HIGHLIGHTS OF CYPRUS TAX SYSTEM TAX BENEFITS …€¦ · HIGHLIGHTS OF CYPRUS TAX SYSTEM & TAX...

22

HIGHLIGHTS OF CYPRUS TAX SYSTEM & TAX BENEFITS FOR THE NON DOMICILE CYPRUS TAX RESIDENTS By Marios Efthymiou Managing Director

Transcript of HIGHLIGHTS OF CYPRUS TAX SYSTEM TAX BENEFITS …€¦ · HIGHLIGHTS OF CYPRUS TAX SYSTEM & TAX...

HIGHLIGHTS OF CYPRUS TAX

SYSTEM

&

TAX BENEFITS FOR THE NON

DOMICILE CYPRUS TAX RESIDENTS

By Marios Efthymiou

Managing Director

WORLDWIDE TAX RATES

• Tax rates vary between tax jurisdictions

STARTING FROM ……………. 0%

………. ENDING UP TO ………40%…..50% ……???

TWO TYPE OF TAXES

•CORPORATE TAX

• INDIVIDUAL TAX

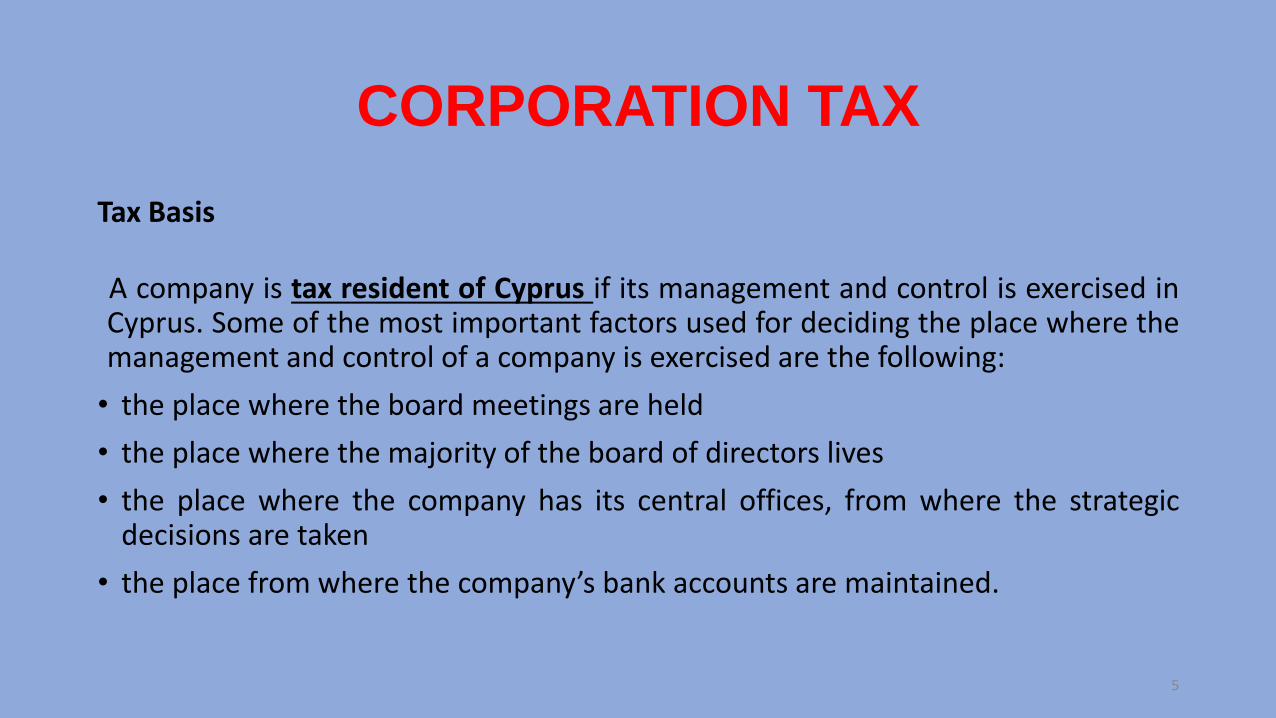

Tax Basis

A company is tax resident of Cyprus if its management and control is exercised inCyprus. Some of the most important factors used for deciding the place where themanagement and control of a company is exercised are the following:

• the place where the board meetings are held

• the place where the majority of the board of directors lives

• the place where the company has its central offices, from where the strategicdecisions are taken

• the place from where the company’s bank accounts are maintained.

