GT MENA EQUITY Fund May 2015 A Hidden market value.

23

GT MENA EQUITY Fund May 2015 A Hidden market value

-

Upload

garry-stevens -

Category

Documents

-

view

214 -

download

0

Transcript of GT MENA EQUITY Fund May 2015 A Hidden market value.

GT MENA EQUITY Fund

May 2015A Hidden market value

2

GT Finance Created in 2000 by Daniel Thierry in association with Cholet Dupont, GT Finance (“GT”), a fully licensed and regulated

entity under the Autorité des Marchés Financiers and the CSSF, is an asset management company that works with institutional investors and large private estates in Europe. GT has a total AUM of over $500 million and is a subsidiary of Cholet Dupont which has an AUM of $3 billion.

GT works in three key areas:

Direct investments in equity and fixed income products: GT is able to offer fixed income and equity products due to the expertise and collective experience of its investment team.

Management of multi-product funds: GT manages complex funds which invest across geographies and asset classes including equity, bonds and other funds.

Money-market funds: GT assists its clients to invest in the money market to take advantage of short term interest rates fluctuations.

The senior management at GT believes that a search for consistent performance and long term sustainability is key to success. They use a conviction-based portfolio management system with no benchmark constraints. GT often starts with a top-down analysis of major economic trends of various geographies leading to a broad asset allocation in order to generate alpha. These thematic based allocations are further defined by a bottom-up analysis of individual securities, resulting in the selection of best-in-class securities. GT uses internal and external research networks to ensure accurate analyses.

3

Characteristics of the MENA Region The investable MENA Universe encompasses 11 countries that stretches from Oman to Morocco, also including Bahrain, Egypt,

Jordan, Kuwait, Lebanon, Qatar, Saudi Arabia, Tunisia and the UAE. The countries enjoy different economic dynamics that allow a diverse investment universe.

To further understand this fast growing region, it would help thinking about each of the 11 MENA countries as part of two main economic sub regions : oil importers (North Africa) and oil exporters (the Gulf Cooperation Council , or GCC). The GCC states generally enjoy similar characteristics such as low debt to GDP, high government spending and large capital reserves.

The innate challenges facing the MENA region, such as the size and depth of its equity market, poor liquidity, political uncertainty are all very well documented. These factors have led to a disconnection between the region’s economic contribution to world output and its current representation in global indexes : While the MENA regions account for an estimated 4.1% of world GDP, they account for only 0.1% of the MSCI All Countries World Index.

Nevertheless, in our opinion, the long term growth potential of the MENA region and the gradual development of its capital markets present investors with an attractive opportunity.

This is based on two key points : 1/ that there is a long term potential going forward, and 2/ that current valuations and yields are generally at attractive levels.

GCC fiscal breakeven oil price, 2015GCC Non-oil GDP Growth expected to sustain a

healthy rate of 4,9%

Source: EFG

4

Investment Thesis: Unlock the value The last decade was marked by the growing contribution of developing countries to the global economy. This trend has

subsequently led to a significant expansion in the emerging markets asset class, as long term investors flocked towards higher yield and more importantly, growth

Following a period of a generally strong performance in emerging markets since the 2008-2009 financial crisis, investors have started to search further afield for investment returns. The natural deceleration of growth in BRIC countries, the superpowers of the emerging markets universe in recent years, has opened the door for lesser known economies to rise through the ranks.

These smaller, fast growing economies, also known as “frontier markets” potentially create the next generation of equity investing. Supported by positive growing demographic trends, relatively young populations, generally attractive factors such as low wage costs, low public and private debt levels and rising consumption, investment in frontier markets offers diversification beyond the more developed and better established markets

With an overall GDP of US$ 2.3 Trillion projected for 2012- forecast to grow to US$ 3.0 Trillion by 2017 and with a population of 250 million, the MENA region represents a sizeable economic bloc that may compare favorably with the larger BRIC countries.

We believe the MENA region can offer investors an early first access to frontier markets, the possible emerging markets of tomorrow. The expected transition from frontier to emerging markets would eventually increase the actual current investment in frontier markets from the US$15 billion to an estimated US$ 550 billion, generally seen in more developed emerging markets.

GCC Countries Debt Profile MENA GDP Forecasts (% y/y)

Source: IMF Source: IMF, EFG Hermes

5

MENA economics 2015 breakeven fiscal oil price indicates that breakeven prices for all GCC countries are higher that our baseline average oil price

assumption of USD 55 per barrel this year. Accordingly, we are estimating budget deficits for all GCC countries in 2015. The magnitude of the deficit as a percentage of GDP will be particularly large for Saudi Arabia and Oman.

