Gujarat International finance tech city

81

1 Gujarat International Finance Tec-City

-

Upload

kunik-swaroop -

Category

Documents

-

view

47 -

download

3

description

GIFT Presentation GUJARAT

Transcript of Gujarat International finance tech city

1

Gujarat International Finance Tec-City

2

Why Invest in India?

3

India has witnessed steady growth and is set to become an economic superpower in the 21st century

GDP growth trajectory

Real GDPUS$ billion

625473

2791591188660

1950

+5%+3%

+5%

3%

+6%

1960 20001970 20051980 1990

+4%

GDP Contribution (%)

20.1

5.02.1

Contribution to incremental GDP growth of major world economies*

*Major economies considered are the BRIC and G6 countries

2000 2020 2050

– Progressive and stable environment

• Commitment to liberalization across political parties, both central and state. WTO an additional catalyst

• A healthy economic environment with stable financial markets

– Increased consumption

• Fast growing middle-class with increased spending ability. A young population ensures savings and investment rates will rise

– Infrastructure growth

• Government, private and international investments in telecom, transport, power and IT parks are driving growth

– Emergence of strong corporate India

• Home grown local innovators and MNCs alike have shaped the landscape and set up large scale profitable businesses

• The next wave of manufacturing will further bolster GDP growth – India will become a global sourcing base in skill intensive sectors

Why growth is likely to sustain

Source: Press Search, Goldman Sachs BRIC report 2003

4

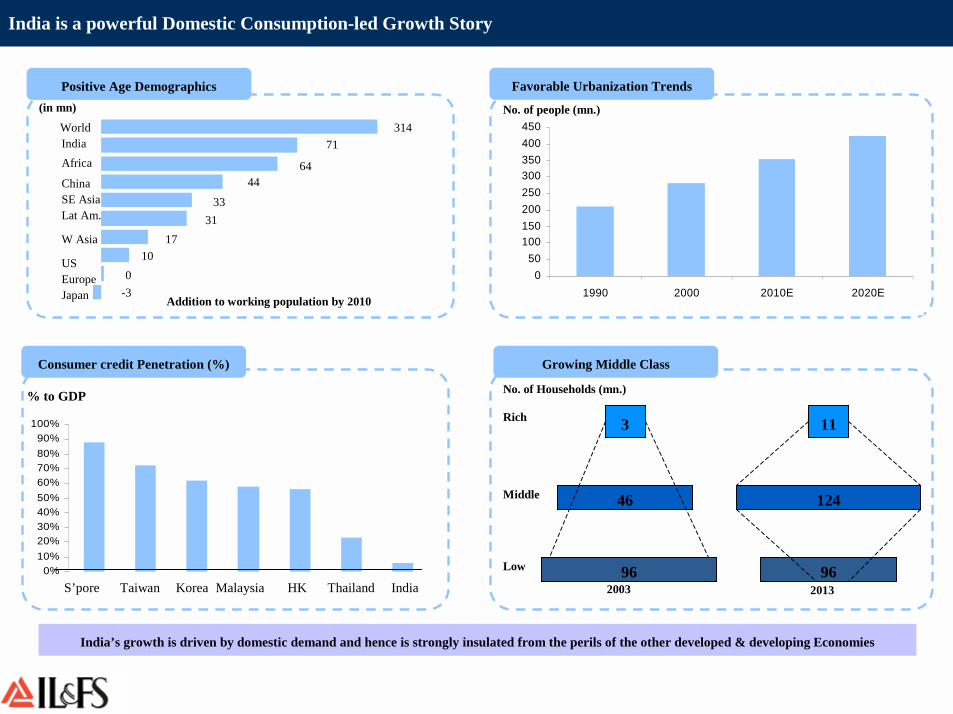

India is a powerful Domestic Consumption-led Growth Story

India’s growth is driven by domestic demand and hence is strongly insulated from the perils of the other developed & developing Economies

0%10%20%30%40%50%60%70%80%90%

100%

S’pore Taiwan Korea Malaysia HK Thailand India

050

100150200250300350400450

1990 2000 2010E 2020E

% to GDP

3 11

46 124

96962003 2013

No. of Households (mn.)

Rich

Middle

Low

No. of people (mn.)(in mn)

Addition to working population by 2010

WorldIndiaAfrica

ChinaSE AsiaLat Am.

W Asia

EuropeUS

Japan

31471

6444

3331

1710

0-3

Favorable Urbanization TrendsPositive Age Demographics

Consumer credit Penetration (%) Growing Middle Class

5

How attractive is India as a destination for doing Business?

6

India is emerging as an ‘Off shoring Hub’ for the entire spectrum of Services

CIO views on % increase in Offshore spending for specific locations*

* change relative to current spending levels

Source: Morgan Stanley Chief Investment Officer Survey, May 2005

India

China

Other Asia

E. Europe

Canada

Other Euro.

Lat Am

56

38

27

22

20

3

2

Source: Citigroup Smith Barney

Select Global companies with Offshoring presence across Services spectrum

India- Most Favored Offshore DestinationOff shoring ‘Sweet Spot’ for Indian Services companies

• Increasing number of Pharmaceutical Companies of US and UK are out

sourcing their clinical research to India

• Leading law firms have been off shoring their operation to India

• Global IT executives willing to move higher-end work offshore; Indian

service providers moving up the value-chain

• Citi, Lehman, JPMC, Morgan Stanley, Meryllynch are off shoring not

just the back end but also the front end business to India

CRO Legal IT Finance

7

What are the USPs for investing in India?

8

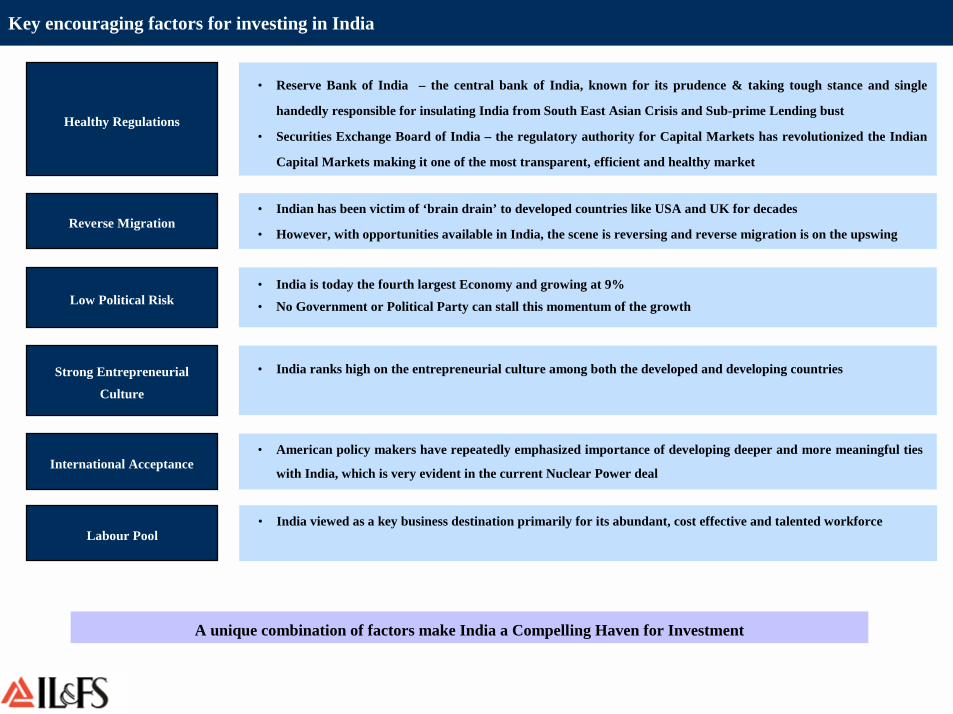

Key encouraging factors for investing in India

A unique combination of factors make India a Compelling Haven for Investment

Healthy Regulations

Reverse Migration

Strong Entrepreneurial

Culture

International Acceptance

• Reserve Bank of India – the central bank of India, known for its prudence & taking tough stance and single

handedly responsible for insulating India from South East Asian Crisis and Sub-prime Lending bust

• Securities Exchange Board of India – the regulatory authority for Capital Markets has revolutionized the Indian

Capital Markets making it one of the most transparent, efficient and healthy market

• Indian has been victim of ‘brain drain’ to developed countries like USA and UK for decades

• However, with opportunities available in India, the scene is reversing and reverse migration is on the upswing

• India ranks high on the entrepreneurial culture among both the developed and developing countries

• American policy makers have repeatedly emphasized importance of developing deeper and more meaningful ties

with India, which is very evident in the current Nuclear Power deal

Low Political Risk• India is today the fourth largest Economy and growing at 9%

• No Government or Political Party can stall this momentum of the growth

Labour Pool• India viewed as a key business destination primarily for its abundant, cost effective and talented workforce

9

Why is Infrastructure the “need of the hour” for India?

10

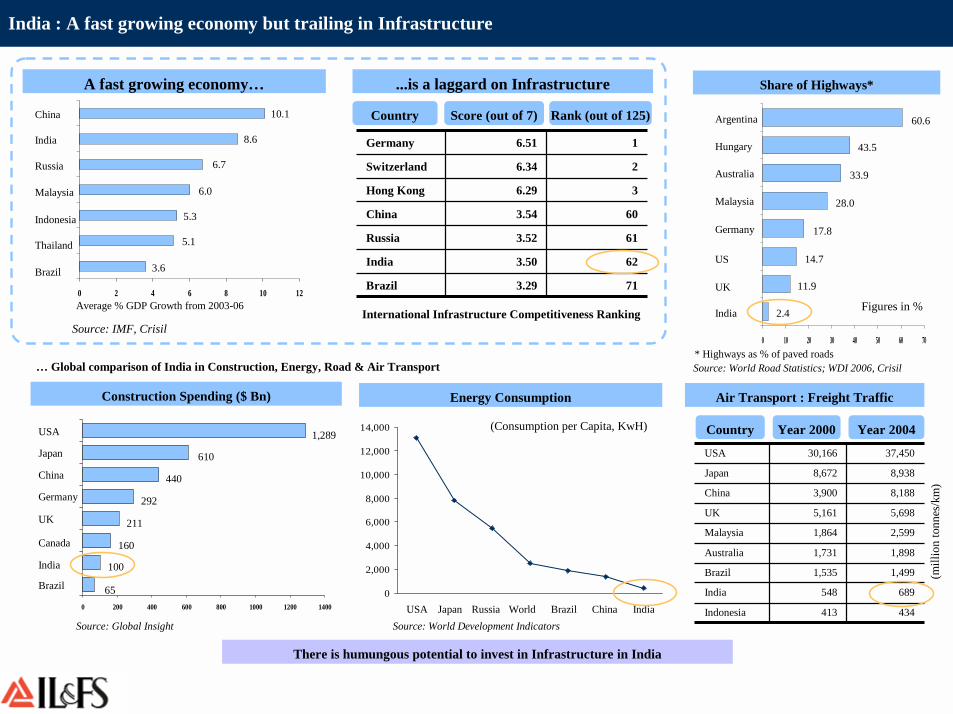

India : A fast growing economy but trailing in Infrastructure

...is a laggard on InfrastructureA fast growing economy…

0 2 4 6 8 10 12

China

India

Russia

Malaysia

Indonesia

Thailand

Brazil

10.1

8.6

6.7

6.0

5.3

5.1

3.6

Average % GDP Growth from 2003-06

Source: IMF, Crisil

613.52Russia

3.29

3.50

3.54

6.29

6.34

6.51

2Switzerland

71Brazil

62India

60China

3Hong Kong

1Germany

International Infrastructure Competitiveness Ranking

Country Score (out of 7) Rank (out of 125)

