IMI Indoor Climate - imiplc.com · President, ICG Michael Preinerstorfer ... 2003 2004 2005 2006...

61

IMI Indoor Climate

Transcript of IMI Indoor Climate - imiplc.com · President, ICG Michael Preinerstorfer ... 2003 2004 2005 2006...

IMI Indoor Climate

AgendaAgenda1. Our Competitive Advantage

2. Growth Drivers1 E Effi i1. Energy Efficiency 2. Emerging Markets 3. New Products

3. Margin Drivers1. Key Account Management2. Engineering Advantage3. LCM

4. Q&As

Management TeamManagement Team

S T Mi h l P i t f Mik C bi MBE R bi V ll tSean ToomesPresident, ICG

Michael PreinerstorferManaging Director, Heimeier & Central Europe

Mike Carbine MBEHead of ICG Emerging Markets

Robin VollertVP W Europe

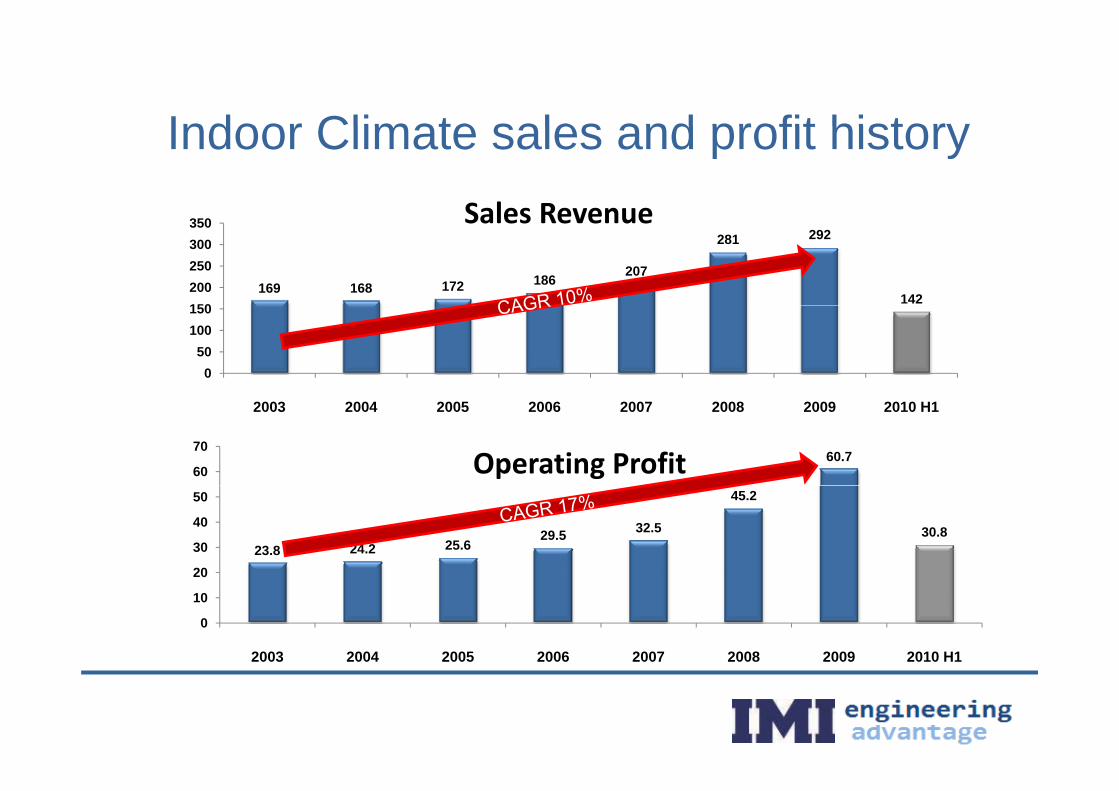

Indoor Climate sales and profit historyIndoor Climate sales and profit history Sales Revenue

169 168 172 186 207

281 292

142150200250300350 Sales Revenue

050

100150

2003 2004 2005 2006 2007 2008 2009 2010 H1

60.760

70Operating Profit

23.8 24.2 25.629.5 32.5

45.2

30.8

20

30

40

50

0

10

20

2003 2004 2005 2006 2007 2008 2009 2010 H1

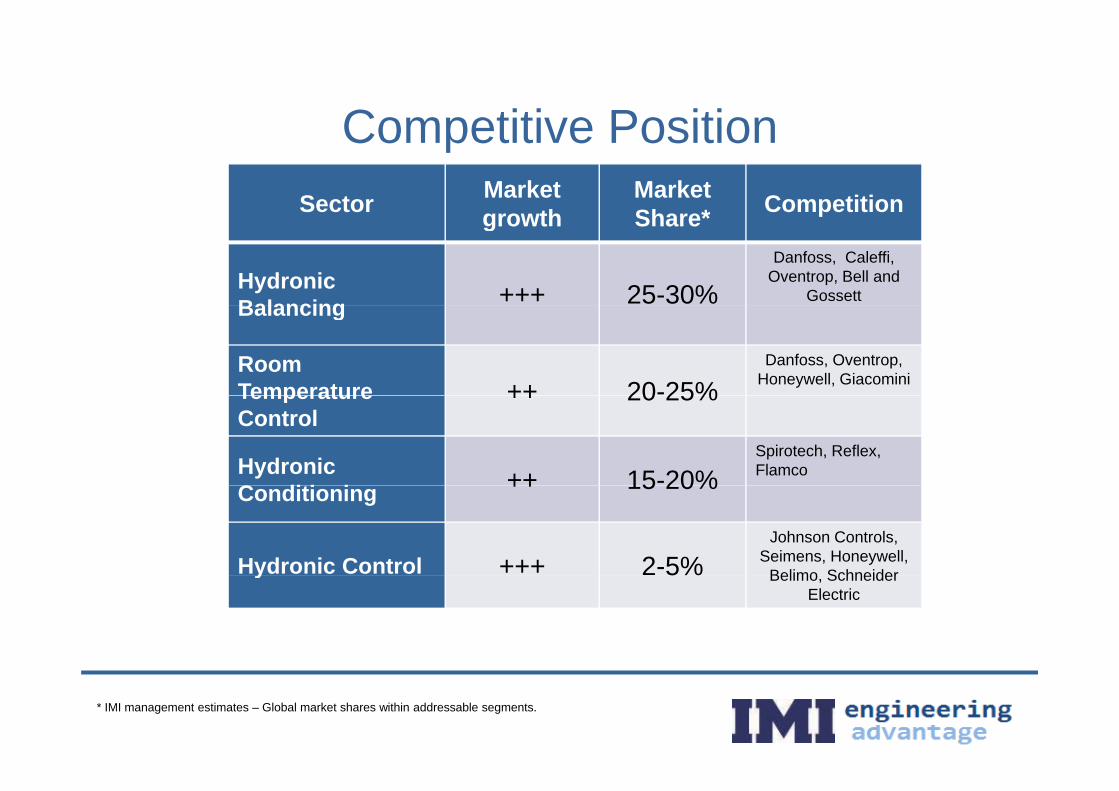

Competitive PositionCompetitive PositionSector Market

growthMarket Share* Competitiongrowth Share* p

HydronicBalancing +++ 25-30%

Danfoss, Caleffi, Oventrop, Bell and

Gossett Balancing

Room Temperature ++ 20-25%

Danfoss, Oventrop, Honeywell, GiacominiTemperature

Control++ 20 25%

HydronicC diti i ++ 15-20%

Spirotech, Reflex, Flamco

Conditioning ++ 15 20%

Hydronic Control +++ 2-5%Johnson Controls,

Seimens, Honeywell, Belimo Schneidery 5% Belimo, Schneider

Electric

* IMI management estimates – Global market shares within addressable segments.

1 Our Competitive Advantage1. Our Competitive Advantage

- What makes us special?

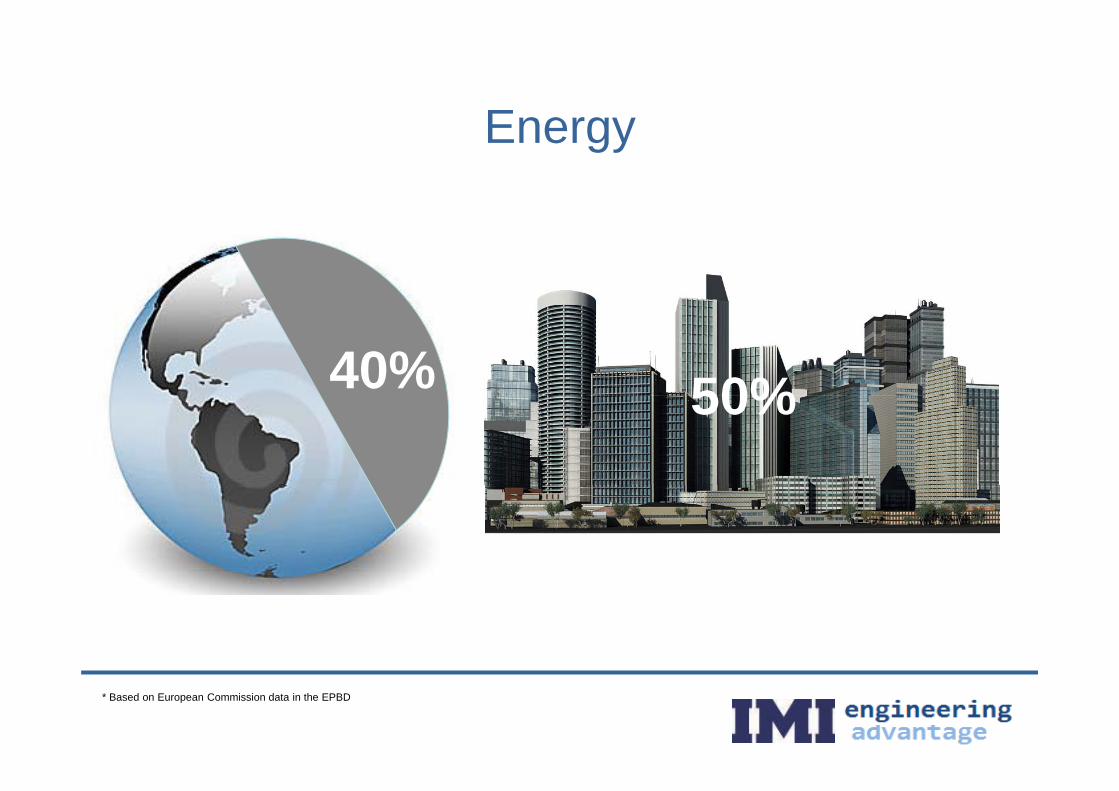

EnergyEnergy

40% 50%50%

* Based on European Commission data in the EPBD

Conditions are highly variableConditions are highly variable

Buildings have many different usesBuildings have many different uses

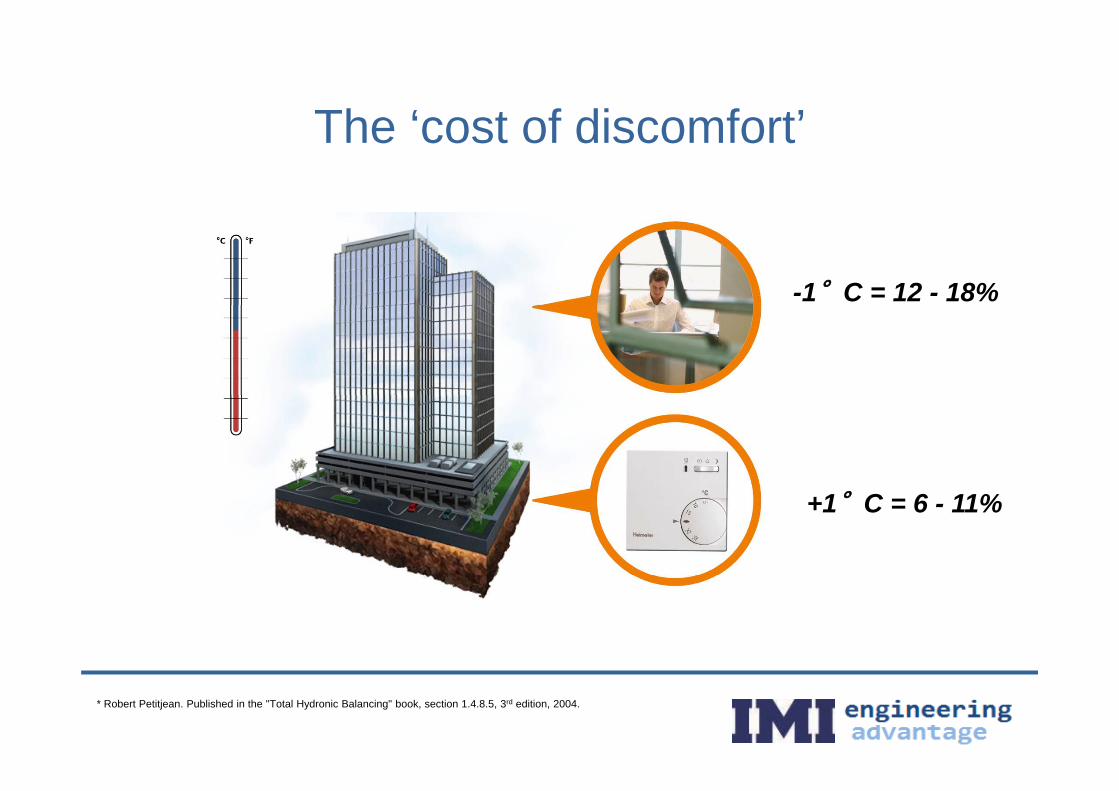

The ‘cost of discomfort’The cost of discomfort

-1°C = 12 - 18%

+1°C = 6 - 11%

* Robert Petitjean. Published in the "Total Hydronic Balancing" book, section 1.4.8.5, 3rd edition, 2004.

