Infrastructure Finance Fundamentals (ADN Capital Ventures)

25

Infrastructure Finance Fundamentals Adam Nicolopoulos, President and CEO February 21, 2012

-

Upload

adam-nicolopoulos -

Category

Documents

-

view

854 -

download

9

Transcript of Infrastructure Finance Fundamentals (ADN Capital Ventures)

Infrastructure Finance Fundamentals

Adam Nicolopoulos, President and CEO

February 21, 2012

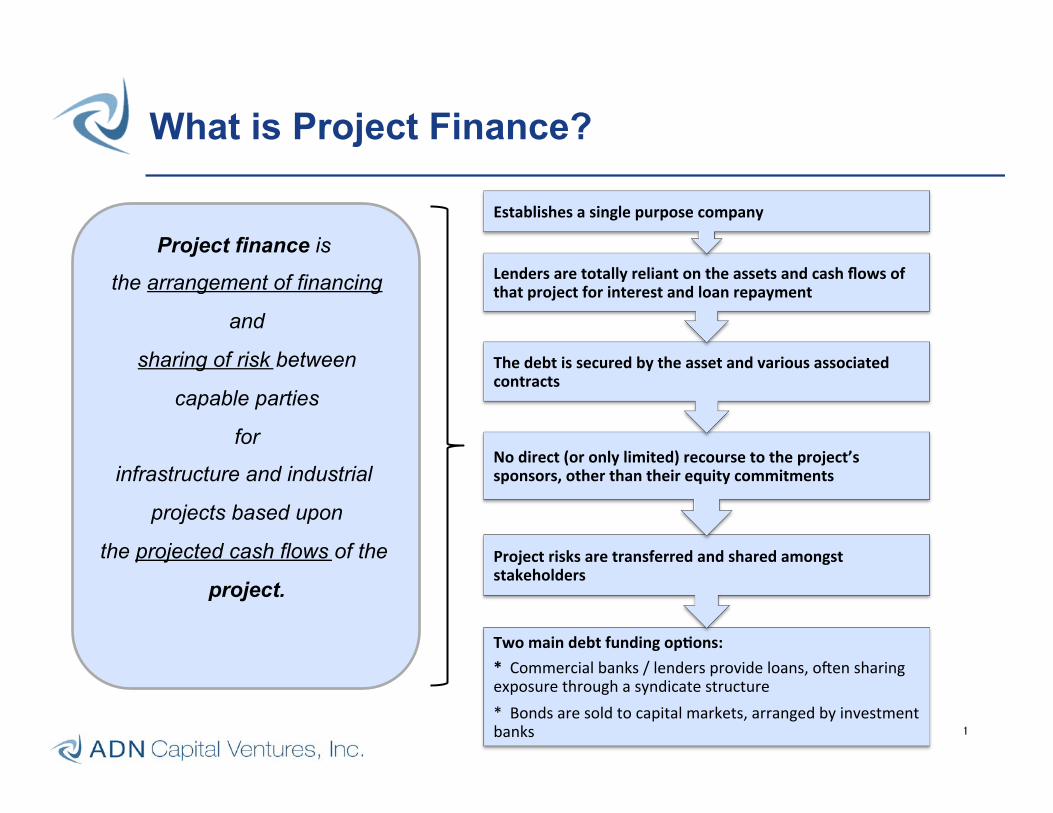

Two main debt funding op�ons: * Commercial banks / lenders provide loans, o�en sharing exposure through a syndicate structure * Bonds are sold to capital markets, arranged by investment banks

Project risks are transferred and shared amongst stakeholders

No direct (or only limited) recourse to the project’s sponsors, other than their equity commitments

The debt is secured by the asset and various associated contracts

Lenders are totally reliant on the assets and cash flows of that project for interest and loan repayment

Establishes a single purpose company

1

What is Project Finance?

Project finance is

the arrangement of financing

and

sharing of risk between

capable parties

for

infrastructure and industrial

projects based upon

the projected cash flows of the

project.

2

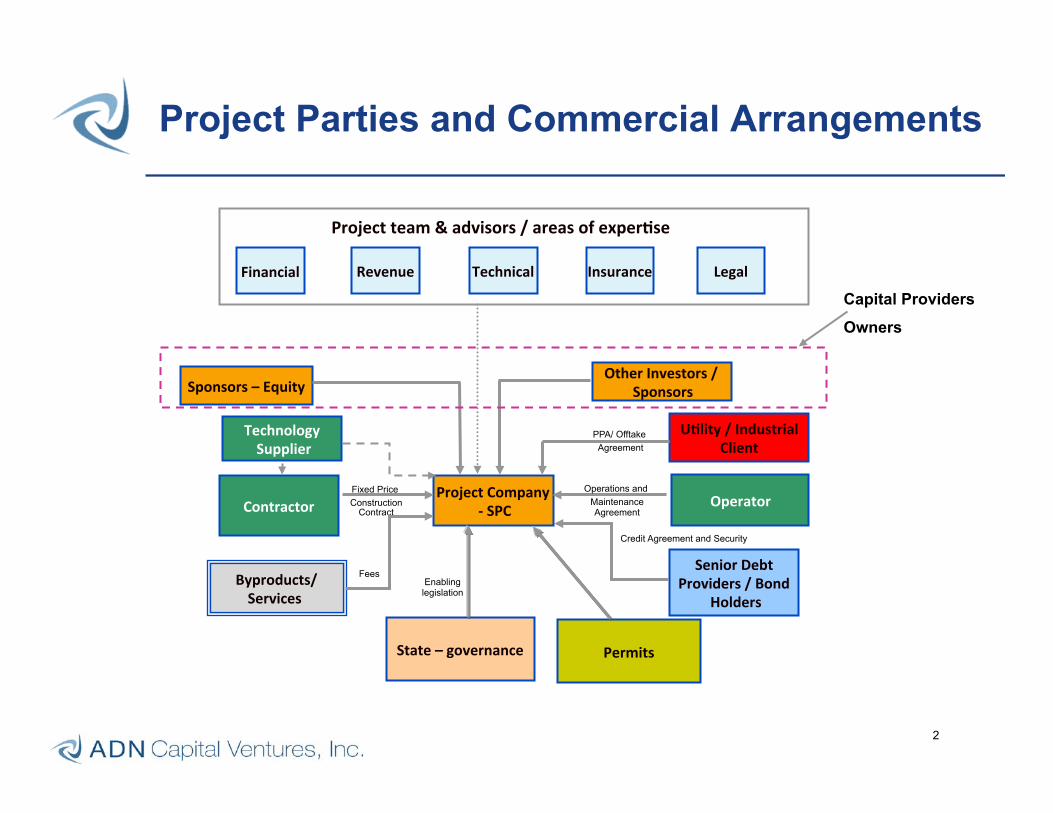

Project Company -‐ SPC Operator

Operations and

Maintenance Agreement Contractor

Technology Supplier

Byproducts/ Services

Fixed Price Construction

Contract

Fees

State – governance

Senior Debt Providers / Bond

Holders

Credit Agreement and Security

Enabling

legislation

Sponsors – Equity Other Investors /

Sponsors

Financial Revenue Insurance Technical Legal

U�lity / Industrial Client

PPA/ Offtake Agreement

Permits

Project team & advisors / areas of exper�se

Capital Providers

Owners

Project Parties and Commercial Arrangements

3

Project Finance is about Sharing Risks

♦ Transfers risk to the private sector / off-loads responsibilities and obligations