We forecast that the sum of fiscal balances for the GCC will drop to an aggregate deficit of USD 121,6 billion this year from a surplus of USD 26 billion in 2014.

We estimate that Saudi Arabia will register a sizable deficit this year of USD 89,3 billion (14% of GDP). To finance this deficit, the government could rely on its vast foreign reserves, amounting to USD 732 billion (equivalent to 97% of GDP) at the end of 2014. They could also issue local currency bonds to finance part of the deficit. At end-2014 domestic public debt to GDP stood at 1,6% of GDP; this low level of debt gives the government ample room to raise debt without jeopardizing its debt sustainability measures.

We estimate total foreign reserves of the GCC block at USD 2,3 trillion, including official reserves plus Sovereign Wealth Fund foreign assets. The UAE and KSA account for 33,3% and 33,1% of the total. In the case of Saudi Arabia, we estimate that the current level of reserves would be used up in eight years based on an annual fiscal deficit equivalent in size to the deficit that we are estimating for this year. On the other hand we estimate that the UAE’s reserves would be depleted in 172 years based on an annual deficit of USD 16 billion.

Estimated reserves and sovereign fund asset (USD billion), as % of 2014 GDP

Years to deplete foreign reserves across the GCC

Source: IMF, EFG Hermes

6

Investment Thesis: Diversification benefits Investing in the MENA region is capitalizing on very strong fundamentals, robust growth, very attractive demographics and reforms

that will bear fruit in the years to come.

Apart from those strong fundamentals, another interesting feature defined MENA countries : its low correlation with the rest of the world.

This low correlation is justified by a strong business model and companies having little exposure to global growth.

Correlation of GCC countries with other regions Correlation of GCC countries with EM and World

Source: IMF Source: IMF, DB Estimates

7

Investment Thesis: Opening of the Saudi market The largest equity market in the MENA region opened to direct foreign investments this summer. In our view, this is a major positive

news for the MENA region.

MSCI may review Saudi status from 2H15 : Accordingly to initial comments, MSCI has been waiting for implementation of the market opening before consulting with investors, a process that may therefore begin in June 2015. A decision on the inclusion of Saudi Arabia in MSCI EM or other indexes would come earliest in June 2016.

Initial potential weight put at 4%. Accordingly to initial comments and before publication of the draft QFI rules, MSCI stated that Saudi Arabia could potentially command a weight of 4% in the EM Index, based on current data at that time, which would make it an index heavyweight. At 4%, Saudi Arabia would be close to parity with index heavyweights Russia (4%) and Mexico (4,5%).

KSA : A substantial second tier emerging market Average daily turnover (USS m)

