H1 2017 IFRS Financial Results - Metalloinvest · H1 2017 IFRS Financial Results ... *Hereinafter...

24

Resources create opportunities Resources create opportunities H1 2017 IFRS Financial Results 22 August 2017

Transcript of H1 2017 IFRS Financial Results - Metalloinvest · H1 2017 IFRS Financial Results ... *Hereinafter...

Resources create opportunitiesResources create opportunities

H1 2017 IFRS Financial Results22 August 2017

2

Disclaimer

The following USD/RUB exchange rates were used for the presentation of those financial results:

Average over the period: Q1 2016 – 74.6283; Q2 2016 – 65.8833; Q1 2017 – 58.8442 ; Q2 2017 – 57.1451.

End of the period: H1 2016 – 64.2575; 2016 – 60.6569; H1 2017 –59.0855.

This presentation of Metalloinvest’s financial results for H1 2017 (the “Presentation”) contains certain forward-looking statements, particularly those relating to

anticipated demand and consumption, global economic conditions, commodity prices, management aims and objectives, strategy, production, anticipated investments

and anticipated completion of previously announced transactions. Metalloinvest will not update these statements to reflect events and circumstances occurring after the

date hereof. By their nature, forward-looking statements involve risks and uncertainties because they relate to events and depend on circumstances that will or may occur

in the future. Actual results may differ from those expressed in such statements depending on a variety of factors, including future levels of industry product supply,

demand and pricing, operational problems, general economic conditions, political stability and economic growth in relevant areas of the world, changes in laws and

governmental regulations, exchange rate fluctuations, development and use of new technology, changes in public expectations and other changes in business conditions,

the actions of competitors, natural disasters and adverse weather conditions, wars and acts of terrorism or sabotage, other factors discussed elsewhere in this document,

as well as other risks affecting Metalloinvest and its operations.

The contents of this Presentation do not constitute or form part of any advertisement of securities, any offer or invitation to issue, sell, purchase, exchange or transfer or

any solicitation of any offer to purchase or subscribe for, any securities of Metalloinvest in any jurisdiction, nor shall this Presentation nor any part of it nor the fact of its

presentation, communication or distribution form the basis of, or be relied on in connection with, any contract or investment decision. Any foreign securities which are

mentioned in this Presentation are not and will not be registered in the Russian Federation by any state authority responsible for registration of such securities and such

securities shall not be admitted to subscription nor shall be publicly available in the Russian Federation and cannot be the subject of any offer in the Russian Federation,

except in the cases permitted by the law of the Russian Federation. No representation or warranty, express or implied, is given by Metalloinvest, its affiliates or any of their

respective advisers, officers, employees or agents, as to the accuracy of the information or opinions or for any loss howsoever arising, directly or indirectly, from any use of

these materials or their contents.

3

Content

I. Key Highlights………...….……….………………..…………………………………........................... 4

II. Operational Results..…….....………………………………………………………………………………... 6

III. Financial Results …...…………………………………………………………………........................... 10

IV. Debt & Credit Ratings…………………………………………………….….................................. 14

V. Subsequent Events……………………………………………………………………………………………... 18

4

KEY HIGHLIGHTS

5

Highlights

Key financialsUSD mn H1 2017 H1 2016 Change

Revenue 3,032 1,931 57.0%

Gross profit 1,556 896 73.7%

EBITDA* 1,061 533 99.1%

EBITDA margin 35.0% 27.6% 7.4 p.p.

Net Income 585 428 36.7%

Capex 188 155 21.3%

USD mn, eop 30.06.2017 31.12.2016 Change

Total Debt 4,468 4,183 6.8%

Short-term debt 289 91 х3.2

Cash & equivalents 866 989 (12.4%)

Net Debt 3,602 3,194 12.8%

Net Debt / EBITDA LTM 2.0х 2.5х (0.5x)

Notes:

*Hereinafter EBITDA stands for EBITDA adjusted according to IFRS requirements. For more details please refer

to IFRS Statements

Net Debt / EBITDA LTM is calculated based on EBITDA for the last 12 months; the indicator has

an informational character and does not contain adjustments as per loan documentation

35

55

75

95

Jan 2016 Jul 2016 Jan 2017 Jul 2017

Iron ore index (62% Fe, CFR China)