The Hydronic challengeThe Hydronic challenge

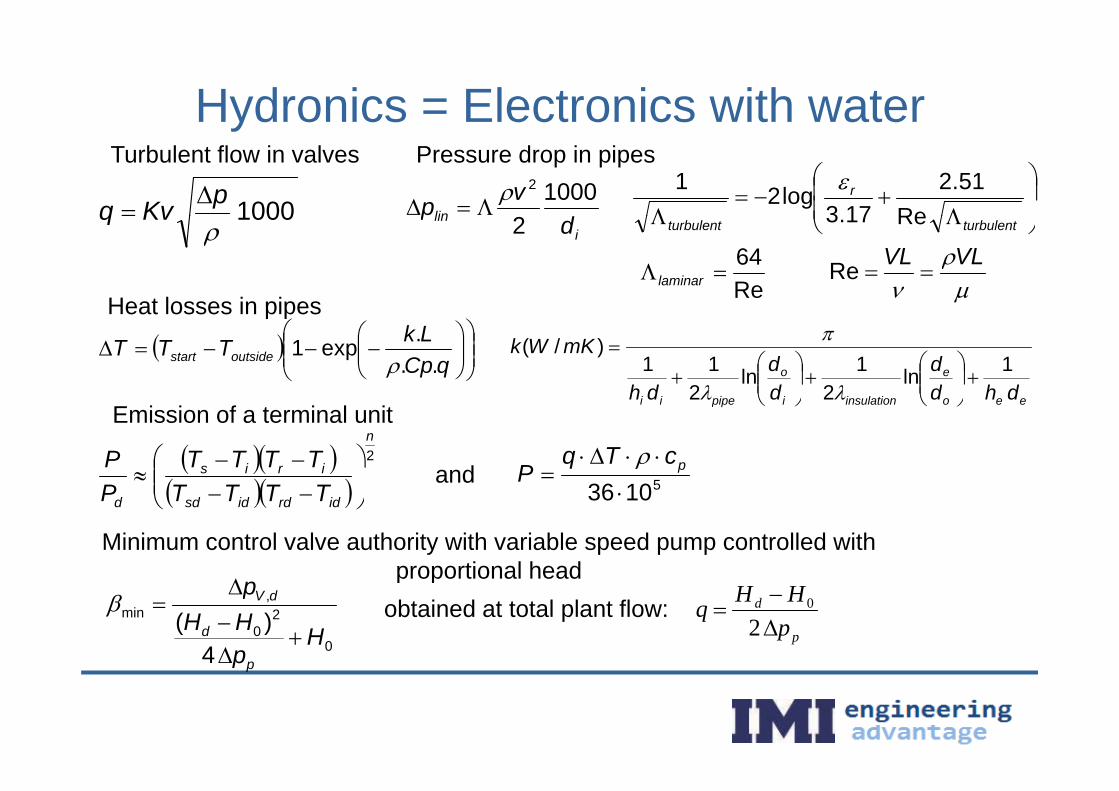

Hydronics = Electronics with water

1000pKvq

Turbulent flow in valves Pressure drop in pipes

linvp 10002

r

Re51.2

173log21

y

1000

Kvqi

lin dp

2

VLVL

Re

turbulentturbulent Re17.3

Re64

laminar

Heat losses in pipesHeat losses in pipes

eo

dhdd

dd

dh

mKWk1ln

21ln

211

)/(

qCpLkTTT outsidestart ...exp1

Emission of a terminal unit

2n

iris

TTTTTTTT

PP

51036

pcTq

P

and

eeoinsulationipipeii dhdddh 22

Minimum control valve authority with variable speed pump controlled with proportional head

idrdidsdd TTTTP

51036

proportional head

p

d

pHHq

2

0

0

20

,min

4)( H

pHHp

p

d

dV

obtained at total plant flow:

pp

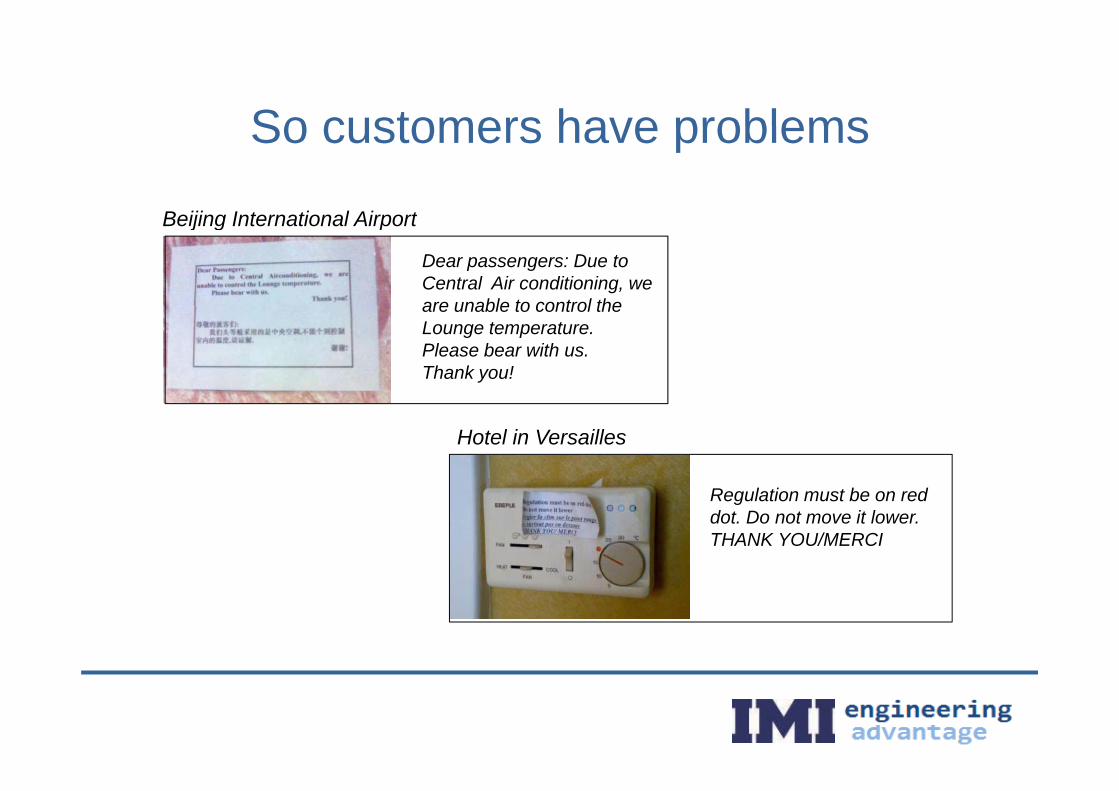

So customers have problemsSo customers have problems

Beijing International AirportBeijing International Airport

Dear passengers: Due to Central Air conditioning, we are unable to control theare unable to control the Lounge temperature.Please bear with us.Thank you!

Hotel in Versailles

Regulation must be on red dot. Do not move it lower.THANK YOU/MERCI

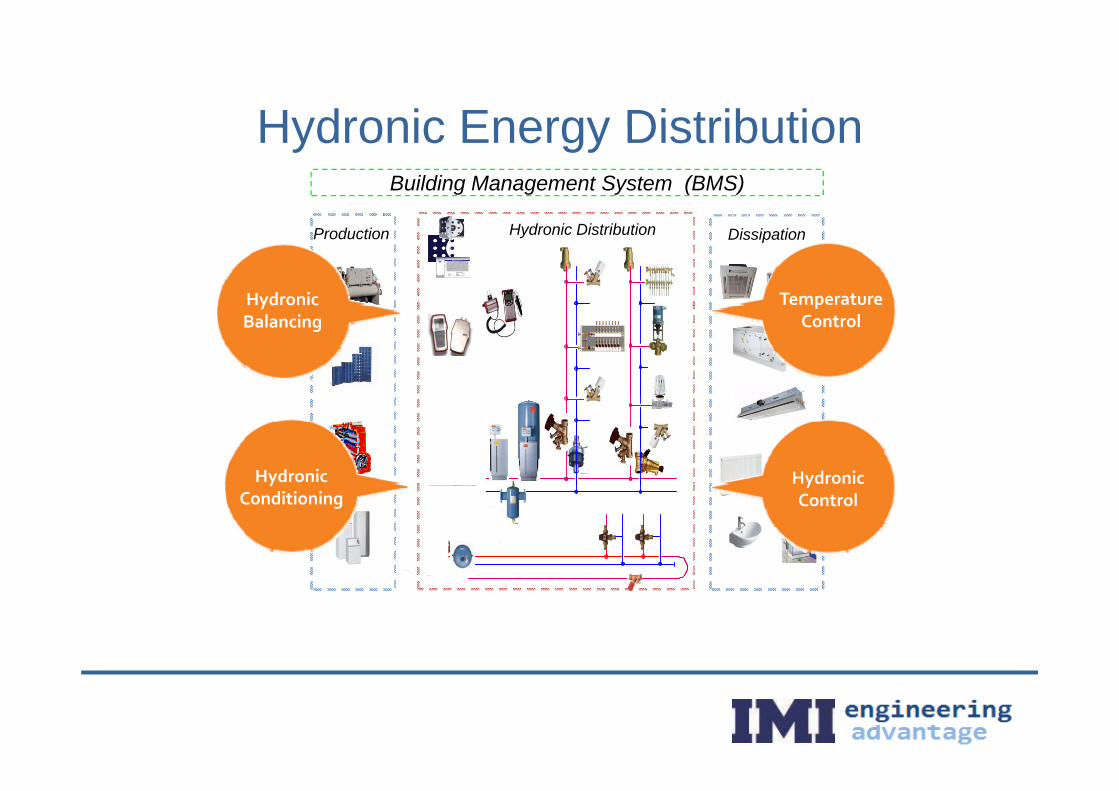

Hydronic Energy DistributionHydronic Energy Distribution Building Management System (BMS)

