Hotels UK Staycations 2021: A Year of Opportunities

18

Hotels UK Staycations 2021: A Year of Opportunities

Transcript of Hotels UK Staycations 2021: A Year of Opportunities

Hotels

UK Staycations2021: A Year of Opportunities

Contents

01

02

03

04

05

06

The Staycation Opportunity in the UK

Household Savings to Fuel Recovery

Hotel Performance in 2020

Looking Forward: Hotel Performance Trends in 2021

Alternative Accommodation in the UK

Investment Trends

Colliers | UK Staycations 2021 | 2

The Staycation Opportunity in the UK01.

Colliers | UK Staycations 2021 | 3

Staycations to dominate the UK hospitality sector

A Staycation surge is expected in 2021 across the UK due to ongoing international travel restrictions and successful domestic vaccine rollouts. This presents a promising opportunity for UK hoteliers to attract people who would previously have chosen to travel abroad for holidays and weekend breaks.

Summary of Supporting Data

The Staycation Opportunity in the UK

Over 50% of UK travellers are expected to take fewer overseas trips in 2021 according to a VisitBritain survey from October 2020.

Domestic travel received 70% of hotel clicks on TripAdvisor in January 2021, where the summer months proved to be the most popular for bookings.

VisitBritain predicts a recovery of £61.7 billion in domestic tourism spend in 2021, up by a staggering 79% compared to 2020.

VisitBritain’s October 2020 survey also suggested a 33% increase in domestic interest in short stay UK breaks, compared to 2020.

Airbnb reported bookings in the USA beat pre-pandemic levels in Q1 of 2021 as lockdown eased nationwide. Booking values jumped 52% (to $10.3bn) and holiday booking for families outpaced smaller groups and solo travellers. This unprecedented rebound in travel is a strong indicator for the UK, as we emerge out of lockdown.

