India Research Banking -...

43

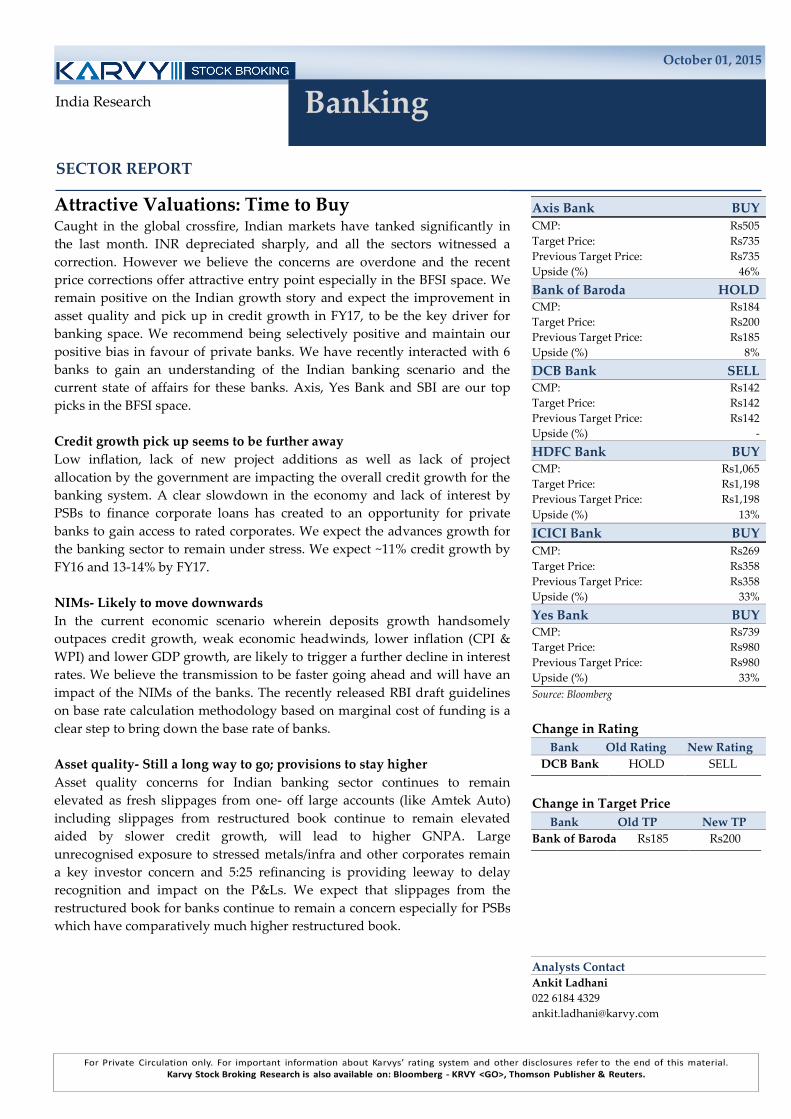

October 01, 2015 Banking India Research SECTOR REPORT Axis Bank BUY CMP: Rs505 Target Price: Rs735 Previous Target Price: Rs735 Upside (%) 46% Bank of Baroda HOLD CMP: Rs184 Target Price: Rs200 Previous Target Price: Rs185 Upside (%) 8% DCB Bank SELL CMP: Rs142 Target Price: Rs142 Previous Target Price: Rs142 Upside (%) - HDFC Bank BUY CMP: Rs1,065 Target Price: Rs1,198 Previous Target Price: Rs1,198 Upside (%) 13% ICICI Bank BUY CMP: Rs269 Target Price: Rs358 Previous Target Price: Rs358 Upside (%) 33% Yes Bank BUY CMP: Rs739 Target Price: Rs980 Previous Target Price: Rs980 Upside (%) 33% Source: Bloomberg Change in Rating Bank Old Rating New Rating DCB Bank HOLD SELL Change in Target Price Bank Old TP New TP Bank of Baroda Rs185 Rs200 Analysts Contact Ankit Ladhani 022 6184 4329 [email protected] Attractive Valuations: Time to Buy Caught in the global crossfire, Indian markets have tanked significantly in the last month. INR depreciated sharply, and all the sectors witnessed a correction. However we believe the concerns are overdone and the recent price corrections offer attractive entry point especially in the BFSI space. We remain positive on the Indian growth story and expect the improvement in asset quality and pick up in credit growth in FY17, to be the key driver for banking space. We recommend being selectively positive and maintain our positive bias in favour of private banks. We have recently interacted with 6 banks to gain an understanding of the Indian banking scenario and the current state of affairs for these banks. Axis, Yes Bank and SBI are our top picks in the BFSI space. Credit growth pick up seems to be further away Low inflation, lack of new project additions as well as lack of project allocation by the government are impacting the overall credit growth for the banking system. A clear slowdown in the economy and lack of interest by PSBs to finance corporate loans has created to an opportunity for private banks to gain access to rated corporates. We expect the advances growth for the banking sector to remain under stress. We expect ~11% credit growth by FY16 and 13-14% by FY17. NIMs- Likely to move downwards In the current economic scenario wherein deposits growth handsomely outpaces credit growth, weak economic headwinds, lower inflation (CPI & WPI) and lower GDP growth, are likely to trigger a further decline in interest rates. We believe the transmission to be faster going ahead and will have an impact of the NIMs of the banks. The recently released RBI draft guidelines on base rate calculation methodology based on marginal cost of funding is a clear step to bring down the base rate of banks. Asset quality- Still a long way to go; provisions to stay higher Asset quality concerns for Indian banking sector continues to remain elevated as fresh slippages from one- off large accounts (like Amtek Auto) including slippages from restructured book continue to remain elevated aided by slower credit growth, will lead to higher GNPA. Large unrecognised exposure to stressed metals/infra and other corporates remain a key investor concern and 5:25 refinancing is providing leeway to delay recognition and impact on the P&Ls. We expect that slippages from the restructured book for banks continue to remain a concern especially for PSBs which have comparatively much higher restructured book.

Transcript of India Research Banking -...

October 01, 2015

Banking

India Research

SECTOR REPORT

Axis Bank BUY

CMP: Rs505

Target Price: Rs735

Previous Target Price: Rs735

Upside (%) 46%

Bank of Baroda HOLD CMP: Rs184

Target Price: Rs200

Previous Target Price: Rs185

Upside (%) 8%

DCB Bank SELL CMP: Rs142

Target Price: Rs142

Previous Target Price: Rs142

Upside (%) -

HDFC Bank BUY CMP: Rs1,065

Target Price: Rs1,198

Previous Target Price: Rs1,198

Upside (%) 13%

ICICI Bank BUY

CMP: Rs269

Target Price: Rs358

Previous Target Price: Rs358

Upside (%) 33%

Yes Bank BUY CMP: Rs739

Target Price: Rs980

Previous Target Price: Rs980

Upside (%) 33%

Source: Bloomberg

Change in Rating

Bank Old Rating New Rating

DCB Bank HOLD SELL

Change in Target Price

Bank Old TP New TP

Bank of Baroda Rs185 Rs200

Analysts Contact

Ankit Ladhani

022 6184 4329

Attractive Valuations: Time to Buy Caught in the global crossfire, Indian markets have tanked significantly in

the last month. INR depreciated sharply, and all the sectors witnessed a

correction. However we believe the concerns are overdone and the recent

price corrections offer attractive entry point especially in the BFSI space. We

remain positive on the Indian growth story and expect the improvement in

asset quality and pick up in credit growth in FY17, to be the key driver for

banking space. We recommend being selectively positive and maintain our

positive bias in favour of private banks. We have recently interacted with 6

banks to gain an understanding of the Indian banking scenario and the

current state of affairs for these banks. Axis, Yes Bank and SBI are our top

picks in the BFSI space.

Credit growth pick up seems to be further away

Low inflation, lack of new project additions as well as lack of project

allocation by the government are impacting the overall credit growth for the

banking system. A clear slowdown in the economy and lack of interest by

PSBs to finance corporate loans has created to an opportunity for private

banks to gain access to rated corporates. We expect the advances growth for

the banking sector to remain under stress. We expect ~11% credit growth by

FY16 and 13-14% by FY17.

NIMs- Likely to move downwards

In the current economic scenario wherein deposits growth handsomely

outpaces credit growth, weak economic headwinds, lower inflation (CPI &

WPI) and lower GDP growth, are likely to trigger a further decline in interest

rates. We believe the transmission to be faster going ahead and will have an

impact of the NIMs of the banks. The recently released RBI draft guidelines

on base rate calculation methodology based on marginal cost of funding is a

clear step to bring down the base rate of banks.

Asset quality- Still a long way to go; provisions to stay higher

Asset quality concerns for Indian banking sector continues to remain

elevated as fresh slippages from one- off large accounts (like Amtek Auto)

including slippages from restructured book continue to remain elevated

aided by slower credit growth, will lead to higher GNPA. Large

unrecognised exposure to stressed metals/infra and other corporates remain

a key investor concern and 5:25 refinancing is providing leeway to delay

recognition and impact on the P&Ls. We expect that slippages from the

restructured book for banks continue to remain a concern especially for PSBs

which have comparatively much higher restructured book.

2

October 01, 2015

Banking

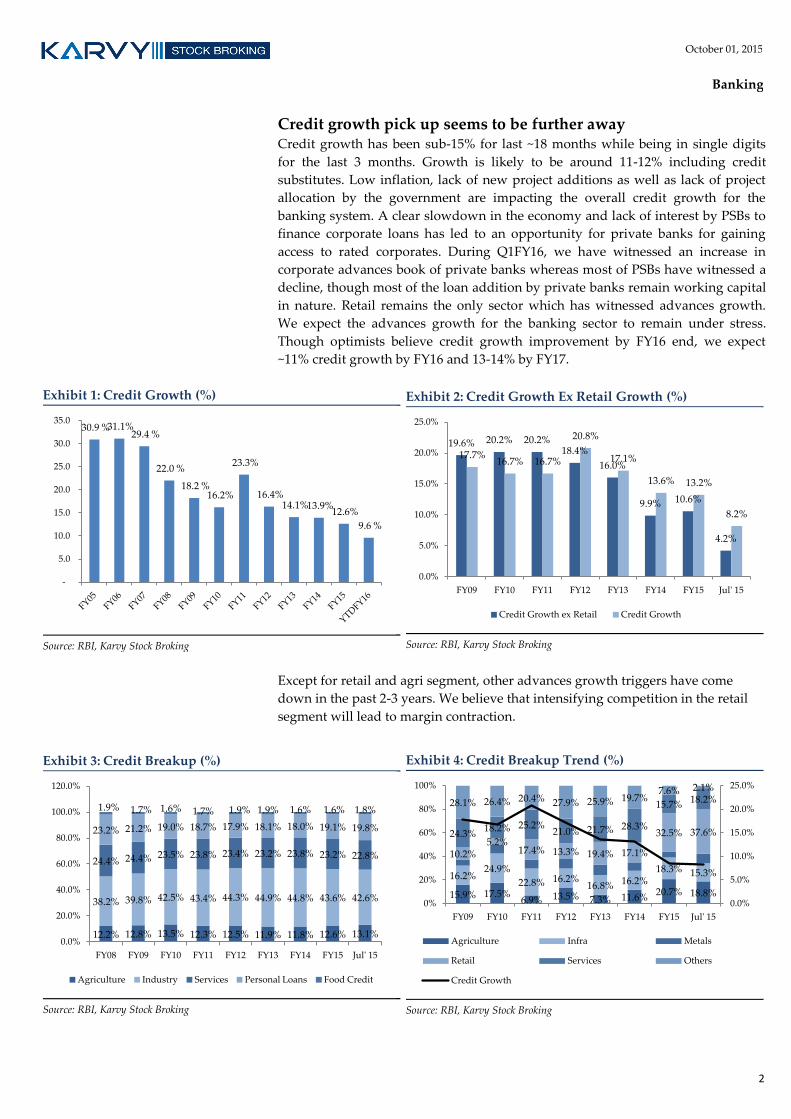

Credit growth pick up seems to be further away Credit growth has been sub-15% for last ~18 months while being in single digits

for the last 3 months. Growth is likely to be around 11-12% including credit

substitutes. Low inflation, lack of new project additions as well as lack of project

allocation by the government are impacting the overall credit growth for the

banking system. A clear slowdown in the economy and lack of interest by PSBs to

finance corporate loans has led to an opportunity for private banks for gaining

access to rated corporates. During Q1FY16, we have witnessed an increase in

corporate advances book of private banks whereas most of PSBs have witnessed a

decline, though most of the loan addition by private banks remain working capital

in nature. Retail remains the only sector which has witnessed advances growth.

We expect the advances growth for the banking sector to remain under stress.

Though optimists believe credit growth improvement by FY16 end, we expect

~11% credit growth by FY16 and 13-14% by FY17.

Exhibit 1: Credit Growth (%)

Source: RBI, Karvy Stock Broking

Exhibit 2: Credit Growth Ex Retail Growth (%)

Source: RBI, Karvy Stock Broking

Except for retail and agri segment, other advances growth triggers have come

down in the past 2-3 years. We believe that intensifying competition in the retail

segment will lead to margin contraction.

Exhibit 3: Credit Breakup (%)

Source: RBI, Karvy Stock Broking

Exhibit 4: Credit Breakup Trend (%)

Source: RBI, Karvy Stock Broking

30.9 % 31.1% 29.4 %

22.0 %

18.2 % 16.2%

23.3%

16.4% 14.1% 13.9%

12.6%

9.6 %

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

19.6% 20.2% 20.2% 18.4%

16.0%

9.9% 10.6%

4.2%

17.7% 16.7% 16.7%

20.8%

17.1%

13.6% 13.2%

8.2%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

FY09 FY10 FY11 FY12 FY13 FY14 FY15 Jul' 15

Credit Growth ex Retail Credit Growth

12.2% 12.8% 13.5% 12.3% 12.5% 11.9% 11.8% 12.6% 13.1%

38.2% 39.8% 42.5% 43.4% 44.3% 44.9% 44.8% 43.6% 42.6%

24.4% 24.4% 23.5% 23.8% 23.4% 23.2% 23.8% 23.2% 22.8%

23.2% 21.2% 19.0% 18.7% 17.9% 18.1% 18.0% 19.1% 19.8%

1.9% 1.7% 1.6% 1.7% 1.9% 1.9% 1.6% 1.6% 1.8%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 Jul' 15

Agriculture Industry Services Personal Loans Food Credit

15.9% 17.5% 6.9% 13.5% 7.3% 11.6%

20.7% 18.8%

16.2% 24.9%

22.8% 16.2% 16.8% 16.2%

18.3% 15.3%

10.2% 5.2%

17.4% 13.3% 19.4% 17.1%

32.5% 37.6% 24.3% 18.2% 25.2%

21.0% 21.7% 28.3%

15.7% 18.2% 28.1% 26.4% 20.4% 27.9% 25.9% 19.7% 7.6% 2.1%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

0%

20%

40%

60%

80%

100%

FY09 FY10 FY11 FY12 FY13 FY14 FY15 Jul' 15

Agriculture Infra Metals

Retail Services Others

Credit Growth

3

October 01, 2015

Banking

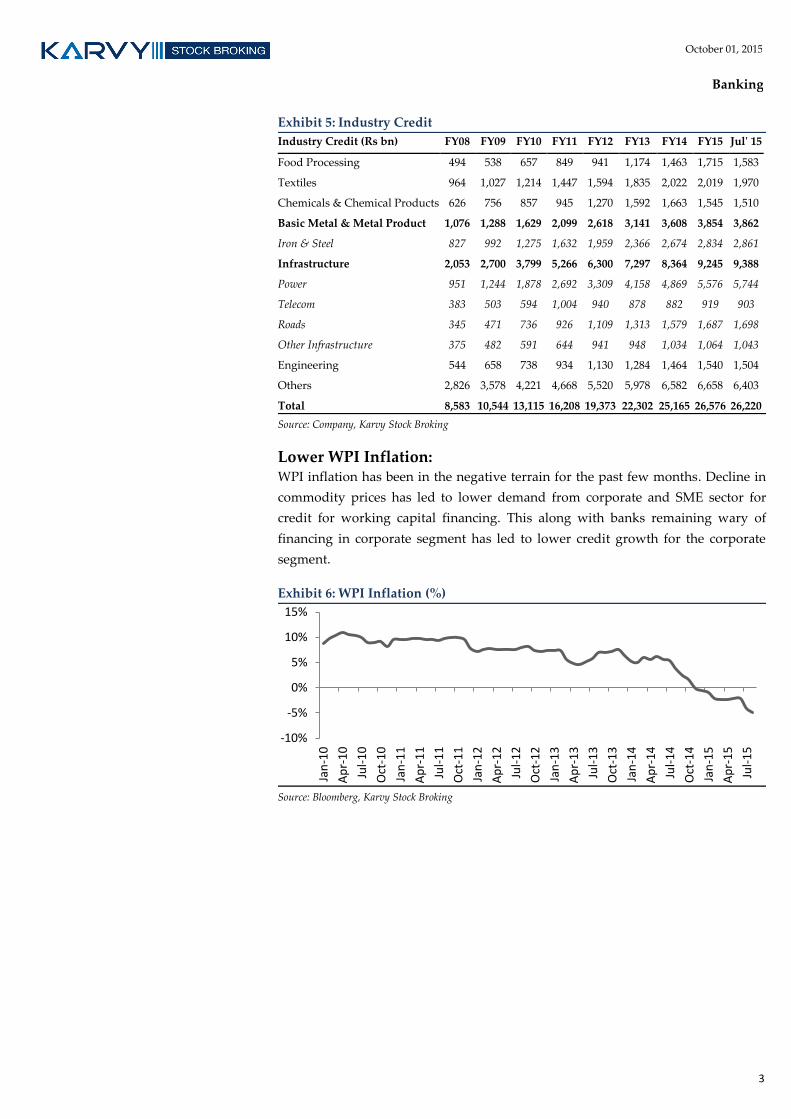

Exhibit 5: Industry Credit

Industry Credit (Rs bn) FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 Jul' 15

Food Processing 494 538 657 849 941 1,174 1,463 1,715 1,583

Textiles 964 1,027 1,214 1,447 1,594 1,835 2,022 2,019 1,970

Chemicals & Chemical Products 626 756 857 945 1,270 1,592 1,663 1,545 1,510

Basic Metal & Metal Product 1,076 1,288 1,629 2,099 2,618 3,141 3,608 3,854 3,862

Iron & Steel 827 992 1,275 1,632 1,959 2,366 2,674 2,834 2,861

Infrastructure 2,053 2,700 3,799 5,266 6,300 7,297 8,364 9,245 9,388

Power 951 1,244 1,878 2,692 3,309 4,158 4,869 5,576 5,744

Telecom 383 503 594 1,004 940 878 882 919 903

Roads 345 471 736 926 1,109 1,313 1,579 1,687 1,698

Other Infrastructure 375 482 591 644 941 948 1,034 1,064 1,043

Engineering 544 658 738 934 1,130 1,284 1,464 1,540 1,504

Others 2,826 3,578 4,221 4,668 5,520 5,978 6,582 6,658 6,403

Total 8,583 10,544 13,115 16,208 19,373 22,302 25,165 26,576 26,220

Source: Company, Karvy Stock Broking

Lower WPI Inflation: WPI inflation has been in the negative terrain for the past few months. Decline in

commodity prices has led to lower demand from corporate and SME sector for

credit for working capital financing. This along with banks remaining wary of

financing in corporate segment has led to lower credit growth for the corporate

segment.