Construction Spending ($ Bn)

Source: Global Insight

0 200 400 600 800 1000 1200 1400

USA

Japan

China

Germany

UK

India

Brazil

1,289

610

440

292

211

160

65

Canada

100

Energy Consumption

Share of Highways*

* Highways as % of paved roadsSource: World Road Statistics; WDI 2006, Crisil

434413Indonesia

689548India

2,5991,864Malaysia

1,535

1,731

5,161

3,900

8,672

30,166

8,938Japan

1,499Brazil

1,898Australia

5,698UK

8,188China

37,450USA

Country Year 2000 Year 2004

Air Transport : Freight Traffic

(mill

ion

tonn

e s/k

m)

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

USA Japan Russia World Brazil China IndiaSource: World Development Indicators

(Consumption per Capita, KwH)

0 10 20 30 40 50 60 70

Argentina

Hungary

Australia

Malaysia

Germany

UK

India

60.6

43.5

33.9

28.0

17.8

14.7

2.4

US

11.9

Figures in %

There is humungous potential to invest in Infrastructure in India

… Global comparison of India in Construction, Energy, Road & Air Transport

11

Mumbai : A case in point

12

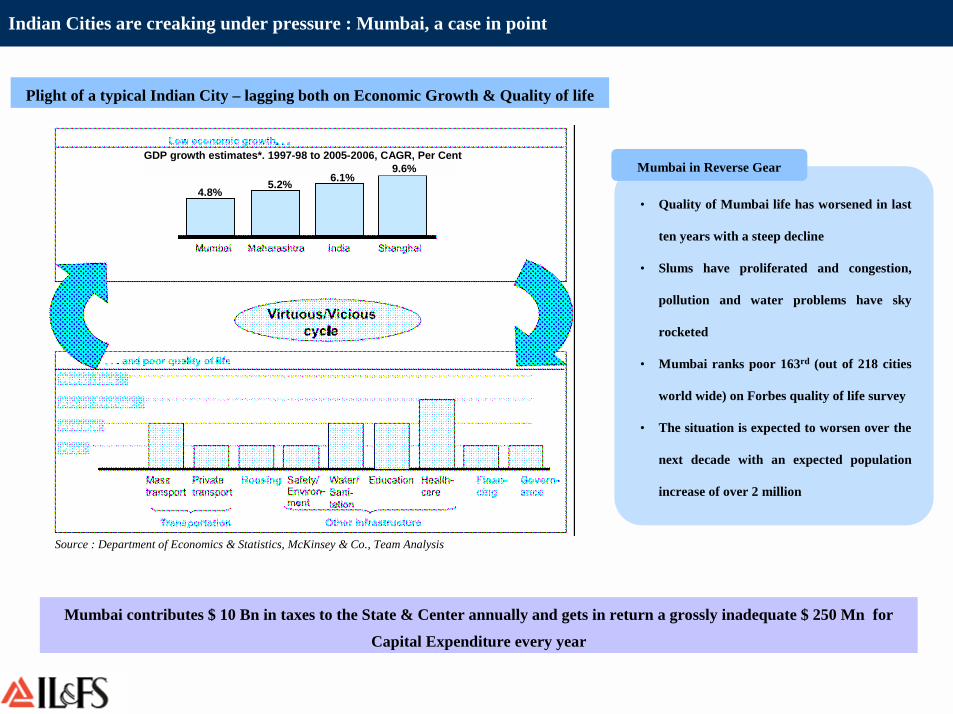

Indian Cities are creaking under pressure : Mumbai, a case in point

Plight of a typical Indian City – lagging both on Economic Growth & Quality of life

• Quality of Mumbai life has worsened in last

ten years with a steep decline

• Slums have proliferated and congestion,

pollution and water problems have sky

rocketed

• Mumbai ranks poor 163rd (out of 218 cities

world wide) on Forbes quality of life survey

• The situation is expected to worsen over the

next decade with an expected population

increase of over 2 million

Mumbai in Reverse Gear

Mumbai contributes $ 10 Bn in taxes to the State & Center annually and gets in return a grossly inadequate $ 250 Mn for

Capital Expenditure every year

Source : Department of Economics & Statistics, McKinsey & Co., Team Analysis

GDP growth estimates*. 1997-98 to 2005-2006, CAGR, Per Cent

4.8%5.2% 6.1%

9.6%

13

Why is Urbanization taking place?

14

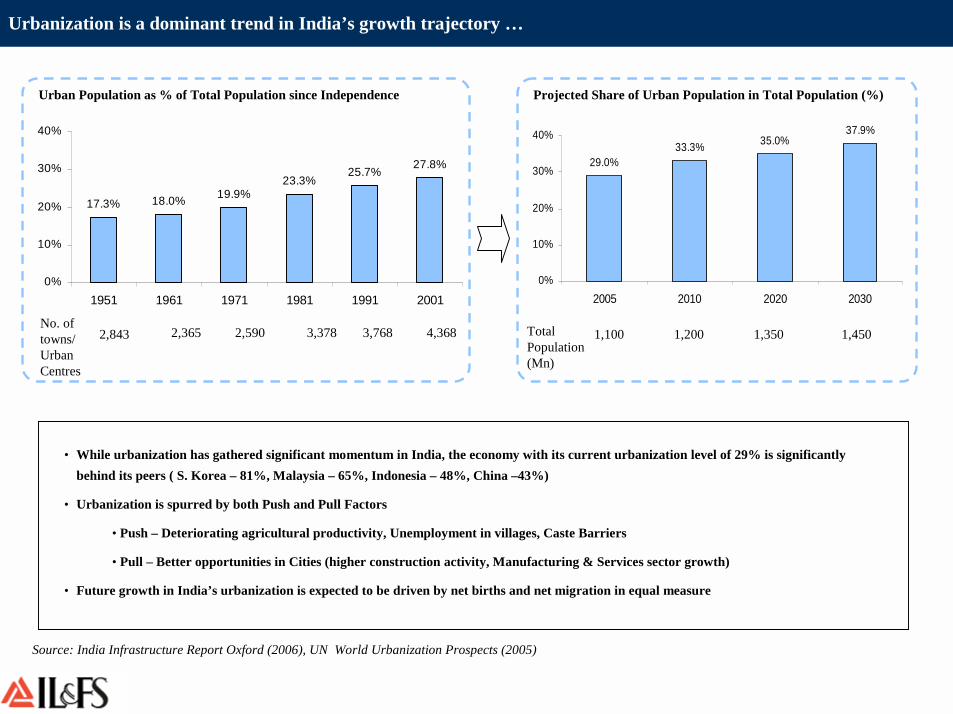

Urbanization is a dominant trend in India’s growth trajectory …

17.3% 18.0% 19.9%23.3%

25.7% 27.8%

0%

10%

20%

30%

40%

1951 1961 1971 1981 1991 2001

No. of towns/ Urban Centres

2,843 2,365 2,590 3,378 3,768 4,368

Urban Population as % of Total Population since Independence

1,100 1,200 1,350 1,450Total Population (Mn)

• While urbanization has gathered significant momentum in India, the economy with its current urbanization level of 29% is significantly behind its peers ( S. Korea – 81%, Malaysia – 65%, Indonesia – 48%, China –43%)

• Urbanization is spurred by both Push and Pull Factors

• Push – Deteriorating agricultural productivity, Unemployment in villages, Caste Barriers

• Pull – Better opportunities in Cities (higher construction activity, Manufacturing & Services sector growth)

• Future growth in India’s urbanization is expected to be driven by net births and net migration in equal measure

Projected Share of Urban Population in Total Population (%)

29.0%33.3% 35.0%

37.9%

0%

10%

20%

30%

40%

2005 2010 2020 2030

Source: India Infrastructure Report Oxford (2006), UN World Urbanization Prospects (2005)

15

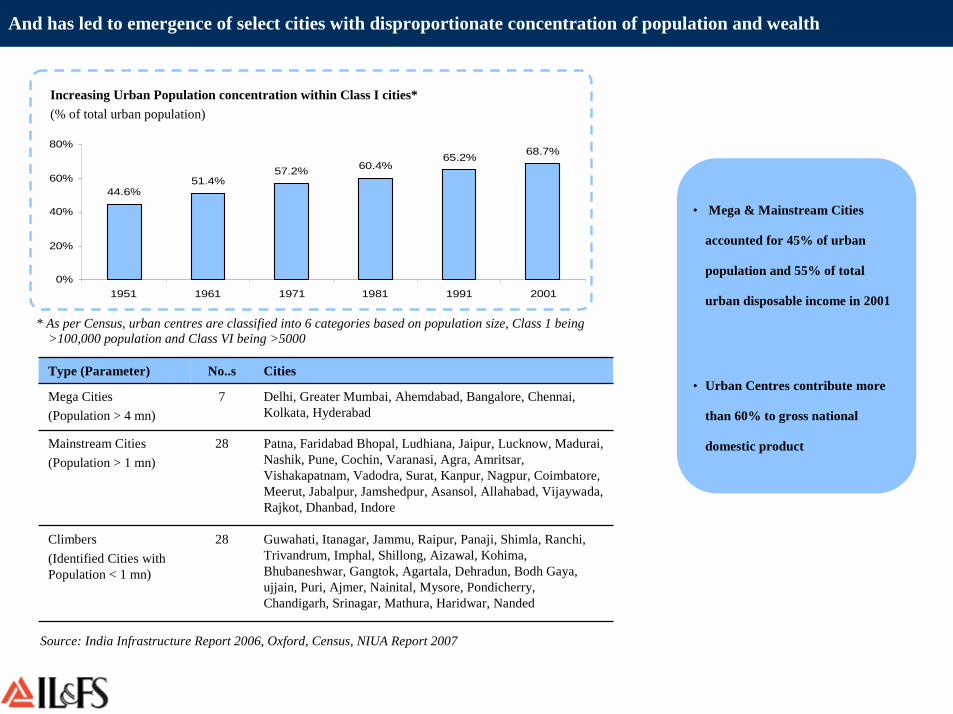

And has led to emergence of select cities with disproportionate concentration of population and wealth

