IMPACT OF E-COMMERCE ON CHANGING CONSUMER...

24

International Journal of Interdisciplinary Research Centre (IJIRC) ISSN: 2455-2275(E) Volume II, Issue 3 March 2016 All rights are reserved 4 IMPACT OF E-COMMERCE ON CHANGING CONSUMER BEHAVIOUR AND PERCEPTION: STUDY OF BANKING SECTOR JAIPUR * Dr. Mamta Jain and * * Mr. Abhineet Saxena and *** Mr. Suresh Kumar Yadav * Associate Professor, Department of Economic Administration and Financial Management, University of Rajasthan Jaipur, Rajasthan, INDIA ** Research Scholar, Department of Economic Administration and Financial Management University of Rajasthan Jaipur, Rajasthan, INDIA *** Research Scholar, Department of Economic Administration and Financial Management University of Rajasthan Jaipur, Rajasthan, INDIA Abstract E-commerce stands for electronic commerce and pertains to trading in goods and services through the electronic medium. As an icon of globalization, e-business has changed and is still changing the way business is conducted around the world. Online business activity i.e. business through internet is called e-commerce. Internet is one component which has recently become the key ingredient of quick and rapid lifestyle. India is showing tremendous growth in the E-commerce. The future does look very bright for e-commerce in Indian banking industry. The research focus on the Internet shopping and online consumer behaviour. Consumer behaviour in retailing and banking refers to the buying behaviour of the ultimate shopper or end consumer. It is all about understanding how people prefer to spend their money and time in buying and consuming various goods and service they desire. The main objective of the paper is to describe the present status of E-Commerce and involvement of banking industry and to obtain quantitative describing the actuality of internet shopping in the case of the India in order to explain the development of internet shopping and its impact on consumer behaviour. The study is based on primary as well as secondary data collected from the IAMAI (Internet and mobile association of India) and RBI reports and a well-structured questionnaire. From the literature review the variables or major areas have been identified to find out the impact of e-commerce on consumer behaviour. This paper support the research questions that E-Commerce has the positive impact on the service management and consumer behaviour. The use of E-Commerce works effectively for the service quality of the banking sector in terms of security, access, communication, reliability, responsiveness and perceived customer services.

Transcript of IMPACT OF E-COMMERCE ON CHANGING CONSUMER...

International Journal of Interdisciplinary Research Centre (IJIRC) ISSN: 2455-2275(E)

Volume II, Issue 3 March 2016

All rights are reserved 4

IMPACT OF E-COMMERCE ON CHANGING CONSUMER

BEHAVIOUR AND PERCEPTION: STUDY OF BANKING SECTOR

JAIPUR

*

Dr. Mamta Jain and * * Mr. Abhineet Saxena and

***Mr. Suresh Kumar Yadav

* Associate Professor, Department of Economic Administration and Financial Management,

University of Rajasthan Jaipur, Rajasthan, INDIA

** Research Scholar, Department of Economic Administration and Financial Management

University of Rajasthan Jaipur, Rajasthan, INDIA

*** Research Scholar, Department of Economic Administration and Financial Management

University of Rajasthan Jaipur, Rajasthan, INDIA

Abstract

E-commerce stands for electronic commerce and pertains to trading in goods and services

through the electronic medium. As an icon of globalization, e-business has changed and is

still changing the way business is conducted around the world. Online business activity i.e.

business through internet is called e-commerce. Internet is one component which has recently

become the key ingredient of quick and rapid lifestyle. India is showing tremendous growth

in the E-commerce. The future does look very bright for e-commerce in Indian banking

industry. The research focus on the Internet shopping and online consumer behaviour.

Consumer behaviour in retailing and banking refers to the buying behaviour of the ultimate

shopper or end consumer. It is all about understanding how people prefer to spend their

money and time in buying and consuming various goods and service they desire.

The main objective of the paper is to describe the present status of E-Commerce and

involvement of banking industry and to obtain quantitative describing the actuality of internet

shopping in the case of the India in order to explain the development of internet shopping and

its impact on consumer behaviour. The study is based on primary as well as secondary data

collected from the IAMAI (Internet and mobile association of India) and RBI reports and

a well-structured questionnaire. From the literature review the variables or major areas have

been identified to find out the impact of e-commerce on consumer behaviour.

This paper support the research questions that E-Commerce has the positive impact on the

service management and consumer behaviour. The use of E-Commerce works effectively for

the service quality of the banking sector in terms of security, access, communication,

reliability, responsiveness and perceived customer services.

International Journal of Interdisciplinary Research Centre (IJIRC) ISSN: 2455-2275(E)

Volume II, Issue 3 March 2016

All rights are reserved 5

Keywords: E-commerce, internet shopping, World Wide Web, consumer behaviour, privacy

and security, consumer trust.

Introduction

E-commerce has become an integral part of the modern life style. As a symbol of

globalization, e-business represents the cutting edge of success in this digital age and it has

changed and is still changing the way business is conducted around the world. The

commercialization of the Internet has driven electronic commerce to become one of the most

capable channels for inter-organizational business processes.

As an icon of globalization and advancement of information technology, it represents the

cutting edge of success in this digital world. In other words the cutting edge for business

today is e-commerce. E-Commerce stands for electronic commerce. It means dealing in

goods and services through the electronic media and internet. On the internet, it relates to a

website of the vendor, who sells products or services directly to the customer from the portal

using a digital shopping cart or digital shopping basket system and allows payment through

credit card, debit card or EFT (Electronic fund transfer) payments. E-commerce or E-business

involves carrying on a business with the help of the internet and by using the information

technology like Electronic Data Interchange (EDI). More simply put, E-Commerce is the

movement of business onto the World Wide Web. E-Commerce has almost overnight become

the dominant online activity.