Exhibit 6: WPI Inflation (%)

Source: Bloomberg, Karvy Stock Broking

-10%

-5%

0%

5%

10%

15%

Jan

-10

Ap

r-1

0

Jul-

10

Oct

-10

Jan

-11

Ap

r-1

1

Jul-

11

Oct

-11

Jan

-12

Ap

r-1

2

Jul-

12

Oct

-12

Jan

-13

Ap

r-1

3

Jul-

13

Oct

-13

Jan

-14

Ap

r-1

4

Jul-

14

Oct

-14

Jan

-15

Ap

r-1

5

Jul-

15

4

October 01, 2015

Banking

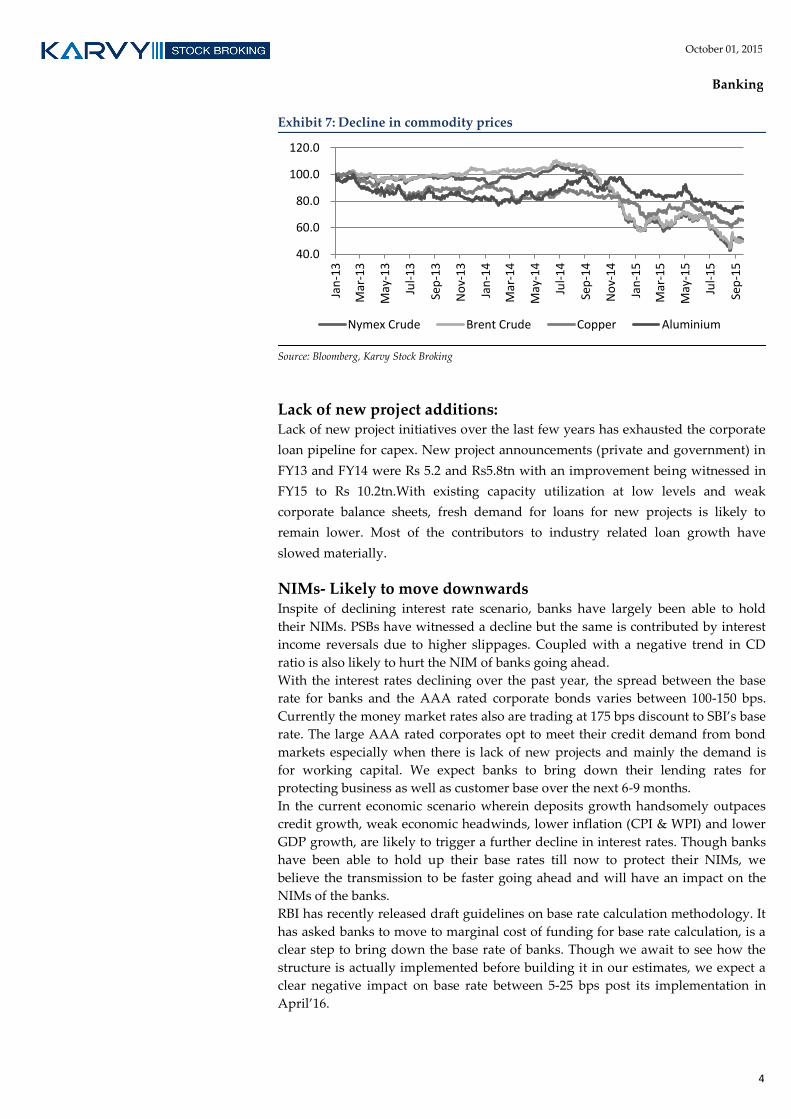

Exhibit 7: Decline in commodity prices

Source: Bloomberg, Karvy Stock Broking

Lack of new project additions: Lack of new project initiatives over the last few years has exhausted the corporate

loan pipeline for capex. New project announcements (private and government) in

FY13 and FY14 were Rs 5.2 and Rs5.8tn with an improvement being witnessed in

FY15 to Rs 10.2tn.With existing capacity utilization at low levels and weak

corporate balance sheets, fresh demand for loans for new projects is likely to

remain lower. Most of the contributors to industry related loan growth have

slowed materially.

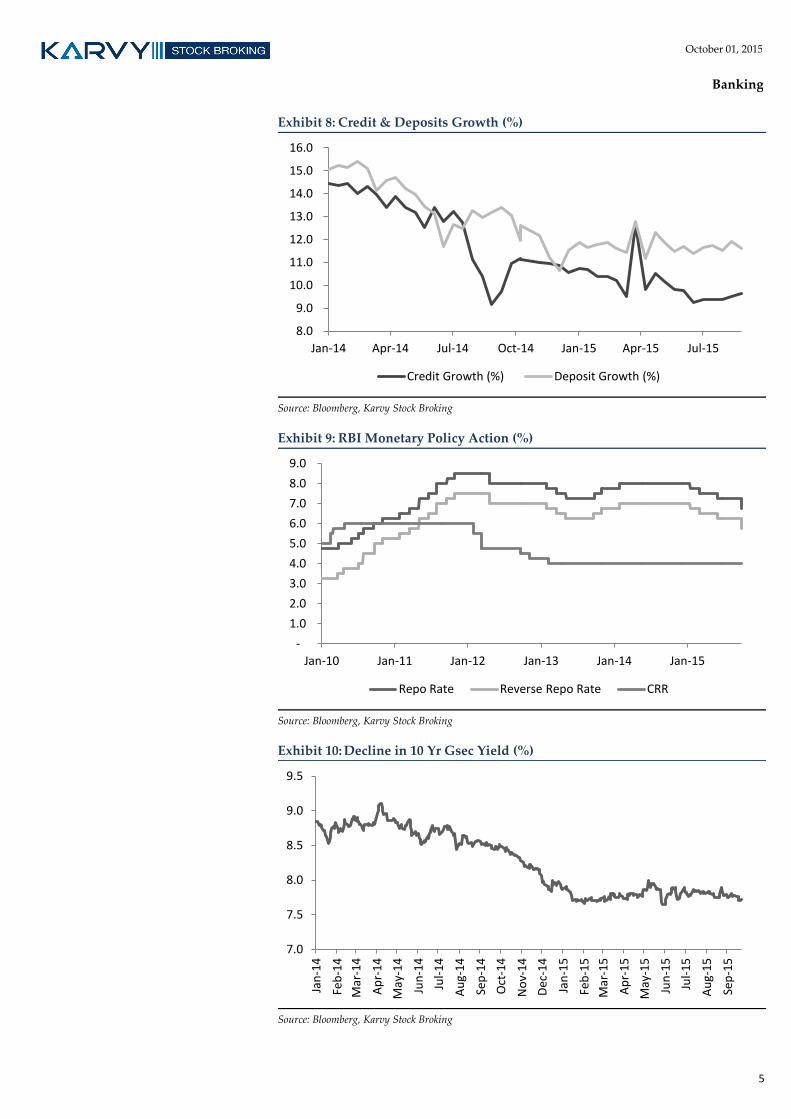

NIMs- Likely to move downwards Inspite of declining interest rate scenario, banks have largely been able to hold

their NIMs. PSBs have witnessed a decline but the same is contributed by interest

income reversals due to higher slippages. Coupled with a negative trend in CD

ratio is also likely to hurt the NIM of banks going ahead.

With the interest rates declining over the past year, the spread between the base

rate for banks and the AAA rated corporate bonds varies between 100-150 bps.

Currently the money market rates also are trading at 175 bps discount to SBI’s base

rate. The large AAA rated corporates opt to meet their credit demand from bond

markets especially when there is lack of new projects and mainly the demand is

for working capital. We expect banks to bring down their lending rates for

protecting business as well as customer base over the next 6-9 months.

In the current economic scenario wherein deposits growth handsomely outpaces

credit growth, weak economic headwinds, lower inflation (CPI & WPI) and lower

GDP growth, are likely to trigger a further decline in interest rates. Though banks

have been able to hold up their base rates till now to protect their NIMs, we

believe the transmission to be faster going ahead and will have an impact on the

NIMs of the banks.

RBI has recently released draft guidelines on base rate calculation methodology. It

has asked banks to move to marginal cost of funding for base rate calculation, is a

clear step to bring down the base rate of banks. Though we await to see how the

structure is actually implemented before building it in our estimates, we expect a

clear negative impact on base rate between 5-25 bps post its implementation in

April’16.

40.0

60.0

80.0

100.0

120.0

Jan

-13

Mar

-13

May

-13

Jul-

13

Sep

-13

No

v-1

3

Jan

-14

Mar

-14

May

-14

Jul-

14

Sep

-14

No

v-1

4

Jan

-15

Mar

-15

May

-15

Jul-

15

Sep

-15

Nymex Crude Brent Crude Copper Aluminium

5

October 01, 2015

Banking

Exhibit 8: Credit & Deposits Growth (%)

Source: Bloomberg, Karvy Stock Broking

Exhibit 9: RBI Monetary Policy Action (%)

Source: Bloomberg, Karvy Stock Broking

Exhibit 10: Decline in 10 Yr Gsec Yield (%)

Source: Bloomberg, Karvy Stock Broking

8.0

9.0

10.0

11.0

12.0

13.0

14.0

15.0

16.0

Jan-14 Apr-14 Jul-14 Oct-14 Jan-15 Apr-15 Jul-15

Credit Growth (%) Deposit Growth (%)

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15

Repo Rate Reverse Repo Rate CRR

7.0

7.5

8.0

8.5

9.0

9.5

Jan

-14

Feb

-14

Mar

-14

Ap

r-1

4

May

-14

Jun

-14

Jul-

14

Au

g-1

4

Sep

-14

Oct

-14

No

v-1

4

Dec

-14

Jan

-15

Feb

-15

Mar

-15

Ap

r-1

5

May

-15

Jun

-15

Jul-

15

Au

g-1

5

Sep

-15

6

October 01, 2015

Banking

Asset quality- Still a long way to go; provisions to stay higher

Asset quality concerns for Indian banking sector continues to remain elevated.

Fresh slippages from one- off large accounts (like Amtek Auto) including

slippages from restructured book continues to remain elevated aided by slower

credit growth, will lead to higher GNPA. Though fresh slippages for the banking

sector are expected to come down along with RBI’s 5-25 special refinancing

scheme, we expect that slippages from the restructured book for banks to continue

to remain a concern especially for PSBs which have comparatively much higher

restructured book.

Indian banking sector had witnessed a strong credit growth in FY05-10 during

which the advances grew by ~24% CAGR. During the period, Indian economy was

booming with GDP growth of average 8.7%. As expected in growth phase, banks

also took large exposures to risky as well as over leveraged groups and then paid

the price post FY2010.

Economic slowdown immediately post such rapid credit expansion has led to a

major growth in asset quality stress for the banks wherein GNPA grew by 42%

CAGR over FY10-14. Though we believe most of the stressed accounts should have

slipped till now, many of them had been given temporary lifeline in the name of

restructuring. Post the closure of restructuring window, RBI has now come out

with refinancing under the 5-25 scheme. The quantum of refinancing is likely to be

smaller as compared to restructuring as the refinancing is applicable only to on-

going standard projects.

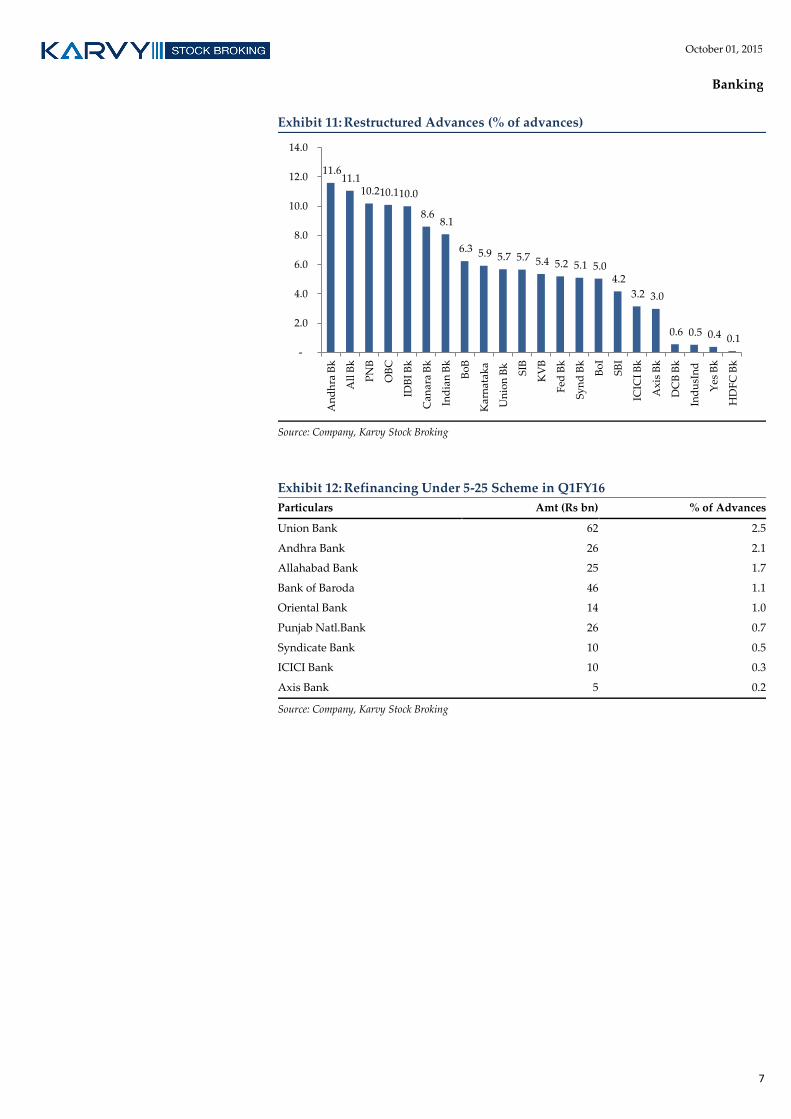

Cumulative slippages of banks from restructured book are already in the range of

20-25% of total restructuring (incl. loans currently under moratorium period). We

expect the slippages from restructured book to continue to remain elevated as

additional loans are expected to be coming out from the moratorium period in

FY16 and FY17.

In the past couple of years, with increasing GNPA, PCR of most of the banks (PSBs

and private) have declined. As the slippages from restructured book is expected to

remain elevated, provision cost is expected to remain higher. Given the already

lower PCR, we expect banks provision cost to remain higher in FY16 and FY17 for

higher slippages, but post that for increasing their PCR to prior levels.

Though fresh slippages are likely to decline, slippages from restructured accounts

will lead to higher slippages though the total stressed assets book (GNPA +

Restructured book) is unlikely to increase sharply. Restructured assets book for

private banks are much smaller as compared to PSBs and we expect slippages for

private banks to be lower than those compared to PSBs in FY16. We foresee some

respite coming in from the asset quality front in FY17 but FY16 will continue to be

a hangover especially for banks with higher restructured book (particularly PSBs).

7

October 01, 2015

Banking

Exhibit 11: Restructured Advances (% of advances)

Source: Company, Karvy Stock Broking

Exhibit 12: Refinancing Under 5-25 Scheme in Q1FY16

Particulars Amt (Rs bn) % of Advances

Union Bank 62 2.5

Andhra Bank 26 2.1

Allahabad Bank 25 1.7

Bank of Baroda 46 1.1

Oriental Bank 14 1.0

Punjab Natl.Bank 26 0.7

Syndicate Bank 10 0.5

ICICI Bank 10 0.3

Axis Bank 5 0.2

Source: Company, Karvy Stock Broking

11.6 11.1

10.2 10.1 10.0

8.6 8.1

6.3 5.9 5.7 5.7 5.4 5.2 5.1 5.0 4.2

3.2 3.0

0.6 0.5 0.4 0.1

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

An

dh

ra B

k

All

Bk

PN

B

OB

C

IDB

I B

k

Can

ara

Bk

Ind

ian

Bk

Bo

B

Kar

nat

ak

a

Un

ion

Bk

SIB

KV

B

Fed

Bk

Sy

nd

Bk

Bo

I

SB

I

ICIC

I B

k

Ax

is B

k

DC

B B

k

Ind

usI

nd

Yes

Bk

HD

FC

Bk

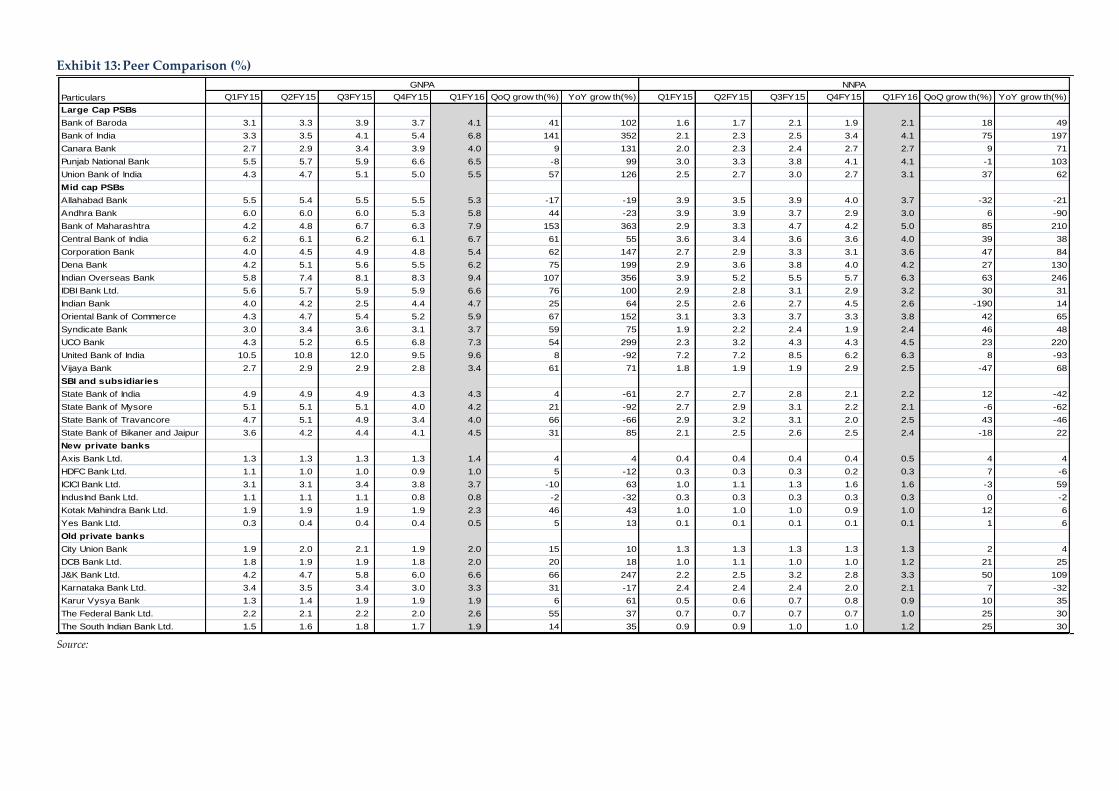

Exhibit 13: Peer Comparison (%)

