domestic liabilities in Spain, is reflected in the sovereign constraint on MAPFRE’s ratings at ‘A−’, one notch higher than the sovereign rating of Spain (BBB+/Positive). MAPFRE is substantially exposed to the Spanish economy as around 60% of its operating profits originate from Spain. However, Fitch believes that MAPFRE’s capital is resilient enough against potential stress from substantial exposure to sovereign debt. Strong Liquidity Position: Fitch expects MAPFRE’s balance sheet to remain liquid and able to support its policyholder liabilities. In 2016, the investment portfolio was composed of highly liquid assets, which support the rating. Conservative Investment Portfolio: In 2016, MAPFRE’s ratio of risky assets to equity as calculated by Fitch was low at 42% (2015: 41%), which supports the rating. However, of MAPFRE’s fixed income and cash investments, 56% are allocated to ‘BBB’ rated instruments. Rating Sensitivities Sovereign Upgrade: The ratings could be upgraded if Spain’s sovereign rating is upgraded, providing that MAPFRE maintains strong earnings and capitalisation. Capital Deterioration: As the Outlook is Positive, Fitch does not anticipate developments with a high likelihood of triggering a downgrade. However, MAPFRE’s ratings could be downgraded on significant losses with a material impact on the group’s capitalisation. Ratings Insurer Financial Strength Ratings MAPFRE ESPANA Compania de Seguros y Reaseguros, S.A. A− MAPFRE Global Risks, S.A. A− MAPFRE Vida SA De Seguros y Reaseguros A− MAPFRE RE, Compania De Reaseguros, S.A. A− MAPFRE, S.A. Long-Term Foreign-Currency IDR A− Senior Unsecured BBB+ Subordinated BBB− Sovereign Risk Long-Term IDR BBB+ Outlooks Insurer Financial Strength Ratings Positive Long-Term Foreign-Currency IDR Positive Sovereign Long-Term IDR Positive Financial Data MAPFRE, S.A. (Consolidated) (EURm) 2016 2015 Gross written premiums 22,813 22,312 Non-life combined ratio (%) 97.4 98.6 Net result 776 709 Total assets 67,882 63,489 Total equity 11,443 10,408 As reported by company Related Research 2017 Outlook: Brazilian Insurance (December 2016) Brazilian Insurance Dashboard (Second-Half 2016) (March 2017) Spain – June 2017 Global Economic Outlook Forecast Analysts Ekaterina Ishchenko +44 20 3530 1532 [email protected] Harish Gohil +44 20 3530 1257 [email protected]

Transcript of Insurance - Corporativo MAPFRE · Insurance 27 July 2017 Spain MAPFRE, S.A. ... Harish Gohil +44...

Insurance

www.fitchratings.com 27 July 2017

Spain

MAPFRE, S.A. And Its Main Operating Subsidiaries

Full Rating Report

Key Rating Drivers

Resilient Underwriting Performance: In 2016, MAPFRE, S.A. demonstrated resilient

underwriting performance despite difficulties in its core markets, including an economic

slowdown in Brazil. The group reported a combined ratio of 97.4% in 2016 (2015: 98.6%). The

improvement in the combined ratio reflects stronger underwriting discipline and cost-saving

initiatives in MAPFRE’s core markets. Fitch Ratings expects MAPFRE’s technical profitability to

remain strong and stable over the next 12-24 months.

Robust Capital Adequacy: Fitch considers MAPFRE to be strongly capitalised, based on a

‘Strong’ score from the agency’s Prism factor-based model (FBM). The group’s regulatory

Solvency II (SII) ratio also was strong at 210% at end-2016 (end-2015: 198%). Own funds

backing the SII ratio largely consist of Unrestricted Tier 1 capital. However, the quality of capital

is somewhat reduced by the goodwill of EUR2.0 billion in 2016 on MAPFRE’s balance sheet,

which is equivalent to 22% of shareholders’ equity.

Low Financial Debt Leverage: MAPFRE’s Fitch-calculated financial leverage was 15% in

2016 (2015: 13%). Fitch considers MAPFRE’s financial leverage ratio as low (the median

guideline for the ‘A’ rating category is 28%) and a positive rating factor.

Strong International Franchise: MAPFRE has a strong market position in Spain, where it is

the leader in the non-life segment, and in Latin America, particularly Brazil. MAPFRE’s share of

Spanish non-life insurance was 14.6%, life 6.3% and Latin American non-life 7.6% in 2016.

This makes it the 11th-largest European and the third-largest Latin American insurance group.

Sovereign Constraint: MAPFRE’s exposure to sovereign debt (Spanish sovereign debt to

equity was 148% at end-2016), used to match domestic liabilities in Spain, is reflected in the

sovereign constraint on MAPFRE’s ratings at ‘A−’, one notch higher than the sovereign rating of

Spain (BBB+/Positive). MAPFRE is substantially exposed to the Spanish economy as around

60% of its operating profits originate from Spain. However, Fitch believes that MAPFRE’s

capital is resilient enough against potential stress from substantial exposure to sovereign debt.

Strong Liquidity Position: Fitch expects MAPFRE’s balance sheet to remain liquid and able

to support its policyholder liabilities. In 2016, the investment portfolio was composed of highly

liquid assets, which support the rating.

Conservative Investment Portfolio: In 2016, MAPFRE’s ratio of risky assets to equity as

calculated by Fitch was low at 42% (2015: 41%), which supports the rating. However, of

MAPFRE’s fixed income and cash investments, 56% are allocated to ‘BBB’ rated instruments.

Rating Sensitivities

Sovereign Upgrade: The ratings could be upgraded if Spain’s sovereign rating is upgraded,

providing that MAPFRE maintains strong earnings and capitalisation.

Capital Deterioration: As the Outlook is Positive, Fitch does not anticipate developments with

a high likelihood of triggering a downgrade. However, MAPFRE’s ratings could be downgraded

on significant losses with a material impact on the group’s capitalisation.