– Development – Construction – Operation – Maintenance – Financing

♦ Brings off-balance-sheet financing

♦ Focuses on life-cycle costs

♦ Introduces private sector disciplines (management, efficiencies, innovation, value engineering)

♦ Improves operating and management efficiencies

construction

operation financing

maintenance

4

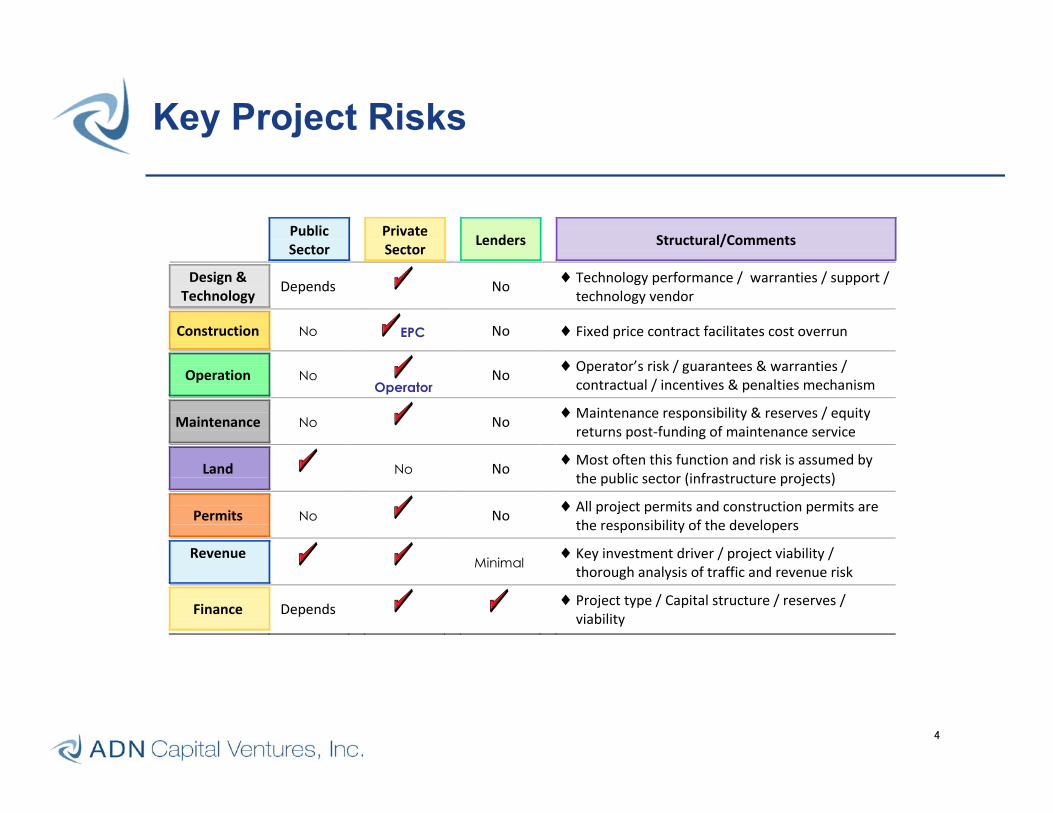

Public Sector

Private Sector

Lenders Structural/Comments

Design & Technology Depends No

♦ Technology performance / warranties / support / technology vendor

Construction No EPC No

♦ Fixed price contract facilitates cost overrun

Operation No

Operator No

♦ Operator’s risk / guarantees & warranties / contractual / incentives & penalties mechanism

Maintenance No No

♦ Maintenance responsibility & reserves / equity returns post-‐funding of maintenance service

Land No No

♦ Most often this function and risk is assumed by the public sector (infrastructure projects)

Permits No No

♦ All project permits and construction permits are the responsibility of the developers

Revenue

Minimal ♦ Key investment driver / project viability /

thorough analysis of traffic and revenue risk

Finance Depends ♦ Project type / Capital structure / reserves /

viability

Key Project Risks

5

(800)

(600)

(400)

(200)

0

200

400

600

800

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30

year of concession

Mill

ions

of U

S$

nom

inal

Opex Capex

Senior debt interest & fees Senior debt repayment

Dividends Tax

Equity subscribed Debt drawdown

Total Revenues

Typical Cash Flow Profile

Requirements for Private Participation

Category Definition

Definition Tightly-bound, ironclad definition of project with good & clean limits

Size Large enough to attract strong international interest, but not so large as to force need for large bidding groups, thus limiting competition

Timeframe Adequate to bring project to completion – balanced, sufficient time to organize tender competition but short enough to maintain high level of bidder interest

Skill-sets Should not require extensive skillsets – avoid complex, extensive multi-purpose projects that require expensive and diverse skills

Interfaces Complex project structure and inter-organizational agreements take longer to implement than simpler networks

“Financeability” Avoid projects with unproven technology, significant business risks, complex implementation techniques, etc.

