IFRS - New Accounting Regulations and What They Mean to Project Managers February 25, 2009 By:...

20

IFRS - New Accounting Regulations and What They Mean to Project Managers February 25, 2009 By: SANJAY SHARMA, CA, PMP, SCPM

-

Upload

leslie-dean -

Category

Documents

-

view

213 -

download

0

Transcript of IFRS - New Accounting Regulations and What They Mean to Project Managers February 25, 2009 By:...

IFRS - New Accounting Regulations and What They Mean to Project Managers

February 25, 2009

By: SANJAY SHARMA, CA, PMP, SCPM

Page 2

2

Agenda

► Presenter’s BIO

► New Accounting Regulations - IFRS?

► IFRS Trends and Benefits

► SEC Roadmap and Timing

► Early Adoption, Comments from CFO roundtables

► Impact on Business and Specifically on IT

► IFRS and Project Management

► New Opportunities and Challenges

► Effect on IT Projects

► Relationship between Complexity and Risk

► Impact on IT applications, e.g. Oracle

► Q & A

Page 3

Presenter’s Bio – SANJAY SHARMA, CA, PMP, SCPMMobile: +1-404-423-1188 | Office: +1-732-516-4158 | [email protected]

► Senior Manager in Application Advisory Services with Ernst & Young, LLP► More than twenty years of progressive experience in financial systems design

and evaluation, program management and strategy and management consulting

► Managed multidisciplinary teams while delivering mission-critical initiatives in the financial services, healthcare, and manufacturing industries

► Successful execution and delivery of initiatives related to IT strategy and planning, ERP package evaluation and implementation, business process reengineering and custom systems development

► Strategic thinker with proven tactical execution experience in different industries and in multiple countries

► Certified Chartered Accountant (CA) from India► Certified Project Management Professional (PMP) from Project Management

Institute► Stanford Certified Project Manager (SCPM) from Stanford University

Page 4

New Accounting Regulations - IFRS?

► International Financial Reporting Standards (IFRS) are a global set of standards for financial accounting and reporting

► At a high level, the biggest difference between IFRS and US GAAP is that IFRS uses a more principles based approach and US GAAP is more prescriptive

► The International Accounting Standards Board has generally avoided issuing interpretations of its standards, leaving more of the implementation of the standards to preparers and auditors

Page 5

IFRS reporting trends

► Every major non-US capital market is moving to IFRS

► Adoption of IFRS in the EU in 2005 (8,000 companies)

► Over 100 countries around the world require or permit IFRS

► IFRS quickly picking up share of Global Fortune 500 companies

► IFRS is becoming the predominant accounting framework outside the US

Top 10 Global Capital Markets

US US GAAP – moving towards IFRS

Japan Convergence to IFRS

UK IFRS

France IFRS

Canada Convergence to IFRS

Germany IFRS

Hong Kong HKFRS (equivalent to IFRS)

Spain IFRS

Switzerland IFRS or US GAAP

Australia AIFRS (equivalent to IFRS)

207

188

29

196

264

116

0

50

100

150

200

250

300

2004 2007

US GAAP

IFRS

Other

Page 6

Benefits of IFRS

► Improved quality of reporting ► Improved transparency and investor confidence ► Reduced accounting complexity► Potential process and cost efficiencies ► Cost of capital ► Process and Technology optimization

Page 7

SEC’s proposed IFRS ‘Roadmap’

► On August 27th, 2008 the SEC issued for public comment a proposed "Roadmap" related to the eventual use of International Financial Reporting Standards (IFRS) by US companies

► The proposed Roadmap anticipates mandatory reporting under IFRS beginning in 2014, 2015 or 2016 depending on the size of the issuer and provides for early adoption in 2009 by a small number of very large companies that meet certain criteria

► It is possible that the SEC will later decide to permit early adoptions for other companies

► The roadmap also identifies several milestones that the SEC will consider in making its decision in 2011 about whether to proceed with mandatory adoption of IFRS

Page 8

Timing is critical

Fiscal2009

Restateopening

balance sheet

Firstyear of IFRS

reporting 2014

2012 and 2013 statements filedunder US standards

IFRS statements are

published withcomparatives for

2012 and 2013plus quarterly information

Fiscal2010

Fiscal2011

Fiscal2012

Fiscal2013

Fiscal2014

Run US GAAP and IFRS reporting parallel

Design and implementation of process, controls and systems

Modification of business operations, tax,regulatory and HR programs

Training

New IFRS standards

Change management, project structure and governance (budget implications, resourcing, etc.)

