1 AARP Tax-Aide Prospective Volunteer Recruitment System 9/30/09.

Instructor Digest 2006-2007 - 1 -

AARP Tax-Aide is a program of the AARP Foundation, offered in conjunction with the IRS.

(Tax Year 2006)

Building o

n 38 Year

s of E

xperi

ence

Serving A

merican

Taxpa

yers

INSTRUCTORDIGEST

Instructor Digest 2006-2007 - 2 -

Table of Contents

Topic Page About AARP Tax-Aide 3 Volunteer Organizational Chart 6 AARP Foundation and AARP 7 Instructor Position Description 10 Activities Schedule 12 Instructor’s Report 13 Responsibilities of Training and Certifying Counselors 14 Preparation Checklist 15 Certification Process 16 Scope of Program 17 Confidentiality and Security of Taxpayer Data 19 Lost or Missing Equipment 21 The Importance of Adult Learning Principles 22 Reimbursement Policies 23 Insurance Coverage 30 Volunteer Assessment of AARP Tax-Aide Program 31 Appendix A: Emerging Issues 33

Instructor Digest 2006-2007 - 3 -

AARP Tax-Aide Mission and Organization Mission: To provide high quality free income tax assistance and tax form preparation to low- and middle-income taxpayers, with special attention to those age 60 and older.

Who We Are AARP Tax-Aide is the nation’s largest volunteer-run tax assistance and preparation service, preparing tax returns and answering tax questions free of charge. AARP Tax-Aide is a program of the AARP Foundation and is offered in conjunction with the IRS.

Where We Serve Our Taxpayers

Most taxpayers receive in-person assistance at one of the estimated 7,000 sites nationwide. Free electronic filing is offered at over 5,000 sites. Sites are located in malls, libraries, banks, senior centers, and other convenient facilities. We also provide shut-in service upon special request, whenever possible. Year-round tax assistance is offered online at www.aarp.org/taxaide. Quality reviewed answers are sent to taxpayers via email within a few business days.

How Many Volunteers Serve

Over 32,000 volunteers make up AARP Tax-Aide. Virtually all provide tax assistance, and 6,500 are also volunteer leaders.

Program Structure & Admin-istration

AARP Tax-Aide is a nationwide, volunteer-run program. Regional and state volunteer leaders share in setting policies while assuming most supervisory and operational responsibilities. Volunteer tax assistance Counselors provide all service-level tax assistance. Instructors provide tax training to Counselors.

Coordinator & Specialist Roles

Coordinators recruit and supervise volunteers at all levels. Local Coordinators (LCs) ensure volunteer recruitment and training, volunteer certification, site creation, site compliance with program policy, database accuracy, activity reporting, and counselor expense reimbursement. District Coordinators (DCs) manage activity at the district level and recruit and supervise Local Coordinators. State Coordinators (SCs) oversee all state activities and set operation policies. Communications Coordinators (CCs) and Technology Coordinators (TCs) support their specialty interests at the local levels. Specialists support administration, partnerships and communications, technology, and training needs at the state level. Regional Coordinators (RCs) guide and supervise State Coordinators and serve on the National Leadership Team (NLT).

National Leadership Team & National Office Staff

The National Leadership Team (NLT) of volunteer Regional Coordinators and National Committee Chairs develop and implement AARP Tax-Aide goals and objectives. National committees support the NLT in the areas of leadership, technology, and training. National Office staff coordinate program policies, maintain relationships with IRS and other key partners, provide administrative support to volunteer leaders, and collect/report administrative data and program impact.

Electronic Filing

AARP Tax-Aide offers free electronic filing at more than 5,000 sites nationwide using IRS provided tax preparation software.

Internet Tax Assistance

Since 1998, AARP Tax-Aide has had a 24-hour year-round Internet tax assistance service at its web site (www.aarp.org/taxaide). Taxpayers can pose questions online and get quality-reviewed answers back within a few business days. Interested volunteers with web access can sign up online at www.aarp.org/tavolunteers. There volunteers will find a link to the online tax assistance registration form.

Instructor Digest 2006-2007 - 4 -

Web Page Features

Located at www.aarp.org/taxaide, our website offers tax assistance, frequently asked tax questions and program information. Information on AARP Tax-Aide volunteer opportunities, which are available from February 1 to April 15 at individual program sites, is also available on the website.

Volunteer Extranet

Located at www.aarp.org/tavolunteers (case sensitive), this site offers information and tools to assist volunteers in performing the responsibilities of their AARP Tax-Aide position.

CyberTax E-Mail Newsletter

Any program volunteer with email is encouraged to receive CyberTax, a nationwide email newsletter containing periodic updates on the program, taxes, and IRS. Email your name, program position, and state to [email protected] to join the CyberTax distribution list.

How to Volunteer Via Telephone and the Web

Interested persons call toll-free, 1-888-OURAARP (1-888-687-2277) and follow the prompts. Or at www.aarp.org/taxaide where an online volunteer recruitment form can be found. Volunteering can be done in either tax preparation assistance and/or leadership positions.

General volunteer position descriptions

Tax Assistance positions require training, successful completion of the IRS certification exam, and agreement to the IRS Standards of Conduct. Leadership positions coordinate program delivery by volunteers at sites at the local, state, or regional level or manage specific program activities such as technology, training, administration, or communication. Although tax training and certification is encouraged, it is not required for many leadership positions.

Organizing the Geographic Territory AARP Tax-Aide regional boundaries are predetermined by the AARP Tax-Aide National Office. State boundaries apply except for California, Florida, Illinois, Minnesota, New York, Ohio, Pennsylvania, and Texas. These heavily populated states are split, with multiple AARP Tax-Aide “states” within their geographic borders. Within states, State Coordinators may organize into whatever geographic districts will provide the most efficient, equitable, or manageable division. A district is the responsibility of one District Coordinator. District Coordinators may divide their district into workable entities for assignment to Local Coordinators. In all cases, the boundaries should be clearly understood by all volunteers and delineated by the responsible Coordinator.

Instructor Digest 2006-2007 - 5 -

AARP Tax-Aide’s CustomersHow Many Customers

During the 2006 tax season, from February 1- April 17, we served over 2,000,000 customers. Over the past 38 years, we have served more than 40 million customers.

Who They Are (from 2005 survey)

Customer Age 10% 18-49 34% 70 – 79 8% 50-59 20% 80+ 24% 60-69 4% no answer

Customer Marital Status

36% Married 60% Not Married

Gender 61% Female 35% Male

Race/Ethnicity (from 2004 survey)

78% White non-Hispanic 4% Hispanic 3% Native American 6% Black or African American 2% Asian/Pacific 1% Other

Household Income (Annual)

42% Under $20,000 18% $30,000-$49,000 25% $20,000-$29,000 4% $50,000 or more

Repeat Customers

24% Once 38% Four+ Times 37% Two - Three Times

Working Status 72% Retired 24% Not Retired

Customers’ Proximity to Site

55% 0 - 3 miles 12% 6 - 9 miles 2% No answer 20% 4 - 5 miles 11% 10+ miles

What They Think Excellent Good Fair Poor

Overall quality of AARP Tax-Aide’s Service 81% 16% 1% 0%

Helpfulness of Volunteers 83% 13% 1% 0%

Tax Knowledge of Volunteers 74% 21% 2% 0%

Would they recommend AARP Tax-Aide to others? 94% 5% 0%

Who would help them with their taxes if they didn’t use AARP Tax-Aide?