28

28

7

No..s

Guwahati, Itanagar, Jammu, Raipur, Panaji, Shimla, Ranchi, Trivandrum, Imphal, Shillong, Aizawal, Kohima, Bhubaneshwar, Gangtok, Agartala, Dehradun, Bodh Gaya, ujjain, Puri, Ajmer, Nainital, Mysore, Pondicherry, Chandigarh, Srinagar, Mathura, Haridwar, Nanded

Climbers(Identified Cities with Population < 1 mn)

Patna, Faridabad Bhopal, Ludhiana, Jaipur, Lucknow, Madurai, Nashik, Pune, Cochin, Varanasi, Agra, Amritsar, Vishakapatnam, Vadodra, Surat, Kanpur, Nagpur, Coimbatore, Meerut, Jabalpur, Jamshedpur, Asansol, Allahabad, Vijaywada, Rajkot, Dhanbad, Indore

Mainstream Cities(Population > 1 mn)

Delhi, Greater Mumbai, Ahemdabad, Bangalore, Chennai, Kolkata, Hyderabad

Mega Cities(Population > 4 mn)

CitiesType (Parameter)

Source: India Infrastructure Report 2006, Oxford, Census, NIUA Report 2007

• Mega & Mainstream Cities

accounted for 45% of urban

population and 55% of total

urban disposable income in 2001

44.6%51.4%

57.2% 60.4%65.2% 68.7%

0%

20%

40%

60%

80%

1951 1961 1971 1981 1991 2001

Increasing Urban Population concentration within Class I cities*(% of total urban population)

* As per Census, urban centres are classified into 6 categories based on population size, Class 1 being >100,000 population and Class VI being >5000

• Urban Centres contribute more

than 60% to gross national

domestic product

16

The Bangalore issue

17

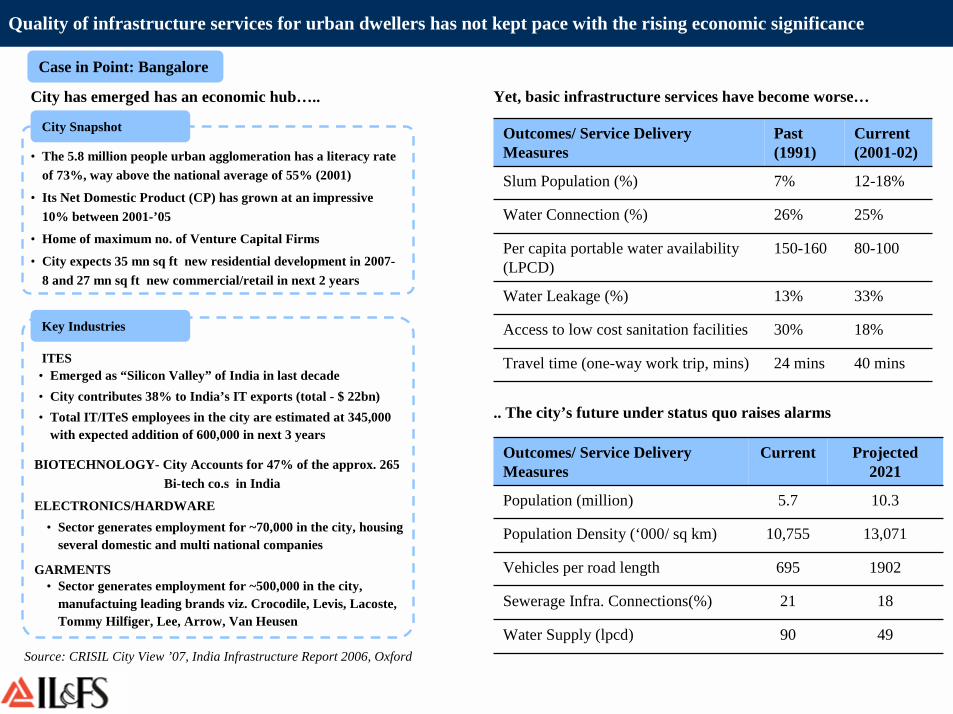

Quality of infrastructure services for urban dwellers has not kept pace with the rising economic significance

Case in Point: Bangalore

City has emerged has an economic hub…..

.. The city’s future under status quo raises alarms

40 mins24 minsTravel time (one-way work trip, mins)

18%30%Access to low cost sanitation facilities

33%13%Water Leakage (%)

80-100 150-160 Per capita portable water availability (LPCD)

25%26%Water Connection (%)

12-18%7%Slum Population (%)

Current (2001-02)

Past (1991)

Outcomes/ Service Delivery Measures

• Sector generates employment for ~70,000 in the city, housing several domestic and multi national companies

Yet, basic infrastructure services have become worse…

Source: CRISIL City View ’07, India Infrastructure Report 2006, Oxford

1821Sewerage Infra. Connections(%)

4990Water Supply (lpcd)

1902695Vehicles per road length

13,07110,755Population Density (‘000/ sq km)

10.35.7Population (million)

Projected 2021

CurrentOutcomes/ Service Delivery Measures

• The 5.8 million people urban agglomeration has a literacy rate of 73%, way above the national average of 55% (2001)

• Its Net Domestic Product (CP) has grown at an impressive 10% between 2001-’05

• Home of maximum no. of Venture Capital Firms

• City expects 35 mn sq ft new residential development in 2007-8 and 27 mn sq ft new commercial/retail in next 2 years

City Snapshot

Key Industries

ITES• Emerged as “Silicon Valley” of India in last decade• City contributes 38% to India’s IT exports (total - $ 22bn)• Total IT/ITeS employees in the city are estimated at 345,000

with expected addition of 600,000 in next 3 years

BIOTECHNOLOGY- City Accounts for 47% of the approx. 265 Bi-tech co.s in India

ELECTRONICS/HARDWARE

• Sector generates employment for ~500,000 in the city, manufactuing leading brands viz. Crocodile, Levis, Lacoste, Tommy Hilfiger, Lee, Arrow, Van Heusen

GARMENTS

18

What is the Solution?

19

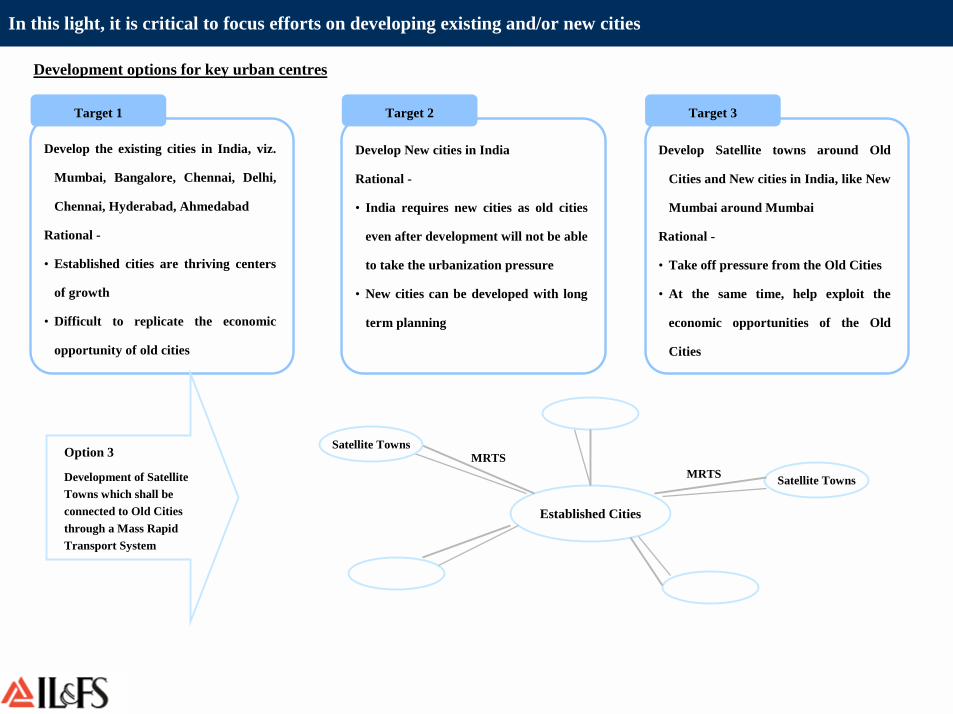

Target 1

Develop the existing cities in India, viz.

Mumbai, Bangalore, Chennai, Delhi,

Chennai, Hyderabad, Ahmedabad

Rational -

• Established cities are thriving centers

of growth

• Difficult to replicate the economic

opportunity of old cities

Target 2 Target 3

Established Cities

Satellite Towns

Satellite Towns

Develop New cities in India

Rational -

• India requires new cities as old cities

even after development will not be able

to take the urbanization pressure

• New cities can be developed with long

term planning

Develop Satellite towns around Old

Cities and New cities in India, like New

Mumbai around Mumbai

Rational -

• Take off pressure from the Old Cities

• At the same time, help exploit the

economic opportunities of the Old

Cities

MRTSMRTSOption 3

Development of Satellite Towns which shall be connected to Old Cities through a Mass Rapid Transport System

In this light, it is critical to focus efforts on developing existing and/or new cities

Development options for key urban centres

20

What is the Rationale for the Solution?