Internet is one component which has recently become the key ingredient of quick and rapid

lifestyle. Be it for communication or explorations, connecting with people or for official

purposes, „internet‟ has become the central-hub for all. Resultantly, Internet growth has led to

a host of new developments, such as decreased margins for companies as consumers turn

more and more to the internet to buy goods and demand the best prices, as observed by C.K

Prahalad, Professor, Business School, and University of Michigan. The internet means that

traditional businesses will change because „‟incumbents (in markets) and large firms do not

have the advantage „‟ just by virtue of being there first or by being of big, he said. The

implication of perfectly competitive market as the world will observe is that market will

produce an efficient allocation of resources. Internet has truly been an effective agent in

changing the fundamental ways of doing business.

International Journal of Interdisciplinary Research Centre (IJIRC) ISSN: 2455-2275(E)

Volume II, Issue 3 March 2016

All rights are reserved 6

There is no single definition of E-Commerce, it means only commercial activity

which is performed or linked to or supported by Electronic Communication. The effects of e-

commerce are already appearing in all areas of business, from customer service to new

product design. It facilitates new types of information based business processes for reaching

and interacting with customers like online advertising and marketing, online order taking and

online customer service.

Facilitators of e-commerce in India

A. Information directories: The products and services a relisted with appropriate sub-

headings to make it easy for a serious information-seeker to find what he wants. Allied

services provided by them: Message boards, chat rooms, forums, etc.

B. Banks:

1) Net banking/phone banking: This is an online banking facility available for savings

account holders as well as current account holders. Some of the special Net banking services

are: Demat accounts for sale/purchase of stocks and shares, Foreign Exchange services,

Direct/Instant payment of bills on the account-holder‟s behalf, Financial Planning.

2) Credit/Debit Cards- Banks facilitate E-commerce by providing the most vital trade

instrument, namely the Credit or Debit Card, without which E-commerce would be

impossible.

Current Stage of Electronic Banking

Current stage is of IT advancement because technology continues to make a dramatic and

profound impact in service industry and radically shapes how services are delivered (Bitner et

al., 2000). The world has become a global village where it has brought a revolution in the

banking industry. The banks appear to be on fast track for IT based products and services.

Deregulation and Liberalization in the financial sector have stimulated financial innovations.

Breath taking developments in the technology of telecommunications and electronic data

processing have further accelerated these changes. Technology has become the fuel for rapid

change. IT is no longer considered as mere transaction processing or confined to management

information system. In its wider definition, it implies the integration of information system

with communication technology and of innovative applications to product manufacturing,

design and control.

Information technology developments in the banking sector have sped up communication and

transactions for clients (Booz et al, 1997). The new technology has radically altered the

International Journal of Interdisciplinary Research Centre (IJIRC) ISSN: 2455-2275(E)

Volume II, Issue 3 March 2016

All rights are reserved 7

traditional ways of doing banking business. Increasingly, the customers in retail sector are

doing business with their banks from the comfortable confines of their homes or offices.

Customers can view the accounts, get account statements, transfer funds, purchase drafts by

just making a few key punches. Availability of ATMs and plastic cards to large extent avoid

customers going to branch premises. EDI is another development that has made its impact

felt in the banking industry. In fact in banking industry, IT is finding its use in five key areas.

- Convenience in product delivery access

- Managing productivity access,

- Product design,

- Adapting to market and customer needs and,

- Access to customer market.

IT is also helping in cutting costs by providing cheaper ways of delivering products to

customers. Banks are moving into the primary services of helping their customers buy things

like automobiles, real estates, in all these areas, IT has been enormous help. The younger age

group customers are much more amenable to using electronic delivery channels rather than

visiting physical branches. Banks have been cautious in launching new services using IT.

Today there is demand for a business which is flexible enough to respond to any fluctuations

in the running of the business. What differentiates an on demand business from its

competition is the fact that it is responsive in real time as the events occur. This is possible

only because all its business processes are thoroughly integrated, and the IT infrastructure

exists in an on demand operating environment.

The rapid growth of e-commerce in India is being driven by greater customer choice

and improved convenience. Having a strong business model coupled with a first class level

of service is critical to success. Before these aspects are explored, it is important to

understand the unique attributes which define e-commerce in India.

Khan and Mahapatra (2009) remarked that technology plays a vital role in improving the

quality of services provided by the business units. One of the technologies which really

brought information revolution in the society is Internet Technology and is rightly regarded

as the third wave of revolution after agricultural and industrial revolution. The cutting edge

for business today is e-Commerce. The effects of e-commerce are already appearing in all

areas of business, from customer service to new product design.

International Journal of Interdisciplinary Research Centre (IJIRC) ISSN: 2455-2275(E)

Volume II, Issue 3 March 2016

All rights are reserved 8

Thompson (2005) introduced that the growth of Internet technology has enormous potential

as it reduces the costs of product and service delivery and extends geographical boundaries in

bringing buyers and sellers together. In simple words, Electronic commerce involves buying

and selling of goods and services over the World Wide Web. Customers can purchase

anything right from a car or a cake sitting comfortably in his room and gift it to someone

sitting miles apart just by click of a mouse. In present environment, technological

development in the field of telecommunication and computer technologies has made

computer networks an integral part of our economic infrastructure. It provides multiple

benefits to consumers and facilitates goods at lesser cost, more choices and saves time.

Consumers can buy goods sitting at their homes or offices. Similarly online services such as

ticketing for all kind of travel, banking, bill payment, hotel bookings etc. have been of

tremendous benefits for consumers. As per industry experts, this industry will increase

exponentially in times to come.