Regulation Required to establish project privatization with defined mechanisms on setting tariffs. Legal framework for the Government to regulate and monitor PPP performance

Technical Factors Wealth of technical data available for more efficient monetization

Land &Permits Clear definition of ownership of land, right of way and permitting process

Competition From other projects or sectors

6

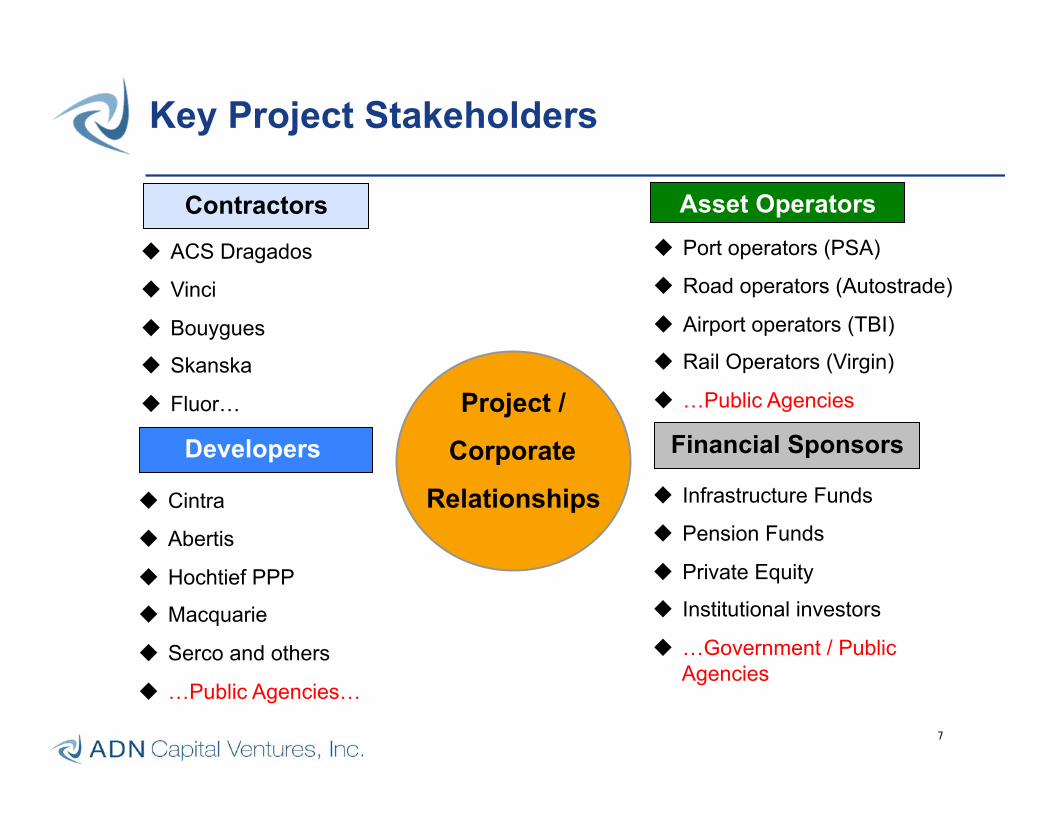

7

Contractors

u ACS Dragados

u Vinci

u Bouygues

u Skanska

u Fluor…

Asset Operators u Port operators (PSA)

u Road operators (Autostrade)

u Airport operators (TBI)

u Rail Operators (Virgin)

u …Public Agencies

Developers

u Cintra

u Abertis

u Hochtief PPP

u Macquarie

u Serco and others

u …Public Agencies…

Financial Sponsors

u Infrastructure Funds

u Pension Funds

u Private Equity

u Institutional investors

u …Government / Public Agencies

Key Project Stakeholders

Project /

Corporate

Relationships

8

IPO Concession/ BOO(T) Trade sale

JV/strateg ic partner Design-‐Build

Manag ement contract

u Ownership of the asset is widely distributed

u Assets are at a mature stage of developments

u “Politically” and socially more acceptable of the privatization options

u Most common form of privatization

u Contractual arrangement and transfer of the “ rights” to manage, operate and maintain a road

u Suitable for greenfield assets

u An existing road operating company or its assets are sold to corporate investors or joint ventures

u Requires careful drafting of bidding terms

u Suitable for mature assets

u Government retains an interest in the asset (minority)

u Majority interest goes to the private sector

u Public procurement of designed projects

u Private bidding for the construction

u Public ownership and public operation

u Contractor receives a (management) fee from the authority based on performance and implementation of services provided

u Fees and charges are paid by users to the asset authority (government)

Forms of Private Sector Involvement

Private Construction

Public Management

Higher

DBB BT BL BTO DBFO BOT BOO(T)

Private Sector Participation

9

Different Models for Infrastructure Delivery

Public Finance Model - USA PPP / Concession Model

Management

Rating

Debt

Equity

Taxation

IRR/dividends

Cost of Debt

Depreciation

þ

Control of Tolls / User Fees

AA-BBB Mostly BBB

100% 55% - 85%

None or possibly development cost / investment

10-20% optional capital structure

None over 10%+

None Incentives-limited tax holiday(s)

None Yes – depends on asset base

[4.0% – 5.5%] [5.5% – 8.5%]