Awareness andknowledge of IFRS

Impact assessment

Preparation ofconversion plan

Page 9

Why consider early adoption?

► Systems: An entity that is considering systems conversion, restructuring of shared services network, etc., may want to incorporate IFRS and a new general ledger account system at the same time to reduce parallel reporting

► Organization structure: A company that already has several or significant foreign operations using IFRS may want to make reporting consistent

► Peer group: If the company’s peer group uses IFRS, even if the company is outside largest 20% of that group, they may want to adopt to be consistent with their peers

► IPO: A new public company may want to avoid a costly change from US GAAP to IFRS in the near future

Page 10

Comments from CFO Roundtables -IFRS Conversion Lessons Learned

► Management buy-in was one of the biggest initial challenges► Do not underestimate the amount of work involved► Need to limit as far as possible double reporting► Definitely not just a technical (accounting) exercise► Changes the way performance is measured and basis of incentive

schemes► Interaction with internal controls and systems is key► Increasing complexity of IFRS and speed of change is requiring

more technical resources► Has increased the volatility of results► Important to align internal and external reporting► Consider the effect on investor relations – timing and nature of

communication

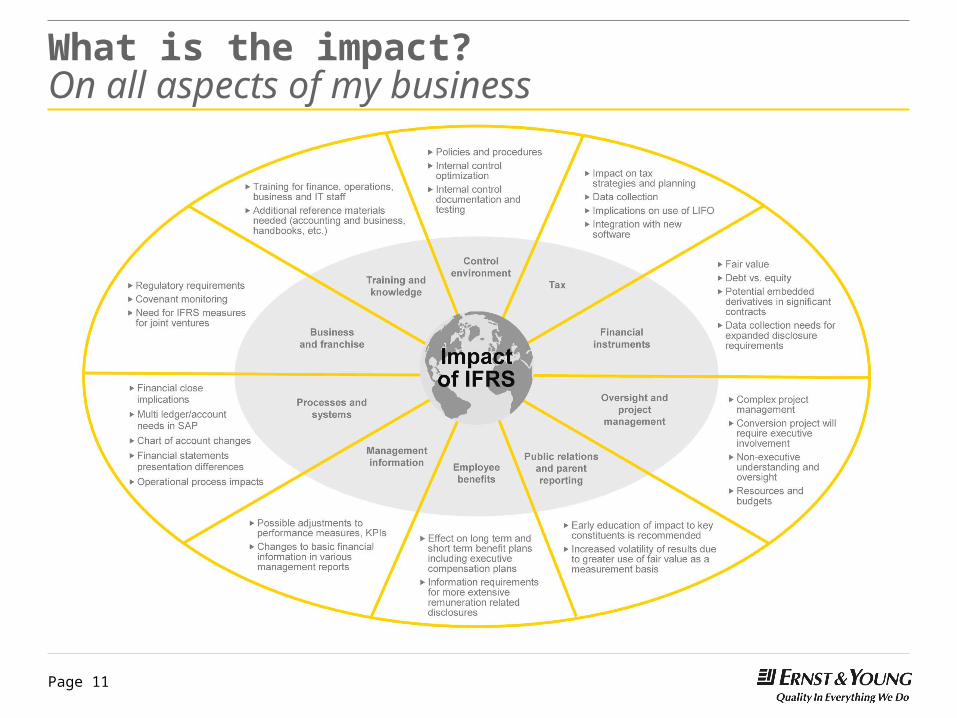

Page 11

What is the impact? On all aspects of my business

Page 12

Many areas of information technology may be impacted by IFRS. Examples include:

Applications

Reports

Data

IT Systems and Processes

Sys

tem

s A

rch

itec

ture

► What re-work is likely, do we have to upgrade?