Colliers | UK Staycations 2021 | 4

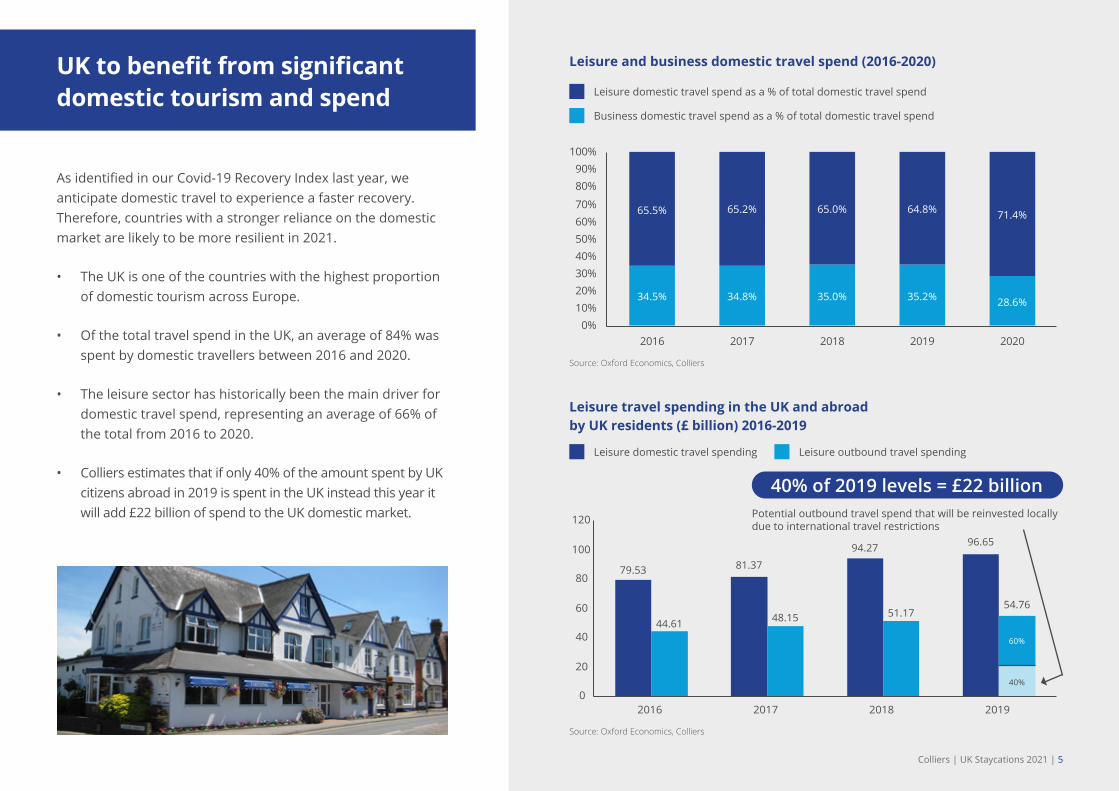

UK to benefit from significant domestic tourism and spend

As identified in our Covid-19 Recovery Index last year, we anticipate domestic travel to experience a faster recovery. Therefore, countries with a stronger reliance on the domestic market are likely to be more resilient in 2021.

• The UK is one of the countries with the highest proportion of domestic tourism across Europe.

• Of the total travel spend in the UK, an average of 84% was spent by domestic travellers between 2016 and 2020.

• The leisure sector has historically been the main driver for domestic travel spend, representing an average of 66% of the total from 2016 to 2020.

• Colliers estimates that if only 40% of the amount spent by UK citizens abroad in 2019 is spent in the UK instead this year it will add £22 billion of spend to the UK domestic market.

34.5% 34.8% 35.0% 35.2% 28.6%

65.5% 65.2% 65.0% 64.8% 71.4%

0%10%20%30%40%50%60%70%

80%90%

100%

2016 2017 2018 2019 2020

79.53 81.37

94.27 96.65

44.61 48.15 51.1754.76

60%

40%

0

20

40

60

80

100

120

2016 2017 2018 2019

Leisure and business domestic travel spend (2016-2020)

Leisure travel spending in the UK and abroad by UK residents (£ billion) 2016-2019

Leisure domestic travel spend as a % of total domestic travel spend

Leisure domestic travel spending

Potential outbound travel spend that will be reinvested locally due to international travel restrictions

Source: Oxford Economics, Colliers

Source: Oxford Economics, Colliers

Leisure outbound travel spending

Business domestic travel spend as a % of total domestic travel spend

40% of 2019 levels = £22 billion

Colliers | UK Staycations 2021 | 5

Household Savings to Fuel Recovery02.

Colliers | UK Staycations 2021 | 6

Savings across the UK increased in 2020

• According to Oxford Economics, the multiple national lockdowns across the UK have produced excess accumulated savings in 2020, equivalent to 12% of the UK’s GDP.

• This is good news for the recovery of the UK economy, as household savings will be a key driver for consumer expansion in the latter half of 2021.

• UK household savings increased by approximately £140 billion during 2020, up a staggering 141% from 2019 levels.

How will this benefit the hotel sector?

In 2019, the highest income earners spent an average of 14.5% of their income on recreation and culture, and a further 10% on restaurants and hotels. We believe this trend will continue in 2021 and that it will result in an increased interest in upscale and luxury accommodation during the year.

We predict an increase in spending within hotels in the form of room upgrades and more expensive meals. Some guests will also be looking for additional recreational experiences during their travels and are therefore likely to spend more on extra services such as spa treatments, afternoon teas and other activities.

All these factors should help hoteliers enhance their revenues by allowing them to increase their Average Daily Rate (ADR), while occupancy levels remain relatively low. In fact, we are already seeing that in some leisure hotels, ADR levels are ahead of 2019 figures.

Source: Oxford Economics, Colliers

£106.9

£80.6£90.2 £98.9

£238.8

141%

7.6%5.7% 6.1% 6.5%

15.8%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

2016 2017 2018 2019 2020

UK Savings, personal sector (ratio and values in billion) 2016 - 2020

Colliers | UK Staycations 2021 | 7

Hotel Performance in 202003.

Colliers | UK Staycations 2021 | 8

Seaside destinations topped the charts whilst urban city centre locations suffered

As we anticipated in our Covid-19 Recovery Index published in July 2020, hotels situated in coastal and leisure destinations across the UK performed better in 2020 when compared to regions such as London and Edinburgh, which have traditionally relied heavily on overseas tourism, corporate demand and the Meetings, Incentives, Conferences and Exhibitions (MICE) sector. This was a direct result of the Staycation effect, which dominated the hospitality sector last year during the brief periods when hotels were open to the general public.