Strategic focusDissipationProduction

Strategic focusHydronic Distribution

Temperature Hydronic pControl

yBalancing

Hydronic Hydronic yControl

yConditioning

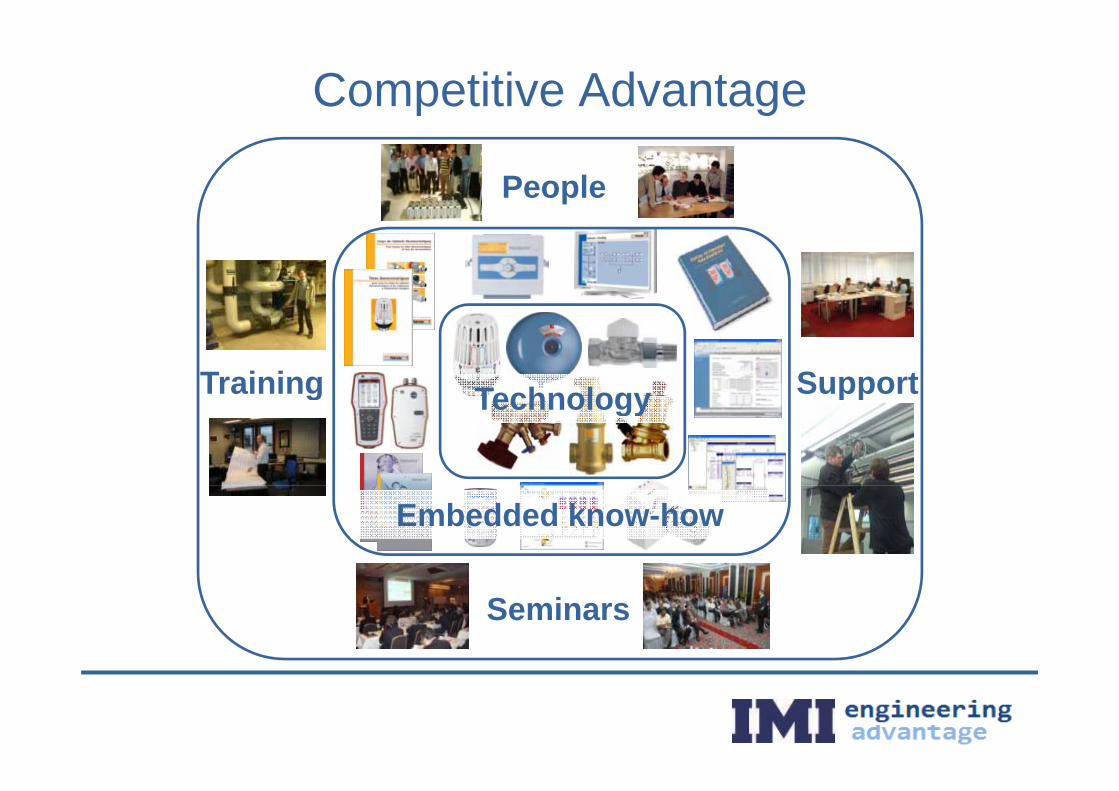

Competitive Advantage

People

TechnologyTraining SupportTechnologyg pp

Embedded know-how

Seminars

Our Destiny

Most customer-focused, most knowledgeable and most innovative

Hydronic Solutions company in the world

2. Growth Drivers

Energy Efficiency, Emerging Markets, New Products

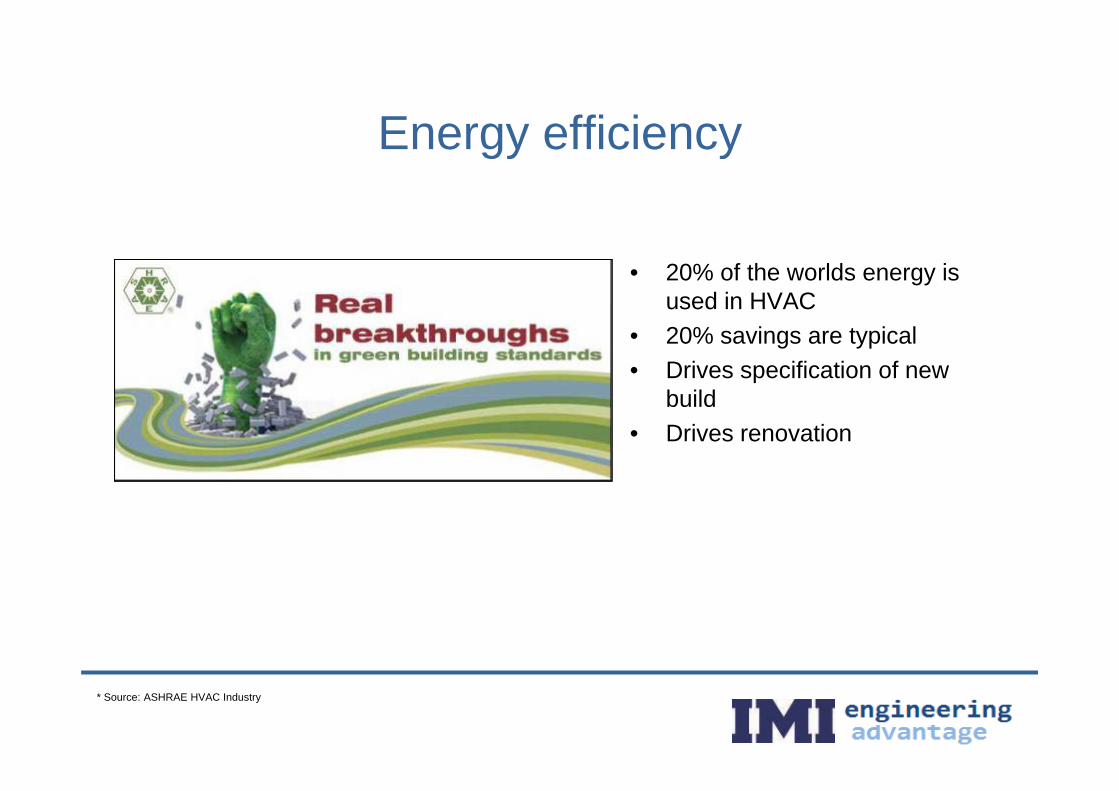

Energy efficiencyEnergy efficiency

• 20% of the worlds energy is used in HVACused in HVAC

• 20% savings are typical• Drives specification of new

buildbuild• Drives renovation

* Source: ASHRAE HVAC Industry

Developers and ownersDevelopers and owners

• Netherlands ING• Netherlands – ING

D i & ti t• Drivers & motivators– Property value– Total cost of ownership– Energy efficiency– Minimise complaints– Reputation

”Modern, green, energy-efficient

buildings have vacancy of only 3% p– Legislation vs market average 10-15%.”

- Henk van Vliet ING Real EstateHenk van Vliet, ING Real Estate

20102010

20502050

”Renovation will be the main opportunity in the coming years for the HVAC industry.pp y g y yEspecially resilient where fuelled by energy-efficiency legislation. The Renovationbusiness is substantially less price-sensitive than new construction (the buildingitself is already financed and HVAC performance known)”y p )