21

Our Dual Return Approach

Before Infrastructure Development After Infrastructure Development

Developed City with infrastructure in place

Real estate price – 5x

Land parcel near to developed city

Real estate price – 0.5x

Distance of 35 – 40 Km

After a period of 5 years

Real estate price – 8x

Develop Infrastructure on the Land Parcel

Real estate price – 5x

Mass Rapid

Transport System

Dual returns for Investors

Health CareSanitation

Waste ManagementWater Supply

TelecommunicationCivil Structures

Independent Power PlantsRoad/ Highways/ Freeways

Investment in Allied Infrastructure of the New City

Investment in Real Estate of the New City

Along with

Steady stream of Cash Flows per annum

The appreciation of Real Estate Price

As in this case from 0.5x to 5x

Example : Independent Power Plant

IPP shall be a JV (74%:26%) between a Power Major & the Fund, hence part of the returns shall come from the Profits of the IPP in form of Dividends

Aim is to Develop Urban

Infrastructure creating

Captive Demands in

Infrastructure and share

the upside with the

investors in

infrastructure as well as

Real Estate

22

Shanghai : A Case in point

23

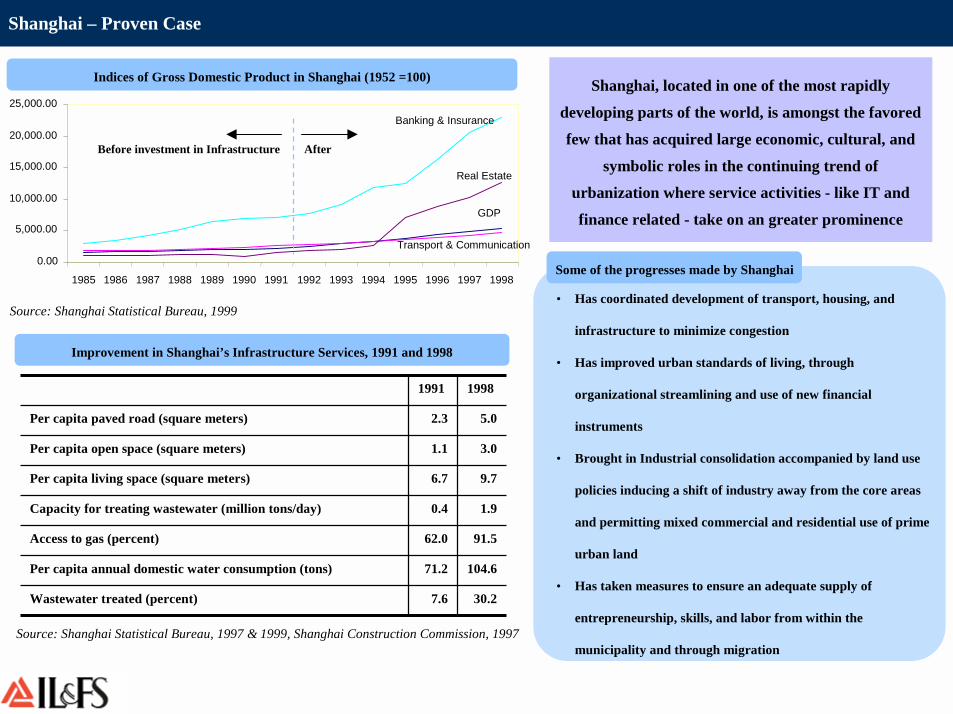

Shanghai – Proven Case

• Has coordinated development of transport, housing, and

infrastructure to minimize congestion

• Has improved urban standards of living, through

organizational streamlining and use of new financial

instruments

• Brought in Industrial consolidation accompanied by land use

policies inducing a shift of industry away from the core areas

and permitting mixed commercial and residential use of prime

urban land

• Has taken measures to ensure an adequate supply of

entrepreneurship, skills, and labor from within the

municipality and through migration

Some of the progresses made by Shanghai

30.27.6Wastewater treated (percent)

104.671.2Per capita annual domestic water consumption (tons)

91.562.0Access to gas (percent)

1.90.4Capacity for treating wastewater (million tons/day)

9.76.7Per capita living space (square meters)

3.01.1Per capita open space (square meters)

5.02.3Per capita paved road (square meters)

19981991

Source: Shanghai Statistical Bureau, 1997 & 1999, Shanghai Construction Commission, 1997

Improvement in Shanghai’s Infrastructure Services, 1991 and 1998

0.00

5,000.00

10,000.00

15,000.00

20,000.00

25,000.00

1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998

GDP

Transport & Communication

Banking & Insurance

Real Estate

Indices of Gross Domestic Product in Shanghai (1952 =100)

Source: Shanghai Statistical Bureau, 1999

Before investment in Infrastructure After

Shanghai, located in one of the most rapidly

developing parts of the world, is amongst the favored

few that has acquired large economic, cultural, and

symbolic roles in the continuing trend of

urbanization where service activities - like IT and

finance related - take on an greater prominence

24

Our Approach to the Solution

25

Improving existing cities & creating Self-sustaining New Cities

Residential Housing Projects

High rise Business District

• Benchmark office high rise district

• Anchor developers to be given land at

concessional rates; efforts to be made in

conjunction with developers to attract key

anchor tenants

Social Infrastructure

Technology

Overall Connectivity/ transport Retail cum entertainment hubs

• Well panned residential housing projects

• Walk to work layouts

• Educational institutes to be established

• International schools for primary education

• Privatised hospitals with infrastructure to

be established

• Broadband FTTP

• WiFi/ Wimax

• Shared IT Services

• MRTS connecting old cities

• Expressway to airport

• High speed train to Bombay

• High quality entertainment malls to be set

up

• Over 60% of the space is planned to be

green

Basic Infrastructure

• Uninterrupted and highly reliable power

supply potentially generated through a

captive power plant in the long run

• Reliance on non-conventional sources

Urban Infrastructure Development

Develop New

Cities

Develop Existing

Cities

Gives Opportunity to develop different aspects of infrastructure considering their inter-dependability & long term demand of next 100 years

Target 1

Target 2

Gives opportunity to take advantage of the already thriving economic potential

New Paradigm in Urban PlanningCity’s master plan to serve as the Vibrant

Hub

26

What is the Deal?

27

Gujarat International Finance Tech-City - GIFT

+• Booming demand in Financial & IT

Services

• India’s financial capital, Mumbai, saddled with crumbling infrastructure and sky-rocketing cost of business operations

• Lack of any methodically planned and developed world-class International Finance Centre (IFC)

• State Govt. of Gujarat (GoG) spearheading a slew of initiatives to usher economic prosperity through public-private efforts and investment in the State

• Gujarat’s economy recorded CAGR of 9% in last 3 years, set itself the highest target CAGR of 11.4 % under India’s 11th 5-year plan

GoG and Infrastructure Leasing and Financial Services Ltd. (IL&FS)join hands to conceive, plan and develop

Gujarat International Finance Tec-City

+• A premium institution with a proven

track record in infrastructure and financial services

• Pioneer in launching infrastructure projects on a PPP model in India

• Widespread experience in planning and development of large-scale commercially viable Infrastructure projects

An Opportunity A Pro-active State Govt IL&FS

28

Where is the Project?

29

• The City additionally benefits from the Sabarmati river demarcating it’s eastern boundary

GIFT is strategically located in close proximity to the commercial hub of Gujarat as well as Mumbai

Gujarat

GandhinagarGIFT

545

8

12

Distance (kms) Primary Travel Mode

Road@- Dedicated 8 lane

expressway; LRTS

Ahmedabad

Air* ( 1 hr flying time),

Train (8 hrs)

Gandhinagar

Mumbai

@ GIFT site currently abuts a four lane National Highway connecting Ahemdabad

and Gandhinagar (LRTS and expressway to be developed)

* Nearest Airport to GIFT, Ahemdabad Intl. Airport, is very well connected to

Mumbai with over 12 flights a day (one way)

30

What is the Value Proposition?

31

GIFT presents a compelling value proposition

GIFT

Integrated Utilities

DefinedPositioning

StrongGovt. Backing

World Class Infrastructure

Excellent Connectivity

• A brand new 506 acre city designed to be a globally benchmarked

International Finance Centre

• Located in the rapidly developing state of Gujarat between it’s State capital,

Gandhinagar, and its commerce capital, Ahemdabad

• To serve as the central business hub for an Integrated Township sprawling

over 27,000 acres

• Developed with the full backing of a proactive and result oriented State

Govt.• Service emerging business requirements in financial services &

IT/ITeS sectors that Mumbai is not in a position to address

• In close proximity to Ahemdabad, a premium tier 2 city, and also

close to Mumbai vis-à-vis other cities

• Be a first of it’s kind development in the country in terms of scale,

scope and quality of offerings

• State of the art physical/social/ IT infrastructure and world class

connectivity at affordable price points • Special Economic Zone benefits including concessionary tax and

regulatory policies for all the stakeholders

• Provide opportunity for business at less than half the cost of Mumbai

32

Who are the Partners to GIFT?

33

Consultants Engaged by GIFTCL

Environmental Aspects

Talent Demand Assessment

Market Demand Assessment

Process Management

ICT Advisory Services

Design & ArchitectureConsortium of East China Architectural Design Institute (ECADI) & Fairwood

India Pvt. Ltd.

IL&FS Ecosmart Limited

34

What is the Bouquet of Offering?

35

This new IFC would be a world-class bouquet of offerings

36

What is the Macro-Economic Perspective?

37

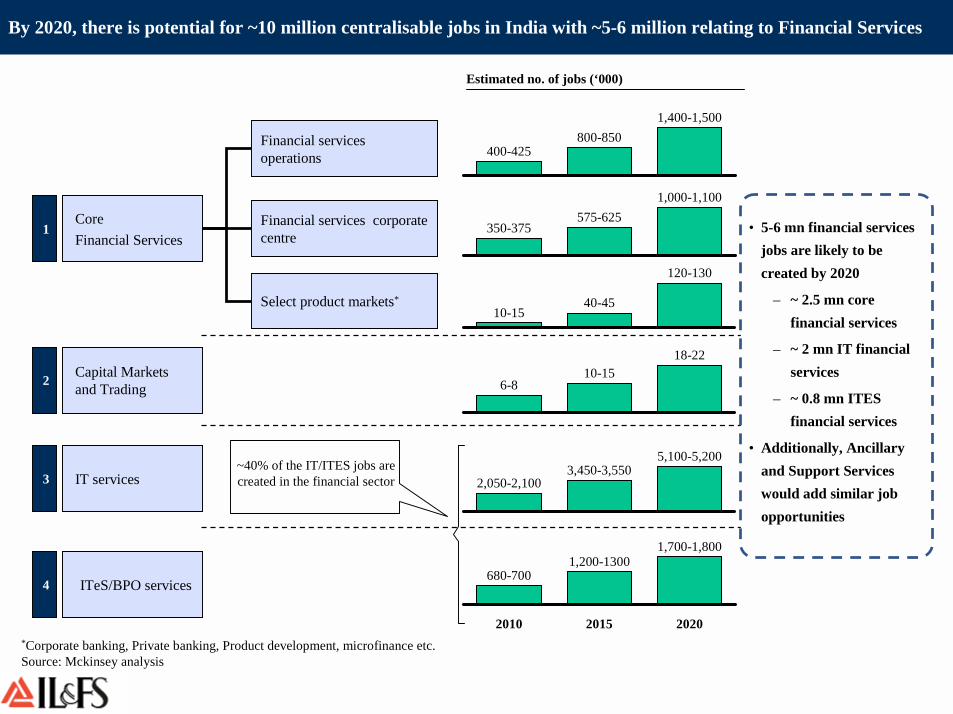

By 2020, there is potential for ~10 million centralisable jobs in India with ~5-6 million relating to Financial Services

37

Estimated no. of jobs (‘000)

400-425800-850

1,400-1,500

350-375575-625

1,000-1,100

10-1540-45

120-130

2,050-2,1003,450-3,550

5,100-5,200

680-700

2010

1,200-1300

2015

1,700-1,800

2020

~40% of the IT/ITES jobs are created in the financial sector

• 5-6 mn financial services jobs are likely to be created by 2020

– ~ 2.5 mn core financial services

– ~ 2 mn IT financial services

– ~ 0.8 mn ITES financial services

• Additionally, Ancillary and Support Services would add similar job opportunities

6-810-15

18-22

*Corporate banking, Private banking, Product development, microfinance etc.Source: Mckinsey analysis

Core Financial Services

IT services

ITeS/BPO services

Financial services operations

Financial services corporate centre

Capital Markets and Trading

Select product markets*

1

3

4

2

38

What is the Target Focus?

