![Modern commercial banking []](https://static.fdocuments.in/doc/165x107/55a494801a28ab081b8b4639/modern-commercial-banking-wwwbconnect24com.jpg)

COMMERCIAL BANKING IN INDIA

38

Name Ashpreet Singh MBA 3 rd Sem. Amity Business School Sub:- Commercial Banking

-

Upload

ashpreet-bhatia -

Category

Education

-

view

79 -

download

5

Transcript of COMMERCIAL BANKING IN INDIA

Name Ashpreet Singh MBA 3rd Sem. Amity Business School Sub:- Commercial Banking

CONTENTS

•HISTORY OF BANKING•COMMERCIAL BANKING•RETAIL BANKING•WHOLESALE BANKING•CORPORATE BANKING•INVESTMENT BANKING

History Of BankingBanking offers several facilities and opportunities. Banks in India were started on British pattern in the beginning of the 19th century. The first half of the 19th century , The East India Company established 3 banks;

• The Bank of Bengal• The bank of Bombay • The Bank of Madras

Commercial Banking

The Commercial Bank of India, also known as Exchange Bank was a bank which was established in Bombay Presidency (now Mumbai), in 1845 of the British Raj period.

INTRODUCTION

A commercial bank is a financial institution that is authorized by law to receive money from businesses and individuals and lend money to them. Commercial banks are open to the public and serve individuals, institutions, and businesses.

SERVICES BY COMMERCIAL BANKS

• Money Withdrawal• Money Transfers• Savings• Loans/Mortgages• Foreign Exchange• 24- hour Banking • Safeguard money

TYPES OF COMMERCIAL BANKS

• DEPOSIT BANKS• INDUSTRIAL BANKS• SAVINGS BANKS• EXCHANGE BANKS• AGRICULTURAL BANKS• MISCELLANEOUS BANKS

COMMERCIAL BANKS CLASSIFIED IN FOLLOWING

• Public Sector /Nationalized Banks(22)• Private Sector Banks (Indian) and(8)• Foreign-Commercial Banks in India(12)

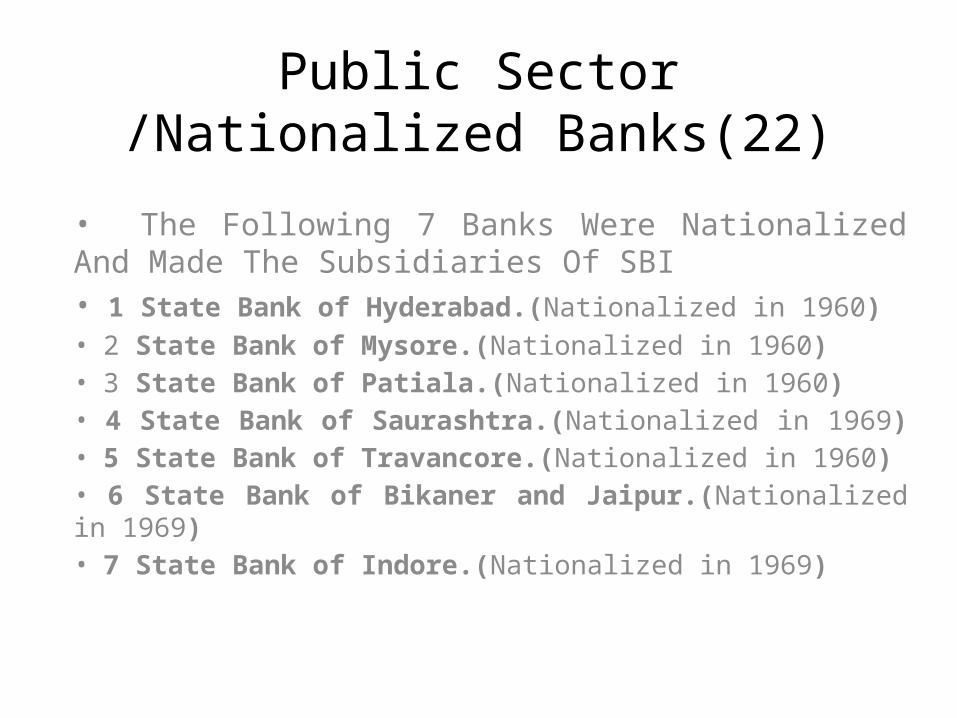

Public Sector /Nationalized Banks(22)