Source: Bloomberg, Morgan Stanley

8

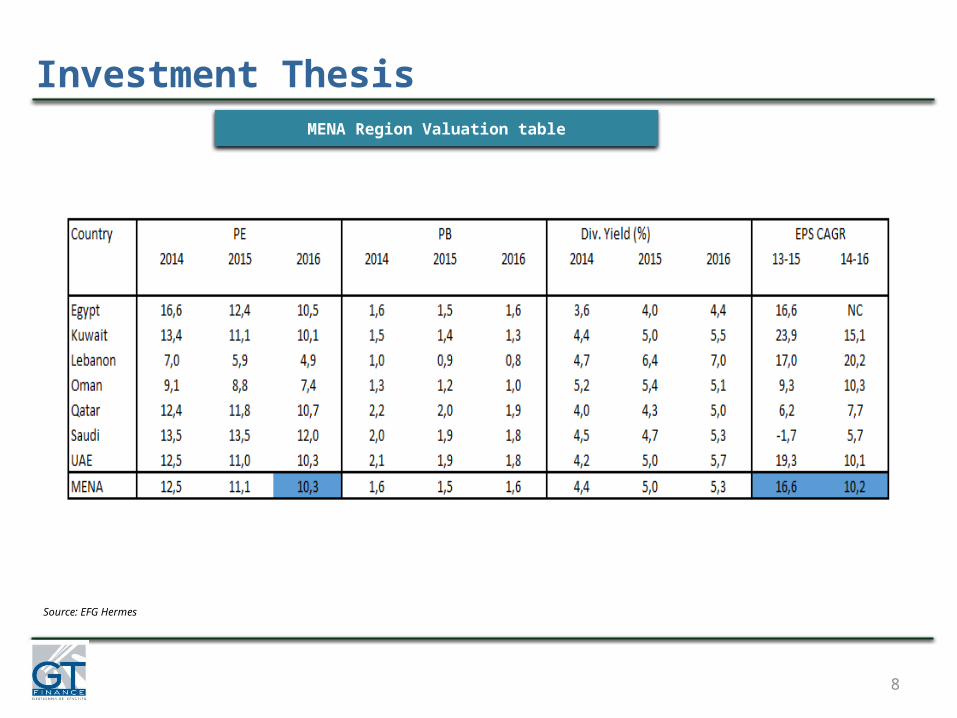

Investment ThesisMENA Region Valuation table

Source: EFG Hermes

9

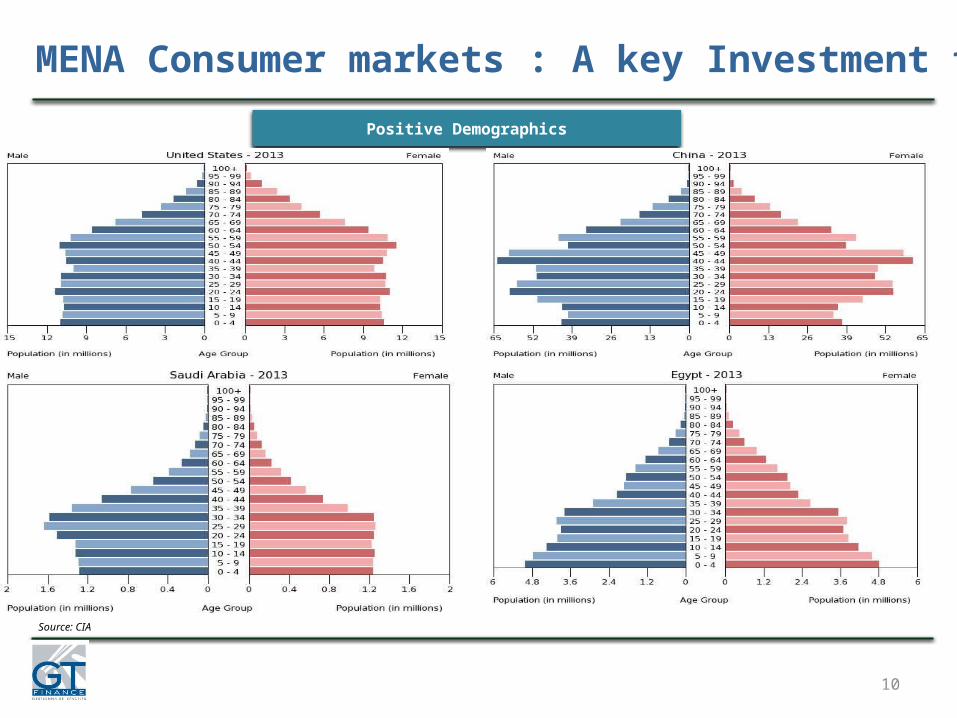

MENA Consumer markets : A key Investment theme We believe that consumer markets in the MENA Region have some of the brightest prospects overall. Demographics are a key

investment driver for the regions. The population is large, young and growing rapidly. Rising income per capita should boost underpenetrated consumer markets.

The MENA region offers much better long term growth prospects than developed markets, especially in countries with favorable demographics profiles : Saudi Arabia and Egypt.

Saudi Arabia, in particular, has a compelling macroeconomic backdrop. Saudi Arabia US$ 580 bn economy is the largest in the MENA region and globally amongst the 20 largest. The combination of demographics and robust economic growth is the underlying factor for high single digit growth in personal disposable income over the 2011-2015 period, and a key driver for making Saudi Arabia one of the world’s youngest and fastest growing consumer markets.

However, Saudi Arabia has a social pressure similar to those that led to uprisings in other countries. We believe that the challenge for the Saudi authorities will be to reduce the unemployment rate within the domestic population. As a support of our view and according to the IMF, the solution for the government to reduce the current unemployment rate by 5% over the next five years, should pass by an acceleration of non oil growth by an average 7.5% in real terms.

It seems that pushing non oil related growth to a higher level would probably mean that government spending would be at least sustained at current high levels, or even increased, which would mean a stronger consumer spending growth rate.

Demographical Statistics in GCC and Egypt GDP per capita (US$) and milk consumption/capita (kg)

Source: IMF, US Census Bureau Source: IMF, DB Estimates

10

MENA Consumer markets : A key Investment theme

Positive Demographics

Source: CIA

11

MENA Consumer markets : Impact of Saudization? While the consumer theme is popular amongst emerging markets, the MENA consumer one should be an even more attractive

investment. This theme should perform very well in Saudi Arabia not only because of demographics, but also because of an increasing working

population, a low consumer leverage, a low retail penetration, wage increases and credit growth. One should remember that Saudi wages are low.

One of the key drivers supporting these factors is the “Saudization” of the workforce. Today, more than 50% of the workforce is non-Saudi. Moreover the labor force participation of Saudi Arabia nationals is as low as 40%. The government has been willing to increase the number of Saudis working in the private sector. Subsequently, over the past few months more that one million expats have left the country.