CORPORATION TAX

5

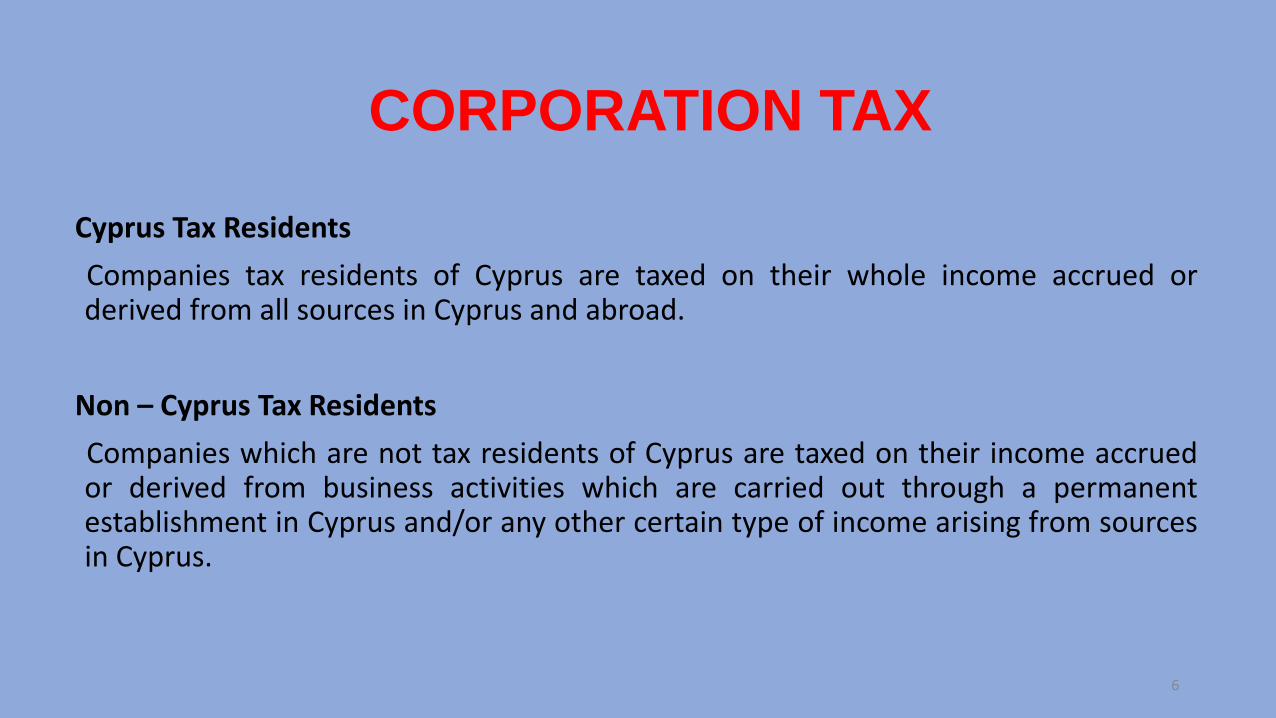

Cyprus Tax Residents

Companies tax residents of Cyprus are taxed on their whole income accrued orderived from all sources in Cyprus and abroad.

Non – Cyprus Tax Residents

Companies which are not tax residents of Cyprus are taxed on their income accruedor derived from business activities which are carried out through a permanentestablishment in Cyprus and/or any other certain type of income arising from sourcesin Cyprus.

CORPORATION TAX

6

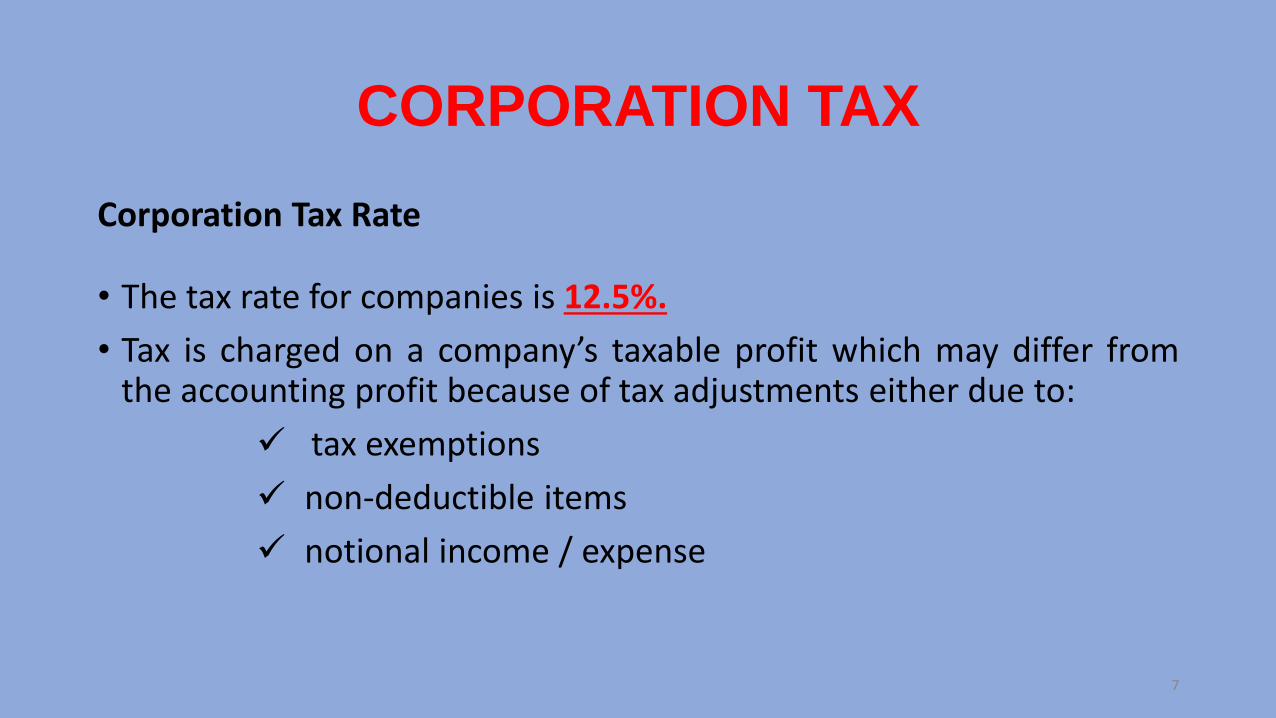

Corporation Tax Rate

• The tax rate for companies is 12.5%.

