In Re: Nokia OYJ (Nokia Corporation) Securities Litigation...

110

i ~ . UNITED STATES DISTRICT COUR T FOR THE SOUTHERN DISTRICT OF NEW YOR K IN RE NOKIA OYJ (NOKIA CORP .) SECURITIES LITIGATION CASE NO . 04 Civ. 2646 (KAK) CONSOLIDATED CLASS ACTION COMPLAINT FOR VIOLATIONS OF FEDERAL SECURITIES LAW S JURY TRIAL DEMANDE D Lead plaintiffs Generic Trading of Philadelphia, LLC ("Generic"), Martin Bergljung an d Gerald Hoberman, by their attorneys, for their Consolidated Class Action Complaint (th e "Complaint") allege the following based upon knowledge with respect to their own acts and upo n other facts obtained through an investigation made by and through plaintiffs' counsel, whic h included a review of United States Securities and Exchange Commission ("SEC") filings b y Nokia OYJ (Nokia Corp .) ("Nokia" or the "Company"), as well as securities analysts reports an d advisories about the Company, press releases, analyst conference calls, and other publi c statements issued by the Company and posted on their website, media reports about the Compan y and information learned from interviews of Nokia former employees and other knowledgeabl e persons . Based upon the substantial facts already uncovered, plaintiffs believe that substantia l additional evidentiary support will exist for the allegations set forth herein after a reasonabl e opportunity for discovery. 2498821

Transcript of In Re: Nokia OYJ (Nokia Corporation) Securities Litigation...

i ~ .

UNITED STATES DISTRICT COURTFOR THE SOUTHERN DISTRICT OF NEW YORK

IN RE NOKIA OYJ (NOKIA CORP.)SECURITIES LITIGATION

CASE NO. 04 Civ. 2646 (KAK)

CONSOLIDATED CLASS ACTIONCOMPLAINT FOR VIOLATIONS OFFEDERAL SECURITIES LAW S

JURY TRIAL DEMANDE D

Lead plaintiffs Generic Trading of Philadelphia, LLC ("Generic"), Martin Bergljung an d

Gerald Hoberman, by their attorneys, for their Consolidated Class Action Complaint (th e

"Complaint") allege the following based upon knowledge with respect to their own acts and upo n

other facts obtained through an investigation made by and through plaintiffs' counsel, whic h

included a review of United States Securities and Exchange Commission ("SEC") filings b y

Nokia OYJ (Nokia Corp .) ("Nokia" or the "Company"), as well as securities analysts reports and

advisories about the Company, press releases, analyst conference calls, and other publi c

statements issued by the Company and posted on their website, media reports about the Company

and information learned from interviews of Nokia former employees and other knowledgeabl e

persons. Based upon the substantial facts already uncovered, plaintiffs believe that substantia l

additional evidentiary support will exist for the allegations set forth herein after a reasonabl e

opportunity for discovery.

2498821

NATURE OF THE ACTIO N

This is a securities class action on behalf of purchasers of the securities of Noki a

between October 16, 2003 and April 15, 2004 (the "Class Period"), seeking to pursue remedie s

under the Securities Exchange Act of 1934 (the "Exchange Act")

2 . Defendant Nokia is a Finnish limited liability company with its executive office s

located at Keilalahdentie 4, FIN-00045 Nokia Group, P .O. Box 226, Espoo, Finland, and it s

principal United States offices at 6000 Connection Drive, Irving, Texas , 75039 . The p rincipal

trading markets for Nokia securities are the New York Stock Exchange, in the form of America n

Depository Receipts ("ADRs") (where about 25% of Nokia's securities traded),and the Helsink i

Exchange (where about 60% of Nokia's securities traded), in the form of shares . In addition,

throughout the class period, the shares were listed on the Frankfurt, Stockholm and Paris stock

exchanges, and Nokia's shares were traded on the London stock exchange until November 2003 .

Nokia's securities were actively traded on each of these exchanges, all efficient market s

throughout the Class Period . As of the end of 2003, Nokia's average number of shares exceede d

4.7 billion. On April 6, 2004, the day that Nokia first announced its disappointing first quarte r

2004 ("1Q04") financial results , Nokia lost about $17 billion of its market capitalization .

3 . For several years, Nokia has been the world leader in mobile communications ,

offering voice-centric mobile telephones, or cell phones, primarily marketed to consumers ,

operating on three major digital transmission technologies, Time Division Multiple Acces s

("TDMA"), Global System for Mobile Communication ("GSM") and Code Division Multiple

Access ("CDMA") . Nokia also marketed, with much less success , sophisticated or "smart" cel l

phones, devices and communications systems and solutions to businesses , multimedia and

22498821

gaming devices (its "N-Gage" product) and worked with phone service operators (such as

AT&T) throughout the world to enhance their mobile systems networks . For the fiscal year

ended December 31, 2003, Nokia's net sales totaled $37 . 1 billion and its net profit totaled $4 .5

billion . The company currently has approximately 50,000 employees, maintains production

facilities in nine count ries , and sells its products in over 130 countries .

4. For years , Nokia dominated the TDMA market , where it held up to a 75% market

share, and the GSM market, particularly in Western Europe, where its market share peaked in

first quarter 2003 ("1Q03") at 52.5% . Beginning in 2002, and throughout the class period, in the

United States, one of Nokia's major markets, Nokia's market share was severely damaged by the

shift by certain major U.S . phone service operators away from the TDMA technology to GSM

technology, and even more by those operators who shifted from the TDMA to the CDM A

technology. Until 2003, Nokia did not competitively market CDMA phones to major operators

in the United States, choosing to attempt to develop its own chipset rather than license the

preferred CDMA chipset developed and furnished to Nokia's competitors by Qualcomm. Only

in mid 2003, did Nokia begin to successfully market low-end CDMA phones to the major

systems operators in the United States, but it continued to lag far behind in the development of

CDMA phones, including the more advanced color and camera CDMA phones . In 2003, Nokia

also lost market share in both the United States and Europe, as a result of its reluctance to

customize phones for major phone service operators, including Verizon, Sprint, T-Mobile .

Vodafone and Orange SA .

5. Most importantly, however, beginning in 2002 Nokia's product roadmap began to

deteriorate and Nokia failed to develop new and competitive phone designs . Instead of tendin g3

2498821

to its core business and upgrading the features and quality of its mobile phones, Nokia poure d

approximately 80% of its research & development budget to launch a series of ill-conceived

"smart phones" that were too bulky or costly for most consumers . With respect to Nokia's core

products, engineers in Nokia's product development and research and development ("R&D" )

were permitted only nine to twelve months to plan and develop a new mobile phone, resulting i n

an erosion in product quality. Corners were cut, particularly on the mid-range phones that fuele d

the phone replacement market . Nokia held weekly meetings to address the quality issue s

plaguing Nokia handsets that had been raised by operators . Approximately two years is require d

to properly develop, release and "ramp-up" a new cell phone .

6. The weaknesses in the design of Nokia's product portfolio were well known

within the company by early 2003 and stemmed from senior management's view that, base d

upon its historical dominance of the market, Nokia could freely disregard its customers '

preferences. Thus, beginning in 2002 and into 2003, senior Nokia officers flatly rejected

repeated requests to develop a "flip" or clamshell phone design despite customer surveys an d