• The top markets experienced a RevPAR decline well below the UK average of 66%, from July – October 2020.

• In contrast, the bottom markets performed much worse than the UK average. Hotel markets such as London, Edinburgh, Manchester and Glasgow, which traditionally rely on international, corporate and MICE demand, suffered greater declines due to the pandemic and its associated restrictions.

However, now that we look ahead into 2021, we can see new trends emerging...

-10.1-13.4

-19.6

-25.8 -27.4

-70.0

-60.0

-50.0

-40.0

-30.0

-20.0

-10.0

0.0

Bournemouth

UK average = -66.2

Eastbourne Plymouth Norwich Brighton

Top 5 Markets - YoY % change in RevPAR (Average July - October 2020)

-68.4 -70.3

UK average = -66.2

-73.0-76.7

-83.0-90.0

-80.0

-70.0

-60.0

-50.0

-40.0

-30.0

-20.0

-10.0

0.0

Birmingham Manchester Glasgow Edinburgh London

Bottom 5 Markets - YoY % change in RevPAR (Average July - October 2020)

Source: STR. 2021 © CoStar Realty Information, Inc, Colliers Note: We have analysed the period between July and October 2020 as these are the months when hotels were open from the end of the first national lockdown to the start of the second national lockdown in the UK.

Colliers | UK Staycations 2021 | 9

Looking Forward: Hotel Performance Trends in 2021

04.

Colliers | UK Staycations 2021 | 10

Looking ahead at 2021 - City breaks to be a popular option

• Leisure hotels located in rural and seaside destinations (Coast & Country) will remain a popular option for domestic tourism and will once again experience high volumes of demand this summer. Nevertheless, we are optimistic that some city centre locations are also likely to benefit from the Staycation market this year.

• Due to the successful vaccination program in the UK and the reopening of amenities that were closed in 2020, such as restaurants, bars, museums, theatres and sporting events, we envisage many travellers will soon opt for domestic city breaks. London, Edinburgh, Manchester, Liverpool and many other cities in the UK will serve as popular alternatives for holidaymakers.

• Business travel is also predicted to return faster than many anticipate and will boost visitor numbers for cities across the UK. People are starting to request physical travel and meetings for business in the second half of 2021, as people are returning to the office and closer to ‘normal life’, at least domestically.

• The Colliers Hospitality Asset Management team (which monitors more than 5,000 rooms on behalf of hotel owners) is seeing strong pick-up in demand for weddings and social events as well as deferred business meetings - particularly from the end of Q3 and into Q4 for 2021.

• Additionally, we believe that December, which is typically an important banqueting month for hotels, will this year achieve similar levels to those of December 2019. We predict this Christmas season will be a bumper period for hotels with large event spaces.

• VisitBritain has adjusted its marketing approach due to the effects of Covid-19. One of its main marketing initiatives for 2021 is the domestic marketing campaign “Escape The Everyday.” This £5 million campaign will focus on inspiring consumers to “book a short break across the UK by showcasing the breadth of experiences available for them to escape to”. The campaign will promote both UK city destinations as well as countryside and coastal locations.

The national tourism campaign aligns with our findings and view that recovery in the UK’s travel and tourism sector during 2021 will be driven by Staycations in both regional and city centre destinations.

Colliers | UK Staycations 2021 | 11

Initiatives to revive city tourism and other major events in 2021

Looking back at the bottom performers in 2020, these cities are now taking additional measures to attract domestic visitors during 2021 in the hope of replacing the loss of some international tourism. These are all cities that have historically been events driven markets for visitation and have also been greatly reliant on international travellers. As a consequence, they have seen the largest decrease in RevPAR during the pandemic.

Visitor attractions in major cities include:

London - Hotel Week in May-June with a variety of deals. The Vincent van Gogh exhibition at Kensington Gardens. Al fresco dining in more than 60 central London streets. London is also going ahead with major events like London Fashion week, Royal Ascot and Wimbledon.

Edinburgh - International Children’s Festival in June and Edinburgh International Festival in August.

Manchester - Created a 400-seat outdoor theatre called Homeground in May and Visit Manchester is running the ‘Have a Night on Us’ hotel promotion.

Glasgow – Hosting the UN Climate Change Conference in November and Glasgow film festival.