• The Following 7 Banks Were Nationalized And Made The Subsidiaries Of SBI• 1 State Bank of Hyderabad.(Nationalized in 1960) • 2 State Bank of Mysore.(Nationalized in 1960)• 3 State Bank of Patiala.(Nationalized in 1960)• 4 State Bank of Saurashtra.(Nationalized in 1969) • 5 State Bank of Travancore.(Nationalized in 1960)• 6 State Bank of Bikaner and Jaipur.(Nationalized in 1969)• 7 State Bank of Indore.(Nationalized in 1969)

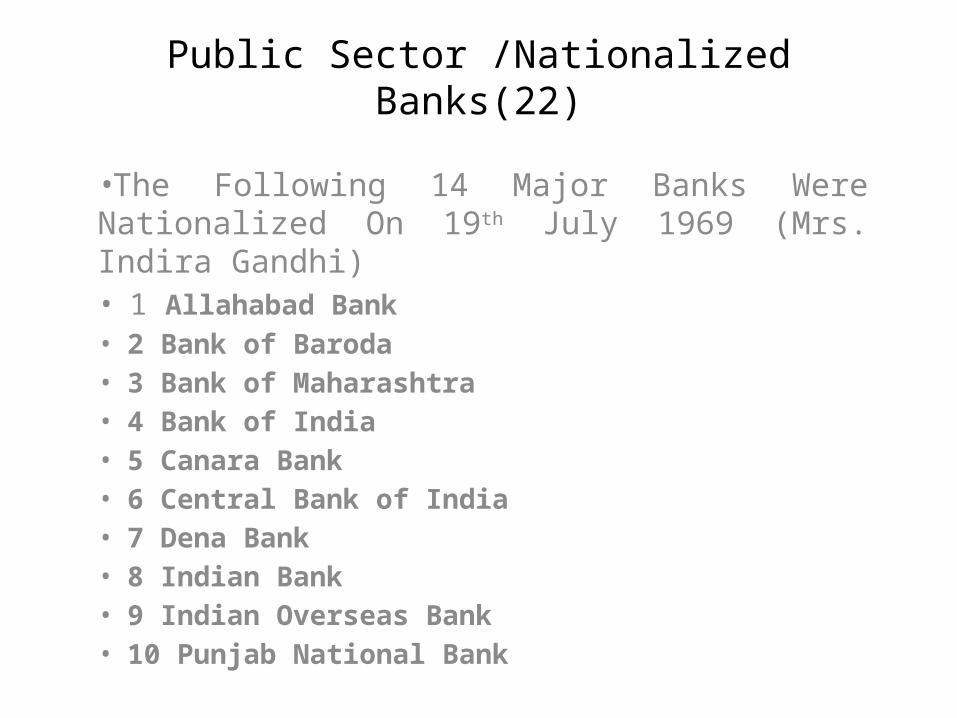

Public Sector /Nationalized Banks(22)

•The Following 14 Major Banks Were Nationalized On 19th July 1969 (Mrs. Indira Gandhi)• 1 Allahabad Bank• 2 Bank of Baroda• 3 Bank of Maharashtra• 4 Bank of India• 5 Canara Bank• 6 Central Bank of India• 7 Dena Bank• 8 Indian Bank• 9 Indian Overseas Bank• 10 Punjab National Bank