USD/ t

Source: Bloomberg

52

65

74

Global iron ore prices

1,9312,330

3,032

Revenue

H1 2016 H2 2016 Н1 2017

533725

1,061

EBITDAH1 2016 H2 2016 H1 2017

3.3x2.5x

2.0x

Net Debt/EBITDA LTM

6

OPERATIONAL RESULTS

7

H1 2017 key developments

• Iron ore production decreased by 1.1%*, due to

a change in ore mixture

• Pellet production remained flat y-o-y

• HBI/DRI production grew by 11.9%, mostly due to

hot tests at HBI-3 at LGOK

• Hot metal production fell by 11.9% following

major maintenance works on a blast furnace

at Ural Steel

• Crude steel production rose by 3.6%, mainly

due to an increase in effective orders

Production volumes

20.4

12.3

2.9

1.5

2.3

20.3

12.9

2.8

1.5

2.4

20.2

12.3

3.3

1.3

2.4

Iron ore

Pellets

HBI/DRI

Hot metal

Crude steel

H1 2016 H2 2016 H1 2017

mn t

Notes:

Data on major plants: LGOK, MGOK, OEMK, Ural Steel

Iron ore refers to iron ore concentrate and sintering ore

*Hereinafter comparison with H1 2016

8

1.5 0.6

3.2 4.3

8.2 7.1

H1 2016 H1 2017

Russia Europe Asia MENA Others*

13.8 13.3

0.9 1.2

1.0 0.6

0.6 0.4

0.70.9

H1 2016 H1 2017

3.3 3.2

Shipment structure

Mining Segment

Steel Segment

• Shipments to Russia accounted for 54% of total shipments,

decreasing by 13.6% in real terms, mainly due to the termination of

pellet delivery to NLMK and reallocation of supplies to the export,

as well as intra-group consumption

• Shipments to Europe grew by 32.9% mainly as a result of increased

pellet supplies to the customers in Poland, Serbia and Germany

• Shipments to Asia declined by 61.8% due to a reallocation

of iron ore concentrate volumes to the domestic market

• Shipments to Russia increased by 32.5%, due to a growth in

deliveries of long steel products under long-term contract, among

other factors

• Shipments to other countries increased by 27.9% mainly due to

a growth in pig iron supplies to Nucor Corporation (USA)

• Shipments to MENA and Europe fell by 39.3% and 43.4%,

respectively, due to a reallocation of shipments to other regions

mn t

mn t

Data on major plants: LGOK, MGOK, OEMK, Ural Steel

* Others include shipments to Americas, CIS countries and Africa. Americas’ share in H1 2017 – 82%

9

Key capex development projects implemented in H1 2017

Source: management accounts* Direct reduced iron** Continuous casting machine*** In terms of financing

Enterprise ProjectCapex in H1 2017,

USD mnShare of

completion***

Min

ing

Se

gm

en

tS

tee

l Se

gm

en

t

Construction of HBI-3 Plant63 83%

Complex for LGOK iron ore concentrate storage

10

Modernisation of DRI*-218

Modernisation of CCM** #1

6

47%

35%

44%

10

FINANCIAL RESULTS

11

734

482

110

293

312

1,233

731

91

312

665

Russia

Europe

Asia

MENA

Other

countries*

H1 2016

H1 2017

Revenue composition

H1 2017 Revenue: USD 3,032 mn

USD mn

12%

19%

12%13%

40%

4%

12%

22%

13%11%

39%

3%

Iron ore Pellets

HBI Pig iron

Steel products Other revenue

H1 2017 – outer circleH1 2016 – inner circle

Revenue by region

Export share59% in H1 2017

vs.62% in H1 2016

* Others include Americas and CIS countries

12

412

113

587

188

936

153

Mining Steel

H1 2016 H2 2016 H1 2017

533

1,061

1,101

(441)

(96)

(35)

(1)

EBITDA H1 2016

Revenue

Cost of sales

Distribution expenses

G&A expenses

Other

EBITDA H1 2017

EBITDA y-o-y dynamics

EBITDA composition

H1 2017 EBITDA: USD 1,061 mn

USD mnSupportive market conditions resulted in more than

two-fold increase of the Mining Segment EBITDA,

accounting for 88% of the Company’s total EBITDA

in H1 2017

EBITDA by segment dynamics

35.0%

27.6%

EBITDA margin

USD mn

13

283381533 44

25

1,061

(144)