Banks play an important role in the development of a E-commerce, as reservoirs of resources

necessary for the economic development. Thus the importance of commercial banks in the

process of E-commerce development has been pointed out regularly by economic thinkers

and policy makers of the country.

Evolution of e-commerce in India

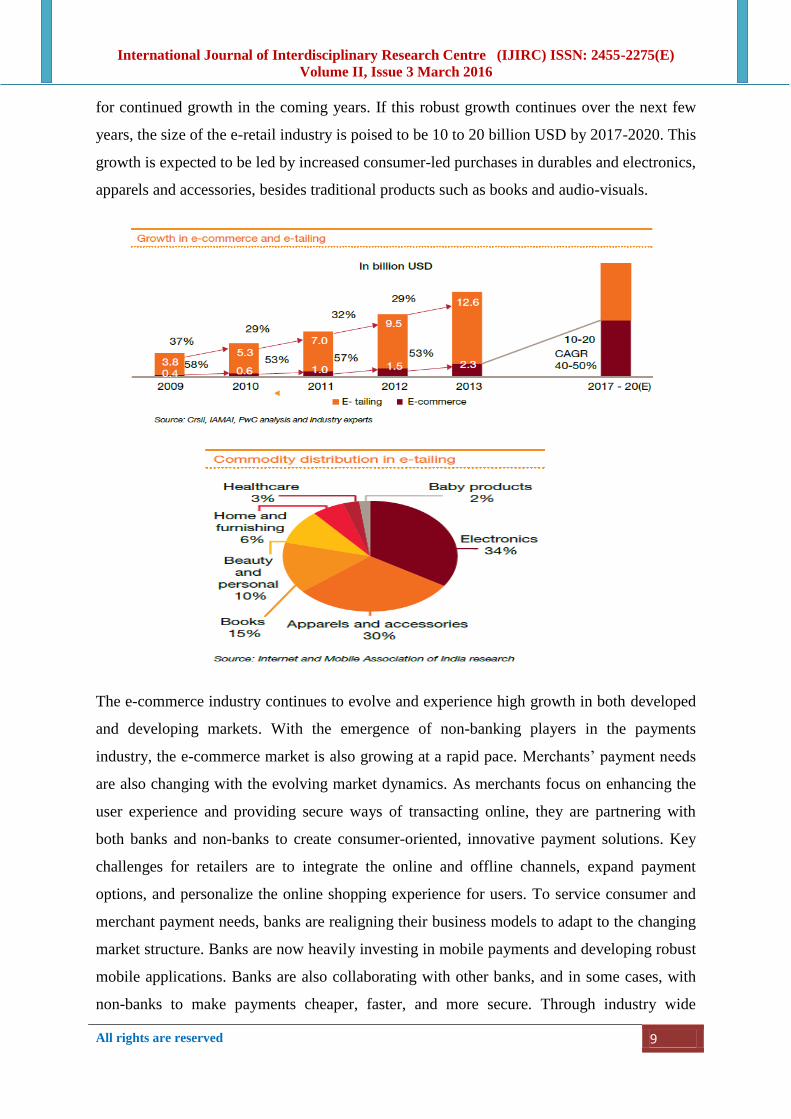

The rapid growth of e-commerce in India:

Today e-commerce is a byword in Indian society and it has become an integral part of our

daily life. There are websites providing any number of goods and services. Then there are

those, which provide a specific product along with its allied services. Over the last two

decades, rising internet and mobile phone penetration has changed the way we communicate

and do business. E-commerce is relatively a novel concept. It is, at present, heavily leaning

on the internet and mobile phone revolution to fundamentally alter the way businesses reach

their customers. While in countries such as the US and China, e-commerce has taken

significant strides to achieve sales of over 150 billion USD in revenue, the industry in India

is, still at its infancy. However over the past few years, the sector has grown by almost 35%

CAGR from 3.8 billion USD in 2009 to an estimated 12.6 billion USD in 20131. Industry

studies by IAMA. However, e-retail in both its forms; online retail and market place, has

become the fastest-growing segment, increasing its share from 10% in 2009 to an estimated

18% in 2013. Calculations based on industry benchmarks estimate that the number of parcel

check-outs in e-commerce portals exceeded 100 million in 2013. However, this share

represents a miniscule proportion (less than 1%) of India‟s total retail market, but is poised

International Journal of Interdisciplinary Research Centre (IJIRC) ISSN: 2455-2275(E)

Volume II, Issue 3 March 2016

All rights are reserved 9

for continued growth in the coming years. If this robust growth continues over the next few

years, the size of the e-retail industry is poised to be 10 to 20 billion USD by 2017-2020. This

growth is expected to be led by increased consumer-led purchases in durables and electronics,

apparels and accessories, besides traditional products such as books and audio-visuals.

The e-commerce industry continues to evolve and experience high growth in both developed

and developing markets. With the emergence of non-banking players in the payments

industry, the e-commerce market is also growing at a rapid pace. Merchants‟ payment needs

are also changing with the evolving market dynamics. As merchants focus on enhancing the

user experience and providing secure ways of transacting online, they are partnering with

both banks and non-banks to create consumer-oriented, innovative payment solutions. Key

challenges for retailers are to integrate the online and offline channels, expand payment

options, and personalize the online shopping experience for users. To service consumer and

merchant payment needs, banks are realigning their business models to adapt to the changing

market structure. Banks are now heavily investing in mobile payments and developing robust

mobile applications. Banks are also collaborating with other banks, and in some cases, with

non-banks to make payments cheaper, faster, and more secure. Through industry wide

International Journal of Interdisciplinary Research Centre (IJIRC) ISSN: 2455-2275(E)

Volume II, Issue 3 March 2016

All rights are reserved 10

initiatives, banks are looking to take advantage of their huge payment network and

infrastructure. Banks are also partnering or acquiring non-bank players in retail payments.