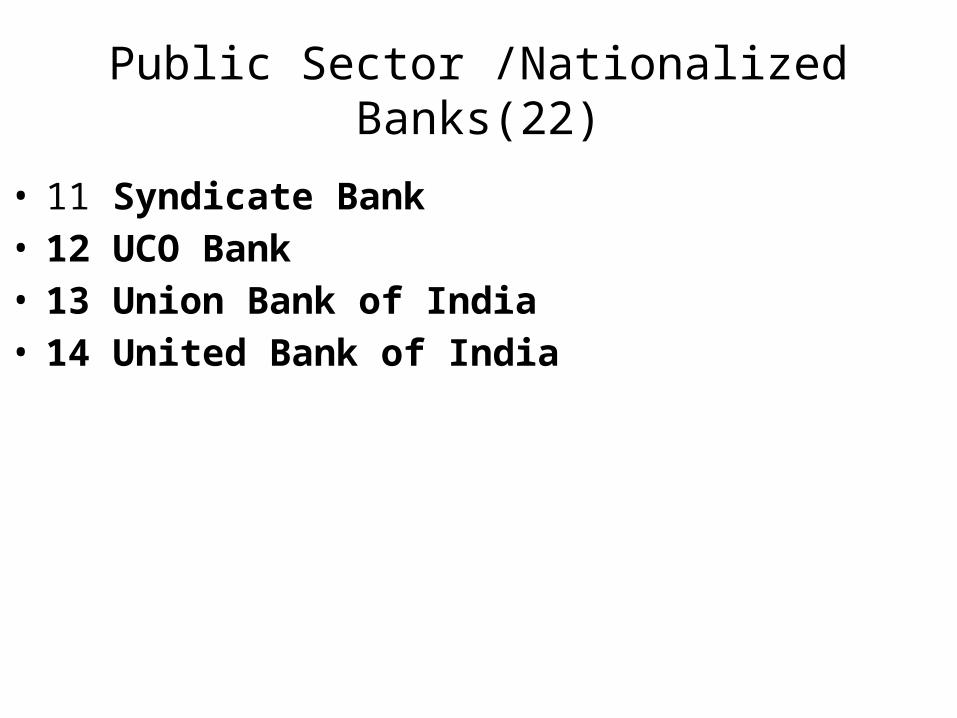

Public Sector /Nationalized Banks(22)

• 11 Syndicate Bank• 12 UCO Bank• 13 Union Bank of India• 14 United Bank of India

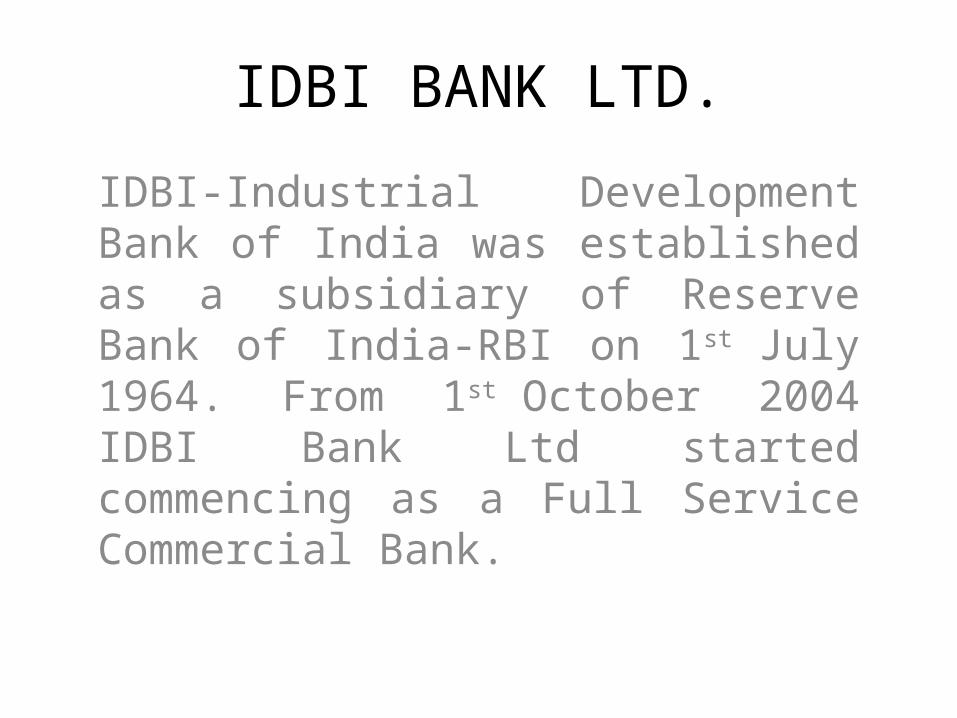

IDBI BANK LTD.

