INDEPENDENCE GROUP NL

25

INDEPENDENCE GROUP NL FULL YEAR RESULTS PRESENTATION 24 August 2015

Transcript of INDEPENDENCE GROUP NL

INDEPENDENCE GROUP NL FULL YEAR RESULTS PRESENTATION

24 August 2015

2

This presentation has been prepared by Independence Group NL (“IGO”) (ABN 46 092 786 304). It should not be considered as an offer or invitation tosubscribe for or purchase any securities in IGO or as an inducement to make an offer or invitation with respect to those securities in any jurisdiction.

This presentation contains general summary information about IGO. The information, opinions or conclusions expressed in the course of this presentationshould be read in conjunction with IGO’s other periodic and continuous disclosure announcements lodged with the Australian Stock Exchange (ASX), which areavailable on the IGO website. No representation or warranty, express or implied, is made in relation to the fairness, accuracy or completeness of theinformation, opinions and conclusions expressed in this presentation.

This presentation includes forward looking information regarding future events, conditions, circumstances and the future financial performance of IGO. Often,but not always, forward looking statements can be identified by the use of forward looking words such as "may", "will", "expect", "intend", "plan", "estimate","anticipate", "continue" and "guidance", or other similar words and may include statements regarding plans, strategies and objectives of management,anticipated production or construction commencement dates and expected costs or production outputs. Such forecasts, projections and information are not aguarantee of future performance and involve unknown risks and uncertainties, many of which are beyond IGO’s control, which may cause actual results anddevelopments to differ materially from those expressed or implied. Further details of these risks are set out below. All references to future production andproduction guidance made in relation to IGO are subject to the completion of all necessary feasibility studies, permit applications and approvals, construction,financing arrangements and access to the necessary infrastructure. Where such a reference is made, it should be read subject to this paragraph and inconjunction with further information about the Mineral Resources and Ore Reserves, as well as any Competent Persons' Statements included in periodic andcontinuous disclosure announcements lodged with the ASX. Forward looking statements in this presentation only apply at the date of issue. Subject to anycontinuing obligations under applicable law or any relevant stock exchange listing rules, in providing this information IGO does not undertake any obligation topublically update or revise any of the forward looking statements or to advise of any change in events, conditions or circumstances on which any suchstatement is based.

There are a number of risks specific to IGO and of a general nature which may affect the future operating and financial performance of IGO and the value of aninvestment in IGO including and not limited to economic conditions, stock market fluctuations, commodity demand and price movements, access toinfrastructure, timing of environmental approvals, regulatory risks, operational risks, reliance on key personnel, reserve and resource estimations, native titleand title risks, foreign currency fluctuations and mining development, construction and commissioning risk. The production guidance in this presentation issubject to risks specific to IGO and of a general nature which may affect the future operating and financial performance of IGO.

Any references to Mineral Resource and Ore Reserve estimates should be read in conjunction with IGO’s 2014 Mineral Resource and Ore Reserveannouncement dated 28 August 2014 (excluding Stockman Ore Reserves) and Stockman Optimisation Study announcement dated 28 November 2014(updated Stockman Ore Reserves), and lodged with the ASX, which are available on the IGO website.

Any references to Mineral Resource and Ore Reserve estimates for Sirius Resources NL (“Sirius” or “SIR”) should be read in conjunction with SIR’s ASXannouncement dated 14 July 2014.

All currency amounts in Australian Dollars (AUD) unless otherwise noted. Cash Costs are in AUD and reported inclusive of royalties and after by-product credits on per unit of payable metal basis. IGO reports All-in Sustaining Costs (AISC) per ounce of gold in AUD for its 30% interest in the Tropicana Gold Mine using the World Gold Council guidelines for

AISC. The World Gold Council guidelines publication was released via press release on 27th June 2013 and is available from the World Gold Council’swebsite.

Cautionary Notes and Disclaimer

3

Business Highlights

Record year in terms of revenue and operating cash flow

Significant growth in dividend reflecting the robustness of the diversified business

All operations succeeded in meeting or beating all production and cash cost guidance

Tropicana has performed, and will continue performing, as a tier one Global asset in terms of cost, grade and cash flow generation

Exploration success demonstrating ability to continue to replace reserves and grow mine life

Announcement of acquisition of Sirius Resources NL (SIR) with the endorsement of major shareholder, Mark Creasy

Aligns with stated strategy of growing a portfolio of tier one assets, leveraging dominant land positions and control of key infrastructure

Replacement financing package in place delivering savings relative to the original Nova package

4

Safety HighlightsSignificant improvement over the past 1-2 years is a credit to our people

0

5

10

15

20

25

30

35

40

45

50

0

2

4

6

8

10

12

14

16

Jul 13 Oct 13 Jan 14 Apr 14 Jul 14 Oct 14 Jan 15 Apr 15 Jul 15

TRIF

R

LTIF

R

12 Mthly Rolling LTIFR 12 Mthly Rolling TRIFR

(1) LTIFR is lost time injury frequency rate expressed in number of injuries per million man-hours worked(2) TRIFR is total recordable injury frequency rate expressed in number of injuries per million man-hours worked

5

Revenue increased by 25% to $499M, a record for IGO

Underlying EBITDA(1) increased by 44% to $213M

Net Profit After Tax increased by 58% to $77M

Net cash flows from operating activities increased by 57% to $202M, a record for IGO

Net cash (cash equivalents and debt) improved 332% to $121M as at 30 June 2015

Total fully franked dividends paid during FY15 were up 175% to 11 cents per share

Final Dividend pool of $13M established with a record date to be set to a date no later than 30 September 2015

In line with dividend policy = pay minimum 30% of NPAT

Combined FY15 interim payment of $14M and FY15 final pool of $13M equates to 35% of FY15 NPAT

Minimum surplus franking balance of $42M available for distribution with future dividends

Financial Highlights

(1) Underlying EBITDA is a non-IFRS measure and comprises net profit or loss after tax, adjusted to exclude tax expense, finance costs, interest income, asset impairments, depreciation and amortisation.

