Half Year Results for the six months ended 31 December ... · 1H14 Group performance •Sales...

22

Presented by: Mick McMahon, CEO 12 February 2014 Half Year Results for the six months ended 31 December 2013 For personal use only

Transcript of Half Year Results for the six months ended 31 December ... · 1H14 Group performance •Sales...

Presented by:

Mick McMahon, CEO 12 February 2014

Half Year Results

for the six months ended 31 December 2013

For

per

sona

l use

onl

y

Disclaimer

This presentation has been prepared by SKILLED Group Limited (ASX:SKE). The information contained in this presentation is of

a general nature only, is not investment advice, and should not be used as the basis for making an investment decision. This

presentation has been prepared without taking into account the investment objectives, financial situation or specific needs of any

particular person.

Except for any statutory liability that cannot be excluded, none of SKILLED Group Limited, its directors, employees or agents

accept any liability, including, without limitation, any liability caused or contributed to by any fault or negligence on their part, for

any loss arising from the use of the information contained in this presentation. In particular, no representation or warranty,

express or implied, is given as to the accuracy, completeness or correctness, likelihood of achievement or reasonableness of any

forecast, or statement as to prospects or expected returns contained in this presentation. Any such forecast, or statement as to

prospects or expected returns are by their nature subject to significant uncertainties and contingencies, and are for indicative

purposes only. Past performance is no guarantee of future performance.

Before making an investment decision, you should consult your financial adviser to determine whether an investment in SKILLED

Group Limited is appropriate in light of your particular investment objectives, financial situation, or specific needs.

PAGE 2

For

per

sona

l use

onl

y

Contents

Group performance

Strategy update

Outlook

Business segments

Appendix

PAGE 3

For

per

sona

l use

onl

y

1H14 Group performance

• Sales revenue declined on pcp, however in line with 2H13

• EBITDA impacted by mining slowdown & overall economic weakness partially offset by cost reductions

and contribution from Broadsword

• Cash flow consistent with pcp and gearing remains conservative post increased investment in

Broadsword and OMSA

• Reported EPS includes impact of non-cash acquisition accounting adjustments

• Interim dividend of 7.5 cps, fully franked, up from 7.0 cps

PAGE 4 Note: all comparisons above are to the prior corresponding period unless stated otherwise. 1 Includes equity accounted income from joint ventures; 2 As per

segment reporting in Half Year Financial Report 3 Debt/(Debt + Equity)

1H14 2H13 1H13

Sales Revenue1 ($m) 906.3 900.3 973.6

Reported NPAT ($m) 21.0 27.9 28.2

Underlying NPAT ($m) 26.0 29.3 29.2

Underlying EBITDA2 ($m) 43.9 46.4 48.7

Operating cash flow (before tax) ($m) 13.1 73.8 15.9

Net debt ($m) 132.9 44.8 67.1

Gearing %3 21.9 8.7 12.8

Reported EPS (cps) 9.0 12.0 12.1

Underlying EPS (cps) 11.1 12.5 12.5

Dividend (cps) 7.5 9.0 7.0

For

per

sona

l use

onl

y

1H14 Results

• Mining sector slowdown

• WFS revenue and margin impacted but partially offset by cost reductions

• Swan revenue significantly lower due to decrease in project activity

• Deferral of activity into 2H impacted ATIVO

• Subdued economic conditions

• WFS slow but underlying business activity stabilised in Q2

• Weaker demand for permanent technical professional roles

• Oil & Gas

• Slow first half in OMS Australia with solid activity levels in NZ and International

• Visible pipeline of oil & gas projects including recent contract wins

• Broadsword revenue in line with expectations

• Continued focus on improving safety performance

• 7% reduction in injury frequency rate (AIFR) vs pcp

• Disciplined management of costs

• $10m cost reduction in 1H14

PAGE 5

For

per

sona

l use

onl

y

Strategy implementation

PAGE 6

Well positioned to benefit from any improvement in economic activity and growth in mining volumes