Source:

Q1FY15 Q2FY15 Q3FY15 Q4FY15 Q1FY16 QoQ grow th(%) YoY grow th(%) Q1FY15 Q2FY15 Q3FY15 Q4FY15 Q1FY16 QoQ grow th(%) YoY grow th(%)

Large Cap PSBs

Bank of Baroda 3.1 3.3 3.9 3.7 4.1 41 102 1.6 1.7 2.1 1.9 2.1 18 49

Bank of India 3.3 3.5 4.1 5.4 6.8 141 352 2.1 2.3 2.5 3.4 4.1 75 197

Canara Bank 2.7 2.9 3.4 3.9 4.0 9 131 2.0 2.3 2.4 2.7 2.7 9 71

Punjab National Bank 5.5 5.7 5.9 6.6 6.5 -8 99 3.0 3.3 3.8 4.1 4.1 -1 103

Union Bank of India 4.3 4.7 5.1 5.0 5.5 57 126 2.5 2.7 3.0 2.7 3.1 37 62

Mid cap PSBs

Allahabad Bank 5.5 5.4 5.5 5.5 5.3 -17 -19 3.9 3.5 3.9 4.0 3.7 -32 -21

Andhra Bank 6.0 6.0 6.0 5.3 5.8 44 -23 3.9 3.9 3.7 2.9 3.0 6 -90

Bank of Maharashtra 4.2 4.8 6.7 6.3 7.9 153 363 2.9 3.3 4.7 4.2 5.0 85 210

Central Bank of India 6.2 6.1 6.2 6.1 6.7 61 55 3.6 3.4 3.6 3.6 4.0 39 38

Corporation Bank 4.0 4.5 4.9 4.8 5.4 62 147 2.7 2.9 3.3 3.1 3.6 47 84

Dena Bank 4.2 5.1 5.6 5.5 6.2 75 199 2.9 3.6 3.8 4.0 4.2 27 130

Indian Overseas Bank 5.8 7.4 8.1 8.3 9.4 107 356 3.9 5.2 5.5 5.7 6.3 63 246

IDBI Bank Ltd. 5.6 5.7 5.9 5.9 6.6 76 100 2.9 2.8 3.1 2.9 3.2 30 31

Indian Bank 4.0 4.2 2.5 4.4 4.7 25 64 2.5 2.6 2.7 4.5 2.6 -190 14

Oriental Bank of Commerce 4.3 4.7 5.4 5.2 5.9 67 152 3.1 3.3 3.7 3.3 3.8 42 65

Syndicate Bank 3.0 3.4 3.6 3.1 3.7 59 75 1.9 2.2 2.4 1.9 2.4 46 48

UCO Bank 4.3 5.2 6.5 6.8 7.3 54 299 2.3 3.2 4.3 4.3 4.5 23 220

United Bank of India 10.5 10.8 12.0 9.5 9.6 8 -92 7.2 7.2 8.5 6.2 6.3 8 -93

Vijaya Bank 2.7 2.9 2.9 2.8 3.4 61 71 1.8 1.9 1.9 2.9 2.5 -47 68

SBI and subsidiaries

State Bank of India 4.9 4.9 4.9 4.3 4.3 4 -61 2.7 2.7 2.8 2.1 2.2 12 -42

State Bank of Mysore 5.1 5.1 5.1 4.0 4.2 21 -92 2.7 2.9 3.1 2.2 2.1 -6 -62

State Bank of Travancore 4.7 5.1 4.9 3.4 4.0 66 -66 2.9 3.2 3.1 2.0 2.5 43 -46

State Bank of Bikaner and Jaipur 3.6 4.2 4.4 4.1 4.5 31 85 2.1 2.5 2.6 2.5 2.4 -18 22

New private banks

Axis Bank Ltd. 1.3 1.3 1.3 1.3 1.4 4 4 0.4 0.4 0.4 0.4 0.5 4 4

HDFC Bank Ltd. 1.1 1.0 1.0 0.9 1.0 5 -12 0.3 0.3 0.3 0.2 0.3 7 -6

ICICI Bank Ltd. 3.1 3.1 3.4 3.8 3.7 -10 63 1.0 1.1 1.3 1.6 1.6 -3 59

IndusInd Bank Ltd. 1.1 1.1 1.1 0.8 0.8 -2 -32 0.3 0.3 0.3 0.3 0.3 0 -2

Kotak Mahindra Bank Ltd. 1.9 1.9 1.9 1.9 2.3 46 43 1.0 1.0 1.0 0.9 1.0 12 6

Yes Bank Ltd. 0.3 0.4 0.4 0.4 0.5 5 13 0.1 0.1 0.1 0.1 0.1 1 6

Old private banks

City Union Bank 1.9 2.0 2.1 1.9 2.0 15 10 1.3 1.3 1.3 1.3 1.3 2 4

DCB Bank Ltd. 1.8 1.9 1.9 1.8 2.0 20 18 1.0 1.1 1.0 1.0 1.2 21 25

J&K Bank Ltd. 4.2 4.7 5.8 6.0 6.6 66 247 2.2 2.5 3.2 2.8 3.3 50 109

Karnataka Bank Ltd. 3.4 3.5 3.4 3.0 3.3 31 -17 2.4 2.4 2.4 2.0 2.1 7 -32

Karur Vysya Bank 1.3 1.4 1.9 1.9 1.9 6 61 0.5 0.6 0.7 0.8 0.9 10 35

The Federal Bank Ltd. 2.2 2.1 2.2 2.0 2.6 55 37 0.7 0.7 0.7 0.7 1.0 25 30

The South Indian Bank Ltd. 1.5 1.6 1.8 1.7 1.9 14 35 0.9 0.9 1.0 1.0 1.2 25 30

Particulars

GNPA NNPA

October 01, 2015

Banking

9

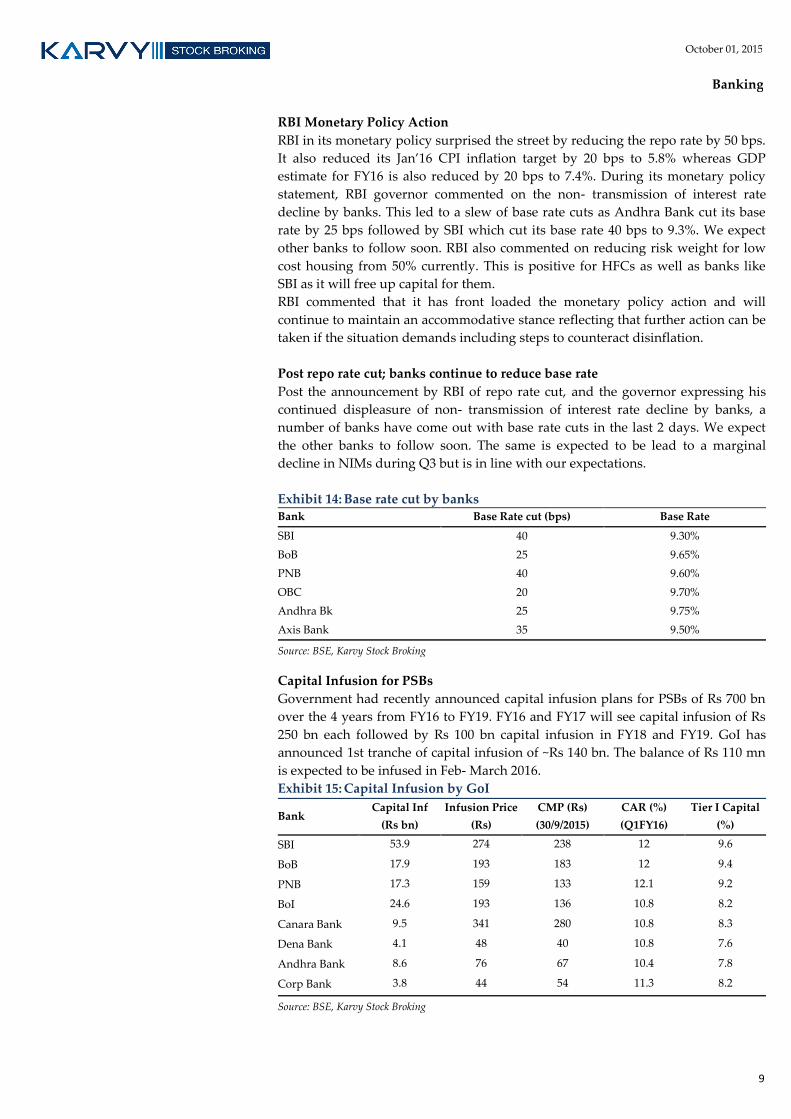

RBI Monetary Policy Action

RBI in its monetary policy surprised the street by reducing the repo rate by 50 bps.

It also reduced its Jan’16 CPI inflation target by 20 bps to 5.8% whereas GDP

estimate for FY16 is also reduced by 20 bps to 7.4%. During its monetary policy

statement, RBI governor commented on the non- transmission of interest rate

decline by banks. This led to a slew of base rate cuts as Andhra Bank cut its base

rate by 25 bps followed by SBI which cut its base rate 40 bps to 9.3%. We expect

other banks to follow soon. RBI also commented on reducing risk weight for low

cost housing from 50% currently. This is positive for HFCs as well as banks like

SBI as it will free up capital for them.

RBI commented that it has front loaded the monetary policy action and will

continue to maintain an accommodative stance reflecting that further action can be

taken if the situation demands including steps to counteract disinflation.

Post repo rate cut; banks continue to reduce base rate

Post the announcement by RBI of repo rate cut, and the governor expressing his

continued displeasure of non- transmission of interest rate decline by banks, a

number of banks have come out with base rate cuts in the last 2 days. We expect

the other banks to follow soon. The same is expected to be lead to a marginal

decline in NIMs during Q3 but is in line with our expectations.

Exhibit 14: Base rate cut by banks Bank Base Rate cut (bps) Base Rate

SBI 40 9.30%

BoB 25 9.65%

PNB 40 9.60%

OBC 20 9.70%

Andhra Bk 25 9.75%

Axis Bank 35 9.50%

Source: BSE, Karvy Stock Broking

Capital Infusion for PSBs

Government had recently announced capital infusion plans for PSBs of Rs 700 bn

over the 4 years from FY16 to FY19. FY16 and FY17 will see capital infusion of Rs

250 bn each followed by Rs 100 bn capital infusion in FY18 and FY19. GoI has

announced 1st tranche of capital infusion of ~Rs 140 bn. The balance of Rs 110 mn

is expected to be infused in Feb- March 2016.

Exhibit 15: Capital Infusion by GoI

Bank Capital Inf

(Rs bn)

Infusion Price

(Rs)

CMP (Rs)

(30/9/2015)

CAR (%)

(Q1FY16)

Tier I Capital

(%)

SBI 53.9 274 238 12 9.6

BoB 17.9 193 183 12 9.4

PNB 17.3 159 133 12.1 9.2

BoI 24.6 193 136 10.8 8.2

Canara Bank 9.5 341 280 10.8 8.3

Dena Bank 4.1 48 40 10.8 7.6

Andhra Bank 8.6 76 67 10.4 7.8

Corp Bank 3.8 44 54 11.3 8.2

Source: BSE, Karvy Stock Broking

October 01, 2015

Banking

10

Valuation and Outlook

We believe that the banking sector is set for another year of slowdown in FY16 but

FY17 looks promising. With a revival in economy along with interest rate

stabilization, we expect earnings of the banks to improve. However for FY16, the

outlook for credit growth remains weak, along with asset quality pressures likely

to negatively impact the earnings growth for the banks. We believe that private

banks are better placed, being well capitalized as well as lower GNPA and

restructured advances which are likely to drive the slippages in FY16. We have

recently interacted with the management of 6 banks in the PSU and private

banking space to understand the current banking scenario as well as the likely

impact of the recent RBI policies on the banking space.

Credit growth is likely to be under pressure along with easing of asset quality

pressures which still seems to be some time away. With NIMs likely to be

impacted by declining interest rates along with the recent RBI guidelines of

marginal cost of funds for base rate calculation, margins are likely to be marginally

lower for FY16 and FY17.

Axis Bank, Yes Bank and SBI are our top picks in the BFSI space.

Change in rating

DCB Bank: Bank has largely maintained its asset quality but we expect

deterioration going ahead. We have maintained our estimates for FY16 and FY17

and our target price. Due to price run-up, we downgrade the stock to Sell with a

target price of Rs142 (2.1x FY17E ABV).

Change in target price

Bank of Baroda: With the appointment of private sector professionals as Chairman

and MD & CEO, the operations are likely to improve, but will likely take some

time. We remain cautious on the PSBs but believe BoB is likely to be the key

beneficiary of economic revival. We upgrade the long term multiple of the stock

from 1x to 1.1x FY17E ABV but retain our Hold rating with a TP of Rs200.

October 01, 2015

Banking

11

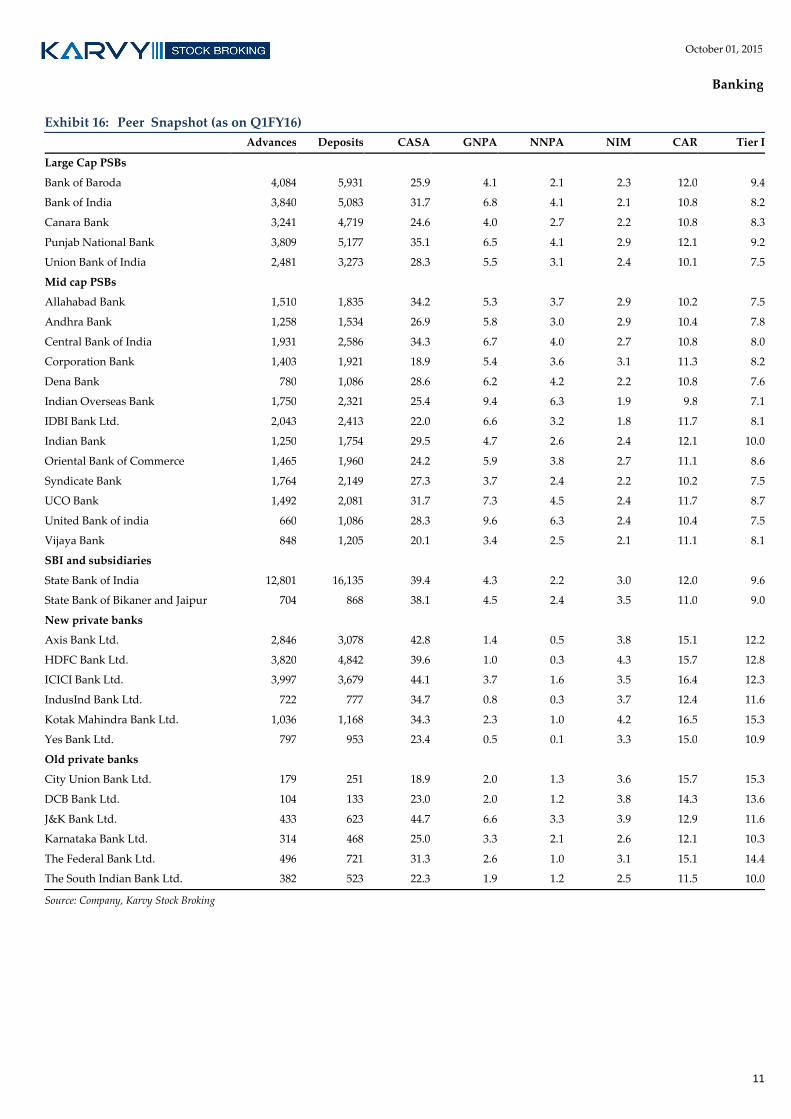

Exhibit 16: Peer Snapshot (as on Q1FY16)