Colliers | UK Staycations 2021 | 12

Cities with further opportunity for Staycation demand in 2021

Cities with continued demand for Staycations in 2021

Staycation Demand in 2021 throughout the UK

In this map we highlight those destinations which Colliers believes will continue to show strong Staycation demand during 2021. We also predict other locations which we believe will see a boost during 2021 from Staycation travellers.

Glasgow Edinburgh

York

Manchester

London

Cambridge

Liverpool

Blackpool

Bristol

Southampton

Plymouth

Bournemouth

Bath

Stratford upon Avon

Eastbourne

Brighton

Norwich

Colliers | UK Staycations 2021 | 13

Alternative Accommodation in the UK

05.

Colliers | UK Staycations 2021 | 14

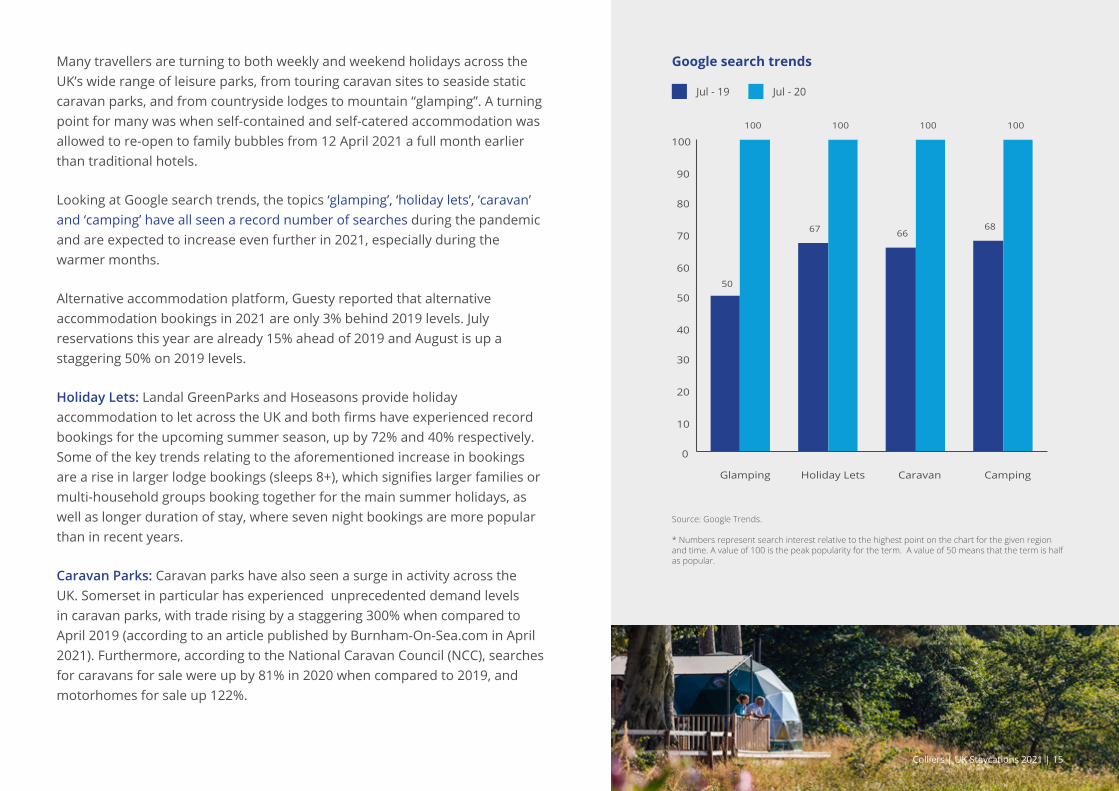

Many travellers are turning to both weekly and weekend holidays across the UK’s wide range of leisure parks, from touring caravan sites to seaside static caravan parks, and from countryside lodges to mountain “glamping”. A turning point for many was when self-contained and self-catered accommodation was allowed to re-open to family bubbles from 12 April 2021 a full month earlier than traditional hotels.

Looking at Google search trends, the topics ‘glamping’, ‘holiday lets’, ‘caravan’ and ‘camping’ have all seen a record number of searches during the pandemic and are expected to increase even further in 2021, especially during the warmer months.