Ratings

Insurer Financial Strength Ratings

MAPFRE ESPANA Compania de Seguros y Reaseguros, S.A.

A−

MAPFRE Global Risks, S.A. A− MAPFRE Vida SA De Seguros y Reaseguros

A−

MAPFRE RE, Compania De Reaseguros, S.A.

A−

MAPFRE, S.A. Long-Term Foreign-Currency IDR A− Senior Unsecured BBB+ Subordinated BBB−

Sovereign Risk Long-Term IDR BBB+

Outlooks

Insurer Financial Strength Ratings Positive Long-Term Foreign-Currency IDR Positive Sovereign Long-Term IDR Positive

Financial Data

MAPFRE, S.A. (Consolidated)

(EURm) 2016 2015

Gross written premiums 22,813 22,312 Non-life combined ratio (%)

97.4 98.6

Net result 776 709 Total assets 67,882 63,489 Total equity 11,443 10,408 As reported by company

Related Research

2017 Outlook: Brazilian Insurance (December 2016)

Brazilian Insurance Dashboard (Second-Half 2016) (March 2017)

Spain – June 2017 Global Economic Outlook Forecast

Analysts

Ekaterina Ishchenko +44 20 3530 1532 [email protected] Harish Gohil +44 20 3530 1257 [email protected]

Insurance

MAPFRE, S.A.

July 2017 2

Business Profile

Large Diversified Composite Insurer Strong international franchise

Well diversified by products, sectors and distribution channels

Acquisitions support international growth strategy

Ratings Range Based on Business Profile IFS rating category AAA AA A BBB <BBB

Very strong business profile Strong business profile Moderate business profile Weak business profile

Source: Fitch

Strong International Franchise

With EUR22.8 billion of gross written premiums (GWP) in 2016, MAPFRE has a strong

franchise in Spain and Latin America. It is the market leader in Spain, with 10.5% market share,

and has a strong presence in Latin America. In non-life and life insurance in Spain, MAPFRE’s

market shares are 14.6% and 6.3%, respectively, and 7.6% in Latin American non-life. This

makes MAPFRE the 11th-largest European insurer and the third-largest insurer in Latin

America. Both Spain and Latin America are core regions for MAPFRE and a profitable source

of growth.

Well Diversified by Products, Sectors and Distribution Channels

MAPFRE underwrites life (including savings) and non-life business, which accounted for 22%

and 78% of GWP, respectively, in 2016. Most of its business is primary insurance, but

MAPFRE acts as a reinsurer through MAPFRE Re Compania De Reaseguros S.A (MAPFRE

RE), which accounts for 17% of total GWP.

MAPFRE has multichannel distribution comprising its own branch network, agents, brokers and

bancassurance agreements, and a wide geographical presence within Spain and Latin America.

Non-life business is predominantly distributed via agents. Life business is distributed through

agents and bancassurance partnerships (such as Bankia, Bankinter and Banco do Brasil).

27.8%

20.0%

15.6%8.5%

11.6%

8.3%7.7%

0.5%

28.7%

18.5%17.1%

7.7%

11.7%

10.4%

5.4% 0.5%

Iberia Brazil MAPFRE RELatam South North America EMEALatam North APAC

Source: MAPFRE SA

Premium Income by GeographyOuter ring: 2016Inner ring: 2015

57.9%

63.1%

18.0%

15.6%

17.9%

20.1%

5.8%

1.6%

-3.8%

8.7%

5.0%

4.2%

-0.3%

-11.1%

-0.4%

-2.2%

-20% 0% 20% 40% 60% 80% 100%

2015

2016

Iberia Brazil Mapfre Re

Latam South N.America Latam North

EMEA APAC

Source: MAPFRE SA

Contribution to Consolidated Results

Source: Mapfre 2016 results presentation

Premium Split by Line of Business2016

General P&C insurance

31%

Health & accidents

5%

Mapfre Re17%

Motor 29%

Life18%

Related Criteria

Insurance Rating Methodology (April 2017)

Insurance

MAPFRE, S.A.

July 2017 3

Acquisitions Support International Growth Strategy

Outside of Iberia and Latin America, MAPFRE’s international insurance operations comprise

subsidiaries in North America, EMEA and Asia Pacific. Most of these operations were acquired

by MAPFRE to strengthen its presence in these regions.

MAPFRE International Acquisitions

Year Company Country

2007 Genel Sigorta Turkey 2008 The Commerce Group USA 2011 Middlesea Insurance Plc Malta 2015 Direct Line Insurance S.p.A. Italy 2015 Direct line Versicherung Aktiengesellschaft Germany 2016 - 2017 PT Asuransi Bina Dana Arta Tbk (ABDA) Indonesia

Source: MAPFRE

In 2015, MAPFRE completed the acquisition of Direct Line in Italy and Germany, both well-

established and growing operations. Direct Line is a leading company in the Italian direct motor

insurance market and the third largest in Germany’s direct motor market. Fitch believes these

acquisitions will allow MAPFRE to strengthen its position in Europe and improve its global

diversification in line with its profitable growth strategy.

In June 2017, MAPFRE obtained the regulatory authorisation to complete the acquisition of a

further 31% of share capital of the Indonesian insurance company PT Asuransi Bina Dana Arta

Tbk (ABDA) for EUR92 million, which was announced in October 2016. MAPFRE will hold a

major interest in the company with 51% of capital and have management control. Through this

acquisition, MAPFRE will complete its entry into the Indonesian insurance market, which began

in October 2013, when it bought 20% of ABDA. ABDA is ranked fifth in the country’s motor

insurance market, with a share of 6.4%.

Insurance

MAPFRE, S.A.

July 2017 4

Ownership is Neutral to Rating

MAPFRE S.A., the top holding company of the MAPFRE group, is listed on the Madrid and

Barcelona stock exchanges. The group operates in 45 countries through 232 subsidiaries.