► What about Front Office and supporting Applications?

► What changes need to be made to key reports?

► How do we identify new data sources?► What Interfaces and Middleware components

need to be updated?► What screen changes, training materials need

to happen? ► What about the historical data?► Do we need new security profiles, SOX

checks etc? ► What Infrastructure impacts does this have?

Page 13

IFRS Issues Reported by Survey Group Key Lessons Learned

Nearly 75% of respondents reported unexpected complexity of technical issues

Need to develop IFRS knowledge as early as possible to avoid last minute “fire drills” and minimize the risk of missed reporting deadlines

Unfamiliarity of numbers arising from changes Education will be a critical component of the IFRS conversion, especially for business unit heads who may not be familiar with the implications of the changes IFRS will bring. Investor relations will also need a strong educational grounding to communicate the effect to investors.

Almost 50% reported that IFRS changes were not fully embedded in back offices and general ledger systems. As a result, “stand alone manual workarounds” were created.

EU companies that used manual workarounds to meet short IFRS deadlines are now redesigning processes and augmenting their systems to eliminate the inefficiencies these workarounds created. U.S. firms will benefit from longer lead times to proactively address these changes if they start acting soon.

Top side solutions don’t work This approach fails to cause the organization to adjust, and the Finance group feels “all the pain”

'We have spent £50m on our IFRS convergence plan and our results are more difficult to interpret now than they were before…People underestimated how much work was involved, how much it would cost and the complications of interpreting financial results that have arisen as a consequence' (Barclays CFO Naguib Kheraj)

According to CA Magazine (Dec/06) almost 60% of those surveyed felt the challenge of IFRS will require the same or more effort than SOX

'We have spent £50m on our IFRS convergence plan and our results are more difficult to interpret now than they were before…People underestimated how much work was involved, how much it would cost and the complications of interpreting financial results that have arisen as a consequence' (Barclays CFO Naguib Kheraj)

According to CA Magazine (Dec/06) almost 60% of those surveyed felt the challenge of IFRS will require the same or more effort than SOX

Conversion effort is costly and complex

Source: Institute of Chartered Accountants in England & Wales

Page 14

IFRS and Project Management

► So what does this all mean to me as a Project Manager ?

Page 15

FutureFuture

► ERP Effectiveness – Increased effectiveness from new and consistent versions of the ERP, fewer instances, less complex interfaces, new product features and service-oriented architectures

► Process Effectiveness – Increased effectiveness resulting from improved financial reporting processes, single data entry for global and multiple books, consistent chart of accounts, more effective operational reporting

► Benefits – Costs reduced and benefits received by improving ERP effectiveness and improving processes in conjunction with IFRS conversion

IFRS conversion creates opportunity

Key considerations:► Ineffective processes and technology will increase the cost of your IFRS conversion efforts► Business and technology improvement opportunities should be the primary driver when planning for

conversion options. IFRS is just only one of the considerations

► Early adaptors may have the most options and find good resources at reasonable rates

Benef

its

Benef

its

Process EffectivenessProcess Effectiveness

ER

P E

ffec

tive

nes

s

Page 16

Key challenges

► Convergence between IFRS and GAAP is likely ► Manual adjustments at consolidation level will not be

sustainable. ► Organizations must capture additional data ► Parallel accounting & reporting will be required