• Tax is charged on a company’s taxable profit which may differ fromthe accounting profit because of tax adjustments either due to:

✓ tax exemptions

✓ non-deductible items

✓ notional income / expense

CORPORATION TAX

7

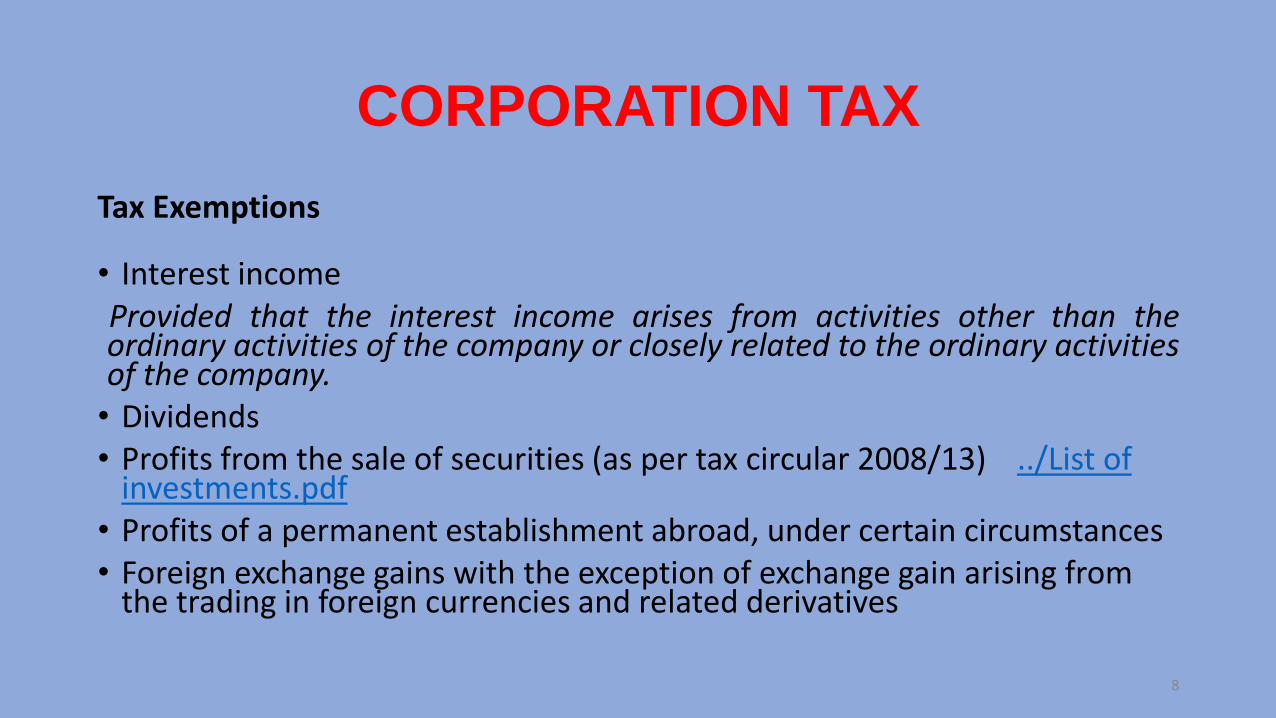

Tax Exemptions

• Interest incomeProvided that the interest income arises from activities other than theordinary activities of the company or closely related to the ordinary activitiesof the company.• Dividends • Profits from the sale of securities (as per tax circular 2008/13) ../List of

investments.pdf• Profits of a permanent establishment abroad, under certain circumstances• Foreign exchange gains with the exception of exchange gain arising from

the trading in foreign currencies and related derivatives

CORPORATION TAX

8

• Special contribution for defence is charged on incomeearned by Cyprus tax residents only (physical persons andlegal entities).

• Non-residents are not subject to the defence contribution.

This includes both non-tax residents as well as taxresidents who are non-domiciled.

9

DEFENCE TAX

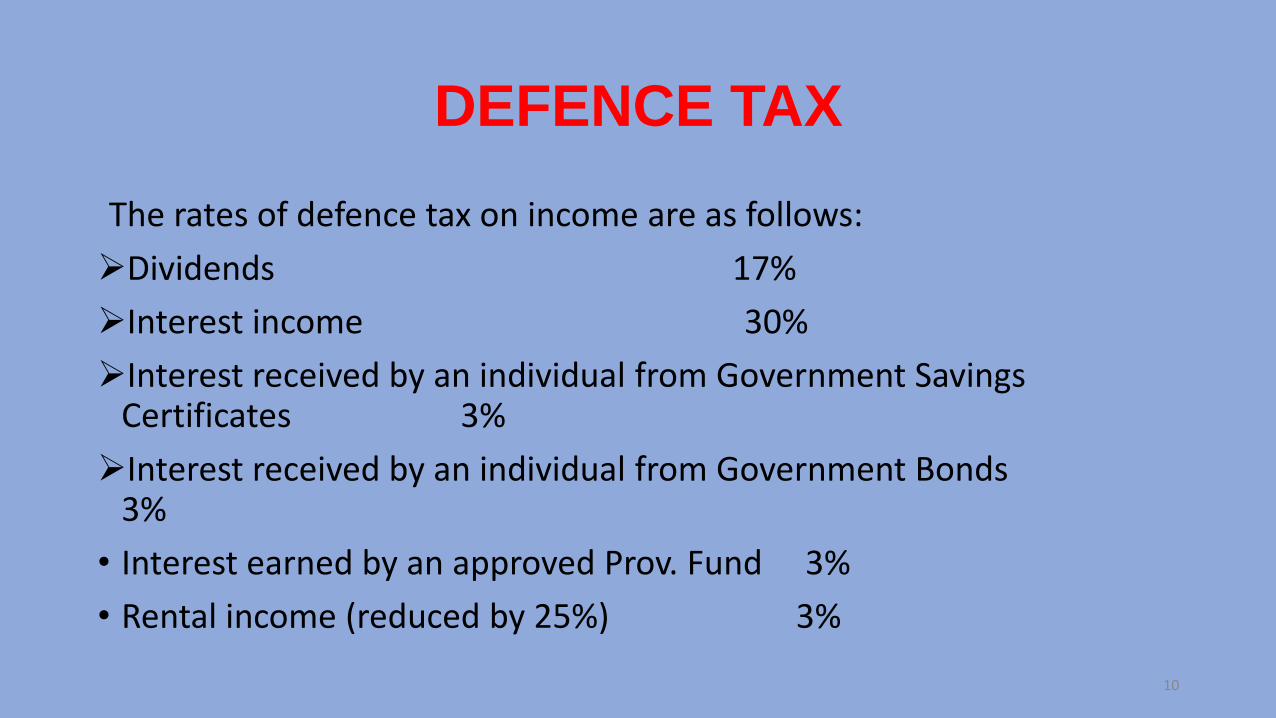

The rates of defence tax on income are as follows:

➢Dividends 17%

➢Interest income 30%

➢Interest received by an individual from Government Savings Certificates 3%

➢Interest received by an individual from Government Bonds 3%

• Interest earned by an approved Prov. Fund 3%

• Rental income (reduced by 25%) 3%

10

DEFENCE TAX

PHYSICAL PERSONS

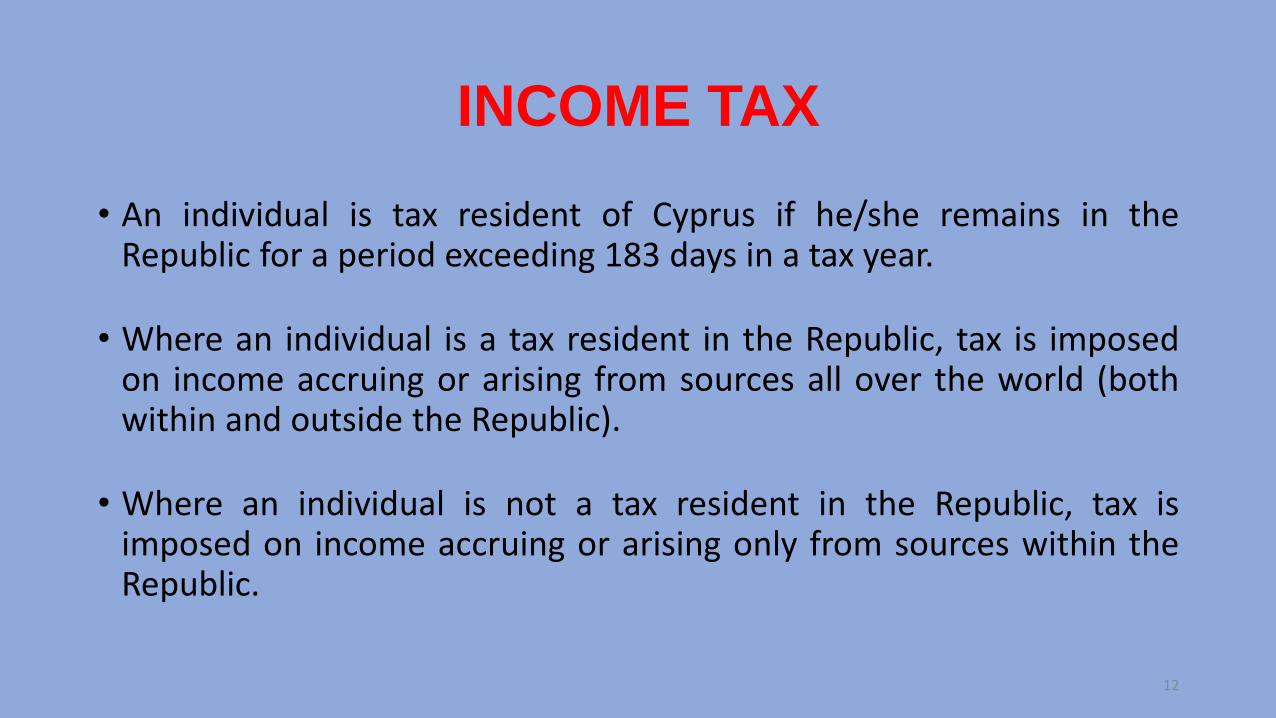

• An individual is tax resident of Cyprus if he/she remains in theRepublic for a period exceeding 183 days in a tax year.

• Where an individual is a tax resident in the Republic, tax is imposedon income accruing or arising from sources all over the world (bothwithin and outside the Republic).

• Where an individual is not a tax resident in the Republic, tax isimposed on income accruing or arising only from sources within theRepublic.