Alternative accommodation platform, Guesty reported that alternative accommodation bookings in 2021 are only 3% behind 2019 levels. July reservations this year are already 15% ahead of 2019 and August is up a staggering 50% on 2019 levels.

Holiday Lets: Landal GreenParks and Hoseasons provide holiday accommodation to let across the UK and both firms have experienced record bookings for the upcoming summer season, up by 72% and 40% respectively. Some of the key trends relating to the aforementioned increase in bookings are a rise in larger lodge bookings (sleeps 8+), which signifies larger families or multi-household groups booking together for the main summer holidays, as well as longer duration of stay, where seven night bookings are more popular than in recent years.

Caravan Parks: Caravan parks have also seen a surge in activity across the UK. Somerset in particular has experienced unprecedented demand levels in caravan parks, with trade rising by a staggering 300% when compared to April 2019 (according to an article published by Burnham-On-Sea.com in April 2021). Furthermore, according to the National Caravan Council (NCC), searches for caravans for sale were up by 81% in 2020 when compared to 2019, and motorhomes for sale up 122%.

50

67 6668

100 100 100 100

0

10

20

30

40

50

60

70

80

90

100

Glamping Holiday Lets Caravan Camping

Google search trends

Jul - 19 Jul - 20

Source: Google Trends. * Numbers represent search interest relative to the highest point on the chart for the given region and time. A value of 100 is the peak popularity for the term. A value of 50 means that the term is half as popular.

Colliers | UK Staycations 2021 | 15

Investment Trends06.

Colliers | UK Staycations 2021 | 16

UK hotel investment declined by 70% in 2020, and the vast majority of the transaction volume occurred during the first quarter. However, there has been a notable increase in sale volumes of hotels in Q1 2021.

• Opportunistic capital has been raised to target distressed hotel real estate in the past year.

• This capital is now targeting markets where there is a quicker recovery, and for many investors, the UK Staycation market is an attractive option.

• Judging by the experience of the Colliers UK Hotels Agency team, who sold 48 UK hotels in 2020, guests are set to return to hotels and transactional activity will increase correspondingly.

• The maturity and resilience of the UK hotel sector coupled with strong domestic tourism contribute to ongoing investor demand.

Substantial uplift

Transactional activity is building, and we have already seen a substantial uplift in enquiries and viewings this year, with the volume of formal viewings up 44% for the first two weeks of March, compared with the same period of the previous month.

At Colliers, we have had an increasing flow of opportunistic buyers contacting us, many from overseas, with strongest interest being expressed in hotels in Staycation locations. It is very clear that there are still numerous well-heeled cash buyers out there, as well as prospective purchasers with support from their banks.

In addition to those seeking to buy hotels, we have observed an increase in alternative use enquiries for lower profit hotels that could receive planning consent for change of use. Our experience of alternative use sales at Colliers last year included residential, educational, self-catering, nursing and care homes, retirement development, and rehabilitation centres.

0

0.5

1

1.5

2

2.5

Q1 2018 Q2 2018 Q3 2018 Q4 2018 Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 Q2 2020 Q3 2020 Q4 2020 Q1 2021

UK average = £1.4bn per quarter

Total Hotel Transaction Volumes in the UK (£ billion), Q1 2018 - Q1 2021

Source: Real Capital Analytics (RCA), Colliers Note: Based on available transactional data from RCA

Colliers | UK Staycations 2021 | 17

Colliers is the licensed trading name of Colliers International Property Advisers UK LLP which is a limited liability partnership registered in England and Wales with registered number OC385143. Our registered office is at 50 George Street, London W1U 7GA. 21181

50 George StreetLondon W1U 7GAcolliers.com

Marc FinneyHead of Hotels & Resorts Consulting+44 7825 602 [email protected]

Ben GodonHead of Hospitality Asset Management+44 7920 501 [email protected]

Julian TroupHead of UK Hotels Agency+44 7825 891 [email protected]

David HossackHead of UK Hotels - Valuation+44 7919 015 [email protected]

Siddhika ShahAssociate Director, Hotels & Resorts Consulting+44 7717 863 [email protected]

Anette BlystadConsultant, Hotels & Resorts Consulting+44 7842 602 [email protected]

Robert SmithsonSenior Surveyor, Hotels Agency+44 7825 171 652 [email protected]

Contact Us