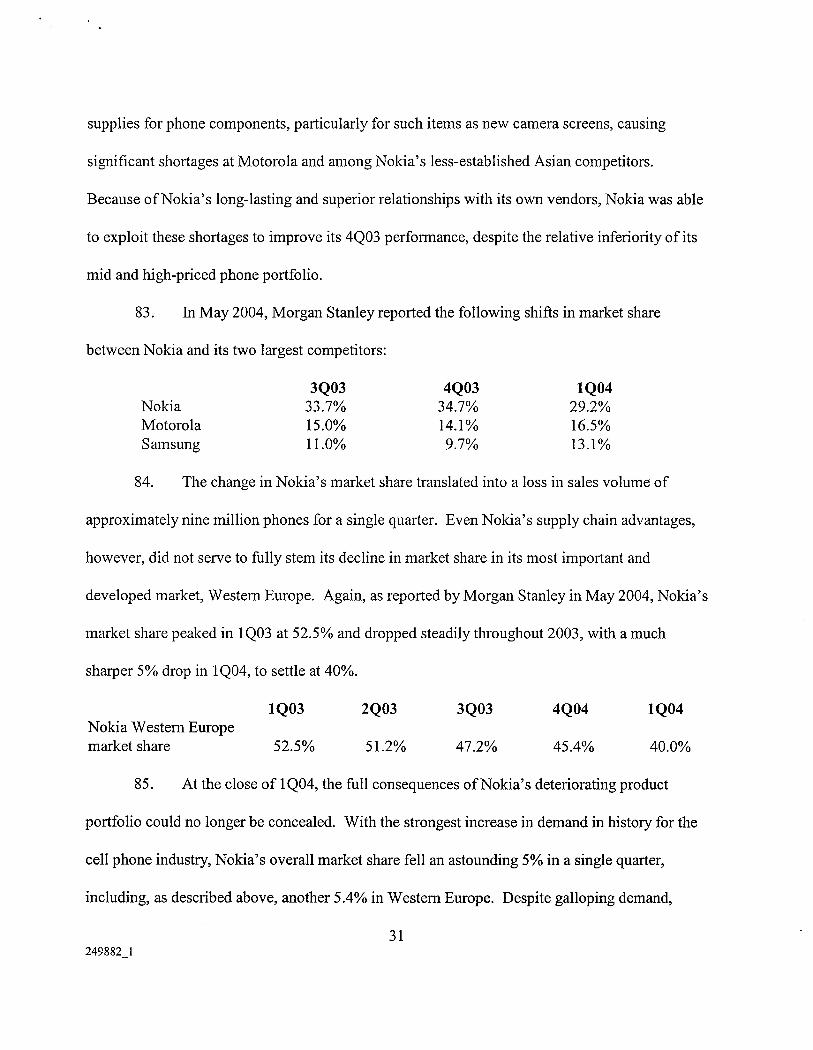

other input indicating Nokia was losing more than 15% of U. S . sales due to this portfoli o

shortcoming . Similarly, Nokia was unwilling to modify its production facilities and invest in

improved color resolution through mega-pixel phones and other features demanded by it s

customers . As a result, the Nokia brand became associated with low-end products, e.g., it was

often the "free" or "penny" phone offered as a promotion by operators, and Nokia becam e

increasingly dependent on new first-time customers in developing countries where Nokia' s

phones sold at lower prices . Throughout 2002 and until fourth quarter 2003, the average sellin g

price ("ASP") of Nokia's phones steadily dropped, sequentially, from quarter-to-quarter .

42498821

Nokia has historically been highly secretive about its phone road map and

provided few details that would allow visibility into its trends in performance to market analyst s

and investors . In 2003, to compensate for its product development problems, Nokia conducted

two major reorganizations in which thousands of employees were laid off or transferre d

including from the new products marketing and development office in Irving, Texas, its interne t

communications office in Mountain View, CA, and from the Company's 300 employee

Broadband Systems Division in Santa Rosa , CA, which the Nokia closed completely in February

of 2003 .

8. Despite the common knowledge within Nokia of its product portfolio

shortcomings, beginning in October 2003, with the announcement of Nokia's third quarter 200 3

("3Q03") results ; at a two-day conference in Dallas , Texas in November 2003 that Noki a

sponsored for market analysts following Nokia's stock ; and throughout January 2004, Nokia' s

CEO and other senior officers aggressively touted the strength of its cell phone product portfolio

and road map, (a schedule of planned new products in development and to be delivered into th e

marketplace in future periods), falsely representing that Nokia's purportedly superior product s

were the primary reason for its financial success, healthy phone ASPs and growing market share .

In fact, Nokia's strong performance in late 2003 was an aberration . In fourth quarter 2003

("4Q03"), despite Nokia 's weak product line-up, a long-term downward trend in Nokia ' s phone

market share and in its ASPs was momentarily interrupted when a massive surge in consume r

demand caused component shortages at Nokia's major competitors, thereby suppressing thei r

sales to Nokia's benefit. In January 2004, despite knowing Nokia's true problems with its phon e

portfolio and product roadmap, and the looming resumption of the negative trend in the ASPs of

52498821

Nokia's phones that would necessarily flow from these product deficiencies, the defendant s

issued guidances to market analysts of expected increases in Nokia sales of 3% to 7% in 1 Q04 ,

as well as increases in its ea rn ings per share . In January 2004, Nokia's CEO also announced that ,

based upon Nokia' s "current momentum ," he expected Nokia to further improve its phon e

market share, particularly in Europe .

9. Even at Nokia's annual shareholders' meeting held on March 25, 2004 -- a mere

two weeks before the disclosure of its shockingly poor 1 Q04 phone sales performance -- Nokia' s

CEO continued to falsely represent that Nokia's purported success was attributable to its "strong "

and "very competitive" phone portfolio :

We reached these goals in part due to our strong product portfolio. As we haveearlier stated, we launched 40 new products last year. This was a record numberof mobile device launches for Nokia during one year . This year, we expect tolaunch a similar number of products . I strongly believe that our product portfoliocontinues to be very competitive.

For 1Q04, the quarter ended March 31, 2004, six days after the shareholders' meeting, Nokia' s

mobile phone sales fell 15%, or $880 million . Nokia's 1Q04 operating profits on its mobil e

phones was even worse -- they fell by 25%, or $300 million . Over the next week, Nokia's CEO

would personally and finally admit the truth, that Nokia's phone portfolio (and roadmap )

particularly in its core mid-range phones sold in the critical phone replacement market was

deficient and that these deficiencies were known to exist since early 2003 .

10. Although defendants were aware that Nokia's 4Q03 performance and the singl e

quarter uptick in its ASP were obtained as a result of factors that would not recur, that certain o f

its newly released high-priced products, such as the N-Gage gaming device, had been soundly

rejected by consumers , and that it was steadily losing market share in Weste rn Europe, its most

F2498821

important market, in large part because defendants had stubbornly refused to customize Noki a

phones for key phone service operators, defendants on January 22, 2004, proclaimed Nokia' s

"best ever performance" and a structural shift in its long-deteriorating trend of its ASPs .

Simultaneously, in making its projections of 3 to 7% sales growth, Nokia's CEO assured

investors that its forecasting was "fact-based," that he received weekly revenue reports, includin g

by reference to the performance of its competitors, and that Nokia "had exceptionally good

visibility throughout the channel ." The CEO further emphasized that for the critical European

market, Nokia expected to gain market share in 1 Q04, and that in Europe, its "produc t

positioning was really well in the fourth quarter, particularly in the high end . "

11 . Despite the strongest industry-wide growth in the history of mobile phones, on

April 6, 2004, defendants shocked the market with the announcement that, rather than increasin g

3% to 7%, Nokia' s net sales had declined 2% . (The severity of Nokia 's predicament became

even clearer when on April 16, 2004 defendants released Nokia's 1 Q04 financial statements that

showed an extraordinary 15% decrease in sales of its core mobile phones business, and

announced that sales would continue to be depressed in later qua rters.) In Nokia's April 6, 2004

press release, Nokia revealed that, "[D]ue to certain gaps in its product portfolio, mainly in th e

mid-range, the company was not able to fully capitalize on positive market developments ." And,

later that day, Ollila admitted that he had seen this shortcoming "early on last year." Although as

late as the March 25, 2004 shareholders conference, Ollila had loudly trumpeted Nokia's releas e

during 2003 of a "record" forty new phones, in reality Nokia's product portfolio had sharpl y

degraded and Nokia simply recirculated the same series 400 phones with different face plates ,

colors and minor cosmetic changes . Nor had there been "new" phones in the roadmap for release7

2498821

in 1 Q04 . Defendants soon revealed additional reasons for Nokia 's poor performance -- th e

failure of the N-Gage gaming device, its misjudgments in the development of clamshells, th e

drift away from TDMA to CDMA technology, and problems in Nokia 's relationships with phone

service operators -- all facts which defendants well knew, and concealed, when they mad e

representations to analysts and investors about Nokia's supposedly robust product portfolio ,

growing success in CDMA , fixed operator relationships , and rosy sales forecasts .

12. With the shock of the April 6, 2004 announcement, the price of Nokia's ADR s

traded in the United States, and its stock traded throughout the world, dropped 16% for a single-

day trading loss in market capitalization of $17 billion . With the additional revelations made o n

April 16, 2004, Nokia's stock price dropped another 9%, for another $8 billion one-day drop i n

Nokia's market capitalization .