52% Pay for

assistance

35% Self or friend

8% IRS

(Source: 2005 AARP Tax-Aide Customer Satisfaction Survey)

Instructor Digest 2006-2007 - 6 -

AARP AARP is a nonprofit, nonpartisan membership organization dedicated to making life better for people 50 and over. We provide information and resources; engage in legislative, regulatory and legal advocacy; assist members in serving their communities; and offer a wide range of unique benefits, special products, and services for our members. These include AARP The Magazine published monthly, AARP Bulletin, our monthly newspaper; AARP Segunda Juventud, our quarterly newspaper in Spanish; NRTA Live & Learn, our quarterly newsletter for 50 +_educators; our web site, www.aarp.org. We have staffed offices in all 50 states, the District of Columbia, Puerto Rico, and the U.S. Virgin Islands. Our State Offices are staffed with an AARP State Director and other employees who work in partnership with volunteers serving in roles such as:

* State President * State Executive Council which includes:

- State Director - State President - State Leadership Volunteer for Advocacy - State Leadership Volunteer for Community Service - State Leadership Volunteer for Communications * State Volunteer Community Specialists * AARP Chapters and NRTA units This field structure creates a dynamic presence in every community and responds to the needs and interests of AARP members at the local level. .

AARP’S VISION, MISSION, GOALS

AARP’s Vision “A society in which everyone ages with dignity and purpose and in which AARP

helps people fulfill their goals and dreams.”

AARP’s Mission

“AARP is dedicated to enhancing quality of life for all as we age. We lead positive social change and deliver value to members through information advocacy and service.”

AARP’s Three Great Goals

AARP’s three great goals: * To be the most successful and acknowledged organization in America for positive social change; * To deliver on our promise to each AARP member; * To be a world leader in global aging.

Welcome to AARP Foundation and AARP! The AARP Foundation and AARP have a long-standing commitment to community service. Through our collective efforts, millions of people are well served each year in communities across the country. AARP Foundation and AARP volunteers are the heart of our community service programs. In your community, you exemplify AARP’s commitment to helping others when offering services through the AARP Tax-Aide program. AARP Foundation The AARP Foundation is AARP’s affiliated 501(c)(3) charity for helping in communities like yours all across America. Founded in 1961, our mission is crucial: to build a society in which everyone ages with dignity, purpose and independence. Foundation programs provide security, protection and empowerment for older persons in need. Low-income older workers receive job training and placement they need to re-join the workforce. Free tax preparation is provided for low-and middle-income individuals, with special attention to those 60 and older. The Foundation’s litigation staff protects the legal rights of older Americans in critical health, long-term care, and consumer and employment situations. Additional programs provide information, education and services to ensure that people over 50 lead lives of independence, dignity and purpose. Foundation programs are funded by grants, tax-deductible contributions and AARP.

AARP Foundation

COO of AARP

Director Foundation Programs

Chief Development Officer Foundation Development

DirectorFinancial Management

DirectorBusiness Operations

Director Legal Advocacy

AARP Foundation Board (appointed by AARP Board; 4

AARP Board Members, CEO of AARP, 3 external)

-DOL: SCSEP -IRS: Tax-Aide -HHS: Legal Hotlines -HHS: Nat'l Legal Training Project -HUD: Reverse Mortgages -CO: ElderWatch -Benefits Outreach -Money Management -Grandparent Information Center -WV: ElderWatch -HHS: WV SMIEPP -CNCS: Partners for Independence -Consumer Fraud Protection -Women’s Leadership Circle

-Direct Response -Planned Giving -Major Gifts -Institutional Support

- Direct Representation - Amicus - 3rd Party

Executive Director AARP Foundation

Director Integration

Instructor Digest 2006-2007 - 7 -

Instructor Digest 2006-2007 - 8 -

AARP Foundation Programs and Services

AARP Tax-Aide volunteers annually provide free tax assistance and preparation service to approximately two million low and moderate income taxpayers, with special attention to those age 60 and older. Electronic filing and on-line tax assistance are also offered by the program. The program’s funding sources include the Internal Revenue Service, AARP and private contributions. 1-888-AARPNOW (toll-free for sites and volunteer opportunities) or www.aarp.org/taxaide. AARP Senior Community Service Employment Program (SCSEP) helps individuals age 55 and older with limited income gain the job skills and work experience necessary to transition to permanent employment. In addition, the program provides over 8 million hours of community service annually to local nonprofit agencies that assist with training program participants, enabling them to expand and provide key services. The program, funded by the US Department of Labor, is sponsored by the AARP Foundation in 76 communities in 22 states and Puerto Rico. www.aarp.org/scsep AARP Money Management Program offers financial education materials for older adults and their caregivers plus daily money management services through volunteers to help older or disabled people who have difficulty budgeting, paying bills and keeping track of financial matters and who have no family or friends able to help. This program is funded by AARP. www.aarpmmp.org AARP Benefits Outreach Program offers assistance to older people with low or moderate incomes to find public and private benefit programs for which they may be eligible, to help pay for prescription drugs, doctor’s bills, groceries, heating bills, property taxes and more. One way this program offers assistance is by encouraging the use of a free website developed by the National Council on Aging: (www.benefitscheckup.org). The Benefits Outreach program is funded by AARP. AARP Foundation Grandparent Information Center (GIC) provides information, referral and outreach for grandparents, policy makers, corporations and direct service providers, with a special emphasis on support for grandparents who provide care for their grandchildren. The program’s funding sources include AARP and private contributions. www.aarp.org/grandparent AARP Reverse Mortgage Education Project is the nation’s leading source of independent consumer information and free counseling about reverse mortgages and less costly alternatives. It trains, tests and provides referrals to a national network of 75 non-profit counselors. The project’s funding sources include the US Department of Housing and Urban Development (HUD) and AARP. www.hecmresources.org AARP National Legal Training Project trains lawyers and other advocates throughout the country in substantive law and advocacy skills to enhance their free and reduced fee services to older Americans, and conducts a “training of trainers” program to produce a cadre of elderlaw trainers who expand the reach of the program. The program’s funding sources include the US Administration on Aging, AARP and private contributions. www.aarp.org/ntltrpro AARP Technical Support for Legal Hotlines Project provides technical assistance, training and materials to statewide legal hotlines that provide free legal advice and brief services by telephone to persons age 60 and over. The project provides similar assistance to help legal aid programs develop legal hotlines and continuously tests new methods for enhancing the productivity and quality of hotlines. The program’s funding sources include the US Administration on Aging, AARP and private contributions. www.legalhotlines.org AARP Elder Watch Projects fight financial exploitation of older Americans in the states of Colorado and West Virginia through direct client assistance to help resolve consumer-based disputes, extensive outreach and education and collection of data. The program’s funding sources include the State’s Attorneys General Office, AARP and private contributions. www.aarpelderwatch.org AARP West Virginia Senior Medicare Patrol Project is a consumer education project dedicated to preventing Medicare and Medicaid fraud, error, waste, and abuse. The program trains retired professionals to educate older West Virginians and their advocates on the identification and reporting of Medicare and