IDBI-Industrial Development Bank of India was established as a subsidiary of Reserve Bank of India-RBI on 1st July 1964. From 1st October 2004 IDBI Bank Ltd started commencing as a Full Service Commercial Bank.

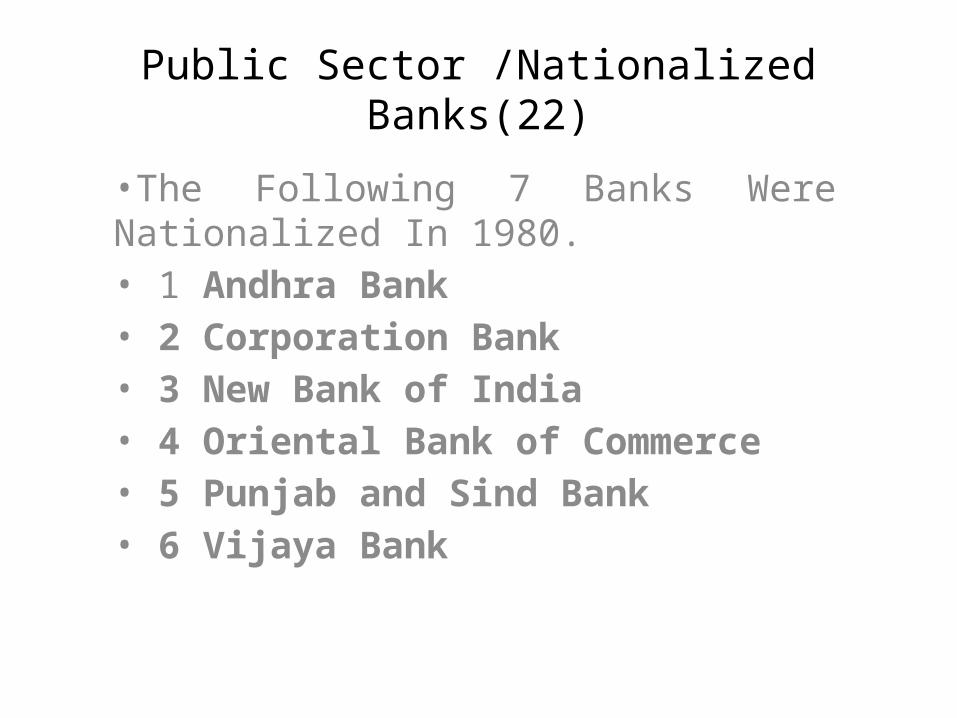

Public Sector /Nationalized Banks(22)

•The Following 7 Banks Were Nationalized In 1980.• 1 Andhra Bank• 2 Corporation Bank• 3 New Bank of India• 4 Oriental Bank of Commerce• 5 Punjab and Sind Bank• 6 Vijaya Bank