State / Public Enterprise Private Sector / Regulated

þþ

10 10

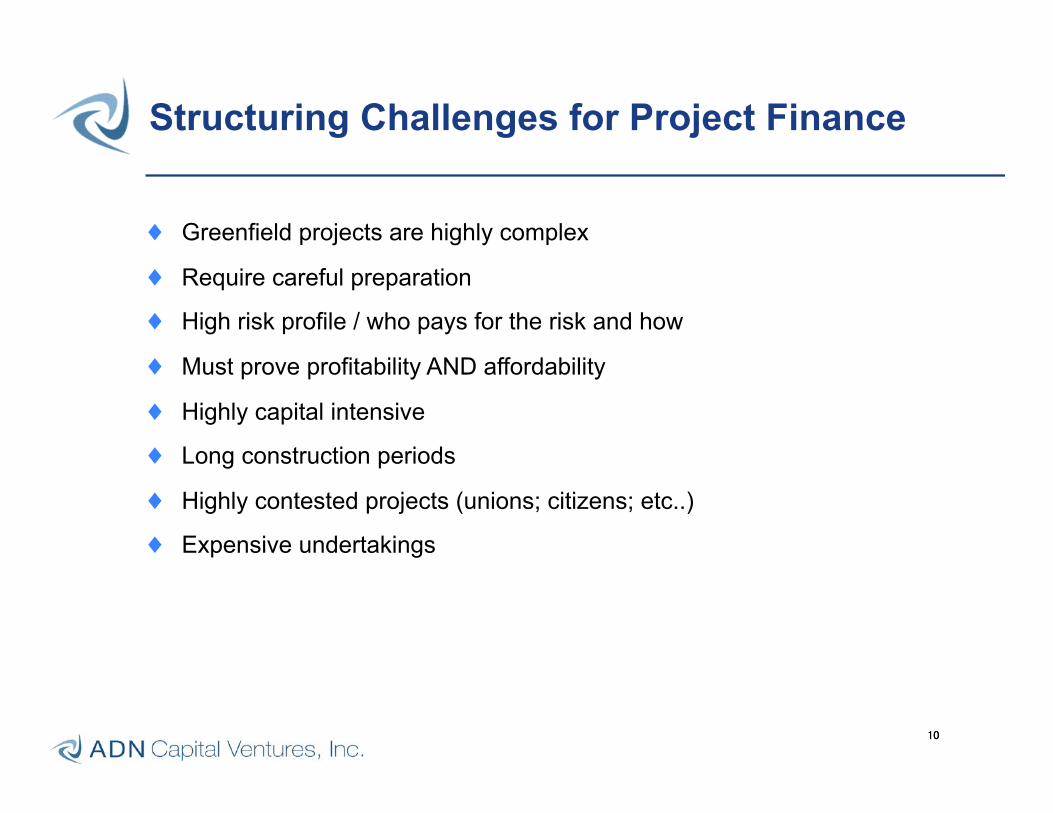

Structuring Challenges for Project Finance

♦ Greenfield projects are highly complex

♦ Require careful preparation

♦ High risk profile / who pays for the risk and how

♦ Must prove profitability AND affordability

♦ Highly capital intensive

♦ Long construction periods

♦ Highly contested projects (unions; citizens; etc..)

♦ Expensive undertakings

11

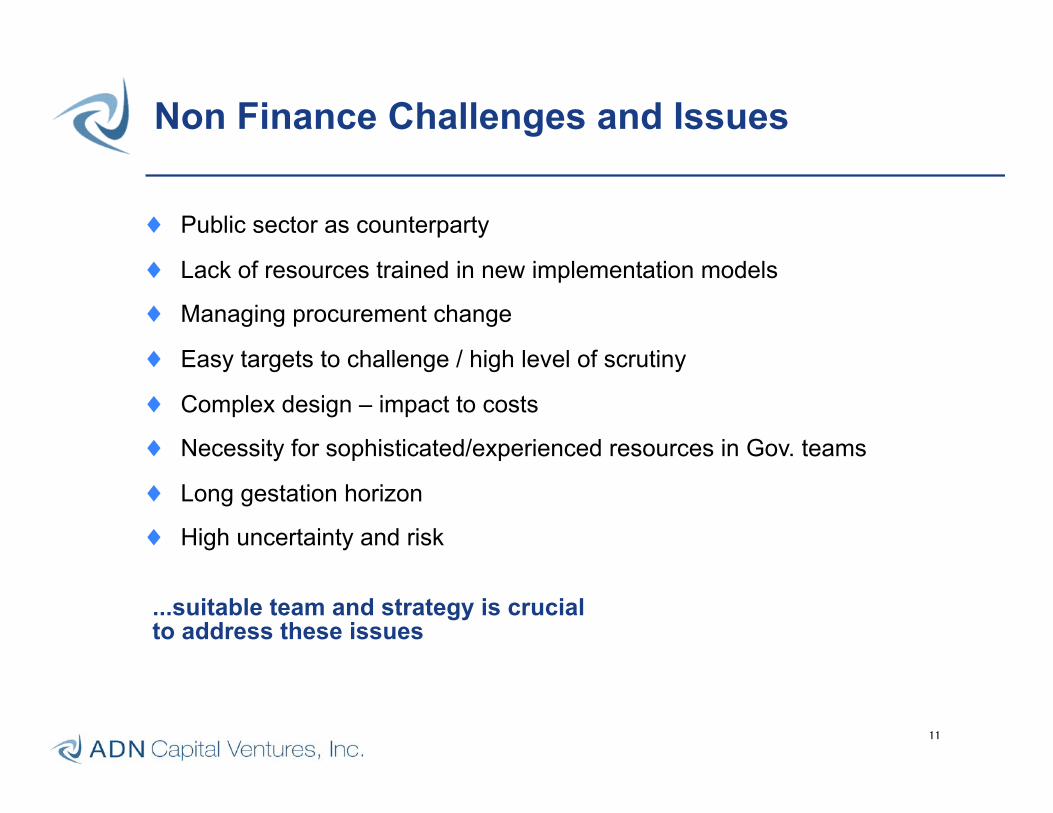

Non Finance Challenges and Issues

♦ Public sector as counterparty

♦ Lack of resources trained in new implementation models

♦ Managing procurement change

♦ Easy targets to challenge / high level of scrutiny

♦ Complex design – impact to costs

♦ Necessity for sophisticated/experienced resources in Gov. teams

♦ Long gestation horizon

♦ High uncertainty and risk

...suitable team and strategy is crucial to address these issues

12

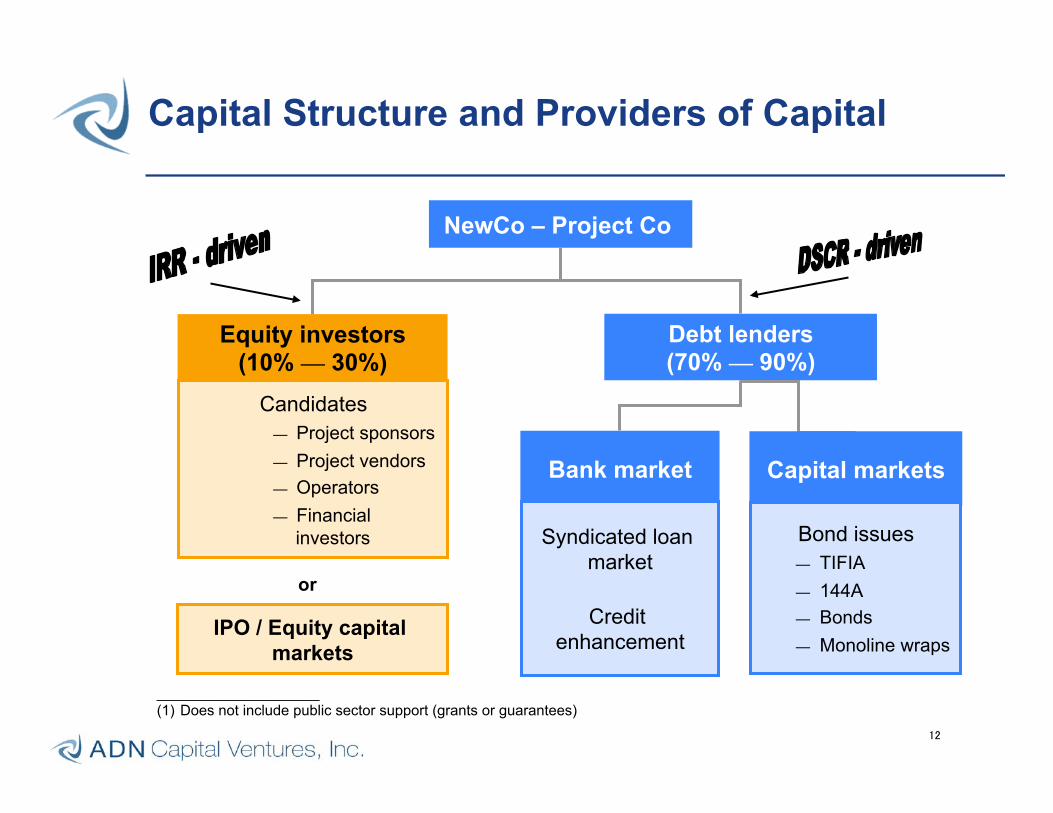

NewCo – Project Co

Debt lenders (70% — 90%)