Instructor Digest 2006-2007 - 9 -

Medicaid fraud, waste, and abuse and provides a system to report suspected errors. The program’s funding sources include the US Administration on Aging and AARP. www.aarp.org/foundation/wvsmp Partners for Independence: Restoring Hope to Seniors is a program to recruit boomer volunteers to provide critically needed services to victims of the 2005 hurricanes. The Foundation is partnering with AARP state offices in Louisiana, Mississippi, and Texas as well as with Faith in Action and Rebuilding Together in this initiative. The program is funded by a grant from the Corporation for National and Community Service and private contributions. AARP Consumer Fraud Prevention Program works with qualified not-for-profit organizations whose volunteers call victims and potential victims of telemarketing and other frauds to inform and educate older people, with a focus on preventing victimization or further victimization. The AARP Foundation Women's Leadership Circle leverages the philanthropic power and passion of women to improve and enhance women's lives as they grow older. The AARP Foundation Women's Leadership Circle (WLC) provides women with the opportunity to explore the image and language of aging; to define paths to economic security and to encourage healthy lifestyles as we lead a national movement to raise awareness of issues faced by women as they age. AARP Foundation Litigation (AFL) defends and expands the rights of older Americans by representing them in significant court cases and by writing friend-of-the-court (amicus) briefs on behalf of AARP. (AFL) is involved in litigation before state and federal appellate courts, state supreme courts, and the U.S. Supreme Court. AARP Foundation Litigation addresses legal issues that affect the daily lives of older persons such as health and long term care, consumer protection including predatory lending, age and disability discrimination in employment, pensions and other retiree benefits. AARP Foundation Disaster Relief and Recovery Fund: Making a Difference The AARP Foundation continues to make a difference on the Gulf Coast region with disaster relief and recovery grants to over 40 local agencies. These agencies are serving older victims of hurricanes who have been displaced, or have health, legal or other needs. Grantees include state and local organizations as well as national organizations such as Rebuilding Together, Boat People SOS, and the National Housing Law Project. Grants made to these agencies are helping with immediate, transitional and longer term needs. As the Gulf Coast begins to recover and rebuild, the AARP Foundation will continue to support state, local and national agencies with grants made from its Disaster Relief and Recovery Fund. In total, the Foundation has donated nearly $1.6 million to organizations operating on the ground in Alabama, Louisiana, Mississippi and Texas. AARP Foundation Development Donating to the AARP Foundation lets donors have “the power to make it better” ™ by strengthening and supporting the Foundation’s efforts to help people over 50 lead lives of independence, dignity and purpose. There are a variety of giving options including outright gifts of cash or appreciated securities, bequests, real and personal property, and through charitable gift annuities and charitable remainder trusts. As a charitable organization, gifts to the AARP Foundation are tax deductible, and they can make a positive difference in the quality of life of our most vulnerable elderly in society. For More Information on AARP Foundation Programs and Services: WEB: You may visit us on the web at www.aarp.org/foundation MAIL: You may write us at: AARP Foundation 601 E Street, NW Washington, DC 20049 PHONE: Or you can call us at 1-888-OUR-AARP (687-2277)

Instructor Digest 2006-2007 - 10 -

AARP Tax-Aide Volunteer Position Description: Instructor (INS) Program: AARP Tax-Aide provides free personal income tax preparation and assistance to low- and middle-income taxpayers, with special attention to those age 60 and over. Purpose of Position: The Instructor has responsibility for Counselor training and certification as determined by the State Coordinator and the State Management Team. Responsibilities of Position: Supported by the policies and procedures of the AARP Foundation and the Policy Manual, the Instructor: ⇒ Attends Instructor workshop and passes all three sections of the test for IRS certification. ⇒ Schedules Counselor training classes, as required. ⇒ Provides instruction on income tax information and tax return preparation, as well as the

need to maintain the confidentiality of taxpayer data at all times,ensures that instruction is provided to all site level volunteers on program policy and administrative procedures, especially confidentiality and security.

⇒ Grades and returns IRS test to Counselors. ⇒ Reviews test results with Counselors and provides guidance for identified weak areas. ⇒ Submits a list of Counselors who successfully pass the IRS test to the state Training

Specialist (TRS), or in accordance with the state's procedures. Qualifications: Instructors must have the ability and knowledge to train volunteers in tax law and preparation of tax returns a district (sub-state geographic area), and must work effectively with diverse populations. Instructors must pass the advanced level of the IRS certification exam. Term of Service: The Instructor is appointed for a one year term, contingent upon satisfactory annual review and certification, and may be reappointed for additional one year terms. Eligibility for Multiple Volunteer Positions: Instructors are eligible for other AARP or AARP Foundation volunteer positions. Time Required: Instructors are expected to provide 20 hours of work per week during tax training season. Travel Required: The Instructor must attend district and or local meetings as well as training sessions as necessary for performance of duties. Training Required: Instructors must acquire a tax proficiency sufficient to train others (as determined by passing the IRS certification exam) as well as knowledge of AARP Tax-Aide program policies. Appointed & Supervision: Instructors are appointed by the District Coordinator (DC) in consultation with the State Coordinator and TRS. Instructors report directly to DCs. Scope of Authority: Instructors train Counselors to assist in the preparation of tax returns for the target population in accordance with program policy. They do not supervise another AARP Tax-Aide volunteer position.

Instructor Digest 2006-2007 - 11 -

Working Relations: Instructors work closely with the TRS, DC, Technology Coordinator (where e-filing) Local Coordinator and other AARP volunteers as required. Progress Review: Instructor performance is monitored on an on-going basis, and reviewed annually by DC with input from the TRS. Available Resources: Instructors will be afforded the necessary guidance, training and materials needed to fulfill their responsibilities. Additional support and training are provided from the AARP Tax-Aide State Coordinator, the IRS and National Office staff. AARP Tax-Aide reimburses volunteers for covered program related expenses as set out in the Policy Manual. Volunteer Policy: AARP Foundation volunteers will receive equal opportunity and treatment throughout recruitment, appointment, training, and service. There will be no discrimination based on age, disabilities, gender, race, national or ethnic origin, religion, economic status, or sexual orientation.

Instructor Digest 2006-2007 - 12 -

Activities Schedule: Instructor September ⇒ Current Instructors submit final expense statement for all expenses incurred prior to

September 30 (end of fiscal year). ⇒ Potential Instructors invited to participate in training by Training Specialist. October ⇒ Attend district meeting as required. If criteria met, receive invitation to Instructor Workshop. December ⇒ Attend Instructor Workshop, and pass IRS test for certification. ⇒ Receive appointment/confirmation letter. Meet with other Instructors to plan Counselor class

schedules, allocate teaching assignments per class and establish grading procedure. ⇒ Prepare lesson plan for Counselor training, verify material orders, classroom dates, facilities,

times, etc. January ⇒ Instruct classes as scheduled, grade and return tests, and report results and certification status

of Counselors to Training Specialist and Local Coordinators. April ⇒ Submit expense statements monthly or quarterly to supervising Coordinator.

ARP Tax-Aide Program Instructor’s Report TO: TRS and Local Coordinators Course Location_____________________ Dates ______________________________

LAST NAME

FIRST NAME

ADDRESS

ZIP

PHONE

STYE

Instructor Digest 2006-2007 - 13 -

RESPONSIBLITIES FOR TRAINING AND CERTIFICATION OF COUNSELORS

Responsibility for Counselor Classes

• The DC has overall responsibility for ensuring that Counselors in the district are trained. However, Instructors, reporting to the DC, have actual responsibility for training the Counselors.