12

INCOME TAX

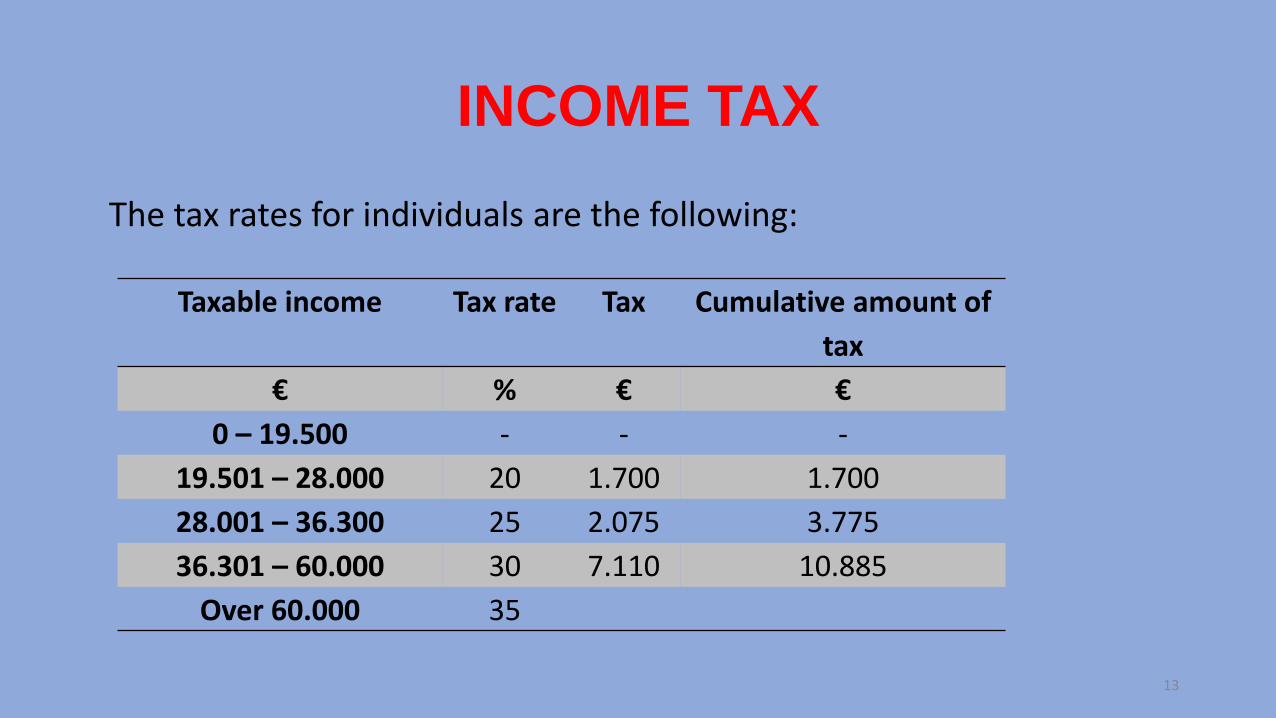

The tax rates for individuals are the following:

13

INCOME TAX

Taxable income Tax rate Tax Cumulative amount of

tax

€ % € €

0 – 19.500 - - -

19.501 – 28.000 20 1.700 1.700

28.001 – 36.300 25 2.075 3.775

36.301 – 60.000 30 7.110 10.885

Over 60.000 35

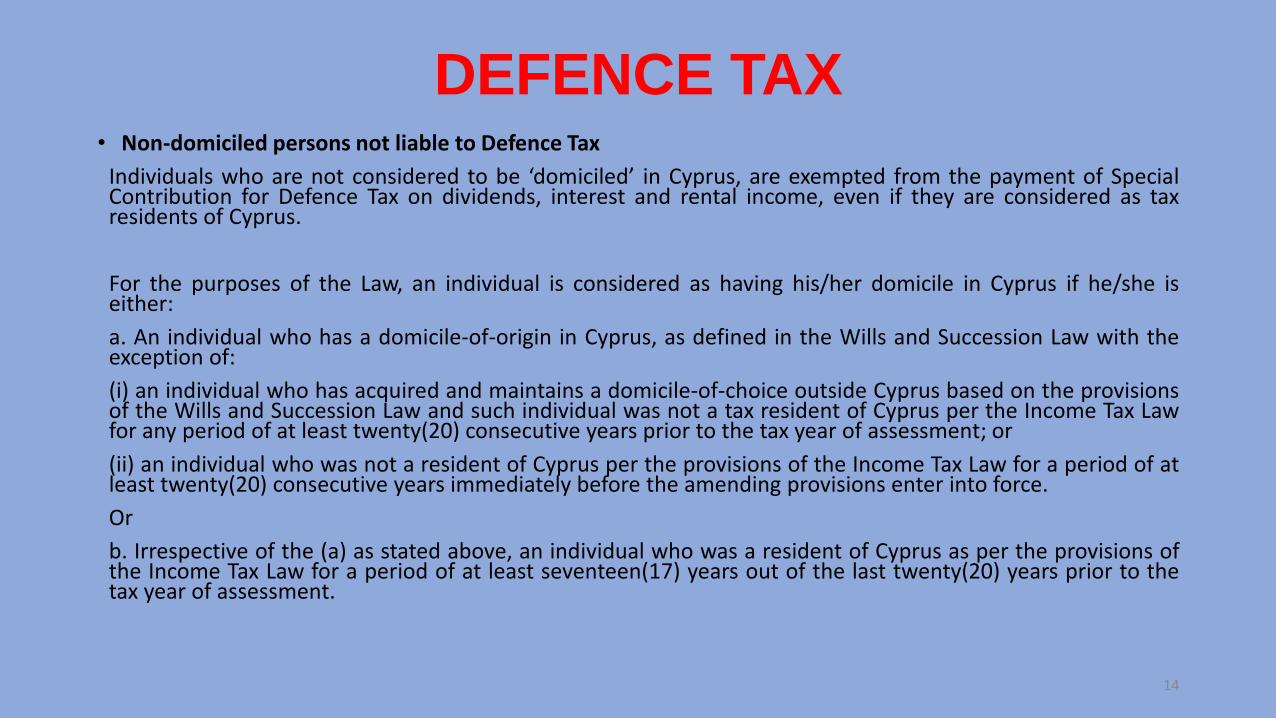

• Non-domiciled persons not liable to Defence Tax

Individuals who are not considered to be ‘domiciled’ in Cyprus, are exempted from the payment of SpecialContribution for Defence Tax on dividends, interest and rental income, even if they are considered as taxresidents of Cyprus.

For the purposes of the Law, an individual is considered as having his/her domicile in Cyprus if he/she iseither:

a. An individual who has a domicile-of-origin in Cyprus, as defined in the Wills and Succession Law with theexception of:

(i) an individual who has acquired and maintains a domicile-of-choice outside Cyprus based on the provisionsof the Wills and Succession Law and such individual was not a tax resident of Cyprus per the Income Tax Lawfor any period of at least twenty(20) consecutive years prior to the tax year of assessment; or

(ii) an individual who was not a resident of Cyprus per the provisions of the Income Tax Law for a period of atleast twenty(20) consecutive years immediately before the amending provisions enter into force.

Or

b. Irrespective of the (a) as stated above, an individual who was a resident of Cyprus as per the provisions ofthe Income Tax Law for a period of at least seventeen(17) years out of the last twenty(20) years prior to thetax year of assessment.