6

Earnings Summary

-10

0

10

20

30

40

50

60

70

80

90

FY13 FY14 FY15

Net Profit After Tax ($M)

0

100

200

300

400

500

600

FY13 FY14 FY15

Revenue ($M)

0

50

100

150

200

250

FY13 FY14 FY15

Underlying EBITDA ($M)

7

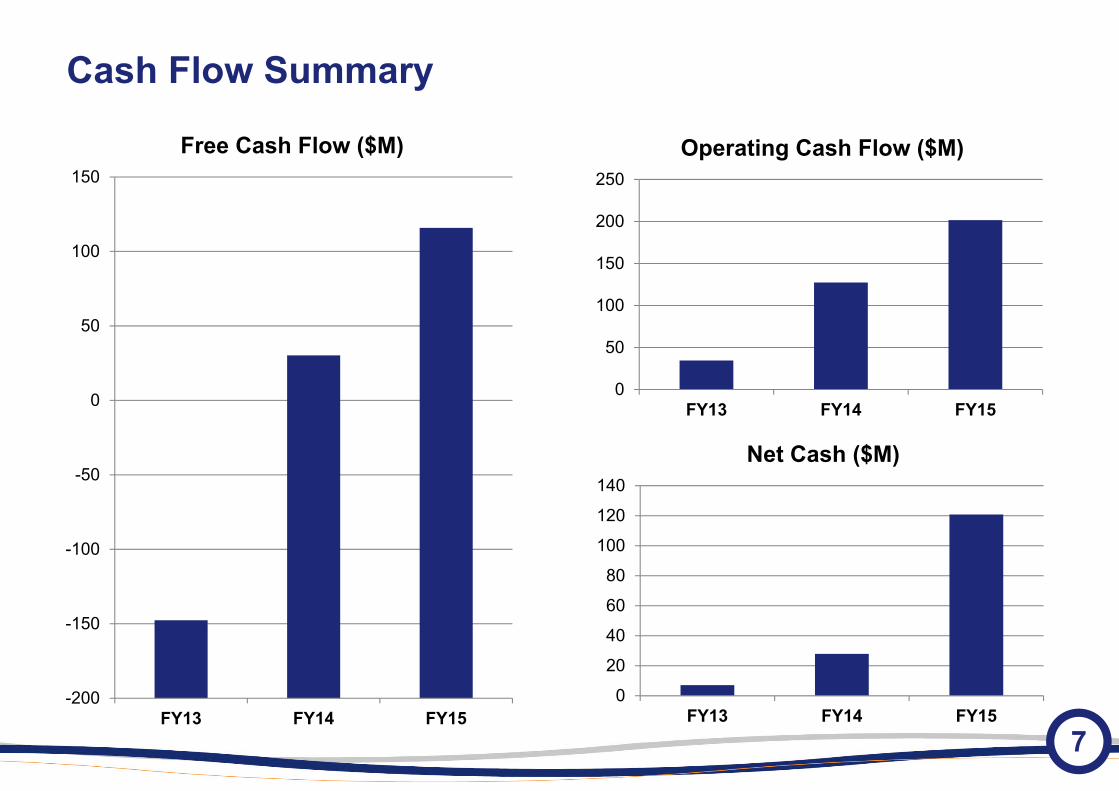

Cash Flow Summary

-200

-150

-100

-50

0

50

100

150

FY13 FY14 FY15

Free Cash Flow ($M)

0

20

40

60

80

100

120

140

FY13 FY14 FY15

Net Cash ($M)

0

50

100

150

200

250

FY13 FY14 FY15

Operating Cash Flow ($M)

8

Summary Income Statement ($M)

FY15 FY14

Revenue from Operations 493.5 397.5Cost of goods sold (240.0) (200.1)Gross profit 253.5 197.4

Other Income 3.7 1.0Exploration and New Business expense (34.8) (39.7)Corporate costs (9.3) (10.5)Other non-production costs (3.8) (6.4)Depreciation and amortisation (98.6) (65.9)Net finance costs (0.8) (5.1)Income tax expense (33.2) (22.1)Net Profit after tax 76.8 48.6

59% higher Tropicana and 16% higher Jaguar contribution offset by 6% lower nickel revenue

Consistent 50% gross profit margin ratio

Foreign exchange gains – more favourable AUD in FY15

Full year D&A charge at Tropicana

58% increase in Net Profit after tax

9

NPAT Analysis ($M)

48.6

76.8

78.9

17.6 (37.4)

(32.6)

(0.6) 1.0 2.6 2.2 1.7 1.5 4.4 (11.1)

-

20

40

60

80

100

120

140

160

Full year of production at Tropicana and better AUD metal prices underpinned higher NPAT