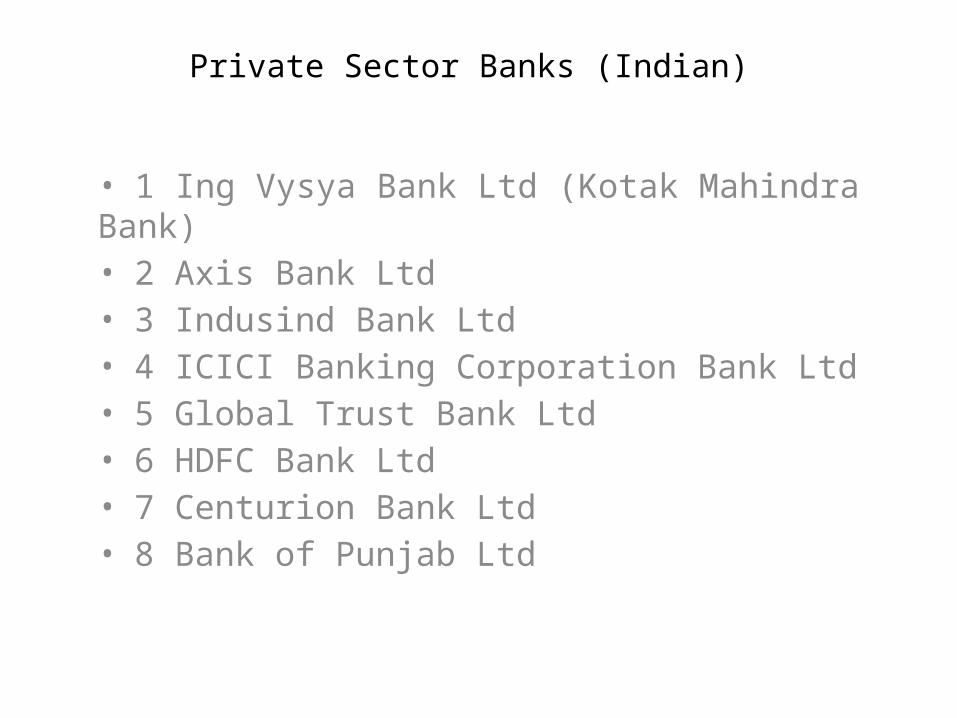

Private Sector Banks (Indian)

• 1 Ing Vysya Bank Ltd (Kotak Mahindra Bank)• 2 Axis Bank Ltd• 3 Indusind Bank Ltd• 4 ICICI Banking Corporation Bank Ltd• 5 Global Trust Bank Ltd• 6 HDFC Bank Ltd• 7 Centurion Bank Ltd• 8 Bank of Punjab Ltd

Foreign-Commercial Banks in India(12)

• 1 American Express Bank Ltd.• 2 ANZ Gridlays Bank Plc.• 3 Bank of America NT & SA• 4 Bank of Tokyo Ltd.• 5 Banquc Nationale de Paris• 6 Barclays Bank Plc• 7 Citi Bank N.C.• 8 Deutsche Bank A.G.• 9 Hongkong and Shanghai Banking Corporation• 10 Standard Chartered Bank.• 11 The Chase Manhattan Bank Ltd.• 12 Dresdner Bank AG