Advances Deposits CASA GNPA NNPA NIM CAR Tier I

Large Cap PSBs

Bank of Baroda 4,084 5,931 25.9 4.1 2.1 2.3 12.0 9.4

Bank of India 3,840 5,083 31.7 6.8 4.1 2.1 10.8 8.2

Canara Bank 3,241 4,719 24.6 4.0 2.7 2.2 10.8 8.3

Punjab National Bank 3,809 5,177 35.1 6.5 4.1 2.9 12.1 9.2

Union Bank of India 2,481 3,273 28.3 5.5 3.1 2.4 10.1 7.5

Mid cap PSBs

Allahabad Bank 1,510 1,835 34.2 5.3 3.7 2.9 10.2 7.5

Andhra Bank 1,258 1,534 26.9 5.8 3.0 2.9 10.4 7.8

Central Bank of India 1,931 2,586 34.3 6.7 4.0 2.7 10.8 8.0

Corporation Bank 1,403 1,921 18.9 5.4 3.6 3.1 11.3 8.2

Dena Bank 780 1,086 28.6 6.2 4.2 2.2 10.8 7.6

Indian Overseas Bank 1,750 2,321 25.4 9.4 6.3 1.9 9.8 7.1

IDBI Bank Ltd. 2,043 2,413 22.0 6.6 3.2 1.8 11.7 8.1

Indian Bank 1,250 1,754 29.5 4.7 2.6 2.4 12.1 10.0

Oriental Bank of Commerce 1,465 1,960 24.2 5.9 3.8 2.7 11.1 8.6

Syndicate Bank 1,764 2,149 27.3 3.7 2.4 2.2 10.2 7.5

UCO Bank 1,492 2,081 31.7 7.3 4.5 2.4 11.7 8.7

United Bank of india 660 1,086 28.3 9.6 6.3 2.4 10.4 7.5

Vijaya Bank 848 1,205 20.1 3.4 2.5 2.1 11.1 8.1

SBI and subsidiaries

State Bank of India 12,801 16,135 39.4 4.3 2.2 3.0 12.0 9.6

State Bank of Bikaner and Jaipur 704 868 38.1 4.5 2.4 3.5 11.0 9.0

New private banks

Axis Bank Ltd. 2,846 3,078 42.8 1.4 0.5 3.8 15.1 12.2

HDFC Bank Ltd. 3,820 4,842 39.6 1.0 0.3 4.3 15.7 12.8

ICICI Bank Ltd. 3,997 3,679 44.1 3.7 1.6 3.5 16.4 12.3

IndusInd Bank Ltd. 722 777 34.7 0.8 0.3 3.7 12.4 11.6

Kotak Mahindra Bank Ltd. 1,036 1,168 34.3 2.3 1.0 4.2 16.5 15.3

Yes Bank Ltd. 797 953 23.4 0.5 0.1 3.3 15.0 10.9

Old private banks

City Union Bank Ltd. 179 251 18.9 2.0 1.3 3.6 15.7 15.3

DCB Bank Ltd. 104 133 23.0 2.0 1.2 3.8 14.3 13.6

J&K Bank Ltd. 433 623 44.7 6.6 3.3 3.9 12.9 11.6

Karnataka Bank Ltd. 314 468 25.0 3.3 2.1 2.6 12.1 10.3

The Federal Bank Ltd. 496 721 31.3 2.6 1.0 3.1 15.1 14.4

The South Indian Bank Ltd. 382 523 22.3 1.9 1.2 2.5 11.5 10.0

Source: Company, Karvy Stock Broking

Banking October 01, 2015

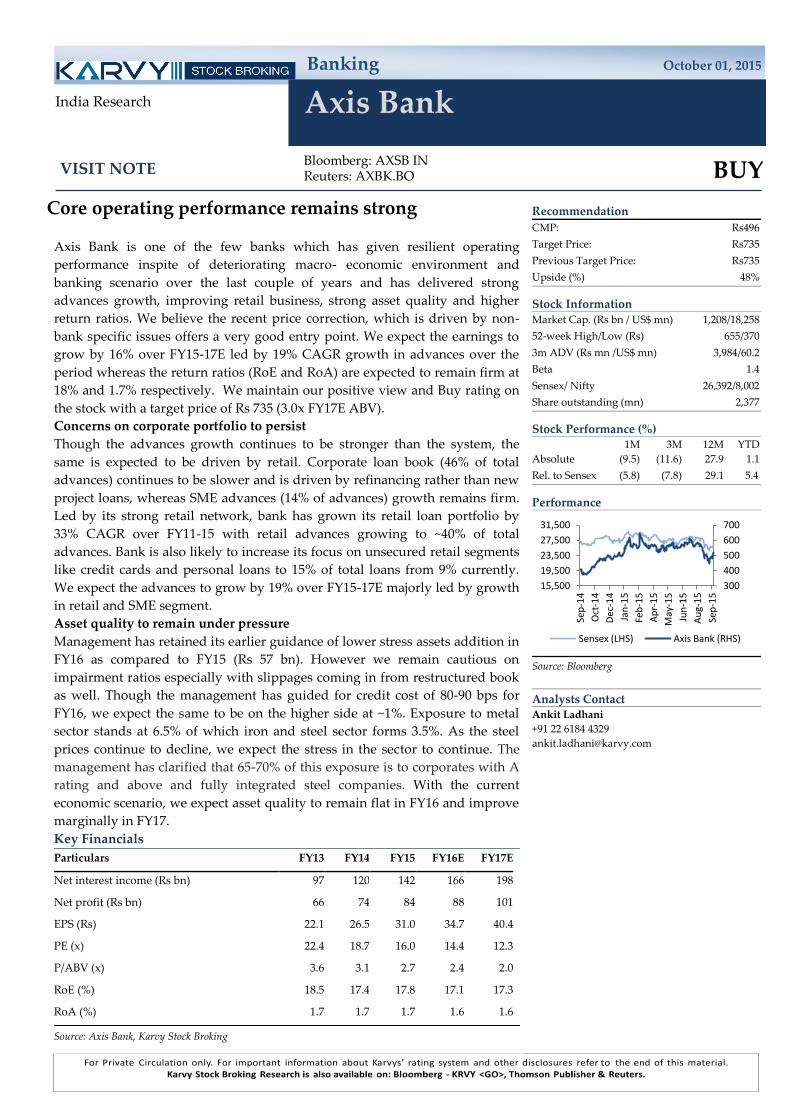

Axis Bank

Bloomberg: AXSB IN Reuters: AXBK.BO

BUY

India Research

VISIT NOTE

Recommendation

CMP: Rs496

Target Price: Rs735

Previous Target Price: Rs735

Upside (%) 48%

Stock Information Market Cap. (Rs bn / US$ mn) 1,208/18,258

52-week High/Low (Rs) 655/370

3m ADV (Rs mn /US$ mn) 3,984/60.2

Beta 1.4

Sensex/ Nifty 26,392/8,002

Share outstanding (mn) 2,377

Stock Performance (%) 1M 3M 12M YTD

Absolute (9.5) (11.6) 27.9 1.1

Rel. to Sensex (5.8) (7.8) 29.1 5.4

Performance

Source: Bloomberg

Analysts Contact Ankit Ladhani

+91 22 6184 4329

300

400

500

600

700

15,500

19,500

23,500

27,500

31,500

Sep

-14

Oct

-14

Dec

-14

Jan

-15

Feb

-15

Ap

r-1

5

May

-15

Jun

-15

Au

g-1

5

Sep

-15

Sensex (LHS) Axis Bank (RHS)

Core operating performance remains strong

Axis Bank is one of the few banks which has given resilient operating

performance inspite of deteriorating macro- economic environment and

banking scenario over the last couple of years and has delivered strong

advances growth, improving retail business, strong asset quality and higher

return ratios. We believe the recent price correction, which is driven by non-

bank specific issues offers a very good entry point. We expect the earnings to

grow by 16% over FY15-17E led by 19% CAGR growth in advances over the

period whereas the return ratios (RoE and RoA) are expected to remain firm at

18% and 1.7% respectively. We maintain our positive view and Buy rating on

the stock with a target price of Rs 735 (3.0x FY17E ABV).

Concerns on corporate portfolio to persist

Though the advances growth continues to be stronger than the system, the

same is expected to be driven by retail. Corporate loan book (46% of total

advances) continues to be slower and is driven by refinancing rather than new

project loans, whereas SME advances (14% of advances) growth remains firm.

Led by its strong retail network, bank has grown its retail loan portfolio by

33% CAGR over FY11-15 with retail advances growing to ~40% of total

advances. Bank is also likely to increase its focus on unsecured retail segments

like credit cards and personal loans to 15% of total loans from 9% currently.

We expect the advances to grow by 19% over FY15-17E majorly led by growth

in retail and SME segment.

Asset quality to remain under pressure

Management has retained its earlier guidance of lower stress assets addition in

FY16 as compared to FY15 (Rs 57 bn). However we remain cautious on

impairment ratios especially with slippages coming in from restructured book

as well. Though the management has guided for credit cost of 80-90 bps for

FY16, we expect the same to be on the higher side at ~1%. Exposure to metal

sector stands at 6.5% of which iron and steel sector forms 3.5%. As the steel

prices continue to decline, we expect the stress in the sector to continue. The

management has clarified that 65-70% of this exposure is to corporates with A

rating and above and fully integrated steel companies. With the current

economic scenario, we expect asset quality to remain flat in FY16 and improve

marginally in FY17.

Key Financials

Particulars FY13 FY14 FY15 FY16E FY17E

Net interest income (Rs bn) 97 120 142 166 198

Net profit (Rs bn) 66 74 84 88 101

EPS (Rs) 22.1 26.5 31.0 34.7 40.4

PE (x) 22.4 18.7 16.0 14.4 12.3

P/ABV (x) 3.6 3.1 2.7 2.4 2.0

RoE (%) 18.5 17.4 17.8 17.1 17.3

RoA (%) 1.7 1.7 1.7 1.6 1.6

Source: Axis Bank, Karvy Stock Broking

13

October 01, 2015

Axis Bank

Unsecured retail segment to drive retail advances

Bank is currently focusing on unsecured personal and credit card loans to drive

the retail advances growth. However housing loans (48% of retail advances) is

expected to report slower growth as will mainly be driven by tier II- IV cities

whereas LAP loan (8% of retail loans) growth is expected to remain strong.

CASA ratio improvement continues

Without the aid of differentiated savings rate, savings account deposits have

grown by 21% CAGR over FY11-15. Share of retail deposits as % of total deposits

increased from 59% in FY11 to 78.5% in Q1FY16. CASA share stands at 42.8% as at

the end of Jun-15. With increased competition expected to come in from the new

private banks, payment banks as well as small finance bank we expect growth in

savings accounts to be slower going ahead. Though Axis will maintain its current

CASA share, any rapid further expansion is likely to be difficult.

NIMs likely to remain stable

Though the bank is targeting growth in the high yielding unsecured retail segment

to support NIMs, led by growth from corporate advances at competitive rates, and

slower CASA growth, we expect the NIMs for the bank to remain largely stable.

Inspite of a decline in interest rates expected in the markets to continue, we expect

Axis to maintain its NIM at ~3.5% going ahead.

Valuation and Outlook

Axis Bank currently remains one of the few banks who have maintained its asset

quality along with advances growth inspite of economic slowdown. We believe

the recent price correction, which is driven by non-bank specific issues offers a

very good entry point. We expect the earnings to grow by 16% over FY15-17E led

by 19% CAGR growth in advances over the period whereas the return ratios (RoE

and RoA) are expected to remain firm at 18% and 1.7% respectively. We maintain

our positive view and Buy rating on the stock with a target price of Rs 735 (3.0X

FY17E ABV).

14

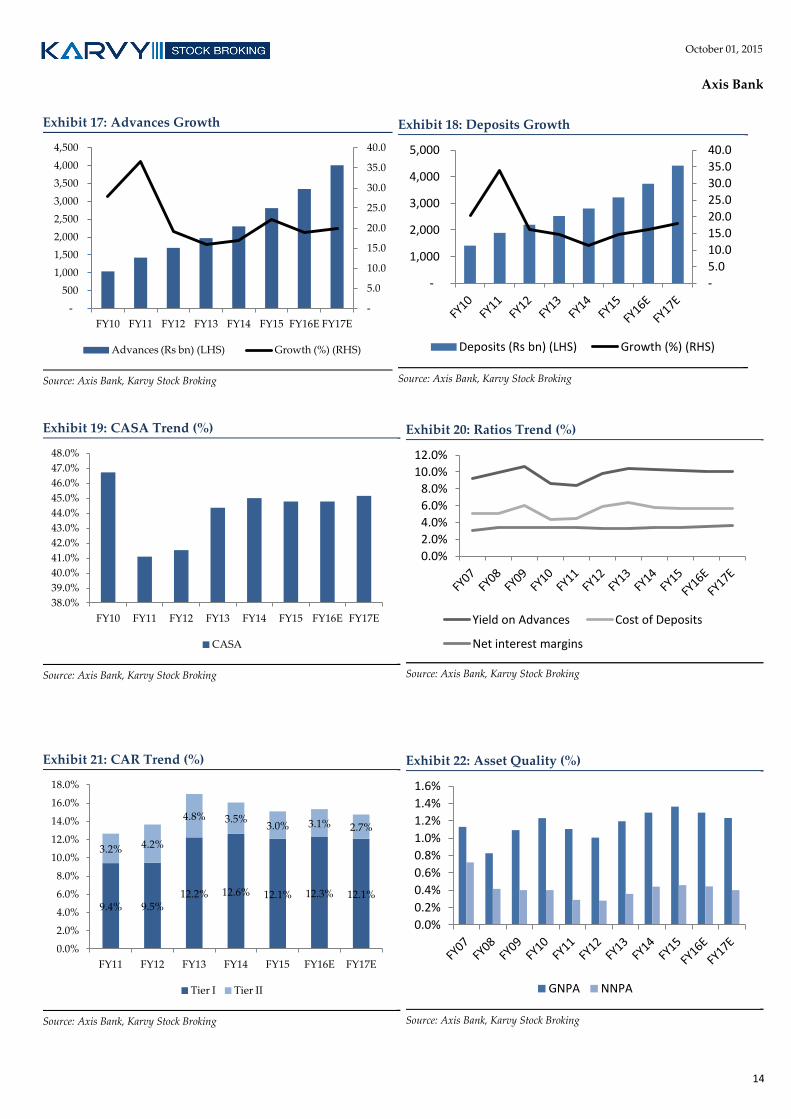

October 01, 2015

Axis Bank

Exhibit 17: Advances Growth

Source: Axis Bank, Karvy Stock Broking

Exhibit 18: Deposits Growth

Source: Axis Bank, Karvy Stock Broking

Exhibit 19: CASA Trend (%)

Source: Axis Bank, Karvy Stock Broking

Exhibit 20: Ratios Trend (%)

Source: Axis Bank, Karvy Stock Broking

Exhibit 21: CAR Trend (%)

Source: Axis Bank, Karvy Stock Broking

Exhibit 22: Asset Quality (%)

Source: Axis Bank, Karvy Stock Broking

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

FY10 FY11 FY12 FY13 FY14 FY15 FY16E FY17E

Advances (Rs bn) (LHS) Growth (%) (RHS)

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

-

1,000

2,000

3,000

4,000

5,000

Deposits (Rs bn) (LHS) Growth (%) (RHS)

38.0%

39.0%

40.0%

41.0%

42.0%

43.0%

44.0%

45.0%

46.0%

47.0%

48.0%

FY10 FY11 FY12 FY13 FY14 FY15 FY16E FY17E

CASA

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

Yield on Advances Cost of Deposits

Net interest margins

9.4% 9.5% 12.2% 12.6% 12.1% 12.3% 12.1%

3.2% 4.2%

4.8% 3.5% 3.0% 3.1% 2.7%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

FY11 FY12 FY13 FY14 FY15 FY16E FY17E

Tier I Tier II

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

1.6%

GNPA NNPA

15

October 01, 2015

Axis Bank

Exhibit 23: Profit and Loss Statement

P &L statement (Rs bn) FY13 FY14 FY15 FY16E FY17E

Interest income 272 306 355 418 494

Interest Expenses 175 187 213 252 296

Net interest income 97 120 142 166 198

Non-interest income 66 74 84 88 101

Fee Income 50 54 61 70 80

Net total income 162 194 226 254 299

Operating expenses 69 79 92 107 125

Employee Expenses 24 26 31 37 44

Pre-provisioning profit 93 115 134 148 173

Provision & Contingency 18 21 23 24 30

PBT 76 93 111 123 144

Tax 24 31 37 41 48

PAT 52 62 74 82 96

Source: Axis Bank, Karvy Stock Broking

Exhibit 24: Balance Sheet

Particulars (Rs bn) FY13 FY14 FY15 FY16E FY17E

Liabilities

Networth 331 382 447 514 593

Deposits 2,526 2,809 3,224 3,740 4,414

Current Deposits 483 487 561 651 775

Savings Deposits 638 778 883 1,024 1,219

Borrowings 440 503 798 1,048 1,216

Other liabilities & provisions 109 138 151 149 180

Total liabilities 3,406 3,832 4,619 5,451 6,403

Assets

Cash & balances with RBI 148 170 198 215 254

Balances with banks & money at call 56 112 163 112 132

Investments 1,137 1,135 1,323 1,511 1,739

Advances 1,970 2,301 2,811 3,345 4,014

Fixed assets 24 24 25 30 36

Other assets 71 90 99 238 228

Total assets 3,406 3,832 4,619 5,451 6,403

Source: Axis Bank, Karvy Stock Broking

16

October 01, 2015

Axis Bank

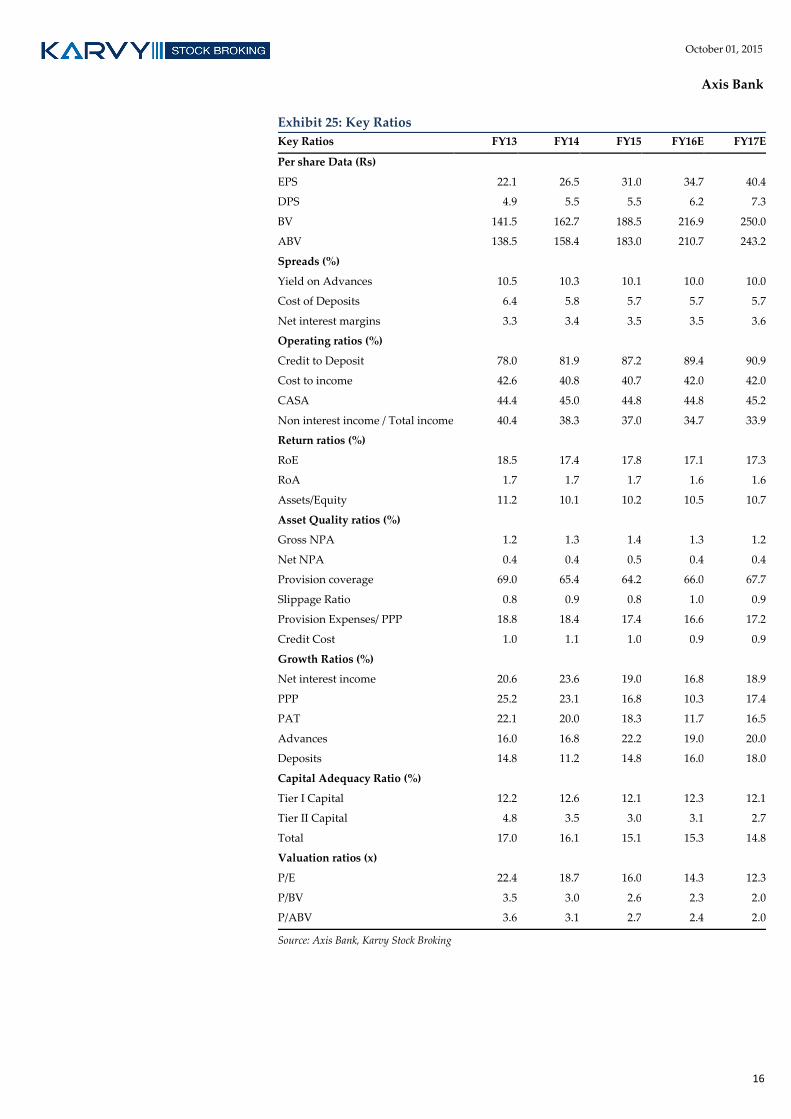

Exhibit 25: Key Ratios

Key Ratios FY13 FY14 FY15 FY16E FY17E

Per share Data (Rs)

EPS 22.1 26.5 31.0 34.7 40.4

DPS 4.9 5.5 5.5 6.2 7.3

BV 141.5 162.7 188.5 216.9 250.0

ABV 138.5 158.4 183.0 210.7 243.2

Spreads (%)

Yield on Advances 10.5 10.3 10.1 10.0 10.0

Cost of Deposits 6.4 5.8 5.7 5.7 5.7

Net interest margins 3.3 3.4 3.5 3.5 3.6

Operating ratios (%)

Credit to Deposit 78.0 81.9 87.2 89.4 90.9

Cost to income 42.6 40.8 40.7 42.0 42.0

CASA 44.4 45.0 44.8 44.8 45.2

Non interest income / Total income 40.4 38.3 37.0 34.7 33.9

Return ratios (%)

RoE 18.5 17.4 17.8 17.1 17.3

RoA 1.7 1.7 1.7 1.6 1.6

Assets/Equity 11.2 10.1 10.2 10.5 10.7

Asset Quality ratios (%)

Gross NPA 1.2 1.3 1.4 1.3 1.2

Net NPA 0.4 0.4 0.5 0.4 0.4

Provision coverage 69.0 65.4 64.2 66.0 67.7

Slippage Ratio 0.8 0.9 0.8 1.0 0.9

Provision Expenses/ PPP 18.8 18.4 17.4 16.6 17.2

Credit Cost 1.0 1.1 1.0 0.9 0.9

Growth Ratios (%)