39

GIFT would focus on nine specific opportunities emerging within Financial Services sector

1. National Financial services operations’ hub

2. Regional/functional Head quarters for financial services players

3. National head quarters for players

4. Private Banking hub for NRIs/ Regional HNWs5. International microfinance hub

Core Financial Services

8. Global Hub for IT services for Financial services sector IT services

9. Global Hub for BPO services for Financial services sectorITeS/BPO

services

6. International commodity trade hub

7. Participation in global capital markets Capital Markets and Trading

Financial services operations

Financial services corporate centre

Select product markets

GIFT’s focus segments

GIFT aims to generate 0.3 mn direct and 0.6 mn indirect employment by

2020

40

What is the Value Proposition for the Occupier?

41

Value proposition for the Occupiers in GIFT

4070300375Lease Rentals (Rs/month)

331,110

52

Mumbai

259,350

40

Delhi

128,310

45

Bangalore

78,000

17

Ahmedabad

Manpower Cost (Rs/ hr)

Workstation Cost (Rs/ 100 sq ft seat/ annum)

Particulars

Comparison of Cost Structure across Cities…

• Both, the Manpower Cost and Workstation Cost at GIFT would be comparable to those in Ahmedabad

• It has to be noted that GIFT is planned to be developed and benchmarked as an International Financial Center for

India and hence the quality of infrastructure at GIFT will be far superior as compared to the existing infrastructure

in these cities

… How GIFT if more attractive than any other City in India

• Infrastructure developments and linkages are done from scratch keeping in mind long term growth in urbanization

• Regional infrastructure and economic growth drivers are cherry picked to suit the occupiers’ need

• Reduction of dependence on local government by Municipal bodies and the new city is run as an enterprise with thrust on self-governance

• Regulatory framework is tailor made as per the needs of the city

• Land and sectoral demand-supply scenario are chosen keeping in mind future growth and land availability

• Demographic profiles is well balanced and controlled

• New city attracts world class Educational Institutes

• Restricted access and high surveillance keeps law and order in check

• Availability of quality workforce is a planned concept with thrust on specific sectors to create ample opportunities and good quality of life to sustain the workforce

Advantages of setting up a New City like GIFT

Cost & Facilities Advantage for the Occupier

Infrastructure Advantage for the Occupier

Source: NASSCOM, DTZ

42

What is the Development Plan?

43

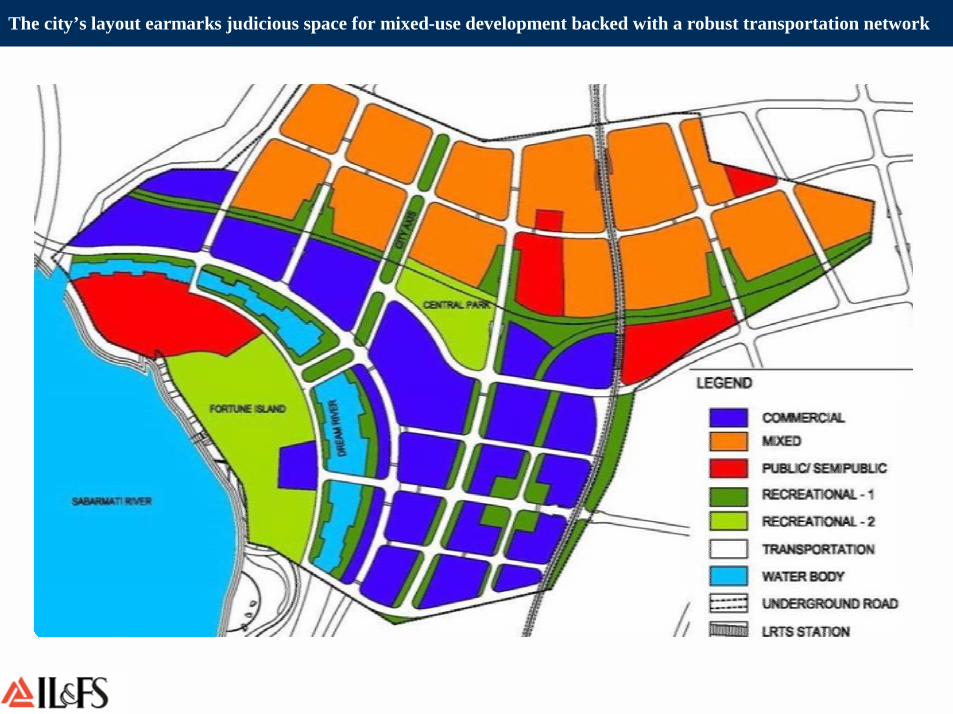

The city’s layout earmarks judicious space for mixed-use development backed with a robust transportation network

43

44

What is the Project Configuration?

45

Real Estate would be a key feature of GIFT’s development plan

Height of 3 landmark buildings above 250 m , 11 buildings above 150 m

45

• Real Estate at GIFT has been planned to cater to 0.3 million working population and 50,000 resident population

• Commercial development is the primary focus of development with ~70% built up space dedicated to it

• However due emphasis would be given towards residential development and social infrastructure as they are vital to keeping the city alive

• GIFT enjoys FSR of 3.65 which would be predominantly used vertically thereby maximizing open spaces and green areas (65% space)

• GIFT’s tallest building, Diamond Towers, would dominate the city skyline with a height of 400 m

0.3%18.2%Transportation

Built Up Area (%)Land Use (%)

67.8%21.6%Commercial

100%

506 acres

1.1%

30.0%

12.8%

16.5% 20.4%Mixed*

Public & Semi -

Public11.3%

Recreational -

Utilities 0.2%

Total100% 75

mn sq ft

* Mixed Use Development to comprise of Residential and Commercial including offices, retail, and recreational

46

How does GIFT compare Internationally?

47

The City has been designed to be at par or above with Globally Benchmarked IFCs

In terms of scale and sheer physical scope, GIFT is being designed to be at or above par with presently acknowledged Globally Benchmarked International Financial Centers (IFCs)

In terms of scale and sheer physical scope, GIFT is being designed to be at or above par with presently acknowledged Globally Benchmarked International Financial Centers (IFCs)

Paris La Defense

Tokyo London Pudong GIFT

Land use Scale (sq km) 1.6 1.6 1.05 1.7 2.02

Construction Scale (in mn sq m) 2.5 1.6 1.1 4.5 7.5

Floor-area Ratio 1.56 1.00 1.05 2.65 3.65

Greenbelt (in thousand sq m) 40 120 50 363 615

Height (m) 200 250 250 490 410

Paris La Defense Tokyo (Shinjuku) London Dockyards Pudong (Lujiazui) GIFT

48

How does GIFT look?

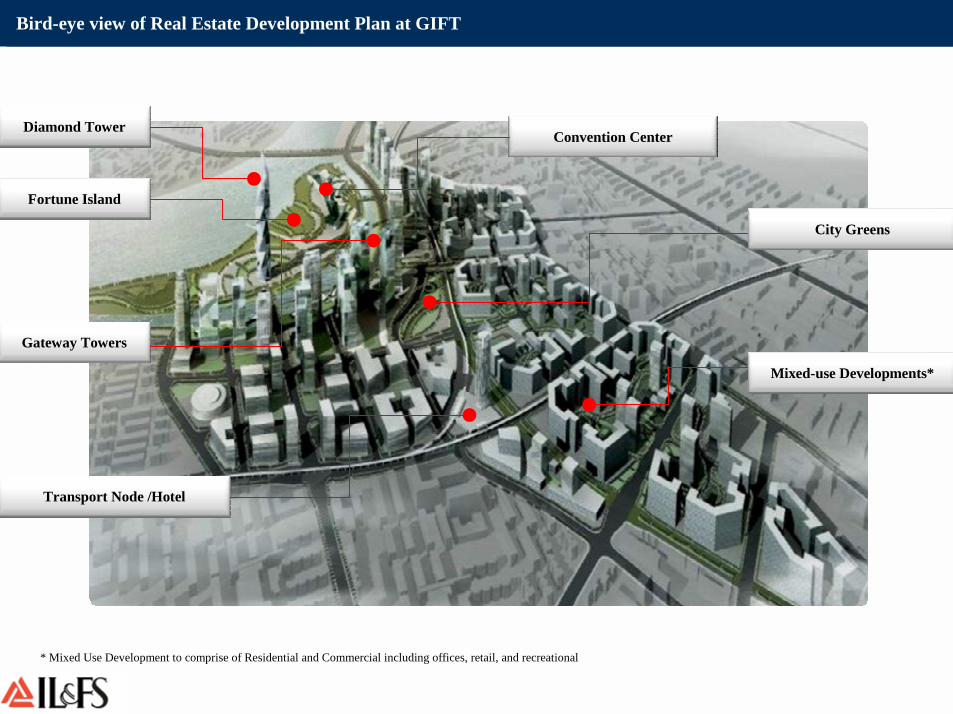

49 49

Diamond Tower

Transport Node /Hotel

Gateway Towers

Fortune Island

Convention Center

Mixed-use Developments*

City Greens

Bird-eye view of Real Estate Development Plan at GIFT

* Mixed Use Development to comprise of Residential and Commercial including offices, retail, and recreational

50

What are the Land Mark Buildings?