Equity investors (10% — 30%)

Candidates — Project sponsors — Project vendors — Operators — Financial

investors

IPO / Equity capital markets

or

Bank market

Syndicated loan market

Credit enhancement

Capital markets

Bond issues — TIFIA — 144A — Bonds — Monoline wraps

Capital Structure and Providers of Capital

____________________ (1) Does not include public sector support (grants or guarantees)

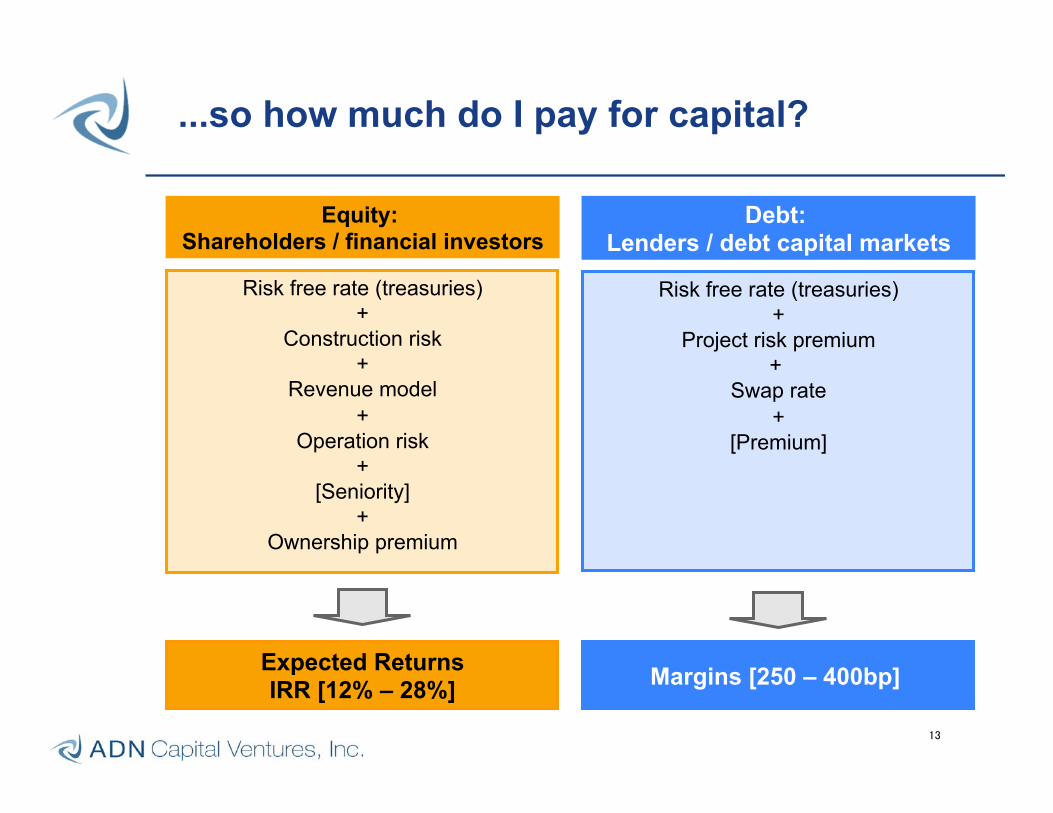

Risk free rate (treasuries) +

Construction risk +

Revenue model +

Operation risk +

[Seniority] +

Ownership premium

Risk free rate (treasuries) +

Project risk premium +

Swap rate +

[Premium]

...so how much do I pay for capital?

Equity: Shareholders / financial investors

Debt: Lenders / debt capital markets

Expected Returns IRR [12% – 28%] Margins [250 – 400bp]