TOP RANKING COMMERCIAL BANKS IN INDIA

1. STATE BANK OF INDIA

2. ICICI Bank Limited

3. Punjab National Bank

4. Canara Bank

5. Bank of Baroda

6. Bank of India

7. Union Bank of India

8. Industrial Development Bank of India Limited

9. Central Bank of India

10. HDFC Bank Limited

11. UCO Bank

12. Syndicate Bank

13. Indian Overseas Bank

14. Oriental Bank of Commerce

15. Allahabad Bank

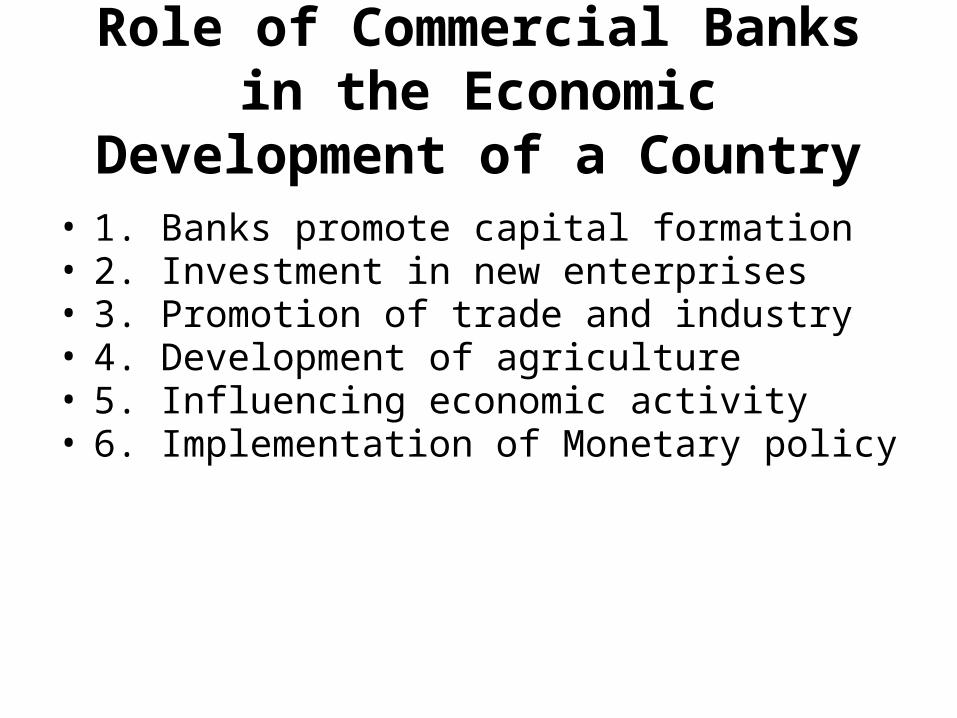

Role of Commercial Banks in the Economic Development of a Country

• 1. Banks promote capital formation• 2. Investment in new enterprises• 3. Promotion of trade and industry• 4. Development of agriculture• 5. Influencing economic activity• 6. Implementation of Monetary policy

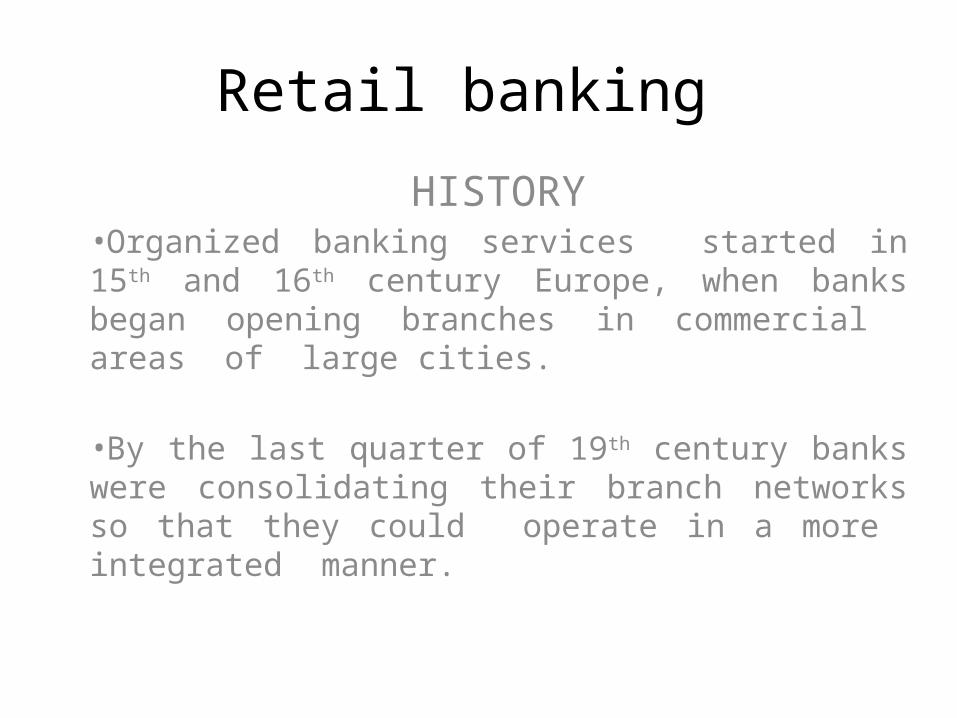

Retail banking

HISTORY•Organized banking services started in 15th and 16th century Europe, when banks began opening branches in commercial areas of large cities.