• The Instructor, in consultation with the LC or DC as appropriate, selects the class site, arranges the physical setup for the class and determines the process for correcting the IRS test. The materials needed for each class are to be ordered by the Instructor for the class, or as otherwise determined by the SMT. Materials needed for the tax preparation sites are to be ordered by the LC.

• A lead Instructor may be designated for a Counselor training with two or more Instructors to ensure all administrative and coordination tasks are planned and executed.

Selecting Candidates for Counselor Classes

• Candidates for Counselor Classes are obtained from the LC for experienced Counselors and from the DC and/or LC for new Counselors.

• If the ADS maintains a computerized database for volunteers, Counselor lists by LC, DC, or zip code can be created from such a program. This list should be previewed by the appropriate Coordinator (s) before letters of invitation are sent out for the new year.

• Many districts schedule separate training classes for new Counselors in order to cover all topics in detail. Experienced Counselors receive a scaled-back training focusing primarily on new and difficult tax topics.

Instructor Digest 2006-2007 - 14 -

Training Materials for Counselor Classes

• The TRS should provide Instructors with sample agendas for new and experienced Counselor Classes.

• The Volunteer Assistor's Guide IRS Pub 678 (VAG), the Volunteer Resource Guide, IRS Pub 4012, and IRS Pub 17 are the primary tools for Counselor training.

Testing the Counselors

• Testing of the Counselors varies by District and by State. • All volunteers must pass the IRS test in order to be certified Counselors.

Evaluations • Key to determining the effectiveness of training is evaluating both the course and

the Instructor. Evaluations should be handed out to students at the start of the class. Students should complete evaluations at the end of class prior to departure.

Mentoring • Data has confirmed year after year that new volunteers leave the program in substantially higher proportions when compared to longer-tenured volunteers. It is important for this reason to mentor and support new volunteers in order to help reduce this attrition. Not only do we want to support new volunteers, we need to ensure they have a firm grasp of needed tax law to produce accurate tax returns. Special attention during training, pairing with an experienced counselor at training and for questions at the site and the more formal second person Quality Review of the new volunteer’s work, are useful ways to offer support as well as verify a new volunteer’s understanding f tax law.

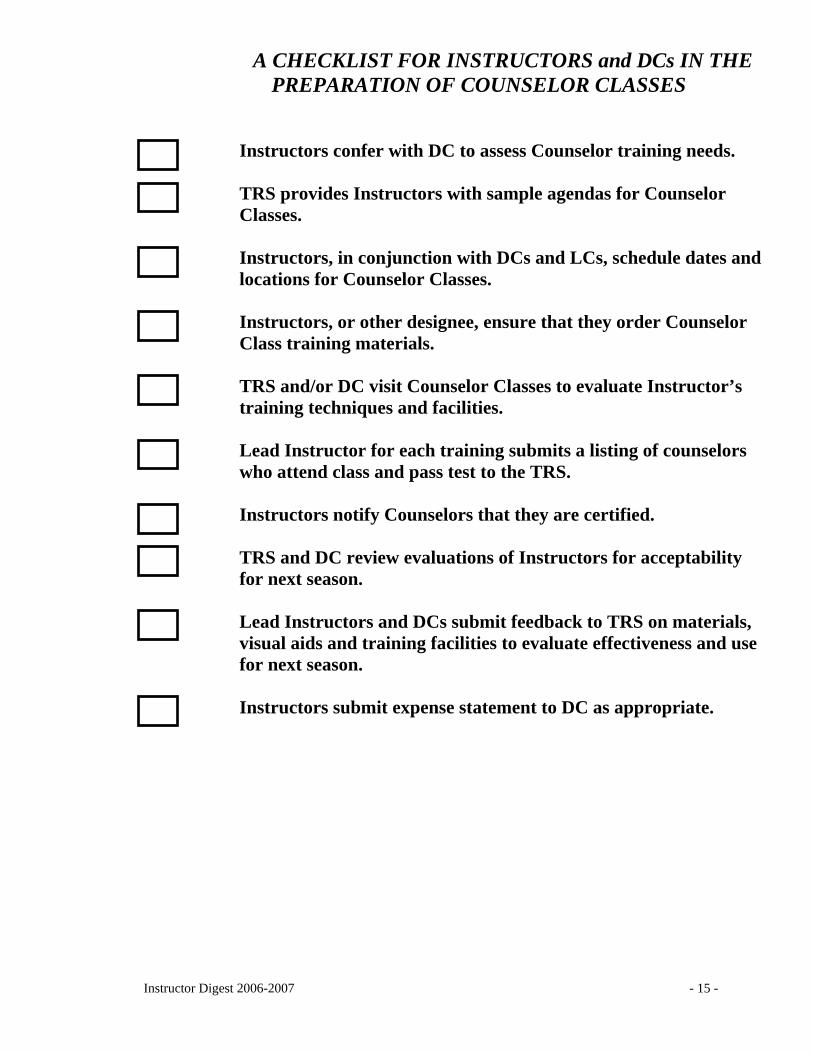

A CHECKLIST FOR INSTRUCTORS and DCs IN THE PREPARATION OF COUNSELOR CLASSES

Instructor Digest 2006-2007 - 15 -

Instructors confer with DC to assess Counselor training needs. TRS provides Instructors with sample agendas for Counselor Classes.

Instructors, in conjunction with DCs and LCs, schedule dates and locations for Counselor Classes.

Instructors, or other designee, ensure that they order Counselor Class training materials.

TRS and/or DC visit Counselor Classes to evaluate Instructor’s training techniques and facilities.

Lead Instructor for each training submits a listing of counselors who attend class and pass test to the TRS.

Instructors notify Counselors that they are certified.

TRS and DC review evaluations of Instructors for acceptability for next season.

Lead Instructors and DCs submit feedback to TRS on materials, visual aids and training facilities to evaluate effectiveness and use for next season.

Instructors submit expense statement to DC as appropriate.

CERTIFICATION, SCOPE OF PROGRAM, RECORDS AND REPORTING

The Certification Process

1) All volunteers who prepare Federal Tax returns must be “certified” under the terms of the Internal Revenue Service (IRS) grant to the AARP Tax-Aide program. (Note:there are no exceptions to the certification process.) To qualify as an AARPP Tax-Aide Counselor, Instructor, or ERO a volunteer must be certified annually and follow a three step process:

Step one: Pass the test. Counselors must be certified at the Advanced Level. Step two: Sign the Volunteer Standards of Conduct. These forms must be kept by local leaders until December 31. Step three: AARP Tax-Aide National Office and the IRS are notified of those who pass the test and are participating in the AARP Tax-Aide program as Counselors, EROs, or Instructors.

The IRS Student Guide will have three segments: Basic, Intermediate, and Advanced. Counselors must be certified at the Advance Level. Counselors provide service only on topics covered at the training and for which they are certified (professionals experience and/or other sources of training are no longer acceptable).

2) Instructors grade the test and inform the volunteer by returning the graded test. In the event a volunteer does not pass the test, the volunteer can pass a retest in order to gain certification. The Instructor or another leader (determined by the SC) must keep the Volunteer Standards of Conduct until December 31.