10

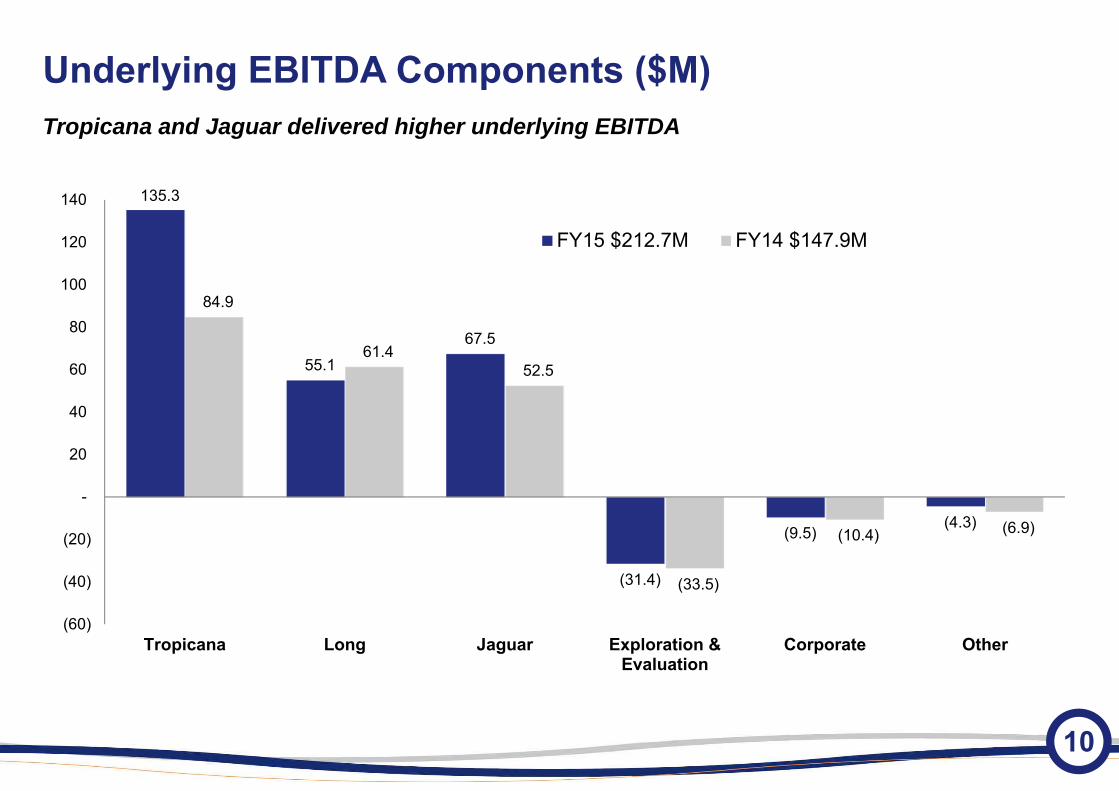

Underlying EBITDA Components ($M)Tropicana and Jaguar delivered higher underlying EBITDA

135.3

55.1 67.5

(31.4)

(9.5)(4.3)

84.9

61.4 52.5

(33.5)

(10.4) (6.9)

(60)

(40)

(20)

-

20

40

60

80

100

120

140

Tropicana Long Jaguar Exploration &Evaluation

Corporate Other

FY15 $212.7M FY14 $147.9M

11

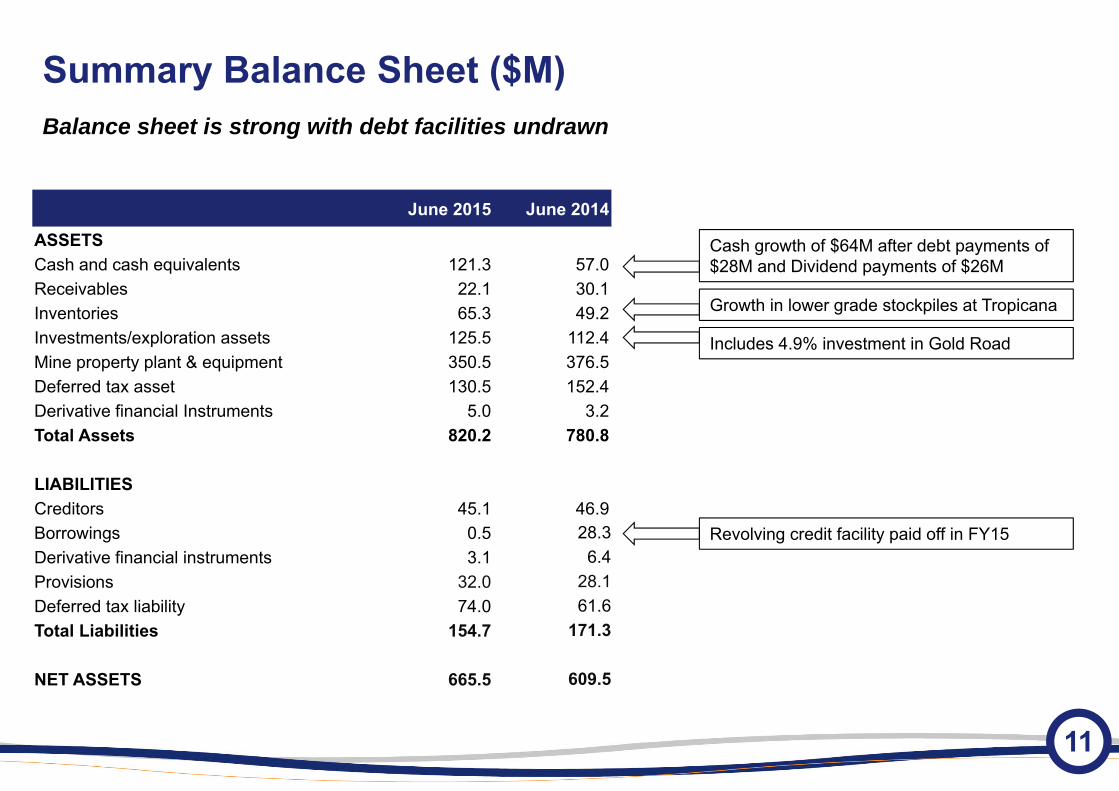

Summary Balance Sheet ($M)