Another issue affecting the GCC region is the remittance problem. Saudi Arabia is the third-largest remittance-sending country. As the GCC countries are trying to improve the ratio of the national working force, the problem should be increasingly considered.

The GCC region is also trying to rein expenses done abroad by local residents, both nationals and expats. One of the best examples is healthcare. The governments are willing to encourage people to go to local hospitals, both private and public.

Proportion of non-Saudis in labour force hassteadily declined since the 1990s

Remittances out of Saudi are the size of Lebanon’s GDP

Source: Central Department of Statistics & Information Source: Haver, BofA Merrill Lynch Global Research

12

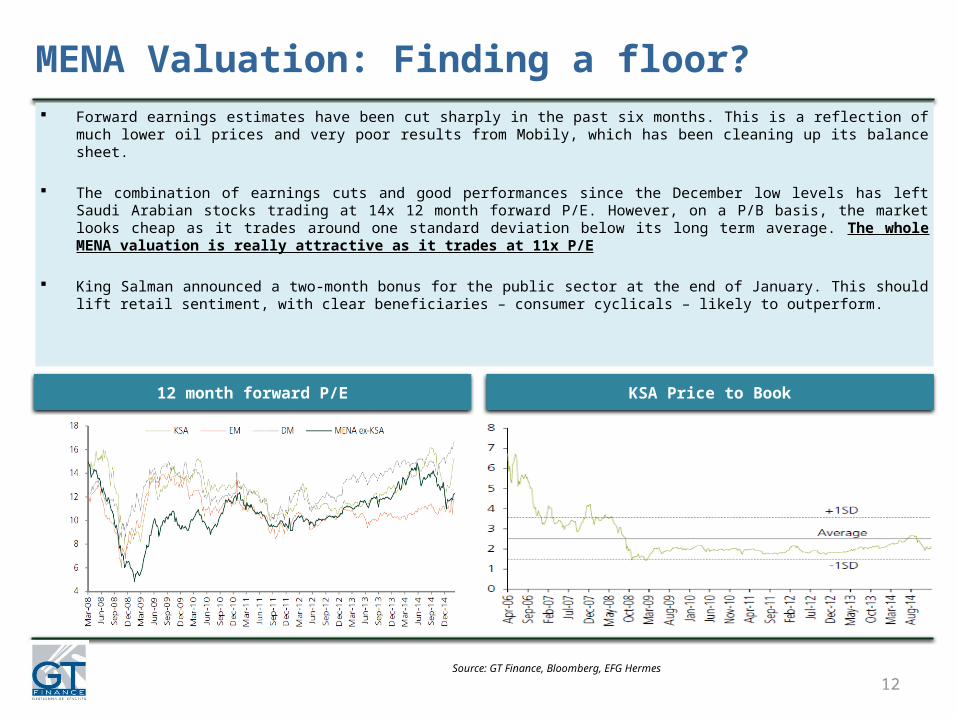

Forward earnings estimates have been cut sharply in the past six months. This is a reflection of much lower oil prices and very poor results from Mobily, which has been cleaning up its balance sheet.

The combination of earnings cuts and good performances since the December low levels has left Saudi Arabian stocks trading at 14x 12 month forward P/E. However, on a P/B basis, the market looks cheap as it trades around one standard deviation below its long term average. The whole MENA valuation is really attractive as it trades at 11x P/E

King Salman announced a two-month bonus for the public sector at the end of January. This should lift retail sentiment, with clear beneficiaries – consumer cyclicals – likely to outperform.

12 month forward P/E KSA Price to Book

Source: GT Finance, Bloomberg, EFG Hermes

MENA Valuation: Finding a floor?