The bottom line is that, though late, banks are now changing the way they conduct their retail

payment business.

State of Online Retail Payments

Over the past decade, the retail payment market has changed structurally and continued to

focus on innovation. Entry of non-banks and availability of cheap, fast, and reliable

technology have changed the focus of payment industry to providing innovative, secure, and

fast payment methods. However, only a few innovations have been game changing so far. It

has also been observed that most innovations are first developed for domestic/niche markets

and then, if successful, applied to other regions. Financial inclusion is driving innovation in

retail payments in developing countries with huge unbanked populations. In a retail payment

system, four parties are involved: the customer, the customer‟s payment service provider, the

merchant, and the merchant‟s payment service provider. Over time, technological

advancements have led to the subsequent addition of new access channels and devices. The

latest additions in the new payment scheme are mobile access channels and mobile devices.

More and more non-bank players are entering the e-payments market, making it more

competitive. But banks still are the most significant players in the payments market.

Innovation in retail payments has attracted more consumers to online shopping, and with the

entry of new players, transaction costs are going down. The use of innovative and new

payment instruments is much lower than traditional payment instruments, but is increasing

rapidly.

Payment process in retail payment:

International Journal of Interdisciplinary Research Centre (IJIRC) ISSN: 2455-2275(E)

Volume II, Issue 3 March 2016

All rights are reserved 11

Chief characteristics of the E-commerce market which impact the consumer behaviour

For developing countries like India, e-commerce offers considerable opportunity. E-

commerce in India is still in nascent stage, but even the most-pessimistic projections indicate

a boom. It is believed that low cost of personal computers, a growing installed base for

Internet use, and an increasingly competitive Internet Service Provider (ISP) market will help

fuel e-commerce growth in Asia‟s second most populous nation.

• ‘Cash-on-delivery’: India has been a vibrant cash economy where the consumer‟s

purchasing behaviour involves an initial overall inspection of the product from different

perspectives and paying subsequently. Further, customers in India do not extend much trust

on the transit facilities for the delivery of the products. This has resulted in „cash-on -

delivery‟ (COD) as a preferred payment option of majority of the Indian consumers buying

online.

• Consumers in India expect the return process to be seamless and convenient. However,

with an expectation of return of the items purchased online, online shoppers have made

available the option to return the purchased goods at the behest of the retailer. Retailers have

considered this option of return to develop trust and confidence which results in seamless

subsequent purchases and positive word-of mouth support.

• Free and quick home delivery is another characteristic of the e-commerce industry in

India. E-retailers offer free delivery of the products within a promised timeline. Though this

may be unsustainable in the long run but e-retailers have to offer the same convenience of

free and quick shipping to compete with other retailers.

Flipkart (inventory-led model)

International Journal of Interdisciplinary Research Centre (IJIRC) ISSN: 2455-2275(E)

Volume II, Issue 3 March 2016

All rights are reserved 12

Flipkart has started as a price comparison online portal with an initial investment of 8,000

USD and later turned into an e-retailing giant which recently ticked the 1 billion USD in

gross merchandise volume. It started with a consignment model where goods were procured

on demand and turned into inventory e-retailer supported by registered suppliers since it

provided better control on the logistics chain. Flipkart established warehouses in Delhi,

Bangalore, Mumbai and Kolkata managing a fine balance between inventory and cost of

delivering goods. Facing difficulties from the 3PLs in the form of higher delivery cost, late

deliveries and faulty products delivered resulting in return and customer dissatisfaction, it has

started its own logistics arm named e-Kart. E-Kart provides a robust back-end support to

Flipkart and ensures timely deliveries. To achieve the economies of scale, recently e-Kart

started providing back-end support to other e-retailers. It has consolidated the market and

added strengths by acquiring We Read, Mime360, Chakpak.com, Letsbuy. com and Myntra

along the way. The company employs around 13,000 employees and plans to add 10,000 to

12,000 more in next one to three years after a recent acquisition of Myntra.

Amazon India (marketplace model)

Amazon started practicing the market place model by launching its site in early 2013 in India.

It started registering electronics goods sellers and ended FY 2013 offering nearly 15 million

products. Amazon India has two fulfilment centers in Mumbai and Bangalore and plans to

start five new fulfilment centres across the country. Known for its strong last-mile delivery

network, Amazon India has set up a logistics arm named Amazon Logistics and started

offering same day delivery.

Delivery of goods to consumer by couriers and postal services is not very reliable in smaller

cities, towns and rural areas. However, many Indian Banks have put the Internet banking

facilities. The speed post and courier system has also improved tremendously in recent years.

Modern computer technology like secured socket layer (SSL) helps to protect against

payment fraud, and to share information with suppliers and business partners. With further

improvement in payment and delivery system it is expected that India will soon become a

major player in the e-commerce market.

Recent Trends in Indian Banking Sector related with E-services:

Today, we are having a fairly well developed banking system with different classes of banks

– public sector banks, foreign banks, private sector banks, regional rural banks and co-

International Journal of Interdisciplinary Research Centre (IJIRC) ISSN: 2455-2275(E)

Volume II, Issue 3 March 2016

All rights are reserved 13

operative banks. The Reserve Bank of India (RBI) is at the paramount of all the banks. The

RBI‟s most important goal is to maintain monetary stability (moderate and stable inflation) in

India. The RBI uses monetary policy to maintain price stability and an adequate flow of

credit. The rates used by RBI to achieve this are the bank rate, repo rate, reverse repo rate and

the cash reserve ratio. Reducing inflation has been one of the most important goals for some

time. Growth and diversification in banking sector has transcended limits all over the world.