MAPFRE is a subsidiary of Cartera MAPFRE S.L. Sociedad Unipersonal, which is 100%

controlled by Fundacion MAPFRE (FM). At the end of 2016, FM held 67.73%, directly and

indirectly, of MAPFRE’s capital. The rest is a free float held by local and foreign shareholders.

FM is a non-profit institution created by MAPFRE in 1975, the main purpose of which is to

promote the well-being of society and citizens across the company footprint. FM works to drive

economic, social and cultural improvements for society’s most disadvantaged people and

groups. Its operations focus on five areas: Accident prevention and road safety, insurance and

social protection, culture, social action, and health promotion.

Organisational Chart 2016

Source: Mapfre SA 2016 annual report

Mapfre SA

International ReinsuranceIberia Latam

North AmericaSpain/Portugal Brazil

EMEALatam North

Latam South APAC

- General Counsel

- Internal Audit

- Business Support

- Strategy and M&A

- Finance

- Investment

- Human Resources

- Resources & Institutional coordination

- Business, Clients and Innovation

Corporate Governance and

Management

Corporate governance and

management are adequate and neutral

for the rating.

MAPFRE’s board consists of 15

members, of whom five are external

directors representing Cartera

MAPFRE. Other directors include four

executive members and six

independent directors.

Insurance

MAPFRE, S.A.

July 2017 5

Industry Profile and Operating Environment

Strong Recovery in the Spanish Insurance Market

The strong recovery of the Spanish economy continued in 4Q16 as GDP grew by 0.7% qoq,

which was the same rate as in 3Q16 and only marginally below the 0.8% in the previous three

quarters. Annual GDP growth was 3.2% in 2016, the same as in 2015. Private consumption

continues to be the main driver, supported by earlier income tax cuts, improving credit

conditions, and a 2.4pp fall in the unemployment rate last year. In light of the resilience of the

recovery, we have revised our GDP forecasts to 2.6% for 2017 and 2.1% for 2018.

Supported by a stronger economy, the Spanish insurance sector continued its recovery and

recorded 12% yoy total premium growth in 2016 (2015: 2.1%). The non-life insurance sector

expanded by 4.5% (2015: 2.4%) with all lines contributing to premium growth. Motor, health

and multi-risk home insurance segments saw an increase in premiums of 5.1%, 5.1%, and

3.1%, respectively. Life insurance and savings products also saw a strong recovery in 2016,

with assets under management increasing by 5.7%.

Sector profitability remained resilient in 2016 and throughout the difficult economic conditions

during the eurozone crisis. Non-life insurance technical profitability in 2016 was strong with a

combined ratio of 93.6% as of December 2016 (2015: 94.7%).

The insurance market in Spain is well developed with a large number of domestic and foreign

companies that offer a comprehensive range of products. The top 10 companies represent

65% of market premiums. The insurance penetration rate is lower than in other developed

economies (5.7% in 2016), offering potentially significant growth opportunities.

Brazilian Insurance: Sector Resilient to Slower Growth

Fitch’s outlook for the Brazilian insurance sector remains stable. The insurance sector is one of

the few that has withstood the significant deterioration in the operating environment in 2015

and 2016. Fitch believes that the Brazilian insurance sector will continue to be resilient and

maintain overall adequate key credit metrics in 2017. In 2016, the growth of insurance

premiums declined, but sector profitability and other key credit metrics have all held up well.

Downward pressure on premium growth could ease somewhat in line with economic

stabilisation, but Fitch does not foresee a significant recovery and forecasts growth to be close

to inflation. This is because GDP growth is likely to be modest.

Fitch expects sector profitability to remain solid in 2017, despite a likely decline in interest rates,

which would exert downward pressure on investment income, and expectations that premium

growth will remain modest. Similar to previous years, sector performance should be supported

by adequate technical results and still meaningful investment income. The latter is positively

correlated with interest rates. This acts as a natural hedge for the sector, as interest rates, and

hence investment income, tend to rise when premium growth slows, partly offsetting the

reduction in the revenue base, and vice versa.

Ratings Range Based on Industry Profile/Operating Environment

IFS rating AAA AA A BBB <BBB

Life insurance

Non-life insurance Reinsurance lines

Source: Fitch

Top 10 Spanish Insurers

2016 Market

share (%)

VidaCaixa 14.9 MAPFRE 10.5 Zurich 8.7 Grupo Mutua Madrileña 7.4 Allianz 5.6 Grupo Catalana Occidente 4.6 Grupo Axa 4.0 Generali 3.9 BBVA Seguros 3.0 Grupo Caser 2.3 % of total GWP 64.9

Source: ICEA, Fitch

Motor32.3%

Health23.6%

Other16.8%

Source: ICEA

Direct Non-life Premiums in Spain2016

Multirisk20.7%

Funeral expenses

6.6%

Sovereign and Country-Related

Constraints

Fitch rates Spain’s Long-Term IDR

‘BBB+’ with a Positive Outlook; the

Country Ceiling is ‘AA+’. The sovereign

rating expresses the maximum limit for

the ratings of most, but not all, issuers in

a given country. At current levels, the

ratings of Spanish insurance

organisations and other corporate issuers

could be constrained by sovereign or

macroeconomic risks.

Due to the sovereign-related constraint of

'A−' applied to MAPFRE's ratings, the

operating entities' IFS ratings and implied

IDRs are at the same level.

Insurance

MAPFRE, S.A.

July 2017 6

Peer Analysis

Smaller But Compares Well with Peers

MAPFRE’s closest peers are the largest European composite insurance groups and some

financial conglomerates with significant insurance operations.