14

DEFENCE TAX

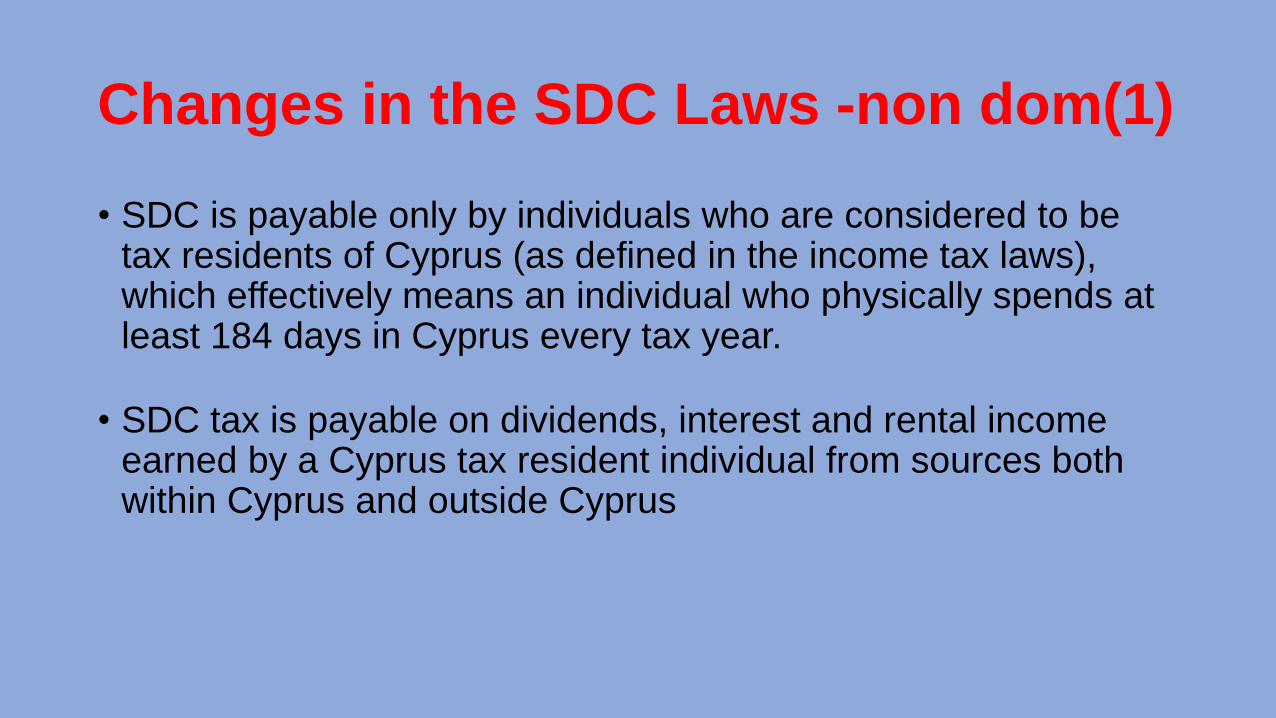

Changes in the SDC Laws -non dom(1)

• SDC is payable only by individuals who are considered to be tax residents of Cyprus (as defined in the income tax laws), which effectively means an individual who physically spends at least 184 days in Cyprus every tax year.

• SDC tax is payable on dividends, interest and rental income earned by a Cyprus tax resident individual from sources both within Cyprus and outside Cyprus

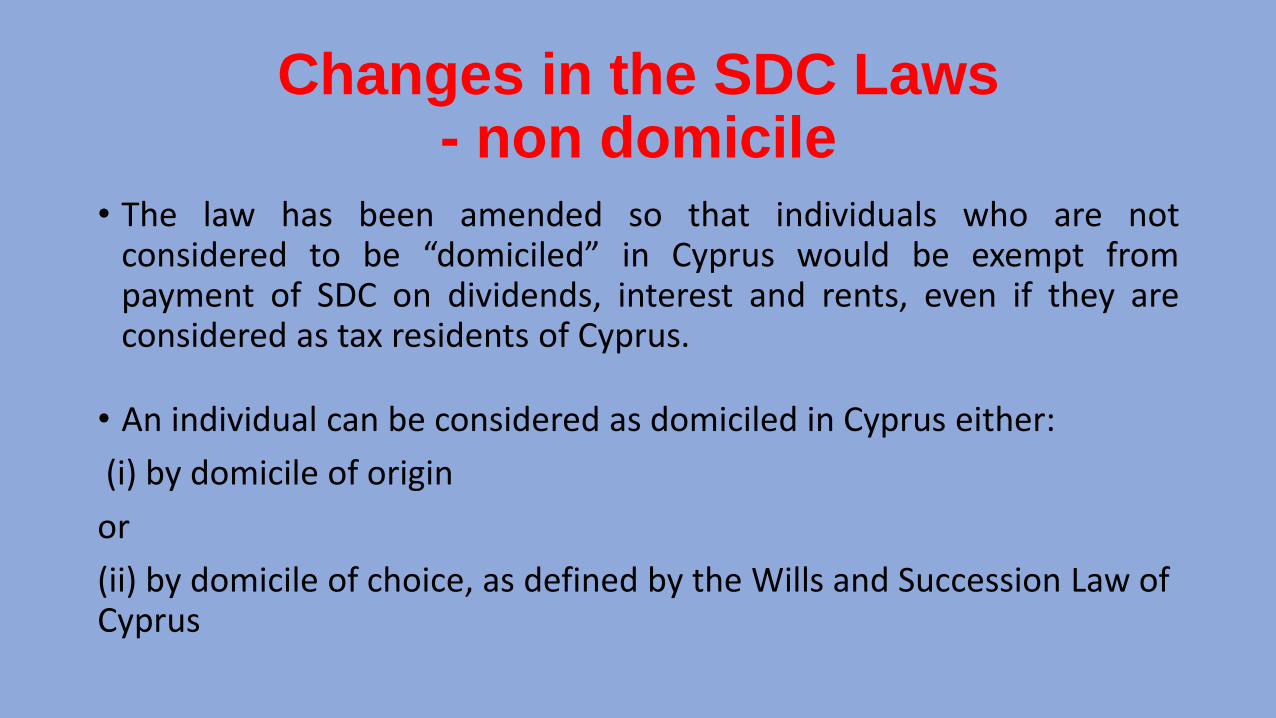

Changes in the SDC Laws - non domicile

• The law has been amended so that individuals who are notconsidered to be “domiciled” in Cyprus would be exempt frompayment of SDC on dividends, interest and rents, even if they areconsidered as tax residents of Cyprus.