13

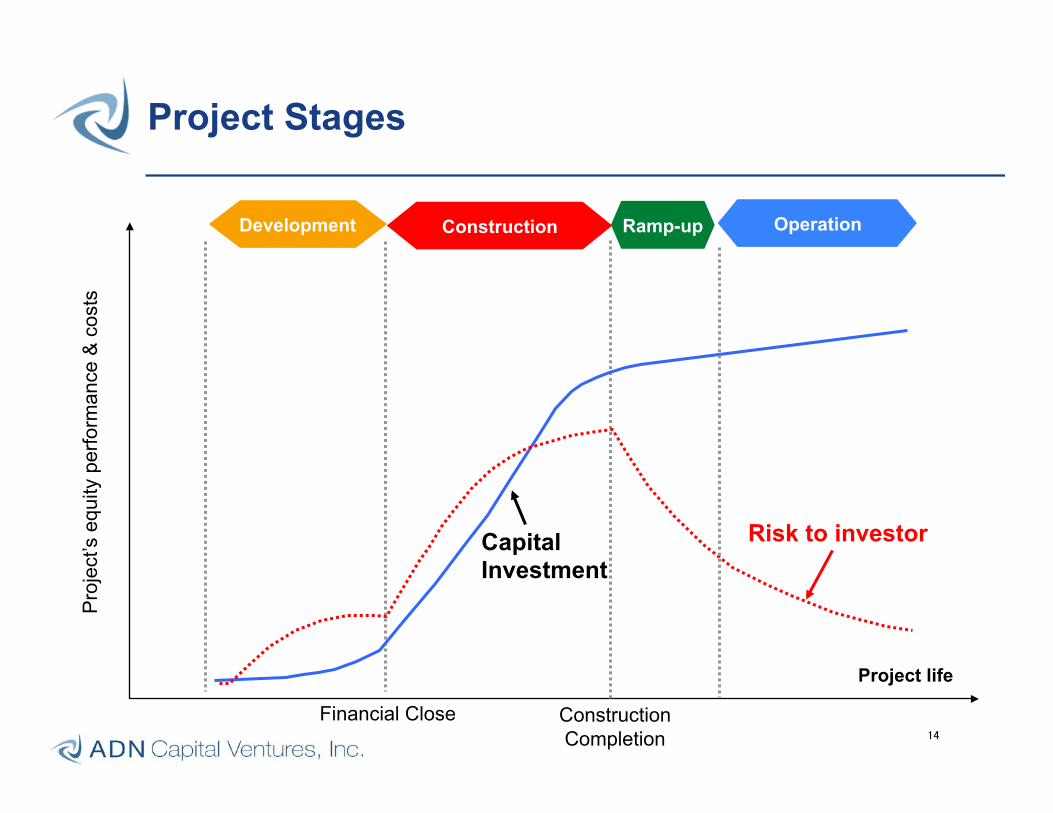

14

Pro

ject

’s e

quity

per

form

ance

& c

osts

Development Construction Operation

Project life

Ramp-up

Capital Investment

Financial Close Construction Completion

Risk to investor

Project Stages

15

Pro

ject

’s e

quity

per

form

ance

& c

osts

Development Construction Operation

Project life

Capital Structure

Equity 20%

[Subsidy 30%]

Debt 50%

Ramp-up

l l

l

Capital Investment

Financial Close Construction Completion

Equity value increased

l

Risk to investor

Project Stages (with Finance Events)

Refinancing

Equity 10-15%

Debt / Bond 85-90%

16

Rationale for Project Equity

♦ …“Skin in the game”…

♦ Economic requirement

♦ Strong management discipline

♦ Accountability on performance

♦ Focus on the “bottom line”

♦ Design innovation

♦ Cost savings over life cycle

♦ EPC – completion on time; on budget and with quality

♦ O&M performance

17

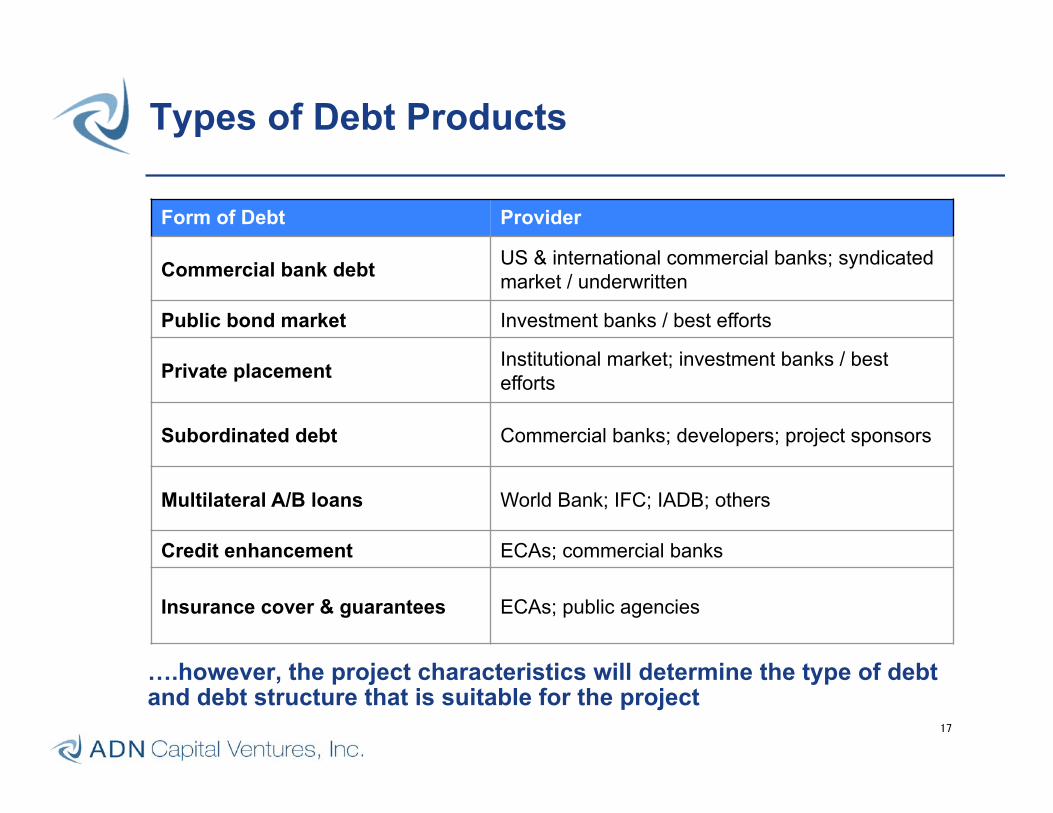

Types of Debt Products

….however, the project characteristics will determine the type of debt and debt structure that is suitable for the project

Form of Debt Provider

Commercial bank debt US & international commercial banks; syndicated market / underwritten