June 2015 June 2014ASSETSCash and cash equivalents 121.3 57.0Receivables 22.1 30.1Inventories 65.3 49.2Investments/exploration assets 125.5 112.4Mine property plant & equipment 350.5 376.5Deferred tax asset 130.5 152.4Derivative financial Instruments 5.0 3.2Total Assets 820.2 780.8

LIABILITIESCreditors 45.1 46.9Borrowings 0.5 28.3Derivative financial instruments 3.1 6.4Provisions 32.0 28.1Deferred tax liability 74.0 61.6Total Liabilities 154.7 171.3

NET ASSETS 665.5 609.5

Cash growth of $64M after debt payments of $28M and Dividend payments of $26M

Growth in lower grade stockpiles at Tropicana

Includes 4.9% investment in Gold Road

Revolving credit facility paid off in FY15

Balance sheet is strong with debt facilities undrawn

12

Comparison of Australian open pit gold operations

200

400

600

800

1,000

1,200

1,400

– 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

2015

E To

tal C

ash

Cos

t + S

usta

inin

g C

apex

(U

S$/o

z)

Estimated productive life (years)

Tropicana (100% basis)

Australian Open Pit Gold Operations(Bubble size is relative production rate)

Source: UBS

Tropicana is a premier low cost, long life gold project

13

0

100

200

300

400

500

600

FY14 FY15 FY16E FY17E FY18E

Gold Production (koz)

Tropicana Production (100% basis)Tropicana benefits from grade streaming until end-2015 then expected to consistently produce 400,000 oz/year

14

Tropicana enhancement opportunities Process plant debottlenecking ongoing

Throughput rates of up to 6.6 Mtpa achieved on monthly basis

Work underway to debottleneck to 7.0-7.5 Mtpa at the Run of Mine grade of ~2 g/t

Resource extension drilling underway

Targets generated by 3D seismic survey

Encouraging results potentially extending mineralisation along strike

Shallow, potentially low cost extensions of mine life

Studies underway to incorporate ~3 Moz of existing resource outside current reserves into mine plan

Aim to maintain current operating margin and extend mine life

Regional exploration continues

New prospects identified in favourable host sequence

15

Sirius transaction highlights Acquisition agreement announced 25 May 2015

Clear strategic rationale for transaction

Acquisition of Sirius is consistent with IGO's clearly defined growth strategy

Delivers shareholders of both companies exposure to Tropicana and Nova

Combines Sirius’ near term development asset with IGO’s strong cash flows

Combined company has a portfolio of high quality assets (margin, mine life, jurisdiction and relevancy)

Transaction unanimously recommended by SIR Board(1) and supported by 35% shareholder, Mark Creasy

Scheme meeting to be held 3 September 2015

Nova Portal(1) The Board of Sirius has unanimously recommended that all Sirius shareholders vote in favour of the Transaction Resolutions, in the absence of a

superior proposal (Refer to the 25 May 2015 ASX announcement for further details).

16

Sirius transaction

Strong support for transaction

Strong strategic rationale for transaction

Supported

Value Growing portfolio of tier 1 assets leveraging dominant land

positions/control of key infrastructure Complementary portfolio creating a long-term growth and yield

investment Diversified across multiple commodity types (Au, Cu, Ni & Zn) and

operations Leverage combined Company’s strong balance sheet and

operational expertise

Transaction has strong support including Creasy endorsement Unanimously recommended by boards of directors of both

companies SIR and IGO management and boards share common vision for

combined business and strategic rationale for transaction Scheme meeting schedule for 3 September 2015

“This transaction brings together the producing assets of Independence and the near production asset of Sirius.” Mark Creasy, 25 May 2015

17

Summary remarks

Nova Jaguar

FY15 Full Year Achieved or bettered guidance on production and cash costs at

all mines Achieved record revenue and operating cash flow Ended FY15 with net cash of $121M Paid 11cps during FY15 and established $13M pool for FY15

fully franked final dividend Outlook Maintain focus on existing operations: safety; operational

discipline; and cost control Continue to strengthen balance sheet Exploration dollars weighted to brownfields opportunities to drive

mine life Continue to target opportunities to sustain and grow the

business in the long term Sirius Scheme Meeting on 3 September 2015 Integration planning completed and project optimisation studies

currently underway

Independence Group NL (www.igo.com.au)Peter Bradford, Managing Director and CEO

24 August 2015

Questions?

19

Resources & Reserves

Competent Persons StatementsExploration ResultsThe information in this report that relates to Exploration Results is a compilation of previously published data for which CompetentPersons consents were obtained. Their consents remain in place for subsequent releases by the Company of the same information inthe same form and context, until the consent is withdrawn or replaced by a subsequent report and accompanying consent. Theinformation in this report has been extracted from the IGO ASX Quarterly Activities Report dated 29 July 2015 and is available on theIGO website www.igo.com.au. The Company confirms that it is not aware of any new information or data that materially affects theinformation included in the original market announcement and that all material assumptions and technical parameters underpinning theestimates in the market announcement continue to apply and have not materially changed. The Company confirms that the form andcontext in which the Competent Person’s findings are presented have not been materially modified from the original marketannouncement.

