INDONESIAN MINING POLICY UPDATE -...

19

bauma FORUM bauma 2013 | 30th International Trade Fair for Construction Machinery, Building Material Machines, Mining Machines, Construction Vehicles and Construction Equipment Munich, April 17 th , 2013 INDONESIAN MINING POLICY UPDATE By: Syawaludin Lubis Director of Environmental Engineering for Mineral and Coal MINISTRY OF ENERGY AND MINERAL RESOURCES

Transcript of INDONESIAN MINING POLICY UPDATE -...

bauma FORUMbauma 2013 | 30th International Trade Fair for Construction Machinery, Building Material Machines, Mining Machines,

Construction Vehicles and Construction Equipment

Munich, April 17th, 2013

INDONESIAN MINING POLICY UPDATE

By:

Syawaludin Lubis

Director of Environmental Engineering for Mineral and Coal

MINISTRY OF ENERGY AND MINERAL RESOURCES

Outline

I. CURRENT CONDITION..........................................................................................

II. POLICY AND REGULATION..................................................................................

III. INVESTMENT OPPORTUNITIES………………………………………………….................

IV. GOVERMENT INCENTIVES AND DISINCENTIVES............................................

V. CLOSING REMARKS............................................................................................

I. CURRENT CONDITION (1)

Demand for energy, materials, water and other key

resources demand is likely to increase rapidly

Indonesia today… …and in 2030

Source: McKinsey Global Institute, 2012

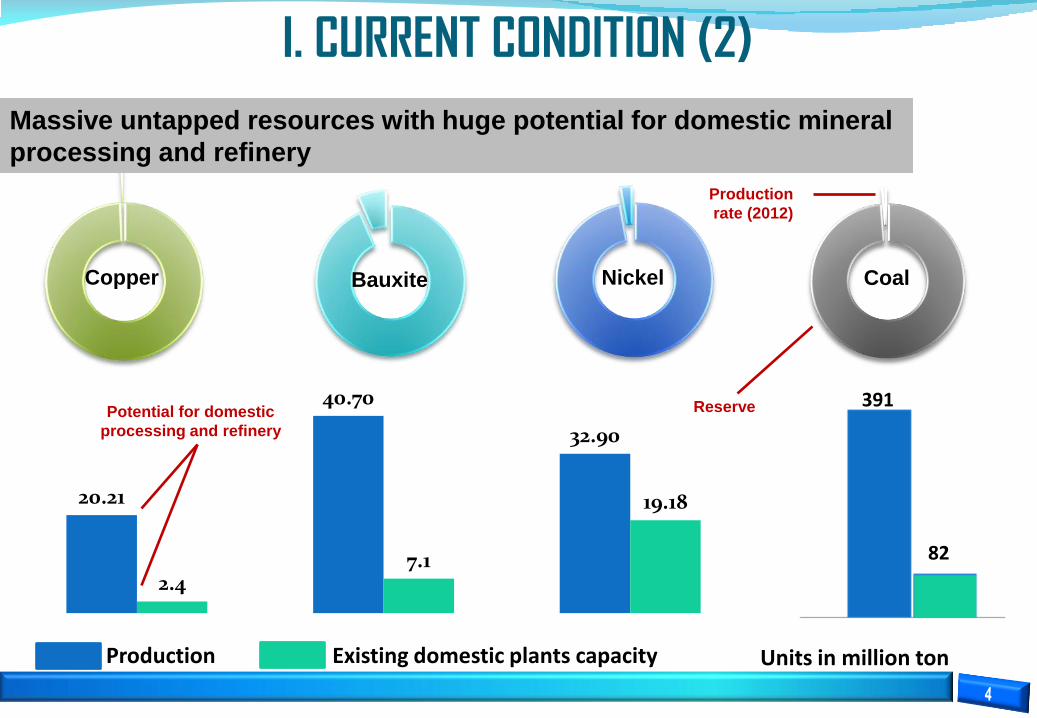

I. CURRENT CONDITION (2)

20.21

40.70

32.90

2.47.1

19.18

Massive untapped resources with huge potential for domestic mineral

processing and refinery

Potential for domestic

processing and refinery

Production Existing domestic plants capacity

391

82

Units in million ton

Copper Bauxite Nickel Coal

Reserve

Production

rate (2012)