• Retained key clients and benefiting from supplier consolidation

Continued to invest in systems and processes to leverage scale

• Benefits flowing through further integration of recruitment and back office processes

• Pilot “Paperless Branch of the Future” opened in Thomastown (VIC)

• ERP (Agresso) system upgrade underway will enable further process improvement and cost reduction

• Integration of Broadsword back office functions to ERP system

Further reduction in the indirect cost base

• $10 million indirect cost reduction delivered in 1H14 from accelerated program

• Expect to deliver a total of ~$15 million cost reduction over the full year

Disciplined investment in future earnings growth

• Building scale in attractive, higher growth sectors - acquisition of Broadsword in oil and gas sector

• Expansion of scale in maintenance and technical trades - acquisition of T & C Services

• Securing key oil and gas contract - manning services for Saipem on the Ichthys LNG Project

For

per

sona

l use

onl

y

PAGE 7

Segment performance

Workforce Services

• Revenue impacted by reduced demand in

resources sector; activity stabilised in 2Q

• Margin pressure from customers across most

sectors; partially offset by sustainable cost

reduction and efficiency improvement

Technical Professionals

• Slowdown in client project activity and pricing

pressure in Swan; expected to continue into 2H

• Weaker demand for permanent technical

professional roles in 1H14

• Trainees and apprentices and Indigenous

employment program performed well

Engineering & Marine Services

• Deferral of activities into 2H impacted ATIVO

and OMS Australia

• Revenue and profitable growth in OMS

International and OMS NZ

• Revenue from Broadsword in line with

expectations; integration progressing well

Note: all comparisons above are to the prior corresponding period unless stated otherwise. 1 Includes equity accounted income from joint ventures.

2 As per segment reporting in Half Year Financial Report.

Sales

$m EBITDA2

$m

Underlying EBITDA margin

Workforce

Services 1H14 452.6 19.4 4.3%

2H13 454.9 18.3 4.0%

1H13 463.4 22.5 4.9%

Technical

Professionals 1H14 202.8 9.3 4.6%

2H13 217.5 11.7 5.4%

1H13 271.4 15.1 5.6%

Engineering &

Marine Services1 1H14 252.3 22.7 9.0%

2H13 227.8 21.6 9.5%

1H13 241.0 19.7 8.2%

Group

Performance1 1H14 906.3 43.9 4.8%

2H13 900.3 46.4 5.2%

1H13 973.6 48.7 5.0%

For

per

sona

l use

onl

y

PAGE 8

$m 1H14 1H13 1H14 vs.

1H13

EBITDA adjusted for non-cash items 38.4 46.5 (8.1)

Decrease/(increase) in working capital (25.3) (30.6) 5.3

Operating cashflow, excluding tax 13.1 15.9 (2.8)

Net tax paid (11.8) (19.8) 8.0

Operating cashflow after tax 1.3 (3.9) 5.2

Net interest paid (3.0) (2.0) (1.0)

CAPEX (8.6) (6.5) (2.1)

Acquisition/earn-out payments1 (52.4) (9.5) (42.9)

Dividends paid (21.0) (18.7) (2.3)

Other (1.2) 1.6 (2.8)

Total cashflow (84.9) (39.0) (45.9)

Opening Net Debt 44.8 27.4 17.4

Cash (inflow)/outflow 84.9 39.0 45.9

Other movements (FX, fees) 3.2 0.7 2.5

Closing Net Debt 132.9 67.1 65.8

Cashflow and net debt

1 Net of cash/debt acquired

67.1

27.3

63.0 17.5

17.5

52.4

0

1

2

3

4

0

20

40

60

80

100

120

140

1H13 2H13 1H14

Broadsword acquisition

OMSA JV increased shareholding

Net Debt (excl acquisitions)

Net interest

132.9

44.8

Net Debt ($m)