Net interest income 20.6 23.6 19.0 16.8 18.9

PPP 25.2 23.1 16.8 10.3 17.4

PAT 22.1 20.0 18.3 11.7 16.5

Advances 16.0 16.8 22.2 19.0 20.0

Deposits 14.8 11.2 14.8 16.0 18.0

Capital Adequacy Ratio (%)

Tier I Capital 12.2 12.6 12.1 12.3 12.1

Tier II Capital 4.8 3.5 3.0 3.1 2.7

Total 17.0 16.1 15.1 15.3 14.8

Valuation ratios (x)

P/E 22.4 18.7 16.0 14.3 12.3

P/BV 3.5 3.0 2.6 2.3 2.0

P/ABV 3.6 3.1 2.7 2.4 2.0

Source: Axis Bank, Karvy Stock Broking

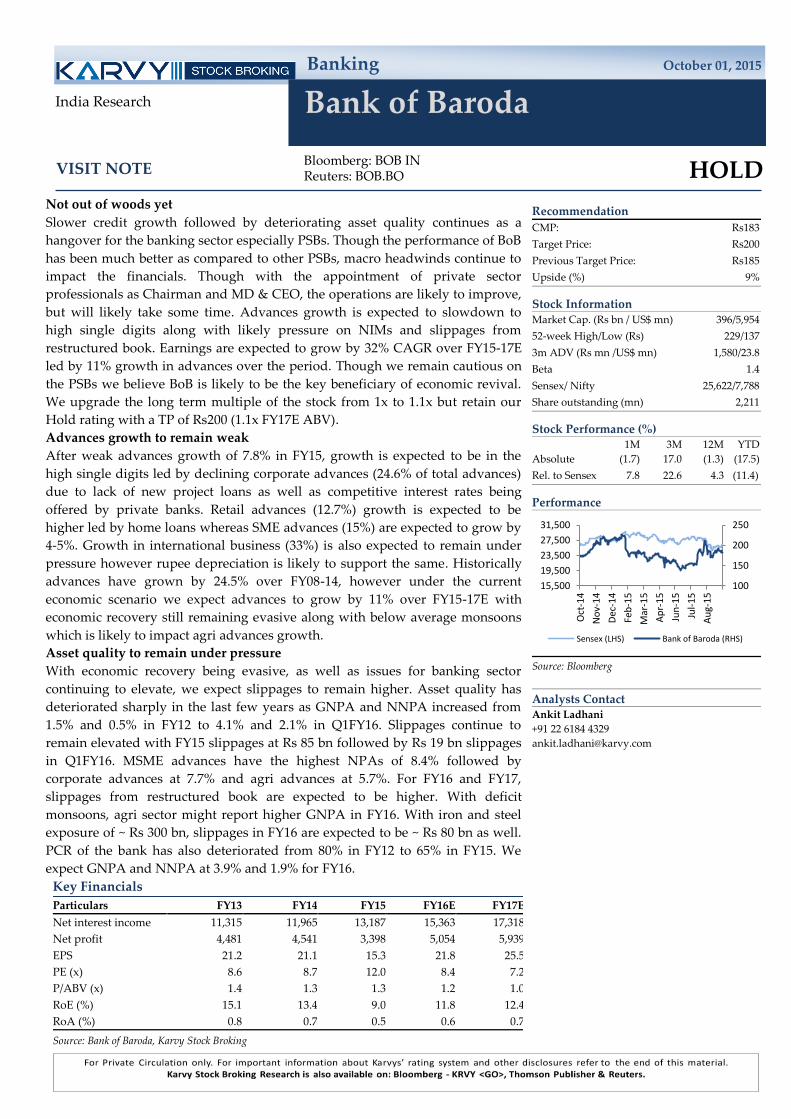

Banking October 01, 2015

Bank of Baroda

Bloomberg: BOB IN Reuters: BOB.BO

HOLD

India Research

VISIT NOTE

Recommendation

CMP: Rs183

Target Price: Rs200

Previous Target Price: Rs185

Upside (%) 9%

Stock Information Market Cap. (Rs bn / US$ mn) 396/5,954

52-week High/Low (Rs) 229/137

3m ADV (Rs mn /US$ mn) 1,580/23.8

Beta 1.4

Sensex/ Nifty 25,622/7,788

Share outstanding (mn) 2,211

Stock Performance (%) 1M 3M 12M YTD

Absolute (1.7) 17.0 (1.3) (17.5)

Rel. to Sensex 7.8 22.6 4.3 (11.4)

Performance

Source: Bloomberg

Analysts Contact Ankit Ladhani

+91 22 6184 4329

100

150

200

250

15,500

19,500

23,500

27,500

31,500

Oct

-14

No

v-1

4

Dec

-14

Feb

-15

Mar

-15

Ap

r-1

5

Jun

-15

Jul-

15

Au

g-1

5

Sensex (LHS) Bank of Baroda (RHS)

Not out of woods yet

Slower credit growth followed by deteriorating asset quality continues as a

hangover for the banking sector especially PSBs. Though the performance of BoB

has been much better as compared to other PSBs, macro headwinds continue to

impact the financials. Though with the appointment of private sector

professionals as Chairman and MD & CEO, the operations are likely to improve,

but will likely take some time. Advances growth is expected to slowdown to

high single digits along with likely pressure on NIMs and slippages from

restructured book. Earnings are expected to grow by 32% CAGR over FY15-17E

led by 11% growth in advances over the period. Though we remain cautious on

the PSBs we believe BoB is likely to be the key beneficiary of economic revival.

We upgrade the long term multiple of the stock from 1x to 1.1x but retain our

Hold rating with a TP of Rs200 (1.1x FY17E ABV).

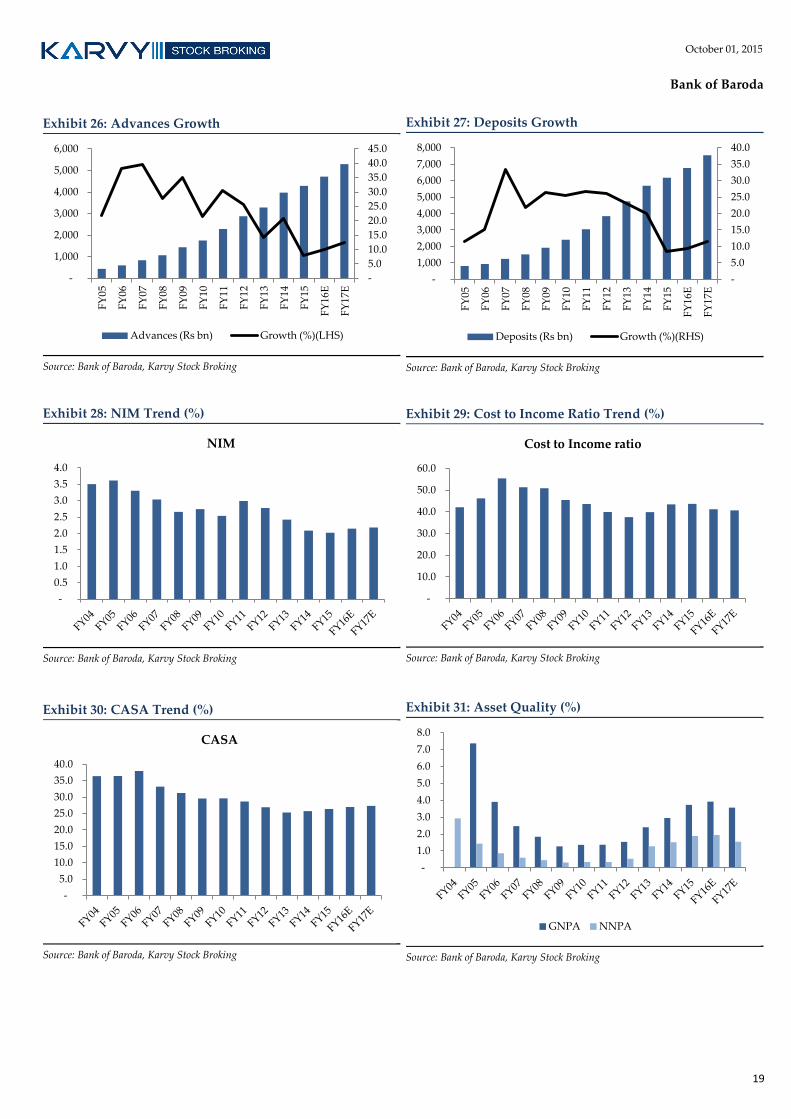

Advances growth to remain weak

After weak advances growth of 7.8% in FY15, growth is expected to be in the

high single digits led by declining corporate advances (24.6% of total advances)

due to lack of new project loans as well as competitive interest rates being

offered by private banks. Retail advances (12.7%) growth is expected to be

higher led by home loans whereas SME advances (15%) are expected to grow by

4-5%. Growth in international business (33%) is also expected to remain under

pressure however rupee depreciation is likely to support the same. Historically

advances have grown by 24.5% over FY08-14, however under the current

economic scenario we expect advances to grow by 11% over FY15-17E with

economic recovery still remaining evasive along with below average monsoons

which is likely to impact agri advances growth.

Asset quality to remain under pressure

With economic recovery being evasive, as well as issues for banking sector

continuing to elevate, we expect slippages to remain higher. Asset quality has

deteriorated sharply in the last few years as GNPA and NNPA increased from

1.5% and 0.5% in FY12 to 4.1% and 2.1% in Q1FY16. Slippages continue to

remain elevated with FY15 slippages at Rs 85 bn followed by Rs 19 bn slippages

in Q1FY16. MSME advances have the highest NPAs of 8.4% followed by

corporate advances at 7.7% and agri advances at 5.7%. For FY16 and FY17,

slippages from restructured book are expected to be higher. With deficit

monsoons, agri sector might report higher GNPA in FY16. With iron and steel

exposure of ~ Rs 300 bn, slippages in FY16 are expected to be ~ Rs 80 bn as well.

PCR of the bank has also deteriorated from 80% in FY12 to 65% in FY15. We

expect GNPA and NNPA at 3.9% and 1.9% for FY16.

Key Financials

Particulars FY13 FY14 FY15 FY16E FY17E

Net interest income 11,315 11,965 13,187 15,363 17,318

Net profit 4,481 4,541 3,398 5,054 5,939

EPS 21.2 21.1 15.3 21.8 25.5

PE (x) 8.6 8.7 12.0 8.4 7.2

P/ABV (x) 1.4 1.3 1.3 1.2 1.0

RoE (%) 15.1 13.4 9.0 11.8 12.4

RoA (%) 0.8 0.7 0.5 0.6 0.7

Source: Bank of Baroda, Karvy Stock Broking

18

October 01, 2015

Bank of Baroda

CASA focus continues but intensive competition likely

With increased competition from other banks for improving liability

franchise, as well as new payment banks coming in and Bandhan having a

strong presence in rural India to start its banking operations, we believe

that banks are likely to find improving the CASA share a challenge

especially SA deposits emanating from the tier IV- VI cities. We believe

that bank will maintain its CASA share at 27% over FY15-17E. NIMs of the

banks are also expected to be hit in FY17, with base rate calculation

expected to be done based on marginal cost of funds. Though rate cuts are

expected going ahead, NIMs are likely to remain flat to marginally

negative.

Adequately capitalized

Bank is adequately capitalized for future growth with CAR of 12% and tier

I capital of 9.4%. The bank has also been allotted capital by GoI of Rs 17.9

bn @ Rs 193 per share. As the bank is currently looking at slower advances

growth, it is unlikely to require additional capital till FY17 end.

Valuation

In- line with the slowdown in economy, advances growth is likely to

remain weak. Though with the appointment of private sector professionals

as Chairman and MD & CEO, the operations are likely to improve,

recovery is still a long way off. Advances growth is expected to slowdown

to high single digits along with likely pressure on NIMs and slippages

from restructured book are likely to lead to earnings growth of 32% over

FY15-17E (lower base in FY15) led by 11% growth in advances over the

period. Though we remain cautious on the PSBs we believe BoB is likely to

be the key beneficiary of economic revival. We upgrade the long term

multiple of the stock from 1x to 1.1x but retain our Hold rating with a TP of

Rs200 (1.1x FY17E ABV).

19

October 01, 2015

Bank of Baroda

Exhibit 26: Advances Growth

Source: Bank of Baroda, Karvy Stock Broking

Exhibit 27: Deposits Growth

Source: Bank of Baroda, Karvy Stock Broking

Exhibit 28: NIM Trend (%)

Source: Bank of Baroda, Karvy Stock Broking

Exhibit 29: Cost to Income Ratio Trend (%)

Source: Bank of Baroda, Karvy Stock Broking

Exhibit 30: CASA Trend (%)

Source: Bank of Baroda, Karvy Stock Broking

Exhibit 31: Asset Quality (%)

Source: Bank of Baroda, Karvy Stock Broking

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

-

1,000

2,000

3,000

4,000

5,000

6,000

FY

05

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16E

FY

17E

Advances (Rs bn) Growth (%)(LHS)

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

FY

05

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

FY

16E

FY

17E

Deposits (Rs bn) Growth (%)(RHS)

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

NIM

-

10.0

20.0

30.0

40.0

50.0

60.0

Cost to Income ratio

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

CASA

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

GNPA NNPA

20

October 01, 2015

Bank of Baroda

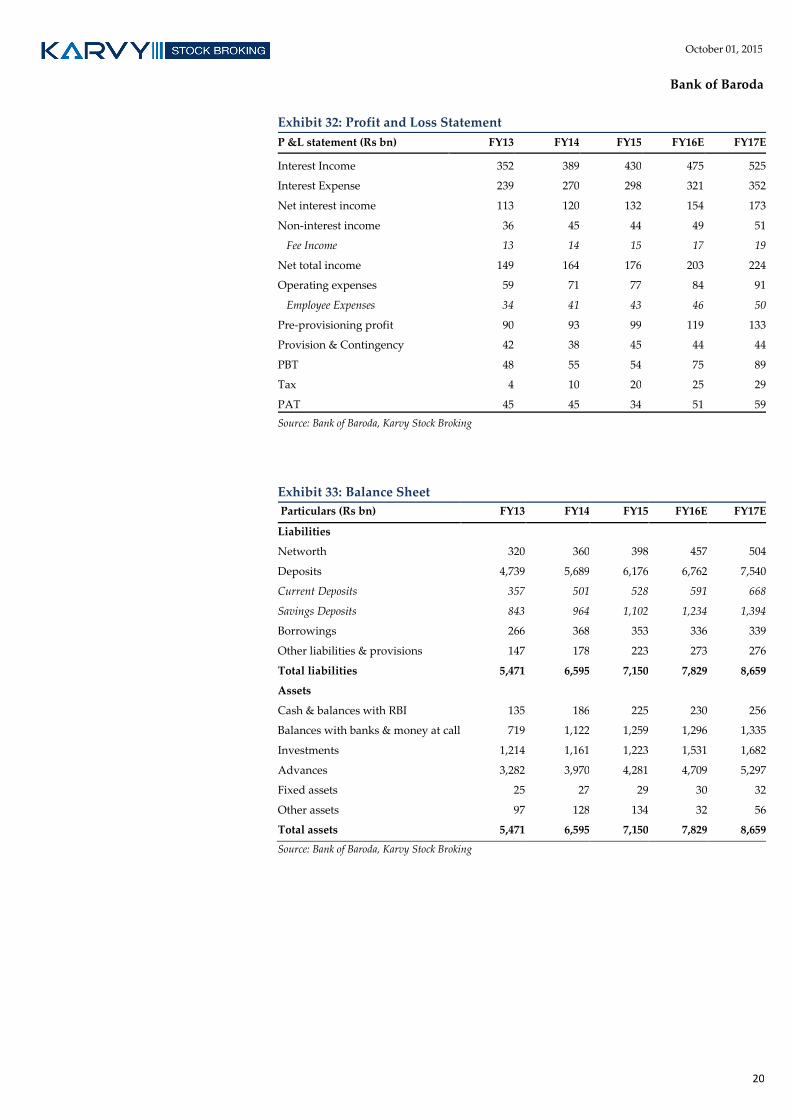

Exhibit 32: Profit and Loss Statement

P &L statement (Rs bn) FY13 FY14 FY15 FY16E FY17E

Interest Income 352 389 430 475 525

Interest Expense 239 270 298 321 352

Net interest income 113 120 132 154 173

Non-interest income 36 45 44 49 51

Fee Income 13 14 15 17 19

Net total income 149 164 176 203 224

Operating expenses 59 71 77 84 91

Employee Expenses 34 41 43 46 50

Pre-provisioning profit 90 93 99 119 133

Provision & Contingency 42 38 45 44 44

PBT 48 55 54 75 89

Tax 4 10 20 25 29

PAT 45 45 34 51 59

Source: Bank of Baroda, Karvy Stock Broking

Exhibit 33: Balance Sheet

Particulars (Rs bn) FY13 FY14 FY15 FY16E FY17E

Liabilities

Networth 320 360 398 457 504

Deposits 4,739 5,689 6,176 6,762 7,540

Current Deposits 357 501 528 591 668

Savings Deposits 843 964 1,102 1,234 1,394

Borrowings 266 368 353 336 339

Other liabilities & provisions 147 178 223 273 276

Total liabilities 5,471 6,595 7,150 7,829 8,659

Assets

Cash & balances with RBI 135 186 225 230 256

Balances with banks & money at call 719 1,122 1,259 1,296 1,335

Investments 1,214 1,161 1,223 1,531 1,682

Advances 3,282 3,970 4,281 4,709 5,297

Fixed assets 25 27 29 30 32

Other assets 97 128 134 32 56

Total assets 5,471 6,595 7,150 7,829 8,659

Source: Bank of Baroda, Karvy Stock Broking

21

October 01, 2015

Bank of Baroda

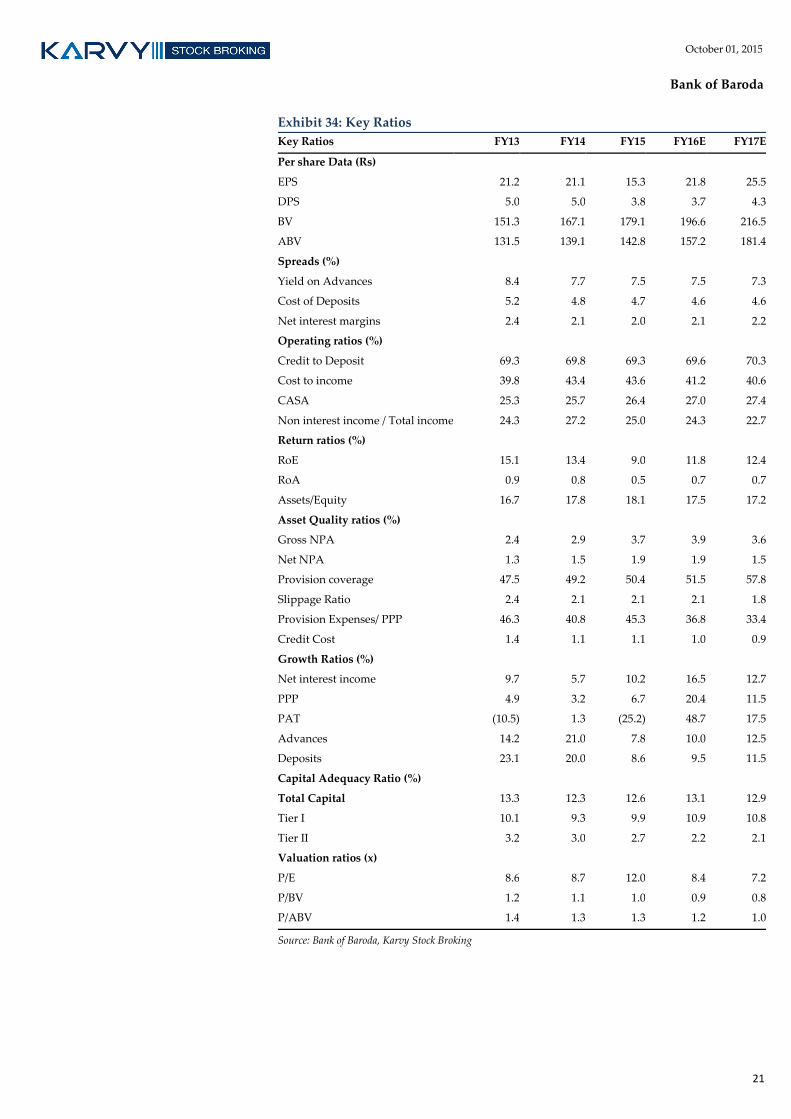

Exhibit 34: Key Ratios

Key Ratios FY13 FY14 FY15 FY16E FY17E

Per share Data (Rs)