In 1991, the Government opened the doors for foreign banks to start their operations in India

and provide their wide range of facilities, thereby providing a strong competition to the

domestic banks, and helping the customers in availing the best of the services. The Reserve

Bank in its bid to move towards the best international banking practices will further sharpen

the prudential norms and strengthen its supervisor mechanism. There has been considerable

innovation and diversification in the business of major commercial banks. Some of them have

engaged in the areas of consumer credit, credit cards, merchant banking, internet and phone

banking, leasing, mutual funds etc. A few banks have already set up subsidiaries for merchant

banking, leasing and mutual funds and many more are in the process of doing so.

Some banks have commenced factoring business.

Role of Information Technology (IT) and Customer Behaviour in Banking:-

IT plays an important role in the banking sector as it would not only ensure smooth passage

of interrelated transactions over the electric medium but will also facilitate complex financial

product innovation and product development. The application of IT and e-banking is

becoming the order of the day with the banking system heading towards virtual banking.

Following are the innovative services offered by the industry in the recent past:

Electronic Payment Services –

E Cheques

Nowadays we are hearing about e-governance, e-mail, e-commerce, e-tail etc. In the same

manner, a new technology is being developed in US for introduction of e-cheque, which will

eventually replace the conventional paper cheque. India, as harbinger to the introduction of e-

cheque, the Negotiable Instruments Act has already been amended to include; Truncated

cheque and E-cheque instruments.

Real Time Gross Settlement (RTGS)

International Journal of Interdisciplinary Research Centre (IJIRC) ISSN: 2455-2275(E)

Volume II, Issue 3 March 2016

All rights are reserved 14

Real Time Gross Settlement system, introduced in India since March 2004, is a system

through which electronics instructions can be given by banks to transfer funds from their

account to the account of another bank. The RTGS system is maintained and operated by the

RBI and provides a means of efficient and faster funds transfer among banks facilitating their

financial operations. As the name suggests, funds transfer between banks takes place on a

„Real Time' basis. Therefore, money can reach the beneficiary instantaneously and the

beneficiary‟s bank has the responsibility to credit the beneficiary's account within two hours.

Electronic Funds Transfer (EFT)

Electronic Funds Transfer (EFT) is a system whereby anyone who wants to make payment to

another person/company etc. can approach his bank and make cash payment or give

instructions/authorization to transfer funds directly from his own account to the bank account

of the receiver/beneficiary. Complete details such as the receiver's name, bank account

number, account type (savings or current account), bank name, city, branch name etc. should

be furnished to the bank at the time of requesting for such transfers so that the amount

reaches the beneficiaries' account correctly and faster. RBI is the service provider of EFT.

Electronic Clearing Service (ECS)

Electronic Clearing Service is a retail payment system that can be used to make bulk

payments/receipts of a similar nature especially where each individual payment is of a

repetitive nature and of relatively smaller amount. This facility is meant for companies and

government departments to make/receive large volumes of payments rather than for funds

transfers by individuals.

Automatic Teller Machine (ATM)

Automatic Teller Machine is the most popular devise in India, which enables the customers

to withdraw their money 24 hours a day 7 days a week. It is a device that allows customer

who has an ATM card to perform routine banking transactions without interacting with a

human teller. In addition to cash withdrawal, ATMs can be used for payment of utility bills,

funds transfer between accounts, deposit of cheques and cash into accounts, balance enquiry

etc.

Point of Sale Terminal

International Journal of Interdisciplinary Research Centre (IJIRC) ISSN: 2455-2275(E)

Volume II, Issue 3 March 2016

All rights are reserved 15

Point of Sale Terminal is a computer terminal that is linked online to the computerized

customer information files in a bank and magnetically encoded plastic transaction card that

identifies the customer to the computer. During a transaction, the customer's account is

debited and the retailer's account is credited by the computer for the amount of purchase.

Tele Banking

Tele Banking facilitates the customer to do entire non-cash related banking on telephone.

Under this devise Automatic Voice Recorder is used for simpler queries and transactions.

For complicated queries and transactions, manned phone terminals are used.

Electronic Data Interchange (EDI)

Electronic Data Interchange is the electronic exchange of business documents like purchase

order, invoices, shipping notices, receiving advices etc. in a standard, computer processed,

universally accepted format between trading partners. EDI can also be used to transmit

financial information and payments in electronic form.

Changing Consumer Behaviour and preferences

Consumer behaviour in retailing and banking refers to the buying behaviour of the ultimate

shopper or end consumer. It is all about understanding how people prefer to spend their

money and time in buying and consuming various goods and service they desire. In the

context of retail sector, retailers would specifically be more interested in understanding the

shopper‟s shopping behaviour. This involves an understanding of the decision variables

regarding what, when and from where to shop (shopping product, timing and choice of

retail store and format etc.). These decision variables could be demographic, psychographic

or behavioural, related to the shopping environment or to the lifestyle of the shopper. A

retailer needs to analyse and understand these decision variables to know the factors that

influence the purchase decision of a shopper. He needs to understand the factors that develop

a positive perception about a retailer in the shoppers‟ mind and then create a self-regulatory

positive reinforcement towards that retailer or the retail store.

International Journal of Interdisciplinary Research Centre (IJIRC) ISSN: 2455-2275(E)

Volume II, Issue 3 March 2016

All rights are reserved 16

Objectives of the Study

The objectives of present study are:

1. To describe the present status of E-Commerce and involvement of banking industry.

2. To analyse the present trends and future trends of E-Commerce in India.

3. To check the barriers of E-Commerce in India.

4. To study the challenges faced by E-Business players in India.

HYPOTHESES OF THE STUDY

H1:- The growth of e-commerce industry is directly related with growth of the online banking

facilities.