(20)(155)

(168)

(233)

(60)

(188)(31)

EB

ITD

A

Inte

rest

Taxe

s

Ch

g.

in N

WC

Ca

pe

x

Oth

ers

FCF

EB

ITD

A

Inte

rest

Taxe

s

Ch

g.

in N

WC

Ca

pe

x

Oth

ers

FCF

Positive free cash flow

USD mn

H1 2016 H1 2017

14

DEBT & CREDIT RATINGS

15

H1 2017 key developments

• Feb-Apr: ING BANK increased the limit of the Company’s two-year

committed revolving credit line from USD 100 mn to USD 200 mn

• May: Tender offer of Eurobonds-2020 and issue of USD 800 mn

Eurobonds-2024 with a 4.85% interest rate

• June: Refinancing of USD 1.03 bn PXF* using funds obtained

through a new PXF-2017 with better pricing terms and maturity

schedule

Debt profile as of 30 June 2017

Sources:IFRS data, management accounts

*Pre-export financing

Total Debt: USD 4,468 mn

Breakdown by sourceBreakdown by currency

H1 2017 – outer circle2016 – inner circle

38%

56%

6%

36%

57%

7%

RUB

USD

EUR

31%

24%16%

22%

7% 31%

25%15%

21%

8% PXF

Eurobonds

RUB bonds

Sberbank

Other

2%

98%

6%

94%

Short-term

Long-term

16

0.90.6 0.4

1.1

0.5

0.20.5

0.3 0.6

1.4

0.3

0.6

0.91.0

0.4

1.3

Liquidity H2 2017 2018 2019 2020 2021 2022 After 2022

Liquidity position and repayment schedule

Notes:

Management accounts

* Undrawn committed credit lines

Cash

USD bn

Cash

*

1.3

Debt maturity schedule as of 31 December 2016 (USD 4.2 bn of total debt)