Resources and ReservesThe information in this report that relates to Mineral Resources or Ore Reserves is a compilation of previously published data for whichCompetent Persons consents were obtained. Their consents remain in place for subsequent releases by the Company of the sameinformation in the same form and context, until the consent is withdrawn or replaced by a subsequent report and accompanyingconsent. The information in this report has been extracted from the IGO ASX Releases for Mineral Resources and Ore Reserves dated28 August 2014 (excluding Stockman Ore Reserves) and 28 November 2014 (Stockman Ore Reserves only), and are available on theIGO website www.igo.com.au. The Company confirms that it is not aware of any new information or data that materially affects theinformation included in the original market announcements and that all material assumptions and technical parameters underpinning theestimates in the market announcements continue to apply and have not materially changed. The Company confirms that the form andcontext in which the Competent Person’s findings are presented have not been materially modified from the original marketannouncements.

20

Resources & Reserves: Tropicana JV (IGO 30%)

Classification Tonnes Mt Au g/t Contained Au Moz Classification Tonnes Mt Au g/t Contained Au Moz

OPEN PIT Measured 22.8 2.11 1.56 OPEN PIT Proved 20.2 2.29 1.49Indicated 73.7 1.89 4.47 Probable 29.7 2.02 1.94Inferred 5.8 2.57 0.48Sub Total 102.4 1.97 6.50

UNDERGROUND Measured - - -Indicated 2.4 3.58 0.27Inferred 6.1 3.07 0.60Sub Total 8.5 3.21 0.87

STOCKPILES Measured 4.9 1.04 0.16 Stockpiles 3.3 1.27 0.13TOTAL TROPICANA Measured 27.7 1.92 1.72

Indicated 76.1 1.94 4.74Inferred 11.9 2.83 1.08

GRAND TOTAL 115.7 2.03 7.54 GRAND TOTAL 53.3 2.08 3.56Notes: Notes:

Reference: ASX Release dated 28 August 2014 for Resources and Reserves. Reference: ASX Release dated 28 August 2014 for Resources and Reserves.

1. For the Open Pit Mineral Resource estimate, mineralisation in the Havana, Havana South, Tropicana and Boston Shaker areas w as calculated w ithin a US$1,550/oz pit optimisation at an AUD:USD exchange rate of 1.03 (A$1,500/oz).2. The Open Pit Mineral Resources have been estimated using the geostatistical technique of Uniform Conditioning, using cut-off grades of 0.3g/t Au for Transported and Saprolite material, 0.4g/t Au for Transitional and Fresh material.3. The Havana Deeps Underground Mineral Resource estimate has been reported outside the US$1,550/oz pit optimisation at a cut-off grade of 1.73g/t Au, w hich w as calculated using a gold price of US$2,000/oz (AUD:USD 1.05) (A$1,896/oz).4. The Havana Deeps Underground Mineral Resource w as estimated using the geostatistical technique of Ordinary Kriging using average drill hole intercepts.6. Mining depletion as at 30 June 2014 has been removed from the 2014 resource estimate.7. Resources are inclusive of Reserves.8. The Competent Persons statement is incorporated in the JORC Code (2012) Competent Persons Statements section of the ASX Release dated 28 August 2014.9. JORC (2012) Table 1 Parameters are in Appendix A of the ASX Release dated 28 August 2014.

Mineral Resource 30 June 2014 Ore Reserve 30 June 2014100% Project 100% Project

1. The Proved and Probable Ore Reserve (30 June 2014) is reported above economic break-even gold cut-off grades of 0.4 g/t for Transported/Upper Saprolite material, 0.5 g/t for Low er Saprolite material, 0.6g/t for Sap-Rock (Transitional) material and 0.7g/t for Fresh material at nominated gold price US$1,100/oz and exchange rate 0.88 AUD:USD (equivalent to A$1,249/oz Au).2. The 30 June 2014 Reserve estimate is updated using the end of June 2014 surveyed surface topography and end of June 2014 stockpile balances. The final pit designs, cut-off grades and the Resource model used are unchanged from the December 2013 estimate.3. Resources are inclusive of Reserves.4. The Competent Persons statement is incorporated in the JORC Code (2012) Competent Persons Statements section in the ASX Release dated 28 August 2014.5. JORC (2012) Table 1 Parameters are in Appendix A of the ASX Release dated 28 August 2014.

21

Resources & Reserves: Long Operation

Classification Tonnes Ni% Ni Tonnes Classification Tonnes Ni% Ni TonnesLONG Measured 70,000 5.5 3,900 LONG Proved 50,000 3.8 1,900

Indicated 270,000 5.5 15,000 Probable 56,000 3.1 1,700Inferred 138,000 5.4 7,400Sub Total 478,000 5.5 26,300 Sub Total 106,000 3.4 3,600

VICTOR SOUTH Measured - - - VICTOR SOUTH Proved 5,000 3.7 200Indicated 188,000 2.0 3,700 Probable 8,000 3.2 200Inferred 28,000 1.6 400Sub Total 216,000 1.9 4,100 Sub Total 13,000 3.4 400

McLEAY Measured 74,000 6.7 4,900 McLEAY Proved 49,000 4.1 1,900Indicated 85,000 4.8 4,100 Probable 3,000 3.3 100Inferred 75,000 4.6 3,400Sub Total 234,000 5.3 12,400 Sub Total 52,000 3.9 2,000