JURISDICTION AND VENUE

13 . The claims asserted herein arise under and pursuant to Sections 10(b) and 20(a) o f

the Exchange Act, 15 U.S.C. §§ 78j(b) and 78(a), and the rules and regulations promulgate d

thereunder by the SEC, including Rule l Ob-5, 17 C .F.R. §240.1 Ob-5 .

14. This Court has jurisdiction over the subject matter of this action pursuant to 2 8

U.S.C. §§ 1331 and 1337, Section 22 of the Securities Act, 15 U .S.C. § 77u, and Section 27 o f

the Exchange Act, 15 U . S .C . §78aa.

15. Pursuant to the "effects test" of extraterritorial jurisdiction this Court ma y

properly exercise subject matter jurisdiction over the claims of (a) all investors who purchased o r

acquired Nokia securities traded on U .S . Markets, and (b) American investors who purchased or

acquired Nokia securities regardless of where those securities traded .

82498821

16. This court may also properly exercise subject matter jurisdiction over the claims

of foreign class members who acquired Nokia ordinary shares traded on foreign markets unde r

the "conduct test" articulated by the Second Circuit, which provides that a federal court has

subject matter jurisdiction if (1) the defendant's activities in the United States were more tha n

`merely preparatory' to a securities fraud conducted elsewhere, and (2) these activities o r

culpable failures to act within the United States `directly caused' the claimed losses .

17. Defendants engaged in extensive securities fraud-related conduct in the U .S . ,

which was part of a single fraudulent scheme spanning the U . S. and Europe . The domestic

conduct was not merely "preparatory" or perfunctory acts, but led directly to losses by bot h

foreign and domestic investors . In addition to the substantial U .S . conduct in furtherance of the

fraud, Nokia has a vast U .S . presence that justifies the exercise of subject matter jurisdiction ove r

the claims of all plaintiffs who, relying on the health and value of Nokia's substantial U .S .

businesses, acquired Nokia securities traded on foreign markets, and were defrauded b y

defendants' misrepresentations .

18. In addition , there was but a single worldwide market for Nokia American

Depositary Shares (securities) which traded in tandem with Nokia stock on foreign exchanges

and that market was defrauded by defendants' conduct, causing extensive effects both in thi s

country and abroad .

19. In addition to Nokia's vast U.S. activities , a significant number of defendants '

false and misleading statements were initially made in the United States, including at a two-day

"Capital Markets Day" conference convened in Dallas, Texas in November 2003 by Nokia an d

several of the individual defendants for market analysts covering Nokia's stock . All of

92498821

defendants' false and misleading statements identified in the Complaint were disseminate d

within the U.S ., including by Forms 20-F and numerous Forms 6-Ks filed with the SEC durin g

the Class Period, as well as in its 2003 Annual Shareholders Report posted on Nokia's website .

20. Prior to and during the Class Period, false and misleading statements not made in

the United States were disseminated into the United States and internationally through the mean s

and instrumentalities of interstate commerce, including but not limited to the mails, interstat e

telephone communications, the internet and the facilities of the national securities markets .

21 . According to the Company's Form 20-F for the fiscal year ended December 31 ,

2003, signed and filed with the SEC on February 6, 2004, over seven percent of Nokia's long-

lived assets, valued at 120 million euros, were located in the U .S . In 2003, Nokia received

approximately $4.5 billion dollars in net sales from the United States, making the United State s

Nokia's largest market . In addition, Nokia Corp. employs approximately 6,600 people in the

United States . Approximately 25% of Nokia's securities trade on the New York Stoc k

Exchange .

22. Venue is proper in this District pursuant to Section 22 of the Securities Act, 1 5

U.S.C . § 377u, Section 27 of the Exchange Act, 15 U . S.C . §78aa, and 28 U .S .C. § 1391(b) .

Nokia is headquartered in Espoo, Finland, but conducts business and maintains a U .S .

headquarters in Irving, Texas and other facilities in Forth Worth, Texas, Mountain View ,

California, Los Angeles, California, San Diego, California and White Plains, New York . In

addition, Nokia and the individual defendants chose to hold Nokia's 2003 and 2004 Capital

Markets Day events, Nokia's annual presentation to market analysts reporting on Nokia's stock,

in the United States .10

2498821

23 . In addition, many of the acts and practices complained of herein, including the

dissemination of materially false and misleading statements, occurred in this District .

24 . In connection with the acts alleged in this Complaint, defendants directly or

indirectly, used the means and instrumentalities of interstate commerce, including but not limite d

to the mails, interstate telephone communications and the facilities of the national securitie s

markets .

THE PARTIE S

25 . Generic Trading of Philadelphia, LLC , Martin Bergljung and Gerald Hoberman

were appointed as Co-Lead Plaintiffs by this Court on August 12, 2004. Co-Lead Plaintiffs

purchased or otherwise acquired the common stock or ADRs of Nokia during the Class Period a t

prices that were artificially inflated by defendants' misrepresentations and omissions and suffere d

damages thereby, as detailed in their certifications incorporated by reference herein and attache d

as Exhibit A .

26 . Defendant Nokia is a Finnish limited liability company with its executive offices

located at Keilalahdentie 4, FIN-00045 Nokia Group, P .O. Box 226, Espoo , Finland, and its

principal United States offices at 6000 Connection Drive, Irving, Texas, 75039 . The Compan y

concentrates its business in four major areas : Mobile Phones, Multimedia, Networks and

Enterprise Solutions . Nokia is the self-described world leader in mobile communications ,

primarily offering voice-centric mobile telephones, enhanced communicators, entertainment and

gaming devices and media and imaging telephones. In fiscal year 2003, Nokia's net sales totale d

$37.1 billion, and its net profits totaled $4 .5 billion. The company currently has approximately

50,000 employees, maintains production facilities in nine countries, and sells its products in over

11249B821

130 countries . The principal trading markets for Nokia securities are the New York Stoc k

Exchange, in the form of ADRs, and the Helsinki Exchanges, in the form of shares . In addition ,

the shares were listed on the Frankfurt, Stockholm, London and Paris stock exchanges. Nokia' s

securities were actively traded on each of these five exchanges, all efficient markets, during th e

Class Period .

27 . Defendant Jorma Ollila was at all relevant times Nokia's Chairman of the Boar d

and Chief Executive Officer . Ollila was the lead presenter at Nokia's Capital Markets Day even t

held in Dallas, Texas in November 2003 .

28. Defendant Pekka Ala-Pietila ("Ala-Pietila ") was at all relevant times Nokia' s

President, and an executive board member.

29. Defendant Matti Alahuhta ("Alahuhta") was at all relevant times Nokia' s

Executive Vice President, Chief Strategy Officer, and an executive board member .

30. Beginning January 1, 2004, Defendant Richard A . Simonson ("Simonson") was

Nokia's Chief Financial Officer and an executive board member.

31 . Defendant Olli-Pekka Kallasvuo ("Kallasvuo") preceded Simonson as Nokia' s

CFO, and was also Nokia's Executive Vice President, General Manager of Mobile Phone s

Division, and an executive board member . Kallasvuo was a key presenter at Nokia's Capita l

Market day event held in Dallas, Texas in November 2003 .

32 . During the class period, Defendant Anssi Vanjoki was a Nokia Executive Vice

President, General Manager of its Multimedia Division, and an executive board member .

Kallasvuo was a key presenter at Nokia's Capital Market day event held in Dallas, Texas i n

November 2003 .12

249882_1

33 . Defendants Ollila, Ala-Pietila, Alahuhta, Simonson, Kallasvuo and Vanjoki ar e

referred to herein as the "Individual Defendants ."

34. During the Class Period, the Individual Defendants, as senior executive officers

and/or directors of Nokia, were privy to confidential and proprietary information concerning

Nokia, its product portfolio and performance, market share, phone sales prices, and present an d

future business prospects . The Individual Defendants also had access to material adverse non-

public information concerning Nokia, as discussed in detail below . Because of their positions

with Nokia, the Individual Defendants had access to non-public information about its business ,

products, markets and present and future business prospects via access to internal corporat e

documents, conversations and connections with other corporate officers and employees ,

attendance at management and board of directors meetings and committees thereof and via

reports and other information provided to them in connection therewith . In light of their publi c

representations to investors and to market analysts, these defendants either knew their statements

were false or were reckless in failing to confirm their truthfulness before they spoke .