H2:- There is a positive Impact of E-Commerce on Changing Consumer Behaviour and

Perception towards banking services.

RESEARCH METHODOLOGY

The study is based on primary as well as secondary data collected from the IAMAI (Internet

and mobile association of India) and RBI reports and a well-structured questionnaire. From

the literature review the variables or major areas have been identified to find out the impact

of e-commerce on consumer behaviour.

Sample Size / Data Collection Methods (Instruments)

In order to understand the studied case more deeply, several sources of data collection were

used. Data was obtained through a survey within a sample of 500 banking consumer.

Information was gathered through questionnaire on consumer‟s perceptions of their banks.

Reposes were presented with 5-point Likert scales, where 1 = "strongly disagree," 3 =

"neither disagree nor agree," and 5 = “strongly agree."

From these data their perceptions regarding E-banking have been explored. Budgetary

constraints forced the elimination of follow-up procedures.

ANALYSIS AND INTERPRETATION OF QUESTIONNAIRE

Demographic analysis:

Population parameters normally influence various decision making process. This section

deals with the demographic factors like Gender, Age, Marital status, Income level of the

respondents, Profession of the respondents, their Educational qualification, Type of Bank

with which they hold their account. The information thus collected from the sample

respondents are analysed using SPSS software.

International Journal of Interdisciplinary Research Centre (IJIRC) ISSN: 2455-2275(E)

Volume II, Issue 3 March 2016

All rights are reserved 17

Gender:

For the purpose of the study, Gender is considered to know how many Male/Female

respondents are there in the total sample which is shown in Table

Gender

Percentage distribution of

Male/Female respondents

Frequency Percent Valid Percent Cumulative

Percent

Valid

Male 435 87.0 87.0 87.0

Female 65 13.0 13.0 100.0

Total 500 100.0 100.0

Figure 1

From above Table it is evident that around 87 % of the respondents are male and only 13% of

them are female. This implies that in the sample, dominant number is male compared to

female members using/accessing to banking services. So it can be conclude that mostly bank

accounts are operated by male respondent being a head of the family.

Age:

Age is another important demographic factor that influences the banking operations. For the

purpose of the present study age of the respondents is classified into five categories. The

same is shown in the following table

Table Age of the Respondents

International Journal of Interdisciplinary Research Centre (IJIRC) ISSN: 2455-2275(E)

Volume II, Issue 3 March 2016

All rights are reserved 18

Age Group

Frequency Percent Valid Percent Cumulative

Percent

Valid

Below 25 years 74 14.8 14.8 14.8

25 to 35 years 128 25.6 25.6 40.4

35 to 50 years 105 21.0 21.0 61.4

50 to 60 years 105 21.0 21.0 82.4

60 and above 88 17.6 17.6 100.0

Total 500 100.0 100.0

Figure 2

1. Marital Status: The marital status will indicate that the accessibility of banking

services to them may be in the form of joint accounts, fixed deposits in the name of

their kids etc with the banks. The same is presented in the following table

Marital Status

Frequenc

y

Percent Valid

Percent

Cumulative

Percent

Valid

Married 297 59.4 59.4 59.4

Unmarried 161 32.2 32.2 91.6

Widow /

Widower 8 1.6 1.6 93.2

Divorced 34 6.8 6.8 100.0

Total 500 100.0 100.0

Majority of the respondents are married. Approximately 60% of the respondents are

International Journal of Interdisciplinary Research Centre (IJIRC) ISSN: 2455-2275(E)

Volume II, Issue 3 March 2016

All rights are reserved 19

Married and only 32.2% are Unmarried. This is because of the fact that most of the

respondents are in the age group of 25 and above years. The samples represent the urban and

rural environment both.

Figure 3

Educational Qualification:

In general accessibility to banking operations are more to the educationally better qualified

compared to less educated people. In the recent past, banking operations are must for

educated and employed people and there is compulsion for the newly joined employees.

Thus, the details of the educational qualifications of the respondent are gathered by the

researcher and tabulated as shown in the table.

Educational Qualification

Frequenc

y

Percent Valid

Percent

Cumulative

Percent

Valid

Under Graduate 70 14.0 14.0 14.0

Graduate 116 23.2 23.2 37.2

Post Graduate/

Professional Degree 130 26.0 26.0 63.2

school education 153 30.6 30.6 93.8

Illiterate 31 6.2 6.2 100.0

Total 500 100.0 100.0

International Journal of Interdisciplinary Research Centre (IJIRC) ISSN: 2455-2275(E)

Volume II, Issue 3 March 2016

All rights are reserved 20

Figure 4

From table it is evident that most of the respondents are educated till school level. Nearly

26.0% of the respondents are post graduates, 23.2% of them are graduates and only 6.2% of

the respondents are Illiterate. This infers that majority of the bank account holders are highly

educated. Although education in general does not have any influence on the banking

operations but still education has a role in it. The above data clearly indicates that education

has strong influence on the banking operations and services. In addition to that, emerging

technologies are also influencing the people to operate banking activities.

Profession / occupation:

The profession of an individual demand the nature and type of banking operations required as

each profession may need different banking operations. Based on the availability of time to

attend their banking operations personally, they may demand other means like ATMs,

Debit/Credit cards, Internet banking, etc., from the banks to perform their transactions. Thus

the need for knowing the profession of the respondents have aroused for the researcher.