Stephane Pasteur, Barbanel Consultants , France

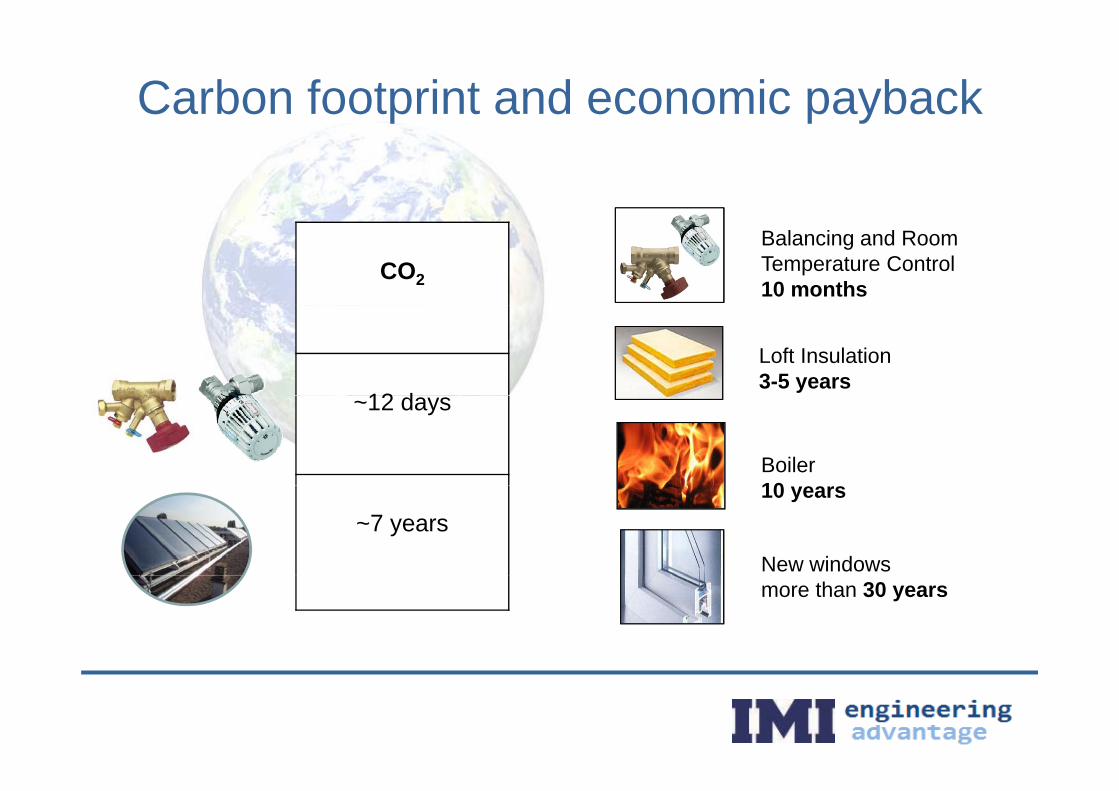

Carbon footprint and economic payback

CO2

Balancing and Room Temperature Control 10 months

12 d

Loft Insulation 3-5 years

~12 days

Boiler 10

~7 years

New windows

10 years

more than 30 years

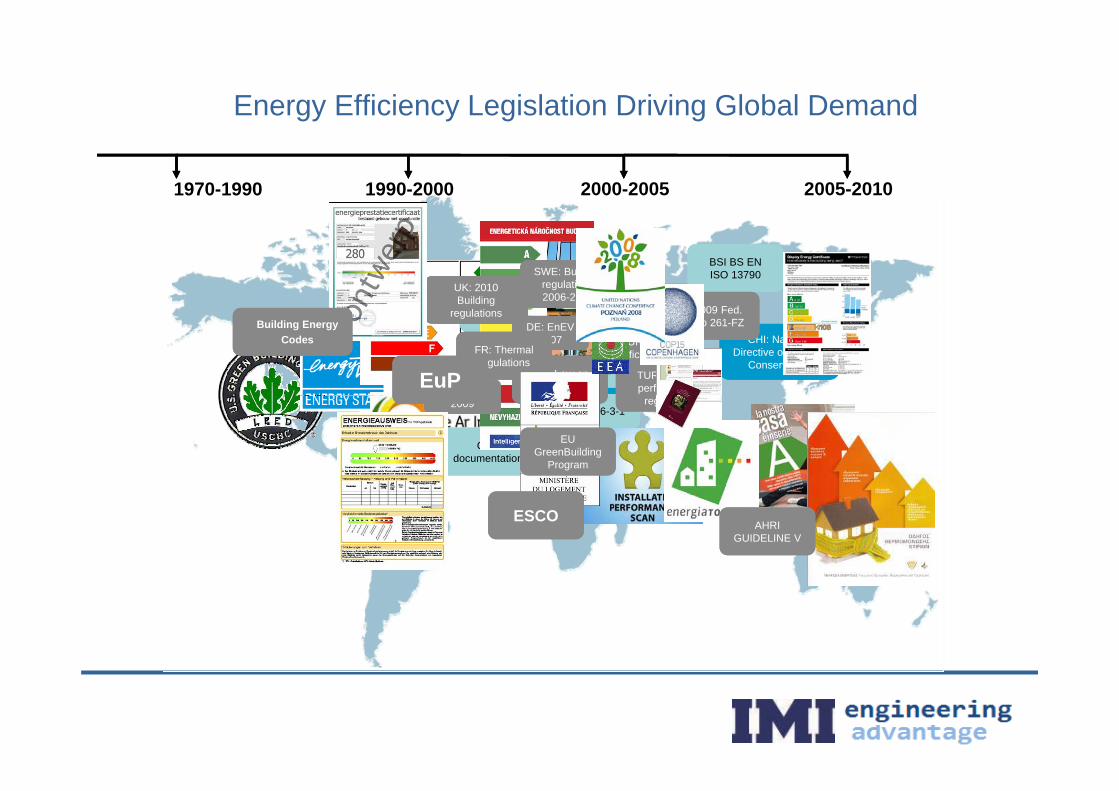

Energy Efficiency Legislation Driving Global Demand

1970-1990 1990-2000 2000-2005 2005-2010

UK: BuildingUK: Building

BSI BS EN ISO 13790BSI BS EN ISO 13790EN ISO

13790:2004EN ISO

13790:2004DE: EnEV2012

DE: EnEV2012

SWE: Building regulations 2006-2012

SWE: Building regulations 2006-2012

RU 2009 F dRU 2009 F d

UK: 2010 Building

UK: 2010 Building

DE: 1st Heating systems regulation

DE: 1st Heating systems regulation

DE: 2nd Heating systems regulation

DE: 2nd Heating systems regulation CHI: National

Directive on Energy Conservation

CHI: National Directive on Energy

ConservationDE: 3rd Heating systems regulation

DE: 3rd Heating systems regulation

DE: 4th Heating systems regulation

DE: 4th Heating systems regulationDE: EnEVDE: EnEV DE: EnEV

2005 vDI2035DE: EnEV

2005 vDI2035FR: Thermal regulation

FR: Thermal regulation

UK: Building regulations

UK: Building regulations EU: Energy Performance of

Buildings Directive (EPBD) 2002/91/EC

EU: Energy Performance of Buildings

Directive (EPBD) 2002/91/ECDE: EnEV

2007DE: EnEV

2007

DE: EnEVDE: EnEVFR: Law on

solar systemsFR: Law on

solar systems

20122012

FR: Thermal regulations

FR: Thermal regulations

RU: 2009 Fed. Law No 261-FZRU: 2009 Fed. Law No 261-FZ

TUR: Energy efficiency lawTUR: Energy efficiency law

TUR: Energy performance TUR: Energy performance

gregulations

gregulations

Building Energy Codes

Building Energy Codes

EuPEuP20052005

CEN documentation

CEN documentation

EN 15316-3-1EN 15316-3-120092009 regulationregulation

EU GreenBuilding

Program

EU GreenBuilding

Program

AHRI GUIDELINE V

AHRI GUIDELINE V

ESCOESCO

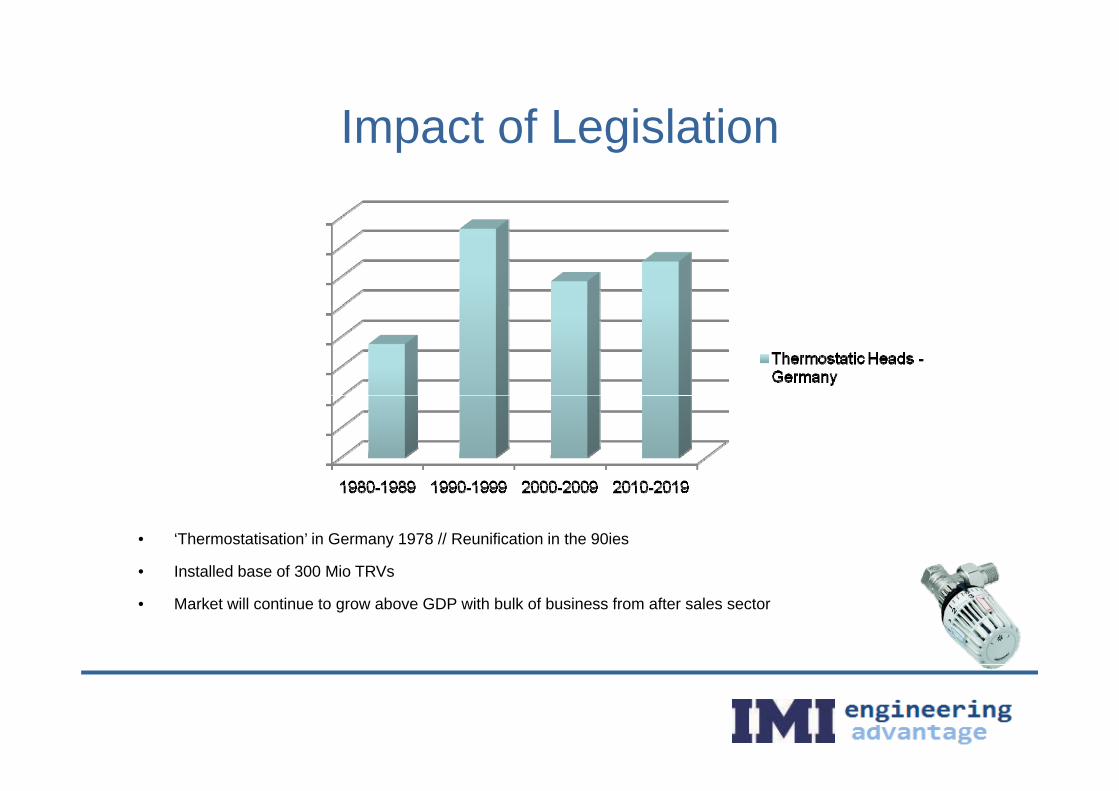

Impact of LegislationImpact of Legislation

Mio

. €

• ‘Thermostatisation’ in Germany 1978 // Reunification in the 90ies

• Installed base of 300 Mio TRVsInstalled base of 300 Mio TRVs

• Market will continue to grow above GDP with bulk of business from after sales sector

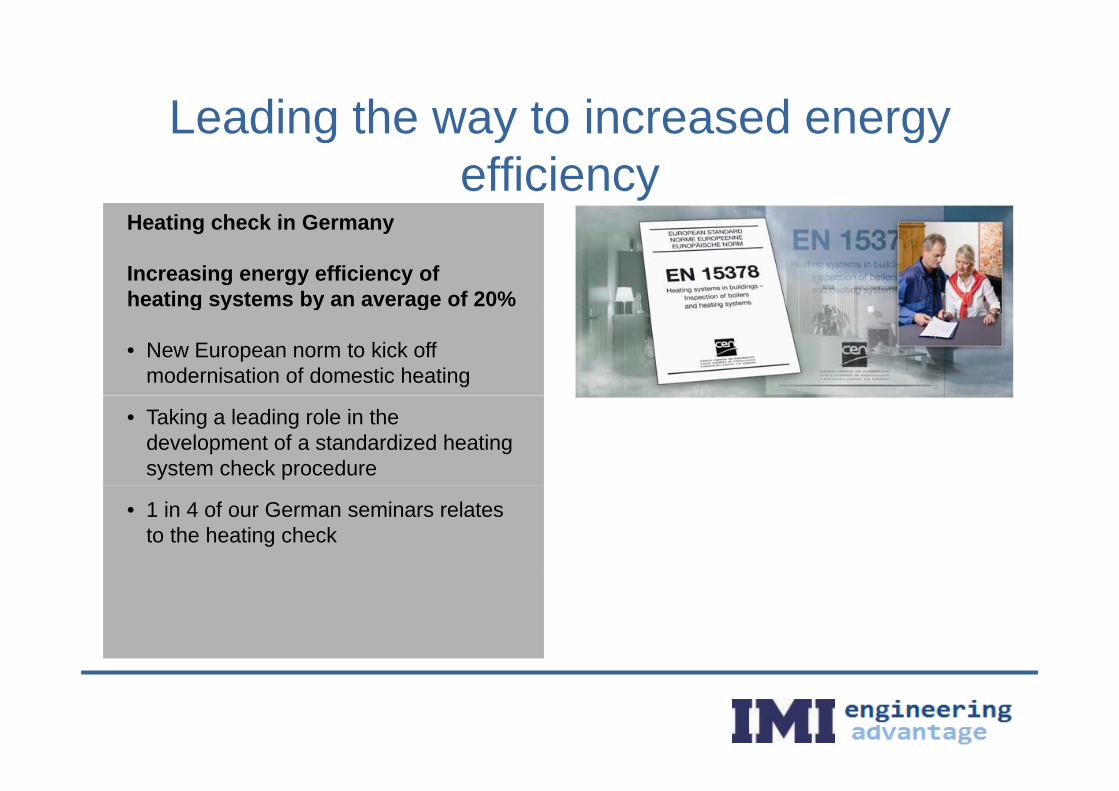

Leading the way to increased energy

H ti h k i G

Leading the way to increased energy efficiency

Heating check in Germany

Increasing energy efficiency of heating systems by an average of 20%heating systems by an average of 20%

• New European norm to kick off modernisation of domestic heating

• Taking a leading role in the development of a standardized heating system check procedure

• 1 in 4 of our German seminars relatesto the heating check

2. Growth Drivers

Energy Efficiency, Emerging Markets, New Products

Accelerating growth in new areasAccelerating growth in new areas

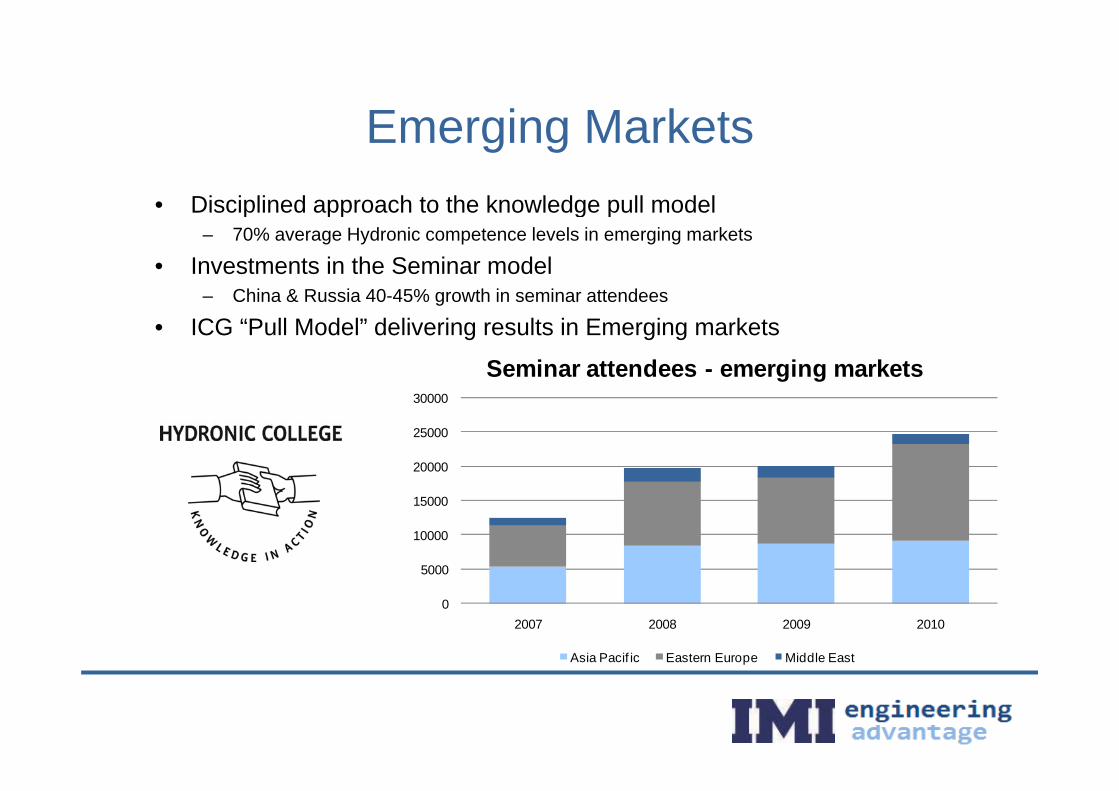

Emerging MarketsEmerging Markets• Disciplined approach to the knowledge pull modelp pp g p

– 70% average Hydronic competence levels in emerging markets

• Investments in the Seminar model– China & Russia 40-45% growth in seminar attendees

• ICG “Pull Model” delivering results in Emerging markets

30000

Seminar attendees - emerging markets

20000

25000

30000

5000

10000

15000

02007 2008 2009 2010

Asia Pacif ic Eastern Europe Middle East

Our Ambitions in ChinaOur Ambitions in China• Knowledge is our foundation

BeijingShenyang

• Knowledge is our foundation• Regional expansion

Hebei

SuzhouXi’anTianjin

QingdaoNanjin

An HuiWuhan

ShanghaiChengdu

Hangzhou Ningbo

Nanjin

Chongquingg g

Shenzhen

GuanghzouIndoor Climate Locations

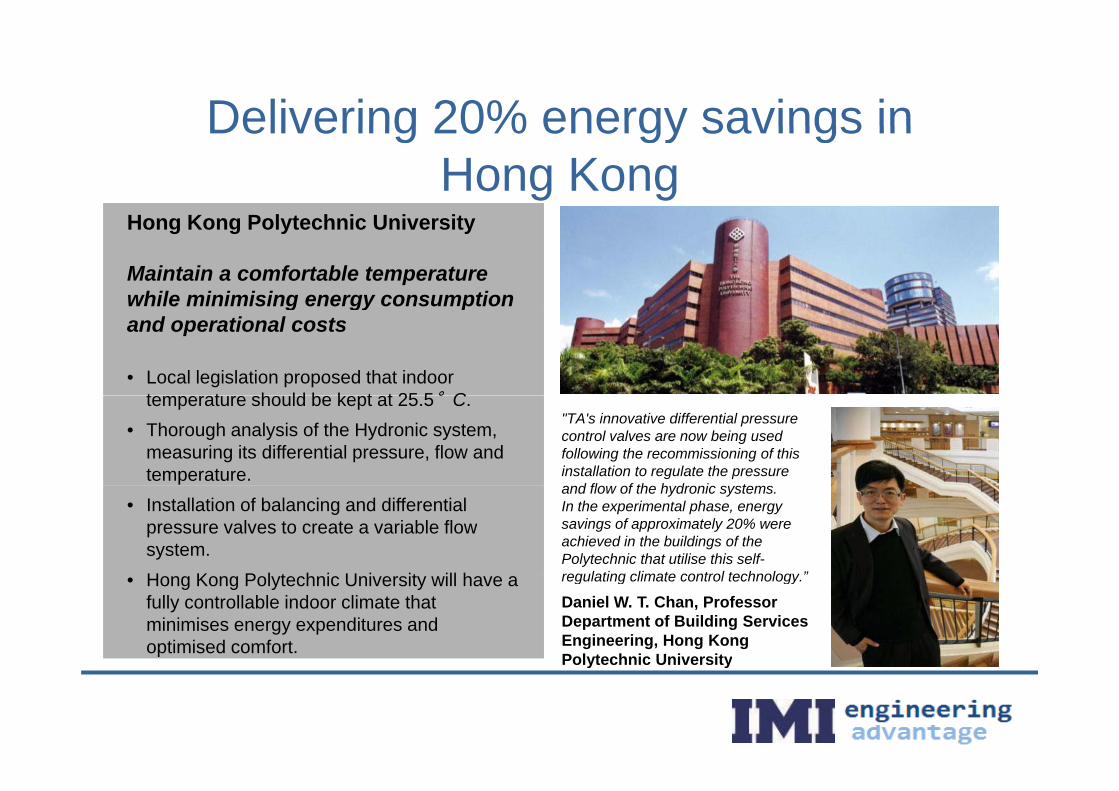

Delivering 20% energy savings in

H K P l t h i U i it

Delivering 20% energy savings in Hong Kong

Hong Kong Polytechnic University

Maintain a comfortable temperature while minimising energy consumptionwhile minimising energy consumption and operational costs

• Local legislation proposed that indoor t t h ld b k t t 25 5°Ctemperature should be kept at 25.5°C.