51

Diamond TowerDiamond TowerThe dominant feature of the cityThe dominant feature of the city

Height Height -- 400 m400 m

Gateway TowersGateway TowersMark entrance to the city from arterial streetsMark entrance to the city from arterial streets

creating identity for the city axis creating identity for the city axis

Some of the Signature Developments at GIFT

51

52

Dream River Dream River

Makes identifiable meeting places with 15m wide promenade.Makes identifiable meeting places with 15m wide promenade.

This promenade will also function as a major spine for pedestriThis promenade will also function as a major spine for pedestrians and will ans and will be a significant recreational facility. be a significant recreational facility.

Convention Center•The low rise building along the river edge on the Fortune Island marks a landmark with the proposed art galleries and museum

Transportation Hub•Transportation Hubs mark the edge of the city

52

Some of the Signature Developments at GIFT

53

What is the Infrastructure Story?

54

GIFT Infrastructure Overview

• All infrastructure services to support businesses including connectivity, IT, walk-to-work housing, security and services to support a globally acceptable quality of life have been integrated into the design of the city

• Common aspects of infrastructure needs and requirements are integrated to ensure planning for sustainable and affordable development to meet the growth of GIFT.

• Modern and innovative technology in infrastructure provision is utilized to improve service levels and to attain a high quality environment.

• All infrastructure and utilities service providers are controlled & coordinated and Targets for quality – waste, water and energy resources – are set within GIFT.

Investment Opportunities for Infrastructure Developers:

• Core Infrastructure- Site Development- Landscaping- Maintenance Systems

• Transportation & Utilities- Roads and Transportation- Water Systems- ICT- Power Generation and

Distribution- HVAC- Domestic Gas Distribution- Waste Management Systems

55

What is the Transportation Linkage?

56

GIFT Infrastructure: Transport

• Transit oriented transport –Walk to work after exiting a major node of the public transport system• Segregated vehicular and pedestrian movement and abundant parking provision• Aim to achieve a modal split of (10:90) between private & public transport• Road network of freeways, expressways, highways, arterial roads, collector streets, and pedestrian paths• Intra-City Travel

• Combination of LRTS and CRT Bus Lanes linking neighborhoods and districts• Max trip time estimated at 30 minutes between the farthest points of the city

• Inter City Travel • – LRTS at GIFT to be linked to the proposed MRTS between Ahemdabad and Gandhinagar

(independent Govt. plan) thereby linking GIFT with other urban regions in Gujarat

Completely developed site with high quality internal roads and landscaping

Rationalized and efficient transport planning, design and engineering resulting in

• Reduced stress on land as resource; • Reduced air and noise pollution; • Energy efficiency; • Increased green belts

Accessibility and linkages:• LRTS, CRT• Underground arterial road• Abundant parking Space

57

What is the Road, Water, Landscaping Plan?

58

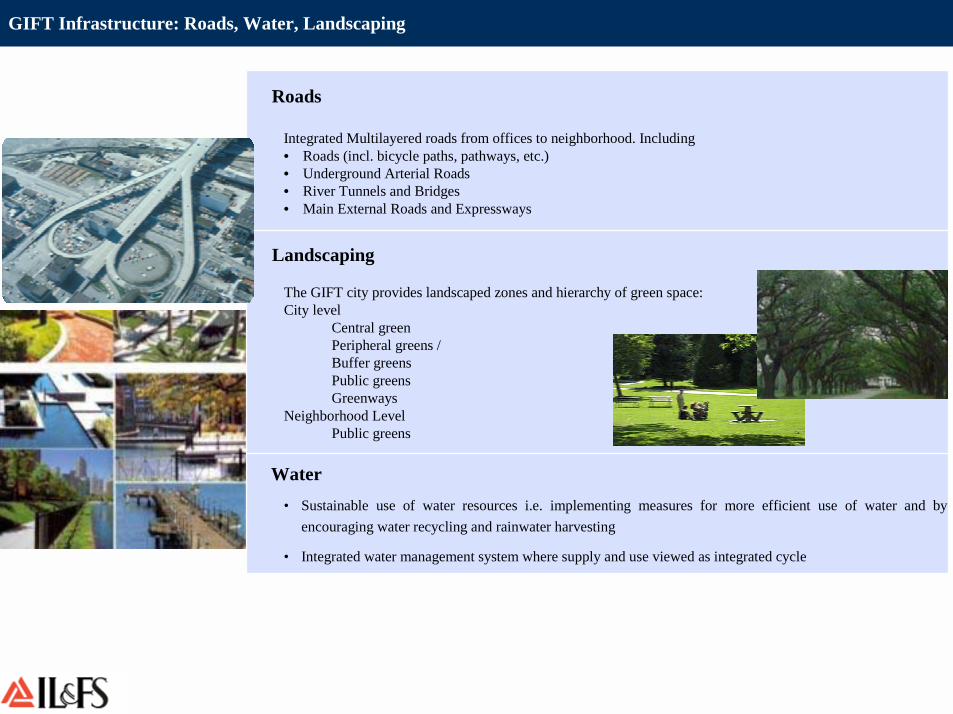

GIFT Infrastructure: Roads, Water, Landscaping

Roads

Integrated Multilayered roads from offices to neighborhood. Including • Roads (incl. bicycle paths, pathways, etc.)• Underground Arterial Roads• River Tunnels and Bridges• Main External Roads and Expressways

Landscaping

The GIFT city provides landscaped zones and hierarchy of green space:City level

Central greenPeripheral greens /Buffer greensPublic greensGreenways

Neighborhood LevelPublic greens

Water • Sustainable use of water resources i.e. implementing measures for more efficient use of water and by

encouraging water recycling and rainwater harvesting

• Integrated water management system where supply and use viewed as integrated cycle

59

What is the support on Utilities?

60

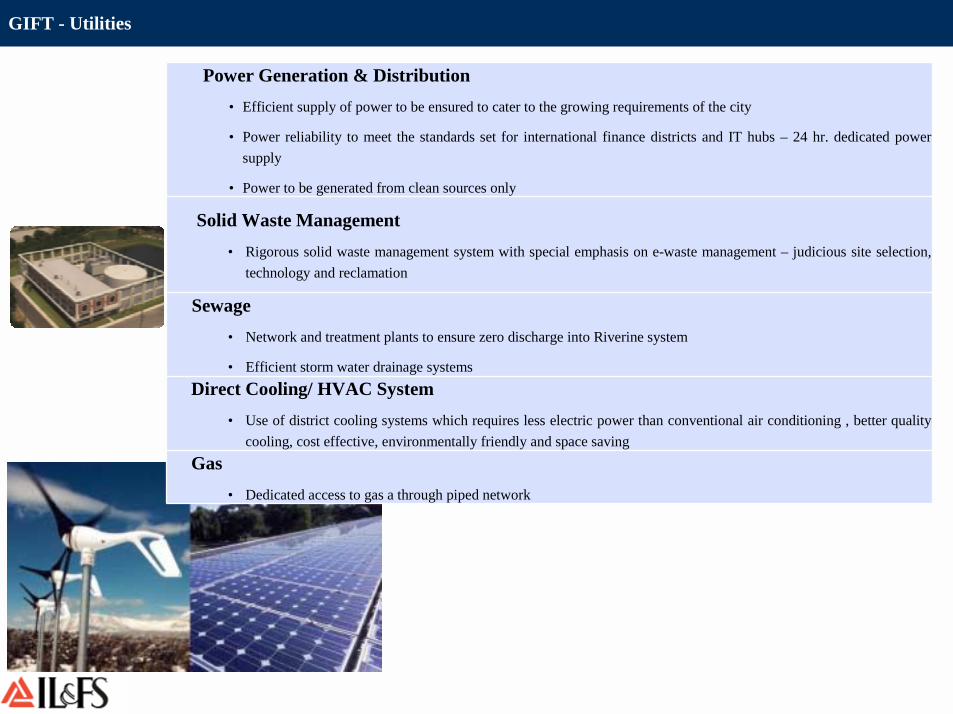

GIFT - Utilities

Direct Cooling/ HVAC System• Use of district cooling systems which requires less electric power than conventional air conditioning , better quality

cooling, cost effective, environmentally friendly and space saving

Sewage• Network and treatment plants to ensure zero discharge into Riverine system

• Efficient storm water drainage systems

Power Generation & Distribution• Efficient supply of power to be ensured to cater to the growing requirements of the city

• Power reliability to meet the standards set for international finance districts and IT hubs – 24 hr. dedicated power supply

• Power to be generated from clean sources only

Solid Waste Management• Rigorous solid waste management system with special emphasis on e-waste management – judicious site selection,

technology and reclamation

Gas• Dedicated access to gas a through piped network

61

How good is the Telecom Connectivity?

62

GIFT - ICT

• Access to high speed network and cutting edge IP based networks allowing seamless voice, video and data integration and use of advanced end user applications.

• Greater bandwidth (due to wired city fibre connected) – a bandwidth of 100 Mbit/s scalable to Gbit/s would be possible from the start.

• Residential and intelligent building services such as high speed internet access, telephony services (VoIP, PSTN), IPTV, video on demand, home security (CCTV alarms), automation (lighting & heating control, energy management, appliances and remote control, etc.)

• A robust tier IV date centre with guaranteed SLAs for uptime with properly backed up remote disaster recovery site as fall back.

• Local area networking, intra office/building wireless access, video conferencing.• A self contained network management and operations to support the services and performance SLAs.

Access to high speed network infrastructure and modern technology

Secured and converged network – lower cost of ownership and improved employee productivity

Universal access gateways and interfaces for citizens on the move, anytime, anywhere

Additional features such as intelligent buildings, e government, etc

Speedy setting-time for businesses with Plug-and-Play services

63

Does GIFT have an SEZ status?