EPS 21.2 21.1 15.3 21.8 25.5

DPS 5.0 5.0 3.8 3.7 4.3

BV 151.3 167.1 179.1 196.6 216.5

ABV 131.5 139.1 142.8 157.2 181.4

Spreads (%)

Yield on Advances 8.4 7.7 7.5 7.5 7.3

Cost of Deposits 5.2 4.8 4.7 4.6 4.6

Net interest margins 2.4 2.1 2.0 2.1 2.2

Operating ratios (%)

Credit to Deposit 69.3 69.8 69.3 69.6 70.3

Cost to income 39.8 43.4 43.6 41.2 40.6

CASA 25.3 25.7 26.4 27.0 27.4

Non interest income / Total income 24.3 27.2 25.0 24.3 22.7

Return ratios (%)

RoE 15.1 13.4 9.0 11.8 12.4

RoA 0.9 0.8 0.5 0.7 0.7

Assets/Equity 16.7 17.8 18.1 17.5 17.2

Asset Quality ratios (%)

Gross NPA 2.4 2.9 3.7 3.9 3.6

Net NPA 1.3 1.5 1.9 1.9 1.5

Provision coverage 47.5 49.2 50.4 51.5 57.8

Slippage Ratio 2.4 2.1 2.1 2.1 1.8

Provision Expenses/ PPP 46.3 40.8 45.3 36.8 33.4

Credit Cost 1.4 1.1 1.1 1.0 0.9

Growth Ratios (%)

Net interest income 9.7 5.7 10.2 16.5 12.7

PPP 4.9 3.2 6.7 20.4 11.5

PAT (10.5) 1.3 (25.2) 48.7 17.5

Advances 14.2 21.0 7.8 10.0 12.5

Deposits 23.1 20.0 8.6 9.5 11.5

Capital Adequacy Ratio (%)

Total Capital 13.3 12.3 12.6 13.1 12.9

Tier I 10.1 9.3 9.9 10.9 10.8

Tier II 3.2 3.0 2.7 2.2 2.1

Valuation ratios (x)

P/E 8.6 8.7 12.0 8.4 7.2

P/BV 1.2 1.1 1.0 0.9 0.8

P/ABV 1.4 1.3 1.3 1.2 1.0

Source: Bank of Baroda, Karvy Stock Broking

Banking October 01, 2015

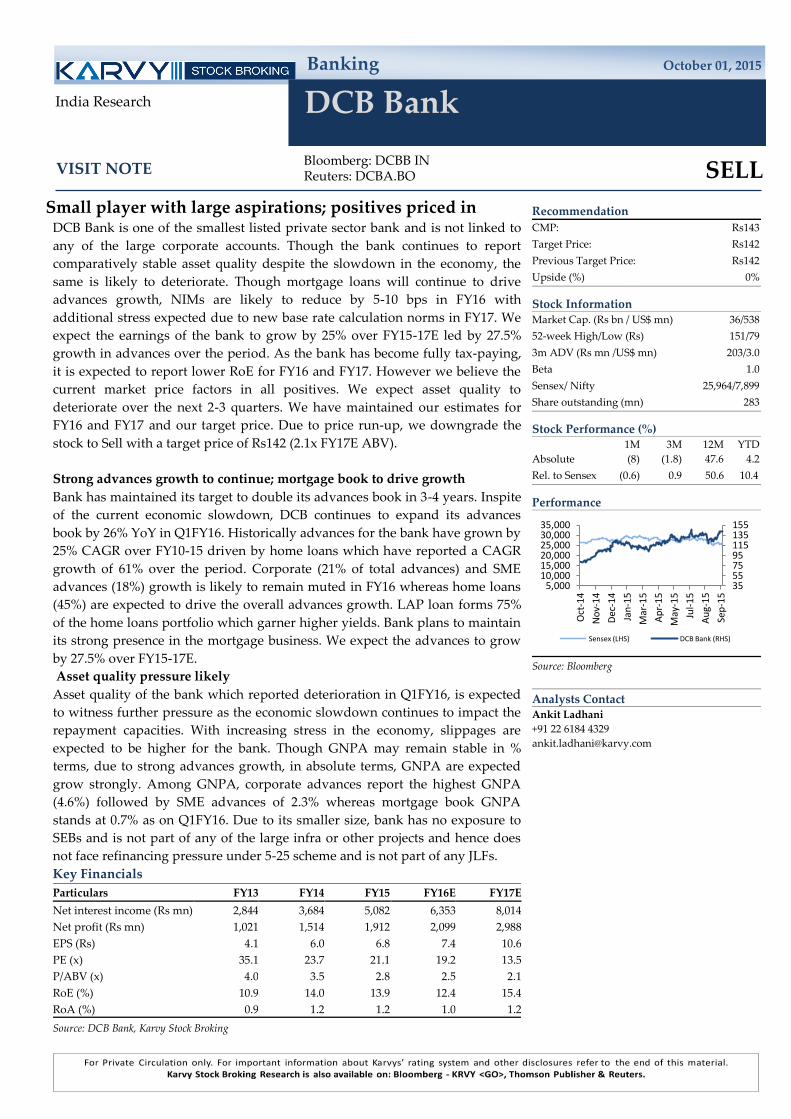

DCB Bank

Bloomberg: DCBB IN Reuters: DCBA.BO

SELL

India Research

VISIT NOTE

Recommendation

CMP: Rs143

Target Price: Rs142

Previous Target Price: Rs142

Upside (%) 0%

Stock Information Market Cap. (Rs bn / US$ mn) 36/538

52-week High/Low (Rs) 151/79

3m ADV (Rs mn /US$ mn) 203/3.0

Beta 1.0

Sensex/ Nifty 25,964/7,899

Share outstanding (mn) 283

Stock Performance (%) 1M 3M 12M YTD

Absolute (8) (1.8) 47.6 4.2

Rel. to Sensex (0.6) 0.9 50.6 10.4

Performance

Source: Bloomberg

Analysts Contact Ankit Ladhani

+91 22 6184 4329

35 55 75 95 115 135 155

5,000 10,000 15,000 20,000 25,000 30,000 35,000

Oct

-14

No

v-1

4

Dec

-14

Jan

-15

Mar

-15

Ap

r-1

5

May

-15

Jul-

15

Au

g-1

5

Sep

-15

Sensex (LHS) DCB Bank (RHS)

Small player with large aspirations; positives priced in DCB Bank is one of the smallest listed private sector bank and is not linked to

any of the large corporate accounts. Though the bank continues to report

comparatively stable asset quality despite the slowdown in the economy, the

same is likely to deteriorate. Though mortgage loans will continue to drive

advances growth, NIMs are likely to reduce by 5-10 bps in FY16 with

additional stress expected due to new base rate calculation norms in FY17. We

expect the earnings of the bank to grow by 25% over FY15-17E led by 27.5%

growth in advances over the period. As the bank has become fully tax-paying,

it is expected to report lower RoE for FY16 and FY17. However we believe the

current market price factors in all positives. We expect asset quality to

deteriorate over the next 2-3 quarters. We have maintained our estimates for

FY16 and FY17 and our target price. Due to price run-up, we downgrade the

stock to Sell with a target price of Rs142 (2.1x FY17E ABV).

Strong advances growth to continue; mortgage book to drive growth

Bank has maintained its target to double its advances book in 3-4 years. Inspite

of the current economic slowdown, DCB continues to expand its advances

book by 26% YoY in Q1FY16. Historically advances for the bank have grown by

25% CAGR over FY10-15 driven by home loans which have reported a CAGR

growth of 61% over the period. Corporate (21% of total advances) and SME

advances (18%) growth is likely to remain muted in FY16 whereas home loans

(45%) are expected to drive the overall advances growth. LAP loan forms 75%

of the home loans portfolio which garner higher yields. Bank plans to maintain

its strong presence in the mortgage business. We expect the advances to grow

by 27.5% over FY15-17E.

Asset quality pressure likely

Asset quality of the bank which reported deterioration in Q1FY16, is expected

to witness further pressure as the economic slowdown continues to impact the

repayment capacities. With increasing stress in the economy, slippages are

expected to be higher for the bank. Though GNPA may remain stable in %

terms, due to strong advances growth, in absolute terms, GNPA are expected

grow strongly. Among GNPA, corporate advances report the highest GNPA

(4.6%) followed by SME advances of 2.3% whereas mortgage book GNPA

stands at 0.7% as on Q1FY16. Due to its smaller size, bank has no exposure to

SEBs and is not part of any of the large infra or other projects and hence does

not face refinancing pressure under 5-25 scheme and is not part of any JLFs.

Key Financials

Particulars FY13 FY14 FY15 FY16E FY17E

Net interest income (Rs mn) 2,844 3,684 5,082 6,353 8,014

Net profit (Rs mn) 1,021 1,514 1,912 2,099 2,988

EPS (Rs) 4.1 6.0 6.8 7.4 10.6

PE (x) 35.1 23.7 21.1 19.2 13.5

P/ABV (x) 4.0 3.5 2.8 2.5 2.1

RoE (%) 10.9 14.0 13.9 12.4 15.4

RoA (%) 0.9 1.2 1.2 1.0 1.2

Source: DCB Bank, Karvy Stock Broking

23

October 01, 2015

DCB Bank

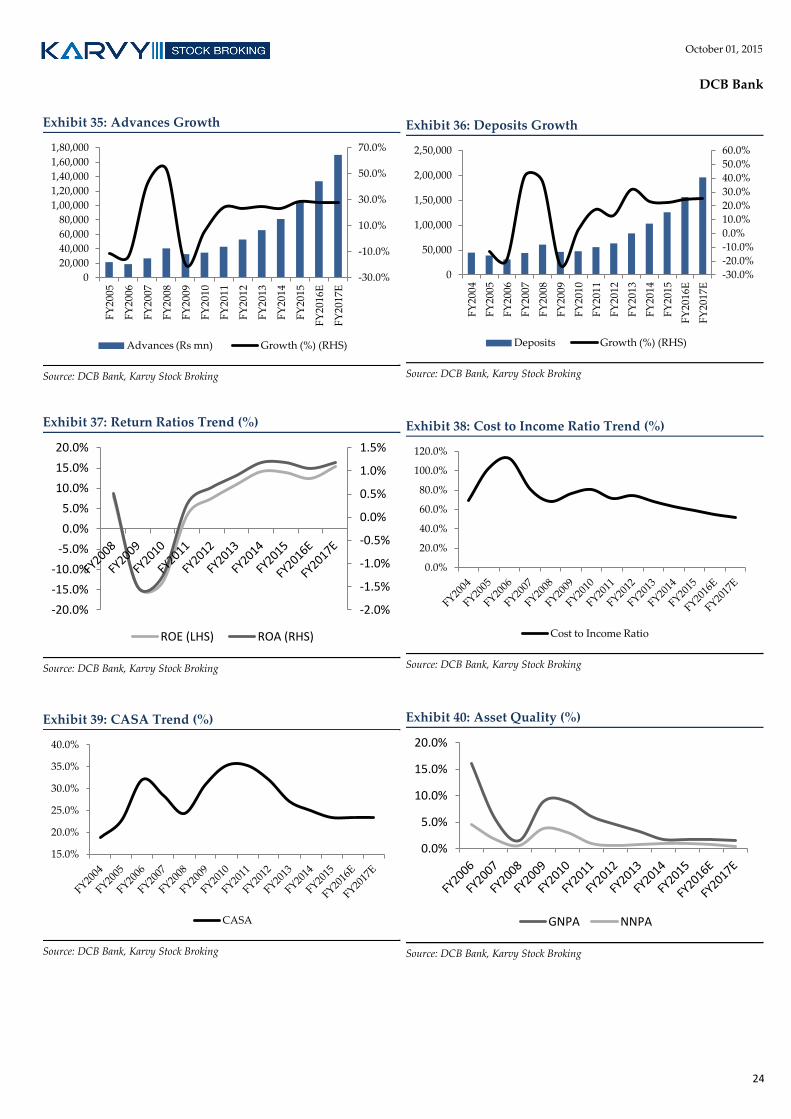

Weak retail liability franchise

In- line with sharp balance sheet expansion, deposits grew by 25% over

FY11-15. Bank focused on balance sheet growth leading to slower CASA

growth. During the period DCB has grown its term deposits book by 22.4%

vs CA and SA deposits growth of 4.2% and 15% leading to a decline in

CASA share to 23.4% in Q1FY16 from 35.2% in FY11. Bank is rapidly

expanding its branch network to increase the share of retail deposits,

however as the overall advances growth is expected to remain higher, we

expect CASA ratio to remain lower.

Aggressive branch expansion likely to keep opex higher

Bank is planning to increase its branch network by 25-30 branches per year

on a base of 154 branches in FY15. The aggressive branch expansion

strategy will keep the operating expenses growth higher. Operating

expenses are expected to grow at 17% CAGR over FY15-17E. However the

sharp advances growth will keep the total income higher leading to cost to

income ratio of 51% in FY17 vs 59% currently.

Adequately capitalized

DCB currently has CAR of 14.3% with tier I capital of 13.6%. We believe

that the bank is adequately capitalized for FY16 growth and that bank is

likely to raise capital in end FY16 or in FY17.

Valuation and Outlook

Though bank continues to report a strong growth in its advances and NII,

the earnings growth is expected to be lower based on higher credit cost and

income tax payments. Return ratios are expected to improve in FY16. We

expect the earnings of the bank to grow by 25% over FY15-17E led by

27.5% growth in advances over the period. As the bank has become fully

tax paying, it is expected to report lower RoE for FY16 and FY17. However

we believe the current market price factors in all positives. We expect asset

quality to deteriorate over the next 2-3 quarters. We have maintained our

estimates for FY16 and FY17 and our target price. Due to price run-up, we

downgrade the stock to Sell with a target price of Rs142 (2.1x FY17E ABV).

24

October 01, 2015

DCB Bank

Exhibit 35: Advances Growth

Source: DCB Bank, Karvy Stock Broking

Exhibit 36: Deposits Growth

Source: DCB Bank, Karvy Stock Broking

Exhibit 37: Return Ratios Trend (%)

Source: DCB Bank, Karvy Stock Broking

Exhibit 38: Cost to Income Ratio Trend (%)

Source: DCB Bank, Karvy Stock Broking

Exhibit 39: CASA Trend (%)

Source: DCB Bank, Karvy Stock Broking

Exhibit 40: Asset Quality (%)

Source: DCB Bank, Karvy Stock Broking

-30.0%

-10.0%

10.0%

30.0%

50.0%

70.0%

0

20,000

40,000

60,000

80,000

1,00,000

1,20,000

1,40,000

1,60,000

1,80,000

FY

20

05

FY

20

06

FY

20

07

FY

20

08

FY

20

09

FY

20

10

FY

20

11

FY

20

12

FY

20

13

FY

20

14

FY

20

15

FY

2016

E

FY

2017

E

Advances (Rs mn) Growth (%) (RHS)

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

0

50,000

1,00,000

1,50,000

2,00,000

2,50,000

FY

20

04

FY

20

05

FY

20

06

FY

20

07

FY

20

08

FY

20

09

FY

20

10

FY

20

11

FY

20

12

FY

20

13

FY

20

14

FY

20

15

FY

2016

E

FY

2017

E

Deposits Growth (%) (RHS)

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

ROE (LHS) ROA (RHS)