• Thorough analysis of the Hydronic system, measuring its differential pressure, flow and temperature.

"TA's innovative differential pressure control valves are now being used following the recommissioning of this installation to regulate the pressure

d fl f th h d i t• Installation of balancing and differential

pressure valves to create a variable flow system. H K P l t h i U i it ill h

and flow of the hydronic systems. In the experimental phase, energy savings of approximately 20% were achieved in the buildings of the Polytechnic that utilise this self-regulating climate control technology ”• Hong Kong Polytechnic University will have a

fully controllable indoor climate that minimises energy expenditures and optimised comfort.

regulating climate control technology.

Daniel W. T. Chan, ProfessorDepartment of Building Services Engineering, Hong Kong Polytechnic Universityo ytec c U e s ty

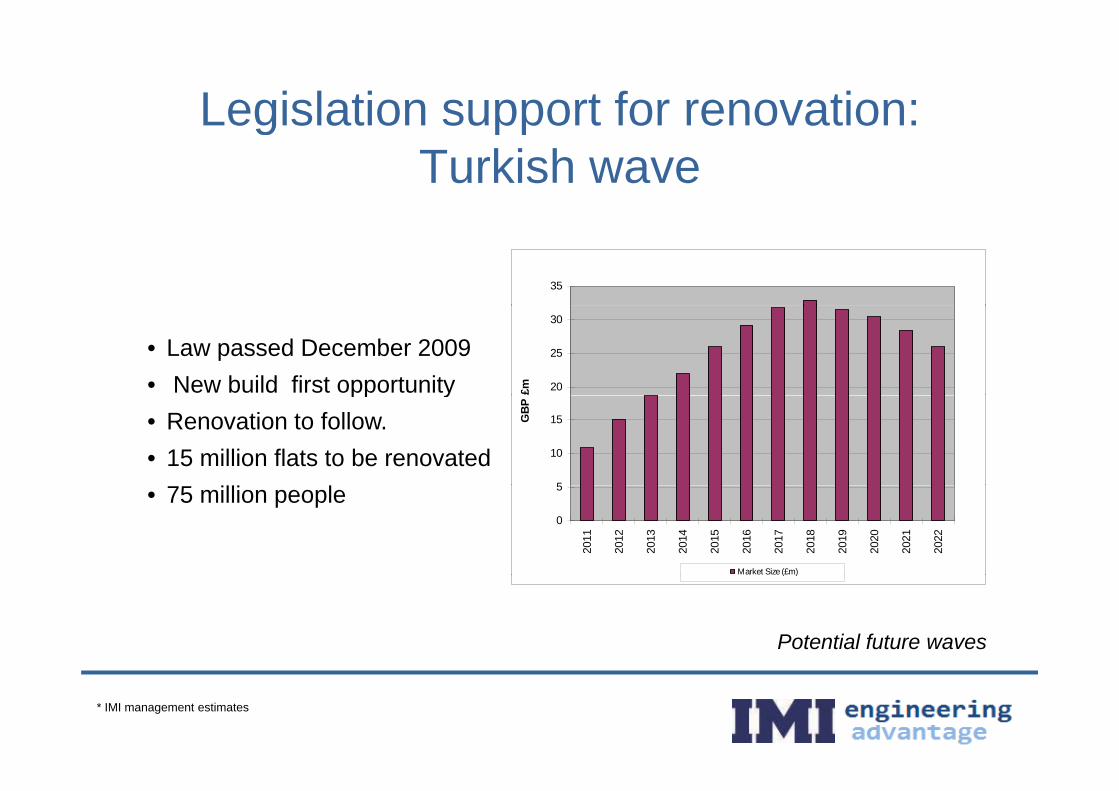

Legislation support for renovation: g ppTurkish wave

35

• Law passed December 2009• New build first opportunity 20

25

30

£mpp y• Renovation to follow.• 15 million flats to be renovated

5

10

15GB

P

• 75 million people0

5

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

Market Size (£m)

Potential future waves

( )

* IMI management estimates

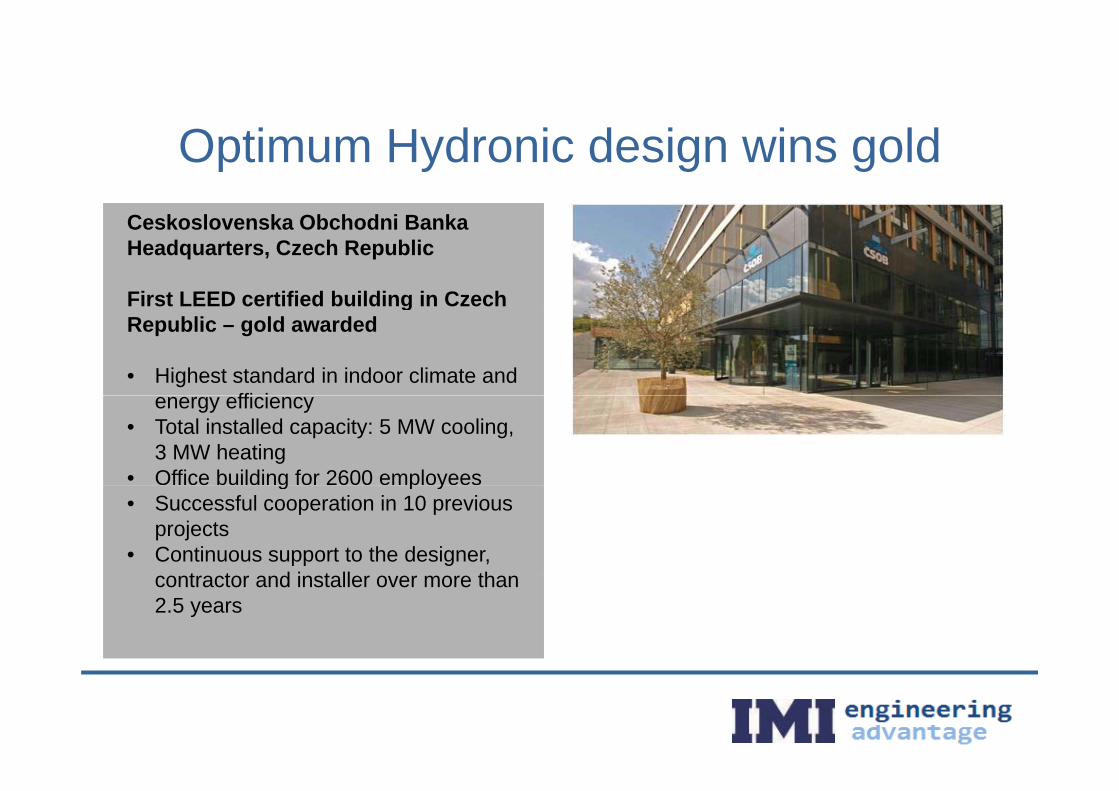

Driving demand for our productsDriving demand for our products

C k l k Ob h d i B k

Optimum Hydronic design wins goldCeskoslovenska Obchodni Banka Headquarters, Czech Republic

First LEED certified building in CzechFirst LEED certified building in Czech Republic – gold awarded

• Highest standard in indoor climate and ffi ienergy efficiency

• Total installed capacity: 5 MW cooling, 3 MW heating

• Office building for 2600 employeesg p y• Successful cooperation in 10 previous

projects• Continuous support to the designer,

t t d i t ll thcontractor and installer over more than 2.5 years

2. Growth Drivers

Energy Efficiency, Emerging Markets, New Products

Extending our competenciesExtending our competencies

Strategic focusWorld Market L d

World market l d Strategic focus Leaderleader

Temperature Hydronic Balancing ControlBalancing

H d i Hydronic Control

New Technology

HydronicConditioning

Aspiring k t Technology

Entrantmarket leader

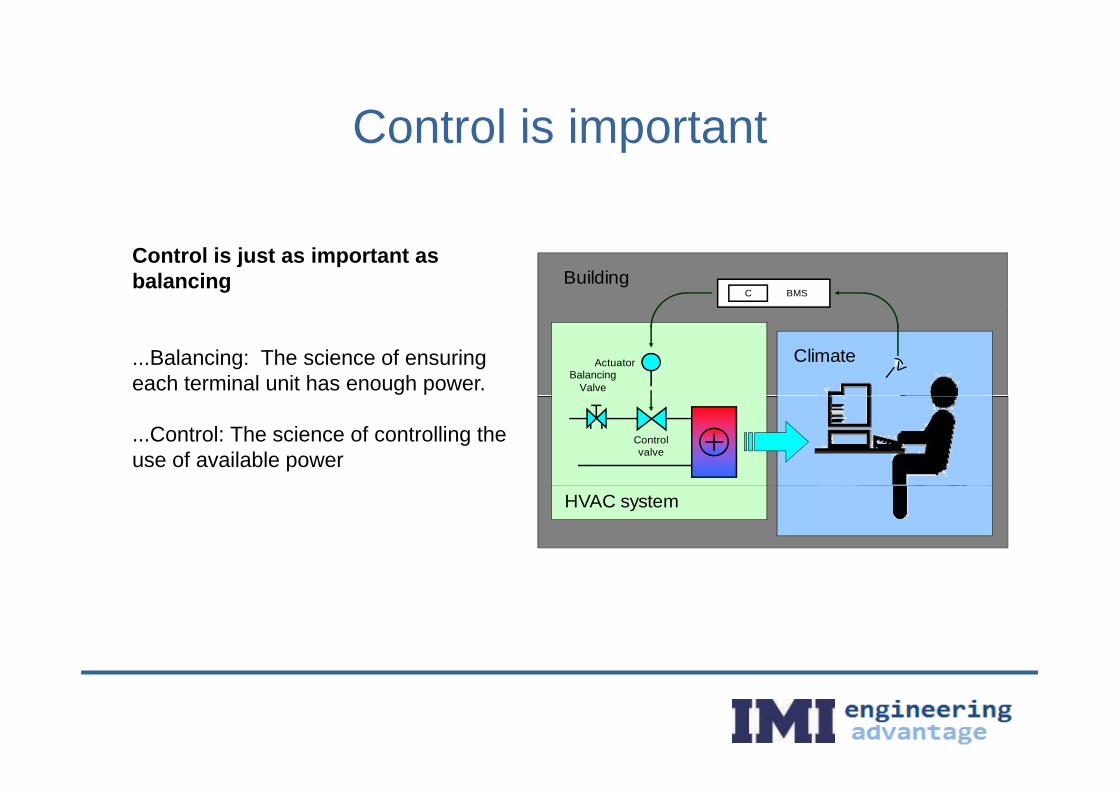

Control is importantControl is important

Control is just as important as balancing

C BMSBuilding

...Balancing: The science of ensuring each terminal unit has enough power.