Public bond market Investment banks / best efforts

Private placement Institutional market; investment banks / best efforts

Subordinated debt Commercial banks; developers; project sponsors

Multilateral A/B loans World Bank; IFC; IADB; others

Credit enhancement ECAs; commercial banks

Insurance cover & guarantees ECAs; public agencies

18

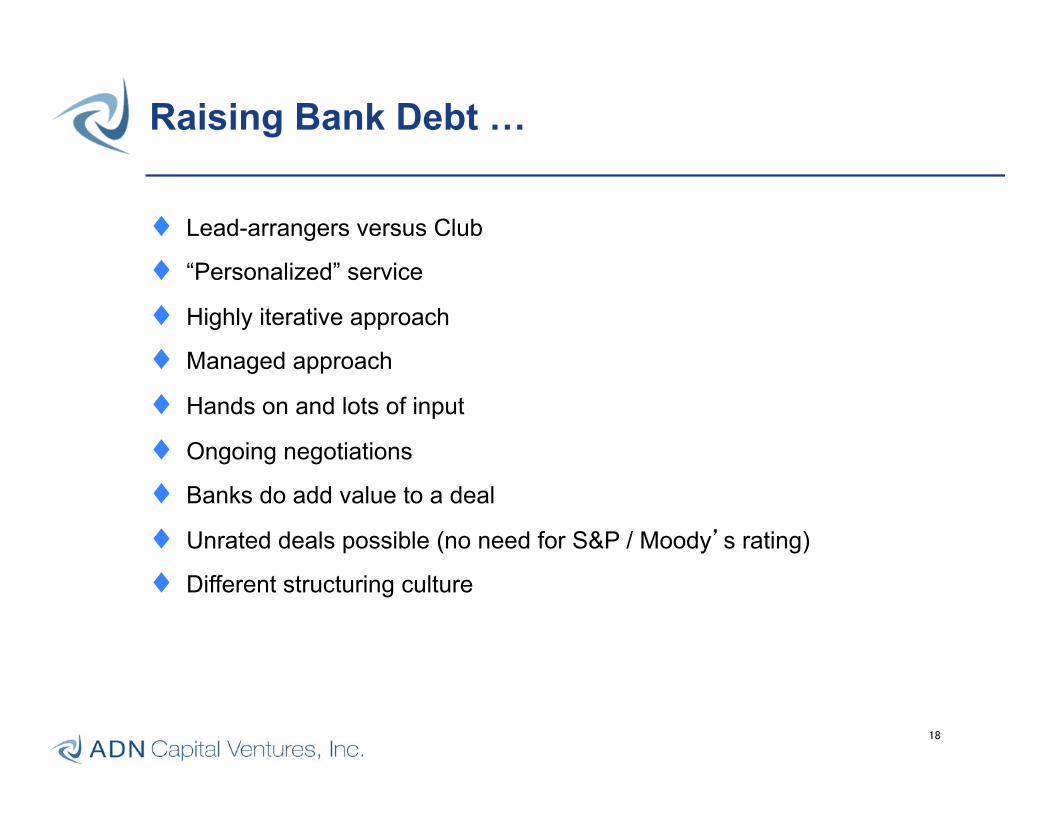

Raising Bank Debt …

♦ Lead-arrangers versus Club

♦ “Personalized” service

♦ Highly iterative approach

♦ Managed approach

♦ Hands on and lots of input

♦ Ongoing negotiations

♦ Banks do add value to a deal

♦ Unrated deals possible (no need for S&P / Moody’s rating)

♦ Different structuring culture

19

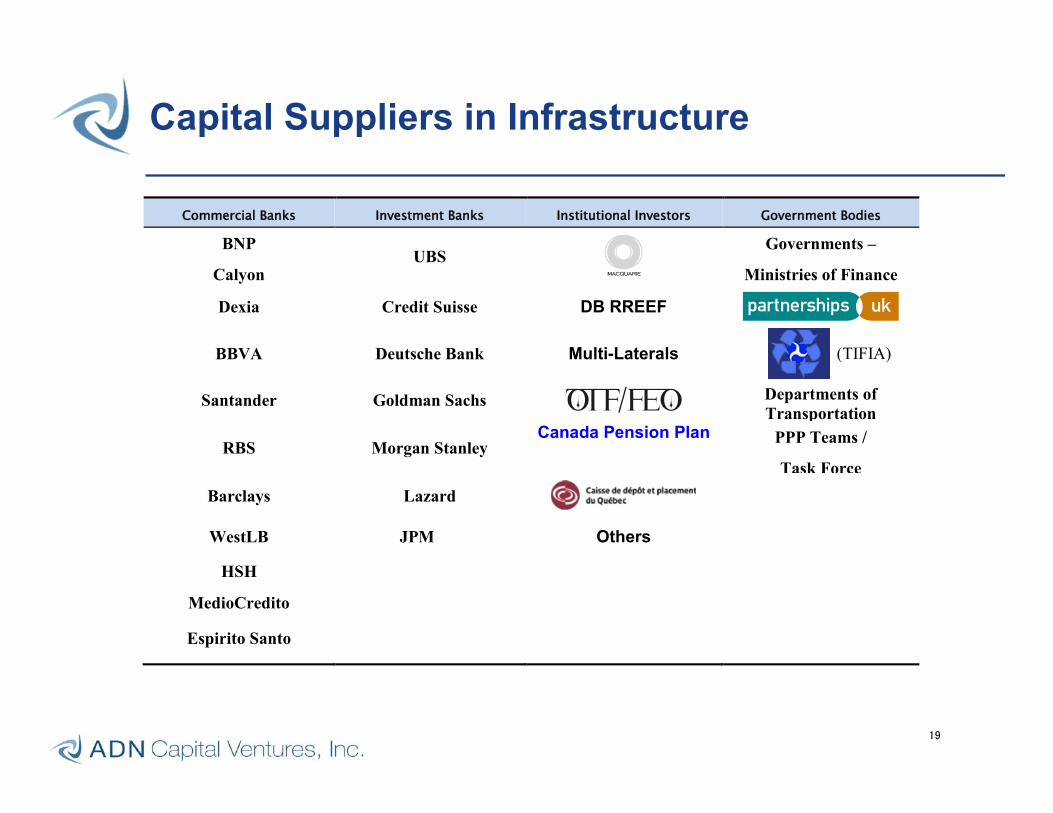

Capital Suppliers in Infrastructure

CCoommmmeerrcciiaall BBaannkkss IInnvveessttmmeenntt BBaannkkss IInnssttiittuuttiioonnaall IInnvveessttoorrss GGoovveerrnnmmeenntt BBooddiieess

BNP

Calyon UBS

Governments –

Ministries of Finance

Dexia Credit Suisse DB RREEF

BBVA Deutsche Bank Multi-Laterals (TIFIA)