•By the last quarter of 19th century banks were consolidating their branch networks so that they could operate in a more integrated manner.

SUMMARY RETAIL BANKING: Retail banking refers to banking in

which banking institutions execute transactions directly with consumers rather than corporations or other banks.

Services offered includes : Savings and checking accounts, mortgages, personal loans, debit cards, credit cards and so forth.

Indian retail banking is showing phenomenal growth

Key drivers: Increased consumerism, Internet, Emergence of new age companies, technology.

Retail Banking

Keeping pace with the 7.5 per cent growth of the Indian economyover the past few years, the retail banking sector in India has also witnessed phenomenal growth. It has faced up to the need of the hour and introduced anytime, anywhere banking, for its customers through ATMs, mobile and internet banking.

EMERGING ISSUES IN HANDLING RETAIL BANKING

• KNOWING CUSTOMER :-Know your Customer’ is a concept which is easier said than practiced. Banksface several hurdles in achieving this.In order to that the product lines are targeted atthe right customers-present and prospective-it is imperative that an integrated view ofcustomers is available to the banks

• TECHNOLOGY ISSUES :- Retail banking calls for huge investments in technology. Whether it is setting up of a Customer Relationship Management System or Establishing Loan Process Automation or providing anytime, anywhere convenience to the vast number of customers or establishing channel/product/customer profitability, technology plays apivotal role.

• PRODUCT INNOVATION:- Product innovation continues to be yet another major challenge. Even though bank after bank is coming out with new products, not all are successful. What is ofcrucial importance is the need to understand the difference between novelty and innovation?

• PROCESS CHANGES:- Business Process Re-engineering is yet another key requirement for banks to handle the growing retail portfolio. Simplified processes and aligning them around delivery of customer service impinging on reducing customer touch-points are of essence.

FUTURE OF RETAIL BANKING

Retail banking has significant past and glorious future over the years. Indian retail banking, according to a report, is likely to grow at a CAGR(Compound annual growth rate) of 28 per cent till 2010 to Rs 97,00 billion. So, although the revolution in retail banking has changed the face of the Indian banking industry as a whole, it has still miles to go.

WHOLESALE BANKING

•Wholesale Banking refers to conducting banking business with industrial and business entities. This includes, corporates, trading houses, multinationals and domestic companies etc. •As opposed to retail banking which deals with ‘man in the street’, wholesale banking is the borrowing and lending of funds to other banks, large multinationals and even government agencies. As a general description it will cover various money markets

WHOLESALE BANKING

• The concept of wholesale banking is to focus on corporate, i.e. Companies, firms, proprietorship concerns, Public Sector, Institutions, societies, Trusts and clubs.

• The size of both deposits and advances is large which were cheap to process.

Key products under Wholesale Banking can be classified as:• Fund-based services • Non-fund-based services • Value-added services and • Internet Banking services

• Fund-based services - Term lending, Short-term Finance - Working Capital Finance, Bill discounting - Structured Finance, Export Credit • Non-Fund-based services - Bank guarantee, Letter of credit - Collection of bills and documents • Value-added Services - Cash management services, - Channel financing, vendor financing, - Real Time Gross Settlement etc.

Corporate banking

• Financial services provided by Banks to the Corporate for meeting their banking and financial needs for

• Setting up new projects• Expansion• Diversification• Modernization• Financial restructuring• Commercial Banking facilities

Scope and Functions of Banks

Creating Money• This is accomplished by the lending and

investing activities of commercial banks in co-operation with the central bank. This results in elastic credit system which is necessary for economic growth. It helps in expansion of productive facilities and operations

Scope and Functions of Banks(contd…)

Transfer of funds• Banks help in financial transactions by transferring

funds by means of cash, cheque, demand deposits, bearer’s order, Electronic transfer of funds, ATM’s etc.