Page 17

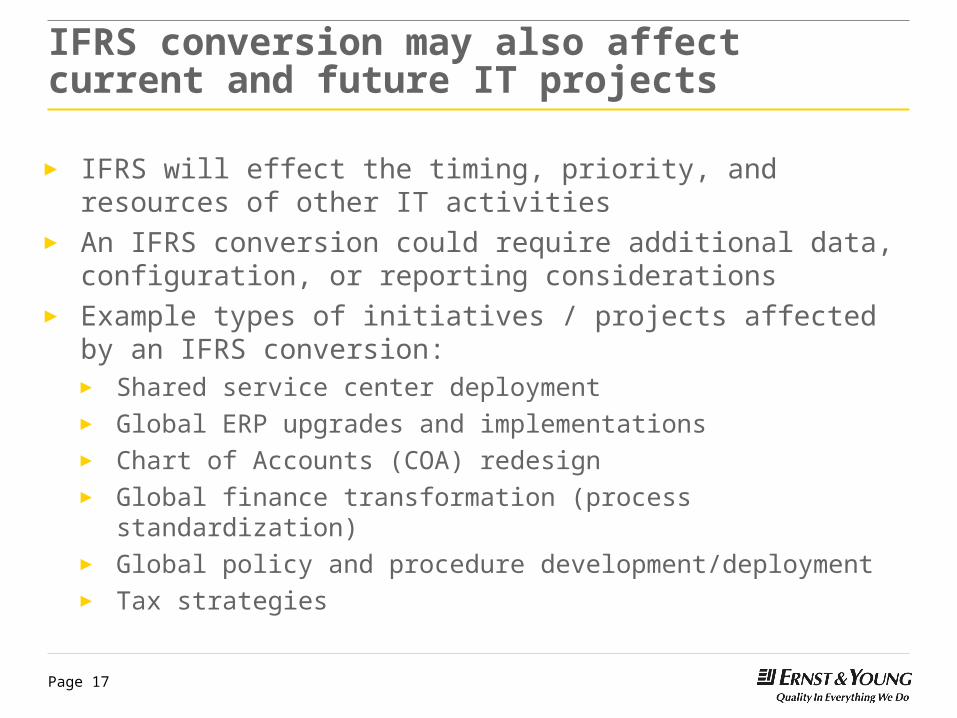

IFRS conversion may also affect current and future IT projects

► IFRS will effect the timing, priority, and resources of other IT activities

► An IFRS conversion could require additional data, configuration, or reporting considerations

► Example types of initiatives / projects affected by an IFRS conversion:► Shared service center deployment► Global ERP upgrades and implementations► Chart of Accounts (COA) redesign► Global finance transformation (process standardization)► Global policy and procedure development/deployment► Tax strategies

Page 18

Factors of Complexity: •Time•Team Size•Level of Innovation and Change•Team Maturity•Team Proximity•Number of Internal/External teams•Capability Maturity•Degree of Learning•Rapid dependent deliverables•Regulated Requirements•Environmental and Safety •Security Requirements

Risk

Complexity

Complexity is the key driver of risk

Risk as a Function ofComplexity

As the degree of COMPLEXITY

increases, so does the RISK, and hence the need for improved governance, risk

management, and program controls

Level of Program Governance Required

Relationship between Complexity and RiskComplex Projects & Programs Challenge Even Sophisticated, Experienced Organizations

Page 19

Representative impact of IFRS on anOracle applications

Minimal Moderate SignificantNone

Oracle Product Oracle Module

Financials

Manufacturing – Discrete

Projects

Human Resources

Projects Costing Resource Management Project Management Project Contracts

General Ledger Fixed Assets Accts. Receivable Accts. Payable E-Business TaxFinl Consoldtn.

Hub Cash

Management

Supply Chain Plng. & Procurement

Bills Of Material CapacityQuality

ImplementationEngineering Work In Progress

Maintenance & Service

Purchasing Inventory

ManagementDemand Planning iProcurement

iSupplier Portal

SourcingAdv. Supply Chain Plng.

Time & Labor Payroll Learning Management Advanced Benefits

Enterprise Asset Management

Spares Management

Order ManagementOrder

ManagementAdvanced Pricing Configurator Release Management

Marketing & Sales MarketingTrade

ManagementQuoting Proposals Incentive Compensation

Projects Billing

Manufacturing – Process

Process Plng.Quality

ManagementRegulatory

Management

Cost Management Scheduling

Cost Management Process Execution Product Dev.

Tele Service Service Contracts Field Service Adv Scheduler

Shipping Sales Contracts iStore

TeleSalesAdvanced

PricingPartner

Management

Page 20

Question / Answer

Q & A