3) The SC, with the SMT, must establish procedures for verifying and ensuring that a list of certified counselors who have passed the basic, intermediate and advanced portions of the test are provided to the IRS by the third business day of February. In addition to the IRS, information about certified counselors who have passed the test must be provided to leaders in AARP Tax-Aide, including the ADS for submission to AARP National Office, the appropriate LCs and DCs, so they have documentation of which volunteers are certified to assist taxpayers in the upcoming tax season. IRS Form 13206, the Volunteer Assistance Summary Report in NOT applicable to AARP Tax-Aide. At the same level, the IRS should be given a list of certified volunteers and the date that each volunteer passed the test and no other personal information. Additionally, the information provided to the IRS will include the components of the test that the volunteer passes. For AARP Tax-Aide volunteers, this level must be the Advanced level. It is not necessary to give the IRS addresses of volunteers along with this listing because the AARP Tax-Aide program has been given an exemption from this requirement. No additional contact information, even email addresses should be provided. If a consolidated roster is required by the IRS Tax

Instructor Digest 2006-2007 - 16 -

Specialist, submission should be determined by the SMT 4) After a counselor successfully completes the training and passes the

test, the lead Instructor should ensure that each Counselor has an AARP Tax-Aide name card and plastic holder.

Joint Statement from the National Technology and Tax Training Committee

• The NTC and NTTC jointly recommend that as part of AARP Tax-Aide training, each Counselor (E-file or Paper) complete at least four comprehensive tax problems (from Pub. 678 W, the Tax-Aide Qualification Workbook or other materials/exercises prepared at the local level) and submit to a designated leader for review and evaluation. {The designated leader/reviewer should have at least three year’s experience using Tax Wise.} The review and evaluating may be carried out by an Instructor, but the words “designated leader” were used instead to provide for flexibility during the demanding training period for prospective Counselors. The training period (usually January) is the busiest time for Instructors. The completion of the four problems by a prospective Counselor (in addition to the regular classroom training and the IRS test) is to show his/her competency as an additional training or coaching aid. Instructors can use this additional way to assist someone’s ability to accurately prepare a return. The reviewed four problems should be used to provide constructive feedback to the prospective Counselor on what he/she needs to work on to improve performance. Without such training for all Counselors, Counselors can pass the IRS test and still not be able to prepare a quality return at a Tax-Aide site. This is true for both paper and computer prepares. Additional practice and experience in preparing returns is a valid approach to improving the capabilities of Counselors and smooth site operations. Experience in doing returns is probable more critical to obtaining a quality return for paper prepares than it is for those using TaxWise; the task of preparing a paper return is actually more difficult than preparing the same return on TaxWise.

Scope of Program

• AARP Tax-Aide has no income thresholds; complexity of return determines our ability to serve.

• Volunteers in the AARP Tax-Aide program may prepare returns dealing with matters included in IRS training materials for the Tax Counseling for the Elderly Program (TC) or in AARP Tax-Aide training classes provided they have been qualified under program procedures. State Coordinators may authorize counselors to be trained and certified in Military/Special Issues of the IRS training materials. Additionally, State Coordinators may authorize counselors to be trained qualified in the preparation of Form

Instructor Digest 2006-2007 - 17 -

1040 X; provided that any counselors to trained and qualified to prepare Form 1040X for a particular year must also have been certified for that tax year for the tax matters addressed on each Form 1040X.

Instructor Digest 2006-2007 - 18 -

Instructor Digest 2006-2007 - 19 -

Confidentiality and Security of Taxpayer Data Whether e-filing or not, protecting the confidentiality and security of taxpayer data has always been a priority focus for this program and you the volunteers. In sharing their sensitive personal data with us, taxpayers have entrusted us and given us a major responsibility to protect that information. In today’s age of stolen identities, this focus is even more critical and urgent. Leaders must ensure that all volunteers understand these responsibilities and abide by them. There are many steps we can take to help ensure that we honor that trust and protect taxpayer information. 1) All Counselors must sign the Standards of Conduct statement (IRS Form 13615) which is

provided in the IRS test or as a separate form. That statement has three bullets addressing the protection of taxpayer data: a) I will safeguard the confidentiality of taxpayer information. b) I will exercise reasonable care in the use and protection of equipment and supplies. c) I will not solicit business from taxpayers I assist or use the knowledge I have gained

about them for any direct or indirect benefit for me or any other specific individual. We have taken the step of clearly noting that the certification of a Counselor now has two significant and critical components. First, the Counselor must pass the IRS test. Second, all Counselors must agree to the Standards of Conduct and note that agreement by signing the statement. We take these statements very seriously and expect that you will as well.

2) Information provided for tax return preparation should not be shared with anyone who does not have a need to know. Individuals have the need to know if their involvement is required to accurately process the information to its final disposition. Examples of “need to know” would include, sharing information for the purpose of obtaining guidance in tax return completion, for electronic transmission, and/or for quality review of the finished tax return. In accordance with 18 USC 1905, which applies to Tax Counseling for the Elderly grantees including AARP, it is not acceptable to share information with others, even another volunteer, if their involvement in the tax return preparation is not required. For instance, sharing income information, birth dates, or even the marital status of taxpayers with other volunteers, taxpayers, family, or friends as a matter of curiosity or interest is not acceptable.

3) Forms 8879 have a three year retention requirement from the return due date or IRS

received date, whichever is later. This information must be sent to the local IRS territory office by the end of April. Forms 8879 must not be kept by AARP Tax-Aide volunteers beyond April 30th.

4) For numerous reasons including taxpayer data security and confidentiality all returns

must be prepared in front of the taxpayer and all records given back to the taxpayer at the end of that assistance session. Required retention of some records for e-filing, such as W-2s and 1099s with federal tax withholding is allowed.

5) Sites must not be located in individual volunteers’ homes. Refer to the section on Site

Instructor Digest 2006-2007 - 20 -

Selection for more guidance regarding sites and maintaining confidentiality.

6) Appropriate steps to secure computers with taxpayer data must be taken at all times. Any piece of equipment, computer (personally owned or site sponsor owned) and/or flash drive, on which taxpayer data resides must contain encryption software. This applies to ALL computers, including personally owned and site sponsor owned computers. Slave computers on a server that never have the taxpayer information do not require encryption software. If all taxpayer data is removed by TPClear or the eraser program from a computer or flash drive prior to its leaving the tax site; it no longer contains taxpayer data and does not require encryption software. However, please make sure that you backup all files and data on an encrypted removable storage media prior to running TPClear or eraser because all taxpayer files and settings are deleted by these programs.

7) By April 30th, taxpayer data must be deleted and purged from all computers, personal or

loaned. For IRS loaned computers, use the wipe disk program loaded on the IRS loaned computers. For non-IRS equipment, use TPClear (if not provided by your site leadership it is available for download on www.aarp.org/tavolunteers).

8) Once the returns are accepted by the IRS, it is highly recommended to copy taxpayer data

to an encrypted removable storage media (memory stick, floppy disk, or CD) and delete it off computers throughout the season. This minimizes the number of taxpayers exposed to potential identity theft if computers are stolen. Removable storage media with taxpayer data must be encrypted and secured at all times to prevent being lost or stolen. Data must be removed from all storage media by the end of the season.

9) During the season, the operating system of any computer containing taxpayer data must

be password-protected. Additionally, the TaxWise™ program must be password-protected. If you have any questions about how to password-protect either, please see a volunteer leader at your site or go to www.aarp.org/tavolunteers for guidance.

10) For states allowing the retention of e-file data for use the following season, Counselors

must allow the taxpayer to opt out of retention. Follow your state’s specific procedures for retention. If the taxpayer agrees to allow retention, his or her signature on the Authorization form is required. Only one person per state, determined by the SC, is allowed to retain the data and it must be held on an encrypted removable storage media. All other computers must be wiped clean (see number six above).