Overall, MAPFRE compares well with peers. In 2016, MAPFRE’s return on equity was in line

with the peer group average and its combined ratio was slightly higher than the average of the

group. MAPFRE’s five-year average reported combined ratio is 96.7% and it continues to target

sub-96%. MAPFRE’s financial leverage is also the lowest of the peer group. However,

MAPFRE is smaller and consequently less diversified than peers. Its high exposure to lower-

rated sovereigns, similar to Generali, acts as a drag on the group’s ratings.

Peer Comparison - 2016

EURm IFS Rating/ Outlook

a Total equity

Return on equity

b (%)

Gross written premium

Total assets

Return on assets

c (%)

Net income

d

Solvency II /SST

ratioe (%)

Reported combined

ratio (%)

Financial leverage

(%)

AXA AA−/Stable 75,880 8.4 94,933 892,783 0.7 5,829 197 96.5 25 Allianz AA/Stable 70,392 10.5 76,331 883,809 0.8 6,883 218 94.3 21 Generali A−/Stable 25,668 8.7 70,513 521,184 0.4 2,081 177 92.5 33 Zurich AA−/Stable 30,054 10.4 41,673 334,882 0.9 3,041 227 98.4 23 MAPFRE A−/Positive 11,444 8.8 22,813 67,882 1.3 776 210 97.4 15

Foreign exchange rates used: Average: USD1 = EUR0.947; Period end: USD1 = EUR0.90359

a Current IFS Ratings of primary operating companies of each group

b Group net income/2015,2016 shareholders' equity

c Group net income/2015,2016 average total assets less reinsurance share of technical provisions

d Net income excludes minorities

e For Zurich Swiss Solvency Test as of 1 January 2017

Source: Companies’ accounts, Fitch

Insurance

MAPFRE, S.A.

July 2017 7

Robust Solvency Position

Strong capital

Low financial leverage

Strong Capital

Fitch believes MAPFRE is strongly capitalised as reflected in the ‘Strong’ Prism FBM score.

The group’s regulatory solvency position is also strong, as reflected in the 210% reported

Solvency II ratio at end-2016 (end-2015: 198%) under the standard formula calculation

approach. The group uses transitional measures for technical provisions and the matching

adjustment. Without the transitional measures for technical provisions and the matching

adjustment the solvency ratio would be 193.4% and 206.6%, respectively. Own funds backing

the Solvency II ratio largely consist of Unrestricted Tier 1 capital (94%).

In 2016, shareholders’ funds (excluding minorities) increased by 6% to EUR9,127 million (end-

2015: EUR8,574 million). This was largely due to an increase in retained earnings and

appreciation of the main currencies. Fitch views MAPFRE’s capital position as strong and

supportive of its current ratings. However, the quality of capital is somewhat reduced by the

goodwill of EUR2.0 billion in 2016 on the balance sheet.

Low Financial Leverage

MAPFRE’s Fitch-calculated financial leverage was 15% in 2016 (2015: 13%). The 2pp increase

in the Fitch-calculated financial leverage ratio was due to the increase in the total financial debt

to EUR2.1 billion (2015: EUR1.6 billion) as MAPFRE issued a 10-year EUR1,000 million senior

bond in May 2016 to replace a EUR1,000 million senior bond that was redeemed in 2015.

Fitch considers MAPFRE’s financial leverage ratio as low (the median guideline for the ‘A’

rating category is 28%) and a positive rating factor.

In March 2017, MAPFRE issued a 30-year EUR600 million callable subordinated bond with a

fixed coupon of 4.375% for the first 10 years. The issuance is a Solvency II Tier 2 instrument

and is given 100% equity credit in Fitch’s Prism FBM model and considered as 100% debt in

the agency’s financial leverage calculations. Fitch does not anticipate any significant impact on

MAPFRE’s financial leverage ratio from this issuance given that MAPFRE called its existing

EUR700 million subordinated bond on 24 July 2017.

Capitalisation and Leverage

2012 2013 2014 2015 2016 Fitch’s expectation

Total equity (including minorities) (EURm) 10,136 9,894 11,469 10,408 11,444 Fitch expects MAPFRE to maintain strong levels of capital adequacy. Regulatory Solvency I ratio (%) 261 246 259 255 n.a.

Regulatory Solvency II ratio (%) n.a. n.a. n.a. 198 210

Total financing and commitments (TFC) (x) 0.2 0.2 0.2 0.2 0.3

Financial leverage (%) 15 14 12 13 15

Net premiums written (non-life) to equity (x) 1.3 1.4 1.2 1.3 1.3

Source: Fitch calculations, company accounts

Insurance

MAPFRE, S.A.

July 2017 8

Strong Fixed-Charge Coverage

MAPFRE’s debt-servicing capabilities were robust at 20x in 2016 (2015: 14x). In 2016,

MAPFRE refinanced its senior debt, substantially reducing the finance costs (there was a

coupon of 5.125% on the previous three-year senior bond versus a 1.625% coupon on the new

10-year senior bond). The subordinated bond issued by MAPFRE in March 2017 that replaces

the subordinated bond MAPFRE called on 24 July 2017, also carries a lower coupon rate.

Good Financial Flexibility

Fitch considers MAPFRE’s financial flexibility as good with proven access to capital markets as

evidenced by the two recent bond issues.

Debt Service Capabilities and Financial Flexibility

(EURm) 2012 2013 2014 2015 2016 Fitch’s expectation

Fixed-charge coverage ratio excluding gains and losses (x) 15 14 13 14 24 Fitch expects MAPFRE’s fixed-charge coverage ratio to remain at current strong levels.

Fixed-charge coverage ratio including gains and losses (x) 18 16 18 18 34

Financial debt interest payments 78 101 99 84 52

Source: Fitch calculations, company accounts

Holding Company Liquidity/

Bank Facilities

In 2016 MAPFRE extended the maturity

of its syndicated loan facility of EUR1bn

from December 2020 to December

2021. At 31 December 2016, EUR480m

was drawn down under the credit facility

(2015: EUR1bn).