These data are tabulated in Table

Occupation

Frequenc

y

Percent Valid

Percent

Cumulative

Percent

Valid

Professional 88 17.6 17.6 17.6

Business 200 40.0 40.0 57.6

House Wife 48 9.6 9.6 67.2

Retired from

job 68 13.6 13.6 80.8

Student 41 8.2 8.2 89.0

Any other 55 11.0 11.0 100.0

Total 500 100.0 100.0

International Journal of Interdisciplinary Research Centre (IJIRC) ISSN: 2455-2275(E)

Volume II, Issue 3 March 2016

All rights are reserved 21

Figure 5

Among total of 500 respondents, nearly 40% of the respondents are Businessman followed by

Professionals with around 17.6%. The professionals include charted accountants, engineers,

MBAs, doctors, scientists etc. Remaining are students, Retired peoples women‟s and others.

Thus it is evident from the data that most of the respondents are busy with their profession

and hardly has time to attend to their banking activities personally. Thus their dependency on

the advanced services offered by the banking sector is very high.

Income level of the respondents:

Higher the income higher the expectations from banking services of an individual. Basically

people who earn more income will naturally have frequent usage of banking operations. It is

natural that availability of funds will lead to allocation of funds to various types of needs

expenses. This study focuses on how far the income of the respondents reflects the above

stated situation. With the help of the data collected from the field this factor is studied. The

same is shown in the following table

Family Income per annum

Frequenc

y

Percent Valid Percent Cumulative

Percent

Valid

Below 2 lakh 105 21.0 21.0 21.0

2 to 3 lakh 149 29.8 29.8 50.8

3 to 4 lakh 92 18.4 18.4 69.2

4 to 5 lakh 58 11.6 11.6 80.8

5 to 6 lakh 42 8.4 8.4 89.2

Above 6 lakh 54 10.8 10.8 100.0

Total 500 100.0 100.0

International Journal of Interdisciplinary Research Centre (IJIRC) ISSN: 2455-2275(E)

Volume II, Issue 3 March 2016

All rights are reserved 22

Figure 6

The income level of the respondents is classified into Six groups. Most of the respondents are

in the income group of 2 to 3lakhs representing 29.8%. Only 21.0% of the respondents have

less than 2 lakh as their annual family income. Around 30% of them are in the income level

of 3-5lakhs. 8.4% of the respondents are in the income level of 5 to 6 lakh. Very few of them

i.e., just 10.8% of them are in the above 6 lakh income level group. It is inferred that majority

of them are in the middle income group.

Consumer response towards exiting E-banking services-

Descriptive Statistics

N Range Mean Std. Deviation Variance

Internet banking services 500 4 3.63 1.443 2.082

Mobile banking services 500 4 2.57 1.318 1.737

Phone Banking services 500 4 2.72 1.492 2.225

ATM facility 500 4 3.56 1.262 1.593

Credit card Facility 500 4 3.01 1.326 1.757

Debit card facility 500 4 3.03 1.315 1.729

Electronic fund transfer 500 4 3.33 1.152 1.326

Bill Payment service 500 4 3.02 1.369 1.873

Inter-Connectivity of

ATM‟s 500 4 3.23 1.363 1.857

Information of new

products and services 500 4 3.60 1.482 2.196

CRM 500 4 3.16 1.319 1.739

International Journal of Interdisciplinary Research Centre (IJIRC) ISSN: 2455-2275(E)

Volume II, Issue 3 March 2016

All rights are reserved 23

Frequency of availing bank services

Descriptive Statistics

N Mean Std.

Deviation

Variance

Others 500 3.32 1.122 1.259

Debit card/ credit

card 500 3.20 1.153 1.329

Cheque clearing 500 3.09 1.391 1.934

Travellers cheque 500 3.08 1.321 1.744

Demand Draft 500 2.98 1.420 2.018

Bank cheque book 500 2.96 1.369 1.874

Overdraft 500 2.83 1.562 2.441

Mail Transfer 500 2.70 1.279 1.636

Hypotheses testing

H1:- The growth of e-commerce industry is directly related with growth of the online

banking facilities.

H2:- There is a positive Impact of E-Commerce on Changing Consumer Behaviour and

Perception towards banking services.

Hypothesis testing is a process by which an analyst tests a statistical hypothesis. The

methodology employed by the analyst depends on the nature of the data used and the

objectives of the analysis. Hypothesis testing is used to infer a result of a hypothesis

performed on sample data from a larger population, which can be either null or alternate. The

objective of hypothesis testing is to either accept or reject the null hypothesis. The procedure

for deciding if a null hypothesis should be accepted or rejected in favour of an alternate

hypothesis is computed from a survey or test result and is analysed to determine if it falls

within a present acceptance region. If it does, the null hypothesis is accepted otherwise

rejected. For testing of Hypotheses primary and secondary data were used. And e-banking

services which are taken for under study related to each other have been grouped in to five

following category in order to testing of hypothesis results.

International Journal of Interdisciplinary Research Centre (IJIRC) ISSN: 2455-2275(E)

Volume II, Issue 3 March 2016

All rights are reserved 24

Testing of Hypotheses Results

S.No Hypotheses Decision

1

Banking customer become more experienced and savvy using

technology-based banking services. Accepted

2

Customers demand a consistent service offering through

multiple banking channels.

Accepted

3

Customers conduct their banking activities in the branch and

through direct channels.

Accepted

4

Customers use Internet banking as the main channel for

interaction with their preferred bank.

Accepted

5

Innovation in the banking channels is a strong customer value

proposition for all generations.

Accepted

Results

The analysis shows that age is related to the decision to stay with or leave service providers.