11) Counselors should act in a manner that promotes confidentiality for the taxpayer. This

includes how they communicate questions and issues during their sessions with taxpayers. Conversations should be held discretely; personal taxpayer information should not be left out in areas that others may get access to them, and computer screens should be minimized or the application closed down if a Counselor needs to leave the work area during an individual tax counseling session. If you believe that the confidentiality of taxpayer data has been compromised due to any of these types of issues, report this to the National Office (within 24 hours) by calling: 1-800-424-2277, ext 6021 or ext 6027 (during business hours), or 1-202-434-6021/6027 (after hours).

Instructor Digest 2006-2007 - 21 -

Lost, Missing, or Damaged Equipment (with or without Taxpayer Data residing on it)

Computers lost, stolen, or damaged with taxpayer data residing on it: Computers used for tax preparation contain information that is private to the taxpayers involved. Should these computers be lost or stolen with taxpayer data it may be possible for others not only to obtain access to private financial information, but to use the data to illegally access bank accounts, credit cards, etc. Quick intervention is extremely important to minimize problems for the taxpayer.

1. 1-800-424-2277, ext 6021 or ext 6027 (during business hours), or 1-202-434-6021/6027 (after hours), must be called immediately (within 24 hours) if ANY computer containing taxpayer data is lost or stolen.

2. If the loss is the result of theft, call the local police to report the theft as soon as you

realize what has happened.

3. Inform your volunteer supervisor about the situation. Computers lost, stolen, or damaged without taxpayer data residing on it: Even with reasonable care and security, AARP or IRS equipment may be stolen or lost in fire, flood, or other natural disasters. Should a loss of AARP or IRS equipment occur, the state’s TCS must be notified. Please tell your supervisor so he or she can get the information to the TCS. If your supervisor is unavailable call 1-800-424-2277 ext 6021 or 6027 (during business hours), or 1-202-434-6021/6027 (after hours), and AARP Tax-Aide staff will make sure the appropriate notification is made.

Instructor Digest, 2006-2007 Season 22

THE IMPORTANCE OF ADULT LEARNING PRINCIPLES Because we are dealing with adult learners, there is a need to emphasize the use of materials and tools to assist the volunteers understanding of the content of the training. Some adults prefer to learn by listening, some by watching and other by doing. As we can, we should try and accommodate all three learning styles. The Internet is a good source of information on adult learning principles as is the library. The use of visuals, overhead transparencies, demonstrations, practice exercises and various techniques are encouraged in the development of the training session to accommodate different learning styles as well as those with impaired vision or hearing.

Instructor Digest, 2006-2007 Season 23

Expense Reimbursement

Period of Eligibility

Counseling expenses are only reimbursable for training activity conducted after October 1 and counseling activity conducted between February 1 through April 20.

Non-Reimbursable Expenses

Expenses for state/local tax assistance cannot be reimbursed when no federal tax assistance is intended to be provided. Meals and refreshments are not reimbursable for any volunteer (i.e. Counselors, Coordinators and Instructors) during Counselor classes and when counseling at regularly scheduled sites, except in rare cases when the SC authorizes overnight stays. The SC must also provide his/her approval signature on the expense statement.

Reimburse- ment Options

Counselors, Client Facilitators (CF) and Electronic Return Originators (EROs) elect a flat rate stipend of $35, OR itemize their expenses. Volunteers in these positions may waive reimbursement, or may choose to be reimbursed. If they choose to be reimbursed, they can only select ONE of these reimbursement options for the entire season. Either reimbursement option covers expenses incurred during the training period and the counseling season as outlined in the “Period of Eligibility” above.

Required Approval Signature

Without exception, all COU, CF, and ERO expense claims require the approval signature of the supervisor. This signature must appear on a Flat-Rate Reimbursement Form or an individual expense statement. Expense claims without this approval will not be processed.

Submission Period for Counseling Expenses

In some cases, volunteers may not be able to wait until May to be reimbursed for training expenses if they incurred lodging expenses. A State Coordinator may authorize preliminary reimbursement for these expenditures. If authorized, expense claim must be approved by the SC prior to it being submitted to the National Office for processing. In these instances, “Preliminary” should be written on the top of the Expense Statement when it is submitted. This will alert the National Office staff that the expense statement is not a final request and needs special handling.

Instructor Digest, 2006-2007 Season 24

Flat-Rate Or No Reimbursement Using Counselor Flat-Rate Reimburse-ment Forms (CFRs)

Only COU, EROs and CFs who elect Flat-Rate reimbursement will be asked by their supervisor to sign a Counselor Flat-Rate Reimbursement Form (CFR) at the end of the tax season. Flat-Rate Reimbursement is a one-time reimbursement option covering all expenses incurred, including training, counseling, and supplies for the year. No names may be added to the CFR, but address corrections are permitted. CFRs are sent to Local Coordinators at the completion of the process of updating the All Volunteer Roster (see Volunteer Roster & Record Keeping section of this guide.)

Flat-Rate w/o Forms

Any Counselors, EROs and CFs who seek Counselor Flat-Rate, but cannot use the flat rate form, may submit their claim on an expense statement.

Itemized Reimbursement Advance Approval Requirements

All itemized counseling expenses, regardless of the volunteer’s position within the program, require advance approval as well as the after-the-fact approval signatures of the immediate supervisor and the State Coordinator or designee. A State Coordinator will establish a dollar threshold under which state-level advance approval and concurrence signatures are waived.

Expense Form Use

Counselors who wish to itemize expenses will receive a blank expense form from their supervisor at the end of the tax season. Detailed records of all claimed expenses must be provided, along with appropriate supporting receipts or other required documentation. Expense statements that do not provide sufficient detail and receipts will not be processed by the National Office and will be returned.

Meal and Refreshments Expenses Not Reimbursed

Meals and refreshments are not reimbursable for any volunteer (i.e. Counselors, Coordinators and Instructors) during Counselor classes and when counseling at regularly scheduled sites, except in rare cases when the SC authorizes overnight stays. In these rare cases, the SC must also provide his/her approval signature on the expense statement. See the section on Miscellaneous expenses for direction on coverage of “coffee and donut” expenses.

Reimbursable Administrative, Training, & Publicity Expenses

Coordinators, not Counselors, EROs, or CFs, may incur reimbursable administrative, training, and publicity expenses, including:

Travel Copying charges (administrative only, not tax returns) Lodging Meals (except as explained above) Postage Training facilities charges (only with SC approval) Supplies Telephone charges

Instructor Digest, 2006-2007 Season 25

Mileage Claims Mileage claims must be documented by listing each date of travel; the location(s) and the roundtrip mileage. The location and roundtrip mileage is needed only once for repeated trips to and from the same location, but the individual dates must be listed. Be sure to include the total mileage also in these cases. Mileage expense forms that are not filled out correctly will be denied at the National Office and returned; therefore it is important to fill out the expense form with the necessary amount of detail and specificity. EXAMPLE of correctly recorded mileage:

EXAMPLE of incorrectly recorded mileage:

Activity Activity & Location Transportation Cost Code Date (including miles driven) I 2/5 Anytown Library, 10 miles

round trip 1 x 10 = 10 miles (@44.5 cents)

$4.45

I Multiple Anytown High school, 8 miles round trip (Feb 5, 12, 19, 26, Mar 5, 12, 15, 19, April 2, 9) 8 x 10 = 80 miles (@44.5 cents)

$35.60

Total cost $40.05

Activity Activity & Location Transportation Cost Code Date (including miles driven) I Multiple Anytown (Feb, March, April)

Total of 90 miles round trip (@44.5 cents)

$40.05 Total cost $40.05

Instructor Digest, 2006-2007 Season 26

Other Non- Reimbursable Expenses

To ensure that the program efficiently uses its limited financial resources, as well as to comply with AARP or IRS policies, the following expenses are not reimbursable: 1. Mileage for a single shut-in visit that exceeds the reimbursable maximum

of 30 miles per roundtrip. In these instances, the first 30 miles is reimbursable, anything over that will not be reimbursed.