13

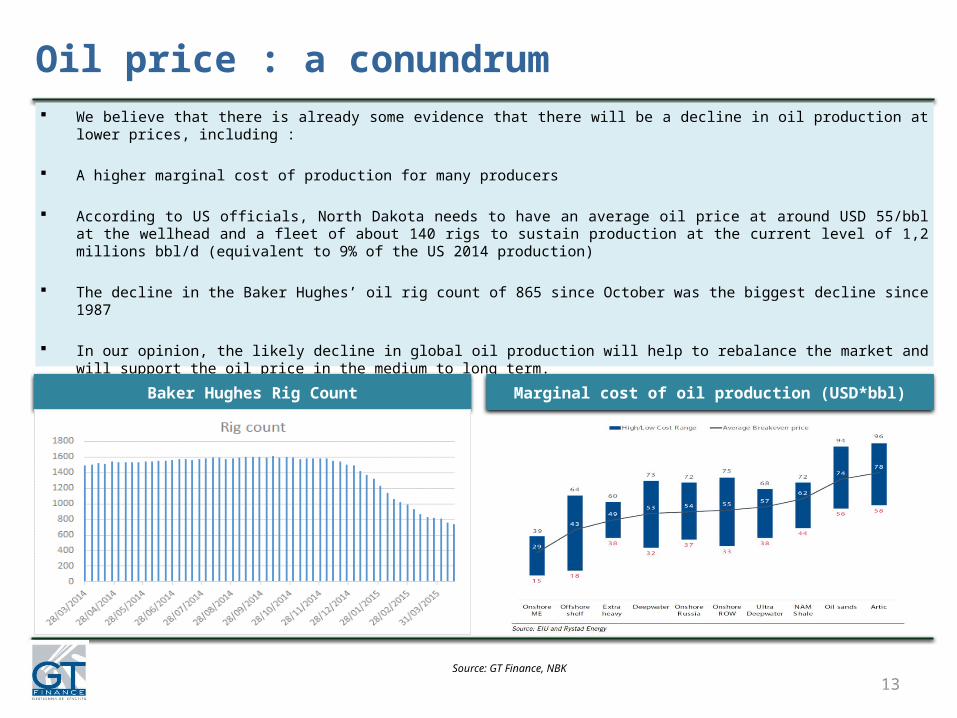

We believe that there is already some evidence that there will be a decline in oil production at lower prices, including :

A higher marginal cost of production for many producers

According to US officials, North Dakota needs to have an average oil price at around USD 55/bbl at the wellhead and a fleet of about 140 rigs to sustain production at the current level of 1,2 millions bbl/d (equivalent to 9% of the US 2014 production)

The decline in the Baker Hughes’ oil rig count of 865 since October was the biggest decline since 1987

In our opinion, the likely decline in global oil production will help to rebalance the market and will support the oil price in the medium to long term.

Baker Hughes Rig Count Marginal cost of oil production (USD*bbl)

Source: GT Finance, NBK

Oil price : a conundrum

14

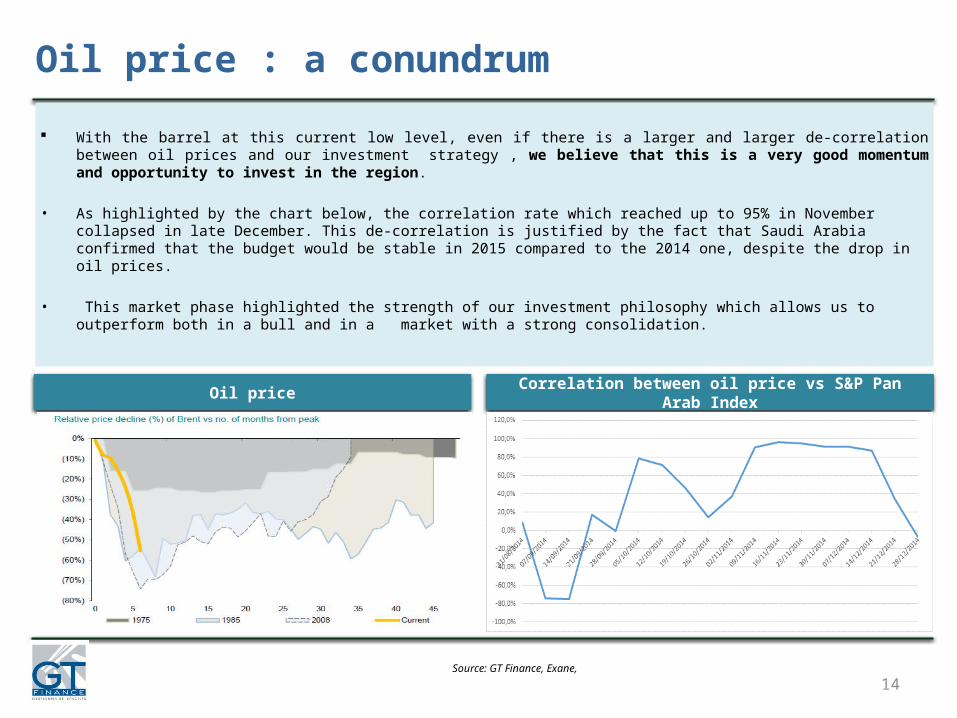

With the barrel at this current low level, even if there is a larger and larger de-correlation between oil prices and our investment strategy , we believe that this is a very good momentum and opportunity to invest in the region.

• As highlighted by the chart below, the correlation rate which reached up to 95% in November collapsed in late December. This de-correlation is justified by the fact that Saudi Arabia confirmed that the budget would be stable in 2015 compared to the 2014 one, despite the drop in oil prices.