64

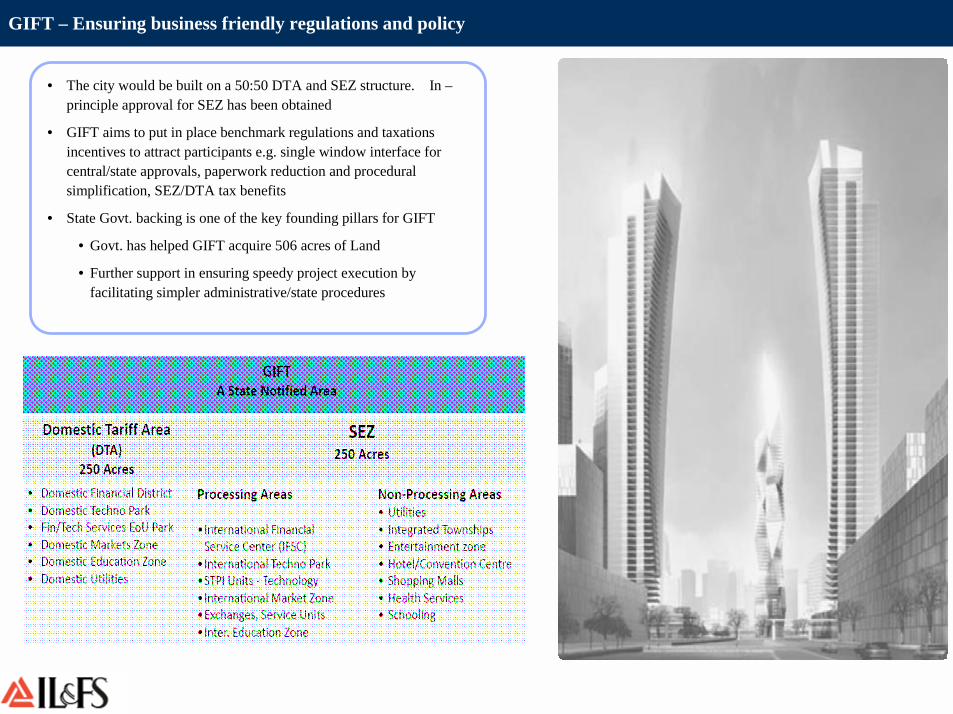

GIFT – Ensuring business friendly regulations and policy

• The city would be built on a 50:50 DTA and SEZ structure. In –principle approval for SEZ has been obtained

• GIFT aims to put in place benchmark regulations and taxations incentives to attract participants e.g. single window interface for central/state approvals, paperwork reduction and procedural simplification, SEZ/DTA tax benefits

• State Govt. backing is one of the key founding pillars for GIFT

• Govt. has helped GIFT acquire 506 acres of Land

• Further support in ensuring speedy project execution by facilitating simpler administrative/state procedures

65

What does GIFT have in store for the Investors?

66

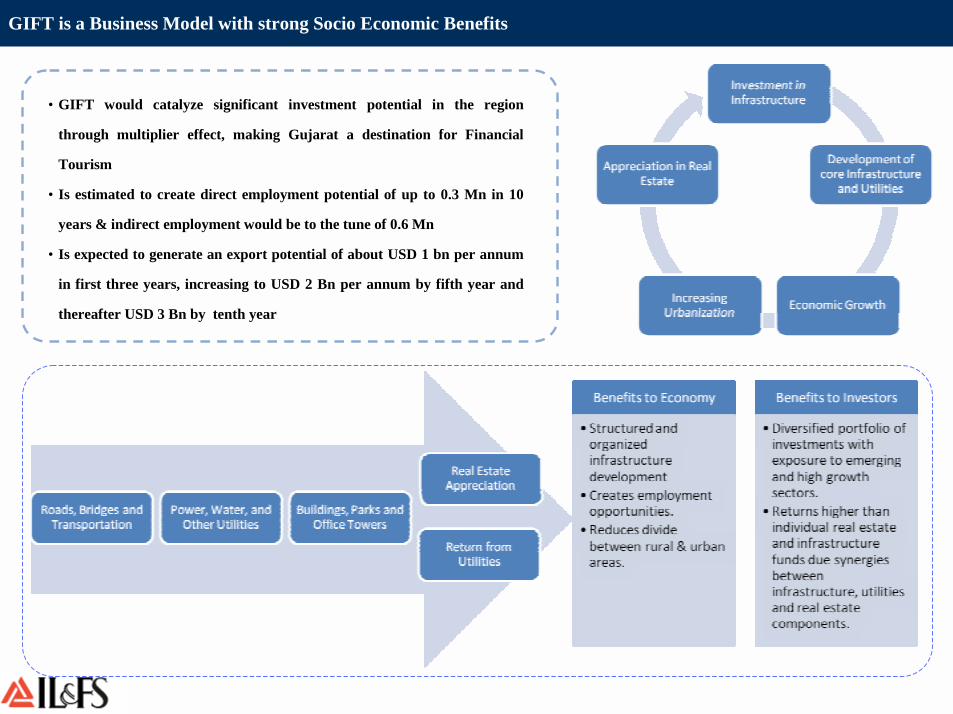

GIFT is a Business Model with strong Socio Economic Benefits

• GIFT would catalyze significant investment potential in the region

through multiplier effect, making Gujarat a destination for Financial

Tourism

• Is estimated to create direct employment potential of up to 0.3 Mn in 10

years & indirect employment would be to the tune of 0.6 Mn

• Is expected to generate an export potential of about USD 1 bn per annum

in first three years, increasing to USD 2 Bn per annum by fifth year and

thereafter USD 3 Bn by tenth year

67

What is the Cost and Phasing?

68

GIFT would be developed in between 2007-2017 at a total cost of ~ US $ 16.33 bn

Core Infrastructure 1.35

Semi Viable Infrastructure 1.37

Utilities 8.31

Buildings 5.31

Total Project Value 16.33

Estimated Project Cost

US Billion

69

How is GIFT being Organized?

70

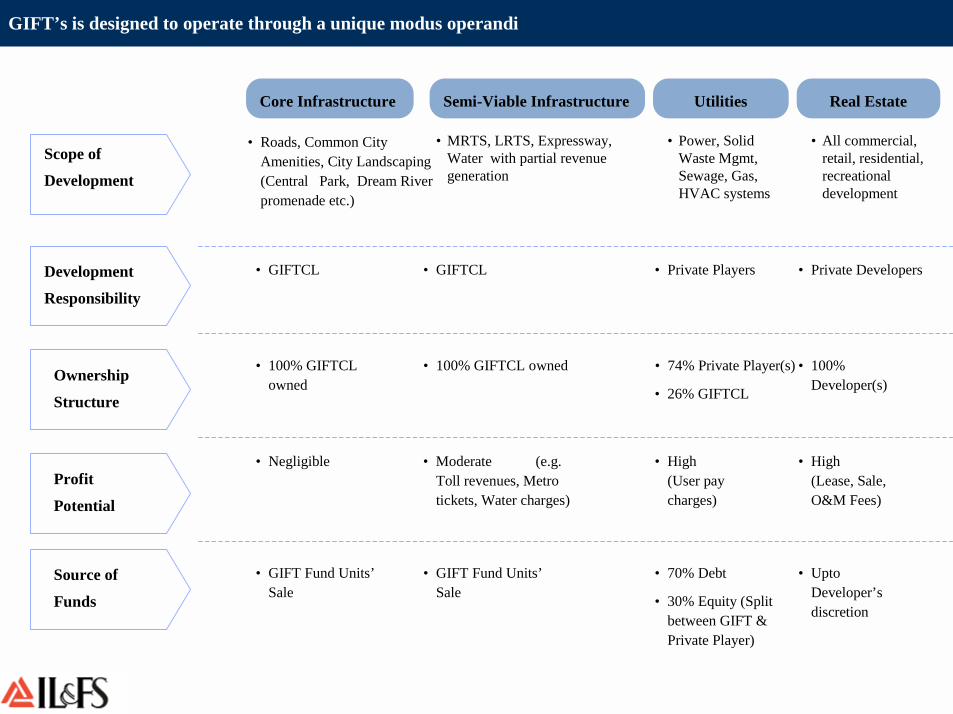

GIFT’s is designed to operate through a unique modus operandi

Real EstateCore Infrastructure

Scope of

Development

Ownership

Structure

• Private Players

Semi-Viable Infrastructure Utilities

Source of

Funds

• Roads, Common City Amenities, City Landscaping (Central Park, Dream River promenade etc.)

• MRTS, LRTS, Expressway, Water with partial revenue generation

Development

Responsibility

• GIFTCL • GIFTCL • Private Developers

• 100% GIFTCL owned

• 100% GIFTCL owned • 74% Private Player(s)

• 26% GIFTCL

• Power, Solid Waste Mgmt, Sewage, Gas, HVAC systems

Profit

Potential

• Negligible • Moderate (e.g. Toll revenues, Metro tickets, Water charges)

• High (User pay charges)

• High (Lease, Sale, O&M Fees)

• All commercial, retail, residential, recreational development

• 100% Developer(s)

• GIFT Fund Units’Sale

• GIFT Fund Units’Sale

• 70% Debt

• 30% Equity (Split between GIFT & Private Player)

• Upto Developer’s discretion

71

What are the Components of the Project cost?

72

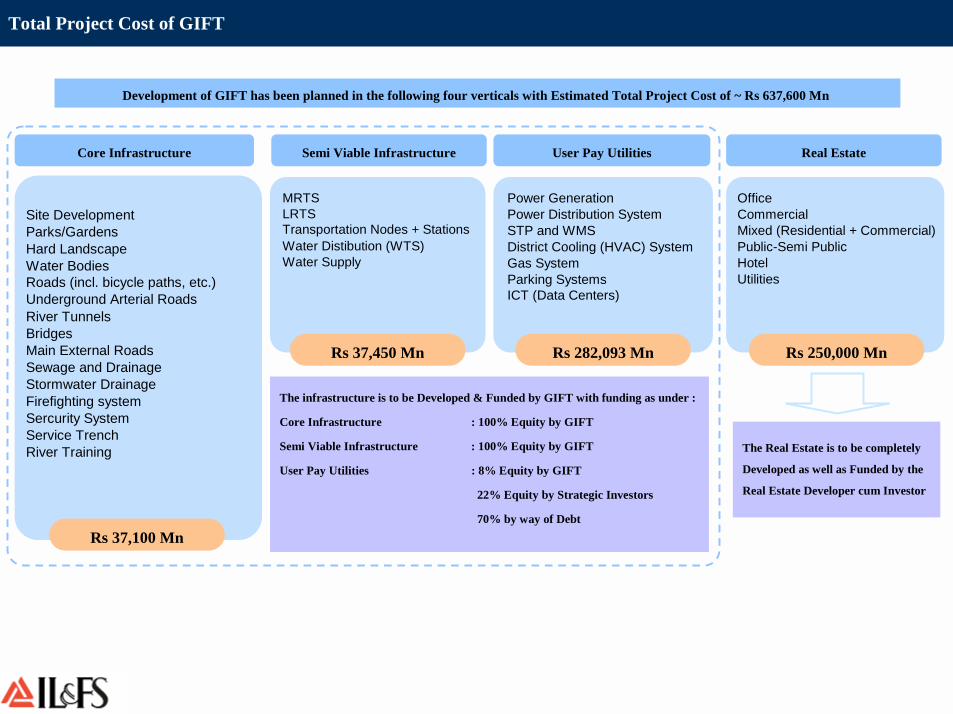

Total Project Cost of GIFT

MRTSLRTS Transportation Nodes + StationsWater Distibution (WTS)Water Supply

Power GenerationPower Distribution SystemSTP and WMSDistrict Cooling (HVAC) SystemGas SystemParking SystemsICT (Data Centers)