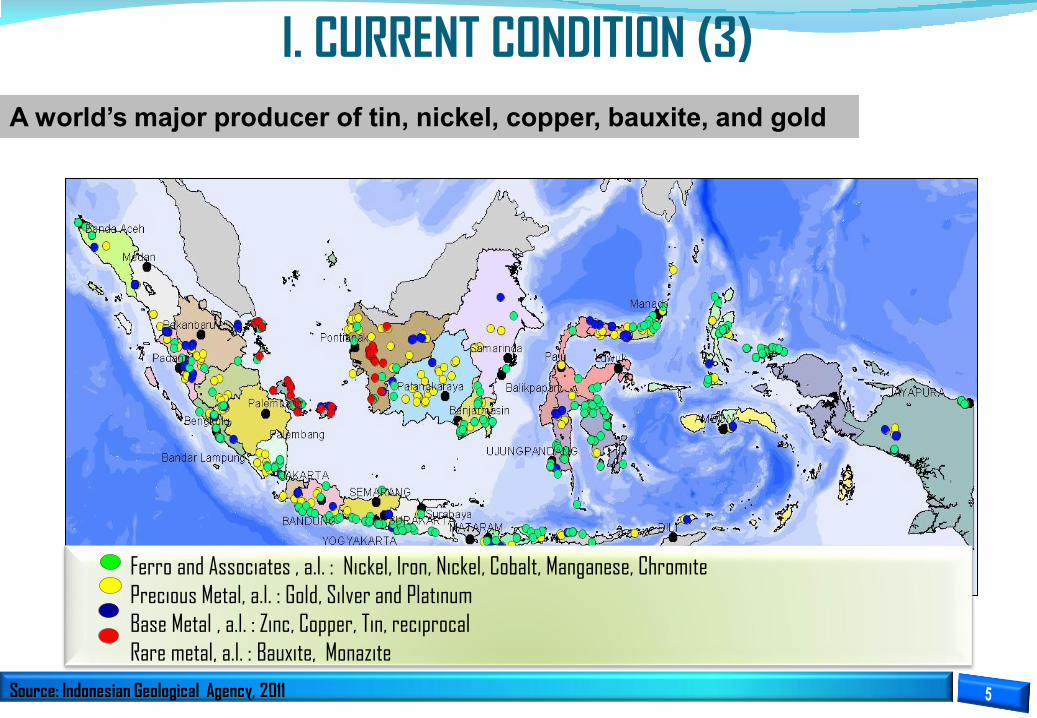

Ferro and Associates , a.l. : Nickel, Iron, Nickel, Cobalt, Manganese, Chromite

Precious Metal, a.l. : Gold, Silver and Platinum

Base Metal , a.l. : Zinc, Copper, Tin, reciprocal

Rare metal, a.l. : Bauxite, Monazite

I. CURRENT CONDITION (3)

Source: Indonesian Geological Agency, 2011

A world’s major producer of tin, nickel, copper, bauxite, and gold

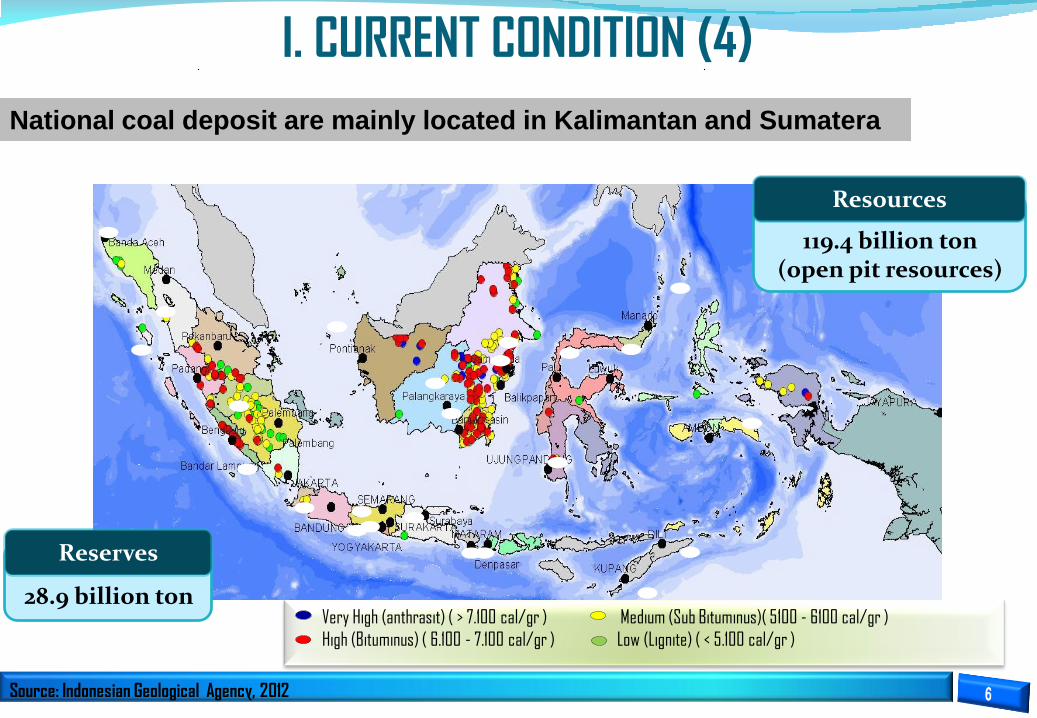

Very High (anthrasit) ( > 7.100 cal/gr ) Medium (Sub Bituminus)( 5100 - 6100 cal/gr )

High (Bituminus) ( 6.100 - 7.100 cal/gr ) Low (Lignite) ( < 5.100 cal/gr )

Source: Indonesian Geological Agency, 2012

I. CURRENT CONDITION (4)

28.9 billion ton

Reserves

119.4 billion ton(open pit resources)

Resources

National coal deposit are mainly located in Kalimantan and Sumatera

MINERALS AND COAL PRODUCTION AND EXPORT (2009-2012)

0

20

40

60

80

2009 2010 2011 2012

Copper (000 ton)

Silver (ton)

Gold (ton)

Tin (000 ton)

Bauxite (mn ton)

Nickel ore (mn ton)

Iron ore (mn ton)