ClimateActuatorBalancing

Valve

...Control: The science of controlling the use of available power

Control valve

HVAC system

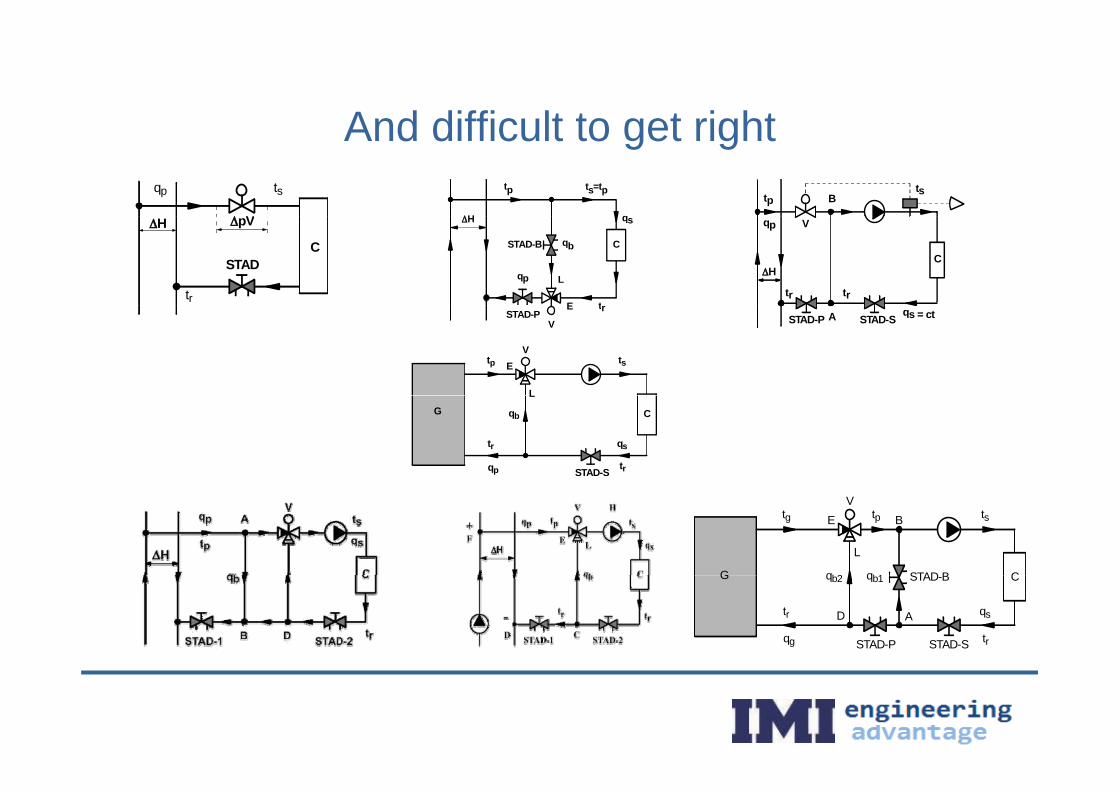

And difficult to get rightAnd difficult to get righttsqp

V qH

ts=tptptp

tsB

tr

pV

STAD

H

C

L

t

qs

qbSTAD-B C

H

E

qptr

qp

H

V

C

trtrSTAD-P

V

E qs = ctSTAD-SSTAD-P A

tp tsEV

L

tr qs

STAD-S

G

qp

L

qb

tr

C

tg tsE

G

V

L

qb2 Cqb1

Btp

STAD B

tr qs

STAD-S

G

qg

qb2

tr

C

D

qb1

A

STAD-B

STAD-P

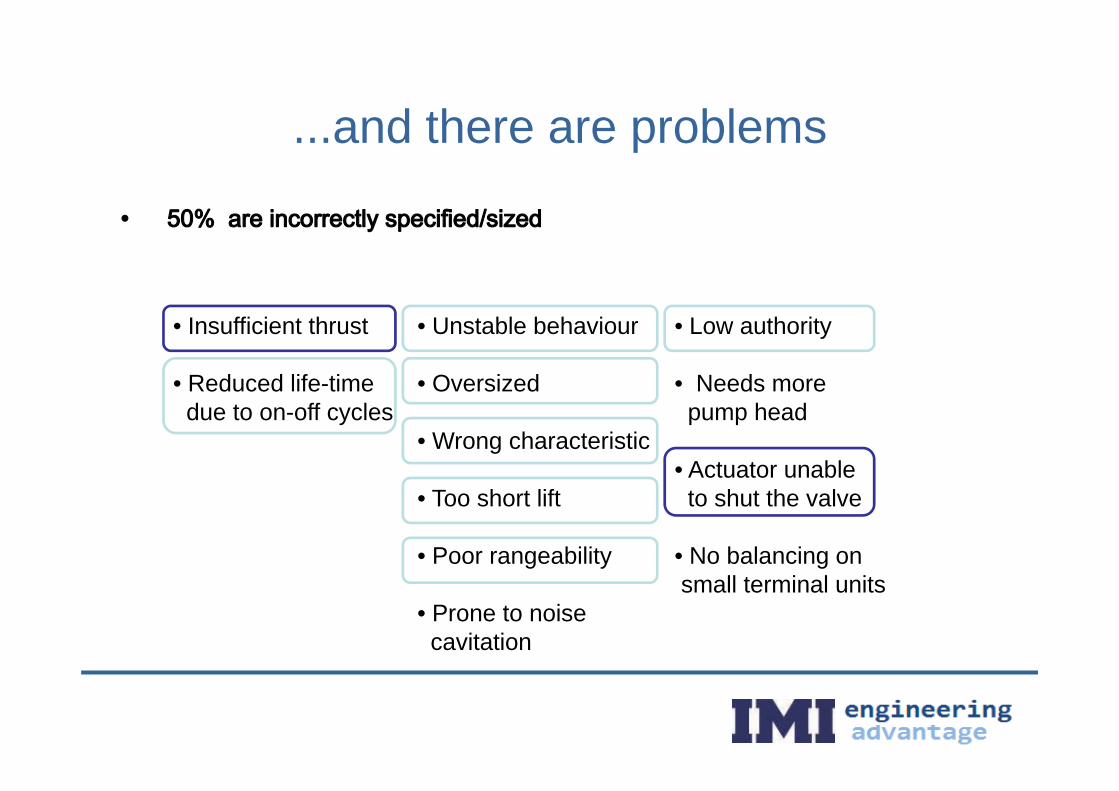

and there are problems...and there are problems

• Unstable behaviour

• Oversized

• Low authority

• Needs more

• Insufficient thrust

• Reduced life-time

• Wrong characteristicpump head

• Actuator unable

due to on-off cycles

• Too short lift

• Poor rangeability

to shut the valve

• No balancing on

• Prone to noise cavitation

small terminal units

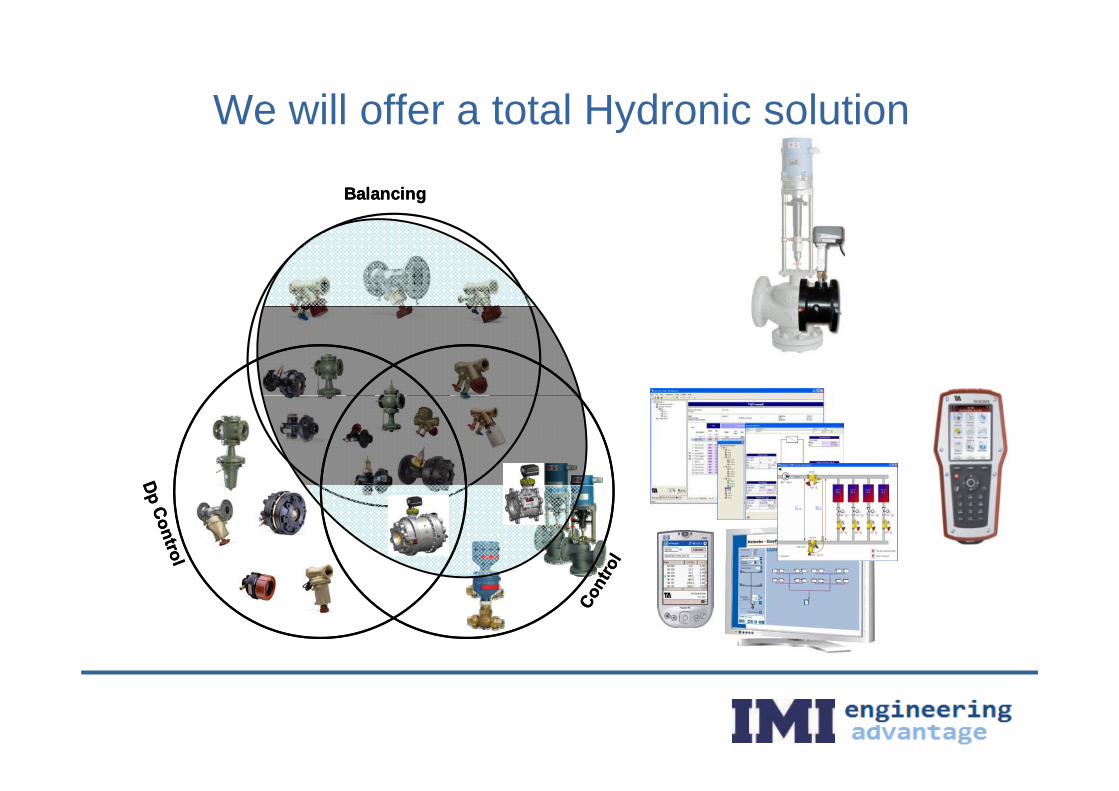

We will offer a total Hydronic solution

BalancingBalancing

y

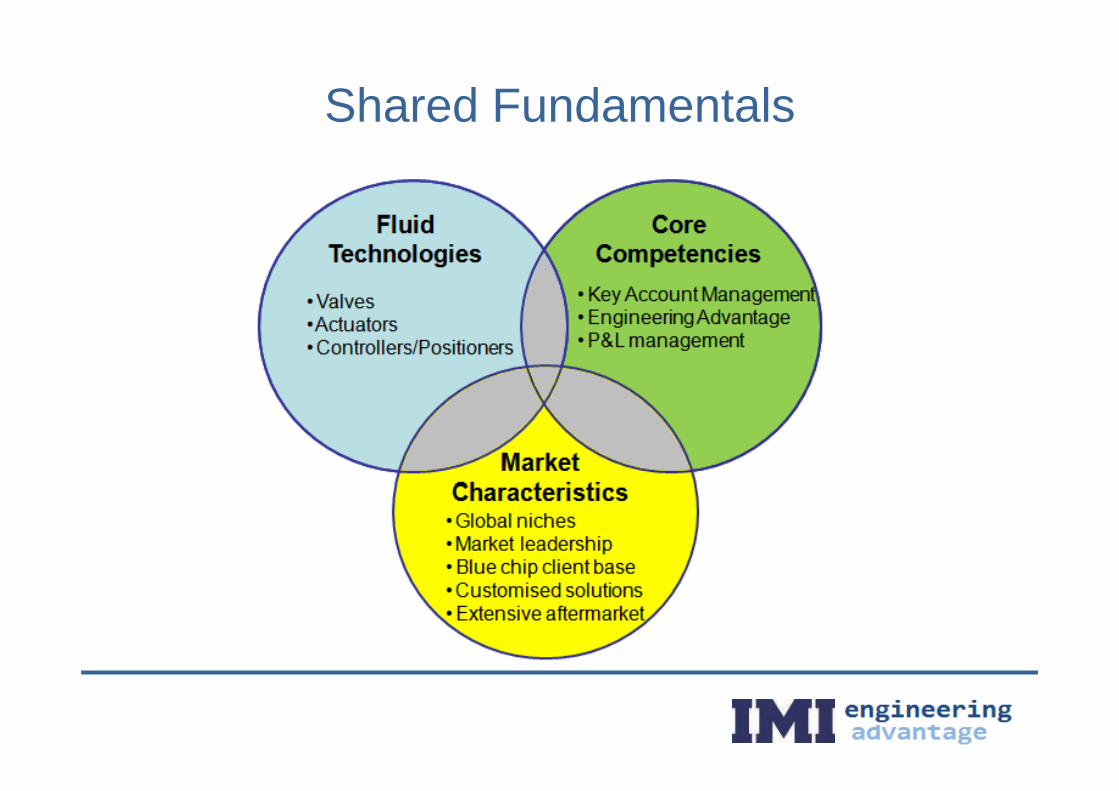

Shared Fundamentals

3. Margin Drivers

Key Account Management, Engineering Advantage, LCM

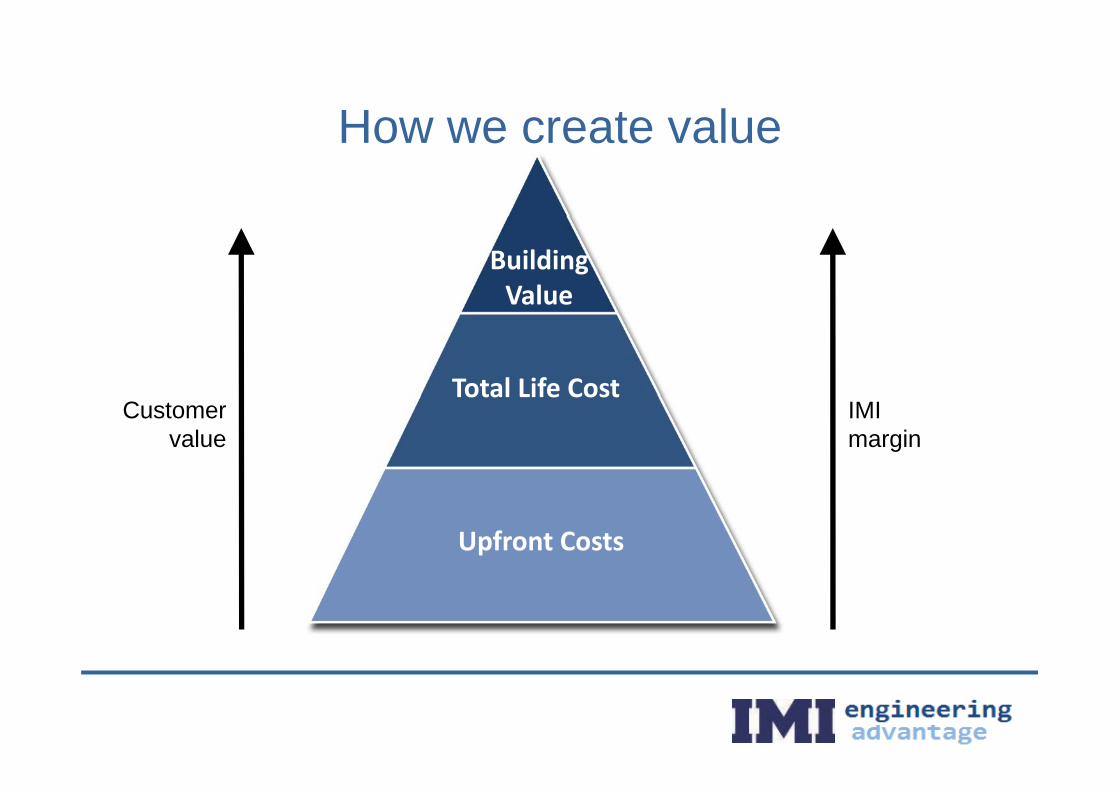

How we create valueHow we create value

Building Value

Total Life CostCustomer

valueIMImargin

Total Life Cost

Upfront Costs

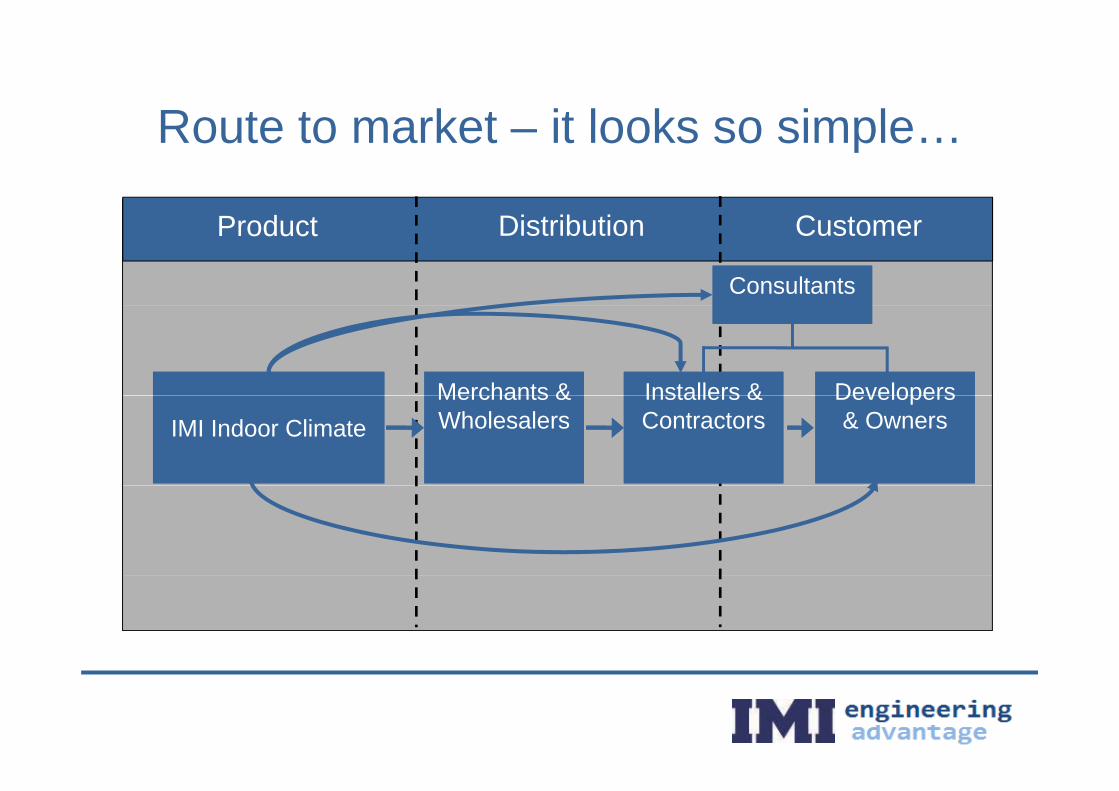

Route to market it looks so simpleRoute to market – it looks so simple…

P d t Di t ib ti C tProduct Distribution Customer

ConsultantsConsultants

Merchants &Merchants & DevelopersDevelopersInstallers &Installers &IMI Indoor ClimateIMI Indoor Climate

Merchants &WholesalersMerchants &Wholesalers

Developers & Owners

Developers & Owners

Installers & ContractorsInstallers & Contractors

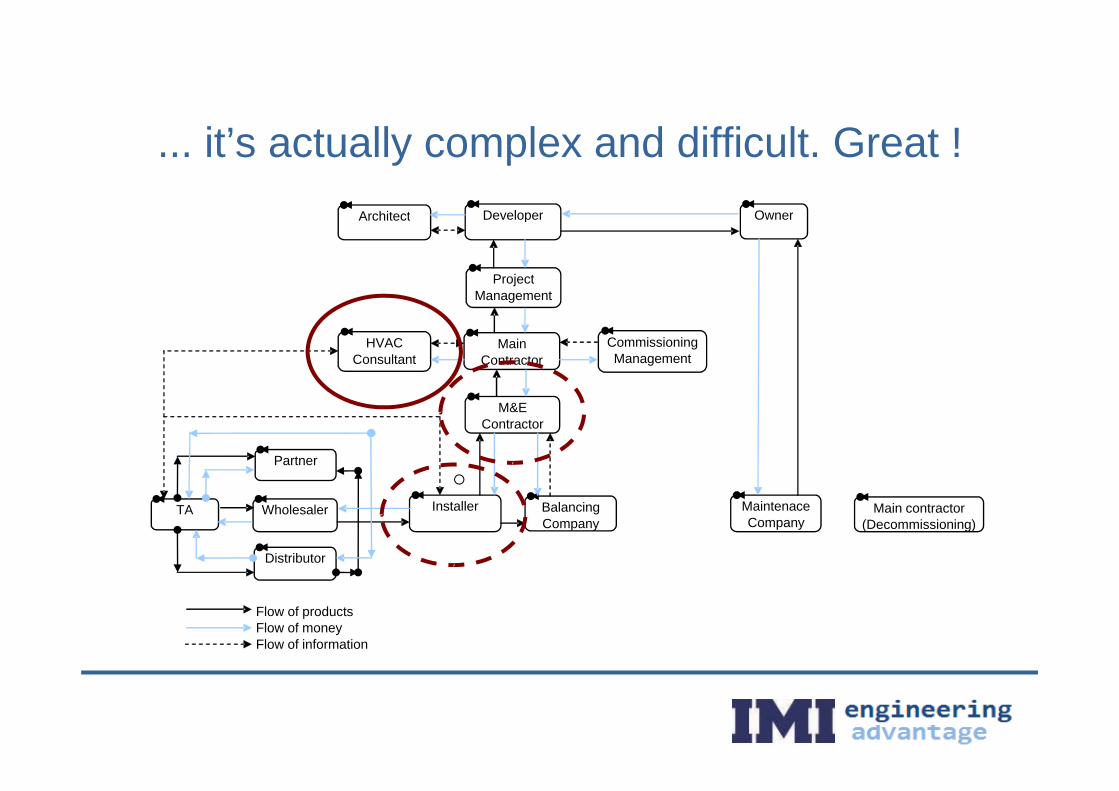

’ ff GDeveloper OwnerArchitect

... it’s actually complex and difficult. Great !