35 . The Individual Defendants are liable as direct participants with respect to th e

wrongs complained of herein . In addition, the Individual Defendants, by reason of their status a s

senior executive officers and/or directors, were "controlling persons" within the meaning o f

Section 20 of the Exchange Act and had the power and influence to cause the Company t o

engage in the unlawful conduct complained of herein . Because of their positions of control, th e

Individual Defendants were able to and did, directly or indirectly, control the conduct of Nokia' s

business .

132498821

36. The Individual Defendants, because of their positions with the Company, and/or

because of their presence when false representations about Nokia were made by other Noki a

officers and employees, controlled and/or possessed the authority to control the contents of its

reports, press releases and presentations to securities analysts and through them, to the investing

public. The Individual Defendants were provided with copies or recordings of the Company' s

reports, press releases and presentations alleged herein to be misleading, prior to or shortly after

their issuance and had the ability and opportunity to prevent their issuance or cause them to be

corrected .

37 . As senior executive officers and/or directors and as controlling persons of a

publicly-traded company whose securities were, and are, registered with the SEC pursuant to the

Exchange Act, and were traded on the NYSE and governed by the federal securities laws, the

Individual Defendants had a duty to disseminate promptly accurate and truthful information with

respect to Nokia's performance, growth, operations, trends, business, products, markets ,

management, revenues, and present and future business prospects and to correct any previously

issued statements that had become materially misleading or untrue, so that the market price of

Nokia's securities would be based upon truthful and accurate information . The Individual

Defendants' misrepresentations and misleading omissions during the Class Period violated thes e

specific requirements and obligations .

38 . The Individual Defendants are liable as participants in a fraudulent scheme and

course of conduct that operated as a fraud or deceit on purchasers of Nokia securities b y

disseminating materially false and misleading statements and/or concealing material advers e

facts . The scheme (i) deceived the investing public regarding Nokia's business, operations,

142498821

management and performance, and the intrinsic value of Nokia securities, and (ii) caused

plaintiffs and members of the Class to purchase Nokia securities at artificially inflated prices .

PLAINTIFF'S CLASS ACTION ALLEGATION S

39. Plaintiff brings this action as a class action pursuant to Federal Rule of Civi l

Procedure 23(a) and (b)(3) on behalf of a Class consisting of all those who purchased the

securities of Nokia between October 16, 2003 and April 15, 2004 (the "Class Period") and wh o

were damaged thereby. Excluded from the Class are defendants, the officers and directors of th e

Company, at all relevant times, members of their immediate families and their legal

representatives, heirs, successors or assigns and any entity in which defendants have or had a

controlling interest .

40. The members of the Class are so numerous that joinder of all members i s

impracticable . Throughout the Class Period, Nokia ADRs were actively traded on the NYSE and

its shares were listed on the Helsinki, Frankfurt, Stockholm and Paris stock exchanges . While

the exact number of Class members is unknown to plaintiffs at this time and can only b e

ascertained through appropriate discovery, plaintiffs believe that there are thousands of member s

in the proposed Class . Record owners and other members of the Class may be identified fro m

records maintained by Nokia, its depositary or its transfer agent and may be notified of th e

pendency of this action by mail, using the form of notice similar to that customarily used in

securities class actions .

41 . Plaintiffs' claims are typical of the claims of the members of the Class as al l

members of the Class are similarly affected by defendants' wrongful conduct in violation o f

federal law that is complained of herein .

152498821

42 . Plaintiffs will fairly and adequately protect the interests of the members of th e

Class and have retained counsel competent and experienced in class and securities litigation .

43 . Common questions of law and fact exist as to all members of the Class an d

predominate over any questions solely affecting individual members of the Class . Among the

questions of law and fact common to the Class are :

a. whether the federal securities laws were violated by defendants' acts a s

alleged herein ;

b. whether statements made by defendants to the investing public during the

Class Period misrepresented material facts about the business and operations of Nokia or omitte d

material facts ; and

to what extent the members of the Class have sustained damages and the

proper measure of damages .

44 . A class action is superior to all other available methods for the fair and efficient

adjudication of this controversy since joinder of all members is impracticable . Furthermore, a s

the damages suffered by individual Class members may be relatively small, the expense and

burden of individual litigation make it impossible for members of the Class to individuall y

redress the wrongs done to them. There will be no difficulty in the management of this action as

a class action.

45 . Purchasers of Nokia ADRs on the NYSE and stock on the foreign exchanges ar e

appropriately included within a single world-wide class because the price of these securitie s

moved in tandem as disclosures were made by Defendants and disseminated throughout the

world-wide market . In addition to filing false and misleading statements with the SEC and

162498821

foreign exchanges, Nokia issued press releases that were published world-wide and posted on its

website . Defendants held conferences in the United States and elsewhere for market analysts ,

and otherwise held interviews with market analysts, so that Defendants' comments about Nokia' s

products and performance were disseminated throughout the world-wide community in analysts '

reports .

SUBSTANTIVE ALLEGATION S

Background

46. In the early 1980s, Nokia began to strengthen its position in th e

telecommunications and consumer electronics markets through a series of acquisitions o f

companies in Sweden. By the late 1980s, through the acquisition of Ericsson's data system s

division Nokia became the largest Scandinavian information technology company . In 1987,

Nokia produced the original hand-portable mobile phone . In 1989, Nokia significantly expanded

its cable operations into continental Europe by acquiring the Dutch cable company, NKF . From

1987 through 1991, Nokia worked closely with operators to create a "wire-free" world by

developing the technology for the Global System for Mobile Communications ("GSM"), th e

digital standard adopted throughout Europe . Since the early 1990s, Nokia has concentrated on its

core telecommunications business . In addition to developing manufacturing and marketing cel l

phones throughout the developed and developing world, over the last 15 years, Nokia worked

with phone systems operators (such as AT&T) to plan, deploy, integrate and operate thei r

networks and mobile servers .

47. Originally Nokia so dominated the industry that the company could dictate which

products operators could incorporate with their phone services . However, as new phone

172498821

manufacturers entered the market and competition escalated in both the United States and

Europe, phone service operators, as the gateway to the primary cell phone market, began t o

exercise their power to pick and choose among the models offered by Nokia and the other cel l

phone manufacturers that would, as a practical matter, become widely available and sold through

their thousands of retail outlets to consumers . These operators also invested vast sums to

advertise, promote and subsidize the costs of the cell phones as part of the service contracts the y

marketed to consumers .

The Development and Shift in Operating System s

48 . Today, mobile phones generally operate on the TDMA, GSM and CDM A

systems . While Europe gravitated to GSM in the late 1980s, the Cellular Telecommunication

Industry Association chose TDMA, which became widely used in the United States . Nokia

overwhelmingly dominated the cell phone market for this TDMA technology, with more than

75% market share . The flexibility to add new features to TDMA, however, is limited, and a

growing technology competition began to replace TDMA by Qualcomm in favor of CDMA

versus the GSM standard used in Europe . AT&T and Cingular replaced their TDMA syste m

with GSM, where Nokia retained a strong market share of 35-40%, but Verizon Wireless an d

Sprint, who together provide service to approximately 50% of United States cell phone

consumers, shifted over to CDMA technology . In 2002, Nokia had a paltry market share i n

CDMA phones, and by 2003 its share had risen to only about 11 .4%. Shifts away from the

TDMA technology accelerated sharply in 2003, and by 2003 the share of the worldwide cel l

phone market using CDMA technology had risen to 21 % . The increasing shift away from

TDMA to GSM, and particularly to CDMA, greatly eroded Nokia's overall market share of the

182498821

world-wide cell phone market . Thus, in 2003, while Nokia often proclaimed its major strides in

improving its CDMA share, it failed to disclose that the on-going and accelerating market shif t

from TDMA (where Nokia ' s share was 75%) to CDMA was severely harming its sales, ASPs

and market share .