Insurance

MAPFRE, S.A.

July 2017 9

Strong Underwriting Profitability Maintained

Resilient non-life underwriting performance

Premium growth in life insurance

Growth and net income exposed to currency movements

Resilient Non-Life Underwriting Performance

In 2016, MAPFRE’s underwriting performance remained resilient despite difficulties in some of

its core markets, including an economic downturn in Brazil. The group reported a combined

ratio of 97.4% in 2016 (2015: 98.6%). The improvement in the combined ratio reflects improved

underwriting discipline and cost-saving initiatives in MAPFRE's core markets. MAPFRE’s target

combined ratio is unchanged at 96% or less.

MAPFRE’s three largest regional segments – Iberia, Brazil and the US – performed well in

2016. In Spain, all main business classes contributed to premium growth and to the technical

result. The 3pp decrease in the combined ratio in Iberia in 2016 was due to improvements in

both loss and expense ratios due to enhancements in claims handling, risk selection and

stricter cost control. In Brazil, higher claims costs resulting from the difficult economic

environment were offset by lower expenses, resulting in an overall improvement in the

combined ratio. MAPFRE USA underwriting result improved in 2016, given the absence of

large weather losses.

Premium Growth in Life Insurance

In 2016, total life insurance GWP increased by 5% to EUR5,113 million from EUR4,870 million

in 2015. The increase in premiums was driven by strong performance in Spain, which saw

premium growth of 18% due to strong sales through the agents’ network and higher demand in

corporate savings policies. In Brazil, life premiums fell by 7% as a result of lower lending

activity by Banco do Brazil, MAPFRE’s strategic partner. Despite the difficult operating

environment, however, Brazil remains the largest contributor to the overall life business result,

followed by Spain.

94101 101

94107

100

119

94 9797 97 98 95103 108 104

94 99

0

20

40

60

80

100

120

140

Iberia Latam north Latamsouth

Brazil EMEA NorthAmerica

APAC Mapfre Re Mapfre SA

(%)

Combined Ratio by Geography2015 - 2016

2016 2015

Source: MAPFRE 2016 Annual Report

Financial Performance and Earnings

(%) 2012 2013 2014 2015 2016 Fitch’s expectation

Net income (EURm) 666 790 845 709 776 Fitch expects MAPFRE to continue to deliver profitable underwriting returns, with a combined ratio below 100%.

Combined ratio (non-life, net earned premium basis) 95.4 96.1 95.8 98.6 97.4

Loss ratio (non-life) 67.4 67.0 68.0 70.0 69.9

Net income return on assets (group) 1.3 1.4 1.4 1.2 1.3

Net income return on equity 9 10 10 8 9

Source: Fitch calculations, company accounts

Insurance

MAPFRE, S.A.

July 2017 10

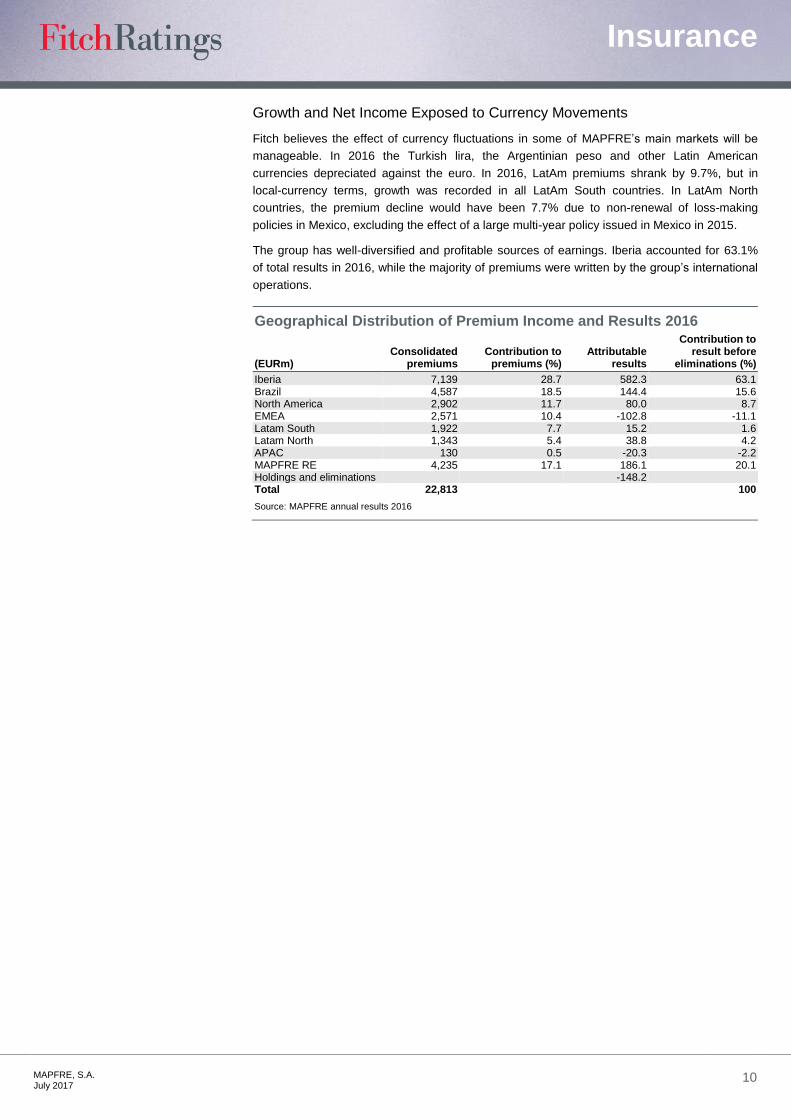

Growth and Net Income Exposed to Currency Movements

Fitch believes the effect of currency fluctuations in some of MAPFRE’s main markets will be

manageable. In 2016 the Turkish lira, the Argentinian peso and other Latin American

currencies depreciated against the euro. In 2016, LatAm premiums shrank by 9.7%, but in

local-currency terms, growth was recorded in all LatAm South countries. In LatAm North

countries, the premium decline would have been 7.7% due to non-renewal of loss-making

policies in Mexico, excluding the effect of a large multi-year policy issued in Mexico in 2015.