2. Instructor workshop expenses for any attendees exceeding the reimbursable maximum of two per counselor class plus all new instructors.

3. Counselors’ e-file training expenses beyond reasonable local travel costs. 4. Payment of any type for counseling sites. 5. Any automobile expenses other than mileage, parking or tolls

reimbursement. 6. Personal expenses: alcoholic beverages, entertainment, flowers, greeting

cards, personal long distance phone calls. 7. All spousal expenses. 8. Postage for mailing IRS Form 9325 (e-filing acknowledgement) to clients. All necessary program supplies/services are provided to COU, ERO and CF volunteers by the National Office and/or volunteer leadership in your state. As a result, the following are not reimbursable: 1. Books, reference materials, training or training materials. 2. Secretarial services or post office box rental. 3. Any permanent equipment such as: briefcases, calculators, copiers, file

cabinets, pencil sharpeners, staplers, staple removers, computer, printers and computer software.

4. Rental of overhead projectors, movie projectors or VCR's; telephone equipment and installation, except at approved Telephone Counseling Sites (see specific guidelines).

5. Equipment maintenance, repair or supplies, including for computers and printers (consult with supervisor for exceptions), projectors (except bulb), VCR's, etc.

6. Paid publicity. 7. Personalized stationery or business cards.

Instructor Digest, 2006-2007 Season 27

Miscellaneous Expense Clarifications

1. When mileage is excessive and air travel is approved by the SC, mileage, parking, additional motel and meal expenses, as a result of travel by car, are reimbursable only to the extent that they do not exceed the cost of quoted airfare plus transportation to and from the airport. In such instances a copy of the airfare quote should be submitted as supporting documentation.

2. Consistent use of isolated locations is discouraged due to the costs involved. Isolated locations are defined as locations that require the majority of the Counselors working at the site to travel in excess of 30 miles roundtrip to provide services at the designated site. Options available to minimize these costs include: a. Scheduling coverage of the site using teams that are present

several times during the season rather than every day. b. Aligning volunteers and sites more closely (either through finding

sites closer to the pool of volunteers or recruiting volunteers that live closer to the population of tax payers being served.)

c. Exploring the possibility of persons being brought to closer sites using senior vans, carpools, etc.

3. End-of-season functions for recognition of Counselors should be confined to pot-luck, coffee and donuts, or other nominal expenditure affairs. In such instances, when the expense statements are submitted for processing, the number of people attending the function must be recorded. Expenses statements that do not include this information will not be processed. Lunches, buffets, and other expensive gatherings cannot be reimbursed. Mileage to/from these functions is also not reimbursable.

4. “Coffee and donuts” expenses are confined to counselor attended trainings. In such examples, the maximum amount of reimbursement is $1.50 per person for the entire training period. This reimbursement is available for SC, DC, or Instructors only. Receipts are required and the number of counselors in attendance must be noted on the receipts.

5. Expenses of maintaining, repairing and supplying consumables for computers and printers for e-filing may require supervisor, SC and/or TCS approval. Ask first! These items are often purchased nationally and may already be available.

6. The AARP Foundation qualifies to receive state sales tax exemptions in 23 states. If your state qualifies, contact Luisa Chaoui (800) 424-2277 ext. 6005 for an exemption packet and instructions.

7. Booths or exhibits at senior fairs should be combined with other AARP or Foundation activities or limited to nominal expenses not to exceed $25.00.

8. Administrative copies produced on personally-owned equipment may be charged at a cost not to exceed 5¢ per copy or the cost of the paper.

9. Current mileage rate is $0.445 per mile. 10. Current flat rate for Counselors is $35.00 per season. 11. Current flat rate for Coordinators, Instructors, & Specialists is $50.00 per

season.

Instructor Digest, 2006-2007 Season 28

Coordinator, Instructor, Specialist Expenses Leadership Reimburse-ment Options

Leaders seeking reimbursement may elect to take the Leadership Flat-Rate Reimbursement or they may itemize expenses for the year. In either case, expense statements should be completed and submitted to the supervising volunteer. Instructions for completing the expense statements are found on the back of the form, and include the necessary approval procedures. Forms are included in the Administrative Packets and are posted on the Extranet at www.aarp.org/tavolunteers. Leaders are asked to submit their expenses on a timely basis in order to enable a clearer picture of the program costs throughout the year. Ideally, expenses should be submitted in: 1. January (for activities held from October through December), 2. During the regular expense submission process from April 16 through June 30

(for any expense they incur from January until June), and 3. September (for any remaining costs associated with the program).

Leadership Flat-Rate Reimburse-ment

Leadership Flat-Rate Reimbursement is a one-time reimbursement option covering all expenses incurred, including coordinating, training, counseling, and supplies for the year. Leaders who choose this option must submit an expense statement noting the year, "Leadership Flat Rate," the amount, and activity code "C." Leaders who elect the flat-rate reimbursement should not submit any other requests for reimbursement for that year. Flat-rate expense statements must be submitted between April 15 and June 30.

Leadership Itemized Expense Reimburse-ment

The Leadership Itemized Expense Reimbursement option also covers all aspects of AARP Tax-Aide work but requires detailed reporting of activities and submission of receipts for all expenses except mileage. Leaders who choose this option will submit their expenses on an expense statement. Itemized counseling expenses are charged to activity code "I" and may only be submitted after April 15. Expenses related to other activities should be submitted close to the time in which they incurred the expense.

Submitting Leadership Expenses for Reimburse-ment for Itemized Expenses

Leaders should submit itemized expense statements monthly or quarterly to enable a more accurate picture of the costs for the program throughout the year. However, at the most basic, all expenses must be submitted by September 30 (if not done so earlier) because this is the end of the fiscal year for the program. When submitting expenses, they should sign the 4 copies of the form, retain one copy (plus one copy of receipts), affix their own labels to the remaining 3 copies and send them (with one copy of receipts attached on top) to their supervising coordinator for approval. The supervisor will retain one copy of the expense form and forward the remaining 2 copies (along with the supporting receipts) to the National Office for processing. Regardless of activity performed, each volunteer has only one supervising coordinator.

Instructor Digest, 2006-2007 Season 29

Expense Approval Procedures Review Authority

Supervising coordinators review expense statements and CFR forms for accuracy and appropriateness, and ensure that all appropriate receipts are attached and that the receipts support the amount being requested. If all is satisfactory, the supervising coordinators sign, add their own ID number as authorization for payment, and retain a copy. Any expense statements not signed by the supervising coordinator of record as shown on the roster will be returned by the National Office.

Designated Alternate Reviewers

Supervising coordinators who will be unavailable for approvals should designate alternates to sign for them. The alternate writes in the name and ID number of the supervisor of record, and signs his/her own name and ID number underneath. The alternate should retain one copy to send to the supervisor of record.