49. The CDMA chip set developed by Qualcomm was licensed to many of the majo r

cell phone manufacturers that marketed phones in the United States. Nokia, however, refused t o

enter into a license agreement with Qualcomm, and for years attempted, with limited success, to

develop its own chipset . Nokia's chipset was generally considered to be inferior to the on e

developed by Qualcomm, and, as a result, Sprint and Verizon refused to purchase Nokia CDM A

phones . The United States operators relented in 2003, when Nokia obtained a CDMA chip from

Texas Instruments. By 2003, however, Nokia had fallen far behind other manufacturers, such a s

Samsung, in developing CDMA phones . The ongoing joke in Nokia's Irving, Texas product

development office was that, when it came to CDMA technology, "instead of twelve months ,

they were on a twelve year cycle . "

50. Throughout 2003, Nokia had managed to develop and market only low-en d

CDMA phones in its traditional "candy-bar" design, which often became the phone that United

States operators gave away in their promotions, or the "penny" cell phone. Business trailed off,

however, when the promotion was dropped, and consumers switched to the Samsung phone

which listed at the same price as Nokia but had substantially more features. Nokia's delay in

developing well-designed CDMA phones with color and imaging features (i.e., camera phones)

degraded its brand, depressed its market share, and reduced its ASPs. As Nokia finally admitte d

192498821

at its "Capital Markets Day" in New York in November 2004, Nokia would not have a fill range

of CDMA phone products until the second halfof 2005 .

Nokia's Refusal to Develop a Clamshell Phon e

51 . Throughout 2002 and 2003, the "flip" or "clamshell" design developed b y

Motorola gained increasing popularity, particularly in the United States. Several former Nokia

employees in the United States, including a former head of United States operations and a head

of United States marketing and sales, recounted repeated requests to senior management i n

Finland for development of a clamshell design phone, citing to repeated customer surveys

showing 15% or more customer demand for this design . The response from Finland? We're

Nokia and they will buy what we sell .

52. For example, in a meeting in Dallas in May 2003, attended by sales personnel and

Tim Eckersley, a Senior VP of Sales, Eckersley stood up and adamantly stated that "there is no

way that Nokia will ever make a silver folding phone ." The reaction of many in sales was

disbelief that Nokia's senior management so deliberately and continuously rejected th e

preferences of Nokia's consumers shown by their market research . For years, Nokia's senior

officers in Finland , including Matti Alahuhta, proclaimed their unwillingness to develop a

clamshell design, despite repeated customer demand for the product, because the widely accepte d

and marketed silver clamshell had originally been designed and popularized by Motorola, for

years Nokia' s closest competitor .

Nokia's Refusal to Customize Phones For Operator s

53 . Historically, outside of the United States and Asia, phone consumers typicall y

first chose a phone brand and then selected the service operator or provider . In the United States,

202498821

service operators have always controlled the major segments of the cell phone market, and

increasingly exercised their power to pick among various manufacturers' models that would b e

offered through their thousands of retail outlets . Control over the distribution of major segments

of cell phones in Europe has, however, steadily shifted from major phone distributors to majo r

service operators, such as Vodafone, the world's largest operator, headquartered in London, an d

France, Telecom S.A. Orange, ("Orange S .A.") Europe's third largest operator . Vodaphone

purchased tens of millions of cell phones from phone manufacturers, and historically turned t o

Nokia for more than 50% of its purchases . Operators in the United States controlle d

approximately 90% of cell phones sales ; in Europe, operators controlled about 50% of th e

market .

54. Until recently, Nokia jealously guarded its brand, often refusing United States an d

European operators' requests for customized phones, including phones bearing the operators '

logos . As more Asian phone manufacturers, such as Sharp and Samsung, developed and

improved their phone portfolios, the operators that had been spurned by Nokia, includin g

T-Mobile, Verizon, Vodafone, and Orange S .A., increasingly turned to them to provide th e

customization that Nokia had refused .

55 . For example, as recently reported in the press, in the fall of 2001, Thomas

Geitner, then Vodafone's head of global products and services, approached Sharp to make cel l

phones with built-in cameras for Vodafone to sell in Europe . In the fall of 2002, as part of a

program called Vodafone Live, Geitner offered to buy Sharp models but only on the condition

that they would be specifically designed to support Vodafone's launch of a picture -messaging

and video games service .21

2498821

56. When Vodafone approached Nokia to outfit Nokia camera phones with Vodafone

Live services, Nokia refused to meet Vodafone's specifications, such as putting Vodafone's re d

logo on the front of the phone, as Sharp and Mitsubishi had agreed to do . As Juha Putkiranta ,

head of Nokia's imaging unit explained, "If the product is Nokia-branded, it needs to feel like a

Nokia product or the brand is worth nothing ." Nokia, as a compromise , agreed to post the

Vodafone logo on the back of its phone . Vodafone launched "Vodafone Live" in Novembe r

2002 with Sharp as the centerpiece of its advertising blitz, and as a result, the Sharp phon e

gained more than 50% of the market for all phones sold with Vodafone Live .

57. Thereafter, in early 2003, Vodafone obtained concessions by Motorola and Sony

Ericsson to customize their phones to meet Vodafone demands . In late 2003, Nokia began to

supply Vodafone with some mid-priced phones that met some, but not all, of its requeste d

criteria -- e .g., Nokia continued to refuse to carry the Vodafone logo on the front of its phone .

58 . Also, as recently reported in the press, in late 2002, Orange S .A. asked Nokia to

create a handset that connected to the internet at the push of a button . Nokia refused . In October

2002, Orange purchased fully tailored phones from companies such as High Tech Computer

Corp. of Taiwan .

59. In February 2003, Orange S .A. officials met with cell phone suppliers to set out

the features they wanted in their cell phones . Orange wanted midrange phones to include, amon g

other things, high resolution color screens, and special keys and software to access Orange' s

services. Defendant Vanjoki told Orange S .A. that Nokia would not be able to introduce those

features at midrange prices until 2004 . Orange then turned to Motorola and other suppliers .

222498821

60. Unlike Nokia, phone manufacturers in Asia actively courted the key phone servic e

operators . For example, LG, a Korean mobile phone manufacturer, aligned itself with Verizo n

by stationing fifty of its engineers in the United States for weeks to help tailor its phones to

Verizon's requirements .

The Weaknesses in the Product Portfoli o

61 . Even beyond the issues described above, Nokia's product portfolio began t o

seriously deteriorate in 2002 . According to a former Nokia employee working in Irving, Texa s

as a liaison between Nokia's research and development and manufacturing divisions, wit h

visibility into Nokia's product roadmap, there is generally a two-year development lag to produc e

a new phone . Nokia's marketing unit would develop the idea for a new phone, its research an d

development group would develop the schematics, and then this employee, as part of th e

mechanical sourcing group, would reach out to suppliers to meet the manufacturin g

requirements . In 2002, there were few products under development, so that it was well know n

that, by early 2004, Nokia would be caught short in its product portfolio .

62. Another former Nokia employee, a Nokia chief hardware engineer in Irving,

Texas, further explained that they were permitted only nine to twelve months to design and

develop new phones, so that the product quality of Nokia's phones began to deteriorate .

According to this source, Nokia "cut corners" on the Model 6100 so that many of the phone s

experienced display problems and were returned by carriers . At least two Nokia high end phone s

would stop working altogether if dropped . Problems in producing the mid-tier TDMA color

phone (Model 6265) were ignored and delayed its introduction . In 2003, it was well known that

many of Nokia's phones sold in the United States had technical problems, and chipsets and

232498821

displays were frequently defective . According to a former technician for Cingular Wireless i n

Tampa, phones supplied to Cingular were often returned because of problems in the phones '

chipsets .

63. By mid-2003, in Irving , Texas, weekly project meetings were held among

members of Nokia's engineering, software, programming, mechanical, field services and fiel d

repair offices with the phone service operators' technical account manager to discuss operators '

concerns with Nokia's products . Each week, the technical account manager would convey th e

operators' "top ten" list of "field failures" or return issues . Cingular was most vocal i n

complaining about quality issues with Nokia phones .

64. Starting in 2002, rather than developing truly new phone products, Noki a

continued to rely upon the same series 400 platform and simply recycled its existing products by

putting different faceplates on them, or modifying minor features like changing the screen t o

blue, to make them look different . At the same time, Samsung and Kyocera were beginning t o

capture large shares of the market with more robust, higher quality and better phone technology .

At one point, developers in the Nokia office in Irving, Texas took apart and examined the

features and technology of a Samsung phone and realized that Nokia's product roadmap for ne w

products could not match Samsung's current model, that, e.g., Nokia lacked the miniaturizatio n

of Samsung's existing phone .

65 . Another former Nokia employee sent from Finland to correct perceived problem s

at Nokia's Marketing and Development office in Irving, Texas confirmed that Nokia's produc t

portfolio and roadmap deficiencies dated back to 2002 and continued into 2003, and that Nokia

issued too many versions of each kind of phone . This source reported viewing at least two

242498821

separate and confidential reports in Irving, Texas, describing significant flaws in the Symbian

Systems technology used in Nokia's cell phones . Nokia owned a substantial stake in Symbian,

and while this operating system was widely used for "smart phones" marketed to consumers, i t

was inferior to Microsoft's operating system for business applications, such as Symbian' s

weakness in supporting corporate e-mail . As a result, despite Nokia's enormous research and

development investments , Nokia sold only 5 . 5 million smart phones in 2003, well below it s

target .