*

RUBUSD, EUR

Debt maturity schedule as of 30 June 2017 (USD 4.5 bn of total debt)USD bn

1.0

0.3 0.4

1.3

0.2

0.5

0.3

0.6

0.3

0.1

0.5

0.9

1.6

0.7

0.2 0.2

Liquidity 2017 2018 2019 2020 2021 2022 After 2022

17

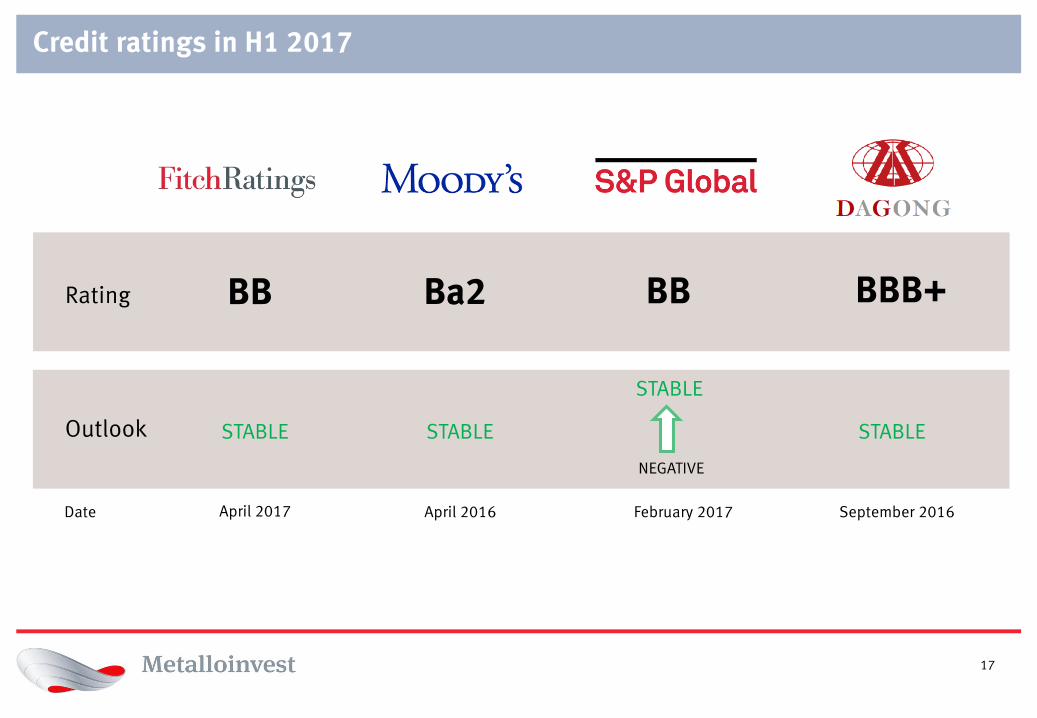

Credit ratings in H1 2017

April 2016 February 2017Date

Rating

STABLESTABLEOutlook

Ba2 BB

STABLE

BBB+

STABLE

September 2016

NEGATIVE

BB

April 2017

18

SUBSEQUENT EVENTS

In July, Metalloinvest launched HBI-3 Plant at LGOK

• Designed capacity of 1.8 mn t HBI per year

• Capex of approximately USD 660 mn

Vladimir Putin has participated in the official launch ceremony of HBI-3 Plant

In August, Metalloinvest announced the signing of supply contracts with the following key Russian

steel companies: EVRAZ, Mechel and Severstal. Deliveries of iron ore concentrate and pellets for a

total amount of 6.8 mn tonnes will be carried out before 30 June 2018

19

SUBSEQUENT EVENTS

July 2017

• Metalloinvest paid a dividend in the total amount of RUB 25.1 bn. The funds from the dividend

were returned in full to the Company for the repayment of existing intragroup loans

• Metalloinvest disposed in full its 1.8% interest in Norilsk Nickel for a total consideration

of USD 400 mn

August 2017

• The Company repaid USD 100 mn of PXF-2016 ahead of the scheduled maturity dates

• Based on the recommendation of Metalloinvest’s Board of Directors, the Company’s

shareholders took the decision to pay a dividend amounting to ~USD 330 mn

20

Q&A SESSION

21

APPENDIX

22

0.44

0.27

0.440.30

2014 2015 2016 H1 2017

Health, Safety & Environment

LTIFR*

Atmospheric emissions**tonnes ‘000

126 124117

59

2014 2015 2016 H1 2017

Health & Safety

Safety is the Company’s top priority

• In H1 2017, LTIFR decreased by 32% vs. 2016

• The Company is committed to a zero fatality rate

Environment

The Company devotes special attention to the environment

• In 2016, Metalloinvest completed reconstruction of thesecond gas purification unit at OEMK. As a result, dust levelsin steelmaking workplaces fell by an average of 50%

• Implementing the best available technologies at HBI-3at LGOK allows the Company to minimise its adverseenvironmental impact

• In 2017, Ural Steel started exploitation of a landfill forindustrial waste with a capacity of 1.2 mn tonnes

Accidents and Fatalities

2620

32

125

03

0

2014 2015 2016 H1 2017

* LTIFR is calculated on the basis of 4 Metalloinvest major plants (LGOK, MGOK, OEMK, Ural Steel ):

(total number of injuries with loss of labour capacity / number of worked man hours) х 1 mn man hours

** Total amount of pollution emission into atmosphere from stationary sources

23

Key financial indicators

USD mn Q2 2017 Q1 2017 Change H1 2017 H1 2016 Change

Revenue 1,512 1,520 (0.5%) 3,032 1,931 57.0%

Gross profit 785 771 1.8% 1,556 896 73.7%

EBITDA 534 527 1.3% 1,061 533 99.1%

EBITDA margin 35.3% 34.7% 0.6 p.p. 35.0% 27.6% 7.4 p.p.

Net Income 194 391 (50.4%) 585 428 36.7%

Capex 126 62 х2.0 188 155 21.3%

Total Debt 4,468 4,303 3.8% 4,468 5,357 (16.6%)

Short-term Debt 289 335 (13.7%) 289 855 (66.2%)

Cash and cash equivalents* 866 869 (0.3%) 866 1,775 (51.2%)

Net Debt 3,602 3,434 4.9% 3,602 3,581 5.9%

Net Debt / EBITDA LTM 2.0x 2.1х (0.1x) 2.0x 3.3х (1.3x)

* Cash & equivalents include short-term bank deposits

24

Investor Relations & Corporate Ratings Department

Contacts

Artem Lavrischev

Director of Investor Relations & Corporate Ratings

T: +7 (495) 981 55 55, ext. 7243

www.metalloinvest.com