Personal ID Label

Supervising coordinators receive a supply of personal ID labels. These are to be affixed over the name and ID section of 2 copies of their own expense statements. Coordinators are urged to use these labels to speed the identification and reimbursement process. If no label is available, enter the volunteer's ID number, name and address, and submit the expense statement.

Temporary & Seasonal Addresses

If the reimbursement check is to be mailed to a temporary or seasonal residence, apply the label in the upper left corner of the statement for verification. Write the name and temporary address in the name/address field, checking the "mail check to" box above the field. National Office records must reflect the volunteer's address during tax season.

Counselor Expense Statement Submission

The supervising Coordinator should submit all expense statements for COU, ERO, and CFs in a batch to the National Office. The batch should contain: 1. The CFR form with the signature of each volunteer who is electing the flat rate

reimbursement associated with their position, and 2. Expense statements, with appropriate supporting documentation and receipts (if

electing to receive itemized reimbursement), with the signature of the volunteer and the approval signature of that volunteer’s supervisor.

The batch should be submitted using the 9x12 business reply envelope (B778) and should be submitted between April 15 and June 30.

Advances For Anticipated Expenses

Under special circumstances, when a Leader or a Counselor’s training expenses cannot wait to be reimbursed, an advance may be authorized at the State Coordinator's request. In some cases, Counselors may not be able to wait until May to be reimbursed for counselor training expenses when lodging is involved. A State Coordinator may authorize and must approve preliminary reimbursement for these expenditures. "Preliminary" should be written on the top of the Expense Statement.

Instructor Digest, 2006-2007 Season 30

Insurance Coverage Accident Insurance Who Is Covered The Foundation provides travel accident insurance coverage for AARP Tax-

Aide volunteer for accidental death and dismemberment and medical expenses for any injury incurred while conducting AARP Foundation business directly related to the volunteer position.

Amount of Coverage

Accidental death and dismemberment benefit of $25,000, and a medical expense benefit of up to $3,000 for any injury incurred while conducting authorized program business directly related to the volunteer position.

Supplemental Nature of Coverage

The medical expense benefit is coordinated with Medicare Part A and Part B or an assumed equivalent insurance coverage, regardless of the insured's age. This is a supplement and should not be viewed as a volunteer's primary insurance.

If An Accident Occurs

If any AARP Tax-Aide volunteer sustains an accidental injury while conducting AARP Tax-Aide business, they should notify the AARP travel accident insurance staff through their supervisor and AARP Tax-Aide State Coordinator. Notification, preferably via email, should be sent to:

AARP Insurance and Risk Management Office Attn: Albert Fierro 601 E Street, NW Washington, DC 20049 Email: [email protected]; Phone: (202) 434-3245

Liability Protection Protection By Virtue of TCE Funding

The Introduction and Administrative Guidelines of the IRS Volunteer Assistor’s Guide states that volunteers are not legally liable under federal law for the returns that they prepare.

Volunteer Liability Act of 1997

The Volunteer Protection Act of 1997 (S.543) provides that certified volunteers are not liable for harm caused by an act or omission if they’re acting within the scope of their responsibilities and the harm was not willful.

Certificate of Insurance for Site Liability

The certificate of insurance for site liability outlines that the AARP Foundation will hold harmless the site in accordance with the insurance coverage provided by AARP. If a certificate is needed for a site, contact your District Coordinator.

Instructor Digest, 2006-2007 Season 31

Volunteer Assessment of AARP Tax-Aide Program You are invited to participate in the assessment of the season, and help shape the improvements for next season. Your personal experience is invaluable -- please share it. The two-part assessment form follows. Please fill out each part and give this form to your supervisor by the date in the box below. Your supervisor will consider your views when submitting his/her own assessment. Regional Coordinators’ summaries go to the AARP Tax-Aide national office for national compilation and reporting back to all program coordinators via Happenings. From: (your name)_____________________________________________________________________ (your title & state)________________________________________________________________ To: (supervisor name)________________________________________________________________ (supervisor title)_________________________________________________________________

Date:______________________________

If your supervisor is a: Local Coordinator

District Coordinator

State Coordinator

Regional Coordinator

Staff Person

Please get this evaluation to him/her by: April 1

April 15

May 1

May 15

May 31

Part 1 Circle appropriate rating numbers All volunteers should rate statements 1 - 14 below. 5 = completely agree 4 = somewhat agree 3= neutral 2 = somewhat disagree 1 = completely disagree.

Disagre Agree

1 Program goals are clearly stated. 1 2 3 4 5 2 The program is well publicized. 1 2 3 4 5 3 Volunteers are well trained. 1 2 3 4 5 4 Testing & certification are consistent & fair. 1 2 3 4 5 5 IRS provides adequate support. 1 2 3 4 5 6 Information is communicated as & when needed. 1 2 3 4 5 7 Materials, forms & supplies are sufficient. 1 2 3 4 5 8 Necessary equipment is available. 1 2 3 4 5 9 Counseling sites are well managed. 1 2 3 4 5 10 Counseling sites have enough counselors. 1 2 3 4 5 11 All tax returns are quality reviewed. 1 2 3 4 5 12 Reports (Summary Activity Reports and Expense) are

submitted accurately & timely1 2 3 4 5

13 Sites are monitored & helped as needed. 1 2 3 4 5 14 Supervisors recognize volunteers’ service. 1 2 3 4 5

See Part II on the reverse side! E 306 (997)

Instructor Digest, 2006-2007 Season 32

Part II (to be completed by all volunteers) 1. What worked well? (describe innovations, successes, goals that were attained) 2. What did not work well? (describe problems that you need help in solving, goals that were not

attained) 3. What new group of taxpayers did you serve? 4. What support do you need? (e.g., training in _______________, communication, publicity,

supplies, equipment, etc.) 5. Specific ideas for program improvement: (e.g., how to reach more customers, bring in more

volunteers, improve training) 6. Other: (let off steam or brag about someone or something) 7. Specific actions I will take to improve AARP Tax-Aide service in my territory or

area of responsibility: 8. Counselors only: If a leadership position -- coordinator, instructor , or both-- were

available, would you be interested in serving?

Yes _____ ___Coordinator No_____ ___Instructor

Thank you for your contribution!

Instructor Digest, 2006-2007 Season 33

Appendix A – Additional Issues

Volunteer Instructor Guide (Pub 1155) incorporates an integrated training approach in Appendix A. This supplemental guidance “integrates” or weaves in tax law with return preparation software. The training is composed of ten modules of instruction. At the conclusion of the training, all lessons Publication 678 will be have been taught. Student information and exercises are in Publication 678, Appendix A. AARP Tax-Aide’s Extranet provides Management Guides, forms and other support documents to AARP Tax-Aide volunteers who have access to the Internet. The address is: www.aarp.org/tavolunteers (this web address is case sensitive). Volunteers may prepare amended (1040X) and military returns only if they are trained to do so. AARP Tax-Aide TRS and trainers can use the Pub 678 Military Supplement, as well as the instructions for the 1040X Form, to train volunteers on these topics if needed at specific AARP Tax-Aide sites. SC, DCs or Instructors can now be reimbursed UP TO $1.50 per Counselor per training session for coffee or any other light refreshment (not per day, a one-time reimbursement only of $1.50 per Counselor attending training period). RECEIPTS ARE REQUIRED.