66 . Others familiar with the failures and quality of Nokia's phones, e .g., from

Prismark, an electronic consulting firm, and at Bell Systems, confirmed that, in 2003, the feature s

of Nokia's phones did not match its competition . For example, Bell Systems over-inventoried

the Nokia 6010, even though Bell had provided it as the "free" phone, because consumers ha d

rejected it .

67. Many of the weaknesses in Nokia's phone portfolio such as the small screens o n

its camera phones, or their poor color resolution due to the failure to provide mega-pixel phones ,

and their monolithic "candy bar" shape, were well-known by senior management in Finland a s

the weaknesses had resulted from management's own calculated decisions to sacrifice innovatio n

to preserve Nokia's cost structure . As Ben Wood, a mobile analyst at market researcher Gartne r

Research, near London, explained in May 2004, "Nokia is focused on running a tight ship at th e

expense of a wow factor ." Moreover, for years, much of Nokia' s success in maintaining high

phone profit margins was attributable to production of the phones in manufacturing facilities tha t

had become highly automated . Growing demands from operators for highly customized phone s

would force Nokia to retool its m anufactu ring to accommodate smaller production runs . Major25

2498821

design changes would thus significantly drive up manufacturing costs and reduce Nokia' s

operating margins .

68. Although as of March 25, 2004, Nokia's CEO was still publicly hawking to it s

shareholders and investors the "record" forty new phones Nokia had released in 2003 as proof o f

Nokia's "strong" and "competitive " product po rtfolio , by April 2004, he had dropped these

pretenses and finally admitted that Nokia's product portfolio had been deficient since early 2003 .

The N-Gage Games Product Failur e

69 . While in 2003 Nokia did little to improve the quality and competitiveness of it s

high volume phone business, in early 2003 Nokia wasted enormous sums of research an d

development dollars on its "smart phones," including on a new but ill-conceived combinatio n

phone and gaming device referred to as "N-Gage ." N-Gage was heavily pushed and promoted in

2003, and was even prominently displayed in every corner of every lobby in all four Nokia

buildings in Irving, Texas . According to a product marketing manager working in Finland an d

Singapore, the marketing department did product research before launching the N-Gage . Despite

Nokia's hype of this product, the research showed that the N-Gage price was too high and th e

design was faulted as not being ergonomic . The device was a physically large phone which had

to be turned on its side for use as a phone and which, because of its small screen, was no t

attractive for playing games . N-Gage was so ill-designed that its batteries needed to be removed

when changing games. Because of its unattractive design, the N-Gage was derisively describe d

throughout the company (in Finland and the United States) and at customers, such as at

GameStop, as the "taco phone." Despite its high retail price (300 Euros), the N-Gage device

262498821

could not begin to compete with other popular gaming devices such as Nintendo's "Pla y

Station."

70. Nokia launched the N-Gage device with great fanfare to 30,000 outlets throughou t

the world on October 7, 2003 . From the beginning, the N-Gage was sold with $100-off

promotions and rebates at outlets such as GameStop . As described by a product marketing

manager for this product, within a month of its launch many employees within Nokia's sales an d

marketing departments in Finland learned the product was unsuccessful . Anssi Vanjoki was the

key backer and cheerleader for the N-Gage product .

71 . Because of the N-Gage's unpopularity, the channels to which it had been

delivered remained "stuffed" after the Christmas season, and the product was either returned or

heavily discounted in 2004 . For example, one account manager in Nokia's Fort Worth plant in

Texas cited a $23 million credit to Target Stores for the return in 1Q04 of unsold N-Gag e

products and accessories .

72. As reflected in Nokia's Form 20-F for 2003, filed on February 6, 2004, it was

Nokia's revenue recognition practice to report sales revenue on its financial statements whe n

delivery occurred, assuming the price was fixed and collectibility was probable . At the same

time, the impact on sales revenues for the rebates and other promotions of its delivered products

was "estimated" based on other past programs :

Nokia records estimated reductions to revenue for customer programs andincentive offerings, including special pricing agreements, price protection andother volume based discounts, mainly in the mobile phone business . Salesadjustments for volume based discount programs are estimated based largely onhistorical activity under similar programs . Price protection adjustments are basedon estimates of future price reductions and certain agreed customer inventories atthe date of the price adjustment .

272498821

73 . Thus, the high-priced (but unsuccessful) N-Gage product that was first released in

the fourth quarter of 2003 ("4Q03"), and remained in retail channels well after the Christma s

rush , served to increase Nokia's year-end 2003 revenues, as well as its ASP, while the actual

high returns and discounts experience by Nokia on the N-Gage served to decrease Nokia's ASP

of Nokia's phones in 1Q04 .

74. In an October 7, 2004 market research report, RBC Capital Markets noted that i n

2004 Nokia's market share in Europe had been impacted by correction in channel inventory .

The Manipulation of Quarterly and Year End Revenues

75 . In 2003, Nokia manipulated and over-repo rted phone sales in violation of the

revenue recognition practice reported in its Form 20F by shipping phones to phone service

operators with the understanding that Nokia would accept the return of the phones that failed to

sell . This practice also violated International Accounting Standards ("IAS") and United States

Generally Accepted Accounting Principles ("GAAP"), particularly Statement of Financia l

Accounting Standard ("SFAS") #48, and the SEC Staff Accounting Bulletin ("SAB") 101 .

76. A former Nokia program manager working at Irving, Texas in 2003 reported that ,

in 2003, he had observed a wide-spread and common practice whereby, each month, sale s

personnel would deliver mobile phones to AT&T, and the other service operators, with the

understanding that unsold phones would be returned to Nokia .

77. Because phones sold to one se rv ice operator , e.g. AT&T, could not be resold t o

another, e .g. Cingular, the returned phones were disassembled at Nokia's factory in Texas . The

process to break down a phone was a time consuming job, requiring about ten minutes per phone ,

282498821

because the pallet had to be taken apa rt . The parts would then be returned to Nokia's supply

inventory .

78. Another former Nokia employee, an account manager in Nokia's Fort Worth plan t

in Texas described Nokia's long-held practice of billing a customer (and recognizing th e

revenue) while continuing to hold the units at the dock in order to manipulate end-of-quarte r

sales numbers . Richard Wooldridge, Nokia's United States National Operations manager,

originally came up with the dock-holding policy, but after the Enron scandal, the undelivered

goods were moved onto trucks where they were held . This practice also manipulated revenue s

and violated the revenue recognition practice reported in Nokia's Form 20-F,1AS and GAAP ,

including SAB 101 .

79. This source related a particularly outrageous example where Brightpoint, Nokia' s

largest United States distributor, specified a significant shipment to be delivered to Indianapoli s

around January 5, 2004. Nokia shipped out these goods in mid-December 2003, about three

weeks early even though the usual required shipping time was 2-3 days .

80. For 4Q03, in order to make Nokia's numbers, Wooldridge and Barbara Carroll ,

another Nokia manager in Texas, also ordered that units known to be defective, including th e

Model 5165 that had significant problems with its LCD displays, be shipped out to customers .

Both managers commented (while the source was present) that 100% of the product would need

to be taken back in 2004 . Wooldridge, in particular, kept saying that, "we're going to be takin g

big hits in the first quarter of 2004," and "we're screwed for first quarter '04 ." Millions of

dollars worth of the Model 5165 was shipped out . Similarly, another model popular in th e

United States, the Model 3285, was shipped out at year-end while Wooldridge and Carroll knew

292498821

it had contained a bad component, the "saw filter" which was inserted in the phone to filter ou t

electrical spikes. Millions of dollars of the defective Model 3285 were shipped out to

Brightpoint in Indianapolis, U .S . Cellular in Chicago, and Alltel in Alpharetta, Ga . This source

then observed the crediting of customers' accounts as the products came flooding back durin g

I Q04 .