MORAN Measured 285,000 7.3 20,800 MORAN Proved 449,000 4.5 20,200Indicated 90,000 6.9 6,300 Probable 120,000 3.1 3,600Inferred 86,000 4.0 3,500Sub Total 461,000 6.6 30,600 Total 569,000 4.2 23,800

STOCKPILES Measured 3,000 3.3 100 STOCKPILES 3,000 3.3 1001,392,000 5.3 73,400 TOTAL 743,000 4.0 29,900

Notes: Notes:

Mineral Resource 30 June 2014 Ore Reserve 30 June 2014

TOTAL

1. Mineral Resources are reported using a 1% Ni Cut-off grade except for the Victor South disseminatedMineral Resource w hich is reported using a cut-off grade of 0.6% Ni.2. Mining depletion as at 30 June 2014 has been removed from the 2014 resource estimate.3. Resources are inclusive of Reserves.4. Ore tonnes have been rounded to the nearest thousand tonnes and nickel tonnes have been roundedto the nearest hundred tonnes. This may result in slight rounding differences in the total values in thetable above.5. The Competent Persons statement is incorporated in the JORC Code (2012) Competent PersonsStatements section of the ASX Release dated 28 August 2014.6. JORC (2012) Table 1 Parameters are in Appendix B of the ASX Release dated 28 August 2014.

1. Ore Reserves are reported above an economic Ni Cut-off value as at 30 June.2. A Net Smelter Return (NSR) value of $214 per ore tonne has been used in the evaluation of the 2014reserve.3. Mining depletion as at 30 June 2014 has been removed from the 2014 reserve estimate.4. Ore tonnes have been rounded to the nearest thousand tonnes and nickel tonnes have been rounded tothe nearest hundred tonnes.5. Revenue factor inputs (US$): Ni $14,508/T, Cu $6,820/T. Exchange rate AU$1.00 : US$0.90.6. The Competent Persons statement is incorporated in the JORC Code (2012) Competent PersonsStatements section of the ASX Release dated 28 August 2014.7. JORC (2012) Table 1 Parameters are in Appendix B of the ASX Release dated 28 August 2014.

Reference: ASX Release dated 28 August 2014 for Resources and Reserves. Reference : ASX Release dated 28 August 2014 for Resources and Reserves.

22

Resources & Reserves: Jaguar Operation

Classification Tonnes Cu% Zn% Ag g/t Au g/t Classification Tonnes Cu% Zn% Ag g/t Au g/t

BENTLEY Measured 706,000 2.2 12.3 172 0.8 BENTLEY Proved 499,000 2.1 12.1 168 0.8Indicated 1,502,000 1.5 8.0 123 0.7 Probable 771,000 1.6 8.8 144 0.8Inferred 631,000 1.2 6.1 101 0.6Stockpiles 16,000 1.8 11.7 166 0.8Sub Total 2,855,000 1.6 8.7 130 0.7 Sub Total 1,270,000 1.8 10.1 154 0.8

STOCKPILES 16,000 1.8 11.7 166 0.8GRAND TOTAL 1,286,000 1.8 10.1 154 0.8

TEUTONIC Measured - - - - - Notes:

BORE Indicated 946,000 1.7 3.6 65 -Inferred 608,000 1.4 0.7 25 -Sub Total 1,554,000 1.6 2.5 49 -

GRAND TOTAL 4,409,000 1.6 6.5 102 -Notes:

Reference: ASX Release dated 28 August 2014 for Resources and Reserves. Reference: ASX Release dated 28 August 2014 for Resources and Reserves.

2. Revenue factor inputs (US$): Cu $6,820/T, Zn $2,070/T, Ag $19.50/troy oz, Au $1,248/troy oz. Exchange rate AU$1.00 : US$0.90.3. Metallurgical recoveries – 82% Cu, 53% Ag, and 43% Au in Cu concentrate; 83% Zn and 22% Ag in Zn concentrate

4. Longitudinal sub-level long hole stoping is the primary method of mining used at Bentley.

5. All Measured Resource and associated dilution w as classified as Proved Reserve. All Indicated Resource and associated dilution w as classif ied as Probable Reserve. No Inferred Resource has been converted into Reserve6. Mining of the Jaguar deposit w as completed on 29 February 2014. All remaining in situ mineralisation w as evaluated and deemed inappropriate for Reserve conversion. The Jaguar underground mine w as subsequently closed.7. Mining depletion as at 30 June 2014 has been removed from the 2014 reserve estimate.8. The Competent Persons statement is incorporated in the JORC Code (2012) Competent Persons Statements section of the ASX Release dated 28 August 2014.9. JORC (2012) Table 1 Parameters are in Appendix C of the ASX Release dated 28 August 2014.

1. Mineral Resources include massive sulphide and stringer sulphide mineralisation. Massive sulphide resources aregeologically defined; stringer sulphide resources for 2014 are reported above cut-off grades of 0.6% Cu for Bentley and 0.7%Cu for Teutonic Bore.2. Block modelling mainly used ordinary kriging grade interpolation methods w ithin w ireframes for all elements and density. TheFlying Spur lens, part of the Bentley deposit, w as estimated using the Inverse Distance Squared Weighting method (IDW2). The new Flying Spur Mineral Resource comprised 449,000t @ 12.6% Zn, 0.6% Cu, 209g/t Ag and 1.7g/t Au (Inferred).3. Mining depletion as at 30 June 2014 has been removed from the 2014 resource estimate for Bentley. Historic mining has been removed from the 2009 resource estimate for Teutonic Bore.4. Resources are inclusive of Reserves.5. Mining of the Jaguar deposit w as completed on 29 February 2014. Economic evaluation of remaining resources has show n that they are not economic at foreseeable metal prices w ithin a reasonable timeframe and have been removed from the 2014 inventory.6. The Teutonic Bore resource estimate is now reported in compliance w ith JORC Code 2012 reporting guidelines. The model is unchanged from the 2009 model.7. The Competent Persons statement is incorporated in the JORC Code (2012) Competent Persons Statements section of the ASX Release dated 28 August 2014.8. JORC (2012) Table 1 Parameters are in Appendices C and D of the ASX Release dated 28 August 2014.