Extension of Credit• Banks lend for agricultural, commercial and

industrial activities of a country. This helps in increasing production, capital investments and in the standard of living

Scope and Functions of BanksFinancing of foreign trade• They help in making payments in the currency the

foreign country example in Francs, Marks, Lira or Pounds by selling foreign exchange. They also issue letter of credit when the importer is not paid immediately by exporter which is more often the case. They also issue Travellers Cheque to international tourists.

Safekeeping of Valuables• They provide a vault for safekeeping of

valuables/securities.

Investment Banking

• Investment banks help companies and governments and their agencies to raise money by issuing and selling securities in the primary market.

• They assist public and private corporations in raising funds in the capital markets (both equity and debt),

• as well as in providing strategic advisory services for mergers, acquisitions and other types of financial transactions.

Investment Banking In India

• SBI was the first Indian public sector bank to set up its investment banking division in 1972.

• SBI Caps and IDBI Caps are two prime examples of �investment banks in India today.

• Currently, there are 300 investment banks registered �with SEBI.

• Currently, without holding a certificate of registration�granted by the Securities and Exchange Board of India,no person can act as a investment banker.

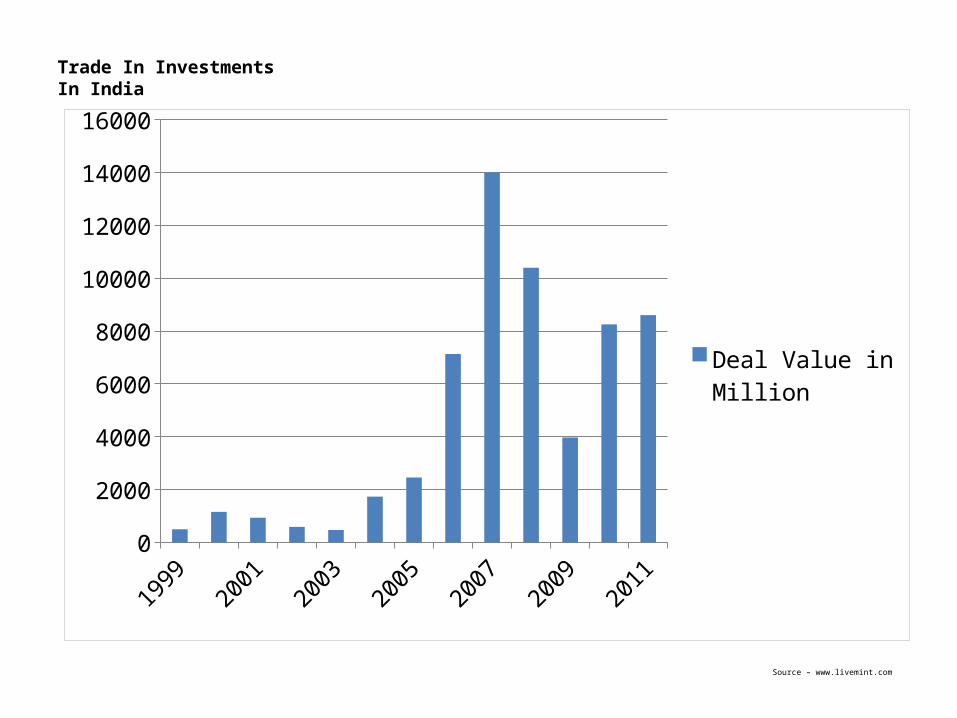

Trade In Investments In India

19992000

20012002

20032004

20052006

20072008

20092010

20110

2000

4000

6000

8000

10000

12000

14000

16000

Deal Value in Million

Source – www.livemint.com

![BANKING SECTOR REFORMS IN INDIA AND CHINA: DOES … Shirai.pdfsector banks” in India and “wholly state-owned commercial banks” [WSCBs] in China). This paper focuses on banking](https://static.fdocuments.in/doc/165x107/5e8f30e2ebb920085854550e/banking-sector-reforms-in-india-and-china-does-shiraipdf-sector-banksa-in-india.jpg)