Nokia's Trends in Market Share and Sales

81 . As described in a July 16, 2004 analyst report by Morgan Stanley, until 4Q0 3

when the sequential phone average selling p rice , ASP, rose by 2.7%, to $128 .70, Nokia' s mobile

phone ASP had been steadily dropping since 1999 :

Sequential QuarterlyNokia Phone ASP Decrease in ASP

1999 179.6 12000 176 .502001 168 .742002 154 .1 51Q 2003 147.75 .8%2Q 2003 136.46 7.6%3Q 2003 125.32 8.2%

In 1 Q04, Nokia's ASP resumed its decline -- by 9 .3 %, or to $116 .69 .

82 . Besides the 4Q03 release of certain high-priced (but unsuccessful) new products ,

such as the N-Gage, the other factor that momentarily broke, in 4Q03, the steady fall in the AS P

for Nokia' s phones, and also temporari ly increased Nokia's market share, involved a sudden

industry-wide surge in demand for cell phones. Demand in developing nations, such as China,

India and Latin America, for first-time and low-priced cell phones significantly increased, but s o

did demand in the phone replacement market in the United States and Europe for phones with

new features, such as for new camera and color phones . This sudden jump in demand outr an

302498821

supplies for phone components, particularly for such items as new camera screens, causin g

significant shortages at Motorola and among Nokia's less-established Asian competitors .

Because of Nokia's long-lasting and superior relationships with its own vendors, Nokia was abl e

to exploit these shortages to improve its 4Q03 performance, despite the relative inferiority of it s

mid and high-priced phone portfolio .

83 . In May 2004, Morgan Stanley reported the following shifts in market share

between Nokia and its two largest competitors :

3Q03 4Q03 1Q04Nokia 33.7% 34.7% 29.2%Motorola 15.0% 14.1% 16.5%Samsung 11.0% 9.7% 13.1%

84. The change in Nokia' s market share translated into a loss in sales volume o f

approximately nine million phones for a single quarter. Even Nokia's supply chain advantages ,

however, did not serve to fully stem its decline in market share in its most important an d

developed market, Western Europe . Again, as reported by Morgan Stanley in May 2004, Nokia' s

market share peaked in 1Q03 at 52 .5% and dropped steadily throughout 2003, with a muc h

sharper 5 % drop in 1Q04, to settle at 40% .

1Q03 2Q03 3Q03 4Q04 1Q04Nokia Western Europ emarket share 52.5% 51 .2% 47.2% 45.4% 40.0%

85 . At the close of 1 Q04, the full consequences of Nokia's deteriorating produc t

portfolio could no longer be concealed . With the strongest increase in demand in history for the

cell phone industry, Nokia's overall market share fell an astounding 5% in a single quarter ,

including, as described above, another 5 .4% in Western Europe . Despite galloping demand ,

312498821

Nokia's mobile phone sales for 1Q04 dropped 15% year over year for a loss in phone sales o f

$880 million . The drop in phone operating profits was even more dramatic -- a 25% decline, o r

$300 million . Nokia ' s 1 Q04 overall operating profits declined 17 % during l Q04. As the cause s

of this negative performance were structural and were long in the making, the newly admitte d

inadequacies in Nokia's product portfolio continued to sharply depress its performance in late r

quarters .

Nokia's False Statements and Misleading Omission s

86. On October 16, 2003, Nokia issued a press release announcing that it had met it s

Third Quarter Sales and earnings per share (`BPS") targets . The release contained the following

statements that were attributed to its CEO, Jorma Ollila :

Following an announced commitment two years ago to strengthen our position inthe global CDMA handset market, I am very happy to say that we have nowdoubled our share to the mid-teens from the same quarter last year . We expect tosee continued momentum in CDMA going into the fourth quarter as we increaseshipments to China , India and all major U . S. CDMA operators .

Recent months have marked our entry into a number of new and exciting areas ofmobility . We have introduced several camera phones, begun shipments of gamesdevices and announced half a dozen phones for new growth markets .

The Nokia N-Gage has just gone on sale at 30 , 000 stores around the world to avery positive initial consumer response. Many outlets sold out of the deviceduring thefirst day of release . Following on f •om this, we are seeing strongorder intake from distributors and retailers.

87 . The statements attributed to Ollila about Nokia performance and "momentum" in

the CDMA market were materially false and/or misleading and omitted mate rial facts needed to

make the statements not misleading because the market shift from TDMA (where Nokia had a

75% share) to CDMA (where , in 2002 , Nokia held only a nominal share and , even in 2003, held

322498821

less than a 15% share) was harming Nokia's sales performance and market share . Moreover, by

2003, Nokia had developed only low end CDMA phones and was far behind its competitors i n

development of high quality and competitive mid-tier and high end CDMA phones because of its

refusal to license the Qualcomm chipset . Nokia's CDMA phone sales performance and

prospects were also being depressed by its refusal to customize its CDMA phones to operators '

specifications .

88 . The statements about new product releases, particularly regarding the N-Gage ,

were materially false and/or misleading and omitted material facts needed to make the statement s

not misleading because consumers' immediate response to N-Gage was highly negative an d

those sales that were made relied heavily on promotional discounts .

89. On October 16, 2003, Defendants Ollila and Olli-Pekka Kallasvuo, Nokia' s

Executive Vice President and General Manager of its Mobile Phones division, hosted a

conference call with the market analysts following Nokia's stock to discuss Nokia's third quarter

2003 ("3Q03") financial performance . During this call, Ollila described the benefits flowing t o

Nokia from its supposed strength in CDMA, and the success of Nokia's distribution strategy, it s

supposed competitive and "feature-rich" product offerings, and its ramp-up of several significant

new products, including the N-Gage and new camera phones :

Of the various technologies, GSM, CDMA, and PDC grew basically in line withoverall year-on-year market growth, while CDMA volumes continued to decline .Nokia's market positions strengthened in the Americas across all the technologies .We have achieved major market share gains in Latin America, where our marketshare currently exceeds the global 39% level . In the USA, we are the clear marketleader and we are well-positioned to make further gains during the holiday season .The strong momentum in CDMA continued, with our CDMA market shar e

doubling from a year ago to the mid-teens . Going into Q4, we see an opportunityfor a major increase in our CDMA volumes in India, China, and the U.S. We

33249882_9

have now achieved the number one position in the Chinese GSM market . Ourdistribution strategy is bearing fruit and Nokia brand is stronger than ever,supported by competitive product offering from low-end to localized feature-richdevices like the pen-based Nokia 6108 . . .

I expect Nokia volume growth in Q4 to exceed the overall market growth . Ouroffering is being strengthened by the ramp-up of several significant new products,such as the Nokia N-Gage, the new imaging phones Nokia 6600 , Nokia 3660,GSM wideband CDMA-based Nokia 7600 and the highly competitive entry-levelcamera phone, the Nokia 3200 series . I am looking forward to a quarter that isexpected to bring Nokia new volume and market share record .

90. In response to a question by analyst Mike Walkley, Ollila elaborated upon Nokia' s

success in CDMA :

Yeah, I think, if we look at the CDMA market, we really are pleased with a verysteady progress that we have made in CDMA now in the last three quarters . Soit's really a consistent good progress, having some of these key operators, Sprintand Verizon in the U.S., Unicorn in China, as well as Reliance in India, as ourcustomers, all of them in volume, shipping in volume as we speak . So we reallyare pleased with how that has worked out. The business model, the dynamics as itis in the CDMA has slightly lower ASPs as our average, has a slightly lowermargin, but it is good business, we are getting a good healthy margin . And wejust love to get that business and really make progress in that segment .

91 . In a question regarding demand for CDMA clamshells in North America an d

Asia, Ollila touted the broader product roadmap for enhanced CDMA phones :

First of all, we want to be present in all the key segments of the CDMA market .And we have introduced our first CDMA camera phone, our imaging product aswe would say, and that phone will be shipping initially in Latin America in Q4and is a good indication of how we will be moving . Then if we look at the phonefactors, we will be moving to a broader set of phone factors also with CDMA,including clamshells . . .

And if we look at the broader set of products and opportunities in CDMA, we areworking with number of multimedia segment products, which will hit the marketsin 2004 and 2005. So, the product's road map is a very exciting one . . .

342498821

Ollila also explained that Nokia's product mix was improving as a result of its new higher-end

offerings:

Yeah, so if you look at the high end, what's the proportion of that in the total, theshare of color in terms of value now accounts for about 50% of the total, and thatwe expect to grow significantly in Q4 . And if you look at the value of cameraphones, we expect that to be in the range of 20% of the total in Q4 . We are wellon our way to that as we speak, so we feel good about that, and that just showsthat the change towards the higher-end offerings is happening.