The group has well-diversified and profitable sources of earnings. Iberia accounted for 63.1%

of total results in 2016, while the majority of premiums were written by the group’s international

operations.

Geographical Distribution of Premium Income and Results 2016

(EURm) Consolidated

premiums Contribution to

premiums (%) Attributable

results

Contribution to result before

eliminations (%)

Iberia 7,139 28.7 582.3 63.1 Brazil 4,587 18.5 144.4 15.6 North America 2,902 11.7 80.0 8.7 EMEA 2,571 10.4 -102.8 -11.1 Latam South 1,922 7.7 15.2 1.6 Latam North 1,343 5.4 38.8 4.2 APAC 130 0.5 -20.3 -2.2 MAPFRE RE 4,235 17.1 186.1 20.1 Holdings and eliminations -148.2 Total 22,813 100

Source: MAPFRE annual results 2016

Insurance

MAPFRE, S.A.

July 2017 11

Prudent Investments but High Concentrations High exposure to Spanish debt

Low-risk asset allocation

High Exposure to Spanish Debt

Fitch assesses MAPFRE’s overall investment portfolio as well balanced and prudent, with over

95% of total investments in fixed income and cash allocated to investment-grade instruments.

However, fixed-income assets have a high degree of concentration in Spanish sovereign debt,

which accounted for 60% of total government bonds at end-2016. Of MAPFRE’s fixed income

and cash investments, 56% are allocated to ‘BBB’-rated instruments.

Breakdown of Fixed-Income Portfolio by Issuer (End-2016)

Government (%) 57 Corporate (%) 20 Of which Of which Spain (%) 60 Spain (%) 24 Rest of Europe (%) 13 Rest of Europe (%) 41 Brazil (%) 13 Brazil (%) 0 Rest of Latin America (%) 7 Rest of Latin America (%) 6 United States (%) 5 United States (%) 24 Others (%) 2 Others (%) 5

Source: MAPFRE 2016 results presentation

Low-Risk Asset Allocation

According to Fitch’s calculations, exposure to equities was only 15% of total equity at end-2016

(end-2015: 14%), which we consider prudently low. The ratio of risky assets to shareholders’

equity was 42% at end-2016, which Fitch also considers strong and supportive of the ratings.

Investment and Asset Risk

(%) 2012 2013 2014 2015 2016 Fitch’s expectation

Unaffiliated shares to equitya 18 22 21 26 28 Fitch does not expect any significant

changes in MAPFRE’s asset mix. Below-investment-grade bonds to equity 15 12 16 13 12

Investments in affiliates to equity 1 2 2 2 2

Risky assets to equity b 34 36 39 41 42

a Ratio includes equities and mutual funds

b Ratio includes equities, mutual funds and non-investment-grade bonds

Source: Fitch calculations, company accounts

Cash2.9%

Other8.4%

Source: MAPFRE 2016 annual results presentation

Investment Portfolio Split2016

Government bonds57.2%

Corporate bonds20.2%

Property4.6%

Mutual funds3.3%

Equities3.4%

6.0%11.9%

13.8%

63.8%

3.8%

0.7%

8.0%

17.8%

13.3%56.3%

3.6%1.0%

AAA AA A BBB BB NR

Source: Fitch, MAPFRE annual reportsAssumed a mapping of MAPFRE's reported credit ratings to Fitch's rating scale

Fixed Income & Cash Investments Credit QualityOuter ring: 2016Inner ring: 2015

Insurance

MAPFRE, S.A.

July 2017 12

Liquid Investment Portfolio

Strong liquidity position

Currency risk exposure manageable

Interest-rate risk manageable

Strong Liquidity Position

Fitch considers MAPFRE’s balance sheet as liquid and able to support its policyholder liabilities.

The agency also considers the investment portfolio liquid and supportive of the rating with over

95% of its fixed-income and cash portfolio allocated to investment-grade, fixed-income

instruments. Fitch believes these are likely to be readily tradable.

Currency Risk Exposure Manageable

MAPFRE has some exposure to currency volatility. Its principal foreign-currency risk arises

because its functional currency is the euro, whereas the currencies of a large part of its

operations include the Brazilian real and US dollar.

Reported premiums and earnings are exposed to exchange rates but capital and shareholders’

equity are also exposed. In 2016, EUR924 million of negative foreign exchange differences

under the company’s shareholders’ funds were recognised at year end, compared to EUR1,142

million in 2015.

MAPFRE closely matches its assets and liabilities by currency exposure, which, in Fitch’s

opinion, keeps the risk relating to changes in exchange rates manageable. Although currency

mismatch risk is minimised in its operations, the group has translation risks because of its

reporting currency.

Interest-Rate Risk Manageable

MAPFRE manages its exposure to interest-rate risk through close matching of the assets and

liabilities exposed to interest-rate fluctuations. At group level, asset and liability durations have

little mismatch, with a duration gap of less than one year, protecting the company against

fluctuations in interest rates.

Asset/Liability and Liquidity Management

(%) 2012 2013 2014 2015 2016

Fitch’s expectation

Liquid assets to policyholder liabilities (life and non-life combined)

100 100 100 100 102 MAPFRE has a liquid balance sheet, which Fitch expects to be maintained.

Source: Fitch, company accounts

Insurance

MAPFRE, S.A.