• An individual can be considered as domiciled in Cyprus either:

(i) by domicile of origin

or

(ii) by domicile of choice, as defined by the Wills and Succession Law of Cyprus

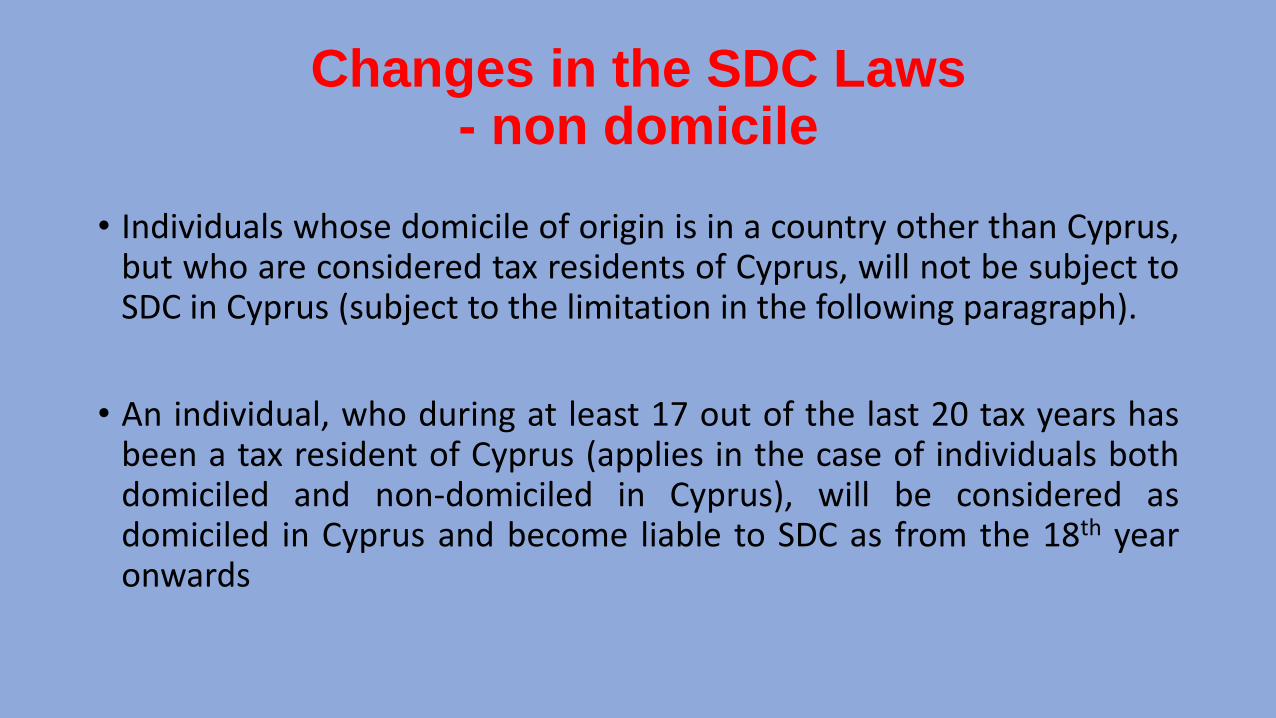

Changes in the SDC Laws - non domicile

• Individuals whose domicile of origin is in a country other than Cyprus,but who are considered tax residents of Cyprus, will not be subject toSDC in Cyprus (subject to the limitation in the following paragraph).

• An individual, who during at least 17 out of the last 20 tax years hasbeen a tax resident of Cyprus (applies in the case of individuals bothdomiciled and non-domiciled in Cyprus), will be considered asdomiciled in Cyprus and become liable to SDC as from the 18th yearonwards

Cyprus tax residency at 60 days

• An amendment to the definition of “Cyprus tax resident individual” asincluded in the Income Tax Law 118 (I)/2002, was recently voted bythe Cyprus Parliament. The amendment is effective from 1 January2017 and provides for an individual to be considered as a Cyprus taxresident under the 60 days scheme under specific conditions.