92. And finally, in response to a question on growth in Asia, and Nokia' s overal l

corporate ASP profile , Ollila emphasized the strength of Nokia's margins in its entry level ,

middle and high-end portfolio :

I think if you are looking at two markets like China and India, these are twomarkets where it is even more pronounced than in some others . That taking anaverage ASP of any other factor really distorts the picture because you have a verystrong high-end segment, but most of it obviously is low and middle, entry leveland middle range phones . So you really have to look at how the segments areperforming. We are getting a healthy margin and that's our main driver . Ahealthy margin from both of those markets and that's coming from both the high-end and middle range, as well as entry .

93. The above-referenced statements in the conference call about Nokia's CDM A

performance and the success of its distribution strategy were false and misleading, and omitte d

facts needed to make the statements not misleading because the market shift from TDMA (where

Nokia had a 75% share) to CDMA (where, in 2002, Nokia held only a nominal share, and, eve n

in 2003, held less than a 15% share) was harming Nokia's sales performance and market share .

By October 2003, Nokia had developed only low end CDMA phones and was far behind it s

competitors in the development of high quality and competitive mid-tier and high end CDMA

phones because of its refusal to license the Qualcomm chipset . In particular, sales to key Unite d

States CDMA operators, Sprint and Verizon, had only begun recently with Nokia's use of the

352498821

Texas Instrument chipset, and these sales continued to be depressed by Nokia's refusal to

customize its products to their specifications .

94. With respect to the purported strength of Nokia's mid- and high-end offerings,

and its product road map, including for clamshells, the statements were false and misleading, and

omitted facts needed to make the statements not misleading because :

a. By 3Q03, Nokia's product portfolio had sharply degraded and Nokia wa s

simply recirculating the same series 400 phone with different face plates, colors, and minor

cosmetic changes. There were major holes in Nokia's mid-tier and high-priced offerings,

including for high resolution color and camera phones, and those high-priced phones (such as the

N-Gage) that were released were ill-designed and were being rejected by consumers .

b. By 3Q03, products in Nokia's "road map," i .e., that were planned and in

development for release over the next several quarters, were also inadequate and noncompetitive

and lacked form designs such as clamshells that Nokia's customer surveys had indicated were in

high demand .

95 . On November 24, 2003 and continuing into November 25, 2003, Nokia hosted a

conference in Dallas, Texas which it termed its "Capital Markets Day" for market analysts

covering Nokia's stock. The event was well-attended by stock analysts from around the world,

many of whom published reports summarizing the representations made by Nokia's officers .

The following Nokia officers attended the event and gave presentations to analysts on Nokia's

behalf: Jorma Ollila (Chairman and CEO), Pertti Korhonen (Senior Vice President and CTO),

Rene Svendsen-Tune (SVP Marketing and Sales Networks), Olli-Pekka Kallasvuo (EVP and GM

Mobile Phones), Niklas Savander (SVP Terminals Business Unit Enterprise Solutions) and Anss i36

2498821

Vanjoki (EVP and GM Multimedia). A webcast of the first day's presentations at the conferenc e

was posted on Nokia's website .

96. In kicking off the conference, Ollila first reiterated Nokia's 4Q03 outlook o r

guidance, and cited to the significance of the positive growth in Nokia's sequential ASPs o f

Nokia's phones during the quarter as proof of "how our strategy is working," noting Nokia' s

"restructuring has really paid off. "

97. Ollila continued , stating that Nokia, "will continue to offer a unique global range

of highly competitive mobile phone products to a large consumer segment," and that Nokia will

assure, "that we get the lowest cost structure and that we get the fast product renewal to ensure

product competitiveness which has been our strength in the past . . . ." He then stated that, "we

have know-how where we can bring mobility to many of these areas, particularly the games ,

imaging, media products, and we have the concepts to make it happen . "

98 . In summing up his introduction to analysts for the first day of the Capital Marke t

Day event, Ollila emphasized that Nokia's supposedly strong product portfolio was the mos t

important reason for Nokia's competitiveness :

First of all, it's all about product. We are a product company. It's all aboutproduct range, the segmentation . The product cycles are being accelerated.That's the push for the market, how we can respond to that and the fact thatindustry is becoming highly competitive . We feel this area is number one amongthe competitive factors for us .

99. Ollila's statements about the significance to Nokia's business prospects of th e

4Q03 growth in Nokia's phone ASP's ; Nokia's product portfolio and "fast product renewal" ; and

Nokia's "know-how" in games, were false and misleading or omitted material facts because :

372498821

a. The growth in Nokia's ASP was attributable to the component shortage at

Nokia's competitors, and to other non-recurring factors, as described in 11169-80.

b. By November 24, 2003, Nokia's product portfolio had sharply degrade d

and Nokia was simply recirculating the same series 400 phone with different face plates, colors,

and minor cosmetic changes . There were major holes in Nokia's mid-tier and high-end offerings ,

including for high resolution color and camera phones .

c. By November 24, 2003, products in Nokia's "road map," i.e., that were

planned and in development for release over the next several quarters, were also inadequate an d

noncompetitive and lacked form designs such as clamshells that Nokia's customer surveys had

indicated were in high demand. Nokia's direction to its engineers to accelerate its "produc t

renewal" had also resulted in defective and inferior new products that were returned to Nokia i n

I Q04 .

d. By November 24, 2003, consumer response on the N-Gage product t o

Nokia marketing and sales personnel was already highly negative .

100. As the day continued, Kallasvuo made a presentation to analysts on Nokia' s

mobile phone business . He began his presentation by explaining the extreme importance o f

Nokia's cost leadership, and the folly of focusing on the different priced segments of Nokia' s

phone portfolio :

Cost leadership will continue to be of extreme importance and I think we reallyneed to continue to be cost leaders in all categories . So the thinking, okay, let'sleave the low end, if you will, aside and concentrate on mid-end, if there is -- mid-end, and the high-end and really escape to that direction . I don't think it is awinning strategy. . . and this low-end, mid-range, high-end thinking continues tobe overly simplistic .

382498821

101 . Kallasvuo's dissembling about the insignificance of the different priced segment s

of Nokia's phone business was false and/or misleading and omitted material facts becaus e

Kallasvuo concealed that, in fact, Nokia had significant holes in its mid-range and high-range

phone portfolio, as well as in its roadmap for these higher-priced phones ; and that thes e

deficiencies had affected and would in the future severely and adversely affect Nokia' s sales

performance , operating profits, market share and phone ASPs .

102 . Kallasvuo then made a presentation on Nokia's CDMA performance, explainin g

Nokia's past development problems and assuring market analysts that these problems had bee n

solved with competitive higher end CDMA phones currently in development :

Now, before moving to the cost leadership I want to tackle CDMA briefly . Notother segments of this business . I will simply make some comments on theCDMA that -- there are many questions here . I'm sure there will be more duringthe course of today and that obviously especially when you are in the U .S.CDMA attracts a lot of attention . So obviously we've got -- we've made somevery good progress in CDMA this year and we are making that progress right nowas we speak. We have doubled our market share and we really can in a veryrealistic way target even higher market shares here . So why is this happeningnow? I think it's very simple . For a long time I think we were under-investing inCDMA when it comes to R&D . We basically did not necessarily completelyunderstand the complexity there is in CDMA market . And really didn't seem toget there how hard we always tried . In the summer of 2000 we made importantdecisions to increase our investments in CDMA, really made a commitmentsaying that now we simply need to pay more by investing more to get thesustainable process and really catch the other players in the industry . And I thinkthis -- what we are seeing now is simply a consequence of that decision. Moneybeing spent, invested -- of course there again that's expense while doing so, andwe are seeing the results .

I think we are now in a situation where we really are competitive when it comes toCDMA engine. And the engine really it's well performed . And now really it'stime for us to make the expansion based on that engine to other -- to morecategories of the market, cover more segments, more high-end if you will . Thepossibility to that is right there and we are doing it right now . And then of coursealso drive CDMA to conversions and push, for instance, Symbian to CDMA . And

392498821

the beauty here is that when doing so the commonality between differentstandards, between CDMA markets and GSM markets will increase . When youmove to the higher layers of software and application platforms, you really canbenefit more from the commonality there between CDMA and GSM. And I thinkthat will increase our competitive position here .

103. Later, in responding to an analyst question that suggested that Nokia should buy a