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

Cost to Income Ratio

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

CASA

0.0%

5.0%

10.0%

15.0%

20.0%

GNPA NNPA

25

October 01, 2015

DCB Bank

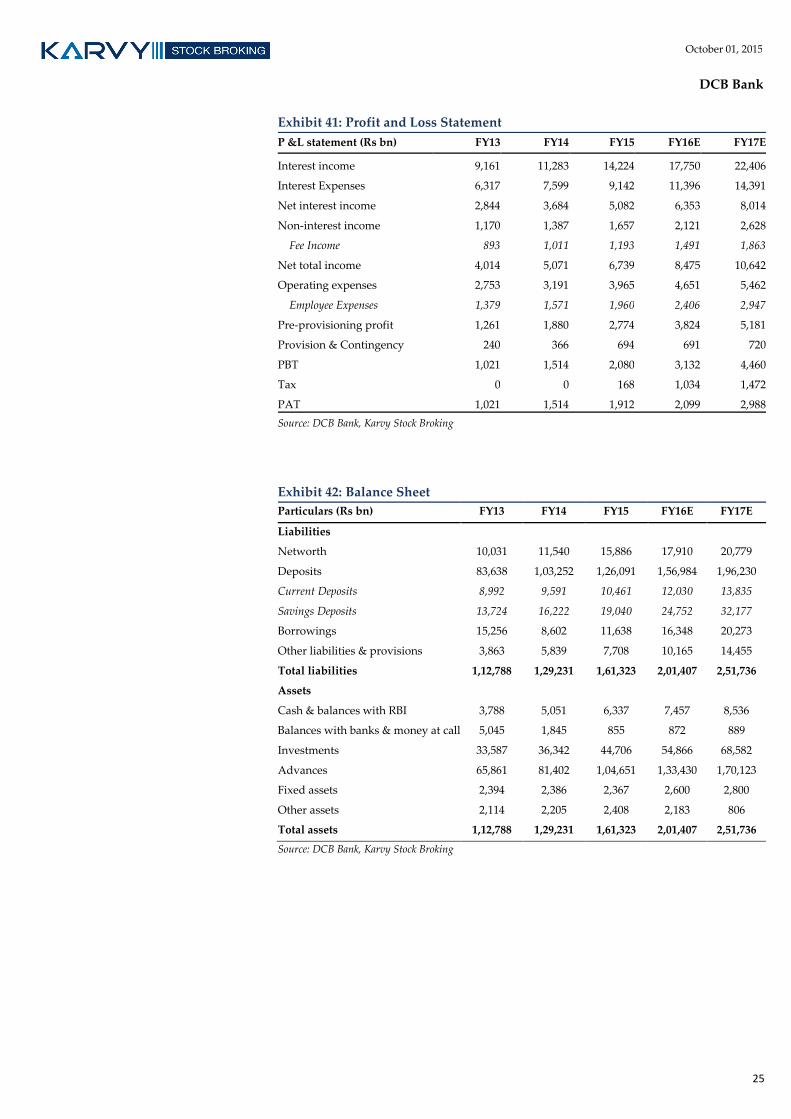

Exhibit 41: Profit and Loss Statement

P &L statement (Rs bn) FY13 FY14 FY15 FY16E FY17E

Interest income 9,161 11,283 14,224 17,750 22,406

Interest Expenses 6,317 7,599 9,142 11,396 14,391

Net interest income 2,844 3,684 5,082 6,353 8,014

Non-interest income 1,170 1,387 1,657 2,121 2,628

Fee Income 893 1,011 1,193 1,491 1,863

Net total income 4,014 5,071 6,739 8,475 10,642

Operating expenses 2,753 3,191 3,965 4,651 5,462

Employee Expenses 1,379 1,571 1,960 2,406 2,947

Pre-provisioning profit 1,261 1,880 2,774 3,824 5,181

Provision & Contingency 240 366 694 691 720

PBT 1,021 1,514 2,080 3,132 4,460

Tax 0 0 168 1,034 1,472

PAT 1,021 1,514 1,912 2,099 2,988

Source: DCB Bank, Karvy Stock Broking

Exhibit 42: Balance Sheet

Particulars (Rs bn) FY13 FY14 FY15 FY16E FY17E

Liabilities

Networth 10,031 11,540 15,886 17,910 20,779

Deposits 83,638 1,03,252 1,26,091 1,56,984 1,96,230

Current Deposits 8,992 9,591 10,461 12,030 13,835

Savings Deposits 13,724 16,222 19,040 24,752 32,177

Borrowings 15,256 8,602 11,638 16,348 20,273

Other liabilities & provisions 3,863 5,839 7,708 10,165 14,455

Total liabilities 1,12,788 1,29,231 1,61,323 2,01,407 2,51,736

Assets

Cash & balances with RBI 3,788 5,051 6,337 7,457 8,536

Balances with banks & money at call 5,045 1,845 855 872 889

Investments 33,587 36,342 44,706 54,866 68,582

Advances 65,861 81,402 1,04,651 1,33,430 1,70,123

Fixed assets 2,394 2,386 2,367 2,600 2,800

Other assets 2,114 2,205 2,408 2,183 806

Total assets 1,12,788 1,29,231 1,61,323 2,01,407 2,51,736

Source: DCB Bank, Karvy Stock Broking

26

October 01, 2015

DCB Bank

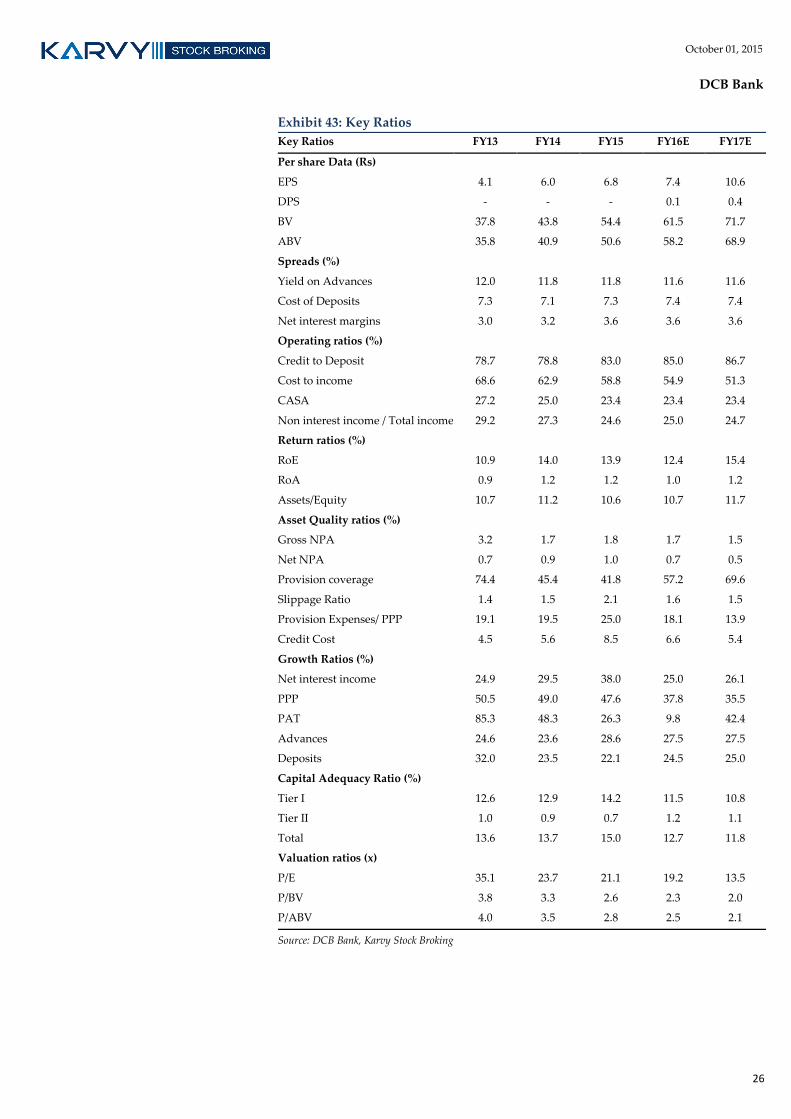

Exhibit 43: Key Ratios

Key Ratios FY13 FY14 FY15 FY16E FY17E

Per share Data (Rs)

EPS 4.1 6.0 6.8 7.4 10.6

DPS - - - 0.1 0.4

BV 37.8 43.8 54.4 61.5 71.7

ABV 35.8 40.9 50.6 58.2 68.9

Spreads (%)

Yield on Advances 12.0 11.8 11.8 11.6 11.6

Cost of Deposits 7.3 7.1 7.3 7.4 7.4

Net interest margins 3.0 3.2 3.6 3.6 3.6

Operating ratios (%)

Credit to Deposit 78.7 78.8 83.0 85.0 86.7

Cost to income 68.6 62.9 58.8 54.9 51.3

CASA 27.2 25.0 23.4 23.4 23.4

Non interest income / Total income 29.2 27.3 24.6 25.0 24.7

Return ratios (%)

RoE 10.9 14.0 13.9 12.4 15.4

RoA 0.9 1.2 1.2 1.0 1.2

Assets/Equity 10.7 11.2 10.6 10.7 11.7

Asset Quality ratios (%)

Gross NPA 3.2 1.7 1.8 1.7 1.5

Net NPA 0.7 0.9 1.0 0.7 0.5

Provision coverage 74.4 45.4 41.8 57.2 69.6

Slippage Ratio 1.4 1.5 2.1 1.6 1.5

Provision Expenses/ PPP 19.1 19.5 25.0 18.1 13.9

Credit Cost 4.5 5.6 8.5 6.6 5.4

Growth Ratios (%)

Net interest income 24.9 29.5 38.0 25.0 26.1

PPP 50.5 49.0 47.6 37.8 35.5

PAT 85.3 48.3 26.3 9.8 42.4

Advances 24.6 23.6 28.6 27.5 27.5

Deposits 32.0 23.5 22.1 24.5 25.0

Capital Adequacy Ratio (%)

Tier I 12.6 12.9 14.2 11.5 10.8

Tier II 1.0 0.9 0.7 1.2 1.1

Total 13.6 13.7 15.0 12.7 11.8

Valuation ratios (x)

P/E 35.1 23.7 21.1 19.2 13.5

P/BV 3.8 3.3 2.6 2.3 2.0

P/ABV 4.0 3.5 2.8 2.5 2.1

Source: DCB Bank, Karvy Stock Broking

Banking October 01, 2015

HDFC Bank

Bloomberg: HDFCB IN Reuters: HDBK.BO

BUY

India Research

VISIT NOTE

Recommendation

CMP: Rs1,069

Target Price: Rs1,198

Previous Target Price: Rs1,198

Upside (%) 12%

Stock Information Market Cap. (Rs bn / US$ mn) 2,545/38,283

52-week High/Low (Rs) 1,128/842

3m ADV (Rs mn /US$ mn) 1,729/26.0

Beta 0.9

Sensex/ Nifty 25,622/7,788

Share outstanding (mn) 2,517

Stock Performance (%) 1M 3M 12M YTD

Absolute (7.6) (0.5) 17.9 6.2

Rel. to Sensex 1.3 4.3 24.5 14.0

Performance

Source: Bloomberg

Analysts Contact Ankit Ladhani

+91 22 6184 4329

550 650 750 850 950 1,050 1,150

15,500

19,500

23,500

27,500

31,500

Oct

-14

No

v-1

4

Dec

-14

Feb

-15

Mar

-15

Ap

r-1

5

Jun

-15

Jul-

15

Au

g-1

5

Sensex (LHS) HDFC Bank (RHS)

Core operations remain intact; upgrade to Buy HDFC Bank, the 2nd largest bank in the private Indian banking space and has

reported consistent and strong operating performance over the past several

years. Inspite of the economic slowdown in the recent years, HDFC Bank has

reported strong advances growth, consistent NIMs and stable asset quality.

Strong liability franchise coupled with healthy retail advances portfolio and

strong fee income growth has driven the earnings CAGR growth of 28% over

FY10-15 led by 23% advances growth over the period. We expect earnings to

grow by 24% CAGR over FY15-17E led by 22% growth in advances over the

period. We maintain our positive bias on the stock and upgrade the bank to Buy

post the recent price correction and maintain our price target of Rs1198 (3.6x

FY17E ABV).

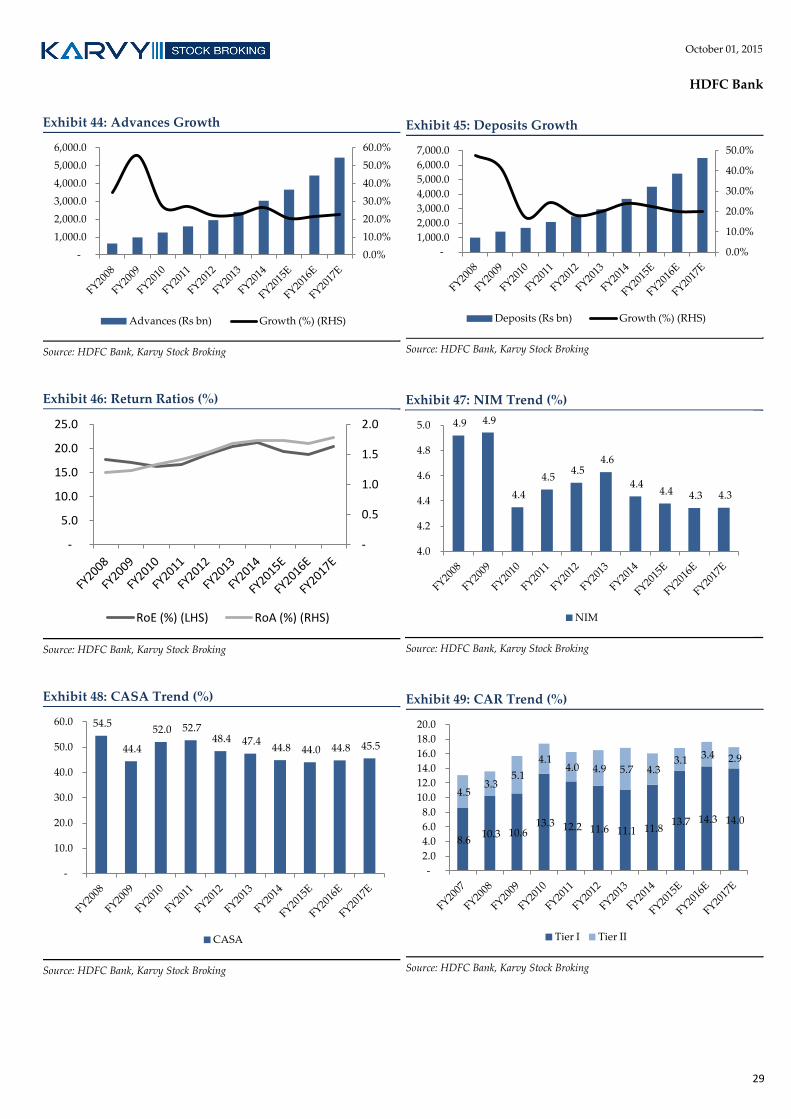

Advances growth to remain healthy

Bank has historically been reporting much higher growth as compared to the

industry as it grew by 23% over FY10-15 and continues to remain focused on

both corporate (47% of domestic loans) and retail advances (53%). In the current

economic scenario, with absence of new project by companies, bank focuses on

working capital loans. Amongst retail advances, bank has been growing strongly

in the credit card, personal loan and mortgage loan segment which have grown

by 33.2%/ 24.2%/ 22.6% CAGR over FY10-15. Auto and CV loans have grown by

~17% over the period. Overseas advances (8% of total advances) have also

reported a strong growth in the past couple of years and have grown from 4% in

FY13. Bank expects the advances growth to be higher than industry and

continues to focus on quality advances rather than targeting growth from a

specific sector. We expect the advances to grow by ~22% over FY15-17E.

Asset quality remains impeccable

Inspite of the current economic scenario, asset quality of HDFC Bank remains

intact. With GNPA of 1% and restructured assets book of 0.1%, asset quality

remains stable and best in class. GNPA for the bank have been around 1% for

the past several years. With some of the best credit appraisal and monitoring

policies we believe that HDFC Bank will be able to maintain its asset quality

going ahead. Though the bank continues to expand in the unsecured personal

loans and credit card segment, the same has helped the bank in maintaining its

higher NIMs and given the bank’s track record, we believe the risk reward is

quite conducive.

Key Financials

Particulars FY13 FY14 FY15 FY16E FY17E

Net interest income (Rs bn) 158 185 224 268 324

Net profit (Rs bn) 67 85 102 125 158

EPS (Rs) 28.3 35.3 40.8 49.9 63.0

PE (x) 37.8 30.2 26.2 21.4 17.0

P/ABV (x) 7.1 6.0 4.4 3.8 3.3

RoE (%) 20.3 21.3 19.4 18.7 20.3

RoA (%) 1.7 1.7 1.7 1.7 1.8

Source: HDFC Bank, Karvy Stock Broking

28

October 01, 2015

HDFC Bank

CASA ratio to improve to 42-43% by FY16

Strong liability is one of the key contributors to the strong NIMs that the bank has

been able to maintain. Bank has been able to maintain its CASA ratio in the range

of 40-44%. CA deposits have grown by 15% over FY10-15 whereas SA deposits

have grown by 20%. However for Q1FY16, CASA ratio has gone below 40% for the

first time in many years led by 38% YoY and 16% QoQ growth in term deposits

whereas CA and SA deposits grew by 23% and 18%. We expect the CASA ratio of

the bank to bounce back as the bank has already reduced its deposits rate along

with Rs 200 bn of FCNR deposits which are to mature in the next 15 – 18 months.

NIM likely to remain stable inspite of base rate cut

HDFC Bank surprised the street with a base rate cut of 35 bps in August end to

9.35%. Inspite of varying interest rate cycles over the years, HDFC Bank has been

able to maintain its strong NIMs in excess of 4.4% post FY07. Bank is already

calculating its base rate using marginal cost of funds and does not expect any

significant competition from payment banks. Though we expect a marginal dip in

NIM in Q2 due to the base rate cut, bank only has ~25% of advances based on

floating rate products. We expect the NIMs for FY16 to be stable at 4.3%.

CAR remains healthy

CAR of the bank remains healthy at 15.7% with tier I capital of 12.8%. With the

phased implementation of the Basel III norms, we expect bank to remain

comfortable.

Healthy return ratios

HDFC Bank continues to maintain healthy return ratios with RoE and RoA of

19.4% and 1.7% in FY15 which continue to remain amongst the highest in the

industry. With strong return ratios, healthy advances book growth, stable NIMs

and impeccable asset quality we expect the return ratios of the bank to remain

stable going ahead as well.

Valuation and Outlook

Strong advances growth, consistent NIMs, strong core fee income growth and

stable asset quality are the key highlights for HDFC Bank. We expect earnings to

grow by 24% CAGR over FY15-17E led by 22% growth in advances over the

period. We maintain our positive bias on the stock and upgrade the stock to Buy

post the recent price correction and maintain our price target of Rs1198 (3.6x

FY17E ABV).