• This market phase highlighted the strength of our investment philosophy which allows us to outperform both in a bull and in a market with a strong consolidation.

Oil price Correlation between oil price vs S&P Pan Arab Index

Source: GT Finance, Exane,

Oil price : a conundrum

15

Investment Strategy Our investment philosophy is to focus on structurally attractive businesses stewarded

by a prudent management team using strong capital discipline to generate returns across the business cycle. Back testing has shown that our selection would have created significant outperformance over the benchmark. We have chosen to focus on attractive valuations, dividend yield and liquidity. As a result, the portfolio can be liquidated within 5 business days (based on AUM of EUR 50 million)..

Country Exclusions

• Eliminate countries with high risks of expropriation or political risk• Libya and Syria and are screened out• Egypt is on the watch list

Universe of 300 investible companies

Formal Bottom Up Screen

• Screen on preset criteria, 2/3 fundamental, 1/3 valuation

• Criteria: Liquidity, ROIC, ROE, Net Debt, Dividend Yield, P/E etc.

Informal Bottom Up Screen

Sourcing Ideas from:• Own experience• Local contacts • Informal screen produces most ideas

Thesis Development• Quality of Franchise with ability to generate ROIC substantially

above cost of capital over the business cycle• Prudent management entrusted to handle cash-flows generated

efficiently either through reinvestment or payment to shareholders• Analyze the risk of default, fraud etc.• Analyze fair value via Discounted Cash Flow analysis and other