ProjectManagement

Developer OwnerArchitect

MainContractor

HVACConsultant

CommissioningManagement

Partner

M&EContractor

TA MaintenaceCompany

Main contractor(Decommissioning)

Wholesaler

Distributor

Installer BalancingCompany

Flow of products Flow of moneyFlow of information

Customer focus!Customer focus!

K i d t t f d th

Customer insight drives our strategy

• Key industry experts from around the world are invited to our regional insight councils

• Driving insight on:– Trends– New technologies– Hydronic issues/opportunities

Energy efficiency legislation– Energy efficiency legislation (EPBD)

– Renovation

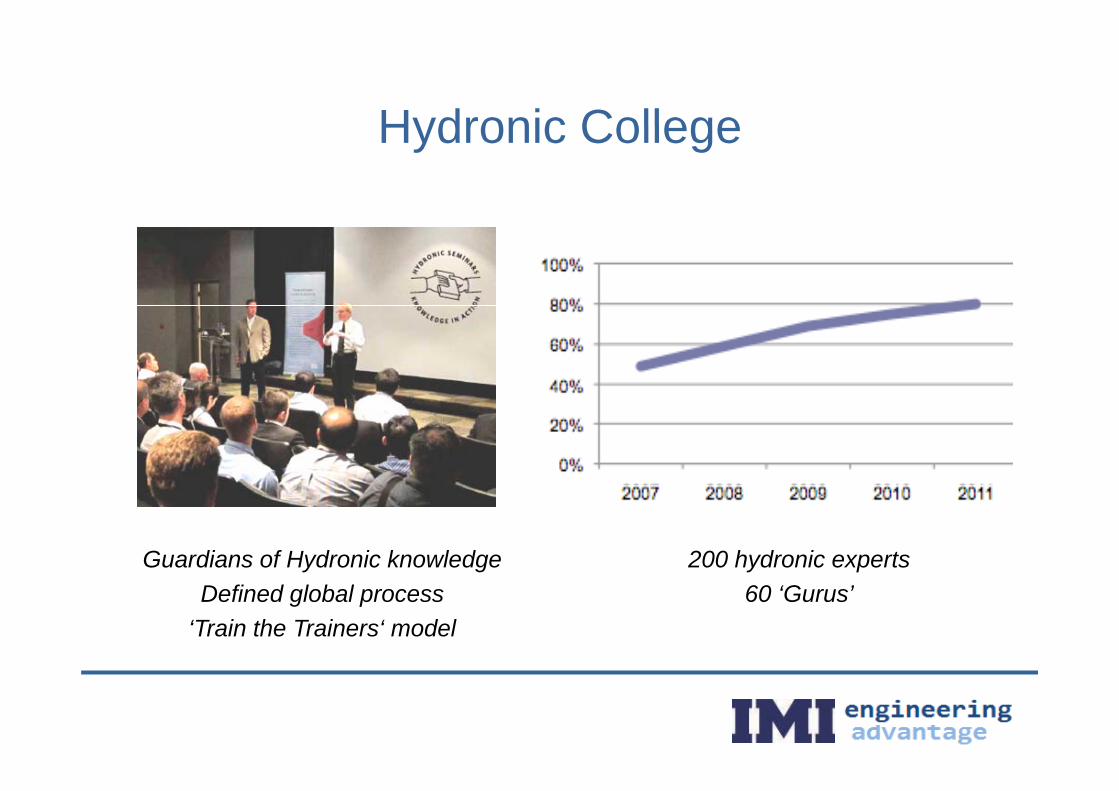

Hydronic CollegeHydronic College

Guardians of Hydronic knowledge 200 hydronic expertsDefined global process

‘Train the Trainers‘ model60 ‘Gurus’

Cid d Ad i i t ti P id t

Our solutions deliver real savingsCidade Administrativa Presidente, Brazil

21% energ sa ings achie ed21% energy savings achieved

• Strong relationship developed over 8 yearsover 8 years

• Ongoing technical support from system design to installation andsystem design to installation and system start up for over one year

Seminars designed to educateSeminars designed to educate

Vienna61 people

Shanghai150 people

Sao Paulo60 people

Dallas150 people

60,000 customers

Barcelona155 people

Tokyo59 people

Bangalore179 people

Taipei73 people

The impact of our seminarsThe impact of our seminars

“The training I received was great! I do not need product training, I can get that from the product catalogue……

Your training is about how the system works and how fluid dynamics and engineering can benefit me I don’t want my time to be wasted withand engineering can benefit me. I don t want my time to be wasted with product training and trying to sell me something. The training I received from TA is something I can put to use tomorrow”