Production

Export

0

200

400

600

800

1000

1200

2009 2010 2011 2012

0

100

200

300

400

500

2009 2010 2011 2012 2013f

mil

lio

n t

on

Domestic use Export

254

275

353

386 391

Coal

Minerals• Indonesia’s overall copper, silver and gold

production were slightly lower during 2010-

2011, however upturn trend seen in 2012

• Significant nickel, bauxite and iron ore

production during 2010-2011 allegedly due to

the ban on exports of raw material in 2014

• Coal production has increased in recent

years in line with the national energy policy

that relies on coal

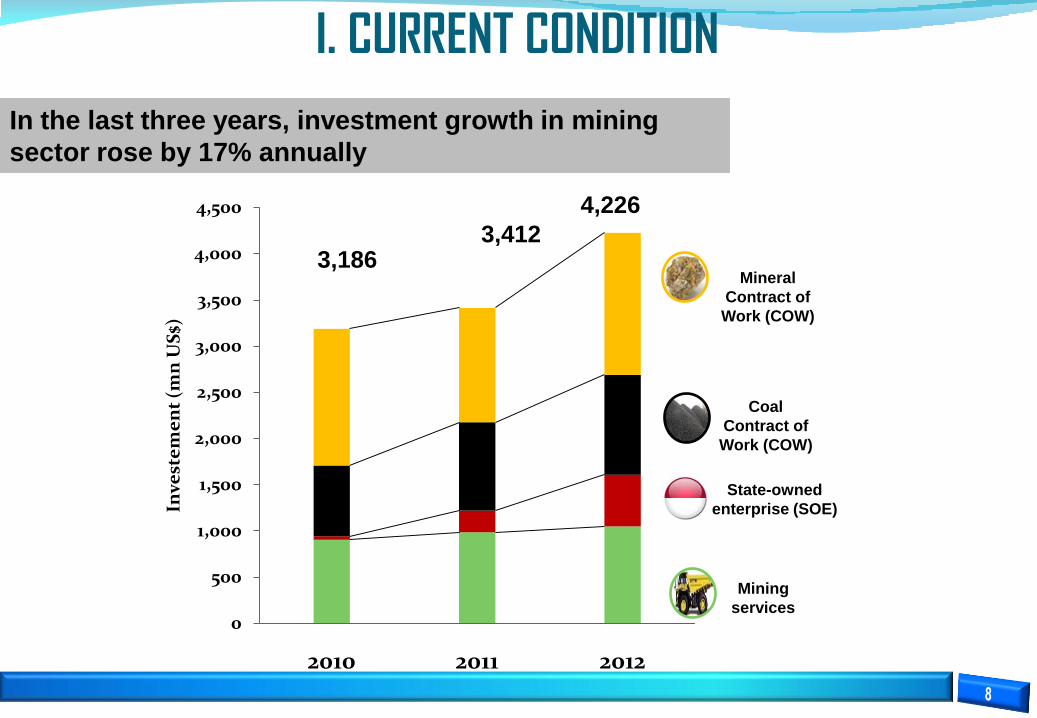

I. CURRENT CONDITION

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

2010 2011 2012

Inve

ste

me

nt

(mn

US

$)

Coal

Contract of

Work (COW)

Mineral

Contract of

Work (COW)

State-owned

enterprise (SOE)

Mining

services

3,1863,412

4,226

In the last three years, investment growth in mining

sector rose by 17% annually

ENERGY AND MINERAL

RESOURCES FOR THE

WELFARE OF THE PEOPLE

II. ROLE OF MINING SECTOR

PRO JOB

(job creation)

PRO GROWTH

(Economic growth)

COMDEV & CSR

PRO POOR

(equitable distribution of income)

GOOD MINING PRACTICE

RECLAMATION & MINE CLOSURE

PRO ENVIRONMENT

(Sustainability and environmentally sound mining)

EMPLOYMENT

LOCAL CONTENT

STATE REVENUE

INVESTMENT

ADDED VALUE

BALANCE OF TRADE

(PRODUCTION, EXPORT,DOMESTIC)

Mining sector has multiple roles in Indonesian economy and serves as a prime-

mover for regional development

II. POLICY AND REGULATION

Law No 4/2009: Mineral and Coal Mining

1945 Constitution

(Art. 33)

Efficient, effective and competitive

mining business activities

Sustainable benefit and

environmentally-sound

mining

Legal certainty in

mining business activities

Domestic market

obligation

Support and develop the

national capability

Source of income and job creation

for local, regional and

state

GR 22/2010:Mining Areas

GR 23/2010:Mining business

activities

GR 55/2010:Direction and Supervision

GR 78/2010:Reclamation and

Mine Closure

GR 24/2012:Review on GR 23/2010

MR 28/2009:Mining Services

MR 34/2009:

DMO

MR 17/2010:Benchmark

Price

MR 12/2011:Mining

Business Areas

MR 7/2012:Mineral

Beneficiation

MR 11/2012:Review on MR 7/2012

Policy

Law

Govt.