methods

Portfolio of 30-60 Companies

Universe

Top-Down Screen

Bottom Up Screens

Company Analysis

Final Portfolio

16

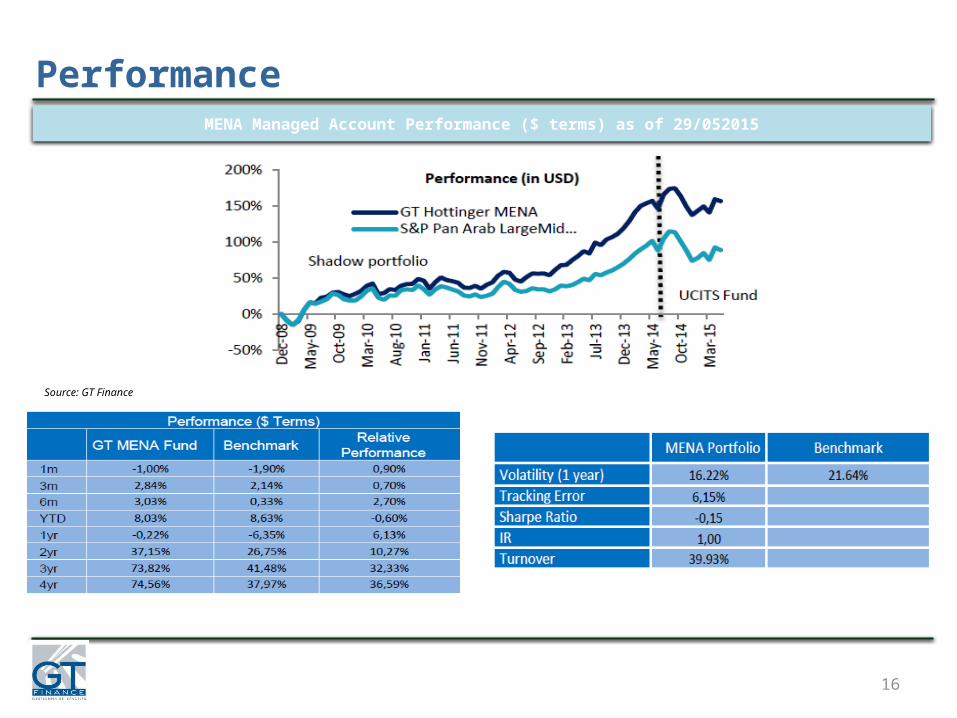

PerformanceMENA Managed Account Performance ($ terms) as of 29/052015

Source: GT Finance

17

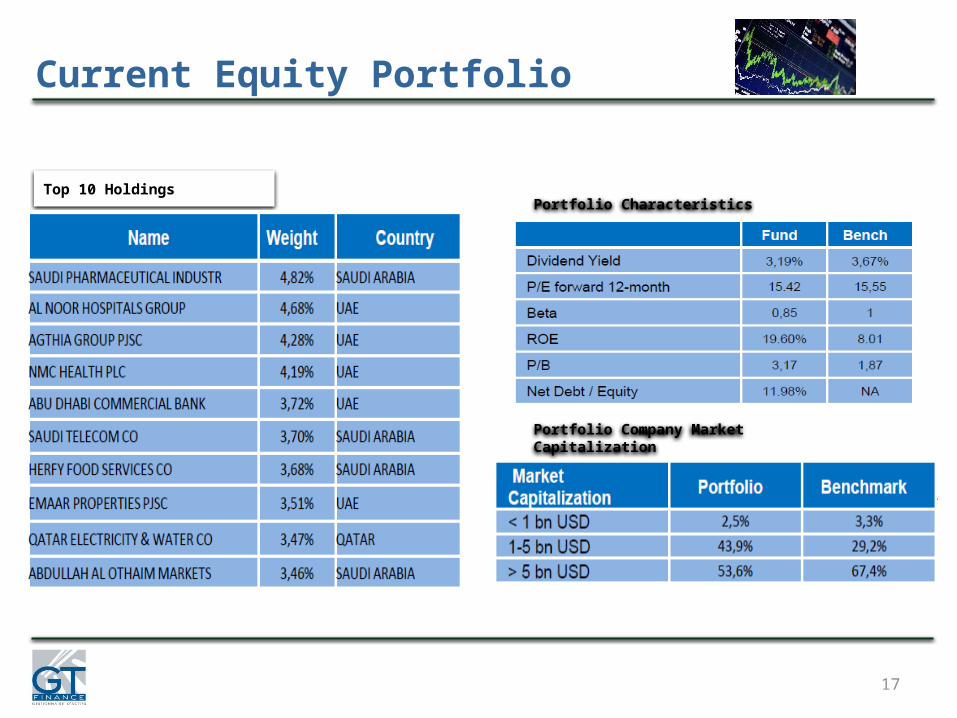

Current Equity Portfolio

Top 10 HoldingsPortfolio Characteristics

Portfolio Company Market Capitalization

18

Current Allocation

Country Allocation Sector Allocation

19

PerformanceGT MENA Equity Fund vs. main competitors ($ terms) since 31/12/2008

Source: GT Finance

10.0% 12.0% 14.0% 16.0% 18.0% 20.0% 22.0%0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%Schroder Middle EastGT MENA Equity

Amundi MENA

T Rowe Price Middle East

Emirates MENA Top Companies

Baring MENA

JP Morgan Middle East

Annualized volatility

Ann

ualiz

ed re

turn

20

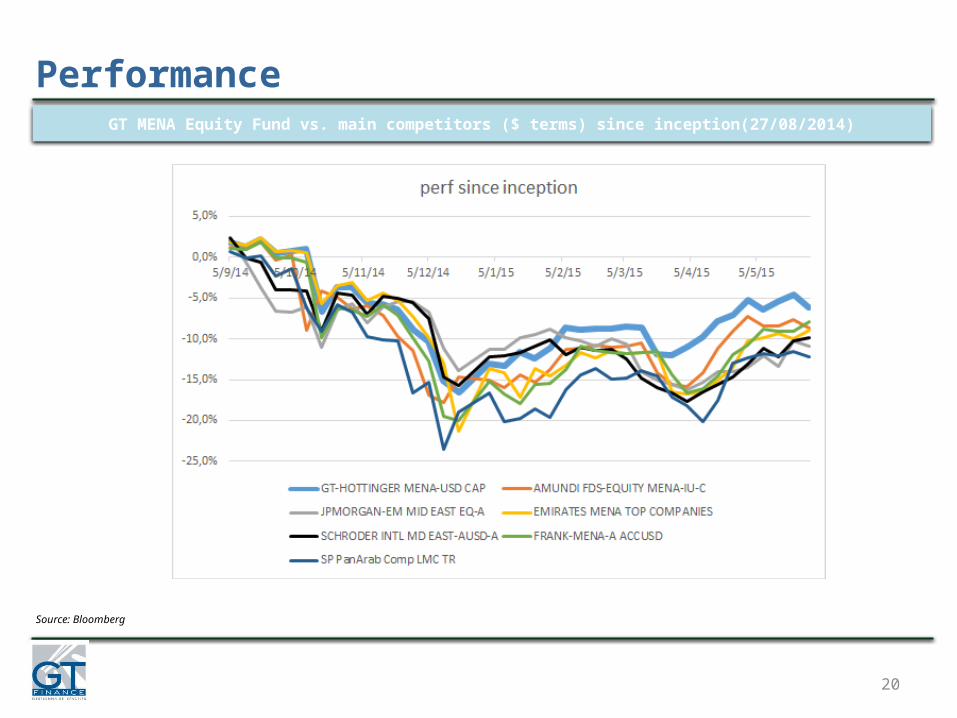

PerformanceGT MENA Equity Fund vs. main competitors ($ terms) since inception(27/08/2014)