September 2010, New York City

3. Margin Drivers

Key Account Management, Engineering Advantage, LCM

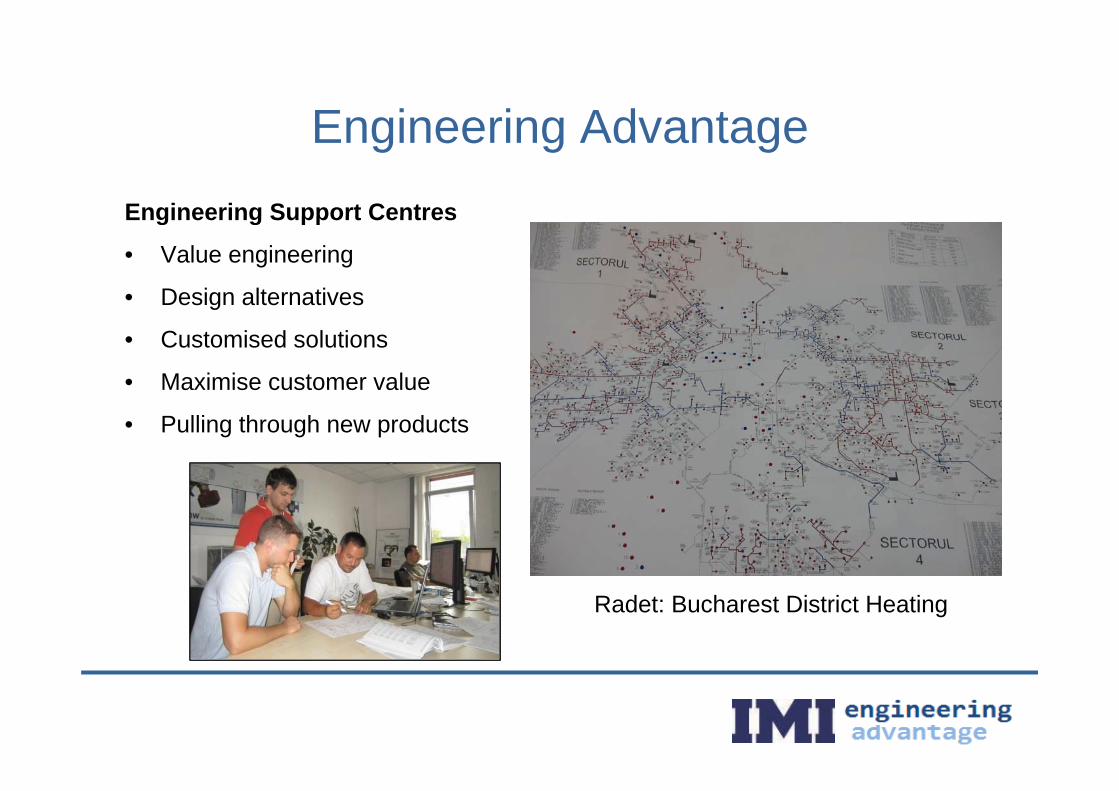

Engineering AdvantageEngineering AdvantageEngineering Support CentresEngineering Support Centres

• Value engineering

• Design alternativesg

• Customised solutions

• Maximise customer value

• Pulling through new productsMasdar City

Radet: Bucharest District Heating

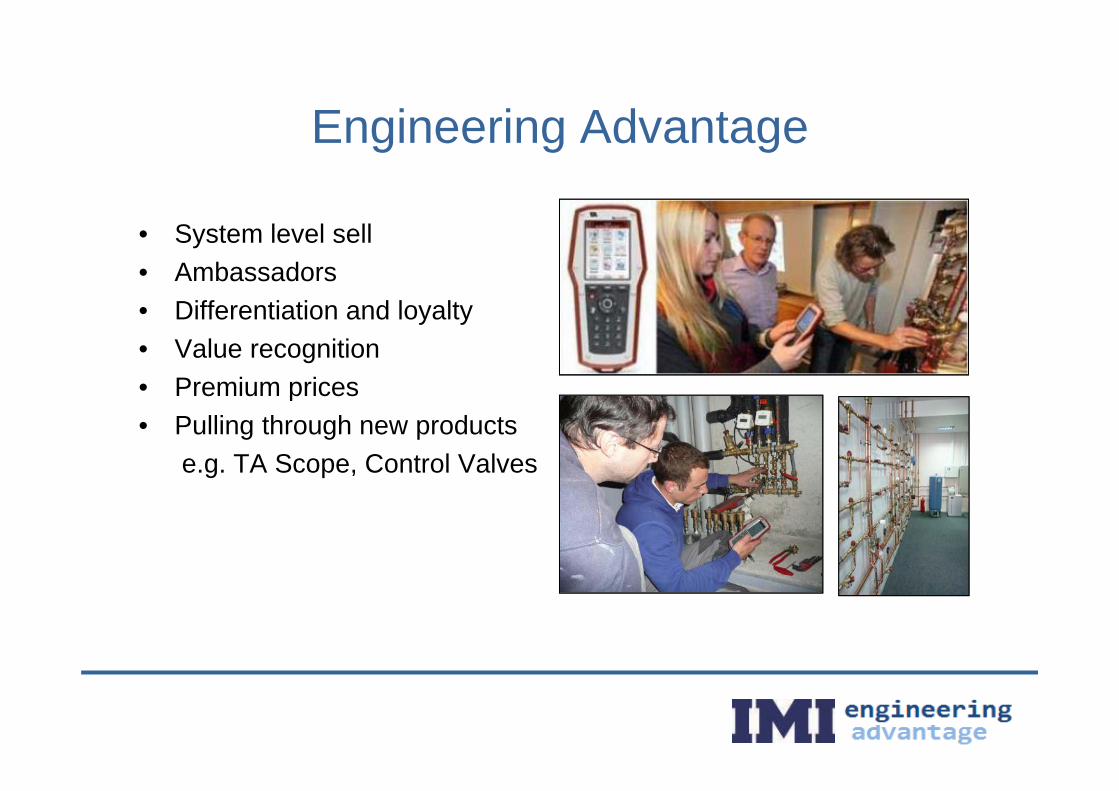

Engineering AdvantageEngineering Advantage

• System level sell• Ambassadors

Differentiation and loyalty• Differentiation and loyalty• Value recognition• Premium pricesPremium prices• Pulling through new products

e.g. TA Scope, Control Valves

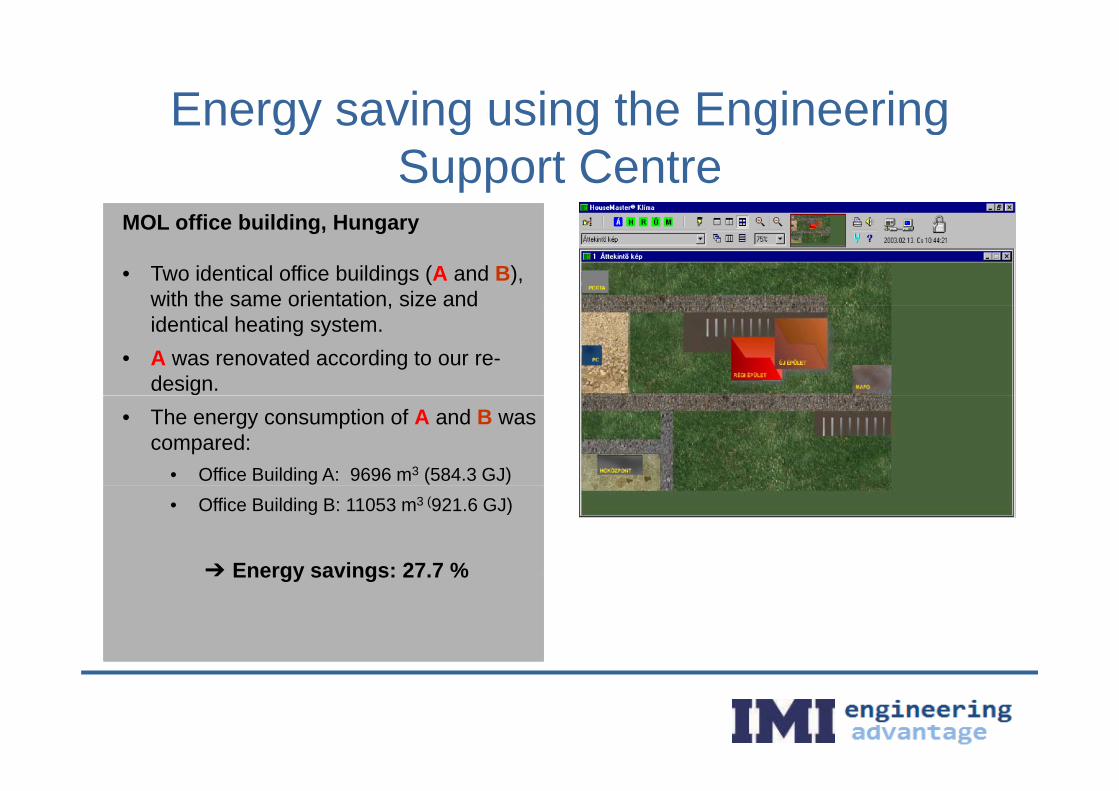

Energy saving using the Engineering

MOL ffi b ildi H

gy g g g gSupport Centre

MOL office building, Hungary

• Two identical office buildings (A and B), with the same orientation, size andwith the same orientation, size and identical heating system.

• A was renovated according to our re-design.

• The energy consumption of A and B was compared:

• Office Building A: 9696 m3 (584.3 GJ)• Office Building B: 11053 m3 (921.6 GJ)

➔ Energy savings: 27.7 %➔ Energy savings: 27.7 %

3. Margin Drivers

Key Account Management, Engineering Advantage, LCM

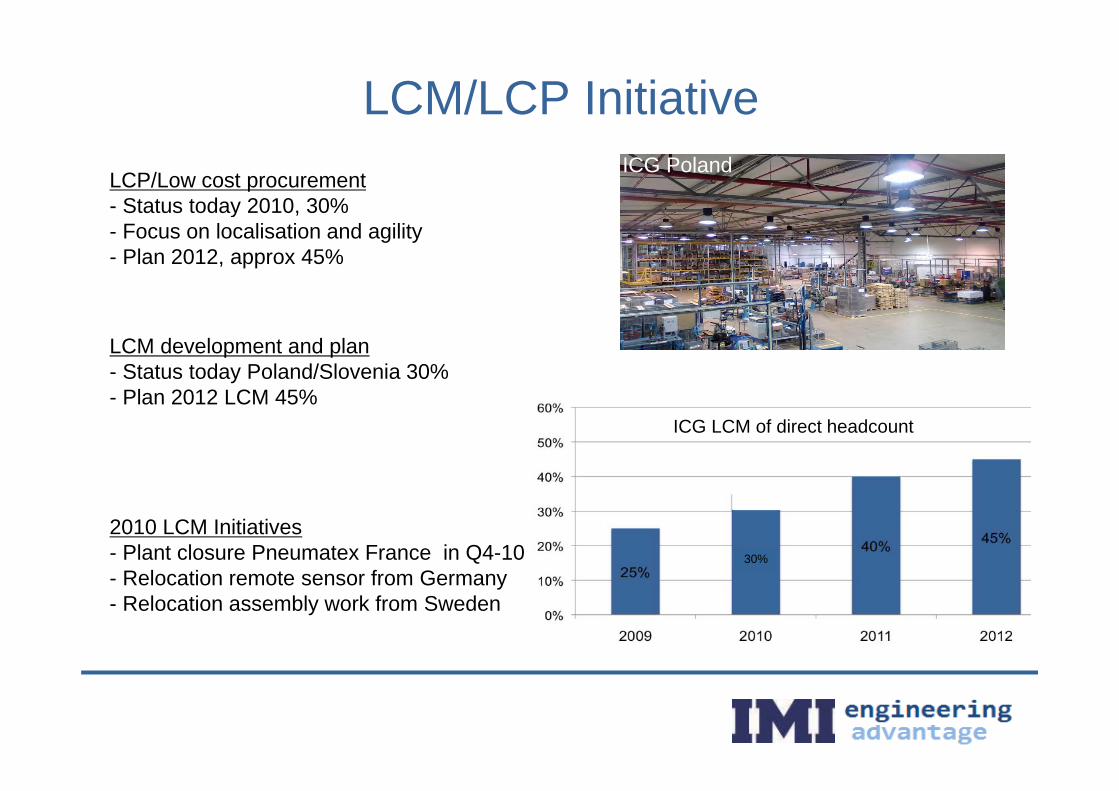

LCM/LCP InitiativeICG Poland

LCP/Low cost procurement- Status today 2010, 30%y- Focus on localisation and agility- Plan 2012, approx 45%

LCM development and plan- Status today Poland/Slovenia 30%

Plan 2012 LCM 45%- Plan 2012 LCM 45%ICG LCM of direct headcount

2010 LCM Initiatives- Plant closure Pneumatex France in Q4-10

Relocation remote sensor from Germany30%

3 529’-3 689’2011

- Relocation remote sensor from Germany- Relocation assembly work from Sweden

3 529 3 689

ICG Poland (new Pneumatex plant)

SummarySummary

1 Our Competitive Advantage1. Our Competitive Advantage

1. Growth Drivers1. Growth Drivers1. Energy Efficiency2. Emerging Markets3. New Products

2 Margin Drivers2. Margin Drivers1. Key Account Management2. Engineering Advantage3. LCM

4. Questions