Regulation

Minister

Regulation

Constitution

MR 4/2013:Deconcentration

MR 2/2013:Supervision on

Regional Government

MR 12/2011:Mining Commercial Business

Area Determination

New mining law and issuance of key implementing regulations

MR 24/2012:Review on

MR 28/2009

II. POLICY AND REGULATION

Mining Smelting Refining End-User

Concentrate Anodes Cathodes Various

Copper

Mining

Iron ore

• Ore dressing• Agglomeration• Iron making• Steelmaking

casting

• Hot forming

• Cold forming

Finished product

Applications

Iron steel

MiningSmelting

(upstream)Refining

(downstream)

Nickel oreNickel matte ,

FerronickelHigh grade nickel

products

Nickel

DownstreamSmelting

Non Existing Industry

Coal

Upgrading

Active carbonCoking coalGasificationLiquefaction

Conversion

High rank coal

2014

Due date for adjustment to minimum beneficiation process requirement

Without more downstream activities, Indonesia will miss the opportunity to increase

employment and profit margins on the value chain because of the absence of

downstream processing industries

III. INVESTMENT OPPORTUNITIES

• G & G survey• Exploration drilling• Expert consultancy

Exploration Stage

• Expert consultancy• OB removal and handling• Sale and rental of heavy equipment• Tailing and waste management• Power plant development (for processing plant

and mine mouth CFPP)• Transportation

Operations Stage

• Expert consultancy• Reclamation &

mine closure

Mine Closure Stage

Up

stre

am &

su

pp

ort

ing

Do

wn

stre

am

Join the bidding scheme for Commercial Business Area

Coal and Metal

Request for ComercialBusiness Area

Stones and Non Metal

or

Mineral processing and refinery plant

Minerals

• Coal gasification• Coal upgrading • Coal liquefaction

Coal

Apply for transporting and selling special permit

Trading support

Investment opportunities available in all phases of mining activities

IV. INVESTMENT OPPORTUNITIES

Copper processing and refinery plantBauxite processing and refinery plantNickel processing and refinery plant

Development of mineral processing and refinery plant/facility exist throughout the whole

economic corridors which were included in MP3EI

IV. INVESTMENT OPPORTUNITIES

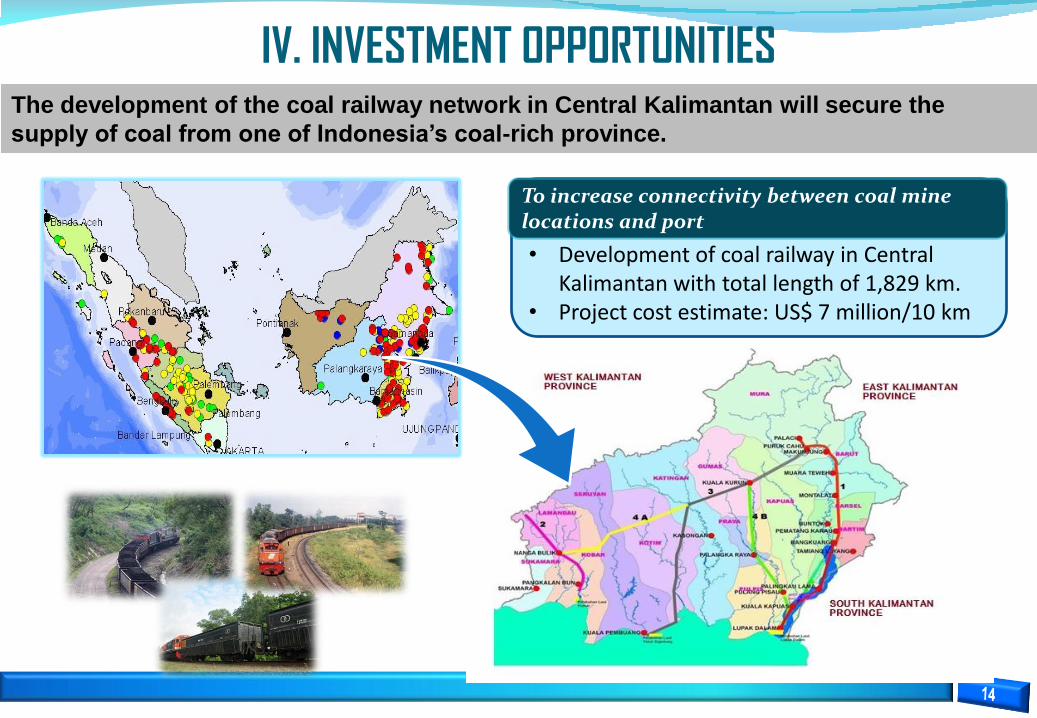

• Development of coal railway in Central Kalimantan with total length of 1,829 km.