In general, when the age group of the customers increases, the customers will have higher

propensity to stay with their banks. results suggested that younger consumers probably have a

higher likelihood of leaving their banks in search of greater convenience, lower prices, higher

deposit interest rates or better services. This may be because younger consumers often must

adjust to significant and substantial changes in their lives. Changes might include such events

as taking up tertiary study, moving away from home, finding a different job, buying a house,

marrying, or having a child. Thus, these consumers thus may have strong reasons for

switching banks.

The test results demonstrated a significant effect in case of demographic factors. This may be

because more highly educated consumers tend to have greater expectations of services. More

educated respondents are also more well-informed. Finally, the effect of respondents'

incomes was examined. Retention for each income group were not similar to one another,

with test results showing a lack of association the between income and retention.

So from the analysis it can be conclude that Innovation in the banking channels is a strong

customer value proposition for all generations and Customer is willing to change to a bank

that offers better technology-based services.

International Journal of Interdisciplinary Research Centre (IJIRC) ISSN: 2455-2275(E)

Volume II, Issue 3 March 2016

All rights are reserved 25

Interpretation

As per Levene's Test for Equality of Variances if p value is p ≤ 0.5 then it can we conclude

that null hypothesis is incorrect and variances are significantly different. On the other side if

p > 0.5 then it can we conclude that null hypothesis is accepted and variances are

insignificant or roughly equal hence assumption is acceptable.

The analysis shows that age is related to the decisions In general, when the age of the

customers increases, the customers will have lower propensity to online banking. This may

be because younger consumers often must adjust to significant and substantial changes in

their lives. Changes might include such events as taking up tertiary study, moving away from

home, finding a different job, buying a house, marrying, or having a child. Thus, these

consumers thus may have strong reasons for Using E-services.

The analysis further shows that education had an effect on customer decisions. The test

results demonstrated a significant effect. This may be because more highly educated

consumers tend to have greater expectations of services. More educated respondents are also

more well-informed. Finally, the effect of respondents' incomes was examined. Customer

decisions for E-banking services for each income group were not similar to one another, with

test results showing a lack of association between income and decisions.

Conclusion

E-Commerce has the positive impact on the service management and consumer behaviour.

And Further more the use of E-Commerce works effectively for the service quality of the

banking sector in terms of security, access, communication, reliability, responsiveness and

perceived customer services.

The Paper discovers the social impact of e-commerce. E-commerce is currently rising at 30%

. Shopping sites like flip-cart, snap-deal, e-Bay Inc. is growing by 60%. The number of

customers of the company has augmented from one million users to 2.5 million in India in the

last four years. Some of the popular imported items imported by Indians include home decor,

branded and unbranded apparel, accessories, and technology products like laptops.

Emergence of international shipping options creates the occasion to reach online consumers

around the globe. Increasing economies with rapidly rising internet diffusion offers an

attractive option for the retailers to expand.

Various studies related to e-services, e-commerce, e-banking pointed out that demographic

profiles of the customers‟ is important factor in using banking services. Hence, we have

International Journal of Interdisciplinary Research Centre (IJIRC) ISSN: 2455-2275(E)

Volume II, Issue 3 March 2016

All rights are reserved 26

tested hypothesis and empirical evidences of study reveal that gender age, education,

profession or occupation and income of the consumers play a significant role in consumer

buying behaviour in E-banking .

References

1. Black, G.S. (2005) is eBay for everyone? An Assessment of Consumer

Demographics, SAM Advanced Management Journal, winter, Vol. 70 Issue 1.

2. BMRB International (2004) Hadley House, 79-81 Uxbridge Road, Ealing, London,

W5 5SU. Internet Monitor Data.

3. Brucks, M. (1985) The effect of product class knowledge on information search

behavior. Journal of Consumer Research, Vol. 2, pp.1–16.

4. Buyer decision processes, 2006, Wikipedia is a registered trademark of the

5. Wikimedia Foundation, Inc. Available at:

http://en.wikipedia.org/wiki/Buyer_decision_processes

6. Cassell J. and Bickmore T. (2000) External manifestations of trustworthiness in the

interface. Communications of the ACM December: 50-56.

7. “E-commerce and Economic Development” Mahesh C Purohit Vishnu Kanta Purohit.

Foundation for Public Economics and Policy Research

8. “Economic And Social Impacts Of E-Commerce” “Dr. Bimal Anjum, Rajesh Tiwari,

CFA” International Journal Of Computing And Corporate Resarch.

9. “Emerging Trend Of E-Commerce In India: Some Crucial Issues, Prospects And

Challenges” Sarbapriya Ray “Computer Engineering And Intelligent Systems ISSN 2222-

1719

10. Fayu Zheng. 2006. Internet shopping and its impact on consumer behavior.

University of Nottingham

11. Lee K. and Chung N. (2000) Effect of virtual reality-driven shopping mall and

consumer‟s purchase intention. Korean Management Review, 29 (3): 377-405.

12. Moon Byeong-Joon (2004) Consumer adoption of the internet as an information search

and product purchase channel: some research hypotheses, Int. J. Internet Marketing

and Advertising, Vol. 1, No. 1.

13. Perner Lars The Psychology of Consumers – Consumer Behavior and Marketing. Los

Angeles, CA.

International Journal of Interdisciplinary Research Centre (IJIRC) ISSN: 2455-2275(E)

Volume II, Issue 3 March 2016

All rights are reserved 27

14. Sheth, J. N., (1983) An integrative theory of patronage preference and behaviour. In:

Darden WR, Lusch RF, editors. Patronage behavior and retail management. Orlando

(FL): Elsevier; 1983.p.9-28.

15. www.rbi.org.in

16. www.googlescholar.com