OfficeCommercialMixed (Residential + Commercial)Public-Semi Public HotelUtilities

Core Infrastructure Semi Viable Infrastructure User Pay Utilities Real Estate

Rs 37,100 Mn

Rs 37,450 Mn Rs 282,093 Mn Rs 250,000 Mn

Development of GIFT has been planned in the following four verticals with Estimated Total Project Cost of ~ Rs 637,600 Mn

The infrastructure is to be Developed & Funded by GIFT with funding as under :

Core Infrastructure : 100% Equity by GIFT

Semi Viable Infrastructure : 100% Equity by GIFT

User Pay Utilities : 8% Equity by GIFT

22% Equity by Strategic Investors

70% by way of Debt

The Real Estate is to be completely

Developed as well as Funded by the

Real Estate Developer cum Investor

Site DevelopmentParks/GardensHard LandscapeWater BodiesRoads (incl. bicycle paths, etc.)Underground Arterial RoadsRiver TunnelsBridgesMain External RoadsSewage and DrainageStormwater DrainageFirefighting systemSercurity SystemService TrenchRiver Training

73

What is the Value Proposition

74

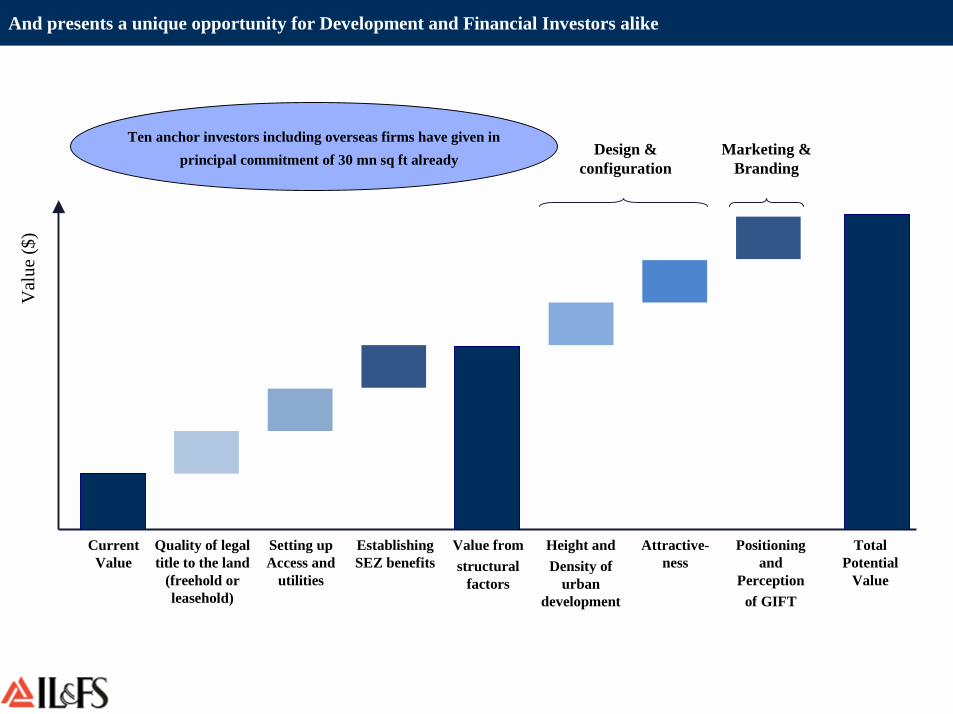

And presents a unique opportunity for Development and Financial Investors alike V

alue

($)

Current Value

Value fromstructural

factors

Design & configuration

Marketing & Branding

Height andDensity of

urban development

Attractive-ness

Positioning and

Perceptionof GIFT

Quality of legal title to the land

(freehold or leasehold)

Setting up Access and

utilities

Establishing SEZ benefits

Total Potential

Value

Ten anchor investors including overseas firms have given in principal commitment of 30 mn sq ft already

75

What is the Team for the Project?

76

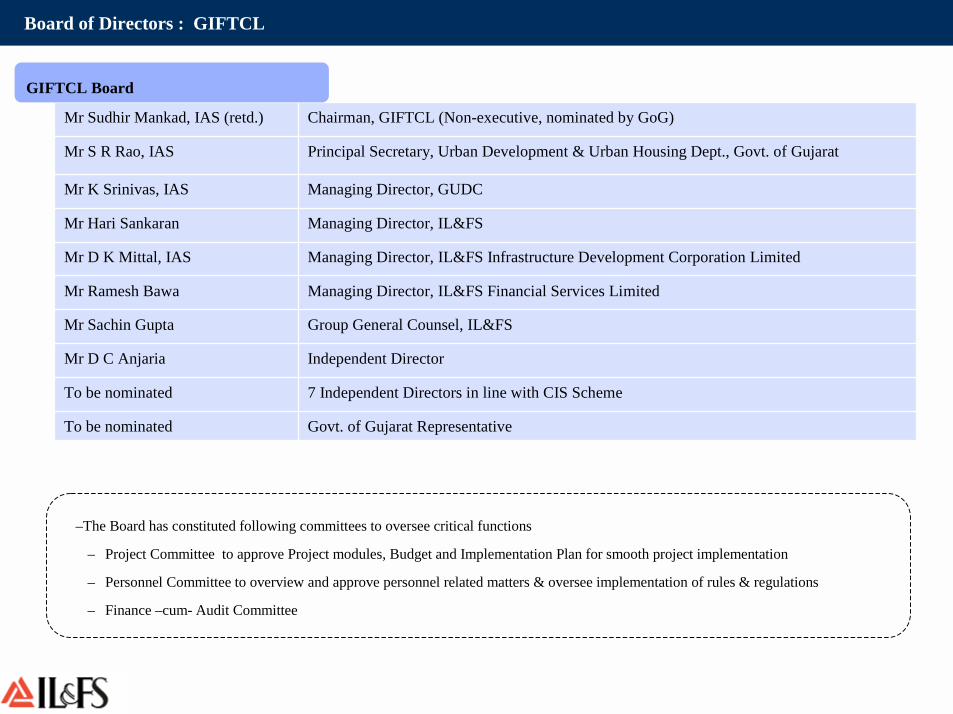

Board of Directors : GIFTCL

Independent DirectorMr D C Anjaria

7 Independent Directors in line with CIS SchemeTo be nominated

Managing Director, IL&FS Infrastructure Development Corporation LimitedMr D K Mittal, IAS

Principal Secretary, Urban Development & Urban Housing Dept., Govt. of GujaratMr S R Rao, IAS

Managing Director, GUDCMr K Srinivas, IAS

Mr Sudhir Mankad, IAS (retd.) Chairman, GIFTCL (Non-executive, nominated by GoG)

Mr Hari Sankaran Managing Director, IL&FS

Mr Ramesh Bawa Managing Director, IL&FS Financial Services Limited

Mr Sachin Gupta Group General Counsel, IL&FS

To be nominated Govt. of Gujarat Representative

GIFTCL Board

–The Board has constituted following committees to oversee critical functions

– Project Committee to approve Project modules, Budget and Implementation Plan for smooth project implementation

– Personnel Committee to overview and approve personnel related matters & oversee implementation of rules & regulations

– Finance –cum- Audit Committee

77

What is the current Project status?

78

Legend

Activity Start Activity DurationActivity End Activity (Continue)

Project Development Activities

Project Activities 2007-08 2010-11Jan-Mar Apr-Jun Jul-Sept Oct-Dec Jan-Mar Apr-Jun Jul-Sept Oct-Dec Jan-Mar Apr-Jun

PROJECT DEVELOPMENTPreparation of Master PlanConcept Design

BuildingsInfrastructure

Approvals & ClearancesHigh Rise ClearanceEnvironmental Studies & ClearanceMaster Plan including GDCR

Detailed DesignBuilding ArchitectureInfrastructure Component

2008-09 2009-10

AprilApril

JuneMay

April

JuneJune

Completed

OngoingOngoing

OngoingOngoingOngoing

C

Continue

79

Legend

Activity Start Activity DurationActivity End

Project Finance and Marketing Activities

Project Activities 2007-08Jan-Mar Apr-Jun Jul-Sept Oct-Dec Jan-Mar Apr-Jun Jul-Sept Oct-Dec Jan-Mar

PROJECT FINANCING & MARKETINGProject StructuringGift FundingSelection of Strategic Partner (PSP)

Viable Infrastructure on PPP ModelSemi-Viable Infrastructure on PPP Model

Project Marketing

2008-09 2009-10

Feb Sept

JuneAprilApril June

SeptOngoing

80

Legend

Activity Start Activity DurationActivity End Activity (Continue)

Project Implementation Activities

Project Activities 2007-08 2010-11Jan-Mar Apr-Jun Jul-Sept Oct-Dec Jan-Mar Apr-Jun Jul-Sept Oct-Dec Jan-Mar Apr-Jun

PROJECT IMPLEMENTATION Surveys & InvestigationsBuilding ApprovalsWater Source DevelopmentExternal Road ConnectivityProcurements of Contractors for Core InfrastructureSite DevelopmentInfrastructure Development

Core InfrastructurePPP Model - Infrastructure Component

Construction of Buildings

2008-09 2009-10

MarJuly

AugMar

SeptApril

May Oct

JuneJuly

Sept

Mar

Ongoing

Ongoing

Ongoing

Continue

Continue

81

Way Forward

Thank You

![Gujarat Arts & Science College, Ahmedabad Computer … · Gujarat Arts & Science College, Ahmedabad Computer Science Department ... Ahmedabad Computer Science Department[Self Finance]](https://static.fdocuments.in/doc/165x107/5ada6c2a7f8b9a137f8d72c4/gujarat-arts-science-college-ahmedabad-computer-arts-science-college-ahmedabad.jpg)