• Project cost estimate: US$ 7 million/10 km

To increase connectivity between coal mine locations and port

The development of the coal railway network in Central Kalimantan will secure the

supply of coal from one of Indonesia’s coal-rich province.

Very High (anthrasit) ( > 7.100 cal/gr ) Medium (Sub Bituminus)( 5100 - 6100 cal/gr )

High (Bituminus) ( 6.100 - 7.100 cal/gr ) Low (Lignite) ( < 5.100 cal/gr )

IV. INVESTMENT OPPORTUNITIES

Coal Gasification (US$ 2.5 billion)Coal Upgrading (US$ 1.1 billion)

Coal Upgrading (US$ 2 billion)Coal Blending (US$ 40-50 million)

Coal Blending (US$ 30-40 million)

Coal Blending (US$ 30-40 million)

Kuala Kapuas, Central Kalimantan

East Kutai Timur, East Kalimantan

Samarinda, East Kalimantan

Tanah Bumbu & Tanah Laut, South Kalimantan

Coal beneficiation plant/facility to be built in Kalimantan—the country’s largest coal

producing region

IV. INVESTMENT OPPORTUNITIES

Copper processing and refinery plantBauxite processing and refinery plantNickel processing and refinery plant

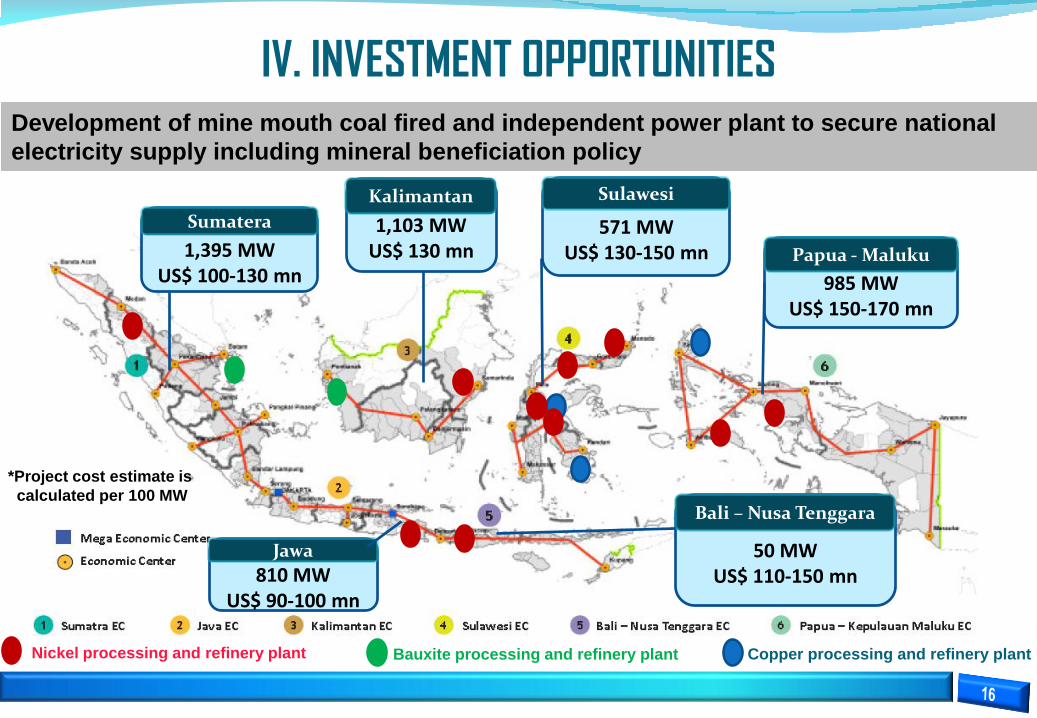

571 MWUS$ 130-150 mn

Sulawesi

985 MWUS$ 150-170 mn

Papua - Maluku

50 MWUS$ 110-150 mn

Bali – Nusa Tenggara

1,103 MWUS$ 130 mn

Kalimantan

810 MWUS$ 90-100 mn

Jawa

1,395 MWUS$ 100-130 mn

Sumatera

*Project cost estimate is

calculated per 100 MW

Development of mine mouth coal fired and independent power plant to secure national