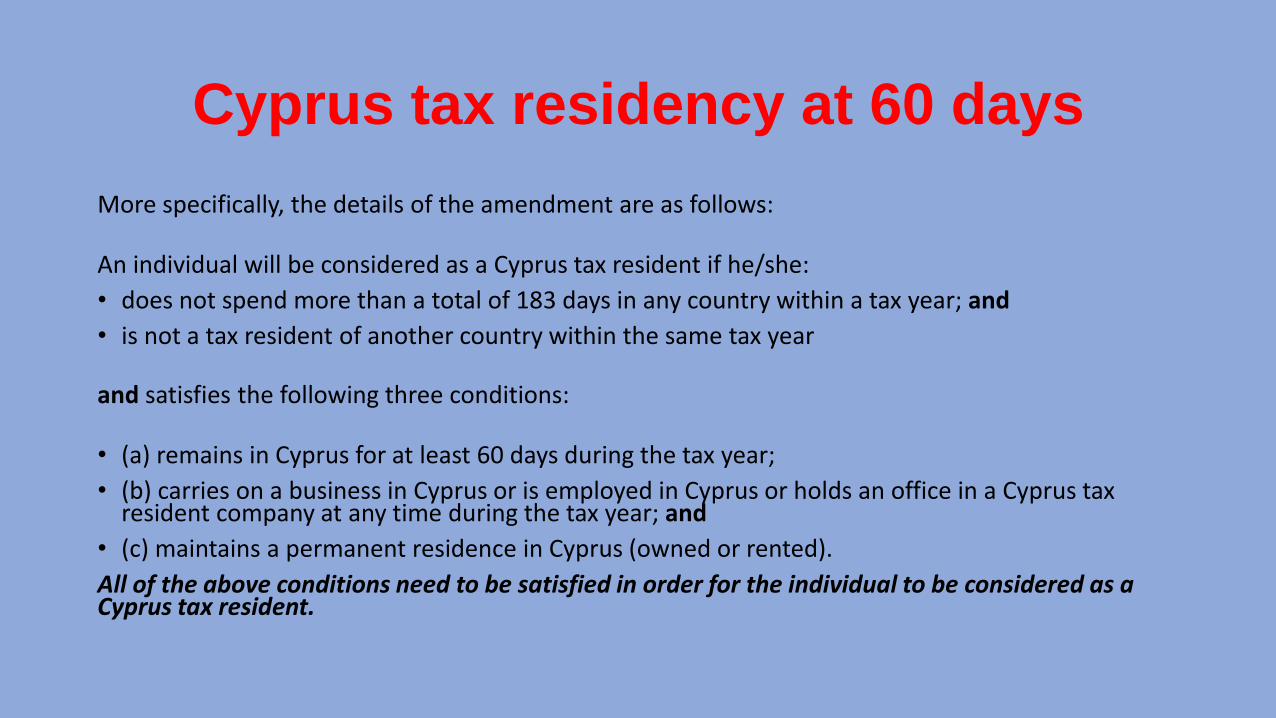

Cyprus tax residency at 60 days

More specifically, the details of the amendment are as follows:

An individual will be considered as a Cyprus tax resident if he/she:

• does not spend more than a total of 183 days in any country within a tax year; and

• is not a tax resident of another country within the same tax year

and satisfies the following three conditions:

• (a) remains in Cyprus for at least 60 days during the tax year;

• (b) carries on a business in Cyprus or is employed in Cyprus or holds an office in a Cyprus tax resident company at any time during the tax year; and

• (c) maintains a permanent residence in Cyprus (owned or rented).

All of the above conditions need to be satisfied in order for the individual to be considered as a Cyprus tax resident.

CONCLUSION

• The key is to avoid the defence tax in order to collect all dividends, interest and rents free from defence tax

• There are two keys you need to have to unlock the doors of success inavoiding defence tax:

1. Tax residency2. Non-domicile

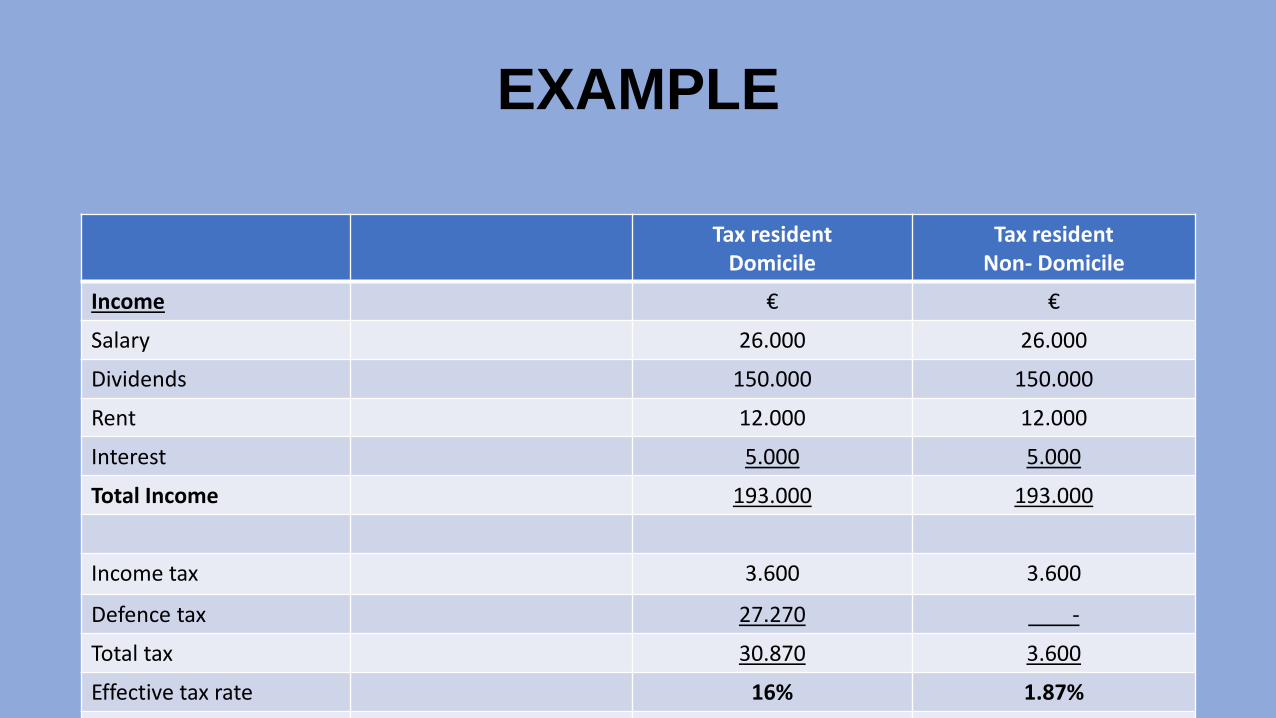

EXAMPLE

Tax resident Domicile

Tax resident Non- Domicile

Income € €

Salary 26.000 26.000

Dividends 150.000 150.000

Rent 12.000 12.000

Interest 5.000 5.000

Total Income 193.000 193.000

Income tax 3.600 3.600

Defence tax 27.270 -

Total tax 30.870 3.600

Effective tax rate 16% 1.87%