Source: Bloomberg

21

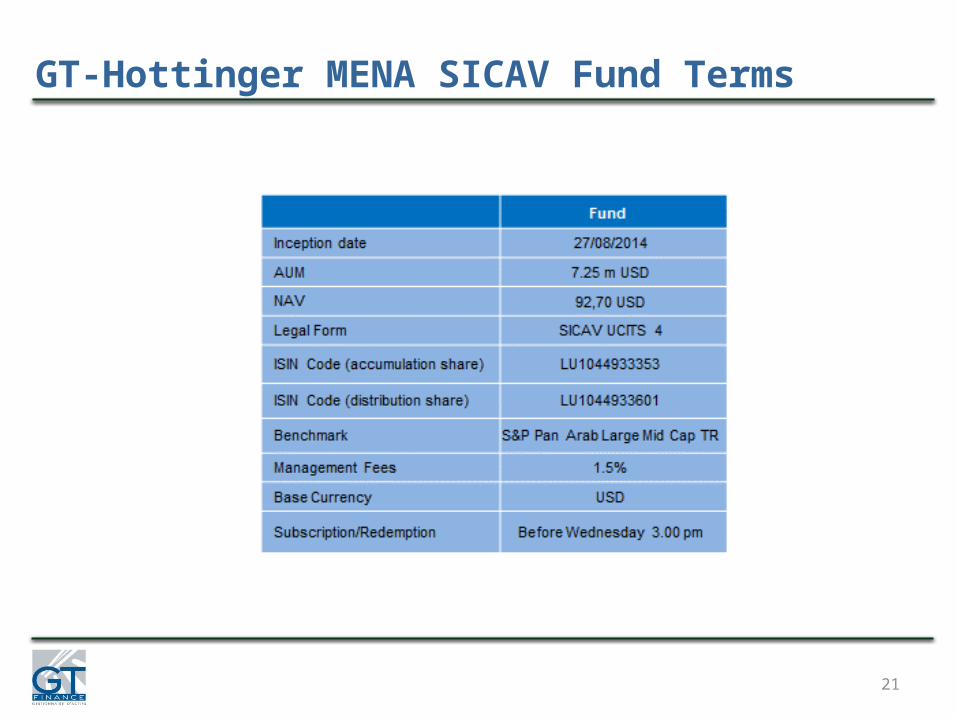

GT-Hottinger MENA SICAV Fund Terms

22

GT Finance Leadership

Arnaud Cayla Managing Director,

CIO,Member of the

board

Arnaud joined GT in December 2011. Prior to that he was a Manager of European and International Equity funds at Barclays Wealth Management, France. He started working at Barclays Investment Managers in 2000 as a "buy side“ financial analyst before becoming head of strategy. Arnaud holds Masters degrees in Banking & International Finance, and Economics from the University of Poitiers.

Rémi de Laboulaye

CFA, Portfolio Manager

Rémi joined GT in 2007 as a hedge fund analyst, specializing on long/short equities and global macro funds. He is the fund manager of Rhin Rhône, a dedicated SICAV focused on bonds and equities with an absolute return objective. He also co-manages the GT Hottinger Income Plus Fund, a fixed income fund with a flexible investment approach. Rémi holds a Masters Degree in Asset Management from the University of Paris IX Dauphine and is a CFA Charterholder.

Daniel Thierry Head of the Supervisory

Board

Daniel founded GT back in the year 2000, and is currently the Director of the IceFund. Prior to working with GT, he was a Director at Worms & Cie from 1995 to 1998, in charge of Permal (a 100% subsidiary) managing assets on behalf of third parties. He also worked at Demachy Worms & Cie as a Director looking after managed funds, fund-of-funds and multi-asset funds. He graduated from Institut d'Etudes Politiques de Paris and holds a Masters in Economics from the University of Paris X Nanterre.

Carlos Tavares-Gravato

Head of Development and RM, Member of

the Board

Carlos joined GT in 2012. Previously, he was a partner at Vendôme Associés, an independent recruitment agency specialised in finance where he was in charge of the Asset Management practice. Carlos had previously held numerous leadership roles in the sale of alternative investment products, warrants and convertible bonds in London and fund management in Paris. He graduated from the Institut d'Etudes Politiques de Paris and holds a postgraduate degree in International Administration from the University of Paris II Panthéon-Assas and a Masters in Law from the University of Lisbon.

GT FINANCE30, place de la Madeleine

75008 ParisTel : +33 1 53 43 20 40 – Fax : +33 1 53 43 20 57

Head of Development & Relationship Manager : M. Carlos Tavares-Gravato

+33 1 53 43 20 46 [email protected]

23

Contact Details