• Seasonal working capital movement ($25m) consistent with pcp

• Capex increased due to additional Broadsword vessel & systems investment

• Gearing of 21.9% remains conservative post investments

For

per

sona

l use

onl

y

Strategy update

For

per

sona

l use

onl

y

PAGE 10

Market leader in the provision of flexible labour

solutions

• Tradespeople, experienced operators & technical

professionals

• Engineering projects & maintenance

• Offshore marine services

Strong position in key growth sectors

• Mining & resources; oil and gas; infrastructure;

telecommunications

• 51% revenue from WA and QLD

Safety leadership in the industry

Industrial relations expertise

~50,000 people employed each year, including:

• ~ 1,000 traineeships and apprenticeships

• ~ 500 Indigenous employees

Long term client relationships

Well established and trusted brand

Extensive branch network across Australia

29%

23%

10% 9% 7% 6% 5% 4%

2% 5%

Oil

& g

as

Min

ing &

resourc

es

FM

CG

Prim

ary

ma

nufa

ctu

rin

g

Gov't &

utilit

ies

Infr

astr

uctu

re

Tra

nsp

ort

& lo

gis

tics

Au

to &

defe

nce

Health

Oth

er

SKILLED Group revenue by sector 1H14

Note: above graphs include notional 1/2 share of joint venture revenue

4%

SKILLED Group revenue by geography 1H14

Our competitive advantage

42%

2%

4%

9%

19%

14% Overseas 6%

4%

For

per

sona

l use

onl

y

PAGE 11

Year 1 - 2

Pe

rfo

rma

nce

Understand the Business Simple clear strategy:

• Core Plus strategy

• SKILLED “re-Engineering”

change program

• Balance sheet repair

• Re-organise / new team

• Improve basic disciplines

Leverage exposure to growth markets & segments

Zero Harm safety refresh

Build capability:

• Leadership & organisation

• Sales & marketing

• Management processes

Deliver benefits:

• Leverage IT system investments

• Cost out, cash improvements

• Non-core assets

“One Team” culture

Leverage exposure to growth markets & segments

Zero Harm safety leadership

Build on brand leadership:

• Strengthen market position

• Leading employer brand

Higher value services

Most efficient operation

• Low cost, high volume

Embedded “One Team” culture Superior returns

Overhead Costs

Reduced Debt

Cash

Conservative Gearing

Unit Costs

EBIT Margin

Cash

ROIC

Revenue & Margin

EBIT Margin

Cash

ROIC

Developing a shared strategy Building capability Profitable growth

Year 5+

Good progress but more to do

For

per

sona

l use

onl

y

Strategy for value growth

Leverage scale and brand

strength in Workforce Services:

• Transformation, cost efficiency, data

based decision support

• Focus on safety and higher skill roles

Blue collar labour

hire &

placements

Branch network and „Back Office‟ systems

Projects &

Maintenance

Offshore Marine

Services Technical

Professionals

Value added services

Sourcing

& supply

of labour

and skills

Client

focused

sales,

service &

operation

Build scale in attractive

higher skill, higher margin

segments

Page 12

For

per

sona

l use

onl

y

Acquisition of T & C Services • Acquisition completed on 11 February 2014, following

favourable shareholder vote

• ATIVO, T&C and Damstra will work side by side in a newly formed SKILLED

Engineering division

• Johannes Risseeuw appointed COO SKILLED Engineering

• Integration commenced

• T & C Services is a leading maintenance services provider to

the manufacturing, mining, heavy industry and utilities sectors

• Maintenance services, asset management and optimisation, as well as

preventative maintenance activities such as shutdowns, equipment

servicing, machinery repair and inspection

• Supported by workshop services including plant and equipment rebuild /

repair, production of spares and consumables, fabrication, machining,

welding and electrical work

• Established presence in NSW and QLD with a blue chip client

base

• Longstanding client relationships built on reputation for safety, quality and

service

• Experienced management team

• Highly skilled workforce (~ 600 employees)

• Key management to remain following the acquisition

Mobile maintenance support to customers

Highly skilled employees

Workshop facilities

Note: excludes Thomas & Coffey Limited construction projects, head office and residual business risks PAGE 13