July 2017 13

Adequate Reserve Adequacy

Favourable claims run-off development

Favourable Claims Run-Off Development

Fitch’s analysis of MAPFRE’s reported claims development triangles suggests that the

development of prior-year reserves has largely been favourable in the past decade. The Fitch-

calculated reserves ratio (net technical reserves to net earned premiums) was 103% at end-

2016. Fitch views this level as adequate. We believe the ratio adequately reflects the group’s

high claims settlement speed and the short-tail nature of its non-life business. A vast majority of

the outstanding provision is released one year after the event.

Reserve Adequacy

(%) 2012 2013 2014 2015 2016 Fitch’s expectation

Loss reserves to CY incurred losses (non-life) (x) 0.6 0.6 0.6 0.6 0.6 Fitch expects MAPFRE’s reserving practice to remain prudent. Loss reserves/equity (non-life) 51 50 48 58 58

Net technical reserves to net earned premiums (non-life) 91 87 95 100 103

Source: Fitch, company accounts

Insurance

MAPFRE, S.A.

July 2017 14

Centralised Reinsurance Programme

Central procurement role for MAPFRE Re

Moderate exposure to natural catastrophes

Central Procurement Role for MAPFRE Re

Fitch understands that MAPFRE Re provides the group with catastrophe risk management

expertise and has a central procurement role in arranging the group’s outwards reinsurance

programme. It also acts as a writer of external inward reinsurance business. MAPFRE Re’s

retrocession panel is strong with most reinsurers rated at least ‘A+’.

Moderate Exposure to Natural Catastrophes

MAPFRE is exposed to natural catastrophe risks. However, in 2011 the company comfortably

withstood the impact of the catastrophes in Japan, New Zealand, Thailand, Asia, Australia and

the US, suggesting adequate business and geographical diversification and reinsurance

protection.

The Spanish insurance industry also benefits from the presence of the Consorcio de

Compensacion de Seguros (Insurance Compensation Consortium in Spain) – the Spanish

government scheme set up to cover the costs of the direct damage from natural hazards and

political and social risks such as terrorism or riots.

Reinsurance, Risk Management and Catastrophe Risk

(%) 2012 2013 2014 2015 2016 Fitch’s expectation

Net written premiums/gross written premiums (non-life)

85 83 84 80 81 Fitch does not expect any significant change in MAPFRE’s reinsurance buying. Reinsurance recoveries to equity (life and non-life) 29 28 26 31 28

Source: Fitch, company accounts

Insurance

MAPFRE, S.A.

July 2017 15

Appendix A: Other Ratings Considerations

Group IFS Rating Approach

MAPFRE is rated on a consolidated group approach, with all the rated subsidiaries

considered ’Core’. All the rated subsidiaries are material in size and support the group’s

strategic objectives. As a result, the operating subsidiaries’ ratings have been aligned with

Fitch’s view of the financial strength of the group as a whole.

Complete Ratings List

Entity Rating type Rating

MAPFRE SA Long-term IDR A−/Positive

Senior unsecured

EUR1000m, 1.625%, maturity May 2026 (ES0224244071) Long-term BBB+

Subordinated debt

EUR600m, 4.375%, maturity 31 Mar 2047 (ES0224244089) Long-term BBB−

MAPFRE Espana Compania de Seguros y Reaseguros, S.A. IFS A−/Positive

MAPFRE Re Compania De Reaseguros S.A IFS A−/Positive

MAPFRE Global Risks Cia International De Seguros y Reaseguros IFS A−/Positive

MAPFRE Vida SA De Seguros y Reaseguros IFS A−/Positive

Source: Fitch, MAPFRE

Notching

For notching purposes, the regulatory environment of Spain is assessed by Fitch as being

Effective, and classified as following a Group Solvency approach.

Notching Summary

Holding Company IDR

Notching between the insurance operating company and holding company IDRs was expanded

by one notch relative to standard notching for a group solvency regulatory environment due to

foreign earnings and/or capital being greater than 30% of the consolidated group total.

IFS Ratings

MAPFRE’s IFS ratings are constrained by the sovereign rating. No rating can exceed the

sovereign constraint, which Fitch has set at ‘A−’ for MAPFRE, one notch above Spain’s sovereign

rating of ‘BBB+’. The sovereign constraint is applied as the last step in the ratings process.

Initially, no constraint is assumed when the unconstrained assessment is derived. A baseline

recovery assumption of Good applies to the unconstrained IFS assessment, and standard

notching was used from the IFS anchor rating to the implied unconstrained operating company

IDR. The sovereign constraint is then applied to all unconstrained ratings above the sovereign

constraint.

Debt

For the senior unsecured debt issued by MAPFRE, S.A., a holding company of the group, Fitch

assumes a ’Below Average’ baseline recovery and the ratings are therefore one notch lower

than the IDR of MAPFRE, S.A.

Hybrids

For hybrids issued by MAPFRE, S.A., the following applies:

A EUR600 million subordinated bond issued in March 2017: a baseline recovery

assumption of Poor and a non-performance risk assessment of Moderate. A three-

notch differential was applied relative to the IDR, which was based on two notches for

recovery and one notch for non-performance risk.

Insurance

MAPFRE, S.A.

July 2017 16

Hybrids – Equity/Debt Treatment

Hybrids Treatment

Hybrid Amount FBM Fitch (%) FBM reg. override (%) FLR debt (%)

MAPFRE, S.A.

ES0224244089 EUR600m 0 100 100

FBM Factor-based capital model; FLR Financial leverage ratio; n.a. Not Applicable For FBM, % tells portion of hybrid value included as Available Capital, both before (Fitch %) and after the Regulatory Override For FLR, % tells portion of hybrid value included as debt in numerator of leverage ratio Source: Fitch

Exceptions to Criteria/Ratings Limitations

None.

Insurance

MAPFRE, S.A.

July 2017 17

The ratings above were solicited by, or on behalf of, the issuer, and therefore,

Fitch has been compensated for the provision of the ratings.