Mineral Resource 30 June 2014 Ore Reserve 30 June 2014

1. Cut-off values w ere based on Net Smelter Return (NSR) values of $180 per ore tonne for direct mill feed and $100 per ore tonne for marginal feed.

Mineral Resources 2009

23

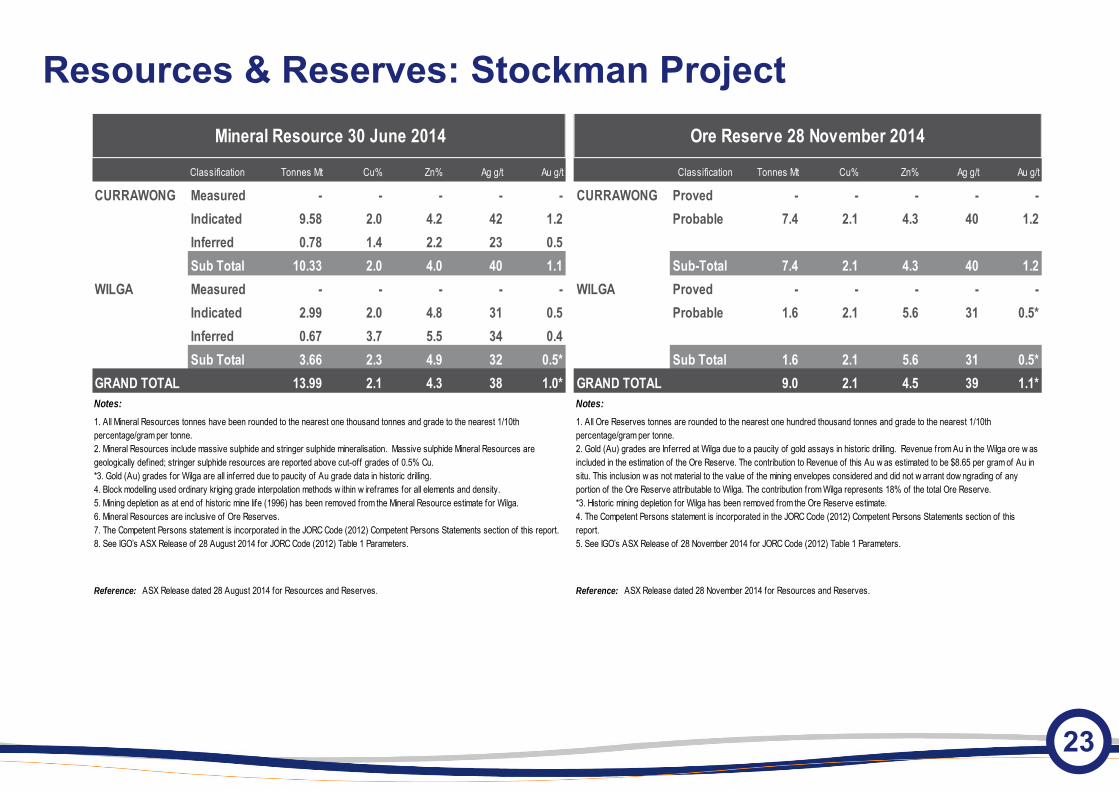

Resources & Reserves: Stockman Project

Classification Tonnes Mt Cu% Zn% Ag g/t Au g/t Classification Tonnes Mt Cu% Zn% Ag g/t Au g/t

CURRAWONG Measured - - - - - CURRAWONG Proved - - - - -Indicated 9.58 2.0 4.2 42 1.2 Probable 7.4 2.1 4.3 40 1.2Inferred 0.78 1.4 2.2 23 0.5Sub Total 10.33 2.0 4.0 40 1.1 Sub-Total 7.4 2.1 4.3 40 1.2

WILGA Measured - - - - - WILGA Proved - - - - -Indicated 2.99 2.0 4.8 31 0.5 Probable 1.6 2.1 5.6 31 0.5*Inferred 0.67 3.7 5.5 34 0.4Sub Total 3.66 2.3 4.9 32 0.5* Sub Total 1.6 2.1 5.6 31 0.5*

GRAND TOTAL 13.99 2.1 4.3 38 1.0* GRAND TOTAL 9.0 2.1 4.5 39 1.1*Notes: Notes:

Reference: ASX Release dated 28 November 2014 for Resources and Reserves.

1. All Ore Reserves tonnes are rounded to the nearest one hundred thousand tonnes and grade to the nearest 1/10th percentage/gram per tonne.2. Gold (Au) grades are Inferred at Wilga due to a paucity of gold assays in historic drilling. Revenue from Au in the Wilga ore w as included in the estimation of the Ore Reserve. The contribution to Revenue of this Au w as estimated to be $8.65 per gram of Au in situ. This inclusion w as not material to the value of the mining envelopes considered and did not w arrant dow ngrading of any portion of the Ore Reserve attributable to Wilga. The contribution from Wilga represents 18% of the total Ore Reserve.*3. Historic mining depletion for Wilga has been removed from the Ore Reserve estimate.4. The Competent Persons statement is incorporated in the JORC Code (2012) Competent Persons Statements section of this report.5. See IGO’s ASX Release of 28 November 2014 for JORC Code (2012) Table 1 Parameters.