For

per

sona

l use

onl

y

Outlook

For

per

sona

l use

onl

y

Outlook

PAGE 15

• Trading conditions remain challenging but second half expected to be stronger

• Workforce Services: overall activity levels appear to have stabilised and benefiting from supplier

consolidation; however continued price pressure in mining impacting margins

• Technical Professionals: reduced activity in mining and related engineering services, primarily in

Swan; Telecommunications expected to strengthen

• Engineering & Marine Services: activity levels improving in maintenance services and oil and

gas, with growth expected from:

• increased activity levels & visible pipeline in oil & gas in the second half; Saipem vessel

mobilisation delayed to end FY14

• Broadsword - additional vessel and opportunity to change the mix of chartered / owned vessels

• initial contribution from T & C Services acquisition

• Cost reduction program expected to deliver ~$15 million in FY14 from initiatives already underway

• Well positioned for longer term benefit from:

• any improvement in economic activity and expansion in mining volumes

• full contribution from the Saipem contract, Broadsword and T&C Services; while the OMSA JV is

expected to reduce from peak levels in line with activity on the Gorgon project

• ongoing strategy implementation supporting further cost reduction

• a strong balance sheet to support dividends and investment in future growth

For

per

sona

l use

onl

y

Business Segments

For

per

sona

l use

onl

y

PAGE 17

Mining & Resources

24%

Primary Manufacturing

17%

FMCG 18%

Infrastructure 11%

Gov't & Utilities

10%

Transport & Logistics

8%

Other 12%

• Initial impact of slowdown in mining and

related services and a slow seasonal build up

into Christmas partially offset by improved

activity in infrastructure and rail sectors

• Well positioned for growth in mining volumes

and improvement in economic activity

• activity levels stabilised in 2Q

• Margins impacted by continued pricing

pressure from clients across most sectors.

• Good progress on sustainable cost reduction

and efficiency improvement:

• cost out program accelerated in 1H14

• partially offsetting reduction in mining activity

1H14 2H13 1H13 1H14 v

2H13

1H14 v

1H13

Revenue ($m) 452.6 454.9 463.4 (0.5)% (2.3%)

EBITDA ($m) 19.4 18.3 22.5 6.2% (13.7%)

EBITDA margin 4.3% 4.0% 4.9% 0.3 (0.6)

Revenue and EBITDA:

Industry Breakdown:

Workforce Services

For

per

sona

l use

onl

y

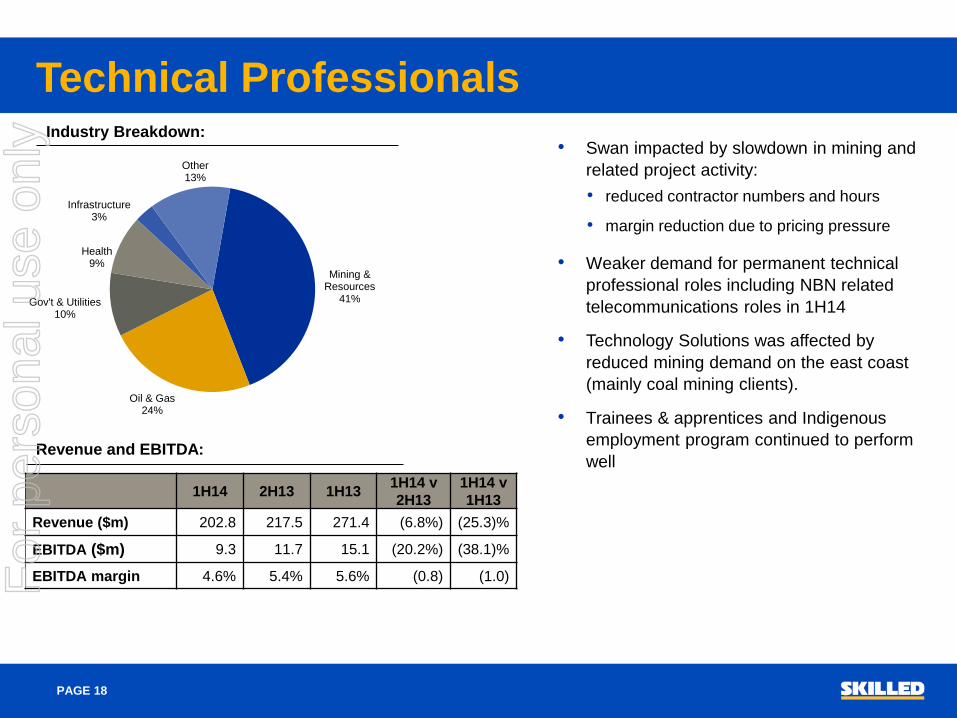

PAGE 18

Revenue and EBITDA:

Industry Breakdown:

Mining & Resources

41%

Oil & Gas 24%

Gov't & Utilities 10%

Health 9%

Infrastructure 3%

Other 13%

• Swan impacted by slowdown in mining and

related project activity:

• reduced contractor numbers and hours

• margin reduction due to pricing pressure

• Weaker demand for permanent technical

professional roles including NBN related

telecommunications roles in 1H14

• Technology Solutions was affected by

reduced mining demand on the east coast

(mainly coal mining clients).

• Trainees & apprentices and Indigenous

employment program continued to perform

well

1H14 2H13 1H13 1H14 v

2H13

1H14 v

1H13

Revenue ($m) 202.8 217.5 271.4 (6.8%) (25.3)%

EBITDA ($m) 9.3 11.7 15.1 (20.2%) (38.1)%

EBITDA margin 4.6% 5.4% 5.6% (0.8) (1.0)

Technical Professionals

For

per

sona

l use

onl

y

PAGE 19

Revenue and EBITDA:

Industry Breakdown:

Oil & Gas 74%

Mining & Resources

10%

FMCG 4%

Transport & Logistics

4%

Other 8%

Revenue by activity:

Manning - domestic

37%

Manning - international

22%

Vessels (incl

manning) 13%

Maintenance 14%

Projects and Shutdowns

14% 1H14 2H13 1H13

1H14 v

2H13

1H14 v

1H13

Revenue ($m) 252.3 227.8 241.0 10.7% 4.7%

EBITDA ($m) 22.7 21.6 19.7 4.8% 15.1%

EBITDA margin 9.0% 9.5% 8.2% (0.5) 0.8

Engineering and Marine Services • ATIVO: Impacted by deferrals of maintenance projects

and shutdowns by clients. Activity levels have stabilised in

recent months.

• Initial contribution from T&C Services in 2H

• OMS: Increased activity in OMS International and OMS

NZ; offset by reduced activity levels in OMS Australia.

Activity levels have ramped up early in the second half.

• Broadsword: Revenue in line with expectations;

integration progressing well.

• Mobilisation of Saipem vessels expected to commence at

the end of FY14

Note: above graphs include notional 1/2 share of joint venture revenue

For

per

sona

l use

onl

y

Appendix

For

per

sona

l use

onl

y

Reconciliation of result

PAGE 21

$m Comments

Underlying NPAT 26.0

Redundancy and branch closure (2.3) Costs incurred to realise $10m cost saving in1H14

Acquisition and integration costs (1.2) T&C Services acquisition costs and Broadsword

integration costs

Amortisation of acquired

intangibles (non-cash) (2.4)

Non-cash amortisation of “customer contracts” in

relation to Broadsword acquisition and increase in

OMSA investment.

Notional interest on deferred

consideration (non-cash) (0.7)

Non-cash notional interest expense on Broadsword

deferred consideration recognised at NPV on

acquisition.

Tax on reconciling items 1.6 Tax expense on above items, where relevant

Reported NPAT 21.0

For

per

sona

l use

onl

y

Contact Details:

Delphine Cassidy

EGM Investor Relations

P: +61 3 8646 6465

M: +61 419 163 467

E: [email protected] For

per

sona

l use

onl

y