Santander Goldman Sachs Departments of Transportation

RBS Morgan Stanley Canada Pension Plan

PPP Teams /

Task Force Barclays Lazard

WestLB JPM Others

HSH

MedioCredito

Espirito Santo

20 20

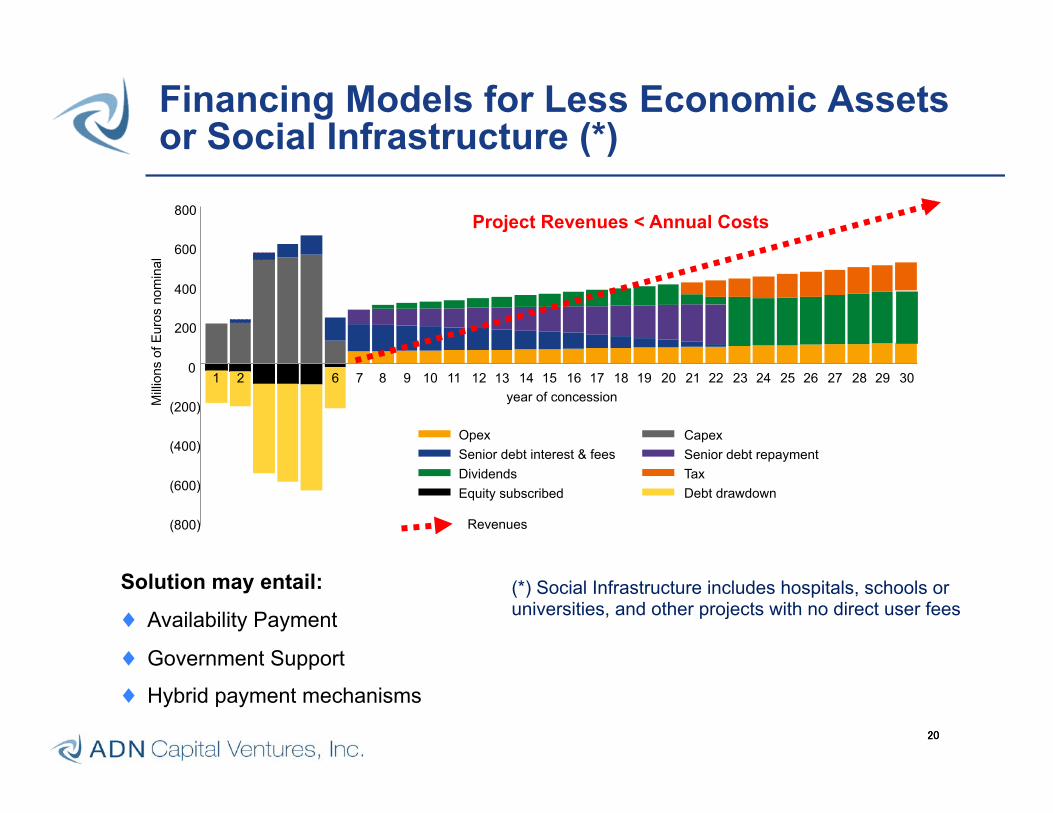

Financing Models for Less Economic Assets or Social Infrastructure (*)

Solution may entail:

♦ Availability Payment

♦ Government Support

♦ Hybrid payment mechanisms

(800)

(600)

(400)

(200)

0

200

400

600

800

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 year of concession M

illio

ns o

f Eur

os n

omin

al

Opex Capex Senior debt interest & fees Senior debt repayment Dividends Tax Equity subscribed Debt drawdown

Revenues

Project Revenues < Annual Costs

(*) Social Infrastructure includes hospitals, schools or universities, and other projects with no direct user fees

21

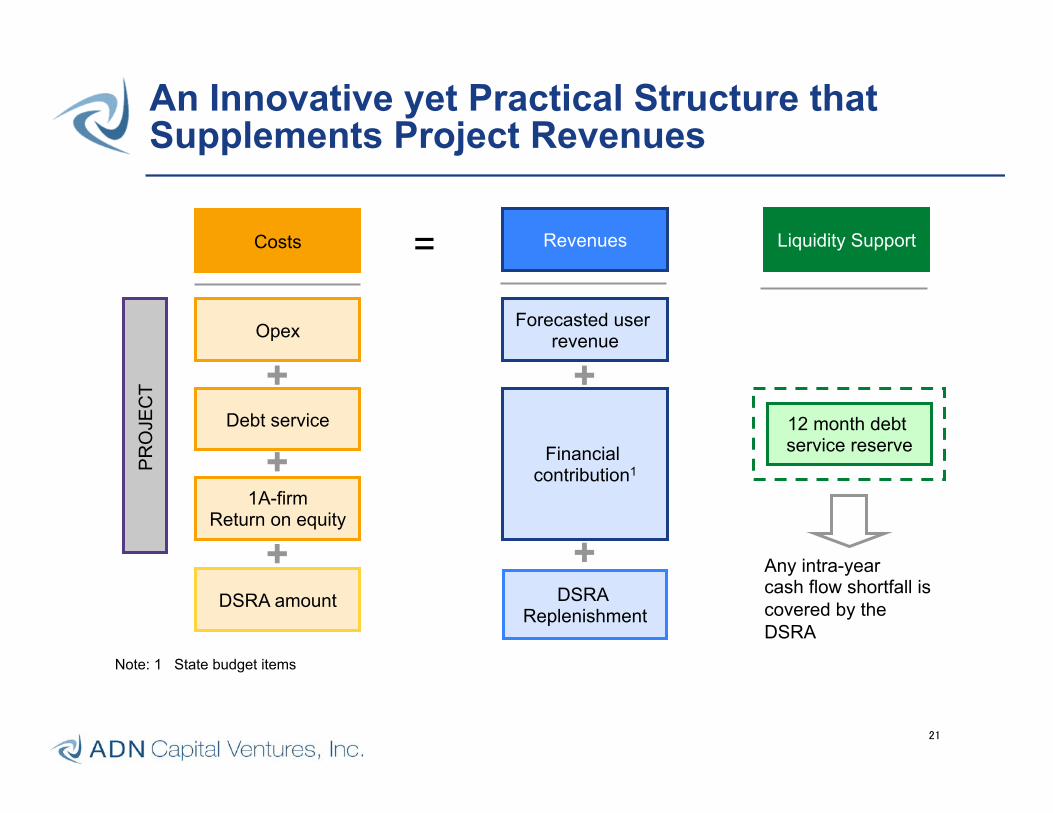

An Innovative yet Practical Structure that Supplements Project Revenues

Note: 1 State budget items

Costs

Opex

Debt service

1A-firm Return on equity

DSRA amount

+

+

+

Revenues

Forecasted user revenue

+

Financial contribution1

DSRA Replenishment

+

PR

OJE

CT

Liquidity Support

12 month debt service reserve

Any intra-year cash flow shortfall is covered by the DSRA

=

22

City Actions for Successful Implementation

♦ Sophisticated management team (leverage private-sector advisors)

♦ Establish clear priorities and objectives (public needs & project aligned)

♦ Maintain transparency throughout the project development

♦ Conduct competitive tender BUT accept unsolicited offers

♦ Mayor’s governance & powers

♦ Create investment incentives (tax deferral, tax holiday, fiscal support)

♦ Standardize tender process

♦ Offer fast track permitting

♦ Stick to the timetable

What have I learned along the way?

23

ü Sound structures that are sustainable (withstand recession)

ü Experienced advisors are worth the money

ü Understand and prioritize objectives

ü Aim for “win-win” among all stakeholders

ü Identify multiple funding options

ü Delays destroy project value ( value of time )

... and…

ü It all about people relationships

24

Scott D. Henderson Director, Finance C40, in partnership with the Clinton Climate Initiative Berkeley, CA 94708 USA Cell: +1 415-548-0099 [email protected] http://live.c40cities.org/

Contacts

Adam Nicolopoulos President and CEO ADN Capital Venture, Inc. 810 College Avenue, Suite 7 Kentfield, California, 94904 USA Office: +1 415-785-4613 Cell: +1 415-246-1765 [email protected] www.adncv.com