ALL FITCH CREDIT RATINGS ARE SUBJECT TO CERTAIN LIMITATIONS AND DISCLAIMERS. PLEASE READ THESE LIMITATIONS AND DISCLAIMERS BY FOLLOWING THIS LINK: HTTPS://FITCHRATINGS.COM/UNDERSTANDINGCREDITRATINGS. IN ADDITION, RATING DEFINITIONS AND THE TERMS OF USE OF SUCH RATINGS ARE AVAILABLE ON THE AGENCY'S PUBLIC WEB SITE AT WWW.FITCHRATINGS.COM. PUBLISHED RATINGS, CRITERIA, AND METHODOLOGIES ARE AVAILABLE FROM THIS SITE AT ALL TIMES. FITCH'S CODE OF CONDUCT, CONFIDENTIALITY, CONFLICTS OF INTEREST, AFFILIATE FIREWALL, COMPLIANCE, AND OTHER RELEVANT POLICIES AND PROCEDURES ARE ALSO AVAILABLE FROM THE CODE OF CONDUCT SECTION OF THIS SITE. FITCH MAY HAVE PROVIDED ANOTHER PERMISSIBLE SERVICE TO THE RATED ENTITY OR ITS RELATED THIRD PARTIES. DETAILS OF THIS SERVICE FOR RATINGS FOR WHICH THE LEAD ANALYST IS BASED IN AN EU-REGISTERED ENTITY CAN BE FOUND ON THE ENTITY SUMMARY PAGE FOR THIS ISSUER ON THE FITCH WEBSITE.

Copyright © 2017 by Fitch Ratings, Inc., Fitch Ratings Ltd. and its subsidiaries. 33 Whitehall Street, NY, NY 10004. Telephone: 1-800-753-4824, (212) 908-0500. Fax: (212) 480-4435. Reproduction or retransmission in whole or in part is prohibited except by permission. All rights reserved. In issuing and maintaining its ratings and in making other reports (including forecast information), Fi tch relies on factual information it receives from issuers and underwriters and from other sources Fitch believes to be credible. Fitch conducts a reasonable investigation of the factual information relied upon by it in accordance with its ratings methodology, and obtains reasonable verification of that information from independent sources, to the extent such sources are available for a given security or in a given jurisdiction. The manner of Fitch’s factual investigation and the scope of the third-party verification it obtains will vary depending on the nature of the rated security and its issuer, the requirements and practices in the jurisdiction in which the rated security is offered and sold and/or the issuer is located, the availability and nature of relevant public information, access to the management of the issuer and its advisers, the availability of pre-existing third-party verifications such as audit reports, agreed-upon procedures letters, appraisals, actuarial reports, engineering reports, legal opinions and other reports provided by third parties, the availability of independent and competent third-party verification sources with respect to the particular security or in the particular jurisdiction of the issuer, and a variety of other factors. Users of Fitch’s ratings and reports should understand that neither an enhanced factual investigation nor any third-party verification can ensure that all of the information Fitch relies on in connection with a rating or a report will be accurate and complete. Ul timately, the issuer and its advisers are responsible for the accuracy of the information they provide to Fitch and to the market in offering documents and other reports. In issuing its ratings and its reports, Fitch must rely on the work of experts, including independent auditors with respect to financial statements and attorneys with respect to legal and tax matters. Further, ratings and forecasts of financial and other information are inherently forward-looking and embody assumptions and predictions about future events that by their nature cannot be verified as facts. As a result, despite any verification of current facts, ratings and forecasts can be affected by future events or conditions that were not anticipated at the time a rating or forecast was issued or affirmed.

The information in this report is provided “as is” without any representation or warranty of any kind, and Fitch does not represent or warrant that the report or any of its contents will meet any of the requirements of a recipient of the report. A Fitch rating is an opinion as to the creditworthiness of a security. This opinion and reports made by Fitch are based on established criteria and methodologies that Fitch is continuously evaluating and updating. Therefore, ratings and reports are the collective work product of Fitch and no individual, or group of individuals, is solely responsible for a rating or a report. The rating does not address the risk of loss due to risks other than credit risk, unless such risk is specifically mentioned. Fitch is not engaged in the offer or sale of any security. All Fitch reports have shared authorship. Individuals identified in a Fitch report were involved in, but are not solely responsible for, the opinions stated therein. The individuals are named for contact purposes only. A report providing a Fitch rating is neither a prospectus nor a substitute for the information assembled, verified and presented to investors by the issuer and its agents in connection with the sale of the securities. Ratings may be changed or withdrawn at any time for any reason in the sole discretion of Fitch. Fitch does not provide investment advice of any sort. Ratings are not a recommendation to buy, sell, or hold any security. Ratings do not comment on the adequacy of market price, the suitability of any security for a particular investor, or the tax-exempt nature or taxability of payments made in respect to any security. Fitch receives fees from issuers, insurers, guarantors, other obligors, and underwriters for rating securities. Such fees generally vary from US$1,000 to US$750,000 (or the applicable currency equivalent) per issue. In certain cases, Fitch will rate all or a number of issues issued by a particular issuer, or insured or guaranteed by a particular insurer or guarantor, for a single annual fee. Such fees are expected to vary from US$10,000 to US$1,500,000 (or the applicable currency equivalent). The assignment, publication, or dissemination of a rating by Fitch shall not constitute a consent by Fitch to use its name as an expert in connection with any registration statement filed under the United States securities laws, the Financial Services and Markets Act of 2000 of the United Kingdom, or the securities laws of any particular jurisdiction. Due to the relative efficiency of electronic publishing and distribution, Fitch research may be available to electronic subscribers up to three days earlier than to print subscribers.

For Australia, New Zealand, Taiwan and South Korea only: Fitch Australia Pty Ltd holds an Australian financial services license (AFS license no. 337123) which authorizes it to provide credit ratings to wholesale clients only. Credit ratings information published by Fitch is not

intended to be used by persons who are retail clients within the meaning of the Corporations Act 2001.