electricity supply including mineral beneficiation policy

IV. INCENTIVES AND DISINCENTIVE

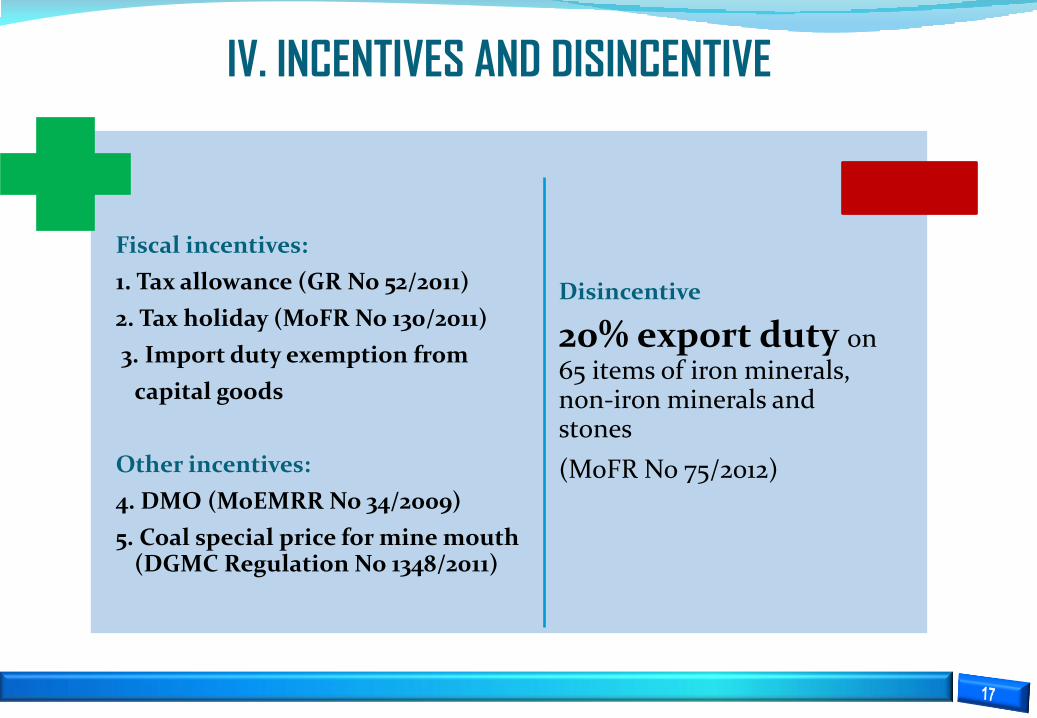

Fiscal incentives:

1. Tax allowance (GR No 52/2011)

2. Tax holiday (MoFR No 130/2011)

3. Import duty exemption from

capital goods

Other incentives:

4. DMO (MoEMRR No 34/2009)

5. Coal special price for mine mouth (DGMC Regulation No 1348/2011)

Disincentive

20% export duty on 65 items of iron minerals, non-iron minerals and stones

(MoFR No 75/2012)

IV. CLOSING REMARKS

1. Indonesia has mineral and coal resources and reserves that still

prospective to be exploited in the future both in the upstream and

mainly to the downstream industry as well.

2. Obligation to increase added value domestically and supporting

regulations provide opportunity for establihsment of mineral

processing and refining plant in Indonesia.

3. Indonesia still needs big investment to develop the potency on

mineral and coal and encourages all private investment,

especially for mineral and coal processing and refinery.

www.djmbp.esdm.go.id