29

October 01, 2015

HDFC Bank

Exhibit 44: Advances Growth

Source: HDFC Bank, Karvy Stock Broking

Exhibit 45: Deposits Growth

Source: HDFC Bank, Karvy Stock Broking

Exhibit 46: Return Ratios (%)

Source: HDFC Bank, Karvy Stock Broking

Exhibit 47: NIM Trend (%)

Source: HDFC Bank, Karvy Stock Broking

Exhibit 48: CASA Trend (%)

Source: HDFC Bank, Karvy Stock Broking

Exhibit 49: CAR Trend (%)

Source: HDFC Bank, Karvy Stock Broking

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

-

1,000.0

2,000.0

3,000.0

4,000.0

5,000.0

6,000.0

Advances (Rs bn) Growth (%) (RHS)

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

-

1,000.0

2,000.0

3,000.0

4,000.0

5,000.0

6,000.0

7,000.0

Deposits (Rs bn) Growth (%) (RHS)

-

0.5

1.0

1.5

2.0

-

5.0

10.0

15.0

20.0

25.0

RoE (%) (LHS) RoA (%) (RHS)

4.9 4.9

4.4

4.5 4.5

4.6

4.4 4.4 4.3 4.3

4.0

4.2

4.4

4.6

4.8

5.0

NIM

54.5

44.4

52.0 52.7 48.4 47.4

44.8 44.0 44.8 45.5

-

10.0

20.0

30.0

40.0

50.0

60.0

CASA

8.6 10.3 10.6

13.3 12.2 11.6 11.1 11.8 13.7 14.3 14.0

4.5 3.3

5.1

4.1 4.0 4.9 5.7 4.3

3.1 3.4 2.9

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

Tier I Tier II

30

October 01, 2015

HDFC Bank

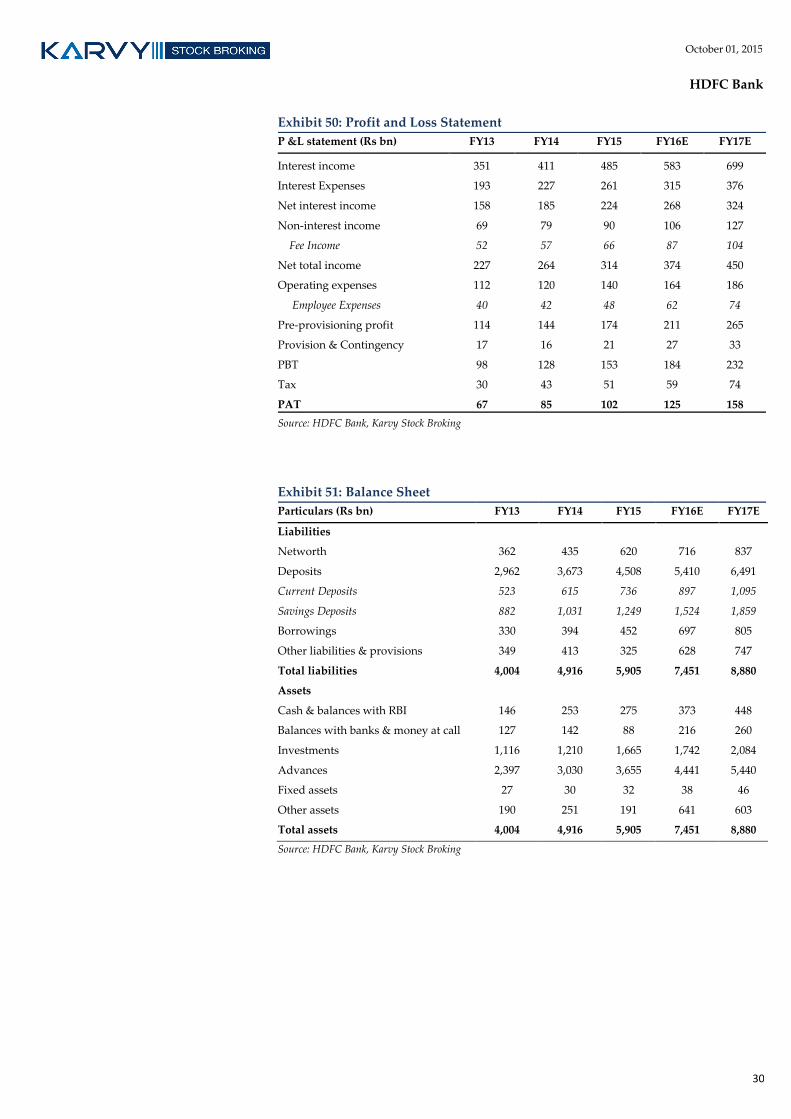

Exhibit 50: Profit and Loss Statement

P &L statement (Rs bn) FY13 FY14 FY15 FY16E FY17E

Interest income 351 411 485 583 699

Interest Expenses 193 227 261 315 376

Net interest income 158 185 224 268 324

Non-interest income 69 79 90 106 127

Fee Income 52 57 66 87 104

Net total income 227 264 314 374 450

Operating expenses 112 120 140 164 186

Employee Expenses 40 42 48 62 74

Pre-provisioning profit 114 144 174 211 265

Provision & Contingency 17 16 21 27 33

PBT 98 128 153 184 232

Tax 30 43 51 59 74

PAT 67 85 102 125 158

Source: HDFC Bank, Karvy Stock Broking

Exhibit 51: Balance Sheet

Particulars (Rs bn) FY13 FY14 FY15 FY16E FY17E

Liabilities

Networth 362 435 620 716 837

Deposits 2,962 3,673 4,508 5,410 6,491

Current Deposits 523 615 736 897 1,095

Savings Deposits 882 1,031 1,249 1,524 1,859

Borrowings 330 394 452 697 805

Other liabilities & provisions 349 413 325 628 747

Total liabilities 4,004 4,916 5,905 7,451 8,880

Assets

Cash & balances with RBI 146 253 275 373 448

Balances with banks & money at call 127 142 88 216 260

Investments 1,116 1,210 1,665 1,742 2,084

Advances 2,397 3,030 3,655 4,441 5,440

Fixed assets 27 30 32 38 46

Other assets 190 251 191 641 603

Total assets 4,004 4,916 5,905 7,451 8,880

Source: HDFC Bank, Karvy Stock Broking

31

October 01, 2015

HDFC Bank

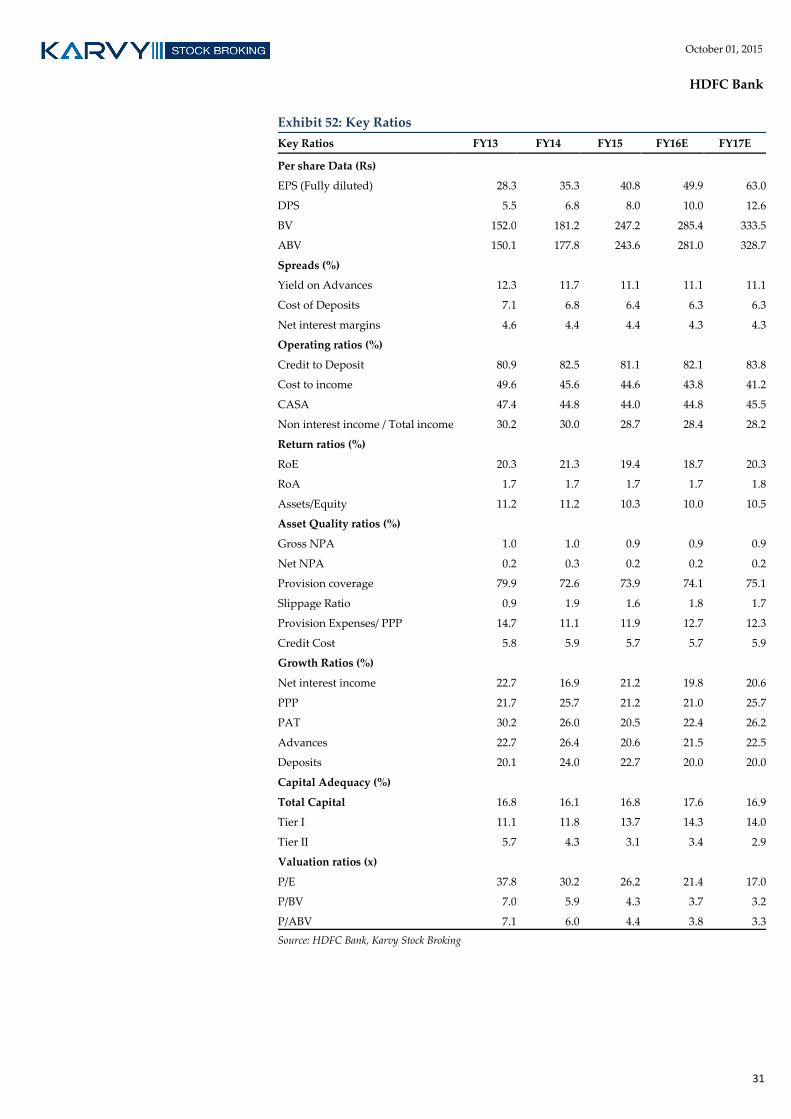

Exhibit 52: Key Ratios

Key Ratios FY13 FY14 FY15 FY16E FY17E

Per share Data (Rs)

EPS (Fully diluted) 28.3 35.3 40.8 49.9 63.0

DPS 5.5 6.8 8.0 10.0 12.6

BV 152.0 181.2 247.2 285.4 333.5

ABV 150.1 177.8 243.6 281.0 328.7

Spreads (%)

Yield on Advances 12.3 11.7 11.1 11.1 11.1

Cost of Deposits 7.1 6.8 6.4 6.3 6.3

Net interest margins 4.6 4.4 4.4 4.3 4.3

Operating ratios (%)

Credit to Deposit 80.9 82.5 81.1 82.1 83.8

Cost to income 49.6 45.6 44.6 43.8 41.2

CASA 47.4 44.8 44.0 44.8 45.5

Non interest income / Total income 30.2 30.0 28.7 28.4 28.2

Return ratios (%)

RoE 20.3 21.3 19.4 18.7 20.3

RoA 1.7 1.7 1.7 1.7 1.8

Assets/Equity 11.2 11.2 10.3 10.0 10.5

Asset Quality ratios (%)

Gross NPA 1.0 1.0 0.9 0.9 0.9

Net NPA 0.2 0.3 0.2 0.2 0.2

Provision coverage 79.9 72.6 73.9 74.1 75.1

Slippage Ratio 0.9 1.9 1.6 1.8 1.7

Provision Expenses/ PPP 14.7 11.1 11.9 12.7 12.3

Credit Cost 5.8 5.9 5.7 5.7 5.9

Growth Ratios (%)

Net interest income 22.7 16.9 21.2 19.8 20.6

PPP 21.7 25.7 21.2 21.0 25.7

PAT 30.2 26.0 20.5 22.4 26.2

Advances 22.7 26.4 20.6 21.5 22.5

Deposits 20.1 24.0 22.7 20.0 20.0

Capital Adequacy (%)

Total Capital 16.8 16.1 16.8 17.6 16.9

Tier I 11.1 11.8 13.7 14.3 14.0

Tier II 5.7 4.3 3.1 3.4 2.9

Valuation ratios (x)

P/E 37.8 30.2 26.2 21.4 17.0

P/BV 7.0 5.9 4.3 3.7 3.2

P/ABV 7.1 6.0 4.4 3.8 3.3

Source: HDFC Bank, Karvy Stock Broking

Banking October 01, 2015

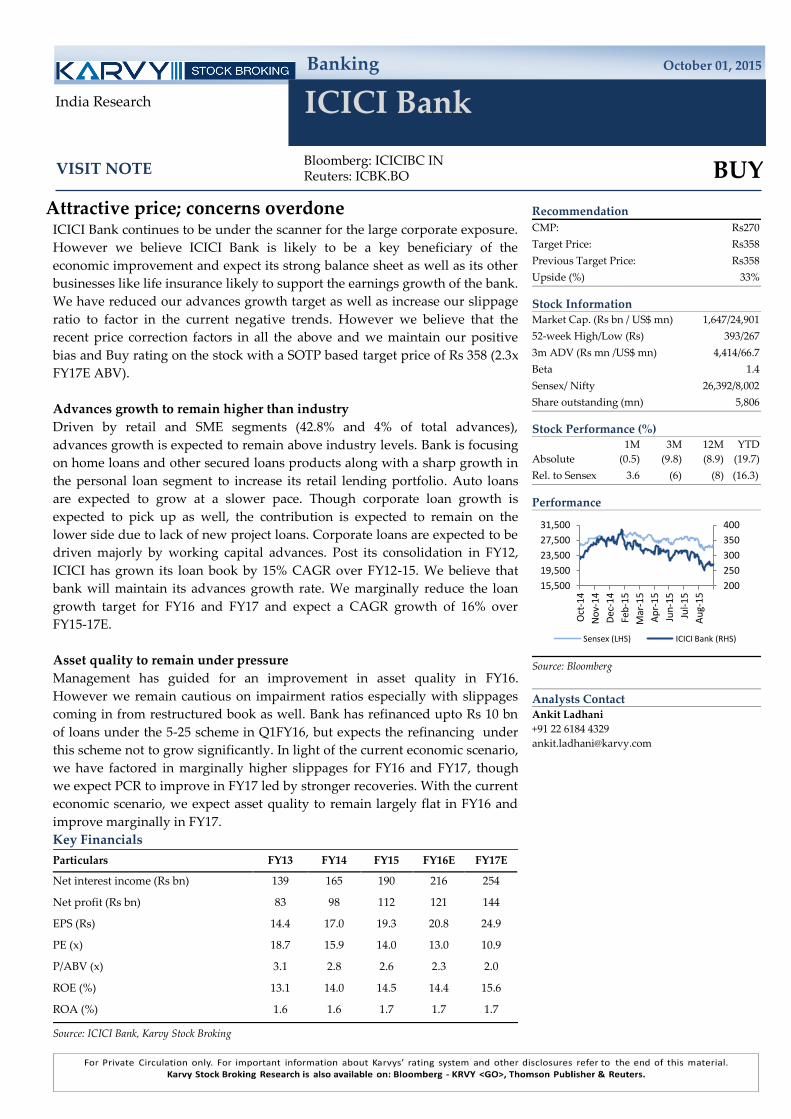

ICICI Bank

Bloomberg: ICICIBC IN Reuters: ICBK.BO

BUY

India Research

VISIT NOTE

Recommendation

CMP: Rs270

Target Price: Rs358

Previous Target Price: Rs358

Upside (%) 33%

Stock Information Market Cap. (Rs bn / US$ mn) 1,647/24,901

52-week High/Low (Rs) 393/267

3m ADV (Rs mn /US$ mn) 4,414/66.7

Beta 1.4

Sensex/ Nifty 26,392/8,002

Share outstanding (mn) 5,806

Stock Performance (%) 1M 3M 12M YTD

Absolute (0.5) (9.8) (8.9) (19.7)

Rel. to Sensex 3.6 (6) (8) (16.3)

Performance

Source: Bloomberg

Analysts Contact Ankit Ladhani

+91 22 6184 4329

200

250

300

350

400

15,500

19,500

23,500

27,500

31,500

Oct

-14

No

v-1

4

Dec

-14

Feb

-15

Mar

-15

Ap

r-1

5

Jun

-15

Jul-

15

Au

g-1

5

Sensex (LHS) ICICI Bank (RHS)

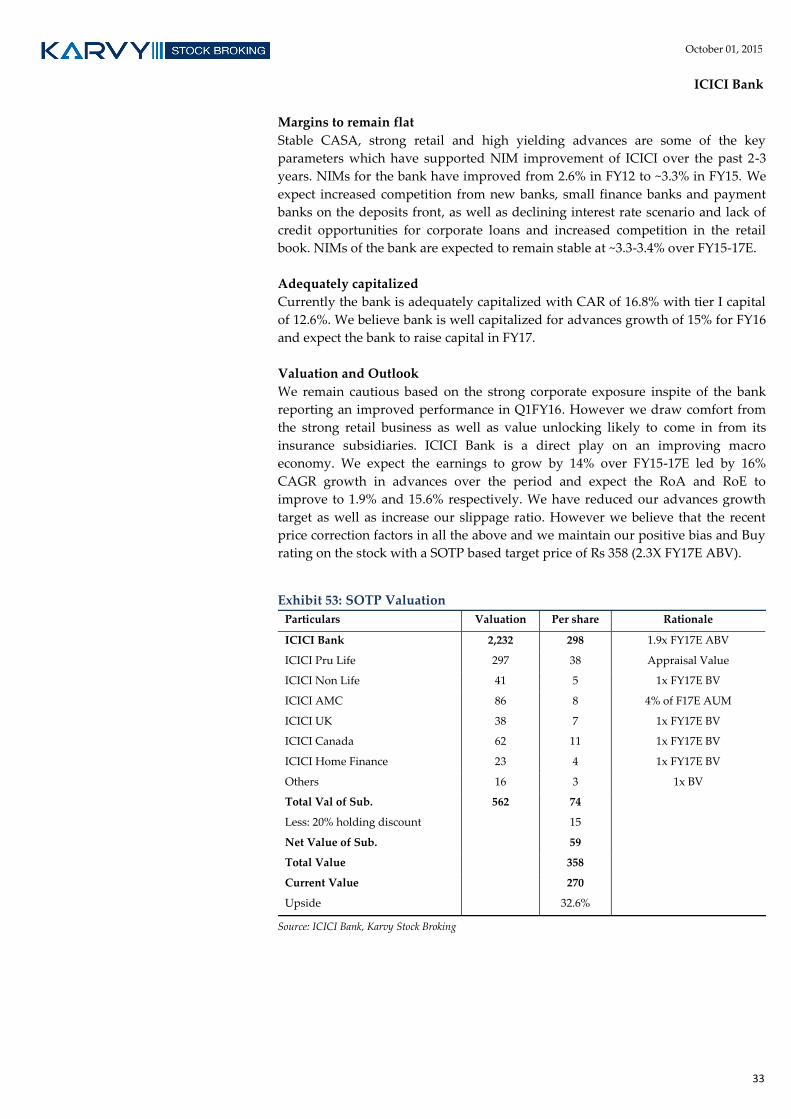

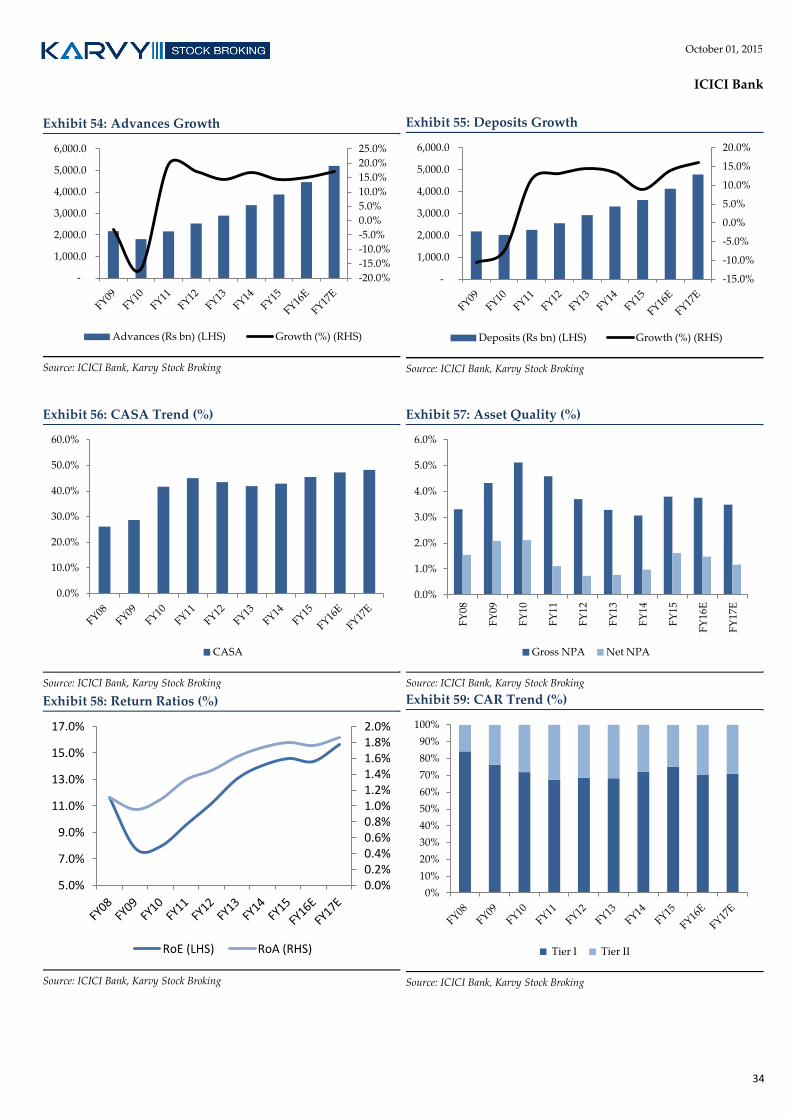

Attractive price; concerns overdone ICICI Bank continues to be under the scanner for the large corporate exposure.

However we believe ICICI Bank is likely to be a key beneficiary of the

economic improvement and expect its strong balance sheet as well as its other

businesses like life insurance likely to support the earnings growth of the bank.

We have reduced our advances growth target as well as increase our slippage

ratio to factor in the current negative trends. However we believe that the