1. All Mineral Resources tonnes have been rounded to the nearest one thousand tonnes and grade to the nearest 1/10th percentage/gram per tonne.2. Mineral Resources include massive sulphide and stringer sulphide mineralisation. Massive sulphide Mineral Resources are geologically defined; stringer sulphide resources are reported above cut-off grades of 0.5% Cu.*3. Gold (Au) grades for Wilga are all inferred due to paucity of Au grade data in historic drilling.4. Block modelling used ordinary kriging grade interpolation methods w ithin w ireframes for all elements and density.5. Mining depletion as at end of historic mine life (1996) has been removed from the Mineral Resource estimate for Wilga.6. Mineral Resources are inclusive of Ore Reserves.7. The Competent Persons statement is incorporated in the JORC Code (2012) Competent Persons Statements section of this report.8. See IGO’s ASX Release of 28 August 2014 for JORC Code (2012) Table 1 Parameters.

Mineral Resource 30 June 2014 Ore Reserve 28 November 2014

Reference: ASX Release dated 28 August 2014 for Resources and Reserves.

24

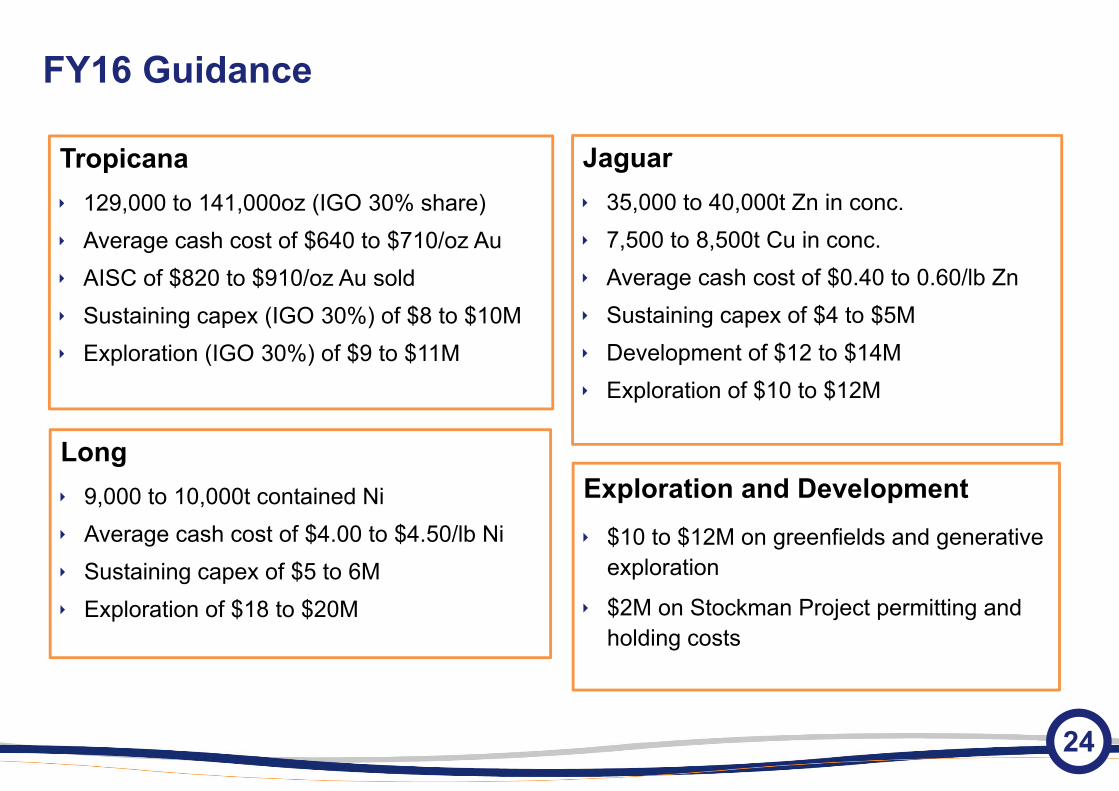

FY16 Guidance

Tropicana 129,000 to 141,000oz (IGO 30% share) Average cash cost of $640 to $710/oz Au AISC of $820 to $910/oz Au sold Sustaining capex (IGO 30%) of $8 to $10M Exploration (IGO 30%) of $9 to $11M

Jaguar 35,000 to 40,000t Zn in conc. 7,500 to 8,500t Cu in conc. Average cash cost of $0.40 to 0.60/lb Zn Sustaining capex of $4 to $5M Development of $12 to $14M Exploration of $10 to $12M

Long 9,000 to 10,000t contained Ni Average cash cost of $4.00 to $4.50/lb Ni Sustaining capex of $5 to 6M Exploration of $18 to $20M

Exploration and Development $10 to $12M on greenfields and generative

exploration

$2M on Stockman Project permitting and holding costs

25

Hedging as at 30 June 2015

Nickel Q1 FY16: 250 t/mth at avg. price of $19,701/t

Copper Q1 FY16: 550t at $8,001/t in Sept 15

Gold FY16: Average 3,208 oz/month zero cost collars (range $1,342 to $1,672/oz)

FY17: 2,500 oz/month zero cost collars to November 2016 (range $1,330 to $1,593/oz)